Filed by Goldman Sachs Middle Market Lending Corp.

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed under Rule14a-12 of the Securities Exchange Act of 1934

Subject Company: Goldman Sachs Middle Market Lending Corp.

Commission FileNo. 000-55746

Goldman Sachs BDC, Inc. (NYSE: GSBD) Goldman Sachs Middle Market Lending Corp. (“MMLC”) GSBD and MMLC Merger December 9, 2019 www.goldmansachsbdc.com

Disclaimer and Forward-Looking Statement This investor presentation may contain forward-looking statements that involve substantial risks and uncertainties. You can identify these statements by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “target,” “estimate,” “intend,” “continue,” or “believe” or the negatives thereof or other variations thereon or comparable terminology. You should read statements that contain these words carefully because they discuss our plans, strategies, prospects and expectations concerning our business, operating results, financial condition and other similar matters. These statements represent the belief of Goldman Sachs BDC, Inc. (the “Company” or “GSBD”) regarding certain future events that, by their nature, are uncertain and outside of the Company’s control. Any forward-looking statement made by us in this presentation speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ, possibly materially from our expectations, include, but are not limited to, the ability of the parties to consummate the merger contemplated by the agreement and plan of merger (the “Merger Agreement”) by and among GSBD, Goldman Sachs Middle Market Lending Corp. (“MMLC”), Evergreen Merger Sub Inc. and Goldman Sachs Asset Management, L.P. (“GSAM”) on the expected timeline, or at all, failure of GSBD or MMLC to obtain the requisite stockholder approval for the Proposals (as defined below) as set forth in the Proxy Statement (as defined below), the ability to realize the anticipated benefits of the merger, effects of disruption on the business of GSBD and MMLC from the proposed merger, the effect that the announcement or consummation of the merger may have on the trading price of GSBD’s common stock on the New York Stock Exchange, the combined company’s plans, expectations, objectives and intentions as a result of the merger, any decision by MMLC to pursue continued operations, any termination of the Merger Agreement, future operating results of GSBD or MMLC, the business prospects of GSBD and MMLC and the prospects of their portfolio companies, actual and potential conflicts of interests with GSAM and other affiliates of Goldman Sachs (as defined below), general economic and political trends and other factors, the dependence of GSBD’s and MMLC’s future success on the general economy and its effect on the industries in which they invest, future changes in laws or regulations and interpretations thereof, and the risks, uncertainties and other factors we identify in the sections entitled “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements” in filings we make with the Securities and Exchange Commission (“SEC”), including those contained in the Proxy Statement, when such documents become available, and it is not possible for us to predict or identify all of them. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. This presentation does not constitute a prospectus and should under no circumstances be understood as an offer to sell or the solicitation of an offer to buy our common stock or any other securities nor will there be any sale of the common stock or any other securities referred to in this presentation in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of such state or jurisdiction. Nothing in these materials should be construed as a recommendation to invest in any securities that may be issued by GSBD or as legal, accounting or tax advice. An investment in securities of the type described herein presents certain risks. GSBD is managed by GSAM, a wholly owned subsidiary of The Goldman Sachs Group, Inc. (“Goldman Sachs”). Nothing contained herein shall be relied upon as a promise or representation whether as to the past or future performance. The information contained in this presentation is summary information that is intended to be considered in the context of other public announcements that we may make, by press release or otherwise, from time to time. We undertake no duty or obligation to publicly update or revise the information contained in this presentation, except as required by law. These materials contain information about GSBD, certain of its personnel and affiliates and its historical performance. You should not view information related to the past performance of GSBD as indicative of GSBD’s future results, the achievement of which cannot be assured. Further, an investment in GSBD is discrete from, and does not represent an interest in, any other Goldman Sachs entity. 2

Disclaimer and Forward-Looking Statement Additional Information and Where to Find It This communication relates to a proposed business combination involving GSBD and MMLC, along with related proposals for which stockholder approval will be sought (collectively, the “Proposals”). In connection with the Proposals, each of GSBD and MMLC intend to file relevant materials with the SEC, including a registration statement on FormN-14, which will include a joint proxy statement of GSBD and MMLC and a prospectus of GSBD (the “Proxy Statement”). This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act. STOCKHOLDERS OF EACH OF GSBD AND MMLC ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE PROXY STATEMENT WHEN IT BECOMES AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS THERETO, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT GSBD, MMLC, THE MERGER AND THE PROPOSALS. Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s web site, http://www.sec.gov or, for documents filed by GSBD, from GSBD’s website at http://www. https://www.goldmansachsbdc.com. Participants in the Solicitation GSBD and MMLC and their respective directors, executive officers and certain other members of management and employees of GSAM and its affiliates, may be deemed to be participants in the solicitation of proxies from the stockholders of GSBD and MMLC in connection with the Proposals. Information about the directors and executive officers of GSBD is set forth in its proxy statement for its 2019 annual meeting of stockholders, which was filed with the SEC on March 21, 2019. Information about the directors and executive officers of MMLC is set forth in its Annual Report on Form10-K for the year ended December 31, 2018, which was filed with the SEC on March 1, 2019 and its proxy statement for its 2019 annual meeting of stockholders, which was filed with the SEC on September 11, 2019. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the GSBD and MMLC stockholders in connection with the Proposals will be contained in the Proxy Statement when such document becomes available. This document may be obtained free of charge from the sources indicated above. 3

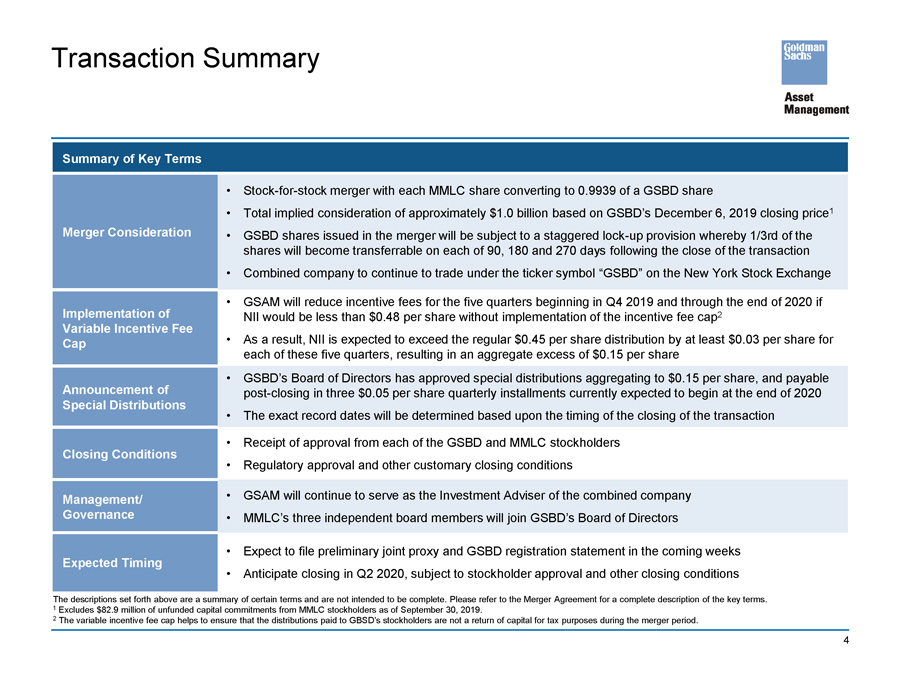

Transaction Summary Summary of Key Terms •Stock-for-stock merger with each MMLC share converting to 0.9939 of a GSBD share • Total implied consideration of approximately $1.0 billion based on GSBD’s December 6, 2019 closing price1 Merger Consideration • GSBD shares issued in the merger will be subject to a staggeredlock-up provision whereby 1/3rd of the shares will become transferrable on each of 90, 180 and 270 days following the close of the transaction • Combined company to continue to trade under the ticker symbol “GSBD” on the New York Stock Exchange • GSAM will reduce incentive fees for the five quarters beginning in Q4 2019 and through the end of 2020 if Implementation of NII would be less than $0.48 per share without implementation of the incentive fee cap2 Variable Incentive Fee Cap • As a result, NII is expected to exceed the regular $0.45 per share distribution by at least $0.03 per share for each of these five quarters, resulting in an aggregate excess of $0.15 per share • GSBD’s Board of Directors has approved special distributions aggregating to $0.15 per share, and payable Announcement of post-closing in three $0.05 per share quarterly installments currently expected to begin at the end of 2020 Special Distributions • The exact record dates will be determined based upon the timing of the closing of the transaction • Receipt of approval from each of the GSBD and MMLC stockholders Closing Conditions • Regulatory approval and other customary closing conditions Management/ • GSAM will continue to serve as the Investment Adviser of the combined company Governance • MMLC’s three independent board members will join GSBD’s Board of Directors • Expect to file preliminary joint proxy and GSBD registration statement in the coming weeks Expected Timing • Anticipate closing in Q2 2020, subject to stockholder approval and other closing conditions The descriptions set forth above are a summary of certain terms and are not intended to be complete. Please refer to the Merger Agreement for a complete description of the key terms. 1 Excludes $82.9 million of unfunded capital commitments from MMLC stockholders as of September 30, 2019. 2 The variable incentive fee cap helps to ensure that the distributions paid to GBSD’s stockholders are not a return of capital for tax purposes during the merger period. 4

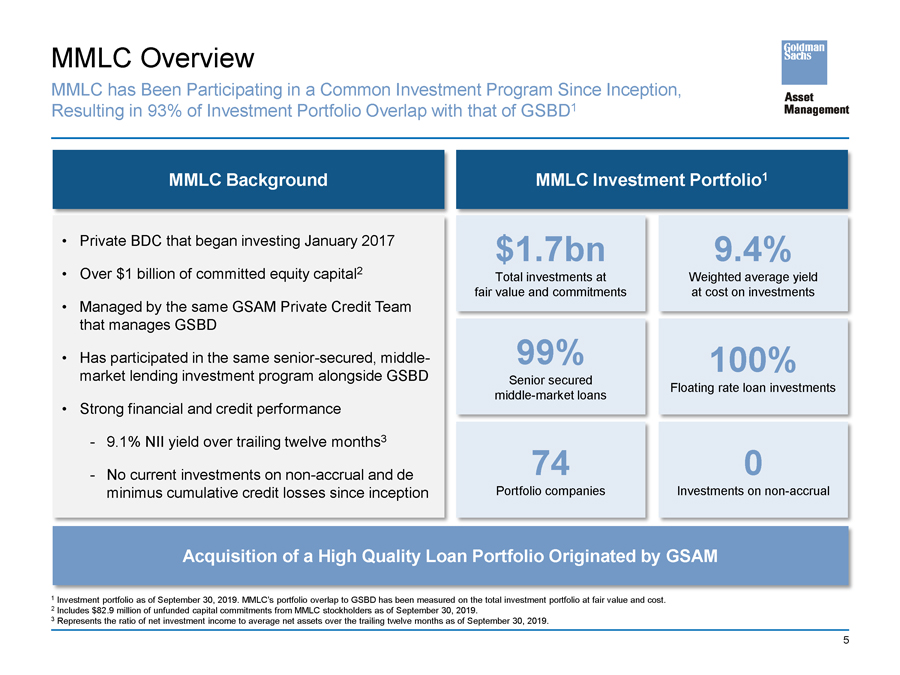

MMLC Overview MMLC has Been Participating in a Common Investment Program Since Inception, Resulting in 93% of Investment Portfolio Overlap with that of GSBD1 MMLC Background • Private BDC that began investing January 2017 • Over $1 billion of committed equity capital2 • Managed by the same GSAM Private Credit Team that manages GSBD • Has participated in the same senior-secured, middle-market lending investment program alongside GSBD • Strong financial and credit performance - 9.1% NII yield over trailing twelve months3 - No current investments onnon-accrual and de minimus cumulative credit losses since inception MMLC Investment Portfolio1 $1.7bn 9.4% Total investments at Weighted average yield fair value and commitments at cost on investments 99% 100% Senior secured Floating rate loan investments middle-market loans 74 0 Portfolio companies Investments onnon-accrual Acquisition of a High Quality Loan Portfolio Originated by GSAM 1 Investment portfolio as of September 30, 2019. MMLC’s portfolio overlap to GSBD has been measured on the total investment portfolio at fair value and cost. 2 Includes $82.9 million of unfunded capital commitments from MMLC stockholders as of September 30, 2019. 3 Represents the ratio of net investment income to average net assets over the trailing twelve months as of September 30, 2019. 5

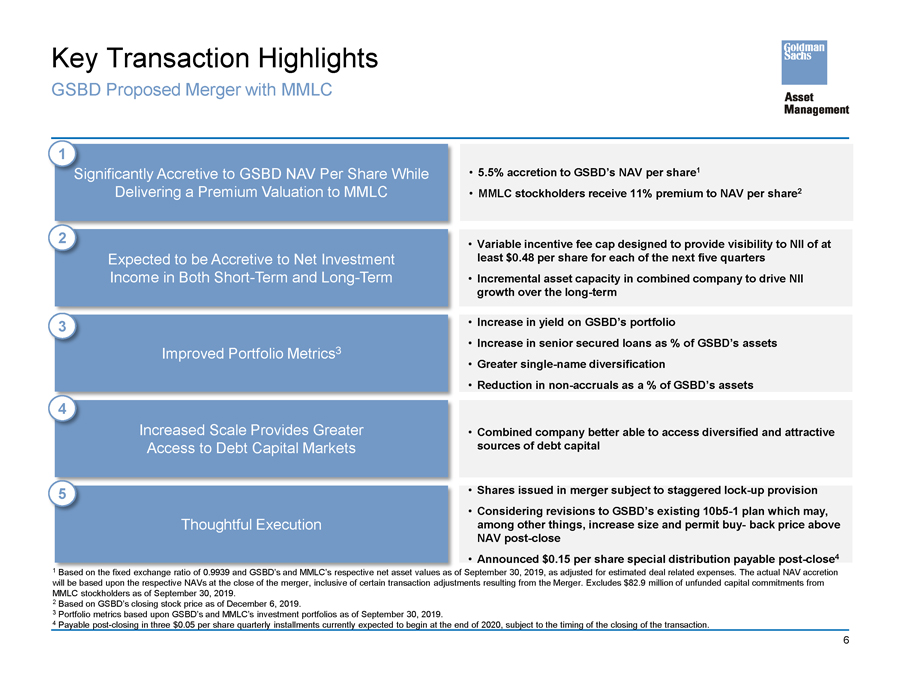

Key Transaction Highlights GSBD Proposed Merger with MMLC 1 significantly Accretive to GSBD NAV Per Share While Delivering a Premium Valuation to MMLC 2 Expected to be Accretive to Net Investment Income in Both Short-Term and Long-Term 3 Improved Portfolio Metrics3 4 Increased Scale Provides Greater Access to Debt Capital Markets 5 Thoughtful Execution • 5.5% accretion to GSBD’s NAV per share1 • MMLC stockholders receive 11% premium to NAV per share2 • Variable incentive fee cap designed to provide visibility to NII of at least $0.48 per share for each of the next five quarters • Incremental asset capacity in combined company to drive NII growth over the long-term • Increase in yield on GSBD’s portfolio • Increase in senior secured loans as % of GSBD’s assets • Greater single-name diversification • Reduction innon-accruals as a % of GSBD’s assets • Combined company better able to access diversified and attractive sources of debt capital • Shares issued in merger subject to staggeredlock-up provision • Considering revisions to GSBD’s existing10b5-1 plan which may, among other things, increase size and permitbuy- back price above NAV post-close • Announced $0.15 per share special distribution payable post-close4 1 Based on the fixed exchange ratio of 0.9939 and GSBD’s and MMLC’s respective net asset values as of September 30, 2019, as adjusted for estimated deal related expenses. The actual NAV accretion will be based upon the respective NAVs at the close of the merger, inclusive of certain transaction adjustments resulting from the Merger. Excludes $82.9 million of unfunded capital commitments from MMLC stockholders as of September 30, 2019. 2 Based on GSBD’s closing stock price as of December 6, 2019. 3 Portfolio metrics based upon GSBD’s and MMLC’s investment portfolios as of September 30, 2019. 4 Payable post-closing in three $0.05 per share quarterly installments currently expected to begin at the end of 2020, subject to the timing of the closing of the transaction. 6

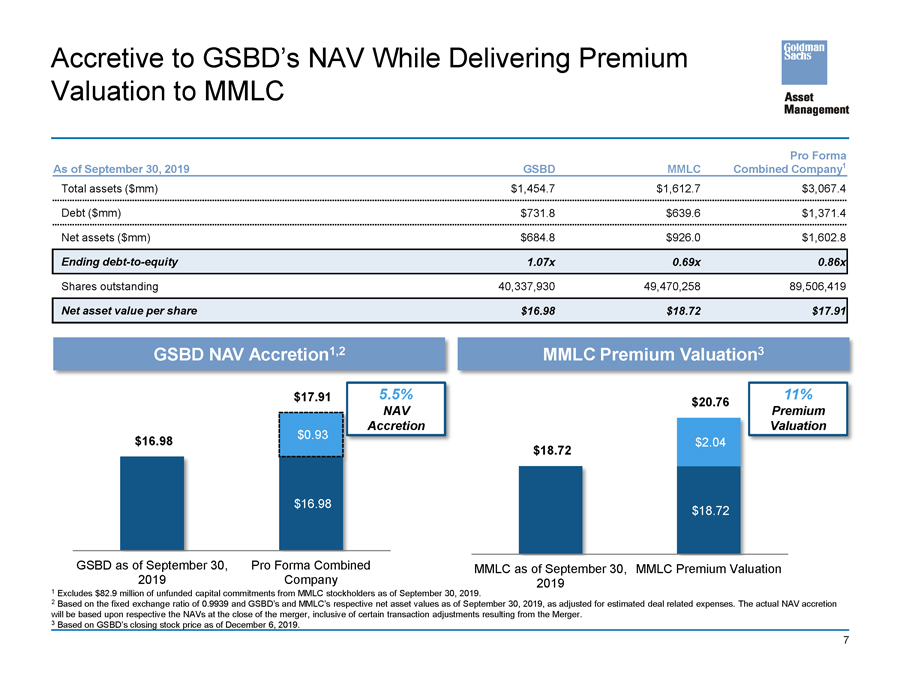

Accretive to GSBD’s NAV While Delivering Premium Valuation to MMLC Pro Forma As of September 30, 2019 GSBD MMLC Combined Company1 Total assets ($mm) $1,454.7 $1,612.7 $3,067.4 Debt ($mm) $731.8 $639.6 $1,371.4 Net assets ($mm) $684.8 $926.0 $1,602.8 Endingdebt-to-equity 1.07x 0.69x 0.86x Shares outstanding 40,337,930 49,470,258 89,506,419 Net asset value per share $16.98 $18.72 $17.91 GSBD NAV Accretion1,2 $17.91 5.5% NAV $0.93 Accretion $16.98 $16.98 GSBD as of September 30, Pro Forma Combined 2019 Company MMLC Premium Valuation3 11% $20.76 Premium Valuation $2.04 $18.72 $18.72 MMLC as of September 30, MMLC Premium Valuation 2019 1 Excludes $82.9 million of unfunded capital commitments from MMLC stockholders as of September 30, 2019. 2 Based on the fixed exchange ratio of 0.9939 and GSBD’s and MMLC’s respective net asset values as of September 30, 2019, as adjusted for estimated deal related expenses. The actual NAV accretion will be based upon respective the NAVs at the close of the merger, inclusive of certain transaction adjustments resulting from the Merger. 3 Based on GSBD’s closing stock price as of December 6, 2019. 7

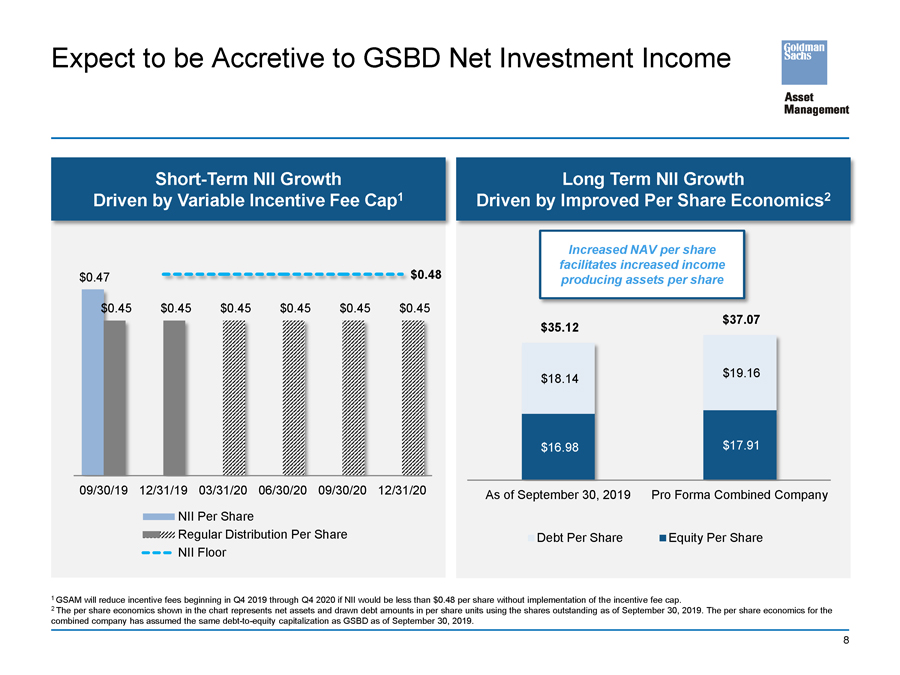

Expect to be Accretive to GSBD Net Investment Income Short-Term NII Growth Driven by Variable Incentive Fee Cap1 $0.47 $0.48 $0.45 $0.45 $0.45 $0.45 $0.45 $0.45 09/30/19 12/31/19 03/31/20 06/30/20 09/30/20 12/31/20 NII Per Share Regular Distribution Per Share NII Floor Long Term NII Growth Driven by Improved Per Share Economics2 Increased NAV per share facilitates increased income producing assets per share $37.07 $35.12 $18.14 $19.16 $16.98 $17.91 As of September 30, 2019 Pro Forma Combined Company Debt Per Share Equity Per Share 1 GSAM will reduce incentive fees beginning in Q4 2019 through Q4 2020 if NII would be less than $0.48 per share without implementation of the incentive fee cap. 2 The per share economics shown in the chart represents net assets and drawn debt amounts in per share units using the shares outstanding as of September 30, 2019. The per share economics for the combined company has assumed the samedebt-to-equity capitalization as GSBD as of September 30, 2019. 8

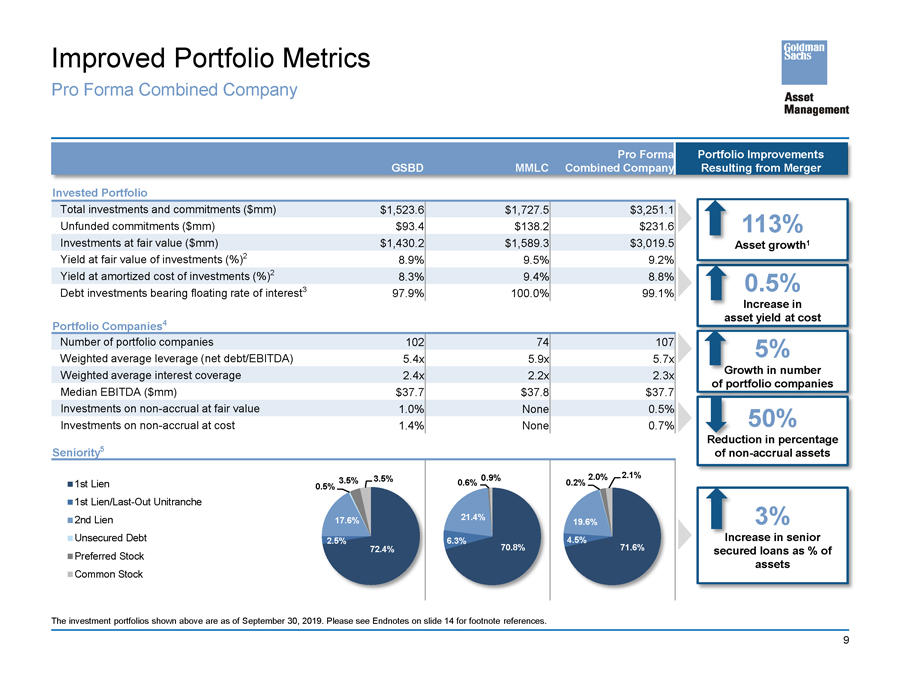

Improved Portfolio Metrics Pro Forma Combined Company Pro Forma GSBD MMLC Combined Company Invested Portfolio Total investments and commitments ($mm) $1,523.6 $1,727.5 $3,251.1 Unfunded commitments ($mm) $93.4 $138.2 $231.6 Investments at fair value ($mm) $1,430.2 $1,589.3 $3,019.5 Yield at fair value of investments (%)2 8.9% 9.5% 9.2% Yield at amortized cost of investments (%)2 8.3% 9.4% 8.8% Debt investments bearing floating rate of interest3 97.9% 100.0% 99.1% Portfolio Companies4 Number of portfolio companies 102 74 107 Weighted average leverage (net debt/EBITDA) 5.4x 5.9x 5.7x Weighted average interest coverage 2.4x 2.2x 2.3x Median EBITDA ($mm) $37.7 $37.8 $37.7 Investments onnon-accrual at fair value 1.0% None 0.5% Investments onnon-accrual at cost 1.4% None 0.7% Seniority5 3.5% 0.9% 2.0% 2.1% 1st Lien 3.5% 0.6% 0.2% 0.5% 1stLien/Last-Out Unitranche 2nd Lien 17.6% 21.4% 19.6% Unsecured Debt 2.5% 6.3% 70.8% 4.5% 71.6% 72.4% Preferred Stock Common Stock Portfolio Improvements Resulting from Merger 113% Asset growth1 0.5% Increase in asset yield at cost 5% growth in number of portfolio companies 50% action in percentage ofnon-accrual assets 3% crease in senior red loans as % of assets The investment portfolios shown above are as of September 30, 2019. Please see Endnotes on slide 14 for footnote references. 9

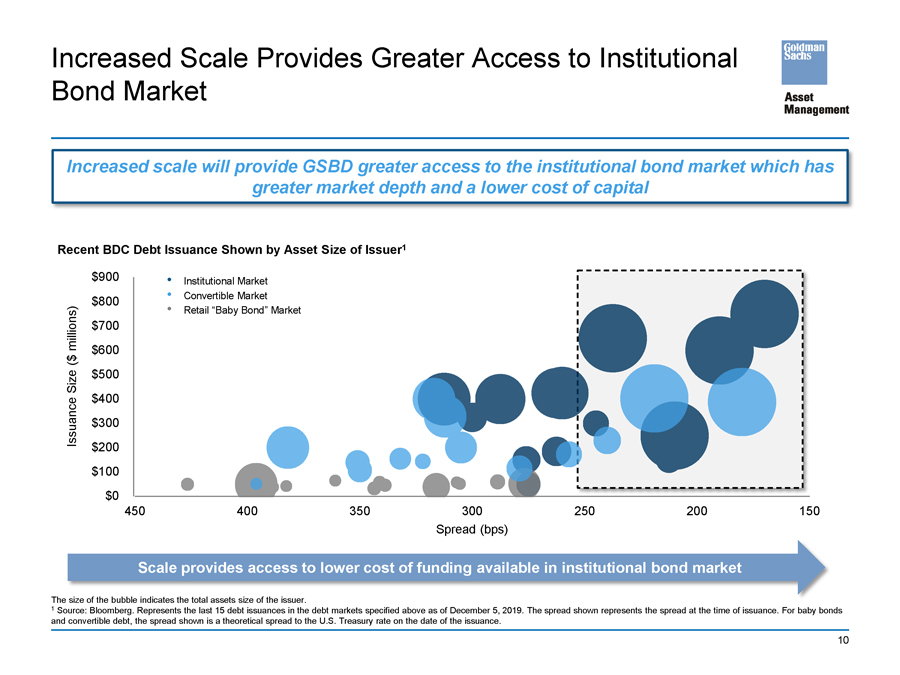

Increased Scale Provides Greater Access to Institutional Bond Market Increased scale will provide GSBD greater access to the institutional bond market which has greater market depth and a lower cost of capital Recent BDC Debt Issuance Shown by Asset Size of Issuer1 $900 • Institutional Market $800 • Convertible Market • Retail “Baby Bond” Market millions) $700 $ $600 ( $500 Size $400 Issuance $300 $200 $100 $0 450 400 350 300 250 200 150 Spread (bps) Scale provides access to lower cost of funding available in institutional bond market The 1 Source: Bloomberg. Represents the last 15 debt issuances in the debt markets specified above as of December 5, 2019. The spread shown represents the spread at the time of issuance. For baby bonds and convertible debt, the spread shown is a theoretical spread to the U.S. Treasury rate on the date of the issuance. 10

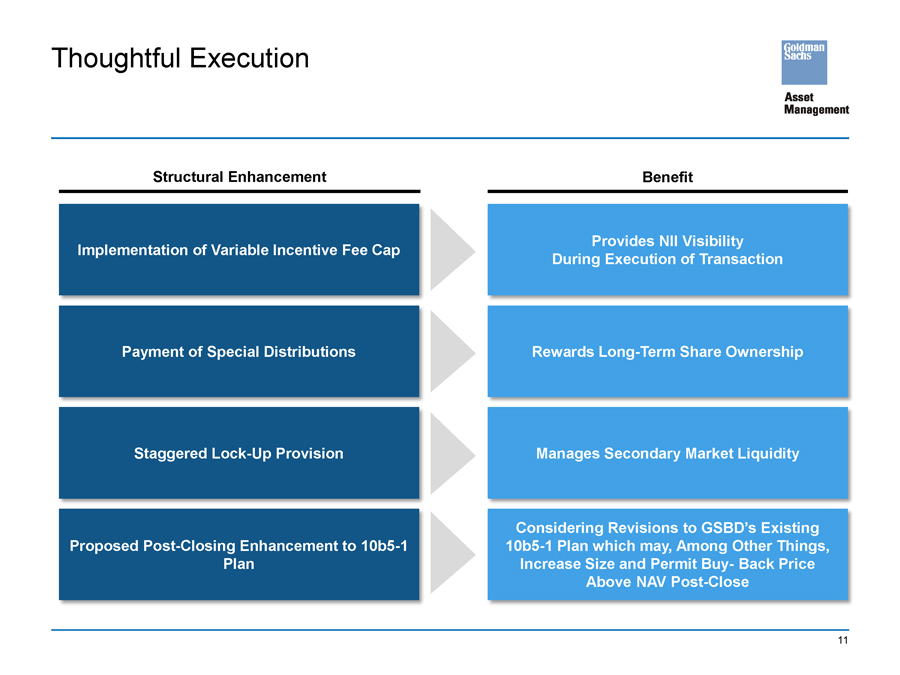

Thoughtful Execution Structural Enhancement Implementation of Variable Incentive Fee Cap Payment of Special Distributions StaggeredLock-Up Provision Proposed Post-Closing Enhancement to10b5-1 Plan Benefit Provides NII Visibility During Execution of Transaction Rewards Long-Term Share Ownership Manages Secondary Market Liquidity Considering Revisions to GSBD’s Existing10b5-1 Plan which may, Among Other Things, Increase Size and PermitBuy- Back Price Above NAV Post-Close 11

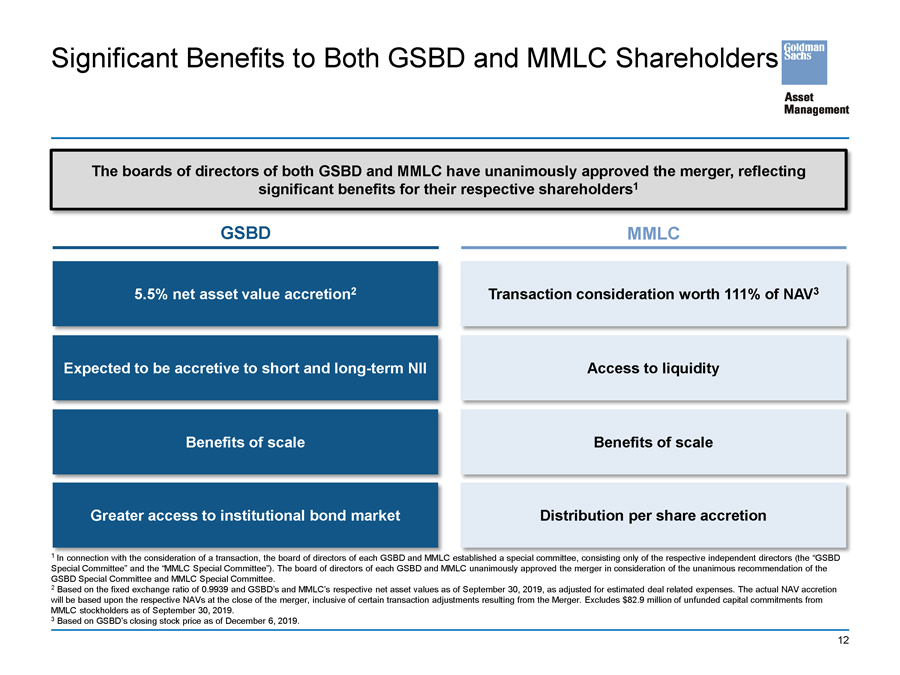

Significant Benefits to Both GSBD and MMLC Shareholders The boards of directors of both GSBD and MMLC have unanimously approved the merger, reflecting significant benefits for their respective shareholders1 GSBD 5.5% net asset value accretion2 Expected to be accretive to short and long-term NII Benefits of scale Greater access to institutional bond market MMLC Transaction consideration worth 111% of NAV3 Access to liquidity Benefits of scale Distribution per share accretion In connection with the consideration of a transaction, the board of directors of each GSBD and MMLC established a special committee, consisting only of the respective independent directors (the “GSBD Special Committee” and the “MMLC Special Committee”). The board of directors of each GSBD and MMLC unanimously approved the merger in consideration of the unanimous recommendation of the GSBD Special Committee and MMLC Special Committee. 2 Based on the fixed exchange ratio of 0.9939 and GSBD’s and MMLC’s respective net asset values as of September 30, 2019, as adjusted for estimated deal related expenses. The actual NAV accretion will be based upon the respective NAVs at the close of the merger, inclusive of certain transaction adjustments resulting from the Merger. Excludes $82.9 million of unfunded capital commitments from MMLC stockholders as of September 30, 2019. 3 Based on GSBD’s closing stock price as of December 6, 2019. 12

Significantly Accretive to GSBD NAV Per Share While Delivering a Premium Valuation to MMLC Expected to be Accretive to Net Investment Income in Both Short-Term and Long-Term Improved Portfolio Metrics Increased Scale Provides Greater Access to Debt Capital Markets Thoughtful Execution 13

Disclosures Endnotes Slide 9: The discussion of the investment portfolio excludes an investment in a money market fund managed by an affiliate of The Goldman Sachs Group, Inc. 1 Measured on total investments at fair value and commitments. 2 Computed based on the (a) annual actual interest rate or yield earned plus amortization of fees and discounts on the performing debt and other income producing investments, divided by (b) the total investments (including investments onnon-accrual andnon-incoming producing investments) at amortized cost or fair value, respectively. 3 The fixed versus floating composition has been calculated as a percentage of performing debt investments, including income producing preferred stock investments. 4 For a particular portfolio company, EBITDA typically represents net income before net interest expense, income tax expense, depreciation and amortization. The net debt to EBITDA represents the ratio of a portfolio company’s total debt (net of cash) and excluding debt subordinated to GSBD’s, MMLC’s or thepro-forma combined company’s investment in a portfolio company, to a portfolio company’s EBITDA. The interest coverage ratio represents the ratio of a portfolio company’s EBITDA as a multiple of a portfolio company’s interest expense. Weighted average net debt to EBITDA is weighted based on the fair value of GSBD’s, MMLC’s or thepro-forma combined company’s debt investments, excluding investments where net debt to EBITDA may not be the appropriate measure of credit risk, such as cash collateralized loans and investments that are underwritten and covenanted based on recurring revenue. Weighted average interest coverage is weighted based on the fair value of GSBD’s, MMLC’s or thepro-forma combined company’s performing debt investments, excluding investments where EBITDA may not be the appropriate measure of credit risk, such as cash collateralized loans and investments that are underwritten and covenanted based on recurring revenue. Median EBITDA is based on GSBD’s, MMLC’s or thepro-forma combined company’s debt investments, excluding investments where EBITDA may not be the appropriate measure of credit risk, such as cash collateralized loans and investments that are underwritten and covenanted based on recurring revenue. As of September 30, 2019, investments where EBITDA may not be the appropriate measure of credit risk represented 23.0%, 28.8% and 26.1% of total debt investments at fair value for GSBD, MMLC and thepro-forma combined company, respectively. Portfolio company statistics are derived from the most recently available financial statements of each portfolio company as of the respective reported end date. Portfolio company statistics have not been independently verified by us and may reflect a normalized or adjusted amount. 5 Measured on a fair value basis. 14