UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-23226)

Listed Funds Trust

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Kent P. Barnes, Secretary

Listed Funds Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 10th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 516-1681

Registrant's telephone number, including area code

Date of fiscal year end: May 31

Date of reporting period: May 31, 2023

Item 1. Reports to Stockholders.

(a)

Wahed FTSE USA Shariah ETF

(HLAL)

Wahed Dow Jones Islamic World ETF

(UMMA)

ANNUAL REPORT

May 31, 2023

Wahed ETFs

Table of Contents

| | |

Shareholder Letter (Unaudited) | 2 |

Shareholder Expense Example (Unaudited) | 6 |

Performance Overview (Unaudited) | 7 |

Schedules of Investments | 9 |

Statements of Assets and Liabilities | 17 |

Statements of Operations | 18 |

Statements of Changes in Net Assets | 19 |

Financial Highlights | 21 |

Notes to Financial Statements | 23 |

Report of Independent Registered Public Accounting Firm | 31 |

Board Consideration and Approval of Continuation of Advisory Agreement (Unaudited) | 32 |

Review of Liquidity Risk Management Program (Unaudited) | 34 |

Trustees and Officers of the Trust (Unaudited) | 35 |

Supplemental Information (Unaudited) | 37 |

Privacy Policy (Unaudited) | 38 |

1

Wahed ETFs

Shareholder Letter

May 31, 2023 (Unaudited)

To Our Shareholders,

We greet you again for with the hope that this letter finds you and your loved ones safe, secure and healthy. The annual period has once again proven volatile and unpredictable, not only for the Wahed FTSE Shariah ETF and Wahed Dow Jones Islamic World ETF (tickers: HLAL and UMMA, respectively, and also each referred to herein individually as a “Fund” and collectively as the “Funds”), but in broader financial markets as well. Though through the last two quarters of 2022, HLAL and UMMA experienced declines followed by a rebound in line with broader interest rate sensitive patterns, the advent of 2023 saw significant fluctuations in market sentiments across time and regions, regarding the path of monetary policy, the potential for a recession and the anticipated trajectory of markets in response, all the while markets steadily moved upward from 2022 lows.

HLAL

It will not be news to most shareholders that inflation and concerns of a recession have continued to be front and center for U.S. and international equities markets and therefore, the Funds as well. With the effects of inflation on the broader U.S. and global economy becoming ever more apparent in the third quarter of 2022, Federal Reserve (“Fed”) Chairman Jerome Powell indicated that interest rates would continue to be raised as needed to restore inflation back to target levels, even if doing so would likely slow GDP growth. The Chairman’s messaging resonated with markets, with equities pricing in slower growth and increasingly higher discount rates as the central banks of the United States, the United Kingdom, Europe, and other developed countries all proceeded to continue their aggressive monetary tightening cycle, as they had previously forewarned. As 2022 wound down, there were signs that inflation was coming under control across the developed world, and as a result all the key central banks began to slow down the pace of the hikes. The market’s hyperfocus on Fed action meant that indicators of economic weakness in the U.S. and abroad such as slowing economic growth and corporate earnings were often viewed positively as propelling the end of the interest rate hiking cycle, while indicators of economic strength such as low unemployment were often viewed negatively as prolonging the hiking cycle. After a relief rally brought on by the U.S. midterm elections and Powell’s suggestions that the Fed may slow the pace of interest rate hikes, market sentiment turned negative again in December despite signs that inflation was coming under control, as the Fed vowed to continue fighting inflation by raising interest rates and keeping rates higher for longer, which dampened the markets’ hopes of an economic recovery.

The arrival of 2023 saw signs that inflation was continuing to subside across the developed world while labor conditions remained stubbornly tight. As a result, the Fed was thought to be nearing the end of its historically aggressive hiking cycle. There was some confusion about how the tight labor market data was reconcilable with Big Tech and other public company layoffs that were dominating the headlines, suggesting that the economic impact of high interest rates may not yet have been fully reflected in the official data, and the Fed’s contractionary policy responses might be divergent from the conditions on the ground. By March, it became clear that the hiking cycle was having a significant impact on the regional banking sector in the U.S., where mark-to-market losses led to bank runs that resulted in the failure of Silicon Valley Bank and other institutions. The focus shifted in April to earnings so that market participants could assess the impact of recent macro events and policies on businesses in the first quarter and what that might suggest about the direction of the economy. Several big tech companies showed considerable resilience, which was attributable to the increasing role of artificial intelligence solutions in their business models. By May, the share prices of many of the tech companies had started to skyrocket. As the month of May wound to a close, market participants wavered back and forth on how much growth from AI should be priced in. As there was already debate on whether the markets were adequately pricing recession risk, now with the AI hype market participants began making direct comparisons to the tech bubble in the early 2000s. This fueled both the pessimism about the tech bubble eventually bursting and the optimism about how much runway still lies ahead before there are any real concerns about being in a bubble.

Of course, HLAL, faced with the difficulties of calendar 2022 and the wide variety of different if not opposing narratives in the first half of 2023, experienced significant volatility. However, being historically more resilient and better performing than broader U.S. equities markets, the Fund continued to do exactly that, providing well-performing Shariah-compliant equity exposure in a passive, buy-and-hold investment style. The higher exposure to the technology sector was a tailwind for HLAL throughout the 12-month period ending May 31, 2023, and we expect it may continue to benefit the Fund as the potential for artificial intelligence continues to be harnessed. Furthermore, the exclusion of financials and highly leveraged companies has resulted in better historical performance for all Islamic funds and indices through the 2008-2009 global financial crisis,

2

Wahed ETFs

Shareholder Letter

May 31, 2023 (Unaudited) (Continued)

and 2023 year to date performance of HLAL also benefited as the market worried about contagion from the regional bank weakness. As we view speculative activities by banks to be cyclically recurring events, we believe the exclusion of financials and highly leveraged companies will also be a long-term driver of outperformance through future cycles.

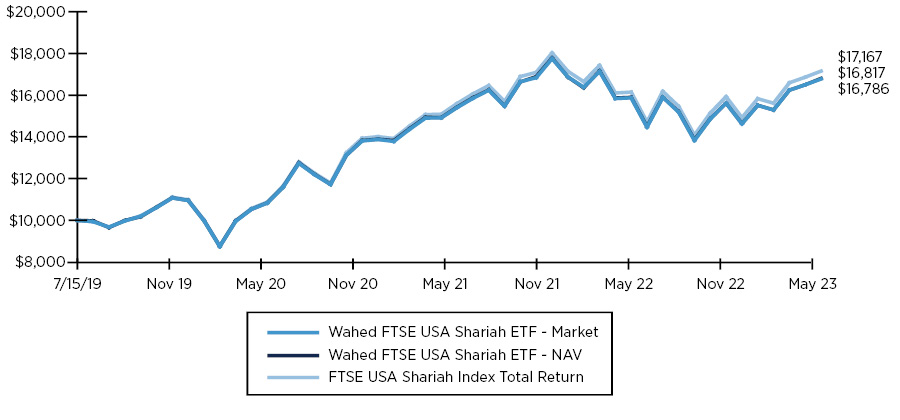

Per the chart below, as of May 31, 2023, HLAL displayed minimal tracking error to the underlying index (FTSE USA Shariah Index), well within the expected variance which is largely due to required fees and dividend distribution associated with the fund. Additionally, relative to conventional indices, HLAL outperformed broader indices.

| | | 1 Month

Total

Return | 3 Month

Total

Return | 6 Month

Total

Return | 9 Month

Total

Return | 1 Year

Total

Return | Cumulative

Total Return

Since Inception

(7/15/2019) |

Wahed FTSE USA Shariah ETF (Ticker: HLAL) | Market | 1.84% | 9.89% | 7.60% | 10.51% | 5.70% | 68.17% |

| | NAV | 1.67% | 9.69% | 7.39% | 10.46% | 5.70% | 67.86% |

FTSE USA Shariah Index Total Return | | 1.72% | 9.86% | 7.69% | 10.96% | 6.23% | 71.67% |

S&P 500 Index | | 0.43% | 5.75% | 3.31% | 7.05% | 2.89% | 48.40% |

MSCI World Islamic | | -1.78% | 4.14% | 2.53% | 10.35% | -0.09% | 24.78% |

Source: Bloomberg, US Bank as of 5/31/2023. Please note that returns over 1 year are not annualized.

Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-976-4747 for fund performance.

Market returns are based upon the midpoint of the bid/ask spread at 4:00 p.m. eastern time (when NAV is normally determined for most ETFs), and do not represent the returns you would receive if you traded shares at other times.

As the Fund continues to grow in size, we do not expect any changes to the Fund’s stated strategy, both in passively tracking its underlying index (FTSE USA Shariah Index Total Return), as well as continuing to validate the underlying shariah methodology with Yasaar / FTSE Russell. Furthermore, the Fund is expected to continue to hold at least 80% of its assets in the index securities and minimize its cash holdings.

UMMA

2023 also saw rapid movement in international equity markets and related volatility. This weighed on the performance of UMMA during the fiscal year ended May 31, 2023, as the Fund gained 4.0% at market.

In many ways, the economic factors contributing to the decline and recovery in U.S. markets were even more pronounced internationally, with market participants finding additional positive signs that global economic conditions may turn out better than expected. On the decline side, these economic factors in the third calendar quarter of 2022 included the strength of the U.S. dollar as a safe haven asset combined with the continuation of weakness in the UK and European political climate which led to foreign currency devaluation. Furthermore, China’s post-lockdown economy was sluggish as the country’s zero-COVID policy continued to impose constraints, which had an impact on other emerging equity markets as well. Interest rate hikes in developed countries and concerns about weakening can weigh even more heavily on emerging economies in the subsequent years. All these factors exacerbated the significant challenges for UMMA in Q3 2022 due to its international focus, and resulted in a quarterly return of -11.5% at market compared with a -4.4% return at market for HLAL over the same period. However on the recovery side, global economic factors elevated UMMA’s performance to a Q4 2022 return of 15.8% at market as compared with 5.6% at market for HLAL over the same period. These factors included China easing pandemic restrictions and reopening its economy and renewed optimism for the semiconductor sector, along with economic indicators showing Euro-area inflation beginning to slow down. The Japanese economy, facing an aging population, experienced less inflation than in other parts of the developed world which was supportive of asset prices in Japan, with the Asia Pacific region appearing closer to the growth phase of the economic cycle than the U.S. and Europe.

3

Wahed ETFs

Shareholder Letter

May 31, 2023 (Unaudited) (Continued)

With the arrival of 2023, and different countries being at different stages of their economic cycles, differences in market performance internationally arose. As January progressed, other developed and emerging markets rallied even further than the U.S., retracing some of the excess losses they faced in 2022 compared to the U.S. The momentum in emerging markets was strong to start the quarter as China came out of its zero-Covid strategy. Meanwhile, in Europe, economists no longer predicted a recession in 2023. The main contributor to these revisions was the surprisingly warm winter, which reduced the need for scarce energy reserves and lowered gas prices. Geopolitical tensions, on the other hand, dampened market sentiment in the quarter, as China and the U.S. struggled to see eye to eye on many issues. The U.S. dollar also weakened during the first quarter of 2023, as it tends to do after rising during selloffs on the equity market. As the second quarter commenced, inflation concerns started to resurface in Europe while in China, where market participants had expected that the end of China’s zero Covid policy would result in an economic boom, the economic and earnings data were somewhat disappointing in May. As a result of these factors, UMMA’s performance, which at 10.9% at market was at par with HLAL in the first quarter of 2023, then lagged HLAL in April and May. With UMMA’s maturation during the most recent fiscal year, we expect that it will continue to provide diversification benefits alongside HLAL, as U.S. and international (ex-U.S.) equities tend to outperform one another at different times.

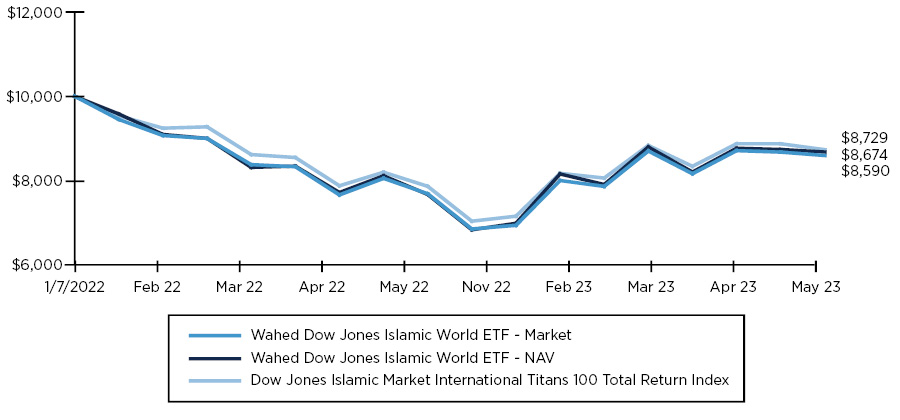

Per the chart below, during the fiscal year ended May 31, 2023, the Fund outperformed its underlying benchmark index (Dow Jones Islamic Market International Titans 100 Total Return Index), and since inception has performed well within the expected variance which were largely due to required fees and dividend distribution associated with the fund. Additionally, relative to conventional indices, UMMA outperformed broader indices during the year.

| | | 1 Month

Total

Return | 3 Month

Total

Return | 6 Month

Total

Return | 9 Month

Total

Return | 1 Year

Total

Return | Cumulative

Total Return

Since Inception

(1/6/2022) |

Wahed Dow Jones Islamic World ETF (Ticker: UMMA) | Market | -0.70% | 5.80% | 6.41% | 13.20% | 4.02% | -13.26% |

| | NAV | -0.93% | 5.33% | 7.43% | 11.85% | 3.20% | -14.10% |

Dow Jones Islamic Market International Titans 100 TR Index | | -1.39% | 4.75% | 6.88% | 11.09% | 2.18% | -12.71% |

ACWI ex-US | | -3.57% | 1.06% | 2.66% | 8.90% | -1.19% | -11.36% |

MSCI World ex-US | | -4.08% | 0.90% | 6.19% | 12.66% | 2.22% | -7.39% |

Source: Bloomberg, US Bank as of 5/31/2023. DJI100XT Index, ACWX US Equity, MXWOU Index. Please note that returns over 1 year are not annualized.

Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-976-4747 for fund performance.

Market returns are based upon the midpoint of the bid/ask spread at 4:00 p.m. eastern time (when NAV is normally determined for most ETFs), and do not represent the returns you would receive if you traded shares at other times.

4

Wahed ETFs

Shareholder Letter

May 31, 2023 (Unaudited) (Continued)

As we have said in the past, Wahed believes that investors should not be disadvantaged for wanting to invest in line with their faith. With HLAL, UMMA, and the continued expansion of our ETF products, we are excited to continue serving our shareholders through adversity and prosperity for years to come.

Sincerely,

Ahmar Shaikh

Head of North America

Wahed Invest LLC

DISCLAIMER

Must be preceded or accompanied by a prospectus.

One cannot invest in an index.

An investment in the Funds is subject to investment risk, including the possible loss of principal. The Funds may trade at a premium or discount to NAV. The Funds have the same risk as the underlying securities traded on the exchange throughout the day. Redemptions are limited and often commission are charged on every trade. The Funds’ shares may be bought and sold on an exchange through a brokerage account. Brokerage commissions and ETF expenses will reduce investment returns. There can be no assurance that an active trading market for ETF shares will be developed or maintained. The risks associated with the Funds are detailed in the “Principal Investment Risk” section of the prospectus and could include factors such as equity market risk, ETF risk, Market Capitalization risk, Market risk, new fund risk, non-diversification risk, passive investment risk, sector risk, tracking risk, ESG risk (as applicable), Shariah-Compliant Investment risk, tracking error risk, and/or underlying index risk.

For Wahed Dow Jones Islamic World ETF, applying ESG criteria to the investment process may exclude securities of certain issuers for non-investment reasons and therefore the Fund may forgo some market opportunities available to funds that do not use ESG or sustainability criteria. Emerging and Frontier markets are subject to greater market volatility, less liquidity, lower trading volume, political and economic instability, uncertainty regarding the existence of trading markets and more governmental limitations on foreign investment than more developed markets. Shariah-Compliant Investing and Islamic principles restrict the Fund’s ability to invest in certain market sectors, such as financial companies and conventional fixed-income securities, and reduce the size of the overall universe in which the Fund can invest. The strategy to reduce the investable universe may limit investment opportunities and adversely affect the Fund’s performance. Because Islamic principles preclude the use of interest-paying instruments, the Fund’s cash reserves do not earn income.

Please refer to the Schedules of Investments in this report for a complete list of Fund holdings.

The Wahed FTSE USA Shariah ETF (HLAL) and Wahed Dow Jones Islamic World ETF are distributed by Quasar Distributors, LLC.

5

Wahed ETFs

Shareholder Expense Example

May 31, 2023 (Unaudited)

As a shareholder of the Funds you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of fund shares; and (2) ongoing costs, including management fees and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in the Funds and to compare these costs with the ongoing costs of investing in other funds. The examples are based on an investment of $1,000 invested at the beginning of the period and held throughout the entire period (December 1, 2022 to May 31, 2023).

ACTUAL EXPENSES

The first line under each Fund in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for your Fund under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line in the table provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of Fund shares. Therefore, the second line in the table is useful in comparing ongoing Fund costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning

Account

Value

12/01/22 | Ending

Account

Value

05/31/23 | Annualized

Expense

Ratios | Expenses

Paid

During the

Period(1) |

Wahed FTSE USA Shariah ETF | | | | |

Actual | $1,000.00 | $ 1,073.90 | 0.50% | $2.59 |

Hypothetical (5% return before expenses) | $1,000.00 | $ 1,022.44 | 0.50% | $2.52 |

Wahed Dow Jones Islamic World ETF | | | | |

Actual | $1,000.00 | $ 1,074.30 | 0.65% | $3.36 |

Hypothetical (5% return before expenses) | $1,000.00 | $ 1,021.69 | 0.65% | $3.28 |

(1) | Expenses are calculated using the Fund’s annualized expense ratio, multiplied by the average account value for the period, multiplied by 182/365 (to reflect the six-month period). |

6

Wahed ETFs

Performance Overview

May 31, 2023 (Unaudited)

Hypothetical Growth of $10,000 Investment

(Since Commencement through 5/31/2023)

ANNUALIZED TOTAL RETURN FOR THE PERIODS ENDED MAY 31, 2023 |

Total Returns | 1 Year | 3 Year | Since

Commencement1 |

Wahed FTSE USA Shariah ETF—NAV | 5.70% | 16.82% | 14.28% |

Wahed FTSE USA Shariah ETF—Market | 5.70% | 16.87% | 14.34% |

FTSE USA Shariah Index Total Return | 6.23% | 17.54% | 14.95% |

1 | The Fund commenced operations on July 15, 2019. |

7

Wahed ETFs

Performance Overview

May 31, 2023 (Unaudited) (Continued)

Hypothetical Growth of $10,000 Investment

(Since Commencement through 5/31/2023)

ANNUALIZED TOTAL RETURN FOR THE PERIODS ENDED MAY 31, 2023 |

Total Returns | 1 Year | Since

Commencement1 |

Wahed Dow Jones Islamic World ETF—NAV | 3.20% | -10.30% |

Wahed Dow Jones Islamic World ETF—Market | 4.02% | -9.68% |

Dow Jones Islamic Market International Titans 100 Total Return Index | 2.18% | -9.27% |

1 | The Fund commenced operations on January 7, 2022. |

The performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. For the most recent month-end performance, please call (855) 976-4747. You cannot invest directly in an index. Shares are bought and sold at market price (closing price), not net asset value (“NAV”), and are not individually redeemed from the Fund. Market performance is determined using the bid/ask midpoint at 4:00 p.m. Eastern time when the NAV is typically calculated. Brokerage commissions will reduce returns. Returns shown include the reinvestment of all dividends and distribution. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The FTSE Global Equity Shariah Index Series has been designed to be used as the basis for Shariah compliant investment products that meet the requirements of investors globally. Using large and mid-cap stocks from the FTSE Global Equity Index Series as a base universe, constituents are then screened against Shariah principles and standards by subject-matter experts at Yasaar Limited, to create a more discrete, certified Shariah compliant index series.

The FTSE USA Shariah Index contains U.S. stocks that meet the aforementioned criteria and is a sub-index of the FTSE Global Equity Shariah Index Series. The FTSE USA Shariah Index has been fully certified as Shariah compliant through a fatwa (Islamic legal opinion) issued by Yasaar Limited.

The Dow Jones Islamic Market International Titans 100 Total Return Index is designed to measure the performance of the largest 100 stocks traded globally that pass rules-based screens for adherence to Shariah investment guidelines.

8

Wahed FTSE USA Shariah ETF

Schedule of Investments

May 31, 2023

| | Shares | | | Value | |

COMMON STOCKS — 98.8% | | | | | | | | |

Administrative and Support Services — 0.2% | | | | | | | | |

Baker Hughes Co. | | | 12,311 | | | $ | 335,475 | |

Robert Half International, Inc. | | | 1,429 | | | | 92,914 | |

Rollins, Inc. | | | 3,145 | | | | 123,661 | |

RXO, Inc. (a) | | | 1,545 | | | | 32,244 | |

| | | | | | | | 584,294 | |

Air Transportation — 0.1% | | | | | | | | |

Delta Air Lines, Inc. (a) | | | 2,210 | | | | 80,289 | |

United Airlines Holdings, Inc. (a) | | | 1,111 | | | | 52,734 | |

| | | | | | | | 133,023 | |

Ambulatory Health Care Services — 0.2% | | | | | | | | |

Laboratory Corp. of America Holdings | | | 1,140 | | | | 242,284 | |

Quest Diagnostics, Inc. | | | 1,515 | | | | 200,965 | |

| | | | | | | | 443,249 | |

Apparel Manufacturing — 0.2% | | | | | | | | |

Lululemon Athletica, Inc. (a) | | | 1,519 | | | | 504,202 | |

| | | | | | | | | |

Beverage and Tobacco Product Manufacturing — 1.7% | | | | | | | | |

Keurig Dr. Pepper, Inc. | | | 11,540 | | | | 359,125 | |

Monster Beverage Corp. (a) | | | 9,826 | | | | 576,000 | |

The Coca-Cola Co. | | | 52,658 | | | | 3,141,576 | |

| | | | | | | | 4,076,701 | |

Broadcasting (except Internet) — 0.1% | | | | | | | | |

Liberty Broadband Corp. - Class A (a) | | | 220 | | | | 16,251 | |

Liberty Broadband Corp. - Class C (a) | | | 1,590 | | | | 117,819 | |

| | | | | | | | 134,070 | |

| | Shares | | | Value | |

Building Material and Garden Equipment and Supplies Dealers — 0.1% | | | | | | | | |

Masterbrand, Inc. (a) | | | 1,764 | | | $ | 18,310 | |

Snap-on, Inc. | | | 653 | | | | 162,506 | |

| | | | | | | | 180,816 | |

Chemical Manufacturing — 12.2% | | | | | | | | |

Abbott Laboratories | | | 23,119 | | | | 2,358,138 | |

Air Products & Chemicals, Inc. | | | 3,018 | | | | 812,265 | |

Albemarle Corp. | | | 1,533 | | | | 296,681 | |

Biogen, Inc. (a) | | | 1,945 | | | | 576,517 | |

BioMarin Pharmaceutical, Inc. (a) | | | 2,535 | | | | 220,393 | |

Bio-Techne Corp. | | | 2,099 | | | | 171,677 | |

Bristol-Myers Squibb Co. | | | 28,640 | | | | 1,845,562 | |

CF Industries Holdings, Inc. | | | 2,674 | | | | 164,478 | |

Church & Dwight Co., Inc. | | | 3,244 | | | | 299,908 | |

Dow, Inc. | | | 9,568 | | | | 466,727 | |

DuPont de Nemours, Inc. | | | 6,250 | | | | 419,938 | |

Eli Lilly & Co. | | | 11,298 | | | | 4,852,039 | |

FMC Corp. | | | 1,690 | | | | 175,895 | |

International Flavors & Fragrances, Inc. | | | 3,473 | | | | 268,428 | |

Linde PLC (b) | | | 6,684 | | | | 2,363,863 | |

Merck & Co., Inc. | | | 34,131 | | | | 3,768,404 | |

Moderna, Inc. (a) | | | 4,482 | | | | 572,396 | |

Pfizer, Inc. | | | 76,226 | | | | 2,898,113 | |

PPG Industries, Inc. | | | 3,138 | | | | 411,988 | |

Regeneron Pharmaceuticals, Inc. (a) | | | 1,391 | | | | 1,023,164 | |

The Estee Lauder Cos., Inc. | | | 3,060 | | | | 563,132 | |

The Mosaic Co. | | | 4,678 | | | | 149,509 | |

The Procter & Gamble Co. | | | 31,727 | | | | 4,521,097 | |

West Pharmaceutical Services, Inc. | | | 992 | | | | 331,953 | |

Westlake Chemical Corp. | | | 438 | | | | 45,530 | |

| | | | | | | | 29,577,795 | |

Clothing and Clothing Accessories Stores — 0.7% | | | | | | | | |

Ross Stores, Inc. | | | 4,502 | | | | 466,497 | |

The TJX Cos., Inc. | | | 15,709 | | | | 1,206,294 | |

| | | | | | | | 1,672,791 | |

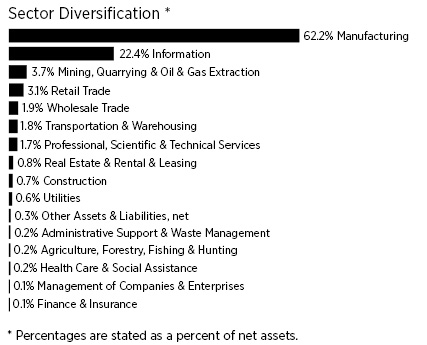

Computer and Electronic Product Manufacturing — 32.8% (c) | | | | | | | | |

Advanced Micro Devices, Inc. (a) | | | 21,554 | | | | 2,547,898 | |

Agilent Technologies, Inc. | | | 3,951 | | | | 457,012 | |

Alphabet, Inc. - Class A (a) | | | 80,848 | | | | 9,933,794 | |

Alphabet, Inc. - Class C (a) | | | 70,384 | | | | 8,683,274 | |

Analog Devices, Inc. | | | 6,818 | | | | 1,211,490 | |

Apple, Inc. | | | 202,282 | | | | 35,854,485 | |

Bio-Rad Laboratories, Inc. - Class A (a) | | | 289 | | | | 107,898 | |

Cisco Systems, Inc. | | | 55,231 | | | | 2,743,324 | |

The accompanying notes are an integral part of the financial statements.

9

Wahed FTSE USA Shariah ETF

Schedule of Investments

May 31, 2023 (Continued)

| | Shares | | | Value | |

Computer and Electronic Product Manufacturing — 32.8% (c) (continued) | | | | | | | | |

Danaher Corp. | | | 8,724 | | | $ | 2,003,205 | |

Dell Technologies, Inc. | | | 3,207 | | | | 143,706 | |

Fortinet, Inc. (a) | | | 8,568 | | | | 585,451 | |

Fortive Corp. | | | 4,883 | | | | 317,932 | |

GE Healthcare Technologies, Inc. | | | 4,764 | | | | 378,786 | |

GlobalFoundries, Inc. (a)(b) | | | 689 | | | | 40,189 | |

Hologic, Inc. (a) | | | 3,174 | | | | 250,397 | |

HP, Inc. | | | 13,323 | | | | 387,166 | |

Illumina, Inc. (a) | | | 2,109 | | | | 414,735 | |

Intel Corp. | | | 56,129 | | | | 1,764,696 | |

Juniper Networks, Inc. | | | 4,300 | | | | 130,591 | |

Lam Research Corp. | | | 1,796 | | | | 1,107,593 | |

Marvell Technology, Inc. | | | 11,439 | | | | 669,067 | |

Masimo Corp. (a) | | | 635 | | | | 102,768 | |

Medtronic PLC (b) | | | 17,929 | | | | 1,483,804 | |

Micron Technology, Inc. | | | 14,471 | | | | 986,922 | |

NetApp, Inc. | | | 2,922 | | | | 193,875 | |

ON Semiconductor Corp. (a) | | | 5,825 | | | | 486,970 | |

QUALCOMM, Inc. | | | 15,043 | | | | 1,706,027 | |

Revvity, Inc. | | | 1,725 | | | | 198,927 | |

Roper Technologies, Inc. | | | 1,410 | | | | 640,450 | |

Teradyne, Inc. | | | 2,101 | | | | 210,499 | |

Thermo Fisher Scientific, Inc. | | | 5,268 | | | | 2,678,567 | |

Trane Technologies PLC (b) | | | 3,160 | | | | 515,807 | |

Trimble, Inc. (a) | | | 3,355 | | | | 156,578 | |

Western Digital Corp. (a) | | | 4,260 | | | | 164,990 | |

Zebra Technologies Corp. - Class A (a) | | | 693 | | | | 181,961 | |

| | | | | | | | 79,440,834 | |

Construction of Buildings — 0.5% | | | | | | | | |

DR Horton, Inc. | | | 4,149 | | | | 443,279 | |

Lennar Corp. - Class A | | | 3,375 | | | | 361,530 | |

Lennar Corp. - Class B | | | 189 | | | | 17,870 | |

NVR, Inc. (a) | | | 37 | | | | 205,506 | |

PulteGroup, Inc. | | | 2,901 | | | | 191,698 | |

| | | | | | | | 1,219,883 | |

Couriers and Messengers — 0.9% | | | | | | | | |

FedEx Corp. | | | 2,867 | | | | 624,949 | |

United Parcel Service, Inc. - Class B | | | 9,970 | | | | 1,664,990 | |

| | | | | | | | 2,289,939 | |

Data Processing, Hosting and Related Services — 0.4% | | | | | | | | |

Fiserv, Inc. (a) | | | 7,936 | | | | 890,340 | |

| | | | | | | | | |

| | Shares | | | Value | |

Electrical Equipment, Appliance and Component Manufacturing — 0.2% | | | | | | | | |

Generac Holdings, Inc. (a) | | | 853 | | | $ | 92,909 | |

Rockwell Automation, Inc. | | | 1,507 | | | | 419,850 | |

Whirlpool Corp. | | | 708 | | | | 91,537 | |

| | | | | | | | 604,296 | |

Fabricated Metal Product Manufacturing — 0.5% | | | | | | | | |

Emerson Electric Co. | | | 7,735 | | | | 600,855 | |

Nucor Corp. | | | 3,442 | | | | 454,551 | |

Stanley Black & Decker, Inc. | | | 2,029 | | | | 152,114 | |

| | | | | | | | 1,207,520 | |

Food Manufacturing — 0.9% | | | | | | | | |

Archer-Daniels-Midland Co. | | | 7,393 | | | | 522,315 | |

Bunge Ltd. (b) | | | 1,906 | | | | 176,572 | |

Mondelez International, Inc. - Class A | | | 18,490 | | | | 1,357,351 | |

The JM Smucker Co. | | | 1,384 | | | | 202,881 | |

| | | | | | | | 2,259,119 | |

Funds, Trusts and Other Financial Vehicles — 0.1% | | | | | | | | |

Garmin Ltd. (b) | | | 2,083 | | | | 214,861 | |

| | | | | | | | | |

Gasoline Stations — 1.6% | | | | | | | | |

Chevron Corp. | | | 26,108 | | | | 3,932,387 | |

| | | | | | | | | |

General Merchandise Stores — 0.2% | | | | | | | | |

Burlington Stores, Inc. (a) | | | 880 | | | | 132,405 | |

Dollar Tree, Inc. (a) | | | 2,735 | | | | 368,897 | |

| | | | | | | | 501,302 | |

Health and Personal Care Stores — 0.2% | | | | | | | | |

Ulta Beauty, Inc. (a) | | | 654 | | | | 268,029 | |

Walgreens Boots Alliance, Inc. | | | 9,827 | | | | 298,446 | |

| | | | | | | | 566,475 | |

Leather and Allied Product Manufacturing — 0.7% | | | | | | | | |

NIKE, Inc. - Class B | | | 16,185 | | | | 1,703,633 | |

| | | | | | | | | |

Machinery Manufacturing — 1.4% | | | | | | | | |

Applied Materials, Inc. | | | 11,283 | | | | 1,504,024 | |

Carrier Global Corp. | | | 11,470 | | | | 469,123 | |

Cummins, Inc. | | | 1,854 | | | | 378,976 | |

Dover Corp. | | | 1,855 | | | | 247,327 | |

IDEX Corp. | | | 1,036 | | | | 206,330 | |

Ingersoll Rand, Inc. | | | 5,348 | | | | 303,018 | |

Xylem, Inc. | | | 2,470 | | | | 247,494 | |

| | | | | | | | 3,356,292 | |

The accompanying notes are an integral part of the financial statements.

10

Wahed FTSE USA Shariah ETF

Schedule of Investments

May 31, 2023 (Continued)

| | Shares | | | Value | |

Management of Companies and Enterprises — 0.1% | | | | | | | | |

LyondellBasell Industries NV - Class A (b) | | | 3,456 | | | $ | 295,626 | |

| | | | | | | | | |

Merchant Wholesalers Durable Goods — 1.3% | | | | | | | | |

Copart, Inc. (a) | | | 5,747 | | | | 503,380 | |

Fastenal Co. | | | 7,776 | | | | 418,738 | |

Flex Ltd. (a)(b) | | | 6,124 | | | | 155,488 | |

Genuine Parts Co. | | | 1,828 | | | | 272,244 | |

Henry Schein, Inc. (a) | | | 1,820 | | | | 134,498 | |

Johnson Controls International PLC (b) | | | 9,133 | | | | 545,240 | |

LKQ Corp. | | | 3,402 | | | | 179,456 | |

TE Connectivity Ltd. (b) | | | 4,311 | | | | 528,011 | |

WW Grainger, Inc. | | | 611 | | | | 396,551 | |

| | | | | | | | 3,133,606 | |

Merchant Wholesalers Nondurable Goods — 0.6% | | | | | | | | |

AmerisourceBergen Corp. | | | 2,195 | | | | 373,479 | |

Cardinal Health, Inc. | | | 3,514 | | | | 289,202 | |

McKesson Corp. | | | 1,840 | | | | 719,146 | |

| | | | | | | | 1,381,827 | |

Mining (except Oil and Gas) — 0.7% | | | | | | | | |

Freeport-McMoRan, Inc. | | | 19,177 | | | | 658,538 | |

Martin Marietta Materials, Inc. | | | 817 | | | | 325,199 | |

Newmont Goldcorp Corp. | | | 10,150 | | | | 411,582 | |

Southern Copper Corp. | | | 996 | | | | 66,503 | |

Vulcan Materials Co. | | | 1,814 | | | | 354,637 | |

| | | | | | | | 1,816,459 | |

Miscellaneous Manufacturing — 4.8% | | | | | | | | |

3M Co. | | | 7,356 | | | | 686,388 | |

Align Technology, Inc. (a) | | | 1,067 | | | | 301,598 | |

Becton Dickinson and Co. | | | 3,790 | | | | 916,270 | |

Boston Scientific Corp. (a) | | | 19,286 | | | | 992,843 | |

DENTSPLY SIRONA, Inc. | | | 2,898 | | | | 104,676 | |

Edwards Lifesciences Corp. (a) | | | 8,385 | | | | 706,269 | |

Johnson & Johnson | | | 35,504 | | | | 5,505,250 | |

STERIS PLC (b) | | | 1,344 | | | | 268,760 | |

Stryker Corp. | | | 4,693 | | | | 1,293,297 | |

Teleflex, Inc. | | | 616 | | | | 144,606 | |

The Cooper Cos., Inc. | | | 649 | | | | 241,123 | |

Zimmer Biomet Holdings, Inc. | | | 2,826 | | | | 359,863 | |

| | | | | | | | 11,520,943 | |

Miscellaneous Store Retailers — 0.1% | | | | | | | | |

Tractor Supply Co. | | | 1,453 | | | | 304,534 | |

| | | | | | | | | |

| | Shares | | | Value | |

Motion Picture and Sound Recording Industries — 0.1% | | | | | | | | |

Take-Two Interactive Software, Inc. (a) | | | 2,137 | | | $ | 294,329 | |

| | | | | | | | | |

Motor Vehicle and Parts Dealers — 0.0% (d) | | | | | | | | |

Advance Auto Parts, Inc. | | | 812 | | | | 59,187 | |

| | | | | | | | | |

Nonmetallic Mineral Product Manufacturing — 0.2% | | | | | | | | |

Corning, Inc. | | | 9,697 | | | | 298,765 | |

Mohawk Industries, Inc. (a) | | | 708 | | | | 65,164 | |

| | | | | | | | 363,929 | |

Nonstore Retailers — 0.1% | | | | | | | | |

eBay, Inc. | | | 7,178 | | | | 305,352 | |

| | | | | | | | | |

Oil and Gas Extraction — 1.5% | | | | | | | | |

Coterra Energy, Inc. | | | 10,688 | | | | 248,496 | |

Devon Energy Corp. | | | 8,876 | | | | 409,184 | |

EOG Resources, Inc. | | | 7,810 | | | | 837,935 | |

Marathon Oil Corp. | | | 8,799 | | | | 194,986 | |

Occidental Petroleum Corp. | | | 10,744 | | | | 619,499 | |

Phillips 66 | | | 6,295 | | | | 576,685 | |

Pioneer Natural Resources Co. | | | 3,185 | | | | 635,216 | |

| | | | | | | | 3,522,001 | |

Other Information Services — 3.3% | | | | | | | | |

Meta Platforms, Inc. - Class A (a) | | | 29,908 | | | | 7,917,246 | |

| | | | | | | | | |

Paper Manufacturing — 0.2% | | | | | | | | |

International Paper Co. | | | 4,902 | | | | 144,315 | |

Packaging Corp. of America | | | 1,246 | | | | 154,541 | |

Westrock Co. | | | 3,503 | | | | 98,119 | |

| | | | | | | | 396,975 | |

Petroleum and Coal Products Manufacturing — 2.8% | | | | | | | | |

Exxon Mobil Corp. | | | 55,641 | | | | 5,685,397 | |

Marathon Petroleum Corp. | | | 6,095 | | | | 639,427 | |

Valero Energy Corp. | | | 5,198 | | | | 556,394 | |

| | | | | | | | 6,881,218 | |

Primary Metal Manufacturing — 0.1% | | | | | | | | |

Steel Dynamics, Inc. | | | 2,146 | | | | 197,217 | |

| | | | | | | | | |

The accompanying notes are an integral part of the financial statements.

11

Wahed FTSE USA Shariah ETF

Schedule of Investments

May 31, 2023 (Continued)

| | Shares | | | Value | |

Professional, Scientific and Technical Services — 2.0% | | | | | | | | |

Amdocs Ltd. (b) | | | 1,486 | | | $ | 139,937 | |

Eaton Corp. PLC (b) | | | 5,347 | | | | 940,537 | |

Exact Sciences Corp. (a) | | | 2,444 | | | | 199,381 | |

F5, Inc. (a) | | | 796 | | | | 117,474 | |

Gartner, Inc. (a) | | | 1,039 | | | | 356,231 | |

Global Payments, Inc. | | | 3,459 | | | | 337,910 | |

Horizon Therapeutics PLC (a)(b) | | | 2,898 | | | | 289,887 | |

ICON PLC (a)(b) | | | 1,094 | | | | 233,055 | |

Omnicom Group, Inc. | | | 2,710 | | | | 238,995 | |

Palo Alto Networks, Inc. (a) | | | 4,013 | | | | 856,334 | |

Paychex, Inc. | | | 4,313 | | | | 452,563 | |

Paycom Software, Inc. | | | 646 | | | | 180,964 | |

The Interpublic Group of Cos., Inc. | | | 5,247 | | | | 195,136 | |

VMware, Inc. - Class A (a) | | | 2,847 | | | | 388,018 | |

| | | | | | | | 4,926,422 | |

Publishing Industries (except Internet) — 17.7% | | | | | | | | |

Adobe, Inc. (a) | | | 6,059 | | | | 2,531,390 | |

Akamai Technologies, Inc. (a) | | | 2,042 | | | | 188,109 | |

ANSYS, Inc. (a) | | | 1,157 | | | | 374,394 | |

Autodesk, Inc. (a) | | | 2,941 | | | | 586,406 | |

Cadence Design Systems, Inc. (a) | | | 3,671 | | | | 847,670 | |

Ceridian HCM Holding, Inc. (a) | | | 1,841 | | | | 113,866 | |

Electronic Arts, Inc. | | | 3,668 | | | | 469,504 | |

Microsoft Corp. | | | 100,787 | | | | 33,097,443 | |

News Corp. - Class A | | | 5,155 | | | | 94,388 | |

News Corp. - Class B | | | 1,601 | | | | 29,586 | |

Okta, Inc. (a) | | | 2,031 | | | | 184,618 | |

PTC, Inc. (a) | | | 1,427 | | | | 191,789 | |

salesforce.com, Inc. (a) | | | 12,974 | | | | 2,898,132 | |

Synopsys, Inc. (a) | | | 2,038 | | | | 927,208 | |

Tyler Technologies, Inc. (a) | | | 550 | | | | 218,328 | |

Yandex NV - Class A (a)(b)(e)(f) | | | 3,809 | | | | — | |

ZoomInfo Technologies, Inc. (a) | | | 3,568 | | | | 88,237 | |

| | | | | | | | 42,841,068 | |

Specialty Trade Contractors — 0.1% | | | | | | | | |

Quanta Services, Inc. | | | 1,940 | | | | 344,505 | |

| | | | | | | | | |

Support Activities for Agriculture and Forestry — 0.2% | | | | | | | | |

Corteva, Inc. | | | 9,622 | | | | 514,681 | |

| | | | | | | | | |

| | Shares | | | Value | |

Support Activities for Mining — 1.5% | | | | | | | | |

ConocoPhillips | | | 16,543 | | | $ | 1,642,720 | |

Diamondback Energy, Inc. | | | 2,319 | | | | 294,861 | |

Halliburton Co. | | | 11,856 | | | | 339,674 | |

Hess Corp. | | | 3,818 | | | | 483,626 | |

Schlumberger Ltd. (b) | | | 19,156 | | | | 820,452 | |

| | | | | | | | 3,581,333 | |

Support Activities for Transportation — 0.2% | | | | | | | | |

Expeditors International of Washington, Inc. | | | 2,132 | | | | 235,181 | |

JB Hunt Transport Services, Inc. | | | 1,119 | | | | 186,839 | |

| | | | | | | | 422,020 | |

Telecommunications — 0.6% | | | | | | | | |

ResMed, Inc. | | | 1,911 | | | | 402,820 | |

T-Mobile U.S., Inc. (a) | | | 7,817 | | | | 1,072,883 | |

| | | | | | | | 1,475,703 | |

Transit and Ground Passenger Transportation — 0.4% | | | | | | | | |

Uber Technologies, Inc. (a) | | | 25,680 | | | | 974,042 | |

| | | | | | | | | |

Transportation Equipment Manufacturing — 3.5% | | | | | | | | |

Aptiv PLC (a)(b) | | | 3,560 | | | | 313,565 | |

Autoliv, Inc. | | | 1,079 | | | | 87,938 | |

BorgWarner, Inc. | | | 2,961 | | | | 131,261 | |

Gentex Corp. | | | 3,189 | | | | 83,743 | |

Lear Corp. | | | 812 | | | | 99,600 | |

PACCAR, Inc. | | | 6,861 | | | | 471,900 | |

Tesla, Inc. (a) | | | 34,865 | | | | 7,110,019 | |

Westinghouse Air Brake Technologies Corp. | | | 2,352 | | | | 217,866 | |

| | | | | | | | 8,515,892 | |

Truck Transportation — 0.2% | | | | | | | | |

Old Dominion Freight Line, Inc. | | | 1,344 | | | | 417,231 | |

| | | | | | | | | |

Utilities — 0.6% | | | | | | | | |

Avangrid, Inc. | | | 945 | | | | 35,466 | |

Constellation Energy Corp. | | | 4,484 | | | | 376,746 | |

First Solar, Inc. (a) | | | 1,385 | | | | 281,100 | |

NRG Energy, Inc. | | | 2,861 | | | | 96,673 | |

Sempra Energy | | | 4,224 | | | | 606,271 | |

Vistra Corp. | | | 4,889 | | | | 117,189 | |

| | | | | | | | 1,513,445 | |

TOTAL COMMON STOCKS (Cost $201,184,262) | | | | | | | 239,410,613 | |

| | | | | | | | | |

The accompanying notes are an integral part of the financial statements.

12

Wahed FTSE USA Shariah ETF

Schedule of Investments

May 31, 2023 (Continued)

| | Shares | | | Value | |

Real Estate Investment Trusts (REITs) — 0.9% | | | | | | | | |

Real Estate — 0.8% | | | | | | | | |

Alexandria Real Estate Equities, Inc. | | | 2,306 | | | $ | 261,639 | |

Prologis, Inc. | | | 12,378 | | | | 1,541,680 | |

Regency Centers Corp. | | | 2,353 | | | | 132,403 | |

| | | | | | | | 1,935,722 | |

Wood Product Manufacturing — 0.1% | | | | | | | | |

Weyerhaeuser Co. | | | 9,979 | | | | 285,998 | |

TOTAL REITS (Cost $2,225,425) | | | | | | | 2,221,720 | |

| | | | | | | | | |

TOTAL INVESTMENTS (Cost $203,409,687) — 99.7% | | | | | | | 241,632,333 | |

Other assets and liabilities, net — 0.3% | | | | | | | 820,293 | |

NET ASSETS — 100.0% | | | | | | $ | 242,452,626 | |

Percentages are stated as a percent of net assets.

PLC - Public Limited Company

(a) | Non-income producing security. |

(b) | Foreign issued security. |

(c) | To the extent the Fund invests more heavily in particular sectors of the economy, its performance will be especially sensitive to developments that significantly affect those sectors. |

(d) | Amount is less than 0.05%. |

(e) | Value determined based on estimated fair value. The value of this security totals $0, which represents 0.00% of total net assets. Classified as Level 3 in the fair value hierarchy. Please refer to Note 2 of the Notes to Financial Statements. |

(f) | Security has been deemed illiquid according to the Fund’s liquidity guidelines. The value of these securities total $0, which represents 0.00% of total net assets. |

The accompanying notes are an integral part of the financial statements.

13

Wahed Dow Jones Islamic World ETF

Schedule of Investments

May 31, 2023

| | Shares | | | Value | |

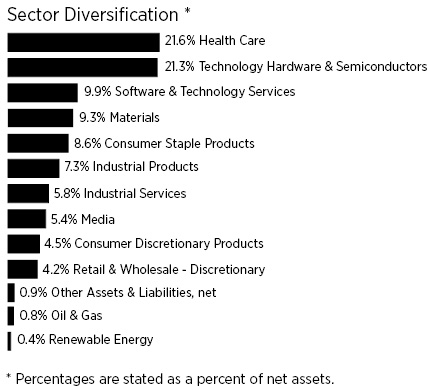

COMMON STOCKS — 99.1% (b) | | | | | | | | |

Aerospace and Defense — 0.7% | | | | | | | | |

Safran SA | | | 2,082 | | | $ | 300,625 | |

| | | | | | | | | |

Apparel and Textile Products — 3.1% | | | | | | | | |

adidas AG | | | 1,059 | | | | 171,043 | |

Compagnie Financière Richemont SA | | | 3,182 | | | | 503,154 | |

Hermès International | | | 205 | | | | 415,639 | |

Kering SA | | | 422 | | | | 224,204 | |

| | | | | | | | 1,314,040 | |

Automotive — 1.5% | | | | | | | | |

BYD Co. Ltd. - Class H | | | 5,179 | | | | 156,397 | |

Denso Corp. | | | 3,064 | | | | 188,842 | |

Ferrari NV | | | 786 | | | | 223,398 | |

NIO, Inc. - ADR (a) | | | 8,703 | | | | 65,534 | |

| | | | | | | | 634,171 | |

Biotechnology and Pharmaceuticals — 18.1% | | | | | | | | |

Astellas Pharma, Inc. | | | 11,259 | | | | 177,892 | |

AstraZeneca PLC | | | 6,356 | | | | 918,534 | |

CSL Ltd. | | | 2,972 | | | | 589,288 | |

Daiichi Sankyo Co. Ltd. | | | 12,006 | | | | 390,132 | |

Genmab A/S (a) | | | 388 | | | | 151,363 | |

GSK PLC | | | 24,182 | | | | 403,533 | |

Novartis AG | | | 14,808 | | | | 1,411,875 | |

Novo Nordisk A/S - Class B | | | 10,056 | | | | 1,606,898 | |

Roche Holding AG - Non-Voting Share | | | 4,429 | | | | 1,396,311 | |

Roche Holding AG - Voting Share | | | 149 | | | | 50,039 | |

Sanofi | | | 6,932 | | | | 701,181 | |

| | | | | | | | 7,797,046 | |

| | Shares | | | Value | |

Chemicals — 3.1% | | | | | | | | |

Air Liquide SA | | | 3,136 | | | $ | 523,692 | |

Givaudan SA | | | 41 | | | | 134,372 | |

Koninklijke DSM NV (e) | | | 1,017 | | | | 123,547 | |

LG Chem Ltd. | | | 263 | | | | 137,321 | |

Shin-Etsu Chemical Co. Ltd. | | | 12,940 | | | | 397,976 | |

| | | | | | | | 1,316,908 | |

Commercial Support Services — 2.9% | | | | | | | | |

Compass Group PLC | | | 26,045 | | | | 710,811 | |

Recruit Holdings Co. Ltd. | | | 10,478 | | | | 321,731 | |

Waste Connections, Inc. | | | 1,570 | | | | 214,277 | |

| | | | | | | | 1,246,819 | |

Construction Materials — 0.5% | | | | | | | | |

Sika AG | | | 880 | | | | 239,120 | |

| | | | | | | | | |

E-Commerce Discretionary — 2.6% | | | | | | | | |

JD.com, Inc. - ADR | | | 28,131 | | | | 917,071 | |

PDD Holdings, Inc. - ADR (a) | | | 3,140 | | | | 205,105 | |

| | | | | | | | 1,122,176 | |

Electrical Equipment — 3.3% | | | | | | | | |

ABB, Ltd. | | | 10,353 | | | | 376,679 | |

Assa Abloy AB - Class B | | | 5,937 | | | | 131,356 | |

Daikin Industries Ltd. | | | 1,769 | | | | 336,289 | |

Schneider Electric SE | | | 3,428 | | | | 589,631 | |

| | | | | | | | 1,433,955 | |

Food — 2.7% | | | | | | | | |

DSM-Firmenich AG (a) | | | 25 | | | | 2,773 | |

Nestle SA | | | 9,979 | | | | 1,177,853 | |

| | | | | | | | 1,180,626 | |

Health Care Facilities and Services — 0.9% | | | | | | | | |

Lonza Group AG | | | 424 | | | | 264,098 | |

Wuxi Biologics Cayman, Inc. (a)(c) | | | 20,127 | | | | 102,971 | |

| | | | | | | | 367,069 | |

Household Products — 5.9% | | | | | | | | |

Kao Corp. | | | 20,491 | | | | 715,275 | |

L’Oréal SA | | | 1,538 | | | | 654,224 | |

Reckitt Benckiser Group PLC | | | 4,484 | | | | 347,120 | |

Unilever PLC | | | 16,138 | | | | 805,860 | |

| | | | | | | | 2,522,479 | |

Industrial Support Services — 0.4% | | | | | | | | |

Ashtead Group PLC | | | 2,790 | | | | 169,439 | |

| | | | | | | | | |

Internet, Media and Services — 5.4% | | | | | | | | |

Meituan - Class B (a)(c) | | | 26,503 | | | | 373,089 | |

NAVER Corp. | | | 1,910 | | | | 287,094 | |

Prosus NV | | | 7,102 | | | | 466,173 | |

The accompanying notes are an integral part of the financial statements.

14

Wahed Dow Jones Islamic World ETF

Schedule of Investments

May 31, 2023 (Continued)

| | Shares | | | Value | |

Internet, Media and Services — 5.4% (continued) | | | | | | | | |

Tencent Holdings Ltd. | | | 30,406 | | | $ | 1,206,413 | |

| | | | | | | | 2,332,769 | |

Machinery — 3.3% | | | | | | | | |

Atlas Copco AB - Class A | | | 15,437 | | | | 224,174 | |

Atlas Copco AB - Class B | | | 9,493 | | | | 119,147 | |

FANUC Corp. | | | 5,663 | | | | 194,475 | |

Keyence Corp. | | | 1,233 | | | | 598,342 | |

SMC Corp. | | | 345 | | | | 185,396 | |

Techtronic Industries Co. Ltd. | | | 10,579 | | | | 98,178 | |

| | | | | | | | 1,419,712 | |

Medical Equipment and Devices — 2.6% | | | | | | | | |

Alcon, Inc. | | | 3,084 | | | | 238,380 | |

EssilorLuxottica SA | | | 1,826 | | | | 327,901 | |

Hoya Corp. | | | 2,164 | | | | 272,059 | |

Olympus Corp. | | | 7,894 | | | | 119,640 | |

Terumo Corp. | | | 4,685 | | | | 142,379 | |

| | | | | | | | 1,100,359 | |

Metals and Mining — 5.7% | | | | | | | | |

Anglo American PLC | | | 7,922 | | | | 218,315 | |

Barrick Gold Corp. | | | 10,299 | | | | 173,809 | |

BHP Group Ltd. | | | 30,842 | | | | 838,692 | |

Franco-Nevada Corp. | | | 1,189 | | | | 172,564 | |

Rio Tinto Ltd. | | | 3,179 | | | | 220,130 | |

Rio Tinto PLC | | | 8,898 | | | | 527,369 | |

Vale SA - ADR | | | 22,188 | | | | 281,344 | |

| | | | | | | | 2,432,223 | |

Oil and Gas Producers — 0.8% | | | | | | | | |

Canadian Natural Resources Ltd. | | | 6,644 | | | | 357,446 | |

Lukoil PJSC - ADR (a)(d)(e) | | | 3,928 | | | | — | |

Lukoil PJSC - GDR (a)(d)(e) | | | 224 | | | | — | |

| | | | | | | | 357,446 | |

Renewable Energy — 0.4% | | | | | | | | |

Vestas Wind Systems A/S (a) | | | 6,244 | | | | 177,294 | |

| | | | | | | | | |

Retail - Discretionary — 1.6% | | | | | | | | |

Fast Retailing Co. Ltd. | | | 1,119 | | | | 261,739 | |

Industria de Diseño Textil SA | | | 6,487 | | | | 216,395 | |

Wesfarmers Ltd. | | | 7,060 | | | | 217,798 | |

| | | | | | | | 695,932 | |

| | Shares | | | Value | |

Semiconductors — 15.4% | | | | | | | | |

ASML Holding NV | | | 2,478 | | | $ | 1,773,963 | |

Infineon Technologies AG | | | 52,565 | | | | 1,946,250 | |

SK Hynix, Inc. | | | 3,343 | | | | 273,535 | |

Taiwan Semiconductor Manufacturing Co. Ltd. - ADR | | | 22,757 | | | | 2,243,613 | |

Tokyo Electron Ltd. | | | 2,915 | | | | 402,986 | |

| | | | | | | | 6,640,347 | |

Software — 6.6% | | | | | | | | |

Constellation Software, Inc. | | | 110 | | | | 223,998 | |

Dassault Systemes SE | | | 4,198 | | | | 183,987 | |

SAP SE | | | 6,572 | | | | 856,042 | |

Shopify, Inc. - Class A (a) | | | 27,830 | | | | 1,590,198 | |

| | | | | | | | 2,854,225 | |

Technology Hardware — 5.8% | | | | | | | | |

Murata Manufacturing Co. Ltd. | | | 3,912 | | | | 229,571 | |

Nidec Corp. | | | 3,290 | | | | 163,423 | |

Samsung Electronics Co. Ltd. | | | 31,744 | | | | 1,707,683 | |

Samsung SDI Co. Ltd. | | | 335 | | | | 181,224 | |

Telefonaktiebolaget LM Ericsson - Class B | | | 18,865 | | | | 97,275 | |

Xiaomi Corp. - Class B (a)(c) | | | 83,642 | | | | 110,479 | |

| | | | | | | | 2,489,655 | |

Technology Services — 3.3% | | | | | | | | |

Adyen NV (a)(c) | | | 184 | | | | 299,500 | |

Amadeus IT Group SA | | | 2,473 | | | | 176,379 | |

Capgemini SE | | | 919 | | | | 159,502 | |

Experian PLC | | | 5,920 | | | | 207,791 | |

RELX PLC | | | 12,195 | | | | 379,374 | |

Wolters Kluwer NV | | | 1,578 | | | | 179,670 | |

| | | | | | | | 1,402,216 | |

Transportation and Logistics — 2.5% | | | | | | | | |

Canadian National Railway Co. | | | 3,652 | | | | 411,223 | |

Canadian Pacific Railway Ltd. (a) | | | 5,678 | | | | 432,084 | |

DSV A/S | | | 1,159 | | | | 222,751 | |

| | | | | | | | 1,066,058 | |

TOTAL COMMON STOCKS (Cost $44,794,440) | | | | | | | 42,612,709 | |

| | | | | | | | | |

TOTAL INVESTMENTS (Cost $44,794,440) — 99.1% | | | | | | | 42,612,709 | |

Other assets and liabilities, net — 0.9% | | | | | | | 368,094 | |

NET ASSETS — 100.0% | | | | | | $ | 42,980,803 | |

Percentages are stated as a percent of net assets.

ADR - American Depositary Receipt

GDR - Global Depositary Receipt

The accompanying notes are an integral part of the financial statements.

15

Wahed Dow Jones Islamic World ETF

Schedule of Investments

May 31, 2023 (Continued)

PLC - Public Limited Company

(a) | Non-income producing security. |

(b) | Foreign issued security. |

(c) | Security exempt from registration pursuant to Rule 144a under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration to qualified institutional investors. |

(d) | Value determined based on estimated fair value. The value of these securities total $0, which represents 0.00% of total net assets. Classified as Level 3 in the fair value hierarchy. Please refer to Note 2 of the Notes to Financial Statements. |

(e) | Security has been deemed illiquid according to the Fund’s liquidity guidelines. The value of these securities total $123,547 which represents 0.29% of total net assets. |

COUNTRY | Percentage of

Net Assets |

Switzerland | 13.5% |

Japan | 11.9% |

United Kingdom | 10.9% |

France | 9.5% |

Canada | 8.3% |

Netherlands | 7.1% |

Cayman Islands | 6.9% |

Germany | 6.9% |

Republic of Korea | 6.0% |

Taiwan | 5.2% |

Denmark | 5.0% |

Australia | 4.4% |

Sweden | 1.3% |

Spain | 0.9% |

Brazil | 0.7% |

China | 0.4% |

Hong Kong | 0.2% |

Russian Federation | 0.0% |

Total Country | 99.1% |

TOTAL INVESTMENTS | 99.1% |

Other assets and liabilities, net | 0.9% |

NET ASSETS | 100.0% |

The accompanying notes are an integral part of the financial statements.

16

Wahed ETFs

Statements of Assets and Liabilities

May 31, 2023

| | | Wahed FTSE USA

Shariah ETF | | | Wahed Dow Jones

Islamic World ETF | |

Assets | | | | | | | | |

Investments, at value (cost $203,409,687 and $44,794,440, respectively) | | $ | 241,632,333 | | | $ | 42,612,709 | |

Cash | | | 488,073 | | | | 220,413 | |

Dividends receivable | | | 412,816 | | | | 100,250 | |

Dividend withholding tax reclaims receivable | | | — | | | | 71,492 | |

Receivable for fund shares sold | | | 1,011,035 | | | | — | |

Total assets | | | 243,544,257 | | | | 43,004,864 | |

| | | | | | | | | |

Liabilities | | | | | | | | |

Payable to Adviser | | | 100,347 | | | | 24,061 | |

Payable for investment securities purchased | | | 991,284 | | | | — | |

Total liabilities | | | 1,091,631 | | | | 24,061 | |

Net Assets | | $ | 242,452,626 | | | $ | 42,980,803 | |

| | | | | | | | | |

Net Assets Consists of: | | | | | | | | |

Paid-in capital | | $ | 219,051,068 | | | $ | 46,578,304 | |

Total distributable earnings (accumulated losses) | | | 23,401,558 | | | | (3,597,501 | ) |

Net Assets | | $ | 242,452,626 | | | $ | 42,980,803 | |

| | | | | | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 6,025,000 | | | | 2,050,000 | |

Net Asset Value, redemption price and offering price per share | | $ | 40.24 | | | $ | 20.97 | |

The accompanying notes are an integral part of the financial statements.

17

Wahed ETFs

Statements of Operations

For the Year Ended May 31, 2023

| | | Wahed FTSE USA

Shariah ETF | | | Wahed Dow Jones

Islamic World ETF | |

Investment Income | | | | | | | | |

Dividend income (net of withholding tax and issuance fees of $- and $134,768, respectively) | | $ | 3,018,447 | | | $ | 708,903 | |

Dividend withholding tax reclaims | | | — | | | | 51,535 | |

Total investment income | | | 3,018,447 | | | | 760,438 | |

| | | | | | | | | |

Expenses | | | | | | | | |

Investment advisory fees | | | 951,849 | | | | 223,330 | |

Total expenses | | | 951,849 | | | | 223,330 | |

Net Investment Income | | | 2,066,598 | | | | 537,108 | |

| | | | | | | | | |

Realized and Unrealized Gain (Loss) on Investments and Foreign Currency | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | |

Investments | | | (8,444,153 | ) | | | (1,597,518 | ) |

Foreign currency transactions | | | — | | | | (2,296 | ) |

Net realized loss on investments and foreign currency transactions | | | (8,444,153 | ) | | | (1,599,814 | ) |

Net change in unrealized appreciation/depreciation on: | | | | | | | | |

Investments | | | 21,521,909 | | | | 2,961,613 | |

Foreign currency translation | | | — | | | | (778 | ) |

Net change in unrealized appreciation/depreciation on investments and foreign currency translation | | | 21,521,909 | | | | 2,960,835 | |

Net realized and unrealized gain on investments | | | 13,077,756 | | | | 1,361,021 | |

Net increase in net assets from operations | | $ | 15,144,354 | | | $ | 1,898,129 | |

The accompanying notes are an integral part of the financial statements.

18

Wahed FTSE USA Shariah ETF

Statements of Changes in Net Assets

| | | Year Ended

May 31, 2023 | | | Year Ended

May 31, 2022 | |

From Operations | | | | | | | | |

Net investment income | | $ | 2,066,598 | | | $ | 1,539,832 | |

Net realized gain (loss) on investments | | | (8,444,153 | ) | | | 8,424,889 | |

Net change in unrealized appreciation/depreciation on investments | | | 21,521,909 | | | | (3,373,278 | ) |

Net increase in net assets resulting from operations | | | 15,144,354 | | | | 6,591,443 | |

| | | | | | | | | |

From Distributions | | | | | | | | |

Distributable earnings | | | (2,037,392 | ) | | | (1,384,308 | ) |

Total distributions | | | (2,037,392 | ) | | | (1,384,308 | ) |

| | | | | | | | | |

From Capital Share Transactions | | | | | | | | |

Proceeds from shares sold | | | 78,185,113 | | | | 79,475,180 | |

Cost of shares redeemed | | | (16,325,058 | ) | | | (26,702,197 | ) |

Net increase in net assets resulting from capital share transactions | | | 61,860,055 | | | | 52,772,983 | |

| | | | | | | | | |

Total Increase in Net Assets | | | 74,967,017 | | | | 57,980,118 | |

| | | | | | | | | |

Net Assets | | | | | | | | |

Beginning of year | | | 167,485,609 | | | | 109,505,491 | |

End of year | | $ | 242,452,626 | | | $ | 167,485,609 | |

| | | | | | | | | |

Changes in Shares Outstanding | | | | | | | | |

Shares outstanding, beginning of year | | | 4,350,000 | | | | 3,000,000 | |

Shares sold | | | 2,125,000 | | | | 2,000,000 | |

Shares redeemed | | | (450,000 | ) | | | (650,000 | ) |

Shares outstanding, end of year | | | 6,025,000 | | | | 4,350,000 | |

The accompanying notes are an integral part of the financial statements.

19

Wahed Dow Jones Islamic World ETF

Statements of Changes in Net Assets

| | | Year Ended

May 31, 2023 | | | Period Ended

May 31, 2022(1) | |

From Operations | | | | | | | | |

Net investment income | | $ | 537,108 | | | $ | 317,520 | |

Net realized gain (loss) on investments and foreign currency transactions | | | (1,599,814 | ) | | | 70,376 | |

Net change in unrealized appreciation/depreciation on investments and foreign currency translation | | | 2,960,835 | | | | (5,144,423 | ) |

Net increase (decrease) in net assets resulting from operations | | | 1,898,129 | | | | (4,756,527 | ) |

| | | | | | | | | |

From Distributions | | | | | | | | |

Distributable earnings | | | (576,603 | ) | | | (162,500 | ) |

Total distributions | | | (576,603 | ) | | | (162,500 | ) |

| | | | | | | | | |

From Capital Share Transactions | | | | | | | | |

Proceeds from shares sold | | | 9,578,095 | | | | 36,975,825 | |

Transaction fees (Note 4) | | | 3,719 | | | | 20,665 | |

Net increase in net assets resulting from capital share transactions | | | 9,581,814 | | | | 36,996,490 | |

| | | | | | | | | |

Total Increase in Net Assets | | | 10,903,340 | | | | 32,077,463 | |

| | | | | | | | | |

Net Assets | | | | | | | | |

Beginning of period | | | 32,077,463 | | | | — | |

End of period | | $ | 42,980,803 | | | $ | 32,077,463 | |

| | | | | | | | | |

Changes in Shares Outstanding | | | | | | | | |

Shares outstanding, beginning of period | | | 1,550,000 | | | | — | |

Shares sold | | | 500,000 | | | | 1,550,000 | |

Shares redeemed | | | — | | | | — | |

Shares outstanding, end of period | | | 2,050,000 | | | | 1,550,000 | |

(1) | The Fund commenced operations on January 7, 2022. |

The accompanying notes are an integral part of the financial statements.

20

Wahed FTSE USA Shariah ETF

Financial Highlights

For a Share Outstanding Throughout Each Period

| | | Year Ended

May 31, 2023 | | | Year Ended

May 31, 2022 | | | Year Ended

May 31, 2021 | | | Period Ended

May 31, 2020(1) | |

Net Asset Value, Beginning of Period | | $ | 38.50 | | | $ | 36.50 | | | $ | 26.00 | | | $ | 25.00 | |

| | | | | | | | | | | | | | | | | |

Income (Loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income(2) | | | 0.40 | | | | 0.40 | | | | 0.36 | | | | 0.40 | |

Net realized and unrealized gain on investments | | | 1.74 | | | | 1.96 | | | | 10.44 | | | | 0.90 | |

Total from investment operations | | | 2.14 | | | | 2.36 | | | | 10.80 | | | | 1.30 | |

| | | | | | | | | | | | | | | | | |

Less distributions paid: | | | | | | | | | | | | | | | | |

From net investment income | | | (0.40 | ) | | | (0.36 | ) | | | (0.30 | ) | | | (0.28 | ) |

From net realized gains | | | — | | | | — | | | | — | | | | (0.02 | ) |

Total distributions paid | | | (0.40 | ) | | | (0.36 | ) | | | (0.30 | ) | | | (0.30 | ) |

| | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | $ | 40.24 | | | $ | 38.50 | | | $ | 36.50 | | | $ | 26.00 | |

| | | | | | | | | | | | | | | | | |

Total return, at NAV(3)(5) | | | 5.70 | % | | | 6.43 | % | | | 41.70 | % | | | 5.30 | % |

Total return, at Market(4)(5) | | | 5.70 | % | | | 6.50 | % | | | 41.81 | % | | | 5.39 | % |

| | | | | | | | | | | | | | | | | |

Supplemental Data and Ratios: | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 242,453 | | | $ | 167,486 | | | $ | 109,505 | | | $ | 32,506 | |

| | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets(6) | | | 0.50 | % | | | 0.50 | % | | | 0.50 | % | | | 0.50 | % |

| | | | | | | | | | | | | | | | | |

Ratio of net investment income to average net assets(6) | | | 1.10 | % | | | 1.01 | % | | | 1.08 | % | | | 1.81 | % |

| | | | | | | | | | | | | | | | | |

Portfolio turnover rate (5)(7) | | | 29 | % | | | 16 | % | | | 19 | % | | | 15 | % |

(1) | The Fund commenced operations on July 15, 2019. |

(2) | Per share net investment income was calculated using average shares outstanding. |

(3) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to the differences between the market price of the shares and the net asset value per share of the Fund. |

(4) | Market value total return is calculated assuming an initial investment made at market value at the beginning of the period, reinvestment of all dividends and distributions at market value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price on the Nasdaq Stock Market. The composite closing price is the last reported sale, regardless of volume, and not an average price, and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the Nasdaq Stock Market. |

(5) | Not annualized for periods less than one year. |

(6) | Annualized for periods less than one year. |

(7) | Excludes in-kind transactions associated with creations and redemptions of the Fund. |

The accompanying notes are an integral part of the financial statements.

21

Wahed Dow Jones Islamic World ETF

Financial Highlights

For a Share Outstanding Throughout Each Period

| | | Year Ended

May 31, 2023 | | | Period Ended

May 31, 2022(1) | |

Net Asset Value, Beginning of Period | | $ | 20.70 | | | $ | 25.00 | |

| | | | | | | | | |

Income (Loss) from investment operations: | | | | | | | | |

Net investment income(2) | | | 0.31 | | | | 0.25 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 0.30 | | | | (4.44 | ) |

Total from investment operations | | | 0.61 | | | | (4.19 | ) |

| | | | | | | | | |

Less distributions paid: | | | | | | | | |

From net investment income | | | (0.34 | ) | | | (0.13 | ) |

Total distributions paid | | | (0.34 | ) | | | (0.13 | ) |

| | | | | | | | | |

Capital Share Transactions: | | | | | | | | |

Transaction fees (See Note 4) | | | 0.00 | (8) | | | 0.02 | |

| | | | | | | | | |

Net Asset Value, End of Period | | $ | 20.97 | | | $ | 20.70 | |

| | | | | | | | | |

Total return, at NAV(3)(5) | | | 3.20 | % | | | -16.76 | % |

Total return, at Market(4)(5) | | | 4.02 | % | | | -16.62 | % |

| | | | | | | | | |

Supplemental Data and Ratios: | | | | | | | | |

Net assets, end of period (000’s) | | $ | 42,981 | | | $ | 32,077 | |

| | | | | | | | | |

Ratio of expenses to average net assets(6) | | | 0.65 | % | | | 0.65 | % |

| | | | | | | | | |

Ratio of net investment income to average net assets(6) | | | 1.56 | % | | | 2.91 | % |

| | | | | | | | | |

Portfolio turnover rate (5)(7) | | | 11 | % | | | 8 | % |

(1) | The Fund commenced operations on January 7, 2022. |

(2) | Per share net investment income was calculated using average shares outstanding. |

(3) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to the differences between the market price of the shares and the net asset value per share of the Fund. |

(4) | Market value total return is calculated assuming an initial investment made at market value at the beginning of the period, reinvestment of all dividends and distributions at market value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price on the Nasdaq Stock Market. The composite closing price is the last reported sale, regardless of volume, and not an average price, and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the Nasdaq Stock Market. |

(5) | Not annualized for periods less than one year. |

(6) | Annualized for periods less than one year. |

(7) | Excludes in-kind transactions associated with creations of the Fund. |

The accompanying notes are an integral part of the financial statements.

22

Wahed ETFs

Notes to Financial Statements

May 31, 2023

1. ORGANIZATION

The Wahed FTSE USA Shariah ETF (“HLAL”) and Wahed Dow Jones Islamic World ETF (“UMMA”) (each a “Fund” and collectively, the “Funds”) are non-diversified series of Listed Funds Trust (the “Trust”), formerly Active Weighting Funds ETF Trust. The Trust was organized as a Delaware statutory trust on August 26, 2016, under a Declaration of Trust amended on December 21, 2018, and is registered with the U.S. Securities and Exchange Commission (the “SEC”) as an open-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

HLAL is a passively-managed exchange-traded fund (“ETF”). The Fund’s objective is to track the total return performance, before fees and expenses, of the FTSE USA Shariah Index (the “Index”). The Index is composed of common stocks of large and mid-capitalization U.S. companies the characteristics of which meet the requirements of the Shariah and are consistent with Islamic principles as interpreted by subject-matter experts.

UMMA is an actively-managed ETF. The Fund’s objective is to seek long-term capital appreciation. UMMA seeks to achieve its objective by investing in a portfolio of global companies (excluding U.S. domiciled companies) the characteristics of which meet the requirements of Shariah and are consistent with Islamic principles as interpreted by subject-matter experts. Wahed Invest LLC (“Wahed” or the “Adviser”), the Fund’s investment adviser, seeks to invest the Fund’s assets in securities similar to the components of, and to achieve returns similar to those of, the Dow Jones Islamic International Titans 100 Index (the “Index”). The Index is a data-driven index owned and maintained by S&P Dow Jones Indices, is designed to measure the stock performance of the largest ex-U.S. companies that have passed rules-based screens for adherence to Shariah investment guidelines.

2. SIGNIFICANT ACCOUNTING POLICIES

Each Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. Each Fund prepares its financial statements in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and follows the significant accounting policies described below.

Use of Estimates

The preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from these estimates.

Share Transactions

The net asset value (“NAV”) per share of each Fund will be equal to each Fund’s total assets minus each Fund’s total liabilities divided by the total number of shares outstanding. The NAV that is published will be rounded to the nearest cent. The NAV is determined as of the close of trading (generally, 4:00 p.m. Eastern Time) on each day the New York Stock Exchange (“NYSE”) is open for trading.

Fair Value Measurement

In calculating the NAV, each Fund’s exchange-traded equity securities will be valued at fair value, which will generally be determined using the last reported official closing or last trading price on the exchange or market on which the security is primarily traded at the time of valuation. Such valuations are typically categorized as Level 1 in the fair value hierarchy described below.

Securities listed on the NASDAQ Stock Market, Inc. are generally valued at the NASDAQ official closing price.

If market quotations are not readily available, or if it is determined that a quotation of a security does not represent fair value, then the security is valued at fair value as determined in good faith by the Adviser using procedures adopted by the Board of Trustees of the Trust (the “Board”). The circumstances in which a security may be fair valued include, among others: the occurrence of events that are significant to a particular issuer, such as mergers, restructurings or defaults; the occurrence of

23

Wahed ETFs

Notes to Financial Statements

May 31, 2023 (Continued)

events that are significant to an entire market, such as natural disasters in a particular region or government actions; trading restrictions on securities; thinly traded securities; and market events such as trading halts and early market closings. Due to the inherent uncertainty of valuations, fair values may differ significantly from the values that would have been used had an active market existed. Fair valuation could result in a different NAV than a NAV determined by using market quotations. Such valuations are typically categorized as Level 2 or Level 3 in the fair value hierarchy described below.

FASB ASC Topic 820, Fair Value Measurements and Disclosures (“ASC 820”) defines fair value, establishes a framework for measuring fair value in accordance with U.S. GAAP, and requires disclosure about fair value measurements. It also provides guidance on determining when there has been a significant decrease in the volume and level of activity for an asset or liability, when a transaction is not orderly, and how that information must be incorporated into fair value measurements. Under ASC 820, various inputs are used in determining the value of the Funds’ investments. These inputs are summarized in the following hierarchy:

| | ● | Level 1 — Unadjusted quoted prices in active markets for identical assets or liabilities that the Funds have the ability to access. |

| | ● | Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar securities, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| | ● | Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3).

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

Foreign securities, currencies and other assets denominated in foreign currencies are translated into U.S. dollars at the exchange rate of such currencies against the U.S. dollar using the applicable currency exchange rates as of the close of the NYSE, generally 4:00 p.m. Eastern Time.

All other securities and investments for which market values are not readily available, including restricted securities, and those securities for which it is inappropriate to determine prices in accordance with the aforementioned procedures, are valued at fair value as determined in good faith under procedures adopted by the Board, although the actual calculations may be done by others. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, or the appropriate stock exchange (for exchange-traded securities), analysis of the issuer’s financial statements or other available documents and, if necessary, available information concerning other securities in similar circumstances.

24

Wahed ETFs

Notes to Financial Statements

May 31, 2023 (Continued)