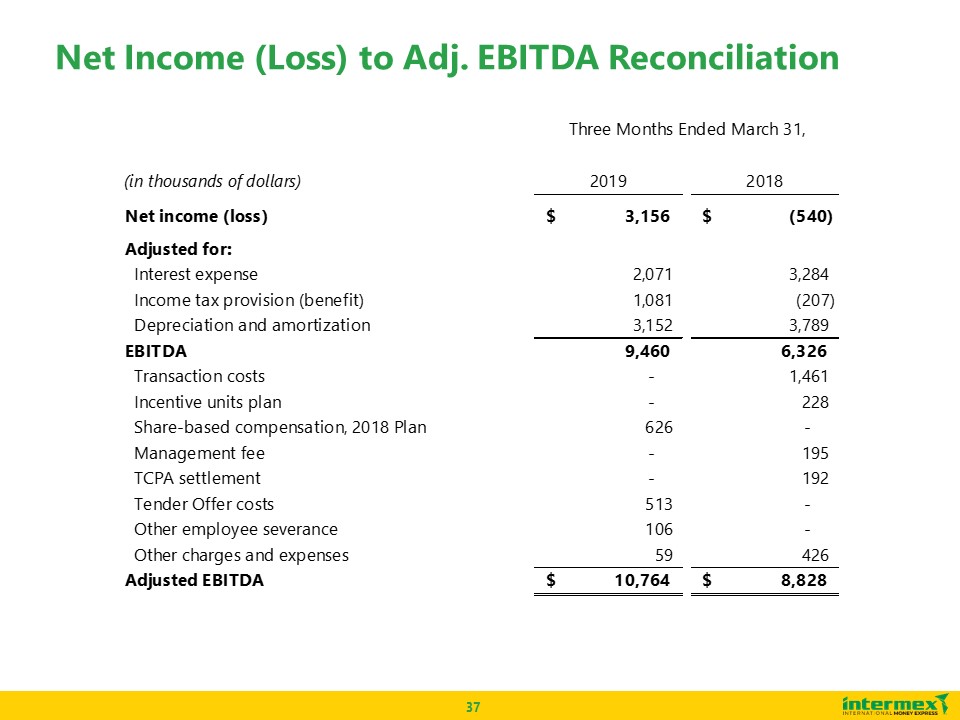

This presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which reflect our current view with respect to certain events that could have an effect on our future financial performance. These statements relate to expectations concerning matters that are not historical fact and may include the words or phrases such as “will,” “should,” “expects,” “believes,” “anticipates,” “plans,” “intends,” “estimates,” “approximately,” “our planning assumptions,” “future outlook,” and similar expressions. Except for historical information, matters discussed in such statements are forward-looking statements. All of these forward-looking statements are based largely on information currently available to our management and on our current expectations, assumptions, estimates, judgments and projections about our business and our industry, and are subject to various risks and uncertainties that could cause actual results to differ materially from historical results or those currently anticipated. While we believe these expectations, assumptions, estimates, judgments and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control. These and other important factors may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements, or could affect our share price. Accordingly, there is no assurance that our expectations will, in fact, occur or that our estimates or assumptions will be correct, and we caution investors and all others not to place undue reliance on such forward-looking statements. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include among other things, competition in the markets in which we operate; our ability to maintain agent relationships on terms consistent with those currently in place; our ability to maintain banking relationships necessary for us to conduct our business; credit risks from our agents and the financial institutions with which we do business; bank failures, sustained financial market illiquidity, or illiquidity at our clearing, cash management or custodial financial institutions; new technology or competitors that disrupt the current ecosystem; cyber-attacks or disruptions to our information technology, computer network systems and data centers; our success in developing and introducing new products, services and infrastructure; customer confidence in our brand and in consumer money transfers generally; our ability to maintain compliance with the regulatory requirements of the jurisdictions in which we operate or plan to operate; international political factors or implementation of tariffs, border taxes or restrictions on remittances or transfers of money out of the United States; changes in tax laws and unfavorable outcomes of tax positions we take; political instability, currency restrictions and devaluation in countries in which we operate or plan to operate; weakness in U.S. or international economic conditions; change or disruption in international migration patterns; our ability to protect our brand and intellectual property rights; our ability to retain key personnel; and other factors described in the “Risk Factors” section in periodic reports we file with the Securities and Exchange Commission. All statements other than statements of historical fact included in this press release are forward-looking statements including, but not limited to, expected financial outlook for the year 2019 and all forward-looking statements that are made or attributable to us are expressly qualified in their entirety by this cautionary notice. Any forward-looking statement that we make in this presentation speaks only as of the date of this presentation. We undertake no obligation to update or revise, or to publicly announce any update or revision to, any of the forward-looking statements made herein, whether as a result of new information, future events or otherwise except as required by law.This presentation includes certain non-GAAP financial measures, including Adjusted EBITDA, Adjusted EBITDA growth, Adjusted EBITDA margin and Revenue CAGR. These non-GAAP financial measures should be considered only as supplemental to, and not as superior to, financial measures prepared in accordance with U.S. GAAP. Please refer to Slides 37, 38 and 39 of this presentation for a reconciliation of Adjusted EBITDA to net income (loss). Adjusted EBITDA is defined as net income (loss) before depreciation and amortization, interest expense, income taxes, and also adjusted to add back certain charges and expenses, such as transaction costs and non-cash compensation costs, as these charges and expenses are not considered a part of our core business operations and are not an indicator of ongoing, future company performance. Safe Harbor Statement / Non-GAAP Financial Measures