Exhibit 99.1

EXHIBIT 99-1

September 21st, 2020

Mr. Neal Goldman

Chairman of the Board

Charles & Colvard, Ltd.

170 Southport Drive

Morrisville, NC 27560

Dear Neal:

Silver Ring Value Partners (“Silver Ring”) has been a shareholder of Charles & Colvard, Ltd. (“Charles & Colvard” or “Company”) since December 2016 and currently owns 2.85M shares representing approximately 9.8% of the common shares outstanding. I am writing this letter with several recommendations as well as a request that you and the Board nominate me and another prospective Board member who I am recommending in this letter to the board at this year’s Annual Meeting.

I want to thank you for the tremendous effort that you have put into guiding our Company during your tenure on the Board. Your hard work in a challenging environment is appreciated by me, and I am sure by other shareholders. I am positive that we would not be where we are today if it weren’t for your leadership.

Silver Ring invested in the Company because of a combination of valuable assets in the form of cash and inventory, as well as the potential for the core business to improve and generate a healthy and growing profit stream going forward. I believe that this approach will resonate with you given that in a 1998 interview you described your own investment approach as one “where we are looking for limited downside, but when the catalyst comes along that can really change the earnings power positively, then I can get significant capital appreciation.”i With the Company’s recent disclosure in its Form 10-K and on the fiscal Q4 2020 earnings conference call of a shift from an organic growth strategy to one that combines efforts at organic growth with acquisitions, I have become concerned that this is not the path towards optimal value realization at this point in time. Pursuing acquisitions risks lowering investors’ margin of safety by replacing cash, which serves to protect our downside, with uncertain investments that could distract management from their efforts to improve the core business. Instead, I recommend the following:

| • | The Company does not consider pursuing any acquisitions until the business has become solidly profitable on a sustained basis |

| • | The Board rigorously pursue an active sale process to sell the company to a strategic acquirer that is able to maximize its long-term value better than the Company can do on its own |

| • | The Board create additional, substantial incentives for the top management team so that in the event of a sale of the Company at a full and fair price they are appropriately rewarded for their efforts |

1

Silver Ring Value Partners Limited Partnership • One Boston Place, Suite 2600, Boston, MA 02108 • www.silverringvaluepartners.com

| • | The Company return the excess cash to shareholders once the business is solidly profitable and doing so will not put our Company in jeopardy |

| • | Management, under the leadership of CEO Don O’Connell, continue on its recently outlined operating strategy of lowering costs while finding creative ways to organically grow the business |

Acquisitions

Acquisitions are challenging under most circumstances, much more so in the current state of our Company. Given your extensive experience in financial markets, I do not need to remind you that the typical beneficiaries of sizable acquisitions have been the targets, not the acquirers. These deals, which collectively have destroyed shareholder value of the acquirers, have been done by smart executives and well-meaning Boards of Directors based on promises of value creation that frequently failed to materialize.

On top of that, we have a small company with a management team that is rightfully focused on turning our business around. The operating strategy outlined by CEO Don O’Connell on the latest earnings call is reasonable, but given the challenging external environment, will take a lot of management effort and attention to successfully execute. Splitting that attention between managing the business and deal-making risks weakening our Company’s execution at a key juncture in its history.

I do not want you to misinterpret what I am saying as an argument that acquisitions are never appropriate. However, I am concerned about potentially dissipating the downside protection for investors afforded by our cash position and the real risk of taking management’s focus away from creating value for the core business organically. What is the downside of considering acquisitions at a later point, from a position of strength once the business is on a more solid footing and generating consistent profits?

Active Sale Process

I commend you and the Board for rejecting the recently rumored bid of $1 per share, which clearly undervalued the company. Even in a liquidation scenario, our Company is worth at least that, given that its net cash + inventory per share are above $1.50 as of the end of the most recent quarter.

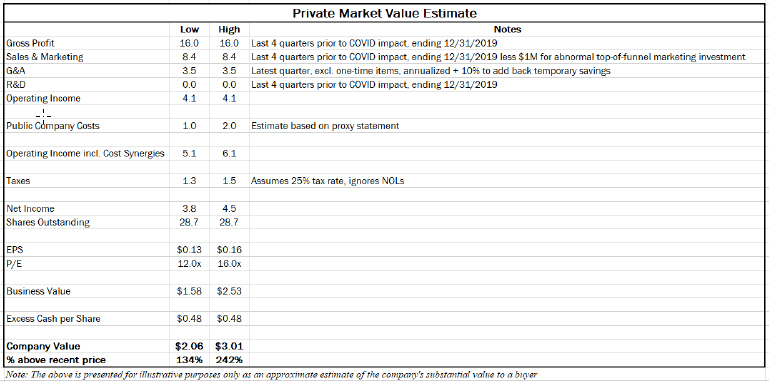

However, I would expect that to an acquirer our Company will be even more valuable. While valuation is never a precise exercise, I believe that reasonable assumptions outlined in the table that follows would yield a value in the range of $2 to $3 per share without substantial improvement in the business from where it was prior to the COVID pandemic:

2

Silver Ring Value Partners Limited Partnership • One Boston Place, Suite 2600, Boston, MA 02108 • www.silverringvaluepartners.com

I am, of course, not privy to actions that you and the Board have or have not undertaken with respect to attempting to sell our Company. I would strongly urge you to actively seek a buyer, through an organized and diligent process, that ideally would have synergies with our business. I can think of a number of companies who might be able to greatly increase the Company’s brand awareness, improve its top-of-funnel marketing and accelerate revenue growth. This would add substantial value beyond the valuation range provided earlier in this letter, which presupposes only cost-based synergies that a financial buyer would be able to obtain.

I am not suggesting that we try to sell in a rush, from a position of weakness or distress. I think our Company’s position is solid and management has a reasonable plan to address the challenges. We should continue on this path and further stabilize the business and resume growth prior to selling the Company.

As long as we obtain a full and fair value for our Company, this path presents the best way forward to unlocking long-term value. Many shareholders have waited patiently for years, and while it is tempting to keep trying to go it alone, that is no longer the optimal path given the scale of our Company.

3

Silver Ring Value Partners Limited Partnership • One Boston Place, Suite 2600, Boston, MA 02108 • www.silverringvaluepartners.com

Additional Management Incentives

In pursuing the sale of the Company we must not disincentivize the management team and employees. That is why I think it would be appropriate to have additional, substantial incentives for the management team for realizing full value for the company. I have specific ideas that I would be glad to share with you, but suffice it to say that these incentives should not reward management merely for the stock price rising from the current, deeply depressed levels. Instead, a reasonable threshold for value creation should be set, and if it is met or exceeded, then management should receive a well-earned substantial reward.

Return of Capital

When the Company raised capital via a secondary equity offering in 2019, the primary purpose was to invest organically in additional top-of-funnel marketing. Since that time, the Board has determined that the returns on the additional top-of-funnel marketing were unacceptably low and has stopped spending capital on that. I commend you and the Board for being mindful of the returns on our capital and being evidence-based in your decision-making.

I have a long-term time horizon and want to optimize the value of our Company for the long-term, as I believe you do. Therefore, I do not think that we should take any return of capital actions that would jeopardize the resiliency of our Company in case the external environment takes a turn for the worse or operational improvements take longer to materialize. However, once the Company is solidly profitable and the external environment has stabilized, I strongly believe it is appropriate to return the shareholders’ capital back to us if there are no compelling organic investment opportunities with high return on capital and low execution risk.

At the end of fiscal Q4 2020 ending June 30th, 2020, the Company’s balance sheet shows cash of $14.6M, of which $0.624M is restricted. The Company also has a PPP loan in the amount of $0.965M. Per share, cash was 51c, and excluding restricted cash and subtracting the amount of the PPP loan cash per share was slightly above 45c.

The stock price, currently around 88c, is near multi-year lows. Returning the cash to the shareholders will provide a substantial return. Furthermore, spending this cash on acquisitions or other uncertain ventures will drastically change the risk profile of the Company as an investment. That is not the assumption under which Silver Ring made its investment, nor do I have reason to believe that other shareholders, many of whom have patiently waited for returns for years, expected this turn of events.

The Company has a $5M asset-backed credit line for working capital. It was free cash flow positive in its latest quarter. Looking at the last 2 years, the largest intra-year seasonal swing in working capital has been less than $3M. These factors lead me to conclude that a very small portion of our current cash balance is required to run the business and that the rest can be safely returned to shareholders once we are confident that the Company can sustain and grow its profits.

4

Silver Ring Value Partners Limited Partnership • One Boston Place, Suite 2600, Boston, MA 02108 • www.silverringvaluepartners.com

Board Seats

I have no doubt that you, given your experience with the Company and your position as the Chairman of the Board, know more about the Company than I do. I am grateful for your efforts to create value for all shareholders. I also believe that smart, well-meaning people can still sometimes disagree as to the right course of action. That disagreement, constructively expressed, can lead to better decisions for everyone involved.

That is why I request that we continue this conversation inside the Boardroom, and that Silver Ring get two board seats at this year’s Annual Meeting, expanding the Board from 5 to 7. As its largest shareholder, Silver Ring has a substantial economic interest in the outcome of these decisions. I am requesting that you nominate the following two new Board members:

Gary Mishuris, CFA (age 41, myself): As someone who has been a professional investor for almost two decades during which I have analyzed hundreds of companies and as a CFA charter holder I am highly qualified to provide a valuable perspective on capital allocation and other matters.

Philip Butler (age 36): Philip was the Founder & CEO of Veya, which grew from a medical school textbook startup into one of Amazon’s top algorithmic sellers, with 20M+ active listings and $60M+ in annual revenue. He is also the Founder & CEO of Dragonfly, a venture-backed company that owns several e-commerce brands, that recently secured $30M in Series A funding.

I thank you for your time in considering my recommendations and requests. I know that time is of the essence given the proximity of the Annual Meeting, so I request the favor of your prompt reply.

Sincerely,

Gary Mishuris, CFA

Managing Partner, Chief Investment Officer

Silver Ring Value Partners Limited Partnership

CC: CEO, Don O’Connell

CC: CFO, Clint Pete

CC: Philip Butler

| i | https://www.twst.com/interview/neal-i-goldman-goldman-capital-management |

5

Silver Ring Value Partners Limited Partnership • One Boston Place, Suite 2600, Boston, MA 02108 • www.silverringvaluepartners.com