| |||||||||

| OUR VISION IS TO BE THE SAFEST, MOST FLUID RAILWAY IN NORTH AMERICA | ||||||||

“At Canadian Pacific, we are committed to the safety of our employees and our communities and protecting the environment where we operate. As part of our protocol, every employee is instructed to first protect themselves and the safety of their colleagues, next look to the safety of the community, and then ensure that the environment is protected. Finally, when each of these criteria has been met, we turn to continuing train operations. Canadian Pacific operates through more than 900 communities and through some of the most incredible landscapes in North America. It is our responsibility to protect this legacy for future generations.” | |||||||||

FRED J. GREEN President and Chief Executive Officer | |||||||||

1 Financial Highlights | 9 | Management’s Discussion and Analysis | 112 | Directors & Committees | |||||

5 Chairman’s Letter to Shareholders | 60 | Financial Statements | ibc | Senior Officers of the Company | |||||

6 CEO’s Letter to Shareholders | 110 | Shareholder Information | |||||||

FINANCIAL HIGHLIGHTS

“2007 was a year with many challenges including a very strong Canadian dollar and volatile fuel prices. However, we delivered in-line with our EPS guidance making this the fourth consecutive year that we met or exceeded our guidance.”

MICHAEL LAMBERT

Executive Vice-President

and Chief Financial Officer

Executive Vice-President

and Chief Financial Officer

| For the year ended December 31 | ||||||||

| (in millions except percentages and per share data) | 2007 | 2006 | ||||||

| Revenues | $ | 4,707.6 | $ | 4,583.2 | ||||

| Operating income | 1,164.2 | 1,128.6 | ||||||

Income, before FX on LTD and other specified items(1) | 672.8 | 627.5 | ||||||

| Net income | 946.2 | 796.3 | ||||||

Diluted earnings per share, before FX on LTD and other specified items(1) | 4.32 | 3.95 | ||||||

| Diluted earnings per share | 6.08 | 5.02 | ||||||

| Dividends declared per share | 0.90 | 0.75 | ||||||

Free cash(1) | 303.4 | 244.9 | ||||||

| Additions to properties | 893.2 | 793.7 | ||||||

Operating ratio, before other specified items(1) | 75.3 | % | 75.4 | % | ||||

Return on capital employed(1) | 9.5 | % | 10.2 | % | ||||

(1)These earnings measures have no standardized meaning prescribed by Canadian GAAP and, therefore, are unlikely to be comparable to similar measures of other companies. These earnings measures and other specified items are described in Management’s Discussion and Analysis in Section 6.0 “Non-GAAP Earnings” and Section 10.0 “Other specified items”.

CP is proud to be the official rail freight services provider for the Vancouver 2010 Olympic and Paralympic Winter Games. On September 24, 2007, CP unveiled the first of its new Olympic Games branded locomotives. These GE Evolution Series locomotives offer the latest in green locomotive technology. Compared to locomotives manufactured 20 years ago, the Evolution Series locomotives produce 60 % fewer smog pollutants and are 20 % more fuel efficient. Canadian Pacific will connect Canadians with the spirit of the 2010 Winter Games through its close connection to the hundreds of communities in Canada in which it operates.

| 2007 ANNUAL REPORT | ||||

| 1 | ||||

LINES OF BUSINESS |  |

CP’s diverse customer and traffic base and a continued focus on our proven strategy of quality revenue growth, consisting of a disciplined yield focus and aggressive market development drove good results in 2007 despite some volatility in some of the markets. Our destination markets have a healthy diversification linked to global, cross-border and domestic markets. Less than 40 % of CP’s book of business is directly linked to North American GDP. With key customer investments in new capacity, a growing portfolio of strategic accounts and strong global fundamentals and markets, CP is “in-motion” and poised to continue its strong performance. |  |

BULK

Our bulk portfolio makes up approximately 44 % of our revenues and is made up of grain, coal, sulphur and fertilizers. These commodities have a global reach with more than two-thirds of our bulk portfolio exported overseas. Strong economic growth in Asia has led to the steady upgrade of diets higher in protein, which in turn is creating demand for increased fertilizers and grain. Continued demand for Canadian metallurgical coal, used in the steel industry, has also supported solid Canadian coal exports. With strong global demand for these bulk products in 2007, CP delivered 4 % year-over-year bulk revenue growth in 2007 against a strong year in 2006.

Our bulk portfolio makes up approximately 44 % of our revenues and is made up of grain, coal, sulphur and fertilizers. These commodities have a global reach with more than two-thirds of our bulk portfolio exported overseas. Strong economic growth in Asia has led to the steady upgrade of diets higher in protein, which in turn is creating demand for increased fertilizers and grain. Continued demand for Canadian metallurgical coal, used in the steel industry, has also supported solid Canadian coal exports. With strong global demand for these bulk products in 2007, CP delivered 4 % year-over-year bulk revenue growth in 2007 against a strong year in 2006.

INTERMODAL

Our Intermodal line of business, representing 29 % of freight revenues, handles goods moving in containers. This encompasses both domestic movements within North America, and the international portion of the business that moves import and export containers from the ports of Vancouver, Montreal, New York/New Jersey and Philadelphia to various destinations within Canada and the US, and from key markets within North America to various ports for export. With continuing strong demand for overseas products, combined with our strategic and diversified customer base, our Intermodal business has delivered consistent growth since 2003.

Our Intermodal line of business, representing 29 % of freight revenues, handles goods moving in containers. This encompasses both domestic movements within North America, and the international portion of the business that moves import and export containers from the ports of Vancouver, Montreal, New York/New Jersey and Philadelphia to various destinations within Canada and the US, and from key markets within North America to various ports for export. With continuing strong demand for overseas products, combined with our strategic and diversified customer base, our Intermodal business has delivered consistent growth since 2003.

| 2007 ANNUAL REPORT | ||||

| 2 | ||||

We have invested in terminals, containers, rail cars and technology systems and we are seeing that investment pay off. CP delivered another strong year in 2007 with 5 % year-over-year revenue growth.

MERCHANDISE

The “Merchandise” line of business is made up of manufactured and semi-manufactured goods that generally move in less than full train shipments. It includes automotive, forest, industrial and consumer products and makes up 27 % of CP’s revenue. Industrial and consumer products, including pipe, chemicals and energy, structural steel and dimensional machinery are key requirements in Alberta’s

rapidly expanding oil sands developments and this business drove year-over-year growth of 4 % in 2007. CP’s strategic partners in the automotive business include the “New Domestics” who continue to grow through new investments like Toyota’s Woodstock, Ontario facility that will be exclusively served by CP when it opens this fall. With key strategic partners and the recent announcement to expand our infrastructure in Alberta’s Industrial Heartland, CP is positioned for growth in its Merchandise franchise.

| 2007 ANNUAL REPORT | ||||

| 3 | ||||

EXECUTION EXCELLENCE

We’ve delivered over the past four years by focusing on Execution Excellence. It’s at the core of our game plan that builds on our fundamentals of quality revenue growth, improved productivity and our talented and dedicated people. It’s how we’ve been successful in the past and how we are creating both near term performance improvement and shareholder value going forward.

QUALITY REVENUE GROWTH

Our quality revenue growth initiatives have delivered topline growth over the last three years as rail fundamentals remain strong and continue to provide pricing opportunities. Our diverse franchise and the global nature of our Book of Business provides balance and has tempered the impact of some of the slowdowns we have seen in some sectors of the North American economy. In 2007, continuing strong demand in global markets drove a market environment that supported improved yield.

PRODUCTIVITY

A relentless focus on improving fluidity in all aspects of our business has produced results. Our three core design principles of velocity, balance and network approach have driven improvements. Initiatives that have improved asset velocity, streamlined processes, and eliminated waste and rework have yielded productivity gains and resulted in cost savings. In 2007, we faced a number of operating challenges, but with our balanced Integrated Operating Plan, we found ways to deliver improved unit cost performance. We moved a record workload of 246 billion GTMs while maintaining our position as the industry leader in train operations safety.

PEOPLE

An engaged and productive workforce is the very foundation of our success. The ideas and ingenuity of our people are constantly challenging the status quo; looking for ways to do things better, more efficiently, more safely. Every employee at CP is charged with pursuing Execution Excellence, in the delivery of a superior product that meets our customers’ needs. Through our people we will achieve our vision of being the safest, most fluid railway in North America.

| ||||

| ||||

| 2007 ANNUAL REPORT | ||||

| 4 | ||||

CHAIRMAN’S LETTER TO SHAREHOLDERS

February 19, 2008

Today’s North American rail industry is playing a pivotal and growing role in driving the continent’s economic prosperity and competitiveness, and Canadian Pacific is at the centre of the action. CP is leading the industry in train operations safety and in finding new, innovative ways to improve efficiency at all levels of the Organization to provide best-in-class scheduled railway service for its customers.

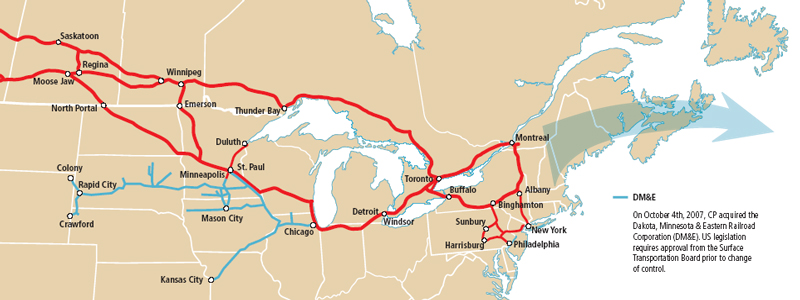

CP is growing both organically and by seizing new opportunities, such as the Company’s two major initiatives in 2007 – the acquisition of the Dakota, Minnesota & Eastern Railroad Corporation (DM&E); and its expansion into Alberta’s growing Industrial Heartland.

There are strong, natural synergies between CP and the DM&E; a growing regional railroad. In addition to the purchase price of US$1.48 billion, CP has committed to spending an additional US$300 million for further upgrading of the DM&E over the next several years. The purchase is still subject to approval by the US Surface Transportation Board (STB) and that decision is expected by late September 2008.

CP’s network expansion in Alberta’s Industrial Heartland northeast of Edmonton positions the Company for growth tied to Canada’s booming oil sands region. Over $20 billion is earmarked for development in the Industrial Heartland, and two major oil sands upgraders are already under construction there.

In our capacity of advising management on the development of the Company’s strategy, your Board was actively involved in both decisions. The Board holds regular strategy sessions with management where we review in detail the Company’s strategic directions.

The Board monitors implementation of the strategy by management, approves major transactions and tracks the outcomes of these transactions on an ongoing basis.

To assist in the fulfillment of Board responsibilities, we’ve continued with our education and orientation program for Directors to ensure they are fully conversant with CP and the railway industry. The program includes orientation, site visits, education sessions and a Directors’ Handbook. In 2007, the Board toured CP’s network management centre in Calgary as well as rail facilities in southern Ontario, including a customer auto facility and associated rail infrastructure. Board meetings were held in Cambridge, Ontario, Montreal and Calgary.

We also enhanced our Board committee structure in 2007.

We changed the composition of the Corporate Governance and Nominating Committee. Instead of being composed of all independent members of the Board, it is now composed of the chairpersons of all five Board committees.

In recognition of its expanded oversight mandate, the Environmental and Safety Committee has been renamed the Health, Safety, Security and Environment Committee. CP’s President and Chief Executive Officer Fred Green joined the committee so it can benefit from his strong interest and expertise in health, safety, security and environmental matters. This further demonstrates the Board’s commitment to working with management to ensure the Company always sets as a priority the health and safety of employees and the public, the security of the railway, and environmental stewardship.

The Board is pleased that management is continuing to enhance disclosure and financial reporting controls in accordance with best practices. Again this year, management

is reporting that its internal controls are effective in accordance with the provisions of the Sarbanes-Oxley Act of 2002.

Stephen Bachand is retiring from the Board in May and on behalf of the whole Board I wish to thank him for his years of valuable service and in particular for the important contributions he made to deliberations on corporate governance, management resources and compensation, and pensions. In 2007, we were pleased to welcome Krystyna Hoeg to the Board and we already appreciate the level of insight she brings to our discussions.

In closing I want to thank Fred Green, his management team and all of the Company’s employees for their impressive efforts in 2007. They grasped opportunities, responded quickly to challenges and delivered solid results. In his letter, Fred Green refers to North America’s ‘rail renaissance’. CP is a leader in that renaissance and by applying the latest technologies and through the ingenuity of CP employees, I am confident your Company will continue to lead the way.

JOHN E. CLEGHORN, O.C., FCA

Chairman of Board

Chairman of Board

| 2007 ANNUAL REPORT | ||||

| 5 | ||||

CHIEF EXECUTIVE OFFICER’S LETTER TO SHAREHOLDERS

February 19, 2008

Canadian Pacific is a company in motion, focused on delivering solid results for our shareholders and making a great franchise even better by building on our significant operational and financial strengths. Our vision is to be the safest, most fluid railway in North America and achieving this goal is based on driving quality revenue growth, improving productivity and developing our people. Through the disciplined implementation of these three pillars, CP is emerging as a high-performance organization and we are positioned to grow.

CP’s financial results in 2007 were in-line with our target range despite significant headwinds, including extreme weather events across our network, labour disruptions, fuel price escalation and a stronger Canadian dollar. We overcame these challenges and met our earnings per share guidance for the fourth consecutive year.

Through our Integrated Operating Plan and co-production agreements with other railways, we have already delivered more than $100 million in savings and productivity improvements in the past three years and plan to deliver more in the future.

We will continue to improve productivity and performance through ‘Execution Excellence’.

With a record of solid financial and operational performance, we are now well-positioned for growth. We announced two strategic initiatives in 2007 that have added an exciting new dimension to our franchise.

We acquired Dakota, Minnesota & Eastern Railroad Corporation (DM&E), the largest regional railroad in the US.

We also moved forward with our plan to expand capacity in Alberta’s booming Industrial Heartland northeast of Edmonton. In 2007, we assembled a rail corridor and lands for development of freight yards and transload facilities.

We continue to see growth in Asia-Pacific trade through the Port of Vancouver, and we are encouraged that the support of the governments of Canada and British Columbia will keep a focus on the need for infrastructure investment in the Pacific Gateway corridor. It is critical that all supply chain partners are engaged to ensure adequate capacity to handle future growth.

Safety is the hallmark of CP’s culture and our corporate identity and we continue to be the industry leader in train operation safety.

However, for CP’s leadership team, this is not good enough. We recognize that we must continuously earn our position as a safety leader, so we are accelerating plans to further improve our safety program. We were deeply saddened last year by the loss of one of our colleagues, locomotive engineer Lonnie Plasko, in a train derailment in British Columbia, and this tragedy is a reminder that our work on safety is never complete.

2007 was a busy year for collective agreements with our unions and we now have several new, progressive agreements in place that have been ratified.

CP continues to invest in the communities where we operate and where our employees and their families live. Our popular Holiday Train program again played an important role in 2007 in raising food, money and awareness for local food banks in Canada and the US. CP will help British Columbia mark its 150th anniversary in 2008 by sponsoring the CP BC ‘Spirit of 150’ Rail Tour, a historic train pulled by CP’s Empress 2816 steam locomotive that will visit communities along CP’s route in the province. CP is also proud to be the official rail freight services provider for the Vancouver 2010 Olympic and Paralympic

| 2007 ANNUAL REPORT | ||||

| 6 | ||||

Winter Games. To be part of this great Canadian event, which will engage our employees and the communities in which we operate, over the next two years, is truly exciting.

I believe North America’s rail renaissance is here to stay, but over the next 20 years the rail industry will need to reach new performance levels in order to meet many challenges – demographic changes; safety and security; environmental issues and climate change; volume growth; and a need for asset renewal. This will require our industry to fundamentally re-engineer core work processes through implementation of new and emerging technologies. At CP, we have created a 20-year ‘Railway of the Future’ vision, complete with specific design objectives that will be our roadmap to addressing these industry issues.

North America’s environmental challenges alone offer the rail industry a significant leadership opportunity. By its nature, rail is an environmentally friendly mode of transport; one double-stack intermodal train takes approximately 250 trucks off of our congested and publicly-funded highways. CP has made significant progress in reducing

its carbon footprint through a number of initiatives. From 1990 through 2006, CP’s freight volumes (as measured by revenue ton-miles) increased 37 %, while our overall emissions increased only 4 %.

Although the economic forecast for 2008 holds the uncertainty of a softer US economy, an increase in fuel costs and a strong Canadian dollar, CP entered the year with good market demand for its bulk commodity franchise. Rail fundamentals are strong by historic standards, and CP’s diverse portfolio and the global nature of our business positions us well. In 2008, we are projecting growth in diluted earnings per share of 8 % to 11 %, revenue growth of 4 % to 6 %, and free cash flow in excess of $250 million.

2007 was a year with many unique external forces including stock market uncertainty, a strengthening Canadian dollar, a major increase in fuel prices and unprecedented credit issues in the marketplace. We are fortunate to have such a seasoned and knowledgeable Board of Directors during these times and I wish to thank our Chairman John Cleghorn and our Board of Directors for their solid guidance and counsel during the year.

CP is indeed a company in motion. We have a great franchise with an excellent book of business serving North America and the fast-growing Asian economy. Our team is committed to becoming a safer, more efficient railroad and we are confident that our approach to creating value, not only for our shareholders but also our customers and our employees, will succeed through 2008 and beyond.

FRED GREEN

Chief Executive Officer

Chief Executive Officer

| 2007 ANNUAL REPORT | ||||

| 7 | ||||

TABLE OF CONTENTS

| 1.0 | Business Profile | 9 | ||||||

| 2.0 | Strategy | 9 | ||||||

| 3.0 | Additional Information | 9 | ||||||

| 4.0 | Financial Highlights | 10 | ||||||

| 5.0 | Operating Results | 11 | ||||||

| 5.1 | Income | 11 | ||||||

| 5.2 | Diluted Earnings per Share | 12 | ||||||

| 5.3 | Operating Ratio | 12 | ||||||

| 5.4 | Return on Capital Employed | 12 | ||||||

| 5.5 | Impact of Foreign Exchange on Earnings | 12 | ||||||

| 6.0 | Non-GAAP Earnings | 14 | ||||||

| 7.0 | Lines of Business | 16 | ||||||

| 7.1 | Volumes | 16 | ||||||

| 7.2 | Revenues | 17 | ||||||

| 7.2.1 | Freight Revenues | 18 | ||||||

| 7.2.2 | Other Revenues | 20 | ||||||

| 7.2.3 | Freight Revenue per Carload | 20 | ||||||

| 8.0 | Performance Indicators | 21 | ||||||

| 8.1 | Safety Indicators | 21 | ||||||

| 8.2 | Efficiency and Other Indicators | 21 | ||||||

| 9.0 | Operating Expenses, Before Other Specified Items | 22 | ||||||

| 10.0 | Other Specified Items | 24 | ||||||

| 11.0 | Other Income Statement Items | 25 | ||||||

| 12.0 | Quarterly Financial Data | 27 | ||||||

| 13.0 | Fourth-quarter Summary | 28 | ||||||

| 13.1 | Operating Results | 28 | ||||||

| 13.2 | Non-GAAP Earnings | 28 | ||||||

| 13.3 | Revenues | 28 | ||||||

| 13.4 | Operating Expenses, Before Other Specified Items | 29 | ||||||

| 13.5 | Other Income Statement Items | 30 | ||||||

| 13.6 | Liquidity and Capital Resources | 30 | ||||||

| 14.0 | Changes in Accounting Policy | 30 | ||||||

| 14.1 | 2007 Accounting Changes | 30 | ||||||

| 14.2 | Future Accounting Changes | 31 | ||||||

| 15.0 | Liquidity and Capital Resources | 31 | ||||||

| 15.1 | Operating Activities | 32 | ||||||

| 15.2 | Investing Activities | 32 | ||||||

| 15.3 | Financing Activities | 32 | ||||||

| 15.4 | Free Cash | 33 | ||||||

| 16.0 | Balance Sheet | 34 | ||||||

| 17.0 | Financial Instruments | 36 | ||||||

| 18.0 | Off-balance Sheet Arrangements | 39 | ||||||

| 19.0 | Acquisition | 40 | ||||||

| 20.0 | Contractual Commitments | 41 | ||||||

| 21.0 | Future Trends and Commitments | 41 | ||||||

| 22.0 | Business Risks and Enterprise Risk Management | 44 | ||||||

| 22.1 | Competition | 44 | ||||||

| 22.2 | Liquidity | 45 | ||||||

| 22.3 | Environmental Laws and Regulations | 45 | ||||||

| 22.4 | Regulatory Authorities | 45 | ||||||

| 22.5 | Labour Relations | 46 | ||||||

| 22.6 | Network Capacity and Volume | 47 | ||||||

| 22.7 | Financial Risks | 47 | ||||||

| 22.8 | General and Other Risks | 48 | ||||||

| 23.0 | Critical Accounting Estimates | 48 | ||||||

| 24.0 | Systems, Procedures and Controls | 51 | ||||||

| 25.0 | Forward-looking Information | 51 | ||||||

| 26.0 | Glossary of Terms | 55 | ||||||

| 2007 ANNUAL REPORT | ||||

| 8 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS

February 19, 2008

This Management’s Discussion and Analysis (“MD&A”) supplements the Consolidated Financial Statements and related notes for year ended December 31, 2007. Except where otherwise indicated, all financial information reflected herein is expressed in Canadian dollars. All information has been prepared in accordance with Canadian generally accepted accounting principles (“GAAP”), except as described in Section 6.0 of this MD&A. In this MD&A, “our”, “us”, “we”, “CP” and “the Company” refer to Canadian Pacific Railway Limited (“CPRL”), CPRL and its subsidiaries, CPRL and one or more of its subsidiaries, or one or more of CPRL’s subsidiaries, as the context may require. Other terms not defined in the body of this MD&A are defined in Section 26.0.

Unless otherwise indicated, all comparisons of results for the fourth quarter of 2007 and 2006 are against the results for the fourth quarter of 2006 and 2005, respectively. Unless otherwise indicated, all comparisons of results for 2007 and 2006 are against the results for 2006 and 2005, respectively.

1.0 Business Profile

Canadian Pacific Railway Limited, through its subsidiaries, operates a transcontinental railway in Canada and the United States and provides logistics and supply chain expertise. Through our subsidiaries, we provide rail and intermodal transportation services over a network of approximately 13,200 miles, serving the principal business centres of Canada from Montreal, Quebec, to Vancouver, British Columbia, and the US Northeast and Midwest regions. Our railway feeds directly into the US heartland from the East and West coasts. Agreements with other carriers extend our market reach east of Montreal in Canada, throughout the US and into Mexico. Through our subsidiaries, we transport bulk commodities, merchandise freight and intermodal traffic. Bulk commodities include grain, coal, sulphur and fertilizers. Merchandise freight consists of finished vehicles and automotive parts, as well as forest and industrial and consumer products. Intermodal traffic consists largely of high-value, time-sensitive retail goods in overseas containers that can be transported by train, ship and truck, and in domestic containers and trailers that can be moved by train and truck.

2.0 Strategy

Our vision is to become the safest and most fluid railway in North America. Through the ingenuity of our people, it is our objective to create long-term value for customers, shareholders and employees by profitably growing within the reach of our rail franchise and through strategic additions. We seek to accomplish this objective through the following three-part strategy:

| □ | generating quality revenue growth by realizing the benefits of demand growth in our bulk, intermodal and merchandise business lines with targeted infrastructure capacity investments linked to global trade opportunities; |

| □ | improving productivity by leveraging strategic marketing and operating partnerships, executing a scheduled railway through our Integrated Operating Plan (“IOP”) and driving more value from existing assets and resources by improving “fluidity”; and |

| □ | continuing to develop a dedicated, professional and knowledgeable workforce that is committed to safety and sustainable financial performance through steady improvement in profitability, increased free cash flow and a competitive return on investment. |

3.0 Additional Information

Additional information, including our Consolidated Financial Statements, MD&A, Annual Information Form, press releases and other required filing documents, is available on SEDAR at www.sedar.com in Canada, on EDGAR at www.sec.gov in the US and on our website at www.cpr.ca. The aforementioned documents are issued and made available in accordance with legal requirements and are not incorporated by reference into this MD&A.

| 2007 ANNUAL REPORT | ||||

| 9 | ||||

4.0 Financial Highlights

| For the year ended December 31 (in millions, except percentages and per-share data) | 2007 | 2006 | 2005 | ||||||||||

| Revenues | $ | 4,707.6 | $ | 4,583.2 | $ | 4,391.6 | |||||||

Operating income, before other specified items(1) | 1,164.2 | 1,128.6 | 1,001.5 | ||||||||||

| Operating income | 1,164.2 | 1,128.6 | 991.2 | ||||||||||

Income, before FX on LTD and other specified items(1) | 672.8 | 627.5 | 528.4 | ||||||||||

| Net income | 946.2 | 796.3 | 543.0 | ||||||||||

| Basic earnings per share | 6.14 | 5.06 | 3.43 | ||||||||||

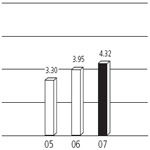

Diluted earnings per share, before FX on LTD and other specified items(1) | 4.32 | 3.95 | 3.30 | ||||||||||

| Diluted earnings per share | 6.08 | 5.02 | 3.39 | ||||||||||

| Dividends declared per share | 0.9000 | 0.7500 | 0.5825 | ||||||||||

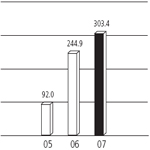

Free cash(1) | 303.4 | 244.9 | 92.0 | ||||||||||

| Total assets as at December 31 | 13,365.0 | 11,415.9 | 10,891.1 | ||||||||||

| Total long-term financial liabilities as at December 31 | 6,562.3 | 5,320.4 | 5,390.3 | ||||||||||

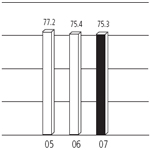

Operating ratio, before other specified items(1) | 75.3 | % | 75.4 | % | 77.2 | % | |||||||

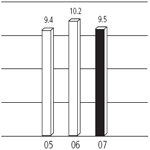

Return on capital employed(1) | 9.5 | % | 10.2 | % | 9.4 | % | |||||||

Diluted EPS, before FX on LTD | Operating Ratio, before | Return on Capital | Free Cash(1) | |||

and other specified items($)(1) | other specified items(%)(1) | Employed(%)(1) | (in millions of dollars) | |||

|  |  |  |

(1) These earnings measures have no standardized meanings prescribed by Canadian GAAP and, therefore, are unlikely to be comparable to similar measures of other companies. These earnings measures and other specified items are described in Section 6.0. A reconciliation of income and diluted EPS, before FX on LTD and other specified items, to net income and diluted EPS, as presented in the financial statements is provided in Section 6.0. A reconciliation of free cash to GAAP cash position is provided in Section 15.4.

| 2007 ANNUAL REPORT | ||||

| 10 | ||||

5.0 Operating Results

5.1 INCOME

Operating income in 2007 was $1,164.2 million, up $35.6 million, or 3.2 %, from $1,128.6 million in 2006.

The growth in 2007 operating income reflected:

| □ | record shipments reflecting continued strong growth in bulk and intermodal products; | |

| □ | import and export growth in intermodal shipments; | |

| □ | higher revenues resulting from increased freight rates; and | |

| □ | lower compensation and benefits expenses. |

These were partially offset by:

| □ | higher fuel prices driven by higher refining charges and West Texas Intermediate (“WTI”) prices, net of fuel recoveries; | |

| □ | higher costs reflecting record volumes in 2007; | |

| □ | the negative impact of the change in FX of approximately $34 million; and | |

| □ | higher costs associated with network disruptions, mainly driven by harsh weather conditions. |

Net income for the year ended December 31, 2007 was $946.2 million, up $149.9 million, or 18.8 %, from $796.3 million in 2006. Net income in 2007 increased primarily due to:

| □ | FX gains on US dollar-denominated long-term debt (“LTD”), reflecting a strengthening in the Canadian dollar; | |

| □ | higher operating income; and | |

| □ | the recognition of equity earnings, starting in October 2007, following our acquisition of the Dakota, Minnesota & Eastern Railroad Corporation (“DM&E” discussed further in Section 19.0), which reduced Other income and charges. |

These increases were partially offset by the after-tax change in estimated fair value of our investment in Canadian third party asset-backed commercial paper (“ABCP” discussed further in Section 11.2).

Operating income in 2006 was $1,128.6 million, an increase of $137.4 million, or 13.9 %, from $991.2 million in 2005.

Operating income, before other specified items, was $1,128.6 million in 2006, up $127.1 million, or 12.7 %, from $1,001.5 million in 2005. The growth in 2006 operating income, before other specified items reflected:

| □ | higher revenues due to increased freight rates across the majority of our business lines; | |

| □ | strong grain volumes; | |

| □ | expense reductions from co-production initiatives and operational benefits produced by our IOP (discussed further in Section 21.3); |

| □ | reductions in management and administrative positions; and | |

| □ | the $18 million gain from the sale of our Latta subdivision (discussed further in Section 21.5). |

The growth in 2006 operating income, before other specified items, was partially offset by:

| □ | a significant reduction in coal volumes (discussed further in Section 7.2.1.2); | |

| □ | higher fuel costs; | |

| □ | higher material costs for freight car and locomotive repairs and train servicing; and | |

| □ | the net impact of the change in FX on US dollar-denominated revenues and expenses. |

There were no other specified items in operating income in 2006.

Net income for the year ended December 31, 2006 was $796.3 million, an increase of $253.3 million, or 46.6 %, from $543.0 million in 2005. Net income in 2006 included a future income tax benefit of $176.0 million recorded in the second quarter of 2006 as a result of reduced Canadian federal and provincial income tax rates (discussed further in Section 10.0).

| 2007 ANNUAL REPORT | ||||

| 11 | ||||

Fuel prices remained volatile. During 2007, we continued to take steps to mitigate the impact of high prices with fuel recovery programs and hedging (discussed further in Section 17.6.1).

5.2 DILUTED EARNINGS PER SHARE

Diluted EPS, which is defined in Section 26.0, was $6.08 in 2007, an increase of $1.06, or 21.1 %, from 2006. Diluted EPS was $5.02 in 2006, an increase of $1.63, or 48.1 %, from 2005. The increases in both 2007 and 2006 reflected an increase in net income, as well as the positive impact of the reduction in the number of shares outstanding due to our share repurchase plan (discussed further in Section 16.5).

Diluted EPS excluding FX gains and losses on long-term debt (“FX on LTD”) and other specified items was $4.32 in 2007, an increase of $0.37, or 9.4 %, from 2006. Diluted EPS excluding FX on LTD and other specified items was $3.95 in 2006, an increase of $0.65, or 19.7 %, from 2005. The increases in both 2007 and 2006 were mainly due to a higher income before FX on LTD and other specified items, as well as the positive impact of the share repurchase program. Diluted EPS excluding FX on LTD and other specified items is discussed further in Section 6.0.

5.3 OPERATING RATIO

Our operating ratio, before other specified items, improved to 75.3 % in 2007, compared with 75.4 % in 2006 and 77.2 % in 2005. The operating ratio provides the percentage

of revenues used to operate the railway. A lower percentage normally indicates higher efficiency in the operation of the railway. Other specified items are discussed further in Section 10.0.

5.4 RETURN ON CAPITAL EMPLOYED

Return on capital employed (“ROCE”) at December 31, 2007 was 9.5 %, compared with 10.2 % in 2006 and 9.4 % in 2005. The decrease in 2007 was primarily due to an increase in net debt resulting from the bridge financing obtained for the acquisition of DM&E, partially offset by an increase in earnings. The improvement in 2006 reflected higher profitability of investments in the railway over the four quarters ended December 31, 2006, compared to the four quarters ended December 31, 2005, primarily driven by higher revenues and improved operating ratio. ROCE is discussed further in Section 6.0.

5.5 IMPACT OF FOREIGN

EXCHANGE ON EARNINGS

EXCHANGE ON EARNINGS

Fluctuations in FX affect our results because US dollar-denominated revenues and expenses are translated into Canadian dollars. US dollar-denominated revenues and expenses are reduced when the Canadian dollar strengthens in relation to the US dollar. Operating income is also reduced because more revenues than expenses are generated in US dollars.

The Canadian dollar strengthened against the US dollar by approximately 4 % in 2007 and by approximately 7 % in 2006. The

average FX rate for converting US dollars to Canadian dollars decreased to $1.08 in 2007 from $1.13 in 2006 and $1.21 in 2005. The adjoining table shows the approximate impact of the change in FX on our revenues and expenses, and income before FX on LTD and other specified items in 2007 and 2006. This analysis does not include the impact of the change in FX on balance sheet accounts or FX hedging activity.

On average, a $0.01 strengthening (or weakening) of the Canadian dollar reduces (or increases) annual operating income by approximately $3 million to $6 million. However, a large movement in FX can lead to a change in operating income that falls outside of the aforementioned range. FX fluctuations decreased operating income by approximately $34 million in 2007 and approximately $28 million in 2006, as illustrated in the adjoining table. From time to time, we use FX forward contracts to partially hedge the impact on our business of FX transaction gains and losses and other economic factors. In addition, we have designated a portion of our US dollar-denominated LTD as a hedge of our net investment in self-sustaining foreign subsidiaries. Our hedging instruments are discussed further in Section 17.0.

In 2007, there was a higher proportion of US dollar-denominated grain traffic, compared with Canadian dollar-denominated grain traffic.

| 2007 ANNUAL REPORT | ||||

| 12 | ||||

EFFECT ON EARNINGS DUE TO THE CHANGE IN FOREIGN EXCHANGE

| For the year ended December 31 (in millions, except foreign exchange rate) | 2007 vs. 2006 | 2006 vs. 2005 | |||||||

| Average annual foreign exchange rates | $1.08 vs. $1.13 | $1.13 vs. $1.21 | |||||||

| Freight revenues | |||||||||

| Grain | $ (24 | ) | $ (24 | ) | |||||

| Coal | (5 | ) | (7 | ) | |||||

| Sulphur and fertilizers | (9 | ) | (10 | ) | |||||

| Forest products | (10 | ) | (16 | ) | |||||

| Industrial and consumer products | (20 | ) | (25 | ) | |||||

| Automotive | (8 | ) | (12 | ) | |||||

| Intermodal | (13 | ) | (19 | ) | |||||

| Other revenues | (2 | ) | (1 | ) | |||||

| Unfavourable effect | (91 | ) | (114 | ) | |||||

| Operating expenses | |||||||||

| Compensation and benefits | 13 | 22 | |||||||

| Fuel | 23 | 30 | |||||||

| Materials | 2 | 3 | |||||||

| Equipment rents | 7 | 12 | |||||||

| Depreciation and amortization | 3 | 4 | |||||||

| Purchased services and other | 9 | 15 | |||||||

| Favourable effect | 57 | 86 | |||||||

| Unfavourable effect on operating income | (34 | ) | (28 | ) | |||||

| Other expenses | |||||||||

| Other income and charges | – | – | |||||||

| Interest expense | 7 | 11 | |||||||

Income tax expense, before FX on LTD and other specified items(1) | 7 | 7 | |||||||

Unfavourable effect on income, before FX on LTD and other specified items(1) | $ (20 | ) | $ (10 | ) | |||||

(1) These earnings measures have no standardized meanings prescribed by Canadian GAAP and, therefore, are unlikely to be comparable to similar measures of other companies. These earnings measures and other specified items are described in Section 6.0.

| 2007 ANNUAL REPORT | ||||

| 13 | ||||

6.0 Non-GAAP Earnings

We present non-GAAP earnings and cash flow information in this MD&A to provide a basis for evaluating underlying earnings and liquidity trends in our business that can be compared with the results of our operations in prior periods. These non-GAAP earnings exclude foreign currency translation effects on LTD, which can be volatile and short term, and other specified items (discussed further in Section 10.0) that are not among our normal ongoing revenues and operating expenses. The adjoining table details a reconciliation of income, before FX on LTD and other specified items, to net income, as presented in the financial statements. Free

cash is calculated as cash provided by operating activities, less cash used in investing activities and dividends paid, and adjusted for the acquisition of DM&E and the investment in ABCP. Free cash is discussed further and is reconciled to the increase in cash as presented in the financial statements in Section 15.4. Earnings measures that exclude FX on LTD and other specified items, ROCE, net-debt to net-debt-plus-equity ratio and free cash as described in this MD&A have no standardized meanings and are not defined by Canadian GAAP and, therefore, are unlikely to be comparable to similar measures presented by other companies. ROCE reported quarterly represents the

return over the current quarter and the previous three quarters. The measure is used by management to assess profitability of investments in the railway. ROCE is measured as income before FX on LTD and other specified items plus after-tax interest expense divided by average net debt plus equity. It does not have a comparable GAAP measure to which it can be reconciled. Net-debt to net-debt-plus-equity ratio (discussed further in Section 15.3.1) represents one of many metrics used in assessing the Company’s capital structure and debt servicing capabilities, and it does not have a comparable GAAP measure to which it can be reconciled.

| 2007 ANNUAL REPORT | ||||

| 14 | ||||

SUMMARIZED STATEMENT OF CONSOLIDATED INCOME

| For the year ended | For the three months ended | |||||||||||||||||||

| (reconciliation of non-GAAP earnings to GAAP earnings) | December 31 | December 31 | ||||||||||||||||||

| (in millions, except diluted EPS and operating ratio) | 2007 | 2006 | 2005 | 2007 | 2006 | |||||||||||||||

| Revenues | $ | 4,707.6 | $ | 4,583.2 | $ | 4,391.6 | $ | 1,188.3 | $ | 1,190.4 | ||||||||||

| Operating expenses, before other specified items | 3,543.4 | 3,454.6 | 3,390.1 | 882.8 | 870.3 | |||||||||||||||

Operating income, before other specified items | 1,164.2 | 1,128.6 | 1,001.5 | 305.5 | 320.1 | |||||||||||||||

| Other income and charges | 17.3 | 27.8 | 18.1 | (3.8 | ) | 6.4 | ||||||||||||||

| Interest expense | 204.3 | 194.5 | 204.2 | 63.4 | 49.8 | |||||||||||||||

Income tax expense, before income tax on FX on LTD and other specified items(1) | 269.8 | 278.8 | 250.8 | 60.8 | 82.9 | |||||||||||||||

Income, before FX on LTD and other specified items(1) | 672.8 | 627.5 | 528.4 | 185.1 | 181.0 | |||||||||||||||

Foreign exchange (gains) losses on long-term debt | ||||||||||||||||||||

| FX on LTD – (gains) losses | (169.8 | ) | 0.1 | (44.7 | ) | (8.3 | ) | 44.9 | ||||||||||||

| Income tax expense on FX on LTD | 44.3 | 7.1 | 22.4 | (3.1 | ) | (9.5 | ) | |||||||||||||

| FX on LTD, net of tax – (gains) losses | (125.5 | ) | 7.2 | (22.3 | ) | (11.4 | ) | 35.4 | ||||||||||||

Other specified items | ||||||||||||||||||||

| Change in estimated fair value of ABCP | 21.5 | – | – | – | – | |||||||||||||||

| Income tax on change in estimated fair value of ABCP | (6.5 | ) | – | – | – | – | ||||||||||||||

| Change in estimated fair value of ABCP, net of tax | 15.0 | – | – | – | – | |||||||||||||||

| Income tax benefits due to tax rate reductions | (162.9 | ) | (176.0 | ) | – | (145.8 | ) | – | ||||||||||||

| Special charge for labour restructuring and asset impairment | – | – | 44.2 | – | – | |||||||||||||||

| Special credit related to environmental remediation | – | – | (33.9 | ) | – | – | ||||||||||||||

| Income tax on other specified items | – | – | (2.6 | ) | – | – | ||||||||||||||

| Other specified items, net of tax | (147.9 | ) | (176.0 | ) | 7.7 | (145.8 | ) | – | ||||||||||||

Net income | $ | 946.2 | $ | 796.3 | $ | 543.0 | $ | 342.3 | $ | 145.6 | ||||||||||

Diluted EPS, before FX on LTD and other specified items(1) | $ | 4.32 | $ | 3.95 | $ | 3.30 | $ | 1.20 | $ | 1.15 | ||||||||||

Diluted EPS, related to FX on LTD, net of tax(1) | 0.81 | (0.04 | ) | 0.14 | 0.07 | (0.23 | ) | |||||||||||||

Diluted EPS, related to other specified items, net of tax(1) | 0.95 | 1.11 | (0.05 | ) | 0.94 | – | ||||||||||||||

Diluted EPS, as determined by GAAP | $ | 6.08 | $ | 5.02 | $ | 3.39 | $ | 2.21 | $ | 0.92 | ||||||||||

Operating ratio, before other specified items(1) | 75.3 | % | 75.4 | % | 77.2 | % | 74.3 | % | 73.1 | % | ||||||||||

Operating ratio, related to other specified items(1) | 0.3 | % | – | 0.2 | % | – | – | |||||||||||||

Operating ratio | 75.6 | % | 75.4 | % | 77.4 | % | 74.3 | % | 73.1 | % | ||||||||||

(1) These earnings measures have no standardized meanings prescribed by Canadian GAAP and, therefore, are unlikely to be comparable to similar measures of other companies. These earnings measures and other specified items are described in this section of the MD&A.

| 2007 ANNUAL REPORT | ||||

| 15 | ||||

6.1 FOREIGN EXCHANGE GAINS AND LOSSES ON LONG-TERM DEBT

FX on LTD arises mainly as a result of translating US dollar-denominated debt into Canadian dollars. We calculate FX on LTD using the difference in FX rates at the beginning and at the end of each reporting period. The FX gains and losses are mainly unrealized and can only be realized when net US dollar-denominated LTD matures or is settled. Income, before FX on LTD and other specified items, is disclosed in the table above and excludes FX on LTD from our earnings in order to eliminate the impact of volatile short-term exchange rate fluctuations. At December 31, 2007, for every $0.01 the Canadian dollar strengthens (or weakens) relative to the US dollar, the conversion of US dollar-denominated long-term debt to Canadian dollars creates a pre-tax FX gain (or loss) of approximately $6 million, net of hedging.

On a pre-tax basis, we recorded the following FX on LTD as the Canadian dollar exchange rate changed at the end of each reporting period:

| □ | FX gains on LTD of $169.8 million in 2007, as the Canadian dollar exchange rate strengthened to $0.9913 relative to the US dollar; | |

| □ | FX losses on LTD of $0.1 million in 2006, as the Canadian dollar exchange rate weakened to $1.1654 relative to the US dollar; and |

| □ | FX gains on LTD of $44.7 million in 2005, as the Canadian dollar exchange rate strengthened to $1.1630 relative to the US dollar. |

Income tax expense (or benefit) related to FX on LTD is discussed further in Section 11.4.

7.0 Lines of Business

7.1 VOLUMES

Changes in freight volumes generally contribute to corresponding changes in freight revenues and certain variable expenses, such as fuel, equipment rents and crew costs.

Volume continued to grow as we moved record volumes, as measured by total revenue ton-miles (“RTM”), in 2007. Volumes in 2007, as measured by total carloads, increased by 79,800, or 3 %, and RTMs increased by approximately 6.5 billion, or 5 %. In 2006, total carloads decreased by 58,100, or 2 %, and RTMs decreased by approximately 2.4 billion, or 2 %.

These increases in carloads and RTMs in 2007 were mainly due to:

| □ | strong Intermodal growth due to strength in global markets and continued offshore sourcing trends; | |

| □ | strong global demand for bulk products; and | |

| □ | increase in average length of haul. |

These increases were partially offset by continued weakness in Forest products due to a slowdown in the US housing market and the impact of the strengthening of the Canadian dollar on Canadian producers. In addition, total carloads in 2007, while up, were adversely affected by the sale of our Latta subdivision in the second quarter of 2006 (discussed further in Section 21.5), which reduced our carloads by approximately 23,000.

The decline in carloads in 2006 was due to both the sale of our Latta subdivision (discussed further in Section 21.5) and the Nickel Spur, which reduced our carloads by 45,000 loads in 2006 (67,000 on an annual basis), as well as a decline in coal carloads due to decreased shipments by our primary coal customer.

With regard to RTMs in 2006, a 16 % increase in grain RTMs due to the strong export market for these products, was more than offset by RTM decreases of 18 %, 13 % and 11 % in Coal, Sulphur and fertilizers, and Forest products, respectively (discussed further in Section 7.2.1). The sale of our Latta subdivision and the Nickel Spur had a lesser impact on RTMs than on carloads, as traffic on both lines was short-haul in nature.

| 2007 ANNUAL REPORT | ||||

| 16 | ||||

VOLUMES

| For the year ended December 31 | 2007 | 2006 | 2005 | |||||||||

Carloads (in thousands) | ||||||||||||

| Grain | 385.0 | 382.8 | 338.7 | |||||||||

| Coal | 269.1 | 281.7 | 352.3 | |||||||||

| Sulphur and fertilizers | 209.8 | 178.3 | 201.8 | |||||||||

| Forest products | 114.1 | 135.0 | 153.7 | |||||||||

| Industrial and consumer products | 313.3 | 316.0 | 322.2 | |||||||||

| Automotive | 168.5 | 165.3 | 168.1 | |||||||||

| Intermodal | 1,238.1 | 1,159.0 | 1,139.4 | |||||||||

Total carloads | 2,697.9 | 2,618.1 | 2,676.2 | |||||||||

Revenue ton-miles (in millions) | ||||||||||||

| Grain | 30,690 | 30,127 | 26,081 | |||||||||

| Coal | 20,629 | 19,650 | 23,833 | |||||||||

| Sulphur and fertilizers | 21,259 | 17,401 | 20,080 | |||||||||

| Forest products | 7,559 | 8,841 | 9,953 | |||||||||

| Industrial and consumer products | 16,987 | 16,844 | 15,936 | |||||||||

| Automotive | 2,471 | 2,450 | 2,361 | |||||||||

| Intermodal | 29,757 | 27,561 | 27,059 | |||||||||

Total revenue ton-miles | 129,352 | 122,874 | 125,303 | |||||||||

7.2 REVENUES

Our revenues are primarily derived from transporting freight. Other revenues are generated mainly from leasing of certain assets, switching fees, land sales and income from business partnerships.

At December 31, 2007, one customer comprised 11.5 % of total revenues and 6.2 % of total accounts receivable. At December 31, 2006 and 2005, the same customer comprised 11.5 % and 14.5 % of total revenues and 5.6 % and 8.0 % of total accounts receivable, respectively.

| For the year ended December 31 (in millions) | 2007 | 2006 | 2005 | |||||||||

| Grain | $ | 938.9 | $ | 904.6 | $ | 754.5 | ||||||

| Coal | 573.6 | 592.0 | 728.8 | |||||||||

| Sulphur and fertilizers | 502.0 | 439.3 | 447.1 | |||||||||

| Forest products | 275.8 | 316.4 | 333.9 | |||||||||

| Industrial and consumer products | 627.9 | 603.8 | 542.9 | |||||||||

| Automotive | 319.0 | 314.4 | 298.0 | |||||||||

| Intermodal | 1,318.0 | 1,256.8 | 1,161.1 | |||||||||

Total freight revenues | 4,555.2 | 4,427.3 | 4,266.3 | |||||||||

| Other revenues | 152.4 | 155.9 | 125.3 | |||||||||

Total revenues | $ | 4,707.6 | $ | 4,583.2 | $ | 4,391.6 | ||||||

| 2007 ANNUAL REPORT | ||||

| 17 | ||||

7.2.1 Freight Revenues

Freight revenues are earned from transporting bulk, merchandise and intermodal goods, and include fuel recoveries billed to our customers. Freight revenues were $4,555.2 million for 2007, an increase of $127.9 million, or 2.9 %. Freight revenues were $4,427.3 million in 2006, an increase of $161.0 million, or 3.8 %.

Freight revenues for 2007 increased mainly due to continued strong growth in bulk products and intermodal shipments along with increases in freight rates including fuel recoveries. These increases were partially offset by:

| □ | a decrease in coal freight rates; | |

| □ | continued weakness in Forest products, mainly lumber and panel, and certain Industrial and consumer products; and | |

| □ | the negative impact of the change in FX of approximately $89 million. |

Freight revenues in 2006 increased mainly due to:

| □ | higher freight rates, including fuel recoveries; | |

| □ | strong growth in grain shipments; and | |

| □ | strong growth in the Alberta economy. |

This increase was partially offset by the negative impact of the change in FX of approximately $113 million and reduced coal volumes.

7.2.1.1 Grain

Canadian grain products, consisting mainly of durum, spring wheat, barley, canola, flax, rye and oats, are primarily transported to ports for export and to Canadian and US markets for domestic consumption. US grain products mainly include durum, spring wheat, corn, soybeans and barley and are shipped from the midwestern US to other points in the Midwest, the Pacific Northwest and the northeastern US. Grain revenues in 2007 were $938.9 million, an increase of $34.3 million, or 3.8 %. Grain

revenues in 2006 were $904.6 million, an increase of $150.1 million, or 19.9%.

Grain revenues increased in 2007 primarily due to:

| □ | a large carryover from the first half of the 2006/07 crop year benefiting the first two quarters of 2007; | |

| □ | a strong export program as a result of strong commodity prices and demand for North American grain; and | |

| □ | higher freight rates. |

These increases were partially offset by the negative impact of the change in FX of approximately $24 million in 2007. In 2007, there was a higher proportion of US-dollar denominated grain traffic, compared with Canadian-dollar denominated grain traffic.

Grain revenues increased in 2006 primarily due to:

| □ | a strong Canadian grain crop reflecting improved quality; | |

| □ | a large carryover from the 2005/06 crop year; | |

| □ | increased shipments of western Canadian grain to the US as a result of a trade tariff being lifted; and | |

| □ | higher freight rates. |

These increases in grain revenues were partially offset by the negative impact of the change in FX of approximately $24 million.

7.2.1.2 Coal

Our Canadian coal business consists primarily of metallurgical coal transported from southeastern British Columbia (“BC”) to the ports of Vancouver, BC and Thunder Bay, Ontario, and to the US Midwest. Our US coal business consists primarily of the transportation of thermal coal and petroleum coke within the US Midwest. Coal revenues in 2007 were $573.6 million, a decrease of $18.4 million, or 3.1 %. Coal revenues in 2006 were $592.0 million, a decrease of $136.8 million, or 18.8 %.

Coal revenues decreased in 2007 primarily due to:

| □ | decreased freight rates; | |

| □ | decrease in carloads due to the sale of the Latta subdivision in the first half of 2006; and | |

| □ | the negative impact of the change in FX of approximately $5 million. |

These decreases were partially offset by increased volumes due to continued strong global demand for metallurgical coal.

The decline in coal revenues in 2006 was due to reduced export coal sales volumes by our primary coal customer and to the sale of our Latta subdivision. The decline also reflected a one-time positive adjustment of $23 million in 2005 for services provided to our primary coal customer in 2004 and the negative impact of the change in FX of approximately $7 million. Additionally, the sale of the Latta subdivision resulted in a decline of approximately 23,000 carloads of US coal in 2006 (representing approximately 40,000 carloads on an annual basis).

7.2.1.3 Sulphur and Fertilizers

Sulphur and fertilizers include potash, chemical fertilizers and sulphur shipped mainly from western Canada to the ports of Vancouver, BC, and Portland, Oregon, and to other Canadian and US destinations. Sulphur and fertilizers revenues in 2007 were $502.0 million, an increase of $62.7 million, or 14.3 %. Revenues in 2006 were $439.3 million, a decrease of $7.8 million, or 1.7 %.

Sulphur and fertilizers revenues increased in 2007 primarily due to an increase in demand for nutrients for bio fuels, partially offset by the negative impact of the change in FX of approximately $9 million.

The decline in 2006 was primarily due to the protracted global potash price negotiations which delayed the start of the shipping year until the third quarter of 2006 and the negative impact of the change in FX of

| 2007 ANNUAL REPORT | ||||

| 18 | ||||

approximately $10 million. Volumes rebounded following the completion of the negotiations; however, in 2006 Sulphur and fertilizers volumes were 23,500 carloads below 2005 volumes.

7.2.1.4 Forest Products

Forest products include lumber, wood pulp, paper products and panel transported from key producing areas in western Canada, Ontario and Quebec to various destinations in North America. Forest products revenues in 2007 were $275.8 million, a decrease of $40.6 million, or 12.8 %. Revenues in 2006 were $316.4 million, a decrease of $17.5 million, or 5.2 %.

Forest products revenues declined in 2007 primarily due to:

| □ | continued soft demand for lumber and panel products caused by a significant slowdown in the US housing market and continued impact from the sub-prime mortgage crisis; | |

| □ | difficult market conditions for our Forest product customers due to the softwood lumber agreement with the US which led to reduced volumes and extended plant shut downs; | |

| □ | the impact of the strengthening of the Canadian dollar, which has led to decreased market competitiveness for Canadian producers; and | |

| □ | the negative impact of the change in FX of approximately $10 million. |

These decreases were partially offset by growth in pulp volumes and price increases which lessened the impact from the volume decline.

Forest products revenues declined in 2006 primarily due to:

| □ | reduced volumes from a softening demand for lumber and panel caused by a decrease in US housing starts; | |

| □ | difficult market conditions for our Forest product customers caused by a strong Canadian dollar and softwood lumber agreement with the US which led to reduced volumes and extended plant shut downs; and | |

| □ | the negative impact of the change in FX of approximately $16 million. |

Offsetting these factors was our strong yield and pricing, which softened the impact from the volume decline.

7.2.1.5 Industrial and Consumer Products

Industrial and consumer products include chemicals, plastics, aggregates, steel, and mine and energy-related products (other than coal) shipped throughout North America. Industrial and consumer products revenues in 2007 were $627.9 million, an increase of $24.1 million, or 4.0 %. Revenues in 2006 were $603.8 million, an increase of $60.9 million, or 11.2 %.

Industrial and consumer products revenues increased in 2007 primarily due to strength in chemical, energy, and plastics shipments to and from Alberta as well as increases in freight rates, which were partially offset by decreased steel volumes as a result of decreased drilling activity for natural gas. The increases were also partially offset by the negative impact of the change in FX of approximately $20 million.

Industrial and consumer products revenues increased in 2006 primarily due to:

| □ | strong demand for steel, energy products and aggregates, largely driven by Alberta oil and gas activity and a strong Alberta economy; | |

| □ | strong worldwide demand for base metals; and | |

| □ | increased freight rates. |

The higher revenues were partially offset by the negative impact of the change in FX of approximately $25 million.

7.2.1.6 Automotive

Automotive consists primarily of the transportation of domestic and import vehicles as well as automotive parts from North American assembly plants and the Port of Vancouver to destinations in Canada and the US. Automotive revenues in 2007 were $319 million, an increase of $4.6 million, or 1.5 %. Revenues in 2006 were $314.4 million, an increase of $16.4 million, or 5.5 %.

Automotive revenues in 2007 were up, reflecting carload growth as new domestics (such as Toyota and Honda) and import volumes continue to increase. Increased volumes from key shippers as a result of certain port of call changes by shipping lines also had a favourable impact on Automotive revenues. These increases were partially offset by the negative impact of the change in FX of approximately $8 million in 2007.

The increase in Automotive revenues in 2006 was primarily due to higher freight rates and increased volumes of imported vehicles, which created growth in long-haul traffic. These increases were partially offset by extended plant shutdowns by domestic auto producers and the negative impact of the change in FX of approximately $12 million.

| 2007 ANNUAL REPORT | ||||

| 19 | ||||

7.2.1.7 Intermodal

Intermodal consists of domestic and international (import-export) container traffic. Our domestic business consists primarily of retail goods moving in containers between eastern and western Canada and to and from the US. The international business handles containers of mainly retail goods between the ports of Vancouver, Montreal, New York/New Jersey and Philadelphia and inland Canadian and US destinations. Intermodal revenues in 2007 were $1,318.0 million, an increase of $61.2 million, or 4.9 %. Revenues in 2006 were $1,256.8 million, an increase of $95.7 million, or 8.2 %.

Intermodal revenues increased in 2007 primarily due to growth in import and export container shipments from the ports of Vancouver and Montreal and increased freight rates, partially offset by the negative impact of the change in FX of approximately $13 million.

International intermodal revenues increased in 2006 as a result of higher freight rates and container volume growth at the ports of Vancouver and Montreal driven by strong global trade. Revenue growth in domestic intermodal was due to increased freight rates, volume and long-haul traffic. These increases were partially offset by an extended strike at a facility at the Port of Philadelphia as well as the negative impact of the change in FX of approximately $19 million.

7.2.2 Other Revenues

Other revenues are generated from leasing certain assets, switching fees, land sales, and business partnerships. Other revenues in 2007 were $152.4 million, a decrease of $3.5 million. Other revenues in 2006 were $155.9 million, an increase of $30.6 million.

The decrease in Other revenues in 2007 was primarily due to a gain of approximately $18 million realized from the sale of our Latta subdivision in second-quarter 2006 (discussed further in Section 21.5), partially offset by an increase in land sales in 2007.

Other revenues increased in 2006 due to a gain of approximately $18 million realized from the sale of our Latta subdivision and increased land sales, in particular, the sale of a property to a university in Montreal.

7.2.3 Freight Revenue per Carload

Freight revenue per carload is the amount of freight revenue earned for every carload moved, calculated by dividing the freight revenue for a commodity by the number of carloads of the commodity transported in the period.

In 2007, total freight revenue per carload remained relatively unchanged from 2006. This reflected 2.0 % improvements in freight rates and mix, which were offset by the negative impact of the change in FX.

Total freight revenue per carload in 2006 increased by $97, or 6.1 %, from 2005. The increase in 2006 was due to higher freight rates, the impact of the sale of our Latta subdivision and Nickel Spur, and an increase in the average length of haul. The increases more than offset the negative impact of the change in FX.

FREIGHT REVENUE PER CARLOAD

| For the year ended December 31 ($) | 2007 | 2006 | 2005 | |||||||||

Freight revenue per carload | 1,688 | 1,691 | 1,594 | |||||||||

| Grain | 2,439 | 2,363 | 2,228 | |||||||||

| Coal | 2,132 | 2,102 | 2,069 | |||||||||

| Sulphur and fertilizers | 2,393 | 2,464 | 2,216 | |||||||||

| Forest products | 2,417 | 2,344 | 2,172 | |||||||||

| Industrial and consumer products | 2,004 | 1,911 | 1,685 | |||||||||

| Automotive | 1,893 | 1,902 | 1,773 | |||||||||

| Intermodal | 1,065 | 1,084 | 1,019 | |||||||||

| 2007 ANNUAL REPORT | ||||

| 20 | ||||

8.0 Performance Indicators

The indicators listed in this table are key measures of our operating performance. Definitions of these performance indicators are provided in Section 26.0.

PERFORMANCE INDICATORS(1)

| For the year ended December 31 | 2007 | 2006 | 2005 | |||||||||

Safety indicators | ||||||||||||

| FRA personal injuries per 200,000 employee-hours | 2.1 | 2.0 | 2.4 | |||||||||

| FRA train accidents per million train-miles | 2.0 | 1.6 | 2.3 | |||||||||

Efficiency and other indicators | ||||||||||||

| Gross ton-miles (“GTM”) of freight (millions) | 246,322 | 236,405 | 242,100 | |||||||||

| Car miles per car day | 142.3 | 137.3 | 124.0 | |||||||||

| US gallons of locomotive fuel consumed per 1,000 GTMs – freight and yard | 1.21 | 1.20 | 1.18 | |||||||||

| Terminal dwell (hours) | 22.2 | 20.8 | 25.8 | |||||||||

| Average train speed (miles per hour) | 23.2 | 24.8 | 22.0 | |||||||||

| Number of active employees – end of period | 15,382 | 15,327 | 16,295 | |||||||||

| Freight revenue per RTM (cents) | 3.52 | 3.60 | 3.40 | |||||||||

| (1) Certain comparative period figures have been updated to reflect new information. | ||

8.1 SAFETY INDICATORS

Safety is a key priority for our management and Board of Directors. Our two main safety indicators – personal injuries and train accidents – follow strict US Federal Railroad Administration (“FRA”) reporting guidelines.

The FRA personal injury rate per 200,000 employee-hours was 2.1 in 2007, compared with 2.0 in 2006 and 2.4 in 2005.

The FRA train accident rate in 2007 was 2.0 accidents per million train-miles, compared with 1.6 and 2.3, respectively, in 2006 and 2005.

8.2 EFFICIENCY AND

OTHER INDICATORS

OTHER INDICATORS

In 2007, CP moved record freight volumes, as measured by GTMs and RTMs. In addition, CP’s IOP generated savings in operating costs driven by increased train weights, yard productivity and improvements in car miles per car day. Offsetting these benefits were:

| □ | difficult weather-related operating conditions, primarily in the first quarter of 2007 and December 2007; |

| □ | a change in traffic mix largely driven by an increase in intermodal trains; and | |

| □ | the impact of having to compress required track maintenance programs into a shorter work season due to the 26-day strike by CP’s maintenance of way employees in Canada during the second quarter of 2007 (“CP strike”). |

GTMs increased 4.2 % to a record of approximately 246.3 billion in 2007. The increase in 2007 was mainly due to increased potash, intermodal and coal traffic. GTMs declined 2.4 % in 2006. The decrease in 2006 was mainly due to lower coal and potash volumes partially offset by higher grain volumes. Fluctuations in GTMs normally drive fluctuations in certain variable costs, such as fuel and train crew costs.

Car miles per car day increased 3.6 % in 2007 and increased 10.7 % in 2006. Car miles per car day increased in both years, as the higher level of demand was handled more efficiently through improved car ordering and tactical fleet management and IOP improvements.

US gallons of locomotive fuel consumed per 1,000 GTMs in both freight and yard activity increased 0.8 % and 1.7 % in 2007 and 2006, respectively. The increase in both years was primarily due to a change in traffic mix largely driven by an increase in intermodal trains. The increases were partially offset by improved execution of our IOP and successful fuel-conservation efforts. In addition, mild winter weather in the first quarter of 2006 helped to reduce fuel consumption in 2006.

Terminal dwell, the average time a freight car resides in a terminal, increased 6.7 % in 2007. The increase in 2007 was primarily due to weather-related issues and concentrated track maintenance programs following the end of the CP strike. Terminal dwell decreased 19.4 % in 2006. The improvement in 2006 was largely due to better processes within our yards and providing seven-day-a-week outlets for all our traffic which minimized the number of times freight cars are handled. Reducing the time freight cars spend waiting in terminals also enabled us to decrease our fleet of cars used.

| 2007 ANNUAL REPORT | ||||

| 21 | ||||

Average train speed decreased 6.5 % in 2007. Average train speed in 2007 was negatively impacted by:

| □ | an increase in the number of bulk trains, which operate at slower speeds and experienced more queuing for unloading in 2007; | |

| □ | network disruptions, which were primarily related to weather events; | |

| □ | temporary power and crew shortages; and | |

| □ | concentrated track maintenance programs following the end of the CP strike. |

Average train speed increased 12.7 % in 2006. Trains moved at faster speeds for longer distances as a result of our expanded track capacity in western Canada, adhering to

our IOP, and co-production agreements with other railroads that allowed us to move trains more efficiently. Train speed also increased as a result of transporting less bulk volumes, which move in heavy trains that travel more slowly.

The number of active employees at December 31, 2007 increased by 55, or 0.4 %. The primary driver for this increase was a higher number of employees working on capital projects in December 2007, due to work schedule delays resulting from the CP strike. The number of active employees at December 31, 2006 decreased by 5.9 %. This decrease was mainly due to job reductions made under restructuring initiatives and fewer employees working

on capital projects. Approximately 7 % of employees were assigned to capital projects at December 31, 2007, compared with approximately 6 % at December 31, 2006.

Freight revenue per RTM decreased by 2.2 % in 2007. The decrease was primarily driven by the negative impact of the change in FX and a decrease in coal freight rates, as well as a change in our overall traffic mix as a result of an increase in the shipment of long haul US grain traffic to the Pacific Northwest and shipment of long haul potash from Saskatchewan to the Port of Vancouver. Freight revenue per RTM increased 5.9 % in 2006. The increase was due to higher freight rates, partially offset by the negative impact of the change in FX.

9.0 Operating Expenses, Before Other Specified Items

OPERATING EXPENSES, BEFORE OTHER SPECIFIED ITEMS

| For the year ended December 31 | 2007 | 2006 | 2005 | ||||||||||||||||||||||||

| (in millions) | Expense(1) | % of revenue | Expense(1) | % of revenue | Expense(1) | % of revenue | |||||||||||||||||||||

| Compensation and benefits | $ | 1,284.2 | 27.3 | $ | 1,327.6 | 29.0 | $ | 1,322.1 | 30.1 | ||||||||||||||||||

| Fuel | 746.8 | 15.9 | 650.5 | 14.2 | 588.0 | 13.4 | |||||||||||||||||||||

| Materials | 215.5 | 4.6 | 212.9 | 4.6 | 203.3 | 4.6 | |||||||||||||||||||||

| Equipment rents | 207.5 | 4.4 | 181.2 | 4.0 | 210.0 | 4.8 | |||||||||||||||||||||

| Depreciation and amortization | 472.0 | 10.0 | 464.1 | 10.1 | 445.1 | 10.1 | |||||||||||||||||||||

| Purchased services and other | 617.4 | 13.1 | 618.3 | 13.5 | 621.6 | 14.2 | |||||||||||||||||||||

Total | $ | 3,543.4 | 75.3 | $ | 3,454.6 | 75.4 | $ | 3,390.1 | 77.2 | ||||||||||||||||||

(1) These earnings measures have no standardized meanings prescribed by Canadian GAAP and,therefore,are unlikely to be comparable to similar measures of other companies. These earnings measures and other specified items are described in Section 6.0.

Operating expenses, before other specified items, were $3,543.4 million in 2007, up $88.8 million, or 2.6%. These expenses were $3,454.6 million in 2006, up $64.5 million, or 1.9%, from $3,390.1 million in 2005.

Operating expenses in 2007 increased primarily due to:

| □ | higher fuel prices driven by higher refining charges and WTI prices; |

| □ | record volumes as measured by GTMs and RTMs in 2007, including change in traffic mix largely driven by an increase in intermodal trains; |

| □ | increased equipment rent expense; and | |

| □ | higher costs associated with network disruptions,mainly driven by harsh weather conditions. |

These increases in operating expenses were partially offset by the positive impact of the change in FX of approximately $57 million and a decrease in compensation and benefits expense.

| 2007 ANNUAL REPORT | ||||

| 22 | ||||

Operating expenses in 2006 were higher primarily due to:

| □ | higher fuel costs; | |

| □ | the increased price of materials used for freight car repairs, primarily related to the replacement of wheel sets, and train servicing; and | |

| □ | increased depreciation and amortization expense. |

These increases were partially offset by improved operating efficiencies, cost-containment initiatives, lower GTMs, and the positive impact of the change in FX of approximately $86 million. In addition, the higher fuel costs were largely recovered in revenue through our fuel recovery program and through the benefits of hedging.

9.1 COMPENSATION AND BENEFITS

Compensation and benefits expense includes employee wages, salaries and fringe benefits. Compensation and benefits expense was $1,284.2 million in 2007, a decrease of $43.4 million. This expense was $1,327.6 million in 2006, an increase of $5.5 million from $1,322.1 million in 2005.

Compensation and benefits expense decreased in 2007 primarily due to:

| □ | lower incentive and stock-based compensation; | |

| □ | lower pension expenses; | |

| □ | the positive impact of the change in FX of approximately $13 million; and | |

| □ | a settlement gain in the third quarter of 2007 on the release of certain post-retirement benefit liabilities due to the assumption of these obligations by a US national multi-employer benefit plan. |

These decreases were partially offset by increased labour expenses due to higher volumes and the negative impact of inflation.

In 2006, compensation and benefits expense increased as a result of inflation, higher pension expenses, and higher stock-

based compensation costs prior to the implementation in the second quarter of 2006 of our Total Return Swap Program (discussed further in Section 17.7.1). These increases were mostly offset by:

| □ | reduced costs as a result of restructuring initiatives (discussed further in Section 21.10); | |

| □ | savings realized from efficiencies gained through our IOP (discussed further in Section 21.3) as well as other productivity improvements; | |

| □ | reduced costs as a result of lower freight volumes; and | |

| □ | the positive impact of the change in FX of approximately $22 million. |

9.2 FUEL

Fuel expense consists of the cost of fuel used by locomotives and includes provincial, state and federal fuel taxes and the impact of our hedging program. Fuel expense was $746.8 million in 2007, an increase of $96.3 million. This expense was $650.5 million in 2006, an increase of $62.5 million from 2005.

Fuel expense in 2007 increased primarily due to:

| □ | higher refining margins and WTI prices; | |

| □ | increased consumption driven by increased volumes; | |

| □ | a lower hedge position in 2007; and | |

| □ | a higher rate of fuel consumption, driven by harsh weather conditions and change in traffic mix largely driven by an increase in intermodal trains. |

The increases were partially offset by the positive impact of the change in FX of approximately $23 million. Fuel price increases are also mitigated by our fuel recovery program.

Fuel expense in 2006 increased due to higher crude oil prices and refining charges, and an unfavourable change in our fuel

consumption rate due to a higher proportion of non-bulk freight traffic. These increases were partially offset by:

| □ | the favourable settlement of prior period recoveries including a fuel excise tax refund; | |

| □ | reduced workload; and | |

| □ | the positive impact of the change in FX of approximately $30 million. |

9.3 MATERIALS

Materials expense includes the cost of materials used for track, locomotive, freight car, and building maintenance. Materials expense was $215.5 million in 2007, an increase of $2.6 million. This expense was $212.9 million in 2006, an increase of $9.6 million from $203.3 million in 2005.

The increase in 2007 was mainly due to the higher cost of materials used for freight car repairs and train servicing, primarily driven by higher wheel consumption as a result of increased volume and harsh winter operating conditions in first-quarter 2007, and an increase in locomotive repair and servicing costs. These increases were partially offset by cost recoveries from third parties and pricing arrangements for wheels.

The increase in 2006 was mainly due to the higher cost of materials for freight car repairs, primarily driven by price increases for replacement of wheel sets and other freight car materials, and train servicing. The increase was partially offset by the positive impact of the change in FX.

9.4 EQUIPMENT RENTS

Equipment rents expense includes the cost to lease freight cars, intermodal equipment and locomotives from other companies, including railways. Equipment rents expense was $207.5 million in 2007, an increase of $26.3 million. This expense was $181.2 million in 2006, a decrease of $28.8 million from $210.0 million in 2005.

| 2007 ANNUAL REPORT | ||||

| 23 | ||||

Equipment rents expense in 2007 increased mainly due to:

| □ | reductions in receipts for the use of our railcars from other railways and customers; | |

| □ | higher equipment rental payments to other railways as a result of network disruptions, mainly driven by harsh weather conditions; and | |

| □ | higher locomotive leasing costs, primarily driven by increased volume. |

These increases were partially offset by the positive impact of the change in FX of approximately $7 million.

The decrease in 2006 was mainly due to more efficient movement of traffic over our network which reduced the number of cars on line, resulting in lower equipment rental payments to other railways and reduced locomotive lease costs. Higher charges to customers for loading and unloading delays and the positive impact of the change in FX of approximately $12 million also contributed to the decrease in 2006. The decrease in 2006 was partially offset by favourable adjustments in 2005 for freight car rentals pertaining to prior periods.