Wells Fargo Commercial Mortgage Trust 2016-LC25

Filed: 10 Nov 16, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-11 | ||

Free Writing Prospectus

Collateral Term Sheet

$954,965,554

(Approximate Initial Pool Balance)

Wells Fargo Commercial Mortgage Trust 2016-LC25

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Ladder Capital Finance LLC

Wells Fargo Bank, National Association

Rialto Mortgage Finance, LLC

National Cooperative Bank, N.A.

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2016-LC25

November 9, 2016

WELLS FARGO SECURITIES | ||

Lead Manager and Sole Bookrunner | ||

Academy Securities Co-Manager | Deutsche Bank Securities Co-Manager | |

| Wells Fargo Commercial Mortgage Trust 2016-LC25 | Certain Terms and Conditions |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (’’SEC’’) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale.

In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| 9 WEST 57TH STREET |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| 9 WEST 57TH STREET |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| 9 WEST 57TH STREET |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| No. 1 – 9 West 57th Street | ||||||||

| Loan Information | Property Information | |||||||

| Mortgage Loan Seller: | Ladder Capital Finance LLC | Single Asset/Portfolio: | Single Asset | |||||

| Credit Assessment (DBRS/Fitch/Moody’s/Morningstar): | AAA/AAA/AAA(sca.pd)/A- | Property Type: | Office | |||||

| Original Principal Balance(1): | $50,000,000 | Specific Property Type: | CBD | |||||

| Cut-off Date Balance(1): | $50,000,000 | Location: | New York, NY | |||||

| % of Initial Pool Balance: | 5.2% | Size: | 1,680,218 SF | |||||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF(1): | $603.33 | |||||

| Borrower Names: | Solow Building Company II, L.L.C.; Solovieff Realty Co. II, L.L.C. | Year Built/Renovated: | 1972/NAP | |||||

| Sponsor: | Sheldon H. Solow | Title Vesting: | Fee / Leasehold | |||||

| Mortgage Rate: | 2.8595% | Property Manager: | Self-managed | |||||

| Note Date: | August 30, 2016 | 4th Most Recent Occupancy (As of)(4): | 56.9% (12/31/2012) | |||||

| Anticipated Repayment Date: | NAP | 3rd Most Recent Occupancy (As of)(4): | 50.9% (12/31/2013) | |||||

| Maturity Date: | September 1, 2026 | 2nd Most Recent Occupancy (As of)(4): | 63.5% (12/31/2014) | |||||

| IO Period: | 120 months | Most Recent Occupancy (As of)(4): | 67.3% (12/31/2015) | |||||

| Loan Term (Original): | 120 months | Current Occupancy (As of)(4): | 63.5% (6/1/2016) | |||||

| Seasoning: | 3 months | |||||||

| Amortization Term (Original): | NAP | Underwriting and Financial Information: | ||||||

| Loan Amortization Type: | Interest-only, Balloon | 4th Most Recent NOI (As of)(5): | $60,972,979 (12/31/2013) | |||||

| Interest Accrual Method: | Actual/360 | 3rd Most Recent NOI (As of)(5): | $67,687,210 (12/31/2014) | |||||

| Call Protection: | L(27),D(86),O(7) | 2nd Most Recent NOI (As of)(5): | $85,164,572 (12/31/2015) | |||||

| Lockbox Type: | Hard/Springing Cash Management | Most Recent NOI (As of)(5): | $97,014,333 (TTM 6/30/2016) | |||||

| Additional Debt(1): | Yes | |||||||

| Additional Debt Type(1)(2): | Pari Passu, Subordinate Debt and Future Mezzanine | |||||||

| U/W Revenues: | $166,714,099 | |||||||

| U/W Expenses: | $58,877,243 | |||||||

| Escrows and Reserves(3): | U/W NOI(6): | $107,836,855 | ||||||

| U/W NCF(6): | $107,098,067 | |||||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NOI DSCR(1): | 3.67x | |||

| Taxes | $9,417,640 | $3,139,213 | NAP | U/W NCF DSCR(1): | 3.64x | |||

| Insurance | $264,333 | $88,111 | NAP | U/W NOI Debt Yield(1): | 10.6% | |||

| Replacement Reserve | $0 | $61,615 | $2,500,000 | U/W NCF Debt Yield(1): | 10.6% | |||

| TI/LC Reserve | $25,000,000 | Springing | $25,000,000 | As-Is Appraised Value: | $3,400,000,000 | |||

| Outstanding TI/LC Reserve | $13,061,790 | $0 | NAP | As-Is Appraisal Valuation Date: | July 28, 2016 | |||

| Free Rent Reserve | $16,462,228 | $0 | NAP | Cut-off Date LTV Ratio(1): | 29.8% | |||

| Deferred Maintenance | $287,500 | $0 | NAP | LTV Ratio at Maturity or ARD(1): | 29.8% | |||

| (1) | See “The Mortgage Loan” section. All statistical information related to balances per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based on the 9 West 57th Street Senior Notes only. The Cut-off Date LTV Ratio, U/W NCF DSCR and U/W NCF Debt Yield based on the 9 West 57th Street Whole Loan, including the 9 West 57th Street Subordinate Companion Note, are 35.3%, 3.08x and 8.9%, respectively. |

| (2) | See “Subordinate and Mezzanine Indebtedness” section. |

| (3) | See “Escrows” section. |

| (3) | See “Historical Occupancy” section. |

| (4) | See “Cash Flow Analysis” section. |

The Mortgage Loan.The mortgage loan (the “9 West 57th Street Mortgage Loan”) is part of a whole loan (the “9 West 57th Street Whole Loan”) evidenced by six seniorparipassu notes (the “9 West 57th Street Senior Notes”) and one subordinate note (the “9 West 57th Street” Subordinate Companion Note”), secured by the fee and leasehold interests in a 50-story office building located on West 57th Street in Manhattan, New York (the “9 West 57th Street Property”). The 9 West 57th Street Whole Loan was originated on August 30, 2016 by JPMorgan Chase Bank, National Association and the Note A-3-A in the original principal amount of $50,000,000 was subsequently purchased by Ladder Capital Finance LLC. The 9 West 57th Street Whole Loan had an original principal balance of $1,200,000,000 has an outstanding principal balance as of the Cut-off Date of $1,200,000,000 and accrues interest at an interest rate of 2.8595%per annum. The 9 West 57th Street Whole Loan had an initial term of 120 months, has a remaining term of 117 months as of the Cut-off Date and requires interest-only payments through the term of the 9 West 57th Street Whole Loan. The 9 West 57th Street Whole Loan matures on September 1, 2026.

Note A-3-A, which will be contributed to the WFCM 2016-LC25 Trust, had an original principal balance of $50,000,000, has an outstanding principal balance as of the Cut-off Date of $50,000,000 and represents a non-controlling interest in the 9 West 57th Street Whole Loan. The controlling Note A-1 and the 9 West 57th Street Subordinate Companion Loan (Note B-1) were contributed to the JPMCC 2016-NINE Trust. Note A-2 was contributed to the JPMCC 2016-JP3 securitization Trust; Note A-3-B is expected to be contributed to the CSAIL 2016-C7 securitization trust; Note A-4 was contributed to the JPMDB 2016-C4 securitization trust and the

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| 9 WEST 57TH STREET |

remaining Note A-5 is currently held by JPMorgan Chase Bank, National Association and is expected to be contributed to future securitization trusts. Notes A-1, A-2, A-3-B, A-4, A-5 and B-1 collectively constitute the “9 West 57th Street Companion Notes”. The related mortgage loan seller provides no assurances that Note A-5 will not be split further. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced Whole Loan Loans—9 West 57th Street Whole Loan” in the Preliminary Prospectus.

Note Summary

| Original Balance | Note Holder | Controlling Piece | ||

| Note A-1 | $670,724,000 | JPMCC 2016-NINE | Yes | |

| Note A-2 | $100,000,000 | JPMCC 2016-JP3 | No | |

| Note A-3-A | $50,000,000 | WFCM 2016-LC25 | No | |

| Note A-3-B | $50,000,000 | CSAIL 2016-C7 | No | |

| Note A-4 | $80,000,000 | JPMDB 2016-C4 | No | |

| Note A-5 | $63,000,000 | JPMCB | No | |

| Note B-1 | $186,276,000 | JPMCC 2016-NINE | No | |

| Total | $1,200,000,000 |

Following the lockout period, on any date before March 1, 2026 the borrower has the right to defease the 9 West 57th Street Whole Loan in whole, but not in part. In addition, the 9 West 57th Street Whole Loan is prepayable without penalty on or after March 1, 2026. The lockout period will expire on the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) the third anniversary of the origination date.

Sources and Uses

| Sources | Uses | |||||||||

| Original whole loan amount | $1,200,000,000 | 100.0% | Loan payoff(1) | $630,769,032 | 52.6 | % | ||||

| Reserves | 64,493,490 | 5.4 | ||||||||

| Closing costs | 19,764,970 | 1.6 | ||||||||

| Return of equity | 484,972,507 | 40.4 | ||||||||

| Total Sources | $1,200,000,000 | 100.0% | Total Uses | $1,200,000,000 | 100.0 | % | ||||

| (1) | The 9 West 57th Street Property was previously securitized in COMM 2012-9W57. |

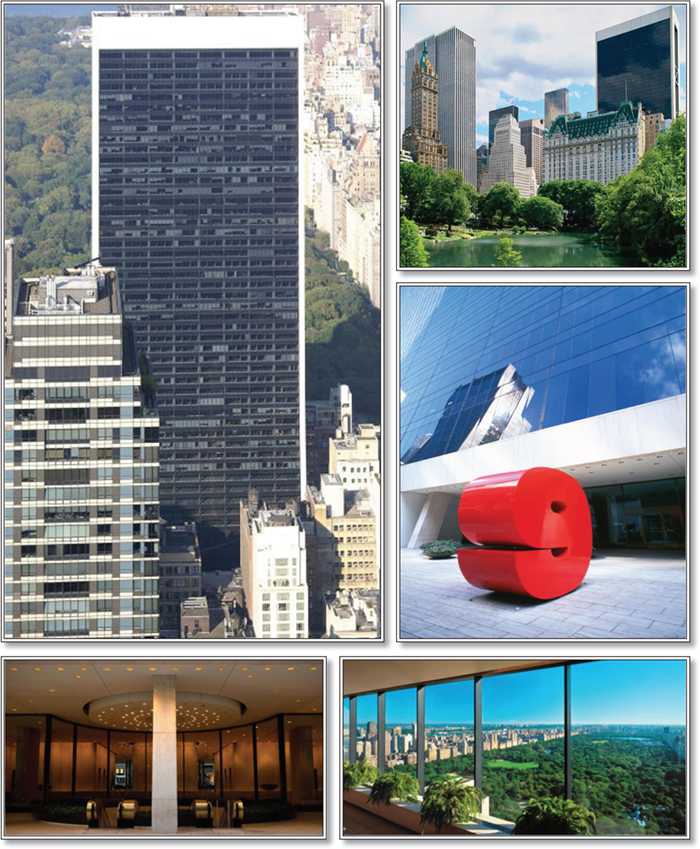

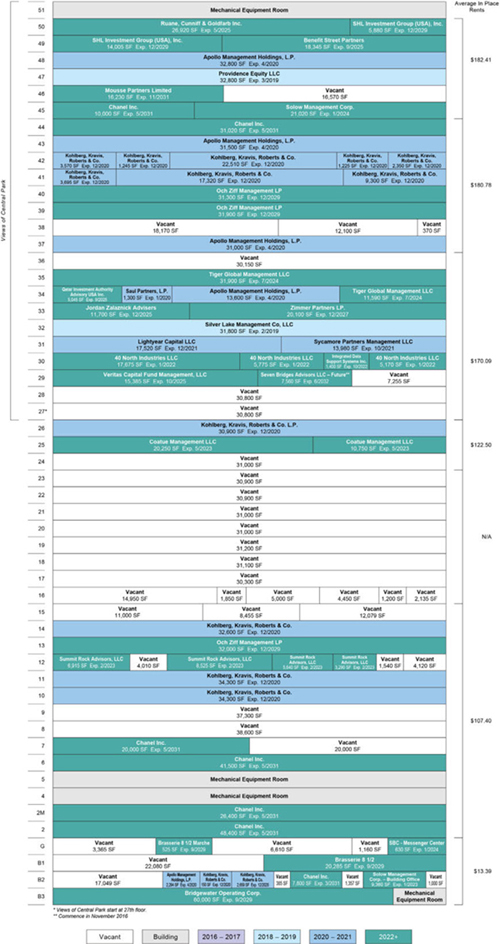

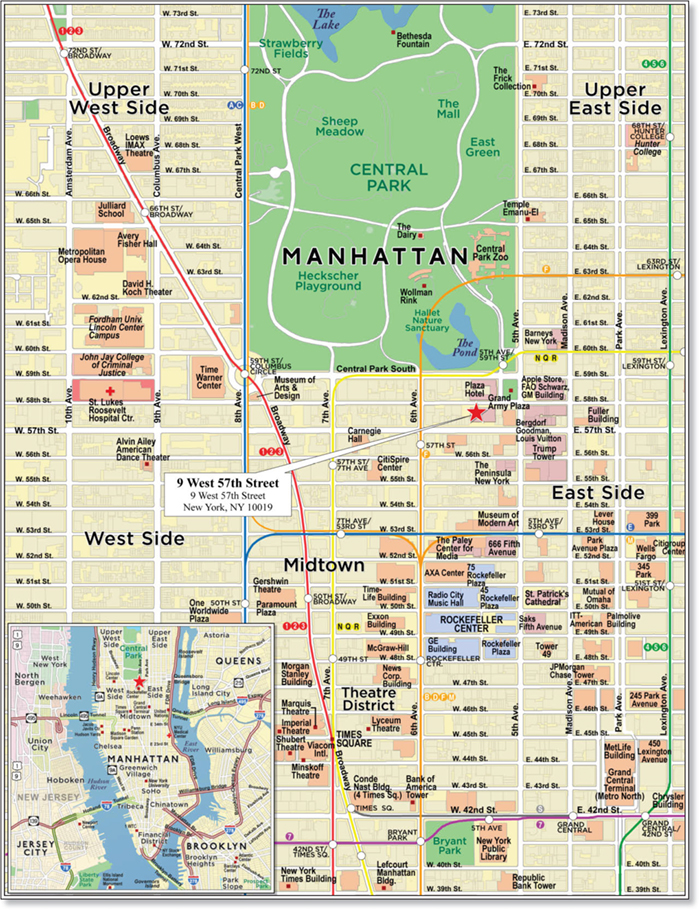

The Property.The 9 West 57th Street Property is a 50-story, 1,680,218 square foot, Class A office building located on West 57th Street in Manhattan, New York, between 5th and 6th Avenues. The 9 West 57th Street Property is located near the 5th Avenue retail corridor and across the street from the Plaza Hotel within the Plaza District Submarket. 9 West 57th Street consists of 50 stories with 47 office levels and three subterranean levels that contain a mix of retail, storage and service areas as well as a 285-space parking garage representing a parking ratio of 0.2 parking spaces per 1,000 square feet of rentable area. The full-service restaurant, Brasserie 8 ½, is located on the first subterranean level. According to the appraisal, the 9 West 57th Street Property is an iconic trophy office building and benefits from its Plaza District location, quality tenancy and unobstructed views of Central Park from the 27th floor and above. As of June 1, 2016, the 9 West 57th Street Property was leased to 26 tenants, including a number of institutional quality tenants. The 9 West 57th Street Property serves as headquarters’ locations for Kohlberg, Kravis, Roberts & Co. (“KKR”), Chanel Inc. (“Chanel”), Apollo Management Holdings, L.P. (“Apollo”), Och Ziff Management LP, Tiger Global Management LLC and Ruane, Cunniff & Goldfarb Inc. The 9 West 57th Street Property commands some of the highest per square foot office rents in Manhattan with certain higher floor in-place rents exceeding $200.00 per square foot on a gross basis. As of June 1, 2016, the 9 West 57th Street Property was 63.5% occupied, which is below the Plaza District Submarket occupancy of 89.9%. The sponsor is currently marketing the approximately 600,000 square feet of vacant space at the 9 West 57th Street Property.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| 9 WEST 57TH STREET |

The following table presents certain information relating to the tenancy at the 9 West 57th Street Property:

Major Tenants

| Tenant Name | Credit Rating (Fitch/Moody’s /S&P)(1) | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF(2) | Annual U/W Base Rent(2) | % of Total Annual U/W Base Rent | Lease Expiration Date | ||||||

| Major Tenants | |||||||||||||

| Kohlberg, Kravis, Roberts & Co. | A/NR/A | 196,124 | 11.7% | $121.48 | $23,825,357 | 16.1% | 12/31/2020(3) | ||||||

| Chanel Inc. | NR/NR/NR | 185,120 | 11.0% | $119.07 | $22,042,082 | 14.9% | 5/31/2031(4) | ||||||

| Apollo Management Holdings, L.P. | A-/NR/A | 111,194 | 6.6% | $167.27 | $18,599,624 | 12.6% | 4/30/2020(5) | ||||||

| Och Ziff Management LP | NR/NR/NR | 95,200 | 5.7% | $180.18 | $17,153,400 | 11.6% | 12/31/2029 | ||||||

| Providence Equity LLC | NR/NR/NR | 51,145 | 3.0% | $204.62 | $10,465,275 | 7.1% | Various(6) | ||||||

| Total Major Tenants | 638,783 | 38.0% | $144.16 | $92,085,738 | 62.2% | ||||||||

| Non-Major Tenants | 428,125 | 25.5% | $130.59 | $55,909,450 | 37.8% | ||||||||

| Occupied Collateral Total | 1,066,908 | 63.5% | $138.71 | $147,995,188 | 100.0% | ||||||||

| Vacant Space | 613,310 | 36.5% | |||||||||||

| Collateral Total | 1,680,218 | 100.0% | |||||||||||

| (1) | Certain ratings are those of the parent company whether or not the parent guarantees the lease. |

| (2) | Annual U/W Base Rent PSF and Annual U/W Base Rent include contractual rent steps through August 9, 2017, totaling $216,500. |

| (3) | Kohlberg, Kravis, Roberts & Co. has acquired an approximately 343,000 square foot condominium at Hudson Yards, an office development in West Midtown, Manhattan. There can be no assurances that KKR will not vacate the property upon lease expiration in December 2020. Excluding KKR from the in-place underwritten base rent, UW NCF DSCR would be equal to 2.30x. |

| (4) | Chanel Inc’s storage lease for 7,800 square feet expires March 31, 2031. |

| (5) | Both of Apollo Management Holdings, L.P.’s 13,600 square foot office lease and the 2,294 square foot storage lease expire on April 15, 2020. |

| (6) | The 51,145 square foot space also includes space leased to Benefit Street Partners, an affiliate of Providence Equity LLC. Providence Equity LLC’s lease for 32,800 square feet expires on March 15, 2019. Benefit Street Partners’ lease for 18,345 square feet expires on September 30, 2025. Benefit Street Partners has the right to terminate its lease as of September 1, 2022 with at least 12 months’ notice and the payment of a termination fee approximately equal to the sum of (i) an amount equal to four months of base rent and (ii) any unamortized brokerage commissions paid by the landlord on account of the lease. |

The following table presents certain information relating to the lease rollover schedule at the 9 West 57th Street Property:

Lease Expiration Schedule(1)(2)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(3)(4) | % of Annual U/W Base Rent | Annual U/W Base Rent PSF(3) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2016 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2017 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2018 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2019 | 2 | 64,600 | 3.8% | 64,600 | 3.8% | $13,089,000 | 8.8% | $202.62 |

| 2020 | 3 | 308,618 | 18.4% | 373,218 | 22.2% | $42,632,981 | 28.8% | $138.14 |

| 2021 | 2 | 31,500 | 1.9% | 404,718 | 24.1% | $5,109,900 | 3.5% | $162.22 |

| 2022 | 2 | 30,020 | 1.8% | 434,738 | 25.9% | $5,204,730 | 3.5% | $173.38 |

| 2023 | 2 | 64,730 | 3.9% | 499,468 | 29.7% | $6,827,514 | 4.6% | $105.48 |

| 2024 | 3 | 65,140 | 3.9% | 564,608 | 33.6% | $10,046,735 | 6.8% | $154.23 |

| 2025 | 5 | 77,395 | 4.6% | 642,003 | 38.2% | $14,301,223 | 9.7% | $184.78 |

| 2026 | 0 | 0 | 0.0% | 642,003 | 38.2% | $0 | 0.0% | $0.00 |

| Thereafter | 8 | 424,905 | 25.3% | 1,066,908 | 63.5% | $50,783,105 | 34.3% | $119.52 |

| Vacant | 0 | 613,310 | 36.5% | 1,680,218 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 27 | 1,680,218 | 100.0% | $147,995,188 | 100.0% | $138.71 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Certain tenants may have lease termination or contraction options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the Lease Expiration Schedule. |

| (3) | Weighted Average Annual U/W Base Rent PSF excludes vacant space. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| 9 WEST 57TH STREET |

The following table presents historical occupancy percentages at the 9 West 57th Street Property:

Historical Occupancy

12/31/2012(1) | 12/31/2013(1)(2) | 12/31/2014(1)(2) | 12/31/2015(1)(2) | 6/1/2016(3) | ||||

| 56.9% | 50.9% | 63.5% | 67.3% | 63.5% |

| (1) | Information obtained from the borrower. |

| (2) | The increase in occupancy from 2013 to 2014 is primarily due to leases signed with SHL Investment Group (USA), Inc. and Benefit Street Partners LLC. The increase from 2014 to 2015 occupancy is primarily driven by leases signed with Tiger Global Management LLC, Qatar Investment Authority Advisory USA Inc. and Veritas Capital Fund Management, LLC. |

| (3) | Information obtained from the underwritten rent roll. |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and the underwritten net cash flow at the 9 West 57th Street Property:

Cash Flow Analysis

| 2013(1) | 2014(1) | 2015(1) | TTM 6/30/2016(1) | U/W(2) | % of U/W Effective Gross Income | U/W $ per SF | |||||||

| Base Rent | $96,419,788 | $104,395,474 | $128,865,929 | $141,867,688 | $147,995,188(3) | 88.8% | $88.08 | ||||||

| Grossed Up Vacant Space | 0 | 0 | 0 | 0 | 82,518,645 | 49.5 | 49.11 | ||||||

| Total Reimbursables | 18,367,753 | 20,686,585 | 18,213,824 | 17,863,714 | 16,775,136 | 10.1 | 9.98 | ||||||

| Other Income | 1,960,765 | 2,011,104 | 1,649,779 | 1,754,505 | 1,943,774 | 1.2 | 1.16 | ||||||

| Less Vacancy & Credit Loss | 0 | 0 | 0 | 0 | (82,518,645)(4) | (49.5) | (49.11) | ||||||

| Effective Gross Income | $116,748,306 | $127,093,163 | $148,729,532 | $161,485,907 | 166,714,099 | 100.0% | $99.22 | ||||||

| Total Operating Expenses | $55,775,327 | $59,405,953 | $63,564,960 | $64,471,574 | $58,877,243 | 35.3% | $35.04 | ||||||

| Net Operating Income | $60,972,979 | $67,687,210 | $85,164,572 | $97,014,333 | $107,836,855 | 64.7% | $64.18 | ||||||

| TI/LC | 0 | 0 | 0 | 0 | 0 | 0.0 | 0.00 | ||||||

| Capital Expenditures | 0 | 0 | 0 | 0 | 738,788 | 0.4 | 0.44 | ||||||

| Net Cash Flow | $60,972,979 | $67,687,210 | $85,164,572 | $97,014,333 | $107,098,067 | 64.2% | $63.74 | ||||||

| NOI DSCR(5) | 2.07x | 2.30x | 2.90x | 3.30x | 3.67x | ||||||||

| NCF DSCR(5) | 2.07x | 2.30x | 2.90x | 3.30x | 3.64x | ||||||||

| NOI DY(5) | 6.0% | 6.7% | 8.4% | 9.6% | 10.6% | ||||||||

| NCF DY(5) | 6.0% | 6.7% | 8.4% | 9.6% | 10.6% |

| (1) | The increase in Net Operating Income from 2013 to 2014 is primarily due to an increase in occupancy from 50.9% to 63.5%. The increase in Net Operating Income from 2014 to 2015 is primarily due to an increase in occupancy from 63.5% to 67.3% and an increase in in-place weighted average base rent per square foot from approximately $97.86 to approximately $113.98 per square foot. The increase in Net Operating Income from 2015 to TTM 6/30/2016 is primarily due to an increase in in-place weighted average base rent from approximately $113.98 to approximately $127.16 per square foot. |

| (2) | The increase from TTM 6/30/2016 Net Operating Income to U/W Net Operating Income is primarily due to the inclusion of tenants who have signed leases, but have not begun paying rent, including Zimmer Partners LP (20,100 square feet) and Seven Bridges Advisors LLC (7,560 square feet). |

| (3) | Annual U/W Base Rent PSF and Annual U/W Base Rent include contractual rent steps through August 9, 2017, totaling $216,500. |

| (4) | The underwritten economic vacancy is 33.1%. The 9 West 57th Street Property was 63.5% leased as of June 1, 2016. |

| (5) | Debt service coverage ratios and debt yields are based on the 9 West 57th Street Senior Notes. |

Appraisal. As of the appraisal valuation date of July 28, 2016 the 9 West 57th Street Property had an “as-is” appraised value of $3,400,000,000. The appraiser of the 9 West 57th Street Property concluded an “as-stabilized” value of $3,750,000,000 as of February 1, 2020.

Environmental Matters. According to a Phase I environmental site assessment dated August 5, 2016 there was no evidence of any recognized environmental conditions at the 9 West 57th Street Property.

Market Overview and Competition.The 9 West 57th Street Property is located in the Plaza District in Midtown Manhattan and in close proximity to the Plaza Hotel, 5th Avenue, the Museum of Modern Art, Rockefeller Center, Carnegie Hall, Radio City Music Hall, Columbus Circle and Grand Central Terminal. Midtown Manhattan is home to numerous national and multinational corporations, such as The Blackstone Group, Bloomberg L.P., Estée Lauder, JPMorgan Chase and NBC. The surrounding area has a number of luxury hotels, including The Four Seasons, The Peninsula, The Plaza and The St. Regis. The property is located along “Billionaire’s Row” which includes several luxury supertall residential condominium developments such as One57, 432 Park, 220 Central Park South and 111 West 57th Street. Certain residential condominium units along “Billionaire’s Row” have sold for up to $9,000 per square foot.

As of the second quarter of 2016, the Plaza District office submarket reported an overall vacancy rate of 10.1% and overall average asking rents of $128.36 per square foot on a gross basis. The appraisal identified four comparable Class A trophy office buildings

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| 9 WEST 57TH STREET |

including the Seagram Building (375 Park Avenue), 667 Madison Avenue, the GM Building (767 5th Avenue) and Lever House (390 Park Avenue) with current asking rents ranging from $125 per square foot to $220 per square foot, on a gross basis, which is in-line with the 9 West 57th Street Property.

The following table presents certain information relating to comparable leases to the 9 West 57th Street Property:

Comparable Leases(1)

| Property Name/Location | Year Built/ Renovated | Stories | Total GLA (SF) | Total Occupancy | Distance from Subject | Tenant Name | Lease Date/Term | Lease Area (SF) | Annual Base Rent PSF | Lease Type | ||||||||||

767 Fifth Avenue New York, NY

| 1968/NAV | 50 | 1,925,000 | 95.6% | 0.2 miles | Seven Valley LLC | June 2016 / 15 Yrs | 2,933 | $220.00 | Gross | ||||||||||

650 Madison Avenue New York, NY

| 1956/1987 | 27 | 603,666 | 85.9% | 0.3 miles | Ocean Road Advisors | April 2016 / 10 Yrs | 6,647 | $160.00 | Gross | ||||||||||

375 Park Avenue New York, NY

| 1958/NAP | 38 | 830,928 | 98.3% | 0.5 miles | Strategic Asset Services LLC | June 2016 / 10 Yrs | 17,519 | $165.00 | Gross | ||||||||||

350 Park Avenue New York, NY

| 1960/2002 | 30 | 567,000 | 100.0% | 0.5 miles | Citco Corporate Services | May 2016 / 10.7 Yrs | 8,092 | $160.00 | Gross | ||||||||||

1095 Avenue of the Americas New York, NY

| 1972/2008 | 41 | 1,484,325 | 97.3% | 1.0 miles | U.S. Bank | June 2016 / 12 Yrs | 68,636 | $95.00 | Gross |

| (1) | Information obtained from the appraisal and a third party market research report. |

The Borrower.The borrowing entities for the 9 West 57th Street Whole Loan are Solow Building Company II, L.L.C. and Solovieff Realty Co. II, L.L.C and each is a Delaware limited liability company and special purpose entity. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the 9 West 57th Street Whole Loan.

The Sponsor.The loan sponsor is Sheldon H. Solow who has been an owner and developer of commercial and residential properties in New York since 1950 and has owned the 9 West 57th Street Property since developing it in 1972. Sheldon H. Solow has a real estate portfolio consisting of approximately 18 commercial and residential properties in New York City, including 265 East 66th Street, One East River Place and 419 East 60th Street.

Escrows.The loan documents provide for upfront reserves in the amount of $9,417,640 for real estate taxes, $264,333 for insurance premiums, $25,000,000 for ongoing tenant improvements and leasing commissions, $16,462,228 for outstanding free rent, $13,061,790 for outstanding tenant improvements and leasing commissions and $287,500 for deferred maintenance. The loan documents require monthly reserve deposits of one-twelfth of the estimated annual real estate taxes (currently equates to $3,139,213 per month), one-twelfth of the estimated annual insurance premiums (currently equates to $88,111 per month), $61,615 for replacement reserves. The loan documents do not require monthly escrows for replacement reserves as long as the balance of the escrow account equals $2,500,000 (“Replacement Reserve Cap”).

The loan documents do not require monthly escrows for tenant improvements and leasing commission reserves as long as the balance of the escrow account remains $25,000,000 (“TI/LC Reserve Cap”). If the balance of the tenant improvement and leasing commissions reserve account is less than the TI/LC Reserve Cap, the borrowers are required to deposit into the reserve $420,055 per month unless (i) the debt service coverage ratio is equal to or greater than 2.50x, (ii) the balance of the reserve account is equal to or greater than $15,000,000 and (iii) the 9 West 57th Street Property is occupied by tenants under leases demising no less than 65.0% of the rentable square footage.

Lockbox and Cash Management.The 9 West 57th Street Whole Loan documents require a lender-controlled lockbox account, which is already in place, and that the borrowers direct tenants to pay their rents directly into such lockbox account. All funds in the lockbox account will be swept daily into the borrowers’ operating account at the clearing bank, unless a Trigger Period (as defined below) has occurred and is continuing, in which event such funds will be swept on a daily basis into the a cash management account controlled by the lender and disbursed on each payment date in accordance with the loan documents.

A “Trigger Period” commences upon the occurrence of (i) an event of default, (ii) the bankruptcy or insolvency of the borrowers, (iii) the bankruptcy or insolvency of the property manager or (iv) the debt service coverage ratio (as calculated in the loan documents) falling below 2.50x based on a trailing three-month basis.

The borrowers will have the right two times in the aggregate in any 12-month period to cure a Trigger Period as follows: (i) if a Trigger Period exists solely by reason of an event of default, the curing and acceptance of such cure by the lender of the applicable event of default (in its sole and absolute discretion), (ii) if a Trigger Period exists solely by reason of a bankruptcy or insolvency of a property manager, the replacement of such manager with a qualified manager pursuant to a management agreement acceptable to the lender within 60 days, (iii) if a Trigger Period exists solely by reason of a the debt service coverage ratio falling below 2.50x for a trailing three-month period, the achievement of the debt service coverage ratio for two consecutive quarters of at least 2.50x on a

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| 9 WEST 57TH STREET |

trailing three-month basis as determined by the lender. In no event will the borrowers have the right to cure a Trigger Period occurring by reason of a borrower bankruptcy.

Property Management. The 9 West 57th Street Property is managed by an affiliate of the borrower.

Assumption. The borrower has the one-time right to transfer the 9 West 57th Street Property provided that certain conditions are satisfied, including: (i) no event of default has occurred and is continuing; (ii) the proposed transferee will be controlled by a person who (a) has demonstrated expertise in owning or operating at least three similar Class A office properties in Manhattan consisting of at least 4,500,000 rentable square feet (exclusive of the 9 West 57thStreet Property), (b) as of a date no more than six months prior to the date of such transfer and assumption, and at all times while the guaranty of recourse obligations and/or environmental indemnity, as each are referred to in clause (iii) below, is outstanding, has (x) total assets of at least $2.0 billion (exclusive of the 9 West 57th Property) in the aggregate, (y) has shareholder/partner equity of at least $1.3 billion (exclusive of the 9 West 57th Street Property) in the aggregate and (z) liquidity in excess of $25.0 million in the aggregate, and (c) whose identity, experience, financial condition and creditworthiness is otherwise acceptable to Lender in all respect; (iv) execution of a recourse guaranty and an environmental indemnity by an affiliate of the transferee; and (v) the lender has received confirmation from DBRS, Fitch, Moody’s and Morningstar that such assumption will not result in a downgrade of the respective ratings assigned to the Series 2016-LC25 certificates and similar confirmations from each rating agency rating any securities backed by any of the 9 West 57th Street Companion Loans.

Partial Release. Not permitted.

Real Estate Substitution.Not permitted.

Subordinate and Mezzanine Indebtedness.The 9 West 57th Street Subordinate Companion Note had an original balance of $186,276,000, has a cut-off date balance of $186,276,000 and is coterminous with the 9 West 57th Street Senior Notes. The 9 West 57th Street subordinate companion loan requires interest-only payments through maturity. The controlling Note A-1 and the 9 West 57th Street Subordinate Companion Note were contributed to the JPMCC 2016-NINE securitization trust, pursuant to which the 9 West 57th Street Whole Loan is serviced and administered.

The sole members of the borrowers are permitted to obtain a mezzanine loan secured by the ownership interests in the related borrower upon satisfaction of certain terms and conditions which include, without limitation, (i) the mezzanine lender meets a qualified lender provision in the loan documents, (ii) the combined loan-to-value ratio on the origination date of the mezzanine loan does not exceed 35.3%, (iii) the combined debt service coverage ratio (as calculated in the loan documents and based on the 12 months immediately preceding the origination date of the mezzanine loan) is not less than 3.08x, and (iv) the mezzanine lender enters into an intercreditor agreement in form and substance reasonably satisfactory to the mortgage lender and the rating agencies.

Ground Lease.The borrowers have pledged both the fee interest in the 9 West 57th Street Property and the leasehold estate. The borrowers are permitted to terminate the ground lease upon certain terms and conditions in the loan documents which include, without limitation, delivery of a new title policy or an endorsement to the existing title policy, confirmation that all space leases will remain in full force and effect and satisfaction of any REMIC requirements.

Terrorism Insurance. The loan documents require that the “all risk” insurance policy required to be maintained by the borrowers provides coverage for terrorism in an amount equal to the full replacement cost of the 9 West 57th Street Property (provided that the borrowers are not required to pay terrorism insurance premiums in excess of two times the premiums for all risk and business interruption coverage (exclusive of terrorism coverage) if the Terrorism Risk Insurance Program Reauthorization Act is no longer in effect). The loan documents also require business interruption insurance covering no less than the 24-month period following the occurrence of a casualty event, together with a 12-month extended period of indemnity.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

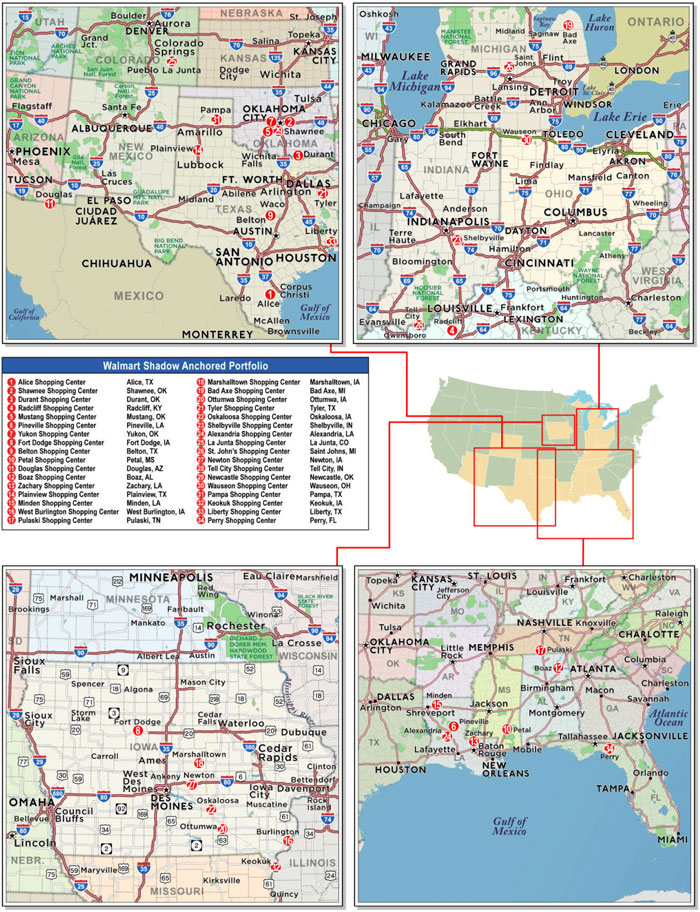

| WALMART SHADOW ANCHORED PORTFOLIO |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| WALMART SHADOW ANCHORED PORTFOLIO |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| No. 2 – Walmart Shadow Anchored Portfolio | ||||||

| Loan Information | Property Information | |||||

| Mortgage Loan Seller: | Ladder Capital Finance | Single Asset/Portfolio: | Portfolio | |||

| Credit Assessment (DBRS/Fitch/Moody’s/Morningstar): | NR/NR/NR/NR | Property Type: | Retail | |||

| Original Principal Balance(1): | $49,500,000 | Specific Property Type: | Shadow Anchored | |||

| Cut-off Date Principal Balance(1): | $49,500,000 | Location: | Various – See Table | |||

| % of Initial Pool Balance: | 5.2% | Size: | 881,524 SF | |||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF(1): | $101.00 | |||

| Borrowers(2): | Various | Year Built/Renovated: | Various – See Table | |||

| Sponsor: | David W. Schostak | Title Vesting(5): | Various | |||

| Mortgage Rate: | 5.5898% | Property Manager: | Self-managed | |||

| Note Date: | September 1, 2016 | 4th Most Recent Occupancy (As of): | 93.9% (12/31/2012) | |||

| Anticipated Repayment Date: | NAP | 3rd Most Recent Occupancy (As of): | 92.1% (12/31/2013) | |||

| Maturity Date: | September 6, 2021 | 2nd Most Recent Occupancy(As of): | 92.2% (12/31/2014) | |||

| IO Period: | 24 months | Most Recent Occupancy (As of): | 93.4% (12/31/2015) | |||

| Loan Term (Original): | 60 months | Current Occupancy (As of): | 93.1% (10/31/2016) | |||

| Seasoning: | 3 months | |||||

| Amortization Term (Original): | 360 months | Underwriting and Financial Information: | ||||

| Loan Amortization Type: | Interest-only, Amortizing Balloon | |||||

| Interest Accrual Method: | Actual/360 | 4th Most Recent NOI (As of): | $8,667,457 (12/31/2013) | |||

| Call Protection: | L(27),D(28),O(5) | 3rd Most Recent NOI (As of): | $9,035,547 (12/31/2014) | |||

| Lockbox Type: | Hard/Upfront Cash Management | 2nd Most Recent NOI (As of): | $9,045,481 (12/31/2015) | |||

| Additional Debt(1)(3): | Yes | Most Recent NOI (As of): | $9,050,388 (TTM 6/30/2016) | |||

| Additional Debt Type(1)(3): | Pari Passu; Mezzanine | |||||

| U/W Revenues: | $12,603,392 | |||||

| U/W Expenses: | $3,145,985 | |||||

| Escrows and Reserves(4): | U/W NOI: | $9,457,407 | ||||

| U/W NCF: | $8,311,424 | |||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NOI DSCR(1): | 1.54x | |

| Taxes | $682,795 | $136,559 | NAP | U/W NCF DSCR(1): | 1.36x | |

| Insurance | $150,051 | $12,504 | NAP | U/W NOI Debt Yield(1): | 10.6% | |

| Replacement Reserves | $0 | $14,692 | $528,915(4) | U/W NCF Debt Yield(1): | 9.3% | |

| TI/LC Reserve | $850,000 | $80,806 | $2,909,034(4) | As-Is Appraised Value: | $118,715,000 | |

| Deferred Maintenance | $218,304 | $0 | NAP | As-Is Appraisal Valuation Date(7): | Various | |

| Tell City Engineering Reserve | $129,000 | $0 | NAP | Cut-off Date LTV Ratio(1): | 75.0% | |

| Ground Rent Reserve | $8,216 | Springing | $8,216 | LTV Ratio at Maturity or ARD(1): | 72.0% | |

(1) | See “The Mortgage Loan” section. All statistical information related to balances per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based on the Walmart Shadow Anchored Portfolio Whole Loan (as defined below). |

| (2) | See “Borrowers” section. |

| (3) | See “Subordinate and Mezzanine Indebtedness” section. The equity interest in the borrower has been pledged to secure mezzanine indebtedness with an original principal balance of $8,613,750. All statistical information related to the balances per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based solely on the Walmart Shadow Anchored Portfolio Whole Loan. As of the Cut-off Date, the Cut-off Date Balance per SF, U/W NCF DSCR, U/W NCF Debt Yield, Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD based on the Walmart Shadow Anchored Portfolio Whole Loan and the Walmart Shadow Anchored Portfolio Mezzanine Loan (as defined below) in the aggregate were $110.77, 1.17x, 8.5%, 82.3% and 79.2%, respectively. |

| (4) | See “Escrows” section. |

| (5) | The Walmart Shadow Anchored Portfolio Whole Loan is secured by the leasehold interests in two of the Walmart Shadow Anchored Portfolio Properties (as defined below) and by the fee interests in the remaining 32 Walmart Shadow Anchored Portfolio Properties. See “Ground Lease” section. |

| (6) | See “Appraisals” section. |

The Mortgage Loan.The mortgage loan (the “Walmart Shadow Anchored Portfolio Mortgage Loan”) is part of a whole loan (the “Walmart Shadow Anchored Portfolio Whole Loan”) that is evidenced by twopari passu promissory notes (Notes A-1 and A-2) and secured by a first mortgage encumbering the fee (or, in 2 cases, the leasehold) interests in 34 retail properties, each shadow anchored by Walmart, across 14 states (the “Walmart Shadow Anchored Portfolio Properties”). The Walmart Shadow Anchored Portfolio Whole Loan was originated on September 1, 2016 by Ladder Capital Finance LLC. The Walmart Shadow Anchored Portfolio Whole Loan had an original principal balance of $89,036,250, has an outstanding principal balance as of the Cut-off Date of $89,036,250 and accrues interest at an interest rate of 5.5898%per annum. The Walmart Shadow Anchored Portfolio Whole Loan had an initial term of 60 months, has a remaining term of 57 months as of the Cut-off Date and requires interest-only payments for the first 24 payments following origination and, thereafter, requires payments of principal and interest based on a 30-year amortization schedule. The Walmart Shadow Anchored Portfolio Whole Loan matures on September 6, 2021.

Note A-1, which will be contributed to the WFCM 2016-LC25 Trust, had an original principal balance of $49,500,000, has an outstanding principal balance as of the Cut-off Date of $49,500,000 and represents the controlling interest in the Walmart Shadow Anchored Portfolio Whole Loan. The non-controlling Note A-2, with an original principal balance of $39,536,250, is expected to be

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| WALMART SHADOW ANCHORED PORTFOLIO |

contributed to one or more future trusts. The mortgage loan evidenced by Note A-2 is referred to herein as the “Walmart Shadow Anchored Companion Loan”. The lender provides no assurances that Note A-2 will not be split further. See“Description of the Mortgage Pool—The Whole Loans—The Serviced Whole Loans” in the Preliminary Prospectus.

Pari Passu Note Summary

| Original Balance | Note Holder | Controlling Piece | ||

| Note A-1 | $49,500,000 | WFCM 2016-LC25 | Yes | |

| Note A-2 | $39,536,250 | Ladder Capital Finance | No | |

| Total | $89,036,250 |

Following the lockout period, the borrower has the right to defease the Walmart Shadow Anchored Portfolio Whole Loan in whole but not in part, on any due date before May 6, 2021. In addition, the Walmart Shadow Anchored Portfolio Whole Loan is prepayable without penalty commencing on May 6, 2021.

Sources and Uses

| Sources | Uses | |||||||||

| Original Whole Loan amount | $89,036,250 | 91.2 | % | Loan payoff(1) | $89,698,349 | 91.9 | % | |||

| Mezzanine Loan | 8,613,750 | 8.8 | Reserves | 2,038,365 | 2.1 | |||||

| Closing costs | 1,464,686 | 1.5 | ||||||||

| Return of equity | 4,448,600 | 4.6 | ||||||||

| Total Sources | $97,650,000 | 100.0 | % | Total Uses | $97,650,000 | 100.0 | % |

| (1) | Seven of the Walmart Shadow Anchored Portfolio Properties were previously securitized in the CSMS 2007-C1 transaction. The remainder of the properties were securitized in the CSMC 2006-C3 and CSMC 2006-C4 transactions but were not directly paid off by the Walmart Shadow Anchored Portfolio Whole loan. |

The Properties.The Walmart Shadow Anchored Portfolio Properties consist of 34 retail properties, each shadow anchored by Walmart, comprised of approximately 881,524 rentable square feet that were built between 2002 and 2006 and are located in 14 states. The related borrowers hold leasehold interests in two of the Walmart Shadow Anchored Portfolio Properties (see “Ground Lease” section) and fee interests in the remaining 32 Walmart Shadow Anchored Portfolio Properties. No property accounts for more than 5.3% of allocated Cut-off Date Principal Balance. Since 2006, the Walmart Shadow Anchored Portfolio Properties have never been below 91.0% occupied. The Walmart Shadow Anchored Portfolio Properties range in size from 10,060 square feet to 39,100 square feet and were 93.1% occupied as of October 31, 2016.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| WALMART SHADOW ANCHORED PORTFOLIO |

The following table presents certain information relating to the Walmart Shadow Anchored Portfolio Properties:

| Property Name | City, State | Allocated Cut-off Date Principal Balance | % of Portfolio Cut-off Date Principal Balance | Occupancy | Year Built/ Renovated | Net Rentable Area (SF) | Appraised Value | Allocated LTV |

| Alice Shopping Center | Alice, TX | $4,763,000 | 5.3% | 91.8% | 2005/NAP | 39,100 | $6,100,000 | 78.1% |

| Shawnee Shopping Center | Shawnee, OK | $4,186,000 | 4.7% | 100.0% | 2004/NAP | 35,640 | $5,360,000 | 78.1% |

| Durant Shopping Center | Durant, OK | $3,834,000 | 4.3% | 100.0% | 2003/2012 | 32,200 | $4,910,000 | 78.1% |

| Radcliff Shopping Center | Radcliff, KY | $3,819,000 | 4.3% | 84.8% | 2005/NAP | 36,900 | $4,890,000 | 78.1% |

| Mustang Shopping Center | Mustang, OK | $3,647,000 | 4.1% | 100.0% | 2004/NAP | 35,849 | $4,670,000 | 78.1% |

| Pineville Shopping Center | Pineville, LA | $3,639,000 | 4.1% | 100.0% | 2002/NAP | 32,300 | $4,660,000 | 78.1% |

| Yukon Shopping Center | Yukon, OK | $3,621,000 | 4.1% | 100.0% | 2004/NAP | 31,500 | $4,560,000 | 79.4% |

| Fort Dodge Shopping Center | Fort Dodge, IA | $3,491,000 | 3.9% | 95.3% | 2004/NAP | 33,700 | $4,470,000 | 78.1% |

| Belton Shopping Center | Belton, TX | $3,389,000 | 3.8% | 100.0% | 2005/NAP | 28,052 | $4,340,000 | 78.1% |

| Petal Shopping Center | Petal, MS | $3,183,000 | 3.6% | 84.8% | 2003/NAP | 30,180 | $4,100,000 | 77.6% |

| Douglas Shopping Center | Douglas, AZ | $3,183,000 | 3.6% | 93.8% | 2004/NAP | 32,140 | $4,100,000 | 77.6% |

| Boaz Shopping Center | Boaz, AL | $3,077,000 | 3.5% | 88.5% | 2004/NAP | 27,900 | $3,940,000 | 78.1% |

| Zachary Shopping Center | Zachary, LA | $3,065,000 | 3.4% | 100.0% | 2002/NAP | 29,600 | $3,925,000 | 78.1% |

| Plainview Shopping Center | Plainview, TX | $2,875,000 | 3.2% | 72.3% | 2005/NAP | 31,720 | $4,510,000 | 63.7% |

| Minden Shopping Center | Minden, LA | $2,796,000 | 3.1% | 95.6% | 2003/NAP | 27,300 | $3,580,000 | 78.1% |

| West Burlington Shopping Center | West Burlington, IA | $2,522,000 | 2.8% | 100.0% | 2004/NAP | 26,100 | $3,230,000 | 78.1% |

| Pulaski Shopping Center | Pulaski, TN | $2,430,000 | 2.7% | 100.0% | 2004/NAP | 28,100 | $3,600,000 | 67.5% |

| Marshalltown Shopping Center | Marshalltown, IA | $2,422,000 | 2.7% | 87.8% | 2004/NAP | 22,900 | $3,140,000 | 77.1% |

| Bad Axe Shopping Center | Bad Axe, MI | $2,382,000 | 2.7% | 100.0% | 2005/NAP | 28,353 | $3,050,000 | 78.1% |

| Ottumwa Shopping Center | Ottumwa, IA | $2,307,000 | 2.6% | 91.9% | 2004/NAP | 22,190 | $3,380,000 | 68.3% |

| Tyler Shopping Center | Tyler, TX | $2,286,250 | 2.6% | 85.9% | 2004/NAP | 35,840 | $3,580,000 | 63.9% |

| Oskaloosa Shopping Center | Oskaloosa, IA | $2,249,000 | 2.5% | 100.0% | 2004/NAP | 20,700 | $2,880,000 | 78.1% |

| Shelbyville Shopping Center | Shelbyville, IN | $2,187,000 | 2.5% | 100.0% | 2005/NAP | 14,150 | $2,800,000 | 78.1% |

| Alexandria Shopping Center | Alexandria, LA | $2,090,000 | 2.3% | 92.2% | 2003/NAP | 20,400 | $2,690,000 | 77.7% |

| La Junta Shopping Center | La Junta, CO | $2,085,000 | 2.3% | 100.0% | 2004/NAP | 20,500 | $2,670,000 | 78.1% |

| St. John’s Shopping Center | Saint Johns, MI | $2,040,000 | 2.3% | 74.0% | 2006/NAP | 29,930 | $3,400,000 | 60.0% |

| Newton Shopping Center | Newton, IA | $2,008,000 | 2.3% | 88.2% | 2004/NAP | 20,300 | $2,610,000 | 76.9% |

| Tell City Shopping Center | Tell City, IN | $1,952,000 | 2.2% | 82.2% | 2005/NAP | 27,000 | $2,740,000 | 71.2% |

| Newcastle Shopping Center | Newcastle, OK | $1,577,000 | 1.8% | 100.0% | 2004/NAP | 11,600 | $2,020,000 | 78.1% |

| Wauseon Shopping Center | Wauseon, OH | $1,406,000 | 1.6% | 100.0% | 2005/NAP | 13,100 | $1,800,000 | 78.1% |

| Pampa Shopping Center | Pampa, TX | $1,374,000 | 1.5% | 100.0% | 2005/NAP | 16,160 | $1,760,000 | 78.1% |

| Keokuk Shopping Center | Keokuk, IA | $1,203,000 | 1.4% | 100.0% | 2004/NAP | 10,160 | $1,540,000 | 78.1% |

| Liberty Shopping Center | Liberty, TX | $1,029,000 | 1.2% | 67.9% | 2006/NAP | 14,960 | $1,960,000 | 52.5% |

| Perry Shopping Center | Perry, FL | $919,000 | 1.0% | 100.0% | 2004/NAP | 15,000 | $1,750,000 | 52.5% |

| Total/Weighted Average | $89,036,250 | 100.0% | 93.1% | 881,524 | $118,715,000 | 75.0% |

The following table presents certain information relating to the tenancies at the Walmart Shadow Anchored Portfolio Properties (based on the portfolio in its entirety):

Major Tenants

| Tenant Name | Credit Rating /S&P)(1) | Tenant NRSF | % of NRSF | Annual U/W Base Rent PSF | Annual U/W Base Rent | % of Total Annual U/W Base Rent | Lease Expiration Date | |

| Major Tenants | ||||||||

| Dollar Tree | NR/Ba2/BB+ | 245,426 | 27.8% | $8.22 | $2,017,160 | 20.8% | Various(2) | |

| Cato’s | NR/NR/NR | 79,910 | 9.1% | $11.34 | $906,555 | 9.3% | Various(2) | |

| Gamestop | NR/Ba1/BB+ | 45,503 | 5.2% | $16.90 | $769,216 | 7.9% | Various(2) | |

| Shoe Show | NR/NR/NR | 41,500 | 4.7% | $10.48 | $434,775 | 4.5% | Various(2) | |

| Sally Beauty | NR/NR/NR | 26,950 | 3.1% | $13.99 | $377,128 | 3.9% | Various(2) | |

| Total Major Tenants | 439,289 | 49.8% | $10.25 | $4,504,834 | 46.4% | |||

| Non-Major Tenants | 380,990 | 43.2% | $13.66 | $5,203,573 | 53.6% | |||

| Occupied Collateral Total | 820,279 | 93.1% | $11.84 | $9,708,407 | 100.0% | |||

| Vacant Space | 61,245 | 6.9% | ||||||

| Collateral Total | 881,524 | 100.0% | ||||||

| (1) | Certain ratings are those of the parent company whether or not the parent guarantees the lease. |

| (2) | See Annex A-1 to the Preliminary Prospectus for detailed information on lease expiration of individual properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| WALMART SHADOW ANCHORED PORTFOLIO |

Historical Sales (PSF) and Occupancy Costs(1)

| Tenant Name | 2013 | 2014 | 2015 | Current Occupancy Cost(2) |

| Dollar Tree | $102 | $105 | $109 | 7.5% |

| Cato’s | $163 | $167 | $166 | 6.8% |

| Shoe Show | $115 | $118 | $97 | 10.1% |

| Sally Beauty | $228 | $236 | $245 | 3.9% |

| (1) | Historical Sales (PSF) and Occupancy Costs were provided by the borrower. Chart includes only tenants who have reported full sales for each respective year. |

| (2) | Current Occupancy Costs are based on the Annual U/W Base Rent and reimbursements and the most recent available historical sales. |

The following table presents certain information relating to the lease rollover schedule at the Walmart Shadow Anchored Portfolio Properties:

Lease Expiration Schedule(1)(2)

Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent | % of Total Annual U/W Base Rent | Annual U/W Base Rent PSF(3) |

| MTM | 7 | 12,500 | 1.4% | 12,500 | 1.4% | $155,500 | 1.6% | $12.44 |

| 2016 | 3 | 7,600 | 0.9% | 20,100 | 2.3% | $85,600 | 0.9% | $11.26 |

| 2017 | 52 | 119,310 | 13.5% | 139,410 | 15.8% | $1,602,251 | 16.5% | $13.43 |

| 2018 | 60 | 171,759 | 19.5% | 311,169 | 35.3% | $2,106,097 | 21.7% | $12.26 |

| 2019 | 55 | 188,860 | 21.4% | 500,029 | 56.7% | $2,093,540 | 21.6% | $11.09 |

| 2020 | 45 | 142,392 | 16.2% | 642,421 | 72.9% | $1,727,315 | 17.8% | $12.13 |

| 2021 | 33 | 111,170 | 12.6% | 753,591 | 85.5% | $1,254,114 | 12.9% | $11.28 |

| 2022 | 2 | 3,200 | 0.4% | 756,791 | 85.9% | $38,400 | 0.4% | $12.00 |

| 2023 | 6 | 26,888 | 3.1% | 783,679 | 88.9% | $314,380 | 3.2% | $11.69 |

| 2024 | 3 | 24,200 | 2.7% | 807,879 | 91.6% | $214,950 | 2.2% | $8.88 |

| 2025 | 0 | 0 | 0.0% | 807,879 | 91.6% | $0 | 0.0% | $0.00 |

| 2026 | 3 | 11,200 | 1.3% | 819,079 | 92.9% | $105,196 | 1.1% | $9.39 |

| Thereafter | 1 | 1,200 | 0.1% | 820,279 | 93.1% | $11,064 | 0.1% | $9.22 |

| Vacant | 0 | 61,245 | 6.9% | 881,524 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 270 | 881,524 | 100.0% | $9,708,407 | 100.0% | $11.84 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the Lease Expiration Schedule. |

| (3) | Weighted Average Annual U/W Base Rent PSF excludes vacant space. |

The following table presents historical occupancy percentages at the Walmart Shadow Anchored Portfolio Properties:

Historical Occupancy

12/31/2012(1) | 12/31/2013(2) | 12/31/2014(2) | 12/31/2015(2) | 10/31/2016(3) | ||||

| 93.9% | 92.1% | 92.2% | 93.4% | 93.1% |

| (1) | Information obtained from a third party source. |

| (2) | Information obtained from the borrower. |

| (3) | Information obtained from the underwritten rent roll. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| WALMART SHADOW ANCHORED PORTFOLIO |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and underwritten net cash flow at the Walmart Shadow Anchored Portfolio Properties:

Cash Flow Analysis

| 2013 | 2014 | 2015 | TTM 6/30/2016 | U/W | % of U/W Effective Gross Income | U/W $ per SF | |||||||

| Base Rent | $8,657,624 | $9,058,380 | $9,288,461 | $9,423,033 | $9,708,407 | 77.0% | $11.01 | ||||||

| Grossed Up Vacant Space | 0 | 0 | 0 | 0 | $903,439 | 7.2 | 1.02 | ||||||

| Total Reimbursables | 2,539,364 | 2,655,932 | 2,787,371 | 2,842,337 | 2,842,337 | 22.6 | 3.22 | ||||||

| Other Income | 691,995 | 504,250 | 199,885 | 52,648 | 52,648 | 0.4 | 0.06 | ||||||

| Less Vacancy & Credit Loss | 0 | 0 | 0 | 0 | (903,439)(1) | (7.2) | (1.02) | ||||||

| Effective Gross Income | $11,888,983 | $12,218,562 | $12,275,717 | $12,318,018 | $12,603,392 | 100.0% | $14.30 | ||||||

| Total Operating Expenses | $3,221,526 | $3,183,015 | $3,230,236 | $3,267,630 | $3,145,985 | 25.0% | $3.57 | ||||||

| Net Operating Income | $8,667,457 | $9,035,547 | $9,045,481 | $9,050,388 | $9,457,407 | 75.0% | $10.73 | ||||||

| TI/LC | 0 | 0 | 0 | 0 | 969,678 | 7.7 | 1.10 | ||||||

| Capital Expenditures | 0 | 0 | 0 | 0 | 176,305 | 1.4 | 0.20 | ||||||

| Net Cash Flow | $8,667,457 | $9,035,547 | $9,045,481 | $9,050,388 | $8,311,424 | 65.9% | $9.43 | ||||||

| NOI DSCR(2) | 1.41x | 1.47x | 1.48x | 1.48x | 1.54x | ||||||||

| NCF DSCR(2) | 1.41x | 1.47x | 1.48x | 1.48x | 1.36x | ||||||||

| NOI DY(2) | 9.7% | 10.1% | 10.2% | 10.2% | 10.6% | ||||||||

| NCF DY(2) | 9.7% | 10.1% | 10.2% | 10.2% | 9.3% |

| (1) | Underwritten economic vacancy is 6.9%. The Walmart Shadow Anchored Properties were 93.1% physically occupied as of October 31, 2016. |

| (2) | The debt service coverage ratios and debt yields are based on the Walmart Shadow Anchored Portfolio Whole Loan. |

Appraisals.As of the appraisal valuation dates ranging from July 12, 2016 to July 30, 2016, the Walmart Shadow Anchored Portfolio Properties had an aggregate “as-is” appraised value of $118,715,000.

The Borrowers. The borrowers are: SFP Pool One Shopping Centers L.P.; SFP Pool Two Shopping Centers L.P.; SFP Pool Three Shopping Centers L.P.; SFP Pool Four Shopping Centers L.P.; and SFP Pool Five Shopping Centers L.P. Each of the borrowers is a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the borrowers delivered a non-consolidation opinion in connection with the origination of the Walmart Shadow Anchored Portfolio Whole Loan. David W. Schostak is the guarantor of certain nonrecourse carveouts under the Walmart Shadow Anchored Portfolio Whole Loan.

The Sponsor. The sponsor is David W. Schostak, who is the co-CEO of Schostak Brothers & Company with his brother Robert Schostak. The Schostaks are a fourth generation real estate family that has been involved in Michigan development, acquisitions, and leasing of retail, office, industrial, residential, and mixed use projects for over 100 years. Mr. Schostak’s current activities include joint ventures, build-to-suit projects, mixed-use developments and a variety of necessity-based retail and open air centers in 24 states. The Schostak family’s portfolio now includes over 100 restaurants including Applebee’s, Del Tacos, MOD Pizzas and Olga’s Kitchens.

The sponsor was involved in three defaults, one loan modification and one discounted payoff for loans he was a sponsor. See “Description of the Mortgage Pool—Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings” in the Preliminary Prospectus.

Escrows.The loan documents provide for upfront reserves in the amount of $682,795 for real estate taxes, $150,051 for insurance, $850,000 for upfront tenant improvements and leasing commissions, $218,304 for deferred maintenance, $129,000 for an engineering reserve, and $8,216 for future ground rent payments. The loan documents also require monthly deposits in an amount equal to one-twelfth of the estimated annual real estate taxes and insurance premiums, which currently equate to $136,559 and $12,504, respectively, $14,692 for replacement reserves (capped at $528,915), and $80,806 for tenant improvements and leasing commissions (capped at $2,909,034).

Lockbox and Cash Management.The Walmart Shadow Anchored Portfolio Whole Loan documents require a lender-controlled lockbox account, which is already in place, and that the borrowers direct tenants to pay their rents directly into such lockbox account. The loan documents also require that all rents received by the borrowers or the property manager will be deposited into the lockbox account within two business days of receipt. Prior to a Sweep Event Period (as defined below), all excess cash flow will be disbursed to the related borrower. Upon a Sweep Event Period, excess cash flow will be held by the lender.

A “Sweep Event Period” will commence upon the earlier of (i) an event of default occurs under the loan documents or the property management agreement, (ii) the aggregate amortizing debt service coverage ratio for the Walmart Shadow Anchored Portfolio

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| WALMART SHADOW ANCHORED PORTFOLIO |

Properties falls below 1.05x at any time and/or (iii) any tenant occupying (physical or economic) more than 10.0% of the entire Walmart Shadow Anchored Portfolio Properties files or bankruptcy, becomes insolvent, or goes dark in the majority of its locations.

Property Management.The Walmart Shadow Anchored Portfolio Properties are managed by an affiliate of the sponsor.

Assumption.The borrower has the right to transfer the Walmart Shadow Anchored Portfolio Properties, provided that no event of default has occurred and is continuing and certain other conditions are satisfied, including (i) the lender’s reasonable determination that the proposed transferee and guarantor satisfy the lender’s credit review and underwriting standards, taking into consideration transferee experience, financial strength and general business standing; (ii) execution of a recourse guaranty and an environmental indemnity by an affiliate of the transferee; and (iii) if requested by the lender, rating agency confirmation from DBRS, Fitch, Moody’s, and Morningstar that the transfer will not result in a downgrade, withdrawal or qualification of the respective ratings assigned to the Series 2016-LC25 certificates and similar confirmations from each rating agency rating any securities backed by the Walmart Shadow Anchored Portfolio Companion Loan with respect to the ratings of such securities.

Partial Release.Not permitted.

Real Estate Substitution.Not permitted.

Subordinate and Mezzanine Indebtedness.Ladder Capital Finance LLC (the “Walmart Shadow Anchored Portfolio Mezzanine Lender”) funded an $8,613,750 mezzanine loan (the “Walmart Shadow Anchored Portfolio Mezzanine Loan”) to SFP LP Holdco L.P. and SFP GP Holdco LLC, each a Delaware limited liability company and the sole member of each borrower under the Walmart Shadow Anchored Portfolio Whole Loan (the “Walmart Shadow Anchored Portfolio Mezzanine Borrower”). The Walmart Shadow Anchored Portfolio Mezzanine Loan is secured by a pledge of the Walmart Shadow Anchored Portfolio Mezzanine Loan Borrowers’ interest in the borrowers under the Walmart Shadow Anchored Portfolio Whole Loan. The Walmart Shadow Anchored Portfolio Mezzanine Loan accrues interest at an interest rate of 11.000%per annum and requires payments of principal and interest based on a 30-year amortization schedule. The Walmart Shadow Anchored Mezzanine Loan matures on September 6, 2021. The rights of The Walmart Shadow Anchored Mezzanine Lender are further described under“Description of the Mortgage Pool–Additional Indebtedness—Mezzanine Indebtedness”in the Preliminary Prospectus.

Ground Lease. Two of the Walmart Shadow Anchored Portfolio Properties are subject to ground leases: (i) the Tyler Shopping Center property is subject to a ground lease with Jack and Peggy Waldie as ground lessor that expires on April 26, 2024 with 15 five-year ground lease extension options, each with $5,000 rent increases; and (ii) the Pulaski Shopping Center property is subject to a ground lease with Wakefield Realty, LLC as ground lessor that expires on October 31, 2023 with 15 five-year ground lease extension options, each with 5% rent increases. See “Description of the Mortgage Pool—Mortgage Pool Characteristics—Fee & Leasehold Estates; Ground Leases” in the Preliminary Prospectus.

I. Terrorism Insurance.The loan documents require that the “all risk” insurance policy required to be maintained by the borrower provide coverage for terrorism in an amount equal to the full replacement cost of the Walmart Shadow Anchored Portfolio Properties. The loan documents also require business interruption insurance provide coverage for no less than the 24-month period following the occurrence of a casualty event, together with a six-month extended period of indemnity.

II.

Windstorm Insurance.The loan documents require windstorm insurance covering the full replacement cost of the Walmart Shadow Anchored Portfolio Properties during the loan term. At the time of closing, the Walmart Shadow Anchored Portfolio Properties had windstorm insurance coverage.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

19

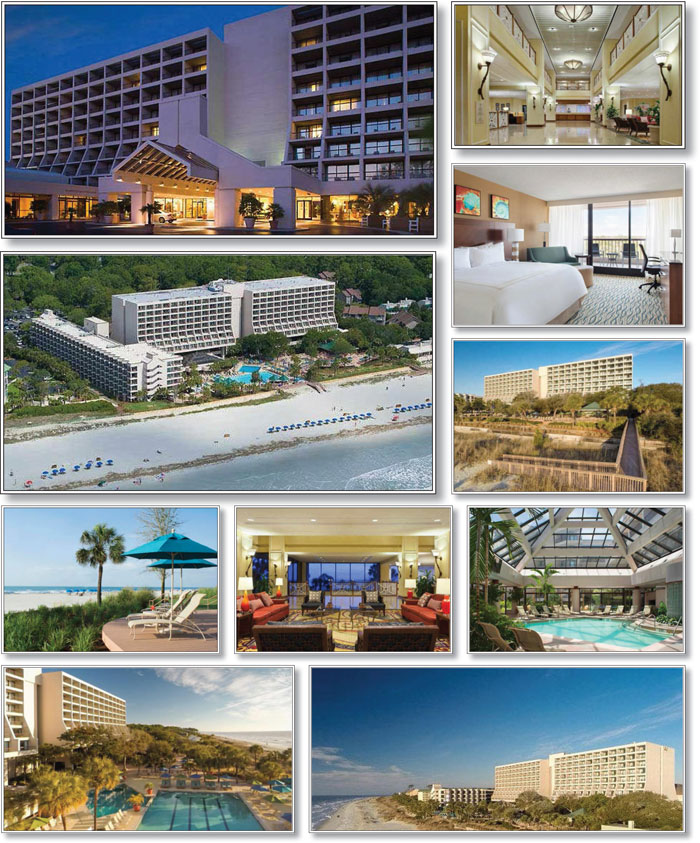

| MARRIOTT HILTON HEAD RESORT & SPA |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

20

| MARRIOTT HILTON HEAD RESORT & SPA |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

21

| No. 3 – Marriott Hilton Head Resort & Spa | ||||||||

| Loan Information | Property Information | |||||||

| Mortgage Loan Seller: | Rialto Mortgage Finance, LLC | Single Asset/Portfolio: | Single Asset | |||||

| Credit Assessment (DBRS/Fitch/Moody’s/Morningstar): | NR/NR/NR/NR | Property Type: | Hospitality | |||||

| Original Principal Balance(1): | $43,000,000 | Specific Property Type: | Full Service | |||||

| Cut-off Date Balance(1): | $42,859,454 | Location: | Hilton Head Island, SC | |||||

| % of Initial Pool Balance: | 4.5% | Size: | 513 Rooms | |||||

| Loan Purpose: | Refinance | Cut-off Date

Balance Per Room(1):

| $190,409 | |||||

| Borrower Name: | Columbia Properties Hilton Head, LLC | Year Built/Renovated: | 1976/2015 | |||||

| Sponsors: | Columbia Sussex Corporation; CSC Holdings, LLC | Title Vesting: | Fee | |||||

| Mortgage Rate: | 4.920% | Property Manager: | Self-managed | |||||

| Note Date: | October 3, 2016 | 4thMost Recent Occupancy (As of): | 58.8% (12/31/2012) | |||||

| Anticipated Repayment Date: | NAP | 3rdMost Recent Occupancy (As of): | 58.7% (12/31/2013) | |||||

| Maturity Date: | October 6, 2026 | 2ndMost Recent Occupancy (As of): | 58.0% (12/31/2014) | |||||

| IO Period: | None | Most Recent Occupancy (As of): | 57.6% (12/31/2015) | |||||

| Loan Term (Original): | 120 months | Current Occupancy (As of): | 59.2% (8/31/2016) | |||||

| Seasoning: | 2 months | |||||||

| Amortization Term (Original): | 300 months | Underwriting and Financial Information: | ||||||

| Loan Amortization Type: | Amortizing Balloon | 4thMost Recent NOI (As of): | $10,285,001 (12/31/2013) | |||||

| Interest Accrual Method: | Actual/360 | 3rdMost Recent NOI (As of): | $9,679,146 (12/31/2014) | |||||

| Call Protection: | L(26),D(90),O(4) | 2ndMost Recent NOI (As of)(3): | $10,387,728 (12/31/2015) | |||||

| Lockbox Type: | Hard/Springing Cash Management | Most Recent NOI (As of)(3): | $11,792,589 (TTM 8/31/2016) | |||||

| Additional Debt(1): | Yes | |||||||

| Additional Debt Type(1): | Pari Passu | U/W Revenues: | $33,338,474 | |||||

| U/W Expenses: | $21,646,100 | |||||||

| U/W NOI: | $11,692,374 | |||||||

| U/W NCF: | $10,025,450 | |||||||

| U/W NOI DSCR(1): | 1.71x | |||||||

| Escrows and Reserves(2): | U/W NCF DSCR(1): | 1.47x | ||||||

| U/W NOI Debt Yield(1): | 12.0% | |||||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NCF Debt Yield(1): | 10.3% | |||

| Taxes | $1,037,750 | $98,833 | NAP | As-Is Appraised Value: | $163,500,000 | |||

| Insurance | $203,170 | $32,249 | NAP | As-Is Appraisal Valuation Date: | August 30, 2016 | |||

| FF&E Reserve | $0 | $138,910 | NAP | Cut-off Date LTV Ratio(1): | 59.7% | |||

| Seasonality Reserve | $3,630,000 | Springing | $3,630,000 | LTV Ratio at Maturity or ARD(1): | 44.7% | |||

| (1) | See “The Mortgage Loan” section. All statistical financial information related to balances per room, loan-to-value ratios, debt service coverage ratios and debt yield are based on the Marriott Hilton Head Resort & Spa Whole Loan. |

| (2) | See “Escrows” section. |

| (3) | See “Cash Flow Analysis” section. |

The Mortgage Loan. The mortgage loan (the “Marriott Hilton Head Resort & Spa Mortgage Loan”) is part of a loan combination (the “Marriott Hilton Head Resort & Spa Whole Loan”) that is evidenced by sixpari passu promissory notes (A-1, A-2A, A-2B, A-3A, A-3B and A-4) that are secured by a first mortgage encumbering a full service hotel property located in Hilton Head Island, South Carolina (the “Marriott Hilton Head Resort & Spa Property”). The Marriott Hilton Head Resort & Spa Whole Loan was co-originated on October 3, 2016 by Rialto Mortgage Finance, LLC and Citigroup Global Markets Realty Corp. The Marriott Hilton Head Resort & Spa Whole Loan had an original principal balance of $98,000,000, has an outstanding principal balance as of the Cut-off Date of $97,679,686 and accrues interest at an interest rate of 4.920%per annum. The Marriott Hilton Head Resort & Spa Whole Loan had an initial term of 120 months, has a remaining term of 118 months as of the Cut-off Date and requires payments of principal and interest based on a 25-year amortization schedule. The Marriott Hilton Head Resort & Spa Whole Loan matures on October 6, 2026.

The Marriott Hilton Head Resort & Spa Mortgage Loan evidenced by Note A-1, which represents a controlling interest in the Marriott Hilton Head Resort & Spa Whole Loan and will be contributed to the WFCM 2015-LC25 Trust. The Marriott Hilton Head Resort & Spa Mortgage Loan had an original principal balance of $43,000,000 and has an outstanding principal balance as of the Cut-off Date of $42,859,454. The non-controlling Notes A-2A, A-2B, A-3A, A-3B and A-4 (the “Marriott Hilton Head Resort & Spa Companion Loans”) had an aggregate original principal balance of $55,000,000. Notes A-2B and A-4 are expected to be contributed to the CGCMT 2016-C3 Trust. Notes A-2A, A-3A and A-3B are expected to be contributed to one or more future securitizations; however, the lender provides no assurances that any non-securitizedparipassu note will not be split further. See “Description of the Mortgage Pool – The Whole Loans – The Serviced Whole Loans – The Marriott Hilton Head Resort & Spa Whole Loan” in the Preliminary Prospectus.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

22

| MARRIOTT HILTON HEAD RESORT & SPA |

Pari Passu Note Summary

| Original Balance | Note Holder | Controlling Interest | ||

| Note A-1 | $43,000,000 | WFCM 2016-LC25 | Yes | |

| Notes A-2B, A-4 | $30,000,000 | CGCMT 2016-C3 | No | |

| Notes A-2A, A-3A, A-3B | $25,000,000 | Citigroup Global Markets Realty Corp. | No | |

| Total | $98,000,000 |

Following the lockout period, the borrower has the right to defease the Marriott Hilton Head Resort & Spa Whole Loan in whole, but not in part, on any date before July 6, 2026. In addition, the Marriott Hilton Head Resort & Spa Whole Loan is prepayable without penalty on or after July 6, 2026. The lockout period will expire on the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) November 6, 2019.

Sources and Uses

| Sources | Uses | |||||||

| Original whole loan amount | $98,000,000 | 87.6% | Loan Payoff(1) | $106,553,280 | 95.3% | |||

| Sponsor’s new cash contribution | 13,827,003 | 12.4 | Reserves | 4,870,920 | 4.4 | |||

| Closing costs | 402,803 | 0.4 | ||||||

| Total Sources | $111,827,003 | 100.0% | Total Uses | $111,827,003 | 100.0% |

| (1) | The Marriott Hilton Head Resort & Spa Property was previously securitized in the JPMCC 2007-CB18 transaction. |

The Property.The Marriott Hilton Head Resort & Spa Property is a 513-room full service hotel located in Hilton Head Island, South Carolina. The Marriott Hilton Head Resort & Spa Property is situated on 13.8 acres and is comprised of two buildings: a 10-story main tower that opened in 1976 and a 5-story south tower that opened in 1985. The Marriott Hilton Head Resort & Spa Property was initially branded as a Hyatt Hotel but was converted to a Marriott brand in 2001. According to the sponsors, during 2011 to mid-2016 approximately $9.2 million of capital was invested by the borrower. Upgrades and renovations included new LCD televisions in all guestrooms and the construction of nine new pool cabanas in 2012; upgrades to HVAC in 2013, and the most recent renovation was completed in 2014/2015, when all of the guestrooms were completely renovated along with public areas and meeting/banquet rooms. According to the sponsor, additional improvements are anticipated to be completed in the near-term, including corridor carpeting, which will be replaced in late 2016, while during 2017, the parking lot will be repaved and meeting rooms will be renovated. The Marriott Hilton Head Resort & Spa Property includes 568 parking spaces resulting in a parking ratio of 1.1 spaces per room. The parking operation allows for self-parking but also includes a valet service.

The Marriott Hilton Head Resort & Spa contains, 321 double queen guestrooms, 167 king guestrooms, 19 one-bedroom suites and six suites. Guestrooms offer either one king-sized bed or two queen beds with a pillow top mattress, sofa, oversized chair, desk, 32-inch flat screen television, in-room safe, coffee maker/tea service, two speaker phones with voicemail, high speed internet service (for a fee), and a mini refrigerator. The Marriott Hilton Head Resort & Spa Property features guestrooms on floors 3-10 within the main tower, and on all five floors of the south tower.