FS Credit Real Estate Income Trust (FSREI)

Filed: 25 Jul 17, 12:00am

As filed with the Securities and Exchange Commission on July 24, 2017.

Registration No. 333-216037

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

PRE-EFFECTIVE

AMENDMENT NO. 2

to

FORM S-11

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

FS CREDIT REAL ESTATE INCOME TRUST, INC.

(Exact name of registrant as specified in governing instruments)

201 Rouse Boulevard

Philadelphia, PA 19112

(215) 495-1150

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

Michael C. Forman

FS Credit Real Estate Income Trust, Inc.

201 Rouse Boulevard

Philadelphia, PA 19112

(215) 495-1150

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Rosemarie A. Thurston

Jason W. Goode

Alston & Bird LLP

1201 West Peachtree Street

Atlanta, GA 30309-3424

(404) 881-7000

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ (Do not check if smaller reporting company) | Smaller Reporting Company | ☐ | |||

| Emerging Growth Company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission and various states is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, PRELIMINARY PROSPECTUS DATED JULY 24, 2017

Maximum Offering of $2,750,000,000 in Shares of Common Stock

FS CREDIT REAL ESTATE INCOME TRUST, INC.

Preliminary Prospectus

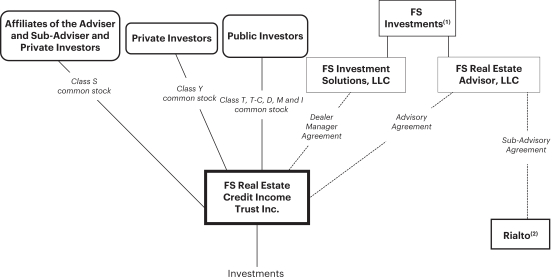

FS Credit Real Estate Income Trust, Inc. is a newly organized Maryland corporation formed to originate, acquire and manage a portfolio of senior loans secured by commercial real estate primarily in the United States. We are focused on floating-rate mortgage loans that are secured by first priority mortgages on transitional commercial real estate properties, but we may also invest in other real estate-related assets, including: (i) other commercial real estate mortgage loans, including fixed-rate loans, subordinated loans, B-Notes, mezzanine loans and participations in commercial mortgage loans; and (ii) commercial real estate securities, including commercial mortgage-backed securities, or CMBS, residential mortgage-backed securities, or RMBS, unsecured debt of listed and non-listed REITs, collateralized debt obligations and equity or equity-linked securities. To a lesser extent we may invest in warehouse loans secured by commercial or residential mortgages, credit loans to commercial real estate companies and portfolios of single family home mortgages. We intend to qualify as a real estate investment trust, or a REIT, for U.S. federal income tax purposes.

We are managed by our adviser, FS Real Estate Advisor, LLC (“FS Real Estate Advisor” or the “adviser”), a subsidiary of our sponsor, Franklin Square Holdings, L.P. (“FS Investments” or the “sponsor”), a national sponsor of alternative investment funds designed for the individual investor. FS Real Estate Advisor has engaged Rialto Capital Management, LLC (“Rialto” or the “sub-adviser”) to act as the sub-adviser.

We are offering on a continuous basis up to $2,750,000,000 in shares of common stock, consisting of up to $2,500,000,000 in shares of common stock in our primary offering and up to $250,000,000 in shares of common stock pursuant to our distribution reinvestment plan. We are offering to sell any combination of five classes of shares of our common stock, Class T, Class T-C, Class D, Class M and Class I shares, with a dollar value up to the maximum offering amount. Class S and Class Y shares will only be offered in this offering pursuant to our distribution reinvestment plan. The share classes have different selling commissions and dealer manager fees, and different ongoing stockholder servicing fees. Prior to the date upon which we begin to accept subscriptions from investors in this offering, the sponsor and Rialto, or their respective affiliates, will purchase an aggregate of $10.0 million of our Class S shares of common stock at $25.00 per share (the “Initial Class S Investment”). Until the date when we first accept subscriptions for shares in this offering, the per share purchase price for shares of our common stock will be $25.00 per share, plus, for Class T and Class T-C shares, applicable selling commissions and for Class T shares, applicable dealer manager fees. Thereafter, the per share purchase price will vary from day-to-day and, on each day, will equal our NAV per share for each class of shares plus, for Class T and Class T-C shares, applicable selling commissions and for Class T shares, applicable dealer manager fees. This is a “best efforts” offering, which means that FS Investment Solutions, LLC, the dealer manager of this offering (the “dealer manager”), will use its best efforts but is not required to sell any specific amount of shares in this offering.

Although we do not intend to list our shares of common stock for trading on an exchange or other trading market, in an effort to provide our stockholders with liquidity in respect of their investment in our shares, we have adopted a share repurchase plan whereby, subject to certain limitations, stockholders may request on a daily basis that we repurchase all or any portion of their shares. The repurchase price per share for each class of common stock will equal the NAV per share for such class on the repurchase date.

Investing in our common stock involves a high degree of risk. You should purchase these securities only if you can afford the complete loss of your investment. See “Risk Factors” beginning on page 36 for risks to consider before buying our shares, including:

| ● | We have no prior operating history and there is no assurance that we will achieve our investment objectives. |

| ● | This is a “blind pool” offering and thus you will not have the opportunity to evaluate our investments before we make them. |

| ● | Since there is no public trading market for shares of our common stock, repurchase of shares by us will likely be the only way to dispose of your shares. Our share repurchase plan will provide stockholders with |

the opportunity to request that we repurchase their shares on a daily basis, subject to certain limitations. Our board of directors may modify, suspend or terminate our share repurchase plan if it deems such action to be in our best interest and the best interest of our stockholders. Finally, we are not obligated by our charter or otherwise to effect a liquidity event at any time. As a result, our shares should be considered as having only limited liquidity and at times may be illiquid. |

| ● | The purchase and repurchase price for shares of our common stock will be based on our NAV and will not be based on any public trading market. Because the valuation of our investments is inherently subjective, our NAV may not accurately reflect the actual price at which our assets could be liquidated on any given day. |

| ● | We cannot guarantee that we will make distributions, and if we do we may fund such distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings, return of capital or offering proceeds, and we have no limits on the amounts we may pay from such sources. |

| ● | We have no employees and are dependent on our adviser and the sub-adviser to conduct our operations. Our adviser and the sub-adviser will face conflicts of interest as a result of, among other things, the allocation of investment opportunities among us and other investment vehicles, the allocation of time of their investment professionals and the substantial fees and expenses that we will pay to the adviser and its affiliates. |

| ● | This is a “best efforts” offering. If we are not able to raise a substantial amount of capital in the near term, our ability to achieve our investment objectives could be adversely affected. |

| ● | There are limits on the ownership and transferability of our shares. |

| ● | Our failure to qualify or remain qualified as a REIT would adversely affect our NAV and the amount of cash available for distribution to our stockholders. |

None of the Securities and Exchange Commission (the “SEC”), the Attorney General of the State of New York or any other state securities regulator has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. The use of forecasts in this offering is prohibited. Any oral or written predictions about the amount or certainty of any cash benefits or tax consequences which may result from an investment in our common stock is prohibited.

| Price to the Public(1) | Selling Commissions | Dealer Manager Fees | Proceeds to Us, Before Expenses | |||||||||||||

Maximum Primary Offering(2) | $ | 2,500,000,000 | $ | 30,000,000 | $ | 6,250,000 | $ | 2,463,750,000 | ||||||||

Class T Shares, Per Share | $ | 26.11 | $ | 0.78 | $ | 0.33 | $ | 25.00 | ||||||||

Class T-C Shares, Per Share | $ | 25.78 | $ | 0.78 | $ | — | $ | 25.00 | ||||||||

Class D Shares, Per Share | $ | 25.00 | — | — | $ | 25.00 | ||||||||||

Class M Shares, Per Share | $ | 25.00 | — | — | $ | 25.00 | ||||||||||

Class I Shares, Per Share | $ | 25.00 | — | — | $ | 25.00 | ||||||||||

Maximum Distribution Reinvestment Plan(2) | $ | 250,000,000 | — | — | $ | 250,000,000 | ||||||||||

| (1) | The per share price shown will apply to the shares sold in this offering until the date when we first accept subscrptions for shares, thereafter, the price at which shares of each class are sold will vary from day-to-day and, on each day will be equal to a price per share equal to our NAV per share for the applicable class of shares plus, for Class T and Class T-C shares, applicable selling commissions and for Class T shares, applicable dealer manager fees. |

| (2) | Assumes that 1/5 of the gross offering proceeds are from the sale of each of our Class T, Class T-C, Class D, Class M and Class I shares. For Class T shares sold in the primary offering, investors will pay selling commissions of up to 3.0% of the purchase price and dealer manager fees of up to 1.25% of the purchase price. For Class T-C shares sold in the primary offering, investors will pay selling commissions of up to 3.0% of the purchase price. We will also pay stockholder servicing fees over time to the dealer manager, subject to limitations on underwriting compensation, equal to 1.0%, 0.85%, 0.3% and 0.3% per annum of the aggregate NAV of our outstanding Class T, Class T-C, Class D and Class M shares, respectively; provided that the stockholder servicing fee for Class T-C shares will be comprised of an advisor stockholder servicing fee of 0.65% per annum, and a dealer stockholder servicing fee of 0.20% per annum, of the aggregate NAV for the Class T-C shares. No stockholder servicing fees will be paid with respect to the Class I, Class S or Class Y shares. The total amount that will be paid over time for other underwriting compensation depends on the average length of time for which shares remain outstanding, the term over which such amount is measured and the performance of our investments. We will also pay or reimburse certain organization and offering expenses. See “Estimated Use of Proceeds,” “Compensation” and “Plan of Distribution”. |

The date of this prospectus is , 2017.

FS Investment Solutions, LLC

Investors who meet the suitability standards described herein may purchase shares of our common stock. See “Suitability Standards” below. Investors seeking to purchase shares of our common stock must proceed as follows:

| ● | Read this entire prospectus, including any documents incorporated by reference herein, and any appendices and supplements accompanying this prospectus. |

| ● | Complete the execution copy of the subscription agreement. A specimen copy of the subscription agreement, including instructions for completing it, is included in this prospectus as Appendix B. |

| ● | Deliver a check or submit a wire transfer for the full purchase price of the shares of our common stock being subscribed for along with the completed subscription agreement to your registered selling representative or investment advisor. Your check should be made payable, or wire transfer directed, to “FS Credit Real Estate Income Trust, Inc.” After you have satisfied the applicable minimum initial purchase requirements for the class of stock you are purchasing ($5,000 for Class T, Class T-C, Class D and Class M shares; $1,000,000 for Class I shares), additional purchases must be in increments of $500, except for purchases made under our distribution reinvestment plan. |

By executing the subscription agreement and paying the total purchase price for the shares subscribed for, each investor attests that he or she meets the suitability standards as stated in the subscription agreement and agrees to be bound by all of its terms.

Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription in whole or in part. We are not permitted to accept a subscription for shares of our common stock until at least five business days after the date you receive this prospectus. Any subscription may be canceled at any time before it has been accepted. See “Plan of Distribution” for additional information regarding subscriptions for shares of our common stock in this offering. If for any reason we reject the subscription, we will return the check or wire, without interest or deduction, within ten business days of rejecting it.

An approved trustee must process and forward to us subscriptions made through individual retirement accounts, or IRAs, Keogh plans and 401(k) plans. In the case of investments made through IRAs, Keogh plans and 401(k) plans, we will send the confirmation and notice of our acceptance to the trustee.

You have the option of placing a transfer on death, or TOD, designation on your shares purchased in this offering. A TOD designation transfers the ownership of the shares to your designated beneficiary upon your death. This designation may only be made by individuals, not entities, who are the sole or joint owners with right to survivorship of the shares. If you would like to place a TOD designation on your shares, you must check the TOD box on the subscription agreement and you must complete and return a TOD form, which you may obtain from your financial advisor.

i

Shares of our common stock are suitable only as a long-term investment for persons of adequate financial means who do not need near-term liquidity from their investment. We do not expect there to be a public market for our shares and thus it may be difficult for you to sell your shares. On a limited basis, you may be able to have your shares repurchased through our share repurchase plan. You should not buy shares of our common stock if you need to sell them in the near future. The minimum initial investment in shares of our common stock that we will accept is $5,000 for Class T, Class T-C, Class D and Class M shares and $1,000,000 for Class I shares.

In consideration of these factors, we require that a purchaser of shares of our common stock have either:

| ● | a net worth of at least $250,000; or |

| ● | a gross annual income of at least $70,000 and a net worth of at least $70,000. |

For purposes of determining whether you satisfy the standards, your net worth is calculated excluding the value of your home, home furnishings and automobiles.

Certain states have established suitability standards in addition to the minimum income and net worth standards described above. Shares will be sold to investors in these states only if they meet the additional suitability standards set forth below. Certain broker-dealers selling shares in the offering may impose greater suitability standards than those set forth above and the state-specific suitability standards set forth below.

Alabama: Alabama investors must have a liquid net worth of at least 10 times their investment in us and our affiliates.

California: A California investor must limit his or her investment in our shares to 10% of his or her net worth. An investment by a California investor that is an accredited investor within the meaning of the Federal securities laws (17 C.F.R. §230.501) is not subject to the foregoing limitation.

Iowa: Iowa investors must (i) have either (a) an annual gross income of at least $100,000 and a net worth of at least $100,000, or (b) a net worth of at least $350,000 (net worth should be determined exclusive of home, auto and home furnishings); and (ii) must limit their aggregate investment in this offering and in the securities of other non-traded real estate investment trusts (REITs) to 10% of such investor’s liquid net worth (liquid net worth should be determined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities). Investors who are accredited investors as defined in 17 C.F.R. § 230.501 of Regulation D under the Securities Act of 1933, as amended, are not subject to the foregoing 10% investment concentration limit.

Kansas: It is recommended by the Office of Kansas Securities Commissioner that Kansas investors limit their aggregate investments in us and other non-traded real estate investment trusts to not more than 10% of their liquid net worth.

Maine: In addition to the suitability standards above, the Maine Office of Securities recommends that a Maine investor’s aggregate investment in our shares and the shares of similar direct participation investments not exceed 10% of the investor’s liquid net worth. For this purpose, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities.

ii

Massachusetts: Massachusetts investors may not invest more than 10% of their liquid net worth in us and in other illiquid direct participation programs.

Missouri: Missouri investors must limit their investment in each class of our common stock to 10% of their liquid net worth.

Nebraska: In addition to the suitability standards above, a Nebraska investor must limit his or her aggregate investment in shares of us and other non-publicly traded REITs to 10% of the investor’s net worth (exclusive of home, home furnishings, and automobiles). Investors who are “accredited investors” as defined in 17 C.F.R. 230.501 are not subject to the foregoing concentration limit.

New Mexico: New Mexico investors may not invest more than 10% of their liquid net worth in our shares, shares of our affiliates and other non-traded REITs.

Oregon: An Oregon investor’s maximum investment in the issuer and affiliates may not exceed 10% of their liquid net worth, excluding home, furnishings and automobiles.

Pennsylvania: Pennsylvania investors may not invest more than 10% of their net worth in us.

Tennessee: Tennessee investors who are not accredited investors may not invest more than 10% of their liquid net worth in us.

Vermont: Accredited investors in Vermont, as defined in 17 C.F.R. §230.501, may invest freely in this offering. In addition to the suitability standards described above, non-accredited Vermont investors may not purchase an amount in this offering that exceeds 10% of the investor’s net worth. For these purposes, “liquid net worth” is defined as an investor’s total assets (not including home, home furnishings, or automobiles) minus total liabilities.

For the purposes of these suitability standards, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities.

Our sponsor and each person selling shares on our behalf must make every reasonable effort to determine that the purchase of shares of our common stock is a suitable and appropriate investment for each investor. In making this determination, our sponsor and the dealer manager will rely upon information provided by the investor to the participating broker-dealer as well as the suitability assessment made by each participating broker-dealer. Before you purchase shares of our common stock, your participating broker-dealer, authorized representative or other person placing shares on your behalf will rely on relevant information provided by you to determine that you:

| ● | meet the minimum income and net worth standards established in your state; |

| ● | are or will be in a financial position appropriate to enable you to realize the potential benefits described in the prospectus; |

| ● | are able to bear the economic risk of the investment based on your overall financial situation; and |

| ● | have an apparent understanding of the fundamental risks of the investment, the risk that you may lose your entire investment, the limited liquidity of our common stock, the restrictions on transferability of our common stock and the tax consequences of the investment. |

Participating broker-dealers are required to maintain for six years records of the information used to determine that an investment in shares of our common stock is suitable and appropriate for a stockholder.

iii

By signing the subscription agreement required for purchases of our common stock, you represent and warrant to us that you have received a copy of this prospectus and that you meet the net worth and annual gross income requirements described above. These representations and warranties help us to ensure that you are fully informed about an investment in our common stock and that all investors meet our suitability standards. In the event you, another stockholder or a regulatory authority attempt to hold us liable because stockholders did not receive copies of this prospectus or because we failed to adhere to each state’s suitability requirements, we will assert these representations and warranties made by you in any proceeding in which such potential liability is disputed in an attempt to avoid any such liability. By making these representations, you do not waive any rights that you may have under federal or state securities laws.

iv

Please carefully read the information in this prospectus and any accompanying prospectus supplements, which we refer to collectively as the “prospectus.” You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell these securities. You should not assume that the information contained in this prospectus is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This prospectus is part of a registration statement that we filed with the Securities and Exchange Commission, or the SEC. Periodically, as material developments occur, we will provide a prospectus supplement that may add, update or change information contained in this prospectus. Any statement that we make in this prospectus will be modified or superseded by any inconsistent statement made by us in a subsequent prospectus supplement. The registration statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this prospectus. You should read this prospectus and the related exhibits filed with the SEC and any prospectus supplements, together with additional information described under “Available Information.”

As soon as reasonably practicable after the end of each day on which the New York Stock Exchange, or the NYSE, is open for unrestricted trading, which we refer to as a “business day,” after the close of the NYSE (generally, 4:00 p.m. Eastern time), which we refer to as the “close of business,” we will (1) post our NAV per share for such day for each share class on our website and (2) make our NAV per share for each share class available on our toll-free telephone line. Our website will also contain this prospectus and any prospectus supplements that have not been superseded by a subsequent supplement. In addition, following the last business day of each month, we will file with the SEC a prospectus supplement disclosing our NAV per share for each share class for each business day in the preceding month. In order to avoid interruptions in the continuous offering of our shares of common stock, we will file an amendment to the registration statement with the SEC on or before such time as the most recent offering price per share of any class of our common stock represents a 20% change from the per share price set forth in the registration statement filed with the SEC, as amended from time to time. There can be no assurance, however, that our continuous offering will not be suspended while the SEC reviews any such amendment, until it is declared effective, if at all.

IMPORTANT NOTE FOR BROKER-DEALERS: This prospectus will be supplemented as soon as reasonably practicable following the last business day of each month with respect to the NAV per share for each share class for each business day in the preceding month and from time to time with respect to other information. All sales literature used in connection with this offering must be accompanied by the current prospectus and all prospectus supplements that have not been superseded by a subsequent supplement.

v

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements about our business, including, in particular, statements about our plans, strategies and objectives. You can generally identify forward-looking statements by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue” or other similar words. These statements include our plans and objectives for future operations, including plans and objectives relating to future growth and availability of funds, and are based on current expectations that involve numerous risks and uncertainties. Assumptions relating to these statements involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to accurately predict and many of which are beyond our control. Although we believe the assumptions underlying the forward-looking statements, and the forward-looking statements themselves, are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that these forward-looking statements will prove to be accurate and our actual results, performance and achievements may be materially different from that expressed or implied by these forward-looking statements. In light of the significant uncertainties inherent in these forward looking statements, the inclusion of this information should not be regarded as a representation by us or any other person that our objectives and plans, which we consider to be reasonable, will be achieved.

You should carefully review the “Risk Factors” section of this prospectus for a discussion of the risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition. Except as otherwise required by federal securities laws, we do not undertake to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

vi

| i |

| ii | ||||

| v | ||||

| vi |

| 1 |

| 10 |

| 36 | ||||

| 36 | ||||

| 40 | ||||

| 47 | ||||

| 50 | ||||

| 58 | ||||

| 60 | ||||

| 68 | ||||

| 70 | ||||

| 73 | ||||

| 82 | ||||

| 100 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 108 | |||

| 109 |

| 117 | ||||

| 128 | ||||

| 134 | ||||

| 138 |

| 167 | ||||

| 168 | ||||

| 183 | ||||

| 184 | ||||

| 190 | ||||

| 196 | ||||

| 197 | ||||

| 198 | ||||

| 198 | ||||

| 198 | ||||

| 198 | ||||

| F-1 | ||||

| A-1 | ||||

| B-1 | ||||

| C-1 | ||||

| D-1 |

vii

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

Set forth below are some of the more frequently asked questions and accompanying answers related to our structure, our management, our business and an offering of this type. They are not a substitute for disclosures elsewhere in this prospectus. You are encouraged to read “Prospectus Summary,” “Risk Factors” and the remainder of this prospectus in their entirety for more detailed information about this offering before deciding to purchase shares of our common stock.

What is FS Credit Real Estate Income Trust, Inc.?

We are a Maryland corporation formed on November 7, 2016 to originate, acquire and manage real estate-related debt investments in the United States. We are focused on floating-rate mortgage loans that are secured by first priority mortgages on transitional commercial real estate properties but we may also invest in other real estate-related assets, including (i) other commercial real estate mortgage loans, including fixed-rate loans, subordinated loans, B-Notes, mezzanine loans and participations in commercial mortgage loans and (ii) commercial real estate securities, including commercial mortgage-backed securities, or CMBS, unsecured debt of publicly listed real estate investment trusts, or REITs, collateralized debt obligations and equity or equity-linked securities. We intend to qualify to be taxed as a REIT for U.S. federal income tax purposes.

What is a REIT?

In general, a REIT is a company that:

| ● | combines the capital of many investors to acquire or provide financing for real estate-related investments; |

| ● | allows individual investors to invest in a large-scale diversified real estate portfolio through the purchase of interests, typically shares, in the REIT; |

| ● | is required to pay distributions to investors of at least 90% of its annual REIT taxable income (which is computed without regard to the dividends-paid deduction, excludes net capital gain and does not necessarily equal net income as calculated in accordance with generally accepted accounting principles in the United States, or GAAP); and |

| ● | is able to qualify to be taxed as a REIT for U.S. federal income tax purposes and therefore avoids the “double taxation” treatment of income that would normally result from investments in a corporation because a REIT does not generally pay federal corporate income taxes on its net income, provided certain income tax requirements are satisfied. |

In this prospectus, we refer to an entity that qualifies and has elected to be taxed as a REIT for U.S. federal income tax purposes as a REIT. We are not yet qualified as a REIT. We intend to elect and qualify to be taxed as a REIT for U.S. federal income tax purposes commencing with our first taxable year of operations.

What is a perpetual-life REIT?

We use the term “perpetual-life REIT” to describe an investment vehicle of indefinite duration focused on real estate debt investments and other real estate-related assets, the shares of common stock of which are generally intended to be sold and repurchased by the issuer on a continuous basis. Public and private pension plan sponsors, endowments, foundations and other pension funds avail themselves of similarly structured, perpetual-life vehicles as one option for allocating a portion of their portfolio to direct investments in real estate and real estate-related assets. As a perpetual-life, publicly-offered REIT, we intend to offer a similar investment option to a broader universe of investors through this offering. While we are not obligated by our charter or otherwise to effect a liquidity event within a certain amount of time, our board of directors

1

may determine at some point in the future to pursue a liquidity event, including a listing of our common stock on a national securities exchange, the sale or other disposition of all or substantially all of our assets or our merger or consolidation with or into another entity.

How is an investment in shares of your common stock different from an investment in a listed REIT?

We do not intend to list our shares for trading on a national securities exchange for the foreseeable future. We believe that a non-listed structure is more appropriate for the long-term nature of the assets in which we intend to invest. This structure allows us to operate with a long-term view, similar to that of other types of private investment funds, instead of managing to quarterly market expectations. An investment in our common stock generally differs from an investment in a listed REIT because: (1) the prices of shares of listed REITs are determined by the public market, which may cause a listed REIT’s stock price to fluctuate at a premium or discount to NAV based on factors such as supply and demand, economic preferences and other market forces, while our offering price is subject to adjustment in accordance with our share pricing policy as a result of changes in the NAV of our shares, which is based on the fair value of our investments; therefore, our stockholders will not be subject to the daily share price volatility associated with the public markets; (2) unlisted investments in real estate debt have historically demonstrated a lower correlation to traditional asset classes, such as stocks and bonds, as compared to the correlation exhibited by listed REITs; and (3) shares of listed REITs are liquid and easily transferable, while shares of our common stock cannot readily be sold and have significant restrictions on their ownership, transferability and repurchase. The determination of our NAV is inherently subjective and our NAV may decrease over time, including as a result of declining asset values.

How is an investment in shares of your common stock different from traditional non-listed REITs?

As compared to the majority of non-listed REITs available to the public in the market today, an investment in shares of our stock generally differs from such REITs in two ways. First, shares of traditional non-listed REITs are typically not valued until two years and 150 days following the launch of their offering, whereas our shares will be valued on a daily basis during this offering. Changes in our daily NAV will reflect factors including, but not limited to, our portfolio income, interest expense, unrealized and realized gains (losses) on assets and accruals for fees, thereby enabling investors to invest in our shares at a price that reflects current market conditions and asset values. See “Net Asset Value Calculation and Valuation Guidelines.” Second, traditional non-listed REITs are generally illiquid, often for periods of eight years or more, with only very limited liquidity provided through share repurchase plans that have significant restrictions on the number of shares that can be repurchased each year and the sources of funding available for these repurchases. In contrast, our stockholders may request, on a daily basis, that we repurchase all or any portion of their shares, subject to limitations that are less restrictive than the repurchase plans of traditional non-listed REITs. See “Share Repurchases.”

Why should I invest in a company that is focused on commercial real estate loans and commercial real estate-related debt securities?

We believe that the absence of many historical sources of debt financing for the commercial real estate market has and will continue to create a favorable environment for experienced commercial real estate lenders to produce attractive, risk-adjusted returns. Furthermore, we believe there is unmet demand for transitional lending for the acquisition of commercial real estate properties that require renovation or repositioning, as many traditional lenders only make loans secured by more stabilized real estate properties. These transitional loans often yield more than loans with similar loan-to-value characteristics that are secured by more stabilized real estate properties as well as commercial real estate assets traded in the securitized markets. The de-leveraging and risk assessment taking place among the large commercial and investment

2

banks and traditional credit providers has left real estate owners with limited options for obtaining debt financing. As a result, the pricing of real estate debt capital has increased and the terms and structure of real estate loans, including borrower recourse, have generally become more favorable for lenders. At the same time, as part of this overall de-leveraging, we expect that portfolios of existing loans and debt instruments secured by commercial real estate will continue to be offered for sale by banks and other institutions at discounts to par value and in some cases with relatively attractive seller financing. In addition, many owners of commercial real estate face maturities on loans that have been syndicated or securitized, or both, and may have difficulty, due to the loan structure and servicing standards, in obtaining extensions even for performing, stabilized assets. You and your financial advisor should determine whether investing in a company that focuses on commercial real estate mortgage loans and commercial real estate-related debt securities would benefit your investment portfolio.

What competitive strengths do you derive from your adviser and the sub-adviser?

We are externally managed by our adviser, FS Real Estate Advisor, LLC. Our adviser is an affiliate of FS Investments, a national sponsor of alternative investment funds designed for the individual investor. FS Real Estate Advisor is led by substantially the same personnel that form the investment and operations teams of the registered investment advisers that manage FS Investments’ other investment vehicles, including business development companies (BDCs) and closed-end funds. FS Real Estate Advisor’s senior management team has significant experience in private debt, private equity and real estate investing, and has developed an expertise in using all levels of the corporate capital structure to produce income-generating investments, while focusing on risk management. The team also has extensive knowledge of the managerial, operational and regulatory requirements of publicly registered alternative asset entities. We believe that the active and ongoing participation by FS Investments and its affiliates in the credit markets, and the depth of experience and disciplined investment approach of FS Real Estate Advisor’s management team, will allow FS Real Estate Advisor to successfully execute our investment strategy. See “Management” for more information on the experience of the members of the senior management team.

Our adviser has engaged Rialto Capital Management, LLC, or Rialto, a leading real estate investment and asset management company, to perform services on behalf of our adviser for us primarily related to the selection of our investments and to assist with the day-to-day management of our investment operations. From 2009 through March 31, 2017, Rialto has participated in approximately $8.0 billion of equity investments, relating to approximately $13.0 billion of real estate loans, securities, commercial and residential properties. As of March 31, 2017, Rialto had approximately $5.4 billion in regulatory assets under management, or RAUM. RAUM, which is calculated for purposes of Rialto’s filings under the Investment Advisers Act of 1940, is comprised of the estimated fair value of assets being managed and unfunded capital commitments.

We expect to capitalize on Rialto’s significant and broad experience managing various real estate strategies across equity and debt. We also expect to capitalize on its national footprint and origination platform to deploy significant amounts of capital in investments with attractive risk-return profiles. As of March 31, 2017, Rialto’s commercial real estate platform, which has approximately 350 associates in seventeen offices across the U.S. and Europe, has originated over $7.3 billion of commercial mortgage loans since its inception and is one of the largest non-bank underwriters of commercial mortgage loans used in CMBS securitizations. As a standalone separately capitalized subsidiary of Lennar Corporation (NYSE: LEN and LEN.B), one of the nation’s largest homebuilders, Rialto is able to use its vertically integrated platform and experienced underwriting team to provide in-house evaluations of a wide variety of loans and markets. We believe Rialto’s ability to pivot throughout real estate cycles, taking advantage of opportunities with the potential to generate attractive risk-adjusted returns across the capital structure, will be a competitive advantage for us in executing upon our investment strategy.

3

Do you currently own any investments?

No, we do not currently own any investments or have any commitments to make any investments. For this reason, this offering is deemed to be a “blind pool” offering.

What are the differences between the various classes of common stock being offered?

We are offering to the public five classes of shares of our common stock: Class T shares, Class T-C shares, Class D shares, Class M shares and Class I shares. In addition, Class S and Class Y shares are only being offered pursuant to our distribution reinvestment plan. The differences among the share classes relate to selling commissions, dealer manager fees and ongoing stockholder servicing fees and, therefore, each class may receive different distributions. See “Description of Shares” and “Plan of Distribution” for a more detailed discussion of the differences between our various classes of shares.

Assuming a NAV per share of $25.00 and assuming applicable stockholder servicing fees are paid until the 7.25% or 1.25% of gross proceeds limit, as applicable, described in “Compensation—Stockholder Servicing Fees” is reached, we expect that a one-time investment in 400 shares of each class of our shares in our primary offering (representing an aggregate NAV of $10,000 for each class) would be subject to the following upfront selling commissions, dealer manager fees and stockholder servicing fees:

| Gross Purchase Price | Upfront Selling Commissions | Upfront Dealer Manager Fees | Annual Stock- holder Servicing Fees | Maximum Stockholder Servicing Fees Over Life of Investment (Length of Time) | Total (Length of Time) | |||||||||||||||

Class T | $ | 10,444 | $ | 313 | $ | 131 | $ | 100 | $281 (3 years) | $725 (3 years) | ||||||||||

Class T-C | $ | 10,308 | $ | 313 | $ | 0 | $ | 85 | $425 (5 years) | $725 (5 years) | ||||||||||

Class D | $ | 10,000 | $ | 0 | $ | 0 | $ | 30 | $125 (4.2 years) | $125 (4.2 years) | ||||||||||

Class M | $ | 10,000 | $ | 0 | $ | 0 | $ | 30 | $725 (24.2 years) | $725 (24.2 years) | ||||||||||

Class I | $ | 10,000 | $ | 0 | $ | 0 | $ | 0 | $0 | $0 | ||||||||||

Class T and Class T-C shares are available through brokerage and transactional-based accounts. Class D shares, Class M shares and Class I shares are generally available for purchase in this offering only (1) through fee-based programs that provide access to Class D, Class M or Class I shares, (2) through participating broker-dealers that have alternative fee arrangements with their clients to provide access to Class D, Class M or Class I shares, (3) through certain registered investment advisers, (4) through bank trust departments or any other organization or person authorized to act in a fiduciary capacity for its clients or customers or (5) other categories of investors that we identify in an amendment or supplement to this prospectus. In addition, Class I shares are available for purchase (1) by endowments, foundations, pension funds and other institutional investors and (2) by our executive officers and directors and their immediate family members, as well as officers and employees of our adviser, the sub-adviser, our sponsor or other affiliates and their immediate family members, and, if approved by our board of directors or our adviser, joint venture partners, consultants and other service providers. If you are eligible to purchase more than one class of shares, you should consider, among other things, the amount of your investment, the length of time you intend to hold the shares, and the selling commissions, dealer manager fees and ongoing stockholder servicing fees attributable to the Class T, Class T-C, Class D and Class M shares, as applicable. Before making your investment decision, please consult with your investment advisor regarding your account type and the classes of common stock you may be eligible to purchase.

4

What is the per share purchase price?

The per share purchase price will vary from day-to-day and, on each day, will equal our NAV per share for each class of shares plus, for Class T and Class T-C shares, applicable selling commissions and for Class T shares, applicable dealer manager fees. You will not know the purchase price per share when you submit your purchase request.

How will you communicate the daily NAV per share?

From and after the business day following the date we first accept subscriptions for shares in this offering, as soon as reasonably practicable after the end of each business day we will post on our website, www.fsinvestments.com, and make available on our toll-free telephone line, 877-628-8575, our NAV per share for such day for each outstanding share class. In addition, as soon as reasonably practicable following the end of each month, we will file with the SEC a prospectus supplement disclosing our NAV per share for each share class for each business day in the preceding month.

Will I be charged a sales load?

If you purchase Class T or Class T-C shares, you may be charged an upfront sales load, subject to reductions for certain categories of purchasers. Investors in Class T shares may pay upfront selling commissions of up to 3.0% of the purchase price per Class T share and dealer manager fees of up to 1.25% of the purchase price per Class T share. Investors in Class T-C shares may pay upfront selling commissions of up to 3.0% of the purchase price per Class T-C share. Selling commissions and dealer manager fees may be lower for certain participating broker-dealers and may vary from one participating broker-dealer to another. Stockholders will not pay selling commissions or dealer manager fees on Class D, Class M or Class I shares or when purchasing shares of any class pursuant to our distribution reinvestment plan. Ongoing stockholder servicing fees are payable with respect to our Class T, Class T-C, Class D and Class M shares. See “Plan of Distribution.”

If I buy shares, will I receive distributions and, if so, how often?

To qualify and maintain our qualification as a REIT for U.S. federal income tax purposes, we will be required to make aggregate annual distributions to our stockholders of at least 90% of our REIT taxable income (which is computed without regard to the dividends-paid deduction, excludes net capital gain and does not necessarily equal net income as calculated in accordance with GAAP). Our board of directors may authorize distributions in excess of those required for us to maintain REIT status depending on our financial condition and such other factors as our board of directors deems relevant. We have not established a minimum distribution level, and we have not established limits on the amount of offering proceeds, borrowings or cash advances we may use to pay distributions. Once we commence paying distributions, we expect to pay distributions monthly and continue paying distributions monthly unless our results of operations, our general financial condition, applicable provisions of Maryland law or other factors make it imprudent to do so.

The per share amount of distributions on Class T, Class T-C, Class D and Class M shares will likely be lower than Class I, Class S and Class Y shares because we will deduct ongoing stockholder servicing fees from the distributions with respect to the Class T, Class T-C, Class D and Class M shares.

We may fund distributions, without limitation as to amount, from any source, which may include borrowing funds, using proceeds from this offering, issuing additional securities or selling assets. To the extent that we pay our required distributions and such distributions exceed our current and accumulated earnings and profits, such excess distributions will be treated first as a return of capital to the extent of a stockholder’s tax basis in his or her shares and then as capital gain.

5

Reducing a stockholder’s tax basis will have the effect of increasing his or her gain (or reducing loss) on a subsequent sale of shares. See “Material U.S. Federal Income Tax Considerations—Taxation of Taxable U.S. Stockholders—Distributions.”

May I reinvest my distributions in additional shares of common stock?

Yes. We have adopted a distribution reinvestment plan for our stockholders that allows our stockholders to elect to reinvest any cash distributions we may declare in additional shares of our common stock. The purchase price for shares pursuant to the distribution reinvestment plan will be the NAV per share of the respective class of common stock in effect on the date that the distribution is payable. Selling commissions and dealer manager fees will not be charged with respect to shares purchased under our distribution reinvestment plan. If you participate in our distribution reinvestment plan, the cash distributions attributable to the class of shares that you own will be automatically invested in additional shares of the same class. Unless a stockholder specifically elects to participate in the distribution reinvestment plan, that stockholder will receive cash distributions. Stockholders who elect to receive distributions in the form of shares of common stock will be subject to the same federal, state and local tax consequences as stockholders who receive their distributions in cash. See “Distribution Reinvestment Plan.” We may terminate or suspend the distribution reinvestment plan at our discretion upon ten business days’ written notice to you; and participants may terminate their participation in the distribution reinvestment plan with ten business days’ written notice to us.

Will I be taxed on the distributions I receive?

Generally, distributions that you receive, including distributions that are reinvested pursuant to our distribution reinvestment plan, will be taxed as ordinary income to the extent they are from current or accumulated earnings and profits. Dividends received from REITs are generally not eligible to be taxed at the lower U.S. federal income tax rates applicable to individuals for “qualified dividends” from C corporations (i.e., corporations generally subject to U.S. federal corporate income tax). We may designate a portion of distributions as capital gain dividends taxable at capital gain rates to the extent we recognize net capital gains from sales of assets. In addition, a portion of your distributions may be considered return of capital for U.S. federal income tax purposes. Amounts considered a return of capital generally will not be subject to tax, but will instead reduce the tax basis of your investment. This, in effect, defers a portion of your tax until your shares are repurchased, you sell your shares or we are liquidated, at which time you generally will be taxed at capital gains rates. Because each investor’s tax position is different, you should consult with your tax advisor. In particular, non-U.S. investors should consult their tax advisors regarding potential withholding taxes on distributions that you receive. See “Material U.S. Federal Income Tax Considerations.”

Can I request that my shares be repurchased?

Yes. Stockholders may request on a daily basis that we repurchase all or any portion of their shares pursuant to our share repurchase plan. However, total repurchases under the share repurchase plan during any calendar quarter are limited to the repurchase of shares whose aggregate value is 5% of the combined NAV of all classes of shares then participating in our share repurchase plan as of the last day of the previous calendar quarter, which means that in any 12-month period, we limit repurchases to approximately 20% of the total NAV. See “Net Asset Value Calculation and Valuation Guidelines” for a description of how our aggregate NAV is calculated and “Share Repurchases” for a full description of our share repurchase plan and its limitations.

What kind of offering is this?

We are offering up to $2,750,000,000 in shares of common stock on a best efforts basis. In a best efforts offering, the broker-dealers and other financial representatives participating in the

6

offering are only required to use their best efforts to sell the shares of our common stock and do not have a firm commitment or obligation to purchase any shares. Therefore, we may not sell all or any of the shares we are offering. We are offering up to $2,500,000,000 in shares of our common stock in our primary offering. We are also offering up to $250,000,000 shares of our common stock under our distribution reinvestment plan. We reserve the right to reallocate shares of our common stock being offered between our primary offering and our distribution reinvestment plan.

It is our intent to conduct a continuous public offering for an indefinite period of time, by filing for additional offerings of our shares, subject to regulatory approval and continued compliance with the rules and regulations of the SEC and applicable state laws. We will endeavor to take all reasonable actions to avoid interruptions in the continuous offering of our shares of common stock, including filing an amendment to the registration statement with the SEC on or before such time as the most recent offering price per share represents a 20% change from the per share price set forth in the registration statement as originally declared effective by the SEC or the price per share set forth in the latest amendment thereto filed with the SEC. There can be no assurance, however, that we will not need to suspend our continuous offering while the SEC and, where required, other regulators, review such amendment until it is declared effective, if at all.

For whom may an investment in your shares be appropriate?

An investment in our shares may be appropriate for you if you:

| ● | meet the minimum suitability standards described above under “Suitability Standards;” |

| ● | seek to allocate a portion of your investment portfolio to a direct investment vehicle with an income-oriented portfolio focused on senior loans secured by transitional commercial real estate in the United States; |

| ● | seek to receive current income through regular distribution payments; |

| ● | wish to obtain the potential benefit of long-term capital appreciation; and |

| ● | are able to hold your shares as a long-term investment and do not need liquidity from your investment quickly in the near future. |

We cannot assure you that an investment in our shares will allow you to realize any of these objectives. An investment in our shares is only intended for investors who do not need the ability to sell their shares quickly in the future since the opportunity to have your shares repurchased under our share repurchase plan may not always be available. See “Share Repurchases.”

Who can purchase shares in this offering?

Residents of most states may buy shares of our common stock pursuant to this prospectus if they have either (1) a net worth of at least $250,000 or (2) an annual gross income of at least $70,000 and a net worth of at least $70,000. However, these minimum levels may vary from state to state, so you should carefully read the suitability requirements explained in the “Suitability Standards” section of this prospectus. For this purpose, net worth does not include your home, home furnishings and personal automobiles. Our suitability standards also require that a potential investor: (i) can reasonably benefit from an investment in us based on such investor’s overall investment objectives and portfolio structuring; (ii) is able to bear the economic risk of the investment based on the prospective stockholder’s overall financial situation; and (iii) has apparent understanding of (a) the fundamental risks of the investment, (b) the risk that such investor may lose his or her entire investment, (c) the lack of liquidity of the shares, (d) the background and qualifications of FS Real Estate Advisor and Rialto and (e) the tax consequences of the investment.

7

Our affiliates may also purchase shares of our common stock. The selling commissions and dealer manager fees paid by stockholders may vary in the dealer manager’s discretion. In addition, the dealer manager may waive or reduce selling commissions and/or dealer manager fees in its discretion for any stockholder, including our affiliates.

Is there a minimum initial investment requirement?

Yes. The minimum initial investment for our Class T, Class T-C, Class D and Class M shares is $5,000 and the minimum initial investment for our Class I shares is $1,000,000. Once you have satisfied the minimum initial purchase requirement for any class of our shares, any additional purchases of shares of such class in this offering must be in amounts of at least $500, except for additional purchases pursuant to our distribution reinvestment plan. These minimum investment levels may be higher in certain states, so you should carefully read the more detailed description under “Suitability Standards.”

What are the risks of an investment in your shares?

An investment in our shares involves significant risk. These risks include, among others: (1) there is no public trading market for shares of our common stock and your ability to dispose of your shares will likely be limited to our share repurchase plan; (2) the amount of distributions we make is uncertain, and we may pay distributions from sources such as borrowings or offering proceeds, which means we would have less cash available for investments and your overall returns may be reduced; (3) you will not have the opportunity to evaluate future investments we will make prior to purchasing shares of our common stock; (4) your purchase price will be based on our daily NAV per share, which may change suddenly or may not reflect changes in our NAV that are not immediately quantifiable; and (5) we will pay substantial fees and expenses to our adviser and its affiliates for this offering, which were not negotiated at arm’s length and may be higher than fees payable to unaffiliated third parties. You should read the “Risk Factors” section of this prospectus, which includes a detailed discussion of material risks that you should consider before you invest in the common stock we are selling pursuant to this prospectus.

Are there any special considerations that apply to employee benefit plans subject to ERISA or other retirement plans that are investing in shares?

Yes. The section of this prospectus entitled “Certain ERISA Considerations” describes certain rules that may be relevant in connection with the purchase of shares by retirement plans subject to ERISA or Section 4975 of the Code. Prospective investors that are employee benefit plans or other plans should read that section of the prospectus very carefully.

Will I receive information regarding the performance of my investment?

Yes. We intend to provide you with periodic updates on our performance and your investment in us, including:

| ● | three quarterly financial reports and investor statements; |

| ● | an annual report; |

| ● | in the case of certain U.S. stockholders, an annual IRS Form 1099-DIV or IRS Form 1099-B, if required, and, in the case of non-U.S. stockholders, an annual IRS Form 1042-S; and |

| ● | confirmation statements after transactions affecting your balance, except reinvestment in distributions in our shares and certain transactions through minimum account investment or withdrawal programs. |

We intend to provide this information to you via U.S. mail or other courier. However, with your permission, we may furnish this information to you by electronic delivery, including, with respect

8

to our annual reports, by notice of the posting of our annual reports on our website, which is www.fsinvestments.com. We also intend to include on our website access to our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K, our proxy statements and other filings we make with the SEC. Our website and the information contained at or connected to our website do not constitute a part of this prospectus.

When will I be provided with tax information?

We intend to mail your Form 1099-DIV tax information, if required, by January 31 of each year.

Who can help answer my questions?

If you have more questions about this offering or if you would like additional copies of this prospectus, you should contact your financial representative or the dealer manager at:

FS Investment Solutions, LLC

201 Rouse Boulevard

Philadelphia, PA 19112

(877) 372-9880

Attention: Investor Services

9

This prospectus summary highlights material information contained elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that is important to you. To understand this offering fully, you should read this entire prospectus carefully, including the “Risk Factors” section, before making a decision to invest in our common stock.

Unless otherwise noted, the terms “we,” “us,” “our” and the “Company” refer to FS Credit Real Estate Income Trust, Inc. In addition, the terms “FS Real Estate Advisor” and the “adviser” refer to FS Real Estate Advisor, LLC, the term “FS Investments” refers to Franklin Square Holdings, L.P. and not its affiliates, the terms “Rialto” and the “sub-adviser” refers to Rialto Capital Management, LLC, and the terms “FS Investment Solutions” and the “dealer manager” refer to FS Investment Solutions, LLC.

FS Credit Real Estate Income Trust, Inc.

We are a newly organized corporation formed to originate, acquire and manage a portfolio of primarily senior loans secured by commercial real estate primarily in the United States. We are focused on floating-rate mortgage loans that are secured by first priority mortgages on transitional commercial real estate properties, but we may also invest in other real estate-related assets, including: (i) other commercial real estate mortgage loans, including fixed-rate loans, subordinated loans, B-Notes, mezzanine loans and participations in commercial mortgage loans; and (ii) commercial real estate securities, including CMBS, RMBS, unsecured debt of listed and non-listed REITs, collateralized debt obligations and equity or equity-linked securities. To a lesser extent we may invest in warehouse loans secured by commercial or residential mortgages, credit loans to commercial real estate companies and portfolios of single family home mortgages.

Subject to regulatory approval of our filings for additional public offerings, we intend to sell shares of our common stock to the public on a continuous basis and for an indefinite period of time. In addition, we will sell our shares at a price based on the NAV of our underlying assets, as calculated by our adviser. Although our common stock will not be listed for trading on a stock market or other trading exchange, we provide our investors with limited liquidity through a share repurchase plan whereby, subject to certain limitations, stockholders may request on a daily basis that we repurchase all or any portion of their shares. The repurchase price per share for each class of common stock submitted for repurchase will be equal to the NAV per share for such class on the repurchase date. As a perpetual-life, non-listed REIT, our investment strategy is not restricted by the need to provide, and our charter does not require that we provide our stockholders with, liquidity through a single terminal “liquidity event”. We believe that our portfolio allocation to certain real-estate related securities and other liquid assets will allow us under normal market conditions to satisfy monthly repurchase requests under our share repurchase plan, and therefore enable our stockholders to obtain liquidity for their investment in us as needed.

We will elect to be taxed as a REIT for federal income tax purposes commencing with our first taxable year of operations. We intend to conduct our operations so that we are not required, as such requirements have been interpreted by the SEC staff, to register as an investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

Our office is located at 201 Rouse Boulevard, Philadelphia, PA 19112 and our telephone number is (215) 495-1150. We maintain a toll-free information line at 877-628-8575 where you can obtain the daily determination of our NAV per share for each share class. You may find additional

10

information about us at our website, www.fsinvestments.com. The contents of our website are not incorporated by reference in, and are not otherwise a part of, this prospectus.

Investment Objectives

Our primary investment objectives are to:

| ● | provide current income in the form of regular, stable cash distributions to achieve an attractive dividend yield; |

| ● | preserve and protect invested capital; |

| ● | realize appreciation in NAV from proactive investment management and asset management; and |

| ● | provide an investment alternative for stockholders seeking to allocate a portion of their long-term investment portfolios to commercial real estate debt with lower volatility than public real estate companies. |

Investment Strategy

We plan to achieve our investment objectives by implementing our investment strategy. Our investment strategy is to originate, acquire and manage a portfolio of senior loans secured by commercial real estate primarily in the United States. We are focused on floating-rate mortgage loans that are secured by first priority mortgages on transitional commercial real estate properties. Transitional mortgage loans typically finance the acquisition of commercial properties that require renovation or repositioning before more permanent financing can be obtained. These loans typically have terms of three years or less, with extension options of one to two years tied to achievement of certain milestones by the borrower, and bear interest at floating rates. Transitional mortgage loans often yield more than loans with similar loan-to-value characteristics that are secured by more stabilized real estate properties as well as commercial real estate assets traded in the securitized markets.

In addition to transitional mortgage loans, we may also invest in other real estate-related assets, including: (i) other commercial real estate mortgage loans, including fixed-rate loans, subordinated loans, B-Notes, mezzanine loans and participations in commercial mortgage loans; and (ii) commercial real estate securities, including CMBS, RMBS, unsecured debt of listed and un-listed REITs, collateralized debt obligations and equity or equity-linked securities. To a lesser extent we may invest in warehouse loans secured by commercial or residential mortgages, credit loans to commercial real estate companies and portfolios of single family home mortgages.

Our focus on debt investments will emphasize the payment of current returns to investors and the preservation of invested capital, as well as capital appreciation. We intend to directly structure, underwrite and originate certain of our debt investments in connection with acquisitions, refinancings, and recapitalizations, as this will provide us with the best opportunity to control our borrower and partner relationships and optimize the terms of our investments.

Because most real estate markets are cyclical in nature, we believe that a broadly diversified investment strategy will allow us to more effectively deploy capital into assets where the underlying investment fundamentals are relatively strong and away from those sectors where such fundamentals are relatively weak. We will seek to create and maintain a portfolio of investments that generates a low volatility income stream of attractive and consistent cash distributions by investing across geographic regions in the United States and across property types, including office, lodging, residential, retail, industrial, and health care sectors.

11

Our investment strategy is expected to capitalize on Rialto’s experience, national footprint and origination platform to deploy significant amounts of capital in investments with attractive risk-return profiles. As of March 31, 2017, Rialto’s commercial real estate platform, which has approximately 350 associates in seventeen offices across the U.S. and Europe, has originated over $7.3 billion of commercial mortgage loans since its inception and is one of the largest non-bank underwriters of commercial mortgage loans used in CMBS securitizations. As a standalone separately capitalized subsidiary of Lennar Corporation, Rialto is able to use its vertically integrated platform and experienced underwriting team to provide in-house evaluations of a wide variety of loans and markets. We believe Rialto’s ability to pivot throughout real estate cycles, taking advantage of opportunities with the potential to generate attractive risk-adjusted returns across the capital structure, will be a competitive advantage for us in executing upon our investment strategy.

See the “Investment Objectives and Strategies” section of this prospectus for a more complete description of our investment policies and the investment limitations imposed by our charter.

Our Board of Directors

We will be managed by FS Real Estate Advisor and our executive officers under the direction of our board of directors, the members of which will be accountable to us and our stockholders as fiduciaries. Our board of directors will also set our policies and make major decisions as required under Maryland law. We currently have two directors, neither of whom is independent. Upon commencement of this offering, we will have a seven-member board of directors, a majority of whom will be independent under the provisions of our charter. Our directors will be elected annually by our stockholders.

FS Real Estate Advisor

FS Real Estate Advisor is a subsidiary of FS Investments, a national sponsor of alternative investment funds designed for the individual investor. FS Investments was founded in 2007 and has established itself as a leader in the world of alternative investments. FS Real Estate Advisor is led by substantially the same personnel that form the investment and operations teams of the registered investment advisers that manage FS Investments’ other affiliated registered investment companies and BDCs.

Our president and chief executive officer, Michael C. Forman, has led FS Real Estate Advisor since its inception. In 2007, he co-founded FS Investments with the goal of delivering alternative investment funds, advised by what FS Investments believes to be best-in-class institutional asset managers, to individual investors nationwide. In addition to leading FS Real Estate Advisor, Mr. Forman currently serves as chairman and chief executive officer of the FS Investments’ funds and their affiliated investment advisers.

12

In addition to managing our investments, the managers, officers and other personnel of FS Real Estate Advisor also currently manage the following entities through affiliated investment advisers:

Name | Entity Type | Investment Focus | Gross Assets(1)(2) | |||

FS Energy and Power Fund | BDC | Primarily invests in the debt and income-oriented equity securities of private U.S. companies in the energy and power industry.

| $4,703,929,000 | |||

FS Global Credit Opportunities Fund(3) | Closed-end management investment company | Primarily invests in secured and unsecured floating and fixed rate loans, bonds and other types of credit instruments.

| $1,971,450,000 | |||

FS Investment Corporation | BDC | Primarily invests in senior secured loans, second lien secured loans and, to a lesser extent, subordinated loans of private U.S. companies.

| $4,282,351,000 | |||

FS Investment Corporation II | BDC | Primarily invests in senior secured loans, second lien secured loans and, to a lesser extent, subordinated loans of private U.S. companies.

| $5,219,405,000 | |||

FS Investment Corporation III | BDC | Primarily invests in senior secured loans, second lien secured loans and, to a lesser extent, subordinated loans of private U.S. companies.

| $3,853,370,000 | |||

FS Investment Corporation IV(4) | BDC | Primarily invests in senior secured loans, second lien secured loans and, to a lesser extent, subordinated loans of private U.S. companies. | $255,946,000 | |||

| FS Energy Total Return Fund(5) | Closed-end management investment company | Primarily invests in the equity and debt securities of natural resource companies. | $100,000 | |||

| FS Multi-Strategy Alternatives Fund(6) | Open-end management investment company | Primarily invests in a broad spectrum of alternative investment strategies with low correlation to equity and fixed income markets. | $100,000 | |||

| (1) | As of March 31, 2017 unless otherwise noted. |

| (2) | The advisory fees earned by each of FS Investment Advisor, LLC, FS Global Advisor, LLC, FB Income Advisor, LLC, FSIC II Advisor, LLC, FSIC III Advisor, LLC and FSIC IV Advisor, LLC, the investment advisers to FS Energy and Power Fund, FS Global Credit Opportunities Fund, FS Investment Corporation, FS Investment Corporation II, FS Investment Corporation III and FS Investment Corporation IV, respectively, are based, in part, on the performance of each respective entity. |

| (3) | As of December 31, 2016. Two funds affiliated with FS Global Credit Opportunities Fund: FS Global Credit Opportunities Fund—T and FS Global Credit Opportunities Fund—ADV, (or together, the “FSGCOF Offered Funds”), which have the same investment objectives and strategies as FS Global Credit Opportunities Fund, currently offer common shares of beneficial interest to the public and invest substantially all of the net proceeds of their respective offerings in FS Global Credit Opportunities Fund. Two other funds affiliated with FS Global Credit Opportunities Fund, FS Global Credit Opportunities Fund—A and FS Global Credit Opportunities Fund—D, or together, the FSGCOF Closed Funds, which also have the same investment objectives and strategies as FS Global Credit Opportunities Fund, closed their respective continuous public offerings to new investors in April 2016. |

| (4) | FS Investment Corporation IV commenced investment operations on January 6, 2016. |

| (5) | FS Energy Total Return Fund commenced operations on March 15, 2017. Gross assets are as of October 31, 2016. |

| (6) | FS Multi-Strategy Alternatives Fund commenced investment operations on May 15, 2017. |

13