Exhibit 99.2 ALTUS MIDSTREAM COMPANY Combination with BCP Raptor Holdco LP October 21, 2021 Nasdaq: ALTMExhibit 99.2 ALTUS MIDSTREAM COMPANY Combination with BCP Raptor Holdco LP October 21, 2021 Nasdaq: ALTM

Disclaimer FORWARD LOOKING STATEMENTS The information in this presentation and the oral statements made in connection therewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included in this presentation, including, without limitation, statements regarding Altus Midstream Company’s (“Altus Midstream”) business, operations, strategy, prospects, plans, estimated financial and operating results, and future financial and operating performance and forecasts, as well as similar information about Apache Corporation (“Apache”), Altus Midstream's ability to effect the transactions described herein and the expected benefits of such transactions, and future plans, expectations, and objectives for the post-combination company's operations after completion of such transactions, are forward-looking statements. When used in this presentation, including any oral statements made in connection therewith, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “prospect,” “plan,” “continue,” “seek,” “guidance,” “might,” “outlook,” “possibly,” “potential,” “would,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current expectations and assumptions about future events that Altus Midstream believes to be reasonable under the circumstances and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, Altus Midstream and Apache disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. Altus Midstream and Apache caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of Altus Midstream and Apache, incident to the development, production, gathering, transportation and sale of oil, natural gas and natural gas liquids. These risks include, but are not limited to, commodity price volatility, low prices for oil and/or natural gas, global economic conditions, uncertainties inherent in the joint venture pipelines referred to herein, inflation, increased operating costs, construction delays and cost over-runs, lack of availability of equipment, supplies, services and qualified personnel, processing volumes and pipeline throughput, uncertainties related to new technologies, geographical concentration of operations, environmental risks, weather risks, security risks, drilling and other operating risks, regulatory changes, regulatory risks (including if Altus Midstream were to become an investment company in the future), the uncertainty inherent in estimating oil and natural gas reserves and in projecting future rates of production, reductions in cash flow, lack of access to capital, Altus Midstream’s ability to satisfy future cash obligations, restrictions in existing or future debt agreements or structured or other financing arrangements, the timing of development expenditures, managing growth and integration of acquisitions, failure to realize expected value creation from acquisitions, and the scope, duration, and reoccurrence of any epidemics or pandemics (including specifically the coronavirus disease 2019 (COVID-19) pandemic) and the actions taken by third parties, including, but not limited to, governmental authorities, customers, contractors, and suppliers, in response to such epidemics or pandemics. Should one or more of the risks or uncertainties described in this presentation and the oral statements made in connection therewith occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements. Additional information concerning these and other factors that may impact Altus Midstream’s operations and projections can be found in its periodic filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2020, and subsequently filed Quarterly Reports on Form 10-Q. Altus Midstream’ SEC filings are available publicly on the SEC’s website at www.sec.gov. INFORMATION ABOUT ALPINE HIGH Information in this presentation about Alpine High, including the reserve and production information set forth within, has been provided by, and is the responsibility of, Apache. Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by reserve engineers. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered. USE OF PROJECTIONS This presentation contains projections for Altus Midstream, including with respect to Altus Midstream’s gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage. Altus Midstream’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, have not expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. These projections are for illustrative purposes only, should not be relied upon as being necessarily indicative of future results, and are subject to the disclaimers under “Forward Looking Statements” above. USE OF NON-GAAP FINANCIAL MEASURES This presentation includes non-GAAP financial measures, including gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage. Altus Midstream believes these non-GAAP measures are useful because they allow Altus Midstream to more effectively evaluate its operating performance and compare the results of its operations from period to period and against its peers without regard to financing methods or capital structure. Altus Midstream does not consider these non-GAAP measures in isolation or as an alternative to similar financial measures determined in accordance with GAAP. The computations of gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage may not be comparable to other similarly titled measures of other companies. Altus Midstream excludes certain items from net (loss) income in arriving at Adjusted EBITDA and distributable cash flow because these amounts can vary substantially from company to company within its industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA and distributable cash flow should not be considered an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as indicators of operating performance. Certain items excluded from Adjusted EBITDA and distributable cash flow are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of Adjusted EBITDA or distributable cash flow. Altus Midstream’s presentation of gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage should not be construed as an inference that its results will be unaffected by unusual or non-recurring terms. ADDITIONAL INFORMATION AND WHERE TO FIND IT In connection with the proposed transaction, Altus Midstream intends to file a proxy statement and other materials with the Securities and Exchange Commission (“SEC”). In addition, Altus Midstream may file other relevant documents with the SEC regarding the proposed transaction. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and stockholders may obtain a free copy of the proxy statement (if and when it becomes available) and other documents filed by Altus Midstream with the SEC at Altus Midstream’s website https://www.altusmidstream.com, or at the SEC’s website, www.sec.gov. The proxy statement and other relevant documents may also be obtained for free from Altus by directing such request to Altus, to the attention of Corporate Secretary, One Post Oak Central, 2000 Post Oak Boulevard, Suite 100, Houston, Texas 77056. PARTICIPANTS IN THE SOLICITATION Altus Midstream and its directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from Altus Midstream’s stockholders in connection with the proposed transaction. Investors and stockholders may obtain more detailed information regarding the names, affiliations and interests of Altus Midstream’s directors and executive officers by reading Altus Midstream’s definitive proxy statement on Schedule 14A, which was filed with the SEC on April 23, 2021. Additional information regarding potential participants in such proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the proxy statement and other relevant materials filed with the SEC in connection with the proposed transaction when they become available. Investors and stockholders should read the proxy statement carefully when it becomes available before making any voting or investment decisions. Investors and stockholders may obtain free copies of these documents from Altus Midstream using the sources indicated above. 2Disclaimer FORWARD LOOKING STATEMENTS The information in this presentation and the oral statements made in connection therewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included in this presentation, including, without limitation, statements regarding Altus Midstream Company’s (“Altus Midstream”) business, operations, strategy, prospects, plans, estimated financial and operating results, and future financial and operating performance and forecasts, as well as similar information about Apache Corporation (“Apache”), Altus Midstream's ability to effect the transactions described herein and the expected benefits of such transactions, and future plans, expectations, and objectives for the post-combination company's operations after completion of such transactions, are forward-looking statements. When used in this presentation, including any oral statements made in connection therewith, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “prospect,” “plan,” “continue,” “seek,” “guidance,” “might,” “outlook,” “possibly,” “potential,” “would,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current expectations and assumptions about future events that Altus Midstream believes to be reasonable under the circumstances and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, Altus Midstream and Apache disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. Altus Midstream and Apache caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of Altus Midstream and Apache, incident to the development, production, gathering, transportation and sale of oil, natural gas and natural gas liquids. These risks include, but are not limited to, commodity price volatility, low prices for oil and/or natural gas, global economic conditions, uncertainties inherent in the joint venture pipelines referred to herein, inflation, increased operating costs, construction delays and cost over-runs, lack of availability of equipment, supplies, services and qualified personnel, processing volumes and pipeline throughput, uncertainties related to new technologies, geographical concentration of operations, environmental risks, weather risks, security risks, drilling and other operating risks, regulatory changes, regulatory risks (including if Altus Midstream were to become an investment company in the future), the uncertainty inherent in estimating oil and natural gas reserves and in projecting future rates of production, reductions in cash flow, lack of access to capital, Altus Midstream’s ability to satisfy future cash obligations, restrictions in existing or future debt agreements or structured or other financing arrangements, the timing of development expenditures, managing growth and integration of acquisitions, failure to realize expected value creation from acquisitions, and the scope, duration, and reoccurrence of any epidemics or pandemics (including specifically the coronavirus disease 2019 (COVID-19) pandemic) and the actions taken by third parties, including, but not limited to, governmental authorities, customers, contractors, and suppliers, in response to such epidemics or pandemics. Should one or more of the risks or uncertainties described in this presentation and the oral statements made in connection therewith occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements. Additional information concerning these and other factors that may impact Altus Midstream’s operations and projections can be found in its periodic filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2020, and subsequently filed Quarterly Reports on Form 10-Q. Altus Midstream’ SEC filings are available publicly on the SEC’s website at www.sec.gov. INFORMATION ABOUT ALPINE HIGH Information in this presentation about Alpine High, including the reserve and production information set forth within, has been provided by, and is the responsibility of, Apache. Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by reserve engineers. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered. USE OF PROJECTIONS This presentation contains projections for Altus Midstream, including with respect to Altus Midstream’s gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage. Altus Midstream’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, have not expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. These projections are for illustrative purposes only, should not be relied upon as being necessarily indicative of future results, and are subject to the disclaimers under “Forward Looking Statements” above. USE OF NON-GAAP FINANCIAL MEASURES This presentation includes non-GAAP financial measures, including gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage. Altus Midstream believes these non-GAAP measures are useful because they allow Altus Midstream to more effectively evaluate its operating performance and compare the results of its operations from period to period and against its peers without regard to financing methods or capital structure. Altus Midstream does not consider these non-GAAP measures in isolation or as an alternative to similar financial measures determined in accordance with GAAP. The computations of gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage may not be comparable to other similarly titled measures of other companies. Altus Midstream excludes certain items from net (loss) income in arriving at Adjusted EBITDA and distributable cash flow because these amounts can vary substantially from company to company within its industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA and distributable cash flow should not be considered an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as indicators of operating performance. Certain items excluded from Adjusted EBITDA and distributable cash flow are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of Adjusted EBITDA or distributable cash flow. Altus Midstream’s presentation of gross profit, adjusted EBITDA, net cash flows provided by operating activities, capital investment, growth capital investments, distributable cash flow, free cash flow, net debt, leverage, distribution coverage should not be construed as an inference that its results will be unaffected by unusual or non-recurring terms. ADDITIONAL INFORMATION AND WHERE TO FIND IT In connection with the proposed transaction, Altus Midstream intends to file a proxy statement and other materials with the Securities and Exchange Commission (“SEC”). In addition, Altus Midstream may file other relevant documents with the SEC regarding the proposed transaction. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and stockholders may obtain a free copy of the proxy statement (if and when it becomes available) and other documents filed by Altus Midstream with the SEC at Altus Midstream’s website https://www.altusmidstream.com, or at the SEC’s website, www.sec.gov. The proxy statement and other relevant documents may also be obtained for free from Altus by directing such request to Altus, to the attention of Corporate Secretary, One Post Oak Central, 2000 Post Oak Boulevard, Suite 100, Houston, Texas 77056. PARTICIPANTS IN THE SOLICITATION Altus Midstream and its directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from Altus Midstream’s stockholders in connection with the proposed transaction. Investors and stockholders may obtain more detailed information regarding the names, affiliations and interests of Altus Midstream’s directors and executive officers by reading Altus Midstream’s definitive proxy statement on Schedule 14A, which was filed with the SEC on April 23, 2021. Additional information regarding potential participants in such proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the proxy statement and other relevant materials filed with the SEC in connection with the proposed transaction when they become available. Investors and stockholders should read the proxy statement carefully when it becomes available before making any voting or investment decisions. Investors and stockholders may obtain free copies of these documents from Altus Midstream using the sources indicated above. 2

Transaction Highlights ► All-stock combination creating an unparalleled, fully-integrated Delaware Basin midstream company • 50 million ALTM Class C shares to be issued to BCP Raptor Holdco LP (“BCP”) Unitholders • Ownership ~50% Blackstone, >20% I Squared Capital, ~20% Apache and >5% Public / Management • BCP leadership team (Jamie Welch, CEO) to operate and manage the pro forma Company • Pro forma company will adopt a new name at closing ► BCP is the parent of EagleClaw Midstream comprising EagleClaw Midstream Ventures, the Caprock and Pinnacle Midstream businesses and a 26.7% interest in Kinder Morgan’s Permian Highway Pipeline (1) ► Committed to maintaining $6.00 per share dividend through 2023 • 100% cash for Class A common shareholders (1) • Targeting at least 5% annual growth thereafter • Dividend reinvestment program to be implemented post closing and available to all shareholders • Class C shareholders have committed 20% or more of their dividends to DRIP through 2023 (2) ► Estimated 2022 Adjusted EBITDA of $800MM to $850MM • Approximately 35% pipeline transportation / 65% gathering and processing • Anticipate $50MM of annual EBITDA synergies by year-end 2023 ► Minimal future growth capital needs results in high free cash flow conversion • Interconnected midstream systems generate >$175MM of capital savings over the next five years ► Targeted close in 1Q22, subject to regulatory and Altus shareholder approvals • Apache has entered into a voting and support agreement to vote in favor of the transaction • Redeeming over 15% of Series A Preferred at closing with cash on hand • Debt refinancing expected in 1Q22 with strong BB ratings profile ► Apache is evaluating a new Alpine High development program beginning in 2022 given current attractive economics 3 (1) Subject to Board approval. (2) Includes run-rate EBITDA synergies.Transaction Highlights ► All-stock combination creating an unparalleled, fully-integrated Delaware Basin midstream company • 50 million ALTM Class C shares to be issued to BCP Raptor Holdco LP (“BCP”) Unitholders • Ownership ~50% Blackstone, >20% I Squared Capital, ~20% Apache and >5% Public / Management • BCP leadership team (Jamie Welch, CEO) to operate and manage the pro forma Company • Pro forma company will adopt a new name at closing ► BCP is the parent of EagleClaw Midstream comprising EagleClaw Midstream Ventures, the Caprock and Pinnacle Midstream businesses and a 26.7% interest in Kinder Morgan’s Permian Highway Pipeline (1) ► Committed to maintaining $6.00 per share dividend through 2023 • 100% cash for Class A common shareholders (1) • Targeting at least 5% annual growth thereafter • Dividend reinvestment program to be implemented post closing and available to all shareholders • Class C shareholders have committed 20% or more of their dividends to DRIP through 2023 (2) ► Estimated 2022 Adjusted EBITDA of $800MM to $850MM • Approximately 35% pipeline transportation / 65% gathering and processing • Anticipate $50MM of annual EBITDA synergies by year-end 2023 ► Minimal future growth capital needs results in high free cash flow conversion • Interconnected midstream systems generate >$175MM of capital savings over the next five years ► Targeted close in 1Q22, subject to regulatory and Altus shareholder approvals • Apache has entered into a voting and support agreement to vote in favor of the transaction • Redeeming over 15% of Series A Preferred at closing with cash on hand • Debt refinancing expected in 1Q22 with strong BB ratings profile ► Apache is evaluating a new Alpine High development program beginning in 2022 given current attractive economics 3 (1) Subject to Board approval. (2) Includes run-rate EBITDA synergies.

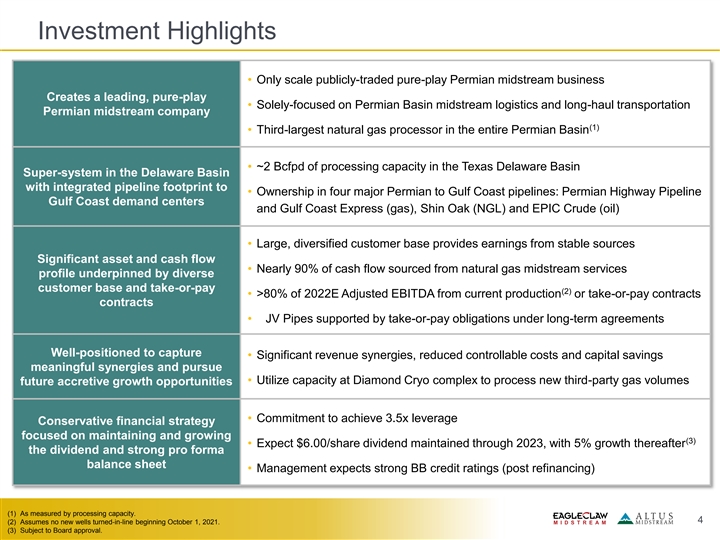

Investment Highlights • Only scale publicly-traded pure-play Permian midstream business Creates a leading, pure-play • Solely-focused on Permian Basin midstream logistics and long-haul transportation Permian midstream company (1) • Third-largest natural gas processor in the entire Permian Basin • ~2 Bcfpd of processing capacity in the Texas Delaware Basin Super-system in the Delaware Basin with integrated pipeline footprint to • Ownership in four major Permian to Gulf Coast pipelines: Permian Highway Pipeline Gulf Coast demand centers and Gulf Coast Express (gas), Shin Oak (NGL) and EPIC Crude (oil) • Large, diversified customer base provides earnings from stable sources Significant asset and cash flow • Nearly 90% of cash flow sourced from natural gas midstream services profile underpinned by diverse customer base and take-or-pay (2) • >80% of 2022E Adjusted EBITDA from current production or take-or-pay contracts contracts • JV Pipes supported by take-or-pay obligations under long-term agreements Well-positioned to capture • Significant revenue synergies, reduced controllable costs and capital savings meaningful synergies and pursue • Utilize capacity at Diamond Cryo complex to process new third-party gas volumes future accretive growth opportunities • Commitment to achieve 3.5x leverage Conservative financial strategy focused on maintaining and growing (3) • Expect $6.00/share dividend maintained through 2023, with 5% growth thereafter the dividend and strong pro forma balance sheet • Management expects strong BB credit ratings (post refinancing) (1) As measured by processing capacity. 4 (2) Assumes no new wells turned-in-line beginning October 1, 2021. (3) Subject to Board approval.Investment Highlights • Only scale publicly-traded pure-play Permian midstream business Creates a leading, pure-play • Solely-focused on Permian Basin midstream logistics and long-haul transportation Permian midstream company (1) • Third-largest natural gas processor in the entire Permian Basin • ~2 Bcfpd of processing capacity in the Texas Delaware Basin Super-system in the Delaware Basin with integrated pipeline footprint to • Ownership in four major Permian to Gulf Coast pipelines: Permian Highway Pipeline Gulf Coast demand centers and Gulf Coast Express (gas), Shin Oak (NGL) and EPIC Crude (oil) • Large, diversified customer base provides earnings from stable sources Significant asset and cash flow • Nearly 90% of cash flow sourced from natural gas midstream services profile underpinned by diverse customer base and take-or-pay (2) • >80% of 2022E Adjusted EBITDA from current production or take-or-pay contracts contracts • JV Pipes supported by take-or-pay obligations under long-term agreements Well-positioned to capture • Significant revenue synergies, reduced controllable costs and capital savings meaningful synergies and pursue • Utilize capacity at Diamond Cryo complex to process new third-party gas volumes future accretive growth opportunities • Commitment to achieve 3.5x leverage Conservative financial strategy focused on maintaining and growing (3) • Expect $6.00/share dividend maintained through 2023, with 5% growth thereafter the dividend and strong pro forma balance sheet • Management expects strong BB credit ratings (post refinancing) (1) As measured by processing capacity. 4 (2) Assumes no new wells turned-in-line beginning October 1, 2021. (3) Subject to Board approval.

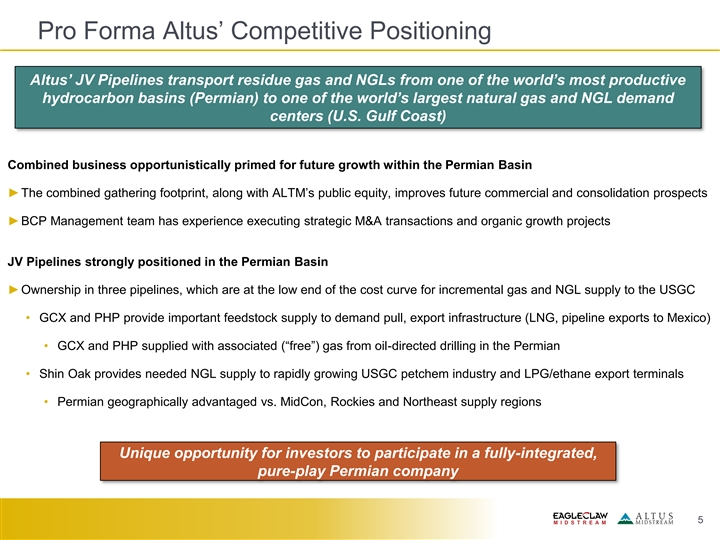

Pro Forma Altus’ Competitive Positioning Altus’ JV Pipelines transport residue gas and NGLs from one of the world’s most productive hydrocarbon basins (Permian) to one of the world’s largest natural gas and NGL demand centers (U.S. Gulf Coast) Combined business opportunistically primed for future growth within the Permian Basin ►The combined gathering footprint, along with ALTM’s public equity, improves future commercial and consolidation prospects ►BCP Management team has experience executing strategic M&A transactions and organic growth projects JV Pipelines strongly positioned in the Permian Basin ►Ownership in three pipelines, which are at the low end of the cost curve for incremental gas and NGL supply to the USGC • GCX and PHP provide important feedstock supply to demand pull, export infrastructure (LNG, pipeline exports to Mexico) • GCX and PHP supplied with associated (“free”) gas from oil-directed drilling in the Permian • Shin Oak provides needed NGL supply to rapidly growing USGC petchem industry and LPG/ethane export terminals • Permian geographically advantaged vs. MidCon, Rockies and Northeast supply regions Unique opportunity for investors to participate in a fully-integrated, pure-play Permian company 5Pro Forma Altus’ Competitive Positioning Altus’ JV Pipelines transport residue gas and NGLs from one of the world’s most productive hydrocarbon basins (Permian) to one of the world’s largest natural gas and NGL demand centers (U.S. Gulf Coast) Combined business opportunistically primed for future growth within the Permian Basin ►The combined gathering footprint, along with ALTM’s public equity, improves future commercial and consolidation prospects ►BCP Management team has experience executing strategic M&A transactions and organic growth projects JV Pipelines strongly positioned in the Permian Basin ►Ownership in three pipelines, which are at the low end of the cost curve for incremental gas and NGL supply to the USGC • GCX and PHP provide important feedstock supply to demand pull, export infrastructure (LNG, pipeline exports to Mexico) • GCX and PHP supplied with associated (“free”) gas from oil-directed drilling in the Permian • Shin Oak provides needed NGL supply to rapidly growing USGC petchem industry and LPG/ethane export terminals • Permian geographically advantaged vs. MidCon, Rockies and Northeast supply regions Unique opportunity for investors to participate in a fully-integrated, pure-play Permian company 5

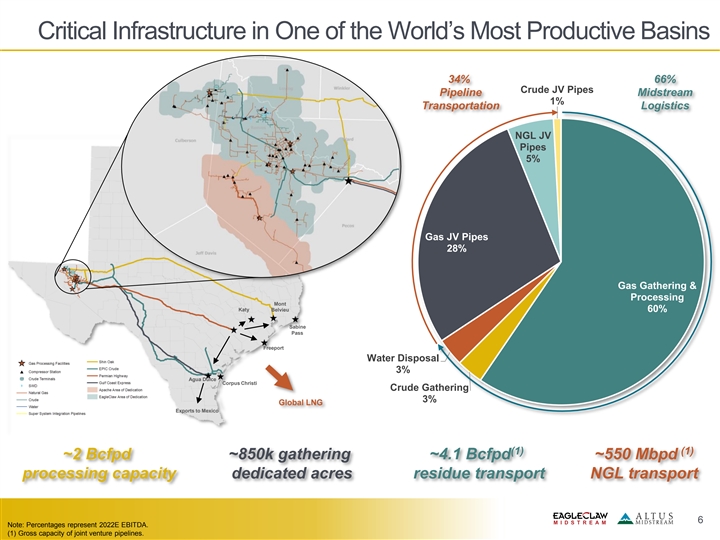

Critical Infrastructure in One of the World’s Most Productive Basins 34% 66% Crude JV Pipes Pipeline Midstream 1% Transportation Logistics NGL JV Pipes 5% Gas JV Pipes 28% Gas Gathering & Processing Mont Katy Belvieu 60% Sabine Pass Freeport Water Disposal 3% Agua Dulce Corpus Christi Crude Gathering 3% Global LNG Exports to Mexico (1) (1) ~2 Bcfpd ~850k gathering ~4.1 Bcfpd ~550 Mbpd processing capacity dedicated acres residue transport NGL transport 6 Note: Percentages represent 2022E EBITDA. (1) Gross capacity of joint venture pipelines. Critical Infrastructure in One of the World’s Most Productive Basins 34% 66% Crude JV Pipes Pipeline Midstream 1% Transportation Logistics NGL JV Pipes 5% Gas JV Pipes 28% Gas Gathering & Processing Mont Katy Belvieu 60% Sabine Pass Freeport Water Disposal 3% Agua Dulce Corpus Christi Crude Gathering 3% Global LNG Exports to Mexico (1) (1) ~2 Bcfpd ~850k gathering ~4.1 Bcfpd ~550 Mbpd processing capacity dedicated acres residue transport NGL transport 6 Note: Percentages represent 2022E EBITDA. (1) Gross capacity of joint venture pipelines.

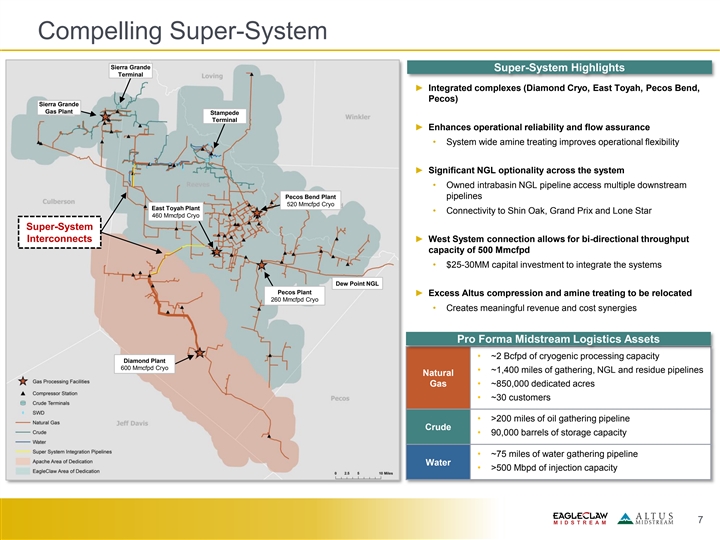

Compelling Super-System Sierra Grande Super-System Highlights Terminal ► Integrated complexes (Diamond Cryo, East Toyah, Pecos Bend, Pecos) Sierra Grande Gas Plant Stampede Terminal ► Enhances operational reliability and flow assurance • System wide amine treating improves operational flexibility ► Significant NGL optionality across the system • Owned intrabasin NGL pipeline access multiple downstream Pecos Bend Plant pipelines 520 Mmcfpd Cryo East Toyah Plant • Connectivity to Shin Oak, Grand Prix and Lone Star 460 Mmcfpd Cryo Super-System Interconnects ► West System connection allows for bi-directional throughput capacity of 500 Mmcfpd • $25-30MM capital investment to integrate the systems Dew Point NGL Pecos Plant ► Excess Altus compression and amine treating to be relocated 260 Mmcfpd Cryo • Creates meaningful revenue and cost synergies Pro Forma Midstream Logistics Assets • ~2 Bcfpd of cryogenic processing capacity Diamond Plant 600 Mmcfpd Cryo • ~1,400 miles of gathering, NGL and residue pipelines Natural Gas • ~850,000 dedicated acres • ~30 customers • >200 miles of oil gathering pipeline Crude • 90,000 barrels of storage capacity • ~75 miles of water gathering pipeline Water • >500 Mbpd of injection capacity 7Compelling Super-System Sierra Grande Super-System Highlights Terminal ► Integrated complexes (Diamond Cryo, East Toyah, Pecos Bend, Pecos) Sierra Grande Gas Plant Stampede Terminal ► Enhances operational reliability and flow assurance • System wide amine treating improves operational flexibility ► Significant NGL optionality across the system • Owned intrabasin NGL pipeline access multiple downstream Pecos Bend Plant pipelines 520 Mmcfpd Cryo East Toyah Plant • Connectivity to Shin Oak, Grand Prix and Lone Star 460 Mmcfpd Cryo Super-System Interconnects ► West System connection allows for bi-directional throughput capacity of 500 Mmcfpd • $25-30MM capital investment to integrate the systems Dew Point NGL Pecos Plant ► Excess Altus compression and amine treating to be relocated 260 Mmcfpd Cryo • Creates meaningful revenue and cost synergies Pro Forma Midstream Logistics Assets • ~2 Bcfpd of cryogenic processing capacity Diamond Plant 600 Mmcfpd Cryo • ~1,400 miles of gathering, NGL and residue pipelines Natural Gas • ~850,000 dedicated acres • ~30 customers • >200 miles of oil gathering pipeline Crude • 90,000 barrels of storage capacity • ~75 miles of water gathering pipeline Water • >500 Mbpd of injection capacity 7

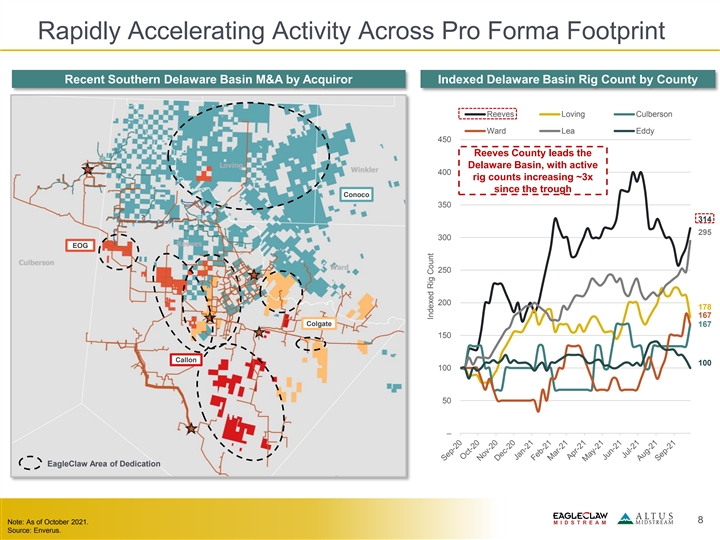

Rapidly Accelerating Activity Across Pro Forma Footprint Recent Southern Delaware Basin M&A by Acquiror Indexed Delaware Basin Rig Count by County Reeves Loving Culberson Ward Lea Eddy 450 Reeves County leads the Delaware Basin, with active 400 rig counts increasing ~3x since the trough Conoco 350 314 295 300 EOG 250 200 178 167 Colgate 167 150 Callon 100 100 50 – EagleClaw Area of Dedication 8 Note: As of October 2021. Source: Enverus. Indexed Rig CountRapidly Accelerating Activity Across Pro Forma Footprint Recent Southern Delaware Basin M&A by Acquiror Indexed Delaware Basin Rig Count by County Reeves Loving Culberson Ward Lea Eddy 450 Reeves County leads the Delaware Basin, with active 400 rig counts increasing ~3x since the trough Conoco 350 314 295 300 EOG 250 200 178 167 Colgate 167 150 Callon 100 100 50 – EagleClaw Area of Dedication 8 Note: As of October 2021. Source: Enverus. Indexed Rig Count

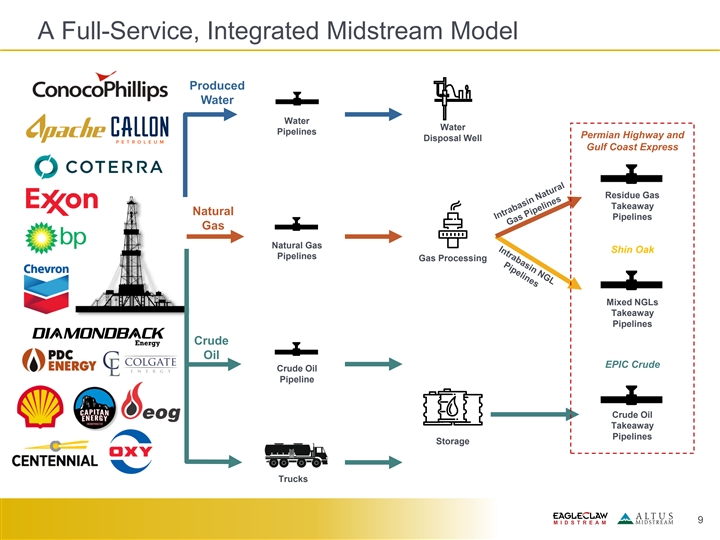

A Full-Service, Integrated Midstream Model Produced Water Water Water Pipelines Permian Highway and Disposal Well Gulf Coast Express Residue Gas Takeaway Natural Pipelines Gas Natural Gas Shin Oak Pipelines Gas Processing Mixed NGLs Takeaway Pipelines Crude Oil EPIC Crude Crude Oil Pipeline Crude Oil Takeaway Pipelines Storage Trucks 9A Full-Service, Integrated Midstream Model Produced Water Water Water Pipelines Permian Highway and Disposal Well Gulf Coast Express Residue Gas Takeaway Natural Pipelines Gas Natural Gas Shin Oak Pipelines Gas Processing Mixed NGLs Takeaway Pipelines Crude Oil EPIC Crude Crude Oil Pipeline Crude Oil Takeaway Pipelines Storage Trucks 9

Pro Forma Organizational Structure (Prior to Refinancing) Public Investors (1) Altus Midstream (ALTM) $661MM $800MM Altus Midstream LP Series A Credit Facility (2) Preferred 100% interest 100% interest Midstream Logistics Pipeline Transportation 100% interest 100% interest 100% interest 100% interest 16% interest 53% interest 33% interest 15% interest Alpine High BCP Raptor I Gulf Coast Permian BCP Raptor II Delaware Link Shin Oak NGL EPIC Crude (EagleClaw + Gathering and Express Highway (Caprock G&P) Pipeline Pipeline Pipeline Pinnacle G&P) (3) Processing Pipeline Pipeline $125MM $60MM ~$490MM Super Senior Super Senior Senior Term (4) Credit Facility Credit Facility Loan A ~$1.18Bn ~$640MM Senior Term Senior Term Prior to a refinancing, additional dividend cash flow benefit from BCP PHP, BCP Raptor II and tangible synergies (4) (4) Loan B Loan B • Loans at BCP’s operating subsidiaries present no crossover or upstream risks / claims to ALTM • Blackstone, I Squared and Apache will reinvest in new shares for at least 20% of their dividends through 2023, which ensures cash dividends to Class A common stock and accelerated redemption of the Series A preferred (1) Blackstone, Apache and I Squared each hold common units in Altus Midstream LP and Class C shares in ALTM that can together be redeemed for Class A Shares in ALTM. (2) Reflects 660,694 units outstanding as of June 30, 2021 at the original issuance price. 10 (3) BCP Raptor’s 26.7% ownership interest in PHP is subject to a project finance Term Loan A facility. (4) As of September 30, 2021.Pro Forma Organizational Structure (Prior to Refinancing) Public Investors (1) Altus Midstream (ALTM) $661MM $800MM Altus Midstream LP Series A Credit Facility (2) Preferred 100% interest 100% interest Midstream Logistics Pipeline Transportation 100% interest 100% interest 100% interest 100% interest 16% interest 53% interest 33% interest 15% interest Alpine High BCP Raptor I Gulf Coast Permian BCP Raptor II Delaware Link Shin Oak NGL EPIC Crude (EagleClaw + Gathering and Express Highway (Caprock G&P) Pipeline Pipeline Pipeline Pinnacle G&P) (3) Processing Pipeline Pipeline $125MM $60MM ~$490MM Super Senior Super Senior Senior Term (4) Credit Facility Credit Facility Loan A ~$1.18Bn ~$640MM Senior Term Senior Term Prior to a refinancing, additional dividend cash flow benefit from BCP PHP, BCP Raptor II and tangible synergies (4) (4) Loan B Loan B • Loans at BCP’s operating subsidiaries present no crossover or upstream risks / claims to ALTM • Blackstone, I Squared and Apache will reinvest in new shares for at least 20% of their dividends through 2023, which ensures cash dividends to Class A common stock and accelerated redemption of the Series A preferred (1) Blackstone, Apache and I Squared each hold common units in Altus Midstream LP and Class C shares in ALTM that can together be redeemed for Class A Shares in ALTM. (2) Reflects 660,694 units outstanding as of June 30, 2021 at the original issuance price. 10 (3) BCP Raptor’s 26.7% ownership interest in PHP is subject to a project finance Term Loan A facility. (4) As of September 30, 2021.

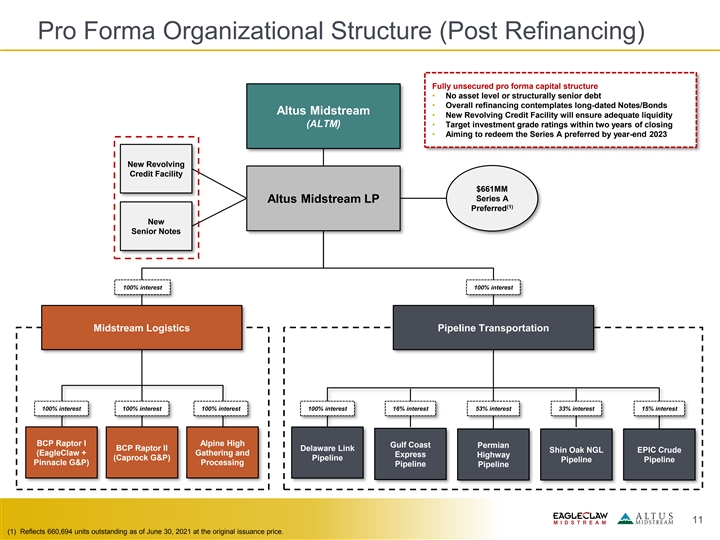

Pro Forma Organizational Structure (Post Refinancing) Fully unsecured pro forma capital structure • No asset level or structurally senior debt • Overall refinancing contemplates long-dated Notes/Bonds Altus Midstream • New Revolving Credit Facility will ensure adequate liquidity (ALTM) • Target investment grade ratings within two years of closing • Aiming to redeem the Series A preferred by year-end 2023 New Revolving Credit Facility $661MM Series A Altus Midstream LP (1) Preferred New Senior Notes 100% interest 100% interest Midstream Logistics Pipeline Transportation 100% interest 100% interest 100% interest 100% interest 16% interest 53% interest 33% interest 15% interest BCP Raptor I Alpine High Gulf Coast Permian BCP Raptor II Delaware Link Shin Oak NGL EPIC Crude (EagleClaw + Gathering and Express Highway (Caprock G&P) Pipeline Pipeline Pipeline Pinnacle G&P) Processing Pipeline Pipeline 11 (1) Reflects 660,694 units outstanding as of June 30, 2021 at the original issuance price.Pro Forma Organizational Structure (Post Refinancing) Fully unsecured pro forma capital structure • No asset level or structurally senior debt • Overall refinancing contemplates long-dated Notes/Bonds Altus Midstream • New Revolving Credit Facility will ensure adequate liquidity (ALTM) • Target investment grade ratings within two years of closing • Aiming to redeem the Series A preferred by year-end 2023 New Revolving Credit Facility $661MM Series A Altus Midstream LP (1) Preferred New Senior Notes 100% interest 100% interest Midstream Logistics Pipeline Transportation 100% interest 100% interest 100% interest 100% interest 16% interest 53% interest 33% interest 15% interest BCP Raptor I Alpine High Gulf Coast Permian BCP Raptor II Delaware Link Shin Oak NGL EPIC Crude (EagleClaw + Gathering and Express Highway (Caprock G&P) Pipeline Pipeline Pipeline Pinnacle G&P) Processing Pipeline Pipeline 11 (1) Reflects 660,694 units outstanding as of June 30, 2021 at the original issuance price.

Overview of BCP Raptor Holdco 12Overview of BCP Raptor Holdco 12

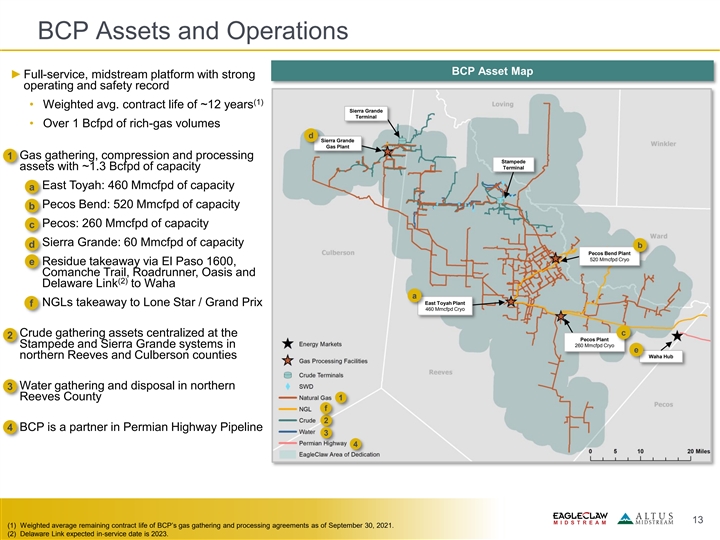

BCP Assets and Operations BCP Asset Map ►Full-service, midstream platform with strong operating and safety record (1) • Weighted avg. contract life of ~12 years Sierra Grande Terminal • Over 1 Bcfpd of rich-gas volumes d Sierra Grande Gas Plant 1• Gas gathering, compression and processing Stampede assets with ~1.3 Bcfpd of capacity Terminal > East Toyah: 460 Mmcfpd of capacity a > Pecos Bend: 520 Mmcfpd of capacity b > Pecos: 260 Mmcfpd of capacity c > Sierra Grande: 60 Mmcfpd of capacity d b Pecos Bend Plant 520 Mmcfpd Cryo e> Residue takeaway via El Paso 1600, Comanche Trail, Roadrunner, Oasis and (2) Delaware Link to Waha a East Toyah Plant > NGLs takeaway to Lone Star / Grand Prix f 460 Mmcfpd Cryo c • Crude gathering assets centralized at the 2 Pecos Plant 260 Mmcfpd Cryo Stampede and Sierra Grande systems in e Waha Hub northern Reeves and Culberson counties 3• Water gathering and disposal in northern Reeves County 1 f 2 4• BCP is a partner in Permian Highway Pipeline 3 4 13 (1) Weighted average remaining contract life of BCP’s gas gathering and processing agreements as of September 30, 2021. (2) Delaware Link expected in-service date is 2023.BCP Assets and Operations BCP Asset Map ►Full-service, midstream platform with strong operating and safety record (1) • Weighted avg. contract life of ~12 years Sierra Grande Terminal • Over 1 Bcfpd of rich-gas volumes d Sierra Grande Gas Plant 1• Gas gathering, compression and processing Stampede assets with ~1.3 Bcfpd of capacity Terminal > East Toyah: 460 Mmcfpd of capacity a > Pecos Bend: 520 Mmcfpd of capacity b > Pecos: 260 Mmcfpd of capacity c > Sierra Grande: 60 Mmcfpd of capacity d b Pecos Bend Plant 520 Mmcfpd Cryo e> Residue takeaway via El Paso 1600, Comanche Trail, Roadrunner, Oasis and (2) Delaware Link to Waha a East Toyah Plant > NGLs takeaway to Lone Star / Grand Prix f 460 Mmcfpd Cryo c • Crude gathering assets centralized at the 2 Pecos Plant 260 Mmcfpd Cryo Stampede and Sierra Grande systems in e Waha Hub northern Reeves and Culberson counties 3• Water gathering and disposal in northern Reeves County 1 f 2 4• BCP is a partner in Permian Highway Pipeline 3 4 13 (1) Weighted average remaining contract life of BCP’s gas gathering and processing agreements as of September 30, 2021. (2) Delaware Link expected in-service date is 2023.

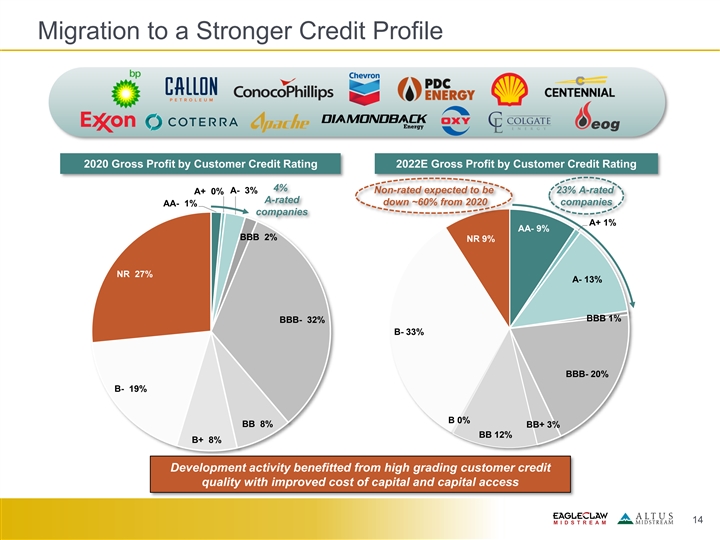

Migration to a Stronger Credit Profile 2020 Gross Profit by Customer Credit Rating 2022E Gross Profit by Customer Credit Rating 4% Non-rated expected to be 23% A-rated A+ 0% A- 3% A-rated down ~60% from 2020 companies AA- 1% companies A+ 1% AA- 9% BBB 2% NR 9% NR 27% A- 13% BBB 1% BBB- 32% B- 33% BBB- 20% B- 19% B 0% BB 8% BB+ 3% BB 12% B+ 8% Development activity benefitted from high grading customer credit quality with improved cost of capital and capital access 14Migration to a Stronger Credit Profile 2020 Gross Profit by Customer Credit Rating 2022E Gross Profit by Customer Credit Rating 4% Non-rated expected to be 23% A-rated A+ 0% A- 3% A-rated down ~60% from 2020 companies AA- 1% companies A+ 1% AA- 9% BBB 2% NR 9% NR 27% A- 13% BBB 1% BBB- 32% B- 33% BBB- 20% B- 19% B 0% BB 8% BB+ 3% BB 12% B+ 8% Development activity benefitted from high grading customer credit quality with improved cost of capital and capital access 14

Pro Forma Financial and ESG Overview 15Pro Forma Financial and ESG Overview 15

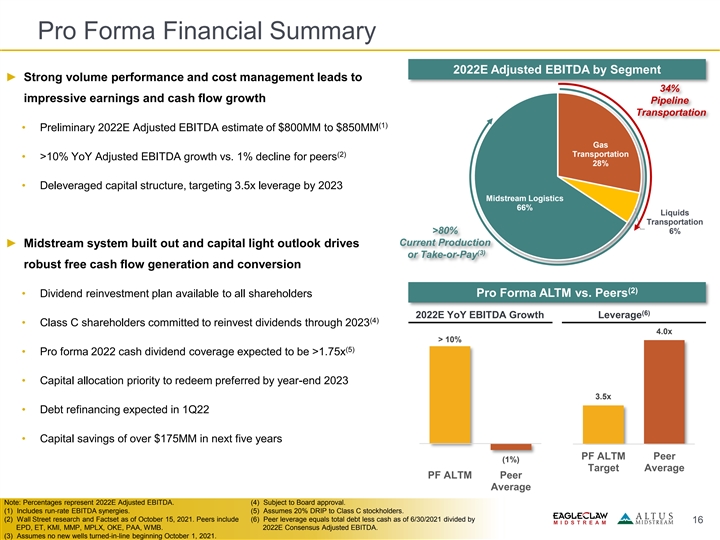

Pro Forma Financial Summary 2022E Adjusted EBITDA by Segment ► Strong volume performance and cost management leads to 34% impressive earnings and cash flow growth Pipeline Transportation (1) • Preliminary 2022E Adjusted EBITDA estimate of $800MM to $850MM Gas (2) Transportation • >10% YoY Adjusted EBITDA growth vs. 1% decline for peers 28% • Deleveraged capital structure, targeting 3.5x leverage by 2023 Midstream Logistics 66% Liquids Transportation >80% 6% Current Production ► Midstream system built out and capital light outlook drives (3) or Take-or-Pay robust free cash flow generation and conversion (2) • Dividend reinvestment plan available to all shareholders Pro Forma ALTM vs. Peers (6) 2022E YoY EBITDA Growth Leverage (4) • Class C shareholders committed to reinvest dividends through 2023 4.0x > 10% (5) • Pro forma 2022 cash dividend coverage expected to be >1.75x • Capital allocation priority to redeem preferred by year-end 2023 3.5x • Debt refinancing expected in 1Q22 • Capital savings of over $175MM in next five years PF ALTM Peer (1%) Target Average PF ALTM Peer Average Note: Percentages represent 2022E Adjusted EBITDA. (4) Subject to Board approval. (1) Includes run-rate EBITDA synergies. (5) Assumes 20% DRIP to Class C stockholders. (2) Wall Street research and Factset as of October 15, 2021. Peers include ( 6 ) P eer leverage equals total debt less cash as of 6/30/2021 divided by 16 EPD, ET, KMI, MMP, MPLX, OKE, PAA, WMB. 2022E Consensus Adjusted EBITDA. (3) Assumes no new wells turned-in-line beginning October 1, 2021.Pro Forma Financial Summary 2022E Adjusted EBITDA by Segment ► Strong volume performance and cost management leads to 34% impressive earnings and cash flow growth Pipeline Transportation (1) • Preliminary 2022E Adjusted EBITDA estimate of $800MM to $850MM Gas (2) Transportation • >10% YoY Adjusted EBITDA growth vs. 1% decline for peers 28% • Deleveraged capital structure, targeting 3.5x leverage by 2023 Midstream Logistics 66% Liquids Transportation >80% 6% Current Production ► Midstream system built out and capital light outlook drives (3) or Take-or-Pay robust free cash flow generation and conversion (2) • Dividend reinvestment plan available to all shareholders Pro Forma ALTM vs. Peers (6) 2022E YoY EBITDA Growth Leverage (4) • Class C shareholders committed to reinvest dividends through 2023 4.0x > 10% (5) • Pro forma 2022 cash dividend coverage expected to be >1.75x • Capital allocation priority to redeem preferred by year-end 2023 3.5x • Debt refinancing expected in 1Q22 • Capital savings of over $175MM in next five years PF ALTM Peer (1%) Target Average PF ALTM Peer Average Note: Percentages represent 2022E Adjusted EBITDA. (4) Subject to Board approval. (1) Includes run-rate EBITDA synergies. (5) Assumes 20% DRIP to Class C stockholders. (2) Wall Street research and Factset as of October 15, 2021. Peers include ( 6 ) P eer leverage equals total debt less cash as of 6/30/2021 divided by 16 EPD, ET, KMI, MMP, MPLX, OKE, PAA, WMB. 2022E Consensus Adjusted EBITDA. (3) Assumes no new wells turned-in-line beginning October 1, 2021.

Expect $50MM+ of Annual EBITDA Synergies ► System integration unlocks over $30MM per year • Processing enhancement and optimization • Ability to leverage Altus’ idle treating equipment • Replace leased compression on EagleClaw system with excess equity compression from Altus ► $20MM per year of immediate, tangible cost synergies (1) • G&A reduction and COMA termination with Apache • Adoption of BCP’s current operating cost structure across the pro forma company 17 (1) Construction, Operations and Maintenance Agreement. Expect $50MM+ of Annual EBITDA Synergies ► System integration unlocks over $30MM per year • Processing enhancement and optimization • Ability to leverage Altus’ idle treating equipment • Replace leased compression on EagleClaw system with excess equity compression from Altus ► $20MM per year of immediate, tangible cost synergies (1) • G&A reduction and COMA termination with Apache • Adoption of BCP’s current operating cost structure across the pro forma company 17 (1) Construction, Operations and Maintenance Agreement.

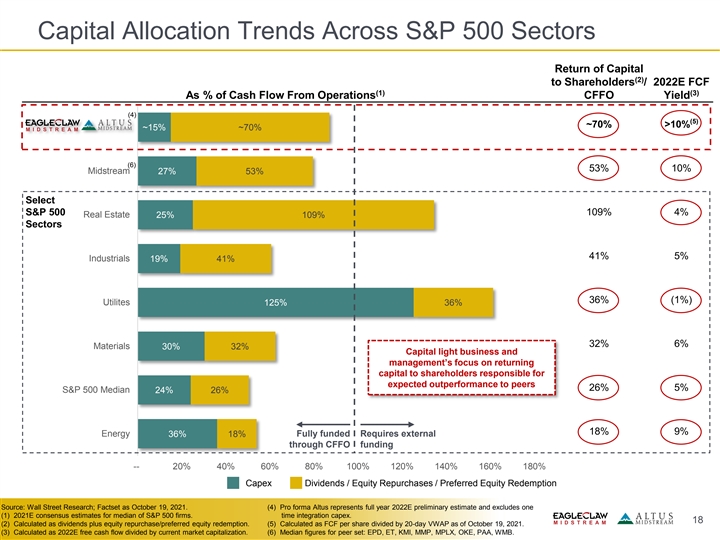

Capital Allocation Trends Across S&P 500 Sectors Return of Capital (2) to Shareholders / 2022E FCF (1) (3) As % of Cash Flow From Operations CFFO Yield (4) (5) ~70% >10% ATLM ~15% ~70% (6) 53% 10% Midstream 27% 53% Select 109% 4% S&P 500 Real Estate 25% 109% Sectors 41% 5% Industrials 19% 41% 36% (1%) Utilites 125% 36% 32% 6% Materials 30% 32% Capital light business and management’s focus on returning capital to shareholders responsible for expected outperformance to peers 26% 5% S&P 500 Median 24% 26% 18% 9% Energy 36% 18% Fully funded Requires external through CFFO funding -- 20% 40% 60% 80% 100% 120% 140% 160% 180% Capex Dividends / Equity Repurchases / Preferred Equity Redemption Source: Wall Street Research; Factset as October 19, 2021. (4) Pro forma Altus represents full year 2022E preliminary estimate and excludes one (1) 2021E consensus estimates for median of S&P 500 firms. time integration capex. 18 (2) Calculated as dividends plus equity repurchase/preferred equity redemption. (5) Calculated as FCF per share divided by 20-day VWAP as of October 19, 2021. (3) Calculated as 2022E free cash flow divided by current market capitalization. (6) Median figures for peer set: EPD, ET, KMI, MMP, MPLX, OKE, PAA, WMB.Capital Allocation Trends Across S&P 500 Sectors Return of Capital (2) to Shareholders / 2022E FCF (1) (3) As % of Cash Flow From Operations CFFO Yield (4) (5) ~70% >10% ATLM ~15% ~70% (6) 53% 10% Midstream 27% 53% Select 109% 4% S&P 500 Real Estate 25% 109% Sectors 41% 5% Industrials 19% 41% 36% (1%) Utilites 125% 36% 32% 6% Materials 30% 32% Capital light business and management’s focus on returning capital to shareholders responsible for expected outperformance to peers 26% 5% S&P 500 Median 24% 26% 18% 9% Energy 36% 18% Fully funded Requires external through CFFO funding -- 20% 40% 60% 80% 100% 120% 140% 160% 180% Capex Dividends / Equity Repurchases / Preferred Equity Redemption Source: Wall Street Research; Factset as October 19, 2021. (4) Pro forma Altus represents full year 2022E preliminary estimate and excludes one (1) 2021E consensus estimates for median of S&P 500 firms. time integration capex. 18 (2) Calculated as dividends plus equity repurchase/preferred equity redemption. (5) Calculated as FCF per share divided by 20-day VWAP as of October 19, 2021. (3) Calculated as 2022E free cash flow divided by current market capitalization. (6) Median figures for peer set: EPD, ET, KMI, MMP, MPLX, OKE, PAA, WMB.

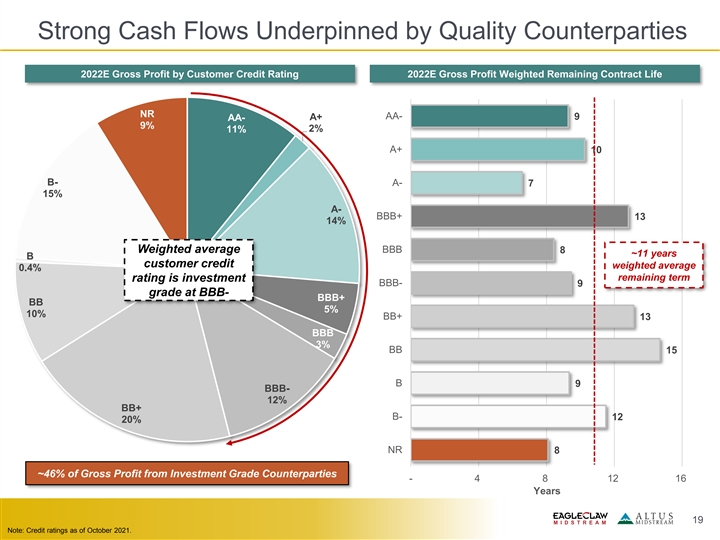

Strong Cash Flows Underpinned by Quality Counterparties 2022E Gross Profit by Customer Credit Rating 2022E Gross Profit Weighted Remaining Contract Life NR AA- A+ 9 AA- 9% 2% 11% A+ 10 B- A- 7 15% A- BBB+ 13 14% Weighted average BBB 8 ~11 years B customer credit weighted average 0.4% remaining term rating is investment BBB- 9 grade at BBB- BBB+ BB 5% 10% BB+ 13 BBB 3% BB 15 B 9 BBB- 12% BB+ B- 12 20% NR 8 ~46% of Gross Profit from Investment Grade Counterparties - 4 8 12 16 Years 19 Note: Credit ratings as of October 2021.Strong Cash Flows Underpinned by Quality Counterparties 2022E Gross Profit by Customer Credit Rating 2022E Gross Profit Weighted Remaining Contract Life NR AA- A+ 9 AA- 9% 2% 11% A+ 10 B- A- 7 15% A- BBB+ 13 14% Weighted average BBB 8 ~11 years B customer credit weighted average 0.4% remaining term rating is investment BBB- 9 grade at BBB- BBB+ BB 5% 10% BB+ 13 BBB 3% BB 15 B 9 BBB- 12% BB+ B- 12 20% NR 8 ~46% of Gross Profit from Investment Grade Counterparties - 4 8 12 16 Years 19 Note: Credit ratings as of October 2021.

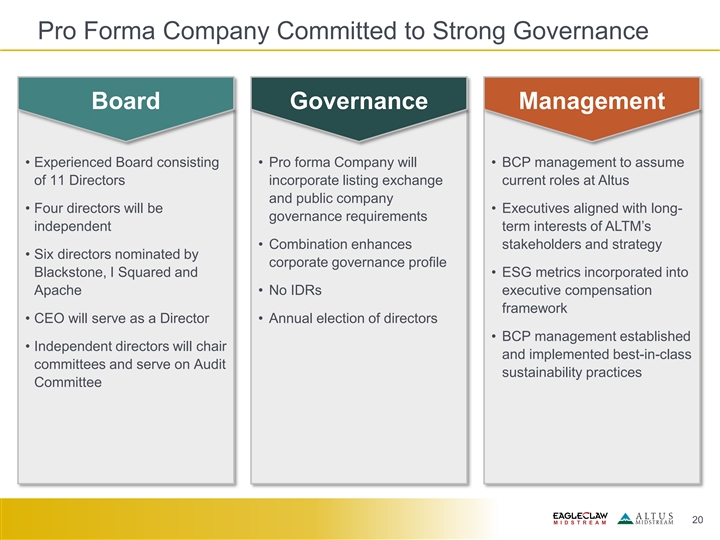

Pro Forma Company Committed to Strong Governance Board Governance Management • Experienced Board consisting • Pro forma Company will • BCP management to assume of 11 Directors incorporate listing exchange current roles at Altus and public company • Four directors will be • Executives aligned with long- governance requirements independent term interests of ALTM’s • Combination enhances stakeholders and strategy • Six directors nominated by corporate governance profile Blackstone, I Squared and • ESG metrics incorporated into Apache • No IDRs executive compensation framework • CEO will serve as a Director • Annual election of directors • BCP management established • Independent directors will chair and implemented best-in-class committees and serve on Audit sustainability practices Committee 20Pro Forma Company Committed to Strong Governance Board Governance Management • Experienced Board consisting • Pro forma Company will • BCP management to assume of 11 Directors incorporate listing exchange current roles at Altus and public company • Four directors will be • Executives aligned with long- governance requirements independent term interests of ALTM’s • Combination enhances stakeholders and strategy • Six directors nominated by corporate governance profile Blackstone, I Squared and • ESG metrics incorporated into Apache • No IDRs executive compensation framework • CEO will serve as a Director • Annual election of directors • BCP management established • Independent directors will chair and implemented best-in-class committees and serve on Audit sustainability practices Committee 20

Focus on Sustainability and Community Sustainable Reporting BCP’s 2020 ESG Report ► Pro Forma Altus to adopt BCP’s sustainability standards while incorporating Altus best practices • 2021 ESG Report to be published mid-2022 • BCP’s inaugural ESG report with detail on par with public midstream peers Key Initiatives ► BCP facilities powered with 100% renewable electricity • Seek to “green” the Alpine High G&P system ► Emissions monitoring and leak detection at facilities • 24/7 FLIR infrared camera monitoring • Fugitive methane detection ► Optimize use of electric compression assets ► Ensure vendor alignment with environmental practices ► Member of several organizations promoting environmental responsibility (The Environmental Partnership, ONE Future) ► Implemented social investment model to support Houston and West Texas communities 21Focus on Sustainability and Community Sustainable Reporting BCP’s 2020 ESG Report ► Pro Forma Altus to adopt BCP’s sustainability standards while incorporating Altus best practices • 2021 ESG Report to be published mid-2022 • BCP’s inaugural ESG report with detail on par with public midstream peers Key Initiatives ► BCP facilities powered with 100% renewable electricity • Seek to “green” the Alpine High G&P system ► Emissions monitoring and leak detection at facilities • 24/7 FLIR infrared camera monitoring • Fugitive methane detection ► Optimize use of electric compression assets ► Ensure vendor alignment with environmental practices ► Member of several organizations promoting environmental responsibility (The Environmental Partnership, ONE Future) ► Implemented social investment model to support Houston and West Texas communities 21

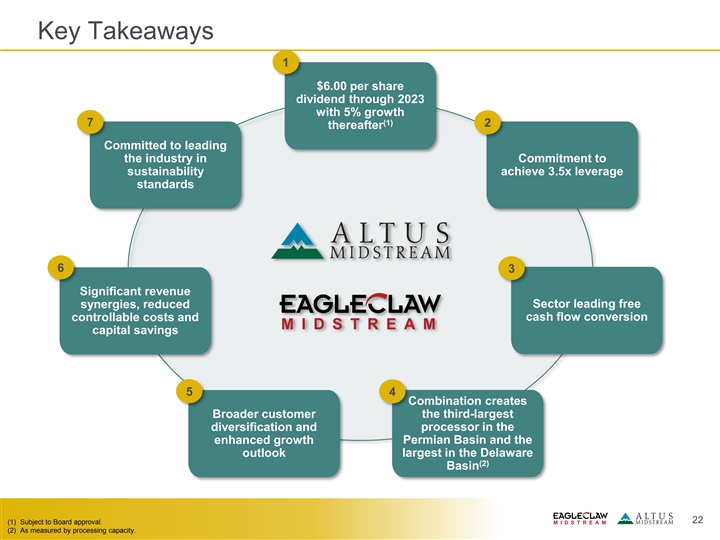

Key Takeaways 1 $6.00 per share dividend through 2023 with 5% growth (1) 7 2 thereafter Committed to leading the industry in Commitment to sustainability achieve 3.5x leverage standards 6 3 Significant revenue synergies, reduced Sector leading free controllable costs and cash flow conversion capital savings 5 4 Combination creates Broader customer the third-largest diversification and processor in the enhanced growth Permian Basin and the outlook largest in the Delaware (2) Basin 22 (1) Subject to Board approval. (2) As measured by processing capacity. Key Takeaways 1 $6.00 per share dividend through 2023 with 5% growth (1) 7 2 thereafter Committed to leading the industry in Commitment to sustainability achieve 3.5x leverage standards 6 3 Significant revenue synergies, reduced Sector leading free controllable costs and cash flow conversion capital savings 5 4 Combination creates Broader customer the third-largest diversification and processor in the enhanced growth Permian Basin and the outlook largest in the Delaware (2) Basin 22 (1) Subject to Board approval. (2) As measured by processing capacity.

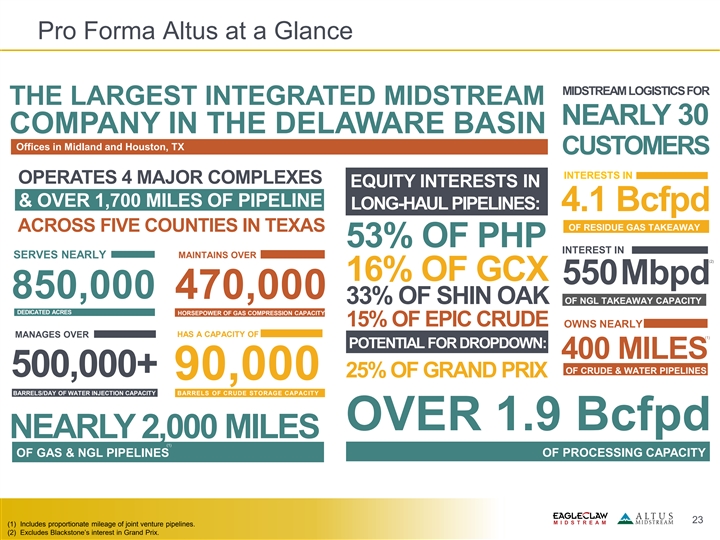

Pro Forma Altus at a Glance MIDSTREAM LOGISTICS FOR THE LARGEST INTEGRATED MIDSTREAM NEARLY 30 COMPANY IN THE DELAWARE BASIN Offices in Midland and Houston, TX CUSTOMERS INTERESTS IN OPERATES 4 MAJOR COMPLEXES EQUITY INTERESTS IN & OVER 1,700 MILES OF PIPELINE LONG-HAUL PIPELINES: 4.1 Bcfpd OF RESIDUE GAS TAKEAWAY ACROSS FIVE COUNTIES IN TEXAS 53% OF PHP INTEREST IN MAINTAINS OVER SERVES NEARLY (2) 16% OF GCX 550Mbpd 850,000 470,000 33% OF SHIN OAK OF NGL TAKEAWAY CAPACITY DEDICATED ACRES HORSEPOWER OF GAS COMPRESSION CAPACITY 15% OF EPIC CRUDE OWNS NEARLY HAS A CAPACITY OF MANAGES OVER (1) POTENTIAL FOR DROPDOWN: 400 MILES OF CRUDE & WATER PIPELINES 500,000+ 25% OF GRAND PRIX 90,000 BARRELS/DAY OF WATER INJECTION CAPACITY BARRELS OF CRUDE STORAGE CAPACITY OVER 1.9 Bcfpd NEARLY 2,000 MILES (1) OF GAS & NGL PIPELINES OF PROCESSING CAPACITY 23 (1) Includes proportionate mileage of joint venture pipelines. (2) Excludes Blackstone’s interest in Grand Prix.Pro Forma Altus at a Glance MIDSTREAM LOGISTICS FOR THE LARGEST INTEGRATED MIDSTREAM NEARLY 30 COMPANY IN THE DELAWARE BASIN Offices in Midland and Houston, TX CUSTOMERS INTERESTS IN OPERATES 4 MAJOR COMPLEXES EQUITY INTERESTS IN & OVER 1,700 MILES OF PIPELINE LONG-HAUL PIPELINES: 4.1 Bcfpd OF RESIDUE GAS TAKEAWAY ACROSS FIVE COUNTIES IN TEXAS 53% OF PHP INTEREST IN MAINTAINS OVER SERVES NEARLY (2) 16% OF GCX 550Mbpd 850,000 470,000 33% OF SHIN OAK OF NGL TAKEAWAY CAPACITY DEDICATED ACRES HORSEPOWER OF GAS COMPRESSION CAPACITY 15% OF EPIC CRUDE OWNS NEARLY HAS A CAPACITY OF MANAGES OVER (1) POTENTIAL FOR DROPDOWN: 400 MILES OF CRUDE & WATER PIPELINES 500,000+ 25% OF GRAND PRIX 90,000 BARRELS/DAY OF WATER INJECTION CAPACITY BARRELS OF CRUDE STORAGE CAPACITY OVER 1.9 Bcfpd NEARLY 2,000 MILES (1) OF GAS & NGL PIPELINES OF PROCESSING CAPACITY 23 (1) Includes proportionate mileage of joint venture pipelines. (2) Excludes Blackstone’s interest in Grand Prix.

Glossary of Terms ► Gross Profit is defined as revenues less cost of goods sold (exclusive of depreciation and amortization) ► Adjusted EBITDA (EBITDA) is defined as net income (loss) including noncontrolling interest before financing costs (net of capitalized interest), net interest expense, income taxes, depreciation, and accretion and adjusting for such items, as applicable, from income from equity method interests. ► Net Cash Flows Provided by Operating Activities (CFFO) represents net income (loss) plus depreciation and amortization, changes in net working capital and other non-cash items ► Capital investment (Capital) is defined as costs incurred in midstream activities, adjusted to exclude asset retirement obligations revisions and liabilities incurred, while including amounts paid during the period for abandonment and decommissioning expenditures ► Growth capital investments is defined as Capital Investment plus Altus’ proportionate share of capital in relation to equity method interests less midstream maintenance capital costs incurred ► Distributable cash flow (DCF) is defined as Adjusted EBITDA less equity interests’ Adjusted EBITDA plus cash distributions from equity interests less maintenance capex, cash tax, preferred unit distributions (whether in kind or in cash) and interest expense ► Free cash flow (FCF) is defined as DCF less growth capital investments ► Net debt is defined as gross debt less cash ► Leverage is defined as net debt divided by Adjusted EBITDA ► Distribution Coverage is defined as DCF divided by cash dividends. Assumes $6.00/share common dividend, 20% DRIP to Blackstone, I Squared and Apache 24Glossary of Terms ► Gross Profit is defined as revenues less cost of goods sold (exclusive of depreciation and amortization) ► Adjusted EBITDA (EBITDA) is defined as net income (loss) including noncontrolling interest before financing costs (net of capitalized interest), net interest expense, income taxes, depreciation, and accretion and adjusting for such items, as applicable, from income from equity method interests. ► Net Cash Flows Provided by Operating Activities (CFFO) represents net income (loss) plus depreciation and amortization, changes in net working capital and other non-cash items ► Capital investment (Capital) is defined as costs incurred in midstream activities, adjusted to exclude asset retirement obligations revisions and liabilities incurred, while including amounts paid during the period for abandonment and decommissioning expenditures ► Growth capital investments is defined as Capital Investment plus Altus’ proportionate share of capital in relation to equity method interests less midstream maintenance capital costs incurred ► Distributable cash flow (DCF) is defined as Adjusted EBITDA less equity interests’ Adjusted EBITDA plus cash distributions from equity interests less maintenance capex, cash tax, preferred unit distributions (whether in kind or in cash) and interest expense ► Free cash flow (FCF) is defined as DCF less growth capital investments ► Net debt is defined as gross debt less cash ► Leverage is defined as net debt divided by Adjusted EBITDA ► Distribution Coverage is defined as DCF divided by cash dividends. Assumes $6.00/share common dividend, 20% DRIP to Blackstone, I Squared and Apache 24