As filed with the Securities and Exchange Commission on June 16, 2017

Registration No. 333-216041

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-4

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

REGIONAL HEALTH PROPERTIES, INC.

(Exact name of Registrant as specified in its charter)

| Georgia | 8051 | 81-5166048 | ||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) | ||||

AdCare Health Systems, Inc. 454 Satellite Blvd. NW Suite 100 Suwanee, Georgia 30024 (678) 869-5116 | Allan J. Rimland President, Chief Executive Officer and Chief Financial Officer AdCare Health Systems, Inc. 454 Satellite Blvd. NW Suite 100 Suwanee, Georgia 30024 (678) 869-5116 | |||||

(Address, including ZIP code, and telephone number, including area code, of Registrant’s principal executive offices) | (Name, address, including ZIP code, and telephone number, including area code, of agent for service) | |||||

COPY TO:

Lori A. Gelchion, Esq.

Rogers & Hardin LLP

2700 International Tower

229 Peachtree Street, NE

Atlanta, Georgia 30303

(404) 522-4700

(404) 525-2224 (facsimile)

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this Form are being offered in connection with formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ Accelerated Filer ☐

Non-accelerated filer ☐ Smaller reporting company ☒

(Do not check if a smaller reporting company)

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer ☐

Calculation of Registration Fee

Title of each class of securities to be registered | Amount to be registered | Proposed maximum aggregate offering price | Amount of registration fee | |||||

| Common Stock, no par value | 22,685,439 (1) | 34,935,576.06 (2) | $4,049.03 (5) | |||||

| 10.875% Series A Cumulative Redeemable Preferred Shares, no par value | 2,761,535(3) | $61,996,460.75(4) | $7,185.39(5) | |||||

| 10.875% Series A Cumulative Redeemable Preferred Shares, no par value | 149,400 (6) | $3,261,402.00(7) | $378.00(5) | |||||

| Total : | $11,612.42 (8) | |||||||

| (1) | Represents the maximum number of shares of common stock, no par value per share (“RHE common stock”), of Regional Health Properties, Inc., a Georgia corporation (“RHE”), that may be issuable pursuant to the merger of AdCare Health Systems, Inc., a Georgia corporation (“AdCare”), with and into RHE (the “merger”), pursuant to the Agreement and Plan of Merger, between AdCare and RHE, as described in the proxy statement/prospectus that forms a part of this Registration Statement (the “merger agreement”), based on the number of shares of common stock, no par value, of AdCare (the “AdCare common stock”) outstanding at the close of business on February 10, 2017, or that may be issuable pursuant to outstanding options, warrants, convertible subordinated notes or other rights prior to the date the merger is expected to be completed. Pursuant to the merger agreement, each outstanding share of AdCare common stock will be converted into one share of RHE common stock. Pursuant to Rule 416, the number of shares of RHE common stock registered includes an indeterminate number of additional shares of RHE common stock that may be issued from time to time upon exercise or conversion of any option, warrant, convertible subordinated promissory note or other right as a result of the anti-dilution provisions thereof. |

| (2) | Pursuant to Rules 457(c) and 457(f)(1) under the Securities Act of 1933, as amended (the “Securities Act”), and solely for purposes of calculating this registration fee, the proposed maximum aggregate offering price is equal to the market value of shares of AdCare common stock (the securities to be converted pursuant to the merger agreement) in accordance with Rule 457(c) under the Securities Act, calculated as follows: the product of (i) $1.54, the average of the high and low prices per share of AdCare common stock on February 9, 2017, as reported on the NYSE MKT; and (ii) 22,685,439 shares of AdCare common stock issued, or that may become issuable, on or after February 10, 2017. |

| (3) | Represents the maximum number of shares of 10.875% Series A Cumulative Redeemable Preferred Shares, no par value, of RHE (the “RHE Series A Preferred Stock”), that may be issuable pursuant to the merger, based on the number of shares of 10.875% Series A Cumulative Redeemable Preferred Shares, no par value, of AdCare (the “AdCare Series A Preferred Stock”) outstanding at the close of business on February 10, 2017. Pursuant to the merger agreement, each outstanding share of AdCare Series A Preferred Stock will be converted into one share of RHE Series A Preferred Stock. |

| (4) | Pursuant to Rules 457(c) and 457(f)(1) under the Securities Act, and solely for purposes of calculating this registration fee, the proposed maximum aggregate offering price is equal to the market value of the shares of AdCare Series A Preferred Stock (the securities to be converted pursuant to the merger agreement) in accordance with Rule 457(c) under the Securities Act, calculated as follows: the product of (i) $22.45, the average of the high and low prices per share of AdCare Series A Preferred Stock on February 7, 2017, as reported on the NYSE MKT; and (ii) 2,761,535, the number of shares of AdCare Series A Preferred Stock outstanding as of the close of business on February 10, 2017. |

| (5) | Reflects the product of (i) .0001159 and (ii) the proposed maximum aggregate offering price. |

(6) Represents the additional shares of RHE Series 10.875% Series A Cumulative Redeemable Preferred Shares that may be issuable pursuant to the merger, based on the number of shares of AdCare Series A Preferred Stock which have been issued or may become issuable after February 10, 2017 and prior to the merger.

| (7) | Pursuant to Rules 457(c) and 457(f)(1) under the Securities Act, and solely for purposes of calculating this registration fee, the proposed maximum aggregate offering price is equal to the market value of the shares of AdCare Series A Preferred Stock (the securities to be converted pursuant to the merger agreement) in accordance with Rule 457(c) under the Securities Act, calculated as follows: the product of (i) $21.83, the average of the high and low prices per share of AdCare Series A Preferred Stock on June 13, 2017, as reported on the NYSE MKT; and |

(ii) 149,400, the number of shares of AdCare Series A Preferred Stock which have been issued or may become issuable after February 10, 2017 and prior to the merger.

| (8) | Of the total registration fee, $11,234.42 was previously paid with the initial filing and first amendment of this Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this proxy statement/prospectus is not complete and may be changed. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. Regional Health Properties, Inc. may not sell or exchange these securities until the registration statement is effective. This proxy statement/prospectus is not an offer to sell or exchange these securities, and is not soliciting an offer to buy these securities, in any state where the offer, sale or exchange is not permitted.

Preliminary Proxy Statement/Prospectus - Subject To Completion, Dated June 16 , 2017

ADCARE HEALTH SYSTEMS, INC.

454 Satellite Blvd. NW

Suite 100

Suwanee, Georgia 30024

[ ], 2017

Dear Shareholders:

I am pleased to invite you to attend a special meeting of shareholders of AdCare Health Systems, Inc., a Georgia corporation, which will be held on [ ], 2017 at [ ], local time, at the Sonesta Gwinnett Place Atlanta located at 1775 Pleasant Hill Road, Duluth, Georgia.

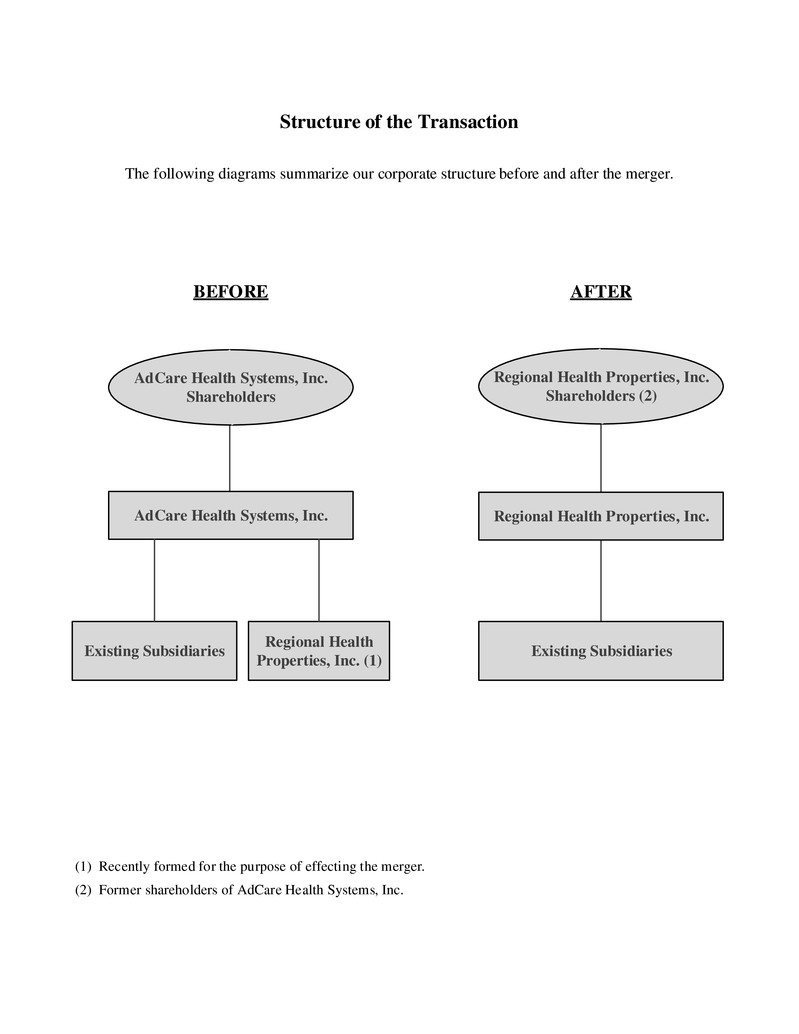

At the special meeting, you will be asked to vote on a proposal to approve an agreement and plan of merger which, if completed, will reorganize our corporate structure whereby Regional Health Properties, Inc., a Georgia corporation and a wholly owned subsidiary of AdCare recently formed for the purpose of the merger (“RHE”), would replace AdCare as the publicly held corporation through which our operations are conducted. We intend to complete this reorganization in order to ensure the effective adoption of certain charter provisions restricting the ownership and transfer of our common stock. This reorganization also provides us the opportunity to continue our business under a name that better reflects our new business model as a healthcare property holding and leasing company.

Our effective adoption of these ownership and transfer restrictions will serve two purposes. First, it will position us to regain compliance with certain NYSE MKT continued listing standards regarding stockholders’ equity. Second, if the board of directors determines for any future taxable year, after further consideration and evaluation, that qualifying for and electing status as a real estate investment trust (“REIT”) under the Internal Revenue Code of 1986, as amended (the “Code”), would be in the best interests of us and our shareholders, then the ownership and transfer restrictions will better position us to comply with certain of the U.S. federal income tax rules applicable to REITs under the Code to the extent such rules relate to the common stock. Similar ownership and transfer restrictions are commonly included in the charters of publicly-traded REITs because they are generally believed to be the most effective mechanism to monitor a REIT’s compliance with certain of the U.S. federal income tax rules that a REIT must satisfy in order to qualify as a REIT under the Code.

To this end, on [], 2017, AdCare entered into an agreement and plan of merger, as may be amended from time to time (the “merger agreement”), pursuant to which AdCare will merge with and into RHE, with RHE being the surviving entity in the merger. At the effective of the merger, RHE will succeed to the assets, continue the business and assume the obligations of AdCare.

At the effective time of the merger: (i) each outstanding share of AdCare common stock will be converted into one share of RHE common stock; and (ii) each outstanding share of AdCare’s 10.875% Series A Cumulative Redeemable Preferred Shares (the “AdCare Series A Preferred Stock”) will be converted into one share of RHE Series A Preferred Stock. As a result, after the merger you will own the same number and percentage of common stock and Series A Preferred Stock of RHE (the new holding company) as you own of AdCare before the merger. We anticipate that, immediately following the completion of the merger, shares of RHE common stock will trade on the NYSE MKT under the symbol “RHE” and that shares of RHE Series A Preferred Stock will trade on the NYSE MKT under the symbol “RHE.PRA.” It is a condition to the completion of the merger that the RHE common stock and RHE Series A Preferred Stock shall have been approved for listing on the NYSE MKT.

The approval of the merger agreement requires the affirmative vote of the holders of a majority of all outstanding shares of AdCare common stock entitled to vote thereon. The holders of AdCare Series A Preferred Stock do not have the right to vote on the proposal to approve the merger agreement.

The board of directors has unanimously adopted the merger agreement and determined the merger agreement and the transactions contemplated thereby advisable and in the best interests of AdCare and its shareholders. The board of directors recommends that all holders of AdCare common stock entitled to vote on the approval of the merger agreement vote “FOR” such approval.

This proxy statement/prospectus is a prospectus of RHE as well as a proxy statement for AdCare and provides you with detailed information about the merger and the special meeting. We encourage you to carefully read this entire proxy statement/prospectus, including all its annexes, and we especially encourage you to read the section entitled “Risk Factors” beginning on page 13.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued by RHE under this proxy statement/prospectus or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated [ ], 2017 and is being first mailed to shareholders on or about [ ], 2017.

| Sincerely, | ||||

| Allan J. Rimland | ||||

| President, Chief Executive Officer and Chief Financial Officer | ||||

ADCARE HEALTH SYSTEMS, INC.

454 Satellite Blvd. NW

Suite 100

Suwanee, Georgia 30024

NOTICE IS HEREBY GIVEN that a special meeting of shareholders of AdCare Health Systems, Inc., a Georgia corporation (“AdCare”), will be held on [ ], 2017 at [ ], local time, at the Sonesta Gwinnett Place Atlanta located at 1775 Pleasant Hill Road, Duluth, Georgia, for the following purposes:

1. to consider and vote upon a proposal to approve the Agreement and Plan of Merger, dated [ ], 2017, as it may be amended from time to time (the “merger agreement”), between AdCare and Regional Health Properties, Inc., a Georgia corporation and a wholly owned subsidiary of AdCare newly formed for purposes of the merger (“RHE”), a copy of which is attached as Annex A to this proxy statement/prospectus (the “merger proposal”); and

2. to consider and vote upon a proposal to approve the adjournment of the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes at the time of the special meeting to approve the merger proposal (the “adjournment proposal”).

On [ ], the board of directors unanimously adopted the merger agreement and determined the merger agreement and the transactions contemplated thereby advisable and in the best interests of AdCare and its shareholders. The board of directors recommends that you vote “FOR” the proposals that are described in more detail in this proxy statement/prospectus.

AdCare reserves the right to cancel or defer the merger, even if the holders of AdCare common stock vote to approve the merger agreement and the other conditions to the completion of the merger are satisfied or waived, if the board of directors determines that the merger is no longer in the best interests of AdCare and its shareholders.

If you are a holder of record of shares of AdCare common stock as of the close of business on [ ], 2017, the record date, you are entitled to notice of, and to vote those shares by proxy or at the special meeting and at any adjournment or postponement of the special meeting. The holders of record of AdCare’s 10.875% Series A Cumulative Redeemable Preferred Shares as of the record date are not entitled to vote on the proposals at the special meeting.

Your vote is important. Whether or not you, as a holder of AdCare common stock, plan to attend the special meeting in person, please complete, sign, date and promptly return the enclosed proxy card in the enclosed envelope. You may also authorize a proxy to vote your shares by telephone or over the Internet as described in your proxy card. Holders of AdCare common stock who return proxy cards by mail or submit a proxy by telephone or over the Internet prior to the special meeting may nevertheless attend the special meeting, revoke their proxies and vote their shares at the special meeting.

We encourage you to read the accompanying proxy statement/prospectus carefully. If you have any questions or need assistance voting your shares, please call our proxy solicitor, Georgeson Inc., toll-free at (888) 293-6812.

By Order of the Board of Directors,

Allan J. Rimland

Corporate Secretary

Suwanee, Georgia

[ ], 2017

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This proxy statement/prospectus constitutes a proxy statement of AdCare and has been mailed to you because you were a holder of AdCare common stock on the record date set by the board of directors and were entitled to notice of a special meeting of AdCare shareholders. Only holders of AdCare common stock as of the record date are being asked to consider and vote at the special meeting upon the merger proposal and the adjournment proposal. This proxy statement/prospectus also constitutes a prospectus of RHE, which is part of the registration statement on Form S-4 filed by RHE to register with the Securities and Exchange Commission (the “SEC”) the RHE common stock and the RHE Series A Preferred Stock that holders of AdCare common stock and holders of AdCare Series A Preferred Stock, respectively, will receive in connection with the merger if the merger agreement is approved and the merger is completed.

You should rely only on the information contained in or incorporated by reference into this proxy statement/prospectus, including the annexes to this proxy statement/prospectus. We have not authorized anyone to provide you with additional or different information. We are not making an offer to sell (or soliciting any offer to buy) any securities, or soliciting any proxy, in any jurisdiction where it is unlawful to do so. You should assume that the information contained in this proxy statement/prospectus is accurate only as of the date on the front of this proxy statement/prospectus. Our business, financial condition, results of operations and prospects may have changed since these dates.

This proxy statement/prospectus does not contain all of the information set forth in the registration statement and the exhibits thereto. For further information with respect to AdCare, RHE and the securities to be issued by RHE in connection with the merger, reference is made to the registration statement, including the exhibits thereto. See the section entitled “Where You Can Find More Information.”

When used in this proxy statement/prospectus, unless otherwise specifically stated or the context otherwise requires, the terms:

| • | “board of directors” or “board” refers to the AdCare board of directors with respect to the period prior to the merger and to the RHE board of directors with respect to the period after the merger; |

| • | “Company”, “AdCare”, “we”, “our” and “us” refer to AdCare and its subsidiaries with respect to the period prior to the merger and to RHE and its subsidiaries with respect to the period after the merger; |

| • | “shareholders” refers to the holders of AdCare capital stock with respect to the period prior to the merger and to the holders of RHE capital stock with respect to the period after the merger; |

| • | “common stock” refers to the common stock, no par value per share, of AdCare with respect to the period prior to the merger and to the common stock, no par value per share, of RHE with respect to the period after the merger; |

| • | “Series A Preferred Stock” refers to the 10.875% Series A Cumulative Redeemable Preferred Shares, no par value per share, of AdCare with respect to the period prior to the merger and to the 10.875% Series A Cumulative Redeemable Preferred Shares, no par value per share, of RHE with respect to the period after the merger; and |

| • | “special meeting” refers the special meeting of shareholders of AdCare Health Systems, Inc., a Georgia corporation, to be held on [ ], 2017 at [ ], local time, at the Sonesta Gwinnett Place Atlanta located at 1775 Pleasant Hill Road, Duluth, Georgia, including any postponement and adjournment thereof. |

As used herein, the term “including” and any variation thereof, means “including without limitation.” The use of the word “or” herein is not exclusive.

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This proxy statement/prospectus may contain statements that constitute forward-looking statements and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by these forward-looking statements.

In some cases you can identify forward-looking statements by terms such as “anticipate,” “project,” “may,” “intend,” “might,” “will,” “could,” “would,” “expect,” “believe,” “estimate,” “potential,” by the negative of these terms and by similar expressions. These forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties, many of which are beyond their ability to control or predict. You should not put undue reliance on any forward-looking statements. These forward-looking statements present our estimates and assumptions only as of the date of this proxy statement/prospectus.

Important factors that could cause actual results to differ materially and adversely from those expressed or implied by the forward-looking statements include:

| • | Our ability to achieve the benefits that we expected to achieve from our transition to a healthcare property holding and leasing company, including increased cash flow, reduced general and administrative expenses, and a lower cost of capital; |

| • | The impact of liabilities associated with our legacy business of owning and operating healthcare properties, including pending and potential professional and general liability claims; |

| • | Our dependence on the operating success of our tenants and their ability to meet their obligations to us; |

| • | The effect of increasing healthcare regulation and enforcement on our tenants, and the dependence of our tenants on reimbursement from governmental and other third-party payors; |

| • | The impact of litigation and rising insurance costs on the business of our tenants; |

| • | The effect of our tenants potentially declaring bankruptcy or becoming insolvent; |

| • | The ability and willingness of our tenants to renew their leases with us upon expiration, and our ability to reposition our properties on the same or better terms in the event of nonrenewal or if we otherwise need to replace an existing tenant; |

| • | The significant amount of our indebtedness, our ability to service our indebtedness, covenants in our debt agreements that may restrict our ability to pay dividends or incur additional indebtedness, and our ability to refinance our indebtedness on favorable terms; |

| • | Our ability to raise capital through equity and debt financings, and the cost of such capital; |

| • | The availability of, and our ability to identify, suitable acquisition opportunities, and our ability to complete such acquisitions and lease the respective properties on favorable terms; and |

| • | Other risks inherent in the real estate business, including uninsured or underinsured losses affecting our properties and the possibility of environmental compliance costs and liabilities. |

The above list of factors that may affect future performance and the accuracy of forward-looking statements is illustrative but by no means exhaustive. Therefore, all forward-looking statements should be evaluated with the understanding of their inherent risk and uncertainty. Except for our ongoing obligations to disclose material information as required by U.S. federal securities laws, we do not intend to update you concerning any future revisions to any forward-looking statements to reflect events or circumstances occurring after the date of this proxy statement/prospectus.

ii

TABLE OF CONTENTS

| Page | |

| QUESTIONS AND ANSWERS ABOUT THE MERGER | |

| STRUCTURE OF THE TRANSACTION | |

| SUMMARY | |

| RISK FACTORS | |

| VOTING AND PROXIES | |

| BACKGROUND OF THE MERGER | |

| REASONS FOR THE MERGER | |

| TERMS OF THE MERGER | |

| DIVIDEND POLICY | |

| OUR BUSINESS | |

| POLICY WITH RESPECT TO CERTAIN ACTIVITIES | |

| REPORT OF REGIONAL HEALTH PROPERTIES INC.’S INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | |

| REGIONAL HEALTH PROPERTIES INC. BALANCE SHEET | |

| REGIONAL HEALTH PROPERTIES INC. NOTES TO THE BALANCE SHEET | |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| DESCRIPTION OF CAPITAL STOCK | |

| COMPARISON OF RIGHTS OF SHAREHOLDERS OF ADCARE AND RHE | |

| MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS | |

| SECURITY OWNERSHIP OF OFFICERS, DIRECTORS AND CERTAIN SHAREHOLDERS | |

| CERTAIN INFORMATION REGARDING DIRECTORS AND EXECUTIVE OFFICERS | |

| DIRECTOR AND EXECUTIVE COMPENSATION | |

| LEGAL MATTERS | |

| EXPERTS | 123 |

| WHERE YOU CAN FIND MORE INFORMATION | 123 |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | |

| ANNEX A AGREEMENT AND PLAN OF MERGER | A-1 |

ANNEX B FORM OF AMENDED AND RESTATED ARTICLES OF INCORPORATION OF REGIONAL HEALTH PROPERTIES, INC. | B-1 |

| ANNEX C FORM OF AMENDED AND RESTATED BYLAWS OF REGIONAL HEALTH PROPERTIES, INC. | C-1 |

iii

QUESTIONS AND ANSWERS ABOUT THE MERGER

What follows are questions that you, as a shareholder of AdCare, may have regarding the merger and the special meeting and the answers to those questions. You are urged to carefully read this proxy statement/prospectus in its entirety because the information in this section may not provide all of the information that might be important to you with respect to the merger and the special meeting. Additional important information is contained in the annexes to this proxy statement/prospectus.

| Q. | What is the merger proposal? What will happen in the merger? |

| A. | At the special meeting, you will be asked to vote on a proposal to approve an agreement and plan of merger to create a new corporate structure for AdCare under which RHE, a Georgia corporation and a wholly owned subsidiary of AdCare, would replace AdCare as the publicly held corporation through which our operations are conducted. Pursuant to the merger agreement, at the effective time of the merger: (i) AdCare will merge with and into RHE; (ii) RHE will be the surviving entity in the merger; and (iii) RHE will succeed to the assets, continue the business and assume the obligations of AdCare. We refer to this transaction in this proxy statement/prospectus as the “merger.” |

As a consequence of the merger:

| • | the outstanding shares of AdCare common stock will convert into the same number of shares of RHE common stock; |

| • | the outstanding shares of AdCare Series A Preferred Stock will convert into the same number of shares of RHE Series A Preferred Stock; |

| • | you will own shares of RHE common stock and RHE Series A Preferred Stock in the same amount and percentage as your holdings in AdCare immediately prior to the merger; |

| • | the existing board of directors and executive officers of AdCare immediately prior to the merger will be the board of directors and executive officers, respectively, of RHE immediately following the merger, and each director and executive officer will continue his directorship or employment, as the case may be, with RHE under the same terms as his directorship or employment with AdCare; |

| • | RHE will have assumed all of AdCare’s equity incentive compensation plans, and all rights to acquire shares of AdCare common stock under any AdCare equity incentive compensation plan will have been converted into rights to acquire RHE common stock pursuant to the terms of the equity incentive compensation plans and other related documents, if any; |

| • | effective at the time of the merger, RHE will become the publicly traded NYSE MKT listed company that will succeed to the assets, continue the business and assume the obligations of AdCare; |

| • | the rights of the holders of RHE common stock and RHE Series A Preferred Stock will be governed by the amended and restated articles of incorporation of RHE (the “RHE Charter”) and the amended and restated bylaws of RHE (the “RHE Bylaws”). The RHE Charter is substantially equivalent to AdCare’s articles of incorporation, as amended (the “AdCare Charter”), except that the RHE Charter at the effective time of the merger will include ownership and transfer restrictions related to the RHE common stock. The RHE Bylaws are substantially equivalent to the Bylaws of AdCare, as amended (the “AdCare Bylaws”); |

| • | there will be no change in the assets we hold or in the business we conduct; and |

| • | there will be no fundamental change to our current operational strategy. |

We have attached to this proxy statement/prospectus a copy of the merger agreement as Annex A, a copy of the form of the RHE Charter as Annex B, and a copy of the form of the RHE Bylaws as Annex C.

| Q. | Why are you reorganizing the corporate structure? |

| A. | We are reorganizing our corporate structure in order to ensure the effective adoption of charter provisions restricting the ownership and transfer of our common stock. By merging AdCare with and into RHE, whose charter at the time of the merger will include the ownership and transfer restrictions related to the RHE common stock, we will ensure such adoption. |

Our effective adoption of these ownership and transfer restrictions will serve two purposes. First, the restrictions will position us to regain compliance with certain NYSE MKT continued listing standards regarding stockholders’ equity. Second, if the board of directors determines for any future taxable year, after further consideration and evaluation, that qualifying for and electing status as a REIT under the Code would be in the best interests of us and our shareholders, then the ownership and

1

transfer restrictions will better position us to comply with certain of the U.S. federal income tax rules applicable to REITs under the Code to the extent such rules relate to the common stock.

NYSE MKT Compliance. The adoption of the transfer and ownership restrictions will permit us under applicable accounting guidance to classify the Series A Preferred Stock as permanent equity on our consolidated balance sheet (instead of temporary equity outside of permanent equity as it is currently classified). Classifying the Series A Preferred Stock as permanent equity will position us to regain compliance with the NYSE MKT continued listing standards regarding stockholders’ equity with which we are not currently in compliance.

Specifically, we are not in compliance with Section 1003(a)(i) (requiring stockholders’ equity of $2.0 million or more if an issuer has reported losses from continuing operations and/or net losses in two of its three most recent fiscal years), Section 1003(a)(ii) (requiring stockholders’ equity of $4.0 million or more if an issuer has reported losses from continuing operations and/or net losses in three of its four most recent fiscal years) and Section 1003(a)(iii) (requiring stockholders’ equity of $6.0 million or more if an issuer has reported losses from continuing operations and/or net losses in its five most recent fiscal years) of the NYSE MKT Company Guide (collectively, the “Stockholders’ Equity Continued Listing Standards”). If we do not regain compliance with the Stockholders’ Equity Continued Listing Standards by October 18, 2017, then the NYSE MKT will delist the common stock and the Series A Preferred Stock. The NYSE MKT may delist the common stock and the Series A Preferred Stock prior to such date if we do not make progress toward compliance consistent with the compliance plan we proposed to the NYSE MKT. See the sections entitled “Risk Factors - Risks Related to the Delisting of Our Securities” and “Reasons for the Merger.”

At March 31, 2017, we had a stockholders’ deficit of $40.7 million. At March 31, 2017, we had $61.4 million of Series A Preferred Stock classified as temporary equity on our balance sheet. If the Series A Preferred Stock had been classified as permanent equity at March 31, 2017, then our stockholders’ equity as of such date would have been $20.7 million.

Consideration of REIT Election. The board of directors is in the process of evaluating the feasibility of the Company in the future qualifying and electing as a REIT under the Code and any potential benefits thereof. The ownership and transfer restrictions will better position us to comply with certain of the U.S. federal income tax rules applicable to REITs under the Code to the extent such rules relate to the common stock. The ownership and transfer restrictions will not apply to the Series A Preferred Stock and, therefore, will not assist us in complying with such rules to the extent they relate to the Series A Preferred Stock. Accordingly, among other things, the Series A Preferred Stock would need to be redeemed or its terms appropriately modified before the Company would elect REIT status under the Code. See “ - What are the requirements to qualify as a REIT under the Code?” below.

There is no assurance that the Company will qualify as a REIT in a future taxable year or, if it were to so qualify, that the board of directors would determine that electing REIT status would be in the best interests of the Company and its shareholders.

See the sections entitled “Risk Factors - Risks Related to the Ownership and Transfer Restrictions” and “Reasons for the Merger.”

| Q. | What is a REIT? |

| A. | A REIT is a company that qualifies for special treatment for U.S. federal income tax purposes because, among other things, it derives most of its income from real estate-based sources and makes a special election under the Code. A corporation that qualifies as a REIT will generally be entitled to a deduction for dividends that it pays and therefore will not be subject to U.S. federal income tax to the extent of such deductions. See the section entitled “Material United States Federal Income Tax Considerations.” |

| Q. | What are the requirements to qualify as a REIT under the Code? |

| A. | For the Company to qualify as a REIT under the Code, among other things: (i) the Company’s stock (including common and preferred stock) must be beneficially owned by 100 or more persons during at least 335 days of a taxable year of 12 months or during a proportionate part of a shorter taxable year (other than the first year for which an election to be a REIT has been made); and (ii) not more than 50% of the value of the outstanding shares of the Company’s stock (including common and preferred stock) may be owned, directly or indirectly, by five or fewer “individuals” (as defined in the Code to include certain entities such as private foundations) during the last half of a taxable year (other than the first taxable year for which an election to be a REIT has been made), which is referred to as the “closely held” rule under the Code. In addition, a person actually or constructively owning 10% or more of the vote or value of the outstanding shares of the Company’s stock (including common |

2

and preferred stock) could lead to a level of affiliation between the Company and one or more of its tenants that could disqualify the Company’s revenues from the affiliated tenants from constituting REIT-compliant income and thereby potentially jeopardize or otherwise adversely impact the Company’s ability to qualify as a REIT.

The Company’s ability to qualify as a REIT would depend upon its compliance at the time of and following the REIT election with various other requirements, including requirements related to: (i) the nature of the Company’s assets being principally real estate or related to real estate leasing, with the potential for investing in the securities of other issuers being very limited; (ii) the sources of the Company’s gross income being principally “rents from real property,” with the balance of any gross income being principally comprised of passive investment income such as interest, dividends and capital gains; (iii) the internal organization of any subsidiaries of the Company and activities being suitably divided between qualified REIT subsidiary and taxable REIT subsidiary roles and responsibilities; and (iv) the sufficiency of distributions to the Company’s shareholders relating to both the Company’s REIT taxable income and any pre-REIT accumulated earnings and profits.

See the section entitled “Material United States Federal Income Tax Considerations.”

| Q. | What are the transfer and ownership restrictions? |

A. | The primary consequence of the adoption of the ownership and transfer restrictions related to the common stock is that, after the merger and subject to the exceptions, waivers and the constructive ownership rules described in the RHE Charter, no person (including any “group” as defined in Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)) may beneficially own, or be deemed to constructively own by virtue of the ownership attribution provisions of the Code, in excess of 9.9% (by value or number of shares, whichever is more restrictive) of the outstanding RHE common stock. In this proxy statement/prospectus, we refer to “transfer and ownership restrictions” as the provisions set forth in Article IX of the RHE Charter and which are described in the section entitled “Description of Capital Stock - Ownership and Transfer Restrictions.” |

| Q. | When and where is the special meeting? |

| A. | The special meeting will be held on [ ], 2017 at [ ], local time, at the Sonesta Gwinnett Place Atlanta located at 1775 Pleasant Hill Road, Duluth, Georgia. |

| Q. | Who can vote at the special meeting? |

| A. | If you are a holder of record of AdCare common stock at the close of business on [ ], 2017, you may vote the shares of AdCare common stock that you hold on the record date at the special meeting. On or about [ ], 2017, we will begin mailing this proxy statement/prospectus to all persons entitled to notice of the special meeting. |

| Q. | What will I be voting on at the special meeting? |

| A. | As a holder of AdCare common stock, you are entitled to, and requested to, vote on the proposal to approve the merger agreement pursuant to which AdCare will be merged with and into RHE, a wholly owned subsidiary of AdCare, with RHE as the surviving entity. In addition, you are requested to vote on the proposal to approve the adjournment of the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes at the time of the special meeting to approve the merger agreement. |

| Q. | Why is my vote important? |

| A. | If you, as a holder of AdCare common stock, do not submit a proxy or vote in person at the meeting, it will be more difficult for us to obtain the necessary quorum to hold the special meeting. In addition, your failure to submit a proxy or to vote in person will have the same effect as a vote against the approval of the merger agreement. If you hold your shares through a broker, bank or other nominee, your broker, bank or other nominee will not be able to cast a vote on the approval of the merger agreement without instructions from you. Failure to provide voting instructions to your broker, bank or other nominee will have the same effect as a vote against approval of the merger agreement. |

| Q. | What constitutes a quorum for the special meeting? |

| A. | A majority of the voting power of the outstanding shares of AdCare common stock entitled to vote at the special meeting, represented in person or by proxy, constitutes a quorum for the special meeting. |

3

| Q. | What vote is required? |

| A. | Approval of the merger proposal requires the affirmative vote of the holders of a majority of all outstanding shares of AdCare common stock entitled to vote on the merger proposal. Approval of the adjournment proposal requires that the votes cast in favor of the adjournment proposal exceed the votes cast against it. As of the close of business on the record date, there were [ ] shares of AdCare common stock outstanding and entitled to vote at the special meeting. Each share of outstanding common stock on the record date is entitled to one vote on each proposal submitted to you for consideration. |

| Q. | How do I vote without attending the special meeting? |

| A. | If you are a holder of AdCare common stock on the record date, you may cause your shares to be voted by completing, signing and promptly returning the proxy card in the self-addressed stamped envelope provided. You may also authorize a proxy to vote your shares by telephone or over the Internet as described in your proxy card. Authorizing a proxy by telephone or over the Internet or by mailing a proxy card will not limit your right to attend the special meeting and vote your shares in person |

If your shares are held by a broker, bank or other nominee, please follow the voting instructions provided by your bank, broker or other nominee to ensure that your shares are represented at the special meeting.

| Q. | Can I attend the special meeting and vote my shares in person? |

| A. | Yes. All shareholders of AdCare common stock are invited to attend the special meeting. Holders of record of AdCare common stock at the close of business on the record date are invited to attend and vote at the special meeting. If your shares are held by a broker, bank or other nominee, then you are not the holder of record. Therefore, to vote at the special meeting, you must bring the appropriate documentation from your broker, bank or other nominee confirming your beneficial ownership of the shares. |

| Q. | If my shares are held in “street name” by my broker, bank or other nominee, will my broker, bank or other nominee vote my shares for me without my instruction? |

| A. | No. If your shares are held in “street name” by your broker, bank or other nominee, you should follow the directions provided by your broker, bank or other nominee. Your broker, bank or other nominee will vote your shares only if you provide instructions on how you would like your shares to be voted. Failure to provide voting instructions to your broker, bank or other nominee will have the same effect as a vote against approval of the merger agreement. |

| Q. | Can I change my vote after I have mailed my signed proxy card? |

| A. | Yes. You can change your vote at any time before your proxy is voted at the special meeting. To revoke your proxy, you must either (i) timely notify the AdCare Corporate Secretary in writing, (ii) timely mail a new proxy card dated after the date of the proxy you wish to revoke, (iii) timely submit a later dated proxy, by telephone or over the Internet by following the instructions on your proxy card or (iv) attend the special meeting and vote your shares in person. Merely attending the special meeting will not constitute revocation of your proxy. If your shares are held through a broker, bank or other nominee, then you should contact your broker, bank or other nominee to change your vote. |

| Q. | Who will be the board of directors and executive officers after the merger? |

| A. | The existing board of directors and executive officers of AdCare immediately prior to the merger will be the board of directors and executive officers, respectively, of RHE immediately following the merger, and each director and executive officer will continue his directorship or employment, as the case may be, with RHE under the same terms as his directorship or employment with AdCare. |

| Q. | Do any of our directors and executive officers have any interests in the merger that are different from mine? |

| A. | No. Our directors and executive officers own shares of AdCare common stock, restricted stock awards and options and warrants to purchase AdCare common stock and, to that extent, their interest in the merger is the same as that of the other holders of shares of AdCare common stock, restricted stock awards and options and warrants to purchase AdCare common stock. |

4

| Q. | Will I have to pay U.S. federal income taxes as a result of the merger? |

| A. | No. You will not recognize gain or loss for U.S. federal income tax purposes as a result of the conversion of shares of AdCare common stock into shares of RHE common stock, or shares of AdCare Series A Preferred Stock into shares of RHE Series A Preferred Stock, in the merger. |

The U.S. federal income tax treatment of holders of AdCare common stock, RHE common stock, AdCare Series A Preferred Stock and RHE Series A Preferred Stock depends in some instances on determinations of fact and interpretations of complex provisions of U.S. federal income tax law for which no clear precedent or authority may be available. In addition, the tax consequences to any particular holder of AdCare common stock, RHE common stock, AdCare Series A Preferred Stock or RHE Series A Preferred Stock may depend on that holder’s particular tax circumstances. We urge you to consult your tax advisor regarding the specific tax consequences, including the federal, state, local and foreign tax consequences, to you in light of your particular investment in, or the tax circumstances of acquiring, holding, exchanging or otherwise disposing of, AdCare common stock, RHE common stock, AdCare Series A Preferred Stock or RHE Series A Preferred Stock.

| Q. | Am I entitled to dissenters’ rights? |

| A. | No. Under Georgia law, you are not entitled to any statutory dissenters’ rights in connection with the merger. |

| Q. | How does the AdCare board of directors recommend I vote on the merger proposal? |

| A. | The AdCare board of directors believes that the merger agreement and the transactions contemplated thereby are advisable and in the best interests of AdCare and its shareholders. The board of directors unanimously recommends that you vote “FOR” the approval of the merger agreement. |

| Q. | When is the merger expected to be completed? |

| A. | We expect to complete the merger no later than [ ]. However, we reserve the right to cancel or defer the merger, even if the holders of AdCare common stock vote to approve the merger agreement and the other conditions to the completion of the merger are satisfied or waived, if the board of directors determines that the merger is no longer in the best interests of AdCare and its shareholders. |

| Q. | What will I receive in connection with the merger? |

| A. | At the effective time of the merger: (i) each outstanding share of AdCare common stock will be converted into one share of RHE common stock; and (ii) each outstanding share of AdCare Series A Preferred Stock will be converted into one share of RHE Series A Preferred Stock. |

| Q. | Will the merger change AdCare’s business or operating strategy? |

| A. | The merger, if completed, will not change our business or operating strategy. See the section entitled “Our Business - Business Strategy.” |

| Q. | What do I need to do now? |

| A. | You should carefully read and consider the information contained in this proxy statement/prospectus, including its annexes. They contain important information about what the AdCare board of directors considered in evaluating and adopting the merger agreement and the transactions contemplated thereby, including the merger. |

You should then complete and sign your proxy card and return it in the enclosed envelope as soon as possible so that your shares will be represented at the special meeting, or submit your proxy by telephone or over the Internet in accordance with the instructions on your proxy card. If your shares are held through a broker, bank or other nominee, then you should receive a separate voting instruction form with this proxy statement/prospectus.

5

| Q. | Should I send in my stock certificates now? |

| A. | No. After the merger is completed, holders of AdCare common stock will receive written instructions from the exchange agent on how to exchange their certificates formerly representing shares of AdCare common stock for certificates representing shares of RHE common stock. Please do not send in your AdCare stock certificates with your proxy. |

| Q. | Will my RHE common stock and RHE Series A Preferred Stock be publicly traded? |

| A. | RHE will apply to list the RHE common stock and RHE Series A Preferred Stock on the NYSE MKT. We expect that, immediately following the completion of the merger, RHE common stock will trade under the symbol “RHE” and RHE Series A Preferred Stock will trade under the symbol “RHE.PRA.” It is a condition to the completion of the merger that the RHE common stock and RHE Series A Preferred Stock shall have been approved for listing on the NYSE MKT. |

| Q. | Will a proxy solicitor be used? |

| A. | Yes. We have engaged Georgeson Inc. to assist in the solicitation of proxies for the special meeting and estimate we will pay Georgeson Inc. a fee of approximately $10,000. We have also agreed to reimburse Georgeson Inc. for certain costs and expenses incurred in connection with the proxy solicitation and to indemnify Georgeson Inc. against certain losses, claims, damages, costs, fees, expenses and liabilities. In addition, our officers and employees may request the return of proxies by telephone or in person, but no additional compensation will be paid to them. |

| Q. | Whom should I call with questions? |

| A. | You should call Georgeson Inc., our proxy solicitor, toll-free at (888) 293-6812 with any questions about the merger, or to obtain additional copies of this proxy statement/prospectus or additional proxy cards. |

6

|

7

SUMMARY

This summary highlights selected information from this proxy statement/prospectus and may not contain all of the information that is important to you. You are urged to carefully read this entire proxy statement/prospectus and the other documents to which this proxy statement/prospectus refers to fully understand the merger. In particular, you should read the annexes attached to this proxy statement/prospectus, including the merger agreement, which is attached as Annex A. You also should read the form of RHE Charter, attached as Annex B, and the form of RHE Bylaws, attached as Annex C, because these documents will govern your rights as a holder of RHE common stock or a holder of RHE Series A Preferred Stock following the merger, as applicable. See the section entitled “Where You Can Find More Information” in this proxy statement/prospectus. For a discussion of the risk factors that you should carefully consider, see the section entitled “Risk Factors” beginning on page 13.

The Companies

AdCare Health Systems, Inc.

454 Satellite Blvd. NW

Suite 100

Suwanee, Georgia 30024

(678) 869-5116

AdCare is a self-managed real estate investment company that invests primarily in real estate purposed for long-term care and senior living. The Company’s business primarily consists of leasing and subleasing healthcare facilities to third-party tenants, which operate such facilities. The facility operators provide a range of healthcare services, including skilled nursing and assisted living services, social services, various therapy services, and other rehabilitative and healthcare services for both long-term and short-stay patients and residents.

As of the date of this proxy statement/prospectus, the Company owned, leased, or managed for third parties 30 facilities primarily in the Southeast. Of the 30 facilities, the Company: (i) leased to third-party operators 14 skilled nursing facilities which it owned and subleased to third-party operators 11 skilled nursing facilities which it leased; (ii) leased to third-party operators two assisted living facilities which it owned; and (iii) managed on behalf of third-party owners two skilled nursing facilities and one independent living facility. On October 6, 2016, the Company completed the sale of nine of its facilities in Arkansas.

See the section entitled “Our Business.”

Regional Health Properties, Inc.

454 Satellite Blvd. NW

Suite 100

Suwanee, Georgia 30024

(678) 869-5116

Regional Health Properties, Inc. is a wholly owned subsidiary of AdCare and was organized in Georgia on January 26, 2017. Prior to the merger, RHE will conduct no business other than that incident to the merger. Following the merger, RHE will succeed to the assets, continue the business and assume the obligations of AdCare.

General

We are reorganizing our corporate structure in order to ensure the effective adoption of charter provisions will position us to regain compliance with the Stockholders’ Equity Continued Listing Standards. Second, if the board of directors determines for any future taxable year, after further consideration and evaluation, that qualifying for and electing status as a REIT under the Code would be in the best interests of us and our shareholders, then the ownership and transfer restrictions will better position us to comply with certain of the U.S. federal income tax rules applicable to REITs under the Code to the extent such rules relate to the common stock. The ownership and transfer restrictions will not apply to the Series A Preferred Stock and, therefore, will not assist us in complying with such U.S. federal income tax rules to the extent they relate to the Series A Preferred Stock. Accordingly, among other things, the Series A Preferred Stock would need to be redeemed or its terms appropriately modified before the Company would elect REIT status under the Code.

We are distributing this proxy statement/prospectus to the holders of AdCare common stock in connection with the solicitation of proxies by the board of directors for the approval of the merger proposal and the adjournment proposal. A copy of the merger agreement is attached to this proxy statement/prospectus as Annex A.

8

The board of directors reserve the right to cancel or defer the merger, even if holders of AdCare common stock vote to approve the merger agreement and the other conditions to the completion of the merger are satisfied or waived, if it determines that the merger is no longer in the best interests of AdCare and its shareholders.

Board of Directors and Executive Officers of RHE (See page 107 )

The existing board of directors and executive officers of AdCare immediately prior to the merger will be the board of directors and executive officers, respectively, of RHE immediately following the merger.

Interests of Directors and Executive Officers in the Merger (See page 105 )

Our directors and executive officers own shares of AdCare common stock, restricted stock awards and options and warrants to purchase AdCare common stock and, to that extent, their interest in the merger is the same as that of the other holders of shares of AdCare common stock, restricted stock awards and options and warrants to purchase AdCare common stock.

Regulatory Approvals (See page 42)

We are not aware of any federal, state or local regulatory requirements that must be complied with or approvals that must be obtained prior to completion of the merger pursuant to the merger agreement and the transactions contemplated thereby, other than compliance with applicable federal and state securities laws and the filing of a certificate of merger as required under the Georgia Business Corporation Code (the “GBCC”).

Comparison of Rights of Shareholders of AdCare and RHE (See page 90 )

The rights of holders of AdCare common stock are currently governed by the GBCC, the AdCare Charter and the AdCare Bylaws. If the merger agreement is approved by the holders of AdCare common stock and the merger is completed then holders of AdCare common stock will become holders of RHE common stock and the rights of holders of RHE common stock will be governed by the GBCC, the RHE Charter and the RHE Bylaws. As described below, some important differences exist between the rights of holders of AdCare common stock and the rights of holders of RHE common stock.

The rights of holders of AdCare Series A Preferred Stock are currently governed by the GBCC, the AdCare Charter and the AdCare Bylaws. If the merger agreement is approved by the holders of AdCare common stock and the merger is completed, then holders of AdCare Series A Preferred Stock will become holders of RHE Series A Preferred Stock and the rights of the holders of RHE Series A Preferred Stock will be governed by the GBCC, the RHE Charter and the RHE Bylaws. The rights of the holders of RHE Series A Preferred Stock would be equivalent to the rights of holders of AdCare Series A Preferred Stock.

The major difference between your rights as a holder of AdCare common stock and your rights as a holder of RHE common stock is that the RHE common stock will be subject to the ownership and transfer restrictions, including that, after the merger and subject to the exceptions, waivers and the constructive ownership rules described in the RHE Charter, no person (including any “group” as defined in Section 13(d)(3) of the Exchange Act) may beneficially own, or be deemed to constructively own by virtue of the ownership attribution provisions of the Code, in excess of 9.9% (by value or number of shares, whichever is more restrictive) of the outstanding RHE common stock. See the sections entitled “Description of Capital Stock - Ownership and Transfer Restrictions.” and “Comparison of Rights of Shareholders of AdCare and RHE.”

The forms of the RHE Charter and RHE Bylaws are attached as Annex B and Annex C, respectively.

Material U.S. Federal Income Tax Consequences of the Merger (See page 91 )

It is a condition to the closing of the merger that we receive an opinion from our tax counsel to the effect that the merger will be treated for U.S. federal income tax purposes as a reorganization under Section 368(a)(1)(F) of the Code. Accordingly, we expect for U.S. federal income tax purposes that:

| • | no gain or loss will be recognized by AdCare or RHE as a result of the merger; |

| • | With respect to the conversion of shares of AdCare common stock into RHE common stock: |

| • | you will not recognize any gain or loss upon the conversion of your shares of AdCare common stock into RHE common stock; |

9

| • | the tax basis of the shares of RHE common stock that you receive pursuant to the merger in the aggregate will be the same as your adjusted tax basis in the shares of AdCare common stock being converted in the merger; and |

| • | the holding period of shares of RHE common stock that you receive pursuant to the merger will include your holding period with respect to the shares of AdCare common stock being converted in the merger, assuming that your AdCare common stock was held as a capital asset at the effective time of the merger. |

| • | With respect to the conversion of shares of AdCare Series A Preferred Stock into RHE Series A Preferred Stock: |

| • | you will not recognize any gain or loss upon the conversion of your shares of AdCare Series A Preferred Stock into RHE Series A Preferred Stock; |

| • | the tax basis of the shares of RHE Series A Preferred Stock that you receive pursuant to the merger in the aggregate will be the same as your adjusted tax basis in the shares of AdCare Series A Preferred Stock being converted in the merger; and |

| • | the holding period of shares of RHE Series A Preferred Stock that you receive pursuant to the merger will include your holding period with respect to the shares of AdCare Series A Preferred Stock being converted in the merger, assuming that your AdCare Series A Preferred Stock was held as a capital asset at the effective time of the merger. |

The U.S. federal income tax treatment of holders of AdCare common stock, RHE common stock, AdCare Series A Preferred Stock and RHE Series A Preferred Stock depends in some instances on determinations of fact and interpretations of complex provisions of U.S. federal income tax law for which no clear precedent or authority may be available. In addition, the tax consequences to any particular holder of AdCare common stock, RHE common stock, AdCare Series A Preferred Stock or RHE Series A Preferred Stock may depend on that holder’s particular tax circumstances. We urge you to consult your tax advisor regarding the specific tax consequences, including the federal, state, local and foreign tax consequences, to you in light of your particular investment in, or tax circumstances of acquiring, holding, exchanging or otherwise disposing of, AdCare common stock, RHE common stock, AdCare Series A Preferred Stock or RHE Series A Preferred Stock.

Recommendation of the Board of Directors (See page 33)

The board of directors has unanimously adopted the merger agreement and determined the merger agreement and the transactions contemplated thereby advisable and in the best interests of AdCare and its shareholders and recommends that all holders of AdCare common stock entitled to vote thereon vote “FOR” the merger proposal.

The board of directors also unanimously recommends that all holders of AdCare common stock entitled to vote on the adjournment proposal vote “FOR” the adjournment proposal.

Date, Time, Place and Purpose of Special Meeting (See page 33)

The special meeting will be held on [ ], 2017 at [ ], local time, at the Sonesta Gwinnett Place Atlanta located at 1775 Pleasant Hill Road, Duluth, Georgia, to consider and vote upon the proposals described in the notice of special meeting.

Shareholders Entitled to Vote (See page 3)

The board of directors has fixed the close of business on [ ], 2017 as the record date for the determination of holders of record of AdCare common stock entitled to receive notice of, and to vote those shares by proxy or at, the special meeting. As of [ ], 2017, there were [ ] shares of common stock outstanding and entitled to vote and [ ] holders of record.

The holders of record of AdCare Series A Preferred Stock as of the record date are not entitled to vote on the proposals at the special meeting.

Vote Required (See page 33)

The affirmative vote of the holders of a majority of the outstanding shares of AdCare common stock entitled to vote is required for the approval of the merger agreement. Accordingly, abstentions and “broker non-votes”, if any, will have the effect of a vote against the proposal to adopt the merger agreement.

10

The board of directors reserves the right to cancel or defer the merger, even if the holders of AdCare common stock vote to adopt the merger agreement and the other conditions to the completion of the merger are satisfied or waived, if the board of directors determines that the merger is no longer in the best interests of AdCare and its shareholders.

The affirmative vote of the holders of a majority of the voting power of the shares of AdCare common stock present in person or represented by proxy at the meeting and entitled to vote is required to approve the adjournment of the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes at the time of the special meeting to approve the proposal to adopt the merger agreement.

No Dissenters’ Rights (See page 42)

Under the GBCC, you will not be entitled to any statutory dissenters’ rights in connection with the merger.

Shares Owned by AdCare’s Directors and Executive Officers (See page 105 )

As of [ ], 2017, the directors and executive officers of AdCare and their affiliates owned and were entitled to vote [ ] shares of AdCare common stock, or [ ]% of the shares outstanding on that date entitled to vote with respect to each of the proposals. We currently expect that each director and executive officer of AdCare will vote the shares of AdCare common stock beneficially owned by such director or executive officer “FOR” approval of the merger agreement and “FOR” the proposal to approve the adjournment of the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes at the time of the special meeting to approve the merger agreement.

Historical Market Price of Common Stock and Series A Preferred Stock

The AdCare common stock and AdCare Series A Preferred Stock are listed and traded on the NYSE MKT under the symbols “ADK” and “ADK.PRA”, respectively.

The following table sets forth for the calendar periods indicated the high and low sale prices per share of the AdCare common stock, the high and low sale prices per share of the AdCare Series A Preferred Stock, the declared dividend per share of AdCare common stock and the declared dividend per share of AdCare Series A Preferred Stock as reported by the NYSE MKT. On February 10, 2017, the last full trading day prior to the public announcement of the proposed merger, the closing sale price of AdCare common stock was $1.55 as reported by the NYSE MKT and the closing sale price per share of AdCare Series A Preferred Stock was $22.95 per share as reported on the NYSE MKT. On [ ], 2017, the latest practicable date before the printing of this proxy statement/prospectus, the closing sale price per share of AdCare common stock on the NYSE MKT was $[ ] per share and the closing sale price per share of AdCare Series A Preferred Stock was $[ ] per share. You should obtain a current stock price quotation for the AdCare common stock and the AdCare Series A Preferred Stock.

| AdCare Common Stock | AdCare Series A Preferred Stock | ||||||||||

| High | Low | Dividend Declared | High | Low | Dividend Declared | ||||||

| Year Ending December 31, 2017 | |||||||||||

| Second Quarter (through June 13, 2017) | $1.29 | $0.90 | --- | $23.32 | $21.00 | $0.68 | |||||

| First Quarter | $1.74 | $1.11 | --- | $23.73 | $21.86 | $0.68 | |||||

| Year Ended December 31, 2016 | |||||||||||

| Fourth Quarter | $2.20 | $1.38 | --- | $25.00 | $19.44 | $0.68 | |||||

| Third Quarter | $2.60 | $1.65 | --- | $23.50 | $20.00 | $0.68 | |||||

| Second Quarter | $2.50 | $1.71 | --- | $22.64 | $20.21 | $0.68 | |||||

| First Quarter | $2.70 | $1.85 | --- | $22.49 | $17.27 | $0.68 | |||||

| Year Ended December 31, 2015 | |||||||||||

| Fourth Quarter | $3.42 | $1.90 | --- | $24.01 | $17.51 | $0.68 | |||||

| Third Quarter | $4.00 | $3.10 | $0.060 | $25.91 | $19.35 | $0.68 | |||||

| Second Quarter | $4.45 | $3.32 | $0.055 | $29.64 | $24.53 | $0.68 | |||||

| First Quarter | $4.50 | $3.79 | $0.050 | $29.50 | $27.00 | $0.68 | |||||

11

It is expected that, immediately following the completion of the merger, RHE common stock and RHE Series A Preferred Stock will be listed and traded on the NYSE in the same manner as shares of AdCare common stock and AdCare Series A Preferred Stock. The current price of AdCare common stock and AdCare Series A Preferred Stock may not be indicative of the market price of RHE common stock or RHE Series A Preferred Stock following the merger.

We are a holding company, and we have no significant operations. We rely primarily on dividends and other distributions from our subsidiaries to us so we may, among other things, pay dividends on our common stock and Series A Preferred stock, if and to the extent declared by the board of directors. The ability of our subsidiaries to pay dividends and make other distributions to us depends on their earnings and may be restricted by the terms of certain agreements governing their indebtedness. If our subsidiaries are in default under such agreements, then they may not pay dividends or make other distributions to us.

In addition, we may only pay dividends on the common stock and the Series A Preferred Stock if we have funds legally available to pay dividends and such payment is not restricted or prohibited by law, the terms of any shares with higher priority with respect to dividends or any documents governing our indebtedness. We are restricted by Georgia law from paying dividends on the common stock and the Series A Preferred Stock if we are not able to pay our debts as they become due in the normal course of business or if our total assets would be less than the sum of our total liabilities plus the amount that would be needed to satisfy preferential rights upon dissolution of shareholders whose preferential rights are superior to those receiving the dividend. In addition, no cash dividends may be declared or paid on the common stock unless full cumulative dividends on the Series A Preferred Stock have been, or contemporaneously are, declared and paid, or declared and a sum sufficient for the payment thereof is set apart for payments, for all past dividend periods. In addition, future debt, contractual covenants or arrangements we or our subsidiaries enter into may restrict or prevent future dividend payments.

12

RISK FACTORS

In addition to the other information in this proxy statement/prospectus, you should carefully consider the specific factors discussed below, together with all the other information contained in this proxy statement/prospectus and the documents incorporated by reference herein. The risks described below are not the only risks that we face. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also impair our business operations. Any of these risks may have a material adverse effect on our business, financial condition, results of operations and cash flows.

Risks Related to the Delisting of Our Securities

If we fail to meet all applicable continued listing requirements of the NYSE MKT and the NYSE MKT determines to delist the common stock and Series A Preferred Stock, the delisting could adversely affect the market liquidity of such securities, impair the value of your investment, adversely affect our ability to raise needed funds and subject us to additional trading restrictions and regulations.

On April 18, 2016, the Company received notice from NYSE Regulation, Inc. (“NYSE Regulation”) that it is not in compliance with the Stockholders’ Equity Continued Listing Standards because the Company reported a stockholders’ deficit of $23.8 million as of December 31, 2015, and net losses for the last five fiscal years. See the section entitled “Questions and Answers About the Merger - Why are you reorganizing the corporate structure?”

As a result, the Company became subject to the procedures and requirements of Section 1009 of the NYSE MKT Company Guide and was required to submit a plan (a “Compliance Plan”) by May 18, 2016 describing the actions the Company has taken or will take to regain compliance with the Stockholders’ Equity Continued Listing Standards during the period ending October 18, 2017 (the “Plan Period”).The Company submitted a Compliance Plan by the May 18, 2016 deadline and was notified on June 2, 2016 that the NYSE Regulation had accepted the Compliance Plan.

During the Plan Period, the Company is subject to periodic review by NYSE MKT, and the common stock and Series A Preferred Stock will continue to be listed on the NYSE MKT pursuant to an extension granted by NYSE Regulation. If the Company is not in compliance with Stockholders’ Equity Continued Listing Standards by October 18, 2017, or if the Company does not make progress consistent with its Compliance Plan during the Plan Period, then NYSE Regulation will initiate delisting proceedings.

We are reorganizing our corporate structure in order to effectively adopt the transfer and ownership restrictions which, among other things, will position us to regain compliance with the Stockholders’ Equity Continued Listing Standards. If the common stock and Series A Preferred Stock are delisted from the NYSE MKT, such securities may trade in the over-the-counter market. If our securities were to trade on the over-the-counter market, selling the common stock and Series A Preferred Stock could be more difficult because smaller quantities of shares would likely be bought and sold, transactions could be delayed, and any security analysts’ coverage of us may be reduced. In addition, in the event the common stock and Series A Preferred Stock are delisted, broker-dealers have certain regulatory burdens imposed upon them, which may discourage broker-dealers from effecting transactions in such securities, further limiting the liquidity of the common stock and Series A Preferred Stock. These factors could result in lower prices and larger spreads in the bid and ask prices for our securities. Such delisting from the NYSE MKT and continued or further declines in our share price could also greatly impair our ability to raise additional necessary capital through equity or debt financing and could significantly increase the ownership dilution to shareholders caused by our issuing equity in financing or other transactions. Any such limitations on our ability to raise debt and equity capital could prevent us from making future investments and satisfying maturing debt commitments.

In addition, if the Company fails for 180 or more consecutive days to maintain a listing of the Series A Preferred Stock on a national exchange, then: (i) the annual dividend rate on the Series A Preferred Stock will be increased from 10.875% per annum to 12.875% per annum on the 181st day; and (ii) the holders of the Series A Preferred Stock will be entitled to vote for the election of two additional directors to serve on the board of directors. Such increased dividend rate and voting rights will continue for so long the Series A Preferred Stock is not listed on a national exchange.

Risks Related to the Ownership and Transfer Restrictions

The ownership and transfer restrictions may prevent or restrict you from acquiring or transferring shares of RHE common stock.

AdCare intends to merge with and into RHE to ensure the effective adoption of the charter provisions restricting the ownership and transfer of the RHE common stock. These ownership and transfer restrictions include that, subject to the exceptions,

13

waivers and the constructive ownership rules described in the RHE Charter, no person (including any “group” as defined in Section 13(d)(3) of the Exchange Act) may beneficially own, or be deemed to constructively own by virtue of the ownership attribution provisions of the Code, in excess of 9.9% (by value or number of shares, whichever is more restrictive) of the outstanding RHE common stock. The RHE Charter also prohibits, among other things, any person from beneficially or constructively owning shares of RHE common stock to the extent that such ownership would cause the Company to fail to qualify as a REIT by reason of being “closely held” under the Code (without regard to whether the ownership interest is held during the last half of a taxable year) or that would cause the Company to otherwise fail to qualify as a REIT. Furthermore, any transfer, acquisition or other event or transaction that would result in RHE common stock being beneficially owned by less than 100 persons (determined without reference to any rules of attribution) will be void ab initio, and the intended transferee shall acquire no rights in such common stock. See “Description of Capital Stock - Ownership and Transfer Restrictions.”

These ownership and transfer restrictions could have the effect of delaying, deferring or preventing a transaction or a change in control of us that might involve a premium price for our capital stock or otherwise be in the best interests of our shareholders.

There is no assurance that the Company will qualify as a REIT in a future taxable year or that, if it were to so qualify, that the board of directors would determine that electing REIT status would be in the best interest of the Company and its shareholders.

The Company does not currently qualify for REIT status under the Code, and the Company has certain structural and operational complexities which would need to be addressed before it could qualify as a REIT under the Code, including the disposition of certain assets or the termination of certain operations which may not be REIT compliant and otherwise effecting some internal reorganization. In addition, because the ownership and transfer restrictions will not apply to the Series A Preferred Stock, the restrictions will not assist us in complying with certain of the U.S. federal income tax rules applicable to REITs under the Code. See “Questions and Answers About the Merger - What are the requirements to qualify as a REIT under the Code?” Accordingly, among other things, the Series A Preferred Stock would need to be redeemed or its terms appropriately modified before the Company would elect REIT status under the Code.