UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO SECTION 13 OR 15(d) of

THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2018

Commission File Number: 333‑216725

ARD Finance S.A.

(Name of Registrant)

56, rue Charles Martel

L‑2134 Luxembourg, Luxembourg

+352 26 25 85 55

(Address of Principal Executive Offices)

David Matthews, Chief Financial Officer

56, rue Charles Martel, L-2134 Luxembourg, Luxembourg

+352 26 25 85 55

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| |

Title of each class | Name of each exchange on which registered |

None | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

7.125% / 7.875% Senior Secured Toggle Notes due 2023

6.625% / 7.375% Senior Secured Toggle Notes due 2023

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:None

Indicate by check mark if each registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act:

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if each registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether each registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “accelerated filer”, “large accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | |

Large Accelerated Filer ☐ | Accelerated Filer | ☐ | Non-Accelerated Filer☒ | Emerging growth company☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term ‘‘new or revised financial accounting standard’’ refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | |

U.S. GAAP ☐ | International Financial Reporting Standards as issued | Other ☐ |

| by the International Accounting Standards Board ☒ | |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 __ Item 18 __

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ☐ No ☒

Definitions and Terminology

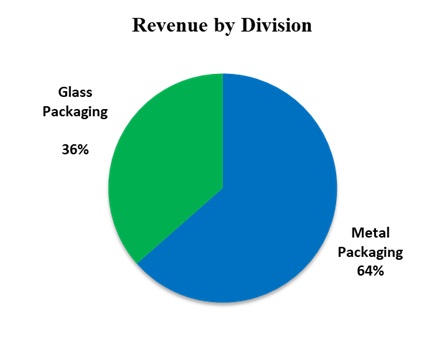

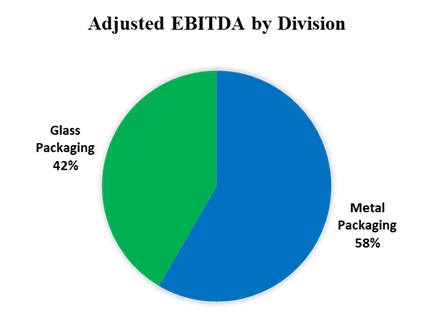

Except where the context otherwise requires or where otherwise indicated, all references to “ARD Finance”, “Company”, the “Group”, “ARD Finance Group”, “we”, “us” and “our” refer to ARD Finance S.A. and its consolidated subsidiaries, and all references to “Ardagh” and “Ardagh Group” refer to Ardagh Group S.A. and its consolidated subsidiaries. When we describe herein our business or operations, such business and operations are the business and operations of our subsidiary, Ardagh Group S.A., and its consolidated subsidiaries, since ARD Finance S.A. has no independent operations of its own, and, in such contexts, references to the “Group”, “we”, “us”, and “our” may refer to Ardagh Group S.A. and its subsidiaries. Ardagh Group’s operations have the following divisions: Metal Packaging and Glass Packaging.

References to legislation are, except where otherwise stated, references to legislation of the United States of America.

In addition, unless indicated otherwise, or the context otherwise requires, references in this annual report to:

| · | | “Articles” are to the Company’s articles of association; |

| · | | “Beverage Can Acquisition” are to the Ardagh Group’s acquisition of certain beverage can manufacturing assets from Ball Corporation and Rexam PLC on June 30, 2016; |

| · | | “Brexit” are to the United Kingdom’s withdrawal from the European Union; |

| · | | “CCIRS” are to cross currency interest rate swaps; |

| · | | “CERCLA” are to the U.S. federal Resource Conservation and Recovery Act and the Comprehensive Environmental Response, Compensation and Liability Act of 1980; |

| · | | “CGUs” are to cash generating units; |

| · | | “Code” are to the U.S. Internal Revenue Code of 1986, as amended; |

| · | | “CPGs” are to Consumer Packaged Goods companies; |

| · | | “CSDs” are to carbonated soft drinks; |

| · | | “EPA” are to the U.S. Environmental Protection Agency; |

| · | | “EU ETS” are to the EU Emissions Trading Scheme; |

| · | | “EWC” are to the European Works Council of Ardagh Group S.A.; |

| · | | “Exchange Act” are to the U.S. Securities Exchange Act of 1934, as amended; |

| · | | “FATCA” are to the U.S. Foreign Account Tax Compliance Act; |

| · | | “IAS” are to the International Accounting Standards; |

| · | | “IASB” are to the International Accounting Standards Board; |

| · | | “IED” are to the EU Industrial Emissions Directive; |

| · | | “IFRS” are to International Financial Reporting Standards; |

| · | | “IPO” are to the initial public offering of Ardagh Group S.A., which closed on March 20, 2017; |

| · | | “IRS” are to the U.S. Internal Revenue Service; |

| · | | “Lean” are to Lean Manufacturing techniques; |

| · | | “Luxembourg Law” are to the provisions of the laws of Luxembourg; |

| · | | “NYSE” are to the New York Stock Exchange; |

| · | | “Parent Company” are to ARD Holdings S.A. (“ARD Holdings”) and/or, where relevant, one or more of its subsidiaries; |

| · | | “PFIC” are to a passive foreign investment company; |

| · | | “PIK Interest” are to interest on the Toggle Notes for any interest period, which can be paid by the Company by increasing the principal amount of the PIK Notes or by issuing Notes in a principal amount equal to such interest; |

| · | | “PIK Notes” are, collectively, to the Ardagh Group’s euro denominated 8.375% Senior PIK Notes due 2019 (in an original issue amount of $250 million) and dollar denominated 8.625% Senior PIK Notes due 2019 (in an original issue amount of $710 million). On September 16, 2016, Ardagh Group repaid these Notes in full; |

| · | | “Ppm” are to parts per million; |

| · | | “REACH” are to the European Union’s regulations concerning the Registration, Evaluation, Authorization and Restriction of Chemicals; |

| · | | “Sarbanes Oxley Act” are to the U.S. Sarbanes Oxley Act of 2002; |

| · | | “Shareholder Agreement” are to the shareholder agreement dated March 20, 2017, entered into between ARD Holdings and Ardagh Group S.A.; |

| · | | “Toggle Notes” are to the Company’s Dollar Toggle Notes and Euro Toggle Notes, the terms of which are classified in full in the Company’s Form F-4 Registration Statement (File No. 333-216725) filed on April 12, 2017; |

| · | | U.S. GAAP are to the Generally Accepted Accounting Principles in the U.S.; |

| · | | “VNA Acquisition” are to the acquisition in 2014 of Verallia North America; and |

| · | | “VNA” are to the Ardagh Group's U.S. glass business, formerly Verallia North America. |

General Information

ARD Finance S.A. (the “Company”) was incorporated under the laws of Luxembourg on May 6, 2011 and is a subsidiary of ARD Holdings S.A. The Company’s registered office is 56, rue Charles Martel, L-2134 Luxembourg, Luxembourg. The Company is registered with the R.C. S. Luxembourg under number B 160806.

The Company is a holding company whose only significant assets as of December 31, 2018 consist of its direct and indirect interest in the share capital of Ardagh Group S.A., a company incorporated and existing under the laws of Luxembourg, and certain related party receivables. Ardagh Group S.A. has Class A common shares listed on the New York Stock Exchange.

Group Consolidated Financial Statements – Basis of Preparation

The consolidated financial statements of the Group have been prepared in accordance with, and are in compliance with IFRS and related interpretations, as adopted by the IASB. IFRS is comprised of standards and interpretations approved by the IASB and IAS and interpretations approved by the predecessor International Accounting Standards Committee that have been subsequently approved by the IASB and remain in effect. References to IFRS hereafter should be construed as references to IFRS as adopted by the IASB.

The consolidated financial statements are presented in U.S. dollar, rounded to the nearest million, and have been prepared under the historical cost convention except, for the following:

| · | | derivative financial instruments are stated at fair value; and |

| · | | employee benefit obligations are measured at the present value of the future estimated cash flows related to benefits earned and pension assets valued at fair value. |

The preparation of consolidated financial information in conformity with IFRS requires the use of critical accounting estimates and assumptions that affect the reported amounts of assets and liabilities and income and expenses. It also requires management to exercise judgment in the process of applying Group accounting policies. These estimates, assumptions and judgments are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances and are subject to continual re-evaluation. However, actual outcomes may differ from these estimates. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements are discussed in the critical accounting estimates, assumptions and judgment.

The consolidated financial statements for the Group were authorized for issue by the board of directors of ARD Finance S.A. on February 20, 2019.

Currencies

In this annual report, unless otherwise specified or the context otherwise requires:

| · | | “$” and “U.S. dollar” each refer to the United States dollar; |

| · | | “€”, “EUR” and “euro” each refer to the euro, the single currency established for members of the European Economic and Monetary Union since January 1, 1999; and |

| · | | “£”, “pounds”, “sterling” and “GBP” refer to pounds sterling, the lawful currency of the United Kingdom. |

With effect from January 1, 2018, the Group changed the currency in which it presents its financial statements from euro to U.S. dollar. This was principally as a result of the board of directors’ assessment that this change in presentation currency will help provide a clearer understanding of the Group’s financial performance and improve comparability of our performance to our peers following the IPO of Ardagh Group S.A. on the NYSE.

The change in our accounting policy impacts all financial statement line items whereby amounts previously reported in euro have been re-presented in U.S. dollar. To illustrate the effect of the re-presentation the previously reported euro consolidated statements of financial position as at December 31, 2017, 2016, 2015 and 2014, consolidated income statements, consolidated statements of comprehensive income and consolidated statements of cash flows for the years ended December 31, 2017, 2016 and 2015 have been set out in Note 26 to the consolidated financial statements.

Safe Harbour Statement

This annual report does not constitute or form part of any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities, including in the United States, nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Specifically, this annual report does not constitute a “prospectus” within the meaning of the U.S. Securities Act of 1933.

The Company routinely posts important information on the Parent Company’s website – http://www.ardholdings-sa.com. This website and the information contained therein or connected thereto shall not be deemed to be incorporated into this annual report.

Forward-Looking Statements

This annual report may contain "forward-looking" statements within the meaning of Section 21E of the Exchange Act and Section 27A of the U.S. Securities Act of 1933. Forward-looking statements reflect the Company’s current expectations and projections about future events at the time, and thus involve uncertainty and risk. The words “believe,” “expect,” “anticipate,” “will,” “could,” “would,” “should,” “may,” “plan,” “estimate,” “intend,” “predict,” “potential,” “continue,” and the negatives of these words and other similar expressions generally identify forward-looking statements. It is possible the Company's future financial performance may differ from expectations due to a variety of factors including, but not limited to, the following:

(i) global and regional economic downturn; (ii) competition from other metal and glass packaging producers and manufacturers of alternative forms of packaging; (iii) increases in metal and glass container manufacturing capacity; (iv) the Company’s inability to maintain relationships with its largest customers or suppliers; (v) less than expected levels of demand; (vi) varied seasonal demands, climate and water conditions, and the availability and cost of raw materials; (vii) currency and interest rate fluctuations; (viii) various environmental requirements; (ix) the Company’s ability to integrate acquired businesses and achieve expected operating efficiencies, cost savings and other synergies; (x) costs associated with post-retirement and post-employment obligations; (xi) operating hazards or unanticipated interruptions at our manufacturing facilities, including labor strikes or work stoppages; (xii) retention of executive and senior management.

Any forward-looking statements in this document are based on certain assumptions and analyses made by the Company in light of its experience and perception of historical trends, current conditions, expected future developments, and other factors it believes are appropriate in the circumstances. Forward-looking statements are not a guarantee of future performance and actual results or developments may differ materially from expectations. While the Company continually reviews trends and uncertainties affecting the Company's results of operations and financial condition, the Company does not assume any obligation to update or supplement any particular forward-looking statements contained in this document.

Non-GAAP Financial Measures

This annual report may contain certain consolidated financial measures such as Adjusted EBITDA, working capital, operating cash flow, Adjusted free cash flow, net debt, Adjusted profit/(loss), and ratios relating thereto that are not calculated in accordance with IFRS or U.S. GAAP. Adjusted EBITDA consists of profit/(loss) for the year before income tax expense/(credit), net finance expense, depreciation and amortization and exceptional operating items.

Non-GAAP financial measures may be considered in addition to GAAP financial information, but should not be used as substitutes for the corresponding GAAP measures. The non-GAAP financial measures used by the Company may differ from, and not be comparable to, similarly titled measures used by other companies.

Part I

Item 1. Identity of Directors, Senior Management and Advisors

Not Applicable

Item 2. Offer Statistics and Expected Timetable

Not Applicable

Item 3. Key Information

| A. | | Selected financial data |

Summary Consolidated Financial and Other Data of ARD Finance S.A.

The financial data of ARD Finance S.A. as of and for the years ended December 31, 2018, 2017 and 2016 and as of December 31, 2015, are derived from the audited consolidated financial statements included in this annual report. The financial data for the year ended December 31, 2014 has been derived from our unaudited consolidated financial statements (which are unaudited as they were re-presented following the change in accounting policy as described in Note 2 to the consolidated financial statements included in this annual report). The summary historical financial data for the year ended December 31, 2014 has been translated from euro to U.S. dollar using the foreign exchange rate at the balance sheet date, or an average rate for the year, as appropriate.

The summary historical financial data set forth below should be read in conjunction with and is qualified in its entirety by reference to the audited consolidated financial statements included in this annual report and the related notes thereto. The following financial data should also be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” also included in this annual report. Our historical results are not necessarily indicative of results to be expected in any future period.

| | | | | | | | | | | |

| | Year ended | |

| | December 31, | |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 | |

Income Statement Data (1) | | (in $ millions except margins and per share data) | |

Revenue | | 9,097 | | 8,596 | | 7,014 | | 5,795 | | 6,316 | |

Cost of sales | | (7,778) | | (7,210) | | (5,786) | | (4,817) | | (5,454) | |

Gross profit | | 1,319 | | 1,386 | | 1,228 | | 978 | | 862 | |

Sales, general and administration expenses | | (433) | | (450) | | (462) | | (353) | | (377) | |

Intangible amortization | | (451) | | (264) | | (191) | | (122) | | (160) | |

Loss on disposal of business | | — | | — | | — | | — | | (214) | |

Operating profit | | 435 | | 672 | | 575 | | 503 | | 111 | |

Net finance expense | | (654) | | (671) | | (681) | | (590) | | (880) | |

(Loss)/profit before tax | | (219) | | 1 | | (106) | | (87) | | (769) | |

Income tax (charge)/credit | | (44) | | 40 | | (66) | | (48) | | 10 | |

(Loss)/profit for the year | | (263) | | 41 | | (172) | | (135) | | (759) | |

| | | | | | | | | | | |

Balance Sheet Data (at year end) | | | | | | | | | | | |

Cash and cash equivalents (2) | | 565 | | 823 | | 818 | | 603 | | 526 | |

Working capital (3) | | 425 | | 566 | | 708 | | 599 | | 738 | |

Total assets | | 10,349 | | 11,191 | | 10,851 | | 6,902 | | 7,425 | |

Net liabilities | | (3,240) | | (3,142) | | (3,150) | | (2,582) | | (2,603) | |

Issued share capital | | — | | — | | — | | — | | — | |

Net borrowings (4) | | 9,605 | | 10,076 | | 10,232 | | 6,972 | | 7,331 | |

Net debt (5) | | 9,153 | | 9,554 | | 9,283 | | 6,369 | | 7,808 | |

| | | | | | | | | | | |

Other Data | | | | | | | | | | | |

Adjusted EBITDA (6) | | 1,478 | | 1,508 | | 1,281 | | 1,041 | | 1,060 | |

Adjusted EBITDA Margin (6) | | 16.2 | % | 17.5 | % | 18.3 | % | 18.0 | % | 16.8 | % |

Adjusted profit/(loss) for the year (7) | | 237 | | 401 | | 155 | | 15 | | (86) | |

Depreciation and amortization (8) | | 714 | | 687 | | 561 | | 449 | | 485 | |

Capital expenditure (9) | | 575 | | 492 | | 351 | | 339 | | 419 | |

Net cash from operating activities | | 734 | | 847 | | 515 | | 633 | | 467 | |

| (1) | | The income statement data presented above is on a reported basis and includes certain exceptional items which, by their incidence or nature, management considers should be adjusted for to enable a better understanding of the financial performance of the Company. A summary of these exceptional items included in the income statement data is as follows: |

| | | | | | | | | | |

| | Year ended |

| | December 31, |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Exceptional Items | | (in $ millions) |

Exceptional cost of sales | | 124 | | 100 | | 15 | | 41 | | 160 |

Exceptional sales, general and administrative expenses | | 19 | | 49 | | 130 | | 48 | | 49 |

Exceptional impairment - goodwill | | 186 | | — | | — | | — | | 41 |

Exceptional loss on disposal of business | | — | | — | | — | | — | | 214 |

Exceptional operating items | | 329 | | 149 | | 145 | | 89 | | 464 |

Exceptional net finance expense | | 28 | | 132 | | 97 | | 15 | | 234 |

Exceptional income tax credit | | (54) | | (138) | | (49) | | (36) | | (107) |

Total exceptional items net of tax | | 303 | | 143 | | 193 | | 68 | | 591 |

For further details on the exceptional items for the years ended December 31, 2018, 2017, and 2016, see Note 4 and Note 6 to the consolidated financial statements of ARD Finance included elsewhere in this annual report.

| (2) | | Cash and cash equivalents include restricted cash as per the note disclosures to the consolidated financial statements included in this annual report. |

| (3) | | Working capital is comprised of inventories, trade and other receivables, contract assets, trade and other payables and current provisions. Other companies may calculate working capital in a manner different to ours. |

| | | | | | | | | | |

| | Year ended |

| | December 31, |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

| | (in $ millions) |

Inventories | | 1,284 | | 1,353 | | 1,186 | | 898 | | 935 |

Trade and other receivables | | 1,053 | | 1,274 | | 1,227 | | 709 | | 840 |

Contract asset | | 160 | | — | | — | | — | | — |

Trade and other payables | | (1,984) | | (1,991) | | (1,632) | | (956) | | (976) |

Current provisions | | (88) | | (70) | | (73) | | (52) | | (61) |

Working capital | | 425 | | 566 | | 708 | | 599 | | 738 |

| (4) | | Net borrowings comprises non‑current and current borrowings, net of deferred debt issue costs and bond premium/discount. |

| (5) | | Net debt is comprised of net borrowings and derivative financial instruments used to hedge foreign currency and interest rate risk, net of cash and cash equivalents. |

| (6) | | To supplement our financial information presented in accordance with IFRS, we use the following additional financial measures to clarify and enhance an understanding of past performance: Adjusted EBITDA, Adjusted EBITDA margin, and Adjusted profit. We believe that the presentation of these financial measures enhances an investor’s understanding of our financial performance. We further believe that these financial measures are useful financial metrics to assess our operating performance from period to period by excluding certain items that we believe are not representative of |

our core business. We use certain of these financial measures for business planning purposes and in measuring our performance relative to that of our competitors. |

Adjusted EBITDA consists of profit/(loss) for the year before income tax expense/(credit), net finance expense, depreciation and amortization and exceptional operating items. Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by revenue. Adjusted EBITDA and Adjusted EBITDA margin are presented because we believe that they are frequently used by securities analysts, investors and other interested parties in evaluating companies in the packaging industry. However, other companies may calculate Adjusted EBITDA and Adjusted EBITDA margin in a manner different from ours. Adjusted EBITDA and Adjusted EBITDA margin are not measurements of financial performance under IFRS and should not be considered an alternative to profit/(loss) as indicators of operating performance or any other measures of performance derived in accordance with IFRS.

The reconciliation of (loss)/profit for the year to Adjusted EBITDA is as follows:

| | | | | | | | | | |

| | Year ended |

| | December 31, |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

| | (in $ millions) |

(Loss)/profit for the year | | (263) | | 41 | | (172) | | (135) | | (759) |

Income tax expense/(credit) | | 44 | | (40) | | 66 | | 48 | | (10) |

Net finance expense | | 654 | | 671 | | 681 | | 590 | | 880 |

Depreciation and amortization | | 714 | | 687 | | 561 | | 449 | | 485 |

EBITDA | | 1,149 | | 1,359 | | 1,136 | | 952 | | 596 |

Exceptional operating items | | 329 | | 149 | | 145 | | 89 | | 464 |

Adjusted EBITDA | | 1,478 | | 1,508 | | 1,281 | | 1,041 | | 1,060 |

| (7) | | Adjusted profit/(loss) for the year is calculated as follows: |

| | | | | | | | | | |

| | Year ended |

| | December 31, |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

| | (in $ millions) |

(Loss)/profit for the year | | (263) | | 41 | | (172) | | (135) | | (759) |

Total exceptional items | | 303 | | 143 | | 193 | | 68 | | 591 |

Intangible amortization | | 265 | | 264 | | 191 | | 122 | | 119 |

Tax credit associated with intangible amortization | | (58) | | (75) | | (57) | | (40) | | (37) |

(Gain)/loss on derivatives | | (10) | | 28 | | — | | — | | — |

Adjusted profit/(loss) for the year | | 237 | | 401 | | 155 | | 15 | | (86) |

Adjusted profit consists of profit/(loss) for the year before total exceptional items (net of tax), (gain)/loss on derivatives, intangible amortization and associated tax credits. Adjusted profit is presented because we believe that it accurately reflects the ongoing cost structure of the company. It excludes total exceptional items and (gain)/loss on derivatives which we consider not representative of ongoing operations because such items are not reflective of the normal earnings potential of the business. We have also adjusted for the amortization of intangible assets and associated tax credits, as this is driven by our acquisition activity which can vary in size, nature and timing compared to other companies within our industry and from period to period. Accordingly, due to the incomparability of acquisition activity among companies and from period to period, we believe exclusion of the amortization associated with intangible assets acquired through our acquisitions and total exceptional items allows investors to better compare and understand our results.

| (8) | | Depreciation, amortization, and gain/(loss) on disposal of property, plant and equipment. |

| (9) | | Capital expenditure is the sum of purchase of property, plant and equipment and software and other intangibles, net of proceeds from disposal of property, plant and equipment. |

| B. | | Capitalization and indebtedness |

Not Applicable

| C. | | Reasons for the offer and use of proceeds |

Not Applicable

When we describe our business or operations in this “Risk Factors” section, such business and operations are the business and operations of our subsidiary, Ardagh Group S.A., and its consolidated subsidiaries, since ARD Finance S.A. has no independent operations of its own. Our business, financial condition, or results of operations could be materially adversely affected by one or more of the risks and uncertainties described below:

Risks Relating to Our Business

Our customers sell to consumers of food & beverages, personal care, household products and pharmaceuticals. If economic conditions affect consumer demand, our customers may be affected and so reduce the demand for our products.

Demand for our packaging depends on demand for the products which use our packaging, which is primarily consumer driven. General economic conditions may adversely impact consumer confidence resulting in reduced spending on our customers’ products and, thereby, reduced or postponed demand for our products.

Adverse economic conditions may also lead to more limited availability of credit, which may have a negative impact on the financial condition, particularly on the purchasing ability, of some of our customers and distributors and may also result in requests for extended payment terms, and result in credit losses, insolvencies and diminished sales channels available to us. Our suppliers may have difficulties obtaining necessary credit, which could jeopardize their ability to provide timely deliveries of raw materials and other essentials to us. The adverse economic conditions may also lead to suppliers requesting credit support or otherwise reducing credit, which may have a negative effect on our cash flows and working capital.

Volatility in exchange rates may also increase the costs of our products that we may not be able to pass on to our customers; impair the purchasing power of our customers in different markets; result in significant competitive benefit to certain of our competitors who incur a material part of their costs in other currencies than we do; hamper our pricing; and increase our hedging costs and limit our ability to hedge our exchange rate exposure.

Changes in global economic conditions may reduce our ability to forecast developments in our industry and plan our operations and costs, resulting in operational inefficiencies. Negative developments in our business, results of operations and financial condition due to changes in global economic conditions or other factors could cause ratings agencies to lower the credit ratings, or ratings outlook, of our short‑ and long‑term debt and, consequently, impair our ability to raise new financing or refinance our current borrowings and increase our costs of issuing any new debt instruments.

Furthermore, the economic outlook could be adversely affected by the risk that one or more eurozone countries could leave the European Monetary Union, or the euro as the single currency of the eurozone could cease to exist. Any of these developments, or the perception that any of these developments are likely to occur, could have a material adverse effect on the economic development of the affected countries and could lead to severe economic recession or depression, and a general anticipation that such risks will materialize in the future could jeopardize the stability of financial markets or the overall financial and monetary system. This, in turn, would have a material adverse effect on our business, financial position, liquidity and results of operations.

In addition, some segments of our markets are more cyclical than others. Our sales in the paints and coatings markets depend mainly on the building and construction industries and the do‑it‑yourself home decorating market. Demand in these markets is cyclical, as to a lesser extent is demand for products such as aerosols. Variations in the demand for

packaging products in these market segments could have a material adverse effect on our business, financial condition and results of operations.

We face intense competition from other metal and glass packaging producers, as well as from manufacturers of alternative forms of packaging.

Metal Packaging

The metal packaging sectors in which Metal Packaging operates are mature, experiencing limited growth in demand in recent years, and competitive. The most competitive part of the metal packaging market is the sale of undifferentiated, standardized food cans. Prices for these products are primarily driven by raw material costs and seasonal capacity, and price competition is sometimes fierce. Competition in the market for customized, differentiated packaging is based on price and, increasingly, on innovation, design, quality and service. Our principal competitors include Ball Corporation, Crown Holdings, Silgan Holdings and Can Pack. To the extent that any one or more of our competitors become more successful with respect to any key competitive factor, our ability to attract and retain customers could be materially and adversely affected, which could have a material adverse effect on our business.

Metal Packaging is subject to substantial competition from producers of packaging made from plastic, carton and composites, particularly from producers of plastic packaging and flexible packaging. Changes in consumer preferences in terms of food processing (e.g., fresh or frozen food content and dry versus wet pet food) or in terms of packaging materials, style and product presentation can significantly influence sales. An increase in Metal Packaging’s costs of production or a decrease in the costs of, or a further increase in consumer demand for, alternative packaging could have a material adverse effect on our business, financial condition and results of operations.

Glass Packaging

Glass Packaging is subject to intense competition from other glass packaging producers, as well as from producers of other forms of rigid and non‑rigid packaging, against whom we compete on the basis of price, product characteristics, quality, customer service, reliability of delivery and the overall attractiveness of our offering. Advantages or disadvantages in any of these competitive factors may be sufficient to cause customers to consider changing suppliers or to use an alternative form of packaging. In some instances, we also face the threat of vertical integration by our customers into the manufacture of their own packaging materials.

Our principal competitors in glass packaging include Anchor Glass and Owens‑Illinois in North America and Owens‑Illinois, Verallia and Vidrala in Europe. Additionally, we face competition from firms that carry out specific export operations at low prices when their domestic markets are at overcapacity or when foreign exchange rates or economic conditions (particularly transport costs) allow this, such as has been seen with the importing of glass containers into the United States from lower cost countries. Despite the generally regional nature of the glass packaging markets, these export operations could have a material negative impact on our business, financial condition and results of operations.

In addition to competing with other large, well‑established manufacturers in the glass packaging industry, we also compete with manufacturers of other forms of rigid packaging, principally plastic packaging and aluminum cans, on the basis of quality, price, service and consumer preference. We also compete with manufacturers of non‑rigid packaging alternatives, including flexible pouches and aseptic cartons, particularly in serving the packaging needs of non‑alcoholic beverage customers, including juice customers and food customers. We believe that the use of glass packaging for alcoholic and non‑alcoholic beverages is subject to consumer taste. In addition, the association of glass packaging with premium items in certain product categories exposes glass packaging to economic variations. Therefore, if economic conditions are poor, we believe that consumers may be less likely to prefer glass packaging over other forms of packaging. We cannot ensure that our products will continue to be preferred by end consumers and that consumer preference will not shift from glass packaging to alternative packaging. A material shift in consumer preference away from glass packaging, or competitive pressures from our various competitors, could result in a decline in sales volume or pricing pressure that would have a material adverse effect on our business, financial condition and results of operations. Furthermore, new threats from container and production innovations in all forms of packaging could disadvantage our existing business. If we are unable to respond to competitive technological advances, our future performance could be materially adversely affected.

Some customers meet some of their metal and glass packaging requirements through self-manufacturing, reducing their external purchases of packaging. In metal packaging, for example, AB InBev manufactures metal packaging through its Metal Container Corporation subsidiary in the United States. In glass packaging, companies which satisfy some of their requirements through self-manufacture include AB InBev and Gallo, which manufacture glass packaging in the United States, and AB InBev and Constellation Brands, which produce glass packaging in Mexico. The potential vertical integration of our customers could introduce new production capacity in the market, which may create an imbalance between glass packaging supply and demand. The growth of vertically integrated operations could have a material negative impact on our future performance.

An increase in metal or glass container manufacturing capacity without a corresponding increase in demand for metal or glass packaging could cause prices to decline, which could have a material adverse effect on our business, financial condition and results of operations.

The profitability of metal or glass packaging companies is heavily influenced by the supply of, and demand for, metal or glass packaging.

We cannot assure you that metal or glass container manufacturing capacity in any of our markets will not increase further in the future, nor can we assure you that demand for metal or glass packaging will meet or exceed supply. If metal or glass container manufacturing capacity increases and there is no corresponding increase in demand, the prices we receive for our products could materially decline, which could have a material adverse effect on our business, financial condition and results of operations.

Because our customers are concentrated, our business could be adversely affected if we were unable to maintain relationships with our largest customers.

For the year ended December 31, 2018, Metal Packaging’s ten largest customers accounted for approximately 42% of its consolidated revenues. For the year ended December 31, 2018, Glass Packaging’s ten largest customers accounted for approximately 43% of its revenues.

We believe our relationships with these customers are good, but there can be no assurance that we will be able to maintain these relationships. For Metal Packaging, approximately two‑thirds of revenues for the year ended December 31, 2018, were under multi‑year supply agreements of varying terms between two and ten years, with the remaining revenues generally under one-year agreements. For Glass Packaging, we also typically sell most of our glass packaging directly to customers under one- to five‑year arrangements. Although these arrangements have provided, and we expect they will continue to provide, the basis for long‑term partnerships with our customers, there can be no assurance that our customers will not cease purchasing our products. If our customers unexpectedly reduce the amount of glass packaging and/or metal cans they purchase from us, or cease purchasing our glass packaging and/or metal cans altogether, our revenues could decrease and our inventory levels could increase, both of which could have an adverse effect on our business, financial condition and results of operations. In addition, while we believe that the arrangements that we have with our customers will be renewed, there can be no assurance that such arrangements will be renewed upon their expiration or that the terms of any renewal will be as favorable to us as the terms of the current arrangements. There is also the risk that our customers may shift their filling operations to locations in which we do not operate. The loss of one or more of these customers, a significant reduction in sales to these customers or a significant change in the commercial terms of our relationship with these customers could have a material adverse effect on our business.

The continuing consolidation of our customer base may intensify pricing pressures or result in the loss of customers, either of which could have a material adverse effect on our business, financial condition and results of operations.

Some of our largest customers have acquired companies with similar or complementary product lines. For example, in 2017 Reckitt Benckiser merged with Mead Johnson Nutrition Company, in 2016 AB InBev acquired SABMiller and in 2015 Kraft Foods Group merged with H.J. Heinz Holding Corporation. Such consolidation has increased the concentration of our net sales with our largest customers and may continue in the future. In many cases, such consolidation may be accompanied by pressure from customers for lower prices. Increased pricing pressures from our customers may have a material adverse effect on our business, financial condition and results of operations. In addition, this consolidation may lead manufacturers to rely on a reduced number of suppliers. If, following the consolidation of one

of our customers with another company, a competitor was to be the main supplier to the consolidated companies, this could have a material adverse effect on our business, financial condition or results of operations.

A significant write down of goodwill would have a material adverse effect on our financial condition and results of operations.

Goodwill at December 31, 2018 totaled $2.0 billion. The Company evaluates goodwill annually (or more frequently if impairment indicators arise) for impairment. The valuation methods used include those requiring the use of a weighted average cost of capital to calculate the present value of the expected future cash flows of the Company’s groups of cash generating units. Future changes in the cost of capital, expected cash flows, or other factors may cause the Company’s goodwill to be impaired, resulting in a non‑cash charge against results of operations to write down goodwill for the amount of the impairment. If a significant write down is required, the charge would have a material adverse effect on the Company’s financial condition and results of operations.

Our profitability could be affected by varied seasonal demands.

Demand for Metal Packaging and Glass Packaging products is seasonal. Metal Packaging’s sales are typically greater in the second and third quarters of the year, with generally lower sales in the first and fourth quarters. Unseasonably cool weather during the summer months can reduce demand for certain beverages packaged in its beverage cans. Weather conditions can reduce crop yields and adversely affect customer demand for fruit and vegetable cans. Metal Packaging’s worldwide seafood canning activities are also affected by variations in local fish catches. The variable nature of the food and seafood packaging businesses and Metal Packaging’s vulnerability to natural conditions could have a material adverse effect on our business, financial condition and results of operations.

Demand for our Glass Packaging products is typically strongest during the summer months and in the period prior to the holidays in December because of the seasonal nature of the consumption of beer and other beverages. Unseasonably cool weather during the summer months can reduce demand for certain beverages packaged in our glass packaging, which could have a material adverse effect on our business, financial condition and results of operations. In addition, we generally schedule shutdowns of our furnaces for rebuilding and repairs of machinery in the first quarter in Europe and around year‑end and the first quarter in North America. If demand for glass packaging should unexpectedly rise during such a shutdown, we would not have the ability to fulfill such demand and may lose potential revenues. These shutdowns and seasonal sales patterns could have a material adverse effect on profitability during the first quarter.

Our profitability could be affected by the availability and cost of raw materials including as a result of changes in tariffs and duties.

The raw materials that we use have historically been available in adequate supply from multiple sources. For certain raw materials, however, there may be temporary shortages due to weather, transportation, production delays or other factors. In such an event, no assurance can be given that we would be able to secure our raw materials from sources other than our current suppliers on terms as favorable as our current terms, or at all. Any such shortages, as well as material increases in the cost of any of the principal raw materials that we use, including the introduction of new tariffs, such as, in 2018, with the introduction of tariffs of 25% on steel and 10% on aluminum in the United States. Further tariffs, duties or other increases in the cost to transport materials to our production facilities, could have a material adverse effect on our business, financial condition and results of operations. Furthermore, the relative price of oil and its products may impact our business, by affecting transport, lacquer and ink costs.

The primary raw materials that we use for Metal Packaging are aluminum ingot and steel (both in tinplate and tin‑free forms). Aluminum ingot is traded daily as a commodity on the London Metal Exchange, which has historically been subject to significant price volatility. Because aluminum is priced in U.S. dollar, fluctuations in the U.S. dollar/euro rate also affect the euro cost of aluminum ingot.

Our business is exposed to both the availability of aluminum and the volatility of aluminum prices, including associated premia. While raw materials are generally available from independent suppliers, raw materials are subject to fluctuations in price and availability attributable to a number of factors, including general economic conditions, commodity price fluctuations (with respect to aluminum on the London Metal Exchange), the demand by other industries for the same

raw materials and the availability of complementary and substitute materials. Adverse economic or financial changes could impact our suppliers, thereby causing supply shortages or increasing costs for our business.

Steel is generally obtained under one‑year contracts with prices that are usually fixed in advance. When such contracts are renewed in the future, our steel costs under such contracts will be subject to prevailing global steel and/or tinplate prices at the time of renewal, which may be different from historical prices. In contrast to aluminum, the hedging market for steel, and in particular that for coking coal, is a relatively new market which does not have the depth of the aluminum market and as a consequence, there might be limitations to place hedges in the market.

We may not be able to pass on all or substantially all raw material price increases, now or in the future. In addition, we may not be able to hedge successfully against raw material cost increases. Furthermore, aluminum and steel prices are subject to considerable volatility in price and demand. While in the past sufficient quantities of aluminum and steel have been generally available for purchase, these quantities may not be available in the future, and, even if available, we may not be able to continue to purchase them at current prices. Further increases in the cost of these raw materials could adversely affect our operating margins and cash flows.

The supplier industries from which Metal Packaging receives its raw materials are relatively concentrated, and this concentration can impact raw material costs. Over the last ten years, the number of major aluminum and steel suppliers has decreased and there remains the possibility of further consolidation among steel suppliers. Further consolidation could hinder our ability to obtain adequate supplies of these raw materials and could lead to higher prices for aluminum and tinplate.

Glass Packaging also consumes significant amounts of raw materials in the manufacturing process, in particular, glass sand, limestone and soda ash (natural or synthetic). Crushed recycled glass (“cullet”) is also a key raw material that is used in variable percentages, depending on the type of glass manufactured and the availability of cullet in a particular market. The combination of higher energy prices and a tight supply market has resulted in a significant increase in price for soda ash. Increases in demand without corresponding increases in supply is putting pressure not only on soda ash, but also on some other raw materials. The price of cullet varies widely from one region to another and is dependent on a number of factors, including glass collection and its effectiveness and the distance of our production sites to population centres where the waste glass is generated. Changes in regulations related to glass collection and recycling can have a significant impact on the availability of cullet and on its price. Any significant increase in the price of the raw materials we use to manufacture glass could have a material negative impact on our business, financial condition and results of operations.

The failure to obtain adequate supplies of raw materials or future price increases could have a material adverse effect on our business, financial condition and results of operations.

Currency, interest rate fluctuations and commodity prices may have a material impact on our business.

Our functional currency is the euro and we present our financial information in U.S. dollar. Insofar as possible, we actively manage currency exposures through the deployment of assets and liabilities throughout the Group and, when necessary and economically justified, enter into currency hedging arrangements to manage our exposure to foreign currency fluctuations by hedging against rate changes with respect to our functional currency, the euro. However, we may not be successful in limiting such exposure, which could adversely affect our business, financial condition and results of operations. In addition, our presented results may be impacted as a result of fluctuations in the U.S. dollar exchange rate versus the euro.

Metal Packaging has production facilities in 21 different countries worldwide. It also sells products to, and obtains raw materials from, companies located in these and different regions and countries globally. As a consequence, a significant portion of consolidated revenue, costs, assets and liabilities of Metal Packaging are denominated in currencies other than the euro, particularly the U.S. dollar, the pound and Brazilian real. The exchange rates between the currencies which we are exposed to, such as the euro, the U.S. dollar, the pound and the Brazilian real, have fluctuated significantly in the past and may continue to do so in the future.

Metal Packaging incurs currency transaction risks primarily on metal purchases (or the hedging of those purchases), as metal prices are denominated in U.S. dollars, and on revenue denominated in currencies other than the euro fulfilled from euro‑participant territories (or the hedging of those sales).

A substantial portion of the assets, liabilities, revenues and expenses of Glass Packaging is denominated in U.S. dollars, pounds, Swedish krona, Danish krone and Polish zloty. Fluctuations in the value of these currencies with respect to the euro have had, and may continue to have, a significant impact on our financial condition and results of operations.

For the year ended December 31, 2018, 64% of our revenues were to countries with currencies other than the euro.

In addition to currency translation risk, we are subject to currency transaction risk. Our policy is, where practical, to match net investments in foreign currencies with borrowings in the same currency. The debt and interest payments relating to our Swedish, Danish and Polish operations are all denominated in euro. Fluctuations in the value of these currencies with respect to the euro may have a significant impact on our financial condition and results of operations.

Changes in exchange rates can affect our ability to purchase raw materials and sell products at profitable prices, reduce the value of our assets and revenues, and increase liabilities and costs.

We are also exposed to interest rate risk. Fluctuations in interest rates may affect our interest expense on existing debt and the cost of new financing. We occasionally use CCIRS to manage this risk, but sustained increases in interest rates could nevertheless materially adversely affect our business, financial condition and results of operations.

In addition, we are exposed to movements in the price of natural gas. We try to ensure that natural gas prices are fixed for future periods but do not always do so because the future prices can be far in excess of the spot price. We do not use commodity futures contracts to limit the fluctuations in prices paid and the potential volatility in earnings and cash flows from future market price movements.

For a further discussion of these matters and the measures we have taken to seek to protect our business against these risks, see “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk”.

It is difficult to compare our results of operations from period to period.

It is difficult to make period‑to‑period comparisons of our results of operations. Our business has been created as a result of a series of acquisitions and other corporate transactions over many years. These acquisitions have had a positive effect on our results of operations in periods following their completion and integration. Furthermore, our sales and, therefore, our net operating income are variable within the fiscal year due to the seasonality described above. Thus, a period‑to‑period comparison of our results of operations may not be meaningful.

Interrupted energy supplies and higher energy costs may have a material adverse effect on our business.

We use natural gas, electrical power, oil, oxygen and, in limited circumstances, liquefied petroleum gas to manufacture our products. These energy sources are vital to our operations and we rely on a continuous power supply to conduct our business. Energy prices are subject to considerable volatility. We are not able to predict to what extent energy prices will vary in the future. If energy costs increase further in the future, we could experience a significant increase in operating costs, which could, if we are not able to recover these costs increases from our customers through selling price increases, have a material adverse effect on our business, financial condition and results of operations.

Our ability to fully pass-through input costs may have an adverse effect on our financial condition and results of operations

A significant number of our sales contracts with customers include provisions enabling us to pass-through increases in certain input costs, which help us deliver consistent margins. However, there is no assurance that the Group will be in a position to fully recover increased input costs from all of our customers, as has been the case with respect to the elevated freight and logistics costs incurred in our Metal Packaging and Glass Packaging businesses in North America during 2018.

Our manufacturing facilities are subject to operating hazards.

Our manufacturing processes include cutting, coating and shaping metal into containers, as well as heating raw materials to extremely high temperatures to make glass, which we then form into glass containers. These processes, which are conducted at high speeds and involve operating heavy machinery and equipment, entail risks and hazards, including industrial accidents, leaks and ruptures, explosions, fires, mechanical failures and environmental hazards, such as spills, storage tank leaks, discharges or releases of hot glass or toxic or hazardous substances and gases. These hazards may cause unplanned business interruptions, unscheduled downtime, transportation interruptions, personal injury and loss of life, severe damage to or the destruction of property and equipment, environmental contamination and other environmental damage, civil, criminal and administrative sanctions and liabilities, and third‑party claims, any of which may have a material adverse effect on our business, financial condition and results of operations.

We are involved in a continuous manufacturing process with a high degree of fixed costs. Any interruption in the operations of our manufacturing facilities may adversely affect our business, financial condition and results of operations.

All of our manufacturing activities take place at facilities that we own or that are leased by the Group. We conduct regular maintenance on all of our operating equipment. However, due to the extreme operating conditions inherent in some of our manufacturing processes, we cannot assure you that we will not incur unplanned business interruptions due to furnace breakdowns or similar manufacturing problems or that such interruptions will not have an adverse impact on our business, financial condition and results of operations. There can be no assurance that alternative production capacity would be available in the future if a major disruption were to occur or, if it were available, that it could be obtained on favorable terms. A disruption in such circumstances could have a material adverse effect on our business, financial condition and results of operations.

To the extent that we experience any furnace breakdowns or similar manufacturing problems, we will be required to make capital expenditures even though we may not have available resources at such time and we may not be able to meet customer demand, which would result in a loss of revenues. As a result, our liquidity may be impaired as a result of such expenditures and loss of revenues.

A mechanical failure or disruption affecting any major operating line may result in a disruption of our ability to supply customers, and standby capacity may not be available. The potential impact of any disruption would depend on the nature and extent of the damage caused to such facility. Further, our facilities in geographically vulnerable areas, including parts of the United States and Italy, may be disrupted by the occurrence of natural phenomena, such as earthquakes, hurricanes, floods, wildfires and tsunamis.

Our business requires relatively high levels of capital expenditures, which we may be unable to fund.

Our business requires relatively high levels of maintenance capital expenditures. We may not be able to make such capital expenditures if we do not generate sufficient cash flow from operations, have funds available for borrowing under our existing credit facilities to cover these capital expenditure requirements or if we were restricted from incurring additional debt to cover such expenditures or as a result of a combination of these factors. If we are unable to meet our capital expenditure plans, we may not be able to maintain our manufacturing capacity, which may negatively impact our competitive position and ultimately, our revenues and profitability. If we are unable to meet our maintenance capital expenditures, our manufacturing capacity may decrease, which may have a material adverse effect on our profitability.

Our expansion strategy may adversely affect our business.

We aim over the longer term to continue to capitalize on strategic opportunities to expand our packaging activities. We believe that such future expansion is likely to require the further acquisition of existing businesses. Because we believe that such businesses may be acquired with modest equity and relatively high levels of financial leverage given the cash‑generating capabilities of our business streams, our leverage may increase in the future in connection with any acquisitions. This could have an adverse effect on our business, financial condition and results of operations. In addition, any future expansion is subject to various risks and uncertainties, including the inability to integrate effectively the operations, personnel or products of acquired companies and the potential disruption of existing businesses and diversion of management’s attention from our existing businesses. Furthermore, there can be no assurance that any future expansions will achieve positive results.

We are subject to various environmental and other legal requirements and may be subject to new requirements of this kind in the future that could impose substantial costs upon us.

Our operations and properties are subject to extensive laws, ordinances, regulations and other legal requirements relating to environmental protection. Such laws and regulations which may affect our operations include, among others, requirements regarding remediation of contaminated soil, groundwater and buildings, water supply and use, natural resources, water discharges, air emissions, waste management, noise pollution, asbestos and other deleterious materials, the generation, storage, handling, transportation and disposal of regulated materials, product safety, and workplace health and safety. Such laws and regulations are also subject to constant review by lawmakers and regulators, which may result in further environmental legal requirements.

We have incurred, and expect to continue to incur, costs to comply with such legal requirements, and these costs are likely to increase in the future. The EPA and other regulators have targeted the glass packaging, flat glass, mineral wool and fiber sectors as part of an enforcement initiative involving high fuel combustion sources. Inquiries and enforcement by other regulators, including demands for more stringent pollution control devices could also result in the need for further capital upgrades to our furnaces and plant operations at substantial cost. We require a variety of permits to conduct our operations, including operating permits such as those required under various U.S. laws, including the federal Clean Air Act, and the EU Industrial Emissions Directive water and trade effluent discharge permits, water abstraction permits and waste permits. We are in the process of applying for, or renewing, permits at a number of our sites. Failure to obtain and maintain the relevant permits, as well as noncompliance with such permits, could have a material adverse effect on our business, financial condition and results of operations.

If we were to violate or fail to comply with these laws and regulations or our permits, we could be subject to criminal, civil and administrative sanctions and liabilities, including substantial fines and orders, or a partial or total shutdown of our operations. For example, in 2017 we settled alleged violations of hazardous waste regulations governing the reuse of electrostatic precipitator dust at our Madera plant in the United States, which occurred in the period prior to the acquisition in 2014 of VNA. As part of this settlement, we paid a civil penalty of $3.5 million and expect to incur increased dust disposal costs, which we estimate to be about $500,000 annually. We cannot assure you that our reuse of electrostatic precipitator dust at our other glass manufacturing plants will not result in regulatory inquiries or enforcement relating to compliance with hazardous waste regulations.

In order to comply with air emission restrictions, significant capital investments may be necessary at some sites. For example, to comply with U.S. environmental regulations and the demands of the EPA, VNA, which we acquired in 2014, agreed to make sizable investments to replace or install new electrostatic precipitators and other equipment in order to control the air emissions at certain sites located in the United States. In 2010, VNA and the EPA signed a global consent decree pursuant to which VNA has made and will continue to make investments estimated at up to an aggregate of $112 million over a ten‑year period, excluding operating costs of the systems installed. In addition, we paid a penalty amounting to $2.5 million excluding interest pursuant to this consent decree.

We have received notices of violation from the EPA for alleged violations under the Clean Air Act’s Prevention of Significant Deterioration, New Source Performance Standards and Title V provisions stemming from past furnace‑related projects at our other glass manufacturing facilities unrelated to our acquisition of VNA, including furnace‑related projects conducted by third parties who owned the facilities before us. The EPA has sent information requests to certain of our glass manufacturing facilities concerning furnace‑related projects, as well as our air pollutant emissions more generally, which could culminate in notices of violation or other enforcement.

In Europe, under the IED and its reference document for “Best Available Techniques” for glass manufacturing plants and metal manufacturing plants with surface treatment using solvents, permitted emissions levels from these plants including ours are reduced substantially periodically. In Germany, technical guidelines, TA Luft, set forth emission thresholds which could potentially result in stricter limits in the future. These types of changes could require additional investment in our affected operations. Our business is also affected by the EU ETS, which limits emissions of greenhouse gases. See “Item 4. Information on the Company–Environmental, Health and Safety and Product Safety Regulation”. This scheme, any future changes to it and any additional measures required to control the emission of greenhouse gases that may apply to our operations could have a material adverse effect on our business, financial condition and results of operations. California has implemented a similar program, which results in the need for us to incur potentially significant

compliance costs, including for the purchase of offsets against our greenhouse gas emissions. Other states where we have operations, such as Washington, are expected to implement similar programs.

Changes to the laws and regulations governing the materials that are used in our manufacturing operations may impact the price of such materials or result in such materials no longer being available, which could have a material adverse effect on our business, financial condition and results of operations. The European Union passed regulations concerning REACH, which place onerous obligations on the manufacturers and importers of substances, preparations and articles containing substances, and which may have a material adverse effect on our business. Furthermore, substances we use may have to be removed from the market (under REACH’s authorization and restriction provisions) or need to be substituted for alternative chemicals which may also adversely impact upon our operations.

Sites at which we operate often have a long history of industrial activities and may be, or have been in the past, engaged in activities involving the use of materials and processes that could give rise to contamination and result in potential liability to investigate or remediate, as well as claims for alleged damage to persons, property or natural resources. Liability may be imposed on us as owners, occupiers or operators of contaminated facilities. These legal requirements may apply to contamination at sites that we currently or formerly owned, occupied or operated, or that were formerly, owned, occupied or operated by companies we acquired or at sites where we have sent waste offsite for treatment or disposal. Regarding assets acquired by us, including the beverage can manufacturing assets, we cannot assure you that our due diligence investigations identified or accurately quantified all material environmental matters related to the acquired facilities. Our closure of a site may accelerate the need to investigate and remediate any contamination at the site.

In addition, we may be required to remediate contaminated third‑party sites where we have sent waste for disposal. Liability for remediation of these third‑party sites may be established without regard to whether the party disposing of the waste was at fault or the disposal activity was legal at the time it was conducted. For example, “Superfund” sites in the United States are the highest priority contaminated sites designated by the federal government as requiring remediation, and costs of their remediation tend to be high. We and a number of other companies have been named as potentially responsible parties to clean up the Lower Duwamish Waterway Superfund Site in Washington, because our Seattle plant is adjacent to the waterway and is alleged to have contributed to its contamination. Whether we will have any liability for investigation and remediation costs at this or any other Superfund site or for costs relating to claims for natural resource damages, and what portion of the costs we must bear, has not been determined.

Changes in product requirements and their enforcement may have a material impact on our operations.

Changes in laws and regulations relating to deposits on, and the recycling of, glass or metal packaging could adversely affect our business if implemented on a large scale in the major markets in which we operate. Changes in laws and regulations laying down restrictions on, and conditions for use of, food contact materials or on the use of materials and agents in the production of our products could likewise adversely affect our business. Changes to health and food safety regulations could increase costs and also might have a material adverse effect on revenues if, as a result, the public attitude toward end‑products, for which we provide packaging, were substantially affected.

Additionally, the effectiveness of new standards such as the ones related to recycling or deposits on different packaging materials could result in excess costs or logistical constraints for some of our customers who could choose to reduce their consumption and even terminate the use of glass or metal packaging for their products. We could thus be forced to reduce, suspend or even stop the production of certain types of products. The regulatory changes could also affect our prices, margins, investments and activities, particularly if these changes resulted in significant or structural changes in the market for food packaging that might affect the market shares for glass, the volumes produced or production costs.

Environmental concerns could lead U.S. or European Union bodies to implement other product regulations that are likely to be restrictive for us and have a material negative impact on our business, financial condition and results of operations. For example, in the European Union, each bottle cannot, in principle, contain more than the applicable heavy metals limit pursuant to Directive 94/62/CE on Packaging and Packaging Waste. There is significant variation, among countries where we sell our products, in the limitation on certain constituents in packaging, which can have the effect of restricting the types of raw materials or amount of recycled glass we use. In turn, these restrictions can increase our operating costs, such as increased energy consumption, and the environmental impacts of our operations.

Similarly, in the United States, some state regulations set the concentration of certain heavy metals in packaging at 100 ppm and provide for an exception to this rule in the event of additions of recycled packaging. Because this exemption has expired in certain states, the bottles manufactured from recycled glass that have a heavy metals concentration higher than 100 ppm could be noncompliant, which could have a negative impact on our earnings, financial condition, assets or image. We have had regulatory inquiries about our compliance and may in the future have additional inquiries or enforcement.

Other changes, such as restrictions on bisphenol A in coatings for some of our products, which have been proposed or adopted in the European Union under the REACH legislation and some of its Member States, have required us to develop substitute materials for our production.

We could incur significant costs in relation to claims of injury and illness resulting from materials present or used at our production sites, or from our use of these sites or other workplace injuries, or from our products.

As is the case in a number of other industrial processes that deal with high temperatures, asbestos was once present in the glass‑making industry, primarily in safety equipment, until measures were taken to substitute this material for other materials made possible through technological advances. Since the 1990s, items made of asbestos have gradually been removed at our sites in Western Europe and the United States. Because of the age of some of our sites, however, asbestos‑cement may have been used in construction and may still be present at these sites. When these buildings are modernized or repaired, the cost of upgrades is higher because of the restrictions associated with removing asbestos‑containing materials.

We are exposed to claims alleging injury or illness associated with asbestos and related compensation over and above the support that may be offered through various existing social security systems in countries where we operate.

Claims associated with our glass manufacturing operations exist and may arise for reasons associated with the work environment unrelated to the presence of asbestos. For example, claims have arisen associated with the acoustic environment generated by forming machines, the use of glass sand in making glass and products likely to contain heavy metals or solvents for decoration. We may also face the risk of work‑related health claims owing to materials present or used at our production sites such as silicosis, and, under certain conditions, Legionnaires’ disease. The U.S. Occupational Safety and Health Administration has implemented a requirement that reduced by 50% the permissible exposure limit to crystalline silica and requires engineering controls or personal protective equipment to safeguard employees from such exposure. The European Union has also set stricter exposure limit values for respirable crystalline silica in work processes under the Carcinogens and Mutagens Directive. This substance is a common mineral found in sand, which is a significant raw material component for glass manufacturing and is also contained in refractories, or bricks, used in glass manufacturing operations. Our costs to meet these reduced limits could be substantial, particularly if it becomes necessary for us to implement broad engineering controls across many of our glass manufacturing plants.

We are also exposed to claims alleging musculoskeletal disorders caused by performing certain repetitive operations or motions. We could also face claims alleging illness or injury from use of the products that we manufacture or sell or from workplace injuries more generally. If these claims succeed, they could have a material adverse impact on our business, financial condition and results of operations.

We may not be able to integrate any future acquisitions effectively.

Even though we have acquired businesses in the past, there is no certainty that any businesses we may acquire in the future will be effectively integrated. If we cannot successfully integrate acquired businesses within a reasonable time frame, we may not be able to realize the potential benefits anticipated from those acquisitions. Our failure to successfully integrate such businesses and the diversion of management attention and other resources from our existing operations could have a material adverse effect on our business, financial condition and results of operations.

Furthermore, even if we are able to integrate successfully the operations of acquired businesses, we may not be able to realize the cost savings, synergies and revenue enhancements that we anticipate either in the amount or within the time frame that we anticipate, and the costs of achieving these benefits may be higher than, and the timing may differ

from, what we expect. Our ability to realize anticipated cost savings and synergies may be affected by a number of factors, including the following:

| · | | the use of more cash or other financial resources on integration and implementation activities than we expect, including restructuring and other exit costs; and |

| · | | increases in other expenses related to acquisitions, which may offset the cost savings and other synergies from such acquisitions. |

We have potential indemnification obligations relating to divestments.

We have disposed of a number of businesses. Pursuant to these agreements, we may be required to provide indemnification to the acquirers for damages resulting from a breach of any representation, warranty or covenants contained therein. The indemnification obligations under these agreements are subject to certain monetary and other limitations. To the extent that we are required to make any significant payments under these indemnification provisions, these payments could adversely impact our business, financial condition and results of operations.

We may be subject to litigation, regulatory investigations, arbitration and other proceedings that could have an adverse effect on us.

We are currently involved in various litigation matters, and we anticipate that we will be involved in litigation matters from time to time in the future. The risks inherent in our business expose us to litigation, including personal injury, environmental litigation, contractual litigation with customers and suppliers, intellectual property litigation, tax or securities litigation, and product liability lawsuits. We cannot predict with certainty the outcome or effect of any claim, regulatory investigation, or other litigation matter, or a combination of these. If we are involved in any future litigation, or if our positions concerning current disputes are found to be incorrect, this may have an adverse effect on our business, financial condition and results of operations, because of potential negative outcomes, the costs associated with asserting our claims or defending such lawsuits, and the diversion of management’s attention to these matters.