UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR

15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of November, 2019

Commission File Number: 000-55899

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

(Exact Name of Registrant as Specified in Its Charter)

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Delegación Álvaro Obregón

01219, Ciudad de México

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F | ☒ | Form 40-F | ☐ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes | ☐ | No | ☒ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes | ☐ | No | ☒ | |

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

TABLE OF CONTENTS

| ITEM | |

| 1. | Third quarter 2019 earnings release of Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México |

| 2. | Third quarter 2019 earnings presentation of Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México |

| 3. | Relevant information dated October 31, 2019 |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO | |||||

| By: | /s/ Hector Chávez Lopez | ||||

| Name: | Hector Chávez Lopez | ||||

| Title: | Executive Director of Investor Relations | ||||

Date: November 1, 2019

Item 1

| Earnings Release | 3Q.2019 |  |

| Banco Santander México |

TABLE OF CONTENTS

| I. | CEO Message / Key Highlights for the Quarter |

| II. | Summary of 3Q19 Consolidated Results |

| III. | Analysis of 3Q19 Consolidated Results |

| IV. | Relevant Events, Transactions and Activities |

| V. | Awards & Recognitions |

| VI. | Sustainability and Social Responsibility |

| VII. | Credit Ratings |

| VIII. | 3Q19 Earnings Call Dial-In Information |

| IX. | Analyst Coverage |

| X. | Definition of Ratios |

| XI. | Consolidated Financial Statements |

| XII. | Notes to Consolidated Financial Statements |

| Earnings Release | 3Q.2019 |

1 |

| Banco Santander México |

Banco Santander México Reports Third Quarter 2019 Net Income of Ps.5,517 Million

| - | Progress on strategy execution to transform the Bank operationally and digitally. |

| - | Loan growth mainly driven by mortgages, credit cards and payroll loans, along with middle-market. |

| - | Continue attracting lower-cost individual deposits, while further enhancing ability to cross-sell products. |

| - | Solid quarter with strong net interest income and healthy asset quality. |

Mexico City – October 31st, 2019, Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México(NYSE: BSMX; BMV: BSMX), (“Banco Santander México” or “the Bank”), today announced financial results for the three-month and nine-month periods ending September 30, 2019.

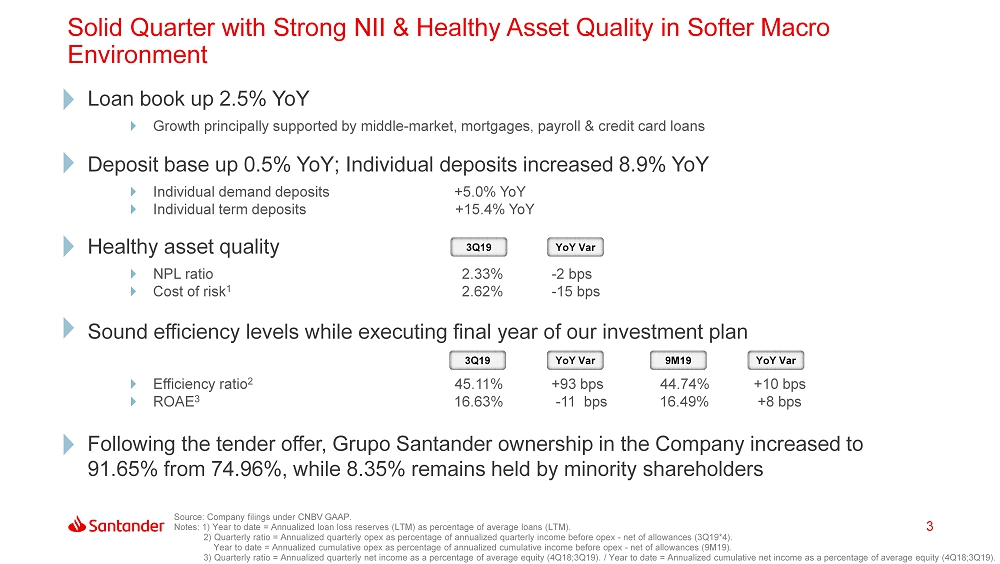

Banco Santander México reported net income of Ps.5,517 million in 3Q19, representing a YoY increase of 8.3% and a QoQ decrease of 1.6%. On a cumulative basis, net income for 9M19 reached Ps.16,416 million, representing a 9.5% YoY increase.

| HIGHLIGHTS | ||||||||||||

| Results(Million pesos) | 3Q19 | 2Q19 | 3Q18 | %QoQ | %YoY | 9M19 | 9M18 | %YoY | ||||

| Net interest income | 16,589 | 16,588 | 15,795 | 0.0 | 5.0 | 49,626 | 45,205 | 9.8 | ||||

| Fee and commission, net | 4,580 | 4,697 | 4,271 | (2.5) | 7.2 | 13,703 | 12,602 | 8.7 | ||||

| Core revenues | 21,169 | 21,285 | 20,066 | (0.5) | 5.5 | 63,329 | 57,807 | 9.6 | ||||

| Provisions for loan losses | 4,478 | 4,454 | 4,796 | 0.5 | (6.6) | 13,250 | 12,913 | 2.6 | ||||

| Administrative and promotional expenses | 9,783 | 9,482 | 9,003 | 3.2 | 8.7 | 28,521 | 26,066 | 9.4 | ||||

| Net income | 5,517 | 5,608 | 5,096 | (1.6) | 8.3 | 16,416 | 14,994 | 9.5 | ||||

| Net income per share1 | 0.81 | 0.83 | 0.75 | (1.6) | 8.3 | 2.42 | 2.21 | 9.4 | ||||

Balance Sheet Data (Million pesos) | Sep-19 | Jun-19 | Sep-18 | %QoQ | %YoY | Sep-19 | Sep-18 | %YoY | ||||

| Total assets | 1,460,741 | 1,368,187 | 1,375,294 | 6.8 | 6.2 | 1,460,741 | 1,375,294 | 6.2 | ||||

| Total loans | 697,326 | 700,329 | 680,120 | (0.4) | 2.5 | 697,326 | 680,120 | 2.5 | ||||

| Deposits | 683,590 | 721,288 | 680,143 | (5.2) | 0.5 | 683,590 | 680,143 | 0.5 | ||||

| Shareholders´ equity | 139,700 | 133,829 | 127,385 | 4.4 | 9.7 | 139,700 | 127,385 | 9.7 | ||||

| Key Ratios(%) | 3Q19 | 2Q19 | 3Q18 | bps QoQ | bps YoY | 9M19 | 9M18 | bps YoY | ||||

| Net interest margin | 5.74 | 5.76 | 5.66 | (2) | 8 | 5.69 | 5.48 | 21 | ||||

| Net loans to deposits ratio | 98.89 | 94.13 | 97.00 | 476 | 189 | 98.89 | 97.00 | 189 | ||||

| ROAE | 16.63 | 17.29 | 16.74 | (66) | (11) | 16.49 | 16.41 | 8 | ||||

| ROAA | 1.55 | 1.63 | 1.51 | (8) | 4 | 1.54 | 1.48 | 6 | ||||

| Efficiency ratio | 45.11 | 44.29 | 44.18 | 82 | 93 | 44.74 | 44.64 | 10 | ||||

| Capital ratio | 16.89 | 16.50 | 16.02 | 39 | 87 | 16.89 | 16.02 | 87 | ||||

| NPLs ratio | 2.33 | 2.23 | 2.35 | 10 | (2) | 2.33 | 2.35 | (2) | ||||

| Cost of Risk | 2.62 | 2.70 | 2.77 | (8) | (15) | 2.62 | 2.77 | (15) | ||||

| Coverage ratio | 130.82 | 136.56 | 127.60 | (574) | 322 | 130.82 | 127.60 | 322 | ||||

| Operating Data | Sep-19 | Jun-19 | Sep-18 | %QoQ | %YoY | Sep-19 | Sep-18 | %YoY | ||||

| Branches | 1,223 | 1,216 | 1,218 | 0.6 | 0.4 | 1,223 | 1,218 | 0.4 | ||||

| Branches and offices2 | 1,411 | 1,394 | 1,385 | 1.2 | 1.9 | 1,411 | 1,385 | 1.9 | ||||

| ATMs | 8,866 | 8,749 | 8,003 | 1.3 | 10.8 | 8,866 | 8,003 | 10.8 | ||||

| Customers | 17,739,373 | 17,220,259 | 16,482,009 | 3.0 | 7.6 | 17,739,373 | 16,482,009 | 7.6 | ||||

| Employees | 19,876 | 19,403 | 18,629 | 2.4 | 6.7 | 19,876 | 18,629 | 6.7 | ||||

1) Accumulated EPS, net of treasury shares (compensation plan) and discontinued operations. Calculated by using weighted number of shares. | ||||||||||||

| 2) Includes cash desks (espacios select, box select and corner select) and SMEs business centers. Excluding brokerage house offices. | ||||||||||||

| Earnings Release | 3Q.2019 |

2 |

| Banco Santander México |

Héctor Grisi, Banco Santander México’s Executive President and CEO, commented:“Our focus on profitable growth delivered another quarter of solid performance, with steady increases in high margin loans and fees. Net income grew over 8% year-on-year, as we attracted more retail deposits, expanded our base of loyal, digital and mobile customers, and cross sold more of our products. The increase came despite a substantially higher effective tax rate as well as additional strategic investments that are further strengthening our retail franchise and making Santander the primary bank of a growing number of Mexicans.

Our performance was particularly gratifying, given softer economic conditions in the third quarter and our ability to maintain asset quality at a healthy level with year-on-year improvements across risk metrics. Driving our loan book were mortgages, credit cards and payroll loans, as well as middle-market lending. Individuals are increasingly attracted to our more modern and user-friendly branch formats, with 180 branches being converted during this year. Our base of digital and mobile customers grew 51% and 69%, respectively, as we continued upgrading our online and mobile banking platforms. This quarter we also formed a strategic alliance with CONTPAQi, a leading supplier of accounting software to over 1 million SMEs in México. Through this partnership, we aim to grow our base of SME customers by 50% within the next four years.

Although both domestic and global macroeconomic environments remain complex and challenging, we are encouraged by more accommodative central bank policies, still moderate inflation, as well as healthy employment levels across almost all sectors in México. And as we near the completion of our three-year investment plan, we continue building a far stronger and more customer-centric bank to maintain our profitable growth momentum in the years ahead.”

| Earnings Release | 3Q.2019 |

3 |

| Banco Santander México |

SUMMARY OF THIRD QUARTER 2019 CONSOLIDATED RESULTS

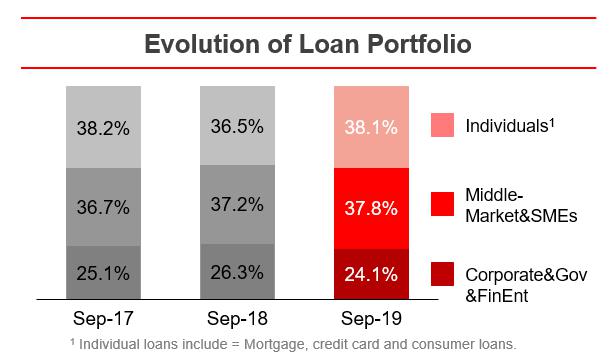

Loan portfolio

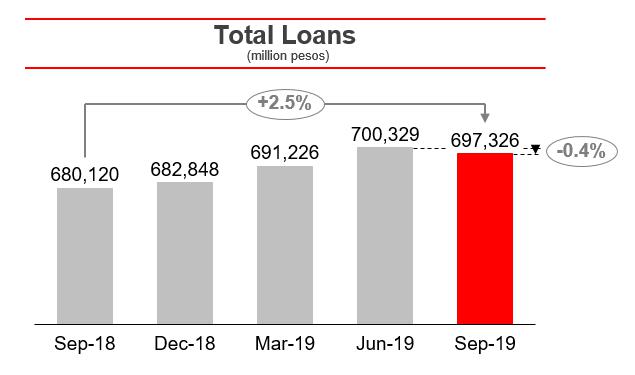

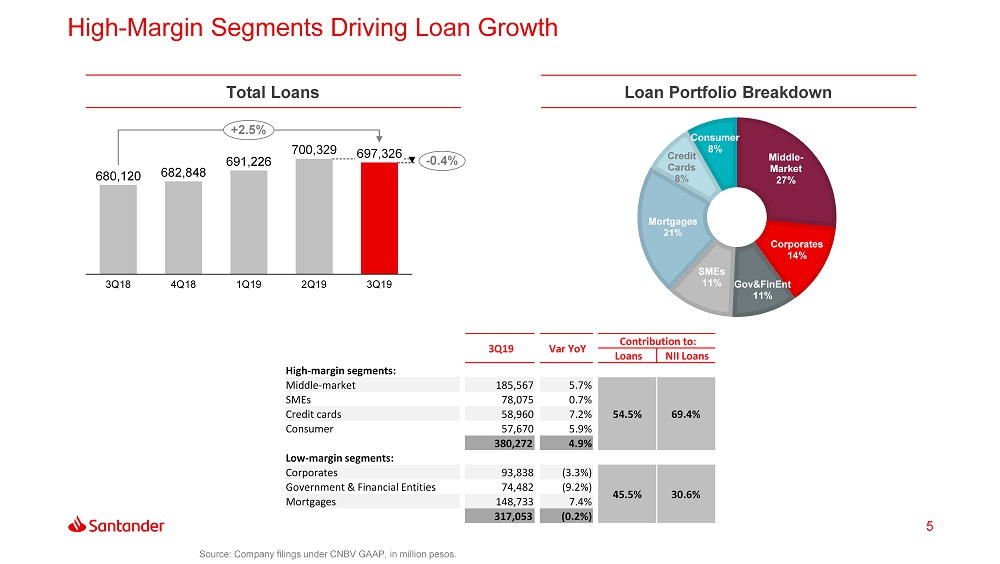

Banco Santander México’s total loan portfolio, as of Sep-19, increased 2.5% YoY, or Ps.17,206 million, to Ps.697,326 million, and decreased 0.4%, or Ps.3,003 million, on a sequential basis.

This slowdown was mainly related to softer growth in commercial and government loans, due to weaker demand and a strong competitive environment. By contrast, individual loan demand remained quite healthy. The Bank continues with a prudent approach to risk management and trading.

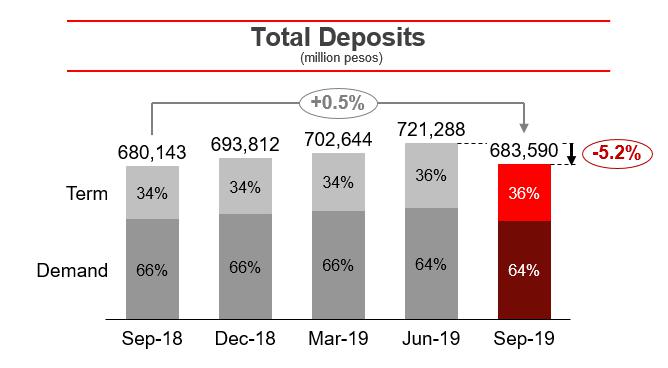

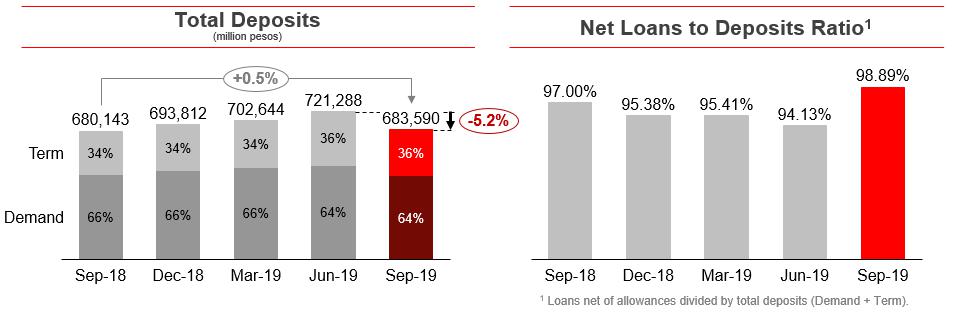

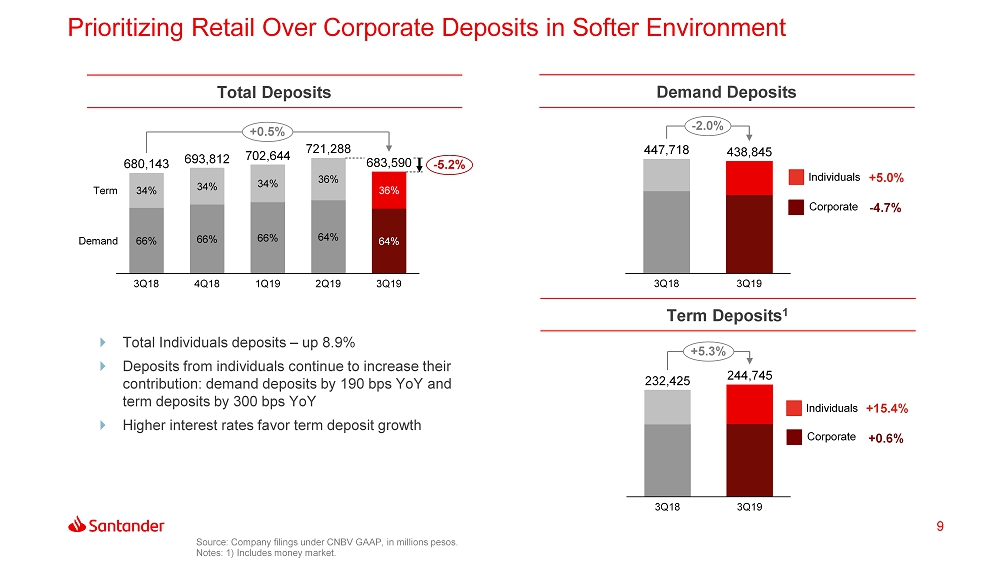

Deposits

Deposits, which represent 82.8% of Banco Santander México’s total funding1, increased 0.5% YoY in Sep-19, and decreased 5.2% sequentially. In turn, term deposits increased by 5.3% YoY, still supported by the high interest rate environment, while demand deposits decreased by 2.0% YoY due to a contraction in demand deposits from corporates of 4.7% YoY. It is worth noting that demand deposits from individuals expanded by 5.0% YoY.

In Sep-19, term deposits from individuals represented 34.9% of total term deposits, compared with 31.8% in Sep-18, and 32.3% in Jun-19. Demand deposits from individuals represented 29.7% of total demand deposits, compared with 27.8% in Sep-18, and 29.8% in Jun-19. Total deposits from individuals expanded 8.9% YoY, supported by the Bank’s strategy focused on prioritizing individual deposits and foregoing certain expensive corporate deposits that resulted in a 2.9% YoY contraction.

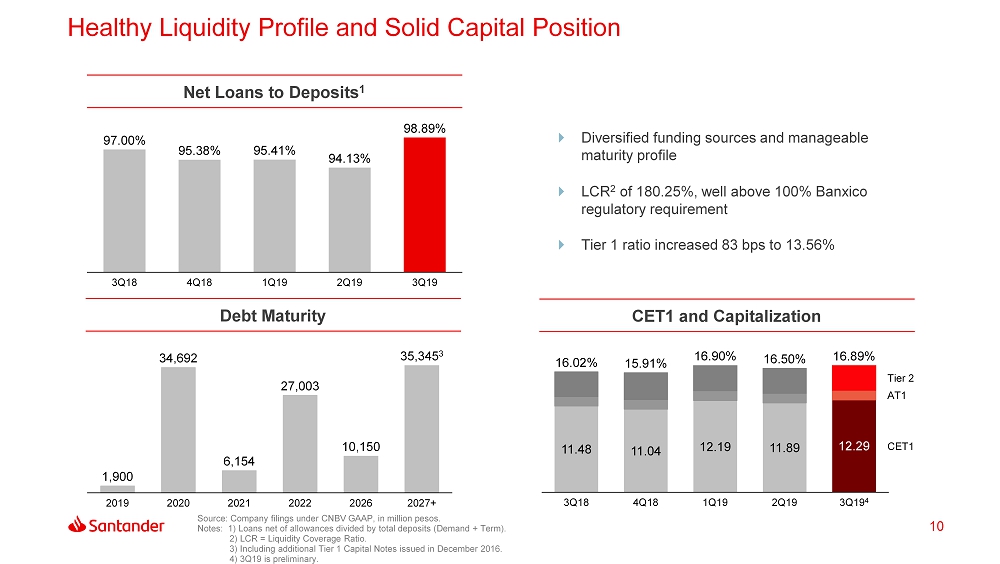

The loans-to-deposits ratio stood at 98.89% in Sep-19, which compares with 97.00% in Sep-18, and 94.13% in Jun-19, maintaining a sound funding position.

______________________

1Total funding includes: deposits, credit instruments issued, bank and other loans and subordinated credit notes.

| Earnings Release | 3Q.2019 |

4 |

| Banco Santander México |

Net income

Banco Santander México reported 3Q19 net income of Ps.5,517 million, representing an increase of 8.3% YoY and a decrease of 1.6% QoQ. On a cumulative basis, net income for the first nine months of the year, reached Ps.16,416 million, representing a 9.5% YoY increase. Net interest income along with fee income drove solid growth, despite a higher effective tax rate.

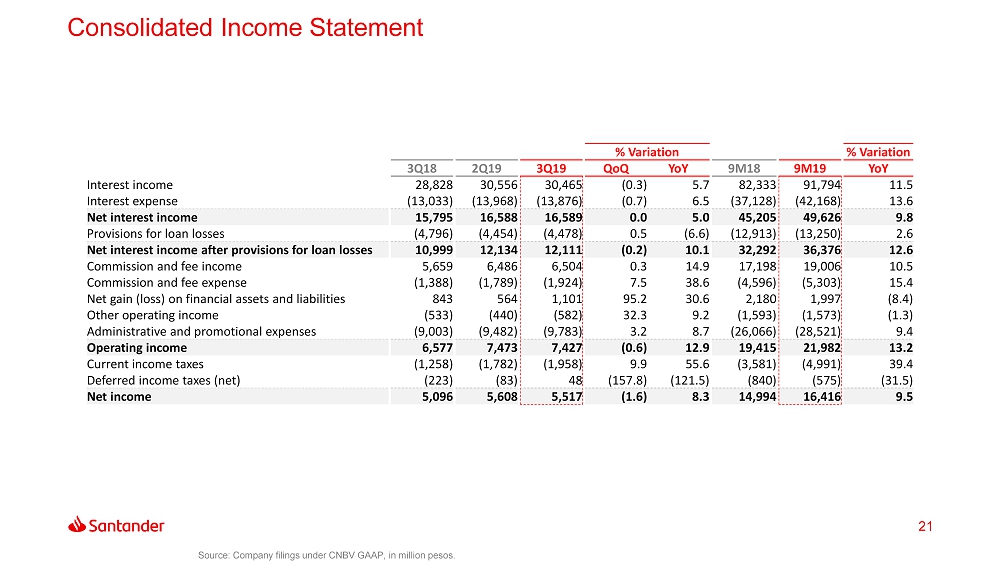

| Net income statement | ||||||||||||

| Million pesos | % Variation | % Variation | ||||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | |||||

| Net interest income | 16,589 | 16,588 | 15,795 | 0.0 | 5.0 | 49,626 | 45,205 | 9.8 | ||||

| Provisions for loan losses | (4,478) | (4,454) | (4,796) | 0.5 | (6.6) | (13,250) | (12,913) | 2.6 | ||||

| Net interest income after provisions for loan losses | 12,111 | 12,134 | 10,999 | (0.2) | 10.1 | 36,376 | 32,292 | 12.6 | ||||

| Commission and fee income, net | 4,580 | 4,697 | 4,271 | (2.5) | 7.2 | 13,703 | 12,602 | 8.7 | ||||

| Net gain (loss) on financial assets and liabilities | 1,101 | 564 | 843 | 95.2 | 30.6 | 1,997 | 2,180 | (8.4) | ||||

| Other operating income | (582) | (440) | (533) | 32.3 | 9.2 | (1,573) | (1,593) | (1.3) | ||||

| Administrative and promotional expenses | (9,783) | (9,482) | (9,003) | 3.2 | 8.7 | (28,521) | (26,066) | 9.4 | ||||

| Operating income | 7,427 | 7,473 | 6,577 | (0.6) | 12.9 | 21,982 | 19,415 | 13.2 | ||||

| Income taxes (net) | (1,910) | (1,865) | (1,481) | 2.4 | 29.0 | (5,566) | (4,421) | 25.9 | ||||

| Net income | 5,517 | 5,608 | 5,096 | (1.6) | 8.3 | 16,416 | 14,994 | 9.5 | ||||

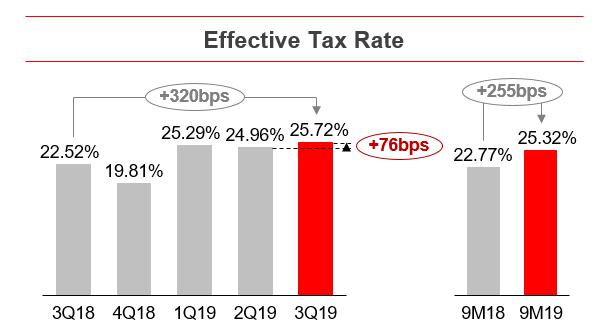

| Effective tax rate (%) | 25.72 | 24.96 | 22.52 | 25.32 | 22.77 | |||||||

| Earnings Release | 3Q.2019 |

5 |

| Banco Santander México |

3Q19 vs 3Q18

The 8.3% year-on-year increase in net income was principally driven by:

| i) | A 5.0%, or Ps.794 million, increase in net interest income, supported by steady growth in high-margin loans; |

| ii) | A 6.6%, or Ps.318 million, decrease in provisions for loan losses, particularly in commercial loans, given that in 3Q18 the Bank made additional provisions for a specific project finance corporate loan; |

| iii) | A 7.2%, or Ps.309 million, increase in net commissions and fees, mainly due to increases in debit and credit card usage and financial advisory services fees; and |

| iv) | A 30.6%, or Ps.258 million, increase in net gains on financial assets and liabilities, mainly resulting from improved market activity that drove higher client flows, supporting market-making activity. |

The increase in net income was partially offset by:

| i) | An 8.7%, or Ps.780 million, increase in administrative and promotional expenses, mainly due to higher technology services, other expenses, depreciation and amortization and taxes and duties; and |

| ii) | A 29.0%, or Ps.429 million, increase in income taxes, which resulted in a 25.72% effective tax rate in the quarter, compared to 22.52% in 3Q18. |

9M19 vs 9M18

Net income growth of 9.5% for 9M19 was mainly due to:

| i) | A 9.8%, or Ps.4,421 million, increase in net interest income, as the Bank focused on driving profitability across the balance sheet; and |

| ii) | An 8.7%, or Ps.1,101 million, increase in net commissions and fees, mainly due to increases in debit and credit card usage, insurance and account management fees. |

The increase in net income was partially offset by:

| i) | A 9.4%, or Ps.2,455 million, increase in administrative and promotional expenses, mainly due to higher other expenses, technology services, depreciation and amortization, personnel expenses and taxes and duties; |

| ii) | A 25.9%, or Ps.1,145 million, increase in income taxes, which resulted in a 25.32% effective tax rate in 9M19, compared to 22.77% in 9M18; |

| iii) | A 2.6%, or Ps.337 million, increase in provisions for loan losses; and |

| iv) | A 8.4%, or Ps.183 million, decrease in net gains on financial assets and liabilities. |

| Earnings Release | 3Q.2019 |

6 |

| Banco Santander México |

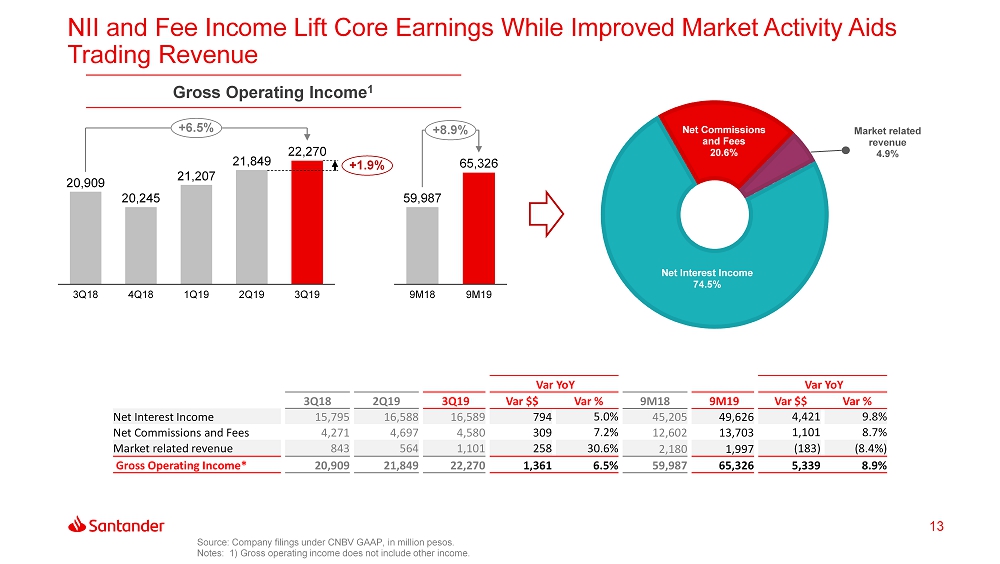

Gross operating income

Banco Santander México’s gross operating income for 3Q19 totaled Ps.22,270 million, representing increases of 6.5% YoY and 1.9% QoQ, driven by strong performance across the business. Core earnings accounted 95% of gross operating income, while market-related income rose above the Bank’s average historical levels of Ps.600 to Ps.800 million. Gross operating income for 9M19 amounted to Ps.65,326 million, increasing 8.9% from 9M18.

Gross operating income is broken down as follows:

| Breakdown gross operating Income (%) | |||||||||||

| Variation (bps) | Variation (bps) | ||||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | YoY | ||||

| Net Interest Income | 74.49 | 75.92 | 75.54 | (143) | (105) | 75.97 | 75.36 | 61 | |||

| Net Commissions and Fees | 20.57 | 21.50 | 20.43 | (93) | 14 | 20.98 | 21.01 | (3) | |||

| Market related revenue | 4.94 | 2.58 | 4.03 | 236 | 91 | 3.06 | 3.63 | (57) | |||

| Gross Operating Income* | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | ||||||

*Does not include other income

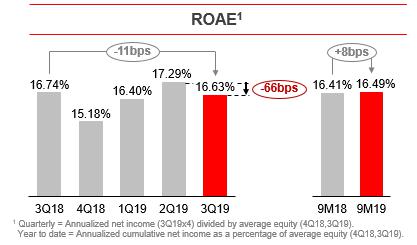

Return on average equity (ROAE)

ROAE for 3Q19 decreased 11 basis points to 16.63%, from 16.74% reported in 3Q18 and by 66 basis points from 17.29% in 2Q19. This level reflects the Ps.4.8 billion cash dividend paid by the bank in May-19. For 9M19, ROAE stood at 16.49%, 8 basis points higher than the 16.41% reported in 9M18.

| Earnings Release | 3Q.2019 |

7 |

| Banco Santander México |

Strategic initiatives and commercial actions

On December 2016, Banco Santander México announced an investment plan for Ps.15 billion over three years with the aim to digitalize operations and to become the primary bank of our customers. The investment plan will end this year, but the Bank’s strategy will remain centered on attracting and retaining customers while increasing their loyalty, expanding cross selling, promoting adoption of our digital platforms, and broadening our value proposition with next generation products and services.

Main progress of our three main strategic pillars on which our investment plan is based:

| Ø | Digitalization of products and processes, transformation of the distribution network, and investment in infrastructure and cutting-edged technology. |

| § | In the digital factory, “Spotlight”, the Bank is working on digital solutions for its customers to be able to do any banking operation or transaction from their smartphones, without the need to go to a branch. The Bank is digitalizing products and processes for its clients and employees and has launched more than 100 functionalities, including new features for its mobile banking app “Súper Móvil”, such as Face ID access, cardless cash withdrawals, a personalized savings plan, “Mis Metas”, the programing of direct debits through “GoPay” for paying services, contactless payments through smart-watches like Garmin and Fitbit, and a new channel to manage credit card clarifications of unrecognized charges through “Súper Móvil” or “Súper Net” without the need for making a phone call or going to a branch. |

| § | This quarter the Bank also launched a new functionality through its App “Super Wallet”, which allows customers to generate the NIP for their credit cards on the App, without the need to call “Súper Línea” to perform this task. |

| § | Santander was the first bank in Mexico ready to use CoDi, incorporating this payment method into its “Súper Móvil” App. |

| § | Launch of “Santander TAP” last quarter, a free function through messaging services like WhatsApp, Facebook or Instagram, that allows Santander customers to make money transfers to Santander customers and non-customers without leaving the chat feature. If the intended recipient does not have a bank account, Santander offers the online opening of a “Super Digital” account to be able to receive the money. “Santander TAP” already has more than 150,000 active customers since its launch 4 months ago. |

| § | Teamed up with FUNO to provide customers a new service model featuring special attention points (Isla Financiera) in shopping centers along with next-generation ATMs, offering more personalized assistance to customers. The first of these modules was opened this quarter, with a total of 50 scheduled to be opened in 39 cities in the coming months. |

| § | Continue with the deployment of next-generation ATMs throughout the country and with constant enhancements to CRM. Added 60 full-function ATMs during the quarter, with 981 in operation at the end of September 2019 and a total of 1,000 by year-end, which would position the Bank to the natural market share in this type of infrastructure. |

| § | During the year, transformed 180 branches according to a new distribution model, which promotes the use of digital channels and self-service, reaching 494 branches under this format. The identification of 818 micro-markets within Mexico has allowed branches to be adapted according to each micro-market’s needs, which is expected to boost volume growth. The Bank also transformed its distribution network model, whereby branch managers are responsible for their branches’ own P&L and cost of risk. |

| Earnings Release | 3Q.2019 |

8 |

| Banco Santander México |

| § | “Super Digital”, a fully digital account which addresses non-banked clients or digital natives who prefer bypassing a branch, now has more than 289,300 accounts since its launch in October 2016. |

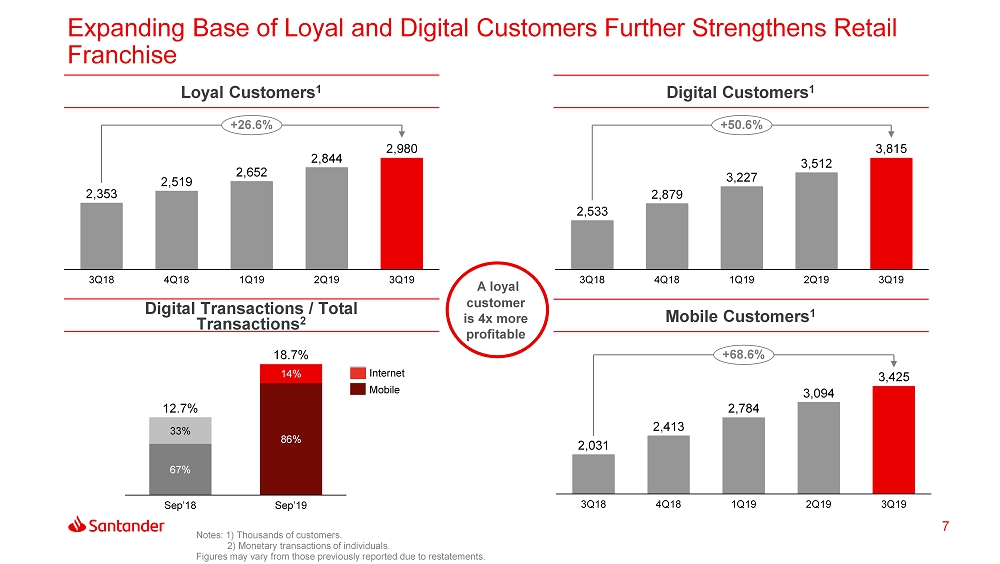

| § | Ongoing efforts to further digitalize the client base and build loyalty, led to a 51% increase in digital clients and 27% in loyal customers as of 3Q19. The number of mobile customers increased 69% in the last 12 months. Mobile monetary transactions accounted for 86% of digital monetary transactions, up from 67% in 3Q18. |

| Ø | On the retail front, investment initiatives are aimed at boosting customer acquisition, cross-selling and building loyalty. |

| § | Our App “Super Wallet” reached 835,500 customers, supporting the migration of our customers to digital banking. The App allows customer to manage their money, block or unblock cards, make contactless payments, check balances, transfer funds, and check their loyalty programs. |

| § | To continue attracting new customers and increase the loyalty of existing ones, Santander has launched several initiatives that are progressing well: |

| - | Santander Plus continues to perform well. As of September 2019, over 6.7 million customers have enrolled in this program, of which 52% are new to the bank. Additional benefits were added to the Santander Plus program this quarter, including an alliance with Repsol, which will give Santander Plus customers Ps.200 cash-back for every Ps.2,000 spent at Repsol gas stations every month. |

| - | The focus on attracting payroll accounts has resulted in 4.56 million customers, of which almost 600,000 are new to the bank in the last twelve months. |

| - | The Santander-Aeroméxico co-branded card has also been very successful, with more than one million cardholders, of which 34% are new. |

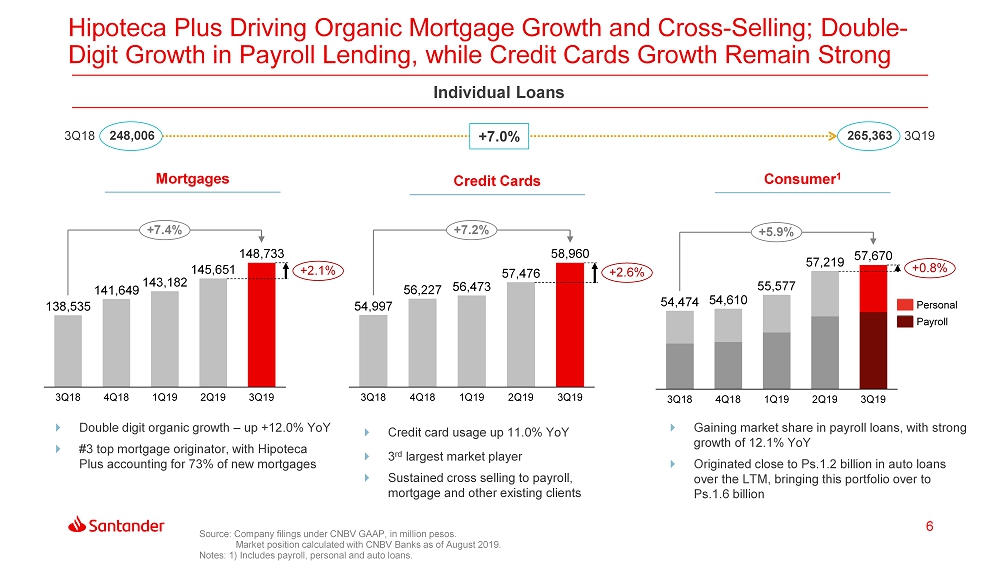

| - | The “Hipoteca Plus” mortgage program is helping attract and maintain loyal customers. This quarter, 73% of new mortgage loans were linked to “Hipoteca Plus”. |

| § | Additionally, in the commercial segment, the Bank continues consolidating a leading position in key segments in Mexico, such as SMEs and middle-market, while it aims to become one of the top three players in corporate and investment banking. |

| - | Launched “Comercio Plus”, a Santander Plus-like program, designed to attract SMEs and individuals with commercial activity, giving them up to Ps.10,000 cash-back per month for their POS’ interests for up to twelve months after their enrollment in the program, seeking to drive loyalty through POS, payroll and financing. |

| - | Announced this quarter a commercial alliance with CONTPAQi, a leading company in accounting software for SMEs, with 35% market share in this segment. Through this alliance, the Bank aims to boost the value offering by reaching more SMEs, while developing financial products that meet their needs and offering credit based on their transactional information. |

| Ø | In addition, the bank’s value proposition is complemented with new offerings, which address other client needs, such as auto financing and insurance. |

| § | In the auto loans business, “Super Auto”, the Bank is working with 657 dealers and more than 100 automotive groups nationwide. By September 2019, the loan portfolio totaled over Ps.1.6 billion. Established alliances with Peugeot, Suzuki and KTM are positioning Banco Santander México as their main financial partner for branded financing of cars and motorcycles and with personalized offers. |

| Earnings Release | 3Q.2019 |

9 |

| Banco Santander México |

| § | With regard to México’s the financial inclusion program, “TUIIO”, at the end of 3Q19, the Bank had 70 branches in 15 states, with more than 70,000 customers, reaching a loan portfolio of Ps.198 million. Since TUIIO began operations, more than half of these customers have used an ATM and/or had obtained a debit card for the first time in their lives. |

| Customers | ||||||

| (Thousands) | % Variation | |||||

| Sep-19 | Jun-19 | Sep-18 | QoQ | YoY | ||

| Loyal Customers1 | 2,980 | 2,844 | 2,353 | 4.8 | 26.6 | |

| Digital Customers2 | 3,815 | 3,512 | 2,533 | 8.6 | 50.6 | |

| Santander Plus | 6,686 | 5,737 | 4,296 | 16.5 | 55.6 | |

| Santander – Aeroméxico | 1,004 | 984 | 903 | 2.0 | 11.2 | |

1 Loyal customers = Clients with non-zero balance and depending on the segment should have between two and four products and between three and ten transactions in the last 90 days.

2 Digital customers = Clients with at least one digital transaction per month in SuperNet or SuperMóvil.

| Earnings Release | 3Q.2019 |

10 |

| Banco Santander México |

ANALYSIS OF THIRD QUARTER 2019 CONSOLIDATED RESULTS

(Amounts expressed in millions of pesos, except where otherwise stated)

Loan portfolio

The evolution of the loan portfolio shows sustained growth in high-margin loan segments, reflecting a continued focus on profitability.

| Portfolio Breakdown | ||||||

| Million pesos | % Variation | |||||

| Sep-19 | Jun-19 | Sep-18 | QoQ | YoY | ||

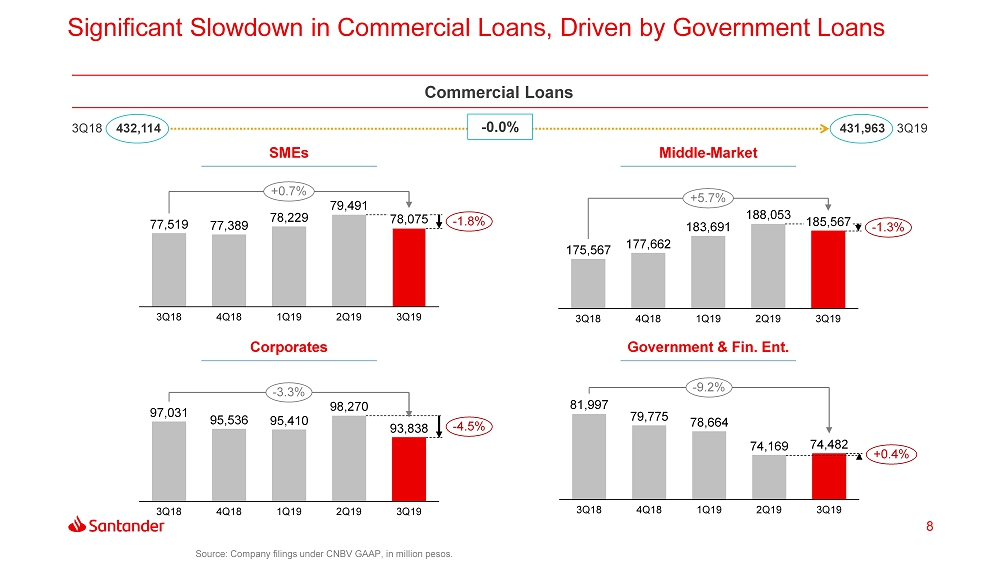

| Commercial | 431,963 | 439,983 | 432,114 | (1.8) | (0.0) | |

| Middle-market | 185,567 | 188,053 | 175,567 | (1.3) | 5.7 | |

| Corporates | 93,838 | 98,270 | 97,031 | (4.5) | (3.3) | |

| SMEs | 78,075 | 79,491 | 77,519 | (1.8) | 0.7 | |

| Government & Financial Entities | 74,482 | 74,169 | 81,997 | 0.4 | (9.2) | |

| Individuals | 265,363 | 260,346 | 248,006 | 1.9 | 7.0 | |

| Consumer | 116,630 | 114,695 | 109,471 | 1.7 | 6.5 | |

| Credit cards | 58,960 | 57,476 | 54,997 | 2.6 | 7.2 | |

| Other consumer | 57,670 | 57,219 | 54,474 | 0.8 | 5.9 | |

| Mortgages | 148,733 | 145,651 | 138,535 | 2.1 | 7.4 | |

| Total | 697,326 | 700,329 | 680,120 | (0.4) | 2.5 | |

The total loan portfolio rose 2.5% YoY, or Ps.17,206 million, to Ps.697,326 million in Sep-19. On a sequential basis, the total loan portfolio decreased 0.4%, or Ps.3,003 million.

Thecommercial loan portfolio is comprised of loans to business and commercial entities, as well as loans to government entities and financial institutions, and represented 61.9% of the total loan portfolio. Excluding loans to government entities and financial institutions, the commercial loan portfolio accounted for 51.3% of the total. Middle-market, Corporate and SME loans represented 26.6%, 13.5% and 11.2% of the total loan portfolio, respectively.

Theindividuals loan portfolio, comprised of mortgages, consumer and credit card loans, represented 38.1% of the total loan portfolio. Mortgage, credit card and consumer loans, represented 21.3%, 8.5% and 8.3% of the total loan portfolio, respectively. The Bank continues with the strategy of prioritizing payroll loans over unsecured personal loans and taking advantage of our strong position in the middle market and SME segments. Since the Bank began focusing on driving payroll loans in 1Q17, it has expanded the share of payroll loans by 9 percentage points to 62.3% of total consumer loans as of 3Q19.

| Earnings Release | 3Q.2019 |

11 |

| Banco Santander México |

| Loan portfolio breakdown | ||||||||

| Million pesos | ||||||||

| Sep-19 | % | Jun-19 | % | Sep-18 | % | |||

| Performing loans | ||||||||

| Commercial | 426,180 | 61.1 | 434,438 | 62.0 | 426,351 | 62.7 | ||

| Individuals | 254,865 | 36.5 | 250,260 | 35.7 | 237,801 | 35.0 | ||

| Consumer | 112,099 | 16.1 | 110,226 | 15.7 | 105,232 | 15.5 | ||

| Credit cards | 56,452 | 8.1 | 54,950 | 7.8 | 52,642 | 7.7 | ||

| Other consumer | 55,647 | 8.0 | 55,276 | 7.9 | 52,590 | 7.7 | ||

| Mortgages | 142,766 | 20.5 | 140,034 | 20.0 | 132,569 | 19.5 | ||

| Total performing loans | 681,045 | 97.7 | 684,698 | 97.8 | 664,152 | 97.7 | ||

| Non-performing loans | ||||||||

| Commercial | 5,783 | 0.8 | 5,545 | 0.8 | 5,763 | 0.8 | ||

| Individuals | 10,498 | 1.5 | 10,086 | 1.4 | 10,205 | 1.5 | ||

| Consumer | 4,531 | 0.6 | 4,469 | 0.6 | 4,239 | 0.6 | ||

| Credit cards | 2,509 | 0.4 | 2,526 | 0.4 | 2,355 | 0.3 | ||

| Other consumer | 2,022 | 0.3 | 1,943 | 0.3 | 1,884 | 0.3 | ||

| Mortgages | 5,967 | 0.9 | 5,617 | 0.8 | 5,966 | 0.9 | ||

| Total non-performing loans | 16,281 | 2.3 | 15,631 | 2.2 | 15,968 | 2.3 | ||

| Total loan portfolio | ||||||||

| Commercial | 431,963 | 61.9 | 439,983 | 62.8 | 432,114 | 63.5 | ||

| Individuals | 265,363 | 38.1 | 260,346 | 37.2 | 248,006 | 36.5 | ||

| Consumer | 116,630 | 16.7 | 114,695 | 16.4 | 109,471 | 16.1 | ||

| Credit cards | 58,960 | 8.5 | 57,476 | 8.2 | 54,997 | 8.1 | ||

| Other consumer | 57,670 | 8.3 | 57,219 | 8.2 | 54,474 | 8.0 | ||

| Mortgages | 148,733 | 21.3 | 145,651 | 20.8 | 138,535 | 20.4 | ||

| Total loan portfolio | 697,326 | 100.0 | 700,329 | 100.0 | 680,120 | 100.0 |

As of Sep-19, commercial loans remained unchanged YoY, reflecting more difficult comps in corporate, government and financial entities loans, as well as the Bank’s prudent and disciplined approach to pricing. Corporate loans decreased 3.3%, with difficult comps and some prepayments, while government and financial entities loans decreased 6.1% and 20.6% YoY, respectively. The Bank has been reducing its exposure to state-owned companies while prioritizing loans to certain states that bring along their payrolls, providing future cross-selling opportunities. Finally, loans to middle-market companies, increased 5.7% YoY, also experiencing some prepayments during the quarter, while SME loans increased 0.7% YoY, reflecting weak loan demand.

Mortgage loans posted a good performance during the quarter, increasing 7.4% YoY and 2.1% sequentially, even after the sale of a Ps.1 billion non-performing loan portfolio in January of this year. The Hipoteca Plus product remains the main driver behind this strong performance, accounting for 73% of total mortgage origination in the quarter. However, mortgage loans were still affected by the run-off of acquired portfolios. Excluding this effect, the mortgage portfolio would have increased 12.0% YoY, higher than average market growth.

Credit card loans increased 7.2% YoY and 2.6% QoQ, while credit card usage continued to grow – up 11.0% this quarter, although a high percentage of customers continued to pay their balances in full. The Bank further expanded this product by cross-selling credit cards to its payroll and Hipoteca Plus customers, while also supporting healthy asset quality and good levels of profitability.

The strategy of prioritizing Banco Santander México’s payroll loans over unsecured personal loans and leveraging a strong position in the middle market and SME segments is driving robust growth in consumer loans. Payroll loans continued expanding at a solid rate during the quarter, increasing 12.1% YoY and 1.2% QoQ, which was above-market growth. However personal loans decreased 8.6% YoY and 1.7% QoQ, as the Bank focused on further strengthening its payroll franchise.

| Earnings Release | 3Q.2019 |

12 |

| Banco Santander México |

Total Deposits

Total deposits in Sep-19 were Ps.683,590 million, an increase of 0.5% YoY and a decrease of 5.2% sequentially. Term deposits increased 5.3% YoY and decreased 6.4% QoQ to Ps.244,745 million. Term deposits from individuals grew 15.4% YoY and 1.0% QoQ, still benefiting from a higher interest rate environment. Demand deposits reached Ps.438,845 million, decreasing 2.0% YoY and 4.5% sequentially. Demand deposits from individuals rose 5.0% YoY, while demand deposits from corporates decreased 4.7% YoY.

The focus on driving profitability across the deposit base, by prioritizing retail deposits and foregoing certain expensive corporate deposits, resulted in a 2.9% YoY contraction in corporate deposits. In turn, individual deposits grew 8.9% YoY, as the Bank continued making headway in attracting and retaining retail clients.

Net interest income

| Net interest income | |||||||||||

| Million pesos | % variation | % variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | ||||

| Interest on funds available | 1,017 | 1,019 | 801 | (0.2) | 27.0 | 2,895 | 2,325 | 24.5 | |||

| Interest on margin accounts | 256 | 266 | 211 | (3.8) | 21.3 | 830 | 727 | 14.2 | |||

| Interest and yield on securities | 4,847 | 4,675 | 5,218 | 3.7 | (7.1) | 14,156 | 14,404 | (1.7) | |||

| Interest and yield on loan portfolio – excluding credit cards | 18,738 | 18,591 | 17,408 | 0.8 | 7.6 | 55,435 | 49,370 | 12.3 | |||

| Interest and yield on loan portfolio related to credit cards | 3,809 | 3,774 | 3,472 | 0.9 | 9.7 | 11,097 | 10,152 | 9.3 | |||

| Commissions collected on loan originations | 136 | 155 | 137 | (12.3) | (0.7) | 423 | 437 | (3.2) | |||

| Interest and premium on sale and repurchase agreements and securities loans | 1,662 | 2,076 | 1,581 | (19.9) | 5.1 | 6,958 | 4,918 | 41.5 | |||

| Interest income | 30,465 | 30,556 | 28,828 | (0.3) | 5.7 | 91,794 | 82,333 | 11.5 | |||

| Daily average interest- earnings assets | 1,156,479 | 1,151,592 | 1,116,683 | 0.4 | 3.6 | 1,162,217 | 1,099,598 | 5.7 | |||

| Interest from customer deposits – demand deposits | (3,299) | (3,188) | (2,715) | 3.5 | 21.5 | (9,500) | (7,673) | 23.8 | |||

| Interest from customer deposits – time deposits | (4,704) | (4,394) | (3,951) | 7.1 | 19.1 | (13,400) | (11,013) | 21.7 | |||

| Interest from credit instruments issued | (893) | (868) | (671) | 2.9 | 33.1 | (2,467) | (2,040) | 20.9 | |||

| Earnings Release | 3Q.2019 |

13 |

| Banco Santander México |

| Interest on bank and other loans | (1,098) | (1,209) | (1,187) | (9.2) | (7.5) | (3,319) | (3,033) | 9.4 | |||

| Interest on subordinated capital notes | (402) | (388) | (442) | 3.6 | (9.0) | (1,205) | (1,306) | (7.7) | |||

| Interest and premium on sale and repurchase agreements and securities loans | (3,480) | (3,921) | (4,067) | (11.2) | (14.4) | (12,277) | (12,063) | 1.8 | |||

| Interest expense | (13,876) | (13,968) | (13,033) | (0.7) | 6.5 | (42,168) | (37,128) | 13.6 | |||

| Daily average interest-bearing liabilities | 1,023,281 | 1,019,172 | 993,960 | 0.4 | 2.9 | 1,029,221 | 974,364 | 5.6 | |||

| Net interest income | 16,589 | 16,588 | 15,795 | 0.0 | 5.0 | 49,626 | 45,205 | 9.8 |

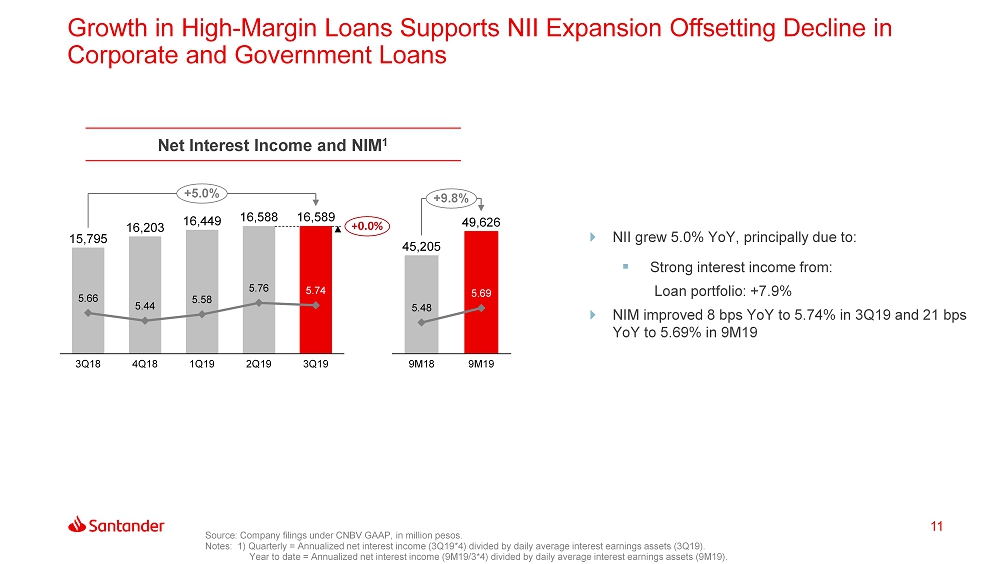

Net interest income in 3Q19 totaled Ps.16,589 million, increasing 5.0% YoY, or Ps.794 million, and remaining flat sequentially.

The 5.0% YoY increase in net interest income resulted from the combination of:

| i) | A 5.7%, or Ps.1,637 million, increase in interest income, to Ps.30,465 million, stemming from a 3.6%, or Ps.39,796 million, increase in average interest-earning assets and a 21 basis points increase in the average interest rate received; and |

| ii) | A 6.5%, or Ps.843 million, increase in interest expense, to Ps.13,876 million, resulting from a 2.9%, or Ps.29,321 million, increase in interest-bearing liabilities and an 18 basis points increase in the average interest rate paid. |

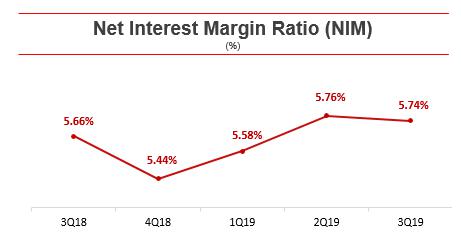

The net interest margin ratio (NIM), calculated using daily average interest-earning assets for 3Q19, stood at 5.74%, compared to 5.66% in 3Q18 and 5.76% in 2Q19. The YoY increase in NIM mainly reflects the Bank’s focus on profitability across the balance sheet, further supported by steady growth in high-margin loans, and despite softer economic conditions. On a cumulative basis, NIM for 9M19 reached 5.69%, an increase of 21 basis points vs. 9M18.

| Earnings Release | 3Q.2019 |

14 |

| Banco Santander México |

Interest Income

Total average interest earning assets in 3Q19 amounted to Ps.1,156,479 million, increasing 3.6%, or Ps.39,796 million, YoY, mainly driven by 5.5% growth, or Ps.35,824 million, in the average loan portfolio, and by 27.7% growth, or Ps.21,515 million, in funds available, partly offset by a 6.1% decrease, or Ps.17,025 million, in investment in securities, by a 0.5% decrease, or Ps.374 million, in repurchase agreements, and by a 0.6% decrease, or Ps.144 million, in margin accounts. Banco Santander México’s interest earning assets are broken down as follows:

| Average Assets (Interest-Earnings Assets) | |||||

| Breakdown (%) | |||||

| 3Q18 | 4Q18 | 1Q19 | 2Q19 | 3Q19 | |

| Loan portfolio | 58.9 | 57.0 | 57.6 | 59.9 | 59.9 |

| Investment in securities | 25.0 | 25.6 | 20.7 | 21.1 | 22.6 |

| Repurchase agreements | 7.0 | 8.5 | 13.4 | 8.6 | 6.8 |

| Funds available | 7.0 | 6.2 | 5.7 | 8.1 | 8.6 |

| Margin accounts | 2.1 | 2.7 | 2.6 | 2.3 | 2.1 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

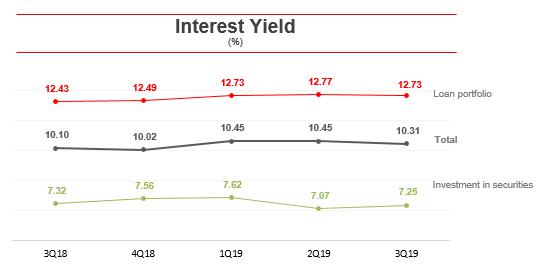

Banco Santander México’s interest income consists mainly of interest from the loan portfolio and commissions on loan originations, which in 3Q19 generated Ps.22,683 million and accounted for 74.5% of total interest income. The remaining interest income of Ps.7,782 million is broken down as follows: 15.9% from investment in securities, 5.5% from repurchase agreements, 3.3% from funds available, and 0.8% from margin accounts.

Interest income for 3Q19 increased 5.7%, or Ps.1,637 million YoY, to Ps.30,465 million, mainly reflecting higher interest income from the total loan portfolio, funds available and repurchase agreements, which increased 8.0%, or Ps.1,667 million, 27.0%, or Ps.216 million, and 5.1%, or Ps.81 million, respectively, partly offset by a 7.1%, or Ps.371 million, decrease in investment in securities.

The average interest yield on interest-earning assets in 3Q19 stood at 10.31%, increasing 21 basis points from 10.10% in 3Q18, supported by steady growth in high-margin loans. Sequentially, the average interest yield on interest-earning assets decreased 19 basis points from 10.50% in 2Q19. During the quarter, the Mexican Central Bank (Banxico) made two interest rate cuts of 25 basis points each, totaling 50 basis points.

In 3Q19, the average interest rate on the total loan portfolio stood at 12.73%, increasing 30 basis points YoY, supported by the Bank’s focus on profitability across the balance sheet. The average interest rate on the consumer portfolio stood at 25.67%, increasing 107 basis points YoY, while the yield of credit card loans stood at 25.68%, increasing 84 basis points YoY, due to the Bank’s strategy of rebalancing its portfolio toward a more profitable product mix. The average interest rate on the investment in securities portfolio stood at 7.25%, decreasing 7 basis points YoY.

| Earnings Release | 3Q.2019 |

15 |

| Banco Santander México |

| Interest income | |||||||||||

| Million Pesos | 3Q19 | 3Q18 | Var YoY | ||||||||

| Average Balance | Interest | Yield (%) | Average Balance | Interest | Yield (%) | Average Balance | Interest (%) | Yield (bps) | |||

| Funds available | 99,263 | 1,017 | 4.01 | 77,748 | 801 | 4.03 | 27.7 | 27.0 | (2) | ||

| Margin accounts | 23,843 | 256 | 4.20 | 23,987 | 211 | 3.44 | (0.6) | 21.3 | 76 | ||

| Investment in securities | 261,740 | 4,847 | 7.25 | 278,765 | 5,218 | 7.32 | (6.1) | (7.1) | (7) | ||

| Loan portfolio | 692,999 | 22,547 | 12.73 | 657,175 | 20,880 | 12.43 | 5.5 | 8.0 | 30 | ||

| Commissions collected on loan originations | 0. | 136 | n.a. | 0 | 137 | n.a. | n.a. | (0.7) | n.a. | ||

| Sale and repurchase agreements and securities loans | 78,634 | 1,662 | 8.27 | 79,008 | 1,581 | 7.83 | (0.5) | 5.1 | 44 | ||

| Interest income | 1,156,479 | 30,465 | 10.31 | 1,116,683 | 28,828 | 10.10 | 3.6 | 5.7 | 21 | ||

As previously explained, the main contributor to interest income growth was the 8.0%, or Ps.1,667 million, increase in interest income from the total loan portfolio. This increase resulted from an 5.5%, or Ps.35,824 million, rise in average loan portfolio volume, and a 30 basis points increase in the average interest rate. Higher interest income from the loan portfolio resulted from the following YoY increases by product:

| § | Commercial: 4.5%, or Ps.18,793 million, with a 10.21% interest yield, which increased 19 bps; |

| § | Mortgages: 7.5%, or Ps.10,184 million, with a 9.99% interest yield, which increased 1 bps; |

| § | Consumer: 6.5%, or Ps.3,493 million, with a 25.67% interest yield, which increased 107 bps; and |

| § | Credit Cards: 6.1%, or Ps.3,354 million, with a 25.68% interest yield, which increased 84 bps. |

Interest income from investment in securities decreased 7.1%, or Ps.371 million, which resulted from the decrease of 6.1%, or Ps.17,025 million, in average volume, and a 7 basis points decrease in the average interest rate. Interest income from repurchase agreements grew 5.1%, or Ps.81 million, which resulted from the combined effect of a 0.5%, or Ps.374 million, decrease in average volume, and a 44 basis points increase in the average interest rate.

Interest expense

Total average interest-bearing liabilities amounted to Ps.1,023,281 million, increasing 2.9%, or Ps.29,321 million YoY, and were driven by increases of 10.8%, or Ps.42,201 million, in demand deposits, 15.0%, or Ps.7,113 million, in credit instruments issued, 2.6%, or Ps.6,882 million, in term deposits, and 2.5%, or Ps.618 million, in subordinated capital notes. These increases were partly offset by a 9.5%, or Ps.19,776 million, decrease, in repurchase agreements and a 12.7%, or Ps.7,717 million, decrease in bank and other loans.

Banco Santander México’s interest-bearing liabilities are broken down as follows:

| Average liabilities (interest-bearing liabilities) | |||||

| Breakdown (%) | |||||

| 3Q18 | 4Q18 | 1Q19 | 2Q19 | 3Q19 | |

| Demand deposits | 39.2 | 37.5 | 39.1 | 40.9 | 42.2 |

| Time deposits | 26.5 | 26.1 | 25.4 | 25.9 | 26.5 |

| Sale and repurchase agreements and securities loans | 20.9 | 23.8 | 23.3 | 19.4 | 18.3 |

| Bank and other loans | 6.1 | 5.5 | 5.4 | 6.1 | 5.2 |

| Credit instruments issued | 4.8 | 4.5 | 4.3 | 5.2 | 5.3 |

| Subordinated capital notes | 2.5 | 2.6 | 2.5 | 2.5 | 2.5 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

| Earnings Release | 3Q.2019 |

16 |

| Banco Santander México |

Banco Santander México’s interest expense consists mainly of interest paid on customer deposits and repurchase agreements, which in 3Q19 amounted to Ps.8,003 million and Ps.3,480 million, respectively, and accounted for 57.7% and 25.1% of interest expense. The remaining interest expense of Ps.2,393 million was paid as follows: 7.9% on bank and other loans, 6.4% on credit instruments issued, and 2.9% on subordinated debentures.

Interest expense for 3Q19 increased 6.5%, or Ps.843 million, to Ps.13,876 million, mainly driven by higher interest expenses on term deposits and demand deposits.

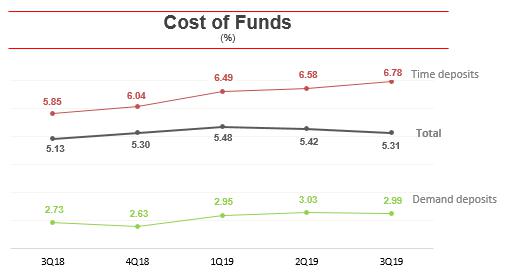

The average interest rate on interest-bearing liabilities increased 18 basis points to 5.31% in 3Q19. For 3Q19, the average interest rate on the main sources of funding increased YoY as follows:

| § | 93 basis points in term deposits, at an average interest rate paid of 6.78%; |

| § | 87 basis points in credit instruments issued, at an average interest rate paid of 6.40%; |

| § | 46 basis points in bank and other loans, at an average interest rate paid of 8.10%; and |

| § | 26 basis points in demand deposits, at an average interest rate paid of 2.99%. |

| Interest expense | |||||||||||

| Million pesos | 3Q19 | 3Q18 | Var YoY | ||||||||

| Average Balance | Interest | Yield (%) | Average Balance | Interest | Yield (%) | Average Balance | Interest (%) | Yield (bps) | |||

| Demand deposits | 431,526 | 3,299 | 2.99 | 389,325 | 2,715 | 2.73 | 10.8 | 21.5 | 26 | ||

| Time deposits | 271,368 | 4,704 | 6.78 | 264,486 | 3,951 | 5.85 | 2.6 | 19.1 | 93 | ||

| Credit instruments issued | 54,608 | 893 | 6.40 | 47,495 | 671 | 5.53 | 15.0 | 33.1 | 87 | ||

| Bank and other loans | 53,055 | 1,098 | 8.10 | 60,772 | 1,187 | 7.64 | (12.7) | (7.5) | 46 | ||

| Subordinated capital notes | 25,257 | 402 | 6.23 | 24,639 | 442 | 7.02 | 2.5 | (9.0) | (79) | ||

| Sale and repurchase agreements and securities loans | 187,467 | 3,480 | 7.26 | 207,243 | 4,067 | 7.68 | (9.5) | (14.4) | (42) | ||

| Interest expense | 1,023,281 | 13,876 | 5.31 | 993,960 | 13,033 | 5.13 | 2.9 | 6.5 | 18 | ||

| Earnings Release | 3Q.2019 |

17 |

| Banco Santander México |

Increases in retail deposits continue to reflect the Bank’s focus on driving profitability in its deposit base. The average balance of demand deposits expanded 10.8%, while the average balance of term deposits rose 2.6%. This volume growth, together with still high interest rates, resulted in increases of 21.5% and 19.1% in interest paid on demand and term deposits, respectively.

The 14.4%, or Ps.587 million, decrease in interest expenses on repurchase agreements resulted from a 9.5%, or Ps.19,776 million, decrease in the average balance and a 42 basis points decrease in the average interest rate paid.

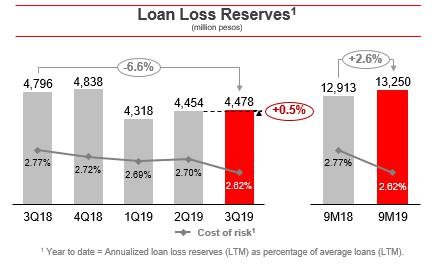

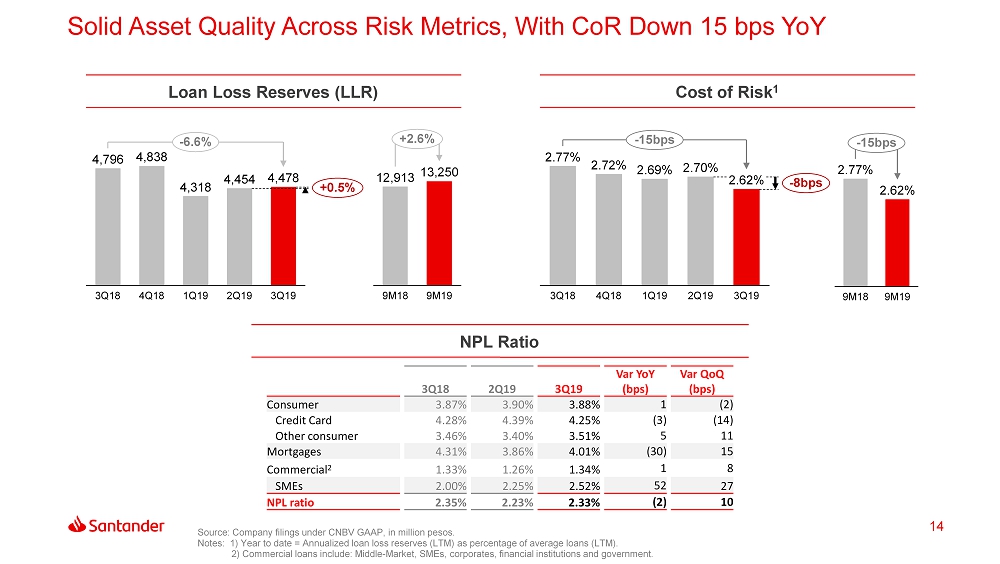

Provisions for loan losses and asset quality

During 3Q19, provisions for loan losses amounted to Ps.4,478 million, which represented a decrease of 6.6%, or Ps.318 million, YoY, and an increase of 0.5%, or Ps.24 million, on a sequential basis. In 3Q18, the Bank made additional provisions for a specific project finance corporate loan, which contributed to easier YoY comps. At the same time, provisions for consumer loans tend to be higher in the second half of the year, due to back-to-school spending in August and September.

Please note that because of new accounting rules effective at the beginning of 2019, banks are required to record recoveries in the provision account. Previously, recoveries were booked in the other income line. For comparative purposes, provisions for 2018 are net of recoveries.

| Loan Loss Reserves | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | YoY | ||||

| Commercial | 1,208 | 1,276 | 1,592 | (5.3) | (24.1) | 3,553 | 4,038 | (12.0) | |||

| Consumer | 2,994 | 2,985 | 2,924 | 0.3 | 2.4 | 9,069 | 8,254 | 9.9 | |||

| Mortgages | 276 | 193 | 280 | 43.1 | (1.3) | 628 | 621 | 1.2 | |||

| Total | 4,478 | 4,454 | 4,796 | 0.6 | (6.6) | 13,250 | 12,913 | 2.6 | |||

| Cost of Risk (%) | ||||||

| Variation (bps) | ||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | ||

| Commercial | 1.10 | 1.20 | 1.40 | (10) | (30) | |

| Consumer | 10.65 | 10.74 | 10.50 | (9) | 15 | |

| Mortgages | 0.90 | 0.92 | 0.62 | (2) | 28 | |

| Total | 2.62 | 2.70 | 2.77 | (8) | (15) | |

| Earnings Release | 3Q.2019 |

18 |

| Banco Santander México |

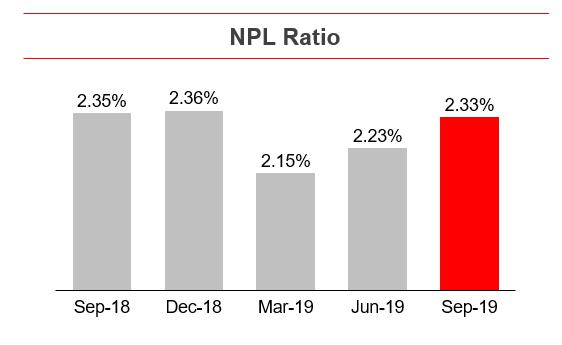

Non-performing loans at Sep-19 increased Ps.313 million YoY, or 2.0%, to Ps.16,281 million, and increased Ps.650 million, or 4.2%, on a sequential basis. The NPL ratio for Sep-19 stood at 2.33%, a 2 basis points decline from 2.35% in Sep-18. Sequentially, the NPL ratio, increased 10 basis points from 2.23% in Jun-19.

The YoY increase in non-performing loans was mainly due to an increase of 6.9%, or Ps.292 million, in consumer loans (including credit cards), together with a 0.3%, or Ps.20 million, increase in commercial loans. Mortgage loans remained stable.

On a sequential basis, Banco Santander México reported a 4.2%, or Ps.650 million, increase in non-performing loans, which resulted from increases in the non-performing loan portfolio of mortgages, commercial and consumer (including credit cards) loans of Ps.350 million, Ps.238 million and Ps.62 million, respectively.

NPLs for the mortgage loan portfolio decreased 30 basis points YoY and increased 15 basis points sequentially. Consumer loan NPLs (including credit cards) increased 1 basis point YoY and decreased 2 basis points QoQ. At the same time, commercial loan NPLs increased 1 basis point YoY and increased 8 basis points sequentially.

The breakdown of the non-performing loan portfolio is as follows: mortgage loans 36.7%, commercial loans 35.5% and consumer loans (including credit cards) 27.8%.

| Non-Performing loan ratio (%) | ||||||

| Variation (bps) | ||||||

| Sep-19 | Jun-19 | Sep-18 | QoQ | YoY | ||

| Commercial | 1.34 | 1.26 | 1.33 | 8 | 1 | |

| Individuals | ||||||

| Consumer | 3.88 | 3.90 | 3.87 | (2) | 1 | |

| Credit Card | 4.25 | 4.39 | 4.28 | (14) | (3) | |

| Other consumer | 3.51 | 3.40 | 3.46 | 11 | 5 | |

| Mortgages | 4.01 | 3.86 | 4.31 | 15 | (30) | |

| Total | 2.33 | 2.23 | 2.35 | 10 | (2) | |

The aforementioned variations in non-performing loans led to an NPL ratio of 2.33% in Sep-19, decreasing 2 basis points from 2.35% in Sep-18 and increasing 10 basis point compared to the 2.23% ratio reported in Jun-19. The current NPL ratio reflects Banco Santander México’s strong focus on prudent risk management and continual monitoring of loan portfolio quality.

Finally, the coverage ratio for Sep-19 stood at 130.82%, an increase from 127.60% in Sep-18 and a decrease from 136.56% in Sep-19.

| Earnings Release | 3Q.2019 |

19 |

| Banco Santander México |

Commission and fee income, net

| Commission and fee income, net | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | ||||

| Commission and fee income | |||||||||||

| Debit and credit card | 2,447 | 2,361 | 1,979 | 3.6 | 23.6 | 7,070 | 5,920 | 19.4 | |||

| Account management | 374 | 352 | 307 | 6.3 | 21.8 | 1,059 | 907 | 16.8 | |||

| Collection services | 727 | 759 | 727 | (4.2) | 0.0 | 2,215 | 2,152 | 2.9 | |||

| Investment funds | 400 | 394 | 397 | 1.5 | 0.8 | 1,164 | 1,174 | (0.9) | |||

| Insurance | 1,217 | 1,383 | 1,152 | (12.0) | 5.6 | 3,760 | 3,475 | 8.2 | |||

| Purchase-sale of securities and money market transactions | 252 | 246 | 212 | 2.4 | 18.9 | 687 | 824 | (16.6) | |||

| Checks trading | 59 | 65 | 58 | (9.2) | 1.7 | 187 | 182 | 2.7 | |||

| Foreign trade | 308 | 352 | 308 | (12.5) | 0.0 | 978 | 937 | 4.4 | |||

| Financial advisory services | 485 | 340 | 281 | 42.6 | 72.6 | 1,181 | 992 | 19.1 | |||

| Other | 235 | 234 | 238 | 0.4 | (1.3) | 705 | 635 | 11.0 | |||

| Total | 6,504 | 6,486 | 5,659 | 0.3 | 14.9 | 19,006 | 17,198 | 10.5 | |||

| Commission and fee expense | |||||||||||

| Debit and credit card | (1,052) | (1,064) | (793) | (1.1) | 32.7 | (3,038) | (2,711) | 12.1 | |||

| Investment funds | (1) | 0 | 0 | 0.0 | 0.0 | (1) | (1) | 0.0 | |||

| Insurance | (39) | (25) | (29) | 56.0 | 34.5 | (87) | (88) | (1.1) | |||

| Purchase-sale of securities and money market transactions | (84) | (33) | (72) | 154.5 | 16.7 | (145) | (200) | (27.5) | |||

| Checks trading | (11) | (4) | (7) | 175.0 | 57.1 | (23) | (21) | 9.5 | |||

| Financial advisory services | (77) | (15) | (1) | 413.3 | — | (103) | (3) | — | |||

| Other | (660) | (648) | (486) | 1.9 | 35.8 | (1,906) | (1,572) | 21.2 | |||

| Total | (1,924) | (1,789) | (1,388) | 7.5 | 38.6 | (5,303) | (4,596) | 15.4 | |||

| Commission and fee income, net | |||||||||||

| Debit and credit card | 1,395 | 1,297 | 1,186 | 7.6 | 17.6 | 4,032 | 3,209 | 25.6 | |||

| Account management | 374 | 352 | 307 | 6.3 | 21.8 | 1,059 | 907 | 16.8 | |||

| Collection services | 727 | 759 | 727 | (4.2) | 0.0 | 2,215 | 2,152 | 2.9 | |||

| Investment funds | 399 | 394 | 397 | 1.3 | 0.5 | 1,163 | 1,173 | (0.9) | |||

| Insurance | 1,178 | 1,358 | 1,123 | (13.3) | 4.9 | 3,673 | 3,387 | 8.4 | |||

| Purchase-sale of securities and money market transactions | 168 | 213 | 140 | (21.1) | 20.0 | 542 | 624 | (13.1) | |||

| Checks trading | 48 | 61 | 51 | (21.3) | (5.9) | 164 | 161 | 1.9 | |||

| Foreign trade | 308 | 352 | 308 | (12.5) | 0.0 | 978 | 937 | 4.4 | |||

| Financial advisory services | 408 | 325 | 280 | 25.5 | 45.7 | 1,078 | 989 | 9.0 | |||

| Other | (425) | (414) | (248) | 2.7 | 71.4 | (1,201) | (937) | 28.2 | |||

| Total | 4,580 | 4,697 | 4,271 | (2.5) | 7.2 | 13,703 | 12,602 | 8.7 | |||

In 3Q19, net commission and fee income totaled Ps.4,580 million, increasing 7.2% YoY, or Ps.309 million, and decreasing 2.5%, or Ps.117 million, QoQ. Commission and fee income increased 14.9%, or Ps.845 million, YoY, while commission and fee expense increased 38.6%, or Ps.536 million.

| Earnings Release | 3Q.2019 |

20 |

| Banco Santander México |

The main contributors to net commissions and fees were credit and debit card fees, which accounted for 30.5% of the total, followed by insurance fees and collection services fees, which accounted for 25.7% and 15.9% of total commissions and fees, respectively.

| Commission and fee income, net | ||||||

| Breakdown (%) | ||||||

| 3Q19 | 2Q19 | 3Q18 | 9M19 | 9M18 | ||

| Credit cards | 30.5 | 27.6 | 27.8 | 29.4 | 25.5 | |

| Insurance | 25.7 | 28.9 | 26.3 | 26.8 | 26.9 | |

| Collection services | 15.9 | 16.2 | 17.0 | 16.2 | 17.1 | |

| Financial advisory services | 8.9 | 6.9 | 6.6 | 7.9 | 7.8 | |

| Investment funds | 8.7 | 8.4 | 9.3 | 8.5 | 9.3 | |

| Account management | 8.2 | 7.5 | 7.2 | 7.7 | 7.2 | |

| Foreign trade | 6.7 | 7.5 | 7.2 | 7.1 | 7.4 | |

| Purchase-sale of securities and money market transactions | 3.7

| 4.5

| 3.3

| 4.0

| 5.0

| |

| Checks trading | 1.0 | 1.3 | 1.2 | 1.2 | 1.3 | |

| Other | (9.3) | (8.8) | (5.9) | (8.8) | (7.5) | |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Net commissions and fees rose 7.2% YoY in 3Q19, mostly as a result of the following increases:

| i) | 17.6%, or Ps.209 million, in debit and credit card fees. Fee income was up 23.6%, driven by sustained higher usage levels and lower origination costs; |

| ii) | 45.7%, or Ps.128 million, in financial advisory services; |

| iii) | 21.8%, or Ps.67 million, in account management, mainly a result of Banco Santander México’s continued focus on being an integral part of its clients’ liquidity management efforts, which led to increased transactional activity; and |

| iv) | 4.9%, or Ps.55 million, in insurance fees, driven by strong cross-selling opportunities among the Bank’s mortgage and payroll customers, along with the performance of the Bank’s digital car insurance platform; |

These positive contributions to net commissions and fees were partly offset by a 71.4%, or Ps.177 million, increase in other commissions and fees paid.

On a cumulative basis, net commissions and fees amounted Ps.13,703 million in 9M19, reflecting a YoY increase of 8.7%, or Ps.1,101 million. Commission and fee income increased 10.5%, while commission and fee expense increased 15.4%.

| Earnings Release | 3Q.2019 |

21 |

| Banco Santander México |

Net gain (loss) on financial assets and liabilities

| Net gain (loss) on financial assets and liabilities | |||||||||||

| Million pesos | % variation | % variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | ||||

| Valuation | |||||||||||

| Foreign exchange | 59 | (129) | (246) | 145.7 | 124.0 | (47) | 329 | (114.3) | |||

| Derivatives | 1,163 | 312 | 1,753 | 272.8 | (33.7) | 4,020 | 7,855 | (48.8) | |||

| Equity securities | 13 | (57) | (278) | 122.8 | 104.7 | 36 | 328 | (89.0) | |||

| Debt instruments | 610 | 1,031 | (145) | (40.8) | 520.7 | 1,594 | (1,348) | 218.2 | |||

| Valuation result | 1,845 | 1,157 | 1,084 | 59.5 | 70.2 | 5,603 | 7,164 | (21.8) | |||

| Purchase / sale of securities | |||||||||||

| Foreign exchange | 156 | 232 | 388 | (32.8) | (59.8) | 586 | 447 | 31.1 | |||

| Derivatives | (1,261) | (1,065) | (1,197) | 18.4 | 5.3 | (5,329) | (6,346) | (16.0) | |||

| Equity securities | 491 | 450 | 355 | 9.1 | 38.3 | 988 | 872 | 13.3 | |||

| Debt instruments | (130) | (210) | 213 | (38.1) | (161.0) | 149 | 43 | 246.5 | |||

| Purchase -sale result | (744) | (593) | (241) | 25.5 | 208.7 | (3,606) | (4,984) | (27.6) | |||

| Total | 1,101 | 564 | 843 | 95.2 | 30.6 | 1,997 | 2,180 | (8.4) | |||

In 3Q19, Banco Santander México reported a Ps.1,101 million net gain from financial assets and liabilities, which compares to gains of Ps.843 million in 3Q18 and Ps.564 million in 2Q19.

The Ps.1,101 million net gain from financial assets and liabilities in the quarter is mostly a result of:

i) A Ps.1,845 million valuation gain, which resulted from gains of Ps.1,163 million, Ps.610 million, Ps.59 million and Ps.13 million in derivative instruments, debt instruments, foreign exchange and equity securities, respectively; and

ii) A Ps.744 million purchase-sale loss related to losses of Ps.1,261 million and Ps.130 million in derivative instruments and debt instruments, respectively. These losses were partly offset by gains of Ps.491 million and Ps.156 million in equity securities and foreign exchange, respectively.

On a cumulative basis, the net gain from financial assets and liabilities for 9M19 reached Ps.1,997 million, representing an 8.4% YoY decrease.

| Earnings Release | 3Q.2019 |

22 |

| Banco Santander México |

Other operating expense

| Other operating income | |||||||||||

| Million pesos | % variation | % variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | ||||

| Cancellation of liabilities and reserves | 216 | 71 | 109 | 204.2 | 98.2 | 376 | 343 | 9.6 | |||

| Interest on personnel loans | 74 | 72 | 71 | 2.8 | 4.2 | 219 | 212 | 3.3 | |||

| Allowance for losses on foreclosed assets | (17) | (18) | (28) | (5.6) | (39.3) | (75) | (75) | 0.0 | |||

| Profit from sale of foreclosed assets | 26 | 43 | 27 | (39.5) | (3.7) | 100 | 70 | 42.9 | |||

| Technical advisory and technology services | 39 | 13 | 10 | 200.0 | 290.0 | 72 | 66 | 9.1 | |||

| Portfolio recovery legal expenses and costs | (268) | (248) | (231) | 8.1 | 16.0 | (769) | (693) | 11.0 | |||

| Premiums paid on guarantees for SMEs loans portfolio | (281) | (198) | (119) | 41.9 | 136.1 | (662) | (368) | 79.9 | |||

| Write-offs and bankruptcies | (379) | (216) | (335) | 75.5 | 13.1 | (905) | (910) | (0.5) | |||

| Income from sale of loan portfolio | 0 | 0 | 0 | 0.0 | 0.0 | 0 | (19) | (100.0) | |||

| Provision for legal and tax contingencies | (28) | (91) | (93) | (69.2) | (69.9) | (187) | (418) | (55.3) | |||

| Others | 36 | 132 | 56 | (72.7) | (35.7) | 258 | 199 | 29.6 | |||

| Total | (582) | (440) | (533) | 32.3 | 9.2 | (1,573) | (1,593) | (1.3) | |||

Other operating expenses in 3Q19 totaled Ps.582 million, up from Ps.533 million in 3Q18 and Ps.440 million reported in 2Q19.

The 9.2%, or Ps.49 million, YoY increase, in other operating expenses in 3Q19 was mainly driven by higher premiums paid on guarantees for SMEs loans portfolio. The increase was partly offset by an increase of 98.2%, or Ps.107 million, in cancellation of liabilities and reserves. On a sequential basis, the 32.3%, or Ps.142 million, increase in other operating expenses, was mainly driven by higher write-offs and bankruptcies of Ps.163 million.

On a cumulative basis, other operating expenses for 9M19 reached Ps.1,573 million, representing a 1.3%, or Ps.20 million, YoY decrease.

| Earnings Release | 3Q.2019 |

23 |

| Banco Santander México |

Administrative and promotional expenses

Administrative and promotional expenses consist of personnel costs, such as payroll and benefits, promotion and advertising expenses, and other general expenses. Personnel expenses consist mainly of salaries, social security contributions, bonuses and a long-term incentive plan for the Bank’s executives. Other general expenses are mainly related to technology and systems, administrative services - mainly outsourced in the areas of information technology - taxes and duties, professional fees, contributions to IPAB, rental of properties and hardware, advertising and communication, surveillance and cash courier services, and expenses related to maintenance, conservation and repair, among others.

| Administrative and promotional expenses | |||||||||||

| Million pesos | % variation | % variation | |||||||||

| 3Q19 | 2Q19 | 3Q18 | QoQ | YoY | 9M19 | 9M18 | 19/18 | ||||

| Salaries and employee benefits | 4,012 | 3,978 | 4,096 | 0.9 | (2.1) | 11,855 | 11,602 | 2.2 | |||

| Credit card operation | 72 | 89 | 80 | (19.1) | (10.0) | 239 | 232 | 3.0 | |||

| Professional fees | 279 | 81 | 414 | 244.4 | (32.6) | 449 | 893 | (49.7) | |||

| Leasehold | 585 | 620 | 536 | (5.6) | 9.1 | 1,802 | 1,706 | 5.6 | |||

| Promotional and advertising expenses | 215 | 216 | 141 | (0.5) | 52.5 | 682 | 607 | 12.4 | |||

| Taxes and duties | 501 | 504 | 365 | (0.6) | 37.3 | 1,489 | 1,263 | 17.9 | |||

| Technology services (IT) | 1,115 | 808 | 780 | 38.0 | 42.9 | 2,862 | 2,210 | 29.5 | |||

| Depreciation and amortization | 868 | 948 | 708 | (8.4) | 22.6 | 2,694 | 2,141 | 25.8 | |||

| Contributions to IPAB | 852 | 848 | 796 | 0.5 | 7.0 | 2,512 | 2,316 | 8.5 | |||

| Cash protection | 253 | 323 | 256 | (21.7) | (1.2) | 899 | 828 | 8.6 | |||

| Others | 1,031 | 1,067 | 831 | (3.4) | 24.1 | 3,038 | 2,268 | 34.0 | |||

| Total | 9,783 | 9,482 | 9,003 | 3.2 | 8.7 | 28,521 | 26,066 | 9.4 | |||

Banco Santander México’s administrative and promotional expenses are broken down as follows:

| Administrative and promotional expenses | ||||||

| Breakdown (%) | ||||||

| 3Q19 | 2Q19 | 3Q18 | 9M19 | 9M18 | ||

| Personnel | 41.0 | 42.0 | 45.5 | 41.6 | 44.5 | |

| Others | 10.5 | 11.3 | 9.1 | 10.7 | 8.8 | |

| Depreciation and amortization | 8.9 | 10.0 | 7.9 | 9.4 | 8.2 | |

| IPAB | 8.7 | 8.9 | 8.8 | 8.8 | 8.9 | |

| Professional fees | 2.9 | 0.9 | 4.6 | 1.6 | 3.4 | |

| Technology services (IT) | 11.4 | 8.5 | 8.7 | 10.0 | 8.5 | |

| Leasehold | 6.0 | 6.5 | 6.0 | 6.3 | 6.5 | |

| Taxes and duties | 5.1 | 5.3 | 4.1 | 5.2 | 4.8 | |

| Cash protection | 2.6 | 3.4 | 2.8 | 3.2 | 3.2 | |

| Promotional and advertising expenses | 2.2 | 2.3 | 1.6 | 2.4 | 2.3 | |

| Credit card operation | 0.7 | 0.9 | 0.9 | 0.8 | 0.9 | |

| Total | 100.0 | 100.0 | 100.00 | 100.0 | 100.0 | |

Administrative and promotional expenses in 3Q19 totaled Ps.9,783 million, compared to Ps.9,003 million in 3Q18 and Ps.9,482 million in 2Q19, increasing 8.7% YoY and 3.2% QoQ, respectively, reflecting the investment plan to enhance the Bank’s operating infrastructure and drive digitalization.

| Earnings Release | 3Q.2019 |

24 |

| Banco Santander México |

The 8.7%, or Ps.780 million, YoY rise in administrative and promotional expenses was mainly due to the following increases:

| i) | 42.9%, or Ps.335 million, in technology services; |

| ii) | 24.1%, or Ps.200 million, in other expenses; |

| iii) | 22.6%, or Ps.160 million, in depreciation and amortization; |

| iv) | 37.3%, or Ps.136 million, in taxes and duties; |

| v) | 52.5%, or Ps.74 million, in promotional and advertising expenses; |

| vi) | 7.0%, or Ps.56 million, in contributions to IPAB; and |

| vii) | 9.1%, or Ps.49 million, in rents. |

These increases were partly offset by the following decreases:

| i) | 32.6%, or Ps.135 million, in professional fees; and |

| ii) | 2.1%, or Ps.84 million, in salaries and employee benefits. |

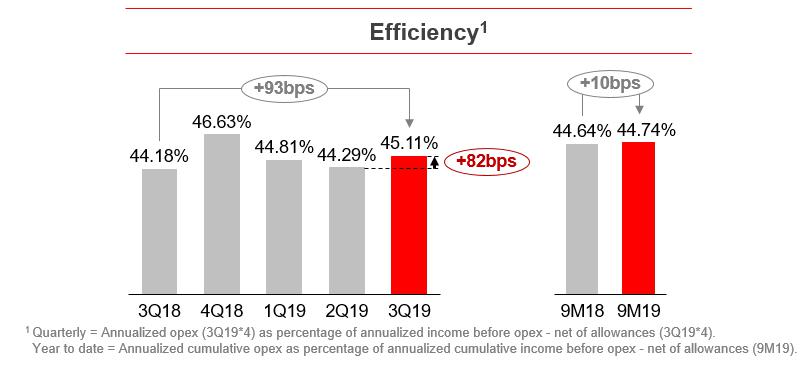

The efficiency ratio for the quarter increased 93 basis points YoY and 82 basis points QoQ to 45.11%. The execution of the Bank’s operational transformation program continues to impact the efficiency ratio.

The recurrence ratio for 3Q19 was 51.37%, down from 51.49% in 3Q18 and lower than the 55.04% reported in 2Q19.

On a cumulative basis, administrative and promotional expenses in 9M19 amounted to Ps.28,521 million, reflecting an increase of 9.4%, or Ps.2,455 million. The efficiency ratio for 9M19 increased 10 basis points YoY from 44.64% in 9M18.

Profit before taxes

Profit before taxes in 3Q19 was Ps.7,427 million, reflecting an increase of 12.9%, or Ps.850 million, YoY and a decrease of 0.6%, or Ps.46 million, QoQ.

On a cumulative basis, profit before taxes for 9M19 amounted to Ps.21,982 million, reflecting a YoY increase of 13.2%, or Ps.2,567 million.

| Earnings Release | 3Q.2019 |

25 |

| Banco Santander México |

Income taxes

In 3Q19, Banco Santander México reported a tax expense of Ps.1,910 million compared to Ps.1,481 million in 3Q18 and Ps.1,865 million in 2Q19. The effective tax rate for the quarter was 25.72%, compared to 22.52% reported in 3Q18 and 24.96% in 2Q19.

On a cumulative basis, the effective tax rate for 9M19 stood at 25.32%, 255 basis points higher than the 22.77% for 9M18.

Capitalization and liquidity

| Capitalization | ||||||

| Million pesos | Sep-19 | Jun-19 | Sep-18 | |||

| CET1 | 94,694 | 90,145 | 85,318 | |||

| Tier 1 | 104,548 | 99,735 | 94,661 | |||

| Tier 2 | 25,610 | 25,296 | 24,448 | |||

| Total Capital | 130,158 | 125,031 | 119,109 | |||

| Risk-weighted assets | ||||||

| Credit risk | 547,898 | 537,963 | 559,555 | |||

| Credit, market and operational risk | 770,793 | 757,894 | 743,422 | |||

| Credit risk ratios: | ||||||

| CET1 (%) | 17.28 | 16.76 | 15.25 | |||

| Tier 1 (%) | 19.08 | 18.54 | 16.92 | |||

| Tier 2 (%) | 4.67 | 4.70 | 4.37 | |||

| Capitalization ratio (%) | 23.76 | 23.24 | 21.29 | |||

| Total capital ratios: | ||||||

| CET1 (%) | 12.29 | 11.89 | 11.48 | |||

| Tier 1 (%) | 13.56 | 13.16 | 12.73 | |||

| Tier 2 (%) | 3.32 | 3.34 | 3.29 | |||

| Capitalization ratio (%) | 16.89 | 16.50 | 16.02 |

Banco Santander México’s capital ratio at Sep-19 was 16.89%, compared to 16.02% and 16.50% at Sep-18 and Jun-19, respectively. The 16.89% capital ratio was comprised of 12.29% of fundamental capital (CET1), 1.28% of additional capital (AT1), and 3.32% of complementary capital (Tier 2).

As of August 2019, Banco Santander México was classified in Category 1, in accordance with Article 134 Bis of the Mexican Banking Law, and the Bank remains in this category per the preliminary results dated September 30, 2019, which is the most recent available analysis.

| Earnings Release | 3Q.2019 |

26 |

| Banco Santander México |

Liquidity coverage ratio (LCR)

Pursuant to the regulatory requirements of Banxico and the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores, or “CNBV”), the average Liquidity Coverage Ratio (LCR or CCL by its Spanish acronym) for 3Q19 was 180.25%, which compares to 141.45% in 3Q18 and 177.56% in 2Q19. (Please refer to note 24 of this report).

Leverage ratio

In accordance with CNBV regulatory requirements, effective June 14, 2016, the leverage ratio was 7.64% for September 2019, 7.67% for June 2019, 7.92% for March 2019, 7.03% for December 2018, and 7.10% for September 2018.

This ratio is defined by regulators and is calculated by dividing core capital (according to Article 2 Bis 6 (CUB)) by adjusted assets (according to Article 1, II (CUB)).

RELEVANT EVENTS, TRANSACTIONS AND ACTIVITIES

Relevant Events

Banco Santander México informed that its Parent Company, issued a material fact announcement

On September 6, 2019, Banco Santander México announced that Banco Santander, S.A., its Parent Company, had published the results of its exchange offer for securities representing the share capital of the Bank. As a result of the exchange offer, the Parent Company’s shareholding in Banco Santander México increased from 74.96% to 91.65% of its share capital, with the remaining 8.35% held by minority shareholders.

Resolution of the Board of Directors of Banco Santander México, in connection with the exchange offers issued by its Parent Company

On August 20, 2019, the board of directors of Banco Santander México, after considering legal opinions as well as financial opinions in connection with the exchange offer delivered by Morgan Stanley & Co. LLC, determined as fair the exchange ratio proposed by Banco Santander, S.A., the Bank’s Parent Company, as part of the tender offer for its shares.

Banco Santander México informed that its Parent Company, issued a material fact announcement

On July 23, 2019, Banco Santander, S.A., the Parent Company of the Banco Santander México, announced that, at its Extraordinary General Meeting, shareholders had approved a capital increase required to acquire the shares in Banco Santander México that were held by minority shareholders.

Relevant Activities

Launch ofObjetivo Protegido Santander

Banco Santander México, in line with its strategy to expand its base of loyal customers and improve profitability, launchedObjetivo Protegido Santander, a savings product with broad benefits for Select segment customers. Using this product, these customers can reach a set financial goal, such as paying for their childrens’ college education. The financial goal is protected by life insurance that covers the customer’s savings plan by delivering the saved amount to beneficiaries, in the event of insured customer’s death.

| Earnings Release | 3Q.2019 |

27 |

| Banco Santander México |

Relevant Transactions

Mexico’s first bank financing with sustainability features

Banco Santander México participated as Administrative Agent and Joint Bookrunner, in Mexico’s first bank financing with sustainability features. With the participation of 11 other banks,Fibra Uno (FUNO) received a multi-currency Revolving Credit Facility for a total amount of Ps.21,350 million disbursed in two tranches, one in the amount of Ps.13,500 million and the other in the amount of $410 million dollars, with a term of five years. Banco Santander México contributed a total amount of Ps.4,000 million for the first tranche.

América Móvil financing

Banco Santander México participated, along with 18 other banks, as Administrative Agent and Joint Bookrunner, in a Revolving Credit Facility forAmérica Móvil, for a total amount of $2.5 billion dollars, with a five-year term. Banco Santander México contributed a total of $168 million dollars for the credit facility.

SUSTAINABILITY AND SOCIAL RESPONSIBILITY

705 homes delivered to victims of earthquakes in Mexico

Since the earthquakes of September 2017, Banco Santander México, along with the civil associationFideicomiso Provivah, has undertaken charitable actions as part of initiatives to help people who were affected by the earthquakes, with the rebuilding and construction of their homes. To date, 705 homes and nine restored classrooms have been delivered, benefiting approximately 5,800 earthquake victims in the six states most affected in the country.

Green Power supply agreement withAMMPER Energía

Banco Santander México entered into a Power Purchase Agreement withAMMPER Energía for the self-supply of green power for approximately 30% of the Bank's total electricity needs.

For more information about Banco Santander México as a sustainable and socially responsible company:https://servicios.santander.com.mx/comprometidos/

| Earnings Release | 3Q.2019 |

28 |

| Banco Santander México |

CREDIT RATINGS

On July 16, 2019, Fitch Ratings affirmed all Banco Santander México credit ratings (see table below). The outlook is ‘Stable’. On the same date, Fitch Ratings affirmed Santander Consumo ratings (see table below).

| Banco Santander México | Fitch Ratings | Moody’s | |

| Global scale | |||

| Foreign currency | |||

| Long term | BBB+ | A3 | |

| Short term | F2 | P-2 | |

| Local currency | |||

| Long term | BBB+ | A3 | |

| Short Term | F2 | P-2 | |

| National scale | |||

| Long term | AAA(mex) | Aaa.mx | |

| Short Term | F1+(mex) | Mx-1 | |

| Rating viability (VR) | bbb | N/A | |

| Support | 2 | N/A | |

| Counterparty risk Assessments (CR) | |||

| Long Term | N/A | A3 (cr) | |

| Short Term | N/A | P-2 (cr) | |

| Standalone BCA | N/A | baa2 | |

| Standalone Adjusted BCA | N/A | baa1 | |

| Outlook | Stable | Negative | |

| International Issuances | |||

| Tier 2 Subordinated Capital Notes due 2028 | BBB- | Baa3 (hyb) | |

| Long Term Senior Unsecured Global Notes due 2022 | BBB+ | A3 | |

| Perpetual Subordinated Non-Preferred Contingent Convertible Additional Tier 1 Capital Notes (AT1) | |||

| Global Scale | |||

| Foreign currency | |||

| Long term | BB | Ba1 (hyb) | |

| Local currency | |||

| Long term | N/A | Ba1(hyb) | |

| National scale | |||

| Long term | N/A | A1.mx (hyb) |

| Earnings Release | 3Q.2019 |

29 |

| Banco Santander México |

| Santander Consumo | Fitch Ratings | ||

| National Scale | |||

| Long term | AAA (mex) | ||

| Short Term | F1+ (mex) | ||

| Outlook | Stable | ||

| Santander Vivienda | HR | ||

| National Scale | |||

| Long term | HR AAA | ||

| Short Term | HR +1 | ||

| Outlook | Stable | ||

Notes:

| § | BCA = Baseline Credit Assessment |

| § | SR = Support Rating |

| § | VR = Viability Rating |

| § | SCP = Standalone Credit Profile |

| § | CR= Counterparty Risk Assessments |

N/A = Not applicable

| Earnings Release | 3Q.2019 |

30 |

| Banco Santander México |

3Q19 EARNINGS CALL DIAL-IN INFORMATION

| Date: | Friday, November, 1st, 2019 |

| Time: | 08:00 a.m. (MCT); 10:00 a.m. (US ET) |

| Dial-in Numbers: | 1-877-407-4018 US & Canada 1-201-689-8471 International & Mexico |

| Access Code: | Please ask for Santander México Earnings Call |

| Webcast: | http://public.viavid.com/index.php?id=136399 |

| Replay: | Starting: Friday, November 1st, 2019 at 1:00 p.m. (US ET) |

| Ending: Friday, November 8th, 2019 at 11:59 p.m. (US ET) | |

| ET Dial-in number: 1-844-512-2921 US & Canada; 1-412-317-6671 International & Mexico Access Code: 13695244 |

ANALYST COVERAGE

Bank of America Merrill Lynch, Barclays, BBVA, Bradesco, Brasil Plural, Banco BTG Pactual, Bx+, Citi, Credit Suisse, GBM, HSBC, Invex, Itaú, JP Morgan, Morgan Stanley, Nau Securities, Signum Research, Scotiabank, UBS and Intercam.

Santander México is covered by the above investment banks and research firms. Please note that any opinions, estimates or forecasts regarding the performance of Santander México issued by the research analysts of these firms reflect their own views, and therefore do not represent the opinions, estimates or forecasts of Santander México or its management. Although Santander México may refer to or distribute such statements, this does not imply that Santander México agrees with or endorses any information, conclusions or recommendations included therein.

DEFINITION OF RATIOS

ROAE:Annualized net income divided by average equity

Efficiency:Annualized administrative and promotional expenses divided by annualized gross operating income (before administrative and promotional expenses and allowances).

Recurrency:Annualized net fees divided by annualized administrative and promotional expenses (net of amortizations and depreciations).

NIM:Financial margin divided by daily average interest earnings assets.

Cost of risk:Annualized provisions for loan losses divided by average loan portfolio

| Note: |

Annualized figures consider

| · | Quarterly ratio = 3Q19x4 |

| · | Average figures are calculated using 3Q18 and 3Q19 |

| Earnings Release | 3Q.2019 |

31 |

| Banco Santander México |

ABOUT BANCO SANTANDER MÉXICO (NYSE: BSMX; BMV: BSMX)

Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México (Banco Santander México), one of Mexico’s leading banking institutions, provides a wide range of financial and related services, including retail and commercial banking, financial advisory and other related investment activities. Banco Santander México offers a multichannel financial services platform focused on mid- to high-income individuals and small- to medium-sized enterprises, while also providing integrated financial services to larger multinational companies in Mexico. As of September 30, 2019, Banco Santander México had total assets of Ps.1,461 billion under Mexican Banking GAAP and more than 17.7 million customers. Headquartered in Mexico City, the Company operates 1,411 branches and offices nationwide and has a total of 19,876 employees.

We, the undersigned under oath to tell the truth declare that, in the area of our corresponding functions, we prepared the information of Banco Santander México contained in this quarterly report, which to the best of our knowledge reasonably reflects its situation.

| HÉCTOR B. GRISI CHECA | DIDIER MENA CAMPOS | |

| Executive President and Chief Executive Officer | Chief Financial Officer | |

| EMILIO DE EUSEBIO SAIZ | JUAN CARLOS GARCÍA CONTRERAS | JUAN RAMÓN JIMÉNEZ LORENZO |

| Deputy General Director Financial Accounting and Control | Executive Director of Intervention | Chief Audit Executive |

The financial information presented in this report has been obtained from the non-audited financial statements prepared in accordance with accounting principles and regulations prescribed by the CNBV applicable to Credit Institution which are subject to the supervision of the CNBV on accounting procedures, published in the Federal Official Gazette on January 31st, 2011. The exchange rate used to convert foreign currency transactions US$ to Mexican pesos is Ps.19.7345.

INVESTOR RELATIONS CONTACT

Héctor Chávez Lopez – Managing Director - IRO

+ 52 (55) 5269-1925

hchavez@santander.com.mx

Investor Relations Team

investor@santander.com.mx

www.santander.com.mx

| Earnings Release | 3Q.2019 |

32 |

| Banco Santander México |

LEGAL DISCLAIMER