UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

☐REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2018

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-35658

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE,

GRUPO FINANCIERO SANTANDER MÉXICO

(Exact name of Registrant as specified in its charter)

United Mexican States

(Jurisdiction of incorporation or organization)

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Delegación Álvaro Obregón

01219 Mexico City

(Address of principal executive offices)

Fernando Borja Mujica

Deputy General Legal and Compliance Director

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE,

GRUPO FINANCIERO SANTANDER MÉXICO

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Delegación Álvaro Obregón

01219 Mexico City

Telephone: +(52) 55-5257-8000

Fax: +52 55-5269-2701

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| |

Title of each class | Name of each exchange on which registered |

American Depositary Shares, each representing five shares of the Series B common stock of Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México., par value of Ps.3.780782962 | New York Stock Exchange |

Series B shares, par value of Ps.3.780782962 | New York Stock Exchange* |

*Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México’s Series B shares are not listed for trading, but are only listed in connection with the registration of the American Depositary Shares, pursuant to the requirements of the New York Stock Exchange.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

U.S.$500,000,000 8.500% Perpetual Subordinated Non-Preferred Contingent Convertible Additional Tier 1 Capital Notes

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of the period covered by the annual report.

Series B shares: 3,322,685,212

Series F shares: 3,464,309,145

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer," accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| | |

Large accelerated filer ☒ | Accelerated filer ☐ | Non-accelerated filer ☐ |

| | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | |

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

TABLE OF CONTENTS

}

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Definitions

Unless otherwise indicated or the context otherwise requires, all references in this annual report on Form 20-F (hereinafter the “Report”) to “Banco Santander México,” the “Bank,” “we,” “our,” “ours,” “us” or similar terms, refer to Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México, together with its consolidated subsidiaries.

When we refer to “Banco Santander Parent” or the “Parent,” we refer to our controlling shareholder, Banco Santander, S.A., a Spanish bank.

When we refer to “Former Holding Company,” we refer to Grupo Financiero Santander México, S.A.B. de C.V., our former parent company.

When we refer to “Grupo Financiero Santander México” we refer to Grupo Financiero Santander México, S.A. de C.V. our new parent company as of January 1, 2018, which is not a public company and is a wholly-owned subsidiary of Banco Santander Parent.

When we refer to Casa de Bolsa Santander, S.A. de C.V., Grupo Financiero Santander México, a Mexican broker-dealer, we refer to the Former Holding Company’s brokerage subsidiary, which is now owned by Grupo Financiero Santander México.

When we refer to “Gestión Santander,” we refer to SAM Asset Management, S.A. de C.V., Sociedad Operadora de Sociedades de Inversión (formerly known as Gestión Santander, S.A. de C.V., Grupo Financiero Santander México) (entity sold in December 2013).

When we refer to “Seguros Santander”, we refer to Zurich Santander Seguros México, S.A. (formerly known as Seguros Santander, S.A., Grupo Financiero Santander) (entity sold in November 2011).

When we refer to the “Santander Group,” we refer to the worldwide Banco Santander Parent conglomerate and its consolidated subsidiaries.

References in this Report to certain financial terms have the following meanings:

| · | | References to “IFRS” are to the International Financial Reporting Standards as issued by the International Accounting Standards Board (“IASB”) and interpretations issued by the IFRS Interpretations Committee. |

| · | | References to “Mexican Banking GAAP” are to the accounting standards and regulations prescribed by the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores, or “CNBV”) for credit institutions, as amended. |

| · | | References to our “audited financial statements” are to the audited consolidated financial statements of Banco Santander México as of December 31, 2017 and 2018, and for each of the fiscal years ended December 31, 2016, 2017 and 2018, together with the notes thereto. The audited financial statements were prepared in accordance with IFRS and are contained in this Report. |

| · | | References herein to “UDIs” are to Unidades de Inversión, a peso-equivalent unit of account indexed for Mexican inflation. UDIs are units of account created by the Mexican Central Bank on April 4, 1995, the value of which in pesos is indexed to inflation on a daily basis, as measured by the change in the National Consumer Price Index (Índice Nacional de Precios al Consumidor). Under a UDI-based loan or financial instrument, the borrower’s nominal peso principal balance is converted either at origination or upon restructuring to a UDI principal balance and interest on the loan or financial instrument is calculated on the outstanding UDI balance of the loan or financial instrument. Principal and interest payments are made by the borrower in an amount of pesos equivalent to the amount due in UDIs at |

the stated value of UDIs on the day of payment. As of December 31, 2018, one UDI was equal to Ps.6.22663 (U.S.$0.3169). |

As used in this Report, the following terms relating to our capital adequacy have the meanings set forth below, unless otherwise indicated. See “Item 4. Information on the Company—B. Business Overview—Supervision and Regulation.”

| · | | “Capital Ratio” refers to the ratio of the total net capital (capital neto) to risk-weighted assets calculated in accordance with the methodology established or adopted from time to time by the CNBV pursuant to the Mexican Capitalization Requirements. |

| · | | “General Rules Applicable to Mexican Banks” means the General Provisions Applicable to Credit Institutions (Disposiciones de Carácter General Aplicables a las Instituciones de Crédito) issued by the CNBV. |

| · | | “Mexican Capitalization Requirements” refers to the capitalization requirements for commercial banks, including Banco Santander México, set forth in the Mexican Banking Law (Ley de Instituciones de Crédito) and in the General Rules Applicable to Mexican Banks, as such laws and regulations may be amended from time to time or superseded. |

| · | | “Tier 1 capital (capital básico)” means the basic capital (capital básico) of the Total Net Capital (capital neto), as such term is determined based on the Mexican Capitalization Requirements, as such determination may be amended from time to time, which is comprised of Fundamental Capital (capital fundamental) and Additional Tier 1 Capital (capital básico no fundamental). |

| · | | “Tier 2 capital (capital complementario)” means the additional capital (capital complementario) of the Total Net Capital (capital neto), as such term is determined based on the Mexican Capitalization Requirements, as such determination may be amended from time to time. |

As used in this Report, the term “billion” means one thousand million (1,000,000,000).

In this Report, the term “Mexico” refers to the United Mexican States, and the terms “Mexican government” or the “government” refer to the federal government of Mexico. References to “U.S.$,” “U.S. dollars” and “dollars” are to United States dollars, and references to “Mexican pesos,” “pesos,” or “Ps.” are to Mexican pesos. References to “euros” or “€” are to the common legal currency of the member states participating in the European Economic and Monetary Union.

Financial and Other Information

Market position. We make statements in this Report about our competitive position and market share in the Mexican financial services industry and the size of the Mexican financial services industry. We have made these statements on the basis of statistics and other information from third-party sources, primarily the CNBV, that we believe are reliable.

Currency and accounting standards. We maintain our financial books and records in pesos. Our consolidated income statement data for each of the years ended December 31, 2014, 2015, 2016, 2017 and 2018 and our consolidated balance sheet data as of December 31, 2014, 2015, 2016, 2017 and 2018, included in this Report, have been audited under the standards of the Public Company Accounting Oversight Board (“PCAOB”), and are prepared in accordance with IFRS. For regulatory purposes, including Mexican Central Bank regulations and the reporting requirements of the CNBV, we concurrently prepare and will continue to prepare and make available to our shareholders, statutory financial statements in accordance with Mexican Banking GAAP, which prescribes generally accepted accounting criteria for all financial institutions in Mexico.

IFRS differs in certain significant respects from Mexican Banking GAAP. We adopted IFRS in 2014. While we have prepared our consolidated financial data as of and for the years ended December 31, 2014, 2015,

2016, 2017 and 2018 in accordance with IFRS, data reported by the CNBV for the Mexican financial sector as a whole as well as individual financial institutions in Mexico, including our own, is prepared in accordance with Mexican Banking GAAP and, thus, may not be comparable to our results prepared in accordance with IFRS. All statements in this Report regarding our relative market position and financial performance vis-à-vis the financial services sector in Mexico, including financial information as to net income, return-on-average equity and non-performing loans, among others, are based, out of necessity, on information obtained from CNBV reports, and accordingly are presented in accordance with Mexican Banking GAAP. Unless otherwise indicated, all financial information provided in this Report has been prepared in accordance with IFRS.

Effect of rounding. Certain amounts and percentages included in this Report and in our audited financial statements have been rounded for ease of presentation. Percentage figures included in this Report have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, certain percentage amounts in this Report may vary from those obtained by performing the same calculations using the figures in our audited financial statements. Certain other amounts that appear in this Report may not sum due to rounding.

Exchange rates and translation into U.S. dollars. This Report contains translations of certain peso amounts into U.S. dollars at specified rates solely for your convenience. These translations should not be interpreted as representations by us that the peso amounts actually represent such U.S. dollar amounts or could, at this time, be converted into U.S. dollars at the rate indicated. Unless otherwise indicated, we have translated peso amounts into U.S. dollars at an exchange rate of Ps.19.65 per U.S.$1.00, the rate calculated on December 31, 2018 (the last business day in December) and published on January 2, 2019 in the Federal Official Gazette by the Mexican Central Bank, as the exchange rate for the payment of obligations denominated in currencies other than pesos and payable within Mexico (tipo de cambio para solventar obligaciones denominadas en moneda extranjera). The translation of income statement transactions expressed in pesos using such rates may result in presentation of dollar amounts that differ from the U.S. dollar amounts that would have been obtained by translating Mexican pesos into U.S. dollars at the exchange rate prevailing when such transactions were recorded. See “Item 3. Key Information—A. Selected Financial Data—Exchange Rates” for information regarding exchange rates between the peso and the U.S. dollar for the periods specified therein.

New impairment model. IFRS 9, Financial instruments establishes new recognition and measurement requirements for financial instruments and became mandatory for financial statement periods commencing January 1, 2018. As of January 1, 2018, the Bank now classifies its financial assets in the following measurement categories: (i) those to be measured subsequently at fair value (either through other comprehensive income or through profit or loss) and (ii) those to be measured at amortized cost. The Bank determines the applicable category of a financial asset based on the business model for managing that financial asset. We applied IFRS 9 in a retrospective manner, by adjusting the opening balance of affected financial instruments at January 1, 2018, without restating prior period amounts. Regarding the recognition of credit risk impairment, the most important change is that the new accounting standard introduces the concept of expected loss, whereas the previous model was based on incurred loss. As of January 1, 2018, the allowance for impairment losses and provisions for off-balance sheet risk increased from Ps.17,961 million to Ps.21,217 million as result of the application of IFRS 9. The Bank has applied these requirements in a retrospective manner, by adjusting the opening balance at January 1, 2018, without restating the comparative financial statements, and as a result, there was no income statement impact. The primary reasons for this increase are the requirements to recognize (i) an allowance for impairment losses for the expected life of the transaction for financial instruments where a significant risk increase has been identified after initial recognition and (ii) use of forward-looking information as the application of this impairment methodology looks to whether there has been a significant increase in credit risk in the allowance for impairment losses and in the provisions for off-balance sheet risk. See Note 2.h to our audited financial statements included elsewhere in this Report for more details on the new recognition and measurement requirements for financial instruments. Because the Bank did not restate prior period amounts upon adoption of IFRS 9, prior period financial information may not be comparable.

GLOSSARY OF SELECTED TERMS

The following is a glossary of selected terms used in this Report.

| |

Afore | An entity established pursuant to Mexican law that manages independent retirement accounts. The main functions of an Afore include, among others, (i) managing pension funds, (ii) creating and managing individual pension accounts for each worker, (iii) creating, managing and operating specialized pension funds known as Siefores, (iv) distributing and purchasing Siefores’ stock, (v) contracting pension insurance, and (vi) distributing, in certain cases, the individual funds directly to the pensioned worker |

| |

ALCO | Our Assets and Liabilities Committee (Comité de Activos y Pasivos), which is responsible for determining guidelines for managing risk with respect to financial margin, net worth and long-term liquidity |

| |

Basel III | An international framework of capital and liquidity standards for internationally active banking organizations that includes, among other things, the definition of capital, capital requirements, the treatment of counterparty credit risk, the leverage ratio and the global liquidity standard. The Basel III framework was designed by the Basel Committee in 2010 |

| |

Basel Committee | Basel Committee on Banking Supervision, which includes the supervisory authorities of twelve major industrial countries |

| |

BIVA | Bolsa Institucional de Valores, S.A. de C.V. |

| |

Bonding Companies Law | Ley Federal de Instituciones de Fianzas |

| |

BSC | Banking Stability Committee (Comité de Estabilidad Bancaria) |

| |

Cetes | Mexican Treasury Bills (Certificados de la Tesorería de la Federación) |

| |

CDI | Certificate of interbank deposit |

| |

CNBV | Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) |

| |

CNSF | Mexican National Insurance and Bonding Commission (Comisión Nacional de Seguros y Fianzas) |

| |

COFECE | Mexican Federal Antitrust Commission (Comisión Federal de Competencia Económica) |

| |

CONSAR | Mexican National Commission for the Mexican Pension Saving System (Comisión Nacional del Sistema de Ahorro para el Retiro) |

| |

CONDUSEF | Mexican National Commission for the Protection and Defense of Financial Service Users (Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros) |

| |

CRM | Customer relationship management |

| |

Exchange Act | Securities Exchange Act of 1934, as amended |

| |

IASB | International Accounting Standards Board |

| |

IFRS | International Financial Reporting Standards, accounting standards issued by the International Accounting Standards Board and interpretations issued by the International Financial Reporting Standards Interpretations Committee |

| |

IMPI | Mexican Institute of Industrial Property (Instituto Mexicano de la Propiedad Industrial) |

| |

Infonavit | Mexican Institute of the National Housing Fund for Workers (Instituto Nacional para el Fomento de la Vivienda de los Trabajadores) |

| |

Insurance Companies Law | Ley General de Instituciones y Sociedades Mutualistas de Seguros |

| |

Investment Services Rules | Disposiciones de Carácter General Aplicables a las Entidades Financieras y otras Personas que Proporcionan Servicios de Inversión |

| |

IPAB | Mexican Institute for the Protection of Bank Savings (Instituto para la Protección al Ahorro Bancario) |

| |

IPC | Mexican Stock Exchange Prices and Quotations Index (Índice de Precios y Cotizaciones) |

| |

Law of the Mexican Central Bank | Ley del Banco de México |

| |

LCR | Liquidity coverage ratio |

| |

LGD | Loss given default |

| |

LIC | Mexican Banking Law (Ley de Instituciones de Crédito) |

| |

LMV | Mexican Securities Market Law (Ley del Mercado de Valores) |

| |

Mexican Banking GAAP | The financial accounting standards and regulations prescribed by the CNBV for financial institutions, as amended |

| |

Mexican Central Bank | Banco de México |

| |

Mexican Corporations Law | Ley General de Sociedades Mercantiles |

| |

Mexican Financial Groups Law | Ley para Regular las Agrupaciones Financieras |

| |

Mexican Stock Exchange | Bolsa Mexicana de Valores, S.A.B. de C.V. |

| |

MIEA | Internal Methodology with Advanced Approach (Metodología Interna con Enfoque Avanzado) |

| |

MIEB | Internal Methodology with Basic Approach (Metodología Interna con Enfoque Básico) |

| |

MORENA | Mexican Political Party “Movimiento de Regeneración Nacional” |

| |

MVE | Market value of equity |

| |

NAFIN | Nacional Financiera, Sociedad Nacional de Crédito, Institución de Banca de Desarrollo, a Mexican government bank that provides support for SMEs |

| |

NAFTA | North American Free Trade Agreement |

| |

National Consumer Price Index | Índice Nacional de Precios al Consumidor |

| |

NIM | Net interest margin |

| |

NIM Sensitivity | Net interest margin sensitivity is the difference between the return on assets and the financial cost of our financial liabilities based on a one-year time frame and a parallel movement of 100 basis points (1%) in market interest rates |

| |

NYSE | New York Stock Exchange |

| |

NSFR | Net Stable Funding Ratio |

| |

Federal Official Gazette | Diario Oficial de la Federación |

| |

PCAOB | Public Company Accounting Oversight Board (United States) |

| |

Public Registry of Commerce | Registro Público de Comercio |

| |

RNV | Mexican National Securities Registry (Registro Nacional de Valores) |

| |

RWA | Risk-weighted assets |

| |

SEC | U.S. Securities and Exchange Commission |

| |

SHCP | Mexican Ministry of Finance and Public Credit (Secretaría de Hacienda y Crédito Público) |

| |

Siefores | Specialized pension funds (Sociedades de Inversión Especializadas de Fondos para el Retiro) established pursuant to Mexican law |

| |

SME | Small and medium-sized enterprises, consisting of small companies with annual revenue of less than Ps.250,000,000 (U.S.$12,721,869). |

| |

Sofoles | Sociedades Financieras de Objeto Limitado, non-banking institutions in Mexico that focus primarily on offering credit or financing for specific purposes (housing, automobiles, personal loans, etc.) to middle- and low-income individuals. All existing Sofol authorizations automatically terminated on July 19, 2013. Existing Sofoles had the option of converting to Sofomes or otherwise extending their corporate purpose to include activities carried out by Sofomes |

| |

Sofomes | Sociedades Financieras de Objeto Múltiple, non-banking institutions in Mexico that engage in lending and/or financial leasing and/or factoring services and may be regulated or non-regulated |

| |

TIIE | Mexican benchmark interbank money market rate (Tasa de Interés Interbancaria de Equilibrio) |

| |

UDI | Unidades de inversión, a peso-equivalent unit of account indexed for Mexican inflation |

| |

VaR | Value at risk, an estimate of the expected maximum loss in the market value of a given portfolio over a one-day time horizon at a 99% confidence interval |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report includes forward-looking statements, principally under the captions “Item 3. Key Information—D. Risk Factors,” “Item 4. Information on the Company—B. Business Overview” and “Item 5. Operating and Financial Review and Prospects.” These statements appear throughout this Report and include statements regarding our intent, belief or current expectations in connection with :

asset growth and sources of funding;

growth of our fee-based business;

expansion of our distribution network;

financing plans;

competition;

impact of regulation and the interpretation thereof;

action to modify or revoke our banking license;

exposure to market risks including interest rate risk, foreign exchange risk and equity price risk;

exposure to credit risks including credit default risk and settlement risk;

projected capital expenditures;

capitalization requirements and level of reserves;

investment in its information technology platform;

liquidity;

trends affecting the economy generally; and

trends affecting our financial condition and our results of operations.

Many important factors, in addition to those discussed elsewhere in this Report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among other things:

changes in capital markets in general that may affect policies or attitudes towards lending to Mexico or Mexican companies;

changes in economic conditions, in Mexico, in particular, in the United States, or globally;

the monetary, foreign exchange and interest rate policies of the Mexican Central Bank;

inflation;

deflation;

unemployment;

unanticipated turbulence in interest rates;

the entry into force of the USMCA or the deterioration of the terms of trade between Mexico and the United States;

the implementation of new economic policy by the new administration in Mexico;

movements in foreign exchange rates;

movements in equity prices or other rates or prices;

changes in Mexican and foreign policies, legislation and regulations;

changes in requirements to make contributions to, for the receipt of support from programs organized by or requiring deposits to be made or assessments observed or imposed by, the Mexican government;

changes in taxes and tax laws;

competition, changes in competition and pricing environments;

our inability to hedge certain risks economically;

economic conditions that affect consumer spending and the ability of customers to comply with obligations;

the adequacy of allowance for impairment losses and other losses;

increased default by borrowers;

our inability to successfully and effectively integrate acquisitions or to evaluate risks arising from asset acquisitions;

technological changes;

changes in consumer spending and saving habits;

increased costs;

unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms;

changes in, or failure to comply with, banking regulations or their interpretation; and

the other risk factors discussed under “Item 3. Key Information—D. Risk Factors” in this Report.

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “forecast” and similar words are intended to identify forward-looking statements. You should not place undue reliance on such statements, which speak only as of the date they were made. We undertake no obligation to update publicly or to revise any forward-looking statements after we distribute this Report because of new information, future events or other factors. Our independent public accountants have neither examined nor

compiled the forward-looking statements and, accordingly, do not provide any assurance with respect to such statements. In light of the risks and uncertainties described above, the future events and circumstances discussed in this Report might not occur and are not guarantees of future performance. Because of these uncertainties, you should not make any investment decision based upon these estimates and forward-looking statements.

ENFORCEMENT OF JUDGMENTS

We are a corporation (sociedad anónima) incorporated in accordance with the laws of Mexico. All of our directors and officers and experts named herein are non-residents of the United States, and all or substantially all of the assets of such persons and substantially all of our assets are located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States upon such persons or to enforce against them or us in United States courts judgments predicated upon the civil liability provisions of United States federal securities laws. We have been advised by our special counsel as to Mexican law, that there is doubt as to the enforceability, in original actions in Mexican courts, of liabilities predicated solely on U.S. federal securities laws and as to the enforceability in Mexican courts of judgments of United States courts obtained in actions predicated upon the civil liability provisions of U.S. federal securities laws. We have been advised by such special Mexican counsel, Ritch, Mueller, Heather y Nicolau, S.C., that no bilateral treaty is currently in effect between the United States and Mexico that covers the reciprocal enforcement of civil foreign judgments. In the past, Mexican courts have enforced judgments rendered in the United States by virtue of the legal principles of reciprocity and comity, consisting of the review in Mexico of the United States judgment, in order to ascertain, among other matters, whether Mexican legal principles of due process, public policy (orden público) and non-violation of Mexican law have been complied with, without reviewing the merits of the subject matter of the case.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

A. Directors and Senior Management

Not applicable.

B. Advisers

Not applicable.

C. Auditors

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

A. Offer Statistics

Not applicable.

B. Method and Expected Timetable

Not applicable.

ITEM 3. KEY INFORMATION

A.Selected Financial Data

The following tables present our selected consolidated financial data for each of the periods indicated. You should read this information in conjunction with our audited financial statements and related notes and the information under “Item 5. Operating and Financial Review and Prospects” included elsewhere in this Report.

We have derived our selected consolidated income statement data for the years ended December 31, 2014, 2015, 2016, 2017 and 2018 and our selected consolidated balance sheet data as of December 31, 2014, 2015, 2016, 2017 and 2018 from our audited financial statements, which have been prepared in accordance with IFRS. We have included in Item 18 hereto our audited financial statements as of December 31, 2017 and 2018 and for each of the three years in the three-year period ended December 31, 2018.

CONSOLIDATED INCOME STATEMENT DATA IN ACCORDANCE WITH IFRS

| | | | | | | | | | | | | | | | | | | | | | | | |

| For the year ended December 31, |

| | 2014 | | | 2015 | | | 2016 | | | 2017 | | | 2018 | | | 2018 | |

| | | | | | | | | | | | | | | | | | | | | | (Millions of U.S. | |

| | (Millions of pesos)(1) | | | dollars) (1)(2) | |

Interest income | | Ps. | 57,956 | | | Ps. | 64,230 | | | Ps. | 77,453 | | | Ps. | 98,002 | | | Ps. | 99,537 | | | U.S. | 5,065 | |

Interest income from financial assets at fair value through profit or loss | | | — | | | | — | | | | — | | | | — | | | | 14,049 | | | | 715 | |

Interest expenses and similar charges | | | (20,386) | | | | (21,242) | | | | (28,323) | | | | (42,158) | | | | (51,589) | | | | (2,625) | |

Net interest income | | | 37,570 | | | | 42,988 | | | | 49,130 | | | | 55,844 | | | | 61,997 | | | | 3,155 | |

Dividend income | | | 137 | | | | 104 | | | | 94 | | | | 150 | | | | 210 | | | | 11 | |

Fee and commission income (net) | | | 12,858 | | | | 13,632 | | | | 13,940 | | | | 14,813 | | | | 15,722 | | | | 800 | |

Gains/(losses) on financial assets and liabilities (net) | | | 2,610 | | | | 2,504 | | | | 3,760 | | | | 3,458 | | | | 1,484 | | | | 76 | |

Exchange differences (net) | | | (11) | | | | 6 | | | | 2 | | | | 6 | | | | — | | | | — | |

Other operating income | | | 509 | | | | 472 | | | | 486 | | | | 669 | | | | 748 | | | | 38 | |

Other operating expenses | | | (2,472) | | | | (3,010) | | | | (3,361) | | | | (3,614) | | | | (4,393) | | | | (223) | |

Total income | | | 51,201 | | | | 56,696 | | | | 64,051 | | | | 71,326 | | | | 75,768 | | | | 3,857 | |

Administrative expenses | | | (19,290) | | | | (20,780) | | | | (22,655) | | | | (25,437) | | | | (28,649) | | | | (1,457) | |

Personnel expenses | | | (9,557) | | | | (10,625) | | | | (11,472) | | | | (12,748) | | | | (14,354) | | | | (730) | |

Other general administrative expenses | | | (9,733) | | | | (10,155) | | | | (11,183) | | | | (12,689) | | | | (14,295) | | | | (727) | |

Depreciation and amortization | | | (1,682) | | | | (1,863) | | | | (2,058) | | | | (2,533) | | | | (2,973) | | | | (151) | |

Impairment losses on financial assets (net) | | | (13,132) | | | | (16,041) | | | | (16,661) | | | | (18,820) | | | | (18,810) | | | | (956) | |

Loans and receivables(3) | | | (13,132) | | | | (16,041) | | | | (16,661) | | | | (18,820) | | | | — | | | | — | |

Financial assets at amortized cost(3) | | | — | | | | — | | | | — | | | | — | | | | (18,806) | | | | (956) | |

Financial assets at fair value through other comprehensive income | | | — | | | | — | | | | — | | | | — | | | | (4) | | | | — | |

Impairment losses on other assets (net) | | | (48) | | | | — | | | | — | | | | — | | | | (5) | | | | — | |

Other intangible assets | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Non-current assets held for sale | | | (48) | | | | — | | | | — | | | | — | | | | (5) | | | | — | |

Provisions (net)(4) | | | (137) | | | | 258 | | | | (881) | | | | (437) | | | | (562) | | | | (28) | |

Gains/(losses) on disposal of assets not classified as non-current assets held for sale | | | 2 | | | | 7 | | | | 20 | | | | 6 | | | | 7 | | | | — | |

Gains/(losses) on disposal of non-current assets held for sale not

classified as discontinued operations | | | (15) | | | | 91 | | | | 71 | | | | 69 | | | | 38 | | | | 2 | |

Operating profit before tax | | | 16,899 | | | | 18,368 | | | | 21,887 | | | | 24,174 | | | | 24,814 | | | | 1,267 | |

Income tax | | | (3,539) | | | | (4,304) | | | | (5,351) | | | | (5,496) | | | | (5,458) | | | | (278) | |

Profit from continuing operations | | | 13,360 | | | | 14,064 | | | | 16,536 | | | | 18,678 | | | | 19,356 | | | | 989 | |

Profit from discontinued operations (net) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Consolidated profit for the year | | Ps. | 13,360 | | | Ps. | 14,064 | | | Ps. | 16,536 | | | Ps. | 18,678 | | | Ps. | 19,356 | | | U.S. | 989 | |

Profit attributable to the Parent | | | 13,359 | | | | 14,051 | | | | 16,536 | | | | 18,678 | | | | 19,353 | | | | 989 | |

Profit attributable to non-controlling interests | | | 1 | | | | 13 | | | | — | | | | — | | | | 3 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Earnings per share from continuing and discontinued operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic earnings per share | | | 1.97 | | | | 2.07 | | | | 2.44 | | | | 2.76 | | | | 2.86 | | | | 0.15 | |

Diluted earnings per share(5) | | | 1.97 | | | | 2.07 | | | | 2.44 | | | | 2.75 | | | | 2.85 | | | | 0.15 | |

Earnings per share from continuing operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic earnings per share | | | 1.97 | | | | 2.08 | | | | 2.44 | | | | 2.76 | | | | 2.86 | | | | 0.15 | |

Diluted earnings per share(5) | | | 1.97 | | | | 2.07 | | | | 2.44 | | | | 2.75 | | | | 2.85 | | | | 0.15 | |

Cash dividend per share(6) | | | 0.51 | | | | 1.00 | | | | 2.58 | | | | 1.31 | | | | 1.36 | | | | 0.07 | |

Weighted average shares outstanding | | | 6,777,381,551 | | | | 6,777,381,551 | | | | 6,777,381,551 | | | | 6,777,381,551 | | | | 6,776,220,369 | | | | 6,776,220,369 | |

Dilutive effect of rights on shares(5) | | | 9,612,806 | | | | 9,612,806 | | | | 9,612,806 | | | | 9,612,806 | | | | 10,773,988 | | | | 10,773,988 | |

Adjusted number of shares | | | 6,786,994,357 | | | | 6,786,994,357 | | | | 6,786,994,357 | | | | 6,786,994,357 | | | | 6,786,994,357 | | | | 6,786,994,357 | |

Dividend paid | | | 3,473 | | | | 6,760 | | | | 17,468 | | | | 8,910 | | | | 9,228 | | | | 470 | |

Basic earnings per share | | | 1.97 | | | | 2.07 | | | | 2.44 | | | | 2.76 | | | | 2.86 | | | | 0.15 | |

Diluted earnings per share | | | 1.97 | | | | 2.07 | | | | 2.44 | | | | 2.75 | | | | 2.85 | | | | 0.15 | |

Dividend pay-out ratio | | | 26.03% | | | | 48.18% | | | | 105.64% | | | | 47.77% | | | | 47.76% | | | | 47.60% | |

| (1) | | Except share and per share amounts. |

| (2) | | Results for the year ended December 31, 2018 have been translated into U.S. dollars, for convenience purposes only, using the exchange rate of Ps.19.65 per U.S.$1.00 as calculated on December 31, 2018 and reported by the Mexican Central Bank in the Federal Official Gazette on January 2, 2019 as the exchange rate for the payment of obligations denominated in currencies other than pesos and payable within Mexico. These translations should not be construed as representations that the pesos amounts represent, have been or could have been converted into, U.S. dollars at such or at any other exchange rate. |

| (3) | | Impairment losses less recoveries of previously written-off loans (net of legal expenses). |

| (4) | | Principally includes provisions for off-balance sheet risk and provisions for tax and legal matters. See “Item 5. Operating and Financial Review and Prospects.” |

| (5) | | To calculate diluted earnings per share, the amount of profit attributable to the Parent and the weighted average number of shares issued, excluding the average number of treasury shares, are adjusted to |

consider all the dilutive effects inherent to potential shares. For additional information on earnings per share, see Note 4.2.ii to our audited financial statements included elsewhere in this Report. |

| (6) | | On December 29, 2014, we paid a dividend of Ps.3,473 million, equal to Ps.0.0430 per share. On May 29, 2015, we paid a dividend of Ps.3,534 million, equal to Ps.0.0437 per share. On December 22, 2015, we paid a dividend of Ps.3,226 million, equal to Ps.0.0399 per share. On May 26, 2016, we paid a dividend of Ps.3,844 million, equal to Ps.0.0475 per share. On December 30, 2016, we paid a dividend of Ps.13,624 million, equal to Ps.0.1685 per share. On May 30, 2017 we paid a dividend of Ps.4,234 million, equal to Ps.0.0524 per share. On December 27, 2017, we paid a dividend of Ps.4,676 million, equal to Ps.0.0578 per share. On June 29, 2018, we paid a dividend of Ps.4,279 million, equal to Ps.0.6304 per share.On December 28, 2018, we paid a dividend of Ps.4,949 million, equal to Ps.0.7292 per share. |

CONSOLIDATED BALANCE SHEET DATA IN ACCORDANCE WITH IFRS

| | | | | | | | | | | | | | | | | | | | | | | | |

| As of December 31, |

| | 2014 | | | 2015 | | | 2016 | | | 2017 | | | 2018(1) | | | 2018(1) | |

| | | | | | | | | | | | | | | | | | | | | | (Millions of U.S. | |

| | (Millions of pesos) | | | dollars)(2) | |

Assets | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and balances with Mexican Central Bank | | Ps. | 51,823 | | | Ps. | 59,788 | | | Ps. | 78,663 | | | Ps. | 57,687 | | | Ps. | 55,310 | | | U.S. | 2,815 | |

Financial assets at fair value through profit or loss | | | — | | | | — | | | | — | | | | — | | | | 267,524 | | | | 13,614 | |

Financial assets held for trading | | | 207,651 | | | | 326,872 | | | | 342,582 | | | | 315,570 | | | | — | | | | — | |

Other financial assets at fair value through profit or loss | | | 32,501 | | | | 28,437 | | | | 42,340 | | | | 51,705 | | | | 107,425 | | | | 5,467 | |

Financial assets at fair value through other comprehensive income | | | — | | | | — | | | | — | | | | — | | | | 155,789 | | | | 7,928 | |

Available-for-sale financial assets | | | 83,340 | | | | 113,873 | | | | 154,644 | | | | 165,742 | | | | — | | | | — | |

Financial assets at amortized cost | | | — | | | | — | | | | — | | | | — | | | | 766,225 | | | | 38,991 | |

Loans and receivables | | | 530,225 | | | | 598,712 | | | | 675,498 | | | | 679,300 | | | | — | | | | — | |

Hedging derivatives | | | 4,740 | | | | 12,121 | | | | 15,003 | | | | 15,116 | | | | 9,285 | | | | 472 | |

Non-current assets held for sale | | | 844 | | | | 1,101 | | | | 1,107 | | | | 1,295 | | | | 1,277 | | | | 65 | |

Tangible assets | | | 5,259 | | | | 5,547 | | | | 5,692 | | | | 6,498 | | | | 8,714 | | | | 443 | |

Intangible assets | | | 4,079 | | | | 4,877 | | | | 5,772 | | | | 6,960 | | | | 8,044 | | | | 409 | |

Tax assets | | | 22,923 | | | | 18,659 | | | | 23,301 | | | | 20,209 | | | | 21,968 | | | | 1,118 | |

Other assets | | | 6,209 | | | | 5,847 | | | | 6,335 | | | | 9,109 | | | | 7,163 | | | | 366 | |

Total assets | | Ps. | 949,594 | | | Ps. | 1,175,834 | | | Ps. | 1,350,937 | | | Ps. | 1,329,191 | | | Ps. | 1,408,724 | | | U.S. | 71,688 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Liabilities | | | | | | | | | | | | | | | | | | | | | | | | |

Financial liabilities at fair value through profit or loss | | Ps. | — | | | Ps. | — | | | Ps. | — | | | Ps. | — | | | Ps. | 255,481 | | | U.S. | 13,001 | |

Financial liabilities held for trading | | | 136,805 | | | | 172,573 | | | | 266,828 | | | | 239,725 | | | | — | | | | — | |

Other financial liabilities at fair value through profit or loss | | | 110,520 | | | | 208,341 | | | | 136,860 | | | | 120,653 | | | | 105,430 | | | | 5,365 | |

Financial liabilities at amortized cost | | | 579,056 | | | | 659,209 | | | | 806,091 | | | | 820,431 | | | | 890,284 | | | | 45,304 | |

Hedging derivatives | | | 4,403 | | | | 9,568 | | | | 14,287 | | | | 11,091 | | | | 8,393 | | | | 427 | |

Provisions (3) | | | 5,988 | | | | 6,580 | | | | 7,202 | | | | 6,730 | | | | 6,800 | | | | 345 | |

Tax liabilities | | | 26 | | | | 643 | | | | 44 | | | | 71 | | | | 194 | | | | 9 | |

Other liabilities | | | 12,300 | | | | 11,162 | | | | 14,398 | | | | 15,080 | | | | 18,855 | | | | 958 | |

Total liabilities | | Ps. | 849,098 | | | Ps. | 1,068,076 | | | Ps. | 1,245,710 | | | Ps. | 1,213,781 | | | Ps. | 1,285,437 | | | U.S. | 65,409 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Shareholders’ equity | | Ps. | 100,704 | | | | 107,328 | | | Ps. | 106,768 | | | Ps. | 116,558 | | | Ps. | 124,240 | | | U.S. | 6,327 | |

Share capital | | | 8,086 | | | Ps. | 8,086 | | | | 8,086 | | | | 8,086 | | | | 25,660 | | | | 1,306 | |

Share premium | | | 16,956 | | | | 16,956 | | | | 16,956 | | | | 16,956 | | | | — | | | | — | |

Accumulated reserves | | | 62,303 | | | | 68,235 | | | | 65,190 | | | | 72,838 | | | | 79,227 | | | | 4,032 | |

Profit for the year attributable to the Parent | | | 13,359 | | | | 14,051 | | | | 16,536 | | | | 18,678 | | | | 19,353 | | | | 989 | |

Valuation adjustments | | | (253) | | | | 372 | | | | (1,596) | | | | (1,177) | | | | (985) | | | | (50) | |

Non-controlling interests | | | 45 | | | | 58 | | | | 55 | | | | 29 | | | | 32 | | | | 2 | |

Total equity | | | 100,496 | | | | 107,758 | | | | 105,227 | | | | 115,410 | | | | 123,287 | | | | 6,279 | |

Total liabilities and equity | | Ps. | 949,594 | | | Ps. | 1,175,834 | | | Ps. | 1,350,937 | | | Ps. | 1,329,191 | | | Ps. | 1,408,724 | | | U.S. | 71,688 | |

| (1) | | Amounts prepared in accordance with IFRS 9. Prior periods have not been restated. See Note 2.h to our audited financial statements included elsewhere in this Report for more details on our change in accounting estimates in connection with the initial adoption of IFRS 9. |

| (2) | | The balance as of December 31, 2018 has been translated into U.S. dollars, for convenience purposes only, using the exchange rate of Ps.19.65 per U.S.$1.00 as calculated on December 31, 2018 and reported by the Mexican Central Bank in the Federal Official Gazette on January 2, 2019 as the exchange rate for the payment of obligations denominated in currencies other than pesos and payable within Mexico. These translations should not be interpreted as representations that the pesos amounts represent, have been or could have been converted into, U.S. dollars at such or at any other exchange rate. |

| (3) | | Includes provisions for pensions and similar obligations, provisions for off-balance sheet risk and provisions for tax and legal matters. See “Item 5. Operating and Financial Review and Prospects.” |

SELECTED RATIOS AND OTHER DATA

All of the selected ratios and other data below (except for number of shares, offices and employee data) are presented in accordance with IFRS unless otherwise noted.

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | 2014 | | | 2015 | | | 2016 | | | 2017 | | | 2018 | |

| | | | | | | | | | | | | | | |

Profitability and performance | | | | | | | | | | | | | | | |

Net interest margin(1) | | 4.80% | | | 4.88% | | | 4.97% | | | 5.34% | | | 5.55% | |

Total margin(2) | | 6.44% | | | 6.42% | | | 6.38% | | | 6.76% | | | 6.96% | |

Return on average total assets (ROAA)(3) | | 1.44% | | | 1.36% | | | 1.50% | | | 1.57% | | | 1.49% | |

Return on average equity (ROAE)(4) | | 14.17% | | | 13.71% | | | 14.89% | | | 16.93% | | | 16.27% | |

Efficiency ratio(5) | | 40.96% | | | 39.94% | | | 38.58% | | | 39.21% | | | 41.74% | |

Net fee and commission income as a percentage of operating expenses(6) | | 61.31% | | | 60.20% | | | 56.41% | | | 52.96% | | | 49.72% | |

Gross yield on average interest earning-assets | | 7.38% | | | 7.27% | | | 7.82% | | | 9.35% | | | 10.14% | |

Average cost of interest bearing liabilities | | 2.85% | | | 2.60% | | | 3.17% | | | 4.52% | | | 5.20% | |

Net interest spread | | 4.53% | | | 4.67% | | | 4.65% | | | 4.83% | | | 4.94% | |

Common stock dividend payout ratio (annual)(7) | | 26.00% | | | 48.11% | | | 105.64% | | | 47.70% | | | 47.76% | |

Average interest-earning assets(8) | | 785,345 | | | 883,735 | | | 989,857 | | | 1,047,976 | | | 1,120,323 | |

Average interest-bearing liabilities(8) | | 716,302 | | | 815,902 | | | 893,128 | | | 932,380 | | | 991,805 | |

Capital adequacy | | | | | | | | | | | | | | | |

Net tangible book value | | 96,417 | | | 102,881 | | | 99,455 | | | 108,450 | | | 115,243 | |

Net tangible book value per share | | 14.23 | | | 15.18 | | | 14.67 | | | 16.00 | | | 17.01 | |

Average equity as a percentage of average total assets | | 10.18% | | | 9.94% | | | 10.10% | | | 9.28% | | | 9.17% | |

Total capital (Mexican Banking GAAP)(9) | | 96,517 | | | 103,639 | | | 109,238 | | | 115,321 | | | 121,454 | |

Tier 1 capital (Mexican Banking GAAP)(9) | | 76,697 | | | 80,328 | | | 81,785 | | | 89,267 | | | 94,035 | |

Tier 1 capital to risk-weighted assets (Mexican Banking GAAP) | | 12.85% | | | 12.10% | | | 11.79% | | | 12.18% | | | 12.32% | |

Total capital to risk-weighted assets (Mexican Banking GAAP)(10) | | 16.17% | | | 15.61% | | | 15.74% | | | 15.73% | | | 15.91% | |

Asset quality | | | | | | | | | | | | | | | |

Non-performing loans as a percentage of total loans(11) | | 3.90% | | | 3.56% | | | 2.93% | | | 2.89% | | | 2.67% | |

Non-performing loans as a percentage of computable credit risk(11)(12) | | 3.66% | | | 3.32% | | | 2.66% | | | 2.57% | | | 2.35% | |

Written-off loans as a percentage of average total loans | | 3.10% | | | 2.85% | | | 3.48% | | | 3.63% | | | 3.00% | |

Written-off loans as a percentage of computable credit risk(12) | | 2.68% | | | 2.42% | | | 3.03% | | | 3.08% | | | 2.51% | |

Allowance for impairment losses as a percentage of average total loans(13) | | 3.49% | | | 3.70% | | | 3.10% | | | 2.83% | | | 3.28% | |

Allowance for impairment losses as a percentage of non-performing loans(11)(13) | | 82.46% | | | 94.97% | | | 101.64% | | | 93.36% | | | 116.75% | |

Allowance for impairment losses as a percentage of written-off loans(13) | | 112.49% | | | 129.98% | | | 89.21% | | | 77.89% | | | 109.34% | |

Allowance for impairment losses as a percentage of total loans(13) | | 3.22% | | | 3.38% | | | 2.98% | | | 2.70% | | | 3.12% | |

Liquidity | | | | | | | | | | | | | | | |

Liquid assets as a percentage of deposits(14) | | 47.32% | | | 46.05% | | | 38.72% | | | 35.41% | | | 36.70% | |

Total Loans, net of allowances, as a percentage of deposits(15) | | 102.15% | | | 71.98% | | | 73.08% | | | 76.61% | | | 79.32% | |

Total loans as a percentage of total funding(16) | | 60.97% | | | 64.88% | | | 64.92% | | | 67.52% | | | 70.18% | |

Deposits as a percentage of total funding(15)(16) | | 69.76% | | | 87.09% | | | 86.18% | | | 85.75% | | | 85.71% | |

Operations | | | | | | | | | | | | | | | |

Offices(17) | | 1,322 | | | 1,354 | | | 1,364 | | | 1,375 | | | 1,393 | |

Employees (full-time equivalent) | | 14,038 | | | 14,674 | | | 14,643 | | | 15,116 | | | 16,016 | |

| (1) | | Net interest margin is defined as net interest income (including dividend income) divided by average interest-earning assets, which are loans, receivables, debt instruments and other financial assets which, yield interest or similar income. |

| (2) | | Total margin is defined as net interest income (including dividend income) plus fee and commission income (net) divided by average interest-earning assets. |

| (3) | | Calculated based upon the average daily balance of total assets. |

| (4) | | Calculated based upon the average daily balance of equity. |

| (5) | | Efficiency ratio is defined as administrative expenses plus depreciation and amortization, divided by total income. |

| (6) | | Net fee and commission income divided by administrative expenses plus depreciation and amortization. |

| (7) | | Dividends paid per share divided by net income per share. |

| (8) | | Average balance sheet data has been calculated based upon the sum of the daily average for each month in the applicable period. |

| (9) | | “Total capital” and “Tier 1 capital” are calculated in accordance with the methodology established or adopted from time to time by the CNBV pursuant to the Mexican Capitalization Requirements. |

| (10) | | Tier 1 capital plus Tier 2 capital divided by total risk-weighted assets, calculated according to the Mexican Capitalization Requirements. |

| (11) | | See Note 2.g to our audited financial statements included elsewhere in this Report for more details on the classification of credit-impaired or non-performing loans. |

| (12) | | Computable credit risk is the sum of the face amounts of loans (including non-performing loans) plus guarantees and documentary credits. At December 31, 2018, total loans were Ps.689,059 million and total guarantees and documentary credits were Ps.94,267 million. When guarantees or documentary credits are contracted, we record them as off-balance sheet accounts. We present the off-balance sheet information to better demonstrate our total managed credit risk. |

| (13) | | Allowance for impairment losses were Ps.15,198 million, Ps.18,749 million, Ps.17,883 million, Ps.16,929 million and Ps.21,516 million as of December 31, 2014, 2015, 2016, 2017 and 2018, respectively. Allowance for impairment losses as of December 31, 2018 have been prepared in accordance with IFRS 9. Prior periods have not been restated. See Note 2.h to our audited financial statements included elsewhere in this Report for more details on our change in accounting estimates in connection with the initial adoption of IFRS 9. |

| (14) | | For the purpose of calculating this ratio, the amount of deposits includes the sum of demand deposits and time deposits. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Composition of Deposits.” |

Liquid assets include cash due from banks and government securities recorded at market prices. We believe we could obtain cash for our liquid assets immediately, although under systemic stress scenarios, we would likely be subject to a discount to the face value of these assets. As of December 31, 2014, 2015, 2016, 2017 and 2018, we had a total amount of liquid assets of Ps.211,751 million, Ps.342,408 million, Ps.308,177 million, Ps.281,690 million and Ps.308,857 million respectively. For the years ended December 31, 2014, 2015, 2016, 2017 and 2018, the average amounts outstanding were Ps.203,061 million, Ps.291,828 million, Ps.315,660 million, Ps.343,395 million and Ps.281,882 million respectively.

As of December 31, 2014, liquid assets were composed of the following: 24.5% cash and balances with the Mexican Central Bank (cash at our branches and automated teller machines (ATM) and the Depósito de Regulación Monetaria (Compulsory Deposits)); 31.6% debt instruments issued by the Mexican Government; and 43.9% debt instruments issued by the Mexican Central Bank.

As of December 31, 2015, liquid assets were composed of the following: 17.5% cash and balances with the Mexican Central Bank (cash at our branches and ATMs and the Depósito de Regulación Monetaria (Compulsory Deposits)); 35.2% debt instruments issued by the Mexican Government; and 47.4% debt instruments issued by the Mexican Central Bank.

As of December 31, 2016, liquid assets were composed of the following: 25.5% cash and balances with the Mexican Central Bank (cash at our branches and ATMs and the Depósito de Regulación Monetaria

(Compulsory Deposits)); 41.7% debt instruments issued by the Mexican Government; and 32.8% debt instruments issued by the Mexican Central Bank.

As of December 31, 2017, liquid assets were composed of the following: 20.5% cash and balances with the Mexican Central Bank (cash at our branches and ATMs and the Depósito de Regulación Monetaria (Compulsory Deposits)); 51.2% debt instruments issued by the Mexican Government; and 28.3% debt instruments issued by the Mexican Central Bank.

As of December 31, 2018, liquid assets were composed of the following: 17.9% cash and balances with the Mexican Central Bank (cash at our branches and ATMs and the Depósito de Regulación Monetaria (Compulsory Deposits)); 59.6% debt instruments issued by the Mexican Government; and 22.5% debt instruments issued by the Mexican Central Bank.

| (15) | | For the purpose of calculating this ratio, the amount of deposits includes the sum of demand deposits and time deposits. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Composition of Deposits.” |

| (16) | | For the purpose of calculating this ratio, the amount of total funding comprises the total of our deposits and repurchase agreements, our total marketable debt securities and the amount of our subordinated liabilities. |

For December 31, 2014, 2015, 2016, 2017, and 2018 our deposits and repurchase agreements amounted to Ps.598,721 million, Ps.743,632 million, Ps.795,852 million, Ps.795,440 million and Ps.841,618 million respectively, and our marketable debt securities amounted to Ps.59,077 million, Ps.87,449 million, Ps.90,003 million, Ps.96,296 million and Ps.103,062 million, respectively. For December 31, 2014, 2015, 2016, 2017 and 2018, our subordinated liabilities amounted to Ps.19,446 million, Ps.22,788 million, Ps.37,576 million, Ps.35,885 million and Ps.37,228 million, respectively.

| (17) | | Includes traditional branches (including those offering Santander Select service), offices and branches that serve SMEs, traditional bank tellers (ventanillas – including those offering Santander Select service), Santander Select offices (including centers (Centros Select), spaces (Espacios Select), box offices and corners) as well as Santander Select units (módulos). |

Exchange Rates

Mexico has had a free market for foreign exchange since 1994 and the Mexican government allows the peso to float against the U.S. dollar. Although the incoming Mexican government has announced that it will adhere to the flexible exchange rate regime, there can be no assurance that the Mexican government will maintain its current policies with regard to the peso or that the peso will not depreciate or appreciate significantly in the future.

External macroeconomic factors such as the normalization of U.S. monetary policy and the volatility in the global financial markets generated by the results of the 2016 U.S. presidential election negatively affected the year-end 2016 peso to U.S. dollar exchange rate, resulting in a 19.54% depreciation of the peso against the U.S. dollar, from Ps.17.25 as of December 31, 2015 to Ps.20.62 as of December 31, 2016. The peso recovered in 2017, appreciating 4.6% to Ps.19.66 as of December 31, 2017. In the second half of 2018, the peso to U.S. dollar exchange rate experienced substantial volatility as a result of external factors, including turbulence in international markets and monetary policy in the U.S., as well as domestic factors, including uncertainty about the economic policy of the incoming Mexican government, and closed at Ps.19.65 as of December 31, 2018, which implied an appreciation of 0.05%.

The following tables set forth, for the periods indicated, the low, high, average and end-of-period exchange rates expressed in pesos per U.S. dollar published by the Mexican Central Bank in the Federal Official Gazette as the exchange rate for the payment of obligations denominated in currencies other than pesos and payable within Mexico. The rates shown below are in nominal pesos and have not been restated in

constant currency units. No representation is made that the peso amounts referred to in this Report could have been or could be converted into U.S. dollars at any particular rate or at all. As of April 29, 2019, the exchange rate for U.S. dollars was Ps.19.01 per U.S. dollar.

| | | | | | | | | | | | | | | |

Year | | Low | | | High | | | Average(1) | | | Period End |

2014 | | Ps. | 12.85 | | | | 14.79 | | | | 13.30 | | | | 14.74 |

2015 | | | 14.56 | | | | 17.38 | | | | 15.88 | | | | 17.25 |

2016 | | | 17.18 | | | | 21.05 | | | | 18.69 | | | | 20.62 |

2017 | | | 17.49 | | | | 21.91 | | | | 18.91 | | | | 19.66 |

2018 | | | 17.98 | | | | 20.72 | | | | 19.24 | | | | 19.65 |

| (1) | | Average of end-of-month exchange rates for 2014, 2015, 2016, 2017 and 2018, respectively. |

| | | | | | | | | | | | | | | |

Month | | Low | | | High | | | Average(1) | | | Period End |

October 2018 | | Ps. | 18.65 | | | Ps. | 20.32 | | | Ps. | 19.19 | | | Ps. | 20.23 |

November 2018 | | | 19.82 | | | | 20.53 | | | | 20.26 | | | | 20.35 |

December 2018 | | | 19.65 | | | | 20.57 | | | | 20.11 | | | | 19.65 |

January 2019 | | | 18.93 | | | | 19.61 | | | | 19.17 | | | | 19.04 |

February 2019 | | | 19.08 | | | | 19.41 | | | | 19.20 | | | | 19.26 |

March 2019 | | | 18.87 | | | | 19.52 | | | | 19.25 | | | | 19.38 |

April 2019 (through April 29) | | | 18.77 | | | | 19.23 | | | | 18.99 | | | | 19.01 |

| (1) | | Average daily exchange rates for October, November and December 2018 and January, February, March and April (through April 29) 2019. |

Unless otherwise indicated, U.S. dollar amounts that have been translated from pesos have been so translated at an exchange rate of Ps.19.65 per U.S.$1.00, the exchange rate as calculated on December 31, 2018 and reported by the Mexican Central Bank in the Federal Official Gazette on January 2, 2019 as the exchange rate for the payment of obligations denominated in currencies other than pesos and payable within Mexico. These translations should not be interpreted as representations that the pesos amounts represent, have been or could have been converted into, U.S. dollars at such or at any other exchange rate.

The Mexican economy has suffered balance-of-payment deficits and shortages in foreign exchange reserves in the past. While the Mexican government, for more than ten years, has not restricted the ability of both Mexican and foreign individuals or entities to convert pesos into U.S. dollars, we cannot assure you that the Mexican government will not institute restrictive exchange control policies in the future. To the extent that the Mexican government institutes restrictive exchange control policies in the future, our ability to transfer or convert pesos into U.S. dollars and other currencies would be adversely affected.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Our business, financial condition and results of operations could be materially and adversely affected if any of the risks described below occur. As a result, the market price of our American Depositary Shares, or ADSs, or our Series B shares could decline, and you could lose all or part of your investment. This annual report also contains forward-looking statements that involve risks and uncertainties. See “Special Note Regarding Forward-Looking Statements.” The risks described below are those known to us or that we currently believe may materially and adversely affect us; other risks not currently known to us may arise

in the future or may reach a greater level of materiality, which may materially and adversely affect us and our business.

Risks Associated with Our Business

We are vulnerable to disruptions and volatility in the global financial markets.

Global economic conditions deteriorated significantly between 2007 and 2009, and many countries, including the United States, fell into recession. Although most countries have recovered, the recovery was uneven among different regions and is vulnerable to the materialization of existing risks. Many major financial institutions, including some of the world’s largest global commercial banks, investment banks, mortgage lenders, mortgage guarantors and insurance companies, experienced, and some continue to experience, significant difficulties. Around the world, there were runs on deposits at several financial institutions, numerous institutions sought additional capital or were assisted by governments, and many lenders and institutional investors reduced or ceased providing funding to borrowers (including to other financial institutions).

Within this context, volatile oil prices and a continuous reduction in Mexico’s oil production, together with any future downturn in manufacturing activity in the U.S., the U.S. administration’s policies on trade and immigration, and volatility in global financial markets, could have an adverse effect on the Mexican economy and its growth prospects, which could have an unfavorable impact on our business. While at the end of 2018, the governments of the three members of NAFTA reached a new trade deal, the United States-Mexico-Canada Agreement (USMCA), in order to come into force it must be ratified by each country’s Congress, a process that faces particular uncertainty in the U.S. after the results of the 2018 midterm elections. In this setting, any setback during the legislative ratification process could have a material adverse effect on the Mexican economy, which could adversely affect credit quality and dampen business volumes. The normalization of U.S. monetary policy, and divergent monetary policies around the world, including in Mexico, might also have a negative impact on the Mexican economy and adversely affect our business.

In particular, we face, among others, the following risks related to the economic downturn:

Reduced demand for our products and services.

Increased regulation of our industry. Compliance with such regulation will continue to increase our costs and may affect the pricing for our products and services, increase our conduct and regulatory risks related to non-compliance and limit our ability to pursue business opportunities.

Inability of our borrowers to timely or fully comply with their existing obligations. Macroeconomic shocks may negatively impact the household income of our retail customers and may adversely affect the recoverability of our retail loans, resulting in increased loan losses.

The process we use to estimate losses inherent in our credit exposure requires complex judgments, including forecasts of economic conditions and how these economic conditions might impair the ability of our borrowers to repay their loans. The degree of uncertainty concerning economic conditions may adversely affect the accuracy of our estimates, which may, in turn, impact the reliability of the process and the sufficiency of our loan loss allowances.

The value and liquidity of the portfolio of investment securities that we hold may be adversely affected.

Any worsening of global economic conditions may delay the recovery of the international financial industry and impact our financial condition and results of operations.

Despite recent improvements in certain segments of the global economy, and in particular the strength of domestic demand in Mexico and the manufacturing sector in the U.S. in 2018, uncertainty remains concerning the future economic environment. Such economic uncertainty could have a negative impact on our business and results of operations. A slowing of economic activity in the U.S. and Mexico, unexpected impacts from U.S. monetary policy or unexpected changes to economic policy in Mexico would likely aggravate the adverse effects of these difficult economic and market conditions on us and on others in the financial services industry.

A return to volatile conditions in the global financial markets could have a material adverse effect on us, including on our ability to access capital and liquidity on financial terms acceptable to us, if at all. If capital markets financing ceases to become available, or becomes excessively expensive, we may be forced to raise the rates we pay on deposits to attract more customers and/or become unable to maintain certain liability maturities. Any such increase in capital markets funding availability or costs or in deposit rates could have a material adverse effect on our interest margins and liquidity.

If all or some of the foregoing risks were to materialize, this could have a material adverse effect on our financing availability and terms and, more generally, on our results, financial condition and prospects.

Our financial results are constantly exposed to market risk. We are subject to fluctuations in interest rates and other market risks, which may materially and adversely affect us and our profitability.

Market risk refers to the probability of variations in our net interest income or in the market value of our assets and liabilities due to volatility of interest rates, inflation, exchange rates or equity prices. Changes in interest rates affect the following areas, among others, of our business:

net interest income;

the volume of loans originated;

credit spreads;

the market value of our securities holdings;

the value of our loans and deposits; and

the value of our derivatives transactions.

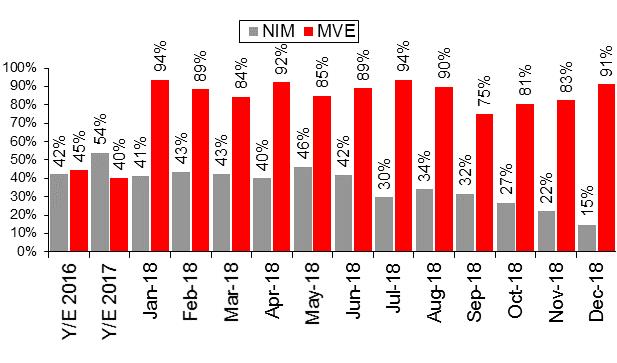

Interest rates are sensitive to many factors beyond our control, including increased regulation of the financial sector, monetary policies and domestic and international economic and political conditions. Variations in interest rates could affect the interest earned on our assets and the interest paid on our borrowings, thereby affecting our net interest income, which comprises the majority of our revenue, reducing our growth rate and potentially resulting in losses. In addition, costs we incur as we implement strategies to reduce interest rate exposure could increase in the future (which, in turn, will impact our results). We monitor our interest rate risk using the Net Interest Margin, or NIM, sensitivity, which is the difference between the return on assets and the financial cost of our financial liabilities based on a one-year period and a parallel movement of 100 basis points (1%) in market interest rates. As of December 31, 2018, the 1% NIM sensitivity was Ps.222 million.

Increases in interest rates may reduce the volume of loans we originate. Sustained high interest rates have historically discouraged customers from borrowing and have resulted in increased delinquencies in outstanding loans and deterioration in the quality of assets. Increases in interest rates may also reduce the propensity of our customers to prepay or refinance fixed-rate loans. Increases in interest rates may reduce the value of our financial assets and may reduce gains or require us to record losses on sales of our

securities or loans. We hold a substantial portfolio of debt securities and loans that have both fixed and floating interest rates.

In addition, we may experience increased delinquencies in a low-interest-rate environment when such an environment is accompanied by high unemployment and recessionary conditions.

We are also exposed to foreign exchange rate risk as a result of mismatches between assets and liabilities denominated in different currencies. Fluctuations in the exchange rate between currencies may negatively affect our earnings and the value of our assets and liabilities.

We are also exposed to equity price risk in our investments in equity securities in the banking book and in the trading portfolio. The performance of financial markets may cause adverse changes in the value of our investment and trading portfolios. The volatility of world equity markets due to the continued economic uncertainty has had a particularly strong impact on the financial sector. Continued volatility may affect the value of our investments in equity securities and, depending on their fair value and future recovery expectations, could become a permanent impairment which would be subject to write-offs against our results. To the extent any of these risks materialize, our net interest income or the market value of our assets and liabilities could be materially adversely affected, which would in turn adversely impact our business.

Market conditions have resulted, and could result, in material changes to the estimated fair values of our financial assets. Negative fair value adjustments could have a material adverse effect on our operating results, financial condition and prospects.

In the past ten years, financial markets have been subject to significant stress resulting in steep falls in perceived or actual financial asset values, particularly due to volatility in global financial markets and the resulting widening of credit spreads. We have material exposures to securities, loans and other investments that are recorded at fair value and are therefore exposed to potential negative fair value adjustments. Asset valuations in future periods, reflecting then-prevailing market conditions, may result in negative changes in the fair values of our financial assets and these may also translate into increased impairments. In addition, the value ultimately realized by us on disposal may be lower than the current fair market value. Any of these factors could require us to record negative fair value adjustments, which may have a material adverse effect on our operating results, financial condition or prospects.

In addition, to the extent that fair values are determined using financial valuation models, such values may be inaccurate or subject to change, as the data used by such models may not be available or may become unavailable due to changes in market conditions, particularly for illiquid assets, and particularly in times of economic instability. In such circumstances, our valuation methodologies require us to make assumptions, judgments and estimates in order to establish fair value, and reliable assumptions are difficult to make and are inherently uncertain and valuation models are complex, making them inherently imperfect predictors of actual results. Any consequential impairments or write-downs could have a material adverse effect on our operating results, financial condition and prospects.

The credit quality of our loan portfolio may deteriorate and our allowance for impairment losses could be insufficient to cover our actual losses, which could have a material adverse effect on us.

Risks arising from changes in credit quality and the recoverability of loans and amounts due from counterparties are inherent in a wide range of our businesses. Non-performing or low credit quality loans have in the past negatively impacted our results of operations and could do so in the future. In particular, the amount of our reported non-performing loans may increase in the future as a result of growth in our total loan portfolio, including as a result of loan portfolios that we may acquire in the future (the credit quality of which may turn out to be worse than we had anticipated), or factors beyond our control, such as adverse changes in the credit quality of our borrowers and counterparties or a general deterioration in economic

conditions. If we were unable to control the level of our non-performing or poor credit quality loans, this could have a material adverse effect on us.

Our allowance for impairment of losses is based on our current assessment of and expectations concerning various factors affecting the quality of our loan portfolio. These factors include, among other things, our borrowers’ financial condition, repayment abilities and repayment intentions, the realizable value of any collateral, the prospects for support from any guarantor, government macroeconomic policies, interest rates and the legal and regulatory environment. Because many of these factors are beyond our control and there is no precise method for predicting loan and credit losses, we cannot assure that our current or future allowance for impairment losses will be sufficient to cover actual losses. If our assessment of and expectations concerning the above-mentioned factors differ from actual developments, if the quality of our total loan portfolio deteriorates for any reason, including the increase in lending to individuals and SMEs and the introduction of new products, or if the future actual losses exceed our estimates of expected losses, we may be required to increase our allowance for impairment losses, which may adversely affect our business. Additionally, in calculating our allowance for impairment losses, we employ qualitative tools and statistical models which may not be reliable in all circumstances and which are dependent upon data that may not be complete.

We believe that recoveries of non-performing loans as a percentage of our total non-performing loan portfolio are likely to decline over time because of the aging of our non-performing loan portfolio. In addition, because the mortgage foreclosure process relating to collateral in Mexico takes three years on average to be fully completed due to procedural requirements under Mexican law, other factors such as third-party claims, mechanic’s liens and deterioration of the relevant property may impair the value of the collateral during the foreclosure process.

Our exposure to individuals and small and medium-sized businesses could lead to higher levels of non-performing loans, allowances for impairment losses and write-offs.