UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811‑23251 |

|

| Invesco High Income 2024 Target Term Fund |

| (Exact name of registrant as specified in charter) |

|

| 1555 Peachtree Street, N.E., Suite 1800 Atlanta, Georgia 30309 |

| (Address of principal executive offices) (Zip code) |

|

| Sheri Morris 1555 Peachtree Street, N.E., Suite 1800 Atlanta, Georgia 30309 |

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (713) 626‑1919

| | |

| Date of fiscal year end: | | 2/28 |

| |

| Date of reporting period: | | 2/28/2023 |

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

(a) The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e‑1 under the Investment Company Act of 1940 is as follows:

| | |

| | |

Annual Report to Shareholders | | February 28, 2023 |

Invesco High Income 2024 Target Term Fund

NYSE: IHTA

Management’s Discussion of Fund Performance

| | | | |

| |

Performance summary | |

For the fiscal year ended February 28, 2023, Invesco High Income 2024 Target Term Fund (the Fund), at net asset value (NAV), outperformed its benchmark, the Bloomberg U.S. CMBS Investment Grade Index. The Fund’s return can be calculated based on either the market price or the NAV of its shares. NAV per share is determined by dividing the value of the Fund’s portfolio securities, cash and other assets, less all liabilities and preferred shares, by the total number of common shares outstanding. Market price reflects the supply and demand for Fund shares. As a result, the two returns can differ, as they did during the fiscal year. | |

| | |

| Performance | | | | |

| Total returns, 2/28/22 to 2/28/23 | | | | |

| Fund at NAV | | | -7.05 | % |

| Fund at Market Value | | | -6.86 | |

Bloomberg U.S. CMBS Investment Grade Index▼ (Broad Market/Style-Specific Index) | | | -7.77 | |

| Market Price Discount to NAV as of 2/28/23 | | | -3.82 | |

| |

Source(s): ▼Bloomberg LP | | | | |

|

| The performance data quoted represent past performance and cannot guarantee comparable future results; current performance may be lower or higher. Investment return, NAV and common share market price will fluctuate so that you may have a gain or loss when you sell shares. Please visit invesco.com/us for the most recent month-end performance. Performance figures reflect Fund expenses, the reinvestment of distributions (if any) and changes in NAV for performance based on NAV and changes in market price for performance based on market price. | |

Since the Fund is a closed-end management investment company, shares of the Fund may trade at a discount or premium from the NAV. This characteristic is separate and distinct from the risk that NAV could decrease as a result of investment activities and may be a greater risk to investors expecting to sell their shares after a short time. The Fund cannot predict whether shares will trade at, above or below NAV. The Fund should not be viewed as a vehicle for trading purposes. It is designed primarily for risk-tolerant long-term investors. | |

Market conditions and your Fund

The beginning of the fiscal year was headlined by a historic rise in inflation along with global geopolitical and economic tensions. Inflation, as measured by the Consumer Price Index, reached 8.5%,1 its highest level in over 40 years. In response, the US Federal Reserve (the Fed) shifted to tighter monetary policy, hiking its Fed funds rate by 0.25%,2 its first increase since 2018. Geopolitical and economic tensions between Ukraine and Russia culminated with the latter invading Ukrainian territory. World leaders levied sanctions against Russia that had material effects on its fixed income markets, particularly sovereign debt and corporates, and levels of liquidity. The Russia-Ukraine war exacerbated inflationary pressures while also exerting downward pressure on economic growth through a surge in commodity/energy prices. Additionally, surges in COVID-19 cases in China exacerbated supply chain issues and aggravated inflation. During the first quarter of 2022, the two-year Treasury yield rose significantly from 0.78% to 2.28%, while the 10-year Treasury increased slightly from 1.63% to 2.32%.3

In the second quarter of 2022, the macro backdrop of tightening financial conditions and slowing economic growth was negative for credit asset classes. Inflation increased further to 9.1% and fixed income markets experienced significant negative performance

as bond sectors felt the impact of rising interest rates with negative performance ranging from -0.9% (Bloomberg Asset-Backed Securities) to -9.8% (Bloomberg US Corporate High Yield).4 Credit spreads increased across all major credit-sensitive sectors, reflecting anticipation of an economic slowdown and increasing concerns about recession risk, with corporate spreads ending the second quarter of 2022 above their long-term historical average. The Fed continued its rapid tightening of monetary policy in an effort to combat inflation via higher interest rates while simultaneously engineering a soft landing to not push the economy into a recession. The Fed aggressively raised its Fed funds rate during the fiscal year: a 0.50% hike in May, three 0.75% hikes in June, July and November, the largest hikes since 1994, a 0.50% hike in December, and a 0.25% hike in January to a target Fed funds rate of 4.50% to 4.75%, the highest since 2006.2 At their January 2023 meeting, the Fed indicated that there were signs of inflation coming down, but not enough to counter the need for more interest rate increases. While rates remained elevated across all maturities on the yield curve, the two-year Treasury rates increased from 1.44% to 4.81% during the fiscal year, while 10-year Treasury rates increased from 1.83% to 3.92%.3 At the end of the fiscal year, the yield curve remained inverted, which historically has been an indicator of a potential recession. However, attractive yields and

encouraging macroeconomic data show signs of a possible rebound for fixed income markets, in our opinion.

CMBS total return, represented by the Bloomberg U.S. CMBS Investment Grade Index, was negative for the fiscal year at -7.77%. The asset class experienced spread widening as broad market volatility caused by inflation concerns and rate hikes by an aggressive Fed weighed on spreads. Despite declining CMBS new issuance volumes, significant outflows from fixed income mutual funds contributed to spread widening during 2022. Fixed income mutual fund outflows have improved materially in January and February of 2023. US commercial real estate’s fundamental improvement witnessed over the past few years has halted given accelerated monetary policy tightening by the Fed. Declining real estate values, increased borrowing costs and tighter mortgage lending standards are likely to increase refinance challenges for borrowers facing near-term loan maturities. We expect post COVID-19 structural changes in demand for office and retail property space will also create challenges for borrowers seeking to obtain funding upon maturity.

Under these market conditions the Fund posted a return of -7.05% for the fiscal year and outperformed its broad market/style-specific benchmark the Bloomberg U.S. CMBS Investment Grade Index. This was largely driven by the Fund’s material underweight duration positioning. Out-of-index exposure to real estate investment trusts (REITs) and emphasis/overweight on BBB-rated credits detracted from relative Fund performance during the fiscal year.

The Fund uses a CMBS repurchase facility as a form of leverage to seek to enhance its potential to produce a high level of current income and return $9.835 per share to shareholders on or around December 1, 2024. The Fund uses leverage because we believe that, over time, it can provide opportunities for additional income and total return for common shareholders. However, the use of leverage also can expose common shareholders to additional volatility. For example, if the prices of securities held by a fund decline, the negative effect of these valuation changes on common share NAV and total return is magnified by the use of leverage. Conversely, leverage may enhance common-share returns during periods when the prices of securities held by a fund generally are rising.

Over the fiscal year, leverage contributed to the Fund’s performance relative to its broad market/style-specific benchmark. At the close of the fiscal year, leverage accounted for approximately 27% of the Fund’s total assets. For more information about the Fund’s use of leverage, see the Notes to Financial Statements later in this report.

Thank you for your investment in Invesco High Income 2024 Target Term Fund.

| 1 | Source: US Bureau of Labor Statistics |

| | |

| 2 | | Invesco High Income 2024 Target Term Fund |

| 2 | Source: Federal Reserve of Economic Data |

| 3 | Source: US Department of the Treasury |

Portfolio manager(s):

Mario Clemente

Kevin Collins

Brian Norris

Dan Saylor

The views and opinions expressed in management’s discussion of Fund performance are those of Invesco Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

See important Fund and, if applicable, index disclosures later in this report.

| | |

| 3 | | Invesco High Income 2024 Target Term Fund |

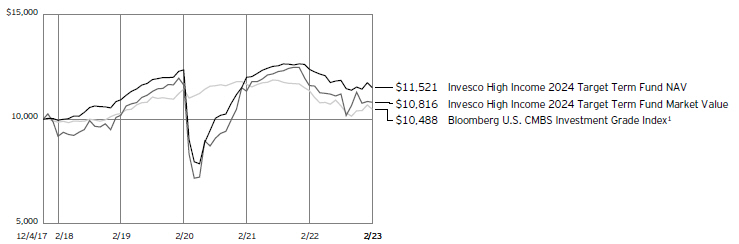

Your Fund’s Long-Term Performance

Results of a $10,000 Investment

Fund and index data from 12/4/17

1 Source: Bloomberg LP

Past performance cannot guarantee future results.

Performance shown in the chart does not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares.

| | |

| 4 | | Invesco High Income 2024 Target Term Fund |

| | | | | | | | |

| |

| Average Annual Total Returns | |

| As of 2/28/23 | |

| | | | NAV | | | | Market | |

| Inception (12/4/17) | | | 2.74 | % | | | 1.51 | % |

| 5 Years | | | 2.97 | | | | 3.31 | |

| 1 Year | | | -7.05 | | | | -6.86 | |

The performance data quoted represent past performance and cannot guarantee future results; current performance may be lower or higher. Please visit invesco.com/performance for the most recent month-end performance.

Performance figures do not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares.

| | |

| 5 | | Invesco High Income 2024 Target Term Fund |

Supplemental Information

| ∎ | Unless otherwise stated, information presented in this report is as of February 28, 2023, and is based on total net assets applicable to common shares. |

| ∎ | Unless otherwise noted, all data is provided by Invesco. |

| ∎ | To access your Fund’s reports, visit invesco.com/fundreports. |

About indexes used in this report

| ∎ | The Bloomberg U.S. CMBS Investment Grade Index consists of publicly issued, fixed rate, nonconvertible, investment grade debt securities. |

| ∎ | The Fund is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Fund may deviate significantly from the performance of the index(es). |

| ∎ | A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

Changes to the Trust’s Governing Documents

At a meeting held on September 19-20, 2022, the Trust’s Board of Trustees (the “Board”) approved changes to the Trust’s Amended and Restated Agreement and Declaration of Trust (the “Declaration of Trust”) and the Trust’s Amended and Restated Bylaws (the “Bylaws”). Capitalized terms not otherwise defined herein shall have the meanings ascribed to them in the Declaration of Trust or Bylaws, as applicable. The following is a summary of certain of these changes. This information may not reflect all of the changes that have occurred since you purchased the Trust.

Declaration of Trust

The Trust’s Declaration of Trust was amended to provide as follows:

| ∎ | “Majority Trustee Vote” means: (a) with respect to a vote of the Board, a vote of the majority of the Trustees then in office, and, if there is one or more Continuing Trustees, a separate vote of a majority of the Continuing Trustees; and (b) with respect to a vote of a committee or sub-committee of the Board, a vote of the majority of the members of such committee or subcommittee, and, if there is one or more Continuing Trustees on such committee or sub-committee, a separate vote of a majority of the Continuing Trustees that are members of such committee or sub-committee. |

| ∎ | “Management Trustee” is a Trustee who has present or former associations with the Trust’s Investment Adviser as causes such person to be an Interested Person of the Trust or its Investment Adviser. |

| ∎ | If a pre-suit demand upon the Board to bring a derivative action is not required under Section 2.4(a) of the Declaration of Trust, Shareholders eligible to bring such derivative action under the Delaware Act who hold at least 10% of the outstanding Shares of the Trust shall join in the demand for the Board to commence such action. |

| ∎ | Shareholders who hold at least 10% of the outstanding Shares of the Trust and have obtained authorization from the Trustees can bring or maintain a direct action or claim for monetary damages against the Trust or the Trustees predicated upon an express or implied right of action under the Declaration of Trust or the 1940 Act. |

| ∎ | With respect to any direct actions or claims, the Board shall be entitled to retain counsel or other advisors in considering the merits of any request for authorization to bring a direct action and may require an undertaking by the Shareholders making such request to reimburse the Trust for the fees and expense of any such counsel or other advisors and other out of pocket expenses of the Trust, in the event that the Board determines not to bring such action. |

| ∎ | The Trust is permitted to redeem or repurchase Shares of any Shareholder liable to the Trust under Section 2.5 of the Declaration of Trust at a value determined by the Board in accordance with the 1940 Act and other applicable law, and to set off against and retain any distributions otherwise payable to any Shareholder liable to the Trust under Section 2.5 of the Declaration of Trust, in payment of amounts due under Section 2.5 of the Declaration of Trust. |

| ∎ | For purposes of Section 2.5 of the Declaration of Trust, the Board may designate a committee of one Trustee to consider a Shareholder request for authorization to bring a direct action if necessary to create a committee with a majority of Trustees who are “independent trustees” (as such term in defined in the Delaware Act). |

| ∎ | The term of any Trustee standing for re-election who fails to receive sufficient votes to be elected to office due to a lack of quorum or a failure of such Trustee or any successor Trustee to such Trustee to receive the required Shareholder vote set forth in the Declaration of Trust shall continue until the annual meeting held in the third succeeding year and until a successor Trustee to such Trustee is duly elected and shall have qualified. |

|

| NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| | |

| 6 | | Invesco High Income 2024 Target Term Fund |

| ∎ | In the event that any Trust Property is held by the Trustees, the right, title and interest of the Trustees in the Trust Property shall vest automatically in each Person who may hereafter become a Trustee. |

| ∎ | Without limiting the Section 4.1 of the Declaration of the Trust and subject to any applicable limitation in the Governing Instrument or applicable law, the Trustees shall have power and authority, [among others], to establish one or more committees or sub-committees, to delegate any of the powers of the Trustees to said committees or sub-committees and to adopt a written charter for one or more of such committees or subcommittees governing its membership, duties and operations and any other characteristics as the Trustees may deem proper, each of which committees of shall be comprised of one or more members as determined by the Trustees and sub-committees shall be comprised of one or more members as determined by the committee or such subcommittee (which may be less than the whole number of Trustees then in office), and may be empowered to act for and bind the Trustees and the Trust as if the acts of such committee or sub-committee were the acts of all the Trustees then in office. |

| ∎ | In accordance with Section 3804(e) of the Delaware Act, any suit, action or proceeding brought by or in the right of any Shareholder or any person claiming any interest in any Shares seeking to enforce any provision of, or based on any matter arising out of, or in connection with, the Declaration of Trust or the Trust, any class or any Shares, including any claim of any nature against the Trust, any Class, the Trustees or officers of the Trust, shall be brought exclusively in the Court of Chancery of the State of Delaware to the extent there is subject matter jurisdiction in such court for the claims asserted or, if not, then in the Superior Court of the State of Delaware, provided, however, that unless the Trust consents in writing to the selection of an alternative forum, the United States District Court for the Southern District of New York shall, to the fullest extent permitted by law, be the sole and exclusive forum for the resolution of any complaint asserting a cause of action arising under the federal securities laws, and all Shareholders and other such Persons hereby irrevocably consent to the jurisdiction of such courts (and the appropriate appellate courts therefrom) in any such suit, action or proceeding and irrevocably waive, to the fullest extent permitted by law, any objection they may make now or hereafter have to the laying of the venue of any such suit, action or proceeding in such court or that any such suit, action or proceeding brought in any such court has been brought in an inconvenient forum and further, IN CONNECTION WITH ANY SUCH SUIT, ACTION, OR PROCEEDING BROUGHT IN ANY SUCH COURT, ALL SHAREHOLDERS AND ALL OTHER SUCH PERSONS HEREBY IRREVOCABLY WAIVE THE RIGHT TO A TRIAL BY JURY TO THE FULLEST EXTENT PERMITTED BY LAW. |

Bylaws

The Trust’s Bylaws were amended to provide as follows:

| ∎ | The Board may, by resolution passed by a Majority Trustee Vote, establish one or more sub-committees of each such Committee, and the membership, duties and operations of each such sub-committee shall be set forth in the written Charter of the applicable Committee. The Board may, by resolution passed by a Majority Trustee Vote, designate one or more additional committees, including ad hoc committees to address specified issues, each of which may, if deemed advisable by the Board of Trustees, have a written charter. |

| ∎ | The Trustees may, in their sole discretion, determine that a meeting of Shareholders may be held partly or solely by means of remote communications. If authorized by the Trustees, in their sole discretion, and subject to such guidelines and procedures as the Trustees may adopt, Shareholders and proxyholders not physically present at a meeting of Shareholders may, by means of remote communications: (a) participate in a meeting of Shareholders; and (b) be deemed present in person and vote at a meeting of Shareholders whether such meeting is to be held at a designated place or solely by means of remote communications, provided that: (i) the Trust shall implement such measures as the Trustees deem to be reasonable (A) to verify that each person deemed present and permitted to vote at the meeting by means of remote communications is a Shareholder or proxyholder; and (B) to provide such Shareholders and proxyholders a reasonable opportunity to participate in the meeting and to vote on matters submitted to the Shareholders; and (ii) if any Shareholder or proxyholder votes or takes other action at the meeting by means of remote communications, a record of such vote or other action shall be maintained by the Trust. The Trustees may, in their sole discretion, notify Shareholders of any postponement, adjournment or a change of the place of a meeting of Shareholders (including a change to hold the meeting solely by means of remote communications) by a document publicly filed by the Trust with the Commission without the requirement of any further notice under the Bylaws. |

| ∎ | Any Shareholder desiring to nominate any person or persons (as the case may be) for election as a Trustee or Trustees of the Trust shall deliver, as part of such Shareholder Notice, a statement in writing with respect to the person or persons to be nominated, together with any persons to be designated as a proposed substitute nominee in the event that a proposed nominee is unwilling or unable to serve, including by reason of any disqualification (a “Proposed Nominee”) and any Proposed Nominee Associated Person setting forth all information required by the Bylaws, including: |

– information required by the Bylaws with respect to any Proposed Nominee Associated Person;

– information to establish to the satisfaction of the Board of Trustees that the Proposed Nominee satisfies the trustee qualifications as set out in the Declaration of Trust;

– any other information relating to such Proposed Nominee or Proposed Nominee Associated Person that would be required to be disclosed in a proxy statement or other filings required to be made in connection with solicitations of proxies for election of trustees in an election contest pursuant to Section 14 of the Exchange Act (even if an election contest is not involved); and

– written and signed certification of each Proposed Nominee that (i) all information regarding such Proposed Nominee included in and/or accompanying the shareholder notice is true, complete and accurate, (ii) such Proposed Nominee is not, and will not become a party to, any agreement, arrangement or understanding (whether written or oral) with any person other than the Trust in connection with service or action as a Trustee of the Trust that has not been disclosed to the Trust, (iii) the Proposed Nominee satisfies the qualifications of persons nominated or seated as trustees as set forth in the Declaration of Trust at the time of their nomination, and (iv) such Proposed Nominee will continue to satisfy the qualifications of persons nominated or seated as trustees as set forth in the Declaration of Trust at the time of their election, if elected.

| ∎ | Any Shareholder who gives a Shareholder Notice of any matter proposed to be brought before the meeting or to elect Proposed Nominees shall deliver, as part of such Shareholder Notice, all statements and representations required by the Bylaws, including: |

– any other information relating to such Shareholder, such beneficial owner, or any Shareholder Associated Person that would be required to be disclosed in a proxy statement or other filing required to be made in connection with the solicitation of proxies by such Person with respect to the proposed business to be brought by such Person before the annual meeting pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated thereunder, whether or not such Person intends to deliver a proxy statement or solicit proxies;

– a statement in writing with respect to the Shareholder and the beneficial owner, if any, on whose behalf the proposal is being made setting forth, among other requirements, the name and address of such Shareholder, as they appear on the Trust’s books, and of such beneficial owner and of any Shareholder Associated Person; the number and class of Shares with respect to such Shares, which

| | |

| 7 | | Invesco High Income 2024 Target Term Fund |

are owned beneficially and of record by such Shareholder, such beneficial owner, and any Shareholder Associated Person; the name of each nominee holder of Shares owned beneficially but not of record by such Shareholder, beneficial owner, or any Shareholder Associated Person, and the number and class of such Shares; and other information related to the foregoing as required by the Bylaws;

– a description of any agreement, arrangement or understanding, whether written or oral (including any derivative or short positions, profit interests, options or similar rights and borrowed or loaned shares) that has been entered into as of the date of the Shareholder Notice by, or on behalf of, such Shareholder, such beneficial owners, or any Shareholder Associated Person (i) the effect or intent of which is to mitigate loss to, manage risk or benefit of share price changes for, or increase or decrease the voting power or pecuniary or economic interest of such Shareholder or, such beneficial owner, or any Shareholder Associated Person; or (ii) related to such proposal; and

– a description of all agreements, arrangements, or understandings (whether written or oral) between or among such Shareholder, such beneficial owners, or any Shareholder Associated Person, and any other person or persons (including their names) in connection with the proposal of such business and any material interest of such person or any Shareholder Associated Person, in such business, including any anticipated benefit therefrom to such person, or any Shareholder Associated Person.

| ∎ | A Shareholder providing notice of any nomination or other business proposed to be brought before an annual meeting of Shareholders shall further update and supplement such notice, if necessary, so that, with respect to nominations of persons for election as a Trustee, any additional information reasonably requested by the Board to determine that each person whom the Shareholder proposes to nominate for election as a Trustee is qualified to act as a Trustee, including information reasonably requested by the Board to determine that such proposed candidate has met the trustee qualifications as set out in the Declaration of Trust, is provided, and such update and supplement shall be received by the Secretary at the principal executive offices of the Trust not later than five (5) business days after the request by the Board for additional information regarding trustee qualifications has been delivered to, or mailed and received by, such Shareholder providing notice of any nomination. |

| ∎ | Notwithstanding the foregoing provisions of this Article and without limiting the generality of any other requirements herein, unless otherwise required by law, a Shareholder shall be disqualified from bringing any business proposed to be brought before a meeting if any of the information in such Shareholder’s notice, or provided in connection therewith, is not correct and complete or if such Shareholder does not comply fully with the representations in such notice. |

For the purposes of the foregoing changes, a “Proposed Nominee Associated Person” of any Proposed Nominee shall mean (A) any person acting in concert with such Proposed Nominee, (B) any direct or indirect beneficial owner of Shares owned of record or beneficially by such Proposed Nominee or person acting in concert with the Proposed Nominee and (C) any person controlling, controlled by or under common control with such Proposed Nominee or a Proposed Nominee Associated Person.

For the purposes of the foregoing changes, a “Shareholder Associated Person” of any beneficial or record shareholder shall mean (A) any person acting in concert with such shareholder, (B) any direct or indirect beneficial owner of Shares owned of record or beneficially by such shareholder or any person acting in concert with such shareholder, (C) any person controlling, controlled by or under common control with such shareholder or a Shareholder Associated Person and (D) any member of the immediate family of such shareholder or Shareholder Associated Person.

The Trust’s Declaration of Trust and Bylaws contain other provisions, including all requirements for the conduct of shareholder meetings, and are available in their entirety upon request to the Trust’s Secretary, c/o Invesco Advisers, Inc., 11 Greenway Plaza, Suite 1000 Houston, TX 77046.

Application of Control Share Provisions

Effective August 1, 2022, the Trust became automatically subject to newly enacted control share acquisition provisions within the Delaware Statutory Trust Act (the “Control Share Provisions”). In general, the Control Share Provisions limit the ability of holders of “control beneficial interests” to vote their shares of a fund above various threshold levels that start at 10% unless the other shareholders of such fund vote to reinstate those rights. “Control beneficial interests” are aggregated to include the holdings of related parties and shares acquired before the effective date of the Control Share Provisions. A fund’s board of trustees may exempt acquisitions from the application of the Control Share Provisions.

The Control Share Provisions require shareholders to disclose any control share acquisition to the Trust within 10 days of such acquisition and, upon request, to provide any related information that the Trust’s Board reasonably believes is necessary or desirable.

The foregoing is only a summary of certain aspects of the Control Share Provisions. Shareholders should consult their own legal counsel with respect to the application of the Control Share Provisions to their beneficial interests of the Trust and any subsequent acquisitions of beneficial interests.

| | |

| 8 | | Invesco High Income 2024 Target Term Fund |

Dividend Reinvestment Plan

The dividend reinvestment plan (the Plan) offers you a prompt and simple way to reinvest your dividends and capital gains distributions (Distributions) into additional shares of your Invesco closed-end Fund (the Fund). Under the Plan, the money you earn from Distributions will be reinvested automatically in more shares of the Fund, allowing you to potentially increase your investment over time. All shareholders in the Fund are automatically enrolled in the Plan when shares are purchased.

Plan benefits

| | You may increase your shares in your Fund easily and automatically with the Plan. |

| | Shareholders who participate in the Plan may be able to buy shares at below-market prices when the Fund is trading at a premium to its net asset value (NAV). In addition , transaction costs are low because when new shares are issued by the Fund, there is no brokerage fee, and when shares are bought in blocks on the open market, the per share fee is shared among all participants. |

| | You will receive a detailed account statement from Computershare Trust Company, N.A. (the Agent), which administers the Plan. The statement shows your total Distributions, date of investment, shares acquired, and price per share, as well as the total number of shares in your reinvestment account. You can also access your account at invesco.com/closed-end. |

| | The Agent will hold the shares it has acquired for you in safekeeping. |

Who can participate in the Plan

If you own shares in your own name, your purchase will automatically enroll you in the Plan. If your shares are held in “street name” – in the name of your brokerage firm, bank, or other financial institution – you must instruct that entity to participate on your behalf. If they are unable to participate on your behalf, you may request that they reregister your shares in your own name so that you may enroll in the Plan.

How to enroll

If you haven’t participated in the Plan in the past or chose to opt out, you are still eligible to participate. Enroll by visiting invesco.com/closed-end, by calling toll-free 800 341 2929 or by notifying us in writing at Invesco Closed-End Funds, Computershare Trust Company, N.A., P.O. Box 505000, Louisville, KY 40233-5000. If you are writing to us, please include the Fund name and account number and ensure that all shareholders listed on the account sign these written instructions. Your participation in the Plan will begin with the next Distribution payable after the Agent receives your authorization, as long as they receive it before the “record date,” which is generally 10 business days before the Distribution is paid. If your authorization arrives after such record date, your participation in the Plan will begin with the following Distribution.

How the Plan works

If you choose to participate in the Plan, your Distributions will be promptly reinvested for you, automatically increasing your shares. If the Fund is trading at a share price that is equal to its NAV, you’ll pay that amount for your reinvested shares. However, if the Fund is trading above or below NAV, the price is determined by one of two ways:

| | 1. | Premium: If the Fund is trading at a premium - a market price that is higher than its NAV - you’ll pay either the NAV or 95 percent of |

| | the market price, whichever is greater. When the Fund trades at a premium, you may pay less for your reinvested shares than an investor purchasing shares on the stock exchange. Keep in mind, a portion of your price reduction may be taxable because you are receiving shares at less than market price. |

| | 2. | Discount: If the Fund is trading at a discount - a market price that is lower than its NAV - you’ll pay the market price for your reinvested shares. |

Costs of the Plan

There is no direct charge to you for reinvesting Distributions because the Plan’s fees are paid by the Fund. If the Fund is trading at or above its NAV, your new shares are issued directly by the Fund and there are no brokerage charges or fees. However, if the Fund is trading at a discount , the shares are purchased on the open market, and you will pay your portion of any per share fees. These per share fees are typically less than the standard brokerage charges for individual transactions because shares are purchased for all participants in blocks, resulting in lower fees for each individual participant. Any service or per share fees are added to the purchase price. Per share fees include any applicable brokerage commissions the Agent is required to pay.

Tax implications

The automatic reinvestment of Distributions does not relieve you of any income tax that may be due on Distributions. You will receive tax information annually to help you prepare your federal income tax return.

Invesco does not offer tax advice. The tax information contained herein is general and is not exhaustive by nature. It was not intended or written to be used, and it cannot be used, by any taxpayer for avoiding penalties that may be imposed on the taxpayer under US federal tax laws. Federal and state tax laws are complex and constantly changing. Shareholders should always consult a legal or tax adviser for information concerning their individual situation.

How to withdraw from the Plan

You may withdraw from the Plan at any time by calling 800 341 2929, by visiting invesco.com/closed-end or by writing to Invesco Closed-End Funds, Computershare Trust Company, N.A., P.O. Box 505000, Louisville, KY 40233-5000. Simply indicate that you would like to withdraw from the Plan, and be sure to include your Fund name and account number. Also, ensure that all shareholders listed on the account sign these written instructions. If you withdraw, you have three options with regard to the shares held in the Plan:

| | 1. | If you opt to continue to hold your non-certificated whole shares (Investment Plan Book Shares), they will be held by the Agent electronically as Direct Registration Book-Shares (Book-Entry Shares) and fractional shares will be sold at the then-current market price. Proceeds will be sent via check to your address of record after deducting applicable fees, including per share fees such as any applicable brokerage commissions the Agent is required to pay. |

| | 2. | If you opt to sell your shares through the Agent, we will sell all full and fractional shares and send the proceeds via check to your address of record after deducting a $2.50 service fee and per share fees. Per share fees include any applicable brokerage commissions the Agent is required to pay. |

| | 3. | You may sell your shares through your financial adviser through the Direct Registration System (DRS). DRS is a service within the securities industry that allows Fund shares to be held in your name in electronic format. You retain full ownership of your shares, without having to hold a share certificate. You should contact your financial adviser to learn more about any restrictions or fees that may apply. |

The Fund and Computershare Trust Company, N.A. may amend or terminate the Plan at any time. Participants will receive at least 30 days written notice before the effective date of any amendment. In the case of termination, Participants will receive at least 30 days written notice before the record date for the payment of any such Distributions by the Fund. In the case of amendment or termination necessary or appropriate to comply with applicable law or the rules and policies of the Securities and Exchange Commission or any other regulatory authority, such written notice will not be required.

To obtain a complete copy of the current Dividend Reinvestment Plan, please call our Client Services department at 800 341 2929 or visit invesco.com/closed-end.

| | |

| 9 | | Invesco High Income 2024 Target Term Fund |

Fund Information

Portfolio Composition†

| | | | | |

| By credit quality | | % of total investments |

| |

| AAA | | | | 6.00 | % |

| |

| AA+ | | | | 2.40 | |

| |

| AA- | | | | 2.70 | |

| |

| A | | | | 5.60 | |

| |

| A- | | | | 8.00 | |

| |

| BBB+ | | | | 3.70 | |

| |

| BBB | | | | 5.30 | |

| |

| BBB- | | | | 34.50 | |

| |

| BB | | | | 9.50 | |

| |

| BB- | | | | 2.00 | |

| |

| B+ | | | | 2.80 | |

| |

| B | | | | 0.30 | |

| |

| CCC | | | | 2.60 | |

| |

| Non-Rated | | | | 9.50 | |

| |

| Cash | | | | 5.10 | |

† Portfolio information is subject to change due to active management. Ratings are based upon using Moody’s Investor Services, Inc. (“Moody’s”), Standard & Poor’s Ratings Services, a Standard & Poor’s Financial Services LLC business (“Standard & Poor’s” or “S&P”), Fitch Ratings, a part of the Fitch Group (“Fitch”), Kroll Bond Rating Agency, Inc. (“Kroll”), DBRS Limited (“DBRS”) and Morningstar Credit Ratings, LLC (“Morningstar”) if any such nationally recognized statistical rating organizations (“NRSROs”) rate the security. If securities are rated differently by the ratings agencies, the highest rating is applied.

Top Five Debt Issuers*

| | | | | | | |

| | | | | % of total net assets |

| | |

| 1. | | Commercial Mortgage Trust | | | | 38.26 | % |

| | |

| 2. | | JPMBB Commercial Mortgage Securities Trust | | | | 17.08 | |

| | |

| 3. | | Citigroup Commercial Mortgage Trust | | | | 11.21 | |

| | |

| 4. | | Morgan Stanley Bank of America Merrill Lynch Trust | | | | 10.42 | |

| | |

| 5. | | FREMF Mortgage Trust | | | | 8.77 | |

The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security.

| * | Excluding money market fund holdings, if any. |

Data presented here are as of February 28, 2023.

| | |

| 10 | | Invesco High Income 2024 Target Term Fund |

Schedule of Investments

February 28, 2023

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Asset-Backed Securities–116.45%(a) | |

| | |

BX Commercial Mortgage Trust,

Series 2021-VOLT, Class D, 6.24%

(1 mo. USD LIBOR + 1.65%), 09/15/2023(b)(c) | | $ | 2,750,000 | | | $ | 2,658,526 | |

| Citigroup Commercial Mortgage Trust, | | | | | | | | |

| Series 2014-GC19, Class AS, 4.35%, 01/10/2024 | | | 5,000,000 | | | | 4,889,524 | |

Series 2014-GC19, Class D, 5.09%, 02/10/2024(b)(d)(e) | | | 500,000 | | | | 469,880 | |

Series 2014-GC19, Class XA, IO, 1.27%, 01/10/2024(d)(f) | | | 35,709,384 | | | | 232,293 | |

Series 2014-GC23, Class D, 4.48%, 07/10/2024(b)(d)(e) | | | 3,000,000 | | | | 2,646,577 | |

| Commercial Mortgage Trust, | | | | | | | | |

Series 2013-CR13, Class D, 4.88%, 12/10/2023(b)(d)(e) | | | 3,250,000 | | | | 2,633,853 | |

Series 2014-CR14, Class C, 4.73%, 01/10/2024(d)(e) | | | 1,000,000 | | | | 935,253 | |

Series 2014-CR19, Class C, 4.70%, 08/10/2024(d)(e) | | | 3,000,000 | | | | 2,852,528 | |

Series 2014-CR19, Class D, 4.70%, 08/10/2024(b)(d)(e) | | | 4,000,000 | | | | 3,651,421 | |

Series 2014-LC15, Class XA, IO, 1.22%, 12/10/2023(d)(f) | | | 33,997,313 | | | | 234,881 | |

Series 2014-UBS4, Class C, IO, 4.81%, 07/10/2024(d)(f) | | | 3,000,000 | | | | 2,709,124 | |

Series 2014-UBS4, Class XD, IO, 0.96%, 06/10/2024(b)(f) | | | 22,741,889 | | | | 256,347 | |

Series 2014-UBS5, Class D, 3.50%, 09/10/2024(b)(d) | | | 4,500,000 | | | | 3,358,321 | |

Series 2014-UBS6, Class C, 4.58%, 12/10/2024(d)(e) | | | 1,287,000 | | | | 1,173,471 | |

Series 2014-UBS6, Class D, 3.94%, 12/10/2024(b)(d)(e) | | | 5,000,000 | | | | 4,066,049 | |

Series 2015-CR22, Class D, 4.07%, 03/10/2025(b)(e) | | | 4,000,000 | | | | 3,425,065 | |

Series 2015-CR23, Class C, 4.42%, 04/10/2025(e) | | | 3,060,000 | | | | 2,820,308 | |

CSAIL Commercial Mortgage Trust,

Series 2017-CX10, Class E, 3.35%, 11/15/2027(b)(e) | | | 4,000,000 | | | | 2,059,129 | |

DBJPM Mortgage Trust,

Series 2017-C6, Class D, 3.18%, 06/10/2027(b)(d)(e) | | | 3,500,000 | | | | 2,507,263 | |

| FREMF Mortgage Trust, | | | | | | | | |

Series 2016-K57, Class C, 3.92%, 08/25/2026(b)(e) | | | 3,000,000 | | | | 2,813,909 | |

Series 2017-K71, Class C, 3.88%, 11/25/2027(b)(e) | | | 3,000,000 | | | | 2,724,409 | |

Series 2017-KF41, Class B, 7.07% (1 mo. USD LIBOR + 2.50%), 11/25/2024(b)(c) | | | 912,121 | | | | 900,560 | |

GS Mortgage Securities Trust, Series 2015-GC30, Class C, 4.20%, 05/10/2025(d)(e) | | | 3,398,000 | | | | 3,039,148 | |

Hilton USA Trust, Series 2016-SFP, Class F, 6.16%, 11/05/2023(b) | | | 3,000,000 | | | | 2,769,556 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| JPMBB Commercial Mortgage Securities Trust, | | | | | | | | |

Series 2013-C12, Class D, 4.22%, 06/15/2023(d)(e) | | $ | 500,000 | | | $ | 480,842 | |

Series 2014-C19, Class B, 4.39%, 04/15/2024(e) | | | 2,500,000 | | | | 2,415,287 | |

Series 2014-C22, Class D, 4.55%, 02/15/2026(b)(d)(e) | | | 3,500,000 | | | | 2,641,419 | |

Series 2014-C23, Class D, 3.98%, 10/15/2024(b)(d)(e) | | | 3,500,000 | | | | 3,009,184 | |

Series 2014-C26, Class D, 3.87%, 12/15/2024(b)(d)(e) | | | 4,954,000 | | | | 4,009,508 | |

| Morgan Stanley Bank of America Merrill Lynch Trust, | | | | | | | | |

Series 2014-C19, Class D, 3.25%, 12/15/2024(b)(d) | | | 4,000,000 | | | | 3,087,741 | |

Series 2015-C22, Class D, 4.20%, 04/15/2025(b)(d)(e) | | | 4,379,676 | | | | 3,515,936 | |

Series 2015-C24, Class D, 3.26%, 07/15/2025(b)(d) | | | 1,300,000 | | | | 1,060,534 | |

Morgan Stanley Capital I Trust, Series 2016-UBS9, Class D, 3.00%, 02/15/2026(b)(d) | | | 3,532,000 | | | | 2,562,109 | |

| Wells Fargo Commercial Mortgage Trust, | | | | | | | | |

Series 2014-LC18, Class D, 3.96%, 12/15/2024(b)(d)(e) | | | 3,500,000 | | | | 2,996,343 | |

Series 2015-NXS2, Class D, 4.42%, 07/15/2025(d)(e) | | | 1,000,000 | | | | 818,948 | |

WFRBS Commercial Mortgage Trust,

Series 2014-LC14, Class D, 4.59%, 02/15/2024(b)(d)(e) | | | 3,500,000 | | | | 3,163,320 | |

Total Asset-Backed Securities

(Cost $98,169,081) | | | | 85,588,566 | |

| | |

| | | Shares | | | | |

| Preferred Stocks–11.62% | | | | | | | | |

| Mortgage REITs–11.62% | | | | | | | | |

New York Mortgage Trust, Inc., 8.00%, Series D, Pfd.(g) | | | 100,000 | | | | 2,033,000 | |

PennyMac Mortgage Investment Trust, 8.00%, Series B, Pfd.(g) | | | 97,000 | | | | 2,314,420 | |

Two Harbors Investment Corp., 7.63%, Series B, Pfd.(g) | | | 98,000 | | | | 2,107,980 | |

Two Harbors Investment Corp., 7.25%, Series C, Pfd.(g) | | | 96,000 | | | | 2,083,200 | |

Total Preferred Stocks

(Cost $9,648,493) | | | | 8,538,600 | |

| | |

| | | Principal

Amount | | | | |

| U.S. Government Sponsored Agency | |

| Mortgage-Backed Securities–0.77% | |

Freddie Mac Multifamily Structured Pass-Through Ctfs., Series 2017- K041,Class X1, IO, 2.76%, 07/25/2024

(Cost $614,318)(d)(f) | | $ | 85,510,242 | | | | 569,917 | |

| | |

| | | Shares | | | | |

| Money Market Funds–6.97% | | | | | | | | |

Invesco Government & Agency Portfolio, Institutional Class,

4.51%(h)(i) | | | 1,793,296 | | | | 1,793,296 | |

Invesco Liquid Assets Portfolio, Institutional Class, 4.64%(h)(i) | | | 1,280,737 | | | | 1,280,994 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 11 | | Invesco High Income 2024 Target Term Fund |

| | | | | | | | | | |

| | | Shares | | Value |

| Money Market Funds–(continued) | | | | | | |

Invesco Treasury Portfolio, Institutional Class, 4.50%(h)(i) | | | | 2,049,481 | | | | $ | 2,049,481 | |

Total Money Market Funds

(Cost $5,123,667) | | | | | 5,123,771 | |

TOTAL INVESTMENTS IN SECURITIES–135.81%

(Cost $113,555,559) | | | | | 99,820,854 | |

| REVERSE REPURCHASE AGREEMENTS–(36.74)% | | | | | (27,000,000 | ) |

| OTHER ASSETS LESS LIABILITIES–0.93% | | | | | 677,665 | |

| NET ASSETS APPLICABLE TO COMMON SHARES–100.00% | | | | $ | 73,498,519 | |

Investment Abbreviations:

| | |

| |

| Ctfs. | | - Certificates |

| IO | | - Interest Only |

| LIBOR | | - London Interbank Offered Rate |

| Pfd. | | - Preferred |

| REIT | | - Real Estate Investment Trust |

| USD | | - U.S. Dollar |

Notes to Schedule of Investments:

| (a) | Maturity date reflects the anticipated repayment date. |

| (b) | Security purchased or received in a transaction exempt from registration under the Securities Act of 1933, as amended (the “1933 Act”). The security may be resold pursuant to an exemption from registration under the 1933 Act, typically to qualified institutional buyers. The aggregate value of these securities at February 28, 2023 was $62,986,959, which represented 85.70% of the Fund’s Net Assets. |

| (c) | Interest or dividend rate is redetermined periodically. Rate shown is the rate in effect on February 28, 2023. |

| (d) | All or a portion of the security is pledged as collateral for open reverse repurchase agreeements. See Note 1J. |

| | | | | | | | | | | | | | | |

| Counterparty | | Reverse

Repurchase

Agreements | | Value of Non-cash

Collateral

Pledged* | | Net

Amount |

| Wells Fargo Bank, N.A. | | | $ | 27,000,000 | | | | $ | (27,000,000 | ) | | $– | |

* Amount does not include excess collateral pledged.

| (e) | Interest rate is redetermined periodically based on the cash flows generated by the pool of assets backing the security, less any applicable fees. The rate shown is the rate in effect on February 28, 2023. |

| (f) | Interest only security. Principal amount shown is the notional principal and does not reflect the maturity value of the security. Interest rate is redetermined periodically based on the cash flows generated by the pool of assets backing the security, less any applicable fees. The rate shown is the rate in effect on February 28, 2023. |

| (g) | Security issued at a fixed rate for a specific period of time, after which it will convert to a variable rate. |

| (h) | Affiliated issuer. The issuer and/or the Fund is a wholly-owned subsidiary of Invesco Ltd., or is affiliated by having an investment adviser that is under common control of Invesco Ltd. The table below shows the Fund’s transactions in, and earnings from, its investments in affiliates for the fiscal year ended February 28, 2023. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Value

February 28, 2022 | | Purchases at Cost | | Proceeds

from Sales | | Change in

Unrealized

Appreciation | | Realized

Gain

(Loss) | | Value

February 28, 2023 | | Dividend Income |

| Investments in Affiliated Money Market Funds: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Invesco Government & Agency Portfolio, Institutional Class | | | $ | 2,673,740 | | | | $ | 6,054,581 | | | | $ | (6,935,025 | ) | | | $ | - | | | | $ | - | | | | $ | 1,793,296 | | | | $ | 38,035 | |

| Invesco Liquid Assets Portfolio, Institutional Class | | | | 1,777,871 | | | | | 4,324,701 | | | | | (4,821,848 | ) | | | | 518 | | | | | (248 | ) | | | | 1,280,994 | | | | | 31,814 | |

| Invesco Treasury Portfolio, Institutional Class | | | | 3,055,703 | | | | | 6,919,521 | | | | | (7,925,743 | ) | | | | - | | | | | - | | | | | 2,049,481 | | | | | 49,441 | |

| Total | | | $ | 7,507,314 | | | | $ | 17,298,803 | | | | $ | (19,682,616 | ) | | | $ | 518 | | | | $ | (248 | ) | | | $ | 5,123,771 | | | | $ | 119,290 | |

| (i) | The rate shown is the 7-day SEC standardized yield as of February 28, 2023. |

| | | | | | | | | | | | | | | | | | | | | | |

| Open Centrally Cleared Interest Rate Swap Agreements(a) |

Pay/ Receive Floating Rate | | Floating Rate Index | | Payment

Frequency | | | (Pay)/

Receive

Fixed

Rate | | Payment

Frequency | | Maturity

Date | | Notional Value | | Upfront

Payments

Paid

(Received) | | Value | | Unrealized

Appreciation |

| Interest Rate Risk | | | | | | | | | | | | | | | | | | | | |

| Receive | | 3 Month USD LIBOR | | | Quarterly | | | (2.83)% | | Semi‑Annually | | 11/29/2024 | | USD | | 3,000,000 | | $- | | $122,390 | | $122,390 |

| Receive | | 3 Month USD LIBOR | | | Quarterly | | | (2.86) | | Semi‑Annually | | 11/29/2024 | | USD | | 12,600,000 | | - | | 507,661 | | 507,661 |

| Total Centrally Cleared Interest Rate Swap Agreements | | | | | | $- | | $630,051 | | $630,051 |

| (a) | Centrally Cleared Swap Agreements collateralized by $183,618 cash held with Merrill Lynch International. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 12 | | Invesco High Income 2024 Target Term Fund |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Open Over-The-Counter Credit Default Swap Agreements(a) |

| Counterparty | | Reference Entity | | Buy/Sell

Protection | | (Pay)/

Receive

Fixed Rate | | Payment

Frequency | | Maturity

Date | | Implied

Credit

Spread(b) | | Notional Value | | Upfront

Payments Paid

(Received) | | Value | | Unrealized

Appreciation

(Depreciation) |

| Credit Risk | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| J.P. Morgan Chase Bank, N.A. | | Markit CMBX North America BBB - Index Series 8, Version 1 | | | | Sell | | | | | 3.00 | % | | | | Monthly | | | | | 10/17/2057 | | | | | 15.177 | % | | | | USD 8,400,000 | | | | | $(301,067) | | | | $ | (1,393,770 | ) | | | $ | (1,092,703 | ) |

| (a) | Open Over-The-Counter Swap Agreements collateralized by $1,410,000 cash held with J.P. Morgan Chase Bank, N.A., the Counterparty. |

| (b) | Implied credit spreads represent the current level, as of February 28, 2023, at which protection could be bought or sold given the terms of the existing credit default swap agreement and serve as an indicator of the current status of the payment/performance risk of the credit default swap agreement. An implied credit spread that has widened or increased since entry into the initial agreement may indicate a deteriorating credit profile and increased risk of default for the reference entity. A declining or narrowing spread may indicate an improving credit profile or decreased risk of default for the reference entity. Alternatively, credit spreads may increase or decrease reflecting the general tolerance for risk in the credit markets generally. |

Abbreviations:

| | |

| LIBOR | | – London Interbank Offered Rate |

| USD | | – U.S. Dollar |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 13 | | Invesco High Income 2024 Target Term Fund |

Statement of Assets and Liabilities

February 28, 2023

| | | | |

| Assets: | | | | |

| |

| Investments in unaffiliated securities, at value (Cost $ 108,431,892) | | $ | 94,697,083 | |

|

| | |

| Investments in affiliated money market funds, at value (Cost $ 5,123,667) | | | 5,123,771 | |

|

| | |

| Other investments: | | | | |

| Variation margin receivable–centrally cleared swap agreements | | | 121,221 | |

|

| | |

| Swaps receivable – OTC | | | 2,800 | |

|

| | |

| Deposits with brokers: | | | | |

| Cash collateral – centrally cleared swap agreements | | | 183,618 | |

|

| | |

| Cash collateral – OTC Derivatives | | | 1,410,000 | |

|

| | |

| Cash | | | 49,842 | |

|

| | |

| Receivable for: | | | | |

| Dividends | | | 59,846 | |

|

| | |

| Interest | | | 454,932 | |

|

| | |

| Investment for trustee deferred compensation and retirement plans | | | 18,634 | |

|

| | |

| Other assets | | | 678 | |

|

| | |

| Total assets | | | 102,122,425 | |

|

| | |

| |

| Liabilities: | | | | |

| |

| Other investments: | | | | |

| Premiums received on swap agreements – OTC | | | 301,067 | |

|

| | |

| Unrealized depreciation on swap agreements–OTC | | | 1,092,703 | |

|

| | |

| Payable for: | | | | |

| Reverse repurchase agreements | | | 27,000,000 | |

|

| | |

| Dividends | | | 5,955 | |

|

| | |

| Accrued fees to affiliates | | | 15,782 | |

|

| | |

| Accrued interest expense | | | 8,827 | |

|

| | |

| Accrued trustees’ and officers’ fees and benefits | | | 1,434 | |

|

| | |

| Accrued other operating expenses | | | 179,504 | |

|

| | |

| Trustee deferred compensation and retirement plans | | | 18,634 | |

|

| | |

| Total liabilities | | | 28,623,906 | |

|

| | |

| Net assets applicable to common shares | | $ | 73,498,519 | |

|

| | |

| | | | |

| Net assets applicable to common shares consist of: | | | | |

| Shares of beneficial interest – common shares | | $ | 85,990,579 | |

|

| | |

| Distributable earnings (loss) | | | (12,492,060 | ) |

|

| | |

| | $ | 73,498,519 | |

|

| | |

| |

| Common shares outstanding, no par value, with an unlimited number of common shares authorized: | | | | |

| Shares outstanding | | | 8,786,390 | |

|

| | |

| Net asset value per common share | | $ | 8.37 | |

|

| | |

| Market value per common share | | $ | 8.05 | |

|

| | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 14 | | Invesco High Income 2024 Target Term Fund |

Statement of Operations

For the year ended February 28, 2023

| | | | |

| Investment income: | | | | |

| |

| Interest | | $ | 5,538,110 | |

|

| | |

| Dividends | | | 740,287 | |

|

| | |

| Dividends from affiliated money market funds | | | 119,290 | |

|

| | |

| Total investment income | | | 6,397,687 | |

|

| | |

| |

| Expenses: | | | | |

| |

| Advisory fees | | | 725,789 | |

|

| | |

| Administrative services fees | | | 11,203 | |

|

| | |

| Custodian fees | | | 7,764 | |

|

| | |

| Interest, facilities and maintenance fees | | | 1,010,016 | |

|

| | |

| Transfer agent fees | | | 15,397 | |

|

| | |

| Trustees’ and officers’ fees and benefits | | | 16,156 | |

|

| | |

| Registration and filing fees | | | 21,260 | |

|

| | |

| Reports to shareholders | | | 10,038 | |

|

| | |

| Professional services fees | | | 99,270 | |

|

| | |

| Other | | | 93,747 | |

|

| | |

| Total expenses | | | 2,010,640 | |

|

| | |

| Less: Fees waived | | | (6,154 | ) |

|

| | |

| Net expenses | | | 2,004,486 | |

|

| | |

| Net investment income | | | 4,393,201 | |

|

| | |

| |

| Realized and unrealized gain (loss) from: | | | | |

| Net realized gain (loss) from: | | | | |

| Unaffiliated investment securities | | | 18,790 | |

|

| | |

| Affiliated investment securities | | | (248 | ) |

|

| | |

| Swap agreements | | | 394,014 | |

|

| | |

| | | 412,556 | |

|

| | |

| Change in net unrealized appreciation (depreciation) of: | | | | |

| Unaffiliated investment securities | | | (11,474,156 | ) |

|

| | |

| Affiliated investment securities | | | 518 | |

|

| | |

| Swap agreements | | | 713,660 | |

|

| | |

| | | (10,759,978 | ) |

|

| | |

| Net realized and unrealized gain (loss) | | | (10,347,422 | ) |

|

| | |

| Net increase (decrease) in net assets resulting from operations applicable to common shares | | $ | (5,954,221 | ) |

|

| | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 15 | | Invesco High Income 2024 Target Term Fund |

Statement of Changes in Net Assets

For the years ended February 28, 2023 and 2022

| | | | | | | | |

| | | 2023 | | | 2022 | |

|

| | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 4,393,201 | | | $ | 4,896,885 | |

| | |

| Net realized gain | | | 412,556 | | | | 26,277 | |

| | |

| Change in net unrealized appreciation (depreciation) | | | (10,759,978 | ) | | | (2,167,732 | ) |

| | |

| Net increase (decrease) in net assets resulting from operations applicable to common shares | | | (5,954,221 | ) | | | 2,755,430 | |

| | |

| Distributions to common shareholders from distributable earnings | | | (3,746,314 | ) | | | (4,493,498 | ) |

| | |

| Net increase in common shares of beneficial interest | | | 6,188 | | | | 45,962 | |

| | |

| Net increase (decrease) in net assets applicable to common shares | | | (9,694,347 | ) | | | (1,692,106 | ) |

| | |

| Net assets applicable to common shares: | | | | | | | | |

| Beginning of year | | | 83,192,866 | | | | 84,884,972 | |

| | |

| End of year | | $ | 73,498,519 | | | $ | 83,192,866 | |

|

| | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 16 | | Invesco High Income 2024 Target Term Fund |

Statement of Cash Flows

For the year ended February 28, 2023

| | | | |

| Cash provided by operating activities: | | | | |

| |

| Net increase (decrease) in net assets resulting from operations applicable to common shares | | $ | (5,954,221 | ) |

|

| | |

| |

| Adjustments to reconcile the change in net assets applicable to common shares from operations to net cash provided by operating activities: | | | | |

| Purchases of investments | | | (7,553,740 | ) |

|

| | |

| Proceeds from sales of investments | | | 3,069,132 | |

|

| | |

| Proceeds from sales of short-term investments, net | | | 237,197 | |

|

| | |

| Amortization of premium on investment securities | | | 1,682,724 | |

|

| | |

| Accretion of discount on investment securities | | | (1,514,123 | ) |

|

| | |

| Net realized gain from investment securities | | | (18,790 | ) |

|

| | |

| Net change in unrealized depreciation on investment securities | | | 11,474,156 | |

|

| | |

| Change in operating assets and liabilities: | | | | |

|

| | |

| Decrease in receivables and other assets | | | 15,675 | |

|

| | |

| Increase in accrued expenses and other payables | | | 65,816 | |

|

| | |

| Net change in transactions in swap agreements | | | (2,093 | ) |

|

| | |

| Net cash provided by operating activities | | | 1,501,733 | |

|

| | |

| Cash provided by (used in) financing activities: | | | | |

| Dividends paid to common shareholders from distributable earnings | | | (3,740,610 | ) |

|

| | |

| Net cash provided by (used in) financing activities | | | (3,740,610 | ) |

|

| | |

| Net decrease in cash and cash equivalents | | | (2,238,877 | ) |

|

| | |

| Cash and cash equivalents at beginning of period | | | 9,006,108 | |

|

| | |

| Cash and cash equivalents at end of period | | $ | 6,767,231 | |

|

| | |

| |

| Non-cash financing activities: | | | | |

| Value of shares of beneficial interest issued in reinvestment of dividends paid to shareholders | | $ | 6,188 | |

|

| | |

| |

| Supplemental disclosure of cash flow information: | | | | |

| |

| Cash paid during the period for taxes | | $ | 39,358 | |

|

| | |

| Cash paid during the period for interest, facilities and maintenance fees | | $ | 1,005,631 | |

|

| | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 17 | | Invesco High Income 2024 Target Term Fund |

Financial Highlights

The following schedule presents financial highlights for a share of the Fund outstanding throughout the periods indicated.

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Years Ended

February 28, | | Year Ended

February 29, | | Year Ended

February 28, |

| | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| Net asset value per common share, beginning of period | | | $ | 9.47 | | | | $ | 9.67 | | | | $ | 10.71 | | | | $ | 10.00 | | | | $ | 9.67 | |

Net investment income(a) | | | | 0.50 | | | | | 0.56 | | | | | 0.54 | | | | | 0.54 | | | | | 0.64 | |

| Net gains (losses) on securities (both realized and unrealized) | | | | (1.17 | ) | | | | (0.25 | ) | | | | (1.01 | ) | | | | 0.73 | | | | | 0.25 | |

| Total from investment operations | | | | (0.67 | ) | | | | 0.31 | | | | | (0.47 | ) | | | | 1.27 | | | | | 0.89 | |

| Less: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Dividends paid to common shareholders from net investment income | | | | (0.43 | ) | | | | (0.51 | ) | | | | (0.56 | ) | | | | (0.56 | ) | | | | (0.56 | ) |

| Distributions from net realized gains | | | | – | | | | | – | | | | | (0.01 | ) | | | | – | | | | | – | |

| Total distributions | | | | (0.43 | ) | | | | (0.51 | ) | | | | (0.57 | ) | | | | (0.56 | ) | | | | (0.56 | ) |

| Net asset value per common share, end of period | | | $ | 8.37 | | | | $ | 9.47 | | | | $ | 9.67 | | | | $ | 10.71 | | | | $ | 10.00 | |

| Market value per common share, end of period | | | $ | 8.05 | | | | $ | 9.09 | | | | $ | 9.36 | | | | $ | 10.33 | | | | $ | 9.55 | |

Total return at net asset value(b) | | | | (7.05 | )% | | | | 3.22 | % | | | | (2.86 | )% | | | | 13.07 | % | | | | 9.86 | % |

Total return at market value(c) | | | | (6.86 | )% | | | | 2.36 | % | | | | (2.51 | )% | | | | 14.19 | % | | | | 10.88 | % |

| Net assets applicable to common shares, end of period (000’s omitted) | | | $ | 73,499 | | | | $ | 83,193 | | | | $ | 84,885 | | | | $ | 94,051 | | | | $ | 87,765 | |

Portfolio turnover rate(d) | | | | 3 | % | | | | 2 | % | | | | 3 | % | | | | 9 | % | | | | 5 | % |

| | | | | |

| Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses: | | | | | | | | | | | | | | | | | | | | | | | | | |

| With fee waivers and/or expense reimbursements | | | | 2.59 | % | | | | 1.63 | % | | | | 1.90 | % | | | | 2.31 | % | | | | 2.40 | % |

| With fee waivers and/or expense reimbursements excluding interest, facilities and maintenance fees | | | | 1.28 | % | | | | 1.20 | % | | | | 1.26 | % | | | | 1.20 | % | | | | 1.22 | % |

| Without fee waivers and/or expense reimbursements | | | | 2.60 | % | | | | 1.63 | % | | | | 1.90 | % | | | | 2.31 | % | | | | 2.41 | % |

| Without fee waivers and/or expense reimbursements excluding interest, facilities and maintenance fees | | | | 1.29 | % | | | | 1.20 | % | | | | 1.26 | % | | | | 1.20 | % | | | | 1.22 | % |

| Ratio of net investment income to average net assets | | | | 5.70 | % | | | | 5.71 | % | | | | 6.61 | % | | | | 5.14 | % | | | | 6.53 | % |

| (a) | Calculated using average shares outstanding. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Not annualized for periods less than one year, if applicable. |

| (c) | Total return assumes an investment at the common share market price at the beginning of the period indicated, reinvestment of all distributions for the period in accordance with the Fund’s dividend reinvestment plan, and sale of all shares at the closing common share market price at the end of the period indicated. Not annualized for periods less than one year, if applicable. |

| (d) | Portfolio turnover is not annualized for periods less than one year, if applicable. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | |

| 18 | | Invesco High Income 2024 Target Term Fund |

Notes to Financial Statements

February 28, 2023

NOTE 1–Significant Accounting Policies

Invesco High Income 2024 Target Term Fund (the “Fund”) is a Delaware statutory trust registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a closed-end management investment company. The Fund is classified as diversified.

The Fund’s investment objectives are to provide a high level of current income and to return $9.835 per share (the original net asset value (the “NAV”) per common share before deducting offering costs of $0.02 per share) (“Original NAV”) to common shareholders on or about December 1, 2024 (the “Termination Date”). The objective to return the Fund’s Original NAV is not an express or implied guarantee obligation of the Fund or any other entity. The Fund intends, on or about the Termination Date, to cease its investment operations, liquidate its portfolio (to the extent possible), retire or redeem its leverage facilities, if any, and distribute all its liquidated net assets to common shareholders of record unless the term is extended for one period of up to six months by a vote of the Fund’s Board of Trustees. The Fund’s ability to successfully return the Original NAV to holders of common shares on or about the Termination Date will depend on market conditions at that time and the success of various portfolio and cash flow management techniques.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance in accordance with Financial Accounting Standards Board Accounting Standards Codification Topic 946, Financial Services – Investment Companies.

The following is a summary of the significant accounting policies followed by the Fund in the preparation of its financial statements.

| A. | Security Valuations - Securities, including restricted securities, are valued according to the following policy. |

Fixed income securities (including convertible debt securities) generally are valued on the basis of prices provided by independent pricing services. Prices provided by the pricing service may be determined without exclusive reliance on quoted prices, and may reflect appropriate factors such as institution-size trading in similar groups of securities, developments related to specific securities, dividend rate (for unlisted equities), yield (for debt obligations), quality, type of issue, coupon rate (for debt obligations), maturity (for debt obligations), individual trading characteristics and other market data. Pricing services generally value debt obligations assuming orderly transactions of institutional round lot size, but a fund may hold or transact in the same securities in smaller, odd lot sizes. Odd lots often trade at lower prices than institutional round lots, and their value may be adjusted accordingly. Debt obligations are subject to interest rate and credit risks. In addition, all debt obligations involve some risk of default with respect to interest and/or principal payments.

A security listed or traded on an exchange is generally valued at its trade price or official closing price that day as of the close of the exchange where the security is principally traded, or lacking any trades or official closing price on a particular day, the security may be valued at the closing bid price on that day. Securities traded in the over-the-counter market are valued based on prices furnished by independent pricing services or market makers. When such securities are valued using prices provided by an independent pricing service they may be considered fair valued. Futures contracts are valued at the daily settlement price set by an exchange on which they are principally traded. U.S. exchange-traded options are valued at the mean between the last bid and asked prices from the exchange on which they are principally traded. Non-U.S. exchange-traded options are valued at the final settlement price set by the exchange on which they trade. Options not listed on an exchange and swaps generally are valued using pricing provided from independent pricing services.

Securities of investment companies that are not exchange-traded (e.g., open-end mutual funds) are valued using such company’s end-of-business-day net asset value per share.

Swap agreements are fair valued using an evaluated quote, if available, provided by an independent pricing service. Evaluated quotes provided by the pricing service are valued based on a model which may include end-of-day net present values, spreads, ratings, industry, company performance and returns of referenced assets. Centrally cleared swap agreements are valued at the daily settlement price determined by the relevant exchange or clearinghouse.

Deposits, other obligations of U.S. and non-U.S. banks and financial institutions are valued at their daily account value.

Foreign securities’ (including foreign exchange contracts) prices are converted into U.S. dollar amounts using the applicable exchange rates as of the close of the New York Stock Exchange (“NYSE”). If market quotations are available and reliable for foreign exchange-traded equity securities, the securities will be valued at the market quotations. Invesco Advisers, Inc. (the “Adviser” or “Invesco”) may use various pricing services to obtain market quotations as well as fair value prices. Because trading hours for certain foreign securities end before the close of the NYSE, closing market quotations may become not representative of market value in the Adviser’s judgment (“unreliable”). If, between the time trading ends on a particular security and the close of the customary trading session on the NYSE, a significant event occurs that makes the closing price of the security unreliable, the Adviser may fair value the security. If the event is likely to have affected the closing price of the security, the security will be valued at fair value in good faith in accordance with Board- approved policies and related Adviser procedures (“Valuation Procedures”). Adjustments to closing prices to reflect fair value may also be based on a screening process of an independent pricing service to indicate the degree of certainty, based on historical data, that the closing price in the principal market where a foreign security trades is not the current value as of the close of the NYSE. Foreign securities’ prices meeting the degree of certainty that the price is not reflective of current value will be priced at the indication of fair value from the independent pricing service. Multiple factors may be considered by the independent pricing service in determining adjustments to reflect fair value and may include information relating to sector indices, American Depositary Receipts and domestic and foreign index futures. Foreign securities may have additional risks including exchange rate changes, potential for sharply devalued currencies and high inflation, political and economic upheaval, the relative lack of issuer information, relatively low market liquidity and the potential lack of strict financial and accounting controls and standards.

Unlisted securities will be valued using prices provided by independent pricing services or by another method that the Adviser, in its judgment, believes better reflects the security’s fair value in accordance with the Valuation Procedures.

Securities for which market prices are not provided by any of the above methods may be valued based upon quotes furnished by independent sources. The last bid price may be used to value equity securities. The mean between the last bid and asked prices may be used to value debt obligations, including corporate loans.

Securities for which market quotations are not readily available are fair valued by the Adviser in accordance with the Valuation Procedures. If a fair value price provided by a pricing service is unreliable, the Adviser will fair value the security using the Valuation Procedures. Issuer specific events, market trends, bid/asked quotes of brokers and information providers and other market data may be reviewed in the course of making a good faith determination of a security’s fair value.

The Fund may invest in securities that are subject to interest rate risk, meaning the risk that the prices will generally fall as interest rates rise and, conversely, the prices will generally rise as interest rates fall. Specific securities differ in their sensitivity to changes in interest rates depending on their individual characteristics. Changes in interest rates may result in increased market volatility, which may affect the value and/or liquidity of certain Fund investments.

Valuations change in response to many factors including the historical and prospective earnings of the issuer, the value of the issuer’s assets, general market conditions which are not specifically related to the particular issuer, such as real or perceived adverse economic conditions, changes in the general outlook for revenues or corporate earnings, changes in interest or currency rates, regional or global instability, natural or environmental disasters, widespread disease or other public health issues, war, acts of terrorism, significant governmental actions or adverse investor sentiment generally and market liquidity. Because of the inherent uncertainties of valuation, the values reflected in the financial statements may materially differ from the value received upon actual sale of those investments.

The price the Fund could receive upon the sale of any investment may differ from the Adviser’s valuation of the investment, particularly for securities that are valued using a fair valuation technique. When fair valuation techniques are applied, the Adviser uses available information, including both observable and unobservable inputs and assumptions, to determine a methodology that will result in a valuation that the Adviser believes approximates market value. Fund securities that are fair valued may be subject to greater fluctuation in their value from one day to the next than would be the case if market quotations were used.

| | |

| 19 | | Invesco High Income 2024 Target Term Fund |

Because of the inherent uncertainties of valuation, and the degree of subjectivity in such decisions, the Fund could realize a greater or lesser than expected gain or loss upon the sale of the investment.