| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206705-08 | ||

April 24, 2017

FREE WRITING PROSPECTUS

STRUCTURAL AND COLLATERAL TERM SHEET

$900,450,312

(Approximate Total Mortgage Pool Balance)

$745,291,000

(Approximate Offered Certificates)

CD 2017-CD4 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

German American Capital Corporation

Citi Real Estate Funding Inc.

Citigroup Global Markets Realty Corp.

Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | Citigroup |

| Co-Lead Managers and Joint Bookrunners | |

| J.P. Morgan | Academy Securities |

| Co-Managers | |

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-206705) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

CD 2017-CD4 Mortgage Trust

Capitalized terms used but not defined herein have the meanings assigned to them in the Preliminary Prospectus expected to be dated April 25, 2017 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

|

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | ||

| Co-Lead Managers and Joint Bookrunners: | Deutsche Bank Securities Inc. and Citigroup Global Markets Inc. | |

| Co-Managers: | J.P. Morgan Securities LLC and Academy Securities, Inc. | |

| Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (64.5%), Citi Real Estate Funding Inc. (“CREFI”) (32.5%) and Citigroup Global Markets Realty Corp. (“CGMRC”) (3.0%)*An indirect wholly owned subsidiary of Deutsche Bank AG | |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association | |

| Operating Advisor: | Park Bridge Lender Services LLC | |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC | |

| Special Servicer: | Rialto Capital Advisors, LLC | |

| Trustee and Certificate Administrator: | Wells Fargo Bank, National Association | |

| Rating Agencies: | Moody’s Investors Service, Inc., S&P Global Ratings, a Standard & Poor’s Financial Services LLC business, Fitch Ratings, Inc. and DBRS, Inc. | |

| Risk Retention Consultation Parties: | Deutsche Bank AG, New York Branch (“DBNY”) and CREFI | |

| U.S. Credit Risk Retention | This securitization transaction will be subject to the credit risk retention rules of Section 15G of the Securities Exchange Act of 1934, as amended. An economic interest in the credit risk of the mortgage loans in this transaction is expected to be retained pursuant to Regulation RR promulgated under Section 15G (“Regulation RR”), as an “eligible vertical interest” in the form of the VRR Interest. GACC will act as retaining sponsor under Regulation RR and is expected on the closing date to (i) offset a portion of its risk retention obligation by transferring approximately 67.53% of the VRR Interest to a “majority-owned affiliate”, DBNY, an originator, and (ii) offset the remaining portion of its risk retention obligation by transferring approximately 32.47% of the VRR Interest to CREFI, an originator, a sponsor, and a mortgage loan seller (which portion of the VRR Interest CREFI is expected to transfer to a “majority-owned affiliate”, CGMRC, a sponsor and a mortgage loan seller). For a discussion of the manner in which the credit risk retention requirements are expected to be satisfied by GACC, as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. | |

| Determination Date: | 6thday of each month, or if such 6th day is not a business day, the immediately following business day, commencing in June 2017. | |

| Distribution Date: | 4thbusiness day following the Determination Date in each month, commencing in June 2017. | |

| Cut-off Date: | With respect to each mortgage loan, the later of the related payment date of such mortgage loan in May 2017 (or, in the case of any mortgage loan that has its first payment date after May 2017, the date that would have been its payment date in May 2017 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) and the related origination date. Unless otherwise noted, all Mortgage Loan statistics are based on balances as of the Cut-off Date. | |

| Closing Date: | On or about May 17, 2017 | |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. | |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. | |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. | |

| Day Count: | 30/360 | |

| Tax Treatment: | REMIC | |

| Rated Final Distribution Date: | May 2050 | |

| Minimum Denominations: | $10,000 and in each case in multiples of $1 thereafter. | |

| Clean-up Call: | 1% (with certain exceptions described under“Pooling and Servicing Agreement—Termination; Retirement of Certificates”in the Preliminary Prospectus) | |

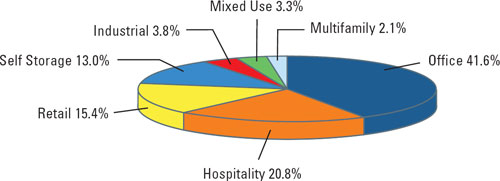

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

CD 2017-CD4 Mortgage Trust |

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance | |

| German American Capital Corporation | 29 | 31 | $581,181,544 | 64.5% | |

| Citi Real Estate Funding Inc. | 16 | 20 | $292,345,006 | 32.5% | |

| Citigroup Global Markets Realty Corp. | 2 | 2 | $26,923,763 | 3.0% | |

| Total: | 47 | 53 | $900,450,312 | 100.0% | |

Pooled Collateral Facts: | |||||

| Initial Outstanding Pool Balance: | $900,450,312 | ||||

| Number of Mortgage Loans: | 47 | ||||

| Number of Mortgaged Properties: | 53 | ||||

| Average Mortgage Loan Cut-off Date Balance: | $19,158,517 | ||||

| Average Mortgaged Property Cut-off Date Balance: | $16,989,629 | ||||

| Weighted Average Mortgage Rate: | 4.6647% | ||||

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 114 | ||||

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 111 | ||||

| Weighted Average Mortgage Loan Seasoning (months): | 3 | ||||

| % of Mortgaged Properties Leased to a Single Tenant: | 19.1% | ||||

Credit Statistics(1): | |||||

| Weighted Average Mortgage Loan U/W NCF DSCR(2): | 1.95x | ||||

| Weighted Average Mortgage Loan Cut-off Date LTV(3)(4): | 57.1% | ||||

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(3): | 50.9% | ||||

| Weighted Average U/W NOI Debt Yield(4): | 11.8% | ||||

Amortization Overview: | |||||

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 27.1% | ||||

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD: | 28.4% | ||||

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 44.5% | ||||

| Weighted Average Remaining Amortization Term (months)(5): | 356 | ||||

Loan Structural Features: | |||||

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 85.8% | ||||

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(6): | 67.6% | ||||

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 26.5% | ||||

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(7): | 70.7% | ||||

| % Mortgage Loans with Upfront Engineering Reserves: | 40.0% | ||||

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 68.5% | ||||

| % Mortgage Loans with In Place Hard Lockboxes: | 66.3% | ||||

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.05x: | 92.9% | ||||

| % of Mortgage Loans with Cash Traps Triggered at Debt Yield ≥ 7.0%: | 6.3% | ||||

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 89.4% | ||||

| Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 4.3% | ||||

| Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with Defeasance or a Yield Maintenance Charge: | 6.3% | ||||

| (1) | With respect to the 95 Morton Street Mortgage Loan, Moffett Place Google Mortgage Loan, Hilton Hawaiian Village Mortgage Loan, Uovo Art Storage Mortgage Loan, Key Center Cleveland Mortgage Loan, 111 Livingston Street Mortgage Loan and Hamilton Crossing Mortgage Loan, the LTV, DSCR and Debt Yield calculations include any relatedpari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to the Moffett Place Google Mortgage Loan, the U/W NCF DSCR is calculated based on the aggregate debt service of the 12-month period commencing February 2022 of the respective mortgage loan and the relatedpari passu companion loans as set forth in the respective non-standard amortization schedule set forth in Annex F to the Preliminary Prospectus. |

| (3) | With respect to the 95 Morton Street Mortgage Loan, the Moffett Place Google Mortgage Loan, the Los Angeles Corporate Center Mortgage Loan and the Malibu Office Mortgage Loan in aggregate, collectively representing approximately 26.7% of the Initial Outstanding Pool Balance, the Cut-off Date LTVs and Maturity Date or ARD LTVs have been calculated based on the “As Stabilized” appraised value. With respect to the Midwest Embassy Suites Portfolio Mortgage Loan and the Key Center Cleveland Mortgage Loan, in aggregate, representing approximately 10.6% of the Initial Outstanding Pool Balance, the Cut-off Date LTVs and Maturity Date or ARD LTVs have been calculated based on the “As Complete” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (4) | With respect to the Amsdell Gateway Self Storage Mortgage Loan representing approximately 0.5% of the Initial Outstanding Pool Balance, the Cut-off Date LTV and U/W NOI Debt Yield are calculated based on the Cut-off Balance net of a related holdback reserve. |

| (5) | Excludes loans which are interest only for the full loan term. |

| (6) | Includes FF&E Reserves. |

| (7) | Represents the percent of the allocated Initial Outstanding Pool Balance of office, retail, mixed use and industrial properties only. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/S&P/Fitch/DBRS) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination | Weighted Average Life (years)(5) | Principal Window (months)(5) | Certificate Principal to Value Ratio(6) | Underwritten NOI Debt Yield(7) |

| Class A-1 | Aaa(sf)/AAA(sf)/AAAsf/AAA(sf) | $28,964,000 | 30.000%(8) | 3.00 | 1 – 59 | 40.0% | 16.9% |

| Class A-2 | Aaa(sf)/AAA(sf)/AAAsf/AAA(sf) | $90,250,000 | 30.000%(8) | 4.90 | 59 – 59 | 40.0% | 16.9% |

| Class A-SB | Aaa(sf)/AAA(sf)/AAAsf/AAA(sf) | $53,102,000 | 30.000%(8) | 7.36 | 59 – 116 | 40.0% | 16.9% |

| Class A-3 | Aaa(sf)/AAA(sf)/AAAsf/AAA(sf) | $192,000,000 | 30.000%(8) | 9.52 | 103 – 116 | 40.0% | 16.9% |

| Class A-4 | Aaa(sf)/AAA(sf)/AAAsf/AAA(sf) | $234,483,000 | 30.000%(8) | 9.77 | 116 – 119 | 40.0% | 16.9% |

| Class X-A(9) | Aa1(sf)/AA+(sf)/AAAsf/AAA(sf) | $669,372,000(10) | N/A | N/A | N/A | N/A | N/A |

| Class A-M | Aa2(sf)/AA+(sf)/AAAsf/AAA(sf) | $70,573,000 | 21.750% | 9.90 | 119 – 119 | 44.7% | 15.1% |

| Class B | NR/AA-(sf)/AA-sf/AA(high)(sf) | $36,355,000 | 17.500% | 9.90 | 119 – 119 | 47.1% | 14.3% |

| Class C | NR/A-(sf)/A-sf/A(high)(sf) | $39,564,000 | 12.875% | 9.90 | 119 – 119 | 49.7% | 13.5% |

NON-OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/S&P/Fitch/DBRS) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination Levels(4) | Weighted Average Life (years)(5) | Principal Window (months)(5) | Certificate Principal to Value Ratio(6) | Underwritten NOI Debt Yield(7) | |

| Class X-B(9) | NR/A-(sf)/A-sf/AA(low)(sf) | $75,919,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-D(9) | NR/NR/BBB-sf/BBB(high)(sf) | $44,910,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-E(9) | NR/NR/BB-sf/BBB(low)(sf) | $21,386,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-F(9) | NR/NR/B-sf/BB(sf) | $8,554,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-G(9) | NR/NR/NR/NR | $35,286,789(10) | N/A | N/A | N/A | N/A | N/A | |

| Class D | NR/NR/BBB-sf/BBB(sf) | $44,910,000 | 7.625% | 9.90 | 119 – 119 | 52.7% | 12.8% | |

| Class E | NR/NR/BB-sf/BB(high)(sf) | $21,386,000 | 5.125% | 9.90 | 119 – 120 | 54.2% | 12.4% | |

| Class F | NR/NR/B-sf/BB(low)(sf) | $8,554,000 | 4.125% | 9.98 | 120 – 120 | 54.7% | 12.3% | |

| Class G | NR/NR/NR/NR | $35,286,789 | 0.000% | 9.98 | 120 – 120 | 57.1% | 11.8% | |

NON-OFFERED VERTICAL RISK RETENTION INTEREST

| Non-Offered Eligible Vertical Interest | Ratings (Moody’s/S&P/Fitch/DBRS) | Initial Retained Certificate Balance or Notional Amount(3) | Initial Subordination | Weighted Average Life (years)(5) | Principal Window (months)(5) | Certificate Principal to Value Ratio(6) | Underwritten NOI Debt Yield(7) |

| VRR Interest(11) | NR/NR/NR/NR | $45,022,522 | N/A | 8.86 | 1 – 120 | N/A | N/A |

| (1) | The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates (the “Principal Balance Certificates”) will equal one of: (i) a fixedper annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related Distribution Date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the rate specified in clause (ii) or (iv) the rate specified in clause (ii) less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. |

| (3) | On the Closing Date, the certificates with the initial Certificate Balances or Notional Amounts set forth in the table under “Initial Retained Certificate Balance or Notional Amount” are expected to be sold directly from the depositor to DBNY and CREFI as described in“Credit Risk Retention” in the Preliminary Prospectus. |

| (4) | The initial subordination levels are calculated based on the initial Certificate Balance. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Non-Risk Retained Certificates (exclusive of the Class X, Class S and Class R certificates), on the other hand,pro rata in accordance with their respective outstanding certificate balances. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| (5) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of certificates with a Certificate Balance is based on (i) modeling assumptions described in the Preliminary Prospectus, (ii) assumptions that there are no prepayments, delinquencies or losses on the mortgage loans and (iii) assumptions that there are no extensions of maturity dates and mortgage loans with anticipated repayment dates, if any, are repaid on the respective anticipated repayment dates. |

| (6) | “Certificate Principal to Value Ratio” for any class with a Certificate Balance is calculated as the product of (a) the weighted average Mortgage Loan Cut-off Date LTV of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of certificates and all other classes with a Certificate Balance, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (7) | “Underwritten NOI Debt Yield” for any class with a Certificate Balance is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all certificates and the denominator of which is the total initial Certificate Balance of the related class of certificates and all other classes with a Certificate Balance, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (8) | The initial subordination levels for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates are represented in the aggregate. |

| (9) | As further described in the Preliminary Prospectus, the pass-through rate applicable to the Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates (collectively, the Class X Certificates”) for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs over (ii)(A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M certificates (based on their Certificate Balances), (B) with respect to the Class X-B certificates, the pass-through rates of the Class B and Class C certificates, (C) with respect to the Class X-D certificates, the pass-through rate of the Class D certificates, (D) with respect to the Class X-E certificates, the pass-through rate of the Class E certificates, (E) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates and (F) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates. |

| (10) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A certificates will be calculated by reference to a notional amount equal to the sum of the Certificate Balances of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M certificates. The interest accrual amounts on the Class X-B certificates will be calculated by reference to a notional amount equal to the sum of the Certificate Balances of the Class B and Class C certificates. The interest accrual amounts on the Class X-D certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class D certificates. The interest accrual amounts on the Class X-E certificates will be calculated by reference to a notional amount equal to the Certificate |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Balance of the Class E certificates. The interest accrual amounts on the Class X-F certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class F certificates. The interest accrual amounts on the Class X-G certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class G certificates. The notional amount of each class of the Class X Certificates is subject to change depending upon the final pricing of the Principal Balance Certificates, as follows: (1) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates whose certificate balance comprises such notional amount is equal to the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), the certificate balance of such class of Principal Balance Certificates may not be part of, and reduce accordingly, such notional amount of the related Class X Certificates (or, if as a result of such pricing the pass-through rate of the related Class X Certificates is equal to zero, such Class X Certificates may not be issued on the Closing Date), and/or (2) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates that does not comprise such notional amount of the related Class X Certificates is equal to less than the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), such class of Principal Balance Certificates may become a part of, and increase accordingly, such notional amount of the related Class X Certificates. |

| (11) | German American Capital Corporation, as the retaining sponsor, is expected to purchase from the depositor, on the Closing Date, an “eligible vertical interest” (as such term is defined in Regulation RR, the “VRR Interest”) in the form of a single vertical security with an aggregate initial certificate balance of approximately $45,022,522, which is expected to represent approximately 5.0% of the aggregate initial certificate balance of all of the ABS interests issued by the issuing entity The VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. The VRR Interest is a class of certificates. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Class A-2 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

| A-2 | CREFI | 95 Morton Street | Office | $95,000,000 | 59 | 42.6% | 2.34x | 10.7% | |

| (1) | This table reflects the Mortgage Loan whose balloon payments will be applied to pay down the Class A-2 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Allocation between VRR Interest and the Non-Risk Retained Certificates: | The aggregate amount available for distribution to holders of the certificates (including the VRR Interest) on each Distribution Date will be: (i) the gross amount of interest, principal, yield maintenance charges and prepayment premiums collected with respect to the Mortgage Loans in the applicable one-month collection period, net of specified expenses of the issuing entity, including fees payable therefrom to, and losses, liabilities, costs and expenses reimbursable or indemnifiable therefrom to, the Master Servicer, the Special Servicer, the Certificate Administrator, the Trustee, the Operating Advisor, the Asset Representations Reviewer and CREFC®; and (ii) allocated to amounts available for distribution to the holders of the VRR Interest, on the one hand, and amounts available for distribution to the holders of the remaining certificates (the “Non-Risk Retained Certificates”), on the other hand. On each Distribution Date, the portion of such aggregate available funds allocable to: (a) the VRR Interest will be the product of such aggregate available funds multiplied by a fraction, expressed as a percentage, the numerator of which is the initial Certificate Balance of the VRR Interest, and the denominator of which is the aggregate initial Certificate Balances of the Principal Balance Certificates and the initial Certificate Balance of the VRR interest (the “Risk Retained Percentage”); and (b) the Non-Risk Retained Certificates will at all times be the product of such aggregate available funds multiplied by the difference between 100% and the Risk Retained Percentage (such difference, the “Non-Risk Retained Percentage”). See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus.

| ||||

| Principal Payments: | Payments in respect of the Non-Risk Retained Percentage of principal on the Non-Risk Retained Certificates will be distributed,first, to the Class A-SB certificates, until the Certificate Balance of such class is reduced to the planned principal balance for the related Distribution Date set forth on Annex E to the Preliminary Prospectus,then, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates, in that order until the Certificate Balance of each such class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the certificates will be distributed,first, to the Class A-1, Class A-2, Class A-SB, Class A-3, and Class A-4 certificates, on apro rata basis, based on the Certificate Balance of each such class,then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates, in that order, in each case until the Certificate Balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed).

Each class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M certificates; (ii) the notional amount of the Class X-B certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C certificates; (iii) the notional amount of the Class X-D certificates will be reduced by the principal distributions and realized losses allocated to the Class D certificates; (iv) the notional amount of the Class X-E certificates will be reduced by the principal distributions and realized losses allocated to the Class E certificates; (v) the notional amount of the Class X-F certificates will be reduced by the principal distributions and realized losses allocated to the Class F certificates and (vi) the notional amount of the Class X-G certificates will be reduced by the principal distributions and realized losses allocated to the Class G certificates.

| ||||

| Interest Payments: | On each Distribution Date, interest accrued for each class of the Non-Risk Retained Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of the Non-Risk Retained Percentage of the aggregate available funds (exclusive of any portion thereof that represents the Non-Risk Retained Percentage of (i) any yield maintenance charges and prepayment premiums and/or (ii) any excess interest accrued after the related anticipated repayment date on any mortgage loan with an anticipated repayment date):first, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates, on apro rata basis, based on the accrued and unpaid interest on each such class andthen, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates, in that order, in each case until the interest payable to each such class is paid in full. | ||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates for each Distribution Date will equal one of: (i) a fixedper annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the rate specified in clause, (ii) or (iv) the rate specified in clause (ii) less a specified rate.

As further described in the Preliminary Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M certificates (based on their Certificate Balances), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rate of the Class B and Class C certificates, (C) with respect to the Class X-D certificates, the pass-through rate of the Class D certificates, (D) with respect to the Class X-E certificates, the pass-through rate of the Class E certificates, (E) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates and (F) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates.

| |||||

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocatedpro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates.

| ||||

| Loss Allocation: | The Non-Risk Retained Percentage of losses will be allocated to each class of Non-Risk Retained Certificates entitled to principal in reverse alphabetical order starting with Class G through and including Class A-M andthen to Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates on apro ratabasis based on the Certificate Balance of each such class. The notional amount of any class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the class(es) of certificates that are component(s) of the notional amount of such class of Class X Certificates.

| ||||

Prepayment Premiums:

| A percentage of the Non-Risk Retained Percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C and Class D certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G certificates on such Distribution Date, and (b) a fraction (expressed as a percentage which can be no greater than 100% nor less than 0%), the numerator of which is the excess of the pass-through rate of each such class of certificates currently receiving principal over the relevant Discount Rate, and the denominator of which is the excess of the Mortgage Rate of the related Mortgage Loan over the relevant Discount Rate.

Prepayment Premium Allocation Percentage for all YM P&I Certificates =

| ||||

| (Pass-Through Rate - Discount Rate) | X | The percentage of the principal distribution amount to such class as described in (a) above | ||

| (Mortgage Rate - Discount Rate) | |||||

The remaining percentage of the Non-Risk Retained Percentage of the prepayment premiums will be allocated to the Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates in the manner described in the Preliminary Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates as Discount Rates decrease and a decrease in the percentage allocated to such classes as Discount Rates rise. | |||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

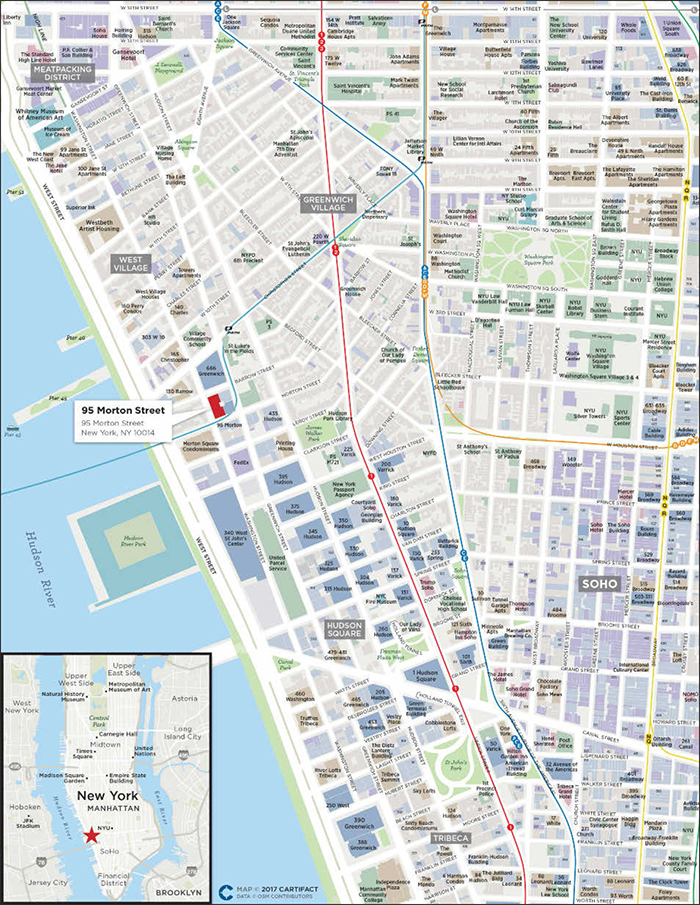

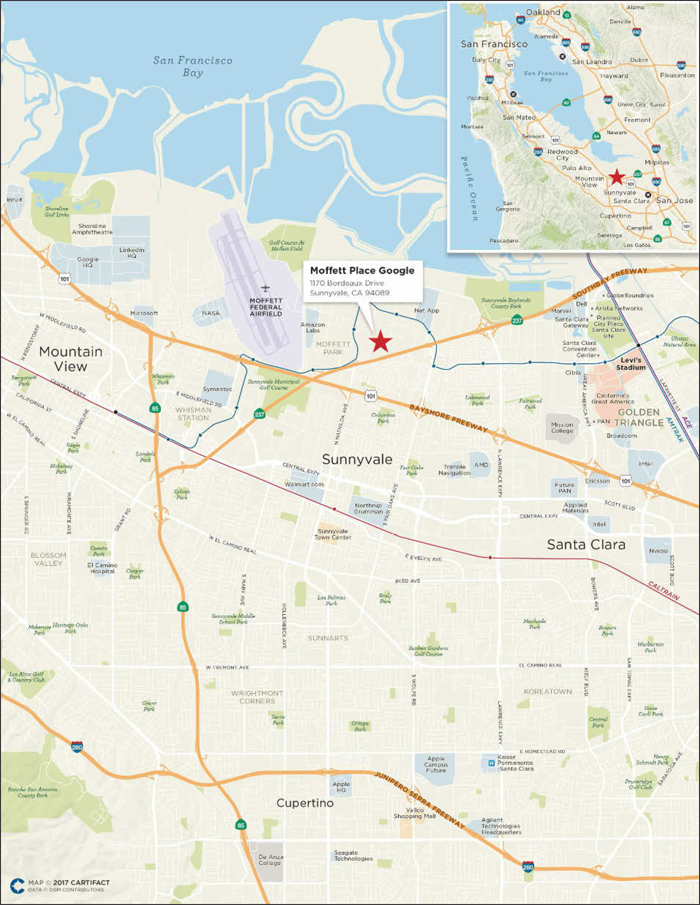

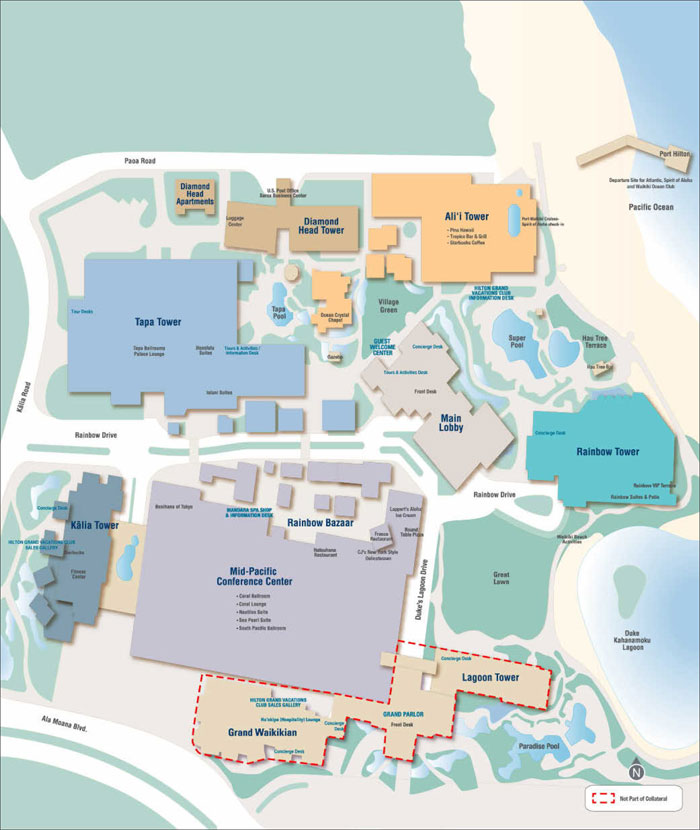

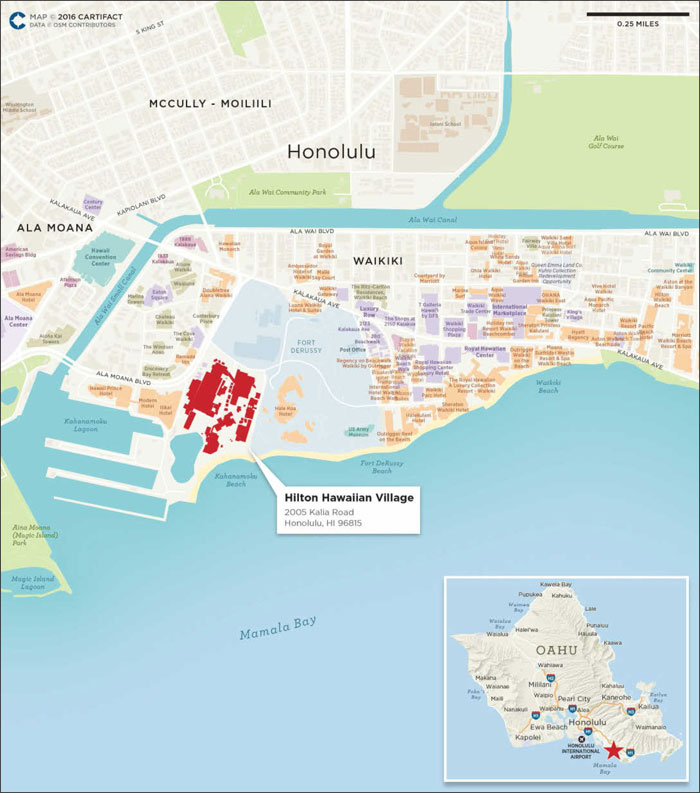

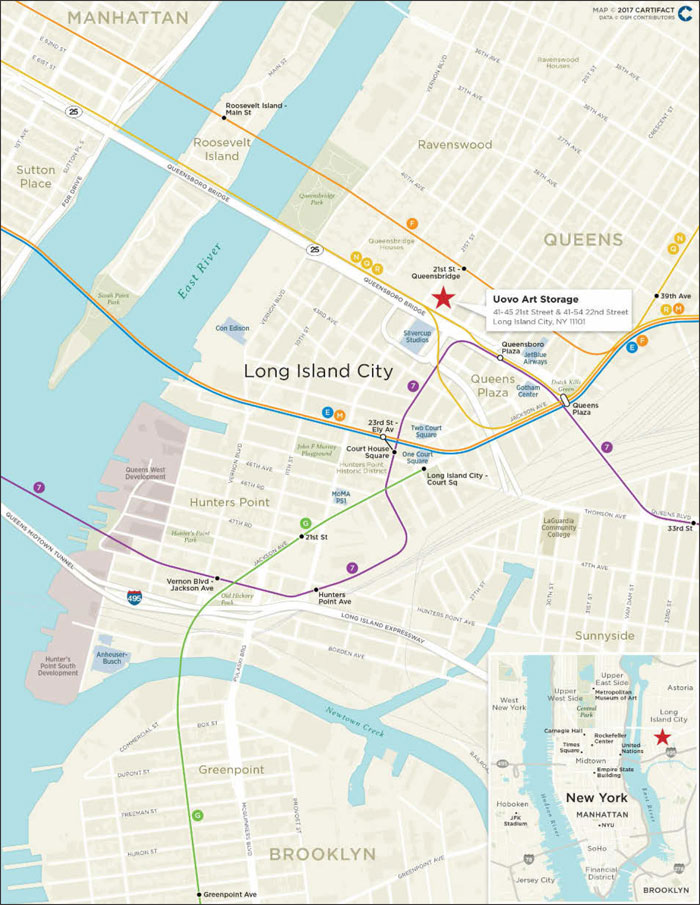

| Whole Loans: | The mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Moffett Place Google, Hilton Hawaiian Village, Uovo Art Storage, Key Center Cleveland, 111 Livingston Street and Hamilton Crossing, each secure both a mortgage loan to be included in the trust fund and one or more other companion loans that will not be included in the trust fund, each of which will bepari passu and/or subordinate in right of payment with the mortgage loan included in the trust fund. We refer to each such group of related loans as a “whole loan”.

The Moffett Place Google whole loan and the 111 Livingston Street whole loan will be principally serviced under the pooling and servicing agreement for the CD 2017-CD3 securitization. The Hilton Hawaiian Village whole loan will be principally serviced under the pooling and servicing agreement for the Hilton USA Trust 2016 HHV securitization. The Uovo Art Storage whole loan will be principally serviced under the pooling and servicing agreement for this securitization. The Key Center Cleveland whole loan and the Hamilton Crossing whole loan will be principally serviced under the pooling and servicing agreement for the CGCMT 2017-P7 securitization.

As of the Closing Date, thepari passu companion loans or the subordinate companion loans in the whole loans are expected to be held by the party identified below under “Companion Loan Summary”.

| ||||

| Control Rights and Directing Certificateholder: | Controlling Class Certificateholders will generally have certain control rights over servicing matters with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. The majority owner or appointed representative of the class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Certificateholder”) will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. Furthermore, the Directing Certificateholder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans.

It is expected that RREF III-D AIV RR, LLC or another affiliate of Rialto Capital Advisors, LLC will be the initial Directing Certificateholder with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans.

For a description of the directing holder for each Non-Serviced Whole Loan, see“Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement—The Directing Certificateholder”in the Preliminary Prospectus.

| ||||

| Control Eligible Certificates: | Class E, Class F and Class G certificates.

| ||||

| Controlling Class: | The Controlling Class will be the most subordinate class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any appraisal reduction amounts and any collateral deficiency amounts allocable to such class, equal to at least 25% of the initial Certificate Balance of such class;provided that if at any time the Certificate Balances of all Control Eligible Certificates, as notionally reduced by any appraisal reduction amounts (but without regard to any collateral deficiency amounts) allocable to such classes, have been reduced to zero, then the “Controlling Class” will be the most subordinate class of Control Eligible Certificates that has an aggregate principal balance greater than zero;provided,further that if at any time the Certificate Balances of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C and Class D certificates have been reduced to zero as a result of the allocation of principal payments on the Mortgage Loans, then the “Controlling Class” will be the most subordinate class of Control Eligible Certificates that has an aggregate Certificate Balance greater than zero (without regard to the application of appraisal reduction amounts or any collateral deficiency amounts to notionally reduce the Certificate Balance of such class).

The Controlling Class as of the Closing Date will be the Class G certificates.

| ||||

| Appraised-Out Class: | Any class of Control Eligible Certificates that has been determined, as a result of appraisal reductions amounts and collateral deficiency amounts allocable to such class, to no longer be the Controlling Class.

| ||||

| |||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Remedies Available to Holders of an Appraised-Out Class: | Holders of the majority of any class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of appraisal reduction amounts and collateral deficiency amounts in respect of such class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Serviced Mortgage Loan for which an Appraisal Reduction Event has occurred or as to which there exists a collateral deficiency amount. Upon receipt of the second appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of the second appraisal, a recalculation of the appraisal reduction amount or collateral deficiency amount is warranted. If warranted, the Special Servicer will direct the Master Servicer to recalculate the appraisal reduction amount or collateral deficiency amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised-Out Class as the Controlling Class. The Holders of an Appraised-Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the class is reinstated as the Controlling Class.

| ||||

| Control Termination Event: | Will occur when (i) the Class E certificates have a Certificate Balance (taking into account the application of any appraisal reduction amounts and collateral deficiency amounts to notionally reduce the Certificate Balance of such class) of less than 25% of the initial Certificate Balance of that class or (ii) a holder of the Class E certificates is the majority Controlling Class Certificateholder and has irrevocably waived its right, in writing, to exercise any of the rights of the Controlling Class Certificateholder and such rights have not been reinstated to a successor Controlling Class Certificateholder (subject to “—Controlling Class” above).

Upon the occurrence and the continuance of a Control Termination Event, the Directing Certificateholder will no longer have any control rights. The Directing Certificateholder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans.

Upon the occurrence and continuation of a Control Termination Event, the Directing Certificateholder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans. Such consultation rights will continue until the occurrence of a Consultation Termination Event.

| ||||

| Consultation Termination Event: | Will occur when (i) there is no class of Control Eligible Certificates that has a then-outstanding Certificate Balance at least equal to 25% of the initial Certificate Balance of such class, in each case, without regard to the application of any appraisal reduction amounts and collateral deficiency amounts; or (ii) a holder of the Class E certificates is the majority Controlling Class Certificateholder and has irrevocably waived its right, in writing, to exercise any of the rights of the Controlling Class Certificateholder and such rights have not been reinstated to a successor Controlling Class Certificateholder (subject to “—Controlling Class” above).

Upon the occurrence and continuance of a Consultation Termination Event, the Directing Certificateholder will have no rights under the PSA other than those rights that all Certificateholders have.

| ||||

| Risk Retention Consultation Parties: | Each risk retention consultation party will have certain non-binding consultation rights with respect to certain material servicing actions. The holder (or group of affiliated holders) of the majority of each of the respective portions of the VRR Interest transferred on the Closing Date by GACC to DBNY and CREFI (by Certificate Balance) will be entitled to appoint a risk retention consultation party. DBNY and CREFI are expected to be appointed as the initial risk retention consultation parties.

| ||||

| Appointment and Replacement of Special Servicer: | The Directing Certificateholder will appoint the initial Special Servicer with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans as of the Closing Date. Prior to the occurrence and continuance of a Control Termination Event, the Directing Certificateholder generally may replace the Special Servicer with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans with or without cause at any time.

Upon the occurrence and during the continuance of a Control Termination Event, the Directing Certificateholder will no longer have the right to replace the Special Servicer and such | ||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

replacement (other than with respect to the Non-Serviced Whole Loans) will occur based on a vote of holders of all voting eligible classes of certificates as described below. See “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Whole Loans.

| |||||

| Replacement of Special Servicer by Vote of Certificateholders: | Other than with respect to Non-Serviced Whole Loans, if a Control Termination Event has occurred and is continuing, upon (i) the written direction of holders of certificates evidencing not less than 25% of the voting rights of all classes of certificates entitled to principal (taking into account the application of appraisal reduction amounts to notionally reduce the Certificate Balances of classes to which such appraisal reduction amounts are allocable) requesting a vote to replace the Special Servicer with a replacement special servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator and Trustee of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the certificates, the Certificate Administrator will be required to promptly post notice of such request on the Certificate Administrator’s website and concurrently provide written notice of such request by mail to all certificateholders of such request and conduct the solicitation of votes of all certificates in such regard. Upon the written direction (within 180 days) of Holders of at least 66-2/3% of a Certificateholder Quorum the Trustee will immediately replace the Special Servicer with the replacement Special Servicer (other than with respect to Non-Serviced Whole Loans).

“Certificateholder Quorum” means, in connection with any solicitation of votes in connection with the replacement of the Special Servicer as described above or the Asset Representations Reviewer as described below, the holders of certificates evidencing at least 50% of the aggregate voting rights (taking into account Realized Losses and, other than with respect to the termination of the Asset Representations Reviewer, the application of any appraisal reduction amounts to notionally reduce the Certificate Balance of the certificates) of all classes of certificates entitled to principal, on an aggregate basis.

In addition, after the occurrence of a Consultation Termination Event, if the Operating Advisor determines that the Special Servicer is not performing its duties in accordance with the Servicing Standard, the Operating Advisor will have the right to recommend the replacement of the Special Servicer (other than with respect to the Non-Serviced Whole Loans). The Operating Advisor’s recommendation to replace the Special Servicer (other than with respect Non-Serviced Whole Loans) must be confirmed by a majority of the voting rights of all classes of certificates entitled to principal (taking into account the application of appraisal reduction amounts to notionally reduce the Certificate Balances of classes to which such appraisal reduction amounts are allocable) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the certificates.

See“Description of the Mortgage Pool—The Whole Loans”and“Pooling and Servicing Agreement”in the Preliminary Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Whole Loans.

| ||||

| Cap on Workout and Liquidation Fees: | The workout fees and liquidation fees payable to a Special Servicer under the PSA will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout fee and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special servicing). In addition, the total amount of workout and liquidation fees actually payable by the Trust under the PSA will be capped in the aggregate at $1,000,000 for each related Mortgage Loan. If a new special servicer begins servicing the related Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap.

| ||||

| Special Servicer Compensation: | The special servicing fee will equal the greater of (i) 0.25%per annum of the stated principal balance of the related specially serviced loan or REO property, as applicable, and (ii) $3,500 | ||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

(or, with respect to any specially serviced loan or REO loan with respect to which the risk retention consultation parties consulted with the special servicer after the occurrence and during the continuance of a consultation termination event, $5,000 for the month in which such consultation occurred). The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration under the PSA (including, without limitation, in the form of commissions, brokerage fees, rebates, or as a result of any other fee-sharing arrangement) from any person (including, without limitation, the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Serviced Mortgage Loan and any related Serviced Companion Loans, if any, and any purchaser of any Serviced Mortgage Loan and any related Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Serviced Mortgage Loan and any related Serviced Companion Loans, the management or disposition of any REO Property, or the performance of any other special servicing duties under the PSA, other than as expressly permitted in the PSA and other than commercially reasonable treasury management fees, banking fees, customary title agent fees and insurance commissions or fees received or retained by the Special Servicer or any of its Affiliates in connection with any services performed by such party with respect to any Mortgage Loan. Subject to certain limited exceptions, the Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement.

| |||||

| Operating Advisor: | With respect to the Serviced Mortgage Loan and any related Serviced Companion Loans and prior to the occurrence of a Control Termination Event, the Operating Advisor will have access to any final asset status report and all information available with respect to the transaction on the Certificate Administrator’s website but will not have any approval or consultation rights. After the occurrence and during the continuance of a Control Termination Event, the Operating Advisor will have consultation rights with respect to certain major decisions and will have additional monitoring responsibilities on behalf of the entire trust.

The Operating Advisor will be subject to termination if holders of at least 15% of the aggregate voting rights of the certificates (in connection with termination and replacement relating to the Mortgage Loans) vote to terminate and replace the Operating Advisor and such vote is approved by holders of more than 50% of the applicable voting rights that exercise their right to vote (in the case of each of such vote and approval, taking into account Realized Losses and the application of any appraisal reduction amounts to notionally reduce the Certificate Balance of the certificates), provided that holders of at least 50% of the applicable voting rights have exercised their right to vote. The holders initiating such vote will be responsible for the fees and expenses in connection with the vote and replacement.

The Operating Advisor will not have consultation rights in respect of Non-Serviced Mortgage Loans.

| ||||

| Asset Representations Reviewer: | The Asset Representations Reviewer will be required to review certain delinquent Mortgage Loans after a specified delinquency threshold has been exceeded and the required percentage of certificateholders vote to direct a review of such delinquent Mortgage Loans. An asset review will occur when either (1) Mortgage Loans with an aggregate outstanding principal balance of 25% or more of the aggregate outstanding principal balance of all of the Mortgage Loans (including any REO loans (or a portion of any REO loan in the case of a whole loan)) held by the issuing entity as of the end of the applicable collection period are delinquent loans or (2)(A) prior to and including the second anniversary of the Closing Date, at least 10 Mortgage Loans are delinquent loans as of the end of the applicable collection period and the outstanding principal balance of such delinquent loans in the aggregate constitutes at least 15% of the aggregate outstanding principal balance of all of the Mortgage Loans (including any REO loans (or a portion of any REO loan in the case of a whole loan)) held by the issuing entity as of the end of the applicable collection period, or (B) after the second anniversary of the Closing Date, at least 15 Mortgage Loans are delinquent loans as of the end of the applicable collection period and the outstanding principal balance of such delinquent loans in the aggregate constitutes at least 20% of the aggregate outstanding principal balance of all of the Mortgage Loans (including any REO loans (or a portion of any REO loan in the case of a whole loan)) held by the issuing entity as of the end of the applicable collection period.

The Asset Representations Reviewer may be terminated and replaced without cause. Upon (i) the written direction of Certificateholders evidencing not less than 25% of the voting rights (taking into account Realized Losses, but without regard to the application of any appraisal | ||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

CD 2017-CD4 Mortgage Trust |

| STRUCTURE OVERVIEW |

reduction amounts to notionally reduce the Certificate Balance of the certificates) requesting a vote to terminate and replace the Asset Representations Reviewer with a proposed successor asset representations reviewer that is an eligible asset representations reviewer, and (ii) payment by such holders to the Certificate Administrator of the reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote, the Certificate Administrator will promptly provide notice to all Certificateholders and the Asset Representations Reviewer of such request by posting such notice on its internet website, and by mailing such notice to all Certificateholders and the Asset Representations Reviewer. Upon the written direction of Certificateholders evidencing at least 75% of a Certificateholder Quorum, the Trustee will terminate all of the rights and obligations of the Asset Representations Reviewer under the PSA by written notice to the Asset Representations Reviewer, and the proposed successor Asset Representations Reviewer will be appointed. See “Pooling and Servicing Agreement—The Asset Representations Reviewer” in the Preliminary Prospectus.

| |||||

| Dispute Resolution Provisions: | Each Mortgage Loan Seller will be subject to the dispute resolution provisions set forth in the PSA to the extent those provisions are triggered with respect to any Mortgage Loan sold to the depositor by such Mortgage Loan Seller and such Mortgage Loan Seller will be obligated under the related mortgage loan purchase agreement to comply with all applicable provisions and to take part in any mediation or arbitration proceedings that may result.

Generally, in the event that a repurchase request as described in the Preliminary Prospectus is not “Resolved” within 180 days after the related Mortgage Loan Seller receives such Repurchase Request, then the enforcing servicer will be required to send a notice to the initial requesting certificateholder (if any) indicating the enforcing servicer’s intended course of action with respect to the Repurchase Request. If (a) the enforcing servicer’s intended course of action with respect to the Repurchase Request does not involve pursuing further action to exercise rights against the related Mortgage Loan Seller with respect to the Repurchase Request and the initial requesting certificateholder, if any, or any other Certificateholder or Certificate Owner wishes to exercise its right to refer the matter to mediation (including nonbinding arbitration) or arbitration, or (b) the enforcing servicer’s intended course of action is to pursue further action to exercise rights against the related Mortgage Loan Seller with respect to the Repurchase Request but the initial requesting certificateholder, if any, or any other Certificateholder or Certificate Owner does not agree with the dispute resolution method selected by the enforcing servicer, then the initial requesting certificateholder, if any, or such other Certificateholder or Certificate Owner may deliver a written notice to the enforcing servicer indicating its intent to exercise its right to refer the matter to either mediation or arbitration.

“Resolved” means, with respect to a Repurchase Request, (i) that the related material defect has been cured, (ii) the related Mortgage Loan has been repurchased in accordance with the related mortgage loan purchase agreement, (iii) a mortgage loan has been substituted for the related Mortgage Loan in accordance with the related mortgage loan purchase agreement, (iv) the applicable Mortgage Loan Seller made the loss of value payment, (v) a contractually binding agreement is entered into between the enforcing servicer, on behalf of the issuing entity, and the related Mortgage Loan Seller that settles the related Mortgage Loan Seller’s obligations under the related mortgage loan purchase agreement, or (vi) the related Mortgage Loan is no longer property of the issuing entity as a result of a sale or other disposition in accordance with the PSA. See “Pooling and Servicing Agreement—Dispute Resolution Provisions” in the Preliminary Prospectus. | ||||

| Liquidated Loan Waterfall: | On liquidation of any Mortgage Loan, all net liquidation proceeds will be applied according to the PSA, so that amounts allocated as a recovery of accrued and unpaid interest will not, in the first instance, include (a) any amount by which the interest portion of P&I Advances previously made was reduced as a result of appraisal reduction amounts and (b) Accrued AB Loan Interest. After the adjusted interest amount is so allocated, any remaining net liquidation proceeds will be allocated to pay principal on the Mortgage Loan until the unpaid principal amount of the Mortgage Loan has been reduced to zero. Any remaining liquidation proceeds would then be allocated as a recovery of (a) accrued and unpaid interest corresponding to the amount by which the interest portion of P&I Advances previously made was reduced as a result of appraisal reduction amounts and (b) any Accrued AB Loan Interest. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

CD 2017-CD4 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date Balances(1) |

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||||

| $3,185,000 | - | $7,499,999 | 13 | $67,951,807 | 7.5% | 4.8299% | 119 | 1.76x | 63.6% | 56.6% |

| $7,500,000 | - | $14,999,999 | 15 | $164,720,033 | 18.3% | 4.7249% | 119 | 1.76x | 62.4% | 53.5% |

| $15,000,000 | - | $24,999,999 | 12 | $237,625,125 | 26.4% | 4.7638% | 117 | 1.71x | 62.0% | 55.4% |

| $25,000,000 | - | $49,999,999 | 2 | $79,803,347 | 8.9% | 4.9512% | 117 | 1.57x | 55.6% | 45.5% |

| $50,000,000 | - | $74,999,999 | 3 | $180,350,000 | 20.0% | 4.5501% | 117 | 2.74x | 50.4% | 45.5% |

| $75,000,000 | - | $95,000,000 | 2 | $170,000,000 | 18.9% | 4.3890% | 84 | 1.92x | 50.1% | 48.0% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Distribution of Mortgage Rates(1) |

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||||

| 4.1995% | - | 4.4999% | 10 | $247,084,147 | 27.4% | 4.2815% | 95 | 2.72x | 43.8% | 42.8% |

| 4.5000% | - | 4.7499% | 13 | $382,532,052 | 42.5% | 4.6603% | 117 | 1.69x | 59.6% | 53.0% |

| 4.7500% | - | 5.5000% | 24 | $270,834,112 | 30.1% | 5.0205% | 118 | 1.62x | 65.5% | 55.3% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Property Type Distribution(1)(5) |

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Number of Rooms/Units/NRA | Weighted Averages | ||||||

Cut-off Date Room/Unit/NRA | Mortgage Rate | Stated Term | Occupancy | U/W NCF DSCR(2) | Cut-off Ratio(3)(4) | Maturity Date or ARD LTV(3) | |||||

| Office | 13 | $374,941,763 | 41.6% | 2,499,123 | $357 | 4.5105% | 103 | 97.7% | 1.85x | 56.2% | 52.4% |

| CBD | 5 | $225,000,000 | 25.0% | 1,113,354 | $444 | 4.4372% | 92 | 99.0% | 1.85x | 51.6% | 49.6% |

| Suburban | 7 | $138,741,763 | 15.4% | 1,330,551 | $230 | 4.6358% | 119 | 95.5% | 1.75x | 64.2% | 57.4% |

| Medical | 1 | $11,200,000 | 1.2% | 55,218 | $203 | 4.4300% | 120 | 100.0% | 2.85x | 48.5% | 48.5% |

| Hospitality | 8 | $186,876,869 | 20.8% | 4,400 | $134,570 | 4.6845% | 116 | 81.0% | 2.84x | 49.1% | 43.7% |

| Full Service | 8 | $186,876,869 | 20.8% | 4,400 | $134,570 | 4.6845% | 116 | 81.0% | 2.84x | 49.1% | 43.7% |

| Retail | 14 | $139,104,578 | 15.4% | 1,094,823 | $229 | 4.8233% | 116 | 95.9% | 1.50x | 67.4% | 56.9% |

| Anchored(6) | 10 | $115,458,744 | 12.8% | 934,642 | $244 | 4.8143% | 116 | 96.3% | 1.49x | 66.4% | 56.4% |

| Unanchored | 4 | $23,645,834 | 2.6% | 160,181 | $156 | 4.8675% | 119 | 94.1% | 1.56x | 71.9% | 58.9% |

| Self Storage | 12 | $116,881,364 | 13.0% | 1,000,936 | $208 | 4.6870% | 118 | 82.7% | 1.70x | 54.1% | 46.5% |

| Art Storage | 2 | $64,784,716 | 7.2% | 380,130 | $275 | 4.7547% | 117 | 77.1% | 1.64x | 50.0% | 40.9% |

| Self Storage | 10 | $52,096,647 | 5.8% | 620,806 | $125 | 4.6029% | 119 | 89.8% | 1.78x | 59.2% | 53.4% |

| Industrial | 3 | $33,850,000 | 3.8% | 822,533 | $42 | 4.7586% | 119 | 100.0% | 1.62x | 66.2% | 59.5% |

| Mixed Use | 1 | $30,000,000 | 3.3% | 2,389,441 | $92 | 5.3100% | 117 | 92.9% | 1.59x | 60.8% | 49.6% |

| Office/Hospitality | 1 | $30,000,000 | 3.3% | 2,389,441 | $92 | 5.3100% | 117 | 92.9% | 1.59x | 60.8% | 49.6% |

| Multifamily | 2 | $18,795,738 | 2.1% | 282 | $66,676 | 5.0326% | 118 | 97.2% | 1.38x | 73.4% | 60.5% |

| Garden | 1 | $10,487,149 | 1.2% | 160 | $65,545 | 4.9000% | 119 | 98.8% | 1.36x | 72.3% | 59.3% |

| Mid-Rise | 1 | $8,308,589 | 0.9% | 122 | $68,103 | 5.2000% | 116 | 95.1% | 1.41x | 74.7% | 62.0% |

| 53 | $900,450,312 | 100.0% | 4.6647% | 111 | 92.0% | 1.95x | 57.1% | 50.9% | |||

Geographic Distribution(1)(5) |

| State/Location | Number of Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||

| New York | 8 | $242,992,389 | 27.0% | 4.5280% | 95 | 1.94x | 49.6% | 46.1% |

| New York City | 5 | $200,803,347 | 22.3% | 4.4612% | 90 | 1.98x | 47.7% | 45.4% |

| New York State | 3 | $42,189,042 | 4.7% | 4.8459% | 119 | 1.74x | 58.4% | 49.6% |

| California | 8 | $217,434,147 | 24.1% | 4.5586% | 118 | 1.64x | 60.9% | 55.3% |

| Southern(7) | 7 | $142,434,147 | 15.8% | 4.5633% | 119 | 1.78x | 61.6% | 55.5% |

| Northern(7) | 1 | $75,000,000 | 8.3% | 4.5498% | 116 | 1.38x | 59.5% | 54.8% |

| Ohio | 4 | $80,478,871 | 8.9% | 4.9720% | 117 | 1.91x | 56.7% | 48.3% |

| Hawaii | 2 | $74,655,000 | 8.3% | 4.3119% | 111 | 3.71x | 39.8% | 37.8% |

| Florida | 8 | $46,326,160 | 5.1% | 4.7788% | 119 | 1.44x | 70.7% | 60.3% |

| Other | 23 | $238,563,744 | 26.5% | 4.8852% | 118 | 1.82x | 64.0% | 54.9% |

| Total/Weighted Average | 53 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

CD 2017-CD4 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date LTV Ratios(1)(3)(4) |

| Range of Cut-off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 31.2% | - | 54.9% | 13 | $392,151,864 | 43.6% | 4.4608% | 103 | 2.40x | 46.1% | 43.1% |

| 55.0% | - | 59.9% | 4 | $123,894,196 | 13.8% | 4.7398% | 117 | 1.70x | 59.3% | 53.4% |

| 60.0% | - | 64.9% | 6 | $70,573,450 | 7.8% | 5.0341% | 118 | 1.71x | 62.0% | 54.5% |

| 65.0% | - | 69.9% | 13 | $205,962,980 | 22.9% | 4.7645% | 117 | 1.56x | 66.7% | 57.9% |

| 70.0% | - | 74.9% | 10 | $100,367,822 | 11.1% | 4.9169% | 118 | 1.53x | 72.5% | 60.5% |

| 75.0% | - | 75.0% | 1 | $7,500,000 | 0.8% | 4.4900% | 120 | 1.50x | 75.0% | 60.6% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Distribution of Maturity Date or ARD LTV Ratios(1)(3) |

| Range of Maturity Date or ARD LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 31.2% | - | 49.9% | 12 | $374,651,864 | 41.6% | 4.5110% | 102 | 2.43x | 46.3% | 42.3% |

| 50.0% | - | 54.9% | 9 | $207,856,017 | 23.1% | 4.7428% | 117 | 1.62x | 59.4% | 53.4% |

| 55.0% | - | 59.9% | 13 | $199,638,495 | 22.2% | 4.7962% | 117 | 1.68x | 67.2% | 58.2% |

| 60.0% | - | 64.0% | 13 | $118,303,936 | 13.1% | 4.7923% | 119 | 1.51x | 69.8% | 61.2% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Distribution of Underwritten NCF Debt Service Coverage Ratios(1) |

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||||

| 1.23x | - | 1.39x | 9 | $177,238,751 | 19.7% | 4.7306% | 116 | 1.35x | 64.2% | 57.2% |

| 1.40x | - | 1.44x | 5 | $30,429,222 | 3.4% | 5.0422% | 118 | 1.42x | 70.0% | 59.5% |

| 1.45x | - | 1.54x | 3 | $23,544,741 | 2.6% | 4.6589% | 119 | 1.47x | 69.0% | 56.1% |

| 1.55x | - | 1.99x | 19 | $364,632,599 | 40.5% | 4.8041% | 118 | 1.70x | 61.1% | 52.7% |

| 2.00x | - | 2.49x | 8 | $231,780,000 | 25.7% | 4.4776% | 94 | 2.27x | 49.3% | 46.5% |

| 2.50x | - | 2.87x | 2 | $16,200,000 | 1.8% | 4.4084% | 120 | 2.83x | 47.9% | 47.9% |

| 2.88x | - | 4.47x | 1 | $56,625,000 | 6.3% | 4.1995% | 114 | 4.47x | 31.2% | 31.2% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Original Terms to Maturity or ARD(1) |

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||||

| 60 | 1 | $95,000,000 | 10.6% | 4.2620% | 59 | 2.34x | 42.6% | 42.6% | ||

| 120 | 46 | $805,450,312 | 89.4% | 4.7122% | 117 | 1.91x | 58.8% | 51.9% | ||

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Distribution of Remaining Terms to Maturity or ARD(1) |

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||||

| 59 | - | 59 | 1 | $95,000,000 | 10.6% | 4.2620% | 59 | 2.34x | 42.6% | 42.6% |

| 103 | - | 117 | 12 | $403,512,062 | 44.8% | 4.7546% | 116 | 2.06x | 54.9% | 48.5% |

| 118 | - | 120 | 34 | $401,938,251 | 44.6% | 4.6696% | 119 | 1.76x | 62.6% | 55.3% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

CD 2017-CD4 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Underwritten NOI Debt Yields(1)(4) |

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||

| 8.1% | - | 8.9% | 9 | $194,824,437 | 21.6% | 4.6591% | 116 | 1.43x | 61.1% | 56.5% |

| 9.0% | - | 9.9% | 9 | $128,088,425 | 14.2% | 4.7328% | 118 | 1.60x | 58.0% | 49.7% |

| 10.0% | - | 12.4% | 18 | $321,067,280 | 35.7% | 4.5859% | 101 | 1.89x | 58.5% | 52.0% |

| 12.5% | - | 14.9% | 6 | $79,450,974 | 8.8% | 4.8561% | 118 | 1.94x | 60.2% | 52.1% |

| 15.0% | - | 21.2% | 5 | $177,019,196 | 19.7% | 4.6786% | 116 | 2.91x | 47.9% | 43.0% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% | ||

Amortization Types(1) |

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV Ratio(3)(4) | Maturity Date or ARD LTV(3) | ||||

| Interest Only, then Amortizing | 17 | $383,185,500 | 42.6% | 4.7457% | 117 | 1.69x | 61.7% | 54.7% |

| Interest Only | 10 | $255,605,000 | 28.4% | 4.3294% | 95 | 2.70x | 43.8% | 43.8% |

| Amortizing Balloon | 19 | $244,309,812 | 27.1% | 4.8717% | 118 | 1.62x | 62.9% | 51.6% |

| Interest Only, then Amortizing, ARD | 1 | $17,350,000 | 1.9% | 4.9000% | 119 | 1.62x | 66.3% | 58.6% |

| Total/Weighted Average | 47 | $900,450,312 | 100.0% | 4.6647% | 111 | 1.95x | 57.1% | 50.9% |

Footnotes:

| (1) | With respect to the 95 Morton Street Mortgage Loan, Moffett Place Google Mortgage Loan, Hilton Hawaiian Village Mortgage Loan, Uovo Art Storage Mortgage Loan, 111 Livingston Street Mortgage Loan, Key Center Cleveland Mortgage Loan, Hamilton Crossing Mortgage Loan, the LTV, DSCR and Debt Yield calculations include any relatedpari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to the Moffett Place Google Mortgage Loan, the U/W NCF DSCR is calculated based on the on the aggregate debt service of the 12-month period commencing February 2022 of the respective mortgage loan and the relatedpari passu companion loans as set forth in the respective non-standard amortization schedule set forth in Annex F to the Preliminary Prospectus. |

| (3) | With respect to the 95 Morton Street Mortgage Loan, the Moffett Place Google Mortgage Loan, Los Angeles Corporate Center Mortgage Loan and the Malibu Office Mortgage Loan, in aggregate, representing approximately 26.7% of the Initial Outstanding Pool Balance, the Cut-off Date LTV and Maturity Date or ARD LTV has been calculated based on the “As Stabilized” appraised value. With respect to the Midwest Embassy Suites Portfolio Mortgage Loan and the Key Center Cleveland Mortgage Loan, in aggregate, representing approximately 10.6% of the Initial Outstanding Pool Balance, the Cut-off Date LTV and Maturity Date or ARD LTV has been calculated based on the “As Complete” appraised value. For additional information please see the “Description of the Mortgage Pool — Appraised Value” in the Preliminary Prospectus. |

| (4) | With respect to the Amsdell Gateway Self Storage Mortgage Loan representing approximately 0.5% of the Initial Outstanding Pool Balance, the Cut-off Date LTV and U/W NOI Debt Yield are calculated based on the Cut-off Balance net of a related holdback reserve. |