Table of Contents

As filed with the Securities and Exchange Commission on November 24, 2020.

Registration No. 333–250838

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AbCellera Biologics Inc.

(Exact name of registrant as specified in its charter)

| British Columbia | 8731 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

2215 Yukon Street

Vancouver, BC V5Y 0A1

(604) 559-9005

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

The Corporation Trust Company

Corporation Trust Center

1209 Orange Street

Wilmington, DE 19801

(302) 658-7581

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Sam Zucker Mitchell S. Bloom James Xu Goodwin Procter LLP 601 Marshall Street Redwood City, CA 94063 (650) 752-3100 | Joseph Garcia Blake, Cassels & Graydon LLP 595 Burrard Street, Suite 2600 Vancouver, BC V7X 1L3 Canada (604) 631-3300 | Carl L. G. Hansen, Ph.D. Andrew Booth Tryn T. Stimart AbCellera Biologics Inc. 2215 Yukon Street Vancouver, BC V5Y 0A1 Canada (604) 559-9005 | Charles S. Kim Kristin VanderPas Divakar Gupta Richard Segal Cooley LLP 4401 Eastgate Mall San Diego, CA 92121 (858) 550-6000 | Shahir Guindi Trevor Scott Osler, Hoskin & Harcourt LLP Suite 1700, Guinness Tower 1055 West Hastings Street Vancouver, BC V6E 2E9 Canada (778) 785-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act

| Large Accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

CALCULATION OF REGISTRATION FEE

| ||||

| Title of each class of securities to be registered | Proposed maximum aggregate offering price(1) | Amount of registration fee(2) | ||

Common shares, no par value per share | $200,000,000 | $21,820 | ||

| ||||

| ||||

| (1) | Estimated solely for the purpose of computing the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. Includes the aggregate offering price of shares that the underwriters have the option to purchase to cover over-allotments, if any. |

| (2) | The registrant previously paid $21,820 of the registration fee with the initial filing of this registration statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 24, 2020

PRELIMINARY PROSPECTUS

Shares

Common Shares

This is the initial public offering of common shares of AbCellera Biologics Inc. We are offering of our common shares. Prior to this offering, there has been no public market for our common shares. We anticipate that the initial public offering price per share of our common shares will be between $ and $ per share. We have applied to list our common shares on the Nasdaq Global Market under the symbol “ABCL.”

We have granted the underwriters an option for a period of 30 days after the date of this prospectus to purchase up to an additional common shares from us at the initial public offering price, less underwriting discounts and commissions.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 and a “smaller reporting company” as defined in the Securities Exchange Act of 1934, as amended and, as such, have elected to take advantage of certain reduced public company reporting requirements for this prospectus and future filings. See “Prospectus Summary—Implications of Being an Emerging Growth Company and a Smaller Reporting Company.”

Investing in our common shares involves risks. See “Risk Factors” beginning on page 15.

Price to Public | Underwriting | Proceeds to | ||||

Per Share | $ | $ | $ | |||

Total | $ | $ | $ |

| (1) | See “Underwriting” for additional disclosure regarding the underwriting discounts and commissions and estimated expenses payable by us. |

Neither the Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2020.

| Credit Suisse | Stifel | Berenberg | SVB Leerink | BMO Capital Markets |

The date of this prospectus is , 2020.

Table of Contents

| Page | ||||

| 1 | ||||

| 15 | ||||

| 62 | ||||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 69 | ||||

| 71 | ||||

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | 73 | |||

MANAGEMENT’S DISCUSSIONAND ANALYSISOF FINANCIAL CONDITIONAND RESULTSOF OPERATIONS | 84 | |||

| 111 | ||||

| 153 | ||||

| 163 | ||||

| 172 | ||||

| 174 | ||||

| 178 | ||||

| 180 | ||||

| 183 | ||||

| 185 | ||||

MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONSFOR U.S. HOLDERS | 193 | |||

| 200 | ||||

| 202 | ||||

| 209 | ||||

| 209 | ||||

| 209 | ||||

| F-1 | ||||

You should rely only on the information contained in this document or to which we have referred you. Neither we nor the underwriters have authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document. Regardless of the time of delivery of this prospectus or of any sale of our common shares, the information in any free writing prospectus that we may provide you in connection with this offering is accurate only as of the date of that free writing prospectus. Our business, financial condition, results of operations and future growth prospects may have changed since those dates.

For investors outside the United States: We have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

Through and including , (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

In this prospectus, unless otherwise specified, all monetary amounts are in U.S. dollars. All references in this prospectus to “$,” “US $,” “dollars” and “USD” mean U.S. dollars. Our consolidated financial statements are presented in U.S. dollars and all references to “$” in our consolidated financial statements mean U.S. dollars. All references to “Canadian dollars” and “CAD $” mean Canadian dollars. Transactions in Canadian dollars are translated to U.S. dollars at exchange rates at the date of such transactions. Period end balances of monetary assets and liabilities in Canadian dollars are translated to U.S. dollars using the period end exchange rate.

i

Table of Contents

This summary highlights information contained in greater detail elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common shares, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes thereto appearing elsewhere in this prospectus. You should also consider, among other things, the information set forth under the sections titled “Risk Factors,” “Special Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case appearing elsewhere in this prospectus. In this prospectus, references to “AbCellera,” the “Company,” “we,” “us,” “our” and similar references refer to AbCellera Biologics Inc. and its wholly owned subsidiaries.

Overview

We believe that the surest path to a better future is through technological advancement and that the new frontier of technology lies at the interface of computation, engineering and biology. Our mission is to improve health with technologies that transform the way that antibody-based therapies are discovered. We aim to become the centralized operating system for next generation antibody discovery.

Our full-stack, artificial intelligence-, or AI, powered drug discovery platform searches and analyzes the database of natural immune systems to find antibodies that can be developed as drugs. We believe our technology increases the speed and the probability of success of therapeutic antibody discovery, including enabling discovery against targets that may otherwise be intractable. Rather than advancing our own clinical pipeline of drug candidates, we forge partnerships with drug developers of all sizes, from large cap pharmaceutical to small biotechnology companies. We empower them to move quickly, reduce cost and tackle the toughest problems in drug development. As of September 30, 2020, we had 94 discovery programs that are either completed, in progress or under contract with 26 partners. As a recent example, in a collaboration with Eli Lilly and Company, or Lilly, we applied our technology stack to co-develop LY-CoV555, a potential antibody therapy to treat and prevent COVID-19. Starting from a single blood sample obtained from a convalescent patient, we and our partners identified a viable antibody drug candidate within three weeks that advanced into clinical testing 90 days after initiation of the program. Lilly progressed into these clinical trials at a greatly accelerated pace as a result of the Coronavirus Treatment Acceleration Program, which is a special emergency program for possible coronavirus therapies created by the U.S. Food and Drug Administration, or FDA, in 2020 to expedite the development of potentially safe and effective life-saving treatments to combat the COVID-19 pandemic. With respect to other or future product candidates, there is no assurance that any of our partners or collaborators will be able to advance a product candidate into clinical development on this timeframe again in the future, or at all. We initiated our partnering program in 2015 and have only had this one program result in clinical milestone payments to us to date and we have not yet had a program receive marketing approval.

Antibodies, which are proteins generated by natural immune systems to fight infection and disease, are amongst the fastest growing class of drugs and are used across multiple therapeutic areas, including oncology, inflammation, neurodegeneration and many others. In 2019, antibody-based therapeutics accounted for over $140.0 billion in sales worldwide and represented five of the top 10 selling therapeutics. The rise of genomics, high-throughput biology and genetic engineering has greatly expanded the opportunity and the ecosystem of innovators working to advance the development of antibody-based therapeutics. There has been a proliferation of biopharmaceutical companies pursuing innovative drug candidate formats and new targets. As new entrants continue to emerge, we believe the total addressable market will continue to expand.

As the field of antibody therapeutics evolves, finding novel antibodies with desired therapeutic properties has become increasingly competitive and demanding. We believe that there are two fundamental problems hindering the discovery and development of next generation antibody-based therapeutics. The first is the state of technology: because of the limitations of legacy discovery approaches, there are many well-validated targets for

1

Table of Contents

which suitable antibodies cannot be found. The second is access: most companies are forced to cobble together fragmented solutions and lack the facilities and expertise needed to prosecute their antibody programs. Both of these problems contribute to the rising cost of drug development and delay bringing needed therapies to patients.

Many emerging and established life sciences companies have been built around technologies that focus on one or a limited number of steps in the discovery process, including immune repertoire sequencing, or RepSeq, single-cell analysis, AI, and transgenic rodent platforms. We believe we uniquely integrate proprietary technologies that address each of these steps, creating a complete solution for our partners. Over the last eight years, we have developed and assembled technologies that unlock the database of natural antibodies. We are democratizing the industry by providing our partners of all sizes with access to our centralized operating system.

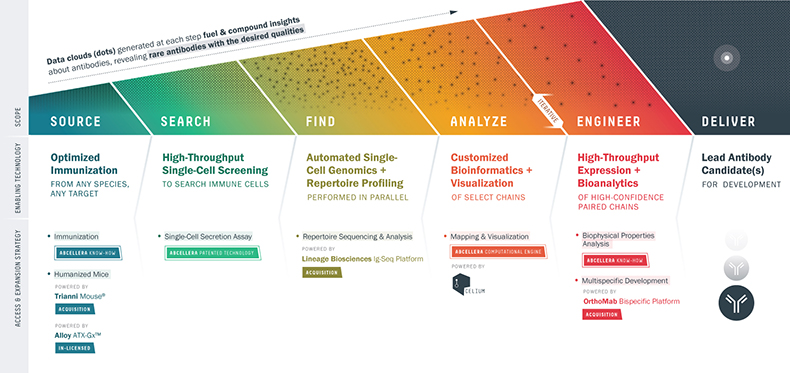

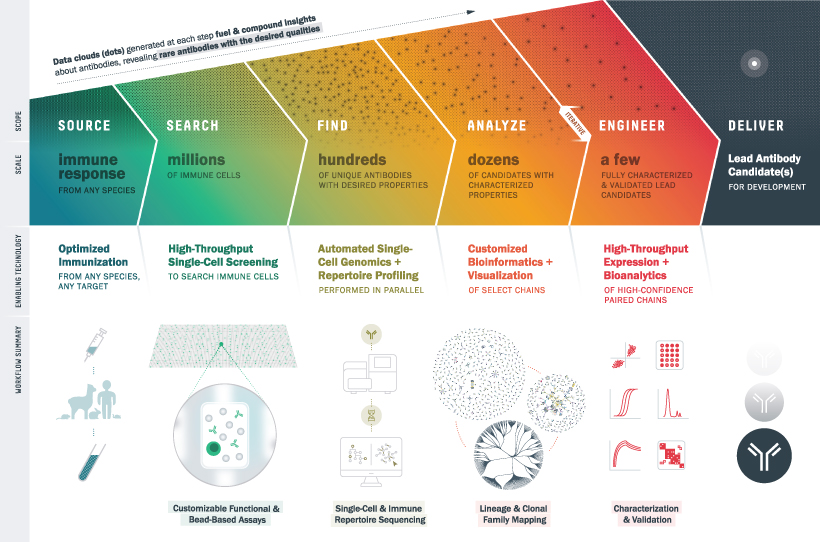

As depicted in Figure 1 below, our technology stack is a chain of interlocking technologies that is designed to enable the identification of antibodies with desired therapeutic properties.

Figure 1: Our Technology Stack

Some notable technologies within our stack that compound the productivity and efficiency of each step of the discovery process include:

| • | Source. We combine proprietary immunization with genetically engineered mouse technologies, including the proprietary suite of humanized mice we acquired in November 2020 in connection with our acquisition of Trianni, Inc., or Trianni, to provide a diverse source of human antibodies. |

| • | Search. Our patented microfluidic single-cell screening technology combines speed, throughput, efficiency, resolution and versatility, enabling rapid and deep searches of natural antibody responses. |

| • | Find. Following the acquisition of Lineage Biosciences Inc., or Lineage, in March 2017, we integrated high-throughput RepSeq technology with our single-cell screening technology to provide leading capabilities for the comprehensive profiling and functional characterization of antibody diversity. |

| • | Analyze. Our internally developed platform, Celium, a powerful computational engine for mining, interacting and visualizing the terabytes of data generated during an antibody discovery campaign, combines software, AI and visualization tools to organize, compute and interactively explore large multidimensional data sets. |

2

Table of Contents

| • | Engineer. We acquired rights to the OrthoMab bispecific technology in June 2020, which is a versatile and clinically-validated protein engineering solution to design and produce bispecific antibodies. |

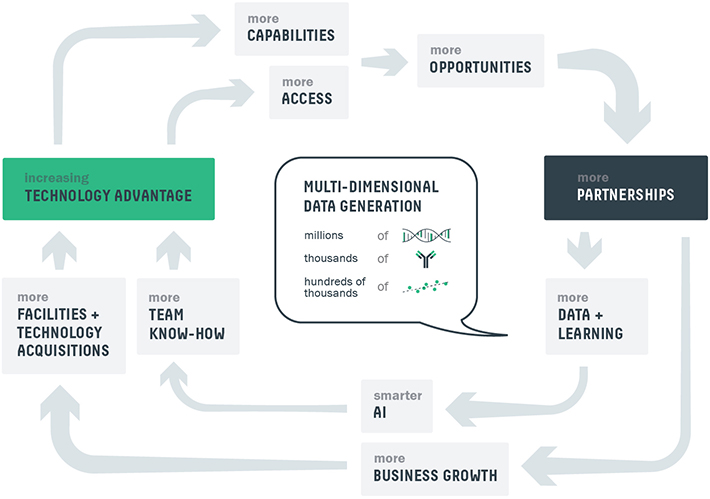

The marriage of advanced data collection and computation creates a flywheel effect that augments our technology. As we run our partnership business, we are amassing unique, multi-dimensional data sets that link measurements at the level of single immune cells with the properties of the antibodies they make and the DNA sequences that encode their function. A single antibody discovery project can generate millions of DNA sequences and single-cell measurements, as well as thousands of target-specific antibodies, each characterized by hundreds of data points. Every project generates more data about the antibody immune response. This creates a competitive advantage whereby Celium extracts insights from the data that allows us to accelerate wet lab experimentation with in silico computation in a continuously iterative process. Because our computation is grounded on real world data, the output of Celium is not theoretical predications. We find real molecules that have been optimized by nature.

Our business thesis is based on the belief that technological advancement can improve the drug development process and that maximizing the value and impact of our work is best achieved through partnerships. In March 2020, we tested these beliefs as we mobilized our response to the COVID-19 pandemic. Working with our partner Lilly, we were able to progress from initiation of discovery to clinical trials in only 90 days. The first clinical development candidate in this collaboration, LY-CoV555, is undergoing clinical trials as both a monotherapy and in combination with another antibody as potential therapeutics for COVID-19. On September 16, 2020, Lilly released the first interim Phase 2 clinical data for the monotherapy arms of the BLAZE-1 study, which showed that treatments of COVID-19 infected patients with LY-CoV555 resulted in a 72% risk reduction in hospitalization as compared to placebo in a study of 465 patients. BLAZE-1 is a randomized, double-blind, placebo-controlled Phase 2 study conducted by Lilly that is designed to assess the efficacy and safety of LY-CoV555 and an additional Lilly product candidate for the treatment of symptomatic COVID-19 in the outpatient setting. The monotherapy arms of BLAZE-1 enrolled mild-to-moderate recently diagnosed COVID-19 patients and the primary endpoint was met at a 2800 mg dose level. Lilly also announced that LY-CoV555 was well-tolerated, with no drug-related serious adverse events reported. In addition to the BLAZE-1 study described above, LY-CoV555 is being evaluated in three other clinical trials, one of which is a Phase 3 trial for prophylaxis of COVID-19. LY-CoV555 was also evaluated in a Phase 3 trial in hospitalized patients. Based on trial data that suggested that LY-CoV555 is unlikely to help hospitalized COVID-19 patients recover from this advanced stage of their disease, Lilly announced on October 26, 2020 that it has stopped enrolling additional patients for treatment with LY-CoV555 in this study. The other clinical trials of LY-CoV555 referred to above to evaluate LY-CoV555 for treatment of mild to moderate COVID-19 and for prophylaxis remain active.

On October 7, 2020, Lilly submitted a request for an Emergency Use Authorization, or EUA, for the LY-CoV555 monotherapy to the FDA, which was granted on November 9, 2020. On October 28, 2020, Lilly announced an agreement with the U.S. government to supply 300,000 vials of LY-CoV555 for $375.0 million. On October 29, 2020, Lilly also announced a fixed price contract for procurement of LY-CoV555 in the amount of $312.5 million with the U.S. Army Contracting Command. On November 22, 2020, Lilly was granted authorization for the LY-CoV555 monotherapy by Health Canada under the Interim Order Respecting the Importation, Sale and Advertising of Drugs for Use in Relation to COVID-19. On November 24, 2020, Lilly announced an agreement with the Canadian government to supply 26,000 doses of LY-CoV555 for the three month period between December 2020 and February 2021, for $32.5 million. Under our partnership with Lilly, we are entitled to receive a specified percentage of proceeds that Lilly receives from these sales. As proud as we are to have played a role in the global response to COVID-19, we believe it is only an example of how our technology can accelerate drug discovery.

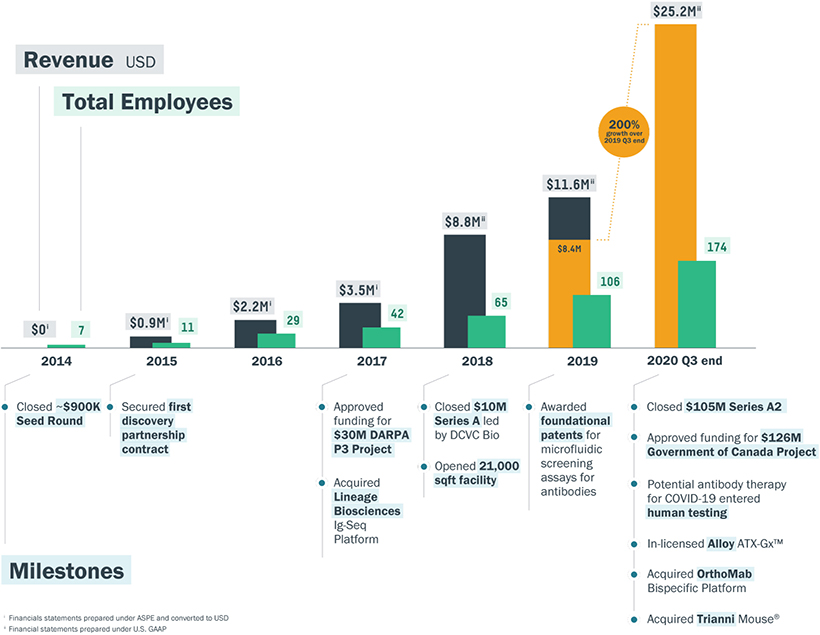

Our business has historically been both high growth and capital efficient. Revenues have grown at a 109% CAGR since 2014. We have generated positive operating cash flow cumulatively since our inception in 2012 and

3

Table of Contents

in every year since 2018. Our partnership agreements include: (i) payments for technology access and performance of research, (ii) downstream payments in the form of clinical and commercial milestones and (iii) royalties on net sales of any approved therapeutics. We structure our agreements in a way that is designed to align our partners’ economic interests with our own. While the vast majority of our historical revenue reflects upfront payments from research programs, we believe the long-term value of our business will be driven by downstream milestone and royalty payments. For the years ended December 31, 2018 and 2019 and the nine months ended September 30, 2019 and 2020, our revenue was $8.8 million, $11.6 million, $8.4 million and $25.2 million, respectively. For the years ended December 31, 2018 and 2019 and the nine months ended September 30, 2019 and 2020, our net income (loss) was $0.3 million, $(2.2) million, $(0.6) million and $1.9 million, respectively. As of September 30, 2020, we have entered into agreements for 94 partnered discovery programs, 71 of which include the potential for milestone and royalty payments from our partners. As of September 30, 2020, we had 174 full-time employees in Canada, the United States and Australia, consisting of 81 scientists, 45 engineers and data scientists and 48 business professionals.

Our Strategy

Our mission is to improve health with technologies that transform the way that antibody-based therapies are discovered. To achieve this mission, we aim to become the operating system for next generation antibody discovery, and to act as an integral part of our partners’ development efforts.

We seek to expand the industry of antibody therapeutics in two ways. First, we believe our technology can solve discovery problems to unlock new opportunities for therapeutic antibody development. Second, by accessing our teams, technologies and facilities, partners can eliminate the extended delays and costs associated with setting up antibody discovery capabilities. Through our partnership business, we aim to enable our partners to start programs without delay and prosecute them at maximum speed.

Our strategy includes:

| • | Creating more value with our existing partnerships. |

| • | Increasing the number of partnerships. |

| • | Expanding our market by delivering a full solution through forward integration. |

| • | Scaling our teams and facilities to meet future demand. |

| • | Increasing our technological differentiation. |

| • | Leveraging synergy of data and computation. |

4

Table of Contents

We believe our strategy creates a virtuous cycle, as depicted in Figure 2 below, that will drive our position as the centralized operating system for antibody discovery.

Figure 2: Our Business Strategy

Our Key Competitive Strengths

Our industry position and success are based on the following key competitive strengths:

| • | Better antibody discovery, from the start. |

| • | A full-stack technology, accessible to all. |

| • | An AI platform built on real world data. |

| • | A unique combination of hardware, software and wetware. |

| • | Industry-innovating business model. |

| • | The flywheel of data, partnerships and technology. |

| • | Strong brand built on performance and third-party recognition. |

| • | Robust IP portfolio including foundation patents. |

| • | Founder-led team, custom-built for interdisciplinary technology development. |

Our Market Opportunity

Antibodies are the fastest growing class of drugs and are used across multiple therapeutic areas, including oncology, inflammation, neurodegeneration and many more. In 2019, antibody-based therapeutics accounted for

5

Table of Contents

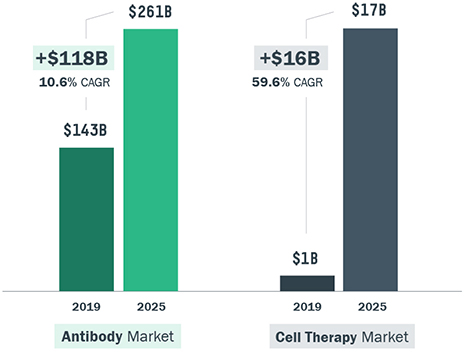

over $140 billion in sales and represented five of the top 10 selling therapeutics worldwide. In 2019, antibodies represented 70% of the sales of all biologics, and 36 antibody therapeutics reached blockbuster status with sales higher than $1.0 billion. The antibody-based therapeutics market is expected to reach approximately $260.0 billion in size by 2025, representing a CAGR of approximately 11% for the period from 2019 to 2025. Further, the more nascent cell therapy market is expected to grow from $1.0 billion in 2019 to over $17.0 billion in 2025, reflecting a CAGR of around 60%. Opportunities for accelerating growth of the antibody therapeutics market include improved access to traditionally difficult targets (e.g., G protein-coupled receptors, or GPCRs, and ion channels), the emergence of new therapeutic modalities (e.g., bispecifics, chimeric antigen receptor T cells, or CAR-T, cell therapy and antibody conjugates) and the ever-expanding number of companies entering the space.

Despite the size of the market, significant challenges exist. Looked at from any perspective, drug development fails too often, takes too long and costs too much.

Our Platform

Our platform is an operating system designed to support many antibody modalities; unlock new targets; increase the speed to clinical development for our partners and increase the potential clinical and commercial success for our partners.

Our full-stack, AI-powered technology sources, searches, decodes and analyzes antibody responses with the ultimate goal of engineering new antibody drug candidates for our partners. Our platform incorporates and integrates modern technology tools from engineering, microfluidics, single-cell analysis, high-throughput genomics, machine learning and hyper-scale data science. We have internally developed, in-licensed or acquired our technologies. We deploy our platform to help our partners in their efforts to identify antibodies with better potency and developability.

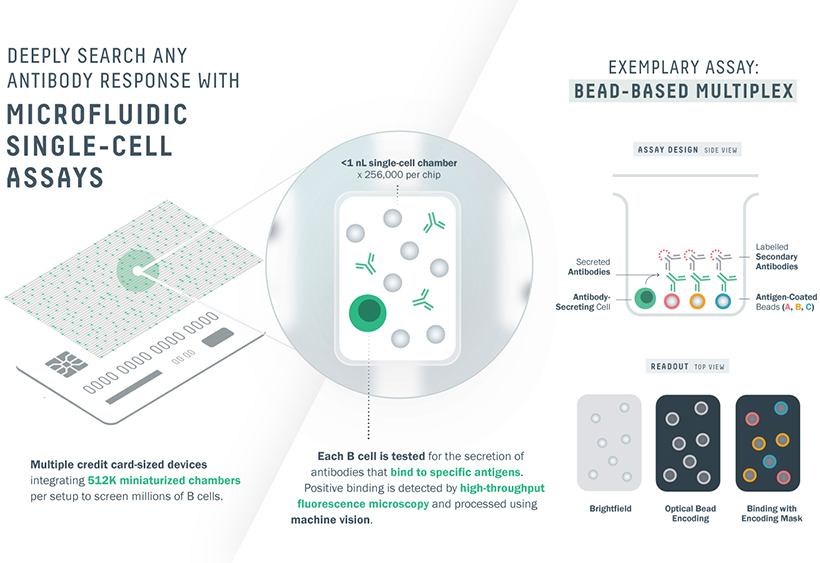

We believe our approach of integrating modern hardware, software and wetware is unique. We have pioneered nanoliter volume single-cell antibody screening methods using microfluidics. Our workflows incorporate proprietary immunization methods, including proprietary engineered mice from which we can discover fully human antibodies, optimized molecular biology protocols and patented protein engineering technologies. The aggregation of these technologies, coupled with our proprietary processes and team, allows us to provide a differentiated offering to our partners.

The computational engine of our platform, Celium, combines software, AI and visualization tools to mine, organize, compute and interactively explore the immense multidimensional data sets that we produce in each antibody discovery campaign. Unlike many AI-based drug discovery approaches, Celium is continually improved with real world data. We iteratively inform wetlab experimentation with in silico computation, and vice versa. The output of our process is not theoretical predictions. We discover real molecules that have been optimized by nature.

6

Table of Contents

We believe our competitive advantage is derived from the integration of multiple proprietary technologies and a seamless workflow. Table 1 below provides how each aspect of our end-to-end technology stack addresses challenges in antibody therapeutic discovery.

Table 1: Our Platform and Solution

Our Partnership Business

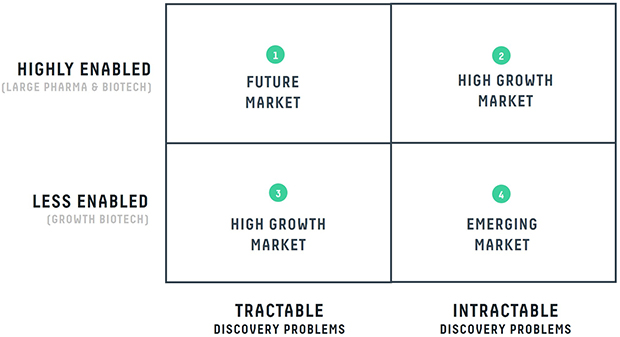

We forge partnerships with large cap pharmaceutical companies, biotechnology companies of all sizes and non-profit and government organizations. Our partners select a target and define the antibody properties needed for therapeutic development. We provide discovery solutions to partners that have a range of discovery capabilities, from the highly enabled to the less enabled. We enable discovery against targets that have traditionally been intractable, and we accelerate programs against less difficult targets.

Our deals emphasize participation in the success and upside of future antibody therapeutics. Our partnership agreements include near-term payments for technology access, research and intellectual property rights, and downstream payments in the form of clinical and commercial milestones, and royalties on net sales. As of September 30, 2020, we had 94 discovery programs that were either completed, in progress or under contract, including 71 with the potential for milestone and royalty payments. Some of the recent publicly disclosed partnerships, established since 2019, include:

| • | IgM Biosciences. Multi-target, multi-year partnership focused on oncology and immunology and announced on September 24, 2020. |

| • | Lilly. Multi-year partnership with 9 targets focused on COVID-19 and additional indications and announced on May 22, 2020. |

| • | Gilead Sciences. Single target partnership focused on infectious disease and announced on June 13, 2019. |

| • | Denali. Multi-year partnership with eight targets focused on neurological diseases and announced on February 28, 2019. |

| • | Novartis. Multi-year partnership with up to 10 targets and announced on February 14, 2019. |

7

Table of Contents

| • | Government of Canada. Commitment of up to CAD $175.6 million ($125.6 million) to expand efforts related to the discovery of antibodies for use in drugs to treat COVID-19, and to build technology and manufacturing infrastructure and announced on May 3, 2020. |

| • | Bill & Melinda Gates Foundation. Two-year agreement focused on high-priority infectious diseases including HIV, malaria and tuberculosis and announced on March 14, 2019. |

Trianni Acquisition

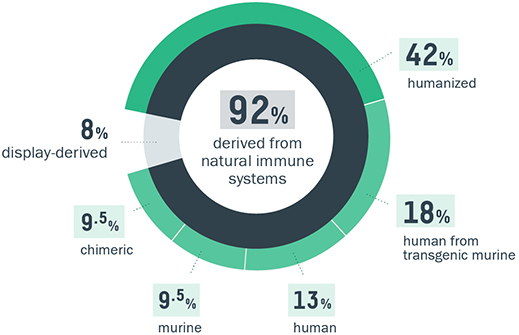

In November 2020, we acquired Trianni. Founded in 2008, Trianni develops next-generation transgenic mice that provide a source of fully-human antibodies for the discovery of therapeutic antibody candidates. To our knowledge, there are only two other companies, Regeneron Pharmaceuticals, Inc. and Kymab, Ltd., that engage in the development and use of humanized rodents in antibody discovery programs and against different therapeutic targets. Immunizing Trianni mice allows for the generation of diverse panels of human antibodies with drug-like properties including high affinity, high specificity and the biophysical properties suitable for manufacturing. In addition to the flagship Trianni mouse, we also acquired a suite of humanized rodent platforms engineered to support next-generation antibody therapy discovery and development. We believe the Trianni mouse technology will allow us to generate more high-quality antibodies against difficult targets and improve the speed of our discovery programs. By integrating a suite of transgenic rodent platforms into our stack, we believe we will be able to negotiate for greater downstream value participation, including higher royalty rates, from successful therapeutic development programs.

In addition to the strategic value of Trianni’s technology, Trianni generates revenues through mouse sales, platform licensing fees and associated downstream milestone payments. Since inception, Trianni has executed over 30 agreements with pharmaceutical companies, biotechnology companies and academic institutions. For 10 of these agreements, Trianni is eligible to receive royalty payments on net sales of therapeutics and diagnostics discovered using the company’s proprietary mice. For eight of the 10 agreements that include potential royalty payments, the partner has the option to buyout royalty payments prior to product approval. We believe the addition of the Trianni mouse, and future next generation transgenic mice under development will allow us to expand the diversity of antibody responses to a wide range of targets, leading to improvements in the quality and speed of our discovery programs.

In connection with the Trianni acquisition, our U.S. subsidiary entered into an agreement and plan of merger for an initial purchase price of $90.0 million, subject to certain adjustments for working capital, indebtedness and expenses. Upon consummation of the merger, Trianni became our wholly owned subsidiary. In addition, we will assign to a former stockholder of Trianni most of the amounts received from a license agreement. We paid the purchase price for the acquisition using the proceeds from the issuance of convertible promissory notes to certain investors in an aggregate amount of approximately $90.0 million, or the Convertible Notes. The Convertible Notes will mature on October 30, 2025, unless earlier prepaid or converted, and will bear interest from October 30, 2021 at an annual rate of 5%, payable annually in arrears on October 30 of each year, beginning on October 30, 2022. Interest on the Convertible Notes is payable in cash or in the form of additional non-convertible notes. The Convertible Notes are convertible at the option of the noteholders into our common shares under certain circumstances, including upon the closing of this offering. Convertible Notes converted upon the closing of this offering will convert at a price of 85% of the initial public offering price.

Risks Associated with Our Business

Our business is subject to numerous risks that you should consider before investing in our company. These risks are described more fully the section titled “Risk Factors” in this prospectus. These risks include, but are not limited to, the following:

| • | We have incurred losses in certain years since inception and we may not be able to generate sufficient revenue to achieve and maintain profitability. |

8

Table of Contents

| • | Our quarterly and annual operating results have fluctuated significantly in the past and may fluctuate significantly in the future, which makes our future operating results difficult to predict and could cause our operating results to fall below expectations. |

| • | Our commercial success depends on the quality of our antibody discovery platform and technological capabilities and their acceptance by new and existing partners in our market. |

| • | If we cannot maintain and expand current partnerships and enter into new partnerships that generate discovery programs for antibodies, our business could be adversely affected. |

| • | In recent periods, we have depended on a limited number of partners for our revenue, the loss of any of which could have an adverse impact on our business. |

| • | Biopharmaceutical drug development is inherently uncertain, and it is possible that none of the drug candidates discovered using our platform that are further developed by our partners will receive marketing approval or become viable commercial products, on a timely basis or at all. |

| • | We may be unable to manage our current and future growth effectively, which could make it difficult to execute on our business strategy. |

| • | We have invested, and expect to continue to invest, in research and development efforts that further enhance our antibody discovery platform. Such investments in technology are inherently risky and may affect our operating results. If the return on these investments is lower or develops more slowly than we expect, our revenue and operating results may suffer. |

| • | Our partners have significant discretion in determining when and whether to make announcements, if any, about the status of our partnerships, including about clinical developments and timelines for advancing collaborative programs, and the price of our common shares may decline as a result of announcements of unexpected results or developments. |

| • | Our partners may not achieve projected discovery and development milestones and other anticipated key events in the expected timelines or at all, which could have an adverse impact on our business and could cause the price of our common shares to decline. |

| • | The life sciences and biotech platform technology market is highly competitive, and if we cannot compete successfully with our competitors, we may be unable to increase or sustain our revenue, or achieve and sustain profitability. |

| • | Our success depends on our ability to protect our intellectual property. |

| • | We have identified a material weakness in our internal control over financial reporting, and we may identify additional material weaknesses in the future or otherwise fail to maintain proper and effective internal controls, which may impair our ability to produce accurate financial statements on a timely basis. |

Corporate Information

We were incorporated in 2012 under the Business Corporations Act (British Columbia), or the BCBCA. Our principal executive offices are located at 2215 Yukon Street Vancouver, British Columbia, V5Y 0A1, Canada and our telephone number is (604) 559-9005. We have six wholly owned subsidiaries, Lineage, a Delaware corporation, Trianni, a California corporation, AbCellera US Holdings Inc., a Delaware corporation, AbCellera Properties Inc., a BCBCA company, AbCellera Properties Columbia Inc., a BCBCA company, and Channel Biologics Pty Ltd., a proprietary company registered in New South Wales, Australia. Our website address is www.abcellera.com. We have included our website address in this prospectus solely as an inactive textual reference. The information contained on or that can be accessed through our website is not incorporated by reference into this prospectus.

AbCellera and other trademarks or service marks of AbCellera, including our subsidiaries appearing in this prospectus are the property of AbCellera. The other trademarks, trade names and service marks appearing in this

9

Table of Contents

prospectus are the property of their respective owners. Solely for convenience, the trademarks and trade names in this prospectus are referred to without the ® and ™ symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto.

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, or JOBS Act, and will remain an emerging growth company until the earlier of (i) the last day of the fiscal year in which we have total annual gross revenues of $1.07 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the closing of this offering; (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission, or SEC. As long as we remain an emerging growth company, we may take advantage of specified reduced disclosure and other public company reporting requirements. These provisions include:

| • | being permitted to provide only two years of audited financials in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure in this prospectus; |

| • | reduced disclosure about our executive compensation arrangements; |

| • | not being required to hold advisory votes on executive compensation or to obtain shareholder approval of any golden parachute arrangements not previously approved; |

| • | an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting; and |

| • | an exemption from compliance with the requirements of the Public Company Accounting Oversight Board regarding the communication of critical audit matters in the auditor’s report on the financial statements. |

We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold shares.

We have elected not to “opt out” of the exemption for the delayed adoption of certain accounting standards, and, therefore, we will adopt new or revised accounting standards at the time private companies adopt the new or revised accounting standard and will do so until such time that we either (i) irrevocably elect to “opt out” of such extended transition period or (ii) no longer qualify as an emerging growth company. We may choose to early adopt any new or revised accounting standards whenever such early adoption is permitted for private companies. As a result of this election, the information that we provide in this prospectus may be different than the information you may receive from other public companies in which you hold equity interests.

We are also a “smaller reporting company” as defined in the Securities Exchange Act of 1934, as amended. We may continue to be a smaller reporting company even after we are no longer an emerging growth company. We may continue to be a smaller reporting company after this offering if either (i) the market value of our shares held by non-affiliates is less than $250.0 million as measured on the last business day of our second fiscal quarter or (ii) our annual revenue was less than $100.0 million during the most recently completed fiscal year and the market value of our shares held by non-affiliates is less than $700.0 million as measured on the last business day of our second fiscal quarter. Specifically, as a smaller reporting company, we may choose to present only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K and have reduced disclosure obligations regarding executive compensation. Further, if we are a smaller reporting company with less than $100.0 million in annual revenue, we would not be required to obtain an attestation report on internal control over financial reporting issued by our independent registered public accounting firm.

10

Table of Contents

The Offering

Common shares offered by us | shares |

Common shares to be outstanding immediately after this offering | shares |

Option to purchase additional shares | The underwriters have an option for a period of 30 days to purchase up to additional common shares at the public offering price, less the estimated underwriting discounts and commissions. |

Use of proceeds | We estimate that the net proceeds to us from the sale of our common shares in this offering will be approximately $ million (or approximately $ million if the underwriters exercise their option to purchase additional shares in full), assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. We currently intend to use the net proceeds from this offering, together with our existing cash and cash equivalents, to continue making investments in research and development efforts towards deepening our technology and expertise along our technology stack, to continue making investments in building our business development team and marketing our solutions to new and existing partners, as well as for general corporate purposes, including working capital, operating expenses and capital expenditures. We may also use a portion of the net proceeds from this offering for the acquisition of businesses, technologies or other assets that we believe are complementary to our own. See “Use of Proceeds” for more information. |

Risk factors | Investment in our common shares involves substantial risks. You should read this prospectus carefully, including the section titled “Risk Factors” and the financial statements and the related notes to those statements appearing elsewhere in this prospectus, before investing in our common shares. |

Proposed Nasdaq Global Market symbol | “ABCL” |

The number of common shares to be outstanding immediately after this offering is based on common shares outstanding as of September 30, 2020 (including our convertible preferred shares on an as-converted basis into an aggregate of common shares, and the conversion of the Convertible Notes into an aggregate of common shares upon the completion of this offering, based on an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover of this prospectus), and excludes:

| • | 4,037,050 common shares issuable upon the exercise of share options outstanding as of September 30, 2020, with a weighted-average exercise price of $2.70 per share; |

| • | 1,341,131 common shares issuable upon the exercise of share options granted after September 30, 2020, with a weighted average price of $27.74 per share; |

11

Table of Contents

| • | 1,316,131 common shares reserved for issuance under our Sixth Amended and Restated Stock Option Plan, or the Current Plan, as of September 30, 2020, which shares will cease to be available for issuance at the time the 2020 Share Option and Incentive Plan, or the 2020 Plan, becomes effective; |

| • | common shares to be reserved for future issuance under our 2020 Plan, which will become available for issuance upon the effectiveness of the registration statement of which this prospectus is a part, plus any future increases in the number of common shares reserved for issuance; and |

| • | common shares to be reserved for future issuance under our 2020 Employee Share Purchase Plan, or the 2020 ESPP, which will become available for issuance upon the effectiveness of the registration statement of which this prospectus is a part, plus any future increases in the number of common shares reserved for issuance. |

Except as otherwise specifically indicated, all information in this prospectus assumes or gives effect to the following:

| • | a one-for- share split of our common shares, which was effected on , 2020; |

| • | no exercise of the underwriters’ option to purchase up to additional common shares in this offering; |

| • | no exercise of the outstanding options described above; |

| • | the conversion of all of our outstanding convertible preferred shares as of September 30, 2020 into an aggregate of common shares immediately prior to the completion of this offering; |

| • | the conversion of the Convertible Notes into an aggregate of common shares upon the completion of this offering, assuming an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover of this prospectus; and |

| • | the filing and effectiveness of our new notice of articles and effectiveness of our new articles, which will occur immediately prior to the completion of this offering. |

12

Table of Contents

Summary Consolidated Financial Data

The following summary consolidated statements of operations data for the years ended December 31, 2018 and 2019 have been derived from our audited consolidated financial statements appearing elsewhere in this prospectus. The summary consolidated statements of operations data for the nine months ended September 30, 2019 and 2020 and the summary consolidated balance sheet data as of September 30, 2020 have been derived from our unaudited condensed consolidated financial statements appearing elsewhere in this prospectus and have been prepared in accordance with U.S. generally accepted accounting principles, or U.S. GAAP, on the same basis as the audited consolidated financial statements. In the opinion of management, the unaudited data reflects all adjustments, consisting only of normal recurring adjustments, necessary for a fair statement of the information in those financial statements. You should read the following summary consolidated financial data together with the “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of this prospectus and our consolidated financial statements and the related notes appearing elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in any future periods, and results for any interim period are not necessarily indicative of results that should be expected for the full fiscal year ending December 31, 2020 or any other period.

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||

| 2018 | 2019 | 2019 | 2020 | |||||||||||||

| (unaudited) | ||||||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||

Consolidated Statement of Operations Data: | ||||||||||||||||

Revenue: | ||||||||||||||||

Research fees | $ | 8,831 | $ | 11,612 | $ | 8,409 | $ | 17,247 | ||||||||

Milestone payments | — | — | — | 8,000 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total revenue | 8,831 | 11,612 | 8,409 | 25,247 | ||||||||||||

Operating Expenses: | ||||||||||||||||

Research and development | 5,803 | 10,113 | 6,804 | 20,757 | ||||||||||||

Sales and marketing | 712 | 1,263 | 792 | 1,610 | ||||||||||||

General and administrative | 2,151 | 2,749 | 1,774 | 6,116 | ||||||||||||

Depreciation | 918 | 1,604 | 1,180 | 1,507 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total operating expenses | 9,583 | 15,729 | 10,550 | 29,990 | ||||||||||||

Loss from operations | (753 | ) | (4,117 | ) | (2,141) | (4,743 | ) | |||||||||

Other income (expense): | ||||||||||||||||

Interest income | (42 | ) | (155 | ) | (111 | ) | (195 | ) | ||||||||

Interest and other expense | 213 | 209 | 127 | 4,896 | ||||||||||||

Foreign exchange (gain) loss | 362 | (186 | ) | (348 | ) | (1,146 | ) | |||||||||

Grants and incentives | (1,594 | ) | (1,774 | ) | (1,239 | ) | (10,217 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total other income | (1,061 | ) | (1,906 | ) | (1,571 | ) | (6,662 | ) | ||||||||

Net earnings (loss) for the period | $ | 309 | $ | (2,211 | ) | $ | (570 | ) | $ | 1,918 | ||||||

|

|

|

|

|

|

|

| |||||||||

Net earnings (loss) per share attributable to common shareholders(1): | ||||||||||||||||

Basic | $ | 0.02 | $ | (0.15 | ) | $ | (0.04 | ) | $ | 0.09 | ||||||

|

|

|

|

|

|

|

| |||||||||

Diluted | $ | 0.02 | $ | (0.15 | ) | $ | (0.04 | ) | $ | 0.08 | ||||||

|

|

|

|

|

|

|

| |||||||||

Weighted-average common shares outstanding(1): | ||||||||||||||||

Basic | 14,943,637 | 15,132,756 | 15,120,734 | 15,241,330 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Diluted | 17,133,611 | 15,132,756 | 15,120,734 | 23,772,353 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Pro forma net loss per share attributable to common shareholders (unaudited)(1): | ||||||||||||||||

Basic | $ | $ | ||||||||||||||

|

|

|

| |||||||||||||

Diluted | $ | $ | ||||||||||||||

|

|

|

| |||||||||||||

Pro forma weighted-average common shares outstanding (unaudited)(1): | ||||||||||||||||

Basic | ||||||||||||||||

|

|

|

| |||||||||||||

Diluted | ||||||||||||||||

|

|

|

| |||||||||||||

13

Table of Contents

| (1) | See Note 5 to our consolidated financial statements and our interim consolidated financial statements, each appearing elsewhere in this prospectus, for details on the calculation of historical and pro forma basic and diluted net loss per share attributable to common shareholders and the weighted-average number of shares used in the computation of the per share amounts. |

| As of September 30, 2020 | ||||||||||||

| Actual | Pro Forma(2) | Pro Forma As Adjusted(3)(4) | ||||||||||

(unaudited) | ||||||||||||

| (in thousands) | ||||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||

Cash and cash equivalents | $ | 91,082 | (5) | $ | $ | |||||||

Working capital(1) | 93,895 | |||||||||||

Total assets | 142,385 | |||||||||||

Total liabilities | 53,147 | |||||||||||

Total preferred stock | 82,208 | |||||||||||

Total shareholders’ equity | 89,238 | |||||||||||

| (1) | We define working capital as current assets less current liabilities. See our consolidated financial statements and related notes appearing elsewhere in this prospectus for further details regarding our current assets and current liabilities. |

| (2) | The pro forma consolidated balance sheet data give effect to (i) the conversion of all of our outstanding convertible preferred shares as of September 30, 2020 into 8,123,048 common shares upon the completion of this offering and (ii) the issuance of the Convertible Notes and receipt of approximately $90.0 million in gross proceeds therefor, and the conversion of the Convertible Notes into an aggregate of common shares upon the completion of this offering, assuming an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover of this prospectus. |

| (3) | The pro forma as adjusted balance sheet data give further effect to the sale and issuance of common shares in this offering at an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| (4) | Each $1.00 increase or decrease in the assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, the pro forma as adjusted amounts of each of our cash and cash equivalents, working capital, total assets, total liabilities and total shareholders’ equity by approximately $ million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. We may also increase or decrease the number of shares we are offering. Each increase or decrease of 1.0 million shares in the number of shares offered by us at the assumed initial public offering price per share would increase or decrease, as applicable, the pro forma as adjusted amounts of each of our cash and cash equivalents, working capital, total assets, total liabilities and total shareholders’ equity by approximately $ million, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. The pro forma as adjusted information is illustrative only, and we will adjust this information based on the actual initial public offering price and other terms of this offering determined at pricing. |

| (5) | Does not reflect payment of approximately $8.0 million to Trianni in connection with the acquisition in November 2020. |

14

Table of Contents

Investing in our common shares involves a high degree of risk. You should carefully consider the risks described below, as well as the other information in this prospectus, including our consolidated financial statements and the related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding whether to invest in our common shares. The occurrence of any of the events or developments described below could materially harm our business, financial condition, results of operations and prospects. In such an event, the market price of our common shares could decline, and you may lose all or part of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations.

Risks Related to Our Business and Strategy

We have incurred losses in certain years since inception and we may not be able to generate sufficient revenue to achieve and maintain profitability.

Our plan is to enter a phase of accelerated growth and we will be investing heavily in our business. We expect to experience variability in revenue and in expenses which makes it difficult to evaluate our business or our prospects. As such, we may incur losses that are materially larger than what we have previously incurred. We have incurred losses in certain years since our inception and anticipate that we will continue to incur significant losses for the foreseeable future. For the years ended December 31, 2018 and 2019, we incurred a net income of $0.3 million and net loss of $2.2 million, respectively, and for the nine months ended September 30, 2020, we had net income of $1.9 million. As of September 30, 2020, we had an accumulated deficit of $2.8 million. We expect that our operating expenses will continue to increase significantly, including as we:

| • | invest in research and development activities to improve our technology and platform; |

| • | market and sell our solutions to existing and new partners; |

| • | acquire businesses or technologies to support the growth of our business; |

| • | attract, hire and retain qualified personnel; |

| • | maintain, expand, enforce, protect and defend our intellectual property portfolio; |

| • | prosecute and defend our ongoing and any future litigation; |

| • | build our new good manufacturing practices, or GMP, manufacturing facility; |

| • | create additional infrastructure to support our operations, including expanding our sales and marketing organization; |

| • | add operational, financial and management information systems and personnel to support our operations as a public company; and |

| • | experience any delays or encounter issues with any of the above. |

Our expenses could increase beyond expectations for a variety of reasons, including as a result of our growth strategy and the increase in our operations. Since our inception, we have financed our operations primarily from revenue from upfront payments generated through our receipt of technology access fees and discovery research fees through the performance of service contracts with our partners, payments from partners upon the satisfaction of clinical milestones, government funding and one off government grants, the incurrence of indebtedness, and from private placements of our common and convertible preferred shares. Given our strategy and plans to invest in enhancing and scaling our business, we will need to generate significant additional revenue to achieve and sustain future profitability. Even if we achieve profitability, we cannot be sure that we will remain profitable for any sustained period of time. We may never be able to generate sufficient revenue to achieve or sustain profitability and our recent and historical growth should not be considered indicative of our future performance.

15

Table of Contents

Our revenue has fluctuated from period to period, and our revenue for any historical period may not be indicative of results that may be expected for any future period.

For the years ended December 31, 2018 and 2019, and for the nine months ended September 30, 2019 and 2020, a substantial portion of our revenue was generated by upfront technology access and research discovery fees through performing research activities for our partners. During the nine months ended September 30, 2020, we received payments from our partnership contracts generated upon the satisfaction of clinical milestones for the first time. Upfront technology access fees are generated upon execution of our partnership agreements. Research and discovery fees are generated by research activities that we perform for our partners, the timing and nature of which are dictated by the commencement of antibody discovery campaigns selected by our partners. Clinical milestone payments are generated upon the achievement of development milestones by our partners with respect to the antibodies that we deliver. As a result, we currently do not generate significant recurring revenue and, until such time as we establish significant recurring revenue, if at all, we will be prone to regular fluctuations in our revenue dependent on the timing of our entry into partnership agreements, our partners initiating discovery programs, and our partners achieving development milestones or commercial sales with respect to drug candidates utilizing antibodies discovered using our platform. We do not expect to generate significant recurring revenue unless and until such time as we secure additional programs under contract that, in the aggregate, result in regular and continuous execution of new partnership contracts, research discovery activities, achievement of development milestones or commencement of commercial sales. However, we are unable to predict whether and the extent to which the minimum annual payments under our partnership agreements will be exceeded, or the timing of the achievement of any milestones under these agreements, if they are achieved at all. In some cases, the timing and likelihood of payments to us under these agreements is dependent on our partners’ successful utilization of the antibodies discovered using our platform, which is outside of our control. Because of these factors, our operating results could vary materially from quarter to quarter from our forecasts.

Our quarterly and annual operating results have fluctuated significantly in the past and may fluctuate significantly in the future, which makes our future operating results difficult to predict and could cause our operating results to fall below expectations.

Our quarterly and annual operating results have fluctuated in the past and may fluctuate in the future, which makes it difficult for us to predict our future operating results. These fluctuations may occur due to a variety of factors, many of which are outside of our control, including, but not limited to:

| • | the level of demand for our antibody discovery platform and solutions, which may vary significantly; |

| • | the timing and cost of, and level of investment in, research, development and commercialization activities relating to our platform and technology, which may change from time to time; |

| • | the start and completion of programs in which our platform is utilized; |

| • | the relative reliability and robustness of our platform, including the data generation and computational tools within our technology stack; |

| • | the introduction of new technologies, platform features or software, by us or others in our industry; |

| • | expenditures that we may incur to acquire, develop or commercialize additional technologies; |

| • | expenditures involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including costs related to our intellectual property litigation with Berkeley Lights, and the outcome of this and any other future patent litigation we may be involved in; |

| • | the degree of competition in our industry and any change in the competitive landscape of our industry, including consolidation among our competitors or future partners; |

| • | natural disasters, outbreaks of disease or public health crises, such as the COVID-19 pandemic; |

| • | the timing and nature of any future acquisitions or strategic partnerships; |

16

Table of Contents

| • | future accounting pronouncements or changes in our accounting policies; and |

| • | general social, political and economic conditions and other factors, including factors unrelated to our operating performance or the operating performance of our competitors. |

For example, this is the first year in which we received payments from a partner upon the satisfaction of clinical milestones. The antibody, LY-CoV555 developed by Eli Lilly and Company, or Lilly, has undergone or is currently undergoing a Phase 1 clinical trial, three Phase 2 clinical trials and one Phase 3 clinical trial, and we have received associated clinical milestone payments this year. Lilly progressed into these clinical trials at a greatly accelerated pace as a result of the Coronavirus Treatment Acceleration Program, which is a special emergency program for possible coronavirus therapies created by the FDA in 2020 to expedite the development of potentially safe and effective life-saving treatments to combat the COVID-19 pandemic. With respect to other or future product candidates, there is no assurance that any of our partners or collaborators will be able to advance a product candidate through clinical development on this timeframe again in the future, or at all. We initiated our partnering program in 2015 and have only had this one program result in clinical milestone payments to us to date and we have not yet had a program receive marketing approval.

The effect of one of the factors discussed above, or the cumulative effects of a combination of factors discussed above, could result in large fluctuations and unpredictability in our quarterly and annual operating results. As a result, comparing our operating results on a period-to-period basis may not be meaningful. Investors should not rely on our past results as an indication of our future performance.

Even if this offering is successful, we may need to raise additional capital to fund our existing operations, improve our platform or expand our operations. If we are unable to raise additional capital on terms acceptable to us or at all or generate cash flows necessary to maintain or expand our operations, we may not be able to compete successfully, which would harm our business, operations, and financial condition.

Based on our current business plan, we believe the net proceeds from this offering, together with our existing cash and cash equivalents and anticipated cash flows from operations, will be sufficient to meet our working capital and capital expenditure needs over at least the next months following the date of this prospectus. If our available cash resources together with our net proceeds from this offering and anticipated cash flow from operations are insufficient to satisfy our liquidity requirements including because of lower demand for our drug-discovery platform, or the realization of other risks described in this prospectus, we may be required to raise additional capital prior to such time through issuances of equity or convertible debt securities, entrance into a credit facility or another form of third party funding or seek other debt financing. Such additional financing may not be available on terms acceptable to us or at all.

In any event, we may consider raising additional capital in the future to expand our business, to pursue strategic investments, to take advantage of financing opportunities or for other reasons. For example, this may include reasons such as to:

| • | increase our sales and marketing efforts to drive market recognition of our platform and address competitive developments; |

| • | fund development and marketing efforts of our current and future programs; |

| • | expand the capabilities of our platform into adjacent therapeutic modalities, including vaccine development and cell therapy; |

| • | acquire, license or invest in technologies; |

| • | acquire or invest in complementary businesses or assets; and |

| • | finance capital expenditures and general and administrative expenses. |

17

Table of Contents

Our present and future funding requirements will depend on many factors, including:

| • | our ability to achieve revenue growth; |

| • | the cost of expanding our operations, including our sales and marketing efforts; |

| • | our rate of progress in selling access to our platform and marketing activities associated therewith; |

| • | our rate of progress in, and cost of research and development activities associated with, antibody discovery; |

| • | the effect of competing technological and market developments; |

| • | the continued impact of the COVID-19 pandemic on global social, political and economic conditions; |

| • | the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including costs related to our intellectual property litigation with Berkeley Lights, and the outcome of this and any other future patent litigation we may be involved in; and |

| • | costs related to any domestic and international expansion. |

The various ways we could raise additional capital carry potential risks. If we raise funds by issuing equity securities, dilution to our shareholders would result. Any preferred equity securities issued also would likely provide for rights, preferences or privileges senior to those of holders of our common shares. If we raise funds by issuing debt securities, those debt securities would have rights, preferences and privileges senior to those of holders of our common shares. Debt financing and preferred equity financing, if available, may also involve agreements that include covenants restricting our ability to take specific actions, such as incurring additional debt, selling or licensing our assets, making product acquisitions, making capital expenditures, or declaring dividends. For example, our agreement with the Canadian Ministry of Western Economic Diversification, or WD Canada, under the Western Innovation Initiative and the Business Scale-up and Productivity programs, as well as our agreement with the Strategic Innovation Fund, or SIF, requires us to obtain the consent of WD Canada or SIF, as applicable, before being able to engage in certain change of control and asset disposition transactions during the term of the agreement. In particular, our agreement with the SIF requires us to obtain consent in the event that an individual or company (or two or more of them acting in concert) acquires the direct or indirect beneficial ownership of 20% or more of our voting securities. In the event consent is not obtained, the agreement may be terminated and we will be obligated to repay all or a portion of the contribution amounts from WD Canada and SIF.

If we are unable to obtain adequate financing or financing on terms satisfactory to us, if we require it, our ability to continue to pursue our business objectives and to respond to business opportunities, challenges, or unforeseen circumstances could be significantly limited, and could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our commercial success depends on the quality of our antibody discovery platform and technological capabilities and their acceptance by new and existing partners in our market.

We utilize our drug-discovery platform to identify antibodies for further development and potential commercialization by our partners. As a result, the quality and sophistication of our platform and technology is critical to our ability to conduct our research discovery activities and to deliver more promising molecules and to accelerate and lower the costs of discovery as compared to traditional methods for our partnerships. In particular, our business depends, among other things, on:

| • | our platform’s ability to successfully identify therapeutic antibodies on the desired timeframes that can ultimately be used to prevent and treat diseases; |

| • | our ability to execute on our strategy to enter into new partnerships with new or existing partners and establish a robust internal pipeline of antibody discovery programs; |

| • | our ability to increase awareness of the capabilities of our technology and solutions; |

| • | our partners’ and potential partners’ willingness to adopt new technologies; |

18

Table of Contents

| • | whether our platform reliably provides advantages over legacy and other alternative technologies and is perceived by customers to be cost effective; |

| • | the rate of adoption of our solutions by pharmaceutical companies, biotechnology companies of all sizes, government organizations and non-profit organizations and others; |

| • | prices we charge for our data packages and the discoveries that we make; |

| • | the relative reliability and robustness of our platform; |

| • | our ability to develop new solutions for partners; |

| • | if competitors develop a platform that performs functional testing of cells at a greater throughput than us; |

| • | the timing and scope of any approval that may be required by the U.S. Food and Drug Administration, or FDA, or any other regulatory body for drugs that are developed based on antibodies discovered by us; |

| • | the impact of our investments in innovation and commercial growth; |

| • | negative publicity regarding our or our competitors’ technologies resulting from defects or errors; and |

| • | our ability to further validate our technology through research and accompanying publications. |

There can be no assurance that we will successfully address any of these or other factors that may affect the market acceptance of our platform or our technology. If we are unsuccessful in achieving and maintaining market acceptance of our platform, our business, financial condition, results of operations and prospects could be adversely affected.

If we cannot maintain and expand current partnerships and enter into new partnerships that generate discovery programs for antibodies, our business could be adversely affected.

We do not have our own pipeline of drug candidates, and instead we focus our efforts on the discovery of antibodies for targets that are selected by our partners. Our partners then use the data packages provided by us to develop their own drug candidates without our involvement. As a result, our success depends on our ability to expand the number and scope of our partnerships. Many factors may impact the success of these partnerships, including our ability to perform our obligations, our partners’ satisfaction with our data packages, our partners’ ability to successfully develop, secure regulatory approval for and commercialize drug candidates using antibodies discovered using our platform, our partners’ internal priorities (including fluctuations in research and developments budgets), our partners’ resource allocation decisions and competitive opportunities, disagreements with partners, the costs required of either party to the partnerships and related financing needs, and operating, legal and other risks in any relevant jurisdiction.

In our partnership programs, we maintain rights to large unique data sets that connect information at the level of single-cell measurements, DNA sequence and protein function. We use this data to create an accelerating flywheel of learning: data generation from our partnership business provides the basis for AI modules that lead to expanded capabilities and faster data generation which supports our partnership business. As a result, in addition to reducing our revenue or delaying the development of our future solutions, the loss of one or more of these relationships may reduce our exposure to such information, thus hindering our efforts to further our technological differentiation and improve our platform.

We engage in conversations with companies regarding potential partnerships on an ongoing basis. These conversations may not result in a commercial agreement. Even if an agreement is reached, the resulting relationship may not be successful, including due to our inability to discover any usable antibodies for the selected targets or the antibodies that we do discover may not be successfully developed or commercialized by our partners. In such circumstances, we would not generate any substantial revenues from such a collaboration in the form of discovery research fees, milestone payments, royalties or otherwise. Speculation in the industry about our existing or potential partnerships can be a catalyst for adverse speculation about us, or our data packages, which can adversely affect our reputation and our business.

19

Table of Contents