Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

TABLE OF CONTENTS

TABLE OF CONTENTS3

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-218707

601 Riverside Avenue

Jacksonville, Florida 32204

Dear Black Knight Financial Services, Inc. Shareholder:

After careful consideration, and upon the recommendation of a special committee of disinterested directors of the board of directors of Black Knight Financial Services, Inc., which we refer to as Black Knight, the board of directors of Black Knight has approved an agreement and plan of merger, which we refer to as the merger agreement, among Black Knight, Black Knight Holdco Corp., which we refer to as New Black Knight, New BKH Merger Sub, Inc., which we refer to as Merger Sub One, BKFS Merger Sub, Inc., which we refer to as Merger Sub Two, Fidelity National Financial, Inc., which we refer to as FNF, and New BKH Corp., which we refer to as New BKH. The merger agreement provides for two mergers that result in Black Knight and New BKH becoming subsidiaries of New Black Knight, a new public holding company.

Prior to the mergers, and as a condition to the consummation of the mergers, FNF will effect a series of separation transactions that will result in the contribution of the shares of Class B common stock of Black Knight beneficially owned by FNF and all of the Class A units, which we refer to as BKFS LLC Units or Units, of Black Knight Financial Services, LLC, which we refer to as BKFS LLC, beneficially owned by FNF, to New BKH and the distribution of all of the shares of New BKHpro rata to the holders of the FNF Group common stock.

In the merger of Merger Sub Two with and into Black Knight, which we refer to as the BKFS merger, Black Knight shareholders (other than New BKH) will receive one share of New Black Knight common stock for each share of Class A common stock of Black Knight that they own. In the merger of Merger Sub One with and into New BKH, which we refer to as the New BKH merger, New BKH shareholders will receive one share of New Black Knight common stock for each share of New BKH common stock that they own.

Upon completion of the transactions contemplated by the merger agreement, Black Knight's former shareholders (other than FNF and its affiliates) will collectively own approximately 45.71% of the common stock of New Black Knight, and New BKH's former shareholders (the holders of FNF Group common stock) will collectively own approximately 54.29% of the common stock of New Black Knight. The New Black Knight common stock is expected to be listed on the New York Stock Exchange, which we refer to as the NYSE.

These are very important transactions, and a special meeting of the shareholders of Black Knight is being called to adopt and approve the merger agreement and the transactions contemplated thereby. Information about the Black Knight special meeting and the specifics of the proposed transactions is contained in this proxy statement/ prospectus. We urge you to read this proxy statement/prospectus and the documents incorporated by reference into this proxy statement/prospectus carefully and in their entirety.In particular, see "Risk Factors" beginning on page 27.

The mergers are conditioned upon, among other things, the approval of the Black Knight shareholders. The affirmative vote of (i) holders of record of a majority of the shares of Black Knight common stock outstanding entitled to vote thereon in favor of the adoption of the merger agreement and (ii) holders of record of a majority of the shares of Black Knight common stock outstanding entitled to vote thereon that are not owned, directly or indirectly, by FNF, any of its subsidiaries (including, without limitation, BKHI, New BKH, New Black Knight, Merger Sub One and Merger Sub Two), collectively, which we refer to as the FNF affiliated shareholders, or any officers or directors of the FNF affiliated shareholders, is required to consummate the BKFS merger. Pursuant to the merger agreement, FNF has agreed to vote shares of Class B common stock of Black Knight beneficially owned by it, currently representing approximately 54.29% of the outstanding voting securities of Black Knight common stock, in favor of the adoption of the merger agreement.

A special committee of disinterested directors of Black Knight, which we refer to as the Black Knight Special Committee, was formed for the purpose of evaluating the transactions contemplated by the merger agreement. The Black Knight Special Committee has (i) determined that the transactions contemplated by

the merger agreement, including the BKFS merger, and any related agreements entered by Black Knight in connection therewith, which we refer to as the related agreements, are fair to, and in the best interests of, Black Knight and its shareholders (other than New BKH or any of its affiliates, including, for the avoidance of doubt, FNF), (ii) approved and declared advisable the execution, delivery and performance of the merger agreement and the related agreements and the consummation of the transactions contemplated therein, (iii) recommended that the board of directors of Black Knight approves and declares advisable the execution, delivery and performance of the merger agreement and the related agreements and the consummation of the transactions contemplated therein, including the BKFS merger, and (iv) resolved to recommend approval of the merger agreement by the holders of shares of Black Knight common stock.

Whether or not you plan to attend the special meeting, please vote as soon as possible to make sure that your shares are represented at that meeting. If you do not vote, it will have the same effect as voting against the merger proposal.

The Black Knight Special Committee has approved and declared advisable the merger agreement and recommends that you vote FOR the adoption of the merger agreement.

Sincerely,  Thomas J. Sanzone Chief Executive Officer |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these transactions or the New Black Knight common stock to be issued in the merger or determined whether this proxy statement/prospectus is accurate or adequate. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated August 25, 2017 and is expected first to be mailed to shareholders on or about that date.

BLACK KNIGHT FINANCIAL SERVICES, INC.

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To Be Held On September 27, 2017

To the Shareholders of Black Knight Financial Services, Inc.:

Notice is hereby given that a special meeting of the shareholders of Black Knight Financial Services, Inc., a Delaware corporation, which we refer to as Black Knight, will be held at 10:00 a.m., local time, on September 27, 2017, at 601 Riverside Avenue, Jacksonville, Florida 32204, for the following purposes:

- 1.

- to consider and vote upon the adoption of the Agreement and Plan of Merger, dated as of June 8, 2017, by and among New BKH Corp., a Delaware corporation, Black Knight, Black Knight Holdco Corp., a Delaware corporation, New BKH Merger Sub, Inc., a Delaware corporation, BKFS Merger Sub, Inc. a Delaware corporation and Fidelity National Financial, Inc., a Delaware corporation; and

- 2.

- to consider and vote upon an adjournment of the special meeting, if necessary or appropriate, to permit further solicitation of proxies if there are not sufficient votes at the special meeting to approve the first proposal described above in accordance with the merger agreement.

The merger agreement and the mergers, along with the other transactions, which would be effected in connection with the mergers, are described more fully in the attached proxy statement/prospectus, and we urge you to read it carefully and in its entirety. Black Knight shareholders have no appraisal rights under Delaware law in connection with the mergers.

Adoption of the merger agreement requires the affirmative vote of (i) holders of a majority of the outstanding voting shares of Black Knight common stock and (ii) holders of a majority of the outstanding voting shares of Black Knight common stock that are not owned, directly or indirectly, by the FNF affiliated shareholders or any officers or directors of the FNF affiliated shareholders, each in favor of adoption of the merger agreement.

The special committee of the board of directors of Black Knight recommends that you vote FOR the adoption of the Agreement and Plan of Merger.

The board of directors of Black Knight has fixed the close of business on August 14, 2017 as the record date for determination of shareholders entitled to notice of, and to vote at, the special meeting and any adjournments or postponements thereof. Only shareholders of record at the close of business on the record date are entitled to notice of, and to vote at (in person or by proxy), the special meeting and at any adjournment or postponement thereof. Each shareholder is entitled to one vote for each share of our common stock held on the record date. A complete list of our shareholders of record entitled to vote at the special meeting will be available for inspection at our principal executive offices at least 10 days prior to the date of the special meeting and continuing through the special meeting for any purpose germane to the meeting. The list will also be available at the meeting for inspection by any shareholder present at the meeting.

To ensure that your shares of common stock are represented at the meeting, you should vote your proxy by completing, signing and dating the enclosed proxy card and returning it promptly in the enclosed envelope, whether or not you expect to attend the special meeting. You may revoke your proxy and vote in person if you decide to attend the meeting.

| Sincerely, | ||

| Michael L. Gravelle Executive Vice President, General Counsel and Corporate Secretary of Black Knight Financial Services, Inc. |

Dated: August 25, 2017.

This proxy statement/prospectus "incorporates by reference" important business and financial information about Black Knight from documents that are not included in or delivered with this proxy statement/prospectus. This information is available to you without charge upon request. For a more detailed description of the information incorporated by reference into this proxy statement/prospectus and how you may obtain it, see "Where You Can Find More Information" on page 195.

You also may obtain any of the documents incorporated by reference into this proxy statement/prospectus from Black Knight or from the Securities and Exchange Commission, which we refer to as the SEC, through the SEC's Internet web site at www.sec.gov. Documents of Black Knight are also available from Black Knight, without charge, excluding any exhibits to those documents that are not specifically incorporated by reference as an exhibit to this proxy statement/prospectus. Black Knight shareholders may request a copy of these documents in writing or by telephone by contacting the applicable department at:

Black Knight Financial Services, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

Attn: Corporate Secretary

If you would like to request documents, please do so by September 19, 2017, to receive them before the special meeting.

In addition, if you have any questions about the transactions, you may contact:

Black Knight Financial Services, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

Attn: Corporate Secretary

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This document, which forms a part of a registration statement on Form S-4 filed with the SEC by New Black Knight, constitutes a prospectus of New Black Knight under Section 5 of the Securities Act with respect to the shares of New Black Knight common stock to be issued to Black Knight and New BKH shareholders in connection with the mergers. This document also constitutes a proxy statement under Section 14(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and the rules thereunder, and a notice of meeting with respect to the special meeting of Black Knight shareholders to consider and vote upon the proposal to approve and adopt the merger agreement.

QUESTIONS AND ANSWERS ABOUT THE TRANSACTIONS | i | |||

SUMMARY | 1 | |||

SELECTED FINANCIAL DATA | 12 | |||

UNAUDITED COMPARATIVE HISTORICAL AND PRO FORMA PER SHARE DATA | 17 | |||

PER SHARE MARKET PRICE AND DIVIDEND INFORMATION OF BLACK KNIGHT | 19 | |||

UNAUDITED PRO FORMA COMBINED FINANCIAL INFORMATION | 20 | |||

RISK FACTORS | 27 | |||

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS | 46 | |||

THE COMPANIES | 48 | |||

THE TRANSACTIONS | 50 | |||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE MERGERS | 68 | |||

THE MERGER AGREEMENT | 71 | |||

THE REORGANIZATION AGREEMENT | 82 | |||

ADDITIONAL AGREEMENTS | 85 | |||

THL INTEREST EXCHANGE AGREEMENT | 88 | |||

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 90 | |||

BUSINESS OF NEW BLACK KNIGHT | 128 | |||

MANAGEMENT OF NEW BLACK KNIGHT FOLLOWING THE TRANSACTIONS | 142 | |||

COMPENSATION OF EXECUTIVE OFFICERS / COMPENSATION ARRANGEMENTS | 150 | |||

DESCRIPTION OF CAPITAL STOCK OF NEW BLACK KNIGHT | 182 | |||

COMPARISON OF RIGHTS OF SHAREHOLDERS BEFORE AND AFTER THE TRANSACTIONS | 187 | |||

THE SPECIAL MEETING | 191 | |||

LEGAL MATTERS | 195 | |||

EXPERTS | 195 | |||

WHERE YOU CAN FIND MORE INFORMATION | 195 | |||

INCORPORATION BY REFERENCE | 196 | |||

INDEX TO FINANCIAL STATEMENTS | ||||

Annex A—Agreement and Plan of Merger | ||||

Annex B—Reorganization Agreement |

QUESTIONS AND ANSWERS ABOUT THE TRANSACTIONS

- Q.

- What are the transactions described in this document?

- A.

- Black Knight Financial Services, Inc., which we refer to as Black Knight, and Fidelity National Financial, Inc., which we refer to as FNF, the beneficial owner of approximately 98.46% of the outstanding shares of Class B common stock of Black Knight, which we refer to as the Black Knight Class B common stock, currently representing 54.29% of the voting securities of Black Knight common stock and 54.29% of the Class A units, which we refer to as BKFS LLC Units or Units, of Black Knight Financial Services, LLC, which we refer to as BKFS LLC, have entered into a transaction involving the indirect distribution of Black Knight shares and BKFS LLC Units held by FNF to the holders of its FNF Group common stock. This transaction involves the following steps:

- •

- Black Knight Holdings, Inc., a wholly-owned subsidiary of FNF that we refer to as BKHI, will contribute to a newly formed corporation New BKH Corp., which we refer to as New BKH (i) all of the Black Knight Class B common stock indirectly owned by FNF and (ii) all of the BKFS LLC Units indirectly owned by FNF, in exchange for 100% of the shares of New BKH common stock, which we refer to as the contribution; following which BKHI will convert into a limited liability company and will then distribute to FNF all of the shares of New BKH common stock held by BKHI;

- •

- shares of New BKH will be distributed as a dividend to holders of the FNF Group common stock, which we refer to as the spin-off, and, together with the contribution, which we refer to as the separation; and

- •

- Black Knight and New BKH will merge with, and continue their existence as, subsidiaries of Black Knight Holdco Corp., which we refer to as New Black Knight, a newly-formed holding company established in connection with the transactions, collectively, which we refer to as the mergers.

We refer to the separation and mergers collectively as the transactions. The terms of the separation and mergers are set forth in the merger agreement and reorganization agreement, respectively, which are each described in this proxy statement/prospectus and attached to this proxy statement/prospectus as Annex A and Annex B, respectively.

- Q.

- What will happen to the holders of Black Knight Class B common stock and BKFS LLC Units?

- A.

- The shares of Black Knight Class B common stock are not affected by the merger agreement. Pursuant to the THL Interest Exchange Agreement (as described in "Additional Agreements—Certain Other Transactions and Relationships—THL Interest Exchange Agreement" below), immediately following the closing of the transactions contemplated by the merger agreement, the Black Knight Class B common stock and the BKFS LLC Units that are owned by certain affiliates of Thomas H. Lee Partners, LP, which we refer to as the THL Interest Holders, will be contributed to New Black Knight in exchange for a number of shares of New Black Knight common stock equal to the number of shares of Black Knight Class B common stock contributed. The remaining shares of Black Knight Class B common stock, which will be held by New BKH prior to the separation, will be cancelled for no consideration following the closing of the transactions contemplated by the merger agreement.

- Q.

- What will happen to the "Up-C" structure of Black Knight?

- A.

- Black Knight currently has an "Up-C" structure, which allows the owners of BKFS LLC to realize tax benefits associated with ownership interests in an entity that is treated as a partnership, or "passthrough" entity, for income tax purposes, while maintaining potential liquidity in Black

i

Knight through an exchange mechanism for cash or shares of Class A common stock of Black Knight, which we refer to as Black Knight Class A common stock. Following the completion of the transactions contemplated by the THL Interest Exchange Agreement, which we refer to as the THL Interest Exchange, and cancellation of all remaining outstanding Black Knight Class B common stock, the Up-C structure will no longer be in place, and BKFS LLC will be an indirect wholly-owned subsidiary of New Black Knight.

- Q.

- What am I being asked to vote on?

- A.

- Black Knight shareholders are being asked to adopt an Agreement and Plan of Merger, dated as of June 8, 2017, which we refer to as the merger agreement, entered into by and among FNF, New BKH, Black Knight, New Black Knight, New BKH Merger Sub, Inc., which we refer to as Merger Sub One, and BKFS Merger Sub, Inc., which we refer to as Merger Sub Two. Subject to the terms of the merger agreement:

- •

- Merger Sub One, a wholly-owned subsidiary of New Black Knight, will merge with and into New BKH, with New BKH as the surviving corporation, which we refer to as the New BKH merger; and

- •

- Merger Sub Two will merge with and into Black Knight, with Black Knight as the surviving corporation, which we refer to as the BKFS merger.

Neither merger will occur unless both mergers occur. Immediately prior to, and as a condition to, the mergers, FNF will complete the separation. Following the mergers, New BKH and Black Knight will be subsidiaries of New Black Knight. New Black Knight will become an independent publicly traded company.

You are also being asked to vote to approve the adjournment of the special meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting to adopt the merger agreement in accordance with its terms.

The vote of New BKH and FNF shareholders on the transactions is not required.

- Q.

- What will I receive in the mergers?

- A.

- As a result of the mergers, Black Knight Class A common shareholders (other than New BKH) will be entitled to receive one share of New Black Knight common stock for each share of Black Knight Class A common stock that they own. See "The Merger Agreement—Merger Consideration—Black Knight Exchange Ratio".

- Q.

- What will the New BKH shareholders receive in the merger?

- A.

- As a result of the mergers, New BKH shareholders will be entitled to receive one share of New Black Knight common stock for each share of New BKH common stock that they own. See "The Merger Agreement—Merger Consideration—New BKH Exchange Ratio".

- Q.

- Why is Black Knight proposing the transactions?

- A.

- Black Knight's principal purposes and reasons for the transactions are:

- •

- the transactions will increase Black Knight's independence of ownership and governance, eliminating FNF's majority control of Black Knight's common stock and the Black Knight board of directors, as well as FNF's majority control of the BKFS LLC Units;

- •

- the transactions will eliminate the market "overhang" resulting from FNF's approximately 54.29% ownership interest in Black Knight;

ii

- •

- the transactions may enhance the liquidity of Black Knight's common stock in the public trading market by increasing the float of New Black Knight's shares immediately after the transactions are completed as compared to the number of beneficial owners of Black Knight common stock prior to the transactions;

- •

- the transactions will eliminate the Up-C structure of Black Knight, thereby eliminating the complexity of Black Knight's capital structure and the reporting and administrative burden of maintaining an additional class of equityholders in BKFS LLC;

- •

- the transactions will allow FNF to dispose of its majority stock ownership in Black Knight and BKFS LLC in a manner that should be less disruptive to the public trading market for the shares of Black Knight's common stock than open market sales;

- •

- if the transactions are not consummated, there is a risk that Black Knight's shareholders (other than FNF and its affiliates) will not have the opportunity to receive a control premium in any future change of control transaction involving Black Knight; and

- •

- the transactions should allow New Black Knight to become eligible for index inclusion in the S&P Midcap 400 and potentially the S&P 500 because it is expected that following the completion of the transactions, New Black Knight will satisfy the S&P Index criteria related to public float that Black Knight does not currently satisfy.

- Q.

- Who will control New Black Knight after the transactions?

- A.

- Although FNF holds a majority noncontrolling interest in the common shares of Black Knight today, immediately following the transactions it is not expected that any person or group will hold a majority interest in New Black Knight.

- Q.

- How will New Black Knight's common stock trade?

- A.

- There is currently no public market for New Black Knight common stock. New Black Knight is expected to trade on the NYSE.

- Q.

- How does my ownership in Black Knight change as a result of the transactions?

- A.

- After the mergers, your rights as a shareholder will be governed by the amended and restated certificate of incorporation and amended and restated bylaws of New Black Knight rather than the current certificate of incorporation and bylaws of Black Knight. However, under the governing documents of New Black Knight, your rights as a shareholder of New Black Knight will be substantially similar to your rights as a shareholder of Black Knight. See the section entitled "Comparison of Rights of Shareholders Before and After the Transactions".

- Q.

- Will the proposal affect current operations? What about the future?

- A.

- The transactions are not expected to have a material effect on the conduct of day-to-day operations by New Black Knight. The Chief Executive Officer of Black Knight, Thomas J. Sanzone, will serve as the Chief Executive Officer of New Black Knight, and substantially all of the other officers of Black Knight will assume the same positions at New Black Knight.

- Q.

- What is the accounting treatment for the transactions?

- A.

- After the completion of the transactions, Black Knight's Up-C structure will no longer be in place. As a result, our consolidated statements of operations will reflect a higher effective tax rate more closely aligned with other C-corporations in the U.S. and will no longer reflect net earnings attributable to noncontrolling interests. Furthermore, the noncontrolling interests amount on our

iii

consolidated balance sheet immediately prior to completion of the transactions will be reclassified, resulting in an increase to shareholders' equity.

- Q.

- What are the U.S. federal income tax consequences to me of the mergers?

- A.

- A U.S. holder who exchanges Black Knight common stock or New BKH common stock for New Black Knight common stock pursuant to the mergers will not recognize any gain or loss, for U.S. federal income tax purposes, upon the exchange, except for gain or loss with respect to cash received in lieu of New Black Knight fractional shares. Such holder will have a tax basis in the New Black Knight common stock received equal to the tax basis of the Black Knight common stock or New BKH common stock surrendered therefor, reduced by any tax basis allocable to the fractional share interests in New Black Knight stock for which cash is received, provided either that the Black Knight common stock or New BKH common stock exchanged does not have a tax basis that exceeds its fair market value or, if it does, that a certain election to reduce the tax basis of the New Black Knight common stock received to its fair market value is not made. The holding period for the New Black Knight common stock received will include the holding period for the Black Knight common stock or New BKH common stock surrendered therefor.

- Q.

- Has FNF set a record date for the distribution of New BKH shares in the spin-off?

- A.

- No. FNF will publicly announce the record date when it has been determined. This announcement will be made prior to completion of the spin-off and the mergers.

- Q.

- What shareholder approvals are needed in connection with the transactions?

- A.

- Approval of the merger agreement requires the affirmative vote of (i) holders of a majority of the outstanding shares of Black Knight Class A common stock and Black Knight Class B common stock, voting together as a single class and entitled to vote thereon, and (ii) holders of a majority of the outstanding shares of Black Knight Class A common stock and Black Knight Class B common stock that are not owned, directly or indirectly, by FNF, any of its subsidiaries (including, without limitation, BKHI, New BKH, New Black Knight, Merger Sub One and Merger Sub Two), collectively, which we refer to as the FNF affiliated shareholders, or any officers or directors of the FNF affiliated shareholders, voting together as a single class and entitled to vote thereon, in each case in favor of adoption of the merger agreement. Pursuant to the merger agreement, FNF has agreed to cause all Black Knight Class B common stock beneficially owned by it, currently representing approximately 54.29% of the total number of outstanding shares of Class A and Class B Black Knight common stock, to be voted in favor of the adoption of the merger agreement.

No vote of FNF shareholders of any class is required in connection with the transactions. New BKH shareholders are not being requested to vote on the transactions, which have already been approved by FNF as the sole shareholder of New BKH prior to the spin-off.

- Q.

- What is the recommendation of the Special Committee of the Black Knight board of directors?

- A.

- The special committee of the Black Knight board of directors, which we refer to as the Black Knight Special Committee, recommends a vote FOR the proposal to adopt the merger agreement.

- Q.

- What do I need to do now?

- A.

- After carefully reading and considering the information contained in this proxy statement/prospectus, please respond by completing, signing and dating your proxy card or voting instruction card and returning it in the enclosed postage-paid envelope or by submitting your voting instruction by telephone or through the Internet, as soon as possible so that your shares may be

iv

represented and voted at the special meeting. If you hold shares registered in the name of a broker, bank or other nominee, that broker, bank or other nominee has enclosed or will provide a voting instruction card for use in directing your broker, bank or other nominee how to vote those shares.

- Q.

- How do I vote if my broker holds my shares in "street name"?

- A.

- Your broker will vote your Black Knight shares only if you provide instructions on how to vote. You should follow the directions provided by your broker regarding how to instruct your broker to vote your shares. Without instructions, your shares will not be voted, which will have the effect of a vote against the merger agreement.

- Q.

- What if I do not vote or abstain?

- A.

- If you do not vote, it will have the same effect as a vote against the merger and the possible adjournment of the special meeting. Shares that are not voted will not count for purposes of calculating a quorum, which is necessary to have a valid meeting of shareholders. If a quorum of shareholders is not present in person or by proxy at the meeting, no vote will be taken on the merger and the other proposals. If you sign your proxy card but do not indicate how you want to vote, your shares of Black Knight common stock will be voted for the merger and other proposals.

- Q:

- Can I change my vote after I have delivered my proxy?

- A:

- Yes. If you are a record holder of Black Knight stock, you can change your vote by:

- •

- completing, signing and dating a new proxy card and returning it by mail so that it is received prior to the meeting;

- •

- voting via telephone or via the Internet by following the instructions provided on your proxy card;

- •

- sending a written notice to the Corporate Secretary of Black Knight that is received prior to the meeting stating that you revoke your proxy; or

- •

- attending the meeting and voting in person by legal proxy, if applicable.

Internet and telephone voters may use the same procedure to revoke or change their votes as they used to cast their original votes. If your shares of Black Knight common stock are held in the name of a bank, broker or other fiduciary and you have directed such person(s) to vote your shares of Black Knight common stock, you should instruct such person(s) to change your vote or obtain a legal proxy to do it yourself. Telephone and internet voting will close at 11:59 p.m. Eastern time on the day before the meeting. Thereafter, voting (including revocation of proxies) can be made by mail or facsimile received prior to the meeting, or in person at the meeting.

- Q.

- Do I have appraisal rights?

- A.

- No. Black Knight shareholders do not have any appraisal rights in connection with the transactions.

- Q.

- When will the transactions occur?

- A.

- The transactions are expected to close by the end of the third quarter of 2017.

v

- Q.

- How will shares of New Black Knight be distributed to me?

- A.

- Prior to the effective time, we will deposit with the exchange agent for your benefit the shares of New Black Knight common stock issuable to you in the BKFS merger. At the effective time, Black Knight will instruct the exchange agent to make book-entry credits for the shares of New Black Knight common stock that you are entitled to receive. Since shares of New Black Knight common stock will be in uncertificated book-entry form, you will receive share ownership statements in place of physical share certificates.

- Q:

- Whom should I call with other questions?

- A:

- If you have questions about the transactions, the special meeting or if you need assistance in voting your shares, you should contact:

if you are a Black Knight shareholder:

Black Knight Financial Services, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

Attn: Michael L. Gravelle, Corporate Secretary

if you are an FNF shareholder:

Fidelity National Financial, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-8100

Attn: Michael L. Gravelle, Corporate Secretary

vi

This document is a proxy statement of Black Knight and a prospectus of New Black Knight. This summary highlights selected information from this document and may not contain all of the information that is important to you. To understand the separation, the mergers and other transactions more fully and for a more complete description of the legal terms of the transactions, you should read carefully this entire document, including the Annexes and the other documents we have referred you to, including in particular copies of the merger agreement and the reorganization agreement that are attached to this proxy statement/prospectus as Annex A and Annex B, respectively. See "Where You Can Find More Information" on page 195.

The Companies (see page 48)

Black Knight Financial Services, Inc.

Black Knight Financial Services, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

Black Knight Financial Services, Inc., which we refer to as Black Knight, together with its subsidiaries, is a leading provider of integrated technology, workflow automation, data and analytics to the mortgage and real estate industries. Black Knight's solutions facilitate and automate many of the mission-critical business processes across the entire mortgage loan life cycle, from origination until asset disposition. Black Knight differentiates itself by the breadth and depth of its comprehensive, integrated solutions and the insight it provides to its clients.

Black Knight has market-leading positions in mortgage processing and technology solutions combined with comprehensive real estate data and extensive analytic capabilities. Black Knight's solutions are utilized by U.S. mortgage originators and mortgage servicers, as well as other financial institutions, investors and real estate professionals, to support mortgage lending and servicing operations, analyze portfolios and properties, operate more efficiently, meet regulatory compliance requirements and mitigate risk.

Black Knight was incorporated in the State of Delaware on October 27, 2014 and on May 26, 2015, it completed its initial public offering in which it issued and sold 20,700,000 shares of its Class A common stock at a price of $24.50 per share. Black Knight is a holding company with an "Up-C" structure and, its business, as described above, is conducted through Black Knight Financial Services LLC, which we refer to as BKFS LLC, and its subsidiaries. Black Knight has a sole managing member interest in BKFS LLC, which grants it the exclusive authority to manage, control and operate the business and affairs of BKFS LLC and its subsidiaries pursuant to the limited liability company agreement of BKFS LLC.

Fidelity National Financial, Inc.

Fidelity National Financial, Inc.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-8100

Fidelity National Financial, Inc., which we refer to as FNF, has organized its business into two groups, FNF Group and FNF Ventures, which we refer to as FNFV.

Through FNF Group, FNF is a leading provider of (i) title insurance, escrow and other title-related services, including trust activities, trustee sales guarantees, recordings and reconveyances and home warranty products and (ii) technology and transaction services to the real estate and mortgage industries. FNF Group is the nation's largest title insurance company operating through its title

1

insurance underwriters—Fidelity National Title Insurance Company, Chicago Title Insurance Company, Commonwealth Land Title Insurance Company, Alamo Title Insurance and National Title Insurance of New York Inc.—which collectively issue more title insurance policies than any other title company in the United States. Through FNF's subsidiary ServiceLink Holdings, LLC, which we refer to as ServiceLink, FNF provides mortgage transaction services including title-related services and facilitation of production and management of mortgage loans. FNF Group also provides industry-leading mortgage technology solutions, including MSP®, the leading residential mortgage servicing technology platform in the U.S., through its majority-owned subsidiary, Black Knight.

Through the FNFV group, FNF owns majority and minority equity investment stakes in a number of entities, including American Blue Ribbon Holdings, LLC, Ceridian HCM, Inc., Fleetcor Technologies, Inc. and Digital Insurance, Inc.

Black Knight Holdco Corp.

Black Knight Holdco Corp.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

Black Knight Holdco Corp., which we refer to as New Black Knight, is a newly-formed corporation, which at the time of this disclosure has not been capitalized but will be prior to the spin-off, that was organized in the State of Delaware on February 3, 2017 for the purpose of holding shares of Black Knight and New BKH Corp., which we refer to as New BKH, following the mergers and serving as the new public company parent of Black Knight. Following the transactions, it is anticipated that New Black Knight's common stock will be listed on New York Stock Exchange, which we refer to as the NYSE.

New BKH Corp.

New BKH Corp.

601 Riverside Avenue

Jacksonville, Florida 32204

Telephone: (904) 854-5100

New BKH Corp. is a wholly-owned subsidiary of FNF. New BKH was organized in the State of Delaware on February 3, 2017 for the purpose of holding shares of Black Knight and the Class A units, which we refer to as the BKFS LLC Units or Units, of Black Knight Financial Services, LLC, which we refer to as BKFS LLC, and effecting the transactions.

New BKH Merger Sub, Inc. and BKFS Merger Sub, Inc.

New BKH Merger Sub, Inc. and BKFS Merger Sub, Inc., which we refer to as Merger Sub One and Merger Sub Two, respectively, are newly-formed corporations that were organized in the State of Delaware on February 3, 2017 for the purpose of effecting the transactions.

THL Interest Holders

THL Equity Fund VI Investors (BKFS-LM), LLC

THL Equity Fund VI Investors (BKFS-NB), LLC

c/o Thomas H. Lee Partners, L.P.

100 Federal Street, 35th Floor

Boston, Massachusetts 02110

Telephone: 617-227-1050

Each of THL Equity Fund VI Investors (BKFS-LM), LLC and THL Equity Fund VI Investors (BKFS-NB), LLC, which we refer to together as the THL Interest Holders, is managed by an affiliate

2

of Thomas H. Lee Partners, L.P. Each of the THL Interest Holders is a limited liability company formed in the State of Delaware for the purpose of holding shares of Black Knight and BKFS LLC Units.

The Transactions (see page 50)

The Separation (see page 50)

Pursuant to the reorganization agreement, FNF will engage in a series of corporate transactions, which we refer to as the separation, including the following:

- •

- Black Knight Holdings, Inc., which we refer to as BKHI, will contribute to New BKH (i) all of the shares of Class B common stock of Black Knight, which we refer to as Black Knight Class B common stock, indirectly owned by FNF and (ii) all of the BKFS LLC Units indirectly owned by FNF, in exchange for 100% of the shares of New BKH common stock, which we refer to as the contribution; following which BKHI will convert into a limited liability company and will then distribute to FNF all of the shares of New BKH common stock held by BKHI; and

- •

- Immediately prior to the consummation of the mergers, FNF will cause all of the shares of New BKH common stock held by FNF to be distributedpro rata to the holders of the FNF Group common stock by means of book-entry transfer through the exchange agent, which we refer to as the spin-off; provided that such distribution shall be subject to the conversion of such shares of New BKH common stock into shares of New Black Knight common stock, pursuant to the merger agreement.

After giving effect to the separation, New BKH, which will be 100% owned by holders of the FNF Group common stock, will own all of the shares of Black Knight Class B common stock and BKFS LLC Units beneficially owned by FNF prior to the separation.

The Mergers (see page 51)

Upon satisfaction or waiver of each of the conditions to the merger agreement and immediately after the separation, Merger Sub One will merge with and into New BKH, which we refer to as the New BKH merger. In the New BKH merger, each outstanding share of New BKH common stock (other than shares owned by New BKH) will be converted into one share of New Black Knight common stock. New BKH will be the surviving corporation in the New BKH merger.

Upon satisfaction or waiver of each of the conditions to the merger agreement and immediately following the New BKH merger, Merger Sub Two will merge with and into Black Knight, which we refer to as the BKFS merger, and together with the New BKH merger, which we refer to as the mergers. In the BKFS merger, each outstanding share of Class A common stock of Black Knight, which we refer to as Black Knight Class A common stock, (other than shares owned by Black Knight) will be converted into one share of New Black Knight common stock. Black Knight will be the surviving corporation in the BKFS merger.

Conditions to Completion of the Mergers (see page 79)

Consummation of the mergers is subject to the satisfaction of certain conditions, including, among others:

- •

- consummation of the separation, including the spin-off, in accordance with the reorganization agreement and applicable law;

- •

- obtaining the affirmative vote of (i) holders of a majority of the outstanding voting shares of Black Knight common stock and (ii) holders of a majority of the outstanding voting shares of Black Knight common stock that are not owned, directly or indirectly, by the FNF affiliated shareholders or any officers or directors of the FNF affiliated shareholders;

3

- •

- there being no law, injunction, judgment or ruling prohibiting the completion of the mergers or making the completion of the mergers illegal;

- •

- the Securities and Exchange Commission, which we refer to as the SEC, declaring effective the registration statement of New BKH on Form S-1 in connection with the spin-off and the registration statement of New Black Knight on Form S-4, of which this proxy statement/prospectus forms a part;

- •

- the shares of New Black Knight common stock deliverable to certain shareholders of New BKH, Black Knight and the THL Interest Holders having been approved for listing on NYSE;

- •

- each party's compliance in all material respects with its obligations under the merger agreement;

- •

- no event or circumstance shall have occurred that has or would reasonably have a "material adverse effect" on New BKH;

- •

- Black Knight's receipt of an opinion from Deloitte Tax LLP, which we refer to as Deloitte Tax, or another nationally recognized accounting or law firm, in form and substance reasonably acceptable to Black Knight, to the effect that the BKFS merger will qualify as a "reorganization" within the meaning of Section 368(a) of the Internal Revenue Code, which we refer to as the IRC, or, alternatively, as a transaction qualifying for nonrecognition of gain and loss under Section 351 of the IRC; and

- •

- New BKH's receipt of an opinion from Deloitte Tax, or another nationally recognized accounting or law firm, in form and substance reasonably acceptable to FNF and New BKH, to the effect that the New BKH merger will qualify as a "reorganization" within the meaning of Section 368(a) of the IRC or, alternatively, as a transaction qualifying for nonrecognition of gain and loss under Section 351 of the IRC.

Termination (see page 81)

The merger agreement may be terminated:

- •

- by mutual consent of the parties;

- •

- by any of the parties if the merger has not been completed by March 8, 2018, subject to certain extension rights;

- •

- by any of the parties if the merger is permanently enjoined;

- •

- by any of the parties if the Black Knight shareholder approval is not obtained;

- •

- by Black Knight, on the one hand, and New BKH, on the other hand, upon an incurable material breach of the merger agreement by the other party or parties; or

- •

- by New BKH if the Black Knight Special Committee withdraws or modifies its recommendation to the Black Knight shareholders regarding the mergers.

THL Interest Exchange Agreement (see page 88)

The THL Interest Exchange Agreement provides that immediately following the closing of the transactions contemplated by the merger agreement, the THL Interest Holders will contribute to New Black Knight all of the Black Knight Class B common stock and all of the BKFS LLC Units owned by the THL Interest Holders in exchange for a number of shares of New Black Knight common stock equal to the number shares of Black Knight Class B common stock contributed pursuant to the THL Exchange Agreement.

Black Knight's Reasons for the Transactions (see page 61)

In the course of reaching their decision to approve and declare advisable the merger agreement and the transactions contemplated thereby, the Black Knight Special Committee considered a number

4

of factors in their deliberations. Those factors are described in "The Transactions—Black Knight's Purpose and Reasons for the Transactions", "Recommendation of the Black Knight Special Committee—Recommendation of the Special Committee".

FNF's Reasons for the Transactions (see page 65)

In the course of reaching its decision to approve and declare advisable the merger agreement, the reorganization agreement and the transactions contemplated thereby, the FNF board of directors considered a number of factors in its deliberations. Those factors are described in "The Transactions—FNF's Reasons for the Transactions".

Accounting Treatment (see page 67)

After the completion of the transactions, Black Knight's Up-C structure will no longer be in place. As a result, our consolidated statements of operations will reflect a higher effective tax rate more closely aligned with other C-corporations in the U.S. and will no longer reflect net earnings attributable to noncontrolling interests. Furthermore, the noncontrolling interest amount on our consolidated balance sheet immediately prior to completion of the transactions will be reclassified, resulting in an increase to shareholders' equity.

Certain Material U.S. Federal Income Tax Consequences of the Mergers (see page 68)

A U.S. holder who exchanges Black Knight common stock or New BKH common stock for New Black Knight common stock pursuant to the mergers will not recognize any gain or loss, for U.S. federal income tax purposes, upon the exchange, except for gain or loss with respect to cash received in lieu of New Black Knight fractional shares. Such holder will have a tax basis in the New Black Knight common stock received equal to the tax basis of the Black Knight common stock or New BKH common stock surrendered therefor, reduced by any tax basis allocable to the fractional share interests in New Black Knight stock for which cash is received, provided either that the Black Knight common stock or New BKH common stock exchanged does not have a tax basis that exceeds its fair market value or, if it does, that a certain election to reduce the tax basis of the New Black Knight common stock received to its fair market value is not made. The holding period for the New Black Knight common stock received will include the holding period for the Black Knight common stock or New BKH common stock surrendered therefor.

Board of Directors and Management of New Black Knight (see page 66)

The directors of New Black Knight following the mergers will consist of the following six members that are the same as the current Black Knight directors: David K. Hunt and Ganesh B. Rao as Class I directors, each of whom shall have a term expiring in 2019, Richard N. Massey and John D. Rood as Class II directors, each of whom shall have a term expiring in 2020 and William P. Foley, II and Thomas M. Hagerty as Class III directors, each of whom shall have a term expiring in 2018. See "Management of New Black Knight Following the Transactions—Board of Directors".

The executive officers of Black Knight immediately prior to the effective time of the BKFS merger will be the initial executive officers of New Black Knight. See "Management of New Black Knight Following the Transactions—Management".

Listing (see page 68)

It is anticipated that shares of New Black Knight will be listed on the NYSE.

5

Interests of Certain Persons in the Transactions (see page 66)

You should be aware that some of the directors and officers of Black Knight have interests in the BKFS merger that may be in addition to or differ from those of Black Knight's shareholders, including, but not limited to:

- •

- the continued employment of Black Knight's executive officers as New Black Knight's executive officers and the continued service of Black Knight's directors as directors of New Black Knight;

- •

- the indemnification of officers and directors of Black Knight by New Black Knight for their services as such up to the time of the consummation of the mergers;

- •

- the fact that William P. Foley II is a director and Chairman of the board of FNF, and each of John D. Rood, Richard N. Massey and Thomas M. Hagerty are directors of FNF and are members of the Black Knight board of directors. FNF currently beneficially owns approximately 98.46% of the outstanding Class B common stock of Black Knight and approximately 54.29% of the outstanding BKFS LLC Units; and

- •

- the fact that Michael L. Gravelle, the Executive Vice President, General Counsel and Corporate Secretary of Black Knight is also the Executive Vice President, General Counsel and Corporate Secretary of FNF.

Special Meeting (see page 191)

Time, Date, Place. The special meeting of shareholders will be held at 10:00 a.m., local time, on September 27, 2017, at 601 Riverside Avenue, Jacksonville, Florida 32204.

Record Date. Only shareholders of record at the close of business on August 14, 2017, as shown in our records, will be entitled to vote, or to grant proxies to vote, at the special meeting. Each share of Black Knight common stock is entitled to one vote. As of the record date, there were 153,479,930 shares of Black Knight common stock outstanding and entitled to vote at the special meeting.

Required Vote (see page 192)

To approve the merger proposal, (i) the holders of a majority of the outstanding shares of Black Knight Class A common stock and Black Knight Class B common stock, voting together as a single class and entitled to vote thereon, and (ii) the holders of a majority of the outstanding shares of Black Knight Class A common stock and Black Knight Class B common stock that are not owned, directly or indirectly, by the FNF affiliated shareholders or the officers or directors of the FNF affiliated shareholders, voting together as a single class and entitled to vote thereon, in each case must vote in favor of adopting the merger agreement and approving the mergers. Because approval of the merger proposal requires the affirmative vote of a majority of shares outstanding and the affirmative vote of a majority of shares outstanding that are not owned, directly or indirectly, by the FNF affiliated shareholders or the officers or directors of the FNF affiliated shareholders, a Black Knight shareholder's failure to vote or abstention will have the same effect as a vote against the merger proposal.

To approve the proposal to adjourn the special meeting, if necessary, a majority of the shares of Black Knight common stock present in person or represented by proxy at the special meeting and entitled to vote must vote in favor of such proposal.

Pursuant to the merger agreement, FNF has agreed to cause all Black Knight Class B common stock beneficially owned by it, currently representing approximately 54.29% of the total number of outstanding shares of Class A and Class B Black Knight common stock, to be voted in favor of the adoption of the merger agreement.

6

No Rights of Dissenting Shareholders (see page 68)

Under Delaware law, you will not have dissenters' or appraisal rights in connection with the mergers or the transactions.

Recommendation of the Black Knight Special Committee

The Black Knight Special Committee has approved and declared advisable the merger agreement, and recommends that the Black Knight shareholders vote FOR the proposal to adopt the merger agreement.

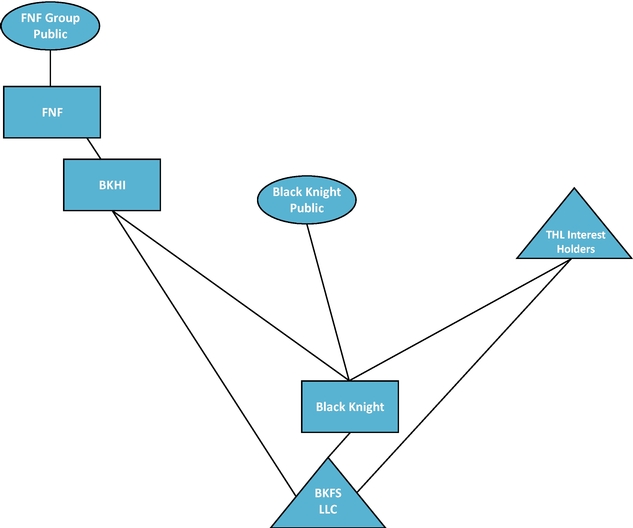

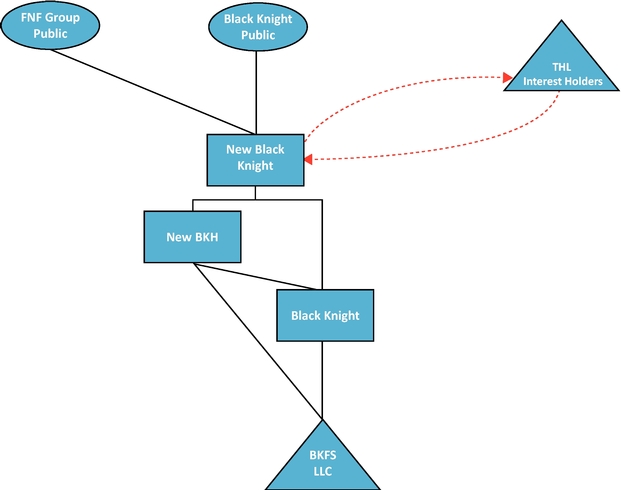

Visual Representation of the Transactions

Pre-Transaction Structure

7

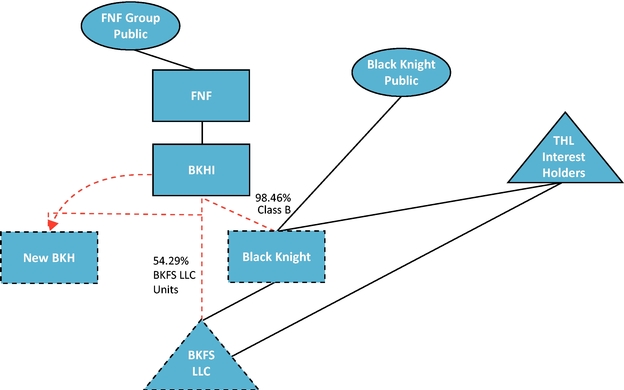

BKHI's Contribution to New BKH

BKHI will contribute to New BKH (i) all of the Black Knight Class B common stock indirectly owned by FNF and (ii) all of the BKFS LLC Units indirectly owned by FNF, in exchange for 100% of the shares of New BKH common stock.

8

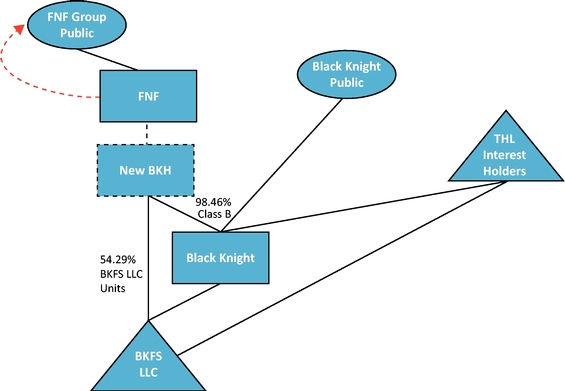

Distribution of New BKH Common Stock to Holders of FNF Group Common Stock

Shares of New BKH common stock will be distributed as a dividend to holders of FNF Group common stock.

9

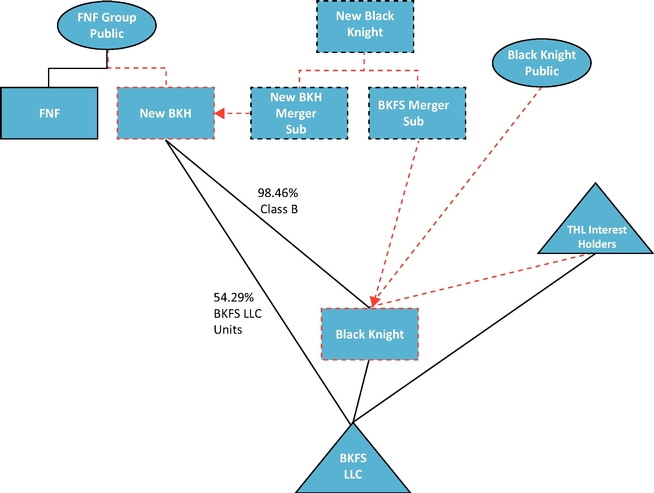

The Mergers

New BKH Merger Sub will merge with and into New BKH. In the New BKH merger, each outstanding share of New BKH common stock (other than shares owned by New BKH) will be converted into one share of New Black Knight common stock. New BKH will be the surviving corporation in the New BKH merger and will continue its existence as a subsdiary of New Black Knight.

Immediately following the New BKH merger, BKFS Merger Sub will merge with and into Black Knight. In the BKFS merger, each outstanding share of Class A common stock of Black Knight (other than shares owned by Black Knight) will be converted into one share of New Black Knight common stock. Black Knight will be the surviving corporation in the BKFS merger and will continue its existence as a subsidiary of New Black Knight.

10

THL Interest Exchange

THL Interest Holders will contribute to New Black Knight all of the Black Knight Class B common stock and all of the BKFS LLC Units owned by the THL Interest Holders in exchange for a number of shares of New Black Knight common stock equal to the number of shares of Black Knight Class B common stock contributed pursuant to the THL Exchange Agreement.

11

The following tables present historical financial data and should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the financial statements and the related footnotes thereto, included elsewhere in this proxy statement/prospectus. Certain reclassifications have been made to the prior year amounts to conform with the 2016 presentation.

On January 2, 2014, FNF acquired Lender Processing Services, Inc., which we refer to as LPS, and the transaction, which we refer to as the LPS Acquisition. As a result, LPS became an indirect, wholly-owned subsidiary of FNF. Following the LPS Acquisition, on January 3, 2014, a series of transactions were effected, which we refer to as the Internal Reorganization. Please refer to "Management's Discussion and Analysis of Financial Condition and Results of Operations—Our History—Acquisition of LPS by FNF and Subsequent Reorganization" on page 92 for additional information on the LPS Acquisition and the Internal Reorganization.

As a result of the Internal Reorganization, BKFS LLC acquired substantially all of the former Technology, Data and Analytics segment of LPS and Fidelity National Commerce Velocity, LLC, which we refer to as Commerce Velocity, a former indirect subsidiary of FNF. BKFS LLC did not acquire the former Transaction Services segment of LPS. On June 2, 2014, two wholly-owned subsidiaries of FNF contributed their respective interests in Property Insight, LLC, which we refer to as Property Insight, to BKFS LLC. In accordance with U.S. generally accepted accounting principles, which we refer to as GAAP, requirements for transactions between entities under common control, the Consolidated and Combined Financial Statements of BKFS LLC have been adjusted to reflect Commerce Velocity and Property Insight as of October 16, 2013, the date on which BKFS LLC was formed. LPS is considered the legal predecessor of BKFS LLC. For financial reporting purposes, BKFS LLC, including Commerce Velocity and Property Insight, is a predecessor for the period from October 16, 2013 through January 1, 2014. BKFS LLC is presented as the successor for periods subsequent to January 1, 2014.

Selected Historical Consolidated and Combined Financial Data of Black Knight

The Consolidated Statements of Operations data for the years ended December 31, 2016, 2015 and 2014 and the Consolidated Balance Sheets data as of December 31, 2016 and 2015 are derived from the audited Consolidated Financial Statements of Black Knight and BKFS LLC included in the Annual Report on Form 10-K, filed on February 24, 2017 and included elsewhere in this prospectus. The selected historical financial data as of June 30, 2017 and for the six months ended June 30, 2017 and 2016 are derived from our unaudited consolidated financial statements, and the Quarterly Report on Form 10-Q, filed with the SEC on July 28, 2017, included elsewhere in this prospectus. The Combined Statement of Operations data for the period from October 16, 2013 through December 31, 2013 and the Consolidated Balance Sheet data as of December 31, 2014 are derived from the audited Consolidated and Combined Financial Statements of Black Knight and BKFS LLC and are not included or incorporated by reference into this proxy statement/prospectus. The Combined Statement of Operations data for the period from October 16, 2013 through December 31, 2013 represents the combined financial data of Commerce Velocity and Property Insight that is not included or incorporated by reference into this proxy statement/prospectus.

12

We have not presented historical information for New BKH or New Black Knight because these entities have not had any corporate activity since their formation other than the issuance of shares of common stock in connection with their initial capitalization.

| | Successor | | Predecessor | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | ||||||||||||||||||||

| | Six months ended June 30, (Unaudited) | | | | | | |||||||||||||||

| | | | | | | ||||||||||||||||

| | Year ended December 31, | | Period from October 16, 2013 through December 31, 2013 | ||||||||||||||||||

| | | ||||||||||||||||||||

| | 2017 | 2016 | 2016 | 2015 | 2014 | | |||||||||||||||

| | | ||||||||||||||||||||

| | (In millions, except per share data) | | | ||||||||||||||||||

Statements of Operations Data: | |||||||||||||||||||||

Revenues | $ | 520.3 | $ | 497.4 | $ | 1,026.0 | $ | 930.7 | $ | 852.1 | $ | 15.0 | |||||||||

Expenses: | |||||||||||||||||||||

Operating expenses | 287.5 | 281.2 | 582.6 | 538.2 | 514.9 | 16.9 | |||||||||||||||

Depreciation and amortization | 102.9 | 97.4 | 208.3 | 194.3 | 188.8 | 1.1 | |||||||||||||||

Transition and integration costs | 4.5 | 1.1 | 2.3 | 8.0 | 119.3 | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Total expenses | 394.9 | 379.7 | 793.2 | 740.5 | 823.0 | 18.0 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Operating income (loss) | 125.4 | 117.7 | 232.8 | 190.2 | 29.1 | (3.0 | ) | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Other income and expense: | |||||||||||||||||||||

Interest expense, net | (30.7 | ) | (33.7 | ) | (67.6 | ) | (89.8 | ) | (128.7 | ) | — | ||||||||||

Other expense, net | (16.5 | ) | (4.8 | ) | (6.4 | ) | (4.6 | ) | (12.0 | ) | — | ||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Total other expense, net | (47.2 | ) | (38.5 | ) | (74.0 | ) | (94.4 | ) | (140.7 | ) | — | ||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Earnings (loss) from continuing operations before income taxes | 78.2 | 79.2 | 158.8 | 95.8 | (111.6 | ) | (3.0 | ) | |||||||||||||

Income tax expense (benefit) | 15.1 | 12.9 | 25.8 | 13.4 | (5.3 | ) | — | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Net earnings (loss) from continuing operations | 63.1 | 66.3 | 133.0 | 82.4 | (106.3 | ) | (3.0 | ) | |||||||||||||

Loss from discontinued operations, net of tax | — | — | — | — | (0.8 | ) | — | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Net earnings (loss) | 63.1 | 66.3 | 133.0 | 82.4 | (107.1 | ) | (3.0 | ) | |||||||||||||

Less: Net earnings (loss) attributable to noncontrolling interests | 42.7 | 43.5 | 87.2 | 62.4 | (107.1 | ) | (3.0 | ) | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Net earnings attributable to Black Knight | $ | 20.4 | $ | 22.8 | $ | 45.8 | $ | 20.0 | $ | — | $ | — | |||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | Six months ended June 30, (Unaudited) | | | | | | |||||||||||||||

| | | | | | | ||||||||||||||||

| | | May 26, 2015 through December 31, 2015 | | | | ||||||||||||||||

| | Year ended December 31, 2016 | | | | |||||||||||||||||

| | 2017 | 2016 | | | | ||||||||||||||||

Net earnings per share attributable to Black Knight Class A common shareholders: | |||||||||||||||||||||

Basic | $ | 0.30 | $ | 0.35 | $ | 0.69 | $ | 0.31 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Diluted | $ | 0.29 | $ | 0.34 | $ | 0.67 | $ | 0.29 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Weighted average shares of Class A common stock outstanding: | |||||||||||||||||||||

Basic | 67.7 | 65.9 | 65.9 | 64.4 | |||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Diluted | 153.0 | 152.7 | 67.9 | 67.9 | |||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

13

| | | | | | | | | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Successor | | Predecessor | ||||||||||||||||||

| | | ||||||||||||||||||||

| | June 30, (Unaudited) | | | | | | |||||||||||||||

| | December 31, | | | ||||||||||||||||||

| | | December 31, 2013 | |||||||||||||||||||

| | 2017 | 2016 | 2016 | 2015 | 2014 | | |||||||||||||||

| | | ||||||||||||||||||||

| | (In millions) | ||||||||||||||||||||

Balance Sheets Data: | |||||||||||||||||||||

Cash and cash equivalents | $ | 99.3 | $ | 28.2 | $ | 133.9 | $ | 186.0 | $ | 61.9 | $ | 7.4 | |||||||||

Total assets | $ | 3,719.2 | $ | 3,703.8 | $ | 3,762.0 | $ | 3,703.7 | $ | 3,598.3 | $ | 88.1 | |||||||||

Total debt (current and long-term) | $ | 1,554.7 | $ | 1,620.8 | $ | 1,570.2 | $ | 1,661.5 | $ | 2,135.1 | $ | — | |||||||||

Selected Historical Combined Financial Data of Commerce Velocity and Property Insight

The following selected unaudited historical combined financial information has been derived from the unaudited financial information of Commerce Velocity and Property Insight that is not included or incorporated by reference into this proxy statement/prospectus.

The selected unaudited financial information as of and for the year ended December 31, 2012 and the period January 1, 2013 through October 15, 2013 is derived from the historical financial records of FNF.

| | January 1, 2013 through October 15, 2013 | Year ended December 31, 2012 | |||||

|---|---|---|---|---|---|---|---|

| | (In millions) | ||||||

Statements of Operations Data: | |||||||

Revenues | $ | 58.2 | $ | 73.5 | |||

Net (loss) earnings | $ | (7.2 | ) | $ | 4.1 | ||

Balance Sheets Data: | |||||||

Total assets | $ | 79.1 | $ | 90.4 | |||

Selected Historical Consolidated Financial Data of LPS

The Consolidated Statement of Operations data for the day ended January 1, 2014 and the Consolidated Balance Sheet data as of January 1, 2014 are derived from the audited Consolidated Financial Statements of LPS. The Consolidated Statements of Operations data for the years ended December 31, 2013 and 2012 and Consolidated Balance Sheets data as of December 31, 2013 and 2012,

14

are derived from the audited Consolidated Financial Statements of LPS not included elsewhere in this proxy statement/prospectus.

| | | Year ended December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | Day ended January 1, 2014 | |||||||||

| | 2013(1) | 2012(1) | ||||||||

| | (In millions, except per share data) | |||||||||

Statements of Operations Data: | ||||||||||

Revenues | $ | — | $ | 1,716.2 | $ | 1,991.3 | ||||

Net (loss) earnings from continuing operations | $ | (39.0 | ) | $ | 104.2 | $ | 79.6 | |||

Net (loss) earnings | $ | (39.0 | ) | $ | 102.7 | $ | 70.4 | |||

Net earnings per share—basic from continuing operations | $ | 1.22 | $ | 0.94 | ||||||

Net earnings per share—basic | $ | 1.20 | $ | 0.83 | ||||||

Weighted average shares—basic | 85.4 | 84.6 | ||||||||

Net earnings per share—diluted from continuing operations | $ | 1.21 | $ | 0.94 | ||||||

Net earnings per share—diluted | $ | 1.19 | $ | 0.83 | ||||||

Weighted average shares—diluted | 85.9 | 84.9 | ||||||||

Balance Sheets Data: | ||||||||||

Cash and cash equivalents | $ | 278.4 | $ | 329.6 | $ | 236.2 | ||||

Total assets | $ | 2,446.6 | $ | 2,486.7 | $ | 2,445.8 | ||||

Total debt (current and long-term) | $ | 1,068.1 | $ | 1,068.1 | $ | 1,068.1 | ||||

Cash dividends per share | $ | — | $ | 0.40 | $ | 0.40 | ||||

- (1)

- On June 30, 2014, we completed the sale of PCLender, the results of which have been included in discontinued operations.

15

Selected Quarterly Financial Data of Black Knight and BKFS LLC (Unaudited)

Selected quarterly financial data is as follows:

| | Quarter Ended | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 31, | June 30, | September 30, | December 31, | |||||||||

| | (In millions, except per share data) | ||||||||||||

2017 | |||||||||||||

Revenues | $ | 258.1 | $ | 262.2 | |||||||||

Earnings from continuing operations before income taxes and noncontrolling interests | $ | 39.9 | $ | 38.3 | |||||||||

Net earnings | $ | 33.9 | $ | 29.2 | |||||||||

Net earnings attributable to Black Knight | $ | 12.2 | $ | 8.2 | |||||||||

Basic earnings per share attributable to Black Knight | $ | 0.18 | $ | 0.12 | |||||||||

Diluted earnings per share attributable to Black Knight | $ | 0.18 | $ | 0.11 | |||||||||

2016 | |||||||||||||

Revenues | $ | 241.9 | $ | 255.5 | $ | 267.1 | $ | 261.5 | |||||

Earnings from continuing operations before income taxes and noncontrolling interests | $ | 39.3 | $ | 39.9 | $ | 38.7 | $ | 40.9 | |||||

Net earnings | $ | 33.1 | $ | 33.2 | $ | 32.4 | $ | 34.3 | |||||

Net earnings attributable to Black Knight | $ | 11.4 | $ | 11.4 | $ | 11.2 | $ | 11.8 | |||||

Basic earnings per share attributable to Black Knight | $ | 0.17 | $ | 0.17 | $ | 0.17 | $ | 0.18 | |||||

Diluted earnings per share attributable to Black Knight | $ | 0.17 | $ | 0.17 | $ | 0.16 | $ | 0.17 | |||||

2015 | |||||||||||||

Revenues | $ | 227.2 | $ | 232.1 | $ | 233.6 | $ | 237.8 | |||||

Earnings from continuing operations before income taxes and noncontrolling interests | $ | 14.7 | $ | 8.2 | $ | 36.4 | $ | 36.5 | |||||

Net earnings | $ | 14.5 | $ | 7.8 | $ | 30.0 | $ | 30.1 | |||||

Net earnings attributable to Black Knight | $ | 0.3 | $ | 9.9 | $ | 9.8 | |||||||

Basic earnings per share attributable to Black Knight | $ | 0.01 | $ | 0.15 | $ | 0.15 | |||||||

Diluted earnings per share attributable to Black Knight | $ | — | $ | 0.15 | $ | 0.14 | |||||||

2014 | |||||||||||||

Revenues | $ | 202.5 | $ | 214.3 | $ | 215.0 | $ | 220.3 | |||||

Net (loss) earnings from continuing operations | $ | (89.7 | ) | $ | (24.6 | ) | $ | (0.2 | ) | $ | 8.2 | ||

Net (loss) earnings | $ | (89.9 | ) | $ | (24.4 | ) | $ | (1.0 | ) | $ | 8.2 | ||

16

UNAUDITED COMPARATIVE HISTORICAL AND PRO FORMA PER SHARE DATA

The following table presents unaudited comparative historical per share data for Black Knight and pro forma per share data for New Black Knight, after giving effect to the separation, the mergers and the THL Interest Exchange. The pro forma per share data of New Black Knight in the table below gives effect to the transactions as if all had been consummated on January 1, 2016, the beginning of the earliest time period presented, for purposes of presenting basic and diluted earnings per share and cash dividends declared per share for the six months ended June 30, 2017 and for the year ended December 31, 2016; and we have assumed the separation, the mergers and the THL Interest Exchange were completed on June 30, 2017 and December 31, 2016 for purposes of presenting the book value per share as of June 30, 2017 and December 31, 2016. This unaudited pro forma combined financial information was prepared using the accounting for transactions between entities under common control under GAAP, which is subject to change and interpretation.

For the Six Months Ended June 30, 2017

(In millions, except per share amounts)

| | Historical | Pro Forma(1) | |||||

|---|---|---|---|---|---|---|---|

Basic: | |||||||

Net earnings attributable to Black Knight | $ | 20.4 | $ | 44.3 | |||

Shares used for basic net earnings per share: | |||||||

Weighted average shares of Class A common stock outstanding | 67.7 | 152.5 | |||||

| | | | | | | | |

Basic net earnings per share | $ | 0.30 | $ | 0.29 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Diluted: | |||||||

Earnings before income taxes | $ | 78.2 | $ | 78.2 | |||

Income tax expense excluding the effect of noncontrolling interests | 33.9 | 33.9 | |||||

| | | | | | | | |

Net earnings / Net earnings attributable to Black Knight | $ | 44.3 | $ | 44.3 | |||

Shares used for diluted net earnings per share: | |||||||

Weighted average shares of Class A common stock outstanding | 67.7 | 152.5 | |||||

Weighted average shares of Class B common stock outstanding | 84.8 | — | |||||

Dilutive effect of unvested restricted shares of Class A common stock | 0.5 | 0.5 | |||||

| | | | | | | | |

Weighted average shares of common stock, diluted | 153.0 | 153.0 | |||||

| | | | | | | | |

Diluted net earnings per share | $ | 0.29 | $ | 0.29 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Dividends declared per diluted share of Class A common stock | $ | — | $ | — | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Book value per diluted share of common stock | $ | 12.55 | $ | 10.42 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

- (1)

- The unaudited pro forma basic and diluted net earnings per share data for New Black Knight assumes that all shares of Black Knight's Class B common stock are converted to shares of New Black Knight's common stock after giving effect to the separation, the mergers and the THL Interest Exchange. The unaudited pro forma diluted net earnings per share data includes the effect of unvested restricted shares.

17

For the Year Ended December 31, 2016

(In millions, except per share amounts)

| | Historical | Pro Forma(1) | |||||

|---|---|---|---|---|---|---|---|

Basic: | |||||||

Net earnings attributable to Black Knight | $ | 45.8 | $ | 102.9 | |||

Shares used for basic net earnings per share: | |||||||

Weighted average shares of Class A common stock outstanding | 65.9 | 150.7 | |||||

| | | | | | | | |

Basic net earnings per share | $ | 0.69 | $ | 0.68 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Diluted: | |||||||

Net earnings attributable to Black Knight | $ | 45.8 | $ | 102.9 | |||

Shares used for diluted net earnings per share: | |||||||

Weighted average shares of Class A common stock outstanding | 65.9 | 150.7 | |||||

Dilutive effect of unvested restricted shares of Class A common stock | 2.0 | 2.0 | |||||

| | | | | | | | |

Weighted average shares of Class A common stock, diluted | 67.9 | 152.7 | |||||

| | | | | | | | |

Diluted net earnings per share | $ | 0.67 | $ | 0.67 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Dividends declared per diluted share of Class A common stock | $ | — | $ | — | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Book value per diluted share of common stock | $ | 12.60 | $ | 10.66 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

- (1)

- The unaudited pro forma basic and diluted net earnings per share data for New Black Knight assumes that all shares of Black Knight's Class B common stock are converted to shares of New Black Knight's common stock after giving effect to the separation, the mergers and the THL Interest Exchange. The unaudited pro forma diluted net earnings per share data includes the effect of unvested restricted shares.

18

PER SHARE MARKET PRICE AND DIVIDEND INFORMATION OF BLACK KNIGHT

The following information on per share market price and dividend information is for Black Knight.

Prior to May 20, 2015, there was no active public market for Black Knight's common stock. On May 20, 2015, Black Knight became a listed company on NYSE and has traded under the ticker symbol "BKFS".

The following table sets forth, for the periods indicated, the high and low closing prices per share of our Class A common stock as reported on NYSE from May 20, 2015 to the date indicated. Black Knight has not paid any dividends.

| | High | Low | |||||

|---|---|---|---|---|---|---|---|

Year ended December 31, 2017 | |||||||

First quarter | $ | 40.00 | $ | 34.45 | |||

Second quarter | $ | 41.90 | $ | 38.10 | |||

Year ended December 31, 2016 | |||||||

First quarter | $ | 31.66 | $ | 26.00 | |||

Second quarter | 37.60 | 28.89 | |||||

Third quarter | 41.04 | 37.00 | |||||

Fourth quarter | 40.38 | 35.75 | |||||

Year Ended December 31, 2015 | |||||||

Second quarter (since May 20, 2015) | $ | 30.87 | $ | 27.11 | |||

Third quarter | 35.35 | 28.54 | |||||

Fourth quarter | 36.25 | 32.07 | |||||

19

UNAUDITED PRO FORMA COMBINED FINANCIAL INFORMATION

The following tables present selected unaudited pro forma combined financial information about our combined balance sheet and statement of earnings, after giving effect to the separation, the mergers and the THL Interest Exchange, as described below. The information under "Unaudited Pro Forma Combined Balance Sheet" in the table below gives effect to the separation, the mergers and the THL Interest Exchange as if all had been consummated on June 30, 2017. The information under "Unaudited Pro Forma Combined Statement of Earnings" in the table below gives effect to the separation, the mergers and the THL Interest Exchange as if all had been consummated on January 1, 2016, the beginning of the earliest time period presented. This unaudited pro forma combined financial information was prepared using the accounting for transactions between entities under common control under U.S. generally accepted accounting principles, or GAAP, which is subject to change and interpretation.

Subject to and in accordance with the reorganization agreement, FNF will engage in a series of corporate transactions, which we refer to as the separation, including the following:

- •

- Black Knight Holdings, Inc., which we refer to as BKHI, will contribute to New BKH (i) all of the shares of Class B common stock of Black Knight, which we refer to as Black Knight Class B common stock, indirectly owned by FNF and (ii) all of the BKFS LLC Units indirectly owned by FNF, in exchange for 100% of the shares of New BKH common stock, which we refer to as the contribution; following which BKHI will convert into a limited liability company and will then distribute to FNF all of the shares of New BKH common stock held by BKHI; and

- •

- Immediately prior to the consummation of the mergers, FNF will cause all of the shares of New BKH common stock held by FNF to be distributedpro rata to the holders of the FNF Group common stock by means of book-entry transfer through the exchange agent, which we refer to as the spin-off; provided that such distribution shall be subject to the conversion of such shares of New BKH common stock into shares of New Black Knight common stock, pursuant to the merger agreement.

After giving effect to the separation, New BKH, which will be 100% owned by holders of the FNF Group common stock, will own all of the Black Knight Class B common stock and BKFS LLC Units beneficially owned by FNF prior to the separation.