UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| FORM 10-K | ||

(Mark One)

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-38221

| PQ Group Holdings Inc. | ||

| Delaware | 81-3406833 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

300 Lindenwood Drive Malvern, Pennsylvania | 19355 | |

| (Address of principal executive offices) | (Zip Code) | |

(610) 651-4400 (Registrant’s telephone number, including area code) | ||

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Title of each class | Name of exchange on which registered | |

| Common stock, par value $0.01 per share | New York Stock Exchange | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ý | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

| Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of PQ Group Holdings Inc. voting and non-voting common equity held by non-affiliates as of June 29, 2018 (the last business day of the registrant’s most recently completed second fiscal quarter) based on the closing sale price of $18.00 per share as reported on the New York Stock Exchange was $711,130,212.

The number of shares of common stock outstanding as of February 25, 2019 was 135,705,568.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the PQ Group Holdings Inc. Proxy Statement for the 2019 Annual Meeting of Stockholders are incorporated by reference into Part III of this report.

PQ GROUP HOLDINGS INC.

INDEX—FORM 10-K

December 31, 2018

| Page | ||

| Item 1. | ||

| Item 1A. | ||

| Item 1B. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| Item 5. | ||

| Item 6. | ||

| Item 7. | ||

| Item 7A. | ||

| Item 8. | ||

| Item 9. | ||

| Item 9A. | ||

| Item 9B. | ||

| Item 10. | ||

| Item 11. | ||

| Item 12. | ||

| Item 13. | ||

| Item 14. | ||

| Item 15. | ||

| Item 16. | ||

i

PART I

Forward-looking Statements

This Annual Report on Form 10-K (“Form 10-K”) includes statements that express our opinions, expectations, beliefs, plans, objectives, assumptions or projections regarding future events or future results and therefore are, or may be deemed to be, “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 (the “Act”). The following cautionary statements are being made pursuant to the provisions of the Act and with the intention of obtaining the benefits of the “safe harbor” provisions of the Act. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should” and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, short- and long-term business operations and objections, and financial needs. Examples of forward-looking statements include, but are not limited to, statements we make regarding our liquidity, including our belief that our current level of operations, cash and cash equivalents, cash flow from operations and borrowings under our credit facilities and other lines of credit will provide us adequate cash to fund the working capital, capital expenditure, debt service and other requirements for our business for the foreseeable future. These forward-looking statements are subject to a number of risks, uncertainties and assumptions. Moreover, we operate in a very competitive and rapidly changing environment and new risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed herein may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Some of the key factors that could cause actual results to differ from our expectations include risks related to:

| • | our exposure to local business risks and regulations in different countries; |

| • | general economic conditions; |

| • | exchange rate fluctuations; |

| • | legal and regulatory compliance; |

| • | significant developments relating to the U.S. administration, U.S. courts’ or the United Kingdom’s referendum on membership in the European Union; |

| • | technological or other changes in our customers’ products; |

| • | our and our competitors’ research and development; |

| • | fluctuations in prices of raw materials and relationships with our key suppliers; |

| • | substantial competition; |

| • | non-payment or non-performance by our customers; |

| • | reliance on a small number of customers; |

| • | potential early termination or non-renewal of customer contracts in our refining services product group; |

| • | reductions in highway safety spending or taxes earmarked for highway safety spending; |

| • | seasonal fluctuations in demand for some of our products; |

| • | retention of certain key personnel; |

| • | realization of our growth projects; |

| • | potential product liability claims; |

| • | existing and potential future government regulation; |

| • | the extensive environmental, health and safety regulations to which we are subject; |

| • | disruption of production and distribution of our products; |

| • | risk of loss beyond our available insurance coverage; |

| • | product quality; |

| • | successful integration of acquisitions; |

| • | our joint venture investments; |

| • | our failure to protect our intellectual property and infringement on the intellectual property rights of third parties; |

| • | information technology risks; |

| • | potential labor disruptions; |

| • | litigation and other administrative and regulatory proceedings; and |

| • | our substantial indebtedness. |

1

The forward-looking statements included herein are made only as of the date hereof. You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. We undertake no obligation to update publicly any forward-looking statements for any reason after the date of this Form 10-K to conform these statements to actual results or to changes in our expectations.

| ITEM 1. | BUSINESS. |

PQ Group Holdings Inc. (“PQ Group Holdings” or the “Company”) was incorporated in Delaware on August 7, 2015. PQ Holdings Inc. (“PQ Holdings”), a manufacturer of specialty catalysts, materials and chemicals, was incorporated in Delaware on June 22, 2007. Founded in 1831, our business has a nearly 200-year history of innovation, enabling environmental improvements in fuel efficiency and emissions, safer highway and airport travel, and healthier personal care products, while improving sustainability of our planet. On October 3, 2017, PQ Group Holdings completed its initial public offering (“IPO”). Our common stock is listed on the New York Stock Exchange under the stock ticker “PQG”.

Eco Services Operations LLC (“Eco Services”), which acquired substantially all of the assets of Solvay USA Inc.’s sulfuric acid refining services business unit on December 1, 2014 (the “2014 Acquisition”), was incorporated in Delaware on July 30, 2014. On May 4, 2016, we consummated a series of transactions (the “Business Combination”) to reorganize and combine the businesses of PQ Holdings and Eco Services under a new holding company, PQ Group Holdings, pursuant to a reorganization and transaction agreement, dated August 17, 2015, as amended, by and among PQ Group Holdings, PQ Holdings, PQ Corporation, Eco Services, Eco Services Holdings LLC, Eco Services Group Holdings LLC and certain investment funds affiliated with CCMP Capital Advisors, LLC (now known as CCMP Capital Advisors, LP; “CCMP”). We refer to the business of PQ Holdings prior to the Business Combination as “legacy PQ” and the business of Eco Services prior to the Business Combination as “legacy Eco.” Unless the context otherwise indicates, the terms “PQ Group Holdings Inc.,” “we,”, “us,” “our,” or the “Company” mean PQ Group Holdings Inc. and subsidiaries.

Our Company

We are an integrated global provider of specialty catalysts, materials and chemicals, and services that enable environmental improvements, enhance consumer products, and improve personal safety. Our value-added products seek to address global demand trends that are often either the subject of significant environmental and safety regulations or are driven by consumer preferences for environmentally friendlier alternative products, which we believe positions us to grow sales in excess of gross domestic product growth rates and provides us with high-margin growth opportunities. Specifically, our products and solutions help companies produce vehicles with improved fuel efficiency and cleaner emissions. Our materials are critical ingredients in consumer products that make teeth brighter and skin softer. We produce highly engineered materials that make highways and airports safer for drivers and pilots. Because our products are predominantly inorganic and carbon-free, we believe we contribute to improving the sustainability of our planet.

We believe we are a leader in each of our product groups, holding what we estimate to be a number one or number two supply share position for products that generated more than 90% of our 2018 sales. We believe that our global footprint and efficient network of strategically located manufacturing facilities provide us with a strong competitive advantage in serving our customers both regionally as well as globally. We believe that we hold our leading supply share positions in the key regions that we serve.

We believe our products deliver significant value to our customers, as demonstrated by our profit margins. Our products typically constitute a small portion of our customers’ overall end-product costs yet are critical to product performance. Our catalysts are highly technical, customized products that require customer collaboration and significant lead and qualification time, capital investment resources, and intellectual property to develop. As a result, we have generally maintained stable margins through macro economic cycles.

In 2018, we served over 4,000 customers globally across many end uses and, as of December 31, 2018, operated 71 manufacturing facilities which are strategically located across six continents. We are highly diversified by business, geography, and end use, and in 2018 the majority of our sales were for applications that have historically had relatively predictable, consistent demand patterns driven by consumption or frequent replacement cycles.

2

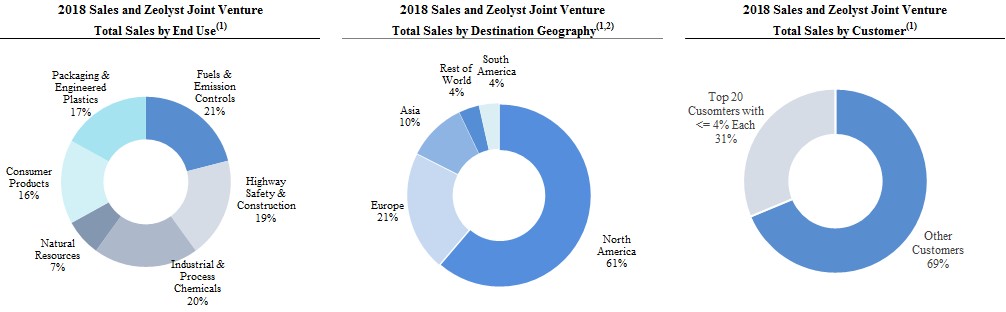

(1) | Percentage calculations include $156.7 million of total sales attributable to our Zeolyst Joint Venture (“Zeolyst JV”), which represents 50% of its total sales for the year ended December 31, 2018. Refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Basis of Presentation” for a description of the treatment of our Zeolyst Joint Venture in our consolidated financial information. |

(2) | Based on the delivery destination for products sold in 2018. |

Our Strategy

We intend to capitalize on our strong business foundation, market-based approach, and experienced management team to grow sales profitably, maintain high margins, deploy capital efficiently and generate free cash flow in order to create shareholder value. We believe that our long history of operational excellence and proven reliability, technology leadership, strong customer relationships, innovation track record and consistent business execution developed from our almost two centuries of combined industry experience positions us well to execute on our business strategy.

Our Industry

Our industry is characterized by constant development of new products and the need to support customers with new product innovation and technical services to meet their challenges, coupled with consistent product quality and a reliable source of supply in a safe and environmentally sustainable manner. Products sold to our customers can be a high value-add even when they represent only a small portion of the overall end product costs, and success can be achieved by helping customers improve their product performance, value, and quality. As a result, operating margins in this sector have historically been high and generally stable through economic cycles. In addition, many products in the specialty chemicals and materials industry benefit from economics that favor incumbent producers because the capital cost to expand existing capacity is typically significantly less than the capital cost necessary to build a new plant. The combination of attractive operating margins and generally predictable maintenance capital expenditure requirements can produce attractive cash flows.

3

Our End Markets

The table below summarizes our key end use applications and products as well as the significant growth drivers in those applications.

2016 Pro Forma Sales and Zeolyst JV Total Sales(1)(2) | |||||

2018 Sales and Zeolyst JV Total Sales(1) | 2017 Sales and Zeolyst JV Total Sales(1) | ||||

| Key End Uses | Significant Growth Drivers | Key PQ Products | |||

| Fuels & Emission Controls | 21% | 21% | 20% | • Global regulatory requirements to: | • Refinery catalysts |

| • Remove nitrogen oxides from emissions | • Emission control catalysts | ||||

| • Remove sulfur from diesel and gasoline | • Catalyst recycling services | ||||

| • Increase gasoline octane in order to improve fuel efficiency while lowering vapor pressure to regulated levels | • Silicate for catalyst manufacturing | ||||

| • Improve lubricant characteristics to improve fuel efficiencies | |||||

| Consumer Products | 16% | 16% | 18% | • Substitution of silicate materials for less environmentally friendly chemical additives in detergent and cleaning end uses | • Silica gels for edible oil and beer clarification |

| • Demand for improved quality and shelf life of beverages | • Precipitated silicas and zeolites for the surface coating, dentifrice, and dishwasher and laundry detergent applications | ||||

| • Demand for improved oral hygiene and appearance | |||||

| Highway Safety & Construction | 19% | 17% | 16% | • Demand for enhanced "dry and wet" visibility of road and airport markings to improve safety | • Reflective markings for roadways and airports |

| • Drive for weight reduction in cements | • Hollow glass beads, or microspheres, for cement additives | ||||

| Packaging & Engineered Plastics | 17% | 17% | 17% | • Demand for increased process efficiency and reduction of by-products in production chemicals | • Catalysts for high-density polyethlene and chemicals syntheses |

| • Demand for high-density polyethlene lightweighting of automotive components | • Antiblocks for film packaging | ||||

| • Enhanced properties in plastic composites for the automotive and electronics industries | • Solid and hollow microspheres for composite plastics | ||||

| Industrial & Process Chemicals | 20% | 21% | 21% | • Demand in the tire industry for reduced rolling resistance | • Silicate precursors for the tire industry |

| • Usage of silicate in municipal water treatment to inhibit corrosion in aging pipelines | • Glass beads, or microspheres, for metal finishing end uses | ||||

| • Growth in manufacturing North America driving demand for metal finishing | |||||

| Natural Resources | 7% | 8% | 8% | • More environmentally friendly drilling fluids for oil and gas production | • Silicates for drilling muds |

| • Recovery in global oil drilling/U.S. copper production | • Sulfuric acid for mining | ||||

| • Growing demand for lighter weight cements in oil and natural gas wells | • Microspheres for oil well cements | ||||

| • Silicates and alum for water treatment mining | |||||

| • Bleaching aids for paper | |||||

4

(1) | Percentage calculations include $156.7 million, $143.8 million and $131.3 million of total sales attributable to our Zeolyst Joint Venture, which represents 50% of its total sales for each of the years ended December 31, 2018, 2017 and 2016, respectively. Refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Basis of Presentation” for a description of the treatment of our Zeolyst Joint Venture in our consolidated financial information. |

(2) | Pro forma information gives effect to the consummation of the Business Combination and the related financing transactions as if they occurred on January 1, 2015. |

Our Competitive Strengths

Favorable Secular Growth Trends Across the Portfolio

We focus on serving end use applications where we believe significant future growth potential exists. Our products address our customers’ needs, which are typically driven either by regulatory regimes or consumer preferences, on a global basis. In addition, our product sales and development efforts are driven by regional infrastructure and development trends. In 2018, a majority of our sales were to end uses such as fuels and emission controls, consumer products, and highway safety and construction that generally do not exhibit as pronounced cyclicality as other applications. We believe that our products incorporate environmental and safety innovative solutions to address evolving customer demands, examples of which include the following:

Light- and heavy-duty diesel engines are subject to a broad set of regulatory requirements, and are expected to be subject to increasingly stricter standards. Countries typically adopt a set of standards that limit the amount of nitrogen oxides, carbon dioxide, and other emissions allowed for diesel engines. The US Environmental Protection Agency and European Union have led other nations in terms of standards that limit the amount of nitrogen oxides, carbon dioxide and other emissions for diesel engines. Current truck standards, Europe VI, have largely been in place since 2010 for North America and since 2014 for Europe. Other emerging regions are expected to implement similar standards over the next two years. Specifically, China announced that it is moving to China VI (equivalent to Euro VI) starting in 2020. India has also announced a similar plan starting in 2020. We believe that compliance with existing regulations as well as any future regulations will offer global opportunities for our zeolite catalyst product group to support our customers in meeting these standards through our sales of emission control catalysts.

Given stringent fuel efficiency standards that are driving the design of new engines and the resulting higher-octane gasoline requirements that can be achieved through alkylate blending, we believe that our refining services product group is well positioned to benefit from any related growth in demand for alkylates.

Increased use of plastics as a substitute for heavier and less versatile materials such as glass and metal is driving increased global demand for polyethylene capacity expansions and production. In particular, these expansions are shifting towards silica-based technology, which we believe will drive growth for our silica catalysts product group.

We believe that additional demand and higher standards for retroreflectivity (or visibility) for roadway and aviation markings will continue to benefit our materials product group. We benefit from increased use and density per mile of road markings that include our products, such as some states and municipalities instituting wider highway striping lines. Further, we anticipate a benefit from recent innovations, including our ThermoDrop® product, which simplifies the road striping operations for our customers by using a new durable thermal plastic road marking material and a new, faster-drying road marking system, Visilok®, which can reduce traffic disruption during striping operations and improve road worker safety by reducing the amount of time needed to complete the road marking process.

We also expect to benefit from trends towards the use of more environmentally friendly products where we believe we have opportunities to displace other less environmentally friendly materials through our Performance Chemicals group. Most of our products are manufactured from commonly found materials such as industrial sand and soda ash, which are more environmentally friendly than carbon-based products. For example, precipitated silicas are displacing carbon black in tires, and solid and hollow microspheres are displacing plastic volumes in lightweighting applications. We have also developed a family of gentle silica-based dentifrice abrasives that produce more effective cleaning toothpastes and we have developed a product family, Britesil silicates, which improves convenience while eliminating phosphates in automatic dishwashing applications.

5

Leading Supply Positions in Key Product Groups

We believe that we maintain a leading supply position in each of our major product groups, holding what we estimate to be the number one or two supply share position in 2018 for products that generated more than 90% of our sales. We believe that our global footprint and efficient network of strategically located manufacturing facilities provides us with a strong competitive advantage in serving our customers both globally and regionally, and that it would be costly for our competitors to replicate our network. These leadership positions serve industries that are attractive due to the need for customized and innovative products, stability of demand, and growth potential driven by the regulatory environment and consumer preferences. We produce value-added products that we believe are critical to the performance characteristics of our customers’ products.

In our Environmental Catalysts and Services business, we primarily compete on a global basis with the exception of our refining services product group, where we operate in North America and hold an estimated number one supply share position in the United States in sulfuric acid regeneration based on 2018 sales volume with an estimated supply share of greater than 50%. We are a leading supplier of refinery hydrocracking finished and support catalysts used to remove sulfur, and emission control catalysts used in the heavy- and light-duty diesel industries to reduce nitrogen oxide emissions. We are also a global supplier of silica catalysts and supports for polyethylene manufacturers and the exclusive supplier of methyl methacrylate (“MMA”) catalysts used in the patented Alpha process practiced by the global MMA leader.

In our Performance Chemicals and Materials business, where we are a leading supplier in the United States, Europe and Latin America, we largely support customers with regional and local production due to costs of shipping. For the chemicals product group, we estimate that we had approximately three times the sodium silicate supply share of our nearest competitor based on 2018 sales volume.

Innovation Track Record

Many of our products require close customer collaboration to address application challenges that are constantly evolving. As a result, we work with our customers over many years in order to develop products to meet customized specifications and performance characteristics while also maintaining strict quality standards. While we are unable to predict future shifts in customer demand, the long lead-time required for product development and commercialization, which can be up to ten years in our Environmental Catalysts and Services business, provides the opportunity for us to build long-term relationships with customers.

These long-term relationships have allowed us to innovate together with our customers to meet evolving demands. For example, we have developed zeolite-based catalysts that are an effective and efficient method to reduce pollutants from heavy- and light-duty diesel engines and enable our customers to meet increasingly stringent vehicle emission standards worldwide. In personal care applications, we have collaborated with leading consumer products companies over a number of years to develop a family of gentle silica-based dentifrice abrasives that produce more effective cleaning toothpastes. In addition, our proprietary silica catalyst has enabled development of a high strength high-density polyethylene (“HDPE”) resin that is used for making lightweight plastic gasoline tanks for automobiles. While we believe we are well positioned to capitalize on future innovation opportunities, the constantly evolving needs of our customers make it difficult to predict the pace or scope of future innovation opportunities.

Long-Term, High-Quality Customer Relationship

We collaborate with leading multinational companies that often seek global solutions. Our customers include large industrial companies such as BASF, Honeywell, and 3M, and global catalyst producers such as Albemarle and W.R. Grace. We also supply catalysts to leading chemical and petrochemical producers such as BASF, Dow Chemical, Lucite, LyondellBasell, and Shell. We supply personal care ingredients and additives to leading consumer products companies such as Unilever and Colgate-Palmolive. We have long-term relationships with our top ten customers, based on 2018 sales, that average more than 50 years. In addition, our customer base is diversified, with our top ten customers in 2018 representing approximately 23% of our sales for the year ended December 31, 2018 and no customer representing more than 4% of our sales during this period. However, the percentage of our sales generated by our top customers may increase in the future as a result of changes in industry dynamics or shifts in customer demand and contracts.

6

Pass-through of Raw Material Costs and Long Term Customer Arrangements

We have been able to mitigate the impact of raw material or energy price volatility using a variety of mechanisms, including hedging and raw material cost pass-through clauses in our sales contracts and other adjustment provisions. For the year ended December 31, 2018, approximately 40% of our Performance Chemicals sales (mostly comprised of sodium silicate sales) were derived from contracts that included raw material pass-through clauses. Most of our refining services contracts feature minimum volume protection and/or quarterly price adjustments for items such as commodity inputs, labor, the Chemical Engineering Plant Cost Index or natural gas. In 2018, approximately 80% of our refining services product group sales were sold under contracts that included some form of raw material pass-through clause. These price adjustments generally reflect our refining services actual cost structure in producing sulfuric acid, and tend to provide us with some protection against volatility in labor, fixed costs and raw material pricing. Freight expenses are generally passed through directly to customers.

Our products are predominantly inorganic and carbon-free, and are produced from readily available raw materials such as industrial sand and soda ash, which prices have historically been less volatile than oil. We also use natural gas in our furnaces where our North American facilities have benefited from the plentiful supplies of shale gas. In addition, we have long-term supply contracts with many of our key raw materials suppliers across our product groups.

Within our Environmental Catalysts and Services business, we partner with customers under long-term contract agreements, mutually exclusive product supply arrangements and/or specified products for certain license production processes. In our refining services product group, approximately 70% of our production capacity serves customers with five to ten year take or pay contracts for our regeneration product line. Excluding contracts with automatic evergreen provisions, approximately 60% of our sulfuric acid volume for the year ended December 31, 2018 was under contracts expiring at the end of 2020 or beyond.

In our silica catalysts product group, we supply under various term agreements ranging from 1 to 10 years for each of polyolefin catalysts, silica supports and support catalysts, and are a mutually exclusive supplier of methyl methacrylate catalyst to a leading global producer. In our zeolite catalysts product group, we operate with a mix of evergreen and various term contracts ranging from 1 to 3 years to supply catalysts and zeolite powders for the refining, petrochemical and chemical industries and nitrogen oxide control catalysts for diesel transportation industries. Within the Performance Chemicals and Materials business, our performance chemical product group operates under customer supply contracts ranging from 1 to 5 years. Our performance materials product group typically operates under customer supply contracts that typically last one year.

Stable Margins and Cash Flow Generation Across Macroeconomic Cycles

We have demonstrated the ability to maintain stable margins while continuing to grow our business in different macroeconomic environments. We believe that the stability of our margins and cash flows during this period is because our value-added products, which are critical to the performance of our customers’ products, typically represent only a small portion of our customers’ overall end-product costs.

Our cash flow generation has been driven, in part, by our disciplined capital investment and tax attributes that may also provide cash flow benefits in the future. As of December 31, 2018, we had $284.2 million of net operating losses for U.S. federal income tax purposes, along with related net operating losses for state tax purposes, and $344.2 million of tax deductible intangibles and goodwill, both of which may provide us with additional cash tax savings in future years in which we generate taxable income.

Experienced Management Team

Our senior management team has substantial industry experience and a proven track record. Their cumulative industry experience extends to a broad range of execution capabilities, including acquisition integration, strategic management, operations, sales and marketing, and new product and application development. In 2016, our management team integrated legacy Eco into our Environmental Catalysts and Services business while also growing the business and successfully implementing cost reduction initiatives. Our senior management team has also reorganized our company from a products-based business to a markets-based business to better align our offerings with the needs of our customers. There is a renewed focus on serving our customers by developing solutions through technical sales, services, and product development, and we have added additional management personnel experienced in innovation and market driven organizations.

7

Our Business Segments

We are an integrated, global provider of specialty catalysts, materials and chemicals, and services that share common end uses, manufacturing techniques, and process technology. For example, all of our product groups address challenges faced by global automotive companies to meet increasingly strict fuel efficiency standards. Our manufacturing platform is based on furnace technology and proprietary knowledge developed from almost two centuries of combined experience applying silicates chemistry production and the development of applications across a broadening set of end uses. All of our product groups produce materials through our furnace process, other than our silica catalysts and zeolite catalysts product groups, which are derivatives of our Performance Chemicals product group. We believe we have a differentiated capability around furnace operations that enables us to operate more efficiently than most of our competitors.

We conduct operations through two reporting segments: (1) Environmental Catalysts and Services, and (2) Performance Materials and Chemicals. In our Environmental Catalysts and Services segment, we have three product groups: silica catalysts, zeolite catalysts, and refining services. We operate our zeolite catalyst product group through Zeolyst International and Zeolyst C.V. (our 50% owned joint venture with CRI Zeolites, an affiliate of Royal Dutch Shell plc. that we refer to collectively as our “Zeolyst Joint Venture”). In our Performance Materials and Chemicals segment, we have two product groups: performance materials and performance chemicals.

The table below summarizes certain information regarding our two reporting segments and our five product groups for the year ended December 31, 2018.

| Year ended December 31, 2018 | |||||||||||||||||||||||||

| Segments and Product Groups | Sales | % of Total Sales | Zeolyst Joint Venture Sales(1) | % of Total Sales and Zeolyst Joint Venture Sales(1)(2) | Net Income | Adjusted EBITDA(1) | % of Total Adjusted EBITDA(1)(3) | ||||||||||||||||||

| (in millions, except percentages) | |||||||||||||||||||||||||

| Environmental Catalysts & Services | |||||||||||||||||||||||||

| Silica Catalysts | $ | 72.1 | 4.5 | % | $ | — | 4.1 | % | |||||||||||||||||

| Zeolite Catalyst | — | — | % | 156.7 | 8.9 | % | |||||||||||||||||||

| Refining Services | 455.6 | 28.3 | % | — | 25.8 | % | |||||||||||||||||||

| Subtotal | $ | 527.7 | 32.8 | % | $ | 156.7 | 38.7 | % | $ | 257.6 | 51.4 | % | |||||||||||||

| Performance Materials & Chemicals | |||||||||||||||||||||||||

| Performance Chemicals | $ | 717.3 | 44.6 | % | $ | — | 40.6 | % | |||||||||||||||||

| Performance Materials | 378.3 | 23.5 | % | — | 21.4 | % | |||||||||||||||||||

| Sales Eliminations | (11.8 | ) | (0.7 | )% | — | (0.7 | )% | ||||||||||||||||||

| Subtotal | $ | 1,083.8 | 67.4 | % | $ | — | 61.3 | % | $ | 243.4 | 48.6 | % | |||||||||||||

| Eliminations/Corporate | (3.3 | ) | (0.2 | )% | — | (37.0 | ) | ||||||||||||||||||

| Total | $ | 1,608.2 | 100.0 | % | $ | 156.7 | 100.0 | % | $ | 58.3 | $ | 464.0 | 100.0 | % | |||||||||||

(1) | Percentage calculations include $156.7 million of total sales attributable to our Zeolyst Joint Venture, which represents 50% of its total sales for the year ended December 31, 2018. Refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Basis of Presentation” for a description of the treatment of our Zeolyst Joint Venture in our consolidated financial information. |

(2) | Percentage calculations exclude $3.3 million in intersegment sales eliminations. |

(3) | Percentage calculations exclude $37.0 million in corporate expenses. |

8

Environmental Catalysts & Services

Our Environmental Catalysts and Services business is a leading global innovator and producer of catalysts for the refinery, emissions control, and petrochemical industries and is also a leading provider of catalyst recycling services to the North American refining industry. We believe our products are critical for our customers in these growing applications and impart essential functionality in chemical and refining production processes and in emission control for engines. Our catalysts are highly technical and customized for our customers, and can require up to ten years of development and collaboration with customers in order to commercialize. Catalyst specifications are constantly evolving in order to address changing customer demands and requirements for lower cost and improved quality. As a result, we must continuously collaborate with our customers to create new and more efficient pathways for the production of chemicals and fuels.

Silica Catalysts. In our silica catalysts product group, we sell both the finished catalyst and catalyst supports, which are critical catalyst components for the production of HDPE, a high strength and high stiffness plastic used in packaging films, bottles, containers, and other molded applications. We also produce a catalyst that is used globally for the production of methyl methacrylate, the monomer for acrylic engineering resins, a clear scratch-resistant plastic used in sheet or molded form to replace glass and as a durable surface coating. Because these catalysts are highly technical and customized for our customers to produce resins with specific properties, they are often covered under long-term supply agreements and, in some cases, we are a customer’s sole source supplier. In addition, we produce silica products that are used to prevent opposite faces of polyolefin and polyester films from adhering to one another during manufacturing or otherwise.

Zeolite Catalysts. Our zeolite catalysts product group is a leading global supplier of emission control catalysts as well as a supplier of specialty catalysts, precursors, and formulations to refineries and downstream petrochemicals and chemical companies. We operate this product group through our 50% share in our Zeolyst Joint Venture. These specialty zeolite-based catalysts are sold to the emission control industry for use in diesel emission control units in both on-road and non-road diesel engines. In addition, our zeolite catalysts product group is a leading supplier to the hydrocracking catalyst industry as a direct seller and supplier to other catalyst suppliers.

Many of our zeolite powders are used in an advanced emission control technology called selective catalytic reduction. This process uses ammonia to react with engine exhaust gases via our catalysts in order to convert nitrogen oxides (NOx), a pollutant, into nitrogen and water. We believe that our zeolite catalysts can enable selective catalytic reduction technology to reduce the amount of nitrogen oxides in such exhaust gases by more than 90%. We believe that this technology is one of the most cost-effective methods to reduce diesel engine emissions. Emission control regulations have created demand for this technology, and we believe that future regulations will generate additional growth and development opportunities for this technology and, as a result, our zeolite catalysts and precursors.

Refining Services. In 2018, we estimate that our refining services product group had a regenerated sulfuric acid supply share in excess of 50% in the United States, which we believe is substantially larger than our closest competitor.

Sulfuric acid is the primary catalyst used in the production of alkylates for gasoline production at refineries. Alkylate is a critical gasoline additive that increases octane and lowers vapor pressure. Alkylate is also a major component of premium gasoline which is needed in order for turbocharged engines to meet increasingly stringent fuel efficiency standards. Our refining services product group provides recycling and end-to-end logistics for refiners who use sulfuric acid in their alkylation units. These recycling units also produce virgin sulfuric acid and sodium bisulfate, which we sell into the water treatment, mining, and general industrial and chemicals industries.

After sulfuric acid is used in an alkylation unit, it becomes spent acid, which is diluted with water and hydrocarbons, and then needs to be recycled before it can be reused. Sulfuric acid regeneration enables refineries to manage their spent acid and obtain fresh acid for reuse in their alkylation processes. Because storage space for fresh and spent acid is typically limited, and the cost to refineries of interruption to their alkylation units would be significant, refineries seek to have a continuous and reliable source of supply for sulfuric acid. By providing regeneration services, as well as purchasing by-product sulfur from customers as a source of energy and for use in manufacturing virgin sulfuric acid, we believe that we provide our refining customers with a full solution for their sulfuric acid needs.

Sulfuric acid is created either through the burning of sulfur in furnaces, or as a by-product of other industrial processes, primarily the smelting of copper and other base metals. We produce a range of high quality virgin sulfuric acid products by burning sulfur in our plants for supply to a diverse set of end uses. Sulfur-burned acid is generally considered to be of higher purity and quality than smelter-produced acid and, as a result, smelter-produced acid is not suitable for some industrial users including several of our larger customers who require higher quality and differentiated sulfuric acid products, such as super-saturated sulfuric acid (oleum) and other high purity specialty acids. Virgin sulfuric acid and regenerated sulfuric acid are

9

manufactured in our regeneration plants using the same production equipment and, in addition, we have one facility in Houston, Texas that produces only virgin sulfuric acid from sulfur.

Competition

Our silica catalysts and zeolite catalysts products groups are leading global catalyst platforms that primarily produce catalysts and services for customers in the petrochemicals and refining industries. In these areas we primarily compete with other global producers such as W.R. Grace, BASF, UOP, and Albemarle, as well as other niche competitors such as Tosoh, Axens, and Haldor Topsoe, and we typically compete on the basis of performance, product consistency, reliability, and responsiveness to changes in customer demand.

Our refining services product group is highly regionalized due to shipping costs and our customer integration requirements. Our network of facilities is concentrated in the major areas of growth in sulfuric acid demand in the United States. Approximately 60% of United States refining capacity is located in the Gulf Coast region and California and our plant locations in these key refining regions enables us to maintain highly efficient supply chain networks with our customers, including in some cases captive pipelines connecting us to our refinery customers. In addition product can be shipped by barge, rail and truck. We compete in the North American refining services industry with competitors such as Chemtrade and Veolia and we compete on the basis of price, reliability, and responsiveness to changes in customer demand, which is a function of scale, proximity to customer locations and operational expertise. We believe that we benefit from industry economics that favor incumbent producers because the capital cost to expand existing capacity is typically significantly less than the capital cost necessary to build a new plant and new plants can involve more challenges in obtaining the necessary local, regional and state permits. In addition, existing supply chains, including captive pipeline connections and other transportation logistics add to the competitive advantages available to incumbent producers. As a result, we believe that our integrated and strategically located network of facilities and end-to-end logistics assets in the United States provide us with a significant competitive advantage and would be costly for our competitors to replicate.

Manufacturing

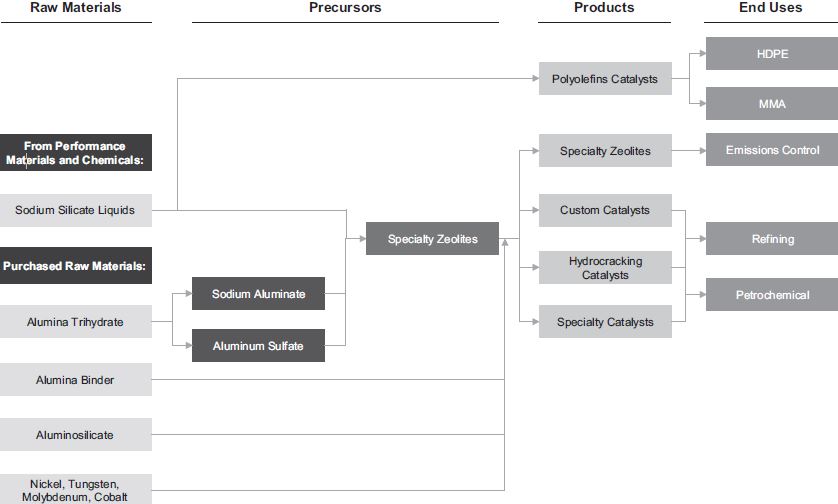

We manufacture our zeolyst-based catalyst products using sodium silicate liquids purchased directly from our performance chemicals product group to make specialty zeolite products. These zeolites are either used directly to produce catalysts or are sold as a precursor to other catalyst manufacturers.

Catalyst Manufacturing Platform

10

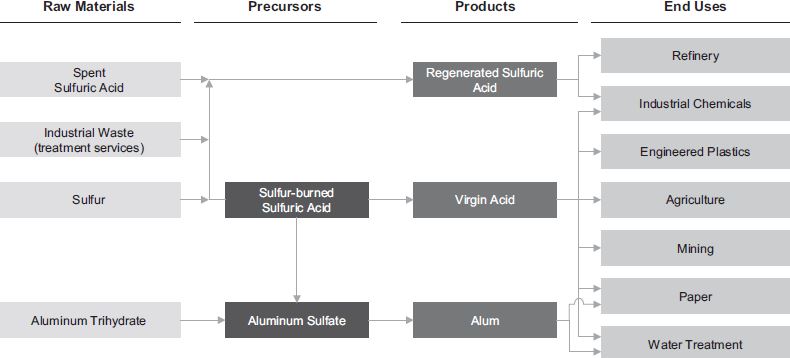

We produce regenerated sulfuric acid and virgin sulfuric acid through our furnace operations. Regenerated sulfuric acid is produced by breaking down the spent acid in our furnace into the usable components of sulfuric acid and water. Virgin sulfuric acid is produced by burning sulfur and certain sulfur-rich components at high temperatures within a furnace. The chart below summarizes the manufacturing platform for our refining services product group.

Refining Services Manufacturing Platform

Performance Materials & Chemicals

Our Performance Materials and Chemicals business is a silicates and specialty materials producer with leading supply positions for the majority of our products sold in North America, Europe, South America, Australia and Asia, except China, serving diverse and growing end uses such as personal and industrial cleaning products, highway beads, fuel efficient tires (“green tires”), surface coatings, and food and beverage. Our products are essential additives, ingredients, and precursors that are critical to the performance characteristics of our customers’ products, yet typically represent only a small portion of our customers’ overall end-product costs. We believe that our global footprint enables us to compete more effectively on a global basis due to the costs associated with shipping these products over extended distances. We believe that our network of strategically located manufacturing facilities allows us to serve our customers at a lower cost than our competitors and with quicker delivery times for our products. Our products are also used in some cases as a substitute for less environmentally friendly materials. For example, specialty silicates are displacing phosphates in dish detergents, precipitated silicas are displacing carbon black in tires, and hollow and solid microspheres are displacing plastic volumes in transportation lightweighting applications. Our Performance Materials and Chemicals business consists of two product groups: performance chemicals and performance materials.

Performance Chemicals. Our performance chemicals product group includes silicate products and derivatives, which are used in a variety of applications such as matting agents in surface coatings, clarifying agents for edible oils and beverages, precursors for green tires, and additives for cleaning and personal care products. Silicates are a family of products manufactured primarily from readily available materials, such as industrial sand and soda ash. These raw materials are typically fused in a furnace and then dissolved in water under pressure to form water-soluble silicates for use in our downstream products, such as precipitated silica and silica gels. We sell our performance chemicals products to customers who use silicates as precursors, such as sodium silicates that are used in the growing precipitated silica end uses, as well as for downstream derivative products, such as silicas used as additives in toothpaste formulation and silica gels that are used as adsorbents in food and beverage manufacturing.

Our performance chemicals product group, which is the backbone of our additives and catalyst platform, is highly regionalized because of the expense of shipping sodium silicates extended distances due to their water content. As a result, our network of regional silicate plants is strategically located to support the customers that we serve. In addition, we maintain

11

a few larger dedicated facilities to service our derivative products. Our performance chemicals product technology requires significant know-how and scale in order to be able to operate in a cost effective manner. We believe that we are the only global silicates producer who can supply all of the major regions, excluding China, and we estimate that we have three times the sodium silicates supply share as our nearest competitor based on 2018 sales volume. Key end uses for our performance chemicals products include catalyst precursors, food and beverage, personal care, cleaning products, coatings, tires, soil stabilization and paper de-inking.

Silicates. Silicates and their family of derivatives, such as silicas, have functional attributes that are used as additives and ingredients to enhance product performance as binders, fillers, flow control agents, and carriers in our customers’ products. Our silicates are used in a diverse range of applications. In detergents and cleaning products, silicates provide corrosion inhibition, alkalinity, emulsification, and deflocculation. In construction materials such as roofing granules, cement, ceramics, adhesives, and coatings, our products are used as a binding agent. In addition, our products are ingredients in consumer products, including personal care and consumer cleaning products, where customers are seeking more environmentally friendly products without loss of effectiveness or performance. We believe that our products have the environmental and safety profile to address these evolving customer demands. Silicates and silicate derivatives are recognized on the Safer Chemicals Ingredients List of the EPA’s Safer Choice program, which we believe positively impacts our ability to compete in consumer product applications.

Silicate Derivatives. Silica derivatives include specialty silicas, zeolite products, spray dry silicates, magnesium silicate, and other specialty chemicals. Silica derivatives are used in personal care products as a binder in pharmaceutical products, and as a source of alkaline in cleaning products, such as industrial cleaners. In addition, our silica derivatives are used in natural resources applications such as in drilling fluids as a lubricant binder. Some of our silicas and zeolites are used by our Environmental Catalysts and Services business to produce catalysts and catalyst precursors. We believe that this internal source of supply is a competitive advantage both for our performance chemicals product group, which can take advantage of opportunities to maximize the use of our sodium silicates production capacity and for our silica catalysts and zeolite catalysts product groups, which are able to access a consistent quality source of precursors.

Silica Gels. Silica gels are used as drying agents or adsorbents and desiccants for food and industrial products. For example, silica gels are used in the brewing industry to remove certain compounds that cause chilled beer to look cloudy, and are used as clarification agents for wines and fruit juices, and as an adsorbent of free fatty acid and other contaminants in the refining of cooking oils. In personal care, silica gels are used as carriers for vitamins and pharmaceuticals, and as a flow conditioner and an oil absorption agent in face powders. In industrial and engineered plastics, silica gels are used for gloss control in coil, wood, general industrial, leather and other high-performance surface coatings applications. In addition, highly-porous specialty silica gels are used in ink-receptive coatings for inkjet media. Some recently developed silica-based products are designed for ultraviolet-cured coatings and other low solvent formulations that offer more environmentally friendly characteristics. Silica gels are also used to create coatings that have significant capacity to absorb ink in order to allow for quick setting of colorants and faster ink dry times, which can improve color density and reduce ink bleed.

Precipitated Silicas. Precipitated silicas represent the largest volume of specialty silica products based on 2018 sales volume, but are also concentrated among a limited number of suppliers. Precipitated silica applications include filler in rubber for green tire applications and gel dentifrice formulations used in toothpaste as an abrasive or thickener. Precipitated silicas are an alternative to calcium carbonates because of their compatibility with different fluorides and their softness. In addition, precipitated silicas are used as functional filler in polyethylene membranes for lead-acid batteries, which are used in most automobiles. In agricultural end uses, precipitated silicas are used as carriers for liquid ingredients in dry animal feeds and as a flow aid and dispersant in insecticide formulations for crop care. We continue to collaborate with our customers to innovate in this industry. For example, we recently worked with certain customers to deliver enhanced products for whitening applications that offer improved cleaning performance with low abrasion.

Zeolites. We produce zeolites by combining sodium silicate with aluminum trihydrate and other materials. These products are used as builders in detergents. We also use these products to serve newer applications such as stabilizers in the production of polyvinylchloride, a titanium dioxide replacement for paints and coatings, and coatings applications for food grade paper.

Other Specialty Silicates. Other specialty silicates that we produce are used for a variety of industrial, personal care, and cleaning products. End uses include refractory, cleaning products, oil processing, hair bleach, fire retardants, water treatment, and adhesives. Our specialty silicate products are also used in drilling fluids for oil and gas wells to maintain drill hole integrity.

12

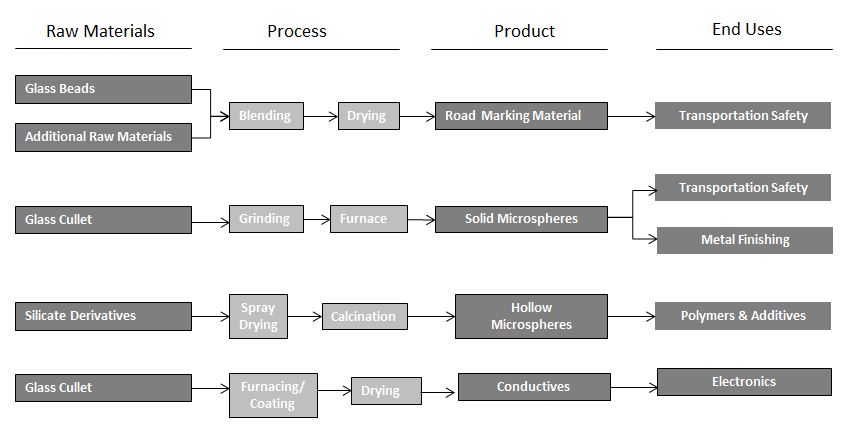

Performance Materials. Our performance materials product group includes specialty glass products, such as highly engineered microspheres made from either recycled glass or fresh batch material using our proprietary furnace operations. We believe that we are an industry leader in North America, Europe, South America, and Asia, excluding China, in microspheres. These products are used in the reflective markings used on roads and runways to enhance visibility at night and in poor weather to improve safety. Our microspheres, which can be solid or hollow, are also used as additives in plastics for lightweighting and in abrasive media, where they are used to clean, peen and debur metal surfaces, such as for turbine blades used in aerospace and power generation industries.

In the highway safety applications, our microspheres are used with a variety of binders, such as water- and solvent-borne paint, epoxy coatings, and thermoplastics. Our microspheres are mixed in with, and/or dropped onto, these binders as pavement markings are being applied. These microspheres remain partly exposed after the markings dry and provide retroreflectivity that increases the visibility of the road markings at night and during inclement weather. We sell these microspheres primarily to federal and state government agencies, municipalities, highway contractors, binder manufacturers and airport agencies. Demand for our performance materials products has grown as a result of increased spending for maintenance and upgrading of existing roads and the construction of new roads around the world. Demand for our highway safety products is principally driven by replacement demand and new road construction and, as such, demand for these products has grown through economic cycles without exhibiting as pronounced cyclicality as other end uses. Highway safety budgets in the United States are typically funded by taxes on gasoline and are not typically tied to economic cycles or to the state and local government budgeting process. The United States federal government has taken an active role in implementing regulations and initiating infrastructure development in an effort to improve highway safety. In addition, the continuing need to maintain and upgrade an aging United States highway infrastructure has translated into relatively consistent government expenditure in this area. The most recent innovation from our performance materials product group is our ThermoDrop® product, which simplifies the road striping operations for our customers by using a new durable thermal plastic road marking material. We have also introduced a new faster-drying road marking system, Visilok®, which can reduce traffic disruption during striping operations and improve road worker safety by reducing the amount of time needed to complete the road marking process.

We also sell highly specialized solid and hollow microspheres and metal coated particles for a variety of uses such as plastic additives, conductive applications, metal finishing, and other industrial and consumer applications. For metal finishing, our performance materials are propelled from blasting equipment to clean, peen, debur, and finish metal in industrial and process chemical end uses. Our performance material products offer the ability to design lighter parts while maintaining strength and reliability. Our performance materials are often a preferred substitute for other media such as industrial sand, aluminum oxide, iron and steel because they do not damage parts and they allow for better process control, limit surface contamination, and can be more environmentally friendly.

Other applications for our microspheres include additives into paints and coatings for thermal insulation, to reduce weight and ingredients in cosmetics to improve feel attributes and improve flow functionality. Our microspheres are also used in drilling fluids to provide lubrication and strength. Within the natural resources industry, our performance materials are used in oil-drilling muds to improve lubricity and reduce friction in horizontal drilling. In addition, our hollow microspheres are used as sensitizers for water-based industrial explosives in mining, quarrying, and construction. Sensitizers are also used in explosives to increase the energy of a detonation.

Competition

In our Performance Materials and Chemicals business, we primarily compete with other global producers such as OxyChem, Grace and Evonik. We believe that our industry leadership position, scale, and industry presence provides us with a competitive advantage over competitors who compete only in particular end uses. We believe that it would be costly and difficult for a new entrant or existing competitor to replicate our breadth or economies of scale in the production of microspheres.

We believe that we are the only global silicates producer with operations in North America, Europe, South America and Australia, and we believe that we have technical and cost advantages in all of these regions as compared to our competitors as a result of the scale and breadth of our product offerings and operations. We compete primarily on a regional basis due to the costs associated with shipping sodium silicates, and we estimate that we had approximately three times the sodium silicate supply share of our nearest competitor based on 2018 sales volume. Our network of regional silicate plants is strategically located to support the industries that we serve. In addition, we maintain a few larger dedicated facilities to service our derivative products. We believe that our network of strategically located manufacturing facilities allows us to serve our customers at a lower cost than our competitors and with quicker delivery times for our products. In the industry

13

served by our Performance Materials and Chemicals business, we compete primarily on the basis of performance, product consistency, quality, reliability, and ability to innovate in response to customer demands. Our competitors are primarily regional suppliers.

Manufacturing

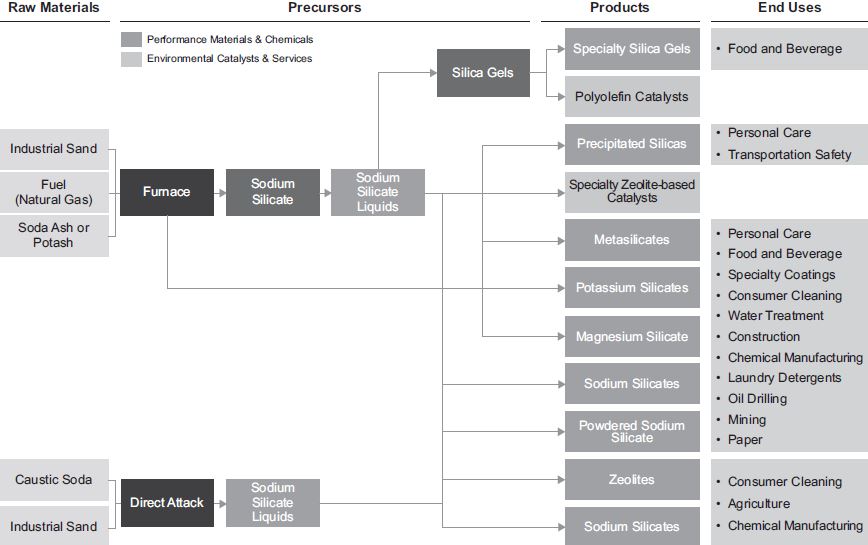

Performance chemicals are produced through an integrated supply chain beginning with regional and large scale upstream production of sodium silicates and downstream derivatives. Sodium silicates are produced regionally because of the expense of shipping sodium silicates extended distances due to their water content. Our sodium silicates are produced by fusing industrial sand and soda ash in our proprietary furnace operations. We dissolve the molten silicate from the furnace into water and sell these products in liquid form. Downstream derivatives are produced through a variety of chemical operations that create aqueous, solid, and gel forms for our products.

For the year ended December 31, 2018, approximately 40% of our North American silicate sales, which represented a significant portion of our performance chemicals product group sales, were derived from contracts that included raw material cost pass-through clauses. Under these contracts, there is usually a time lag of between three and nine months for cost changes to pass-through, depending on the magnitude of the change, industry dynamics and the terms of the particular contract.

Performance Chemicals Manufacturing Platform

14

We produce our highway safety products and other microspheres by crushing raw materials, such as recycled glass or cullet, and then feeding these raw materials into a furnace. The product is coated or treated in other ways to meet particular customer and end use specifications. The beads are then bagged and stocked for shipment. The flowchart below outlines our performance materials’ production process.

Performance Materials Manufacturing Platform

Raw Materials

We estimate that our raw materials costs represent approximately 40% of total cost of goods sold in the year ended December 31, 2018. Our products are predominantly inorganic and carbon-free, and are produced from readily available raw materials such as industrial sand and soda ash, which prices have historically been less volatile than oil. We also use natural gas in our furnaces where our North American facilities have benefited from the plentiful supplies of shale gas. In addition, we have long-term supply contracts with many of our key raw materials suppliers across our product groups. We have also been able to mitigate the impact of raw material or energy price volatility using a variety of mechanisms, including hedging and raw material cost pass-through clauses in our sales contracts and other adjustment provisions.

We are able to negotiate our supply agreements for our key raw materials based on our leading industry position and global scale in an effort to achieve competitive pricing. We also maintain a raw material quality audit and qualification program designed to ensure that the material we purchase satisfies stringent quality requirements. Key raw materials for our product groups include:

| Key Raw Materials | Product Group | |

| Soda Ash | Performance Chemicals, Refining Services, Performance Materials | |

| Sodium hydroxide ("caustic soda") | Performance Chemicals, Refining Services | |

| Cullet | Performance Materials | |

| Sulfur | Refining Services | |

| Industrial sand | Performance Chemicals, Performance Materials | |

| Aluminum trihydrate | Performance Chemicals, Refining Services | |

While natural gas is not a direct feedstock for any individual product, we use natural gas powered furnaces to heat raw materials and create the chemical reactions necessary to manufacture our products. We maintain multiple suppliers

15

wherever possible and we seek to hedge our exposure to fluctuations in prices for natural gas through hedging activity in the United States, forward purchases of natural gas in the United States, Canada, and Europe, and the use of pass-through clauses for raw material and natural gas costs in our customer contracts. However, we may not be successful in passing through all increases in raw material costs or maintaining an uninterrupted supply of natural gas for all of our furnaces. See “Risk Factors-Risks Related to Our Business - If we are unable to pass on increases in raw material prices, including natural gas, to our customers or to retain or replace our key suppliers, our results of operations and cash flows may be negatively affected”.

Joint Ventures

We have entered into several long-standing joint ventures to supplement our businesses and access other geographic locations, minimize costs and accelerate growth in areas we believe have significant business potential, with the most significant of these joint ventures including the following:

Zeolyst Joint Venture. Our Zeolyst Joint Venture is a long-standing partnership with CRI Zeolites Inc., which is an affiliate of Royal Dutch Shell, that dates back to 1988 and is focused on the development, manufacture and sale of zeolite-containing catalysts through manufacturing facilities located in Kansas and the Netherlands. We combine our expertise in zeolite supply and technology with our partner’s expertise in global refinery catalyst sales and technology. We have a 50% ownership stake in our Zeolyst Joint Venture. We supply sodium silicates from our performance chemicals product group to the Zeolyst Joint Venture to make specialty zeolites, which are used as precursors in emission control and custom catalysts. We also produce specialty zeolites that are precursors for the production of hydrocracking catalysts and other refinery and petrochemical catalysts that are used by our other product groups and sold to third parties. We manage the production of these specialty zeolites due to our expertise in zeolite production. These catalysts include aromatic catalysts that upgrade aromatic by-product streams, dewaxing catalysts that improve lube oil performance and diesel cold flow performance, and paraffin isomerization catalysts that upgrade olefins to high octane gasoline blending components for refinery and petrochemical customers.

PQ Holdings Mexicana S.A. de C.V. PQ Holdings Mexicana was established in 2000 as a joint venture with Solvay Alkalis, Inc. for the manufacture, marketing and sale of various chemicals, including sodium silicate, through manufacturing facilities in Tlalnepantla and Guadalajara, Mexico. We have an 80% ownership stake in PQ Holdings Mexicana.

Research and Development

We benefit from the highly-skilled technical capabilities of our employees dedicated to new product development. We operate six research and development facilities in the United States, Canada, the United Kingdom, the Netherlands, France and Spain. Our research and development activities are directed toward the development of new and improved products, processes, systems and applications for customers. Our research and development team is organized to support each of our operating businesses and staffed with experienced scientists, technical service representatives and process engineers with direct knowledge of our products. This business group and customer-oriented team structure provides strong links between our product development and manufacturing functions and our customer collaboration and specifications. These connections enable us to focus our development on timely and relevant products for our customers while remaining attentive to manufacturing considerations to enable us to produce new products profitably and in a timely manner. Product development activities are organized into research and development projects that are subject to regular reviews by the business teams in order to understand and address our customers’ evolving needs and invest in our growth by prioritizing innovation driven by these identified needs. In addition, we hold senior-level project reviews to ensure best practices are shared and consistent metrics are used to determine a project’s merit and the size of the potential opportunity.

Intellectual Property

We evaluate on a case-by-case basis how best to use patents, trademarks, copyrights, trade secrets and other available intellectual property protections in order to protect our products and our critical investments in research and development, manufacturing and marketing. We focus on securing and maintaining patents for certain inventions such as composition-of-matter, while maintaining other inventions such as process improvements as trade secrets, derived from our market-based business model, in an effort to maximize the value of our product portfolio and manufacturing capabilities and reinforce our competitive advantage. Our policy is to seek appropriate intellectual property protection for significant product and process developments in the major areas where the relevant products are manufactured or sold. Patents may cover products, processes, intermediate products and product uses. Patents extend for varying periods in accordance with the date of patent application filing and the legal life of patents in the various countries in which the patents are registered. The protection

16

afforded, which may also vary from country to country, depends upon the type of subject matter covered by the patent and the scope of the claims of the patent.

In most industrial countries, patent protection may be available for new substances and formulations, as well as for unique applications and production processes. However, given the geographical scope of our business and our continued growth strategy, there are regions of the world in which we do business or may do business in the future where intellectual property protection may be limited and difficult to enforce. Moreover, we monitor our competitors’ products and, if circumstances were to dictate that we do so, we would vigorously challenge the actions of others that conflict with our patents, trademarks and other intellectual property rights. We maintain appropriate information security policies and procedures reasonably designed to ensure the safeguarding of confidential information including, where appropriate, data encryption, access controls and employee awareness training.

We own or have rights to a number of patents relating to our products and processes. As of December 31, 2018, we owned 52 patented inventions in the United States, with approximately 309 patents issued in countries around the world and approximately 120 patent applications pending worldwide covering more than 20 additional inventions. As of December 31, 2018, we also had trademark rights in approximately 613 trademark registrations worldwide, including approximately 77 U.S. trademark registrations. We also have approximately 37 pending trademark applications, which include applications in the United States and worldwide. In addition to our registered and applied-for intellectual property portfolio, we also claim ownership of certain trade secrets and proprietary know-how developed by and used in our business. Including our joint ventures, we are party to certain arrangements whereby we license in the right to use certain intellectual property rights in connection with our business.

Seasonality

Seasonal changes and weather conditions typically affect our performance materials and refining services product groups. In particular, our performance materials product group generally experiences lower sales and profit in the first and fourth quarters of the year because highway striping projects typically occur during warmer weather months. Additionally, our refining services product group typically experiences similar seasonal fluctuations as a result of higher demand for gasoline products in the summer months. As a result, our working capital requirements tend to be higher in the first and fourth quarters of the year, which can adversely affect our liquidity and cash flows. Because of this seasonality associated with certain of our product groups, results for any one quarter are not necessarily indicative of the results that may be achieved for any other quarter or for the full year.

Employees

As of December 31, 2018, we had 3,188 employees worldwide, of which 1,455 were employed in the United States, 503 were employed in Canada, Mexico, Brazil and Argentina, 888 were employed throughout Europe, 38 were employed in South Africa and 99 were employed in Indonesia. Our remaining employees are dispersed throughout Asia and Australia, primarily in Australia, China, Thailand and Japan. As of December 31, 2018, approximately 50% of our employees were represented by a union, works council or other employee representative body. We believe we have good relationships with our employees and their respective works councils, unions or other bargaining representatives. There have been no labor strikes or work stoppages in these locations in recent history.

Environmental Regulations

Obtaining, producing and distributing many of our products involve the use, storage, transportation and disposal of toxic and hazardous materials. We are subject to extensive, evolving and increasingly stringent national and local environmental laws and regulations, which address, among other things, the following:

| • | emissions to the air; |

| • | discharges to soils and surface and subsurface waters; |

| • | other releases into the environment; |

| • | prevention, remediation or abatement of releases of hazardous materials into the indoor or outdoor environment; |

| • | generation, handling, storage, transportation, treatment and disposal of waste materials; |

| • | maintenance of safe conditions in the workplace; |

17

| • | registration and evaluation of chemicals; |

| • | production, handling, labeling or use of chemicals used or produced by us; and |

| • | stewardship of products after manufacture. |

We apply the principles of the Environmental Management standard of the International Organization for Standardization (ISO 14001) at our facilities throughout the world. For chemical facilities in the United States, we also adhere to the Responsible Care RC14001 Technical Specifications of the American Chemistry Council.

We maintain policies and procedures to monitor and control environmental, health and safety risks, and to monitor compliance with applicable state, national, and international environmental, health and safety requirements. We have a strong environmental, health and safety organization. We have a staff of professionals who are responsible for environmental health, safety and product regulatory compliance. We have implemented a corporate audit program for all of our facilities. However, we cannot provide assurance that we will at all times be in full compliance with all applicable environmental laws and regulations. We expect that stringent environmental regulations will continue to be imposed on us and our industry in general. Evolving chemical regulation programs throughout the world could impose testing requirements or restrictions on our chemical raw materials and products. These programs include the 2016 amendments to the U.S. Toxic Substances Control Act, under which the EPA will prioritize and evaluate chemicals for regulation, the E.U. REACH regulations, which have ongoing registration and evaluation requirements with associated testing costs and potential restrictions, the Korea REACH law, which is requiring registration and potentially testing of chemicals, and similar programs being developed in Taiwan, Turkey, India, and elsewhere. Based on our chemicals and the various regulations promulgated to date, we do not anticipate costly testing requirements or severe restrictions, but cannot guarantee that we will not be subject to requirements for our products or raw materials that could materially affect our operations.

Environmental Remediation. Environmental laws and regulations require mitigation or remediation of the effects of the disposal or release of chemical substances. Under some of these regulations, as the current or former owner or operator of a property, we could be held liable for the costs of removal or remediation of hazardous substances on or under the property, without regard to whether we knew of or caused the contamination, and regardless of whether the practices that resulted in the contamination were permitted at the time they occurred. Many of our current or former production sites have an extended history of industrial use, and it is impossible to predict precisely what effect these laws and regulations will have on us in the future. Soil and groundwater contamination requiring investigation and remediation has been discovered at some of the sites, and might occur or be discovered at other sites. Several active and former facilities currently are undergoing investigation and remediation, including sites in Rahway, NJ; Dominguez, CA; Martinez, CA; and Tacoma, WA.