| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207361-05 | ||

June 14, 2017 HSBCCo-ManagerCredit SuisseCo-Lead Manager and Joint BookrunnerNatixisCo-Lead Manager and Joint BookrunnerCSAIL 2017-C8 Commercial Mortgage Trust Free Writing Prospectus Structural and Collateral Term Sheet Credit Suisse Commercial Mortgage Securities Corp.as DepositorCommercial Mortgage Pass-Through Certificates Series 2017-C8 Column Financial, Inc. Natixis Real Estate Capital LLC Benefit Street Partners CRE Finance LLCas Sponsors and Mortgage Loan SellersTHE DEPOSITOR HAS FILED A REGISTRATION STATEMENT (INCLUDING A PROSPECTUS) WITH THE SEC (SEC FILE NO. 333-207361) FOR THE OFFERING TO WHICH THIS COMMUNICATION RELATES. BEFORE YOU INVEST, YOU SHOULD READ THE PROSPECTUS IN THAT REGISTRATION STATEMENT AND OTHER DOCUMENTS THE ISSUER HAS FILED WITH THE SEC FOR MORE COMPLETE INFORMATION ABOUT THE ISSUER AND THIS OFFERING. YOU MAY GET THESE DOCUMENTS FOR FREE BY VISITING EDGAR ON THE SEC WEB SITE AT WWW.SEC.GOV. ALTERNATIVELY, CREDIT SUISSE WILL ARRANGE TO SEND YOU THE PROSPECTUS IF YOU REQUEST IT BY CALLING TOLL FREE 1-800-221-1037.

STATEMENT REGARDING ASSUMPTIONS AS TO

SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This material is for your information, and neither Credit Suisse Securities (USA) LLC nor the other underwriters (collectively, the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Neither this document nor anything contained herein shall form the basis for any contract or commitment whatsoever. The information contained herein is preliminary as of the date hereof. These materials are subject to change, completion or amendment from time to time. The information contained herein will be superseded by similar information delivered to you prior to the time of sale, including as part of the Preliminary Prospectus referred to herein relating to the CSAIL 2017-C8 Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates (the “Offering Document”). The information supersedes any such information previously delivered. The information should be reviewed only in conjunction with the entire Offering Document. All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document in its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Free Writing Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the appropriateness of the assumptions used in preparing the Computational Materials, or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters nor any of their respective affiliates makes any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities.

This document contains forward-looking statements. Those statements are subject to certain risks and uncertainties that could cause the success of collections and the actual cash flow generated to differ materially from the information set forth herein. While such information reflects projections prepared in good faith based upon methods and data that are believed to be reasonable and accurate as of the dates thereof, the depositor undertakes no obligation to revise these forward-looking statements to reflect subsequent events or circumstances. Individuals should not place undue reliance on forward-looking statements and are advised to make their own independent analysis and determination with respect to the forecasted periods, which reflect the issuer’s view only as of the date hereof.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this Free Writing Prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

2

Publicly Offered Certificates

| Class | Expected Ratings (KBRA/Fitch/DBRS/Moody’s) | Approximate Initial Certificate Principal Balance or Notional Amount(1) | Approximate Initial Available Certificate Principal Balance or Notional Amount(1)(2) | Approximate Initial Retained Certificate Principal Balance or Notional Amount(1)(2) | Approximate Initial Credit Support | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| A-1 | AAA(sf)/AAAsf/AAA(sf)/Aaa(sf) | $17,863,000 | $17,125,000 | $738,000 | 30.000%(6) | 2.82 | 1-56 | 35.5% | 17.5% |

| A-2 | AAA(sf)/AAAsf/AAA(sf)/Aaa(sf) | $163,585,000 | $156,828,000 | $6,757,000 | 30.000%(6) | 4.72 | 56-58 | 35.5% | 17.5% |

| A-3 | AAA(sf)/AAAsf/AAA(sf)/Aaa(sf) | $142,336,000 | $136,457,000 | $5,879,000 | 30.000%(6) | 9.61 | 114-117 | 35.5% | 17.5% |

| A-4 | AAA(sf)/AAAsf/AAA(sf)/Aaa(sf) | $213,505,000 | $204,687,000 | $8,818,000 | 30.000%(6) | 9.88 | 117-120 | 35.5% | 17.5% |

| A-SB | AAA(sf)/AAAsf/AAA(sf)/Aaa(sf) | $30,449,000 | $29,191,000 | $1,258,000 | 30.000%(6) | 7.26 | 58-114 | 35.5% | 17.5% |

| X-A | AAA(sf)/AAAsf/AAA(sf)/Aa1(sf) | $651,885,000(7) | $624,959,000 | $26,926,000 | N/A | N/A | N/A | N/A | N/A |

| X-B | AAA(sf)/A-sf/A(high)(sf)/NR | $78,065,000(7) | $74,840,000 | $3,225,000 | N/A | N/A | N/A | N/A | N/A |

| A-S | AAA(sf)/AAAsf/AAA(sf)/Aa3(sf) | $84,147,000 | $80,671,000 | $3,476,000 | 19.625% | 9.96 | 120-120 | 40.8% | 15.2% |

| B | AA-(sf)/AA-sf/AA(sf)/NR | $44,608,000 | $42,765,000 | $1,843,000 | 14.125% | 9.96 | 120-120 | 43.6% | 14.3% |

| C | A-(sf)/A-sf/A(sf)/NR | $33,457,000 | $32,075,000 | $1,382,000 | 10.000% | 9.96 | 120-120 | 45.7% | 13.6% |

Privately Offered Pooled Certificates(8)

| Class | Expected Ratings (KBRA/Fitch/DBRS/Moody’s) | Approximate Initial Certificate Principal Balance or Notional Amount(1) | Approximate Initial Available Certificate Principal Balance or Notional Amount(1)(2) | Approximate Initial Retained Certificate Principal Balance or Notional Amount(1)(2) | Approximate Initial Credit Support | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| D | BBB-(sf)/BBB-sf/BBB(sf)/NR | $32,442,000 | $31,102,000 | $1,340,000 | 6.000% | 9.96 | 120-120 | 47.7% | 13.0% |

| E | BB-(sf)/BB-sf/BB(sf)/NR | $18,248,000 | $17,494,000 | $754,000 | 3.750% | 9.96 | 120-120 | 48.9% | 12.7% |

| F | B-(sf)/B-sf/B(high)(sf)/NR | $7,097,000 | $6,803,000 | $294,000 | 2.875% | 9.96 | 120-120 | 49.3% | 12.6% |

| NR | NR/NR/NR/NR | $23,318,563 | $22,355,000 | $963,563 | 0.000% | 9.96 | 120-120 | 50.8% | 12.2% |

Privately Offered Loan-Specific Certificates

| Class | Expected Ratings (DBRS) | Approximate Initial Certificate Principal Balance or Notional Amount(1) | Approximate Initial Available Certificate Principal Balance or Notional Amount(1) | Approximate Initial Retained Certificate Principal Balance or Notional Amount(1) | Approximate Initial Credit Support | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Loan- Specific Certificate Principal to Value Ratio(9) | Loan- Specific Underwritten NOI Debt Yield(10) |

| 85BD-A | AA(low)(sf) | $7,000,000 | $6,650,000 | $350,000 | 90.278% | 9.96 | 120-120 | 27.0% | 14.7% |

| 85BD-X | BBB(sf) | $72,000,000 | $68,400,000 | $3,600,000 | N/A | N/A | N/A | N/A | N/A |

| 85BD-B | A(low)(sf) | $33,000,000 | $31,350,000 | $1,650,000 | 44.444% | 9.96 | 120-120 | 32.1% | 12.4% |

| 85BD-C | BBB(low)(sf) | $32,000,000 | $30,400,000 | $1,600,000 | 0.000% | 9.96 | 120-120 | 37.0% | 10.8% |

| (1) | Approximate, subject to a variance of plus or minus 5%. |

| (2) | On the Closing Date, the certificates (other than the Privately Offered Loan-Specific Certificates and the Class R certificates) with the initial certificate balances or notional amounts, as applicable, set forth in the table under “Initial Retained Certificate Balance or Notional Amount” are expected to be sold by the Underwriters to Natixis as described in “Credit Risk Retention” in the Preliminary Prospectus relating to the Publicly Offered Certificates, dated June 14, 2017 (the “Preliminary Prospectus”). Additionally, with respect to the Class F and Class NR certificates, the Approximate Initial Available Certificate Principal Balance or Notional Amount of each of the Class F and Class NR certificates (collectively, the “HRR Certificates”) is subject to change based on final pricing of all certificates and the final determination of the Class F and Class NR certificates that will be retained by the retaining |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

third-party purchaser as part of the sponsor’s satisfaction of its U.S. risk retention requirements. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the HRR Certificates, see “Credit Risk Retention” in the Preliminary Prospectus.

| (3) | Assumes 0% CPR / 0% CDR and a June 29, 2017 closing date. Based on “Modeling Assumptions” as described in the Preliminary Prospectus relating to the Publicly Offered Certificates, dated June 14, 2017 (the “Preliminary Prospectus”). Capitalized terms used but not defined herein have the meanings ascribed to them in the Preliminary Prospectus. |

| (4) | The “Certificate Principal to Value Ratio” for any class (other than the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial certificate principal balance of such class of certificates and all classes of principal balance certificates senior to such class of certificates and the denominator of which is the total initial certificate principal balance of all of the principal balance certificates. The Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificate Principal to Value Ratios are calculated in the aggregate for those classes as if they were a single class. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (5) | The “Underwritten NOI Debt Yield” for any class (other than the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage loans and (b) the total initial certificate principal balance of all of the classes of principal balance certificates divided by the total initial certificate principal balance for such class and all classes of principal balance certificates senior to such class of certificates. The Underwritten NOI Debt Yield for each class of the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates is calculated in the aggregate for those classes as if they were a single class. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

| (6) | The credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates are represented in the aggregate. |

| (7) | The notional amounts of the Class X-A and Class X-B certificates (collectively, the “Class X Certificates”) are defined in the Preliminary Prospectus. |

| (8) | The Class Z and Class R certificates are not shown above. |

| (9) | The “Loan-Specific Certificate Principal to Value Ratio” for the Class 85BD-A, Class 85BD-B and Class 85BD-C certificates is calculated as the total of the initial certificate principal balance of such class of certificates, all classes of principal balance certificates senior to such class of certificates and the related A Notes divided by the 85 Broad Street appraised value of $652.0 million as of April 30, 2017. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (10) | The “Loan-Specific Underwritten NOI Debt Yield” for the Class 85BD-A, Class 85BD-B and Class 85BD-C is calculated as the 85 Broad Street UW NOI of $25,930,418 divided by the total of the total initial certificate principal balance for such class all classes of principal balance certificates senior to such class of certificates and the related A Notes. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

Summary of Transaction Terms

| Securities: | $811,055,563 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Managers and Bookrunners: | Credit Suisse Securities (USA) LLC and Natixis Securities Americas LLC, as Co-Lead Managers and Joint Bookrunners, and HSBC Securities (USA) Inc., as Co-Manager. |

| Mortgage Loan Sellers: | Natixis Real Estate Capital LLC (“Natixis”) (46.3%), Benefit Street Partners CRE Finance LLC (“BSP”) (32.0%) and Column Financial, Inc. (“Column”) (24.4%). |

| Master Servicer: | Wells Fargo Bank, National Association (“Wells Fargo”). |

| Special Servicer: | Midland Loan Services, a dvision of PNC Bank, National Association (“Midland”). |

| Directing Certificateholder: | Eightfold Real Estate Capital Fund V, L.P. or another affiliate of Eightfold Real Estate Capital, L.P. |

| Trustee: | Wilmington Trust National Association (“Wilmington”). |

| Certificate Administrator: | Wells Fargo. |

| Operating Advisor: | Park Bridge Lender Services LLC (“Park Bridge”). |

| Asset Representations Reviewer: | Park Bridge. |

| U.S. Credit Risk Retention: | For a discussion of the manner by which Natixis, as retaining sponsor, intends to satisfy the credit risk requirements of the Credit Risk Retention Rules, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Risk Retention Consultation Party: | Natixis. |

| Closing Date: | On or about June 29, 2017. |

| Cut-off Date: | With respect to each mortgage loan, the respective due date for the monthly debt service payment that is due in June 2017 (or, in the case of any mortgage loan that has its first due date in July 2017, the date that would have been its due date in June 2017 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month.) |

| Distribution Date: | The 4th business day following each Determination Date, commencing in July 2017. |

| Determination Date: | 11thday of each month, or if the 11th day is not a business day, then the business day immediately following such 11th day, commencing in July 2017. |

| Rated Final Distribution Date: | The Distribution Date in June 2050. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC regular interests for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class X-A, Class X-B, Class A-S, Class B and Class C certificates will be offered publicly (the “Publicly Offered Certificates”). The Class D, Class E, Class F, Class NR and Class R certificates (the “Privately Offered Certificates”) and the Class Z certificates will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The certificates willnot constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

| Optional Termination: | 1% clean-up call (or, if the 71 Fifth Ave mortgage loan remains an asset of the trust fund, the product of (x) the product of (A) the percentage that is calculated by dividing (A) the sum of the outstanding principal balance of the 71 Fifth Ave mortgage loan and 1% of the outstanding principal balance of the aggregate principal balance of the mortgage loans as of the Cut-off Date by (B) the aggregate principal balance of the mortgage loans as of the Cut-off Date and (y) the aggregate principal balance of the mortgage loans as of the Cut-off Date). |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| Analytics: | The transaction is expected to be available on Bloomberg Financial Markets, L.P., CMBS.com, Inc., Thomson Reuters Corporation, Trepp, LLC, Intex Solutions, Inc., Moody’s Analytics and BlackRock Financial Management, Inc. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

Collateral Characteristics(1)

| Loan Pool | |

| Initial Pool Balance (“IPB”)(2): | $811,055,563 |

| Number of Mortgage Loans: | 32 |

| Number of Mortgaged Properties: | 55 |

| Average Cut-off Date Balance per Mortgage Loan: | $25,345,486 |

| Weighted Average Current Mortgage Rate: | 4.4871% |

| 10 Largest Mortgage Loans as % of IPB: | 62.9% |

| Weighted Average Remaining Term to Maturity: | 106 |

| Weighted Average Seasoning: | 2 |

| Credit Statistics | |

| Weighted Average UW NCF DSCR(3)(4): | 2.48x |

| Weighted Average UW NOI Debt Yield(3): | 12.2% |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(3)(5): | 50.8% |

| Weighted Average Maturity Date LTV(3)(5): | 46.7% |

| Other Statistics | |

| % of Credit Assessed Mortgage Loans(6): | 39.9% |

| % of Mortgage Loans with Additional Debt: | 41.0% |

| % of Mortgaged Properties with Single Tenants: | 13.1% |

| Amortization | |

| Weighted Average Original Amortization Term(7): | 355 |

| Weighted Average Remaining Amortization Term(7): | 355 |

| % of Mortgage Loans with Interest-Only: | 54.7% |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 26.5% |

| % of Mortgage Loans with Amortizing Balloon: | 15.7% |

| % of Mortgage Loans with Interest-Only, followed by ARD Structure | 3.1% |

| Cash Management(8) | |

| % of Mortgage Loans with In-Place, Hard Lockboxes: | 70.5% |

| % of Mortgage Loans with Springing Lockboxes: | 15.8% |

| % of Mortgage Loans with In-Place, Soft Lockboxes: | 7.8% |

| % of Mortgage Loans with No Lockbox: | 4.5% |

| % of Mortgage Loans with Hard Commercial Units & Soft Residential Units Lockbox | 1.4% |

| Reserves | |

| % of Mortgage Loans Requiring Upfront or Ongoing Tax Reserves: | 76.4% |

| % of Mortgage Loans Requiring Upfront or Ongoing Insurance Reserves: | 72.4% |

| % of Mortgage Loans Requiring Upfront or Ongoing CapEx Reserves(9): | 80.4% |

| % of Mortgage Loans Requiring Upfront or Ongoing TI/LC Reserves(10): | 53.9% |

| (1) | Except where expressly stated otherwise, statistical information in this table does not include the 85 Broad Street trust subordinate companion loan. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6 the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (4) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (5) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

| (6) | At least one of Moody’s, Fitch, DBRS or KBRA have indicated that the credit characteristics of each of Loan Nos. 1, 2, 3, 6, 12 and 13, in the context of their inclusion in the Initial Pool Balance, are consistent with an investment grade obligation. |

| (7) | Excludes eleven (11) mortgage loans that are interest-only or interest-only, ARD for the entire term. |

| (8) | For a detailed description of cash management, refer to“Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts—Lockbox Accounts” in the Preliminary Prospectus. |

| (9) | CapEx Reserves include FF&E reserves for hospitality properties. |

| (10) | Calculated only with respect to Cut-off Date Balance of mortgage loans secured by industrial, office, mixed use and retail properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

Collateral Characteristics

| Originator | Sponsor | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of IPB | |||||||||

| Natixis(1)(2) | Natixis | 10 | 12 | $353,686,428 | 43.6 | % | ||||||||

| BSP | BSP | 16 | 36 | 259,684,135 | 32.0 | |||||||||

| Column Financial, Inc.(2)(3) | Column | 6 | 7 | 197,685,000 | 24.4 | |||||||||

| Total: | 32 | 55 | $811,055,563 | 100.0 | % | |||||||||

| (1) | Loan No. 2, originated by Natixis, representing approximately 9.9% of IPB, is part of a whole loan that was co-originated by JPMorgan Chase Bank, National Association, Natixis, Société Générale, Deutsche Bank AG, New York Branch and Barclays Bank PLC. |

| (2) | One of the two notes that secures Loan No. 1, identified as note A-A-2, represents approximately 2.5% of IPB, is part of a whole loan that was originated by Natixis. The other note that secures Loan No. 1, identified as note A-A-1, represents approximately 8.6% of IPB, and was acquired by Column from Natixis prior to the date hereof. Such mortgage loan was underwritten in accordance with the procedures described under “Transaction Parties—The Sponsors and Mortgage Loan Sellers—Natixis Real Estate Capital LLC” in the preliminary prospectus. The “Number of Mortgage Loans” shown in the table above for Natixis does not include this note; however, the “Aggregate Principal Balance of Mortgage Loans” and the “Approx. % of Initial Pool Balance” shown in the table above for Natixis do include this note. |

| (3) | Loan No. 27, representing approximately 0.8% of IPB, was originated by Regions Bank, an Alabama state banking corporation, and acquired and re-underwritten by Column in accordance with the procedures described under “Transaction Parties—The Sponsors and Mortgage Loan Sellers—Column Financial, Inc.” in the preliminary prospectus. |

Ten Largest Mortgage Loans

| No. | Loan Name | Mortgage Loan Seller | No. of Properties | Cut-off Date Balance | % of IPB | SF/ Rooms/ Units | Property Type | UW NCF DSCR(1)(2) | UW NOI Debt Yield(1) | Cut-off Date LTV(1) | Maturity Date LTV(1) | Credit Assessment (Moody’s/Fitch/ DBRS/KBRA) |

| 1 | 85 Broad Street | Column / Natixis | 1 | $90,000,000 | 11.1% | 1,118,512 | Office | 4.11x | 15.3% | 25.9% | 25.9% | NR/BBB-/ AA(low)/BBB+ |

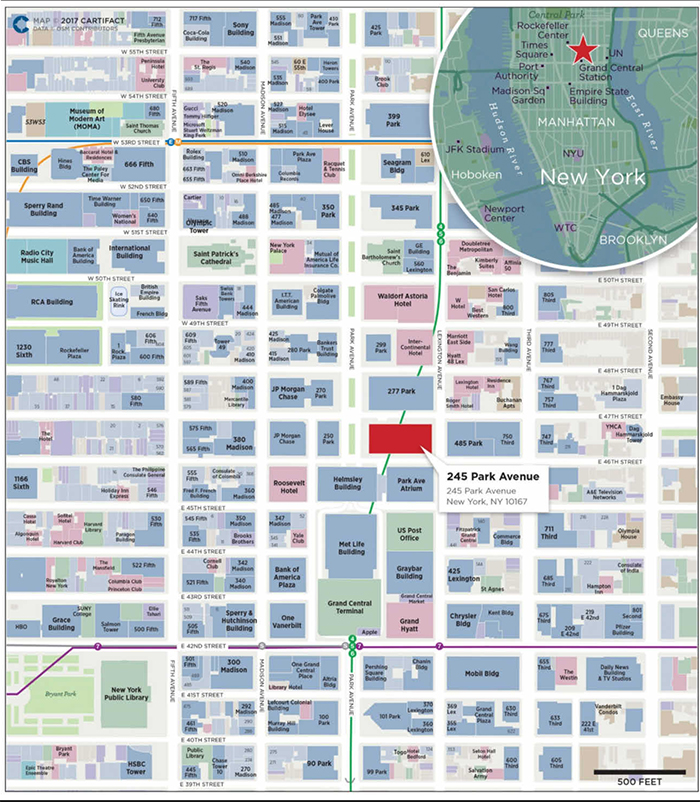

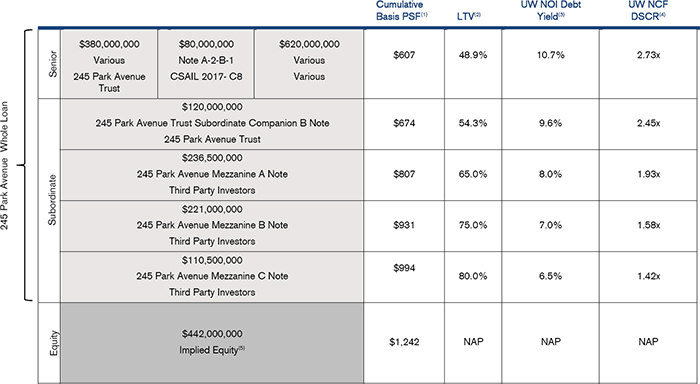

| 2 | 245 Park Avenue | Natixis | 1 | 80,000,000 | 9.9 | 1,723,993 | Office | 2.73x | 10.7% | 48.9% | 48.9% | NR/BBB-/ NR/BBB |

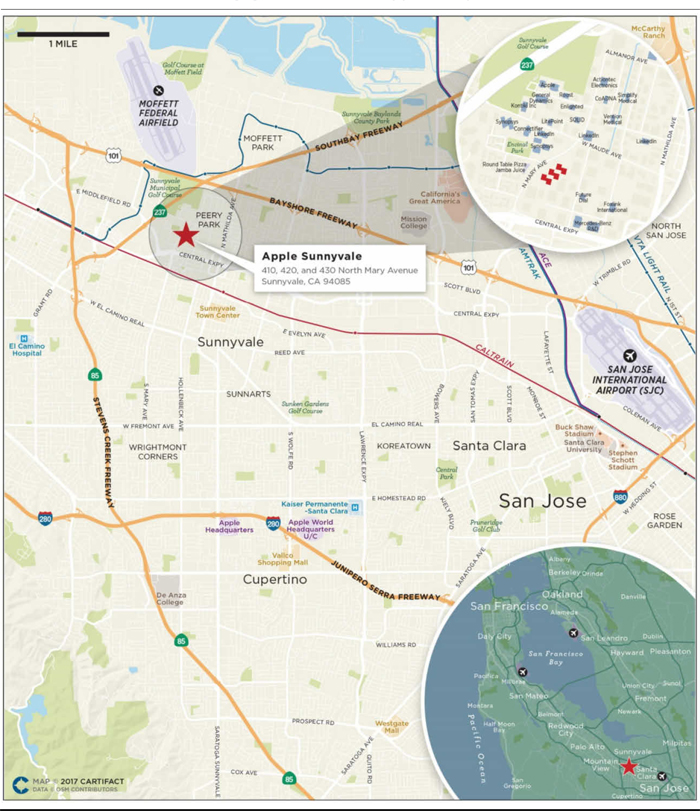

| 3 | Apple Sunnyvale | Natixis | 1 | 70,350,000 | 8.7 | 349,758 | Office | 3.40x | 14.6% | 35.7% | 35.7% | Baa3/BBB-/ A/BBB- |

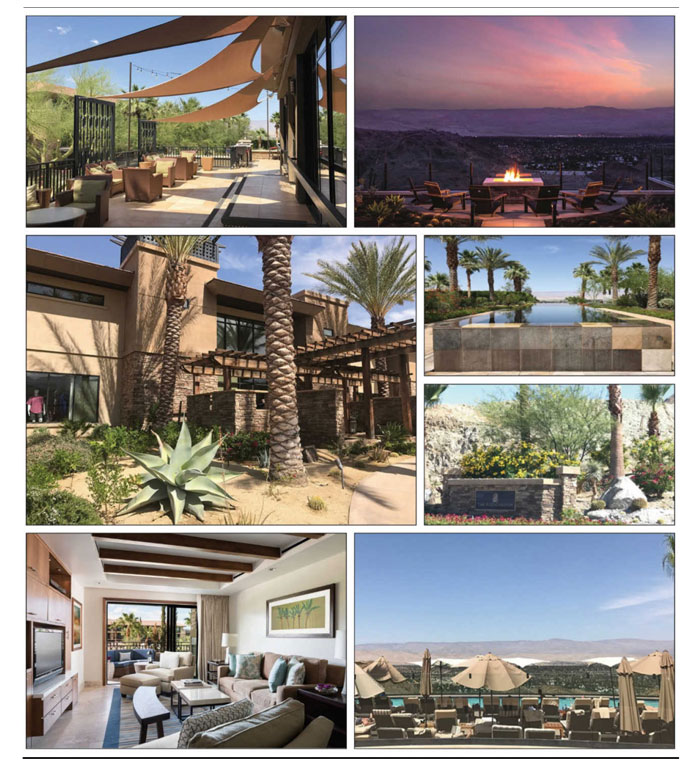

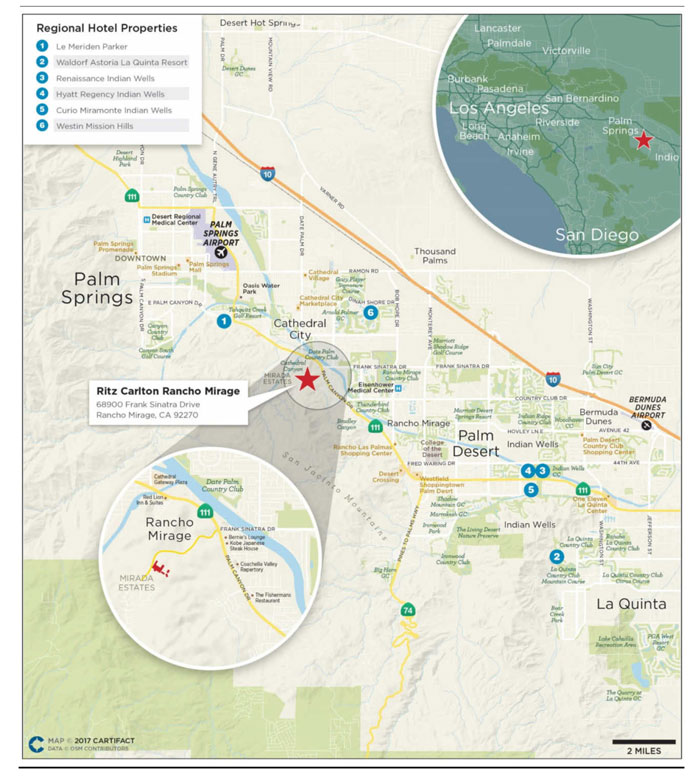

| 4 | Ritz Carlton Rancho Mirage | Column | 1 | 54,000,000 | 6.7 | 244 | Hotel | 1.81x | 13.4% | 58.2% | 58.2% | NR/NR/NR/NR |

| 5 | Hotel Eastlund | Column | 1 | 41,000,000 | 5.1 | 168 | Hotel | 1.74x | 12.1% | 59.8% | 51.7% | NR/NR/NR/NR |

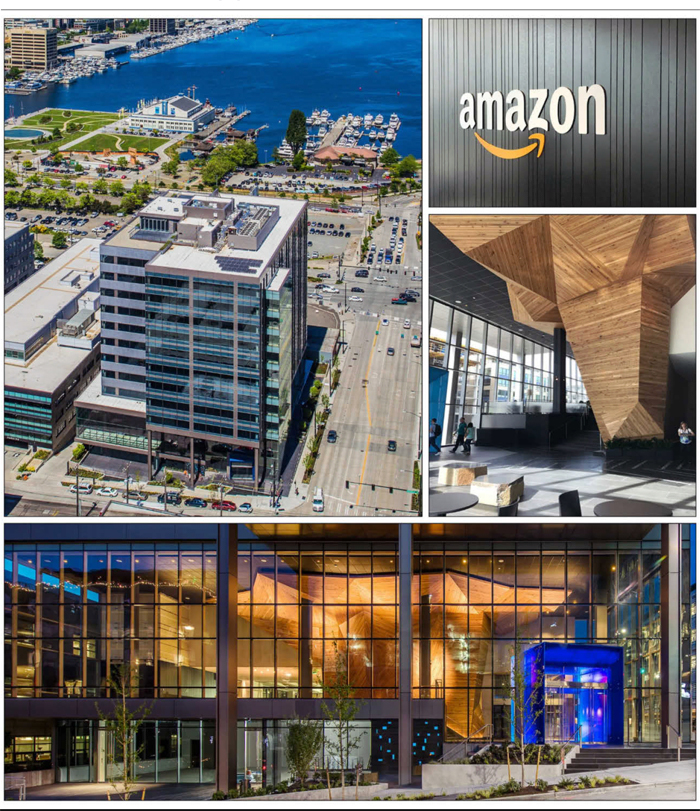

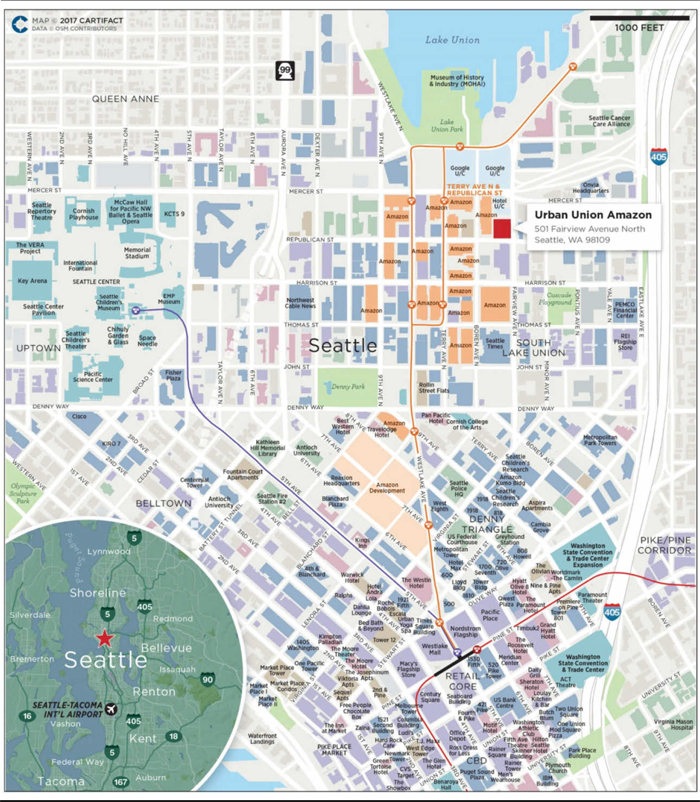

| 6 | Urban Union Amazon | Natixis | 1 | 38,231,428 | 4.7 | 295,793 | Office | 5.44x | 18.7% | 23.1% | 23.1% | A2/AA/AAA/AA- |

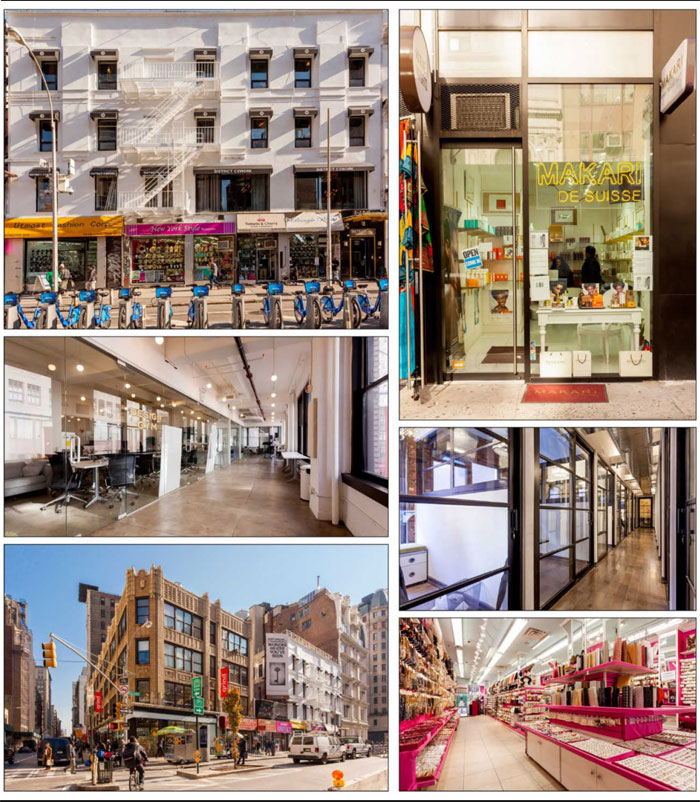

| 7 | Broadway Portfolio | Natixis | 3 | 38,000,000 | 4.7 | 77,419 | Various | 1.59x | 7.6% | 59.8% | 59.8% | NR/NR/NR/NR |

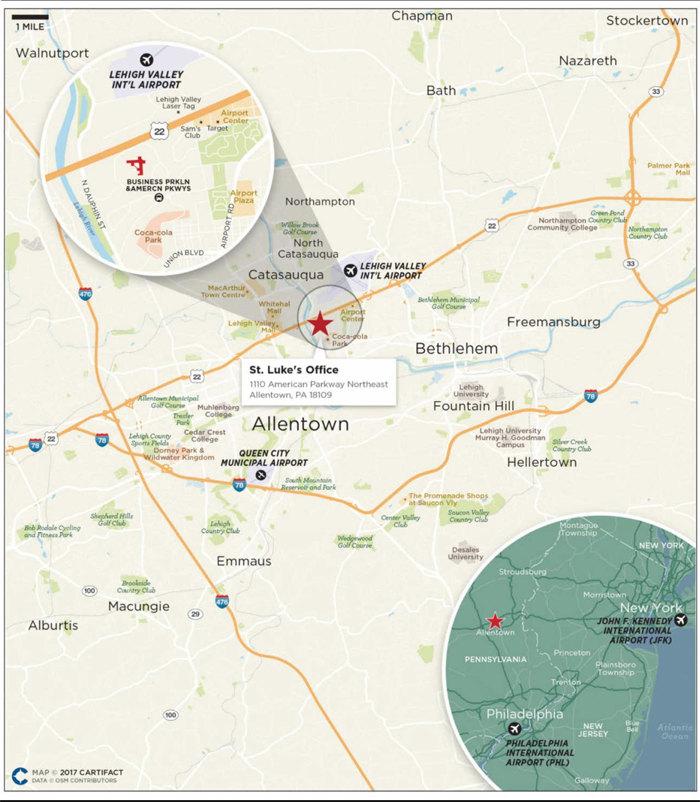

| 8 | St. Luke’s Office | BSP | 1 | 34,000,000 | 4.2 | 566,622 | Office | 1.72x | 11.8% | 55.4% | 46.4% | NR/NR/NR/NR |

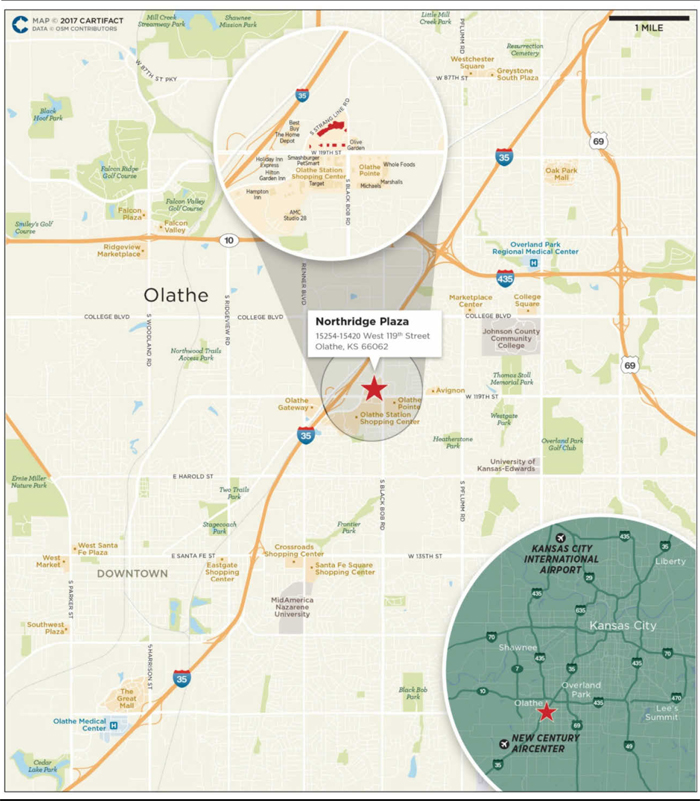

| 9 | Northridge Plaza | BSP | 1 | 32,500,000 | 4.0 | 209,652 | Retail | 1.38x | 9.3% | 64.9% | 55.8% | NR/NR/NR/NR |

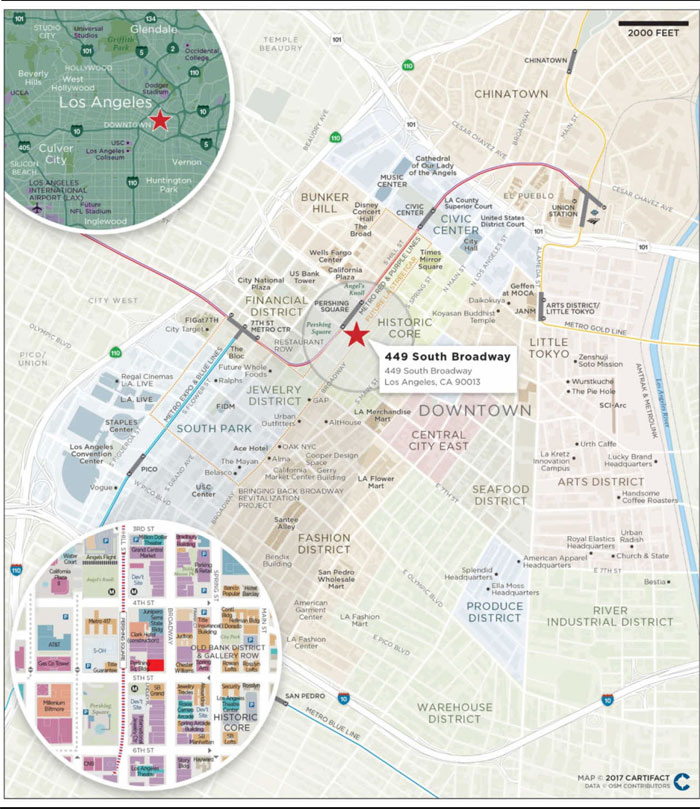

| 10 | 449 South Broadway | Natixis | 1 | 31,750,000 | 3.9 | 88 | Multifamily | 1.70x | 7.9% | 64.1% | 64.1% | NR/NR/NR/NR |

| Top 3 Total/Weighted Average | 3 | $240,350,000 | 29.6% | 3.44x | 13.6% | 36.4% | 36.4% | |||||

| Top 5 Total/Weighted Average | 5 | $335,350,000 | 41.3% | 2.97x | 13.4% | 42.8% | 41.8% | |||||

| Top 10 Total/Weighted Average | 12 | $509,831,428 | 62.9% | 2.79x | 12.6% | 46.2% | 44.3% | |||||

| (1) | In the case of Loan Nos. 1, 2, 3, 6, 7 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (2) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

Whole Loan Summary

| No. | Loan Name | Trust Cut-off Date Balance | Pari Passu Companion Loan Cut-off Date Balance | Whole Loan Cut-off Date Balance(1)(2) | Lead Pooling and Servicing Agreement | Master Servicer | Special Servicer |

| 1 | 85 Broad Street | $90,000,000 | $79,000,000 | $358,600,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 2 | 245 Park Avenue | $80,000,000 | $1,000,000,000 | $1,200,000,000 | PRKAV 2017-245P | Wells Fargo | AEGON |

| 3 | Apple Sunnyvale | $70,350,000 | $34,000,000 | $186,240,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 6 | Urban Union Amazon | $38,231,428 | $24,000,000 | $149,207,361 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 7 | Broadway Portfolio | $38,000,000 | $20,000,000 | $58,000,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 8 | St. Luke’s Office | $34,000,000 | $17,000,000 | $51,000,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 11 | Columbus Office Portfolio I | $30,000,000 | $15,300,000 | $45,300,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 13 | Acropolis Garden | $20,000,000 | $25,000,000 | $45,000,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 14 | Alexandria Corporate Park | $20,000,000 | $14,500,000 | $34,500,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 16 | Garden Multifamily Portfolio | $18,000,000 | $39,500,000 | $57,500,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| 25 | Marble Hall Gardens | $11,500,000 | $10,000,000 | $21,500,000 | CSAIL 2017-C8 | Wells Fargo | Midland |

| (1) | In the case of Loan Nos. 1, 2, 3 and 6, includes subordinate debt of one or more B notes. |

| (2) | In the case of Loan Nos. 2, 3, 6 and 8, excludes one or more mezzanine loans. |

Additional Debt Summary

| No. | Loan Name | Trust Cut-off Date Balance | Subordinate and Mezzanine Debt Cut-off Date Balance(1) | Total Debt Cut-off Date Balance(1)(2) | Mortgage Loan UW NCF DSCR | Total Debt UW NCF DSCR | Mortgage Loan Cut- off Date LTV | Total Debt Cut-off Date LTV | Mortgage Loan UW NOI Debt Yield | Total Debt UW NOI Debt Yield |

| 1 | 85 Broad Street | $90,000,000 | $189,600,000 | $358,600,000 | 4.11x | 1.75x | 25.9% | 55.0% | 15.3% | 7.2% |

| 2 | 245 Park Avenue | $80,000,000 | $688,000,000 | $1,768,000,000 | 2.73x | 1.42x | 48.9% | 80.0% | 10.7% | 6.5% |

| 3 | Apple Sunnyvale | $70,350,000 | $128,210,000 | $232,560,000 | 3.40x | 1.32x | 35.7% | 79.6% | 14.6% | 6.6% |

| 6 | Urban Union Amazon | $38,231,428 | $166,367,944 | $228,599,372 | 5.44x | 1.03x | 23.1% | 85.0% | 18.7% | 5.1% |

| 8 | St. Luke’s Office | $34,000,000 | $14,000,000 | $65,000,000 | 1.72x | 1.12x | 55.4% | 70.7% | 11.8% | 9.3% |

| (1) | In the case of Loan Nos. 2, 3, 6 and 8, includes one or more mezzanine loans. In the case of Loan Nos. 1, 2, 3 and 6, the subordinate debt includes one or more B notes, secured debt and unsecured debt. |

| (2) | Includes the mortgage loan in this securitization,pari passu loans, subordinate debt and mezzanine debt. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

Mortgaged Properties by Type(1)

| Weighted Average | |||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | Occupancy | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Office | |||||||||

| CBD | 3 | $208,231,428 | 25.7% | 90.9% | 3.82x | 14.2% | 34.2% | 34.2% | |

| Suburban | 9 | 159,174,350 | 19.6 | 94.1% | 2.39x | 12.8% | 51.0% | 46.0% | |

| Subtotal | 12 | $367,405,778 | 45.3% | 92.2% | 3.20x | 13.6% | 41.5% | 39.3% | |

| Hotel | |||||||||

| Full Service | 2 | $95,000,000 | 11.7% | 77.5% | 1.78x | 12.8% | 58.9% | 55.4% | |

| Select Service | 1 | 16,660,000 | 2.1 | 72.8% | 1.49x | 12.0% | 68.3% | 55.4% | |

| Limited Service | 1 | 6,150,000 | 0.8 | 71.1% | 1.92x | 16.0% | 64.1% | 45.0% | |

| Subtotal | 4 | $117,810,000 | 14.5% | 76.5% | 1.74x | 12.9% | 60.5% | 54.9% | |

| Retail | |||||||||

| Anchored | 4 | $62,279,367 | 7.7% | 93.5% | 1.56x | 9.5% | 64.3% | 57.2% | |

| Unanchored | 2 | 32,975,000 | 4.1 | 81.7% | 1.53x | 9.9% | 60.1% | 52.0% | |

| Single Tenant | 5 | 22,350,001 | 2.8 | 100.0% | 1.59x | 10.0% | 58.2% | 52.5% | |

| Subtotal | 11 | $117,604,368 | 14.5% | 91.4% | 1.56x | 9.7% | 61.9% | 54.8% | |

| Multifamily | |||||||||

| Garden | 20 | $52,997,381 | 6.5% | 97.2% | 1.50x | 10.1% | 66.2% | 54.9% | |

| Mid-Rise | 1 | 31,750,000 | 3.9 | 97.7% | 1.70x | 7.9% | 64.1% | 64.1% | |

| Cooperative | 1 | 20,000,000 | 2.5 | 0.0% | 5.31x | 20.4% | 25.4% | 25.4% | |

| Subtotal | 22 | $104,747,381 | 12.9% | 78.8% | 2.29x | 11.4% | 57.8% | 52.1% | |

| Mixed Use | |||||||||

| Office/Retail | 3 | $46,182,433 | 5.7% | 79.1% | 1.53x | 8.1% | 61.2% | 59.4% | |

| Subtotal | 3 | $46,182,433 | 5.7% | 79.1% | 1.53x | 8.1% | 61.2% | 59.4% | |

| Industrial | |||||||||

| Flex | 2 | $32,305,605 | 4.0% | 96.8% | 1.41x | 10.8% | 66.8% | 56.1% | |

| Subtotal | 2 | $32,305,605 | 4.0% | 96.8% | 1.41x | 10.8% | 66.8% | 56.1% | |

| Other | |||||||||

| Leased Fee | 1 | $25,000,000 | 3.1% | 0.0% | 3.74x | 14.7% | 19.2% | 19.2% | |

| Subtotal | 1 | $25,000,000 | 3.1% | 0.0% | 3.74x | 14.7% | 19.2% | 19.2% | |

| Total / Wtd. Avg.: | 55 | $811,055,563 | 100.0% | 84.7% | 2.48x | 12.2% | 50.8% | 46.7% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6 the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. In the case of Loan No. 12, with an anticipated repayment date, Maturity Date LTV, is calculated through or as of, as applicable, the related anticipated repayment date. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. In the case of Loan No. 12, with an anticipated repayment date, Maturity Date LTV is calculated through or as of, as applicable, the related anticipated repayment date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

Mortgaged Properties by Location(1)

| State | Number of Properties | Cut-off Date Principal Balance | % of IPB | Weighted Average | ||||

| Occupancy | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||||

| NY | 8 | $268,750,000 | 33.1% | 72.6% | 3.29x | 12.9% | 38.7% | 38.7% |

| CA | 3 | 156,100,000 | 19.2 | 91.0% | 2.50x | 12.8% | 49.3% | 49.3% |

| PA | 2 | 50,660,000 | 6.2 | 85.1% | 1.64x | 11.9% | 59.6% | 49.4% |

| OR | 1 | 41,000,000 | 5.1 | 80.4% | 1.74x | 12.1% | 59.8% | 51.7% |

| OH | 11 | 38,452,174 | 4.7 | 87.1% | 1.56x | 11.5% | 70.3% | 60.3% |

| WA | 1 | 38,231,428 | 4.7 | 100.0% | 5.44x | 18.7% | 23.1% | 23.1% |

| KS | 1 | 32,500,000 | 4.0 | 88.2% | 1.38x | 9.3% | 64.9% | 55.8% |

| NV | 2 | 30,405,605 | 3.7 | 80.2% | 1.49x | 10.3% | 63.6% | 52.8% |

| GA | 4 | 26,609,398 | 3.3 | 98.9% | 1.33x | 9.5% | 67.2% | 55.9% |

| VA | 1 | 20,000,000 | 2.5 | 100.0% | 1.32x | 10.5% | 65.1% | 55.0% |

| FL | 3 | 18,649,460 | 2.3 | 90.5% | 1.64x | 12.0% | 58.9% | 47.4% |

| NJ | 1 | 14,875,000 | 1.8 | 92.9% | 1.64x | 10.3% | 60.7% | 55.4% |

| CT | 1 | 13,230,000 | 1.6 | 100.0% | 1.41x | 9.0% | 64.7% | 57.0% |

| MD | 1 | 11,500,000 | 1.4 | 96.2% | 1.74x | 11.8% | 68.5% | 56.3% |

| LA | 2 | 10,027,089 | 1.2 | 94.4% | 1.61x | 11.2% | 61.1% | 50.5% |

| UT | 1 | 9,250,000 | 1.1 | 98.8% | 1.30x | 10.1% | 67.0% | 58.0% |

| TX | 2 | 6,775,000 | 0.8 | 100.0% | 1.25x | 8.2% | 65.3% | 57.6% |

| AZ | 1 | 6,567,261 | 0.8 | 75.4% | 1.39x | 11.6% | 65.0% | 55.2% |

| MA | 1 | 3,900,541 | 0.5 | 100.0% | 1.50x | 10.1% | 56.3% | 48.6% |

| WY | 1 | 3,133,245 | 0.4 | 100.0% | 1.86x | 9.6% | 63.3% | 63.3% |

| MI | 2 | 3,036,522 | 0.4 | 95.1% | 1.37x | 9.4% | 71.7% | 59.0% |

| MO | 1 | 2,816,755 | 0.3 | 100.0% | 1.86x | 9.6% | 63.3% | 63.3% |

| IN | 2 | 2,391,652 | 0.3 | 98.2% | 1.37x | 9.4% | 71.7% | 59.0% |

| KY | 2 | 2,194,435 | 0.3 | 96.7% | 1.37x | 9.4% | 71.7% | 59.0% |

| Total/Wtd. Avg.: | 55 | $811,055,564 | 100.0% | 84.7% | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. In the case of Loan No. 12, with an anticipated repayment date, Maturity Date LTV, is calculated through or as of, as applicable, the related anticipated repayment date. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. In the case of Loan No. 12, with an anticipated repayment date, Maturity Date LTV is calculated through or as of, as applicable, the related anticipated repayment date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

Cut-off Date Principal Balance

| Weighted Average | |||||||||

| Range of Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 5,000,000 - 9,999,999 | 7 | $44,719,350 | 5.5% | 5.1662% | 118 | 1.53x | 11.0% | 64.2% | 54.8% |

| 10,000,000 - 14,999,999 | 6 | 76,594,786 | 9.4 | 4.9560% | 118 | 1.50x | 10.2% | 66.0% | 56.3% |

| 15,000,000 - 19,999,999 | 5 | 84,910,000 | 10.5 | 4.8937% | 120 | 1.59x | 10.2% | 62.8% | 53.9% |

| 20,000,000 - 34,999,999 | 7 | 193,250,000 | 23.8 | 4.6605% | 119 | 2.23x | 11.9% | 53.9% | 48.3% |

| 35,000,000 - 49,999,999 | 3 | 117,231,428 | 14.5 | 4.3387% | 96 | 2.90x | 12.8% | 47.8% | 45.0% |

| 50,000,000 - 90,000,000 | 4 | 294,350,000 | 36.3 | 4.0898% | 94 | 3.14x | 13.5% | 40.4% | 40.4% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

Mortgage Interest Rates

| Weighted Average | ||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) | |

| 3.3812% - 3.9999% | 5 | $253,231,428 | 31.2% | 3.5594% | 110 | 3.93x | 14.7% | 32.0% | 32.0% | |

| 4.0000% - 4.4999% | 4 | 132,725,000 | 16.4 | 4.3054% | 86 | 2.66x | 12.0% | 47.9% | 47.3% | |

| 4.5000% - 4.9999% | 9 | 198,627,381 | 24.5 | 4.7916% | 118 | 1.58x | 10.1% | 60.1% | 53.0% | |

| 5.0000% - 5.4999% | 10 | 132,942,694 | 16.4 | 5.1151% | 118 | 1.54x | 11.1% | 67.6% | 56.7% | |

| 5.5000% - 5.9000% | 4 | 93,529,061 | 11.5 | 5.7171% | 83 | 1.59x | 12.1% | 62.0% | 57.6% | |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% | |

Original Term to Maturity/ARD in Months

| Weighted Average | |||||||||

| Original Term to Maturity/ARD in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 60 | 3 | $162,581,428 | 20.0% | 4.5049% | 57 | 3.35x | 15.2% | 40.2% | 40.2% |

| 120 | 29 | 648,474,135 | 80.0 | 4.4826% | 119 | 2.27x | 11.5% | 53.4% | 48.3% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

Remaining Term to Maturity/ARD in Months

| Weighted Average | |||||||||

| Remaining Term to Maturity/ARD in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 56 - 60 | 3 | $162,581,428 | 20.0% | 4.5049% | 57 | 3.35x | 15.2% | 40.2% | 40.2% |

| 61 - 120 | 29 | 648,474,135 | 80.0 | 4.4826% | 119 | 2.27x | 11.5% | 53.4% | 48.3% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

Original Amortization Term in Months

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| Interest Only | 11 | $469,031,428 | 57.8% | 4.0915% | 97 | 3.18x | 13.3% | 41.3% | 41.3% |

| 270 | 1 | 6,150,000 | 0.8 | 5.2500% | 120 | 1.92x | 16.0% | 64.1% | 45.0% |

| 300 | 1 | 16,660,000 | 2.1 | 5.0800% | 120 | 1.49x | 12.0% | 68.3% | 55.4% |

| 360 | 19 | 319,214,135 | 39.4 | 5.0226% | 118 | 1.52x | 10.7% | 63.6% | 54.2% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

Remaining Amortization Term in Months

| Weighted Average | |||||||||

| Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| Interest Only | 11 | $469,031,428 | 57.8% | 4.0915% | 97 | 3.18x | 13.3% | 41.3% | 41.3% |

| 270 - 300 | 2 | 22,810,000 | 2.8 | 5.1258% | 120 | 1.60x | 13.1% | 67.2% | 52.6% |

| 301 - 359 | 5 | 48,584,135 | 6.0 | 5.3425% | 116 | 1.40x | 10.3% | 67.5% | 56.4% |

| 360 - 360 | 14 | 270,630,000 | 33.4 | 4.9652% | 119 | 1.54x | 10.7% | 62.9% | 53.8% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

Amortization Types

| Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| Interest Only | 10 | $444,031,428 | 54.7% | 4.1034% | 96 | 3.15x | 13.2% | 42.5% | 42.5% |

| IO-Balloon | 10 | 214,690,000 | 26.5 | 4.8730% | 118 | 1.56x | 10.9% | 62.5% | 53.8% |

| Balloon | 11 | 127,334,135 | 15.7 | 5.2934% | 119 | 1.46x | 10.6% | 66.0% | 54.4% |

| Interest Only, ARD | 1 | 25,000,000 | 3.1 | 3.8800% | 116 | 3.74x | 14.7% | 19.2% | 19.2% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

Interest Only Periods(5)

| Weighted Average | |||||||||

| Interest Only Periods | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 12 - 24 | 7 | $179,810,000 | 22.2% | 4.9245% | 118 | 1.58x | 11.2% | 62.4% | 53.3% |

| 25 - 48 | 2 | 20,005,000 | 2.5 | 4.8037% | 119 | 1.36x | 8.7% | 64.9% | 57.2% |

| 49 - 60 | 4 | 177,456,428 | 21.9 | 4.4913% | 62 | 3.21x | 14.8% | 41.9% | 41.5% |

| 61 - 120 | 8 | 306,450,000 | 37.8 | 3.8722% | 119 | 3.09x | 12.3% | 41.8% | 41.8% |

| Total/Wtd. Avg.: | 21 | $683,721,428 | 84.3% | 4.3369% | 104 | 2.67x | 12.6% | 47.9% | 45.2% |

Underwritten Net Cash Flow Debt Service Coverage Ratios(2)(3)

| Weighted Average | |||||||||

| Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 1.21 - 1.49 | 13 | $187,193,530 | 23.1% | 5.1204% | 119 | 1.39x | 9.9% | 65.1% | 55.0% |

| 1.50 - 1.74 | 8 | 213,430,605 | 26.3 | 4.7886% | 117 | 1.67x | 10.4% | 62.2% | 56.3% |

| 1.75 - 1.99 | 4 | 71,100,000 | 8.8 | 5.5109% | 73 | 1.83x | 13.2% | 58.8% | 56.4% |

| 2.00 - 2.99 | 2 | 95,750,000 | 11.8 | 3.7764% | 120 | 2.64x | 10.6% | 50.3% | 50.3% |

| 3.00 - 5.44 | 5 | 243,581,428 | 30.0 | 3.7166% | 91 | 4.17x | 16.0% | 27.6% | 27.6% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

| (5) | Excluding eleven (11) loans that have no interest-only period during the loan term. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

LTV Ratios as of the Cut-off Date(1)(2)

| Weighted Average | ||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) | |

| 19.2% - 44.9% | 5 | $243,581,428 | 30.0% | 3.7166% | 91 | 4.17x | 16.0% | 27.6% | 27.6% | |

| 45.0% - 54.9% | 2 | 85,000,000 | 10.5 | 3.7341% | 120 | 2.68x | 10.8% | 49.2% | 48.6% | |

| 55.0% - 59.9% | 7 | 217,250,000 | 26.8 | 4.9950% | 103 | 1.72x | 11.1% | 58.3% | 53.9% | |

| 60.0% - 64.9% | 7 | 116,177,381 | 14.3 | 4.6832% | 119 | 1.57x | 9.4% | 63.7% | 57.4% | |

| 65.0% - 69.9% | 9 | 118,084,955 | 14.6 | 5.2911% | 118 | 1.48x | 11.2% | 67.9% | 57.4% | |

| 70.0% - 71.7% | 2 | 30,961,800 | 3.8 | 5.2486% | 119 | 1.30x | 9.4% | 71.7% | 59.5% | |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% | |

LTV Ratios as of the Maturity Date(1)(2)

| Weighted Average | |||||||||

| Range of Maturity/ARD Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| 19.2% - 34.9% | 4 | $173,231,428 | 21.4% | 3.5086% | 105 | 4.49x | 16.6% | 24.3% | 24.3% |

| 35.0% - 44.9% | 2 | 75,350,000 | 9.3 | 4.2648% | 61 | 3.30x | 14.5% | 36.9% | 36.2% |

| 45.0% - 54.9% | 7 | 207,372,381 | 25.6 | 4.4305% | 119 | 2.06x | 11.1% | 54.8% | 49.0% |

| 55.0% - 59.9% | 15 | 274,439,955 | 33.8 | 5.0764% | 106 | 1.58x | 10.5% | 63.4% | 57.3% |

| 60.0% - 64.1% | 4 | 80,661,800 | 9.9 | 4.9362% | 118 | 1.60x | 9.8% | 67.4% | 62.1% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

Prepayment Protection

| Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| Defeasance | 28 | $571,474,135 | 70.5% | 4.7267% | 113 | 1.97x | 11.1% | 57.7% | 52.5% |

| Defeasance/Yield Maintenance | 3 | 198,581,428 | 24.5 | 3.6957% | 85 | 4.11x | 15.7% | 28.8% | 28.8% |

| Yield Maintenance | 1 | 41,000,000 | 5.1 | 4.9800% | 117 | 1.74x | 12.1% | 59.8% | 51.7% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

Loan Purpose

| Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(1)(2)(4) |

| Refinance | 22 | $446,714,135 | 55.1% | 4.8965% | 111 | 1.89x | 11.2% | 57.7% | 52.0% |

| Acquisition | 10 | 364,341,428 | 44.9 | 3.9851% | 101 | 3.22x | 13.6% | 42.2% | 40.1% |

| Total/Wtd. Avg.: | 32 | $811,055,563 | 100.0% | 4.4871% | 106 | 2.48x | 12.2% | 50.8% | 46.7% |

| (1) | In the case of Loan No. 12, with an anticipated repayment date, Remaining Loan Term and Maturity Date LTV are calculated through or as of, as applicable, the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 1, 2, 3, 6, 7, 8, 11, 13, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the relatedpari passu companion loan(s). In the case of Loan Nos. 1, 2, 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 2, 3, 6 and 8, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

| (3) | For each partial interest-only mortgage loan, the UW NCF DSCR is calculated using the first principal and interest payment to be made into the trust during the term of the mortgage loan once amortization has commenced. |

| (4) | In the case of Loan No. 21, the Cut-off Date LTV and Maturity Date LTV are calculated based upon an “as-stabilized” appraised value as of October 1, 2017. The as-is Cut-off Date LTV is 75.2%. |

Previous Securitization History(1)

| No. | Loan / Property Name | Location | Property Type | Previous Securitization |

| 22 | Walmart Shopping Center Moultrie | Moultrie, GA | Retail | JPMCC 2006-CB17 |

| 23 | Valley View I | Las Vegas, NV | Industrial | WBCMT 2007-C30 |

| 26 | Plaza 7-21 | Salt Lake City, UT | Mixed Use | MSC 2007-IQ16 |

| 30 | Walgreens - WY and MO | Various, Various | Retail | JPMCC 2007-LDPX |

| (1) | The table above represents the properties for which the previously existing debt was most recently securitized, based on information provided by the related borrower or obtained through searches of a third-party database. While loans secured by the above mortgaged properties may have been securitized multiple times in prior transactions, mortgage loans in this securitization are only listed in the above chart if the mortgage loan in this securitization paid off a loan in another securitization. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

Class A-2(1)

| No. | Loan Name | Location | Cut-off Date Balance | % of IPB | Maturity/ARD Balance | % of Certificate Class | Original Loan Term | Remaining Loan Term | UW NCF DSCR(2) | UW NOI Debt Yield(2) | Cut-off Date LTV Ratio(2) | Maturity Date LTV Ratio(2) |

| 3 | Apple Sunnyvale | Sunnyvale, CA | $70,350,000 | 8.7% | $70,350,000 | 43.0% | 60 | 57 | 3.40x | 14.6% | 35.7% | 35.7% |

| 4 | Ritz Carlton Rancho Mirage | Rancho Mirage, CA | $54,000,000 | 6.7% | $54,000,000 | 33.0% | 60 | 58 | 1.81x | 13.4% | 58.2% | 58.2% |

| 6 | Urban Union Amazon | Seattle, WA | $38,231,428 | 4.7% | $38,231,428 | 23.4% | 60 | 56 | 5.44x | 18.7% | 23.1% | 23.1% |

| Total /Wtd. Avg.: | $162,581,428 | 20.0% | $162,581,428 | 60 | 57 | 3.35x | 15.2% | 40.2% | 40.2% | |||

| (1) | The table above presents the mortgage loans whose balloon payments would be applied to pay down the majority of the principal balance of the Class A-2 certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments prior to the maturity date, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of certificates, including the Class A-2 certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | In the case of Loan Nos. 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related pari passu companion loan(s). In the case of Loan Nos. 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the subordinate companion loan(s) or other subordinate indebtedness. In the case of Loan Nos. 3 and 6, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the mezzanine loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

Structural Overview

| Order of Distribution: | On each Distribution Date, funds available for distribution from the pooled mortgage loans, net of specified trust expenses, yield maintenance charges, prepayment premiums and excess interest distributable to the Class Z Certificates, will be distributed in the following amounts and order of priority (in each case to the extent of remaining pooled available funds):

First:To interest on the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class X-A and Class X-B certificates, up to, andpro rata in accordance with, their respective interest entitlements.

Second:To the extent of funds allocated to principal and available for distribution: (i) first,to principal on the Class A-SB certificates, until the certificate balance of the Class A-SB certificates is reduced to the scheduled principal balance for the related distribution date set forth in Annex E to the Preliminary Prospectus, (ii) second,to principal on the Class A-1 certificates, until the certificate balance of the Class A-1 certificates has been reduced to zero, (iii)third,to principal on the Class A-2 certificates, until the certificate balance of the Class A-2 certificates has been reduced to zero, (iv) fourth,to principal on the Class A-3 certificates, until the certificate balance of the Class A-3 certificates has been reduced to zero, (v)fifth, to principal on the Class A-4 certificates until the certificate balance of the Class A-4 certificates has been reduced to zero and (vi)sixth, to principal on the Class A-SB certificates, until the certificate balance of the Class A-SB certificates has been reduced to zero. If the certificate balance of each and every class of certificates other than the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates has been reduced to zero as a result of the allocation of mortgage loan losses to those certificates, funds available for distributions of principal will be distributed to the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates,pro rata, based on their respective certificate balances, without regard to the distribution priorities described above or the planned principal balance of the Class A-SB certificates.

Third:To reimburse the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates,pro rata, for any previously unreimbursed losses on the mortgage loans allocable to principal that were previously borne by those classes, together with interest on that amount at the pass-through rate for such class.

Fourth:(i)first, to interest on the Class A-S certificates in the amount of their interest entitlement; (ii)second, to the extent of funds allocated to principal remaining after any distributions in respect of principal to each class of certificates with a higher payment priority (in this case, the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates), to principal on the Class A-S certificates until their certificate balance is reduced to zero; and (iii)third, to reimburse the Class A-S certificates for any previously unreimbursed losses on the mortgage loans allocable to principal that were previously borne by that class, together with interest at its pass-through rate.

Fifth:(i)first, to interest on the Class B certificates in the amount of their interest entitlement; (ii)second, to the extent of funds allocated to principal remaining after any distributions in respect of principal to each class of certificates with a higher payment priority (in this case, the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB and Class A-S certificates), to principal on the Class B certificates until their certificate balance |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| Order of Distribution (continued): | is reduced to zero; and (iii)third, to reimburse the Class B certificates for any previously unreimbursed losses on the mortgage loans allocable to principal that were previously borne by that class, together with interest at its pass-through rate.

Sixth:(i)first, to interest on the Class C certificates in the amount of their interest entitlement; (ii)second, to the extent of funds allocated to principal remaining after any distributions in respect of principal to each class of certificates with a higher payment priority (in this case, the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-S and Class B certificates), to principal on the Class C certificates until their certificate balance is reduced to zero; and (iii)third, to reimburse the Class C certificates for any previously unreimbursed losses on the mortgage loans allocable to principal that were previously borne by that class, together with interest at its pass-through rate.

Seventh:After the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class X-A, Class X-B, Class A-S, Class B and Class C certificates are paid all amounts to which they are entitled, the remaining funds available for distribution will be used to pay interest and principal and to reimburse any unreimbursed losses to the Class D, Class E, Class F and Class NR certificates sequentially in that order in a manner analogous to that described in clausesixthabove with respect to the Class C certificates, until the certificate balance of each such class is reduced to zero.

The holders of the 85 Broad Street loan-specific certificates will only be entitled to receive distributions at the related pass-through rate in respect of, and will only incur losses with respect to, the 85 Broad Street trust subordinate companion loan, which is included as an asset of the issuing entity, but not part of the pool of mortgage loans backing the other classes of certificates, as described under “—Realized Losses” below.

For more detailed information regarding the distributions on the pooled certificates, see “Description of the Certificates—Distributions—Priority of Distributions” in the Preliminary Prospectus. |

Realized Losses:

| The certificate balances of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-S, Class B, Class C, Class D, Class E, Class F and Class NR certificates will each be reduced without distribution on any Distribution Date as a write-off to the extent of any loss realized on the mortgage loans allocated to such class of certificates on such Distribution Date. On each Distribution Date, any such write-offs will be applied to such classes of certificates in the following order, in each case until the related certificate balance is reduced to zero:first, to the Class NR certificates;second, to the Class F certificates;third, to the Class E certificates;fourth, to the Class D certificates;fifth, to the Class C certificates;sixth, to the Class B certificates;seventh, to the Class A-S certificates; and,finally,pro rata, to the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates, based on their then-current respective certificate balances. The notional amount of the Class X-A certificates will be reduced to reflect reductions in the certificate balances of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB and Class A-S certificates resulting from allocations of losses realized on the mortgage loans. The notional amount of the Class X-B certificates will be reduced to reflect reductions in the certificate balance of the Class B and Class C certificates resulting from allocations of losses realized on the mortgage loans.

The certificate balances of the privately offered 85 Broad Street loan-specific certificates will each be reduced without distribution on any Distribution Date as a write off to the |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| Realized Losses (continued): | extent of any loss realized on the 85 Broad Street trust subordinate companion loan allocated to such class of certificates on such Distribution Date. On each Distribution Date, any such write offs will be applied to such classes of certificates:first, to the Class 85-D certificates,second, to the Class 85-C certificates,third, to the 85-B certificates and,then, to the 85-A certificates, in each case until the related certificate balance is reduced to zero. The notional amount of the Class X-85 certificates will be reduced to reflect reductions in the certificate balances of the 85 Broad Street loan-specific certificates resulting from allocations of losses realized on the 85 Broad Street trust subordinate companion loan. |

| Prepayment Premiums and Yield Maintenance Charges: | On each Distribution Date, each yield maintenance charge collected on the pooled mortgage loans during the one-month period ending on the related Determination Date is required to be distributed to certificateholders (excluding the Class E, Class F, Class NR, Class Z and Class R certificates) as follows: (1)pro rata, between (x) the group (the “YM Group A”) of Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class X-A and Class A-S certificates, and (y) the group (the “YM Group B” and collectively with the YM Group A, the “YM Groups”) of the Class X-B, Class B, Class C and Class D certificates, based upon the aggregate amount of principal distributed to the classes of pooled principal balance certificates in each YM Group on such Distribution Date, and (2) as among the respective classes of pooled principal balance certificates in each YM Group in the following manner: (A) on apro rata basis in accordance with their respective entitlements in those yield maintenance charges, to each class of pooled principal balance certificates in such YM Group with a certificate balance in an amount equal to the product of (x) a fraction whose numerator is the amount of principal distributed to such class of pooled principal balance certificates on such Distribution Date and whose denominator is the total amount of principal distributed to all of the certificates in such YM Group with certificate balances on such Distribution Date, (y) the Base Interest Fraction for the related principal prepayment with respect to such class of pooled principal balance certificates, and (z) the aggregate amount of such yield maintenance charge allocated to such YM Group; and (B) the portion of such yield maintenance charge allocated to such YM Group remaining after such distributions to the applicable class(es) of pooled principal balance certificates in such YM Group, in the case of amounts distributable to YM Group A, to the Class X-A certificates and in the case of amounts distributable to YM Group B, to the Class X-B certificates.

Any yield maintenance charges payable in respect of the 85 Broad Street trust subordinate companion loan will be distributed to the 85 Broad Street loan-specific certificates and will not be allocated to the other classes of certificates.

The “Base Interest Fraction” with respect to any principal prepayment on any mortgage loan and with respect to any class of Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-S, Class B, Class C and Class D certificates is a fraction (a) whose numerator is the greater of (x) zero and (y) the difference between (i) the pass-through rate on such class of certificates and (ii) the discount rate used in accordance with the related mortgage loan documents in calculating the yield maintenance charge with respect to such principal prepayment and (b) whose denominator is the greater of zero and the difference between (i) the mortgage loan rate on such mortgage loan (or serviced whole loan) and (ii) the discount rate used in accordance with the related mortgage loan documents in calculating the yield maintenance charge with respect to such principal prepayment; |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

19

| Prepayment Premiums and Yield Maintenance Charges (continued): | provided,however, that under no circumstances will the Base Interest Fraction be greater than one or less than zero. If such discount rate is greater than or equal to the lesser of (x) the mortgage loan rate on the related mortgage loan and (y) the pass-through rate described in the preceding sentence, then the Base Interest Fraction will equal zero;provided,however, that if such discount rate is greater than or equal to the mortgage loan rate, but less than the pass-through rate, the fraction will be one.

If a prepayment premium (calculated as a fixed percentage of the amount prepaid) is imposed in connection with a prepayment rather than a yield maintenance charge, then the prepayment premium so collected will be allocated as described above. For this purpose, the discount rate used to calculate the Base Interest Fraction will be the discount rate used to determine the yield maintenance charge for mortgage loans that require payment at the greater of a yield maintenance charge or a minimum amount equal to a fixed percentage of the principal balance of the mortgage loan or, for mortgage loans that only have a prepayment premium based on a fixed percentage of the principal balance of the mortgage loan, such other discount rate as may be specified in the related loan documents.