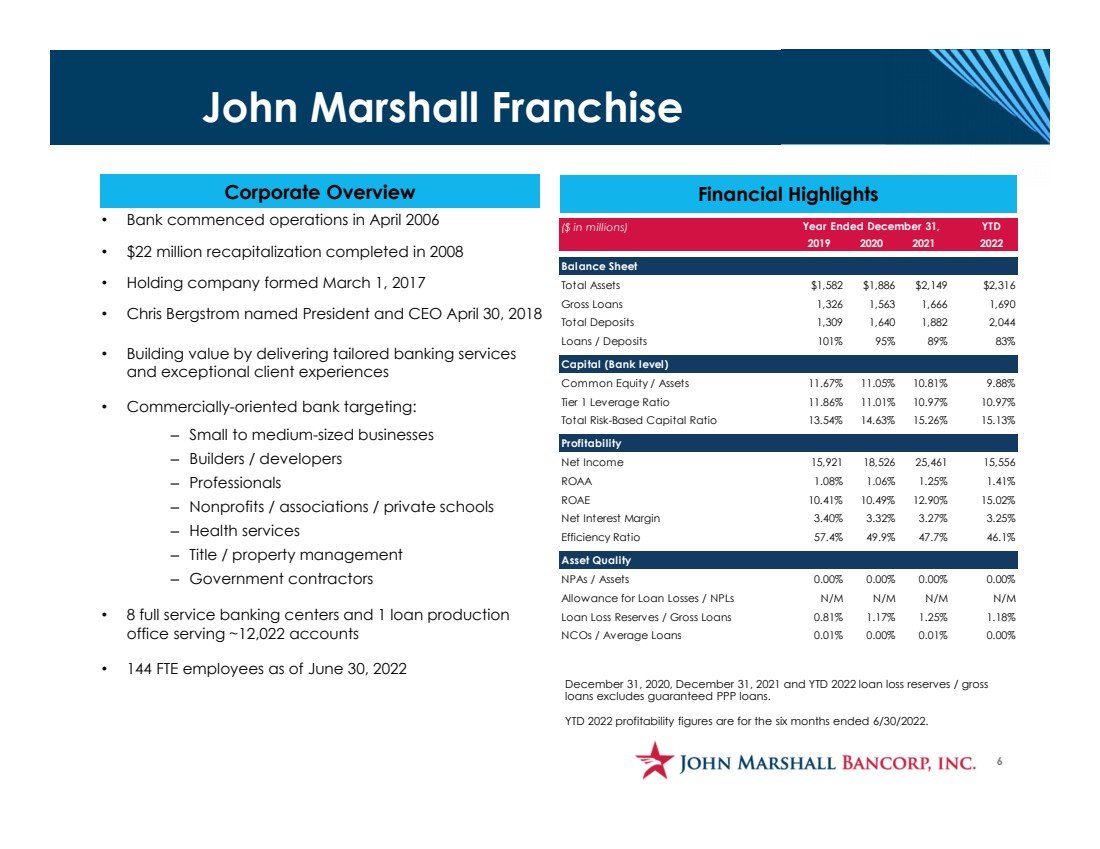

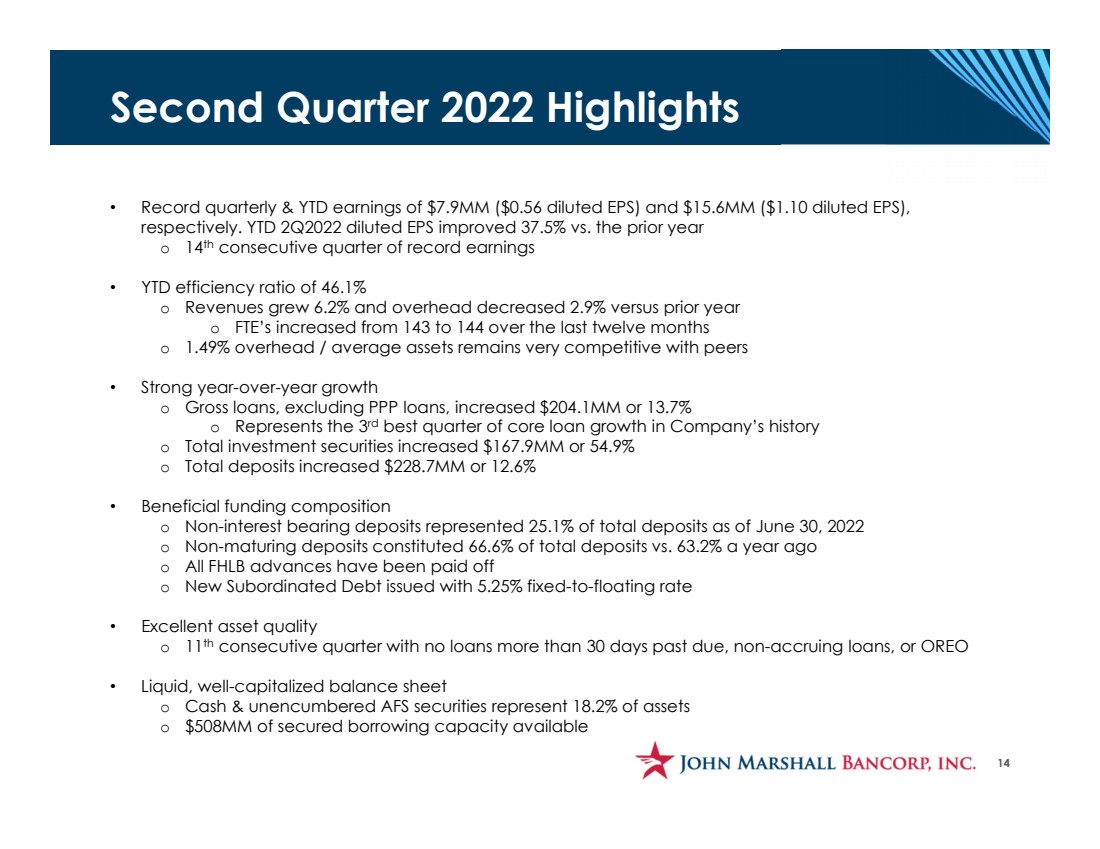

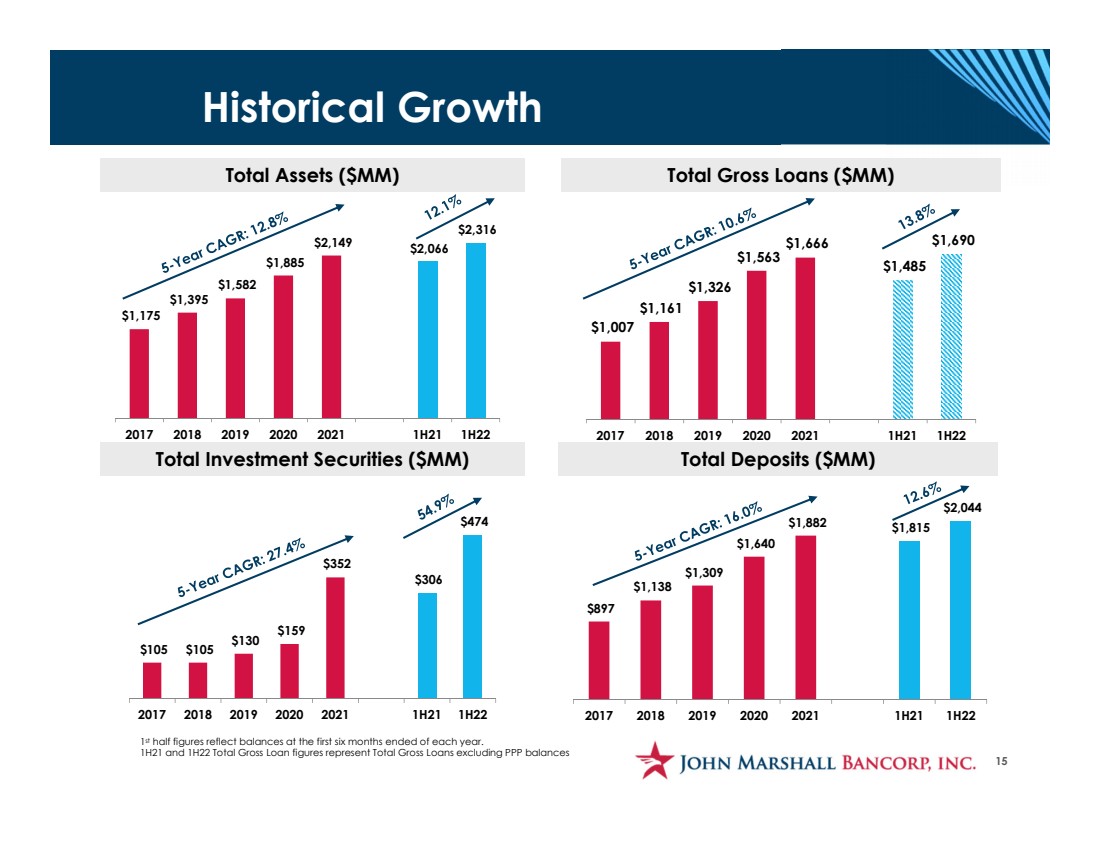

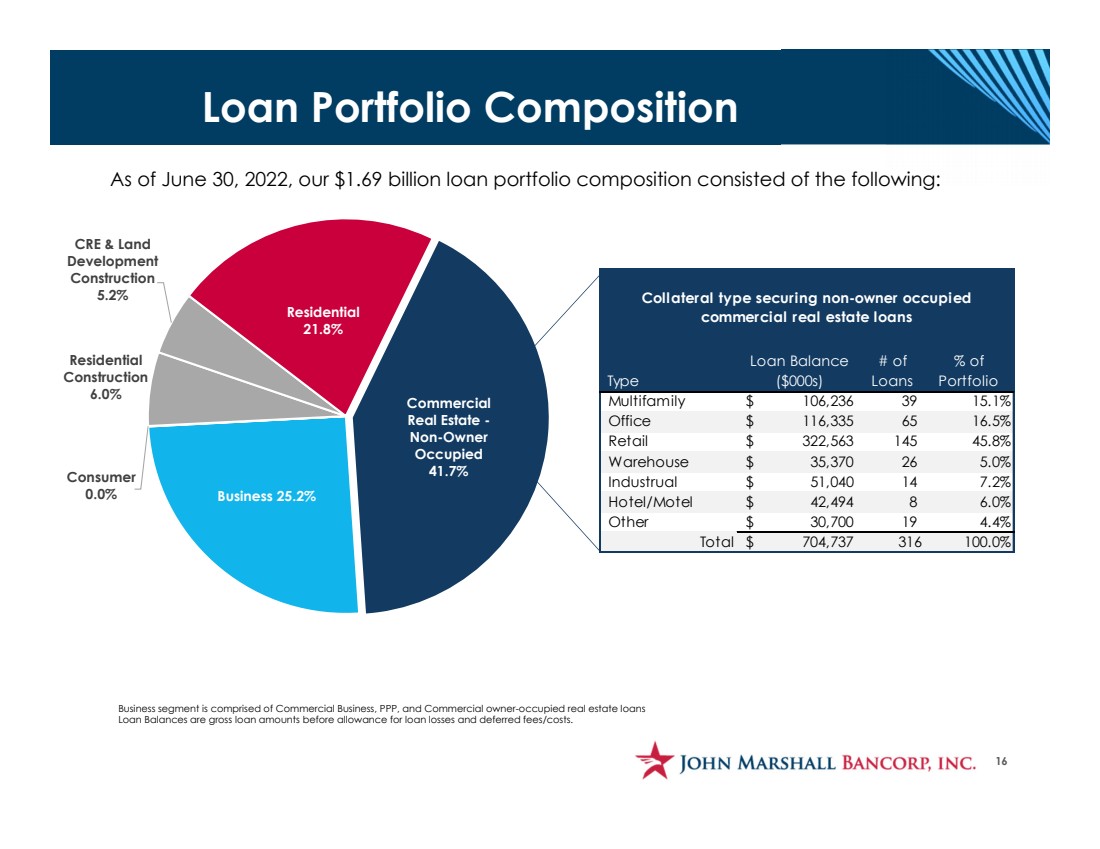

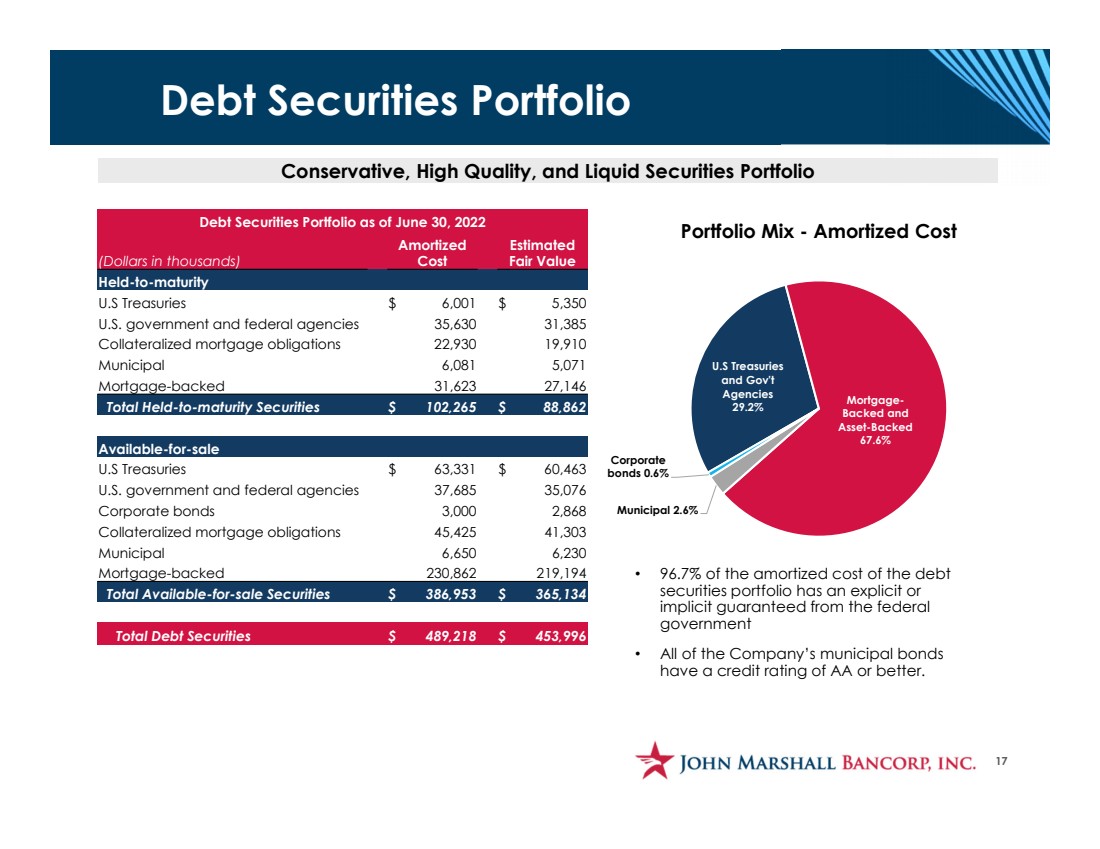

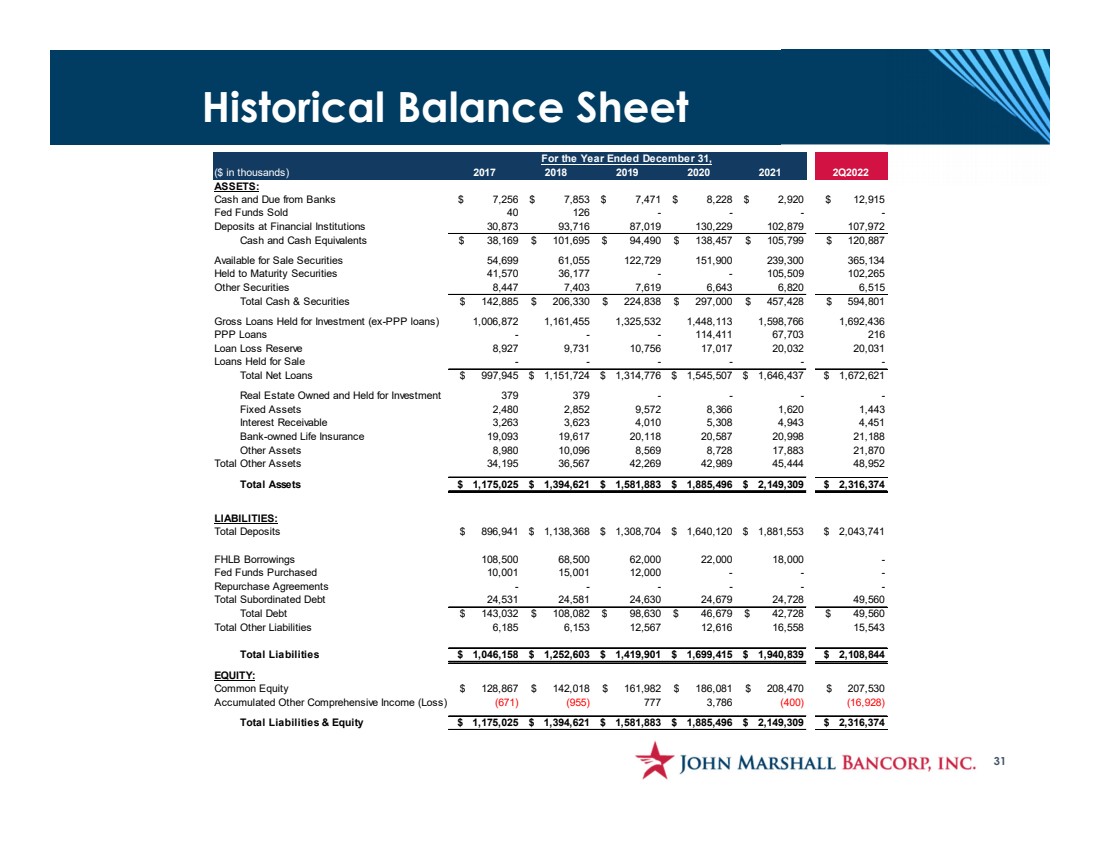

| Historical Balance Sheet31 ($ in thousands)201720182019202020212Q2022ASSETS: Cash and Due from Banks $ 7,256 $ 7,853 $ 7,471 $ 8,228 $ 2,920 $ 12,915 Fed Funds Sold 40 126 - - - - Deposits at Financial Institutions 30,873 93,716 87,019 130,229 102,879 107,972 Cash and Cash Equivalents $ 38,169 $ 101,695 $ 94,490 $ 138,457 $ 105,799 $ 120,887 Available for Sale Securities 54,699 61,055 122,729 151,900 239,300 365,134 Held to Maturity Securities 41,570 36,177 - - 105,509 102,265 Other Securities 8,447 7,403 7,619 6,643 6,820 6,515 Total Cash & Securities $ 142,885 $ 206,330 $ 224,838 $ 297,000 $ 457,428 $ 594,801 Gross Loans Held for Investment (ex-PPP loans) 1,006,872 1,161,455 1,325,532 1,448,113 1,598,766 1,692,436 PPP Loans - - - 114,411 67,703 216 Loan Loss Reserve 8,927 9,731 10,756 17,017 20,032 20,031 Loans Held for Sale - - - - - - Total Net Loans $ 997,945 $ 1,151,724 $ 1,314,776 $ 1,545,507 $ 1,646,437 $ 1,672,621 Real Estate Owned and Held for Investment 379 379 - - - - Fixed Assets 2,480 2,852 9,572 8,366 1,620 1,443 Interest Receivable 3,263 3,623 4,010 5,308 4,943 4,451 Bank-owned Life Insurance 19,093 19,617 20,118 20,587 20,998 21,188 Other Assets 8,980 10,096 8,569 8,728 17,883 21,870 Total Other Assets 34,195 36,567 42,269 42,989 45,444 48,952 Total Assets $ 1,175,025 $ 1,394,621 $ 1,581,883 $ 1,885,496 $ 2,149,309 $ 2,316,374 LIABILITIES: Total Deposits $ 896,941 $ 1,138,368 $ 1,308,704 $ 1,640,120 $ 1,881,553 $ 2,043,741 FHLB Borrowings 108,500 68,500 62,000 22,000 18,000 - Fed Funds Purchased 10,001 15,001 12,000 - - - Repurchase Agreements - - - - - - Total Subordinated Debt 24,531 24,581 24,630 24,679 24,728 49,560 Total Debt $ 143,032 $ 108,082 $ 98,630 $ 46,679 $ 42,728 $ 49,560 Total Other Liabilities 6,185 6,153 12,567 12,616 16,558 15,543 Total Liabilities $ 1,046,158 $ 1,252,603 $ 1,419,901 $ 1,699,415 $ 1,940,839 $ 2,108,844 EQUITY: Common Equity $ 128,867 $ 142,018 $ 161,982 $ 186,081 $ 208,470 $ 207,530 Accumulated Other Comprehensive Income (Loss)(671)(955) 777 3,786 (400)(16,928) Total Liabilities & Equity $ 1,175,025 $ 1,394,621 $ 1,581,883 $ 1,885,496 $ 2,149,309 $ 2,316,374 For the Year Ended December 31, |