UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6‑K

REPORT OF FOREIGN PRIVATE ISSUER

Pursuant to Rule 13a-16 or 15d-16 under the

Securities Exchange Act of 1934

Securities Exchange Act of 1934

For the month of November, 2020

Commission File Number: 001-38262

LOMA NEGRA COMPAÑÍA INDUSTRIAL ARGENTINA SOCIEDAD ANÓNIMA

(Exact Name of Registrant as Specified in its Charter)

(Exact Name of Registrant as Specified in its Charter)

LOMA NEGRA CORPORATION

(Translation of Registrant’s name into English)

(Translation of Registrant’s name into English)

Cecilia Grierson 355, 4th Floor Zip Code C1107CPG – Capital Federal Republic of Argentina |

(Address of principal executive offices) |

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

Table of Contents

Item | Description |

| 1 | Loma Negra Relevant Event |

3Q20 Results Conference Call

Disclaimer and Forward-Looking Statement This presentation may contain forward-looking statements within the meaning of federal securities law that are subject to risks and uncertainties. These statements are only predictions based upon our current expectations and projections about possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” “predict,” “potential,” “seek,” “forecast,” or the negative of these terms or other similar expressions. The forward-looking statements are based on the information currently available to us. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements, including, among others things: changes in general economic, political, governmental and business conditions globally and in Argentina, changes in inflation rates, fluctuations in the exchange rate of the peso, the level of construction generally, changes in cement demand and prices, changes in raw material and energy prices, changes in business strategy and various other factors. You should not rely upon forward-looking statements as predictions of future events. Although we believe in good faith that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. Any or all of Loma Negra’s forward-looking statements in this release may turn out to be wrong. You should consider these forward-looking statements in light of other factors discussed under the heading “Risk Factors” in Company’s Annual Report on Form 20-F, as well as periodic filings made on Form 6-K, which are filed with or furnished to the United States Securities and Exchange Commission.Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this release to conform these statements to actual results or to changes in our expectations.The Company presented some figures converted from Argentine pesos to U.S. dollars for comparison purposes. The exchange rate used to convert Pesos to U.S. dollars was the reference exchange rate (Communication “A” 3500) reported by the Central Bank for U.S. dollars. The information presented in U.S. dollars is for the convenience of the reader only. Certain figures included in this report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be arithmetic aggregations of the figures presented in previous quarters.Note: Loma Negra’s financial information has been prepared in accordance with the Argentine Securities Commission (Comisión Nacional de Valores-CNV) and with International Financial Reporting Standards. Following the categorization of Argentina as a country with a three-year cumulative inflation rate greater than 100%, the country is considered highly inflationary in accordance with IFRS. Consequently, starting July 1, 2018, the Company is reporting results applying IFRS rule IAS 29. IAS 29 requires that results of operations in hyperinflationary economies are reported as if these economies were highly inflationary as of January 1, 2018, and thus year-to-date, together with comparable results, should be restated adjusting for the change in general purchasing power of the local currency, using official indices. For comparison purposes and a better understanding of our underlying performance, in addition to presenting ‘As Reported’ results, we are also disclosing selected figures as previously reported excluding rule IAS 29. Additional information in connection with the application of rule IAS 29 can be found in our earnings report.

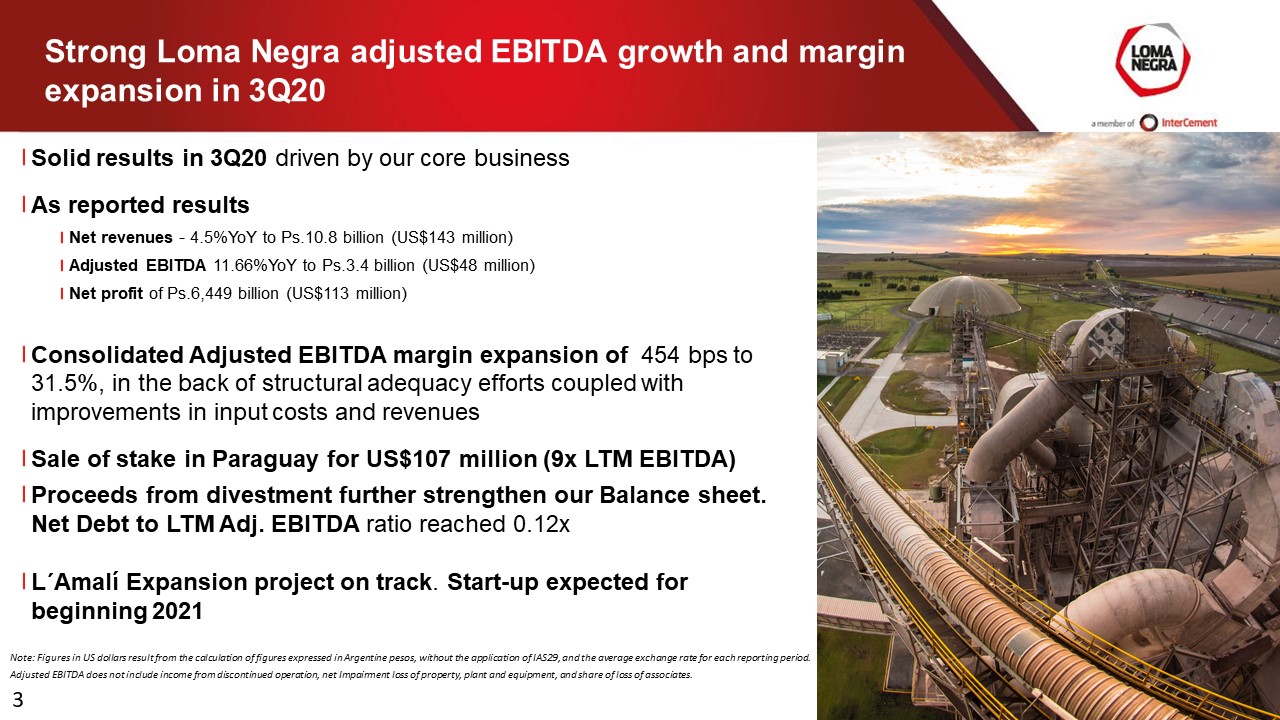

Strong Loma Negra adjusted EBITDA growth and margin expansion in 3Q20 Solid results in 3Q20 driven by our core businessAs reported resultsNet revenues - 4.5%YoY to Ps.10.8 billion (US$143 million)Adjusted EBITDA 11.66%YoY to Ps.3.4 billion (US$48 million)Net profit of Ps.6,449 billion (US$113 million)Consolidated Adjusted EBITDA margin expansion of 454 bps to 31.5%, in the back of structural adequacy efforts coupled with improvements in input costs and revenuesSale of stake in Paraguay for US$107 million (9x LTM EBITDA)Proceeds from divestment further strengthen our Balance sheet. Net Debt to LTM Adj. EBITDA ratio reached 0.12xL´Amalí Expansion project on track. Start-up expected for beginning 2021 3 Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, without the application of IAS29, and the average exchange rate for each reporting period.Adjusted EBITDA does not include income from discontinued operation, net Impairment loss of property, plant and equipment, and share of loss of associates.

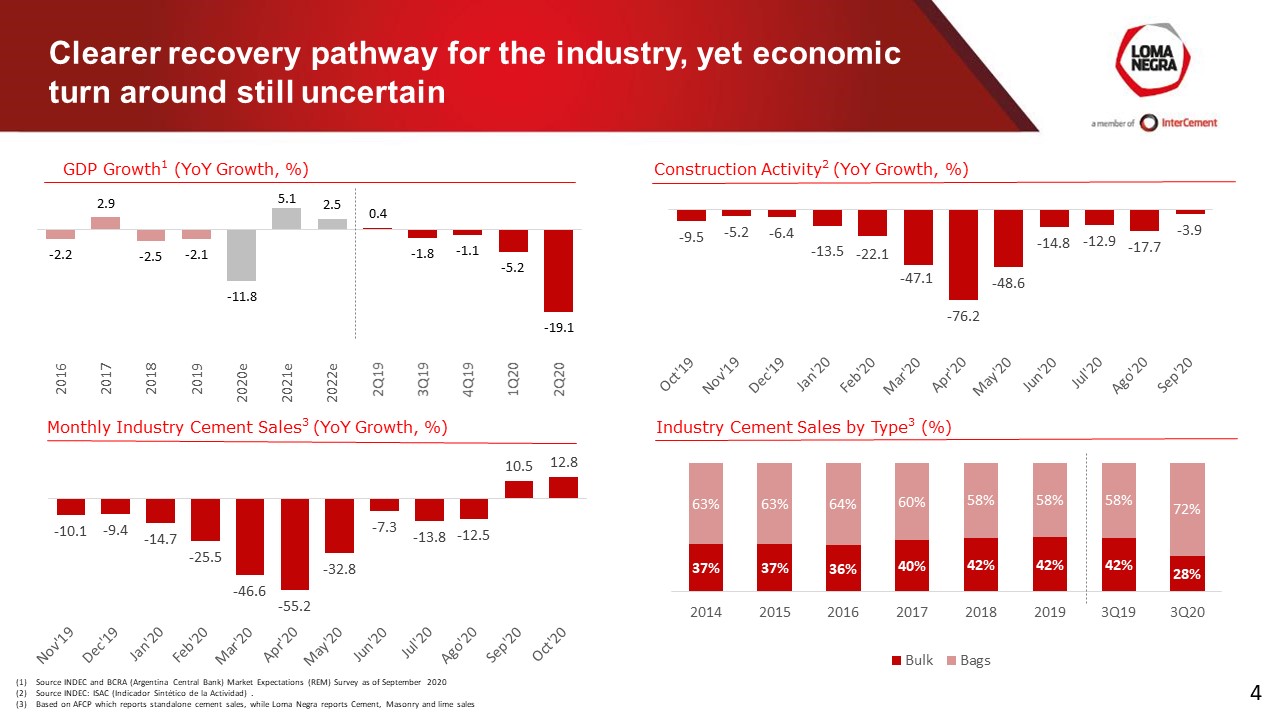

Clearer recovery pathway for the industry, yet economic turn around still uncertain Source INDEC and BCRA (Argentina Central Bank) Market Expectations (REM) Survey as of September 2020Source INDEC: ISAC (Indicador Sintético de la Actividad) . Based on AFCP which reports standalone cement sales, while Loma Negra reports Cement, Masonry and lime sales GDP Growth1 (YoY Growth, %) Construction Activity2 (YoY Growth, %) Monthly Industry Cement Sales3 (YoY Growth, %) Industry Cement Sales by Type3 (%) 4

Cement revenues up 5.3%, while consolidated revenues drop 4.5% impacted by other segments Revenue Performance:Cement, masonry & lime: up 5.3% YoY. Volumes growth of 2.9%, explained by robust rebound in Bag, couple with favorable pricing Concrete: dropped by 75.5% YoY with Volumes down 70.2%. Large private or public infrastructure works virtually non-existent Railroad: down 29.8% YoY. Softer volumes of Frac-sand and building materials further impacted by weaker pricesAggregates: dropped by 24.4% YoY. Volumes down 25.2%, severely impacted by a standstill in public and private larger works Sales Volumes 3Q20 3Q19 % Chg. Cement, masonry & lime MM Tn 1.53 1.49 2.9% Concrete MM m3 0.06 0.19 -70.2% Railroad MM Tn 1.06 1.13 -5.8% Aggregates MM Tn 0.19 0.26 -25.2% Revenues (AR$ million) 3Q20 3Q19 % Chg. 10,054 9,546 5.3% 348 1,419 -75.5% 790 1,125 -29.8% 131 173 -24.4% Total Net Revenues1 10,054 11,260 -4.5% 5 Sales volumes include inter-segment sales and Other segments

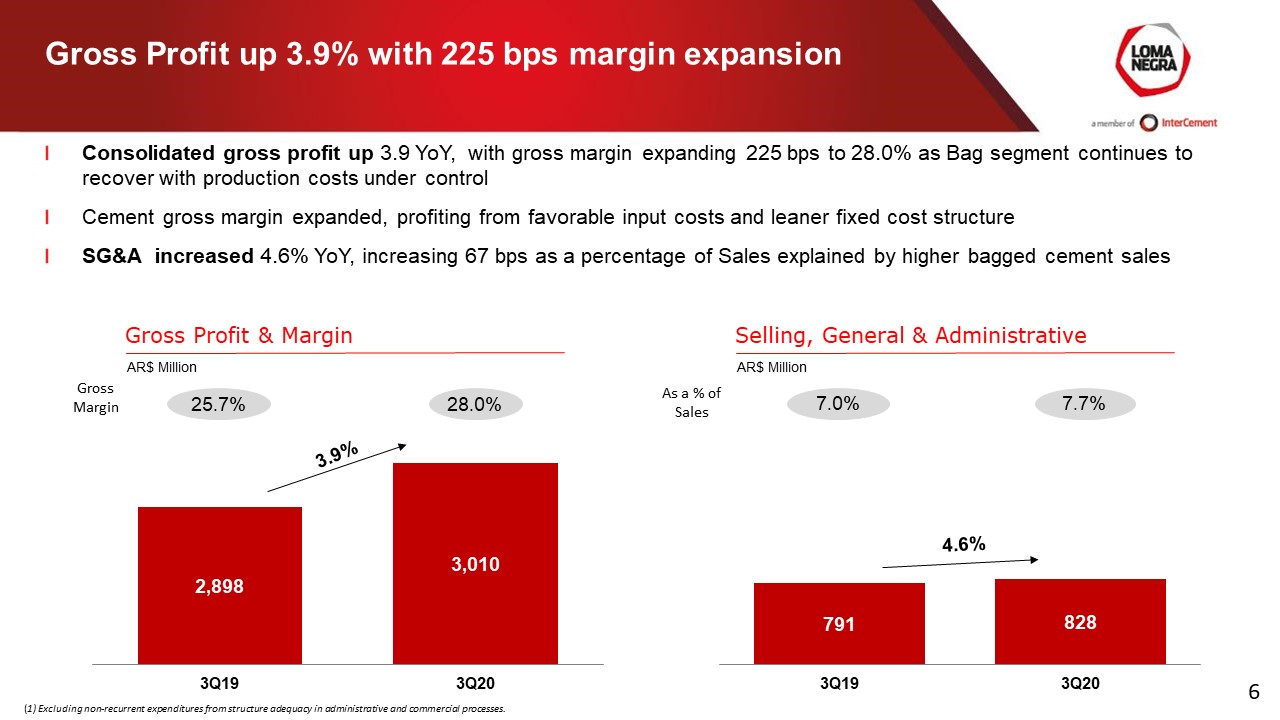

Gross Profit up 3.9% with 225 bps margin expansion Gross Profit & Margin AR$ Million Consolidated gross profit up 3.9 YoY, with gross margin expanding 225 bps to 28.0% as Bag segment continues to recover with production costs under controlCement gross margin expanded, profiting from favorable input costs and leaner fixed cost structureSG&A increased 4.6% YoY, increasing 67 bps as a percentage of Sales explained by higher bagged cement sales Selling, General & Administrative AR$ Million As a % of Sales 7.0% 4.6% Gross Margin 28.0% 25.7% 3.9% 6 7.7% (1) Excluding non-recurrent expenditures from structure adequacy in administrative and commercial processes.

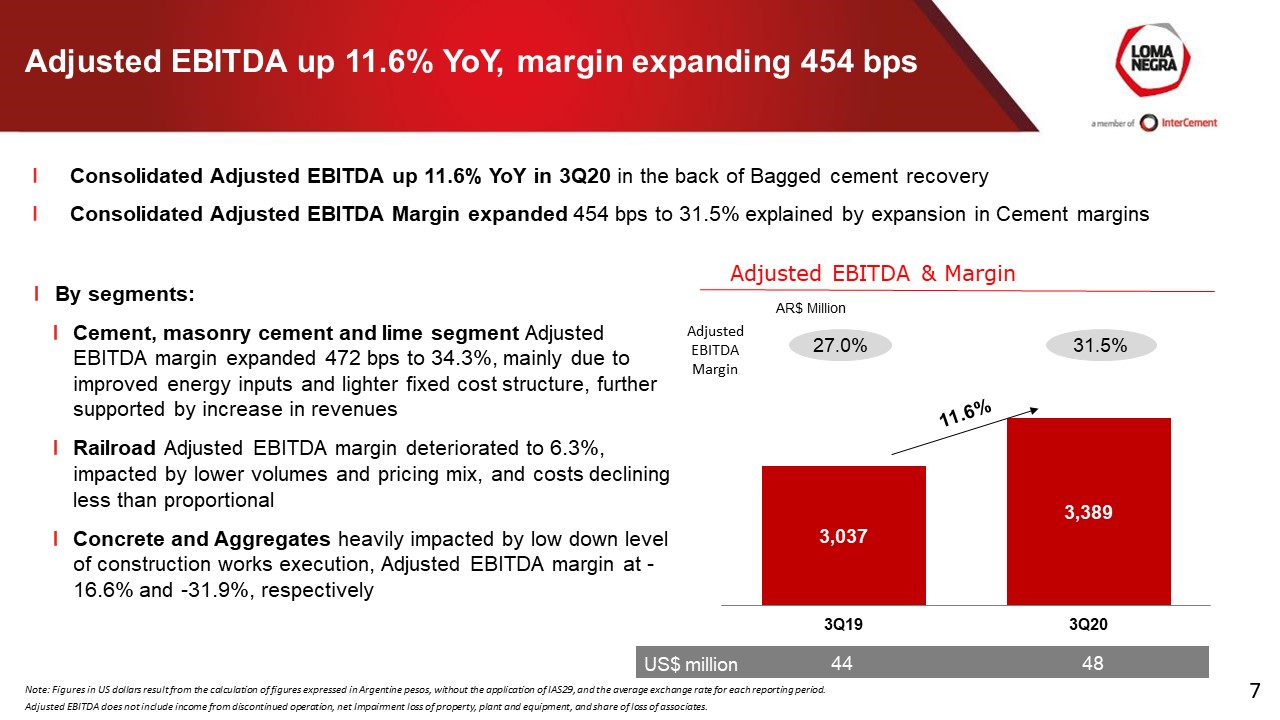

Adjusted EBITDA up 11.6% YoY, margin expanding 454 bps Adjusted EBITDA & Margin AR$ Million By segments:Cement, masonry cement and lime segment Adjusted EBITDA margin expanded 472 bps to 34.3%, mainly due to improved energy inputs and lighter fixed cost structure, further supported by increase in revenuesRailroad Adjusted EBITDA margin deteriorated to 6.3%, impacted by lower volumes and pricing mix, and costs declining less than proportionalConcrete and Aggregates heavily impacted by low down level of construction works execution, Adjusted EBITDA margin at -16.6% and -31.9%, respectively 44 48 US$ million 31.5% 27.0% Adjusted EBITDA Margin 7 Consolidated Adjusted EBITDA up 11.6% YoY in 3Q20 in the back of Bagged cement recoveryConsolidated Adjusted EBITDA Margin expanded 454 bps to 31.5% explained by expansion in Cement margins 11.6% Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, without the application of IAS29, and the average exchange rate for each reporting period.Adjusted EBITDA does not include income from discontinued operation, net Impairment loss of property, plant and equipment, and share of loss of associates.

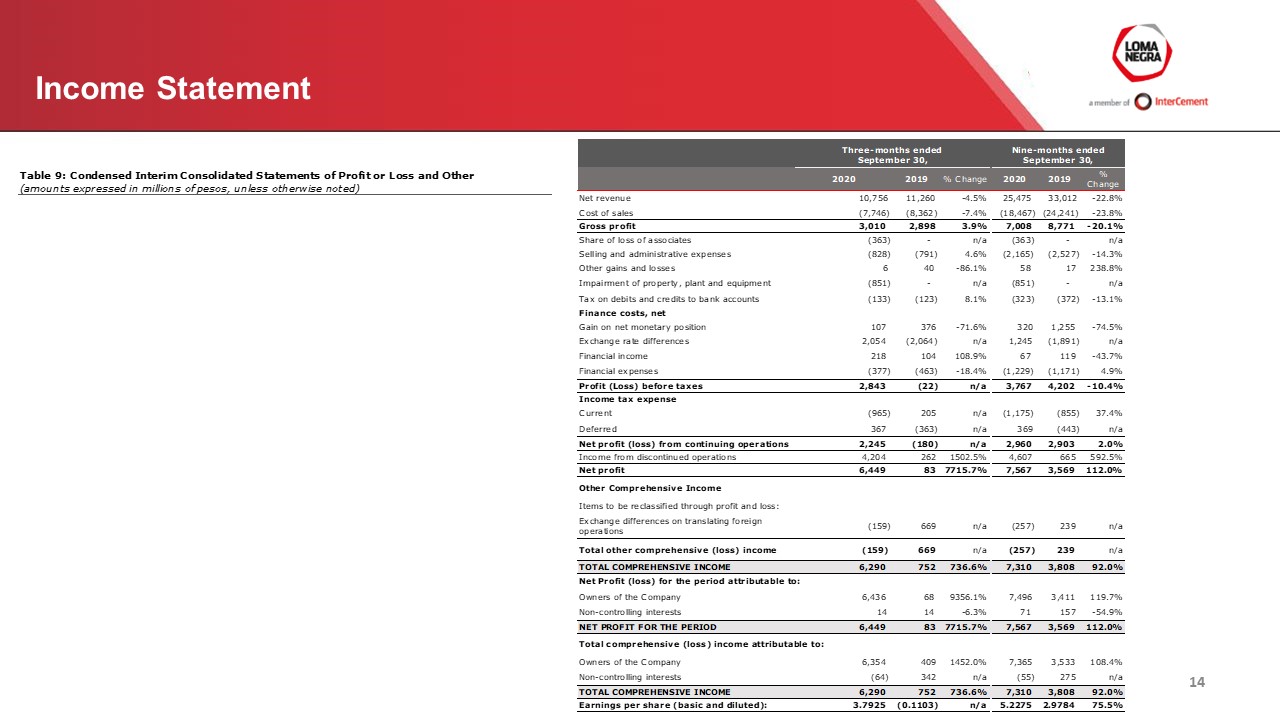

Net profit boosted by sale of Paraguay operations Net Profit AR$ Million 113 US$ million Net Profit breakdown:Adjusted EBITDA increased 11.6% YoYTotal finance gain net of Ps.2,001 million in 3Q20 compared to a loss of Ps.2,046 million in 3Q19Foreign exchange gain of Ps.2,054 million in 3Q20, compared to Ps.2,064 million loss in 3Q19Net Financial expense, declined by Ps.199 million due to lower total Financial Debt Gain on net monetary position was Ps.270 million lower in 3Q20 compared to 3Q19Net impairment loss on Railway and Aggregate property, plant and equipment and share of loss of Railway for Ps.1,213 millionNet Profit from continuing operations resulted in Ps. 2,245 millionIncome from discontinued operations in Paraguay was Ps. 4,204 millionNet Profit of Ps.6,449 million compared to Ps.83 million in 3Q19 Finance Costs, net AR$ Million 8 (9) 6,367 83 6,449 Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, without the application of IAS29, and the average exchange rate for each reporting period.Adjusted EBITDA does not include income from discontinued operation, net Impairment loss of property, plant and equipment, and share of loss of associates.

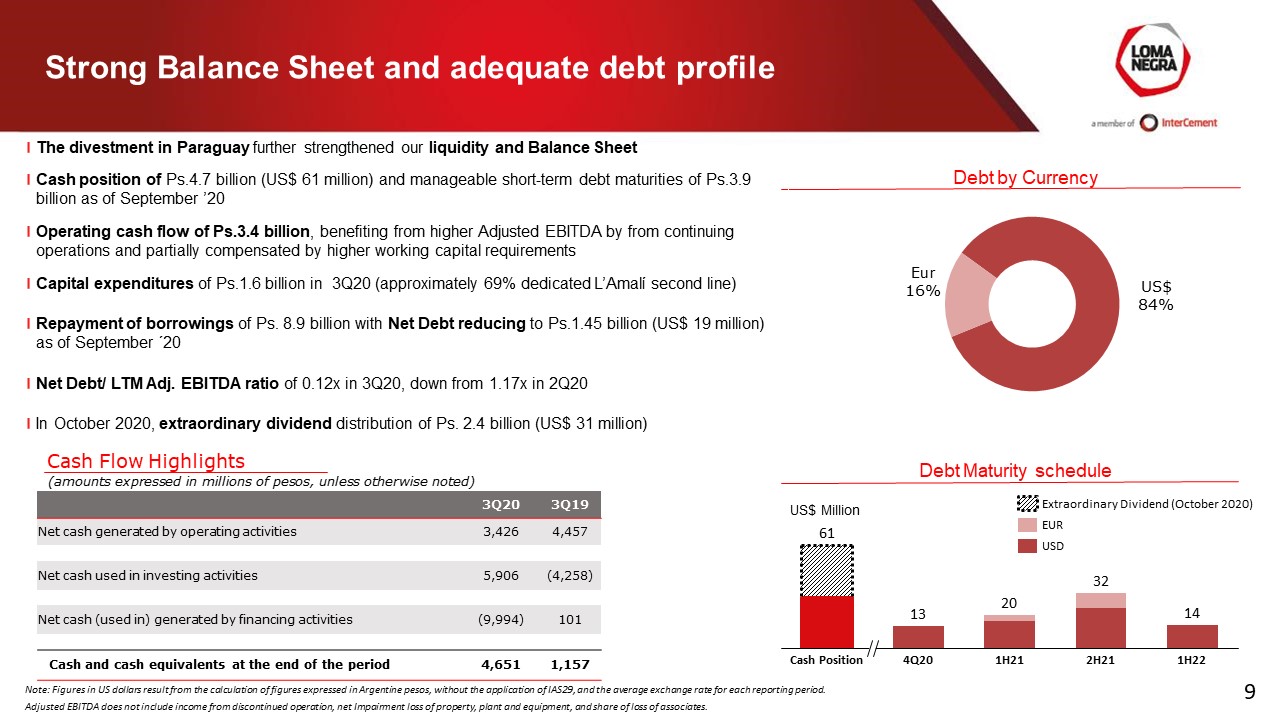

Strong Balance Sheet and adequate debt profile Debt by Currency Debt Maturity schedule The divestment in Paraguay further strengthened our liquidity and Balance Sheet Cash position of Ps.4.7 billion (US$ 61 million) and manageable short-term debt maturities of Ps.3.9 billion as of September ’20Operating cash flow of Ps.3.4 billion, benefiting from higher Adjusted EBITDA by from continuing operations and partially compensated by higher working capital requirementsCapital expenditures of Ps.1.6 billion in 3Q20 (approximately 69% dedicated L’Amalí second line)Repayment of borrowings of Ps. 8.9 billion with Net Debt reducing to Ps.1.45 billion (US$ 19 million) as of September ´20Net Debt/ LTM Adj. EBITDA ratio of 0.12x in 3Q20, down from 1.17x in 2Q20 In October 2020, extraordinary dividend distribution of Ps. 2.4 billion (US$ 31 million) 3Q20 3Q19 Net cash generated by operating activities 3,426 4,457 Net cash used in investing activities 5,906 (4,258) Net cash (used in) generated by financing activities (9,994) 101 Cash and cash equivalents at the end of the period 4,651 1,157 9 Cash Flow Highlights US$ Million Cash Position 2H21 4Q20 1H21 1H22 13 61 20 32 14 Extraordinary Dividend (October 2020) EUR USD Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, without the application of IAS29, and the average exchange rate for each reporting period.Adjusted EBITDA does not include income from discontinued operation, net Impairment loss of property, plant and equipment, and share of loss of associates.

Looking forward Resiliency under challenging times, deliver of margin and EBITDA growth in our core business, supported by our strong commercial and operational performanceClearer recovery pathway for the industry driven almost exclusively by household and retail demand, with monthly record high volumes for bagged cement. Although more economic sectors in the country are reopening for business, full economic turn around still uncertain Seamlessly executed the sale of our Paraguayan operation generating excellent shareholder returnL´Amalí project on track. Key strategic piece expected to inaugurate at the beginning of 2021 10

Questions & Answers

Exhibit: Summary Financial Statements

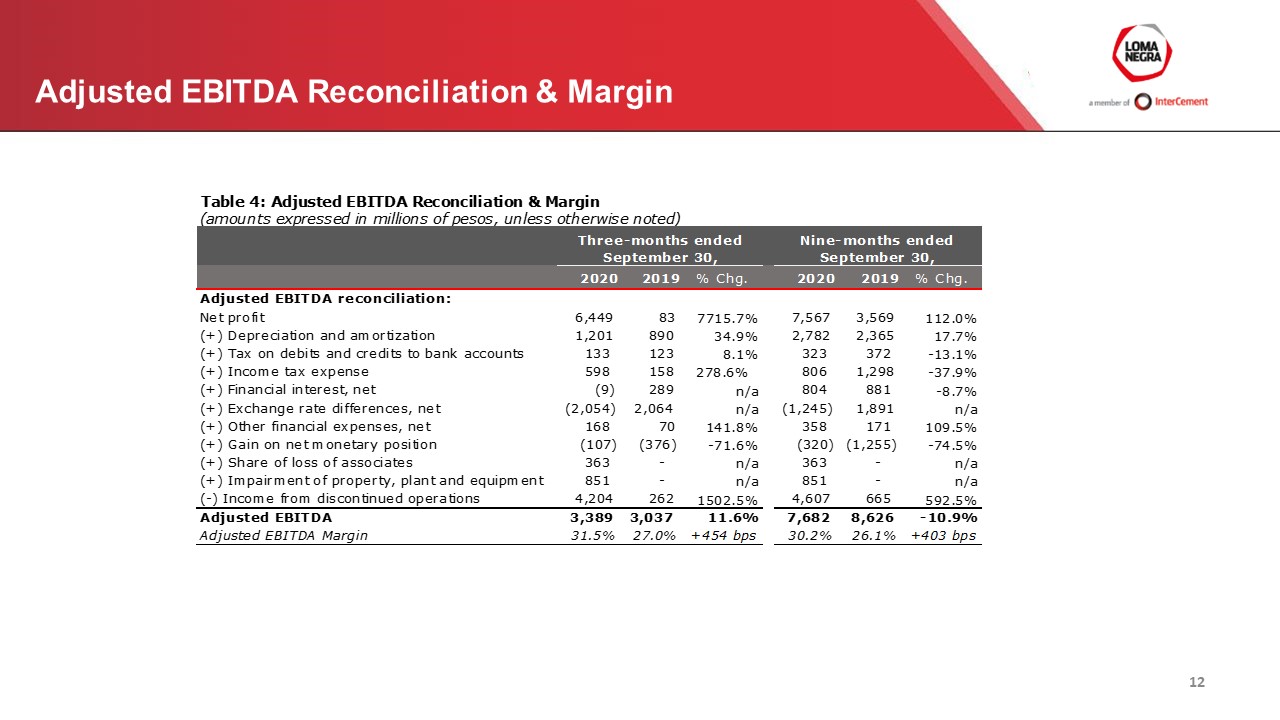

Adjusted EBITDA Reconciliation & Margin 13

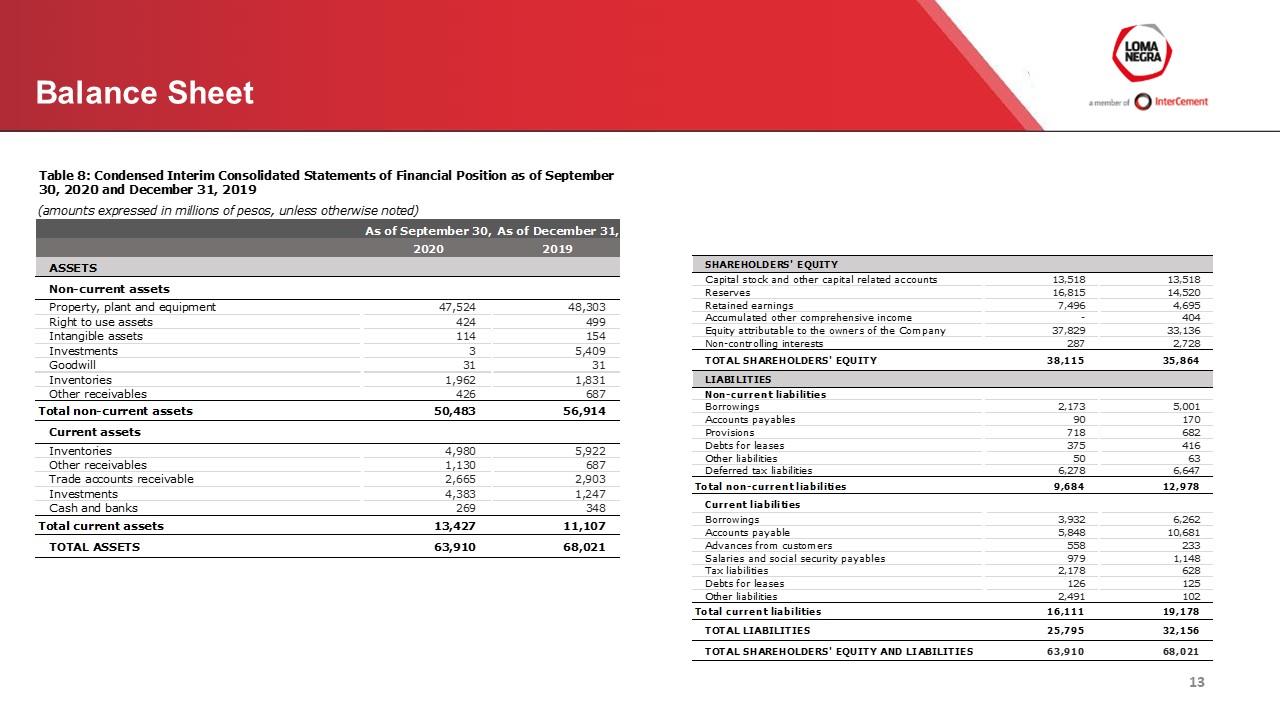

Balance Sheet 14

Income Statement 15

Statement of Cash Flows 16

IR Contact Marcos I. GradinChief Financial Officer and Investor RelationsGaston PinnelInvestor Relations Manager+54-11-4319-3050investorrelations@lomanegra.com

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Loma Negra Compañía Industrial Argentina Sociedad Anónima

Date: November 12, 2020 | By: | /s/ Marcos I. Gradin | |

| Name: | Marcos I. Gradin | ||

| Title: | Chief Financial Officer | ||