UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

FORM 6‑K

_______________

_______________

REPORT OF FOREIGN PRIVATE ISSUER

Pursuant to Rule 13a-16 or 15d-16 under the

Securities Exchange Act of 1934

Securities Exchange Act of 1934

For the month of March, 2022

Commission File Number: 001-38262

_______________

LOMA NEGRA COMPAÑÍA INDUSTRIAL ARGENTINA SOCIEDAD ANÓNIMA

(Exact Name of Registrant as Specified in its Charter)

(Exact Name of Registrant as Specified in its Charter)

LOMA NEGRA CORPORATION

(Translation of Registrant’s name into English)

(Translation of Registrant’s name into English)

_______________

Cecilia Grierson 355, 4th Floor Zip Code C1107CPG – Capital Federal Republic of Argentina |

(Address of principal executive offices) |

_______________

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

Table of Contents

Item | Description | |

| 1 | Relevant event |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Loma Negra Compañía Industrial Argentina Sociedad Anónima | |||||

Date: March 10, 2022 | By: | /s/ | Marcos I. Gradin | ||

Name: | Marcos I. Gradin | ||||

Title: | Chief Financial Officer | ||||

4Q21-ResultsConference Call

Disclaimer and Forward-Looking Statement This presentation may contain forward-looking statements within the meaning of federal securities law that are subject to risks and uncertainties. These statements are only predictions based upon our current expectations and projections about possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” “predict,” “potential,” “seek,” “forecast,” or the negative of these terms or other similar expressions. The forward-looking statements are based on the information currently available to us. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements, including, among others things: changes in general economic, political, governmental and business conditions globally and in Argentina, changes in inflation rates, fluctuations in the exchange rate of the peso, the level of construction generally, changes in cement demand and prices, changes in raw material and energy prices, changes in business strategy and various other factors. You should not rely upon forward-looking statements as predictions of future events. Although we believe in good faith that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. Any or all of Loma Negra’s forward-looking statements in this release may turn out to be wrong. You should consider these forward-looking statements in light of other factors discussed under the heading “Risk Factors” in Company’s Annual Report on Form 20-F, as well as periodic filings made on Form 6-K, which are filed with or furnished to the United States Securities and Exchange Commission.Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this release to conform these statements to actual results or to changes in our expectations.The Company presented some figures converted from Argentine pesos to U.S. dollars for comparison purposes. The exchange rate used to convert Pesos to U.S. dollars was the reference exchange rate (Communication “A” 3500) reported by the Central Bank for U.S. dollars. The information presented in U.S. dollars is for the convenience of the reader only. Certain figures included in this report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be arithmetic aggregations of the figures presented in previous quarters.Note: Loma Negra’s financial information has been prepared in accordance with the Argentine Securities Commission (Comisión Nacional de Valores-CNV) and with International Financial Reporting Standards. Following the categorization of Argentina as a country with a three-year cumulative inflation rate greater than 100%, the country is considered highly inflationary in accordance with IFRS. Consequently, starting July 1, 2018, the Company is reporting results applying IFRS rule IAS 29. IAS 29 requires that results of operations in hyperinflationary economies are reported as if these economies were highly inflationary as of January 1, 2018, and thus year-to-date, together with comparable results, should be restated adjusting for the change in general purchasing power of the local currency, using official indices. For comparison purposes and a better understanding of our underlying performance, in addition to presenting ‘As Reported’ results, we are also disclosing selected figures as previously reported excluding rule IAS 29. Additional information in connection with the application of rule IAS 29 can be found in our earnings report. 1

Cement business continues to deliver world class margin with demand almost reaching all time highsAs reported resultsNet revenues -3.8% to Ps. 19.3 billion (US$ 187 million; +16.6%)Adjusted EBITDA -10.0% to Ps. 6.4 billion (US$ 63 million; +9.1%)Net Profit of Ps. 2.8 billionConsolidated Adjusted EBITDA margin reached 33.3%, contracting 231 bps YoY and expanding 693 bps from 3Q21FY21 EBITDA of US$ 215 million and margin of 31.4%Solid balance sheet with Net Debt to LTM Adj. EBITDA ratio of -0.12xL’Amalí´s second line in full production Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, as previously reported (without the application of IAS29) and the average exchange rate for each reporting period. LOMA continues to deliver strong results 2

Macro & Industry contextRevenues and Volumes 3

GDP Growth1 (YoY Growth, %) Construction Activity2 & Monthly Industry Cement Sales3 (YoY Growth, %) Monthly Industry Cement Sales3 (‘000 tons) Industry Cement Sales by Type3 (%) Apr Feb Jan Mar May Jul Nov Jun Aug Dec Sep Oct 2018 2021 2019 2020 Source INDEC and BCRA (Argentina Central Bank) Market Expectations (REM)Source INDEC: Construction activity indicator, ISAC (Indicador Sintético de la Actividad) . Based on AFCP which reports standalone cement sales, while Loma Negra reports Cement, Masonry and lime salesEne’ 22 : As of the date of this presentation, ISAC figures were not released Cement demand almost reached all time highs in 2021 4 Ene’22 Dic’21 Abr’21 Feb’21 Dec’20 Mar’21 Jan’21 May’21 Jun’21 Jul’21 Ago’21 Sep’21 Oct’21 Nov’21 322 135 Feb’22 ISAC Cement Industry 4 2022

Revenue Performance:Cement, masonry & lime: decreased 4.8% YoY, with volumes expanding 3.5% with a softer pricing dynamicConcrete: down by 0.4% YoY. Volumes down due to the impact of an extraordinary infrastructure work in 4Q20, compensated with solid pricing performanceRailroad: increased by 8.1% YoY. Volumes decrease by 3.2% compensated by an increase in pricing and sales mixAggregates: surged by 51.9% YoY. Volume increase of 14.0% coupled with a recovery in pricing and a positive pricing mix Sales Volumes (1) Revenues (AR$ million) (2) Total Net Revenues 19,257 20,019 -3.8% Sales volumes include inter-segment salesSales revenues include inter-segment sales and Other segments 4Q21 4Q20 % Chg. Cement, masonry & lime MM Tn 1.68 1.62 3.5% Concrete MM m3 0.13 0.15 -14.5% Railroad MM Tn 1.13 1.17 -3.0% Aggregates MM Tn 0.25 0.22 14.0% 4Q21 4Q20 % Chg. 17,452 18,328 -4.8% 1,360 1,365 -0.4% 1,560 1,442 8.1% 369 243 51.9% Revenue down 3.8% in 4Q21Sound expansion across all segments for the full year 5 2021 2020 % Chg. 65,925 57,356 14.9% 5,325 3,072 73.3% 5,980 5,427 10.2% 1,108 606 82.8% 73,668 62,827 17.3% 2021 2020 % Chg. 6.13 5.16 18.7% 0.52 0.30 73.4% 4.33 3.79 14.1% 0.84 0.57 47.1%

Business Performance 6

Consolidated gross profit declined 7.9% YoY, with gross margin contracting 152 bps to 34.6% mainly impacted by lower top line performance for the 4Q21. Sound recovery of 22.5% for the FY21.Compression in cement margin partially offset by an improvement in Concrete and Aggregates. SG&A increased by 20.9% YoY mainly due to a recognition of an allowance for doubtful receivables in the Railroad segment , reaching 9.9% as % of sales. Tighter margins on 4Q21 and expansion for FY21 7 Gross Profit & Margin AR$ Million Gross Margin 34.6% 36.2% -7.9% 30.3% 31.6% +22.5% Selling, General & Administrative AR$ Million As a % of Sales 8.3% 7.9% 8.6% 9.9% +21.4% +20.9%

Adjusted EBITDA & Margin AR$ Million Consolidated Adjusted EBITDA Margin reached 33.3%, down 231 bps YoY, expanding 693 bps from 3Q21By segmentsCement, masonry cement and lime segment Adjusted EBITDA margin stood at 37.4%, contracting 306 bps YoY primarily due to lower top line performanceConcrete Adjusted EBITDA margin recovered to 6.1% from -19.2% in 4Q20Railroad Adjusted EBITDA margin decreased to negative 12.9% due to the impact produced by a recognition of an allowance for doubtful receivablesAggregates Adjusted EBITDA margin recovered but remains negative 1,2% from -9.9% in 4Q20 58 US$ million 35.6% Adjusted EBITDA Margin Consolidated Adjusted EBITDA of US$63 million in the 4Q21, down 10% when measured in Ps. For FY21, EBITDA stood at US$215 million, up 15.4% when measured in Ps. 63 -10.0% 31.4% Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, as previously reported (without the application of IAS29) and the average exchange rate for each reporting period. Record performance for the FY 2021 8 15.4% 171 215 33.3% 31.9%

Bottom line Financial performance 9

Net Profit Attributable to Owners AR$ Million US$ million Net Profit breakdown:Adjusted EBITDA decreased by 10.0% YoYTotal finance cost of Ps.143 million in 4Q21 compared to a net gain of Ps.935 million in 4Q20Foreign exchange gain of Ps. 195 million in 4Q21, compared to Ps. 407 million gain in 4Q20Gain on net monetary position was Ps.80 million in 4Q21 compared to Ps.729 million on 4Q20Net Financial expense, increased by Ps. 217 million to Ps. 418 million compared to Ps. 201 million YoY due to lower FX depreciation effect compared with the evolution of the inflation rate Net Profit Attributable to Owners of the Company in 4Q21 was Ps. 2.9 billion, down from Ps. 4.5 billion in 4Q20. The full year comparison is affected by the divestment in Paraguay in FY2020 and an increase in the income tax rate that impacted in FY2021 Finance Costs, net AR$ Million 49 2 Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, as previously reported (without the application of IAS29) and the average exchange rate for each reporting period. Net Profit down 37% affected by lower operating performance and higher financial cost 10

Debt by Currency Debt Maturity schedule Cash position and Investments of Ps. 5.3 billion and total debt at Ps. 2.5 billion as of end of 4Q21Net Cash position of Ps. 2.8 billion (US$ 27 mm) at Dic’21 with Debt reduction of US$16 million in the quarterNet Debt/ LTM Adj. EBITDA ratio of -0.12x in FY21 compared with 0.16x in FY20In 4Q21, Operating cash generation was Ps. 5.2 billions with lower profitability partially offset by positive working capital effect. For FY2021, cash generation from operating activities was Ps. 15.0 billions boosted by a higher profitability affected by the increase in the income tax rate Capital expenditures of Ps.2.2 billion in 4Q21 and Ps.6.9 billion for FY 2021 (L’Amalí expansion represented 27% and 45% accordingly)Share Repurchased in 4Q21 amounted Ps. 0.7 billion and Ps. 2.4 billion for FY2021 amounts expressed in millions of pesos 4Q21 4Q20 FY21 FY20 Net cash generated by operating activities 5,228 6,044 15,050 17,189 Net cash used in investing activities (2,265) (2,624) (8,845) (2,158) Net cash (used in) generated by financing activities (2,490) (4,801) (8,760) (15,854) Cash and cash equivalents at the end of the period 3,306 6,605 3,306 6,605 Note: Figures in US dollars result from the calculation of figures expressed in Argentine pesos, as previously reported (without the application of IAS29) and the average exchange rate for each reporting period. US$ Million Cash Position 3Q 2022 1Q 2022 2Q 2022 17 2023 4Q 2022 Ps. USD Robust balance sheet with positive cash position US$24 MM 11 Cash Flow Highlights

2021 Outlook 12

2021 cement demand almost reached record highsFor 2022 we expect growth to continue, following a similar trend of recent monthsAmid the outcome of political and macroeconomic challenges, we remain focused on delivering strong resultsL´Amalí´s new line in full production, meeting all expectationsWe release our first Sustainability Report sharing the progress made in this area and our commitment with the environment, the communities where we operate and other stakeholders Looking into 2022 13 Inauguration of L’Amali’s second line New Sustainability Report L’Amalí´s two lines

Financial Tables 14

Adjusted EBITDA Reconciliation & Margin

Balance Sheet

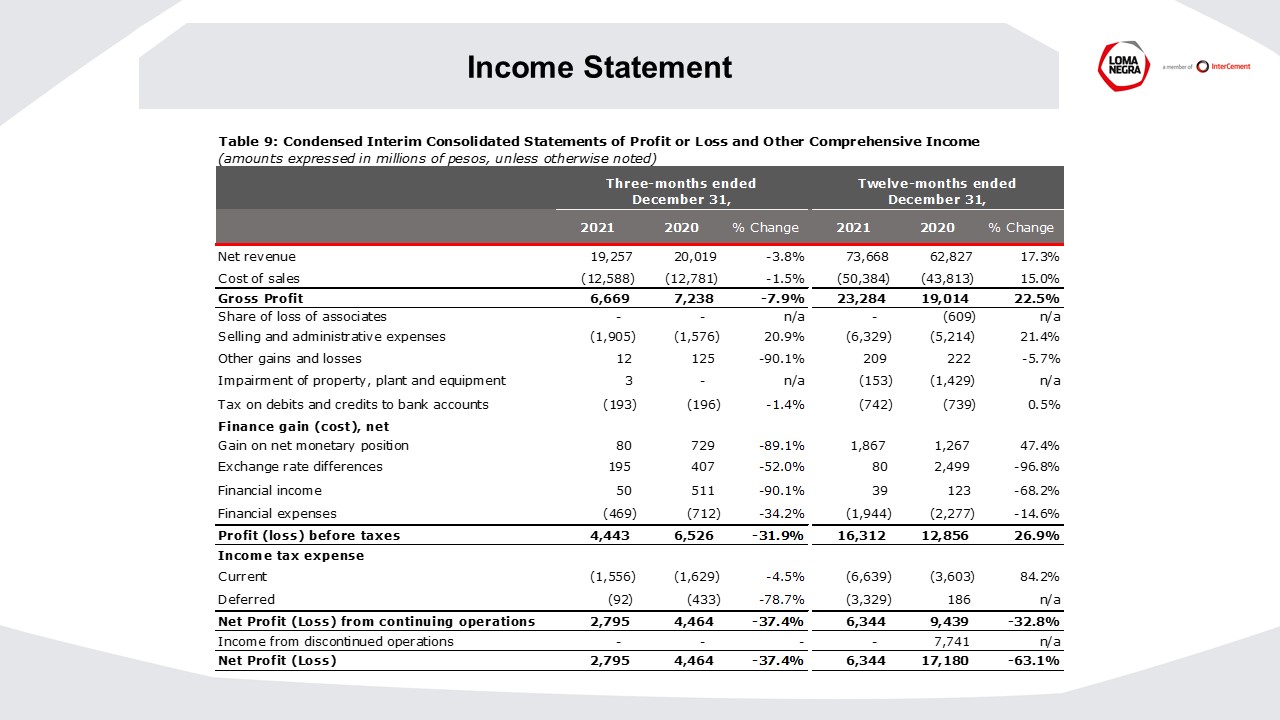

Income Statement

Statement of Cash Flows

Thank you! IR ContactMarcos I. GradinChief Financial Officer and Investor RelationsDiego M. JalónHead of Investor Relations+54 (11 ) 4319-3050investorrelations@lomanegra.com