Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☒ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☐ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☐ | Soliciting Material Pursuant to§240.14a-12 | |

Starwood Real Estate Income Trust, Inc.

(Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box)

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

Table of Contents

Starwood Real Estate Income Trust, Inc.

1601 Washington Avenue, Suite 800

Miami Beach, Florida 33139

June 17, 2019

Dear Stockholders:

You are cordially invited to attend the 2019 Annual Meeting of Stockholders (the “Annual Meeting”) of Starwood Real Estate Income Trust, Inc., a Maryland corporation (the “Company”), which will be held at 9:30 a.m., Eastern Daylight Time, on Wednesday, July 31, 2019, at the 1 Hotel Brooklyn Bridge, 60 Furman Street, Brooklyn, New York 11201. At the Annual Meeting, stockholders will be asked to consider and vote upon:

| • | the election of nine director nominees listed in this Proxy Statement; |

| • | the ratification of the appointment of Deloitte & Touche LLP as our independent registered public accounting firm for the year ending December 31, 2019; |

| • | four separate proposals to make amendments to our Articles of Amendment and Restatement (the “charter”); |

| • | a proposal to permit our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved; and |

| • | such other business as may properly come before the Annual Meeting and any adjournments or postponements thereof. |

Details concerning those matters to come before stockholders at the Annual Meeting are described in this Proxy Statement.

Management and the Board of Directors unanimously recommend that you voteFOR all nominees for directors listed in the Proxy Statement,FOR the appointment of Deloitte & Touche LLP as our independent registered public accounting firm for 2019,FOR each of the four proposed charter amendments, andFOR the proposal to permit our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved.

It is important that your shares be represented at the Annual Meeting and voted in accordance with your wishes. Whether or not you plan to attend the meeting, we urge you to complete a proxy as promptly as possible — by Internet, telephone or mail — so that your shares will be voted at the Annual Meeting. This will not limit your right to vote in person or to attend the meeting.

IMPORTANT NOTICE REGARDING AVAILABILITY OF PROXY MATERIALS FOR THE

Our Proxy Statement, form of proxy card and 2018 Annual Report to stockholders are also available at

|

On behalf of the Board of Directors and management, I thank you for your continuing support.

| Sincerely, |

/s/ Barry Sternlicht |

| Barry Sternlicht, Chairman of the Board |

Table of Contents

Starwood Real Estate Income Trust, Inc.

1601 Washington Avenue, Suite 800

Miami Beach, Florida 33139

NOTICE OF 2019 ANNUAL MEETING OF STOCKHOLDERS AND PROXY STATEMENT

To our Stockholders:

We hereby notify you that Starwood Real Estate Income Trust, Inc., a Maryland corporation (the “Company”), is holding its 2019 Annual Meeting of Stockholders (the “Annual Meeting”) at 9:30 a.m., Eastern Daylight Time, on Wednesday, July 31, 2019, at the 1 Hotel Brooklyn Bridge, 60 Furman Street, Brooklyn, New York 11201. At the Annual Meeting, stockholders will be asked to consider and vote upon:

| 1. | the election of nine director nominees listed in the Proxy Statement; |

| 2. | the ratification of the appointment of Deloitte & Touche LLP as our independent registered public accounting firm for the year ending December 31, 2019; |

| 3. | four separate proposals to make amendments to our Articles of Amendment and Restatement; |

| 4. | a proposal to permit our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved; and |

| 5. | such other business as may properly come before the Annual Meeting and any adjournments or postponements thereof. |

You can vote your shares of common stock at the Annual Meeting and any adjournments or postponements thereof if the Company’s records show that you were a stockholder of record as of the close of business on May 31, 2019, the record date for the Annual Meeting.

Stockholders, whether or not they expect to be present at the Annual Meeting, are requested to authorize a proxy to vote their shares electronically via the Internet, by telephone or by completing and returning the proxy card. Voting instructions are printed on your proxy card and included in the accompanying Proxy Statement. Any person giving a proxy has the power to revoke it at any time prior to the meeting and stockholders who are present at the meeting may withdraw their proxies and vote in person.

| Sincerely, |

/s/ Matthew Guttin |

| Matthew Guttin |

| Chief Compliance Officer and Secretary |

June 17, 2019

Table of Contents

i

Table of Contents

Table of Contents

Starwood Real Estate Income Trust, Inc.

1601 Washington Avenue, Suite 800

Miami Beach, Florida 33139

PROXY STATEMENT FOR

2019 ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON JULY 31, 2019

This Proxy Statement is being furnished by and on behalf of the Board of Directors of Starwood Real Estate Income Trust, Inc., a Maryland corporation, in connection with the solicitation of proxies to be voted at the Annual Meeting. This Proxy Statement and the enclosed proxy card will be first mailed on or about June 17, 2019 to stockholders of record as of the close of business on May 31, 2019. Our 2018 Annual Report on Form10-K was previously mailed to stockholders. The words “Starwood Real Estate Income Trust,” “we,” “our,” “us,” and “our company” refer to Starwood Real Estate Income Trust, Inc., together with its consolidated subsidiaries, including Starwood REIT Operating Partnership L.P. (the “Operating Partnership”), a Delaware limited partnership of which we are the general partner, unless the context requires otherwise. The term “Advisor” refers to Starwood REIT Advisors, L.L.C., our advisor. The Advisor is part of Starwood Capital Group (together with its affiliates, “Starwood Capital”), a private real estate investment firm. Starwood Capital Group Holdings, L.P. serves as our sponsor.

GENERAL INFORMATION ABOUT THE ANNUAL MEETING AND VOTING

In this section of the Proxy Statement, we answer some common questions regarding our 2019 Annual Meeting and the voting of shares at the meeting.

Where and when will the Annual Meeting be held?

The Annual Meeting will be held at the 1 Hotel Brooklyn Bridge, 60 Furman Street, Brooklyn, New York 11201 at 9:30 a.m., Eastern Daylight Time, on Wednesday, July 31, 2019.

What is this document and why have I received it?

This Proxy Statement and the enclosed proxy card are being furnished to you, as a stockholder of Starwood Real Estate Income Trust, because our Board of Directors is soliciting your proxy to vote at the Annual Meeting. This Proxy Statement contains information that stockholders should consider before voting on the proposals to be presented at the meeting.

We intend to mail this Proxy Statement and accompanying proxy card on or about June 17, 2019 to all stockholders of record entitled to vote at the meeting.

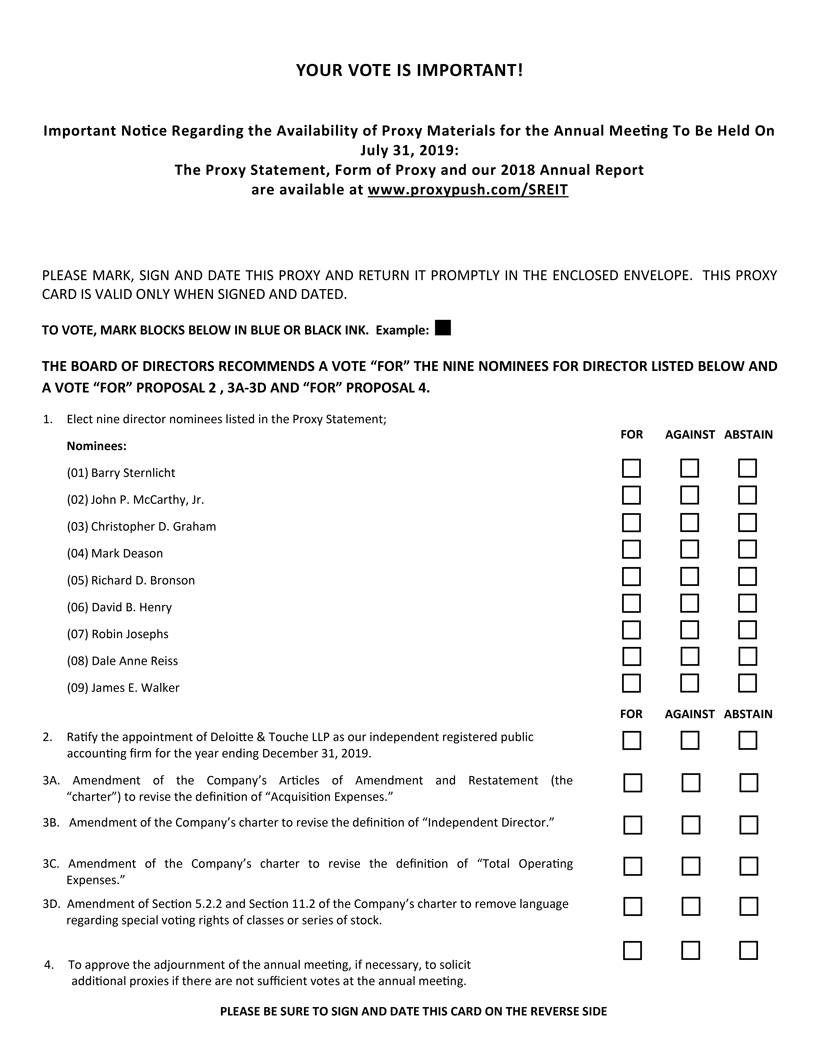

There are eleven proposals scheduled to be considered and voted on at the Annual Meeting:

| • | Proposal 1:Election of nine director nominees listed herein; |

| • | Proposal 2:Ratification of the appointment of Deloitte & Touche LLP, as our independent registered public accounting firm for the year ending December 31, 2019; |

1

Table of Contents

| • | Proposals 3A-3D:Amendments to our charter; and |

| • | Proposal 4:Permission for our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved. |

What is the required vote for approval of each proposal?

Proposal 1: Election of nine director nominees listed herein.The affirmative vote of a majority of the shares entitled to vote that are present in person or by proxy at the Annual Meeting is required for the election of each nominee for director. Abstentions and brokernon-votes will have the effect of a vote against the nominees.

Proposal 2: Ratification of the appointment of Deloitte &Touche LLP (“Deloitte”) as our independent registered public accounting firm the year ending December 31, 2019.A majority of the votes cast at the Annual Meeting in person or by proxy is required to approve the auditor ratification proposal. Abstentions, if any, will not affect the outcome of this proposal. Your shares may be voted on for this proposal if they are held in the name of a brokerage firm even if you do not provide the brokerage firm with voting instructions.

Proposals 3A-3D: Amendments to our charter.The affirmative vote of a majority of all votes entitled to be cast on each charter amendment proposal is required to approve each charter amendment proposal. Abstentions and brokernon-votes will have the effect of a vote against each charter amendment proposal.

Proposal 4: Permitting our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved.A majority of the votes cast at the Annual Meeting in person or by proxy is required to approve the adjournment proposal. Abstentions and brokernon-votes will not affect the outcome of this proposal.

There is no cumulative voting for these proposals, and appraisal rights are not applicable to the matters being voted upon.

How does the Board of Directors recommend that I vote?

Our Board of Directors recommends that you vote your shares as follows:

| • | FORthe election of each of the nine director nominees listed herein; |

| • | FORthe ratification of the appointment of Deloitte as our independent registered public accounting firm for the year ending December 31, 2019; |

| • | FOReach of the proposed amendments to our charter; and |

| • | FORpermitting our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the foregoing proposals if there are not sufficient votes for the proposals to be approved. |

Holders of record of our shares of common stock as of the close of business on May 31, 2019 (the “Record Date”) will be entitled to vote at the Annual Meeting. As of the Record Date, there were 10,884,175 Class S shares, 466,188 Class T shares, 494,298 Class D shares, and 4,241,726 Class I shares of our common stock issued and outstanding for a total of 16,086,388 shares of our common stock issued and outstanding. You are entitled to one vote for each share you held as of the Record Date.

2

Table of Contents

How do I vote if I am a registered stockholder?

If you are a registered stockholder (that is, if your shares are registered on our records in your name and not in the name of your broker or nominee), you may authorize a proxy to vote your shares in any of the following ways described below, or in person by attending the Annual Meeting:

| • | via the Internet by going towww.proxypush.com/SREITand following theon-screen directions. Please have your proxy card in hand when accessing the website, as it contains a12-digit control numberrequired to record your voting instructions via the Internet; |

| • | by phone by calling the number listed on the proxy card,(866)250-6203, and following the recorded instructions, or by dialing (844)236-8917 and speaking to a live agent. You will need the12-digitcontrol numberincluded on your proxy card in order to record your voting instructions by telephone; or |

| • | by mail by marking, signing, dating and returning the enclosed proxy card. |

If you authorize a proxy by telephone or Internet, you do not need to mail your proxy card. See the attached proxy card for more instructions on how to vote your shares.

All proxies that are properly executed and received by our Secretary prior to the Annual Meeting, and are not revoked, will be voted at the Annual Meeting. Even if you plan to attend the Annual Meeting in person, we urge you to return your proxy card or submit a proxy by telephone or via the Internet to assure the representation of your shares at the Annual Meeting.

How do I vote if I hold my shares in “street name”?

If your shares are held by your bank or broker as your nominee (in “street name”), you should receive a proxy or voting instruction form from the institution that holds your shares and follow the instructions included on that form regarding how to instruct your broker to vote your shares.

If your shares are held in street name and you wish to attend the Annual Meeting and/or vote in person, you must bring your broker or bank voting instruction card and a proxy, executed in your favor, from the record holder of your shares. In addition, you must bring valid government-issued photo identification, such as a driver’s license or a passport.

How can I authorize a proxy to vote over the Internet or by telephone?

To authorize a proxy to vote electronically via the Internet, go towww.proxypush.com/SREITand follow the instructions. Please have your proxy card in hand when accessing the website, as it contains a12-digit control numberrequired record your voting instructions via the Internet.

If you have access to a touch-tone telephone, you may authorize your proxy by dialing(866)250-6203and following the recorded instructions, or by dialing(844)236-8917 and speaking to a live agent. You will need the12-digit control numberincluded on your proxy card in order to record your voting instructions by telephone.

You can authorize a proxy to vote via the Internet or by telephone at any time prior to 11:59 p.m., Eastern Daylight Time, July 30, 2019, the day before the Annual Meeting.

What if I return my proxy but do not mark it to show how I am voting?

If you submit a signed proxy without indicating your vote on any matter, the designated proxies will vote to elect all nine director nominees as directors, to approve the ratification of the appointment of Deloitte & Touche as our independent registered public accounting firm for 2019, to approve each of the amendments to our charter and to permit our Board of Directors to adjourn the Annual Meeting, if necessary, to solicit additional proxies in favor of the proposals in this Proxy Statement.

3

Table of Contents

What if other matters come up at the Annual Meeting?

At the date this Proxy Statement went to press, we did not know of any matters to be properly presented at the Annual Meeting other than those referred to in this Proxy Statement. If other matters are properly presented for consideration at the meeting or any adjournment or postponement thereof and you are a stockholder of record and have submitted a proxy card, the persons named in your proxy card will have the discretion to vote on those matters for you.

Can I change my vote or revoke my proxy after I authorize my proxy?

Yes. At any time before the vote on a proposal, you can change your vote either by:

| • | executing or authorizing, dating and delivering to us a new proxy with a later date that is received no later than July 30, 2019; |

| • | authorizing a proxy again via the Internet or by telephone at a later time before the closing of those voting facilities at 11:59 p.m., Eastern Daylight Time, on July 30, 2019; |

| • | sending a written statement revoking your proxy card to our Secretary or any corporate officer of our company, provided such statement is received no later than July 30, 2019; or |

| • | attending the Annual Meeting, revoking your proxy and voting your shares in person. |

Your attendance at the Annual Meeting will not, by itself, revoke a proxy previously authorized by you. We will honor the proxy card or authorization with the latest date.

Proxy revocation notices should be sent to Starwood Real Estate Income Trust, Inc., 1601 Washington Avenue, Suite 800, Miami Beach, FL 33139. Attention: Secretary. New paper proxy cards should be sent to Mediant, PO Box 8035 Cary, NC 27512-9916.

How do I vote my shares in person at the Annual Meeting?

First, you must satisfy the requirements for admission to the Annual Meeting (see below). Then, if you are a stockholder of record as of the close of business on the Record Date, and prefer to vote your shares at the Annual Meeting, you must bring proof of identification along with your proof of stock ownership. You may vote shares held in “street name” at the Annual Meeting only if you obtain a signed proxy from the record holder (broker, bank or other nominee) giving you the right to vote the shares.

Even if you plan to attend the Annual Meeting, we encourage you to authorize a proxy to vote your shares in advance by Internet, telephone or mail so that your vote will be counted even if you later decide not to attend the Annual Meeting.

Do I need a ticket to be admitted to the Annual Meeting?

You will need your proof of identification along with proof of stock ownership to enter the Annual Meeting. If your shares are held beneficially in the name of a bank, broker or other holder of record and you wish to be admitted to attend the Annual Meeting, you must present proof of your stock ownership, such as a bank or brokerage account statement.

Do I also need to present identification to be admitted to the Annual Meeting?

Yes, all stockholders must present a form of personal identification in order to be admitted to the Annual Meeting.

NO CAMERAS, RECORDING EQUIPMENT, ELECTRONIC DEVICES, LARGE BAGS, BRIEFCASES OR PACKAGES WILL BE PERMITTED AT THE ANNUAL MEETING.

4

Table of Contents

We will convene the Annual Meeting if stockholders representing the required quorum of shares of our common stock entitled to vote either sign and return their paper proxy cards, authorize a proxy to vote electronically or telephonically or attend the meeting. The presence, either in person or by proxy, at the Annual Meeting of at least 50% of all the votes entitled to be cast on any matter will constitute a quorum. Under our bylaws, if a quorum is not present at the Annual Meeting, in addition to an adjournment pursuant to Proposal 4, the Chairman of the Annual Meeting may adjourn the Annual Meeting to a date not more than 120 days from the original Record Date for the Annual Meeting without notice other than an announcement at the Annual Meeting. If you sign and return your paper proxy card or authorize a proxy to vote electronically or telephonically, your shares will be counted to determine whether we have a quorum even if you abstain or fail to vote as indicated in the proxy materials. Brokernon-votes and abstentions will also be considered present for the purpose of determining whether we have a quorum.

A “brokernon-vote” occurs when a broker does not vote on a matter on the proxy card because the broker does not have discretionary voting power for that particular matter and has not received voting instructions from the beneficial owner.

Representatives of Mediant, our solicitor, will count the votes and will serve as the independent inspector of election.

Where can I find the voting results of the Annual Meeting?

We intend to announce preliminary voting results at the Annual Meeting and then disclose the final results in a Current Report on Form8-K filed with the Securities and Exchange Commission (the “SEC”) within four business days after the date of the Annual Meeting.

How can I get additional copies of this Proxy Statement or other information filed with the SEC relating to this solicitation?

You may obtain additional copies of this Proxy Statement by calling our solicitor, Mediant, toll-free at (844)236-8917.

Where can I get more information about Starwood Real Estate Income Trust?

Prior to this solicitation, we have provided you with our Annual Report on Form10-K that contains our audited financial statements. We also file reports and other documents with the SEC. You can view these documents at the SEC’s website,www.sec.gov.You can also find more information on our website,www.starwoodnav.reit.

How is this solicitation being made?

This solicitation is being made primarily by the mailing of these proxy materials. Supplemental solicitations may be made by mail or telephone by our officers and representatives, who will receive no extra compensation for their services. The expenses in connection with this solicitation, including preparing and mailing these proxy materials, will be borne by us. We will reimburse brokerage firms and others for their reasonable expenses in forwarding solicitation material to the beneficial owners of our common stock. We have hired Mediant to assist us in the distribution of our proxy materials and for the solicitation of proxy votes. We will pay Mediant customary fees and expenses for these services of approximately $2,500.

Upon request, we will also reimburse brokerage houses and other custodians, nominees and fiduciaries for forwarding proxy and solicitation materials to stockholders.

5

Table of Contents

Will my vote make a difference?

Yes. Your vote is needed to ensure that the proposals can be acted upon.YOUR VOTE IS VERY IMPORTANT!Your immediate response will help avoid potential delays and may save us significant additional expenses associated with soliciting stockholder votes. We encourage you to participate in the governance of our company.

6

Table of Contents

PROPOSAL 1 — ELECTION OF DIRECTORS

There are currently nine members of the Board of Directors. On May 10, 2019, the Board of Directors unanimously nominated the nine directors listed below forre-election to the Board of Directors at the Annual Meeting. All of the nominees are willing to serve as directors but, if any of them should decline or be unable to act as a director, the individuals designated in the proxy cards as proxies will exercise the discretionary authority provided to vote for the election of such substitute nominee selected by our Board of Directors, unless the Board of Directors acts to reduce the size of the Board of Directors in accordance with our bylaws. The Board of Directors has no reason to believe that any such nominees will be unable or unwilling to serve.

Nominees for Election as Directors

The names, ages as of May 1, 2019 and existing positions with us of the nominees are as follows:

Name | Age | Position | ||||

Barry Sternlicht | 58 | Chairman of the Board | ||||

John P. McCarthy, Jr. | 57 | Chief Executive Officer, President and Director | ||||

Christopher D. Graham | 44 | Chief Investment Officer and Director | ||||

Mark Deason | 41 | Head of Asset & Portfolio Management and Director | ||||

Richard D. Bronson | 74 | Independent Director | ||||

David B. Henry | 70 | Independent Director | ||||

Robin Josephs | 59 | Independent Director | ||||

Dale Anne Reiss | 71 | Independent Director | ||||

James E. Walker | 56 | Lead Independent Director | ||||

The principal occupations and certain other information about the nominees, including their length of service as directors, are set forth below.

Barry S. Sternlicht has served as the Chairman of our Board of Directors since our formation in June 2017. He has been the Chairman of the Board and Chief Executive Officer of Starwood Capital, a privately-held global investment firm with over $63 billion in assets under management, since its formation in 1991. He also serves as the Chairman of the board of directors and the Chief Executive Officer of Starwood Property Trust, Inc. (NYSE: STWD) (“Starwood Property Trust”) the Chairman and Chief Executive Officer of Starwood Capital Group Management, LLC, a registered investment advisor and an affiliate of the Company. Over the past 27 years, Mr. Sternlicht has structured investment transactions with an aggregate asset value in excess of $100 billion. From 1995 to 2005, he was the Chairman and Chief Executive Officer of Starwood Hotels & Resorts Worldwide, Inc., an NYSE-listed hotel and leisure company that he founded. Mr. Sternlicht is the former Chairman of the Board of TRI Pointe Group (NYSE: TPH) and the former Chairman of the Board of Baccarat S.A., a crystal maker headquartered in Baccarat, France. In 2008, Mr. Sternlicht founded and became the Chairman and Chief Executive Officer of SH Group, a hotel management company that owns and manages the Baccarat Hotels & Resorts and 1 Hotels brands. Mr. Sternlicht is also on the Board of Directors of Invitation Homes (NYSE: INVH) (“Invitation Homes”) and The Estée Lauder Companies (NYSE: EL), as well as the Real Estate Roundtable and A.S. Roma, the professional Italian football club based in Rome. He previously served on the Board of Directors of Restoration Hardware (NYSE: RH) and as theco-Chairman of the Board of Directors of Starwood Waypoint Homes, a predecessor company of Invitation Homes. Additionally, he serves on the boards of the Robin Hood Foundation (of which he is the former Chairman), the Dreamland Film & Performing Arts Center and the Executive Advisory Board of Americans for the Arts. He is a member of the U.S. Olympic and Paralympic Foundation Trustee Council, the World Presidents Organization and the Urban Land Institute. Mr. Sternlicht received a Bachelor of Arts degree, magna cum laude, with honors from Brown University. He later earned a Master of Business Administration degree with distinction from Harvard Business School. Mr. Sternlicht provides our Board of Directors with a wealth of investment management experience along with extensive experience in real estate finance and development, and our Board of Directors believes Mr. Sternlicht provides a valuable perspective as its Chairman.

7

Table of Contents

John P. McCarthy, Jr. has served as our Chief Executive Officer and President since our formation in June 2017 and as a member of our Board of Directors and the Advisor’s Investment Committee since November 2017. Mr. McCarthy has also served as Managing Director of Starwood Capital since July 2015, where he is responsible for managing and expanding relationships with Starwood Capital’s investors around the world. Mr. McCarthy previously served Global Head of Asset Management for Starwood Capital from March 2009 to May 2012, during which time he also served as a member of Starwood Capital’s Investment Committee. Prior to rejoining Starwood Capital, Mr. McCarthy served as Deputy Head of Europe for the Abu Dhabi Investment Authority (“ADIA”) from June 2012 to May 2015. During this time, Mr. McCarthy served on ADIA’s Executive and Global Strategy committees. Prior to this, Mr. McCarthy served GlobalCo-Head of Asset Management for Lehman Brothers Real Estate Private Equity from June 2005 to February 2009 and was a Partner at O’Connor Capital Partners (“O’Connor”),Co-Head of European Business and Head of European Asset Management. Prior to joining O’Connor, Mr. McCarthy previously worked for 17 years at GE Capital, where he held a variety of positions, including managing the firm’s real estate investing activities across Central Europe. Mr. McCarthy received a B.S. degree in finance from the University of Connecticut, and an M.B.A. with a concentration in accounting from Fordham University. Mr. McCarthy provides our Board of Directors with extensive investment management experience, particularly in connection with international markets.

Christopher D. Graham has served as our Chief Investment Officer since our formation in June 2017, as a member of our Board of Directors since January 2018 and as a member of the Advisor’s Investment Committee since November 2017. Mr. Graham has served as Senior Managing Director and Head of Real Estate Acquisitions for the Americas at Starwood Capital since January 2013, supervising its investments in North, South and Central America. Mr. Graham is responsible for originating, structuring, underwriting and closing investments in all property types and is a member of the investment committee of Starwood Capital. At Starwood Capital, he has managed Starwood Land Ventures and overseen Starwood Capital’s investments in approximately 10,000 residential lots. In addition, he has overseen the acquisition of approximately $300 million ofnon-performing, single-family residential loans. Prior to joining Starwood Capital in 2002, Mr. Graham served as Director of the Financial Consulting Group for the Eastern Region of CB Richard Ellis (“CBRE”) in Washington, D.C. from May 1999 to September 2000, as Associate Director, Eastern Region of Investment Properties Group of CBRE from March 1998 to May 1999 and as an analyst and a consultant in the Financial Consulting Group of CBRE from July 1996 to March 1998. Mr. Graham received a B.B.A. in finance from James Madison University and an M.B.A. from Harvard Business School. Mr. Graham provides our Board of Directors with extensive investment experience.

Mark Deason has served as our Head of Asset & Portfolio Management since April 2019 and as a member of our Board of Directors and the Advisor’s Investment Committee since November 2017. Mr. Deason has served as Managing Director and Head of U.S. Asset Management at Starwood Capital since September 2016. In this role, Mr. Deason is responsible for overseeing the asset management of allnon-hotel assets, as well as Starwood Capital’s development function in the United States. While at Starwood Capital, Mr. Deason has participated in investments throughout the capital structure, including commercial, hospitality and residential acquisitions and developments. Prior to becoming a Managing Director, Mr. Deason served as a Senior Vice President at Starwood Capital since January 2011. Prior to joining Starwood Capital in 2003, Mr. Deason worked for Merrill Lynch & Co., Inc. in the firm’s real estate investment banking group, assisting west coast real estate, hospitality and gaming companies with a range of capital origination and mergers and acquisitions activities. He is a policy board member at the Fisher Center for Real Estate and Urban Economics and a member of the Milken Institute and the Urban Land Institute. Mr. Deason received a B.A. degree in business economics with a minor in accounting from the University of California, Los Angeles. Mr. Deason’s experience in asset management and acquisitions, particularly in the commercial sector, brings significant value to our Board of Directors in evaluating our portfolio and investment strategy.

Richard D. Bronson has served as a member of our Board of Directors since November 2017. Since 2000, Mr. Bronson has served as the Chief Executive Officer of The Bronson Companies, LLC, a real estate development company based in Beverly Hills, California. Mr. Bronson has been involved in the development of

8

Table of Contents

several shopping centers and office buildings throughout the United States. Mr. Bronson serves as the chairman of U.S. Digital Gaming, an online gaming technology provider based in Beverly Hills, California, and as a director of Starwood Property Trust and Invitation Homes. Mr. Bronson previously served as a director of Mirage Resorts, Inc. and Tri Pointe Homes, Inc. (NYSE: TPH) and as President of New City Development, an affiliate of Mirage Resorts, Inc., where he oversaw many of the company’s new business initiatives and activities outside Nevada. Mr. Bronson is on the board of the Neurosurgery Division at UCLA Medical Center. He is a member of the Western Real Estate Business Editorial Board. Mr. Bronson has also served as Vice President of the International Council of Shopping Centers, an association representing 50,000 industry professionals in more than 80 countries. Mr. Bronson is the founder and president of Native American Empowerment, LLC, a private company dedicated to monitoring, advocating and pursuing Native American gaming opportunities and tribal economic advancement. Mr. Bronson’s experience and knowledge in the real estate industry provides our Board of Directors with valuable insight into potential investments and the current state of the real estate markets.

David B. Henry has served as a member of our Board of Directors since January 2018. Mr. Henry served as Chief Executive Officer and Vice Chairman of Kimco Realty Corporation (NYSE: KIM) (“Kimco”), a publicly traded REIT, from December 2009 to January 2016, and in other capacities at Kimco since April 2001. Before joining Kimco in April 2001, Mr. Henry served in various capacities at GE Capital Real Estate (“GE Capital”) since 1978, including as GE Capital’s Senior Vice President and Chief Investment Officer from 1998 to 2001. Mr. Henry also served as Chairman of GE Capital’s Investment Committee and as a member of its Credit Committee. Before joining GE Capital, Mr. Henry served as Vice President for Republic Mortgage Investors from 1973 to 1978. Mr. Henry serves on the Board of Directors of HCP, Inc. (NYSE: HCP), a publicly traded healthcare REIT; VEREIT, Inc. (NYSE: VER), a publicly traded net lease REIT; Tanger Outlet Centers (NYSE: SKT), a publicly traded shopping center REIT; Columbia Property Trust (NYSE: CXP), a publicly tradedClass-A office REIT; and Fairfield County Bank, a private Connecticut mutual savings bank. Mr. Henry is a past trustee and served as 2011-2012 Chairman of the International Council of Shopping Centers, and was a former Vice Chairman of the Board of Governors of the National Association of Real Estate Investment Trusts. Mr. Henry also serves on the real estate advisory boards of New York University and Baruch College and is a past member of the Columbia University Real Estate Forum. Mr. Henry received a B.S. in Business Administration from Bucknell University and an M.B.A. from the University of Miami in Miami, Florida. Mr. Henry’s extensive involvement with REITs which target a broad spectrum of assets helps provide our Board of Directors with an understanding of the market in which it competes for capital and investments.

Robin Josephs has served as a member of our Board of Directors since November 2017. Ms. Josephs has served on the board of directors of iStar Financial Inc. (NYSE: STAR) (“iStar”), a real estate investment and development firm, since March 1998 and served as lead director since May 2007, with duties that include presiding at all executive sessions of the independent directors and serving as principal liaison between the chairman and the independent directors. Ms. Josephs is also chair of iStar’s nominating and corporate governance committee and a member of iStar’s compensation committee. Ms. Josephs also serves on the board of directors of Safehold, Inc. (NYSE: SAFE) which had its IPO in June 2017 and invests in ground leases. She currently serves as a director, chair of the compensation committee and a member of the audit committee of MFA Financial, Inc. (NYSE: MFA), which is primarily engaged in investing in residential mortgage-backed securities, and as a director and member of the audit committee and compensation committee of QuinStreet, Inc. (NASDAQ: QNST), a vertical marketing and online media company. Ms. Josephs previously served as a director and member of the audit and compensation committees of Plum Creek Timber Company, Inc. (NYSE: PCL) from 2003 until its sale to Weyerhaeuser Company in 2016. From 2005 to 2007, Ms. Josephs served as a managing director of Starwood Capital. Previously, Ms. Josephs was a senior executive with Goldman Sachs & Co. in various capacities. Ms. Josephs is a trustee of the University of Chicago Cancer Research Foundation. Ms. Josephs received a B.S. degree in economics from the Wharton School of the University of Pennsylvania and an M.B.A. from Columbia University. Ms. Josephs’ previous employment as an investment banking professional and her extensive experience as a director of public companies brings valuable knowledge of finance, capital markets and corporate governance to our Board of Directors.

9

Table of Contents

Dale Anne Reiss has served as a member of our Board of Directors since November 2017. Ms. Reiss served as the Global and the Americas Director of Real Estate Hospitality and Construction at Ernst & Young LLC from 1995 until her retirement in 2008. Following her retirement, Ms. Reiss continued to consult to the firm until 2011. Ms. Reiss has served as Managing Director of Artemis Advisors LLC, a real estate restructuring and consulting firm, since June 2008. Ms. Reiss has also served as Senior Managing Director of Brock Capital Group LLC, a boutique investment bank, since December 2009 and Chairman of its affiliate, Brock Real Estate LLC, which specializes in raising capital and mezzanine financing. Ms. Reiss currently serves as director, chair of the audit committee and member of the nominating/governance committee of iStar Financial Inc. (NYSE: STAR), and as a director of Tutor Perini Corporation (NYSE: TPC) where she is chair of the audit committee. Ms. Reiss served as a director of CYS Investments, Inc. (NYSE: CYS) until its merger with Two Harbors Investment Corp. (NYSE: TWO) in 2018, and as a director and chair of the compensation committee of Care Capital Properties, Inc. (NYSE: CCP) until its merger with Sabra Health Care REIT, Inc. (NASDAQ: SBRA) in 2017. She is governor of the Urban Land Institute Foundation where she is also as a past board member. Ms. Reiss received a B.S. degree in economics and accounting from the Illinois Institute of Technology and an M.B.A. in finance and statistics from the University of Chicago. Ms. Reiss is a certified public accountant. Ms. Reiss’s more than 40 years’ experience in advising public and private real estate and hospitality companies, corporations and financial institutions in all aspects of development, investment and finance, provides our board with valuable knowledge of historic and current opportunities in the real estate market. Ms. Reiss is a financial expert.

James E. Walker has served as a member of our Board of Directors since November 2017 and serves as our lead independent director. From April 2008 until December 2016, Mr. Walker served as a Managing Partner of Fir Tree Partners (“Fir Tree”), a global alternative investment firm with over $10 billion of assets. Mr. Walkerco-founded Fir Tree’s real estate opportunity funds andco-led the development of Fir Tree’s real estate effort. At Fir Tree, Mr. Walker was jointly responsible for overall firm management, identified new areas of investment opportunity and led numerous activist opportunities. He was also a member of the Fir Tree’s real estate investment committee and Chairman of its risk committee. Prior to joining Fir Tree in 2008, Mr. Walker was aco-founder and Managing Partner of Black Diamond Capital Management, LLC (“Black Diamond”), a privately held investment management firm specializing in both performing andnon-performing debt. Prior to joining Black Diamond, he was a senior member of Kidder, Peabody & Co.’s structured finance group where he managed a proprietary investment vehicle. Mr. Walker began his career in structured finance at Bear Stearns & Co. in the asset-backed securities group. He holds a B.S. in economics from Boston College’s Carroll School of Management. Mr. Walker’s extensive experience in real estate-related investing and the management of alternative investment vehicles provides our Board of Directors with valuable insight into potential investments and capital markets transactions.

At the Annual Meeting, we will vote each valid proxy returned to us for the nominees listed above unless the proxy specifies otherwise. Proxies may not be voted for more than nine nominees for director. While our board does not anticipate that any of the nominees will be unable to stand for election as a director at the Annual Meeting, if that is the case, proxies will be voted in favor of such other person or persons as our Board of Directors may designate.

VOTING RECOMMENDATION

OUR BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS THAT YOU VOTE “FOR” THE ELECTION OF EACH OF THE DIRECTOR NOMINEES NAMED ABOVE.

10

Table of Contents

Our business is managed by our Advisor, subject to the oversight and direction of our Board of Directors. Our Board of Directors has nine members and is currently comprised of Messrs. Sternlicht, McCarthy, Graham, Deason, Bronson, Henry, Walker and Mses. Reiss and Josephs.

Director Independence

Under our charter, a majority of our directors must be independent directors, except for a period of up to 60 days after the death, removal or resignation of an independent director pending the election of a successor independent director. Consistent with the NASAA REIT Guidelines, our charter defines an independent director as a director who is not and has not for the last two years been associated, directly or indirectly, with Starwood Capital. A director is deemed to be associated with Starwood Capital if he or she owns any interest (other than an interest in us or an immaterial interest in an affiliate of us) in, is employed by, is an officer or director of, or has any material business or professional relationship with Starwood Capital, the Advisor or any of their affiliates, performs services (other than as a director) for us, or serves as a director or trustee for more than three REITs sponsored by Starwood Capital or advised by the Advisor. A business or professional relationship will be deemed material per se if the gross revenue derived by the director from Starwood Capital exceeds 5% of (1) the director’s annual gross revenue derived from all sources during either of the last two years or (2) the director’s net worth on a fair market value basis. An indirect relationship is defined to include circumstances in which the director’s spouse, parents, children, siblings, mothers- orfathers-in-law, sons- ordaughters-in-law or brothers- orsisters-in-law is or has been associated with Starwood Capital. Our charter requires that a director have at least three years of relevant experience and demonstrate the knowledge required to successfully acquire and manage the type of assets that we intend to acquire to serve as a director. Our charter also requires that at all times at least one of our independent directors must have at least three years of relevant real estate experience.

Based upon its review, our Board of Directors has affirmatively determined that each of Messrs. Bronson, Henry, Walker and Mses. Reiss and Josephs are “independent” members of our Board of Directors under all applicable standards for independence, including with respect to committee service on our Audit Committee. Please note that this Proxy Statement contains a proposal to amend the definition of “Independent Director” under our charter. See Proposal 3B for additional information.

Board of Directors Composition

We do not have a standing nominating committee. Our Board of Directors has determined that it is appropriate not to have a nominating committee because our Board of Directors presently considers all matters for which a nominating committee would be responsible. Each member of our Board of Directors participates in the consideration of nominees. Our Board of Directors believes that the significance of each director nominee’s qualifications, experience, attributes and skills is particular to that individual, meaning that there is no single test applicable to all director candidates. The effectiveness of the board is best evaluated as a group of directors, rather than at an individual director level. As a result, our Board of Directors has not established specific minimum qualifications that must be met by each individual wishing to serve as a director. When evaluating candidates for a position on our Board of Directors, the Board of Directors considers the potential impact of the candidate, along with his or her particular experiences, on the board as a whole. The diversity of a candidate’s background or experiences, when considered in comparison to the background and experiences of other members of the Board of Directors, may or may not impact the board’s view as to the candidate. In evaluating director candidates, our Board of Directors considers all factors that it deems relevant.

In recommending director nominees to our Board of Directors, our Board of Directors solicits candidate recommendations from its current members and our management. Our Board of Directors also will consider recommendations made by stockholders for director nominees who meet the established director criteria set forth above. In evaluating the persons recommended as potential directors, our Board of Directors will consider each

11

Table of Contents

candidate without regard to the source of the recommendation and take into account those factors that our Board of Directors determines are relevant. Stockholders may directly nominate potential directors by satisfying the procedural requirements for such nomination as provided in Article II, Section 11(a)(2) of our bylaws.

In conducting its annual self-assessment and nominating the director nominees, our Board of Directors determined that each director nominee has the business experience, skills, perspectives, independent and diversity in relation to our company’s needs. In addition to a demonstrated record of business and professional accomplishment, each of our director nominees has substantial experience serving on boards, including our Board of Directors and boards of other organizations. Each of our directors has gained substantial insight as to the operation of our company and has demonstrated a commitment to discharging his or her oversight responsibilities as a director.

For so long as the Advisory Agreement is in effect, the Advisor has the right to nominate, subject to the approval of such nomination by our Board of Directors, three affiliated directors to the slate of directors to be voted on by our stockholders at our annual meeting of stockholders; provided, however, that such number of director nominees shall be reduced as necessary by a number that will result in a majority of directors being independent of Starwood Capital. Our Board of Directors must also consult with the Advisor in connection with (i) its selection of each independent director for nomination to the slate of directors to be voted on at the annual meeting of stockholders, and (ii) filling any vacancies created by the removal, resignation, retirement or death of any director.

Our Board of Directors currently has one standing committee: an Audit Committee. The audit committee charter is available on our website,www.starwoodnav.reit,under the “Investor Relations — Literature” tab.

Audit Committee

The Audit Committee is currently comprised of Mses. Reiss and Josephs and Mr. Walker, with Ms. Reiss serving as the committee’s chairperson. All Audit Committee members are “independent,” consistent with the qualifications set forth our charter and Rule10A-3 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), applicable to boards of directors in general and audit committees in particular. Ms. Reiss is qualified as an audit committee financial expert within the meaning of Item 407(d)(5) of RegulationS-K under the Exchange Act. The Audit Committee assists the Board of Directors in overseeing:

| • | our accounting and financial reporting processes; |

| • | the integrity and audits of our financial statements; |

| • | our compliance with legal and regulatory requirements; |

| • | the qualifications and independence of our independent auditors; and |

| • | the performance of our internal and independent auditors. |

In addition, the Audit Committee selects the independent auditors to audit our annual financial statements and reviews with the independent auditors the plans and results of the audit engagement. The audit committee also approves the auditand non-audit services provided by the independent public accountants and the fees we pay for these services.

The Audit Committee has adopted procedures for the processing of complaints relating to accounting, internal control and auditing matters. The Audit Committee oversees the review and handling of any complaints submitted pursuant to the forgoing procedures and of any whistleblower complaints subject to Section 21F of the Exchange Act.

Meetings

Directors are expected to attend Board meetings and meetings of the committees on which they serve, to spend the time needed and to meet as frequently as necessary, in order to discharge their responsibilities

12

Table of Contents

properly. Our Board of Directors conducts its business through meetings of the Board of Directors, actions taken by written consent in lieu of meetings and by actions of its committees. During the fiscal year ended December 31, 2018, the Board of Directors held five meetings and the Audit Committee held four meetings. Each director attended at least 75% of the combined number of meetings of the Board of Directors and meetings of committees on which he or she served during the period in 2018 in which he or she served as a director or member of such committee, as applicable.

We do not have a formal policy regarding attendance by directors at our annual meeting of stockholders but invite and encourage all directors to attend. We make every effort to schedule our annual meeting of stockholders at a time and date to permit attendance by directors, taking into account the directors’ schedules and the timing requirements of applicable law. We did not hold an annual meeting of stockholders in 2018.

Executive Sessions

Ournon-management directors periodically hold executive sessions at which management is not present. Our Corporate Governance Guidelines provide that the presiding independent director, if any, or a director designated by thenon-management directors shall serve as such presiding director.

Board Leadership Structure and Role in Risk Oversight

The Board of Directors has structured itself in a manner that it believes allows it to perform its oversight function effectively. A majority of our directors are independent. Our offices of Chairman of the Board of Directors and Chief Executive Officer are separate even though such separation is not required. Mr. Sternlicht, as our Chairman of the Board of Directors, is responsible for our strategic direction and oversight, while Mr. McCarthy, as our Chief Executive Officer, is responsible for the execution of our business strategy, financial affairs and operations.

In addition, the Board of Directors has determined that since the Chairman of the Board of Directors is not an independent director, a lead independent director should be appointed by a majority of our independent directors. Our independent directors have appointed Mr. Walker to serve as our lead independent director. Key responsibilities of our lead independent director include, among others, presiding at executive sessions of independent directors, facilitating communications between the independent directors and the Chairman of the Board of Directors and Chief Executive Officer, and calling meetings of the independent directors, as necessary.

As with every business, we confront and must manage various risks including financial and economic risks related to the performance of our portfolio and how our investments have been financed. Pursuant to our charter and bylaws and the Maryland General Corporation Law, our business and affairs are managed under the direction of our Board of Directors. Our Advisor is responsible for theday-to-day management of risks we face, while our Board of Directors has responsibility for establishing broad corporate policies for our overall operation and for the direction and oversight of our risk management. Members of our Board of Directors keep informed of our business by participating in meetings of our Board of Directors and the Audit Committee, by reviewing analyses, reports and other materials provided to them by and through discussions with our Advisor and our executive officers.

In connection with their oversight of risks to our business, our Board of Directors and the Audit Committee consider feedback from our Advisor concerning the risks related to our business, operations and strategies. The Audit Committee also assists the Board in fulfilling its oversight responsibilities with respect to risk management in the areas of financial reporting, internal controls and compliance with legal and regulatory requirements. Our compensation policies and practices, pursuant to which we pay no cash compensation to our Advisor’s officers and employees since they are compensated by our Advisor or its affiliates, do not create risks that are reasonably likely to have a material adverse effect on us. With respect to cybersecurity risk oversight, the Board and/or the

13

Table of Contents

Audit Committee receive periodic reports and/or updates from management on the primary cybersecurity risks facing our company and our Advisor and the measures we and our Advisor are taking to mitigate such risks. In addition to such reports, the Board or the Audit Committee receive updates from management as to changes to our and the Advisor’s cybersecurity risk profile or certain newly identified risks.

Code of Ethics

We have adopted a Code of Ethics that applies to all of our directors, officers and employees (if any), and to all of the officers and employees of the Advisor, including our principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. Our Code of Ethics, as it relates to those also covered by Starwood Capital’s code of conduct, operates in conjunction with, and in addition to, Starwood Capital’s code of conduct. Our Code of Ethics is designed to comply with SEC regulations relating to codes of conduct and ethics. Our Code of Ethics is available on our website,www.starwoodNAV.reit,under the “Investor Relations — Literature” tab.

Any waiver of the Code of Ethics may be made only by our Board or the Audit Committee and will be promptly disclosed as required by law. Any modifications to the Code of Ethics will be reflected on our website.

Corporate Governance Guidelines

We have also adopted Corporate Governance Guidelines to advance the functioning of our Board of Directors and its committees and to set forth our Board of Directors’ expectations as to how it and they should perform its and their respective functions. Our Corporate Governance Guidelines are available on our website,www.starwoodNAV.reit,under the “Investor Relations — Literature” tab.

Annual Board Self-Assessment

Our Board of Directors annually conducts a self-evaluation (with anonymous responses permitted) to determine whether it and the Audit Committee are functioning effectively and to identify opportunities to enhance their effectiveness.

Stockholder Nominations and Communications Policy

Stockholders may communicate with the Board of Directors or any of its directors. Stockholders who wish to communicate with the Board of Directors may do so by sending written communications addressed to our Secretary, c/o Starwood Real Estate Income Trust, Inc., 1601 Washington Avenue, Suite 800, Miami Beach, Florida 33139, except in situations where such communications relate to accounting matters, in which case, stockholders should send such communications to the Chairperson, Starwood Real Estate Income Trust, Inc. Audit Committee at the address above. All communications will be compiled by our Secretary, who will determine whether they should be presented to our Board of Directors. The purpose of this screening is to avoid having our Board of Directors consider irrelevant or inappropriate communications (such as advertisements and solicitations). Our Secretary will submit all appropriate communications to our Board of Directors, the Audit Committee or the relevant individual director(s), as appropriate. All communications directed to the Audit Committee that relate to questionable accounting or auditing matters involving our company will be promptly and directly forwarded to the Audit Committee.

14

Table of Contents

The following table sets forth the positions, ages as of April 1, 2019 and selected biographical information for our executive officers. Biographical information for Messrs. Sternlicht, McCarthy, Graham and Deason is provided above under “Proposal 1 — Election of Directors — Nominees for Election as Directors.”

Name | Age | Position | ||||

Barry S. Sternlicht | 58 | Chairman of the Board | ||||

John P. McCarthy, Jr. | 57 | Chief Executive Officer, President and Director | ||||

Christopher D. Graham | 44 | Chief Investment Officer and Director | ||||

Dave Guiteau | 44 | Chief Financial Officer and Treasurer | ||||

Matthew S. Guttin | 40 | Chief Compliance Officer and Secretary | ||||

Robert Geimer | 51 | Head of Asset Management & Operations | ||||

Sean Harris | 35 | Manager of Acquisitions | ||||

Mark Deason | 41 | Head of Asset & Portfolio Management and Director | ||||

Dave Guiteau has served as our Chief Financial Officer and Treasurer and as a member of the Advisor’s Investment Committee since April 2019. Prior to joining Starwood Capital, Mr. Guiteau held various financial roles with AIG Global Real Estate, including Chief Financial Officer from July 2012 to March 2019 and as a Managing Director overseeing the financial accounting and reporting for AIG Global Real Estate’s portfolio of private equity real estate funds from September 2002 to June 2010. From July 2010 to July 2012, Mr. Guiteau served as the Chief Financial Officer of Hunter Roberts Construction Group, a New York-based general contractor. Mr. Guiteau began his career at Arthur Andersen, LLP where he was an audit manager in the firm’s real estate and hospitality services group in its New York office, focusing on public and private real estate clients. Mr. Guiteau received a B.B.A. degree in public accounting from Hofstra University. He is also a certified public accountant.

Matthew S. Guttin has served as our Secretary since October 2017 and as our Chief Compliance Officer since our formation in June 2017. Mr. Guttin has also served as Chief Compliance Officer for Starwood Capital since August 2010. As the Chief Compliance Officer, Mr. Guttin is responsible for overseeing the firm’s regulatory and compliance program. Before joining Starwood Capital, Mr. Guttin practiced corporate finance and real estate law at Cahill Gordon & Reindel, LLP, Fried, Frank, Harris Shriver & Jacobson, LLP and DiSanto LLP. Mr. Guttin is an employee of Rinaldi, Finkelstein & Franklin, L.L.C., Starwood Capital’s lead outside counsel. Mr. Guttin received a B.S. in Political Science from the University of Rochester and a J.D. from Georgetown University Law Center. He is licensed to practice law in New York and Connecticut, and holds the Series 7 and Series 24 licenses.

Robert Geimer has served as our Head of Asset Management & Operations since October 2017. Mr. Geimer has served as Senior Vice President of Asset Management at Starwood Capital since January 2003. In this position, Mr. Geimer’s principal responsibilities include playing a senior role on the asset management team for a diverse portfolio of national and international real estate assets. He manages the development and execution of investment and exit strategies, manages resources relatedto day-to-day decision-making, and plays an integral role in the review and approval of annual business plans with partners and third-party fee managers. Prior to hisnearly 20-year career with Starwood Capital, Mr. Geimer served as an Asset Manager and Portfolio Controller with Greystone Realty, LLC, the real estate management group for New York Life Insurance Co. Before joining Greystone Realty, LLC, Mr. Geimer was an employed by Compass Retail, Inc. a former division of Equitable Real Estate Group, Inc. Mr. Geimer received a B.S. degree from the West Virginia University School of Business and is a certified public accountant.

Sean Harris has served as our Manager of Acquisitions since October 2017. Mr. Harris has served as an Acquisitions Associate and Assistant to Mr. Sternlicht, the Chairman and CEO of Starwood Capital, since August 2016. Prior to joining Starwood Capital in 2016, Mr. Harris served as a Director of Acquisitions and

15

Table of Contents

Investment Management at Monday Properties, LLC since December 2012, wherehe co-led acquisitions, investment management, and capital markets. Before joining Monday Properties, LLC as an Associate in July 2010, Mr. Harris was employed by Ernst & Young LLC in the Transaction Real Estate group. Mr. Harris received B.S. degrees in finance and accounting from East Carolina University and a MAcc from the Max M. Fisher College of Business at The Ohio State University.

16

Table of Contents

COMPENSATION OF DIRECTORS AND EXECUTIVE OFFICERS

We are externally managed by the Advisor and currently have no employees. Our executive officers serve as officers of the Advisor and are employees of the Advisor or one or more of its affiliates. The Advisory Agreement between our company, the Operating Partnership and the Advisor dated December 15, 2017 (the “Advisory Agreement”) provides that the Advisor is responsible for managing our investment activities, as such our executive officers do not receive any cash compensation from us or any of our subsidiaries for serving as our executive officers but, instead, receive compensation from the Advisor. In addition, we do not reimburse the Advisor for compensation it pays to our executive officers. The Advisory Agreement does not require our executive officers to dedicate a specific amount of time to fulfilling the Advisor’s obligations to us under the Advisory Agreement. Accordingly, the Advisor has informed us that it cannot identify the portion of the compensation it awards to our executive officers that relates solely to such executives’ services to us, as the Advisor does not compensate its employees specifically for such services. Furthermore, we do not have employment agreements with our executive officers, we do not provide pension or retirement benefits, perquisites or other personal benefits to our executive officers, our executive officers have not received any nonqualified deferred compensation and we do not have arrangements to make payments to our executive officers upon their termination or in the event of a change in control of us.

Although we do not pay our executive officers any cash compensation, we pay the Advisor the fees described below under the heading “Transactions with Related Persons and Certain Control Persons.”

Non-Employee Director Compensation

We compensate each of our independent directors with an annual retainer of $65,000, plus an additional retainer of $10,000 to the chairperson of our audit committee. We intend to pay in quarterly installments 75% of this compensation in cash and the remaining 25% in an annual grant of Class I restricted stock based on the most recent prior month’s NAV. The restricted stock will generally vest one year from the date of grant.

We do not pay our directors additional fees for attending board meetings, but we reimburse each of our directors forreasonable out-of-pocket expenses incurred in attending board and committee meetings (including, but not limited to, airfare, hotel and food). Our directors who are affiliated with Starwood Capital, including the Advisor, receive no additional compensation for serving on the Board of Directors or committees thereof.

The following table sets forth the compensation to our directors for the fiscal year ended December 31, 2018:

Name | Fees Earned or Paid in Cash | Stock Awards(1) | Total | |||||||||

Barry S. Sternlicht | $ | — | $ | — | $ | — | ||||||

John P. McCarthy, Jr. | — | — | — | |||||||||

Christopher D. Graham | — | — | — | |||||||||

Mark Deason | — | — | — | |||||||||

Richard D. Bronson | 48,731 | 23,040 | 71,771 | |||||||||

David B. Henry | 44,680 | 20,320 | 65,000 | |||||||||

Robin Josephs | 48,731 | 23,040 | 71,771 | |||||||||

Dale Anne Reiss | 56,233 | 26,580 | 82,813 | |||||||||

James E. Walker | 48,731 | 23,040 | 71,771 | |||||||||

| (1) | Includes the total value in restricted stock granted to each of the Company’s independent directors during 2018. The grants of Class I restricted shares were made in April 2018 and May 2018 and vest in April 2019 and May 2019, respectively. Both grants were valued based on a NAV per share of $20.00, in accordance with the independent director compensation policy, for grants made during the escrow period. |

17

Table of Contents

Independent Director Restricted Share Plan

We have adopted a restricted share plan which permits our Board of Directors to grant restricted stock and/or restricted stock units to our independent directors in order to: (i) attract and retain independent directors by affording them an opportunity to share in our future successes, (ii) strengthen the mutuality of interests between such independent directors and our stockholders, and (iii) provide the independent directors with a proprietary interest in maximizing our growth, profitability and overall success.

We have authorized and reserved an aggregate maximum number of 200,000 shares for issuance under the restricted share plan. The maximum aggregate number of shares of our Class I common stock associated with any award granted under the restricted share plan in any calendar year to any one independent director is 10,000. In the event of a transaction between us and our stockholders that causesthe per-share value of our Class I common stock to change (including, without limitation, any stock dividend, stocksplit, spin-off, rights offering or large nonrecurring cash dividend), the share authorization limits under the plan will be adjusted proportionately and the Board of Directors will make such adjustments to the plan and awards as it deems necessary, in its sole discretion, to prevent dilution or enlargement of rights immediately resulting from such transaction. In the event of a stock split, a stock dividend or a combination or consolidation of the outstanding shares of common stock into a lesser number of shares, the authorization limits under the plan will automatically be adjusted proportionately and the shares then subject to each award will automatically be adjusted proportionately without any change in the aggregate purchase price.

Our Board of Directors may in its sole discretion at any time determine that all or a portion of a participant’s awards will become fully vested. The plan will automatically expire on the tenth anniversary of the date on which it is approved by our Board of Directors, unless extended or earlier terminated by our Board of Directors. Our Board of Directors may terminate the plan at any time. The expiration or other termination of the plan will not, without the participant’s consent, have an adverse impact on any award that is outstanding at the time the plan expires or is terminated. Our Board of Directors may amend the plan at any time, but no amendment will adversely affect any award without the participant’s consent and no amendment to the plan will be effective without the approval of our stockholders if such approval is required by any law, regulation or rule applicable to the plan.

The following table summarizes information, as of December 31, 2018, relating to our equity compensation plans pursuant to which shares of our common stock or other equity securities may be granted from time to time:

Plan category | (a) Number of securities to be issued upon exercise of outstanding options, warrants, and rights | (b) Weighted-average exercise price of outstanding options, warrants, and rights | (c) Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a) | |||||||||

Equity compensation plans approved by security holders | — | $ | — | 194,174 | ||||||||

Equity compensation plans not approved by security holders | N/A | N/A | N/A | |||||||||

Total | — | $ | — | 194,174 | ||||||||

Our Board of Directors is responsible for determining the form and amount of compensation that is paid to our independent directors. In addition, our executive officers may make recommendations regarding the compensation level for the independent directors and provide comparison data. Our Board of Directors periodically assesses the level of independent director compensation, taking into account the responsibilities and duties of the independent directors and the time required to perform those duties. In determining the level of independent director compensation, our Board of Directors attempts to be consistent with market practices, but does not set compensation at a level that would call into question the independent directors’ objectivity.

18

Table of Contents

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act requires our directors and executive officers, and persons who own more than ten percent of a registered class of our equity securities, to file with the SEC, within specified time frames, initial reports of beneficial ownership and reports of changes in ownership of our shares of common stock. Officers, directors and greater than ten percent stockholders are required by SEC regulation to furnish us with copies of all Section 16(a) forms they file with the SEC. None of the foregoing persons were required to file Section 16(a) forms during the fiscal year ended December 31, 2018.

Compensation Committee Interlocks and Insider Participation

We currently do not have a compensation committee of our Board of Directors. Our Board of Directors believes it is appropriate for us not to have a compensation committee because our executive officers are compensated by our Advisor and not by us. Accordingly, we have not included a Compensation Committee Report or a Compensation Discussion and Analysis in this proxy statement. In 2018, our entire Board of Directors determined the compensation of our independent directors. As noted above, we have no employees. During the fiscal year ended December 31, 2018, none of our executive officers served as:

| • | a member of the compensation committee (or other board committee performing equivalent functions or, in the absence of any such committee, the entire board of directors) of another entity, one of whose executive officers served on our Board of Directors; or |

| • | a director of another entity, one of whose executive officers served on our Board of Directors. |

Security Ownership of Certain Beneficial Owners and Management

The following table sets forth, as of April 30, 2019, information regarding the number and percentage of shares owned by each director, our chief executive officer, each executive officer, all directors and executive officers as a group, and any person known to us to be the beneficial owner of more than 5% of outstanding shares of our common stock. Beneficial ownership is determined in accordance with the rules of the SEC and includes securities that a person has the right to acquire within 60 days. The address for each of the persons named below is in care of our principal executive offices at 1601 Washington Avenue, Suite 800, Miami Beach, Florida 33139.

Name of Beneficial Owner | Number of Shares Beneficially Owned(1) | Percent of All Shares | ||||||

Directors and Executive Officers | ||||||||

Barry S. Sternlicht(2) | 252,224 | 2 | % | |||||

John P. McCarthy, Jr. | 15,133 | * | ||||||

Christopher D. Graham | — | — | ||||||

Dave Guiteau | — | — | ||||||

Matthew S. Guttin | — | — | ||||||

Robert Geimer | — | — | ||||||

Sean Harris | 2,471 | * | ||||||

Mark Deason | — | — | ||||||

Richard D. Bronson(3) | 1,162 | * | ||||||

David B. Henry(3) | 1,025 | * | ||||||

Robin Josephs(3) | 1,162 | * | ||||||

Dale Anne Reiss(3) | 1,341 | * | ||||||

James E. Walker(3) | 1,162 | * | ||||||

|

|

|

| |||||

All directors and executive officers as a group | 275,680 | 2 | % | |||||

|

|

|

| |||||

| * | Represents less than 1%. |

| (1) | All shares listed in the table above are Class I shares. |

19

Table of Contents

| (2) | As of March 28, 2019, Starwood Real Estate Income Holdings, L.P. owned 251,045 Class I shares, which are deemed to be beneficially owned by Mr. Sternlicht. |

| (3) | Each of our independent directors received a grant of restricted Class I shares, as part of their annual compensation, on April 3, 2018, which will vest on April 3, 2019, and a grant of restricted Class I shares on May 4, 2018, which will vest on May 4, 2019. |

20

Table of Contents

TRANSACTIONS WITH RELATED PERSONS AND CERTAIN CONTROL PERSONS

The following describes all transactions during the fiscal year ended December 31, 2018 and currently proposed transactions involving us, our directors, our Advisor, Starwood Capital and any affiliate thereof.

Our Relationship with Our Advisor and Starwood Capital

We are externally managed by our Advisor, Starwood REIT Advisors, L.L.C., a Delaware limited liability company, which is responsible for sourcing, evaluating and monitoring our investment opportunities and making decisions related to the acquisition, management, financing and disposition of our assets, in accordance with our investment objectives, guidelines, policies and limitations, subject to oversight by our Board of Directors. The Advisor is a subsidiary of our sponsor, Starwood Capital Group Holdings, L.P. All of our officers and directors, other than the independent directors, are employees of Starwood Capital. We have and will continue to have certain relationships with the Advisor and its affiliates.

Advisory Agreement

We are managed and advised by the Advisor pursuant to the Advisory Agreement that first became effective December 15, 2017; however, we did not commence active operations until December 21, 2018, when we had satisfied the minimum offering requirement in our initial public offering and our Board of Directors authorized the release of proceeds from escrow to us.

Pursuant to the Advisory Agreement and subject to the supervision of our Board of Directors, the Advisor is responsible for, among other things:

| • | serving as an advisor to us and the Operating Partnership with respect to the establishment and periodic review of our investment guidelines and our and the Operating Partnership’s investments, financing activities and operations; |

| • | sourcing, evaluating and monitoring our and Operating Partnership’s investment opportunities and executing the acquisition, management, financing and disposition of our and Operating Partnership’s assets, in accordance with our investment guidelines, policies and objectives and limitations, subject to oversight by our Board of Directors; |

| • | with respect to prospective acquisitions, purchases, sales, exchanges or other dispositions of investments, conducting negotiations on our and Operating Partnership’s behalf with sellers, purchasers, and other counterparties and, if applicable, their respective agents, advisors and representatives, and determining the structure and terms of such transactions; |

| • | providing us with portfolio management and other related services; |

| • | serving as our advisor with respect to decisions regarding any of our financings, hedging activities or borrowings; and |

| • | engaging and supervising, on our and Operating Partnership’s behalf and at our and the Operating Partnership’s expense, various service providers. |

The above summary is provided to illustrate the material functions that the Advisor performs for us and it is not intended to include all of the services that may be provided to us by the Advisor or third parties.

Management Fee, Performance Participation Interest and Expense Reimbursements