THE PERFECTLY GREEN CORP CONSOLIDATED FINANCIAL STATEMENTS (WITH INDEPENDENT AUDITOR’S REPORT THEREON) DECEMBER 31, 2017 AND 2016

THE PERFECTLY GREEN CORP. TABLE OF CONTENTS Page

INDEPENDENT AUDITOR’S REPORT 1

CONSOLIDATED FINANCIAL STATEMENTS:

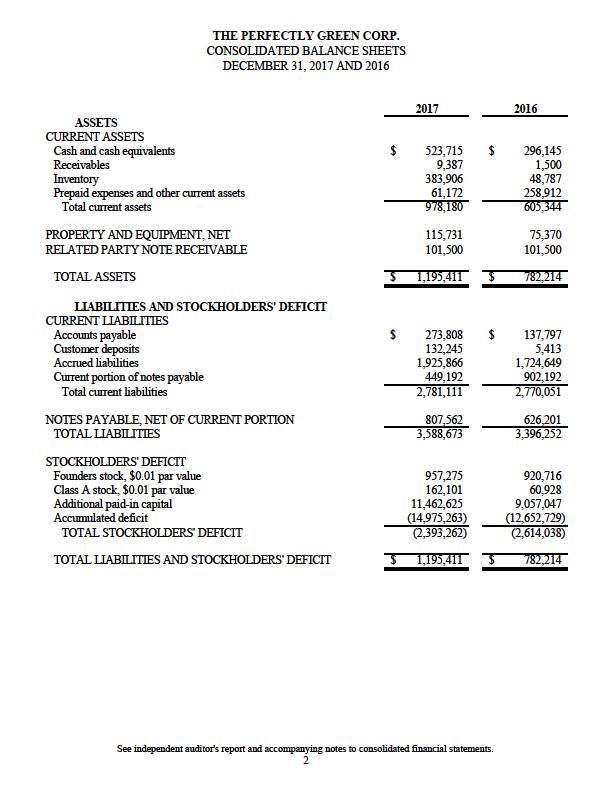

Consolidated Balance Sheets at December 31, 2017 and 2016 2

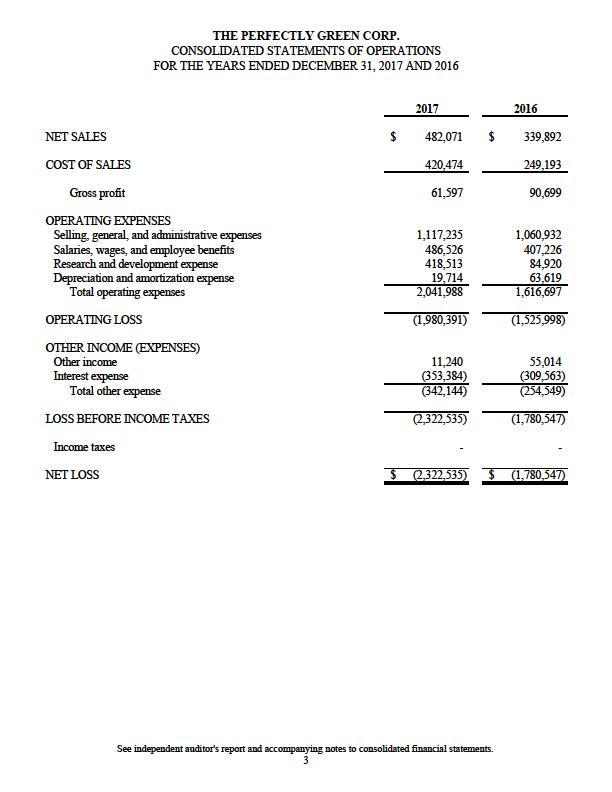

Consolidated Statements of Operations for the years ended December 31, 2017 and 2016 3

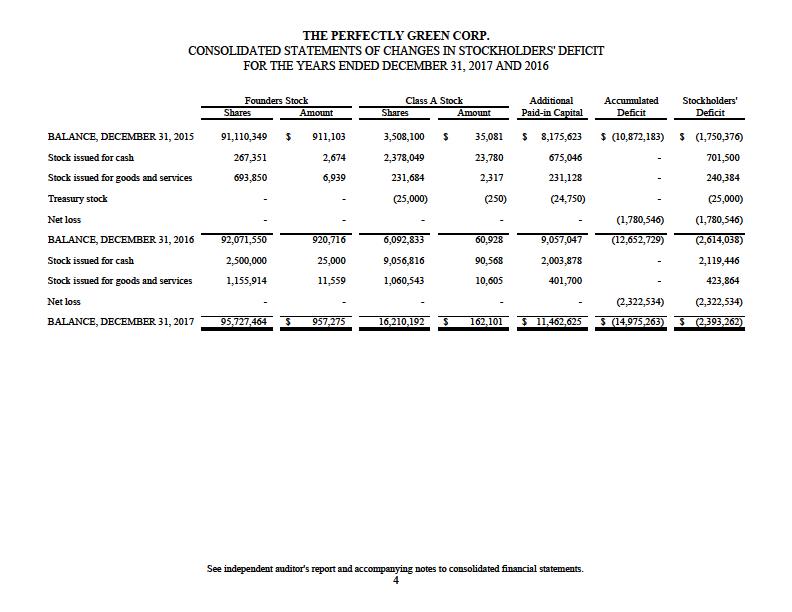

Consolidated Statements of Changes in Stockholders’ Deficit

for the years ended December 31, 2017 and 2016 4

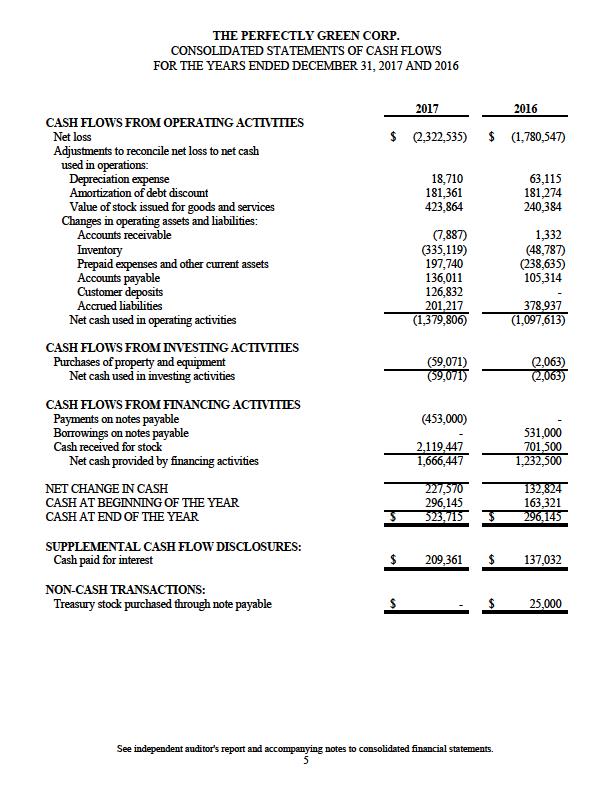

Consolidated Statements of Cash Flows

for the years ended December 31, 2017 and 2016 5

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 6

MONTGOMERY COSCIA GREILICH LLP 972.748.0300 p 972.748.0700 f INDEPENDENT AUDITOR’S REPORT

To the Board of Directors and Stockholders of The Perfectly Green Corp.: We have audited the accompanying consolidated financial statements of The Perfectly Green Corp., which comprise the consolidated balance sheets as of December 31, 2017 and 2016, and the related consolidated statements of operations, changes in stockholders’ deficit, and cash flows for the years then ended, and the related notes to the consolidated financial statements. Management’s Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated balance sheets that are free from material misstatements, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement in the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statement. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the consolidated financial statements referred to above presents fairly, in all material respects, the financial position of The Perfectly Green Corp. as of December 31, 2017 and 2016, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America. Uncertainty Regarding Going Concern The accompanying consolidated financial statements have been prepared assuming that The Perfectly Green Corp. will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, there are substantial doubts about the Company’s ability to continue as a going concern as a result of recurring losses and negative operating cash flows; however, as a result of the announced share exchange agreement (See Note 12), the doubts regarding the going concern could be alleviated. Our opinion is not modified with respect to this matter.

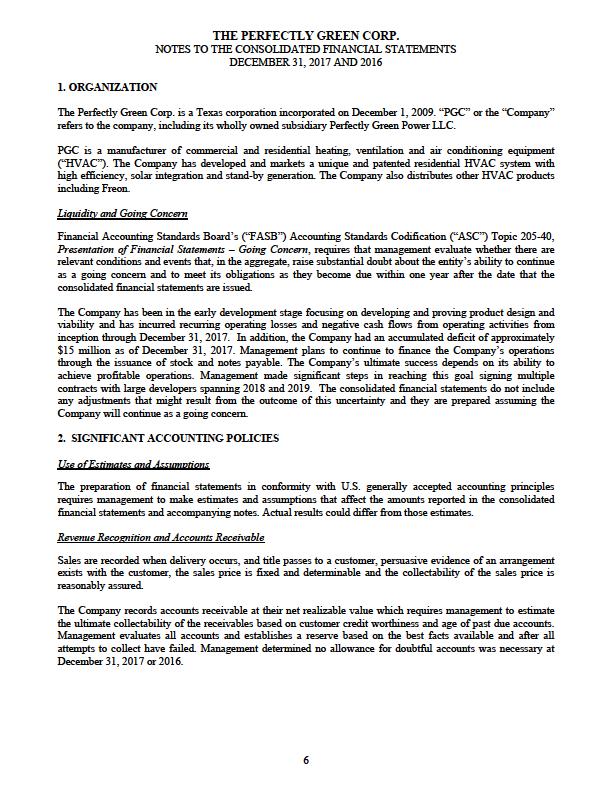

THE PERFECTLY GREEN CORP. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 1. ORGANIZATION

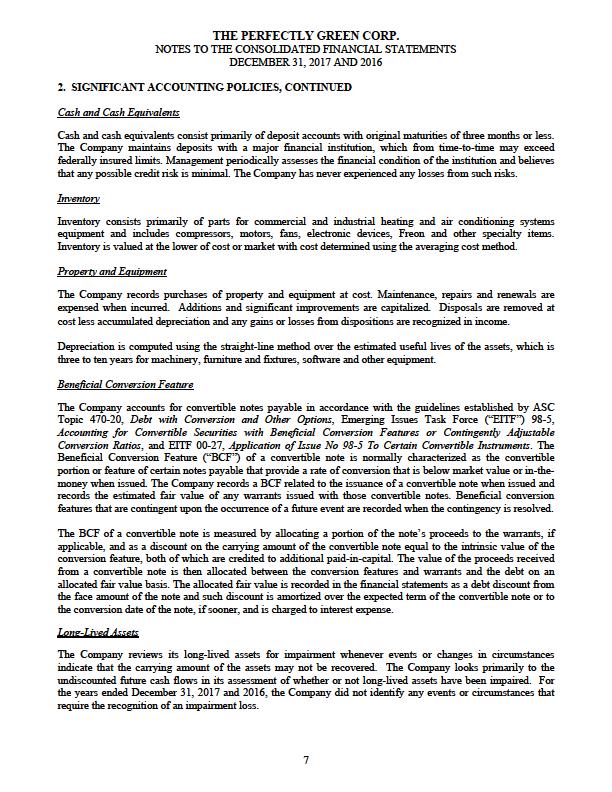

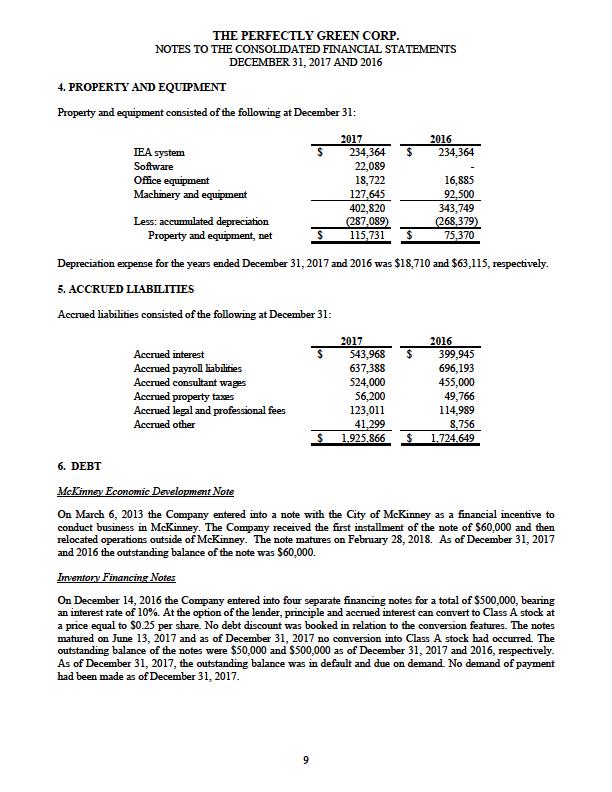

The Perfectly Green Corp. is a Texas corporation incorporated on December 1, 2009. “PGC” or the “Company” refers to the company, including its wholly owned subsidiary Perfectly Green Power LLC. PGC is a manufacturer of commercial and residential heating, ventilation and air conditioning equipment (“HVAC”). The Company has developed and markets a unique and patented residential HVAC system with high efficiency, solar integration and stand-by generation. The Company also distributes other HVAC products including Freon. Liquidity and Going Concern Financial Accounting Standards Board’s (“FASB”) Accounting Standards Codification (“ASC”) Topic 205-40, Presentation of Financial Statements – Going Concern, requires that management evaluate whether there are relevant conditions and events that, in the aggregate, raise substantial doubt about the entity’s ability to continue as a going concern and to meet its obligations as they become due within one year after the date that the consolidated financial statements are issued. The Company has been in the early development stage focusing on developing and proving product design and viability and has incurred recurring operating losses and negative cash flows from operating activities from inception through December 31, 2017. In addition, the Company had an accumulated deficit of approximately $15 million as of December 31, 2017. Management plans to continue to finance the Company’s operations through the issuance of stock and notes payable. The Company’s ultimate success depends on its ability to achieve profitable operations. Management made significant steps in reaching this goal signing multiple contracts with large developers spanning 2018 and 2019. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty and they are prepared assuming the Company will continue as a going concern. 2. SIGNIFICANT ACCOUNTING POLICIES Use of Estimates and Assumptions The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates. Revenue Recognition and Accounts Receivable Sales are recorded when delivery occurs, and title passes to a customer, persuasive evidence of an arrangement exists with the customer, the sales price is fixed and determinable and the collectability of the sales price is reasonably assured. The Company records accounts receivable at their net realizable value which requires management to estimate the ultimate collectability of the receivables based on customer credit worthiness and age of past due accounts. Management evaluates all accounts and establishes a reserve based on the best facts available and after all attempts to collect have failed. Management determined no allowance for doubtful accounts was necessary at December 31, 2017 or 2016. 2. SIGNIFICANT ACCOUNTING POLICIES, CONTINUED Cash and Cash Equivalents Cash and cash equivalents consist primarily of deposit accounts with original maturities of three months or less. The Company maintains deposits with a major financial institution, which from time-to-time may exceed federally insured limits. Management periodically assesses the financial condition of the institution and believes that any possible credit risk is minimal. The Company has never experienced any losses from such risks. Inventory Inventory consists primarily of parts for commercial and industrial heating and air conditioning systems equipment and includes compressors, motors, fans, electronic devices, Freon and other specialty items. Inventory is valued at the lower of cost or market with cost determined using the averaging cost method. Property and Equipment The Company records purchases of property and equipment at cost. Maintenance, repairs and renewals are expensed when incurred. Additions and significant improvements are capitalized. Disposals are removed at cost less accumulated depreciation and any gains or losses from dispositions are recognized in income. Depreciation is computed using the straight-line method over the estimated useful lives of the assets, which is three to ten years for machinery, furniture and fixtures, software and other equipment. Beneficial Conversion Feature The Company accounts for convertible notes payable in accordance with the guidelines established by ASC Topic 470-20, Debt with Conversion and Other Options, Emerging Issues Task Force (“EITF”) 98-5, Accounting for Convertible Securities with Beneficial Conversion Features or Contingently Adjustable Conversion Ratios, and EITF 00-27, Application of Issue No 98-5 To Certain Convertible Instruments. The Beneficial Conversion Feature (“BCF”) of a convertible note is normally characterized as the convertible portion or feature of certain notes payable that provide a rate of conversion that is below market value or in-themoney when issued. The Company records a BCF related to the issuance of a convertible note when issued and records the estimated fair value of any warrants issued with those convertible notes. Beneficial conversion features that are contingent upon the occurrence of a future event are recorded when the contingency is resolved. The BCF of a convertible note is measured by allocating a portion of the note’s proceeds to the warrants, if applicable, and as a discount on the carrying amount of the convertible note equal to the intrinsic value of the conversion feature, both of which are credited to additional paid-in-capital. The value of the proceeds received from a convertible note is then allocated between the conversion features and warrants and the debt on an allocated fair value basis. The allocated fair value is recorded in the financial statements as a debt discount from the face amount of the note and such discount is amortized over the expected term of the convertible note or to the conversion date of the note, if sooner, and is charged to interest expense. Long-Lived Assets The Company reviews its long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be recovered. The Company looks primarily to the undiscounted future cash flows in its assessment of whether or not long-lived assets have been impaired. For the years ended December 31, 2017 and 2016, the Company did not identify any events or circumstances that require the recognition of an impairment loss. 2. SIGNIFICANT ACCOUNTING POLICIES, CONTINUED Stock-Based Transactions The Company periodically issues Class A stock as an incentive to purchasers of its residential and commercial HVAC units in exchange for inventories from vendors. The Company recognizes stock transactions on the date the transactions occurs at their estimated fair values. To measure the fair values of the stock transactions, the Company utilizes the current, or most recent, selling prices of Class A stock. Shipping and Handling Shipping and handling costs are included as a component of cost of sales. Research and Development Expense Research and development costs are expensed as incurred. Advertising The cost of advertising is expensed as incurred. The Company incurred $126,560 and $68,954 for sales and advertising costs for the years ended December 31, 2017 and 2016, respectively. Income Taxes Income taxes are provided based on the liability method, which results in income tax assets and liabilities arising from temporary differences. Temporary differences are differences between the tax basis of assets and liabilities and their reported amounts in the consolidated financial statements that will result in taxable or deductible amounts in future years. The liability method requires the effect of tax rate changes on current and accumulated deferred income taxes to be reflected in the period in which the rate change was enacted. The liability method also requires that deferred tax assets be reduced by a valuation allowance unless it is more likely than not that the assets will be realized. We establish valuation allowances when necessary to reduce deferred tax assets to the amounts expected to be realized. We evaluate the need for, and the adequacy of, valuation allowances based on the expected realization of our deferred tax assets. The factors used to assess the likelihood of realization include historical earnings, our latest forecast of taxable income, and available tax planning strategies that could be implemented to realize the net deferred tax assets. We may recognize a tax benefit from uncertain tax positions only if it is at least more likely than not that the tax position will be sustained upon examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the consolidated financial statements from such a position are measured based on the largest benefit that has a greater than fifty percent likelihood of being realized upon settlement with the taxing authorities. There were no identified tax benefits that were considered uncertain positions at December 31, 2017 or 2016. 3. NOTE RECEIVABLE On December 9, 2014 the Company entered into a $101,500 note receivable with a stockholder of the Company. The principle amount of the note and any unpaid interest shall be due on December 24, 2020. The note bears an interest rate of 10% and at the borrower’s option, the unpaid principle and interest can be converted to Company stock at the current market rate but no less than $0.50 per share. The balance of the note at December 31, 2017 and 2016 was $101,500. Accrued interest receivable was $31,993 and $20,787 as of December 31, 2017 and 2016, respectively, and is included in other current assets in the consolidated balance sheets. 4. PROPERTY AND EQUIPMENT Property and equipment consisted of the following at December 31:

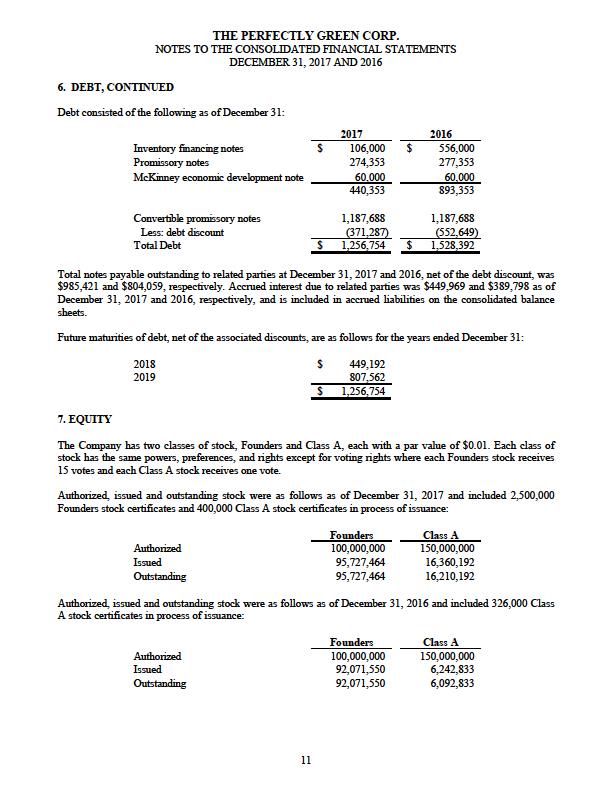

6. DEBT McKinney Economic Development Note On March 6, 2013 the Company entered into a note with the City of McKinney as a financial incentive to conduct business in McKinney. The Company received the first installment of the note of $60,000 and then relocated operations outside of McKinney. The note matures on February 28, 2018. As of December 31, 2017 and 2016 the outstanding balance of the note was $60,000. Inventory Financing Notes On December 14, 2016 the Company entered into four separate financing notes for a total of $500,000, bearing an interest rate of 10%. At the option of the lender, principle and accrued interest can convert to Class A stock at a price equal to $0.25 per share. No debt discount was booked in relation to the conversion features. The notes matured on June 13, 2017 and as of December 31, 2017 no conversion into Class A stock had occurred. The outstanding balance of the notes were $50,000 and $500,000 as of December 31, 2017 and 2016, respectively. As of December 31, 2017, the outstanding balance was in default and due on demand. No demand of payment had been made as of December 31, 2017. 6. DEBT, CONTINUED Inventory Financing Notes, Continued On April 29, 2016 the Company entered into a $56,000 promissory note, bearing an interest rate of 10%. At the option of the lender, principle and accrued interest can convert to Class A stock at a price equal to $0.25 per share. No debt discount was booked in relation to the conversion features. The note matured on July 1, 2016 and the outstanding balance of the note was $56,000 as of December 31, 2017 and 2016. As of December 31, 2017 and 2016, the outstanding balance was in default and due on demand. No demand of payment had been made as of December 31, 2017. Convertible Promissory Notes On June 13, 2013 the Company entered into a promissory note with a stockholder of the Company for $190,179. The note matured on December 31, 2013 and bears an interest rate of 10%. At the option of the lender, principle and accrued interest can convert to Founders stock at a price equal to $0.15 per share. A debt discount of $39,938 was booked at the time of agreement and was fully amortized as of December 31, 2013. The outstanding balance of the note was $190,179 as of December 31, 2017 and 2016. As of December 31, 2017 and 2016, the outstanding balance was in default and due on demand. No demand of payment had been made as of December 31, 2017. On July 14, 2014 the Company entered into an agreement, with a stockholder of the Company, to combine previously held convertible promissory notes and outstanding accrued interest into one convertible promissory note of $997,488. The note matures on December 31, 2019 and bears an interest of 10%. At the option of the lender, principle and accrued interest can convert to Founders stock (or Class A stock if no Founders stock remain in treasury at the time of conversion) at a price equal to $0.15 per share, or 6,649,920 Founders stock as of December 31, 2017 and 2016. A debt discount of $997,488 was booked at the time of agreement and as of December 31, 2017 and 2016 the debt discount was $371,287 and $552,649, respectively. Amortization of the discount for the years ended December 31, 2017 and 2016 was $181,361 and $181,274, respectively, which is included with interest expense in the consolidated statements of operations. Promissory Notes On August 8, 2014, the Company entered into a note agreement with a stockholder of the Company for $75,000. The note bears interest at 10% per annum and had an initial maturity date of August 31, 2014 which was extended in September 2017 to March 31, 2018. On February 26, 2015, the Company entered into a note agreement with a stockholder of the Company for $45,778. The note bears interest at 10% per annum and had an initial maturity date of April 26, 2015 which was extended in September 2017 to March 31, 2018. On January 28, 2016, the Company entered into a note agreement with a stockholder of the Company for $48,243. The note bears interest at 10% per annum and had an initial maturity date of April 28, 2016 which was extended in September 2017 to March 31, 2018. On August 8, 2011, the Company entered two separate loans for $43,333 and $65,000. The notes bear an interest of 1.9% and on August 7, 2016 the notes matured, and the interest rate increased to a default rate of 8%. The outstanding balance of the loans was $105,333 and $108,333 as of December 31, 2017 and 2016, respectively. As of December 31, 2017 and 2016, the outstanding balance was in default and due on demand. No demand of payment had been made as of December 31, 2017. 6. DEBT, CONTINUED Debt consisted of the following as of December 31:

Total notes payable outstanding to related parties at December 31, 2017 and 2016, net of the debt discount, was $985,421 and $804,059, respectively. Accrued interest due to related parties was $449,969 and $389,798 as of December 31, 2017 and 2016, respectively, and is included in accrued liabilities on the consolidated balance sheets.

Future maturities of debt, net of the associated discounts, are as follows for the years ended December 31: 7. EQUITY The Company has two classes of stock, Founders and Class A, each with a par value of $0.01. Each class of stock has the same powers, preferences, and rights except for voting rights where each Founders stock receives 15 votes and each Class A stock receives one vote. Authorized, issued and outstanding stock were as follows as of December 31, 2017 and included 2,500,000 Founders stock certificates and 400,000 Class A stock certificates in process of issuance:

Authorized, issued and outstanding stock were as follows as of December 31, 2016 and included 326,000 Class A stock certificates in process of issuance:

8. INCOME TAXES The Company has experienced net operating losses since its inception. The Company’s management believes it is more likely than not that the net deferred tax assets will not be fully realized based on its operating history. Therefore, the Company has provided a full valuation allowance against deferred tax assets at December 31, 2017 and 2016. At December 31, 2017 and 2016, the Company had accumulated net operating losses totaling approximately $9.2 and $10.2 million, respectively. The net operating loss carry-forwards will begin to expire in future periods if not utilized. There were no significant differences between the United States federal statutory rates and income tax expense except for valuation allowances. At December 31, 2017 and 2016, the Company had no unrecognized tax benefits or accrued interest and penalties related to unrecognized income tax benefits. 9. COMMITMENTS AND CONTINGENCIES The Company is obligated under a non-cancelable operating lease that will expire on December 31, 2020. Future minimum lease payments under operating leases are as follows for the years ended December 31: Rent expense was $121,114 and $134,846 for the years ended December 31, 2017 and 2016, respectively. 10. RELATED PARTY TRANSACTIONS The Company has a note receivable with a stockholder of the Company as disclosed in Note 3. The Company has multiple note payable agreements with stockholders of the Company as disclosed in Note 6. The Company accrued for consultant wages to a related party which are included in accrued liabilities in the consolidated balance sheets and totaled $524,000 and $455,000 at December 31, 2017 and 2016, respectively. 11. LITIGATION The Company is occasionally party to litigation matters in the ordinary course of business. Although the results of the litigation cannot be predicted with certainty, management believes the final outcomes of such matters will not have a material effect on the Company’s position or operations. 12. SUBSEQUENT EVENTS The Company evaluated all material events or transactions that occurred after December 31, 2017, the consolidated balance sheet date, through April 9, 2019, the date these financial statements were issued, and identified the following subsequent events: During 2018, the Company converted and settled certain outstanding notes payable, along with their accrued interest, through stock issuances. On January 20, 2019, the Company entered into a share exchange agreement with Atlantic Acquisition II, Inc. for whereas the Company will exchange 100% of the outstanding Founders and Class A stock for 91% of Atlantic Acquisition II, Inc.