Exhibit 99.1

1 Investor Presentation December 2017 This document does not constitute an offer to sell, nor the solicitation of an offer to purchase, any securities, insurance or investment product . A registration statement on Form S - 1 has been filed with the Securities and Exchange Commission regarding the Company’s initial public offering of common stock, but is not yet effective . No offer or solicitation will be made prior to the effectiveness of the registration statement . The terms and conditions set forth herein are prospective in nature and may vary, possibly substantially, from the terms and conditions of any subsequent offering . The information provided herein was compiled by Advantage Insurance Inc . from sources deemed to be reliable, however no representation or warranty is made with respect to the accuracy or completeness of such information . This document does not purport to contain all of the information that may be relevant . Prospective investors should conduct their own investigation and analysis of the Company and the data set forth in this presentation and other information provided for or on behalf of the Company, and consult their advisors and other qualified persons to verify the accuracy of the information herein . Past performance of Advantage Insurance Inc . , any investment product or investment manager is not indicative of future returns . This document is confidential and may not be reproduced, in whole or in part, without the prior written consent of Advantage Insurance Inc . Neither the Securities and Exchange Commission nor any other state securities commission regulatory body has approved or disapproved of the securities of the Company or passed upon the accuracy or adequacy of this presentation . Any representation to the contrary is a criminal offense . The date of this presentation is December 1 , 2017 .

2 Important Information This presentation and all information being conveyed at the meeting you are attending with certain members of management of Advantage Insurance Inc . (together with its consolidated subsidiaries, “Advantage”), and on behalf of Advantage, representatives of Raymond James & Associates, Inc . is strictly confidential . Prior to this meeting, you agreed to maintain the confidentiality of the information you are receiving at this meeting, which you confirmed via email . Therefore, this presentation and all information you hear or learn at this meeting is subject to your agreement of confidentiality and shall remain strictly confidential in accordance with such agreement . Except as otherwise indicated, this presentation speaks as of the date hereof . The delivery of this presentation shall not, under any circumstances, create any implication that there has been no change in the affairs of Advantage after the date hereof . This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security of Advantage, in any jurisdiction in which it is unlawful for such person to make an offering or solicitation . Certain information contained in this presentation is forward – looking and predictive in nature . Predictive information and forward - looking statements include, but are not limited to, discussions related to Advantage’s expectations about the future direction of the insurance industry, the performance of its business including its investments, its liquidity and capital resources and other speculative statements . These forward - looking statements are not historical facts, and are based on information available to Advantage management, as well as assumptions made by Advantage management . When we use the words “believe,” “anticipate,” “estimate,” “expect,” “intend” and similar expressions in this presentation or the negative version of those words, we are identifying forward - looking statements . Although Advantage management believes that the expectations, projections and potential future events reflected in these forward - looking statements are reasonable, we can give no assurance that these expectations will ultimately prove to be accurate, either eventually or at a precise point in time . The retrospective validity of our forward - looking statements is subject to certain risks, uncertainties and assumptions, including those risks described in “Risk Factors” in Advantage’s registration statement on Form S - 1 filed with the Securities and Exchange Commission . Due to these various risks, uncertainties and assumptions, actual events or the actual financial and operating performance of Advantage may differ materially from those set out in our forward - looking statements . Unless otherwise required by law, we disclaim any obligation to update our view or modify any historical forward - looking statements, risk factors, or other information, whether as a result of new information, future developments or otherwise . Information contained in this presentation includes information about Advantage’s historical operating and financial performance . Past results are not necessarily indicative of future performance, which is dependent upon many factors, most of which are beyond Advantage’s control . The information contained in this presentation is not a guarantee of future performance by Advantage, and actual outcomes and results may differ materially from any historic, pro forma or projected financial results indicated herein . Certain of the financial information contained herein is unaudited . Other financial and operating information is considered non - GAAP financial measures . The Securities and Exchange Commission mandates that non - GAAP financial measures should be considered in addition to and not as a substitute for, or superior to, comparable financial measures presented in accordance with GAAP . Certain financial information included in this presentation is based on estimates developed by Advantage’s management . We believe these estimates are reasonable as of the date of this presentation . These and other estimates made by Advantage management are subject to change and may ultimately prove to be incorrect . The information in this presentation is not all - inclusive and does not contain all information that a financially literate person would reasonably require to properly evaluate Advantage, its business, and future prospects . Advantage does not have any obligation to update this presentation and the information may change at any time without notice . Certain of the information used in preparing this presentation was obtained from third parties or public sources, including GSO Capital Partners International LLP and its affiliates (together, “GSO”) . No representation or warranty, express or implied, is made or given by or on behalf of Advantage or GSO or any other person as to the accuracy, completeness or fairness of such information, and Advantage accepts no responsibility or liability for any such third party or publicly available information . This document is not financial, legal, tax, insurance or investment advice . Any person evaluating Advantage for any commercial purpose should seek out qualified experts to provide financial, legal, tax, insurance and investment advice regarding any commercial relationship or financial transaction with Advantage . Advantage’s principal executive offices are located at American International Plaza, Suite 710 , 250 Muñoz Rivera Avenue, San Juan, Puerto Rico 00918 and its principal internet address is www . advantagelife . com . The information contained in, or accessible through, Advantage’s website is not part of this document . This document is restricted from general distribution and is intended to be used by accredited investors who are prospective purchasers of insurance contracts or services from subsidiaries of Advantage, or securities issued by Advantage .

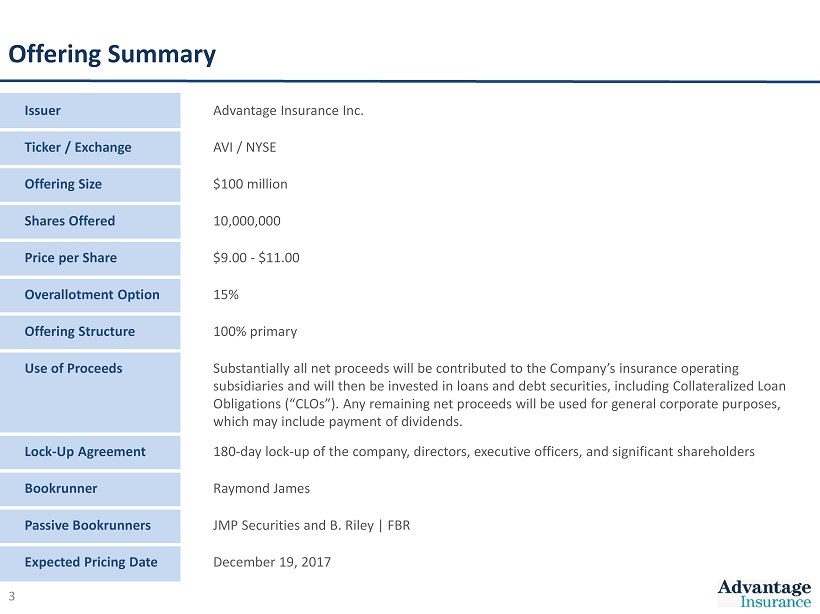

3 Offering Summary Issuer Advantage Insurance Inc. Ticker / Exchange AVI / NYSE Offering Size $100 million Shares Offered 10,000,000 Price per Share $9.00 - $11.00 Overallotment Option 15% Offering Structure 100% primary Use of Proceeds Substantially all net proceeds will be contributed to the Company’s insurance operating subsidiaries and will then be invested in loans and debt securities, including Collateralized Loan Obligations (“ CLOs”). Any remaining net proceeds will be used for general corporate purposes, which may include payment of dividends. Lock - Up Agreement 180 - day lock - up of the company, directors, executive officers, and significant shareholders Bookrunner Raymond James Passive Bookrunners JMP Securities and B. Riley | FBR Expected Pricing Date December 19, 2017

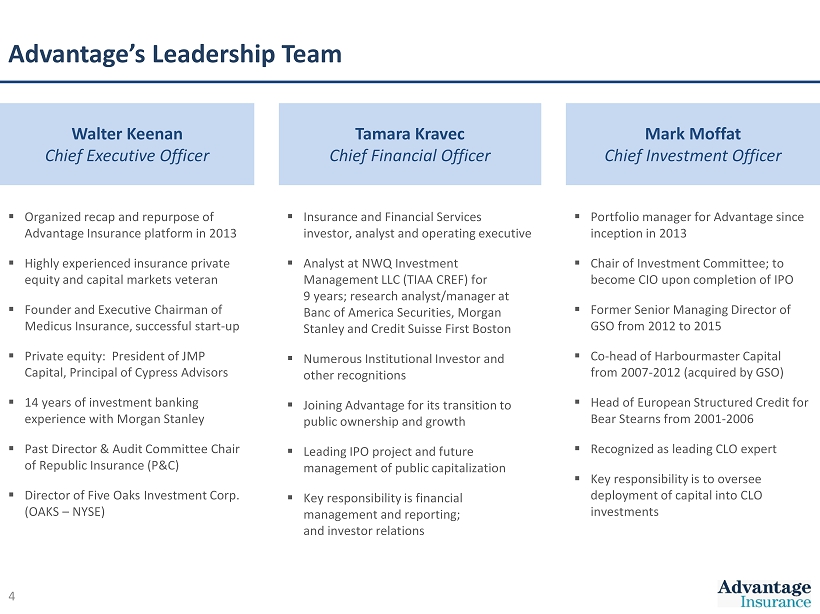

4 Advantage’s Leadership Team Walter Keenan Chief Executive Officer Tamara Kravec Chief Financial Officer Mark Moffat Chief Investment Officer ▪ Organized recap and repurpose of Advantage Insurance platform in 2013 ▪ Highly experienced insurance private equity and capital markets veteran ▪ Founder and Executive Chairman of Medicus Insurance, successful start - up ▪ Private equity: President of JMP Capital, Principal of Cypress Advisors ▪ 14 years of investment banking experience with Morgan Stanley ▪ Past Director & Audit Committee Chair of Republic Insurance (P&C) ▪ Director of Five Oaks Investment Corp. (OAKS – NYSE) ▪ Insurance and Financial Services investor, analyst and operating executive ▪ Analyst at NWQ Investment Management LLC (TIAA CREF) for 9 years; research analyst/manager at Banc of America Securities, Morgan Stanley and Credit Suisse First Boston ▪ Numerous Institutional Investor and other recognitions ▪ Joining Advantage for its transition to public ownership and growth ▪ Leading IPO project and future management of public capitalization ▪ Key responsibility is financial management and reporting; and investor relations ▪ Portfolio manager for Advantage since inception in 2013 ▪ Chair of Investment Committee; to become CIO upon completion of IPO ▪ Former Senior Managing Director of GSO from 2012 to 2015 ▪ Co - head of Harbourmaster Capital from 2007 - 2012 (acquired by GSO) ▪ Head of European Structured Credit for Bear Stearns from 2001 - 2006 ▪ Recognized as leading CLO expert ▪ Key responsibility is to oversee deployment of capital into CLO investments

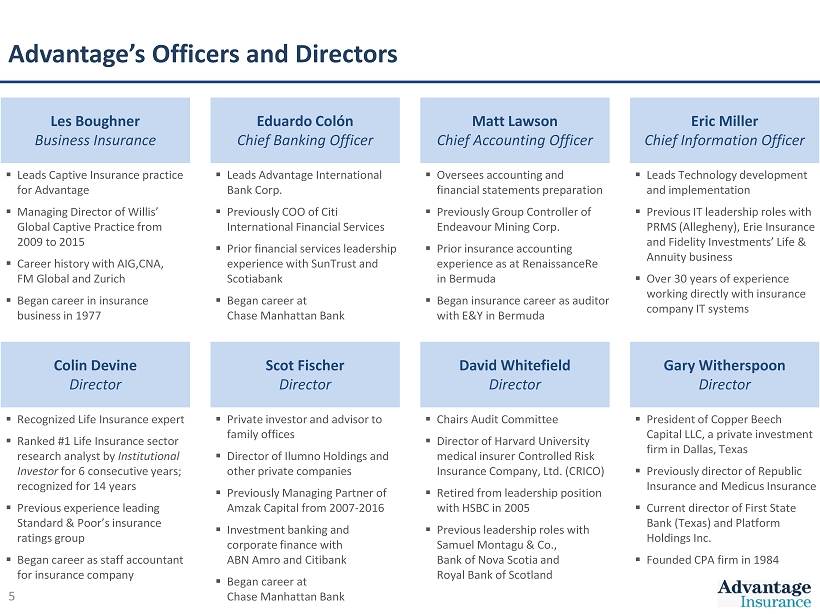

5 Advantage’s Officers and Directors Les Boughner Business Insurance Eduardo Colón Chief Banking Officer Matt Lawson Chief Accounting Officer Eric Miller Chief Information Officer ▪ Leads Captive Insurance practice for Advantage ▪ Managing Director of Willis’ Global Captive Practice from 2009 to 2015 ▪ Career history with AIG,CNA, FM Global and Zurich ▪ Began career in insurance business in 1977 ▪ Leads Advantage International Bank Corp. ▪ Previously COO of Citi International Financial Services ▪ Prior financial services leadership experience with SunTrust and Scotiabank ▪ Began career at Chase Manhattan Bank ▪ Oversees accounting and financial statements preparation ▪ Previously Group Controller of Endeavour Mining Corp. ▪ Prior insurance accounting experience as at RenaissanceRe in Bermuda ▪ Began insurance career as auditor with E&Y in Bermuda ▪ Leads Technology development and implementation ▪ Previous IT leadership roles with PRMS (Allegheny), Erie Insurance and Fidelity Investments’ Life & Annuity business ▪ Over 30 years of experience working directly with insurance company IT systems Colin Devine Director Scot Fischer Director David Whitefield Director Gary Witherspoon Director ▪ Recognized Life Insurance expert ▪ Ranked #1 Life Insurance sector research analyst by Institutional Investor for 6 consecutive years; recognized for 14 years ▪ Previous experience leading Standard & Poor’s insurance ratings group ▪ Began career as staff accountant for insurance company ▪ Private investor and advisor to family offices ▪ Director of Ilumno Holdings and other private companies ▪ Previously Managing Partner of Amzak Capital from 2007 - 2016 ▪ Investment banking and corporate finance with ABN Amro and Citibank ▪ Began career at Chase Manhattan Bank ▪ Chairs Audit Committee ▪ Director of Harvard University medical insurer Controlled Risk Insurance Company, Ltd. (CRICO) ▪ Retired from leadership position with HSBC in 2005 ▪ Previous leadership roles with Samuel Montagu & Co., Bank of Nova Scotia and Royal Bank of Scotland ▪ President of Copper Beech Capital LLC, a private investment firm in Dallas, Texas ▪ Previously director of Republic Insurance and Medicus Insurance ▪ Current director of First State Bank (Texas) and Platform Holdings Inc. ▪ Founded CPA firm in 1984

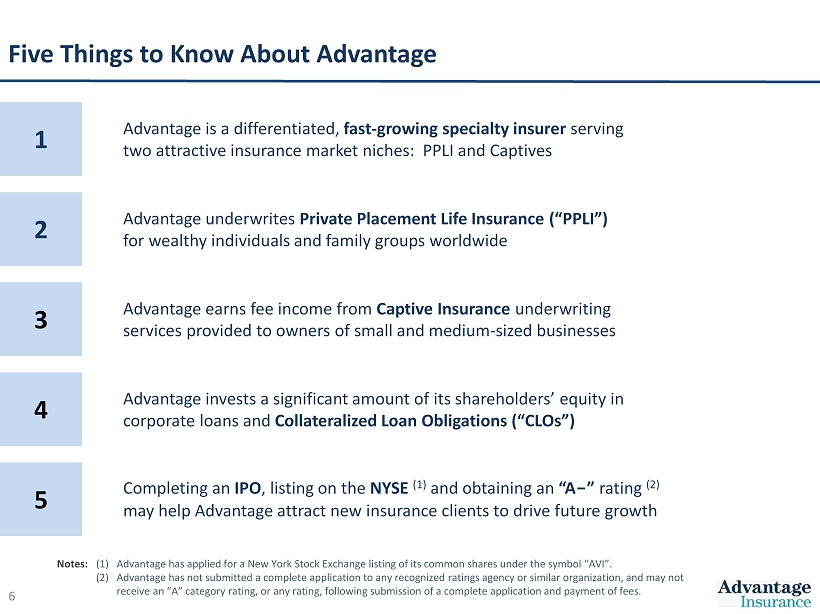

6 Five Things to Know About Advantage 1 Advantage is a differentiated, fast - growing specialty insurer serving two attractive insurance market niches: PPLI and Captives 2 Advantage underwrites Private Placement Life Insurance (“PPLI”) for wealthy individuals and family groups worldwide 3 Advantage earns fee income from Captive Insurance underwriting services provided to owners of small and medium - sized businesses 4 Advantage invests a significant amount of its shareholders’ equity in corporate loans and Collateral ized Loan Obligation s (“CLOs”) 5 Completing an IPO , listing on the NYSE (1) and obtaining an “A - ” rating (2) may help Advantage attract new insurance clients to drive future growth Notes: (1) Advantage has applied for a New York Stock Exchange listing of its common shares under the symbol “AVI”. (2) Advantage has not submitted a complete application to any recognized ratings agency or similar organization, and may not receive an “A” category rating, or any rating, following submission of a complete application and payment of fees.

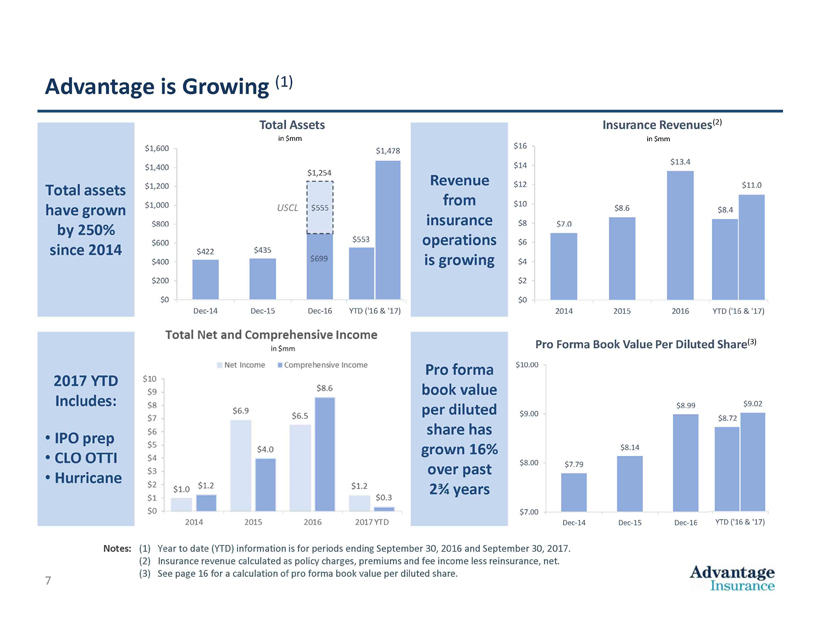

7 $7.79 $8.14 $8.99 $9.02 $7.00 $8.00 $9.00 $10.00 Dec-14 Dec-15 Dec-16 9/30/17 Pro Forma Book Value Per Diluted Share $7.0 $8.6 $13.4 $11.0 $0 $2 $4 $6 $8 $10 $12 $14 $16 2014 2015 2016 2017 YTD Insurance Revenues in $mm $422 $435 $699 $1,478 $555 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 Dec-14 Dec-15 Dec-16 9/30/17 Total Assets in $mm USCL $1,254 $553 $1,478 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 Dec-14 Dec-15 Dec-16 YTD ('16 & '17) Total Assets in $mm USCL $1,254 Advantage is Growing (1) Revenue from insurance operations is growing Pro forma book value p er d iluted s hare has grown 16% over past 2¾ years 2017 YTD Includes: • IPO prep • CLO OTTI • Hurricane Total assets have grown by 250% since 2014 (2) Notes: (1) Year to date (YTD) information is for periods ending September 30, 2016 and September 30, 2017. (2) Insurance revenue calculated as policy charges, premiums and fee income less reinsurance, net. (3) See page 16 for a calculation of pro forma book value per diluted share. $8.4 $11.0 $0 $2 $4 $6 $8 $10 $12 $14 $16 2014 2015 2016 YTD ('16 & '17) Insurance Revenues in $mm $8.72 $9.02 $7.00 $8.00 $9.00 $10.00 Dec-14 Dec-15 Dec-16 YTD ('16 & '17) Pro Forma Book Value Per Diluted Share (3)

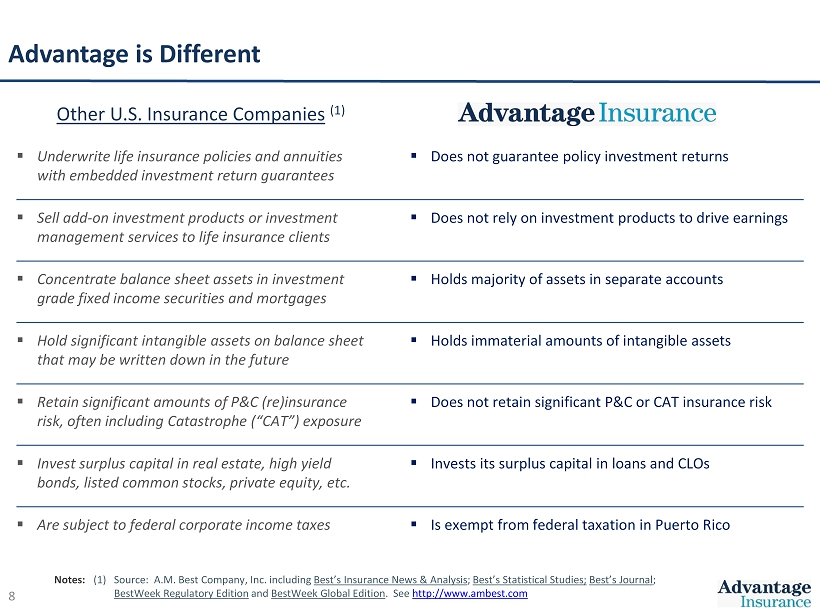

8 Advantage is Different Other U.S. Insurance Companies (1) ▪ Underwrite life insurance policies and annuities with embedded investment return guarantees ▪ Does not guarantee policy investment returns ▪ Sell add - on investment products or investment management services to life insurance clients ▪ Does not rely on investment products to drive earnings ▪ Concentrate balance sheet assets in investment grade fixed income securities and mortgages ▪ Holds majority of assets in separate accounts ▪ Hold significant intangible assets on balance sheet that may be written down in the future ▪ Holds immaterial amounts of intangible assets ▪ Retain significant amounts of P&C (re)insurance risk, often including Catastrophe (“CAT”) exposure ▪ Does not retain significant P&C or CAT insurance risk ▪ Invest surplus capital in real estate, high yield bonds, listed common stocks, private equity, etc. ▪ Invests its surplus capital in loans and CLOs ▪ Are subject to federal corporate income taxes ▪ Is exempt from federal taxation in Puerto Rico Notes: (1) Source: A.M. Best Company, Inc. including Best’s Insurance News & Analysis ; Best’s Statistical Studies; Best’s Journal ; BestWeek Regulatory Edition and BestWeek Global Edition . See http://www.ambest.com

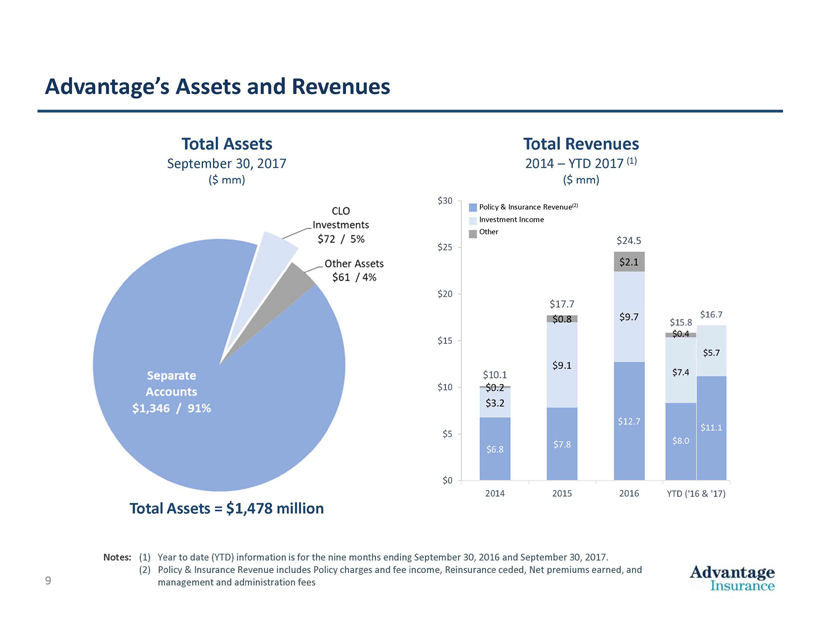

9 Advantage’s Assets and Revenues Notes: (1) Year to date (YTD) information is for the nine months ending September 30, 2016 and September 30, 2017. (2) Policy & Insurance Revenue includes Policy charges and fee income, Reinsurance ceded, Net premiums earned, and management and administration fees $6.8 $7.8 $12.7 $8.0 $3.2 $9.1 $9.7 $7.4 $0.2 $0.8 $2.1 $0.4 $10.1 $17.7 $24.5 $15.8 $0 $5 $10 $15 $20 $25 $30 2014 2015 2016 2016 YTD Total Revenues in $mm $15.8 $16.7 $0 $5 $10 $15 $20 $25 $30 2014 2015 2016 YTD ('16 & '17) Insurance Revenues in $mm $0.4 $8.0 $11.1 $5.7 $7.4 Policy & Insurance Revenue (2) Investment Income Other Total Assets = $1,478 million Total Assets September 30, 2017 ($ mm) Total Revenues 2014 – YTD 2017 (1) ($ mm)

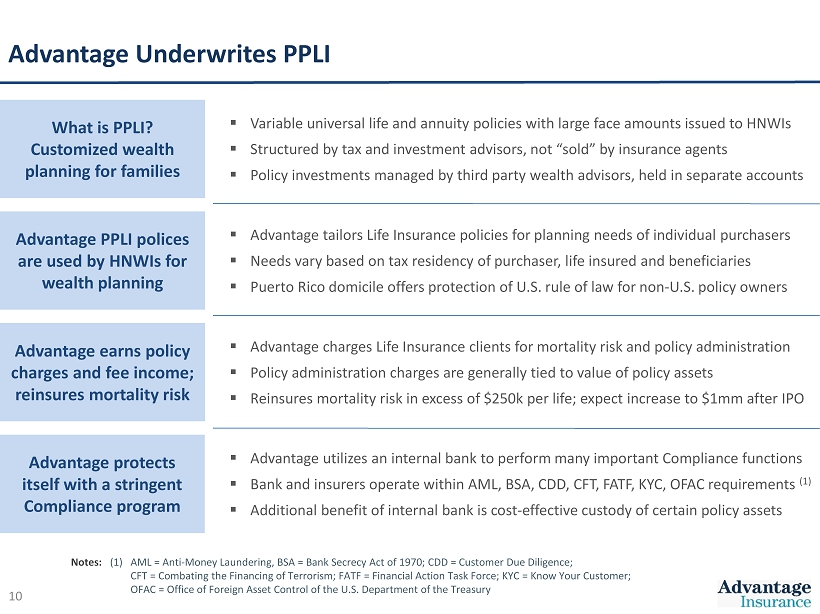

10 Advantage Underwrites PPLI What is PPLI? Customized wealth planning for families Advantage earns policy charges and fee income; reinsures mortality risk Advantage protects itself with a stringent Compliance program ▪ Variable universal life and annuity policies with large face amounts issued to HNWIs ▪ Structured by tax and investment advisors, not “sold” by insurance agents ▪ Policy investments managed by third party wealth advisors, held in separate accounts Advantage PPLI polices are used by HNWIs for wealth planning ▪ Advantage charges Life Insurance clients for mortality risk and policy administration ▪ Policy administration charges are generally tied to value of policy assets ▪ Reinsures mortality risk in excess of $250k per life; expect increase to $1mm after IPO ▪ Advantage utilizes an internal bank to perform many important Compliance functions ▪ Bank and insurers operate within AML, BSA, CDD, CFT, FATF, KYC, OFAC requirements (1) ▪ Additional benefit of internal bank is cost - effective custody of certain policy assets ▪ Advantage tailors Life Insurance policies for planning needs of individual purchasers ▪ Needs vary based on tax residency of purchaser, life insured and beneficiaries ▪ Puerto Rico domicile offers protection of U.S. rule of law for non - U.S. policy owners Notes: (1) AML = Anti - Money Laundering, BSA = Bank Secrecy Act of 1970; CDD = Customer Due Diligence; CFT = Combating the Financing of Terrorism; FATF = Financial Action Task Force; KYC = Know Your Customer; OFAC = Office of Foreign Asset Control of the U.S. Department of the Treasury

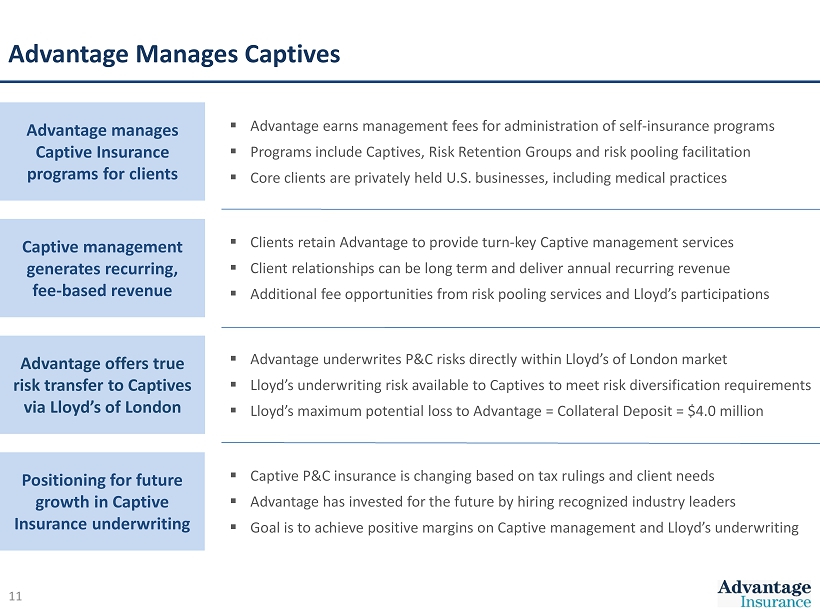

11 Advantage Manages Captives Advantage manages Captive Insurance programs for clients Advantage offers true risk transfer to Captives via Lloyd’s of London Positioning for future growth in Captive Insurance underwriting ▪ Advantage earns management fees for administration of self - insurance programs ▪ Programs include Captives, Risk Retention Groups and risk pooling facilitation ▪ Core clients are privately held U.S. businesses, including medical practices Captive management generates recurring, fee - based revenue ▪ Advantage underwrites P&C risks directly within Lloyd’s of London market ▪ Lloyd’s underwriting risk available to Captives to meet risk diversification requirements ▪ Lloyd’s maximum potential loss to Advantage = Collateral Deposit = $4.0 million ▪ Captive P&C insurance is changing based on tax rulings and client needs ▪ Advantage has invested for the future by hiring recognized industry leaders ▪ Goal is to achieve positive margins on Captive management and Lloyd’s underwriting ▪ Clients retain Advantage to provide turn - key Captive management services ▪ Client relationships can be long term and deliver annual recurring revenue ▪ Additional fee opportunities from risk pooling services and Lloyd’s participations

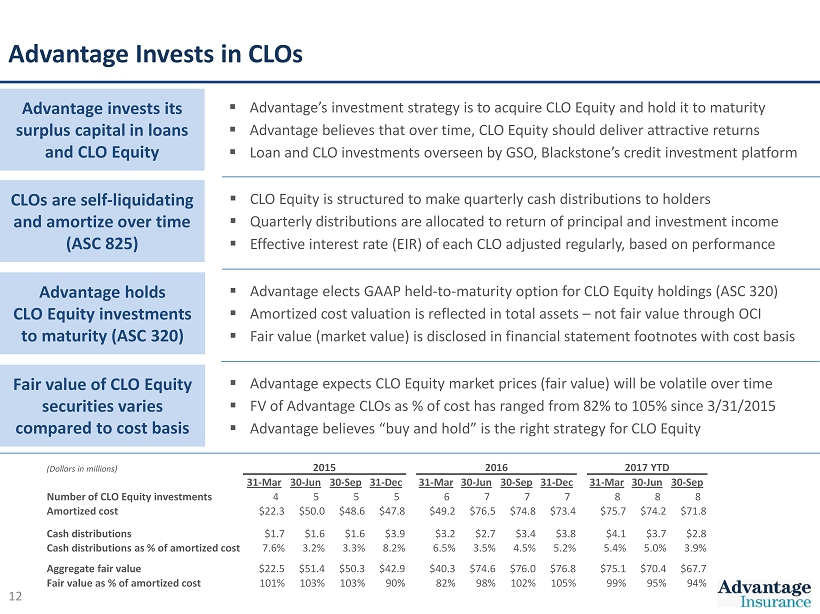

12 Advantage Invests in CLOs Fair value of CLO Equity securities varies compared to cost basis Advantage invests its surplus capital in loans and CLO Equity ▪ Advantage expects CLO Equity market prices (fair value) will be volatile over time ▪ FV of Advantage CLOs as % of cost has ranged from 82% to 105% since 3/31/2015 ▪ Advantage believes “buy and hold” is the right strategy for CLO Equity ▪ Advantage’s investment strategy is to acquire CLO Equity and hold it to maturity ▪ Advantage believes that over time, CLO Equity should deliver attractive returns ▪ Loan and CLO investments overseen by GSO, Blackstone’s credit investment platform Advantage holds CLO Equity investments to maturity (ASC 320) ▪ Advantage elects GAAP held - to - maturity option for CLO Equity holdings (ASC 320) ▪ Amortized cost valuation is reflected in total assets – not fair value through OCI ▪ Fair value (market value) is disclosed in financial statement footnotes with cost basis CLOs are self - liquidating and amortize over time (ASC 825) ▪ CLO Equity is structured to make quarterly cash distributions to holders ▪ Quarterly distributions are allocated to return of principal and investment income ▪ Effective interest rate (EIR) of each CLO adjusted regularly, based on performance (Dollars in millions) 2015 2016 2017 YTD 31 - Mar 30 - Jun 30 - Sep 31 - Dec 31 - Mar 30 - Jun 30 - Sep 31 - Dec 31 - Mar 30 - Jun 30 - Sep Number of CLO Equity investments 4 5 5 5 6 7 7 7 8 8 8 Amortized cost $22.3 $50.0 $48.6 $47.8 $49.2 $76.5 $74.8 $73.4 $75.7 $74.2 $71.8 Cash distributions $1.7 $1.6 $1.6 $3.9 $3.2 $2.7 $3.4 $3.8 $4.1 $3.7 $2.8 Cash distributions as % of amortized cost 7.6% 3.2% 3.3% 8.2% 6.5% 3.5% 4.5% 5.2% 5.4% 5.0% 3.9% Aggregate fair value $22.5 $51.4 $50.3 $42.9 $40.3 $74.6 $76.0 $76.8 $75.1 $70.4 $67.7 Fair value as % of amortized cost 101% 103% 103% 90% 82% 98% 102% 105% 99% 95% 94%

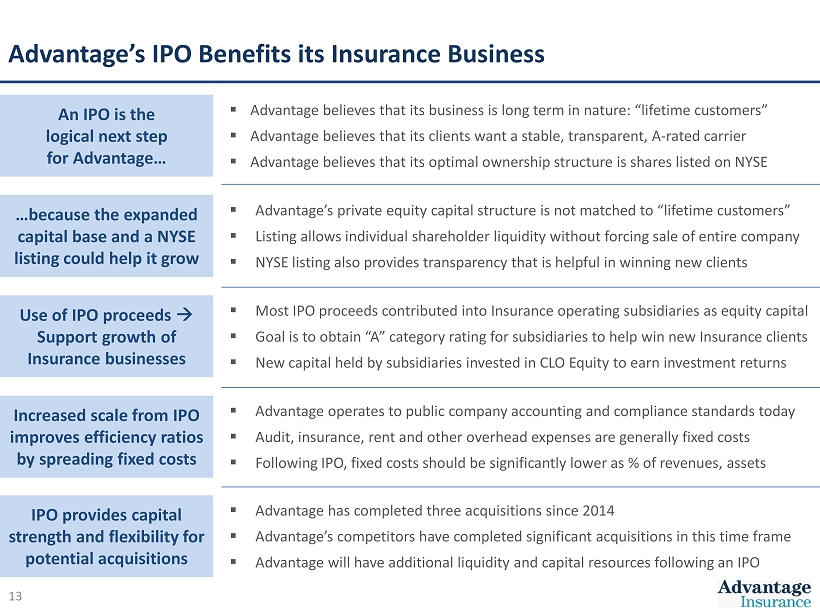

13 Advantage’s IPO Benefits its Insurance Business …because the expanded capital base and a NYSE listing could help it grow An IPO is the logical next step for Advantage… Use of IPO proceeds Support growth of Insurance businesses ▪ Advantage believes that its business is long term in nature: “lifetime customers” ▪ Advantage believes that its clients want a stable, transparent, A - rated carrier ▪ Advantage believes that its optimal ownership structure is shares listed on NYSE Increased scale from IPO improves efficiency ratios by spreading fixed costs ▪ Advantage’s private equity capital structure is not matched to “lifetime customers” ▪ Listing allows individual shareholder liquidity without forcing sale of entire company ▪ NYSE listing also provides transparency that is helpful in winning new clients ▪ Most IPO proceeds contributed into Insurance operating subsidiaries as equity capital ▪ Goal is to obtain “A” category rating for subsidiaries to help win new Insurance clients ▪ New capital held by subsidiaries invested in CLO Equity to earn investment returns ▪ Advantage operates to public company accounting and compliance standards today ▪ Audit, insurance, rent and other overhead expenses are generally fixed costs ▪ Following IPO, fixed costs should be significantly lower as % of revenues, assets IPO provides capital strength and flexibility for potential acquisitions ▪ Advantage has completed three acquisitions since 2014 ▪ Advantage’s competitors have completed significant acquisitions in this time frame ▪ Advantage will have additional liquidity and capital resources following an IPO

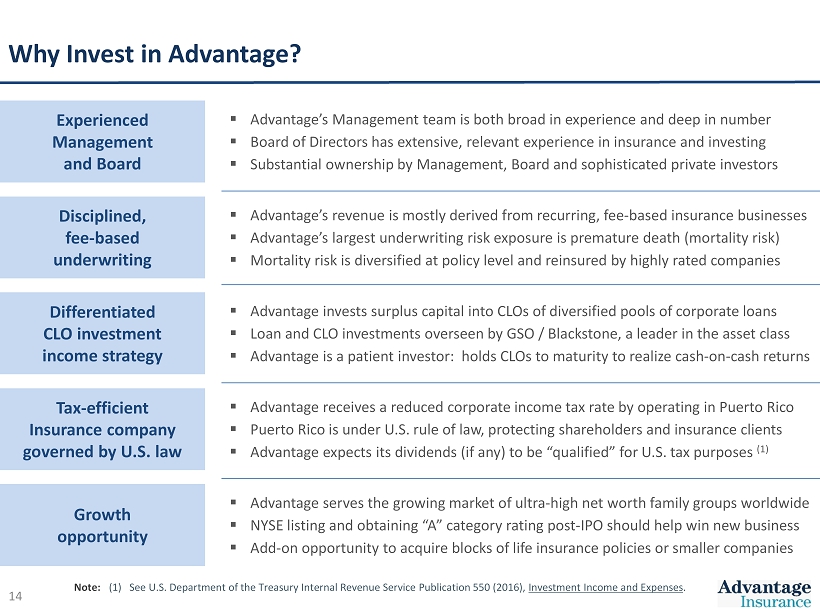

14 Why Invest in Advantage? Disciplined, fee - based underwriting Tax - efficient Insurance company governed by U.S. law Growth opportunity ▪ Advantage’s revenue is mostly derived from recurring, fee - based insurance businesses ▪ Advantage’s largest underwriting risk exposure is premature death (mortality risk) ▪ Mortality risk is diversified at policy level and reinsured by highly rated companies Differentiated CLO investment income strategy ▪ Advantage receives a reduced corporate income tax rate by operating in Puerto Rico ▪ Puerto Rico is under U.S. rule of law, protecting shareholders and insurance clients ▪ Advantage expects its dividends (if any) to be “qualified” for U.S. tax purposes (1) ▪ Advantage serves the growing market of ultra - high net worth family groups worldwide ▪ NYSE listing and obtaining “A” category rating post - IPO should help win new business ▪ Add - on opportunity to acquire blocks of life insurance policies or smaller companies ▪ Advantage invests surplus capital into CLOs of diversified pools of corporate loans ▪ Loan and CLO investments overseen by GSO / Blackstone, a leader in the asset class ▪ Advantage is a patient investor: holds CLOs to maturity to realize cash - on - cash returns Experienced Management and Board ▪ Advantage’s Management team is both broad in experience and deep in number ▪ Board of Directors has extensive, relevant experience in insurance and investing ▪ Substantial ownership by Management, Board and sophisticated private investors Note: (1) See U.S. Department of the Treasury Internal Revenue Service Publication 550 (2016), Investment Income and Expenses .

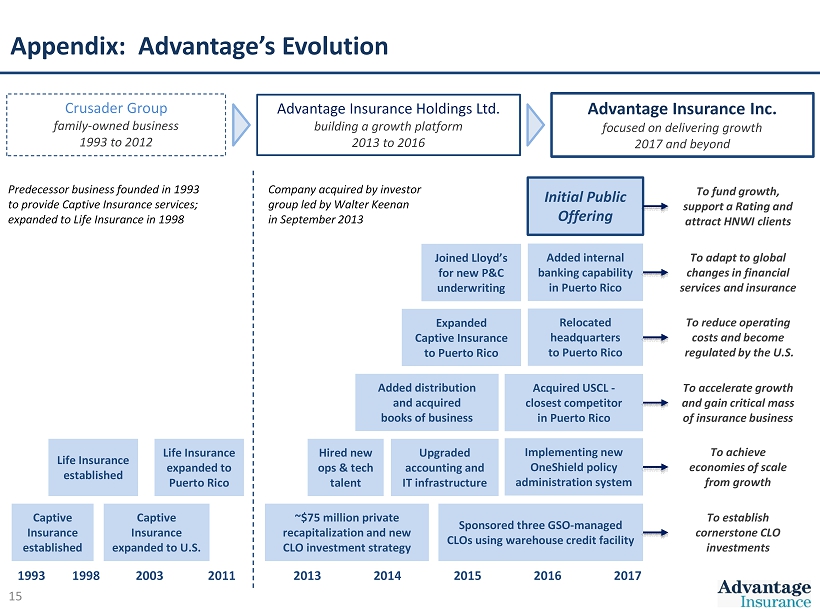

15 Appendix: Advantage’s Evolution Captive Insurance expanded to U.S. Captive Insurance established Crusader Group family - owned business 1993 to 2012 Advantage Insurance Holdings Ltd. building a growth platform 2013 to 2016 Advantage Insurance Inc. focused on delivering growth 2017 and beyond Hired new ops & tech talent Expanded Captive Insurance to Puerto Rico Implementing new OneShield policy administration system Acquired USCL - closest competitor in Puerto Rico Added internal banking capability in Puerto Rico Sponsored three GSO - managed CLOs using warehouse credit facility Initial Public Offering ~$75 million private recapitalization and new CLO investment strategy Added distribution and acquired books of business Upgraded accounting and IT infrastructure Relocated headquarters to Puerto Rico To fund growth, support a Rating and attract HNWI clients To adapt to global changes in financial services and insurance To reduce operating costs and become regulated by the U.S. To accelerate growth and gain critical mass of insurance business To achieve economies of scale from growth To establish cornerstone CLO investments Company acquired by investor group led by Walter Keenan in September 2013 Predecessor business founded in 1993 to provide Captive Insurance services; expanded to Life Insurance in 1998 1993 2003 1998 2011 2013 2017 2014 2015 2016 Joined Lloyd’s for new P&C underwriting Life Insurance established Life Insurance expanded to Puerto Rico

16 Appendix: Summary Balance Sheet and Income Statement ($000, except per share) At or For the Nine Months At or For the Years Ended December 31, Ended September 30, 2014 2015 2016 2016 2017 Income Statement Data: Revenue 10,127$ 17,737$ 24,539$ 15,810$ 16,675$ Investment Income 3,168 9,140 9,709 7,383 5,686 Net Income 951 6,866 6,482 3,924 1,192 Other comprehensive (loss) / income 294 (2,882) 2,125 2,051 (875) Total comprehensive income 1,245 3,984 8,607 5,975 317 Balance Sheet Data: Total assets 422,297$ 435,275$ 1,253,737$ 552,750$ 1,478,278$ Separate account assets 330,681 337,803 1,114,849 446,516 1,345,892 Other assets 11,970 19,238 55,165 27,929 54,703 Investments and cash 79,776 78,234 83,723 78,305 77,683 Total shareholders' equity 81,922 86,040 93,513 89,064 93,261 Per Share Data: Basic earnings per common share 1.99$ 16.89$ 18.18$ 10.74$ 3.69$ Diluted earnings per common share 0.11 0.73 0.66 0.40 0.11 Weighted average common shares outstanding 478,316 406,428 356,467 365,199 323,386 Diluted average common shares outstanding 8,686,316 9,352,747 9,867,467 9,704,885 10,405,326

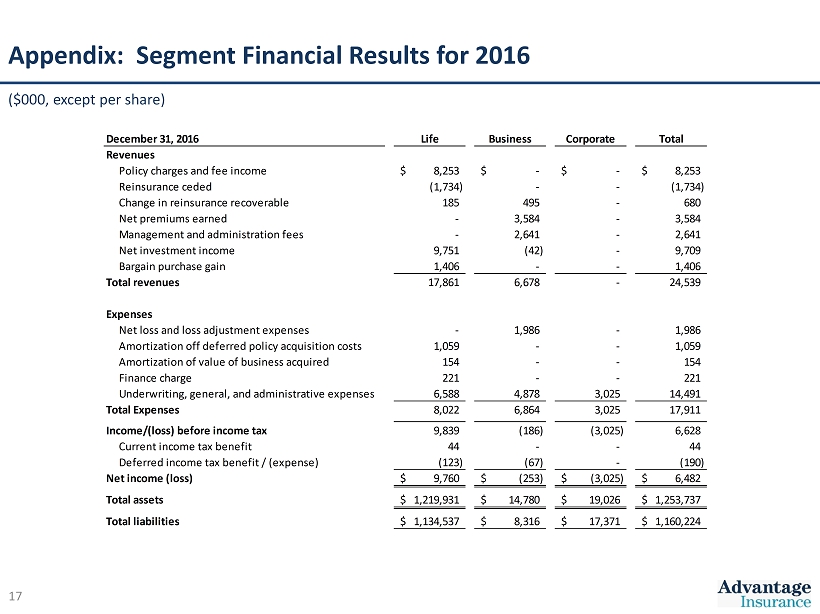

17 Appendix: Segment Financial Results for 2016 ($000, except per share) December 31, 2016 Life Business Corporate Total Revenues Policy charges and fee income 8,253$ -$ -$ 8,253$ Reinsurance ceded (1,734) - - (1,734) Change in reinsurance recoverable 185 495 - 680 Net premiums earned - 3,584 - 3,584 Management and administration fees - 2,641 - 2,641 Net investment income 9,751 (42) - 9,709 Bargain purchase gain 1,406 - - 1,406 Total revenues 17,861 6,678 - 24,539 Expenses Net loss and loss adjustment expenses - 1,986 - 1,986 Amortization off deferred policy acquisition costs 1,059 - - 1,059 Amortization of value of business acquired 154 - - 154 Finance charge 221 - - 221 Underwriting, general, and administrative expenses 6,588 4,878 3,025 14,491 Total Expenses 8,022 6,864 3,025 17,911 Income/(loss) before income tax 9,839 (186) (3,025) 6,628 Current income tax benefit 44 - - 44 Deferred income tax benefit / (expense) (123) (67) - (190) Net income (loss) 9,760$ (253)$ (3,025)$ 6,482$ Total assets 1,219,931$ 14,780$ 19,026$ 1,253,737$ Total liabilities 1,134,537$ 8,316$ 17,371$ 1,160,224$

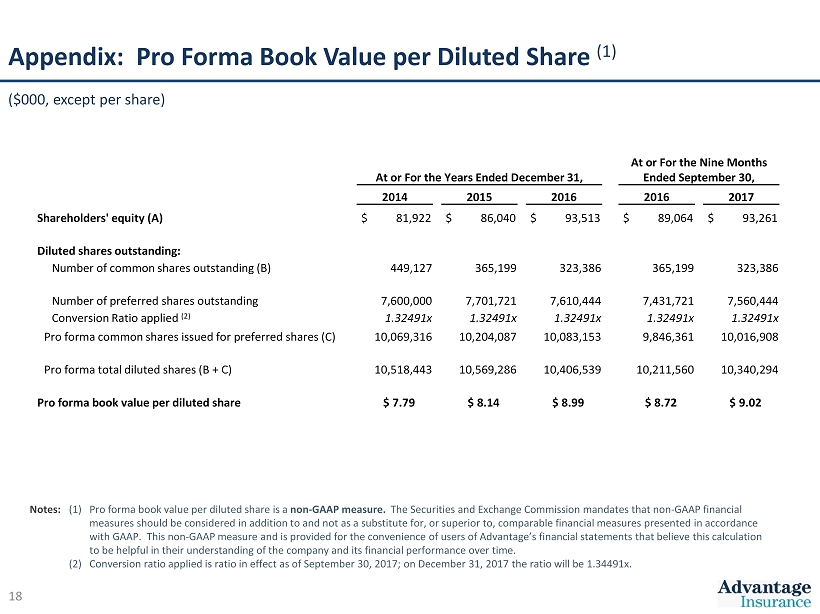

18 At or For the Years Ended December 31, At or For the Nine Months Ended September 30, 2014 2015 2016 2016 2017 Shareholders' equity (A) $ 81,922 $ 86,040 $ 93,513 $ 89,064 $ 93,261 Diluted shares outstanding: Number of common shares outstanding (B) 449,127 365,199 323,386 365,199 323,386 Number of preferred shares outstanding 7,600,000 7,701,721 7,610,444 7,431,721 7,560,444 Conversion Ratio applied (2) 1.32491x 1.32491x 1.32491x 1.32491x 1.32491x Pro forma common shares issued for preferred shares (C) 10,069,316 10,204,087 10,083,153 9,846,361 10,016,908 Pro forma total diluted shares (B + C) 10,518,443 10,569,286 10,406,539 10,211,560 10,340,294 Pro forma book value per diluted share $ 7.79 $ 8.14 $ 8.99 $ 8.72 $ 9.02 Appendix: Pro Forma Book Value per Diluted Share (1) Notes: (1) Pro forma book value per diluted share is a non - GAAP measure. The Securities and Exchange Commission mandates that non-GAAP financial measures should be considered in addition to and not as a substitute for, or superior to, comparable financial measures prese nte d in accordance with GAAP. This non - GAAP measure and is provided for the convenience of users of Advantage’s financial statements that believe this calculation to be helpful in their understanding of the company and its financial performance over time. (2) Conversion ratio applied is ratio in effect as of September 30, 2017; on December 31, 2017 the ratio will be 1.34491x. ($000, except per share)