Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2018

Commission file number:001-38333

ESTRE AMBIENTAL, INC.

(Exact name of Registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

4509, Avenida Brigadeiro Faria Lima, 8th Floor

04538-133 São Paulo, SP, Brazil

(Address of principal executive offices)

Felipe Rodriguez, Interim Chief Financial Officer

4509, Avenida Brigadeiro Faria Lima, 8th Floor

04538-133 São Paulo, SP, Brazil

Telephone No.: +55 11 2124-3265

e-mail: ir@estre.com.br

(Name, Telephone,E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which | ||

| Ordinary shares, par value $0.0001 per share | ESTR | NASDAQ Capital Market | ||

| Warrants | ESTRW | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2018, the Registrant had:

45,636,732 ordinary shares issued and outstanding, par value $0.0001 per share.

5,550,000 Class B Shares issued and outstanding, par value $0.0001 per share.

27,916,921 outstanding warrants exercisable on aone-for-one basis for ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes☐ No☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes☐ No☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes☐ No☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of RegulationS-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes☒ No☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, anon-accelerated filer, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, and “emerging growth company” in Rule12b-2 of the Exchange Act.

| Large accelerated filer☐ | Accelerated filer☐ | Non-accelerated filer☒ | Emerging growth company☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. N/A

Item 17☐ Item 18☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule12b-2 of the Exchange Act).

Yes☐ No☒

Table of Contents

| Page | ||||

| 1 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

| 7 | ||||

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 7 | |||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 47 | ||||

| 47 | ||||

| 53 | ||||

| 70 | ||||

| 71 | ||||

| 71 | ||||

| 72 | ||||

| 72 | ||||

| 100 | ||||

| 105 | ||||

| 106 | ||||

| 111 | ||||

F. Commitments and Contingencies (Tabular Disclosure of Contractual Obligations) | 111 | |||

| 111 | ||||

| 111 | ||||

| 111 | ||||

| 114 | ||||

| 116 | ||||

| 118 | ||||

| 119 | ||||

| 119 | ||||

| 119 | ||||

| 122 | ||||

| 125 | ||||

| 125 | ||||

| 125 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

i

Table of Contents

| Page | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 144 | ||||

D. Exchange Controls and other Limitations Affecting Security Holders | 147 | |||

| 148 | ||||

| 153 | ||||

| 153 | ||||

| 153 | ||||

| 154 | ||||

ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 154 | |||

ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 156 | |||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| 157 | ||||

| 157 | ||||

ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 158 | |||

| 158 | ||||

| 158 | ||||

B. Management’s Annual Report on Internal Control Over Financial Reporting | 158 | |||

C. Attestation Report of the Registered Public Accounting Firm | 160 | |||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| 161 | ||||

ITEM 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 161 | |||

ITEM 16E. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 161 | |||

| 162 | ||||

| 162 | ||||

| 162 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

ii

Table of Contents

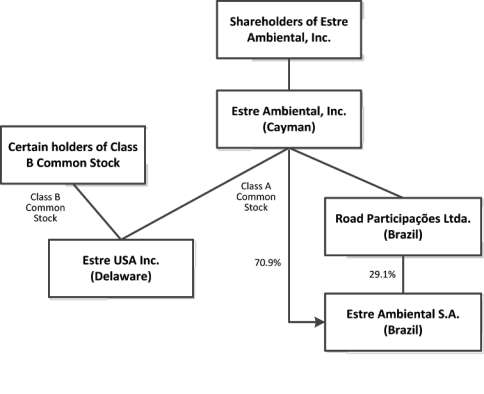

In this annual report, except as otherwise indicated or as the context otherwise requires, “Estre,” “we,” “us” and “our” refers to Estre Ambiental, Inc. and its subsidiaries on a consolidated basis, including Estre Ambiental S.A., Estre’s main operating subsidiary, and, unless the context otherwise requires, the predecessor companies that have been merged out of existence with and into it. Except as otherwise indicated or as the context otherwise requires, the “Company” refers to Estre Ambiental S.A. and the “Registrant” refers to Estre Ambiental, Inc. All references to “Brazil” are to the Federative Republic of Brazil. All references to percent ownership interests in the Registrant do not take into account treasury shares.

In addition, in this document, unless otherwise specified or the context otherwise requires:

“$,” “US$” and “U.S. dollar” each refer to the United States dollar.

“R$” and “reais” each refer to the Brazilian real.

“ABRELPE” means the Brazilian Association of Public Cleaning and Waste Management (Associação Brasileira de Empresas de Limpeza Pública e Resíduos Especiais).

“audited financial statements” means our audited consolidated financial statements as of December 31, 2018 and 2017 and for the years ended December 31, 2018, 2017 and 2016, and the related notes thereto.

“Angra” means Angra Infra Multiestratégia Fundo de Investimento em Participações.

“Angra Put Option Agreement” means the put option agreement between Angra and the Company pursuant to which Angra had the right to sell all of its shares to the Company at a specified price. As a result of this agreement, Angra transferred 8,871,895 shares to the Company, which are currently held in treasury. As described elsewhere in this annual report, we were required to pay the exercise price of approximately R$40.3 million by September 6, 2018. No payments in respect of the exercise price have been made as of the date of this annual report.

“BFRS” means the Brazilian Federal Revenue Service.

“BNDES” means the Brazilian National Economic and Social Development Bank (Banco Nacional de Desenvolvimento Econômico e Social).

“C&I” means commercial and industrial, generally referring to our operations and customers not part of the public sector or affiliated with governmental agencies.

“Central Bank” means theBanco Central do Brasil, or Brazilian Central Bank.

“Class B Shares” means the Class B shares, par value US$0.0001 per share, of the Registrant.

“Code” means the Internal Revenue Code of 1986, as amended.

“Companies Law” means the Companies Law of the Cayman Islands (2018 Revision).

“Debt Instruments” means instruments governing the two existing debentures issued by the Company and one debt confession instrument entered into by the Company. All debentures issued pursuant to the Debt Instruments are currently held by Banco BTG Pactual S.A., Banco Santander (Brasil) S.A. and Itaú Unibanco S.A.

“Debt Restructuring” means our debt restructuring carried out on December 26, 2017, pursuant to which we applied US$110.6 million from the total cash investments received by us in the context of the Transaction to partially prepay certain of our existing debentures and related debt acknowledgment instrument, each denominated in Brazilian reais, coupled with a partial debt write-down and the refinancing of the balance of our existing debentures and related debt acknowledgment instrument through the amendment and restatement of the terms of such debt instruments with new terms.

1

Table of Contents

“Designated Stock Exchange” means any national securities exchange including NASDAQ Capital Market or NASDAQ.

“Employee Compensation Entity” means Estre Ambiental Employee SPV, Inc., a Cayman Islands exempted company.

“Estre USA” refers to Estre USA Inc., a Delaware corporation, formerly known as Boulevard Acquisition Corp. II, which name was changed to Estre USA Inc. on December 21, 2017 in connection with the Transaction. References to Estre USA prior to December 21, 2017 shall be deemed references to its predecessor entity, Boulevard Acquisition Corp. II.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“IASB” means the International Accounting Standards Board.

“IBGE” means the Governmental Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística).

“IFRS” means International Financial Reporting Standards, as issued by the IASB.

“Incentive Plan” means our 2017 Incentive Compensation Plan.

“Internal Evaluation Process” means the internal evaluation that we conducted at the direction of a special committee of our board of directors comprised of independent members of our board of directors in the aftermath of the Brazilian Federal Police’s execution of search warrants at our corporate offices and the premises of Soma on March 1, 2018, which was designed for the specific purpose of evaluating our supply relationships and related matters at the Company, including Soma and our joint ventures and which was conducted by external legal counsel working together with external forensic service providers.

“IRS” means the U.S. Internal Revenue Service.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012, as amended.

“Memorandum and Articles” means the amended and restated memorandum and articles of association of the Registrant.

“Merger” means the merger of Merger Sub with and into Estre USA, with Estre USA surviving such merger as a partially-owned subsidiary of the Registrant.

“Merger Sub” means BII Merger Sub Corp., which entity was merged into Estre USA, with Estre USA surviving such merger as a partially-owned subsidiary of the Registrant.

“MSW” means municipal solid waste.

“NASDAQ” means The NASDAQ Stock Market LLC.

“ordinary shares” means the ordinary shares, par value US$0.0001 per share, of the Registrant.

“PCAOB” means the Public Company Accounting Oversight Board.

“PFIC” means passive foreign investment company.

“PIPE Investment” means the private investment in public equity pursuant to which we issued 15,438,000 of our ordinary shares and 3,748,600 warrants to purchase ordinary shares at US$11.50 per share to certain institutional investors unaffiliated with us.

“PIPE Investors” means the institutional investors unaffiliated with us that purchased our ordinary shares and warrants as part of the PIPE Investment.

2

Table of Contents

“public warrants” means the warrants included in the units sold in Estre USA’s initial public offering, as converted in the Merger such that they represent the right to acquire ordinary shares of the Registrant, with each public warrant being exercisable for one of our ordinary shares, in accordance with its terms.

“Pre-Closing Restructuring” means the restructuring that the Company and the Registrant have completed immediately prior to effecting the Merger, pursuant to which, the holders of Company shares (other than Angra) contributed their shares of the Company to the Registrant in exchange for an aggregate of up to 27,001,886 ordinary shares, and the Company became a subsidiary of the Registrant. In addition, 1,983,000 of our ordinary shares were issued to the Employee Compensation Entity immediately prior to the closing of the Merger.

“private placement warrants” means the warrants to purchase Estre USA Class A Common Stock that were outstanding immediately prior to the closing of the Transaction that were purchased in a private placement in connection with Estre USA’s initial public offering, as converted in the Merger such that they represent the right to acquire ordinary shares of the Registrant, with each public warrant being exercisable for one of the Registrant’s ordinary shares, in accordance with its terms.

“Refinanced Debt” refers to our outstanding debentures issued pursuant to the Debt Instruments, as amended in connection with the Debt Restructuring.

“Registration Rights andLock-Up Agreement” means the Registration Rights andLock-Up Agreement to be entered into by and among the Registrant, the Sponsor and certain other persons and entities which will hold ordinary shares upon the Closing pursuant to the terms of the Transaction Agreement in connection with, and as a condition to the consummation of, the Transaction.

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002 and the rules promulgated thereunder.

“Sponsor” means Boulevard Acquisition Sponsor II, LLC, a Delaware limited liability company.

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Soma” means (i) after September 11, 2017, “SPE Soma – Soluções em Meio Ambiente Ltda.”, our consolidated, majority-owned subsidiary, of which we hold 82.0% as of December 31, 2017, that we operate together with Corpus Saneamento e Obras Ltda. (“Corpus”), our third party partner and (ii) prior to September 11, 2017, Consórcio Soma – Soluções em Meio Ambiente, a joint operation with Corpus, in each case, through which we provide urban cleaning and street sweeping services to the municipality of São Paulo.

“Transaction” refers, collectively, to thePre-Closing Restructuring, the Merger, the PIPE Investment and the Debt Restructuring, together with the other transactions ancillary thereto.

“warrants” means the public warrants, the private placement warrants and the warrants issued in a private placement to an investor that purchased ordinary shares in the PIPE Investment that have the same terms as the private placement warrants.

3

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The December 2017 Transaction

On December 21, 2017, we consummated a series of transactions resulting in our current status as a public company in the United States, as described below:

| • | On December 21, 2017, we completed our(i) Pre-Closing Restructuring, pursuant to which the holders of the Company’s common shares contributed these common shares to the Registrant in exchange for an aggregate of 27,001,886 ordinary shares of the Registrant, and as a result of such contribution became a indirectly-owned subsidiary of the Registrant, and (ii) merger with Estre USA, pursuant to which BII Merger Sub Corp. merged with and into Estre USA Inc., with Estre USA as the surviving entity, and Estre USA became a partially-owned subsidiary of the Registrant, which is referred to herein as the Merger (in addition, 1,983,000 of the Registrant’s ordinary shares were issued to the Employee Compensation Entity immediately prior to the closing of the Merger). |

| • | Also on December 21, 2017, the Registrant issued 15,438,000 of the Registrant’s ordinary shares and 3,748,600 warrants to purchase the Registrant’s ordinary shares at US$11.50 per share to certain institutional investors unaffiliated with us pursuant to a private investment in public equity, which we refer to as the PIPE Investment. For more information on the PIPE Investment, see “Item 10.C. Additional Information—Material Contracts—PIPE Subscription Agreements.” |

| • | As a result of the Merger and the PIPE Investment, we received a total US$139.9 million cash investment (comprising US$11.2 million from existing shareholders of Estre USA that did not redeem their public shares in connection with the Merger, and US$128.7 million from the proceeds of the sale of our ordinary shares to PIPE Investors), of which US$110.6 million was used to reduce certain of our indebtedness pursuant to a simultaneous Debt Restructuring, coupled with a partial debt write-down and the refinancing of the balance of the debentures and related debt acknowledgment instrument through the amendment and restatement of the terms of such instruments with new terms. |

We refer to the events described above as the “Transaction” in this annual report. For more information, see “Item 10.C. Additional Information—Material Contracts—the Transaction.”

Prior to the Transaction, the Registrant had limited or no assets, operations or activities. The Registrant was incorporated to become the holding entity of the Company to effect the Transaction. Considering that substantially all of the shareholders of the Company exchanged their shares of the Company for shares of the Registrant, the Transaction was accounted for as a reverse recapitalization transaction. The historical operations of the Registrant are deemed to be those of the Company.

The financial statements included in this report reflect (i) the restated operating results of the Company prior to the Transaction for the year ended December 31, 2016, as described under “Item 5.A. Operating and Financial Review and Prospects—Operating Results—Internal Evaluation Process and Previous Restatement of Financial Statements” below; (ii) the consolidated results of the Registrant and the Company following the Transaction; (iii) the assets and liabilities of the Company at their historical cost; and (iv) the Registrant’s equity and earnings per share for all periods presented, each of which were previously reflected in our annual report on Form20-F for the year ended December 31, 2017 which was filed with the SEC. The number of ordinary shares issued by the Registrant as a result of the Transaction are reflected retroactively to December 31, 2016 for purposes of calculating earnings per share in all prior periods presented.

The audited financial statements in this annual report have been prepared in accordance with IFRS as issued by IASB.

4

Table of Contents

In this annual report, we rely on and refer to information and statistics regarding the waste management services industry and our competitors from market research reports and other publicly available sources, including from ABRELPE, the International Solid Waste Association, Eurostat, Biocycle, the Central Bank and IBGE. We have supplemented such information where necessary with our own internal estimates and information obtained from discussions with our customers, taking into account publicly available information about other industry. Although we have no reason to believe that these sources are not reliable or that any of this information is not accurate or complete in all material respects, we have not independently verified any such information and, therefore, cannot guarantee its accuracy or completeness.

We maintain our books and records inreais. However, solely for the convenience of the reader, we have translated certain amounts included in this annual report fromreais into U.S. dollars using the selling rate as reported by the Central Bank, as of December 31, 2018 of R$3.8742 to US$1.00 or, where expressly indicated, at an average selling exchange rate prevailing during a certain period. All such currency translations should not be considered representations that any such amounts represent, or could have been, or could be, converted into, U.S. dollars orreais at that or at any other exchange rate. See “Item 3.A. Key Information—Selected Financial Data—Exchange Rate Information” for more detailed information regarding the translation ofreais into U.S. dollars.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This annual report contains a number of forward-looking statements, including statements about our financial conditions, results of operations, earnings outlook and prospects and may include statements for the period following the date of this annual report. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements are based on the current expectations of our management, as applicable, and are inherently subject to uncertainties and changes in circumstance and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” those discussed and identified in public filings made with the SEC by us and the following:

| • | changes in market prices, customer demand and preferences and competitive conditions; |

| • | general economic, political and business conditions in Brazil, particularly in the geographic markets we serve and others in which we intend to serve; |

| • | fluctuations in inflation and interest rates to which our debt is indexed; |

| • | our significant level of indebtedness and fixed obligations; |

| • | the risk that we may lose contracts through competitive bidding or be required to substantially lower prices in order to retain certain contracts, which could negatively impact our revenues, operating margins and operating cash flow generation, including the risk of compromising our capacity to meet financial obligations; |

| • | the outcome of investigations by government authorities under the applicable anti-corruption laws or otherwise, including the currently ongoing Operation Descarte, Operation Quinto Ano and other actions in relation to our former controlling shareholder; |

5

Table of Contents

| • | the outcome of alleged tax infringement charges by the Brazilian tax authorities and the possibility of further tax infringement charges relating to other facts and periods, including in relation to ongoing investigations and inquiries of the tax authorities; |

| • | the recruitment, compensation and retention of key personnel; |

| • | our ability to successfully defend ourselves in connection with various ongoing and future judicial, administrative or other third-party proceedings that could interrupt or materially limit our operations, divert our management’s attention and result in adverse judgments, settlements or fines and create negative publicity; |

| • | the strength and security of our information technology infrastructure and internal controls and our ability to successfully implement our remediation plan to address certain weaknesses in our internal controls; |

| • | our ability to retain our customers given that a significant portion of our revenue is derived from a small number of customers; |

| • | our ability to collect for the services we provide, which is dependent on the financial condition of our customers, especially that of our public sector customers; |

| • | our ability to successfully obtain or renew the necessary licenses to operate new landfills or expand existing ones; |

| • | our ability to adequately establish reserves and provisions for landfill site closure and post-closure costs and contamination-related costs; |

| • | existing and future governmental regulation, including in relation to environmental liabilities; |

| • | our ability to detect and prevent money laundering, improper payments and other illegal activities; |

| • | labor disputes, employee strikes and other labor-related disruptions, including in connection with negotiations with unions; |

| • | our ability to successfully implement our strategy, including those initiatives designed to improve our results of operations, including the restructuring of our debt and possibility of extrajudicial reorganization or a judicially-supervised reorganization process; and |

| • | other factors or trends affecting our financial condition or results of operations, including those factors identified or discussed under “Item 3.D.—Key Information—Risk Factors.” |

Should one or more of these risks or uncertainties materialize, or should any of the assumptions made by our management prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

All subsequent written and oral forward-looking statements contained in this annual report and attributable to us or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this annual report. Except to the extent required by applicable law or regulation, we undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events.

6

Table of Contents

PART I

| ITEM 1. |

Not Applicable.

| ITEM 2. |

Not Applicable.

| ITEM 3. |

| A. |

The following selected financial information should be read in conjunction with “Presentation of Financial and Other Information,” “Item 5. Operating and Financial Review and Prospects” and our audited financial statements, which are included in this annual report.

The selected financial data as of and for the years ended December 31, 2018 and 2017 and for the three years ended December 31, 2018 have been derived from our audited financial statements, prepared in accordance with IFRS, and included in this annual report.

Statement of Profit and Loss

| For the year ended December 31, | ||||||||||||||||||||||||

| 2018 | 2018 | 2017 (restated)(1) | 2016 (restated)(1) | 2015 (restated)(1) | 2014 (restated)(1) | |||||||||||||||||||

| (in millions of US$)(2) | (in millions of R$) | |||||||||||||||||||||||

Continuing operations | ||||||||||||||||||||||||

Revenue from services rendered | 325.4 | 1,260.6 | 1,345.8 | 1,380.0 | 1,328.9 | 1,282.6 | ||||||||||||||||||

Cost of services | (252.7 | ) | (979.2 | ) | (942.2 | ) | (1,003.7 | ) | (974.9 | ) | (932.9 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross profit | 72.6 | 281.4 | 403.6 | 376.3 | 354.0 | 349.6 | ||||||||||||||||||

Operating income (expenses) | ||||||||||||||||||||||||

General and administrative expenses | (84.5 | ) | (327.3 | ) | (256.5 | ) | (231.1 | ) | (222.5 | ) | (248.3 | ) | ||||||||||||

Selling expenses, net | 1.4 | 5.3 | (6.7 | ) | 10.5 | 13.3 | (56.3 | ) | ||||||||||||||||

Share of (loss) profit of an associate | (0.9 | ) | (3.3 | ) | (1.0 | ) | 10.2 | 11.1 | 40.6 | |||||||||||||||

Other operating expenses, net | (148.8 | ) | (576.5 | ) | (31.1 | ) | (80.6 | ) | (24.7 | ) | 139.3 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (232.8 | ) | (901.8 | ) | (295.3 | ) | (291.0 | ) | (222.9 | ) | (124.7 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Profit (loss) before finance income and expenses | (160.1 | ) | (620.4 | ) | 108.3 | 85.3 | 131.1 | 224.9 | ||||||||||||||||

Finance expenses | (65.0 | ) | (251.7 | ) | (532.2 | ) | (397.1 | ) | (384.0 | ) | (415.7 | ) | ||||||||||||

Finance income | 30.0 | 116.3 | 108.3 | 51.7 | 30.1 | 27.4 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Loss before income and social contribution taxes | (195.1 | ) | (755.8 | ) | (315.6 | ) | (260.1 | ) | (222.7 | ) | (163.4 | ) | ||||||||||||

Current income and social contribution taxes | (10.7 | ) | (41.6 | ) | (17.6 | ) | (54.3 | ) | (5.4 | ) | (48.6 | ) | ||||||||||||

Deferred income and social contribution taxes | 19.7 | 76.5 | 371.1 | (49.8 | ) | 12.6 | 41.6 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Profit (loss) for the year from continuing operations | (186.1 | ) | (720.9 | ) | 37.9 | (364.2 | ) | (215.5 | ) | (170.4 | ) | |||||||||||||

Discontinued operations(1) | ||||||||||||||||||||||||

Profit after income and social contribution tax from discontinued operations | 7.9 | 30.5 | 14.4 | 3.3 | (0.6 | ) | (44.8 | ) | ||||||||||||||||

Profit (loss) for the year | (178.2 | ) | (690.5 | ) | 52.3 | (360.9 | ) | (215.0 | ) | (215.2 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Attributable to: | ||||||||||||||||||||||||

Equity holders of the parent | (168.5 | ) | (652.8 | ) | 43.8 | (360.8 | ) | (215.0 | ) | (195.8 | ) | |||||||||||||

Non-controlling interests | (9.7 | ) | (37.7 | ) | 8.5 | (0.2 | ) | (0.0 | ) | (19.4 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (178.2 | ) | (690.5 | ) | 52.3 | (360.9 | ) | (215.0 | ) | (215.2 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

7

Table of Contents

| For the year ended December 31, | ||||||||||||||||||||||||

| 2018 | 2018 | 2017 (restated)(1) | 2016 (restated)(1) | 2015 (restated)(1) | 2014 (restated)(1) | |||||||||||||||||||

| (in millions of US$)(2) | (in millions of R$) | |||||||||||||||||||||||

Earnings (loss) per share(3) | ||||||||||||||||||||||||

- Basic, profit (loss) for the year attributable to equity holders of the parent (inReais) | (3.6919 | ) | (14.3032 | ) | 0.9596 | (7.9057 | ) | (4.7101 | ) | (4.2905 | ) | |||||||||||||

- Diluted, profit (loss) for the year attributable to equity holders of the parent (inReais) | (3.5382 | ) | (13.7076 | ) | 0.9585 | (7.9057 | ) | (4.7101 | ) | (4.2905 | ) | |||||||||||||

Earnings (loss) per share from continuing operations | ||||||||||||||||||||||||

- Basic, profit (loss) from continuing operations attributable to equity holders of the parent (inReais)(4) | (3.8537 | ) | (14.9299 | ) | 0.6453 | (7.9777 | ) | (4.6110 | ) | (3.7469 | ) | |||||||||||||

- Diluted, profit (loss) from continuing operations attributable to equity holders of the parent (in Reais)(4) | (3.6932 | ) | (14.3082 | ) | 0.6446 | (7.9777 | ) | (4.6110 | ) | (3.7469 | ) | |||||||||||||

| (1) | In 2018, our energy business, which is part of the Value Recovery segment, was classified as discontinued operations, and as a result of that classification, the statement of profit and loss for the years ended December 31, 2017, 2016, 2015 and 2014 have been restated for comparative purposes. See note 1.5.1 to our audited financial statements included elsewhere in this annual report. |

| (2) | Solely for the convenience of the reader, the amounts in reais for the year ended December 31, 2018 has been translated into U.S. dollars using the rate of R$3.8742 per U.S. dollar, which was the commercial selling rate for U.S. dollars as of December 31, 2018, as reported by the Central Bank. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate. See “—Exchange Rate Information” below. |

| (3) | Given that the Registrant is a new parent entity established to effect a share for share exchange in connection with the Transaction, and its audited financial statements have been presented as a continuation of the existing group, the number of shares taken as being issued for both the current and preceding periods was the number of shares issued by the new parent entity (Estre Ambiental, Inc.). In the calculation of earnings per share for the year ended December 31, 2016 presented in the audited financial statements, there were no changes in the number of outstanding ordinary shares of Estre Ambiental S.A. for that period that should be reflected in the calculation. Therefore, the weighted average number of shares was the same for all periods. |

| (4) | The calculation of basic earnings (loss) per share is based on the net income attributable to controlling equity holders of the Registrant and the proportional weighted average number of shares outstanding during the year. Diluted earnings per share is based on the net income attributable to controlling equity holders, as adjusted by the weighted average number of shares outstanding during the year assuming conversion of all potentially dilutive shares. For additional information, see note 34 to our audited financial statements included elsewhere in this annual report. |

8

Table of Contents

Balance Sheet

| As of December 31, | ||||||||||||||||||||

| 2018 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| (in millions of US$)(1) | (in millions of R$) | |||||||||||||||||||

Assets | ||||||||||||||||||||

Current Assets | ||||||||||||||||||||

Cash and cash equivalents | 4.9 | 18.9 | 84.7 | 31.1 | 47.8 | |||||||||||||||

Marketable securities | 0.0 | 0.0 | 0.0 | — | 12.1 | |||||||||||||||

Trade accounts receivable | 129.5 | 501.8 | 669.2 | 716.8 | 512.7 | |||||||||||||||

Contract asset. | 31.1 | 120.3 | — | — | — | |||||||||||||||

Inventories | 2.2 | 8.6 | 11.4 | 8.7 | 8.1 | |||||||||||||||

Taxes recoverable | 25.4 | 98.4 | 101.9 | 117.8 | 92.1 | |||||||||||||||

Receivables from divestiture | 2.4 | 9.3 | — | — | 41.3 | |||||||||||||||

Other receivables | 8.3 | 32.0 | 34.9 | 38.8 | 34.6 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| 203.7 | 789.3 | 902.1 | 913.2 | 748.7 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Assets held for sale | 21.0 | 81.5 | 6.6 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total current assets | 224.8 | 870.8 | 908.7 | 913.2 | 748.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Noncurrent Assets | ||||||||||||||||||||

Marketable securities | 0.0 | 0.0 | — | — | 24.2 | |||||||||||||||

Related Parties | 0.6 | 2.2 | 14.5 | 9.8 | 21.3 | |||||||||||||||

Trade accounts receivable | 31.3 | 121.1 | 108.9 | 5.7 | 4.8 | |||||||||||||||

Taxes recoverable | 8.1 | 31.2 | 52.1 | 4.5 | 22.2 | |||||||||||||||

Prepaid expenses | 0.0 | 0.1 | 0.2 | 3.3 | 4.5 | |||||||||||||||

Deferred taxes | — | — | 0.0 | 41.1 | 25.9 | |||||||||||||||

Other receivables | 5.3 | 20.6 | 14.5 | 7.7 | 12.2 | |||||||||||||||

Fair value of call option | — | — | — | — | 20.9 | |||||||||||||||

Investments | 2.0 | 7.7 | 7.2 | 114.7 | 104.3 | |||||||||||||||

Property, plant and equipment | 132.2 | 512.1 | 689.5 | 694.5 | 691.8 | |||||||||||||||

Intangible assets | 15.2 | 59.0 | 588.2 | 553.8 | 607.1 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total noncurrent assets | 194.6 | 754.0 | 1,475.1 | 1,434.9 | 1,539.6 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total assets | 419.3 | 1,624.7 | 2,383.8 | 2,348.0 | 2,288.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Liabilities and Equity | ||||||||||||||||||||

Current liabilities | ||||||||||||||||||||

Loans and financing | 155.3 | 601.5 | 14.1 | 16.7 | 64.1 | |||||||||||||||

Debentures | 249.4 | 966.4 | — | 1,665.6 | 1,417.1 | |||||||||||||||

Provision for landfill closure | 1.4 | 5.6 | 20.7 | 15.5 | — | |||||||||||||||

Trade accounts payable | 44.7 | 173.3 | 128.1 | 108.4 | 96.5 | |||||||||||||||

Labor payable | 25.4 | 98.5 | 117.9 | 106.9 | 97.6 | |||||||||||||||

Tax liabilities | 39.2 | 151.7 | 169.5 | 295.3 | 214.8 | |||||||||||||||

Accounts payable from acquisition of investments | — | — | — | 4.9 | 47.0 | |||||||||||||||

Related parties | 21.2 | 82.1 | 82.8 | 2.6 | 23.1 | |||||||||||||||

Advances from customers | 3.9 | 15.0 | 16.5 | 0.6 | 3.5 | |||||||||||||||

Accounts payable for land and intangible asset acquisition | 1.4 | 5.4 | 9.0 | 9.1 | 10.6 | |||||||||||||||

Other liabilities | 5.1 | 19.8 | 33.0 | 29.5 | 6.5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| 547.1 | 2,119.4 | 591.6 | 2,255.1 | 1,980.9 | ||||||||||||||||

Liabilities directly associated with the assets held for sale | 10.6 | 41.2 | 23.8 | 24.2 | 17.9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

9

Table of Contents

| As of December 31, | ||||||||||||||||||||

| 2018 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| (in millions of US$)(1) | (in millions of R$) | |||||||||||||||||||

Total current liabilities | 557.7 | 2,160.6 | 615.4 | 2,279.4 | 1,998.8 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Noncurrent liabilities | ||||||||||||||||||||

Loans and financing | 6.9 | 26.8 | 371.4 | 10 | 20.2 | |||||||||||||||

Debentures | — | — | 1,069.0 | — | — | |||||||||||||||

Provision for landfill closure | 25.0 | 96.8 | 92.9 | 86.1 | 83.1 | |||||||||||||||

Provision for legal proceedings | 18.1 | 70.3 | 147.8 | 245.5 | 185.6 | |||||||||||||||

Accounts payable from acquisition of investments | — | — | — | 4.9 | 26.7 | |||||||||||||||

Tax liabilities | 93.5 | 362.3 | 395.8 | 236.1 | 213.1 | |||||||||||||||

Deferred taxes | 13.5 | 52.3 | 137.0 | 175.6 | 110.6 | |||||||||||||||

Accounts payable for land and intangible asset acquisition | 1.2 | 4.8 | 10.4 | 7.6 | 13.1 | |||||||||||||||

Other liabilities | 0.1 | 0.2 | 0.2 | 39.9 | 18.3 | |||||||||||||||

Total noncurrent liabilities | 158.3 | 613.4 | 2,224.4 | 805.7 | 670.6 | |||||||||||||||

Equity | ||||||||||||||||||||

Capital | 0.0 | 0.0 | 0.0 | 108.1 | 108.1 | |||||||||||||||

Capital reserve | 282.6 | 1,094.7 | 1,068.2 | 748.5 | 743.7 | |||||||||||||||

Other comprehensive income | (0.0 | ) | (0.0 | ) | 1.8 | 1.7 | 1.5 | |||||||||||||

Treasury shares | — | — | — | (37.4 | ) | (37.4 | ) | |||||||||||||

Accumulated losses | (563.6 | ) | (2,183.4 | ) | (1,520.8 | ) | (1,564.5 | ) | (1,203.8 | ) | ||||||||||

Non-controlling interest | (15.6 | ) | (60.5 | ) | (5.1 | ) | 6.6 | 6.7 | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total equity (capital deficiency) | (296.6 | ) | (1,149.2 | ) | (455.9 | ) | (737.1 | ) | (381.1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total liabilities and equity | 419.3 | 1,624.7 | 2,383.8 | 2,348.0 | 2,288.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (1) | Solely for the convenience of the reader, the amounts in reais for the year ended December 31, 2018 has been translated into U.S. dollars using the rate of R$3.8742 per U.S. dollar, which was the commercial selling rate for U.S. dollars as of December 31, 2018, as reported by the Central Bank. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate. See “—Exchange Rate Information” below. |

CONSOLIDATED STATEMENT OF CASH FLOW

| For the year ended December 31, | ||||||||||||||||||||

| 2018 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| (in millions of US$)(1) | ||||||||||||||||||||

Net cash (used in) provided by | ||||||||||||||||||||

Operating activities | 5.4 | 21.0 | 243.3 | 213.5 | 235.2 | |||||||||||||||

Investing activities | (22.4 | ) | (86.9 | ) | (200.3 | ) | (166.7 | ) | (90.1 | ) | ||||||||||

Financing activities | 0.4 | 1.7 | 10.6 | (63.5 | ) | (210.4 | ) | |||||||||||||

| (1) | Solely for the convenience of the reader, the amounts in reais for the year ended December 31, 2018 has been translated into U.S. dollars using the rate of R$3.8742 per U.S. dollar, which was the commercial selling rate for U.S. dollars as of December 31, 2018, as reported by the Central Bank. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate. See “Exchange Rate Information” below. |

10

Table of Contents

Segment Information

The table below sets forth our statement of profit or loss by business segment for the periods indicated:

For the year ended December 31, 2018:

| Collection & Cleaning Services | O&G | Landfills | Value Recovery | Corporate | Eliminations | Consolidated | ||||||||||||||||||||||

| (in thousands of R$) | ||||||||||||||||||||||||||||

Domestic customers | 817,145 | 12,749 | 401,140 | 29,553 | — | — | 1,260,587 | |||||||||||||||||||||

Inter-segment | 44,831 | 45 | 55,427 | 1,777 | — | (102,080 | ) | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total revenue from services | 861,976 | 12,794 | 456,567 | 31,330 | — | (102,080 | ) | 1,260,587 | ||||||||||||||||||||

Cost of services | (731,424 | ) | (13,511 | ) | (306,673 | ) | (29,119 | ) | (2,253 | ) | 103,797 | (979,183 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Gross profit (loss) | 130,552 | (717 | ) | 149,894 | 2,211 | (2,253 | ) | 1,717 | 281,404 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Operating income/(expenses) | ||||||||||||||||||||||||||||

General and administrative expenses | (40,793 | ) | (96 | ) | (1,761 | ) | (187 | ) | (284,472 | ) | 23 | (327,286 | ) | |||||||||||||||

Selling expenses, net | (8,433 | ) | (189 | ) | (26,981 | ) | (1,782 | ) | 42,709 | — | 5,324 | |||||||||||||||||

Share of profit of an associate | — | — | — | — | (650,080 | ) | 646,741 | (3,339 | ) | |||||||||||||||||||

Other operating income (expenses), net | 1,225 | (6 | ) | 4,949 | (122 | ) | (580,829 | ) | (1,723 | ) | (576,506 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| (48,001 | ) | (291 | ) | (23,793 | ) | (2,091 | ) | (1,472,672 | ) | 645,041 | (901,807 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before finance income and expenses | 82,551 | (1,008 | ) | 126,101 | 120 | (1,474,925 | ) | 646,758 | (620,403 | ) | ||||||||||||||||||

Finance expenses | 14,788 | (541 | ) | (14,244 | ) | (77 | ) | (251,619 | ) | — | (251,693 | ) | ||||||||||||||||

Finance income | 8,536 | 73 | 6,535 | 603 | 100,566 | — | 116,313 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before income and social contribution taxes | 105,875 | (1,476 | ) | 118,392 | 646 | (1,625,978 | ) | 646,758 | (755,783 | ) | ||||||||||||||||||

(-) Current income and social contribution taxes | (26,621 | ) | — | (479 | ) | — | (14,523 | ) | — | (41,623 | ) | |||||||||||||||||

(-) Deferred income and social contribution taxes | 292 | — | — | — | 76,196 | — | 76,488 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) for the year | 79,546 | (1,476 | ) | 117,913 | 646 | (1,564,305 | ) | 646,758 | (720,918 | ) | ||||||||||||||||||

Discontinued operations | ||||||||||||||||||||||||||||

Profit (loss) after tax for the year resulting from continuing operations | — | — | — | 3,285 | 27,169 | — | 30,454 | |||||||||||||||||||||

Net income (loss) for the year | 79,546 | (1,476 | ) | 117,913 | 3,931 | (1,537,136 | ) | 646,758 | (690,464 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

11

Table of Contents

For the year ended December 31, 2017:

| Collection & Cleaning Services | O&G | Landfills | Value Recovery | Corporate | Eliminations | Consolidated | ||||||||||||||||||||||

| (in thousands of R$) | ||||||||||||||||||||||||||||

Domestic customers | 911,652 | 25,524 | 371,840 | 36,833 | — | — | 1,345,849 | |||||||||||||||||||||

Inter-segment | 17,171 | 331 | 83,558 | 897 | — | (101,957 | ) | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total revenue from services | 928,823 | 25,855 | 455,398 | 37,730 | — | (101,957 | ) | 1,345,849 | ||||||||||||||||||||

Cost of services | (673,024 | ) | (21,152 | ) | (316,305 | ) | (24,428 | ) | (9,303 | ) | 101,957 | (942,255 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Gross profit (loss) | 255,799 | 4,703 | 139,093 | 13,302 | (9,303 | ) | — | 403,594 | ||||||||||||||||||||

Operating income/(expenses) | ||||||||||||||||||||||||||||

General and administrative expenses | (38,309 | ) | (42 | ) | 1,290 | (842 | ) | (218,629 | ) | — | (256,532 | ) | ||||||||||||||||

Selling expenses, net | (16,261 | ) | — | 37,468 | 280 | (28,128 | ) | — | (6,641 | ) | ||||||||||||||||||

Share of profit of an associate | — | — | — | — | 83,384 | (84,404 | ) | (1,020 | ) | |||||||||||||||||||

Other operating income (expenses), net | (15,335 | ) | (4,509 | ) | (41,719 | ) | 76,349 | (45,911 | ) | — | (31,125 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| (69,905 | ) | (4,551 | ) | (2,961 | ) | 75,787 | (209,284 | ) | (84,404 | ) | (295,318 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before finance income and expenses | 185,894 | 152 | 136,132 | 89,089 | (218,587 | ) | (84,404 | ) | 108,276 | |||||||||||||||||||

Finance expenses | (132,234 | ) | 889 | (37,757 | ) | (36 | ) | (363,037 | ) | — | (532,175 | ) | ||||||||||||||||

Finance income | 8,276 | 70 | 948 | 81 | 98,906 | — | 108,281 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before income and social contribution taxes | 61,936 | 1,111 | 99,323 | 89,134 | (482,718 | ) | (84,404 | ) | (315,618 | ) | ||||||||||||||||||

(-) Current income and social contribution taxes | (8,613 | ) | — | (4,030 | ) | (62 | ) | (4,838 | ) | — | (17,543 | ) | ||||||||||||||||

(-) Deferred income and social contribution taxes | 22,552 | — | 16,897 | — | 331,635 | — | 371,084 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) for the year | 75,875 | 1,111 | 112,190 | 89,072 | (155,921 | ) | (84,404 | ) | 37,923 | |||||||||||||||||||

Discontinued operations Profit (loss) after tax for the year resulting from continuing operations | 6,506 | — | 799 | 7,037 | — | — | 14,342 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Net income (loss) for the year | 82,381 | 1,111 | 112,989 | 96,109 | (155,921 | ) | (84,404 | ) | 52,265 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

12

Table of Contents

For the year ended December 31, 2016, as restated:

| Collection & Cleaning Services | O&G | Landfills | Value Recovery | Corporate | Eliminations | Consolidated | ||||||||||||||||||||||

| (in thousands of R$) | ||||||||||||||||||||||||||||

Foreign customers | — | — | — | — | — | — | — | |||||||||||||||||||||

Domestic customers | 869,333 | 62,799 | 420,293 | 27,606 | — | — | 1,380,031 | |||||||||||||||||||||

Inter-segment | 52,689 | 78 | 29,505 | 1,632 | — | (83,904 | ) | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total revenue from services | 922,022 | 62,877 | 449,798 | 29,238 | — | (83,904 | ) | 1,380,031 | ||||||||||||||||||||

Cost of services | (678,058 | ) | (41,583 | ) | (337,335 | ) | (22,002 | ) | (8,674 | ) | 83,904 | (1,003,748 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Gross profit (loss) | 243,964 | 21,294 | 112,463 | 7,236 | (8,674 | ) | — | 376,283 | ||||||||||||||||||||

Operating income/(expenses) | ||||||||||||||||||||||||||||

General and administrative expenses | (38,105 | ) | (783 | ) | (10,206 | ) | (343 | ) | (163,680 | ) | (17,933 | ) | (231,050 | ) | ||||||||||||||

Selling expenses, net | 268 | 897 | 26,293 | 8,532 | (25,495 | ) | 10,495 | |||||||||||||||||||||

Share of profit of an associate | — | — | — | — | 139,714 | (129,562 | ) | 10,152 | ||||||||||||||||||||

Other operating income (expenses), net | (12,402 | ) | 213 | 962 | 4 | (69,328 | ) | — | (80,551 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| (50,239 | ) | 327 | 17,049 | 8,193 | (118,789 | ) | (147,495 | ) | (290,954 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before finance income and expenses | 193,725 | 21,621 | 129,512 | 15,429 | (127,463 | ) | (147,495 | ) | 85,329 | |||||||||||||||||||

Finance expenses | (27,110 | ) | (1,326 | ) | (732 | ) | (11 | ) | (367,954 | ) | — | (397,133 | ) | |||||||||||||||

Finance income | 1,506 | 1 | 18 | 16 | 50,122 | — | 51,663 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) before income and social contribution taxes | 168,121 | 20,296 | 128,798 | 15,434 | (445,295 | ) | (147,495 | ) | (260,141 | ) | ||||||||||||||||||

(-) Current income and social contribution taxes | — | — | — | (1 | ) | (54,336 | ) | — | (54,337 | ) | ||||||||||||||||||

(-) Deferred income and social contribution taxes | — | — | — | — | (49,755 | ) | — | (49,755 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Profit (loss) for the year | 168,121 | 20,296 | 128,798 | 15,433 | (549,386 | ) | (147,495 | ) | (364,233 | ) | ||||||||||||||||||

Discontinued operations Profit (loss) after tax for the year resulting from continuing operations | — | — | 41 | 3,247 | — | — | 3,288 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Net income (loss) for the year | 168,121 | 20,296 | 128,839 | 18,680 | (549,386 | ) | (147,495 | ) | (360,945 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Exchange Rate Information

The Brazilian foreign exchange system allows the purchase and sale of foreign currency and the international transfer of reais by any person or legal entity, regardless of the amount, subject to certain regulatory procedures.

Since 1999, the Central Bank has allowed the U.S. dollar-real exchange rate to float freely. Since then, the U.S. dollar-real exchange rate has fluctuated considerably.

The Central Bank has intervened occasionally to control unstable movements in foreign exchange rates. We cannot predict whether the Central Bank or the Brazilian government will continue to permit the real to float freely or will intervene in the exchange rate market through the return of a currency band system or otherwise. See “—D. Risk Factors—Risks Related to Brazil—The Brazilian economy and we may be negatively impacted by exchange rate instability.”

The real may depreciate or appreciate against the U.S. dollar substantially. See “—D. Risk Factors—Risks Related to Brazil—The Brazilian economy and we may be negatively impacted by exchange rate instability.”

Furthermore, Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or there are substantial reasons to foresee a serious imbalance, the Brazilian government may impose temporary restrictions on the remittances of foreign capital abroad and on the conversion of Brazilian currency into foreign currencies. We cannot assure you that such measures will not be taken by the Brazilian government in the future. See “—D. Risk Factors—Risks Related to Brazil—The Brazilian economy and we may be negatively impacted by exchange rate instability.”

13

Table of Contents

For convenience purposes only, the amounts in reais for the year ended December 31, 2018 presented throughout this annual report have been translated to U.S. dollars using the rate R$3.8742 per U.S. dollar, which was the commercial selling rate for U.S. dollars as of December 31, 2018, as reported by the Central Bank. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate. Therealhas fluctuated significantly over the course of 2018 due in part to the general strengthening of the U.S. dollar worldwide and reflecting lower Brazilian interest rates and a high degree of political uncertainty.

The following table shows the period end, average, high and low commercial sellingreal/U.S. dollar exchange rate reported by the Central Bank on its website for the periods and dates indicated.

| R$ per US$1.00 | ||||||||

| Year Ended December 31, | Low | High | Average(1) | Period End | ||||

2013 | 1.95 | 2.45 | 2.16 | 2.34 | ||||

2014 | 2.20 | 2,74 | 2.35 | 2.66 | ||||

2015 | 2.58 | 4.19 | 3.34 | 3.90 | ||||

2016 | 3.12 | 4.16 | 3.48 | 3.26 | ||||

2017 | 3.05 | 3.44 | 3.19 | 3.31 | ||||

2018 | 3.14 | 4.19 | 3.66 | 3.87 | ||||

| (1) | Represents the average of exchange rates on each day of each month during the periods indicated. |

| B. |

Not applicable.

| C. |

Not applicable.

| D. |

An investment in our ordinary shares carries a significant degree of risk. You should carefully consider the following risks and other information in this annual report, including our audited financial statements included elsewhere in this annual report, before you decide to purchase our ordinary shares. Additional risks and uncertainties of which we are not presently aware or that we currently deem immaterial could also affect our business operations and financial condition. If any of these risks actually occur, our business, financial condition, results of operations or prospects could be materially affected. As a result, the trading price of our ordinary shares could decline and you could lose part or all of your investment.

Risks Related to Our Business

We may lose contracts through competitive bidding or be required to substantially lower prices in order to retain certain contracts, which could negatively impact our revenues.

We derive a significant portion of our revenues from markets in which we have exclusive arrangements pursuant to municipal contracts. Our municipal contracts are for a specified term and are, or will be, subject to competitive bidding in the future. Although we intend to bid on additional municipal contracts in our target markets from time to time if and when suitable opportunities arise, we may not, if ever, be successful in winning bids, especially considering the significant increase in competitivity and margin compression in the market during the course of 2018. In addition, municipalities may unilaterally terminate any agreements on grounds of serving the public interest. If we are unable to replace revenue from contracts lost through competitive bidding or early termination or from lowering prices pursuant to the competitive bidding process for existing contracts, our revenues could decline.

Governmental action may also affect our exclusive arrangements. Municipalities may decide to develop their own landfills, on an optional or mandatory basis, which may cause us to lose customers. If we are not able to replace lost revenues within a reasonable time period, our business results of operations and financial condition could be adversely affected. Additionally, the loss of municipal contracts through competitive bidding, early termination or governmental action could cause long lived tangible and intangible assets to be impaired and require a charge against earnings.

14

Table of Contents

In addition, the risks described under “—Risks Related to Compliance and Control” have caused, and may in the future cause, us to be unable to participate in certain competitive bidding processes, which may cause a significant decline in our revenues. For example, Estre was classified as a Compliance High Risk Supplier by Petrobras in the past and, as such, was not permitted to participate in certain of Petrobras’ bidding processes.

A significant portion of our revenue is derived from a small number of customers, and partial or full loss of revenues from any such customer may adversely affect our revenues and results of operations. In particular, the municipality of São Paulo is currently serviced based on a short-term temporary contract which will end on June 1, 2019. The loss of business from the São Paulo contract will have a material adverse impact on us.

Our customer base includes a mix of customers operating in both the private and public sectors. As of December 31, 2018, we had 138 municipal customers and more than 3,000 private sector customers, serving approximately 31 million individual customers daily. Although we have a diversified customer base across our four business segments, our top 13 customers accounted for 72.9% of our total net revenue in the year ended December 31, 2018. In addition, our top 5 costumers represent 38.2% of our revenue from the Landfills segment, totaling 12.1% of our total net revenue and 8 customers accounted for 93.7% or more of our revenue from the Collection & Cleaning segment, totaling 60.7% of total net revenue in the year ended December 31, 2018.

In addition, we rely significantly on certain municipal customers within our Collection & Cleaning segment as a source of revenues, namely the municipalities of São Paulo and Curitiba. Together, our contracts with the municipalities of São Paulo and Curitiba represented 79.0% of the net revenues from services rendered for the Collection & Cleaning segment for the year ended December 31, 2018, and 39.9% of our total net revenues from services that year. Competitive bidding processes are inherently subject to a high degree of uncertainty, and there can be no guarantee that past practices will be indicative of future success. As described below under “—Our contract with the municipality of São Paulo”, we will no longer provide services in São Paulo as of June 1, 2019 when our emergency temporary contract will be terminated. As described below under “Our contract with the municipality of Curitiba”, our contract with Curitiba has been renewed and we signed a five-year contract on January 3, 2019.

Moreover, we cannot assure you that we will be the successful bidder in bidding processes for any other competitive bidding process we participate in. In addition, even if we are successful in the bidding process and enter into new contracts with our most significant customers, the terms of the contracts might differ and might not be as favorable to us as those contracts currently in place, resulting in less revenue from these customers. The loss or adverse modification of any material customer contract could have a material adverse effect on our business, results of operations and financial condition.

While Brazilian law does not allow the term extension of government contracts already expired, public administrators may exercise their right to hire the same contractor on a provisional basis for a temporary period based on a waiver of the bidding process. Provisional service pursuant to a temporary contract may be with any service provider, not just the last serving contractor. These temporary contracts must be limited to a180-day term, counted as of the occurrence of the exceptional circumstances giving rise to the auction delay, and may be terminated by the municipality at its discretion at any time, including as a result of the conclusion of the formal bidding process. As a general rule, temporary contracts entered into on an emergency basis may not be extended. However, as the collection of MSW is considered an essential service under Brazilian law, once the initial180-day period expires on a temporary contract, municipalities may continue to extend for subsequent180-day periods.

Our contract with the municipality of São Paulo

We have been servicing the São Paulo contract through Soma since 2011. Our contract with the municipality of São Paulo for urban cleaning and street sweeping services represented approximately 25.5% of our revenues in 2018 (29.1% of our revenues in 2017). This contract expired in the end of 2017, and we are currently providing urban cleaning services to the city of São Paulo pursuant to a temporary contract. The temporary contract was first entered into on December 15, 2017 and expired in June 2018. On June 12, 2018, we further extended the temporary contract until the end of 2018. In December 2018, we further extended the temporary contract until the end of May 2019 and, on May 2, 2019, we were informed that our emergency contract with the municipality of São Paulo will be terminated on June 1, 2019, at which point we will no longer provide services in São Paulo. The extended temporary contract introduced in June 2018 certain significant changes to the contractual arrangement. Most significantly, under the extended temporary contract, the city of São Paulo has been divided into six separate parcels for urban cleaning, whereas under the previous contract the city had been divided into two parcels only. We, through Soma, were awarded only two parcels under the extended temporary contract, which reflects a significant decrease of our service area, since we previously serviced one of the only two parcels. As a result these changes, monthly revenues under the extended temporary contract decreased approximately 40% starting in June 2018 and as a result our revenues from the contract with the municipality of São Paulo for urban cleaning and street sweeping services decreased to approximately 31.8% of our revenues in 2018.

15

Table of Contents

After a series of delays, a new bid for the São Paulo contract was initiated in October 2018, in which the Company participated. In connection with the bidding process, São Paulo has divided the urban cleaning contract into six separate parcels, in line with the extended temporary contracts entered into in June 2018. The Company was not the bidder with the lowest price for any of the six parcels in São Paulo and, on May 2, 2019, we were informed that our emergency contract with the municipality of São Paulo will be terminated on June 1, 2019, at which point we will no longer provide services in São Paulo. The loss of the São Paulo cleaning contract will result in a significant reduction in our revenues, which will have an adverse impact on us.

Considering the significance of the São Paulo contract in terms of revenues, it can be expected that our revenues will materially decrease upon the termination of the contract. According to management estimates, and based on our original revenue expectations for 2019, the impact of losing the São Paulo contract on an annualized basis will result in an estimated decrease in revenues of 25.1%.

A relevant part of our operational structure is designed to serve the São Paulo contract and, upon its termination, we will be required to significantly reallocate resources, including the termination of employees currently servicing this contract and/or closure of certain facilities and projects solely related to our current operations in São Paulo, all of which will have a cash impact in the short-term of approximately R$22 million, which amount is stated after taking account of the cash expected to be generated from the sale of assets previously used in such operation. Furthermore, given the medium and long term nature of the majority of our contracts, we will not have the flexibility to immediately offset a decrease in revenues by increasing prices. Given the staggered timing of attractive competitive bidding opportunities occurring only on an intermittent basis as existing contracts come due, we will likely face challenges to quickly replace the lost revenues with new collections business. Given the size of the city of São Paulo, being the largest city in Brazil in terms of population according to 2017 IBGE data, we would likely have to secure several smaller contracts to replace the revenues lost under the contract. The significant loss of revenues could, in turn, impact our ability to comply with the covenants under any of our indebtedness or make payments as they come due.

Our contract with the municipality of Curitiba

Cavo, which we acquired in 2011, has been servicing the Curitiba contract since 1995. Our contract with the municipality of Curitiba for collections, urban cleaning and street cleaning comprised approximately 12.0% of the Company’s revenues in 2018 (12.5% in 2017). In October 2018, we won the competitive bidding process for the Curitiba collections and cleaning contract. We signed a five-year contract on January 3, 2019 with a maximum value of R$844.8 million (a reduction in price of approximately 14.1% compared with the previous contract) and are currently providing the contractual services to Curitiba. In connection to the new contract, we are required to incur in expenses in order to comply with the terms of the new contract, which could further affect our short-term liquidity and therefore impact our ability to make payments as they become due.

As of December 31, 2018 we recorded significant negative working capital and capital deficiency, we are currently in breach of certain financial covenants and contractual obligations, and our ability to avoid a judicial reorganization is dependent on our ability to successfully complete a debt restructuring and significantly improve our liquidity position

We incurred net losses from continuing operations of R$720.9 million and R$364.2 million in the years ended December 31, 2018, and 2016, respectively, and while we recorded profits from continuing operations of R$37.9 million in 2017, such results were primarily driven by the gains recorded under deferred income and social contribution taxes as a result of our recognition of tax loss carryforwards in connection with our participation in the Brazilian Tax Regularization Program. As of December 31, 2018, we recorded negative working capital (calculated as total current assets minus total current liabilities) of R$1,289.8 million and a capital deficiency (calculated as total assets minus total liabilities) of R$1,149.2 million. As of December 31, 2017, we recorded working capital of R$293.4 million and a capital deficiency of R$455.9 million, and as of December 31, 2016, we recorded negative working capital of R$1,366.2 million and a capital deficiency of R$737.1 million.

16

Table of Contents

As a result of liquidity constraints, the Company was not able to comply with the financial covenants included in its Debt Instruments for the year ended on December 31, 2018 and we are currently in breach of such covenants. In addition, on March 6, 2018, Angra confirmed the exercise of its put option to sell all of its shares of the Company. While we were required to pay the exercise price of approximately R$40.3 million by September 6, 2018, as of the date of this annual report, we have not yet made any payments to Angra due to our liquidity constraints, and the rescheduled payment terms are still being negotiated. See “Major Shareholders and Related Party Transactions—Share Put Option Agreement” and “—We are in default under the Angra Put Option Agreement, and if we are unable to reach an agreement with Angra to resolve the default, Angra can exercise remedies against us” below. Our management has identified several significant obligations arising during 2019 that require funding through liquidity, primarily relating to (a) the payments we are required to make for severance and other demobilization costs related to discontinued operations (for example, the contract with the municipality of São Paulo for cleaning services, which will be terminated on June 1, 2019, at which point we will no longer provide services in São Paulo) and (b) capital expenditures (e.g., new trucks and equipment) required in connection with contract renewals, such as the investment obligations arising under the contract with the municipality of Curitiba for cleaning services, which was renewed on January 3, 2019 for an additional five year period. Furthermore, as of December 31, 2018, the Company had aggregate overdue trade accounts of R$85.9 million, and there can be no assurance that such trade creditors will not demand immediate payment or use a variety of legal remedies to enforce their claims, which may further constrain our liquidity, further jeopardize our ability to continue as a going concern and increase the risk that we become subject to bankruptcy proceedings.

We are engaged in efforts to generate liquidity in order to improve our liquidity position and fund our obligations, including negotiations in respect of the sale of certain assets, which sales will likely require the approval of the holders of our Debt Instruments. In addition, the Company, with the approval of our board of directors, has initiated negotiations with the holders of the Debt Instruments, as well as other relevant creditors including Angra, with the goal of restructuring its financial and such other debt. In that regard, the Company engaged an outside restructuring advisor as well as outside legal counsel to advise in connection with the debt restructuring process. The Company is currently seeking to conclude the debt restructuring process in the course of 2019.

There can be no assurance that the debt restructuring process will be successful or that we will be able to generate sufficient liquidity in order to fully address our liquidity concerns. Our inability to significantly improve our liquidity position and comply with our financial covenants and other payment obligations, including overdue amounts owed to trade creditors, could have a material adverse effect on us and result in an extrajudicial reorganization or a judicially-supervised reorganization process, which may result in our shareholders losing their entire investment.

We have a significant level of indebtedness, including debt issued pursuant to the Debt Instruments, which is secured by a significant amount of our assets and contains financial covenants; we are currently in breach of our financial covenants and such breach and our high level of indebtedness generally may materially adversely affect us and our ability to successfully implement our strategic plan and continue our operations and may result in our bankruptcy.

We have substantial indebtedness. As of December 31, 2018, our total financial indebtedness, consisting primarily of outstanding balances on our debentures and working capital loans and, to a lesser extent, BNDES loans and financings and finance leases, was R$1,594.7 million, as compared to R$1,454.5 million and R$1,692.3 million as of December 31, 2017 and 2016, respectively. Of these total amounts, 97.6% of our total indebtedness was linked to floating rates as of December 31, 2018 as compared to 98.7% and 99.1% as of December 31, 2017 and 2016, respectively.

Furthermore, a significant part of our assets have been pledged as collateral to secure repayment of the Refinanced Debt. The Refinanced Debt is secured by collateral consisting of: (i) a lien on all real estate relating to the operational landfills; (ii) a lien on all material subsidiaries controlled, directly or indirectly, by us; (iii) a fiduciary assignment of the remaining balance originated from the foreclosure of liens described in this paragraph; and (iv) corporate guarantees of all material subsidiaries controlled, directly or indirectly, by us. The debt admission instrument related to our first issuance of debentures is also secured by a fiduciary assignment of certain real estate assets owned by us. In addition, the Refinanced Debt is secured by a fiduciary lien on all (except for 4.38% secured for the benefit of Angra) of the Company’s common shares as security for the payment of all obligations related to the Refinanced Debt. For further information, see “Item 5.B. Operating Financial Review and Prospects —Indebtedness—Debentures—Debt Restructuring and Refinanced Debt.”

17

Table of Contents

The Debt Instruments also contain financial and other covenants. In particular, they require us to maintain certain financial ratios, which are measured semi-annually as of June 30 and December 31 of each year, on a Company consolidated basis, starting on December 31, 2018. As of December 31, 2018, the Company did not comply with its financial covenants, i.e. (i) the Company’s consolidated annual net debt to EBITDA ratio was 7.9x and exceeded the permitted maximum ratio of 4.0x, and (ii) the debt service coverage ratio of the Company was negative 15.6x, below the mimimum ratio of 1.2x. As a consequence of ournon-compliance with the financial covenants under the Debt Instruments, lenders are entitled to accelerate the debt obligations. The Company has initiated negotiations with the holders of its Debt Instruments and we currently do not expect that the relevant creditors will accelerate the debt obligations in the near future. However, the lenders have not provided any formal waivers with respect to thenon-compliance of the financial covenants.