UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 27a-16 or 15d-16

under the Securities Exchange Act of 1934

For the month of January, 2025

Commission File Number: 001-38376

Central Puerto S.A.

(Exact name of registrant as specified in its charter)

Port Central S.A.

(Translation of registrant’s name into English)

Avenida Thomas Edison 2701

C1104BAB Buenos Aires

Republic of Argentina

+54 (11) 4317-5000

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

CENTRAL PUERTO S.A

| -2- |

Central Puerto S.A.

Consolidated financial statements for the nine-month period ended September 30, 2024

| -3- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

Registered office: Av. Edison 2701 - Ciudad Autónoma de Buenos Aires - República Argentina

FISCAL YEAR N° 33 BEGINNING JANUARY 1, 2024 FINANCIAL STATEMENTS

FOR THE NINE-MONTH PERIOD ENDED SEPTEMBER 30, 2024

CUIT (Argentine taxpayer identification number): 33-65030549-9. Date of registration with the Public Registry of Commerce:

| – | Of the articles of incorporation: March 13, 1992. |

| – | Of the last amendment to by-laws: December 29, 2022. |

Registration number with the IGJ (Argentine regulatory agency of business associations): 1.855, Book 110, Volume A of Corporations.

Expiration date of the articles of incorporation: March 13, 2091.

The Company is not enrolled in the Statutory Optional System for the Mandatory Acquisition of Public Offerings.

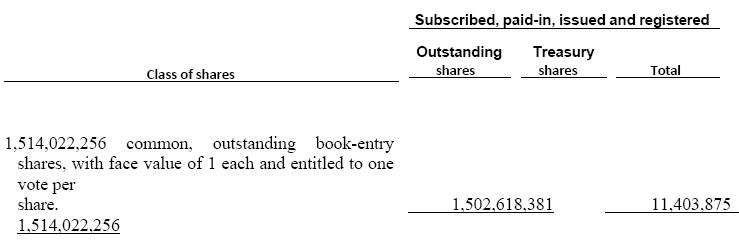

CAPITAL STRUCTURE

(stated in pesos)

| -4- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

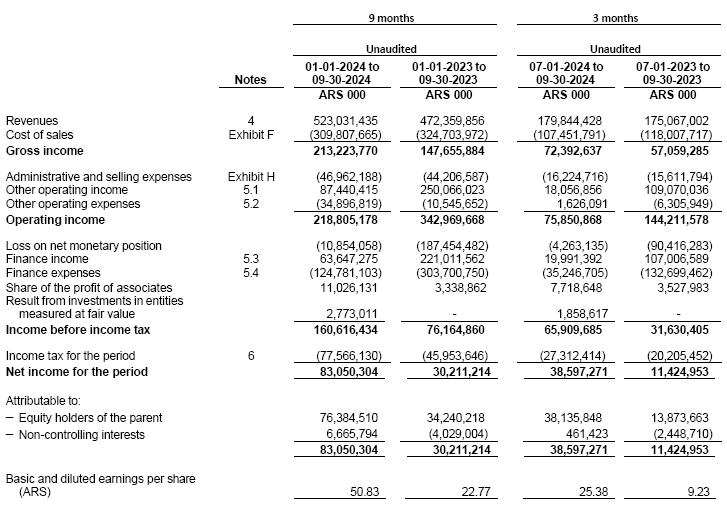

CONSOLIDATED STATEMENT OF INCOME

for the three and nine-month period ended September 30, 2024

| -5- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

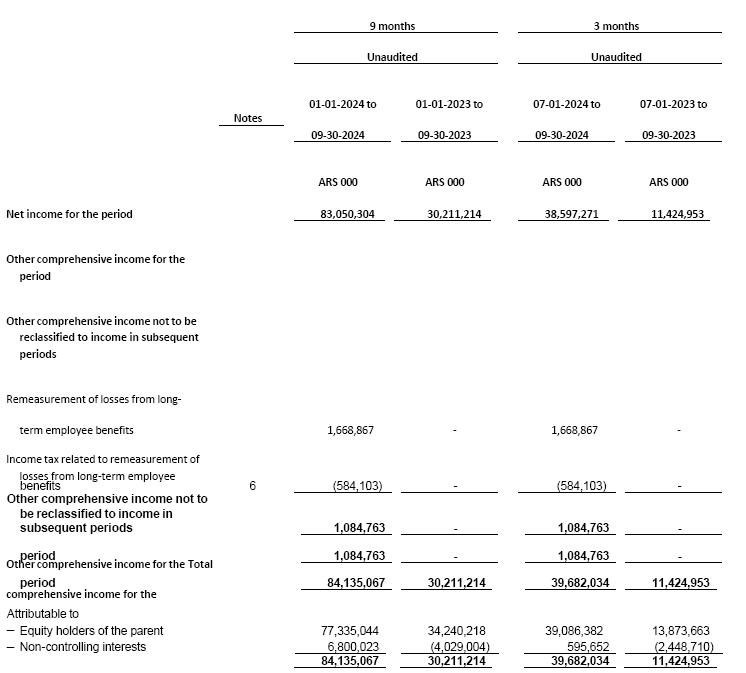

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

for the three and nine-month period ended September 30, 2024

| -6- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

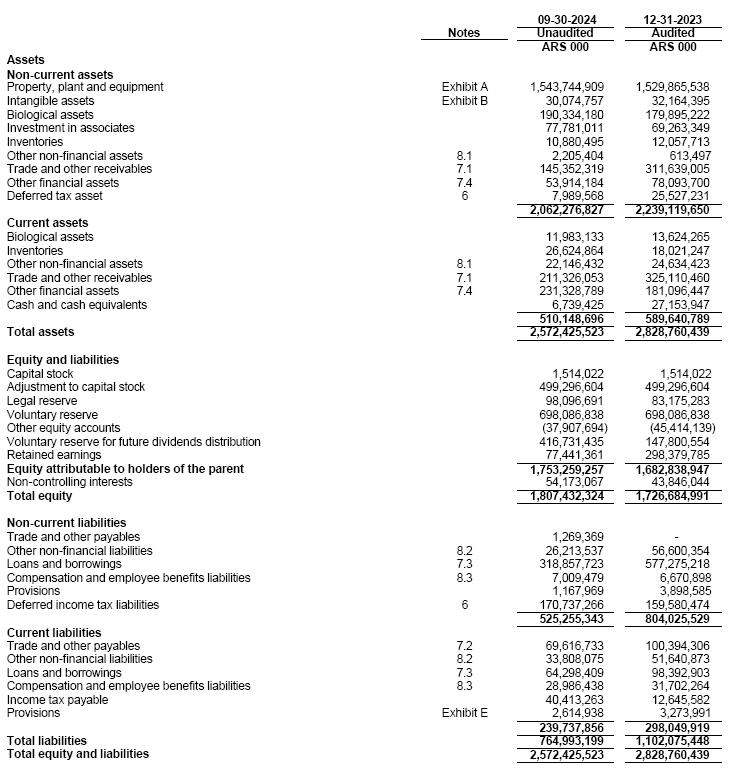

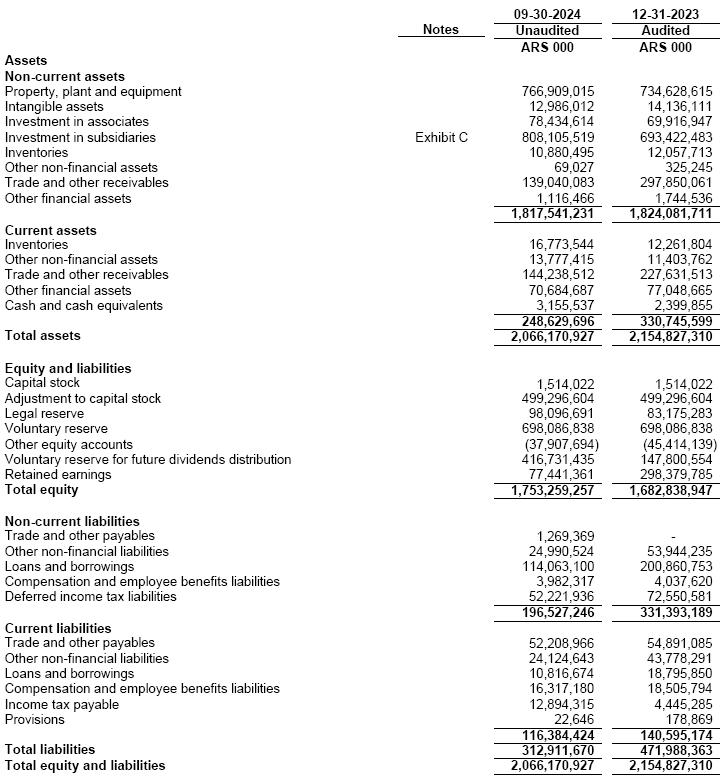

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

as at September 30, 2024

| -7- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

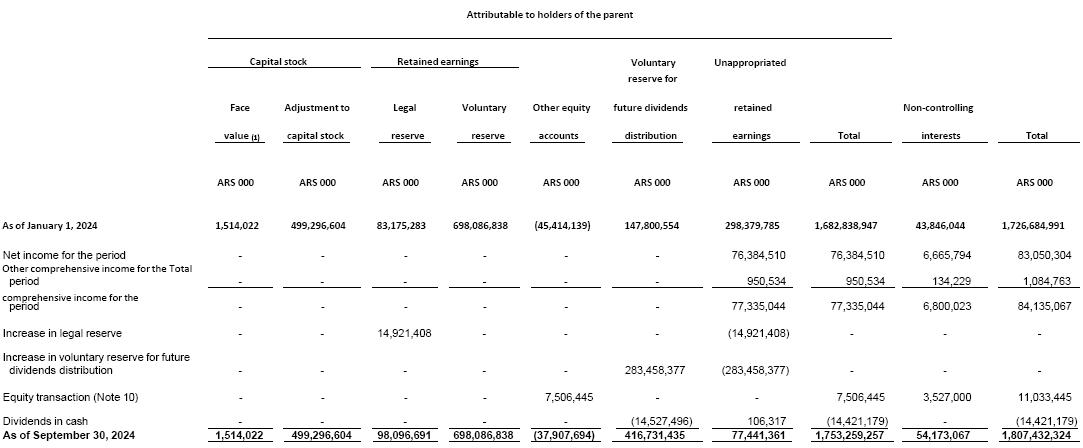

CENTRAL PUERTO S.A. |

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

for the nine-month period ended September 30, 2024

| (1) | 11,403,875 common shares are held by subsidiaries. |

| -8- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

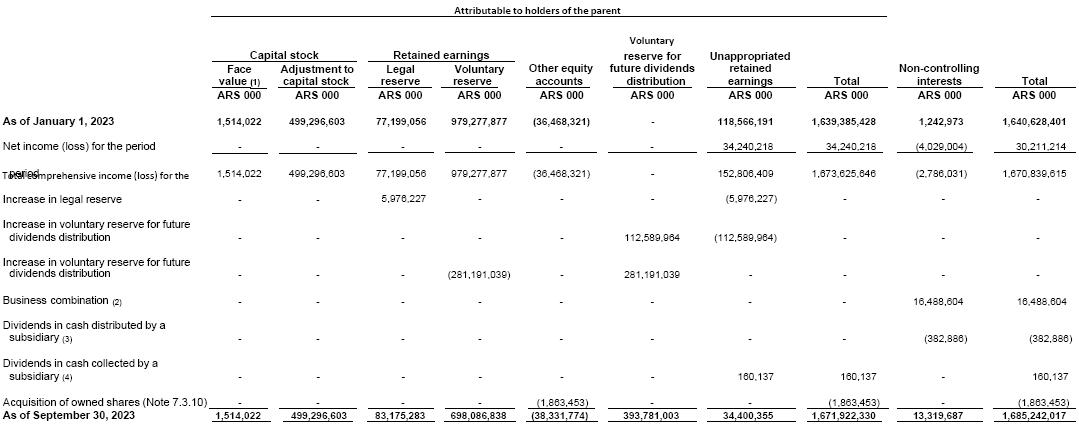

CENTRAL PUERTO S.A. |

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

for the nine-month period ended September 30, 2023

| (1) | 10,403,968 common shares are held by subsidiaries. | |

| (2) | Corresponds to the incorporation of the non-controlling interest resulting from the business combination with Central Costanera S.A. as described in Note 2.3.20 to the consolidated financial statements for the year ended December 31, 2023, already issued. | |

| (3) | Distribution of dividends in cash approved by the Shareholders’ Meeting of the subsidiary Central Vuelta de Obligado S.A. held on May 24, 2023. | |

| (4) | Dividend collection by the subsidiary Proener S.A.U. in relation to the dividends distribution decided by the Company’s Shareholders Meeting of the Company. |

| -9- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

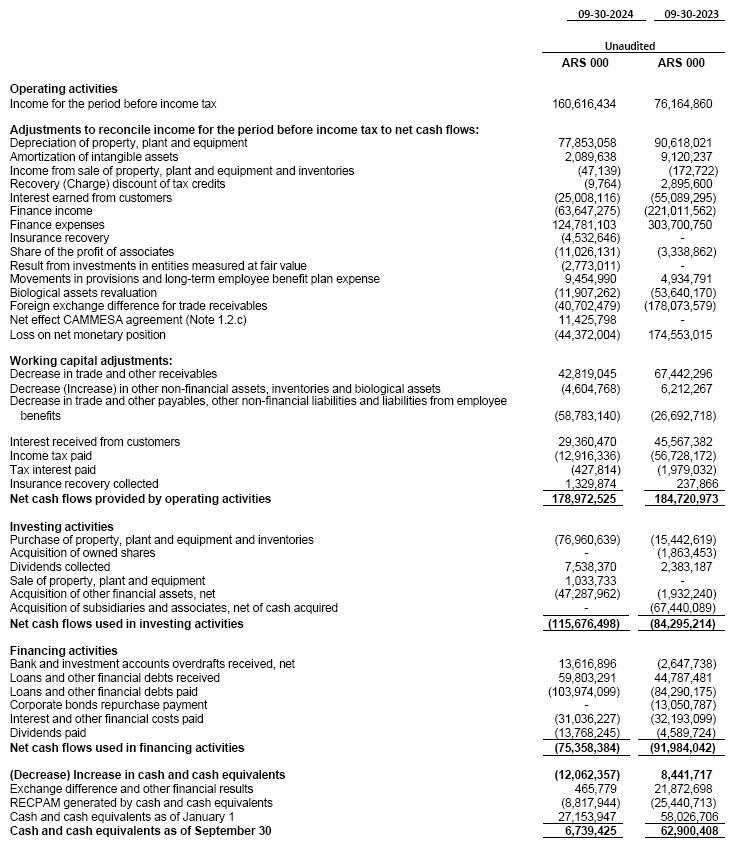

CONSOLIDATED STATEMENT OF CASH FLOWS

for the nine-month period ended September 30, 2024

| -10- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

for the nine-month period ended September 30, 2024

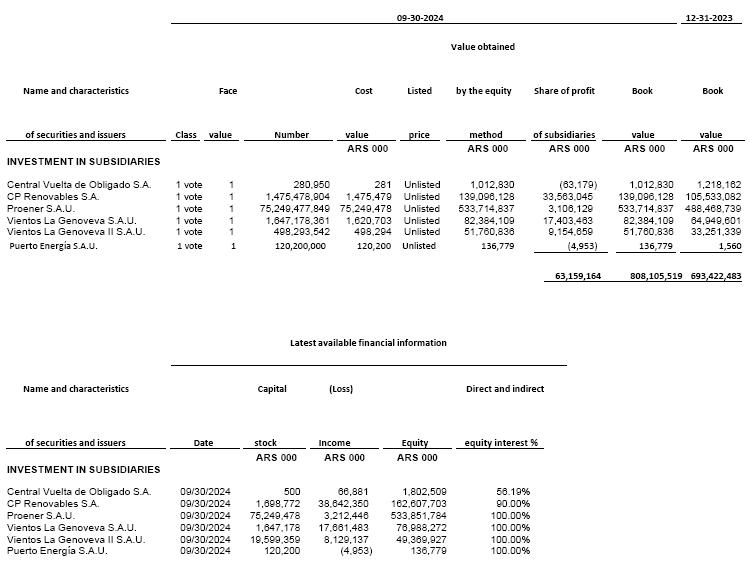

| 1. | Corporate information and main business |

Central Puerto S.A. (hereinafter the “Company”, ”we”, “us” or “CEPU”) and the companies that make up the business group (hereinafter the “Group”) form an integrated group of companies pertaining to the energy sector. The Group is mainly engaged in electric power generation.

CEPU was incorporated pursuant to Executive Order No. 122/92. We were formed in connection with privatization process involving Servicios Eléctricos del Gran Buenos Aires S.A. (“SEGBA”) in which SEGBA’s electricity generation, transportation, distribution and sales activities were privatized.

On April 1, 1992, Central Puerto S.A., the consortium-awardee, took possession over SEGBA’s Nuevo Puerto and Puerto Nuevo plants, and we began operations.

Our shares are listed on the BCBA (“Buenos Aires Stock Exchange”), and, since February 2, 2018, they are listed on the NYSE (“New York Stock Exchange”), both under the symbol “CEPU”.

In order to carry out its electric energy generation activity the Group owns the following assets:

| – | Our Puerto complex is composed of two facilities, Central Nuevo Puerto (“Nuevo Puerto”) and Central Puerto Nuevo (“Puerto Nuevo”), located in the port of the City of Buenos Aires. Our Puerto complex’s facilities include steam turbines plants and a Combined Cycle plant and has a current installed capacity of 1,747 MW. |

| – | Our Luján de Cuyo plants are located in Luján de Cuyo, Province of Mendoza and have an installed capacity of 576 MW and a steam generating capacity of 125 tons per hour. |

| – | The Group also owns the concession right of the Piedra del Águila hydroelectric power plant located at the edge of Limay river in Neuquén province. Piedra del Águila has four 360 MW generating units. |

| – | The Group is engaged in the management and operations of the thermal plants José de San Martín and Manuel Belgrano through its equity investees Termoeléctrica José de San Martín S.A. (“TJSM”) and Termoeléctrica General Belgrano S.A. (“TMB”). Those entities operate the two thermal generation plants with an installed capacity of 865 MW and 873 MW, respectively. Additionally, through its subsidiary Central Vuelta de Obligado S.A. (“CVO”) the Group is engaged in the operation of the thermal plant Central Vuelta de Obligado, with an installed capacity of 816 MW. |

| – | The thermal station Brigadier López located in Sauce Viejo, Province of Santa Fe, with an installed power of 280.5 MW (open-cycle operation). |

| – | The thermal cogeneration plant Terminal 6 - San Lorenzo located in Puerto General San Martín, Santa Fe Province, with an installed power of 391 MW and 340 tn/h of steam production. |

| – | The thermal station Costanera located in the City of Buenos Aires operates a thermal generation plant which is made by six turbo-steam units with an installed power capacity of 661 MW and two combined cycle plants with an installed power capacity of 1,128 MW. |

| – | Generation plants using renewable energy sources with a total installed capacity of 473.8 MW of commercially available installed capacity from renewable energy sources, distributed as follows: (i) wind farm La Castellana 100.8 MW; (ii) wind farm La Castellana II 15.2 MW; (iii) wind farm La Genoveva 88.2 MW; (iv) wind farm La Genoveva II 41.8 MW; (v) wind farm Achiras 48 MW; (iv) wind farm Los Olivos 22.8 MW, (vii) wind farm Manque 57 MW and (viii) solar farm Guañizuil II A 100 MW. |

| -11- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

The Group is also engaged in the natural gas distribution public sector service in the Cuyo and Centro regions in Argentina, through its equity investees belonging to ECOGAS Group. On July 19, 2018, the National Gas Regulation Entity (Enargas) filed the Company with the Registry of Traders and Trade Agreements of Enargas.

Also, through Proener S.A.U., a company fully controlled by CPSA, the Group is engaged in the forest activity since Proener S.A.U. is the parent company of: a) Forestal Argentina S.A. and Loma Alta Forestal S.A.; such companies own forestry assets which consist of 72,000 hectares approximately in Entre Ríos and Corrientes provinces, in which 43,000 hectares approximately are planted with eucalyptus and pine tree, and b) Empresas Verdes Argentina S.A., Las Misiones S.A. and Estancia Celina S.A.; such companies own forest assets that are made of approximately 89,431 hectares in Corrientes province, from which 27,300 are planted with pine tree (over a total 36,900 hectares plantable area).

Finally, the Group has begun to participate in the mining sector through an interest in the Diablillos silver and gold mining project located in northwestern Argentina (see Note 11.1).

The issuance of Group’s consolidated financial statements of the nine-month period ended September 30, 2024 was approved by the Company’s Board of Directors on November 7, 2024.

| 1.1. | Overview of Argentine Electricity Market |

Transactions among different participants in the electricity industry take place through the wholesale electricity market (“WEM”) which is a market in which generators, distributors and certain large users of electricity buy and sell electricity at prices determined by supply and demand (“Term market”) and also, where prices are established on an hourly basis based on the economic production cost, represented by the short term marginal cost measured at the system’s load center (“Spot market”). CAMMESA (Compañía Administradora del Mercado Mayorista Eléctrico Sociedad Anónima) is a quasi-government organization that was established to administer the WEM and functions as a clearing house for the different market participants operating in the WEM. Its main functions include the operation of the WEM and dispatch of generation and price calculation in the Spot market, the real-time operation of the electricity system and the administration of the commercial transactions in the electricity market.

After the Argentine economic crisis in 2001 and 2002 and the Convertibility Law, the costs of generators increased as a result of the Argentine peso devaluation. In addition, the price of fuel for their generation increased as well. The increasing generation costs combined with the freezing of rates for the final user decided at the time by National Government led to a permanent deficit in CAMMESA accounts, which faced difficulties to pay the energy purchases to generators. Due to this structural deficit, the Secretariat of Energy issued a series of regulations to keep the electricity market working despite the deficit.

| -12- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 1.2. | Amendments to WEM regulations |

| a) | Secretariat of Energy Resolution No. 574/2023, 2/2024, 33/2024 and 78/2024. PEN Decree No. 718/2024 |

On July 11, 2023, Resolution No. 574/2023 was published, which extended for 60 days (with the possibility of being extended for 60 days more) the termination date for the Concession Agreement of the Hydroelectric Power Station Piedra del Águila, among other Argentine Hydroelectric Power Stations, whose concession term ends during 2023.

On January 17, 2024, through Resolution No. 2/2024, published in the Official Gazette, the transition period of the concession agreement was extended for 60 days as from February 28, 2024. Then, through Resolution No. 33/2024, published in the Official Gazette on March 18, 2024, the termination term of the concession agreement was extended again for 60 days as from April 28, 2024, so that such term expires on June 27, 2024.

| -13- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

On May 17, 2024, through Resolution No. 78/2024, the transition period of the concession contract was extended until the end of the term established in the contract, that is, December 28, 2024.

On August 12, 2024, PEN Decree No. 718/2024 was published in the Official Gazette, which extended for one year the term to continue operating the Piedra del Águila Hydroelectric Complex to CPSA in its capacity as concessionaire, with a maximum date of December 28, 2025. The aforementioned Decree also establishes that, within one hundred and eighty days of its publication, the Secretariat of Energy will call for a National and International Public Tender in order to proceed with the sale of the stock package of the companies created for each of the hydroelectric power stations of Comahue.

| b) | Secretariat of Energy Resolution No. 9/2024, 99/2024, 193/2024, 233/2024 y 285/2024, Secretariat for the Coordination of Energy and Mining Resolution No. 20/2024 |

On February 8, 2024, Resolution No. 9/2024 of the Secretariat of Energy was published in the Official Gazette. This Resolution updated the power and energy remuneration values of the generation not committed under contracts. In addition, Exhibits I to IV of Resolution 869 were replaced and a 74% increase as from February 1, 2024 was established.

On June 14, 2024, Resolution No. 99/2024 issued by the Secretariat of Energy was published in the Official Gazette, through which the power and energy remuneration values of the generation not committed under contracts were updated. Such resolution replaces Exhibits I to V of Resolution No. 9/2024 and establishes a 25% increase as from June 1, 2024.

On August 2, 2024, Resolution No. 193/2024 issued by the Secretariat of Energy was published in the Official Gazette, through which the power and energy remuneration values of the generation not committed under contracts were updated. Such resolution replaces Exhibits I to V of Resolution No. 99/2024 and establishes a 3% increase as from August 1, 2024.

On August 30, 2024, Resolution No. 233/2024 issued by the Secretariat of Energy was published in the Official Gazette, through which the power and energy remuneration values of the generation not committed under contracts were updated. Such resolution replaces Exhibits I to V of Resolution No. 193/2024 and establishes a 5% increase as from September 1, 2024.

On September 30, 2024, Resolution No. 285/2024 issued by the Secretariat of Energy was published in the Official Gazette, through which the power and energy remuneration values of the generation not committed under contracts were updated. Such resolution replaces Exhibits I to V of Resolution No. 233/2024 and establishes a 2,7% increase as from October 1, 2024.

After the closing of the period, on November 1, 2024, Resolution No. 20/2024 issued by the Secretariat of Coordination of Energy and Mining was published in the Official Gazette, through which the power and energy remuneration values of the generation not committed under contracts were updated. Such resolution replaces Exhibits I to V of Resolution No. 285/2024 and establishes a 6% increase as from November 1, 2024.

| c) | Secretariat of Energy Resolution No 294/2024 |

On October 2, 2024, Resolution No. 294/2024 ("Resolution 294") issued by the Secretariat of Energy was published in the Official Gazette, which establishes a "Contingency and Forecast Plan for critical months of the 2024/2026 period", defining measures that cover the supply of generation, transportation and distribution of energy.

| -14- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

For generation, an additional, complementary and exceptional remuneration is proposed subject to a commitment of availability in machines that are not committed to contracts with the MEM or that have not adhered to S.E. Resolution No. 59/2023.

Adhering to this regulation, generators assume a commitment to power availability for each unit, at certain times of the day, characterized as critical, during the working days of the summer months (December to March) and winter (June to August). Remuneration prices are defined in dollars, both for compliance with power availability (US$2,000/MW-month) and for the energy generated in the hours included in the evaluation periods indicated above, as shown below:

To determine the remuneration of each unit, the prices of power and energy will be affected by a criticality factor, which may vary between 0.75 and 1.25, depending on the nodes in which the units are linked to the transmission system.

The units belonging to the Group that may adhere to this resolution are the ST (steam turbine) units located in Buenos Aires and Luján de Cuyo and the GT (gas turbine) units located in Luján de Cuyo and at the Brigadier López thermal power plant. As of the date of issuance of these financial statements, those units have not been adhered to Resolution 294.

| d) | Secretariat of Energy Resolution No 58/2024 y 66/2024 |

On May 8, 2024, Secretariat of Energy Resolution No. 58/2024 as amended by Resolution No. 66/2024 was published in the Official Gazette (the “Resolution”) whereby an exceptional, temporary, and unique payment regime was established for MEM transactions for December 2023, and January and February 2024. Such Resolution (i) orders CAMMESA to prepare and determine the amounts of the credit for the economic transactions with each of MEM Creditor Agents in a term of 5 (five) working days as from the entering into force of the Resolution; (ii) establishes that the lack of agreement regarding such amounts authorizes the Creditor Agents to resort to the corresponding judicial, administrative and/or out-of-court means; (iii) and establishes that once the amounts are determined and the corresponding agreements entered into, CAMMESA shall pay the transactions as follows: a) the settlement for the transactions for December 2023 and January 2024 shall be paid 10 (ten) working days counted as from the date of individual agreements through the delivery of bond AE38 USD; the calculation of nominal amounts to be delivered per each bond shall be at the reference exchange rate (Communication “A” 3500) at the quote in force at closing on the date of the formal acceptance by Creditor Agents; b) settlement for February 2024 shall be paid with available funds in bank accounts authorized in CAMMESA for collection and with the available funds for the transferences made by the Argentine State to the Unified Fund destined at the Stabilization Fund. The Group´s MEM economic transactions for December 2023 and January and February 2024 amount to 30,681,066, 30,930,604 and 40,511,360 (VAT included), respectively.

On May 23, 2024, the Group entered into agreements with CAMMESA within the framework established by the Resolution. As a result of such agreements, the Group recorded a 22,941,766 loss under the line “Agreements with CAMMESA -SE Resolutions No. 58/2024 and 66/2024” within the item “Other operating expenses” of the consolidated income statement for the nine-month period ended September 30, 2024. During the months of May and June 2024, the AE38 USD bond swap was made for MEM economic transactions of December 2023 and January 2024, and the total MEM economic transaction of February 2024 has been collected.

| -15- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 2. | Basis of preparation of the consolidated financial statements |

| 2.1. | Applied Professional Accounting Standards |

The Company prepares its condensed consolidated financial statements pursuant to the regulations in force of the Argentine Securities Commission (CNV) on Chapter III, Title IV of the CNV Regulations (N.T. 2013 as amended). Under section 1 of such section of the Regulations, companies issuing negotiable instruments must present their condensed consolidated financial statements applying Technical Resolution 26 of the Argentine Federation of Professional Councils in Economic Sciences (“FACPCE”), which resolution establishes the application of the International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”), its amendments and adoption circulars of IFRS that FACPCE may establish in accordance with such Technical Resolution. Interim condensed financial statements must apply the International Accounting Standard 34 (“IAS”) “Interim Financial Reporting”.

| 2.2. | Basis of presentation and consolidation |

These condensed consolidated financial statements for the nine-month period ended September 30, 2024 were prepared applying the financial information framework prescribed by CNV as mentioned in Note 2.1.

In preparing these condensed consolidated financial statements, the Group applied the significant accounting policies, estimates and assumptions described in notes 2.3 and 2.4 of the issued financial statements for the year ended December 31, 2023.

These condensed consolidated financial statements include all the necessary information for a proper understanding by their users of the relevant facts and transactions subsequent to the issuance of the last annual financial statements for the year ended December 31, 2023 and up to the date of these interim condensed consolidated financial statements. However, these condensed consolidated financial statements include neither all the information nor the disclosures required for the annual financial statements prepared in accordance with IAS 1 (Presentation of financial statements). Therefore, these condensed consolidated financial statements must be read together with the annual financial statements for the year ended December 31, 2023.

The Group’s consolidated financial statements are presented in Argentine pesos, which is the Group’s functional currency, and all values have been rounded to the nearest thousand (ARS 000), except when otherwise indicated.

| 2.2.1. | Measuring unit |

The financial statements as at September 30, 2024, including the figures for the previous period (this fact not affecting the decisions taken on the financial information for such periods) were restated to consider the changes in the general purchasing power of the functional currency of the Company (Argentine peso) pursuant to IAS 29 and General Resolution No. 777/2018 of the Argentine Securities Commission. Consequently, the financial statements are stated in the current measurement unit at the end of the reported period.

The effects caused by the application of IAS 29 are detailed in note 2.2.2 to the issued consolidated financial statements for the year ended December 31, 2023.

Regard being had to the mentioned index, the inflation was of 101.58%% and 103.15%% in the nine-month periods ended September 30, 2024 and 2023, respectively.

| -16- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 2.3. | Changes in accounting policies |

New standards and interpretations adopted

As from the fiscal year beginning January 1, 2024, the Group has applied for the first time certain new and/or amended standards and interpretations as issued by the IASB.

Below is a brief description of the new and/or amended standards and interpretations adopted by the Group and their impact on these consolidated financial statements.

Amendments to IAS 1: Classification of Liabilities as Current or Non-current

In January 2020 and October 2022, the IASB issued amendments to paragraphs 69 to 76 of IAS 1 to specify the requirements for classifying liabilities as current or non-current. The amendments clarify: (i) What is meant by a right to defer settlement, (ii) that a right to defer must exist at the end of the reporting period; (iii) that classification is unaffected by the likelihood that an entity will exercise its deferral right and (iv) that only if an embedded derivative in a convertible liability is itself an equity instrument would the terms of a liability not impact its classification.

In addition, a requirement has been introduced to require disclosure when a liability arising from a loan agreement is classified as non-current and the entity’s right to defer settlement is contingent on compliance with future covenants within twelve months.

These amendments have not had a significant impact on the Group's condensed financial statements.

Supplier Finance Arrangements - Amendments to IAS 7 and IFRS 7

In May 2023, the IASB issued amendments to IAS 7 Statement of Cash Flows and IFRS 7 Financial Instruments: Disclosures to clarify the characteristics of supplier finance arrangements and require additional disclosure of such arrangements. The disclosure requirements in the amendments are intended to assist users of financial statements in understanding the effects of supplier finance arrangements on an entity’s liabilities, cash flows and exposure to liquidity risk.

The transition rules clarify that an entity is not required to present information in any interim period in the year of initial application of the amendments. Therefore, these amendments have had no significant impact on the Group's condensed financial statements.

Amendments to IFRS 16: Lease liability in subsequent sale and leaseback

In September 2022, IASB issued amendments to IFRS 16 to clarify the requirements a seller-lessee uses to measure liabilities in a leaseback from a subsequent sale and leaseback transaction to guarantee the seller- lessee does not recognize any amount of the gain or loss that relates to the right of use it retains.

These amendments have not had a significant impact on the Group's condensed financial statements.

| -17- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 3. | Operating segments |

The following provides summarized information of the operating segments for the nine-month periods ended September 30, 2024 and 2023:

| (1) | Includes information from associates. | |

| (2) | Includes income (expenses) related to resale of gas transport and distribution capacity. | |

| (3) | Includes result from investments in entities measured at fair value. |

| -18- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 4. | Revenues |

| 5. | Other income and expenses |

| 5.1. | Other operating income |

| (1) | Includes 16,384,814 and 17,793,349 related to CVO receivables for the nine-month periods ended September 30, 2024 and 2023, respectively. | |

| (2) | Includes 37,435,505 and 169,655,393 related to CVO receivables for the nine-month periods ended September 30, 2024 and 2023, respectively. | |

| (3) | Includes 4,706,742 and 6,978,157 related to CVO receivables for the three-month periods ended September 30, 2024 and 2023, respectively. | |

| (4) | Includes 10,314,491 and 76,452,089 related to CVO receivables for the three-month periods ended September 30, 2024 and 2023, respectively. |

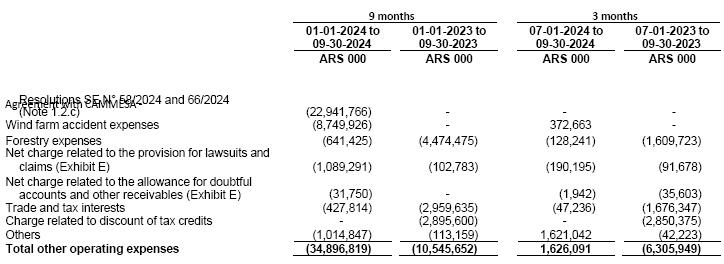

| 5.2. | Other operating expenses |

| -19- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

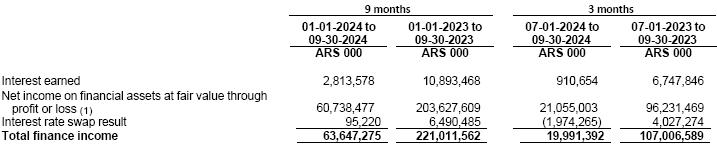

| 5.3. | Finance income |

| (1) | Net of 349,807 corresponding to turnover tax for the nine-month periods ended September 30, 2024 and 910,484 for the nine-month period ended September 30, 2023. |

| 5.4. | Finance expenses |

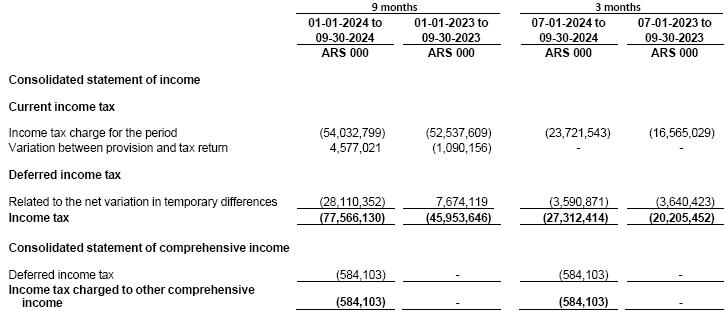

| 6. | Income tax |

The major components of income tax during the nine-month periods ended September 30, 2024 and 2023, are the following:

Consolidated statements of income and comprehensive income

| -20- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

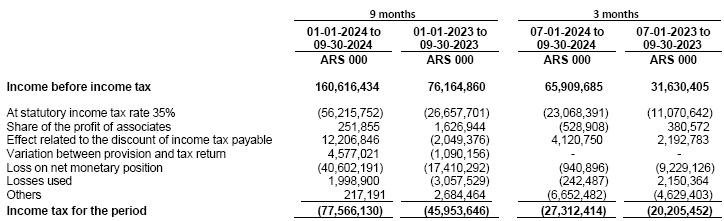

The reconciliation between income tax in the consolidated statement of income and the accounting income multiplied by the statutory income tax rate for the nine-month periods ended September 30, 2024 and 2023, is as follows:

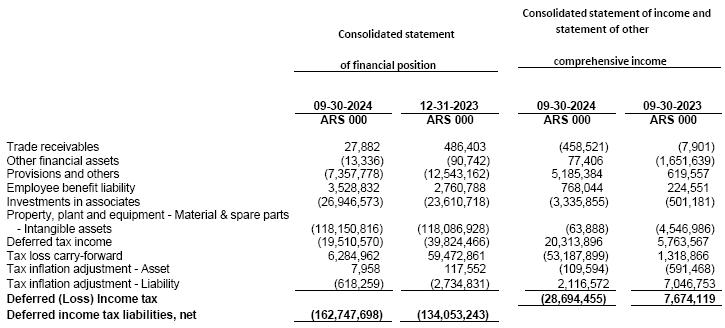

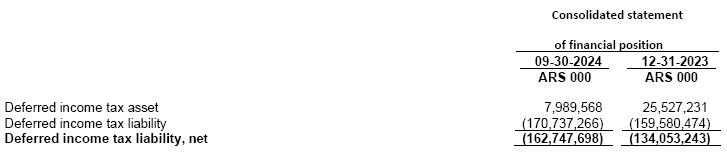

Deferred income tax

Deferred income tax relates to the following:

Deferred income tax liability, net, disclosed in the consolidated statement of financial position

| -21- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 7. | Financial assets and liabilities |

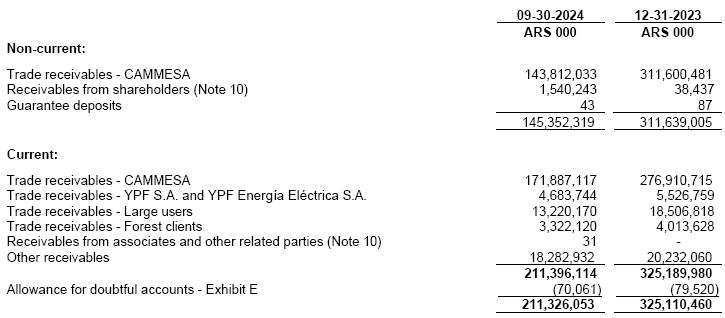

| 7.1. | Trade and other receivables |

CVO receivables: As described in note 1.2.a) to the issued consolidated financial statements as of December 31, 2023, in 2010 the Company approved a new agreement with the former Energy Secretariat (the “CVO agreement”) and as from March 20, 2018, CAMMESA granted the commercial operations as a combined cycle of Central Vuelta de Obligado thermal power plant (the “Commercial Approval”).

Receivables under CVO agreement are disclosed under “Trade receivables - CAMMESA”. CVO receivables are expressed in USD and they accrue LIBOR interest at a 5% rate. Due to the fact that as from June 30, 2023, the calculation and publication of the LIBO rate were suspended, as at the issuance date of these financial statements, the Company and the enforcement authorities are still in the process of defining the new applicable interest rate, in accordance with the recommendations of the local and international regulatory entities, the market good practices and the characteristics and particulars of such credit.

As a consequence of the Commercial Approval and in accordance with the CVO agreement, the Company collects the CVO receivables converted in US dollars in 120 equal and consecutive installments.

During the nine-month periods ended September 30, 2024 and 2023, collections of CVO receivables belonging to CPSA amounted to 56,610,401 and 57,058,198, respectively. Also, collections of CVO receivables belonging to Central Costanera S.A. amounted to 2,870,033 and 2,212,742 during the nine-month period ended September 30, 2024 and during the period between the acquisition date of such company and September 30, 2023, respectively.

The information on the Group’s objectives and credit risk management policies is included in Note 17 to the issued consolidated financial statements as of December 31, 2023.

The breakdown by due date of trade and other receivables due as of the related dates is as follows:

| -22- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 7.2. | Trade and other payables |

Trade payables are non-interest bearing and are normally settled on 60-day terms, except for those with longer maturities as defined in the respective contracts.

The information on the Group’s objectives and financial risk management policies is included in Note 17 to the issued consolidated financial statements as of December 31, 2023.

For the terms and conditions of payables to related parties, refer to Note 10.

| 7.3. | Loans and borrowings |

| (1) | Net of debt issuance costs. |

| 7.3.1. | Loans from the IIC-IFC Facility |

On October 20, 2017 and January 17, 2018, CP La Castellana S.A.U. and CP Achiras S.A.U. (both of which are subsidiaries of CPR), respectively, agreed on the structuring of a series of loan agreements in favor of CP La Castellana S.A.U. and CP Achiras S.A.U., for a total amount of USD 100,050,000 and USD 50,700,000, respectively, with: (i) International Finance Corporation (IFC) on its own behalf, as Eligible Hedge Provider and as an implementation entity of the Intercreditor Agreement Managed Program; (ii) Inter-American Investment Corporation (“IIC”), as lender on its behalf, acting as agent for the Inter-American Development Bank (“IDB”) and on behalf of IDB as administrator of the Canadian Climate Fund for the Private Sector in the Americas (“C2F”, and together with IIC and IDB, “Group IDB”, and together with IFC, “Senior Creditors”).

In accordance with the terms of the agreement subscribed by CP La Castellana S.A.U., USD 5 million accrue an interest rate equal to LIBOR plus 3.5%, and the rest at LIBOR plus 5.25%, until August 15, 2023. As a consequence of the suspension of LIBO rate, occurred on June 30, 2023, CP La Castellana S.A.U., together with IDB Group and IFC amended loan agreements on June 29, 2023, replacing LIBO rate with the Secured Overnight Financing Rate (SOFR) plus a fixed Credit Adjustment Spread (CAS) of 0.26161% applicable as from August 15, 2023. The loan is amortizable quarterly in 52 equal and consecutive installments as from February 15, 2019.

| -23- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

In accordance with the terms of the agreement subscribed by CP Achiras, USD 40.7 million accrue a fixed interest rate equal to 8.05%, and the rest accrue a 6.77% fixed interest rate. The loan is amortizable quarterly in 52 equal and consecutive installments as from May 15, 2019.

As per the executed loan agreement and among other obligations undertaken, the subsidiaries CP La Castellana and CP Achiras committed to keep a Historical Senior Debt Service Coverage Ratio of at least 1.20:1.00 until the project’s termination date. Such ratio is calculated by dividing the addition of EBITDA for the last most recent four financial quarters previous to the calculation date by the amount of all scheduled overdue debt payments in those four quarters.

In addition, as guarantee of the obligations undertaken, the subsidiaries CP La Castellana and CP Achiras has a pledge in favor of IFC and IIC with a first degree recording on the financed asset.

Other related agreements and documents, such as the Guarantee and Sponsor Support Agreement (the “Guarantee Agreement” by which CPSA completely, unconditionally and irrevocably guarantees, as the main debtor, all payment obligations undertaken by CP La Castellana and CP Achiras until the projects reach the commercial operations date) hedging agreements, guarantee trusts, a mortgage, guarantee agreements on shares, guarantee agreements on wind turbines, direct agreements and promissory notes have been signed.

As of February 16, 2023, CP La Castellana and CP Achiras has fulfilled all the requirements and conditions to prove the occurrence of the project’s compliance date. As a result, the Guarantee Agreement posted by CPSA was released.

We also agreed to maintain, unless otherwise consented to in writing by each senior lender, ownership and control of the CP La Castellana and CP Achiras as follows: (i) until each project completion date, (a) we shall maintain (x) directly or indirectly, at least seventy percent (70%) beneficial ownership of CP La Castellana and CP Achiras; and (y) control of the CP La Castellana and CP Achiras; and (b) CP Renovables shall maintain

(x) directly, ninety-five percent (95%) beneficial ownership of CP La Castellana and CP Achiras; and (y) control of CP La Castellana and CP Achiras. In addition, (ii) after each project completion date, (a) we shall maintain

(x) directly or indirectly, at least fifty and one tenth percent (50.1%) beneficial ownership of each of CP La Castellana, CP Achiras and CP Renovables; and (y) control of each of CP La Castellana, CP Achiras and CP Renovables; and (b) CP Renovables shall maintain control of CP La Castellana and CP Achiras. Finally, there are certain requirements to be fulfilled in order to distribute dividends from CP La Castellana and CP Achiras.

As of September 30, 2024, the Group has met such obligations.

Under the subscribed trust guarantee agreement, as of September 30, 2024 and as of December 31, 2023, there are trade receivables with specific assignment for the amount of 5,061,911 and 4,191,164, respectively.

As of September 30, 2024 and as of December 31, 2023, the balance of these loans amounts to 80,355,942 and 150,947,645, respectively.

| -24- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 7.3.2. | Borrowing from Kreditanstalt für Wiederaufbau (“KfW”) |

On March 26, 2019 the Company entered into a loan agreement with KfW for an amount of USD 56 million in relation to the acquisition of two gas turbines, equipment and related services relating to the Luján de Cuyo cogeneration unit project.

In accordance with the terms of the agreement, the loan accrues an interest equal to LIBOR plus 1.15%. As a consequence of the suspension of LIBO rate, occurred on June 30, 2023, the Company and KfW amended the loan agreement on June 30, 2023, replacing LIBO rate with the Secured Overnight Financing Rate (SOFR) plus a fixed Credit Adjustment Spread (CAS) of 0.26161%. The loan is amortizable quarterly in 47 equal and consecutive installments as from the day falling six months after the commissioning of the gas turbines and equipment.

| -25- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

Pursuant to the loan agreement, among other obligations, CPSA has agreed to maintain as of December 31 of each year a debt ratio of no more than 3.5:1.00. As of the date of issuance of this financial statement, the Company has complied with that requirement.

As of September 30, 2024 and as of December 31, 2023, the balance of this loan amounts to 23,072,659 and 49,450,841, respectively.

| 7.3.3. | Loan from Citibank N.A., JP Morgan Chase Bank N.A. and Morgan Stanley Senior Funding INC. |

On June 12, 2019, the Company entered into a loan agreement with Citibank N.A., JP Morgan Chase Bank N.A. and Morgan Stanley Senior Funding INC. for USD 180 million to fund the acquisition of the Thermal Station Brigadier López.

According to the terms of the agreement, this loan accrues at a variable interest rate based on the LIBO rate plus a margin. Due to the suspension of the LIBO rate on June 30, 2023, the Company and Citibank N.A., JP Morgan Chase Bank N.A. and Morgan Stanley Senior Funding INC amended the loan agreement on August 16, 2023, replacing the LIBO rate with the Secured Overnight Financing Rate (SOFR) plus a Credit Adjustment Spread (CAS) of 0.26161% applicable as from September 12, 2023.

Considering the restrictions imposed by the Argentine Central Bank (“BCRA”) described in Note 13, two amendments to the loan agreement were entered into on December 22, 2020 and June 15, 2021 whereby the amortization calendar was modified so as to comply with BCRA requirements. As part of such amendments, the applicable interest rates were increased in 200 basic points and then in 125 basic points, and limitations were established for the payment of dividends as follows: no dividends could be paid during 2021, only up to USD 25 million could be paid during 2022, and only up to USD 20 million could be paid during 2023.

On October 19, 2023, the Company paid in advance the principal for an amount of USD 49,043,078, under the terms and conditions of the loan agreement, thus after such payment, the principal owed amounts to USD 6,056,922 due on January 2024. This way, more than 80% of the loan was repaid. Therefore, as from that date, the dividend payment limitation was no longer effective.

As of December 31, 2023, the balance of this loan amounted to 9,912,539. The loan balance was totally paid at due date.

| 7.3.4. | Loan from the IFC to the subsidiary Vientos La Genoveva S.A.U. |

On June 21, 2019, Vientos La Genoveva S.A.U., a CPSA subsidiary, entered into a loan agreement with IFC on its own behalf, as Eligible Hedge Provider and as an implementation entity of the Managed Co-Lending Portfolio Program (MCPP) administered by IFC, for an amount of USD 76.1 million.

Pursuant to the terms of the agreement subscribed with Vientos La Genoveva S.A.U., this loan accrues an interest rate equal to LIBOR plus 6.50% until August 15, 2023. As a consequence of the suspension of LIBO rate, occurred on June 30, 2023, Vientos La Genoveva S.A.U. together with IFC amended this agreement on June 14, 2023, replacing LIBO rate with the Secured Overnight Financing Rate (SOFR) plus a fixed Credit Adjustment Spread (CAS) of 0.26161% applicable as from August 15, 2023. The loan is amortizable quarterly in 55 installments as from November 15, 2020.

As per the executed loan agreement and among other obligations undertaken, the subsidiary Vientos La Genoveva S.A.U. committed to keep a Historical Senior Debt Service Coverage Ratio of at least 1.20:1.00 until the project’s termination date. Such ratio is calculated by dividing the addition of EBITDA for the last most recent four financial quarters previous to the calculation date by the amount of all scheduled overdue debt payments in those four quarters.

In addition, as guarantee of the obligations undertaken, the subsidiary Vientos La Genoveva S.A.U. has a pledge in favor of IFC with a first degree recording on the financed asset.

| -26- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

Other related agreements and documents, such as the Guarantee and Sponsor Support Agreement (the “Guarantee Agreement” by which CPSA completely, unconditionally and irrevocably guarantees, as the main debtor, all payment obligations undertaken by Vientos La Genoveva S.A.U until the project reaches the commercial operations date) hedging agreements, guarantee trusts, guarantee agreements on shares, guarantee agreements on wind turbines, direct agreements and promissory notes have been signed.

Pursuant to the Guarantee Agreement, among other customary covenants for this type of facilities, CPSA has committed, until the project completion date, to maintain (i) a leverage ratio of not more than 3.5:1.00; and (ii) an interest coverage ratio of not less than 2.00:1.00. In addition, CPSA, upon certain conditions, agreed to make certain equity contributions to Vientos La Genoveva S.A.U.

Finally, there are certain requirements to be fulfilled in order to distribute dividends from Vientos La Genoveva S.A.U.

As of September 30, 2024, the Group has met such obligations.

Under the subscribed trust guarantee agreement, as of September 30, 2024 as of December 31, 2023, there are trade receivables with specific assignments for the amounts of 8,449,526 and 11,132,578, respectively.

As of September 30, 2024 and as of December 31, 2023, the balance of the loan amounts to 56,089,189 and 101,141,518, respectively.

| 7.3.5. | Loan from Banco de Galicia y Buenos Aires S.A. to CPR Energy Solutions S.A.U. |

On May 24, 2019, CPR Energy Solutions S.A.U. (subsidiary of CPR) entered into a loan agreement with Banco de Galicia y Buenos Aires S.A. for an amount of USD 12.5 million to fund the construction of the wind farm “La Castellana II”.

According to the executed agreement, this loan accrues a fixed interest rate equal to 8.5% during the first year, which will be increased 0.5% per annum until the sixty-first interest period. The loan is amortizable quarterly in 25 installments as from May 24, 2020.

As per the executed loan agreement, the subsidiary CPR Energy Solutions S.A.U. committed to keep: (i) a financial debt and EBITDA ratio lower than 2.25, and (ii) an EBITDA and financial debts services ratio higher than 1.10, both until the total payment of the owed amounts. As of June 29, 2024, the subsidiary obtained waivers to comply with the mentioned ratios and other contractual obligations in relation to the wind farm accident expenses included in the line of Other operating expenses of the income statement for the nine-month period ended on such date. Finally, there are certain requirements such subsidiary must fulfill for dividend payments.

In addition, as guarantee of the obligations undertaken, the subsidiary CPR Energy Solutions S.A.U. has a pledge in favor of Banco de Galicia y Buenos Aires with a first degree recording on the financed asset.

Other agreements and related documents, like the Collateral (in which CPSA totally, unconditionally and irrevocably guarantees, as main debtor, all the payment obligations assumed by CPR Energy Solutions S.A.U. until total fulfillment of the guaranteed obligations or until the project reaches the commercial operation date, what it happens first) -, guarantee agreements on shares, guarantee agreements on wind turbines, promissory notes and other agreements have been executed.

On September 3, 2021, CPR Energy Solutions S.A.U. has fulfilled all the requirements and conditions to prove the occurrence of the project’s compliance date. As a result, the Collateral posted by the Company was released.

As of September 30, 2024 and as of December 31, 2023, the balance of this loan amounts to 3,891,090 and 9,076,208, respectively.

| -27- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 7.3.6. | Loan from Banco Galicia y Buenos Aires S.A. to subsidiary Vientos La Genoveva II S.A.U. |

On July 23, 2019, subsidiary Vientos La Genoveva II S.A.U. entered into a loan agreement with Banco de Galicia y Buenos Aires S.A. for an amount of USD 37.5 million.

According to the executed agreement, this loan accrues LIBOR plus 5.95% As a consequence of the suspension of LIBO rate, occurred on June 30, 2023, Vientos La Genoveva II S.A.U. and Banco de Galicia y Buenos Aires S.A. entered into an amendment agreement on July 21, 2023, whereby the interest rate changed to the Secured Overnight Financing Rate (SOFR) plus a fixed Credit Adjustment Spread (CAS) of 0.42826% applicable as of July 24, 2023. The loan is amortizable quarterly in 26 installments starting on the ninth calendar month counted from the disbursement date.

Within the framework of the loan agreement, the subsidiary Vientos La Genoveva II S.A.U. committed to keep: (i) a financial debt and EBITDA ratio lower than 3.75 until the end of June 2025 and lower than 2.25 from that date onwards; and (ii) an EBITDA and financial debts services ratio higher than 1.00 until late June 2025 and higher than 1.10 from that date onwards, both until the total payment of the owed amounts. Finally, there are certain requirements such subsidiary must fulfill for dividend payments. As of September 30, 2024, the subsidiary has met such obligations.

In addition, as guarantee of the obligations undertaken, the subsidiary Vientos la Genoveva II S.A.U. has a pledge in favor of Banco de Galicia y Buenos Aires with a first degree recording on the financed asset.

Other agreements and related documents, like the Collateral (in which CPSA totally, unconditionally and irrevocably guarantees, as main debtor, all the payment obligations assumed by Vientos La Genoveva II S.A.U. until total fulfillment of the guaranteed obligations or until the project reaches the commercial operation date, what it happens first) -, guarantee agreements on shares, guarantee agreements on wind turbines, direct agreements and promissory notes have been signed.

On September 3, 2021, Vientos La Genoveva II S.A.U. has fulfilled all the requirements and conditions to prove the occurrence of the project’s compliance date. As a result, the Collateral posted by the Company was released.

As of September 30, 2024 and as of December 31, 2023, the balance of this loan amounts to 11,863,790 and 26,958,649, respectively.

| 7.3.7. | Financial trust corresponding to Thermal Station Brigadier López |

Within the framework of the acquisition of Thermal Station Brigadier López, the Company assumed the capacity of trustor in the financial trust previously entered into by Integración Energética Argentina S.A., which was the previous owner of the thermal station. The financial debt balance at the transfer date of the thermal station was USD 154,662,725.

According to the provisions of the trust agreement, the financial debt accrued an interest rate equal to the LIBO rate plus 5% or equal to 6.25%, whichever is higher, and it was monthly amortizable. On April 5, 2022, this loan has been paid in full.

Under the subscribed trust guarantee agreement, as of September 30, 2024 and as of December 31, 2023, there are trade receivables with specific assignment for the amounts of 884,757 and 1,783,501, respectively.

As of the date of these financial statements, procedures needed for the financial trust liquidation are being made.

| 7.3.8. | CP Manque S.AU. and CP Los Olivos S.A.U. Program of Corporate Bonds |

On August 26, 2020, under Resolution No. RESFC-2020 - 20767 - APN.DIR#CNVM, the public offering of the Global Program for the Co-Issuance of Simple Corporate Bonds (not convertible into shares) by CP Manque S.A.U. and CP Los Olivos S.A.U. (both subsidiaries of CPR, and together the “Co-issuers”) for the amount of up to USD 80,000,000 was authorized.

| -28- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

Within the framework of the mentioned program, on September 2, 2020, Corporate Bonds Class I were issued for an amount of USD 35,160,000 at a fix 0% interest rate expiring on September 2, 2023; and Corporate Bonds Class II were issued for 1,109,925 at a variable interest rate equivalent to BADLAR, plus an applicable margin of 0.97% expiring on September 2, 2021. After such maturity date, Corporate Bonds Class I and Class II were fully paid.

Finally, on June 26, 2024 and considering the decisions taken at the Special General Shareholders’ Meetings of Co-Issuers dated May 13, 2024, CNV decided to cancel the authorization duly granted to Co-Issuers for the Public Offering of its corporate bonds, the advanced cancellation of the mentioned global co-issuance program and the ending of CNV corporate control over Co-Issuers.

| 7.3.9. | CPSA Notes Program |

On July 31, 2020, the Special Shareholders’ Meeting of the Company approved the creation of a new global issuance program of corporate bonds for a maximum amount of up to USD 500,000,000 (or its equivalent in other currency), which shall be issued at short, mid or long term, simple, not convertible into shares, under the terms of the Corporate Bonds Act (the “Program”). Moreover, the Board of Directors was granted the powers to determine and establish the conditions of the Program and of the corporate bonds to be issued under it provided they had not been expressly determined at the Shareholders’ Meeting. On October 29, 2020, CNV approved the creation of such program, which shall expire on October 29, 2025, in accordance with the regulations in force.

Within this program framework, the Company issued two types of corporate bonds. On the one hand, on September 17, 2023, the paying in and liquidation of the Class A Corporate Bond (CB) took place, denominated, paid-in and payable in US dollars abroad. The characteristics of this CB are the following: i) face value issued: USD 37,232,818, ii) interest rate, determined by bidding: 7%, iii) periodicity of the interest coupon: six months, iv) amortization: bullet, v) term: 30 months to be counted as from September 17, 2023 and vi) applicable law and deposit place: Argentina, Caja de Valores S.A. On the other hand, on October 17, 2023, the paying in and liquidation of the international bond denominated “10% Senior Notes due 2025” (Class B CB) took place. Such bond is denominated, paid-in and payable in US dollars abroad, under the Reg S scheme. The characteristics of this bond are the following: i) face value issued: USD 50,000,000, ii) interest rate, determined by bidding: 10%, iii) periodicity of the interest coupon: six months, iv) amortization: bullet, v) term: 24 months to be counted as from October 17, 2023 and vi) applicable law and deposit place: New York, Euroclear.

Finally, on October 20, 2023, the Company decided to reopen the Class A CB. This procedure allows to offer in the market a security which replicates the conditions of the security already offered, incorporating the interest rate determined in the original offer (7%) and to bid the price. As a result of this process, the Company issued additional USD 10,000,000 for the Class A CB, with an issuance price of 102.9%.

| 7.3.10. | CPSA´s Shares Buyback Program |

On August 24, 2023, the Company's Board of Directors approved the creation of a new program for the acquisition of the shares issued by the Company as per the regulations in force, for a maximum amount of up to USD 10,000,000 or the lowest amount from the acquisition until reaching 10% of the share capital and for a 180-calendar-day period counted as from the business day following the publication of the purchase in the market’s media, which shall be subject to any term renewal or extension.

The acquisition procedures may be conducted by the Company and/or its subsidiaries with a daily limit for operations of up to 25% of the average volume of daily transactions for the share in the markets in which it is listed, considering to such end the previous 90 trading business days. The maximum price to be paid is USD 8 per American Depositary Receipt (“ADR”) in the NYSE and up to a maximum of ARS 605 per share in BYMA, which was increased to ARS 800 per share as per the decision of the Company's Board of Directors on October 17, 2023. As of September 30, 2024, CPSA acquired 2,299,993 of its own shares under the program for a total amount of 3,345,800.

| -29- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

The operations conducted through both programs have been recorded as own shares acquisitions in accordance with IAS 32. Therefore, the consideration paid for such shares was directly recorded against Equity under the “Other equity accounts” item.

| 7.3.11. | Mitsubishi Corporation Loan |

On November 29, 1996, the Company Central Costanera S.A. entered into an Agreement with Mitsubishi Corporation for the installation of a combined cycle power station. The original agreement includes a USD 192.5 million financing in 12 years counted as from the provisional reception of the project, with an annual 7.42 % fixed rate and a semester capital and interest amortization.

On October 27, 2014, Central Costanera S.A. and Mitsubishi Corporation agreed on the restructuring of such liabilities. Among the main restructuring conditions, the following stand out: accrued and accumulated interest remission as of September 30, 2014 for the amount of USD 66,061,897; the rescheduling of capital due date for the amount of USD 120,605,058 for an 18-year term, with a 12-month grace period, which must be totally paid before December 15, 2032; a minimum annual payment of USD 3,000,000 in concept for capital, in quarterly installments; an annual 0.25% fixed rate; and certain dividend payment restrictions were agreed on.

Considering the restrictions imposed by the Argentine Central Bank described on Note 13, several amendments to the loan agreement were entered into as from September 30, 2020.

The loan considers certain financial restrictions, which as of September 30, 2024 have been completely fulfilled by Central Costanera S.A. Moreover, as guarantee of the obligations undertaken, Central Costanera S.A. has a pledge in favor of Mitsubishi Corporation with a first degree recording on the financed asset. The amount of the pledge varies according to the refinancing obtained.

As of September 30, 2024 and as of December 31, 2023, the liabilities balance amounts to 43,428,861 and 68,802,922, respectively.

| 7.3.12. | Loan from Equinor Wind Power AS |

As a result of the acquisition of the solar farm Guañizuil II A, the Group assumed the liabilities corresponding to the loan granted to the subsidiary Cordillera Solar VIII (“CSVIII”) by its previous shareholder Equinor Wind Power AS for a capital amount of USD 62,199,879 and interest for USD 8,983,951. As a guarantee for such loan, CSVIII gave a first-grade pledge over certain properties, plant, and equipment of such company in favor of Equinor Wind power AS.

On October 18, 2023, both parties agreed on a refinancing plan for a 24-month term counted as from the refinancing date at a 9% annual rate. In addition, on such dates, CSVIII paid an amount of USD 40 million with funds obtained through the loan described on Note 7.3.13.

Moreover, as a result of the acquisition, the Group acquired the liabilities for the loan Junior Shareholder Loan Agreement granted to CSVIII for a USD 1,768,897 balance, which on October 18, 2023, was refinanced at a 9% annual rate to be paid 24 months after the refinancing date.

On September 6 and October 7, 2024, both loans were totally paid.

As of September 30, 2024 and as of December 31, 2023, the loans balance amounts to 1,866,069 and 29,500,990, respectively.

| -30- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 7.3.13. | Loan from Banco Santander International |

On October 18, 2023, the subsidiary Cordillera Solar VIII S.A. agreed on financing with Banco Santander International for an amount of USD 40 million with a 6.5% annual rate to be paid on the 24 months after the granting of the loan.

As of September 30, 2024 and as of December 31, 2023, the balance of this loans amounts to 39,976,513 and 66,069,990, respectively.

| 7.3.14. | Short-term loans for import financing |

As of September 30, 2024, the subsidiary Vientos La Genoveva II S.A.U. agreed on several short-term loans with Banco Santander S.A. (Uruguay) for a total amount of USD 5,435,603. These loans accrue a 7% annual interest rate, maturing between November 29, 2024 and March 9, 2025.

The loans described above are to finance the acquisition of trackers, panels and inverters and transformation centers to be installed in the San Carlos solar farm (see Note 11.2).

As of September 30, 2024, CPSA has several short-term loans with Banco Santander S.A. (Uruguay) for a total of USD 4,432,049,049 to finance the acquisition of equipment to be used in the Brigadier Lopez thermal station combined cycle closure project. These loans accrue interest between 7% and 8% effective annual rate with maturities between October 14, 2024 and April 30, 2025. Subsequent to the end of the period, on October 18, 2024, CPSA entered into another short-term loan with Banco Santander S.A. (Uruguay) under the same conditions for an amount of USD 16,785 at an effective annual rate of 7%, maturing on January 9, 2025.

As of September 17, 2024, the subsidiary Central Costanera S.A. has subscribed a short-term loan with Banco Santander S.A. (Uruguay) for a total amount of USD 1,288,451 to finance the import of materials and equipment. This loan accrues interest at an effective annual rate of 7%, with maturity scheduled for December 27, 2024.

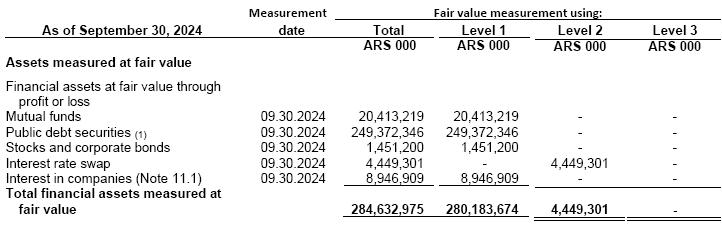

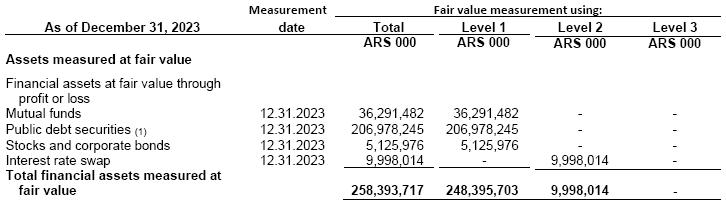

| 7.4. | Quantitative and qualitative information on fair values Valuation techniques |

The fair value reported in connection with the above-mentioned financial assets and liabilities is the amount at which the instrument could be exchanged in a current transaction between willing parties, other than in a forced or liquidation sale. The following methods and assumptions were used to estimate the fair values:

Management assessed that the fair values of current trade receivables approximate their carrying amounts largely due to the short-term maturities of these instruments.

The Group measures long-terms receivables at fixed and variable rates based on discounted cash flows. The valuation requires that the Group adopt certain assumptions such as interest rates, specific risk factors of each transaction and the creditworthiness of the customer.

Fair value of quoted debt securities, mutual funds, stocks and corporate bonds is based on price quotations at the end of each reporting period.

The fair value of debts and loans accruing interest is equivalent to their book value, except for the loan granted by Mitsubishi Corporation to the controlled company Central Costanera S.A.

Fair value hierarchy

The following tables provides, by level within the fair value measurement hierarchy, the Company’s financial assets, that were measured at fair value on recurring basis as of September 30, 2024 and as of December 31, 2023:

| -31- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| (1) | Includes 158,713,293 corresponding to government securities issued by the National Government and 90,659,053 corresponding to T-BILLs. |

| (1) | Includes 94,868,997 corresponding to government securities issued by the National Government and 112,109,248 corresponding to T-BILLs. |

There were no transfers between hierarchies and there were not significant variations in assets values.

The information on the Group’s objectives and financial risk management policies is included in Note 17 to the issued financial statements as at December 31, 2023.

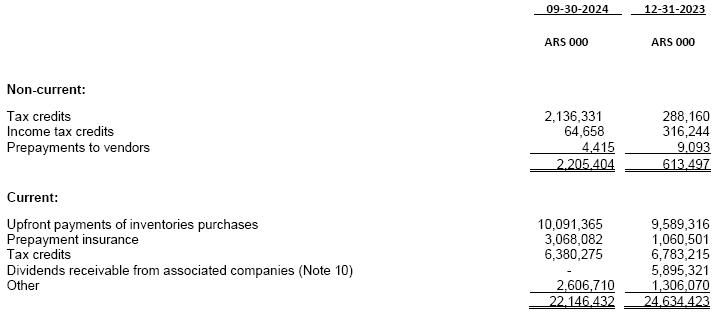

| 8. | Non-financial assets and liabilities |

| 8.1. | Other non-financial assets |

| -32- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

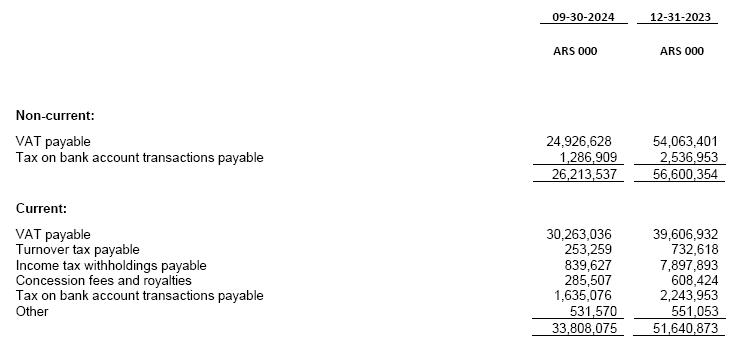

| 8.2. | Other non-financial liabilities |

| 8.3. | Compensation and employee benefits liabilities |

| 9. | Equity reserves |

On April 28, 2023, the Shareholders’ Meeting of the Company approved to increase the legal reserve in the amount of 5,976,228 and to allocate the remaining unappropriated earnings as of December 31, 2022 to create a voluntary reserve in order to be applied to future dividends payment based on the evolution of the Company´s financial situation and according to current Company´s dividends distribution policy. On September 15, 2023, such reserve was increased in 281,191,039 through the partial deallocation of the voluntary reserve as decided by the Company’s Shareholders’ Meeting on such date.

On November 2, 2023, the Company’s Board of Directors decided to partially deallocate the voluntary reserve intended for dividends payment so as to distribute a dividend equivalent to 29.72 ARS per share.

On December 1, 2023, the Company’s Board of Directors decided to partially deallocate the voluntary reserve intended for dividends payment so as to distribute a dividend equivalent to 32.431222 ARS per share.

On December 15, 2023, the Company’s Board of Directors decided to partially deallocate the voluntary reserve intended for dividends payment so as to distribute a dividend equivalent to 11 ARS per share.

On January 2, 2024, the Company’s Board of Directors decided to partially deallocate the voluntary reserve intended for dividends payment so as to distribute a dividend equivalent to 5.75 ARS per share.

On April 30, 2024, the Shareholders’ Meeting of the Company approved to increase the legal reserve in the amount of 14,921,408 and to allocate the remaining unappropriated earnings as of December 31, 2023 to increase a voluntary reserve in order to be applied to future dividends payment based on the evolution of the Company´s financial situation and according to current Company´s dividends distribution policy.

| -33- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

After the end of the period, on November 7, 2024, the Company´s Board of Directors decided to partially deallocate the voluntary reserve intended for dividends payment so as to distribute a dividend equivalent to 39.47 ARS per share.

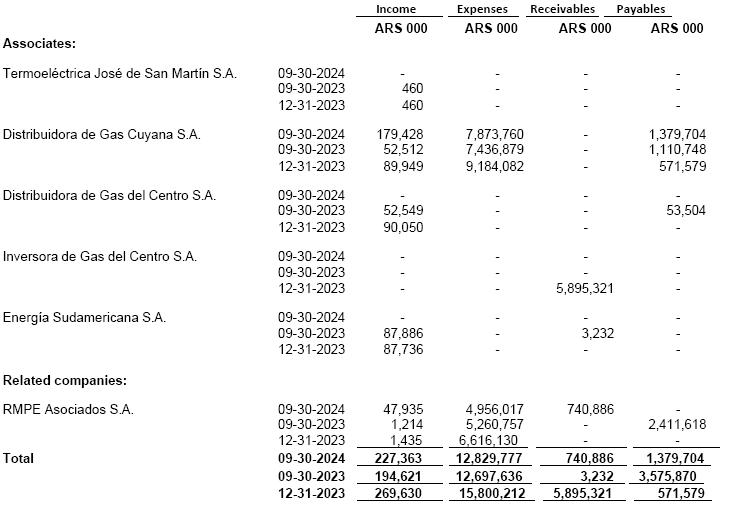

| 10. | Information on related parties |

The following table provides the transactions performed and the accounts payable to/receivable from related parties as of the corresponding period/year:

Balances and transactions with shareholders

As of September 30, 2024 and as of December 31, 2023, there is a balance with shareholders of 1,540,243 and 38,437, respectively, corresponding to the personal property tax entered by the Company under the substitute decision maker scheme.

Terms and conditions of transactions with related parties

Balances at the related reporting period-ends are unsecured and interest free. There have been no guarantees provided or received for any related party receivables or payables.

| -34- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

For the nine-month periods ended September 30, 2024 and 2023 the Group has not recorded any impairment of receivables relating to amounts owed by related parties. This assessment is undertaken at the end of each reporting period by examining the financial position of the related party and the market in which the related party operates.

During the nine-month period ended September 30, 2024, the Group sold 2,92% of its shareholding in controlled companies, without such implying the loss of control over such companies. As per IFRS 10, the effects of such transaction were directly recognized in equity.

| 11. | Contracts, acquisitions and agreements |

| 11.1. | Acquisition of equity interest in AbraSilver Resource Corp. |

On April 22, 2024, Proener S.A.U. entered into a shares subscription agreement for a 4% interest in the capital stock of AbraSilver Resource Corp. (a Canadian company listed in the Canadian stock market), which is the owner of the silver-gold project Diablillos located in the Northwest region of Argentina. The price of the transaction amounted to 10,000,000 Canadian dollars. The investment is valued at fair value at the end of the reporting period and classified under the item “Other Financial Assets - Non-Current”.

| 11.2. | San Carlos Solar Power Station |

During 2022, within the framework of MEyM Resolution No. 281/2017, the Company was awarded the project “Parque Solar San Carlos” (solar power station) for a 10 MW power. This project will be built in San Carlos, Salta province. On March 27, 2024, the agreements for the construction of the solar farm were signed with the Chinese company Shanghai Electric Power Construction Company Ltd. Argentina. As of the date of these financial statements, the solar park is in the process of construction.

| 11.3. | Granted guarantees |

The Group has posted a bank guarantee to cover the obligations undertaken under the Concession Agreement of Complejo Hidroeléctrica Piedra del Águila for 168,756. In turn, and as a result of the provisions of PEN Decree No. 718/24 (see Note 1.2.a), the Group provided a surety bond in the amount of USD 4,500,000 as a guarantee for the extension of the Concession Agreement with a maximum term until December 28, 2025.

On March 19, 2009, the Group entered into a pledge agreement with the former Secretariat of Energy to secure its obligations in favor of FONINVEMEM trusts by virtue of the operation and maintenance agreement of the Timbúes and Manuel Belgrano power stations, by which it pledged as a collateral 100% of the shares in TSM and TMB.

On the other hand, shares acquired by the Group in Central Costanera S.A. have a pledge for which the Group will follow the procedure to achieve its extinguishment.

Regarding the agreement described in Note 7.3.13 and 7.3.14, the Group has granted T-BILLs as compliance guarantee, which are included under non-current other financial assets.

Likewise, the Group entered into various guaranteed agreements to provide performance assurance of its obligations arising from the agreements described in Notes 1.2.a) to the consolidated financial statements for the year ended December 31, 2023, already issued and in Notes 7.3.1, 7.3.3, 7.3.4, 7.3.5, 7.3.6, 7.3.11 and 7.3.12.

| -35- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

| 12. | Tax integral inflation adjustment |

Pursuant to Law no. 27,468, modified by Law no. 27,430 to determine the amount of taxable net profits for fiscal years commencing January 1, 2019, the inflation adjustment calculated on the basis of the provisions set forth in the income tax law will have to be added to or deducted from the fiscal year’s tax result. This adjustment will only be applicable (a) if the variance percentage of the consumers price index (“IPC”) during the 36 months prior to fiscal year closing is higher than 100%, and (b) for the first, second, and third fiscal year as of its effective date, the accumulated IPC variance is higher than 55%, 30% or 15% of such 100%, respectively. The positive or negative tax inflation adjustment, depending on the case, corresponding to the first, second and third period commenced as from January 1, 2018, which must be calculated in case of verifying the statements on the foregoing paragraphs (a) y (b), shall be charged in a sixth for that fiscal period and the remaining five sixths, equally, in the immediately following fiscal periods.

At December 31, 2019 and during the following fiscal years, such conditions have been already met. Consequently, the current and deferred income tax have been booked in the fiscal year ended December 31, 2019 including the effects derived from the application of the tax inflation adjustment under the terms established by the income tax law.

| 13. | Measures in the Argentine economy |

On December 10, 2023, new government authorities took office, which authorities issued a series of measures among whose main objectives the following stand out: flexibility of regulations for economic development, reduction of expenses towards reducing fiscal deficit, reduction of subsidies, among others. Within the context of the new government, there was a significant devaluation of the Argentine peso which was reflected on the official exchange rate.

Foreign exchange market

As from December 2019, the BCRA issued a series of communications whereby it extended indefinitely the regulations on Foreign Market and Foreign Exchange Market issued by BCRA that included regulations on exports, imports and previous authorization from BCRA to access the foreign exchange market to transfer profits and dividends abroad, as well as other restrictions on the operation in the foreign exchange market.

Particularly, as from September 16, 2020, Communication “A” 7106 established, among other measures referred to human persons, the need for refinancing the international financial indebtedness for those loans from the non-financial private sector with a creditor not being a related counterparty of the debtor expiring between October 15, 2020 and March 31, 2021. The affected legal entities were to submit before the Central Bank a refinancing plan under certain criteria: that the net amount for which the foreign exchange market was to be accessed in the original terms did not exceed 40% of the capital amount due for that period and that the remaining capital had been, as a minimum, refinanced with a new external indebtedness with an average life of 2 years. This point shall not be applicable when indebtedness is taken from international entities and official credit agencies, among others. As from April 1, 2021, through Communication “A” 7230, BCRA decided to establish at the equivalent of USD 2 million the maximum amount per calendar month whereby the debtor would access the foreign exchange market for repaying the indebtedness described in point 7 of Communication “A” 7106, operating until December 31, 2021 (successively extended until December 31, 2023 through BCRA Communications “A” 7466 and 7621). Since December 31, 2023, the provisions on point 7 of Communication “A” 7106 (as amended and extended) have had no more effects. The effects of this regulation for the Company are described in Notes 7.3.3 and 7.3.11.

As of the issuance date of these financial statements, after the new authorities took office on December 10, 2023, the restrictions for the payment of imports with customs entry record prior to December 13, 2023 were reduced, while other BCRA restrictions to access to the Unique and Free Exchange Rate Market and to operate in the exchange rate market are kept.

| -36- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

CENTRAL PUERTO S.A. |

Income Tax

On June 16, 2021, the Argentine Executive Power passed Law No. 27630, which established changes in the corporate income tax rate for the fiscal periods commencing as from January 1, 2021. Such law establishes payment of the tax based on a structure of staggered rates regarding the level of accumulated taxable net income. The estimated amounts in this scale will be annually adjusted, considering the annual variation of the consumer price index provided by the INDEC corresponding to October of the year prior to the adjustment compared with the same month of the previous year. For fiscal year 2023 the applicable scale was the following: 25% up to an accumulated taxable net income of 14.3 million Ps.; 30% for the excess of such amount up to 143 million Ps.; and 35% for the excess of such amount. Meanwhile, for fiscal year 2024 the applicable scale is the following: 25% up to an accumulated taxable net income of 34.7 million Ps.; 30% for the excess of such amount up to 347 million Ps.; and 35% for the excess of such amount.

Passing of Law No. 27742 “Law of Bases”

On June 28, 2024, Law No. 27742 (“Law of Bases”) was passed, which Law came into force after its enactment by the Executive Power.

Regarding energy, the Law of Bases modifies laws that form the regulatory framework of hydrocarbons, natural gas, biofuels, electricity, among others. These changes are projected with the aim of rearranging the relationship between the government and the market so as to give predominance to private initiatives in order to gain in competitive terms and maximize the rent obtained.

In this regard, the Law of Bases enables the Executive Power to modify the Laws No. 15336 on Electrical Energy and No. 24065 on the Regulatory Framework of Electric Energy, by guaranteeing the following bases:

| – | Free international trade of electricity. |

| – | Free trade, competition and expansion of markets, and the possibility for the final user to choose the supplier. |

| – | A clear establishment of the different items to be paid by the final user. |

| – | The development of electricity transportation infrastructure through open, transparent, efficient and competitive mechanisms. |

| – | The review of administrative structures of the electricity sector, modernizing and professionalizing them. |

The Law of Bases combines the gas and electricity regulators (ENRE and Enargas) in one National Gas and Electricity Regulatory Entity, which shall have the same functions as the current ones.

| 14. | Restrictions on income distribution |

Pursuant to the General Legal Entities Law and the Bylaws, 5% of the profits made during the fiscal year must be assigned to the statutory reserve until such reserve reaches 20% of the Company’s Capital Stock.

The profits that are distributed to human persons of Argentina and abroad and foreign legal entities are subject to a withholding of 7% as dividend tax, to the extent that such profits correspond to fiscal years closed after December 31, 2017.

In addition, certain loan agreements establish requirements to distribute dividends (see Notes 7.3.1, 7.3.4, 7.3.5, 7.3.6 and 7.3.11).

| -37- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

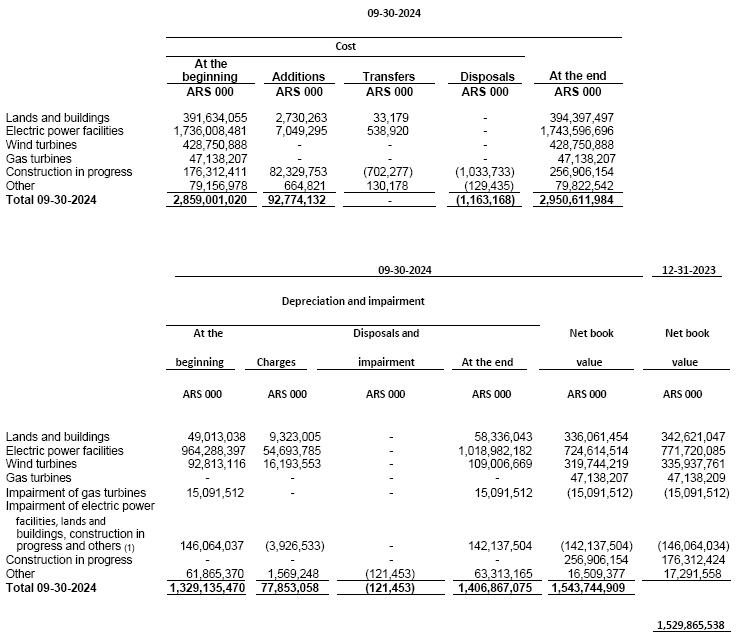

EXHIBIT A

CENTRAL PUERTO S.A.

PROPERTY, PLANT AND EQUIPMENT

AS OF SEPTEMBER 30, 2024 AND AS OF DECEMBER 31, 2023

| (1) | See note 2.3.8. to the issued financial statements as at December 31, 2023. |

| -38- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |

EXHIBIT B

CENTRAL PUERTO S.A.

INTANGIBLE ASSETS

AS OF SEPTEMBER 30, 2024 AND AS OF DECEMBER 31, 2023

| (1) | See note 2.3.8. to the issued financial statements as at December 31, 2023. |

| -39- |

English translation of the consolidated financial statements originally filed in Spanish with the Argentine Securities Commission (“CNV”). |