The Registrant has adopted a code of ethics that applies to the Registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. There have been no amendments to, or waivers in connection with, the Code of Ethics during the period covered by this Report.

| Item 3. | Audit Committee Financial Expert. |

The Registrant's Board has determined that J. Charles Cardona, a member of the Audit Committee of the Board, is an audit committee financial expert as defined by the Securities and Exchange Commission (the "SEC"). J. Charles Cardona is "independent" as defined by the SEC for purposes of audit committee financial expert determinations.

| Item 4. | Principal Accountant Fees and Services. |

(a) Audit Fees. The aggregate fees billed for each of the last two fiscal years (the "Reporting Periods") for professional services rendered by the Registrant's principal accountant (the "Auditor") for the audit of the Registrant's annual financial statements or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $36,261 in 2023 and $36,986 in 2024.

(b) Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by the Auditor that are reasonably related to the performance of the audit of the Registrant's financial statements and are not reported under paragraph (a) of this Item 4 were $9,829 in 2023 and $7,332 in 2024. These services consisted of one or more of the following: (i) agreed upon procedures related to compliance with Internal Revenue Code section 817(h), (ii) security counts required by Rule 17f-2 under the Investment Company Act of 1940, as amended, (iii) advisory services as to the accounting or disclosure treatment of Registrant transactions or events and (iv) advisory services to the accounting or disclosure treatment of the actual or potential impact to the Registrant of final or proposed rules, standards or interpretations by the Securities and Exchange Commission, the Financial Accounting Standards Boards or other regulatory or standard-setting bodies.

The aggregate fees billed in the Reporting Periods for non-audit assurance and related services by the Auditor to the Registrant's investment adviser (not including any sub-investment adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the Registrant ("Service Affiliates"), that were reasonably related to the performance of the annual audit of the Service Affiliate, which required pre-approval by the Audit Committee were $0 in 2023 and $0 in 2024.

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax advice, and tax planning ("Tax Services") were $3,342 in 2023 and $3,342 in 2024. These services consisted of: (i) review or preparation of U.S. federal, state, local and excise tax returns; (ii) U.S. federal, state and local tax planning, advice and assistance regarding statutory, regulatory or administrative developments; (iii) tax advice regarding tax qualification matters and/or treatment of various financial instruments held or proposed to be acquired or held, and (iv) determination of Passive Foreign Investment Companies. The aggregate fees billed in the Reporting Periods for Tax Services by the Auditor to Service Affiliates, which required pre-approval by the Audit Committee were $8,158 in 2023 and $7,799 in 2024.

(d) All Other Fees. The aggregate fees billed in the Reporting Periods for products and services provided by the Auditor, other than the services reported in paragraphs (a) through (c) of this Item,

were $1 in 2023 and $2 in 2024. These services consisted of a review of the Registrant's anti-money laundering program.

The aggregate fees billed in the Reporting Periods for Non-Audit Services by the Auditor to Service Affiliates, other than the services reported in paragraphs (b) through (c) of this Item, which required pre-approval by the Audit Committee, were $0 in 2023 and $0 in 2024.

(e)(1) Audit Committee Pre-Approval Policies and Procedures. The Registrant's Audit Committee has established policies and procedures (the "Policy") for pre-approval (within specified fee limits) of the Auditor's engagements for non-audit services to the Registrant and Service Affiliates without specific case-by-case consideration. The pre-approved services in the Policy can include pre-approved audit services, pre-approved audit-related services, pre-approved tax services and pre-approved all other services. Pre-approval considerations include whether the proposed services are compatible with maintaining the Auditor's independence. Pre-approvals pursuant to the Policy are considered annually.

(e)(2) Note. None of the services described in paragraphs (b) through (d) of this Item 4 were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) None of the hours expended on the principal accountant's engagement to audit the registrant's financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant's full-time, permanent employees.

Non-Audit Fees. The aggregate non-audit fees billed by the Auditor for services rendered to the Registrant, and rendered to Service Affiliates, for the Reporting Periods were $1,886,566 in 2023 and $1,486,377 in 2024.

Auditor Independence. The Registrant's Audit Committee has considered whether the provision of non-audit services that were rendered to Service Affiliates, which were not pre-approved (not requiring pre-approval), is compatible with maintaining the Auditor's independence.

| Item 5. | Audit Committee of Listed Registrants. |

Not applicable.

Not applicable.

Dreyfus Treasury and Agency Liquidity Money Market Fund

ANNUAL FINANCIALS AND OTHER INFORMATION

IMPORTANT NOTICE – CHANGES TO ANNUAL AND SEMI-ANNUAL REPORTS

The Securities and Exchange Commission (the “SEC”) has adopted rule and form amendments which have resulted in changes to the design and delivery of annual and semi-annual fund reports (“Reports”). Reports are now streamlined to highlight key information. Certain information previously included in Reports, including financial statements, no longer appear in the Reports but will be available online within the Semi-Annual and Annual Financials and Other Information, delivered free of charge to shareholders upon request, and filed with the SEC.

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.bny.com/investments and sign up for eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon

Family of Funds.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

Contents

Please note the Annual Financials and Other Information only contains Items 7-11 required in Form N-CSR. All other required items will be filed with the SEC.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies. Dreyfus Treasury and Agency Liquidity Money Market FundStatement of Investments

| | | | | |

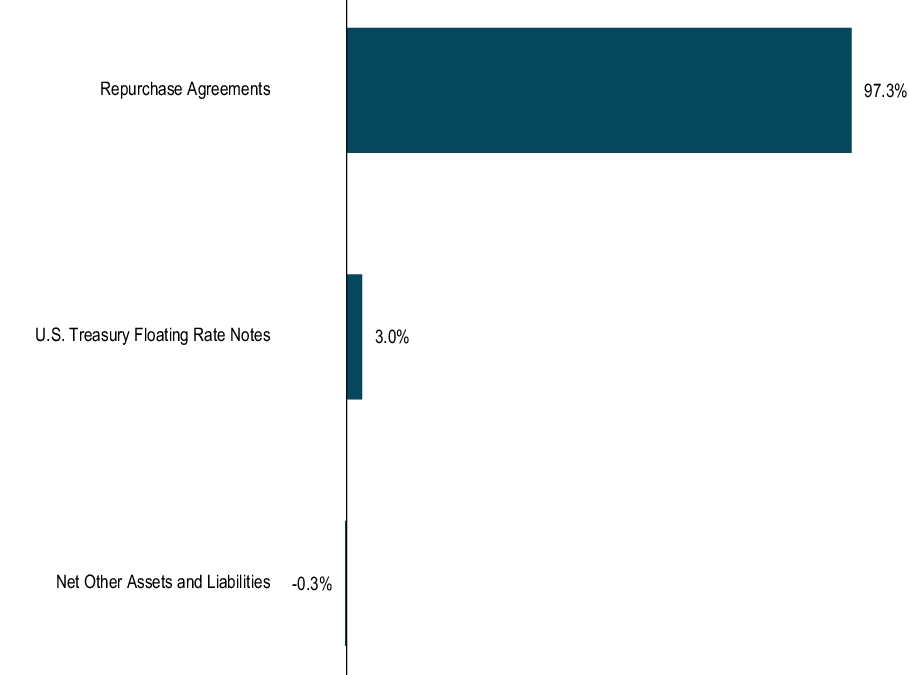

U.S. Treasury Floating Rate Notes — 3.0% | | | | | |

12/3/2024 (3 Month USBMMY + 0.20%)(a) | | | | | |

12/3/2024 (3 Month USBMMY + 0.17%)(a) | | | | | |

Total U.S. Treasury Floating Rate Notes

(cost $280,001,479) | | | | | |

Repurchase Agreements — 97.3% | | | | | |

Banco Santander SA, Tri-Party Agreement thru BNY, dated 11/29/2024, due at 12/2/2024 in the amount of $438,165,710 (fully collateralized by: U.S. Treasuries (including strips), 0.75%-4.63%, due 2/28/2026- 2/15/2041, valued at $446,760,040) | | | | | |

Credit Agricole CIB, Tri-Party Agreement thru BNY, dated 11/29/2024, due at 12/2/2024 in the amount of $575,219,458 (fully collateralized by: U.S. Treasuries (including strips), 0.63%-4.88%, due 1/15/2025- 8/15/2032, valued at $586,500,062) | | | | | |

Federal Reserve Bank of New York, Tri-Party Agreement thru BNY, dated 11/29/2024, due at 12/2/2024 in the amount of $5,001,895,833 (fully collateralized by: U.S. Treasuries (including strips), 0.63%-3.13%, due 8/15/2025-11/15/2031, valued at $5,001,895,874) | | | | | |

Fixed Income Clearing Corp., Tri-Party Agreement thru Nothern Trust Company, dated 11/29/2024, due at 12/2/2024 in the amount of $1,000,381,667 (fully collateralized by: U.S. Treasuries (including strips), 2.62%-4.00%, due 12/31/2028-2/15/2029, valued at $1,020,000,000) | | | | | |

Fixed Income Clearing Corp., Tri-Party Agreement thru State Street Corp., dated 11/29/2024, due at 12/2/2024 in the amount of $500,191,250 (fully collateralized by: U.S. Treasuries (including strips), 4.50%, due 3/31/2026, valued at $510,000,091) | | | | | |

HSBC Securities USA, Inc., Tri-Party Agreement thru BNY, dated 11/29/2024, due at 12/2/2024 in the amount of $1,050,400,750 (fully collateralized by: U.S. Treasuries (including strips), 0.00%, due 2/15/2025-5/15/2054, valued at $1,071,000,000) | | | | | |

Natixis Fund, Tri-Party Agreement thru BNY, dated 11/29/2024, due at 12/2/2024 in the amount of $500,190,833 (fully collateralized by: U.S. Treasuries (including strips), 0.00%-4.63%, due 1/2/2025- 5/15/2054, Cash Collateral Pledge in amount of $52,211,833, valued at $510,000,000) | | | | | |

Total Repurchase Agreements

(cost $9,063,000,000) | | | | | |

Total Investments (cost $9,343,001,479) | | | | | |

Liabilities, Less Cash and Receivables | | | | | |

| | | | | |

USBMMY—U.S. Treasury Bill Money Market Yield |

| Variable rate security—interest rate resets periodically and rate shown is the interest rate in effect at period end. Date shown represents the earlier of the next interest reset date or ultimate maturity date. Security description also includes the reference rate and spread if published and available. |

See notes to financial statements.

STATEMENT OF ASSETS AND LIABILITIES

November 30, 2024

| | |

| | |

Investments in securities—See Statement of Investments

(including repurchase agreements of $9,063,000,000)—Note 1(b) | | |

| | |

| | |

| | |

| | |

Due to BNY Mellon Investment Adviser, Inc. and affiliates—Note 2(b) | | |

Cash overdraft due to Custodian | | |

Trustees’ fees and expenses payable | | |

| | |

| | |

| | |

Composition of Net Assets ($): | | |

| | |

Total distributable earnings (loss) | | |

| | |

| | |

(unlimited number of $.001 par value shares of Beneficial Interest authorized) | | |

Net Asset Value Per Share ($) | | |

See notes to financial statements.

Year Ended November 30, 2024

| |

| |

| |

| |

| |

Trustees’ fees and expenses—Note 2(c) | |

| |

| |

Chief Compliance Officer fees—Note 2(b) | |

Prospectus and shareholders’ reports | |

| |

Shareholder servicing costs—Note 2(b) | |

| |

| |

Less—reduction in fees due to earnings credits—Note 2(b) | |

| |

Net Investment Income, representing net increase in net assets resulting from operations | |

See notes to financial statements.

STATEMENT OF CHANGES IN NET ASSETS

| |

| | |

| | |

| | |

Net realized gain (loss) on investments | | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | |

| | |

Distributions to shareholders | | |

Beneficial Interest Transactions ($1.00 per share): | | |

Net proceeds from shares sold | | |

| | |

Increase (Decrease) in Net Assets from Beneficial Interest Transactions | | |

Total Increase (Decrease) in Net Assets | | |

| | |

| | |

| | |

See notes to financial statements.

The following table describes the performance for the fiscal periods indicated. All information reflects financial results for a single fund share. Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption at net asset value on the last day of the period. Net asset value total return includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions.

| |

| | | | | |

| | | | | |

Net asset value, beginning of period | | | | | |

| | | | |

| | | | | |

| | | | | |

Dividends from net investment income | | | | | |

Dividends from net realized gain on investments | | | | | |

| | | | | |

Net asset value, end of period | | | | | |

| | | | | |

Ratios/Supplemental Data (%): | | | | |

Ratio of total expenses to average net assets | | | | | |

Ratio of net expenses to average net assets | | | | | |

Ratio of net investment income to average net assets | | | | | |

Net Assets, end of period ($ x 1,000) | | | | | |

| Amount represents less than $.001 per share. |

See notes to financial statements.

NOTES TO FINANCIAL STATEMENTS

NOTE 1—

Significant Accounting Policies:

Dreyfus Treasury and Agency Liquidity Money Market Fund (the “fund”) is the sole series of Dreyfus Institutional Liquidity Funds (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified open-end management investment company. The fund’s investment objective is to seek as high a level of current income as is consistent with the preservation of capital and the maintenance of liquidity. BNY Mellon Investment Adviser, Inc. (the “Adviser”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY”), serves as the fund’s investment adviser. BNY Mellon Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Adviser, is the distributor of the fund’s shares, which are sold to the public without a sales charge. Dreyfus, a division of Mellon Corporation (the “Sub-Adviser”), an indirect wholly-owned subsidiary of BNY and an affiliate of the Adviser, serves as the fund’s sub-adviser.

The fund operates as a “government money market fund” as that term is defined in Rule 2a-7 under the Act. It is the fund’s policy to maintain a constant net asset value (“NAV”) per share of $1.00, and the fund has adopted certain investment, portfolio valuation and dividend and distribution policies to enable it to do so. There is no assurance, however, that the fund will be able to maintain a constant NAV per share of $1.00.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the SEC under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund is an investment company and applies the accounting and reporting guidance of the FASB ASC Topic 946 Financial Services-Investment Companies. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The Trust enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: Investments in securities are valued at amortized cost in accordance with Rule 2a-7 under the Act. If amortized cost is determined not to approximate fair market value, the fair value of the portfolio securities will be determined by procedures established by and under the general oversight of the Trust’s Board of Trustees (the “Board”) pursuant to Rule 2a-5 under the Act.

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements. These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, money market securities are valued using amortized cost, in accordance with rules under the Act. Generally, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected within Level 2 of the fair value hierarchy.

NOTES TO FINANCIAL STATEMENTS (continued)

The following is a summary of the inputs used as of November 30, 2024 in valuing the fund’s investments:

| Level 1 -

Unadjusted

Quoted Prices | Level 2- Other

Significant

Observable Inputs | Level 3-

Significant

Unobservable

Inputs | |

| | | | |

Investments in Securities:† | | | | |

U.S. Treasury Floating Rate Notes | | | | |

| | | | |

| See Statement of Investments for additional detailed categorizations, if any. |

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Interest income, adjusted for accretion of discount and amortization of premium on investments, is earned from settlement date and is recognized on the accrual basis. Realized gains and losses from securities transactions are recorded on the identified cost basis.

The fund may enter into repurchase agreements with financial institutions, deemed to be creditworthy by the Adviser, subject to the seller’s agreement to repurchase and the fund’s agreement to resell such securities at a mutually agreed upon price. Pursuant to the terms of the repurchase agreement, such securities must have an aggregate market value greater than or equal to the terms of the repurchase price plus accrued interest at all times. If the value of the underlying securities falls below the value of the repurchase price plus accrued interest, the fund will require the seller to deposit additional collateral by the next business day. If the request for additional collateral is not met, or the seller defaults on its repurchase obligation, the fund maintains its right to sell the underlying securities at market value and may claim any resulting loss against the seller. The collateral is held on behalf of the fund by the tri-party administrator with respect to any tri-party agreement. The fund may also jointly enter into one or more repurchase agreements with other funds managed by the Adviser in accordance with an exemptive order granted by the SEC pursuant to section 17(d) and Rule 17d-1 under the Act. Any joint repurchase agreements must be collateralized fully by U.S. Government securities.

For financial reporting purposes, the fund elects not to offset assets and liabilities subject to a Repurchase Agreement, if any, in the Statement of Assets and Liabilities. Therefore, all qualifying transactions are presented on a gross basis in the Statement of Assets and Liabilities. As of November 30, 2024, the impact of netting of assets and liabilities and the offsetting of collateral pledged or received, if any, based on contractual netting/set-off provisions in the Repurchase Agreement are detailed in the following table:

| | |

Gross amount of Repurchase Agreements, at value, as disclosed in the Statement of Assets and Liabilities | | |

Collateral (received)/posted not offset in the Statement of Assets and Liabilities | | |

| | |

| The value of the related collateral received by the fund exceeded the value of the repurchase agreement by the fund. See Statement of Investments for detailed information regarding collateral received for open repurchase agreements. |

(c) Market Risk: The value of the securities in which the fund invests may be affected by political, regulatory, economic and social developments. Events such as war, acts of terrorism, the spread of infectious illness or other public health issue, recessions, or other events could have a significant impact on the fund and its investments. Recent examples include pandemic risks related to COVID-19 and aggressive measures taken world-wide in response by governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines of large populations, and by businesses, including changes to operations and reducing staff.

Repurchase Agreement Counterparty Risk: The fund is subject to the risk that a counterparty in a repurchase agreement could fail to honor the terms of the agreement.

(d) Dividends and distributions to shareholders: It is the policy of the fund to declare dividends daily from net investment income. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund

NOTES TO FINANCIAL STATEMENTS (continued)

may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”). To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended November 30, 2024, the fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended November 30, 2024, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended November 30, 2024 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At November 30, 2024, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $321,782 and accumulated capital losses $43,487.

The fund is permitted to carry forward capital losses for an unlimited period. Furthermore, capital loss carryovers retain their character as either short-term or long-term capital losses.

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net realized capital gains, if any, realized subsequent to November 30, 2024. The fund has $43,487 of short-term capital losses which can be carried forward for an unlimited period.

The tax character of distributions paid to shareholders during the fiscal years ended November 30, 2024 and November 30, 2023 were as follows: ordinary income $548,124,856 and $602,987,594, respectively.

At November 30, 2024, the cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes (see the Statement of Investments).

NOTE 2—

Management Fee, Sub-Advisory Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement with the Adviser, the management fee is computed at the annual rate of .08% of the value of the fund’s average daily net assets and is payable monthly.

Pursuant to a sub-investment advisory agreement between the Adviser and the Sub-Adviser, the Adviser pays to the Sub-Adviser a monthly fee of 50% of the monthly management fee the Adviser receives from the fund with respect to the value of the sub-advised net assets of the fund, net of any fee waivers and/or expense reimbursements made by the Adviser.

(b) The fund has an arrangement with BNY Mellon Transfer, Inc., (the “Transfer Agent”), a subsidiary of BNY and an affiliate of the Adviser, whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset Transfer Agent fees. For financial reporting purposes, the fund includes transfer agent net earnings credits, if any, as an expense offset in the Statement of Operations.

The fund has an arrangement with The Bank of New York Mellon (the “Custodian”), a subsidiary of BNY and an affiliate of the Adviser, whereby the fund will receive interest income or be charged overdraft fees when cash balances are maintained. For financial reporting purposes, the fund includes this interest income and overdraft fees, if any, as interest income in the Statement of Operations.

The fund compensates the Transfer Agent, under a transfer agency agreement, for providing transfer agency and cash management services for the fund. The majority of Transfer Agent fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended November 30, 2024, the fund was charged $60 for transfer agency services. These fees are included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $13.

The fund compensates the Custodian, under a custody agreement, for providing custodial services for the fund. These fees are determined based on net assets, geographic region and transaction activity. During the period ended November 30, 2024, the fund was charged $198,341 pursuant to the custody agreement.

During the period ended November 30, 2024, the fund was charged $19,942 for services performed by the fund’s Chief Compliance Officer and his staff. These fees are included in Chief Compliance Officer fees in the Statements of Operations.

NOTES TO FINANCIAL STATEMENTS (continued)

The components of “Due to BNY Mellon Investment Adviser, Inc. and affiliates” in the Statement of Assets and Liabilities consist of: Management fee of $587,210, Custodian fees of $59,938, Chief Compliance Officer fees of $2,705 and Transfer Agent fees of $16.

(c) Each board member of the fund also serves as a board member of other funds in the BNY Mellon Family of Funds complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Trustees of Dreyfus Treasury and Agency Liquidity Money Market Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Dreyfus Treasury and Agency Liquidity Money Market Fund (the “Fund”) (the sole fund constituting Dreyfus Institutional Liquidity Funds (the “Trust”)), including the statement of investments, as of November 30, 2024, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (the sole fund constituting Dreyfus Institutional Liquidity Funds) at November 30, 2024, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

These financial statements are the responsibility of the Trust’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Trust in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Trust is not required to have, nor were we engaged to perform, an audit of the Trust’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purposes of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2024, by correspondence with the custodian, brokers and others; when replies were not received from brokers and others, we preformed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more investment companies in the BNY Mellon Family of Funds since at least 1957, but we are unable to determine the specific year.

New York, New York

January 23, 2025

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes, the fund hereby reports 100.00% of ordinary income dividends paid during the fiscal period ended November 30, 2024 as qualifying interest related dividends.

Item 8. Changes in and Disagreements with Accountants for Open-End Management Investment Companies (Unaudited)

Item 9. Proxy Disclosures for Open-End Management Investment Companies (Unaudited)

Item 10. Remuneration Paid to Directors, Officers, and Others of Open-End Management Investment Companies (Unaudited)

Each board member also serves as a board member of other funds in the BNY Mellon Family of Funds complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets. Trustees fees paid by the fund are within Item 7. Statement of Operations as Trustees’ fees and expenses.

Item 11. Statement Regarding Basis for Approval of Investment Advisory Contracts (Unaudited)

© 2025 BNY Mellon Securities CorporationCode-4123NCSRAR1124

| Item 12. | Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies. |

Not applicable.

| Item 13. | Portfolio Managers for Closed-End Management Investment Companies. |

Not applicable.

| Item 14. | Purchases of Equity Securities By Closed-End Management Investment Companies and Affiliated Purchasers. |

Not applicable.

| Item 15. | Submission of Matters to a Vote of Security Holders. |

There have been no material changes to the procedures applicable to Item 15.

| Item 16. | Controls and Procedures. |

| (a) | The Registrant's principal executive and principal financial officers have concluded, based on their evaluation of the Registrant's disclosure controls and procedures as of a date within 90 days of the filing date of this report, that the Registrant's disclosure controls and procedures are reasonably designed to ensure that information required to be disclosed by the Registrant on Form N-CSR is recorded, processed, summarized and reported within the required time periods and that information required to be disclosed by the Registrant in the reports that it files or submits on Form N-CSR is accumulated and communicated to the Registrant's management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure. |

| (b) | There were no changes to the Registrant's internal control over financial reporting that occurred during the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant's internal control over financial reporting. |

| Item 17. | Disclosure of Securities Lending Activities for Closed-End Management Investment Companies. |

Not applicable.

| Item 18. | Recovery of Erroneously Awarded Compensation. |

Not applicable.

(a)(1) Code of ethics referred to in Item 2.

(a)(3) Not applicable.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

Dreyfus Institutional Liquidity Funds

By: /s/ David J. DiPetrillo

David J. DiPetrillo

President (Principal Executive Officer)

Date: January 17, 2025

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this Report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated.

By: /s/ David J. DiPetrillo

David J. DiPetrillo

President (Principal Executive Officer)

Date: January 17, 2025

By: /s/ James Windels

James Windels

Treasurer (Principal Financial Officer)

Date: January 17, 2025

EXHIBIT INDEX

| (a)(1) | Code of ethics referred to in Item 2. |

| (a)(2) | Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940. (EX-99.CERT) |

| (b) | Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940. (EX-99.906CERT) |