| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207340-05 | ||

October 20, 2017 FREE WRITING PROSPECTUS COLLATERAL TERM SHEET $743,403,651 (Approximate Total Mortgage Pool Balance) UBS 2017-C5 UBS Commercial Mortgage Securitization Corp.DepositorUBS AG Cantor Commercial Real Estate Lending, L.P. Ladder Capital Finance LLC Natixis Real Estate Capital LLC Société Générale Rialto Mortgage Finance, LLC Sponsors and Mortgage Loan Sellers UBS Securities LLC Cantor Fitzgerald & Co. Société Générale Co-Lead Managers and Joint Bookrunners NATIXIS Academy Securities Co-Managers The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (’’SEC’’) (SEC File No. 333-207340) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-877-713-1030 (8 a.m. – 5 p.m. EST). The Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale and ultimately by the final prospectus relating to the offered certificates. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward- looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) that have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of the offered certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the offered certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of UBS Securities LLC, Cantor Fitzgerald & Co., SG Americas Securities, LLC, Natixis Securities Americas LLC or Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the offered certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The offered certificates described herein are not suitable investments for all investors. In particular, you should not purchase any class of offered certificates unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with such class of certificates. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity and the aggregate amount and timing of distributions on the offered certificates are subject to material variability from period to period and give rise to the potential for significant loss over the life of such certificates. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered certificates involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the certificates. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered certificates described in this free writing prospectus.

This free writing prospectus is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this free writing prospectus may not pertain to any securities that will actually be sold. The information contained in this free writing prospectus may be based on assumptions regarding market conditions and other matters as reflected in this free writing prospectus. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this free writing prospectus should not be relied upon for such purposes. The Underwriters and their respective affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this free writing prospectus may, from time to time, have long or short positions in, and buy or sell, the offered certificates mentioned in this free writing prospectus or derivatives thereof (including options). Information contained in this free writing prospectus is current as of the date appearing on this free writing prospectus only. None of UBS Securities LLC, Cantor Fitzgerald & Co., SG Americas Securities, LLC, Natixis Securities Americas LLC or Academy Securities, Inc. provides accounting, tax or legal advice.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

The issuing entity will be relying upon an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Other Risks Relating to the Certificates—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

UBS 2017-C5

Capitalized terms used but not defined herein have the meanings assigned to them in the preliminary prospectus expected to be dated October 25, 2017 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | |

| Co-Lead Managers and Joint Bookrunners: | UBS Securities LLC Cantor Fitzgerald & Co.

|

| Co-Managers: | Natixis Securities Americas LLC Academy Securities, Inc. |

| Mortgage Loan Sellers: | UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS AG”) 37.6%, Cantor Commercial Real Estate Lending, L.P. (“CCRE”) 18.4%, Ladder Capital Finance LLC (“LCF”) 14.9%, Natixis Real Estate Capital LLC (“Natixis”) 11.0%, Société Générale (“SG”) 10.6%, Rialto Mortgage Finance, LLC (“RMF”) 7.5% |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Trustee: | Wells Fargo Bank, National Association |

| Certificate Administrator: | Wells Fargo Bank, National Association |

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc., Moody’s Investors Service, Inc. and S&P Global Ratings, Inc. |

| U.S. Credit Risk Retention: | UBS AG is expected to act as the“retaining sponsor”for this securitization and intends to satisfy the U.S. credit risk retention requirement through the purchase by KKR Real Estate Credit Opportunity Partners Aggregator I L.P., as a third party purchaser (as defined in Regulation RR), from the initial purchasers, on the Closing Date, of an “eligible horizontal residual interest”. The aggregate estimated fair value of the “eligible horizontal residual interest” will equal at least 5% of this estimated fair value of all of the Certificates (other than the Class R certificates) issued by the issuing entity. The pooling and servicing agreement will include the required provisions applicable to an operating advisor necessary for the securitization to comply with the credit risk retention rules utilizing the “third party purchaser” option. See “Operating Advisor” below. For additional information, see “Credit Risk Retention” below. |

| EU Credit Risk Retention: | The transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Determination Date: | The 11th day of each month, or if such 11th day is not a business day, the succeeding business day, commencing in December 2017. |

| Distribution Date: | The 4th business day following the Determination Date in each month, commencing in December 2017. |

| Cut-off Date: | The mortgage loans will be considered part of the trust fund as of their respective cut-off dates. The cut-off date with respect to each mortgage loan is the respective due date for the monthly debt service payment that is due in November 2017 (or, in the case of any mortgage loan that has its first due date after November 2017, the date that would have been its due date in November 2017 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). |

| Closing Date: | On or about November 8, 2017 |

| Clean-up Call: | 1.0%

|

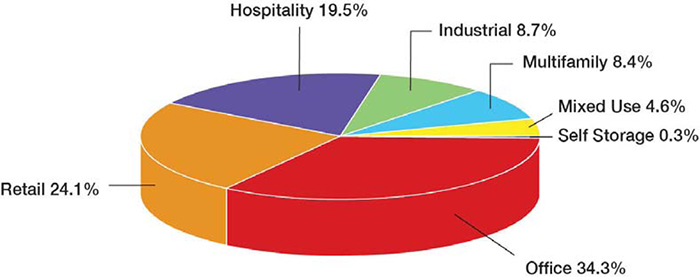

| Distribution of Collateral by Property Type | |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

UBS 2017-C5

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance(1) |

| UBS AG | 17 | 56 | $279,553,812 | 37.6% |

| Cantor Commercial Real Estate Lending, L.P. | 11 | 12 | $136,465,789 | 18.4% |

| Ladder Capital Finance LLC | 7 | 24 | $111,094,306 | 14.9% |

| Natixis Real Estate Capital LLC | 4 | 14 | $81,722,688 | 11.0% |

| Société Générale | 4 | 19 | $78,550,000 | 10.6% |

| Rialto Mortgage Finance, LLC | 6 | 6 | $56,017,057 | 7.5% |

| Total | 49 | 131 | $743,403,651 | 100.0% |

| Pooled Collateral Facts: | |

| Initial Outstanding Pool Balance: | $743,403,651 |

| Number of Mortgage Loans: | 49 |

| Number of Mortgaged Properties: | 131 |

| Average Mortgage Loan Cut-off Date Balance: | $15,171,503 |

| Average Mortgaged Property Cut-off Date Balance: | $5,674,837 |

| Weighted Average Mortgage Rate: | 4.346% |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 110 |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 108 |

| Weighted Average Mortgage Loan Seasoning (months): | 2 |

| % of Mortgaged Properties Leased to a Single Tenant: | 24.0% |

| % of Mortgaged Properties Leased to a Single Tenant Excluding Portfolio(2): | 6.4% |

| Credit Statistics: | |

| Weighted Average Mortgage Loan U/W NCF DSCR(3): | 2.37x |

| Weighted Average Mortgage Loan Cut-off Date LTV(3)(4): | 54.6% |

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(3)(4): | 49.6% |

| Weighted Average U/W NOI Debt Yield(3): | 12.2% |

| Amortization Overview: | |

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 28.7% |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD: | 44.8% |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 26.5% |

| Weighted Average Remaining Amortization Term (months)(5): | 354 |

| (1) | Unless otherwise indicated, all references to “% of Outstanding Pool Balance” in this Term Sheet reflect a percentage of the aggregate principal balance of the mortgage pool as of the Cut-off Date, after application of all payments of principal due during or prior to November 2017. |

| (2) | Excludes mortgage loans secured by multiple properties leased to the same tenant. |

| (3) | With respect to any mortgage loan that is part of a whole loan, unless otherwise indicated, LTV, DSCR and Debt Yield calculations in this Term Sheet include any related pari passu companion loans and exclude any subordinate companion loans, as applicable. Additionally, LTV, DSCR and Debt Yield figures in this Term Sheet are calculated for mortgage loans without regard to any additional indebtedness that may be incurred at a future date. |

| (4) | With respect to mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as the 237 Park Avenue, the Cut-off Date LTV and Maturity Date LTV has been calculated based on the “As-Is Assuming Reserves” value of $1,310,000,000 as of May 22, 2017, which assumes upfront reserves of $81,365,605 for capital expenditures and tenant improvements and leasing costs for recently signed leases in addition to a $7,500,000 escrow and letters of credit in an aggregate amount of $8,500,000 to cover interest and free rent payments, specifically for a portion of the free rent provided to The New York and Presbyterian Hospital and Her Majesty the Queen in Right of Canada spaces. With respect to the AHIP Northeast Portfolio III Mortgage Loan, the Cut-off Date LTV Ratio and Maturity Date LTV is based on the Appraised Value of $87.5 million, which assumes the “As-Complete” appraised value as of June 1, 2018 for the Fairfield Inn & Suites Baltimore – White Marsh Mortgaged Property, the SpringHill Suites – Bellport Mortgaged Property and the Hampton Inn Baltimore – White Marsh Mortgaged Property, and June 1, 2019 for the Homewood Suites – Egg Harbor Mortgaged Property. The Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD with respect to the Mortgage Loan based on the aggregate $82.5 million “As-Is” appraised value is 63.5% and 58.2%, respectively. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as DoubleTree Wilmington, the Cut-off Date LTV and Maturity Date LTV has been calculated based on the “As-Complete” value of $42.4 million as of September 20, 2018, which assumes the completion of a Property Improvement Plan which has been reserved for. The Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD based on the $37.0 million “As-Is” appraised value are 74.3% and 61.5%, respectively. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Holiday Inn Express Tallahassee, the Cut-off Date LTV and Maturity Date LTV has been calculated based on the “Upon Completion” value of $14,000,000 as of April 1, 2018, which assumes the completion of a Property Improvement Plan (“PIP”). At origination, the borrower deposited $1,034,000 into a PIP reserve to cover the cost of such PIP. The Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD based on the $13.0 million “As-Is” appraised value are 71.9% and 54.3%, respectively. For additional information, see “Description of the Mortgage Pool—Mortgage Pool Characteristics – Appraised Value” in the Preliminary Prospectus and the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (5) | Excludes mortgage loans that are interest-only for the full loan term. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

| Mortgage Loan Information | Property Information | |||||||

| Mortgage Loan Seller(1): | UBS AG | Single Asset/Portfolio: | Portfolio | |||||

| Credit Assessment (Fitch/KBRA/Moody’s/S&P): | [ ] | Location: | Burbank, CA | |||||

| General Property Type: | Office | |||||||

| Original Balance(2): | $40,000,000 | Detailed Property Type: | CBD | |||||

| Cut-off Date Balance(2): | $40,000,000 | Title Vesting: | Fee | |||||

| % of Initial Pool Balance: | [.]% | Year Built/Renovated: | Various | |||||

| Loan Purpose: | Acquisition | Size: | 2,087,579 SF | |||||

| Borrower Sponsors: | Blackstone Property Partners; The Worthe Real Estate Group, Inc. | Cut-off Date Balance per SF(2): | $182 | |||||

| Maturity Date Balance per SF(2): | $182 | |||||||

| Mortgage Rate: | 3.5410% | Property Manager:

| The Worthe Real Estate Group, Inc. (borrower-related)

| |||||

| Note Date: | 9/19/2017 | |||||||

| First Payment Date: | 11/6/2017 | |||||||

| Maturity Date: | 10/6/2024 | |||||||

| Original Term to Maturity: | 84 months | |||||||

| Original Amortization Term: | 0 months | |||||||

| IO Period: | 84 months | |||||||

| Seasoning: | 1 month | Underwriting and Financial Information | ||||||

| Prepayment Provisions(3): | YM0.5 (25); DEF/YM0.5 (52); O (7) | UW NOI(6): | $68,486,656 | |||||

| Lockbox/Cash Mgmt Status: | Hard/Springing | UW NOI Debt Yield(2): | 18.1% | |||||

| Additional Debt Type(2)(4): | Pari Passu/Subordinate Debt | UW NOI Debt Yield at Maturity(2): | 18.1% | |||||

| Additional Debt Balance(2)(4): | $339,000,000/$281,000,000 | UW NCF DSCR(2): | 4.64x | |||||

| Future Debt Permitted (Type): | No (N/A) | Most Recent NOI(6): | $54,023,848 (6/30/2017 TTM) | |||||

| Reserves(5) | 2nd Most Recent NOI(6): | $44,798,547 (12/31/2016) | ||||||

| Type | Initial | Monthly | Cap | 3rd Most Recent NOI(6): | $34,442,280 (12/31/2015) | |||

| RE Tax: | $0 | Springing | N/A | Most Recent Occupancy(7): | 92.4% (8/31/2017) | |||

| Insurance: | $0 | Springing | N/A | 2nd Most Recent Occupancy: | 88.8% (12/31/2016) | |||

| Replacements: | $0 | Springing | N/A | 3rd Most Recent Occupancy: | 88.4% (12/31/2015) | |||

| TI/LC: | $14,151,048 | Springing | N/A | Appraised Value (as of): | $1,038,000,000 (8/24/2017) | |||

| Window Repairs Reserve: | $18,000,000 | $0 | N/A | Cut-off Date LTV Ratio(2): | 36.5% | |||

| Free Rent Reserve: | $3,617,000 | Springing | N/A | Maturity Date LTV Ratio(2): | 36.5% | |||

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Loan Amount(2): | $660,000,000 | 63.5% | Purchase Price: | $1,027,500,000 | 98.9% | |

| Borrower Equity: | $378,783,040 | 36.5% | Reserves: | $35,768,047 | 3.4% | |

| Prorations(8): | ($42,173,543) | (4.1%) | ||||

| Closing Costs: | $17,688,535 | 1.7% | ||||

| Total Sources: | $1,038,783,040 | 100.0% | Total Uses: | $1,038,783,039 | 100.0% | |

| (1) | The Burbank Office Portfolio Whole Loan (as defined below) was co-originated by Deutsche Bank AG, New York Branch and UBS AG. |

| (2) | The Burbank Office Portfolio Mortgage Loan (as defined below) is part of the Burbank Office Portfolio Whole Loan, which is comprised of ninepari passusenior promissory notes with an aggregate principal balance of $379,000,000 and two subordinate promissory notes with an aggregate principal balance of $281,000,000. The Cut-off Date Balance per SF, Maturity Date Balance per SF, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV Ratio presented above are based on the aggregate principal balance of the promissory notes comprising the Burbank Office Portfolio Senior Loan, without regard to the Burbank Office Portfolio Subordinate Companion Loans (as defined below). The Cut-off Date Balance per SF, Maturity Date Balance per SF, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV Ratio numbers based on the entire $660,000,000 Burbank Office Portfolio Whole Loan are $316, $316, 10.4%, 10.4%, 2.67x, 63.6% and 63.6%, respectively. |

| (3) | Prior to the open prepayment date of April 6, 2024, the Burbank Office Portfolio Whole Loan can be prepaid with (i) defeasance after the earlier to occur of (a) November 6, 2020 and (b) the first monthly payment date following the end of the two-year period commencing on the closing date of the securitization of the last Burbank Office Portfolio Whole Loan promissory note or (ii) yield maintenance. Partial release is permitted. See “Release of Property” below for further discussion of release requirements. |

| (4) | See “The Mortgage Loan” and “Additional Secured Indebtedness (not including trade debts)” below for further discussion of additional debt. |

| (5) | See “Escrows and Reserves” below for further discussion of reserve requirements. |

| (6) | The increase in UW NOI over historical periods is primarily driven by the expiration of rent abatements, recently executed leases and leases going into effect. See “Cash Flow Analysis” for further discussion of historical operating performance. |

| (7) | Includes Lopez Accounting Group (552 SF), which took occupancy at the Central Park Property on September 1, 2017, and Turner Broadcasting (5,435 SF), which has a rent commencement date of January 1, 2018. |

| (8) | Includes credits for rent and parking abatements, leasing costs, capital improvements that are the responsibility of certain separate joint ventures comprised of affiliates of The Worthe Real Estate Group, Inc. and certain third parties, balance sheet cash purchased by the borrower sponsors and prorations for rents, taxes, operating expenses and security deposits. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

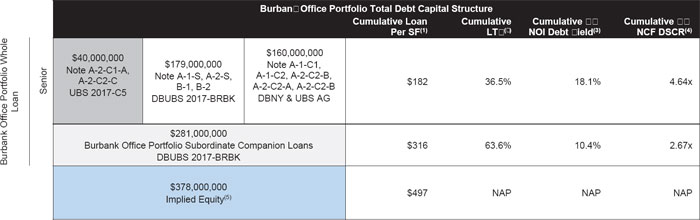

The Mortgage Loan. The largest mortgage loan (the “Burbank Office Portfolio Mortgage Loan”) is part of a whole loan (the “Burbank Office Portfolio Whole Loan”) with an original principal balance of $660,000,000. The Burbank Office Portfolio Whole Loan is secured by the first priority fee mortgages encumbering a four-property portfolio of office developments totaling 2,087,579 SF located in Burbank, California within the Burbank Media District (collectively, the “Burbank Office Portfolio Properties”). The Burbank Office Portfolio Whole Loan was co-originated by UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS AG”) and Deutsche Bank AG, New York Branch (“DBNY”). The Burbank Office Portfolio Whole Loan is comprised of (i) a senior loan, evidenced by nine seniorpari passunotes, with an aggregate outstanding principal balance of $379,000,000 (collectively, the “Burbank Office Portfolio Senior Loan”) and (ii) a subordinate companion loan, evidenced by two subordinate notes, with an aggregate outstanding principal balance of $281,000,000 (the “Burbank Office Portfolio Subordinate Companion Loans”), each as described below. Promissory Notes A-2-C1-A and A-2-C2-C, with an aggregate outstanding principal balance of $40,000,000, represents the Burbank Office Portfolio Mortgage Loan and will be included in the UBS 2017-C5 Trust. Promissory Notes A-1-S and A-2-S, with an aggregate outstanding principal balance of $179,000,000, and the Burbank Office Portfolio Subordinate Companion Loans, are expected to be contributed to the DBUBS 2017-BRBK Trust. The remaining seniorpari passuPromissory Notes A-1-C1, A-1-C2, A-2-C1-B, A-2-C2-A and A-2-C2-B, with an aggregate principal balance of $160,000,000, (the “Burbank Office Portfolio Pari Passu Companion Loans”) are currently held by UBS AG and DBNY, or affiliates thereof, and are expected to be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The Burbank Office Portfolio Whole Loan will be serviced pursuant to the trust and servicing agreement for the DBUBS 2017-BRBK Trust. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus.

| Burbank Office Portfolio Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Anticipated Note Holder | Controlling Piece |

| Note A-1-S | $127,400,000 | $127,400,000 | DBUBS 2017-BRBK | Yes |

| Note A-1-C1 | $50,000,000 | $50,000,000 | DBNY | No |

| Note A-1-C2 | $50,000,000 | $50,000,000 | DBNY | No |

| Note A-2-S | $51,600,000 | $51,600,000 | DBUBS 2017-BRBK | No |

| Note A-2-C1-A | $30,000,000 | $30,000,000 | UBS 2017-C5 | No |

| Note A-2-C2-B | $20,000,000 | $20,000,000 | UBS AG | No |

| Note A-2-C2-A | $25,000,000 | $25,000,000 | UBS AG | No |

| Note A-2-C2-B | $15,000,000 | $15,000,000 | UBS AG | No |

| Note A-2-C2-C | $10,000,000 | $10,000,000 | UBS 2017-C5 | No |

| Note B-1 | $168,600,000 | $168,600,000 | DBUBS 2017-BRBK | No |

| Note B-2 | $112,400,000 | $112,400,000 | DBUBS 2017-BRBK | No |

| Total | $660,000,000 | $660,000,000 | ||

| (1) | Cumulative Loan Per SF is calculated based on 2,087,579 SF. |

| (2) | Based on the “as-is” appraised value of $1.038 billion ($497 PSF) as of August 24, 2017 per the appraisal. |

| (3) | Based on the UW NOI of $68,486,656. |

| (4) | Based on the UW NCF of $63,159,124 and the coupon of 3.5410% on the Burbank Office Portfolio Whole Loan. |

| (5) | Implied Equity is based on the “as-is” appraised value of $1.038 billion, less debt of $660.0 million. |

The Borrowers and the Borrower Sponsors. The borrowers are 3800 Alameda Owner, LLC, Catalina Media Development, LLC, 3500 Partners, LLC, 3100 Partners, LLC, 2255 Partners LLC, and MSN III and IV LLC, each a Delaware limited liability company, and Avon Empire Partners, LLC, a California limited liability company (collectively, the “Burbank Office Portfolio Borrower”), each a single-purpose entity structured to be bankruptcy remote. Blackstone Property Partners Lower Fund 1 L.P., an affiliate of the Blackstone Property Partners borrower sponsor, is the nonrecourse carve-out guarantor (the “Burbank Office Group Guarantor”). Notwithstanding anything to the contrary, so long as one or more entities affiliated with Blackstone Property Partners is the guarantor or substitute guarantor, the Burbank Office Group Guarantor will not be required to maintain a minimum net worth, excluding its interest in the Burbank Office Portfolio Properties, of $150,000,000. See “Description of the Mortgage Pool—Non-Recourse Carveout Limitation” in the Preliminary Prospectus.

The borrower sponsors are Blackstone Property Partners (“Blackstone”) and The Worthe Real Estate Group, Inc. (“Worthe”). Blackstone is the largest private equity real estate investment manager in the world with $104 billion of real estate assets under management through its debt strategy businesses.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

The breadth of Blackstone’s portfolio includes premier properties in many top locations in the U.S., Europe, Asia and Latin America, with a diverse mix of hospitality, office, retail, industrial, and residential investments, with aggregate value of gross assets of approximately $200 billion. Blackstone’s portfolio includes approximately 222 million SF of office space globally, making it one of the largest owners of office properties in the U.S. Worthe is a real estate development firm specializing in media and technology campuses in Los Angeles. With an existing portfolio of 37 assets totaling approximately 5.4 million SF, Worthe is the largest owner and manager of real estate by square footage in Burbank and currently manages the Burbank Office Portfolio Properties. In connection with the origination of the Burbank Office Portfolio Whole Loan, Blackstone, through one or more affiliates, acquired an 80.0% interest in each of the Burbank Office Portfolio Properties from certain separate joint ventures comprised of affiliates of Worthe and certain third parties and Worthe, through one or more affiliates, acquired or retained the remaining 20.0% interest in each property in the Burbank Office Portfolio Properties.

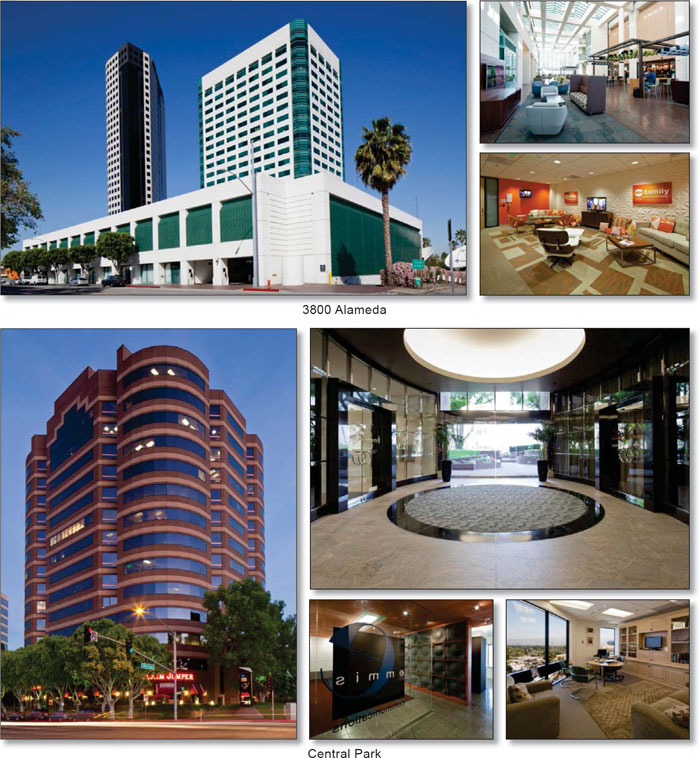

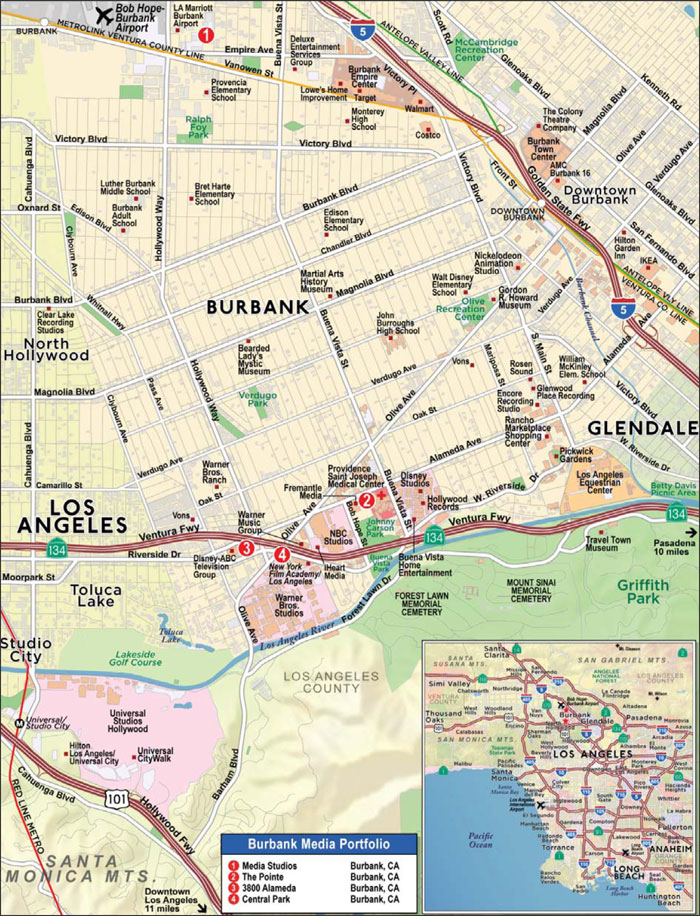

The Properties. The Burbank Office Portfolio Properties are comprised of four office properties totaling 2,087,579 SF located in Burbank, California in the Burbank Media District. The Burbank Office Portfolio Properties were constructed between 1969 and 2009 and range in size from 256,159 SF to 926,365 SF. The Burbank Office Portfolio Properties are approximately 92.4% occupied as of August 31, 2017 and are leased to 53 tenants, including many prominent media and entertainment companies. Approximately 68.1% of the total NRA is leased to investment grade tenants. Excluding The Pointe Property, which was developed in 2009, the Burbank Office Portfolio has a 10-year historical occupancy average of 96.0%.

The following tables present certain information relating to the Burbank Office Portfolio Properties:

| Portfolio Summary | |||||||||

| Property Name | Location | Year Built/ Renovated | Net Rentable Area (SF)(1) | UW NCF | % of UW NCF | Allocated Cut-off Date Balance(2) | % of Allocated Cut-off Date Balance | Appraised Value | Allocated Cut-off Date LTV Ratio(2) |

| Media Studios | Burbank, CA | 1996-2006/N/A | 926,365 | $22,575,888 | 35.7% | $143,244,773 | 37.8% | $410,000,000 | 34.9% |

| The Pointe | Burbank, CA | 2009/N/A | 480,167 | $18,626,181 | 29.5% | $122,083,939 | 32.2% | $325,000,000 | 37.6% |

| 3800 Alameda | Burbank, CA | 1984/2008 | 424,888 | $13,797,326 | 21.8% | $69,856,591 | 18.4% | $183,000,000 | 38.2% |

| Central Park | Burbank, CA | 1984/N/A | 256,159 | $8,159,730 | 12.9% | $43,814,697 | 11.6% | $120,000,000 | 36.5% |

| Total/Wtd. Avg. | 2,087,579 | $63,159,124 | 100.0% | $379,000,000 | 100.0% | $1,038,000,000 | 36.5% | ||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Based on the Burbank Office Portfolio Senior Loan amount. |

The Media Studios Property is comprised of five, Class A office buildings totaling 926,365 SF and is 85.9% occupied as of August 31, 2017. Phase I was completed in 1996 and Phases II through V were completed between 1998 and 2006, and the buildings range in size between 95,430 SF and 230,145 SF. Situated on 14.8 acres, the property is LEED Gold Certified and has also received Energy Star recognition in recent years. The Media Studios Property contains a 209-seat, 12,000 SF dual-screen screening room, two full-service commissary facilities, and a 12,000 SF fitness center equipped with locker rooms and showers. Additional amenities on site include a jogging track, sand volleyball court, putting green, basketball courts, landscaped gardens, public art installations and a shuttle service. Wi-Fi network connectivity is provided throughout the campus for the outdoor seating plazas and picnic areas. Parking at the property is provided via 2,960 spaces (3.3 spaces per 1,000 SF). The largest tenants at the Media Studios Property are Kaiser Foundation Health Plan (S&P: AA-), which comprises 21.0% of property NRA and 24.5% of property UW Base Rent, and Walt Disney Pictures (Fitch/Moody’s/S&P: A/A2/A+), which comprises 16.2% of property NRA and 18.9% of property UW Base Rent.

The Pointe Property is a 480,167 SF Class A, 14-story office building and is 95.6% occupied as of August 31, 2017. Built in 2009, the property is LEED Gold Certified and has received Energy Star recognition in recent years. The property features panoramic views with floor-to-ceiling glass windows, outdoor seating and dining patio, and a full-service health club. In addition, The Pointe Property contains two electric vehicle charging stations and a full-service detailing center for car washes and details. Parking at the property is provided via 1,391 spaces (2.9 spaces per 1,000 SF). The Pointe Property’s largest tenant is Legendary (Fitch/S&P: BBB/BB), which utilizes its space at the property for its headquarters operations. Legendary, which comprises 22.0% of property NRA and 23.2% of property UW Base Rent, is a media company with film, television, digital, and comics productions, that have realized gross ticket sales, in aggregate, of over $10 billion worldwide at box offices.

The 3800 Alameda Property is a 424,888 SF Class A, 21-story office building and is 100.0% occupied as of August 31, 2017. The property was built in 1984 and redeveloped in 2008. Disney (NYSE: DIS; Fitch/Moody’s/S&P: A/A2/A+) is the primary tenant at the property (98.3% of property NRA, 98.8% of property UW Base Rent) and its corporate headquarters are located approximately 1.2 miles away. The 3800 Alameda property serves as the world headquarters for Radio Disney and broadcasting home for ESPN, Disney Channel, Disney Junior, Disney XD and Freeform. There are transmission facilities in the lobby and subterranean levels that are utilized by Disney and its affiliated channels in addition to numerous satellite dishes installed on the adjacent seven-story parking structure, which is also collateral for the 3800 Alameda property. In total, there are approximately 12 networks transmitted from the property. Over the past 20 years, Disney has invested approximately $40.0 million into the property, including $9.0 million since 2008. Parking at the property is provided via 1,084 spaces (2.6 spaces per 1,000 SF).

The Central Park property is a 256,159 SF Class A, 14-story office building situated on 1.5 acres and is 97.3% occupied as of August 31, 2017. The property was built in 1984 and there are current plans for a $1.5 million renovation to the lobby slated for 2018. The property features a City National Bank on the ground floor, full-service Claim Jumper Restaurant, and a full-service car wash and detailing service center. Parking at the property is provided via 734 spaces (2.9 spaces per 1,000 SF). The largest tenant at the Central Park Property is Turner Broadcasting (Fitch/Moody’s/S&P: BBB+/Baa2/BBB), which comprises 24.7% of property NRA and 25.0% of property UW Base Rent.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

The following table presents certain information relating to the leases at the Burbank Office Portfolio Properties:

| Tenant Summary(1) | ||||||||

| Tenant Name | Property | Credit Rating (Fitch/Moody’s/ S&P)(2) | Tenant SF | Approximate % of SF | Annual UW Base Rent | % of Total Annual Base UW Rent | Annual UW Base Rent PSF(3) | Lease Expiration |

| Disney | 3800 Alameda | A/A2/A+ | 417,731 | 20.0% | $17,734,050 | 21.5% | $42.45 | Various(4) |

| Kaiser Foundation Health Plan | Media Studios | NR/NR/AA- | 194,145 | 9.3% | $7,804,629 | 9.5% | $40.20 | 5/31/2024 |

| Warner Bros. | Central Park/The Pointe | BBB+/Baa2/BBB | 162,047 | 7.8% | $7,395,121 | 9.0% | $45.64 | Various(5) |

| Walt Disney Pictures | Media Studios | A/A2/A+ | 149,840 | 7.2% | $6,015,360 | 7.3% | $40.15 | Various(6) |

| Legendary | The Pointe | BBB/NR/BB | 105,522 | 5.1% | $5,092,656 | 6.2% | $48.26 | Various(7) |

| Yahoo(8) | Media Studios | A-/Baa1/BBB+ | 105,400 | 5.0% | $4,340,568 | 5.3% | $41.18 | 5/31/2020 |

| Hasbro | Media Studios | BBB+/Baa1/BBB | 80,000 | 3.8% | $3,165,717 | 3.8% | $39.57 | 1/31/2027 |

| FremantleMedia(9) | The Pointe | NR/NR/BBB+ | 72,328 | 3.5% | $3,361,082 | 4.1% | $46.47 | 10/31/2024 |

| Turner Broadcasting | Central Park | BBB+/Baa2/BBB | 63,283 | 3.0% | $2,658,911 | 3.2% | $42.02 | 2/29/2024 |

| TiVo Corporation(10) | Media Studios | NR/NR/NR | 61,732 | 3.0% | $3,294,637 | 4.0% | $53.37 | 6/30/2019 |

| Subtotal/Wtd. Avg. | 1,412,028 | 67.6% | $60,862,732 | 73.9% | $43.10 | |||

| Remaining Tenants(11) | 517,161 | 24.8% | $21,498,744 | 26.1% | $41.57 | |||

| Vacant Space | 158,390 | 7.6% | $0 | 0.0% | $0.00 | |||

| Total/Wtd. Avg. | 2,087,579 | 100.0% | $82,361,475 | 100.0% | $42.69 | |||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Ratings provided are for the parent company of the entity listed in the “Tenant Name” field whether or not the parent company guarantees the lease. |

| (3) | Total/Wtd. Avg. Annual UW Base Rent PSF excludes vacant space. |

| (4) | Disney leases 357,820 SF and 59,911 SF at the 3800 Alameda Property, with lease expirations on March 27, 2021 and March 27, 2023, respectively. |

| (5) | Warner Bros. leases 99,853 SF at The Pointe Property with lease expirations on November 30, 2025 and 60,092 SF and 2,102 SF at the Central Park Property, with lease expirations on June 30, 2022, and December 31, 2017, respectively. Warner Bros. has the option to terminate 99,853 SF of its space at The Pointe Property on December 31, 2022 upon 12 months’ written notice and payment of a termination fee. |

| (6) | Walt Disney Pictures leases 131,172 SF and 18,668 SF at the Media Studios Property, with lease expirations on May 31, 2021 and April 30, 2022, respectively. |

| (7) | Legendary leases 70,018 SF and 35,504 SF at The Pointe Property, with lease expirations on October 31, 2024 and March 31, 2025, respectively. |

| (8) | Yahoo is currently dark but paying rent. |

| (9) | FremantleMedia has the option to terminate its lease on August 31, 2020 upon written notice by May 31, 2019. |

| (10) | TiVo Corporation subleases 6,881 SF to Jones Lang LaSalle at the Media Studios Property. The sublease is coterminous with TiVo Corporation’s lease with an expiration date of June 30, 2019. |

| (11) | Includes Lopez Accounting Group (552 SF), which took occupancy at the Central Park Property on September 1, 2017, and Turner Broadcasting (5,435 SF), which has a rent commencement date of January 1, 2018. |

The following table presents certain information relating to the lease rollover schedule at the Burbank Office Portfolio Properties:

| Lease Rollover Schedule(1)(2) | ||||||||

| Year | # of Leases Rolling | SF Rolling | Approx. % of Total SF Rolling | Approx. Cumulative % of SF Rolling | UW Base Rent PSF Rolling(3) | Total UW Base Rent Rolling | Approx. % of Total Rent Rolling | Approx. Cumulative % of Total Rent Rolling |

| MTM | 0 | 0 | 0.0% | 0.0% | $0.00 | $0 | 0.0% | 0.0% |

| 2017 | 2 | 20,621 | 1.0% | 1.0% | $43.39 | $894,797 | 1.1% | 1.1% |

| 2018 | 7 | 21,968 | 1.1% | 2.0% | $32.42 | $712,294 | 0.9% | 2.0% |

| 2019 | 12 | 136,665 | 6.5% | 8.6% | $47.29 | $6,462,928 | 7.8% | 9.8% |

| 2020 | 10 | 153,456 | 7.4% | 15.9% | $41.18 | $6,319,707 | 7.7% | 17.5% |

| 2021 | 24 | 584,705 | 28.0% | 43.9% | $42.79 | $25,020,075 | 30.4% | 47.8% |

| 2022 | 15 | 193,351 | 9.3% | 53.2% | $42.90 | $8,295,186 | 10.1% | 57.9% |

| 2023 | 7 | 119,380 | 5.7% | 58.9% | $44.05 | $5,258,128 | 6.4% | 64.3% |

| 2024 | 12 | 403,458 | 19.3% | 78.3% | $43.16 | $17,414,635 | 21.1% | 85.4% |

| 2025 | 5 | 135,357 | 6.5% | 84.7% | $46.95 | $6,354,445 | 7.7% | 93.2% |

| 2026 | 0 | 0 | 0.0% | 84.7% | $0.00 | $0 | 0.0% | 93.2% |

| 2027 | 6 | 113,795 | 5.5% | 90.2% | $41.20 | $4,688,890 | 5.7% | 98.9% |

| 2028 & Beyond | 7 | 46,433 | 2.2% | 92.4% | $20.25 | $940,392 | 1.1% | 100.0% |

| Vacant | 0 | 158,390 | 7.6% | 100.0% | $0.00 | $0 | 0.0% | 100.0% |

| Total/Wtd. Avg. | 107 | 2,087,579 | 100.0% | $42.69 | $82,361,475 | 100.0% | ||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the lease rollover schedule. |

| (3) | Wtd. Avg. UW Base Rent PSF Rolling excludes vacant space. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

The Market. The Burbank Office Portfolio Properties are located within the Burbank Media District submarket within the larger Los Angeles North market area. According to the appraisal, the Los Angeles North office market contains a total inventory of approximately 55.4 million SF across 600 buildings. As of the second quarter 2017, the office submarket had a direct vacancy rate of 11.3% and a weighted average rental rate of $32.21 PSF, compared to 11.7% and $31.56 PSF, respectively as of year-end 2016. The Burbank Media District submarket contains a total inventory of 3.3 million SF across 19 buildings, a direct vacancy rate of 11.3%, a direct weighted average rental rate of $41.52 PSF and registered 88,569 SF of net absorption in the second quarter of 2017. As of the August 31, 2017 rent roll, the Burbank Office Portfolio has a vacancy rate of 7.6% and a weighted average rental rate of $42.69 PSF.

According to the appraisal, Burbank is the central hub of the global entertainment industry and is the location for three major studios: Disney, Warner Bros., and Comcast’s NBCUniversal. Burbank is also home to over 700 media-related corporations, including television networks, broadcasting companies and music labels. Other entertainment-related companies in the city include Clear Channel, BET, Photo-Cam Motion Picture Laboratories, Broadcast Equipment Rental Corporation (the largest video equipment rental facility in the nation), DC Comics, Rhino Entertainment, Sony, Playboy Enterprises, and Fremantle. The appraisal did not forecast any new construction over the next several years.

The following table presents certain office market information of the East Valley/Tri-Cities grouping within the Los Angeles North market as of the second quarter of 2017:

| Office Market and Submarket Overview(1) | ||||||

| Submarket | Inventory (SF) | Number of Buildings | Direct Vacancy Rate | Overall Vacancy Rate | Direct Net Absorption 2Q2017 | Direct Wtd. Avg. Rental Rate (PSF) |

| Burbank Media District | 3,333,707 | 19 | 11.3% | 11.9% | 88,569 | $41.52 |

| Universal City/Studio City | 1,884,655 | 16 | 3.7% | 3.9% | (7,679) | $34.08 |

| Burbank - City Center | 3,122,300 | 34 | 12.7% | 18.8% | 168,593 | $37.08 |

| Glendale | 5,918,006 | 42 | 11.1% | 11.0% | (6,803) | $32.16 |

| Pasadena | 7,497,885 | 60 | 14.1% | 15.6% | (196,006) | $39.84 |

| Pasadena East | 1,167,737 | 10 | 22.3% | 22.3% | 8,034 | $24.72 |

| North Hollywood | 1,171,666 | 13 | 4.9% | 5.2% | 50,433 | $34.44 |

| Total/Wtd. Avg. | 24,095,956 | 194 | 11.9% | 13.3% | 105,141 | $13.33 |

| (1) | Information is based on the appraisals. |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and the Underwritten Net Cash Flow at the Burbank Office Portfolio Properties:

| Cash Flow Analysis | |||||||||||

| 2014 | 2015(1) | 2016(1) | 6/30/2017 TTM(1) | UW(1) | UW PSF | ||||||

| Gross Potential Rent | $67,639,603 | $68,834,347 | $76,592,277 | $69,584,091(2) | $95,053,054(3) | $45.53 | |||||

| Total Recoveries | $1,854,343 | $2,141,190 | $2,957,882 | $2,308,227 | $2,376,993 | $1.14 | |||||

| Other Income(4) | $7,989,377 | $9,375,318 | $10,645,375 | $10,621,644 | $10,017,115 | $4.80 | |||||

| Less Vacancy & Credit Loss | ($15,247,577) | ($19,053,673) | ($17,348,782) | $0 | ($6,813,889) | ($3.26) | |||||

| Effective Gross Income | $62,235,747 | $61,297,183 | $72,846,752 | $82,513,963 | $100,633,272 | $48.21 | |||||

| Total Operating Expenses | $25,988,009 | $26,854,903 | $28,048,205 | $28,490,114 | $32,146,616 | $15.40 | |||||

| Net Operating Income | $36,247,737 | $34,442,280 | $44,798,547 | $54,023,848 | $68,486,656 | $32.81 | |||||

| Capital Expenditures | $0 | $0 | $0 | $0 | $521,895 | $0.25 | |||||

| TI/LC | $0 | $0 | $0 | $0 | $4,805,637 | $2.30 | |||||

| Net Cash Flow | $36,247,737 | $34,442,280 | $44,798,547 | $54,023,848 | $63,159,124 | $30.25 | |||||

| Occupancy % | 97.8%(5) | 88.4% | 88.8% | 91.7% | 92.4% | ||||||

| NOI DSCR(6) | 2.66x | 2.53x | 3.29x | 3.97x | 5.03x | ||||||

| NCF DSCR(6) | 2.66x | 2.53x | 3.29x | 3.97x | 4.64x | ||||||

| NOI Debt Yield(6) | 9.6% | 9.1% | 11.8% | 14.3% | 18.1% | ||||||

| NCF Debt Yield(6) | 9.6% | 9.1% | 11.8% | 14.3% | 16.7% | ||||||

| (1) | The increase in UW NOI over historical periods is primarily driven by the expiration of rent abatements, recently executed leases and leases going into effect. The 3800 Alameda Property had rent abatements of $10.4 million, $11.2 million and $11.4 million in 2014, 2015 and 2016, respectively. UW NOI does not include a deduction for base rent abatements because base rent abatements for the underwritten leases either do not have any base rent abatements or the remaining abated rent amounts were substantially reserved at origination in the unfunded obligations reserve. |

| (2) | 6/30/2017 TTM Gross Potential Rent is shown net of rent rebates. |

| (3) | UW Gross Potential Rent is based on the underwritten rent roll and includes (i) for non-investment grade tenants, rent steps through October 1, 2018 of $2,480,650, (ii) for investment grade tenants, the average base rent over their respective lease terms of $3,397,039, and (iii) vacancy gross up of $6,813,889. |

| (4) | Other Income includes parking revenue and other miscellaneous income. |

| (5) | 2014 Occupancy excludes The Pointe Property, which was developed in 2009 but in a lease up until 2015. |

| (6) | Debt service coverage ratios and debt yields are based on the Burbank Office Portfolio Senior Loan totaling $379,000,000 and exclude the Burbank Office Portfolio Subordinate Companion Loans. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Burbank, CA | Collateral Asset Summary – Loan No. 1 Burbank Office Portfolio

| Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 36.5% 4.64x 18.1% |

Escrows and Reserves. The Burbank Office Portfolio Borrower deposited in escrow $18,000,000 for window repairs, $14,151,048 for outstanding tenant allowances and $3,617,000 for outstanding free rent and during the continuance of a Cash Sweep Period (as defined below), is required to escrow monthly (i) 1/12 of the annual estimated tax payments, (ii) 1/12 of the annual insurance premiums, (iii) 1/12 of the amount equal to the aggregate net rentable square footage of the Burbank Office Portfolio Properties (if applicable, excluding the net rentable square footage of any released property) times $0.25 for capital expenditures (the “Monthly Replacement Reserve Deposit”), subject to a cap of an amount equal to the Monthly Replacement Reserve Deposit times 12 and (iv) 1/12 of the amount equal to the aggregate net rentable square footage of the Burbank Office Portfolio Properties (if applicable, excluding the net rentable square footage of any released property) times $1.25 for tenant improvements and leasing commissions (the “Monthly Rollover Reserve Deposit”), subject to a cap of an amount equal to the Monthly Rollover Reserve Deposit times 12. Upon the cure of a Cash Sweep Period, such monthly deposits for tax, insurance, capital expenditures and tenant improvements and leasing commissions will be waived and the amounts in such reserve accounts will be released to the Burbank Office Portfolio Borrower.

Lockbox and Cash Management. A hard lockbox is in place with respect to the Burbank Office Portfolio Whole Loan. The Burbank Office Portfolio Whole Loan has springing cash management during the continuance of a Cash Sweep Period (as defined below). During the continuance of a Cash Sweep Period, funds in the lockbox account are required to be transferred to the cash management account up to two times per week and such funds in the cash management account are required to be applied on each monthly payment date to fund the required reserves deposits as described above under “Escrows and Reserves,” pay debt service on the Burbank Office Portfolio Whole Loan, pay operating expenses for the Burbank Office Portfolio and disburse the remainder to an account to be held by the lender as additional security for the Burbank Office Portfolio Whole Loan (or upon the cure of a Cash Sweep Period,provided that no event of default has occurred and is continuing, to the Burbank Office Portfolio Borrower).

A “Cash Sweep Period” will occur upon (i) an event of default, (ii) any bankruptcy action involving the Burbank Office Portfolio Borrower, the guarantor or any TRS Entity (as defined below), or (iii) the debt yield for the Burbank Office Portfolio Whole Loan falling below 7.0% for two consecutive calendar quarters. A Cash Sweep Period will continue until, in regard to clause (i) above, the cure of such event of default and acceptance of such cure by the lender, in regard to clause (ii) above, in the event of an involuntary bankruptcy action, upon the filing being discharged, stayed or dismissed within 90 days of such filing, or in regard to clause (iii) above, (a) the debt yield for the Burbank Office Portfolio Whole Loan is equal to or greater than 7.0% for two consecutive calendar quarters or (b) the Burbank Office Portfolio Borrower prepays the Burbank Office Portfolio Whole Loan in an amount sufficient to achieve a debt yield equal to or greater than 7.0%.

Additional Secured Indebtedness (not including trade debts). In addition to the Burbank Office Portfolio Mortgage Loan, the Burbank Office Portfolio Properties also secure seven additionalpari passusenior notes, which combined with the Burbank Office Portfolio Mortgage Loan comprise the Burbank Office Portfolio Senior Loan in the aggregate principal amount of $379,000,000, and two subordinate notes with an aggregate principal balance of $281,000,000 comprising the Burbank Office Portfolio Subordinate Companion Loans. The Burbank Office Portfolio Subordinate Companion Loans are coterminous with the Burbank Office Portfolio Senior Loan and accrue interest at 3.5410%. The Burbank Office Portfolio Mortgage Loan along with the other notes that comprise the Burbank Office Portfolio Senior Loan are eachpari passu in right of payment and the Burbank Office Portfolio Senior Loan is senior in right of payment to the Burbank Office Portfolio Subordinate Companion Loans. The holders of the Burbank Office Portfolio Mortgage Loan, the other notes that comprise the Burbank Office Portfolio Senior Loan and the Burbank Office Portfolio Subordinate Companion Loans have entered into a co-lender agreement which sets forth the allocation of collections on the Burbank Office Portfolio Whole Loan. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans” in the Preliminary Prospectus.

Mezzanine Loan and Preferred Equity.Not permitted.

Release of Property. The Burbank Office Portfolio Borrower may obtain the release of any Burbank Office Portfolio Property,providedthat, among other things, (i) no event of default has occurred and is continuing, (ii) the Burbank Office Portfolio Borrower pays the Release Amount (as defined below) along with any yield maintenance premium, (iii) the debt yield with respect to the remaining Burbank Office Portfolio Properties is no less than the greater of (a) the debt yield at origination of the Burbank Office Portfolio Whole Loan and (b) the debt yield immediately prior to the release,provided,however, that the debt yield is not required to be greater than 10.0%. In the event that such debt yield requirement is not satisfied and the release of such property is in connection with a sale of such property to a third party, the Burbank Office Portfolio Borrower will be permitted to obtain the release of such property upon the payment of an amount equal to the greater (i) of the Release Amount and (ii) the lesser of (a) lender’s allocation of 100% of the net sales proceeds for such property and (b) an amount necessary to, after giving effect to such release, satisfy the debt yield requirement set forth above, along with any yield maintenance premium required. For the purposes of calculating the debt yield relating to the release of one or more properties, the Burbank Office Portfolio Borrower may elect to deliver a letter of credit in the maximum aggregate amount of $15,000,000 as additional collateral for the Burbank Office Portfolio Whole Loan to be counted against the outstanding principal balance of the Burbank Office Portfolio Whole Loan.

The “Release Amount” is an amount equal to (i) for The Pointe Property, 110%, and (ii) for the Media Studios Property, 3800 Alameda Property and Central Park Property, 105%, of the Allocated Cut-off Date Balance of such property (identified in the “Portfolio Summary” chart above).

Release of Parcel. The Burbank Office Portfolio Borrower may obtain the release of any unimproved non-income producing land located at any Burbank Office Portfolio Property, for which no value was attributed to such unimproved non-income producing land in the applicable appraisal, without any requirements to pay any portion of any allocated loan amount, Release Amount, prepayment fees or yield maintenance premium,provided that certain terms and conditions as specified in the loan agreement are satisfied.

TRS Entities.The Central Park Property, The Pointe Property and two parcels of the Media Studios Property have taxable REIT subsidiary (“TRS”) structures in place with respect to certain café, fitness and transportation elements of the applicable parcels (individually, a “TRS Entity”, and collectively, the “TRS Entities”). Each TRS Entity is a special purpose, bankruptcy remote, Delaware limited liability company. The TRS Entities have mortgaged their respective interests and are non-borrower parties to the loan agreement and other loan documents with respect to all applicable representations, warranties and covenants. The TRS Entities are not, however, obligors under the notes.

Terrorism Insurance. The Burbank Office Portfolio Borrower is required to obtain insurance against acts of terrorism for loss resulting from perils and acts of terrorism in amounts and with terms and conditions applicable to commercial property, general liability, business income and umbrella liability insurance required pursuant to the Burbank Office Portfolio Whole Loan documents.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| New York, NY 10028 | Collateral Asset Summary – Loan No. 2 Yorkshire & Lexington Towers | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 22.5% 4.28x 12.0% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| New York, NY 10028 | Collateral Asset Summary – Loan No. 2 Yorkshire & Lexington Towers | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 22.5% 4.28x 12.0% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| New York, NY 10028 | Collateral Asset Summary – Loan No. 2 Yorkshire & Lexington Towers | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 22.5% 4.28x 12.0% |

| Mortgage Loan Information | Property Information | ||||||

| Mortgage Loan Seller: | UBS AG | Single Asset/Portfolio: | Portfolio | ||||

| Credit Assessment (Fitch/KBRA/Moody’s/S&P): | [ ] | Location: | New York, NY 10028 | ||||

| General Property Type: | Multifamily | ||||||

| Original Balance(1): | $40,000,000 | Detailed Property Type: | High Rise | ||||

| Cut-off Date Balance(1): | $40,000,000 | Title Vesting: | Fee | ||||

| % of Initial Pool Balance: | [ ]% | Year Built/Renovated: | Various/2014-2017 | ||||

| Loan Purpose: | Refinance | Size: | 827 Units | ||||

| Borrower Sponsors: | The Chetrit Group LLC; Stellar Management LLC | Cut-off Date Balance per Unit(1): | $241,838 | ||||

| Mortgage Rate: | 2.7400% | Maturity Date Balance per Unit(1): | $241,838 | ||||

| Note Date: | 10/3/2017 |

Property Manager: |

Jumeaux Management LLC (borrower-related) | ||||

| First Payment Date: | 11/6/2017 | ||||||

| Maturity Date: | 10/6/2022 | ||||||

| Original Term to Maturity: | 60 months | ||||||

| Original Amortization Term: | 0 months | ||||||

| IO Period: | 60 months | ||||||

| Seasoning: | 1 month | ||||||

| Prepayment Provisions: | LO (25); DEF (28); O (7) | Underwriting and Financial Information | |||||

| Lockbox/Cash Mgmt Status: | Soft/Springing | UW NOI(4): | $23,948,124 | ||||

| Additional Debt Type(2): | Pari Passu/Subordinate Debt/Mezzanine | UW NOI Debt Yield(1): | 12.0% | ||||

| Additional Debt Balance(2): | $160,000,000/$200,000,000/$150,000,000 | UW NOI Debt Yield at Maturity(1): | 12.0% | ||||

| Future Debt Permitted (Type): | No (N/A) | UW NCF DSCR(1): | 4.28x | ||||

| Reserves(3) | Most Recent NOI(4): | $12,322,089 (6/30/2017 TTM) | |||||

| Type | Initial | Monthly | Cap | 2nd Most Recent NOI: | $9,556,571 (12/31/2016) | ||

| RE Tax: | $2,724,408 | $681,102 | N/A | 3rd Most Recent NOI: | $10,053,207 (12/31/2015) | ||

| Insurance: | $89,787 | $29,929 | N/A | Most Recent Occupancy: | 92.0% (9/24/2017) | ||

| Replacements: | $0 | $11,369 | (3) | 2nd Most Recent Occupancy: | 78.7% (12/31/2016) | ||

| TI/LC: | $0 | $12,640 | N/A | 3rd Most Recent Occupancy: | 67.0% (12/31/2015) | ||

| Debt Service Shortfall: | $2,000,000 | $0 | N/A | Appraised Value (as of)(5): | $890,000,000 (8/15/2017) | ||

| Renovation/Tenant Buyout: | $3,500,000 | $0 | N/A | Cut-off Date LTV Ratio(1)(5): | 22.5% | ||

| Holdback Reserve Funds: | $4,102,064 | $0 | N/A | Maturity Date LTV Ratio(1)(5): | 22.5% | ||

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Loan Amount(1): | $400,000,000 | 72.7% | Loan Payoff: | $394,073,271 | 71.6% | |

| Mezzanine Loans(1): | $150,000,000 | 27.3% | Reserves: | $12,416,259 | 2.3% | |

| Closing Costs: | $19,423,650 | 3.5% | ||||

| Return of Equity: | $124,086,820 | 22.6% | ||||

| Total Sources: | $550,000,000 | 100.0% | Total Uses: | $550,000,000 | 100.0% | |

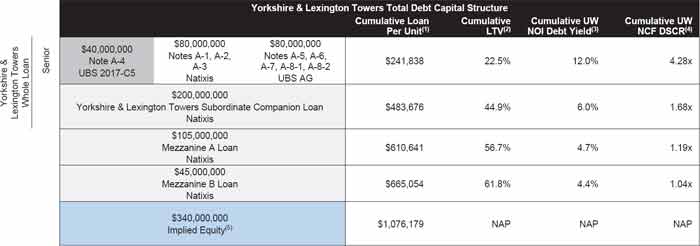

| (1) | The Yorkshire & Lexington Towers Mortgage Loan (as defined below) is part of the Yorkshire & Lexington Towers Whole Loan (as defined below), which is comprised of ninepari passupromissory notes with an aggregate original principal balance of $200,000,000 and one subordinate promissory note with an original principal balance of $200,000,000. The Yorkshire & Lexington Towers Whole Loan is accompanied by the Yorkshire & Lexington Towers Mezzanine Loans (as defined below) with an aggregate original principal balance of $150,000,000. The Cut-off Date Balance per Unit, Maturity Date Balance per Unit, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV Ratio presented above are based on the aggregate principal balance of the promissory notes comprising the Yorkshire & Lexington Towers Senior Loan (as defined below), without regard to the Yorkshire & Lexington Towers Subordinate Companion Loan (as defined below). The Cut-off Date Balance per Unit, Maturity Date Balance per Unit, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV based on the Yorkshire & Lexington Towers Whole Loan is $483,676, $483,676, 6.0%, 6.0%, 1.68x, 44.9% and 44.9%, respectively. The Cut-off Date Balance per Unit, Maturity Date Balance per Unit, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV based on the Yorkshire & Lexington Towers Whole Loan and the Yorkshire & Lexington Towers Mezzanine Loans are $665,054, $665,054, 4.4%, 4.4%, 1.04x, 61.8% and 61.8%, respectively. |

| (2) | See “The Mortgage Loan”, “Additional Secured Indebtedness (not including trade debts)”and “Mezzanine Loan and Preferred Equity” below for further discussion of additional debt. |

| (3) | See “Escrows and Reserves” below for further discussion of reserve requirements. |

| (4) | The increase in NOI is driven by a combination of higher occupancy levels and higher rental rates due to the conversion of rent stabilized units into free market units, unit renovations, and improved property amenities. UW NOI is underwritten to the occupancy as of the September 24, 2017 rent roll of 92.0%, compared to occupancy of 83.6% as of June 30, 2017. See “Cash Flow Analysis”table below for further discussion of the Yorkshire & Lexington Towers Properties’ (as defined below) operating performance. See “Risk Factors—Risks Relating to the Mortgage Loans—Multifamily Properties Have Special Risks” in the Preliminary Prospectus. |

| (5) | The Cut-off Date LTV Ratio and Maturity Date LTV Ratio numbers presented above are based on the aggregate “as-is” appraised value of the Yorkshire & Lexington Towers Properties of $890.0 million, as of August 15, 2017. The appraisal concluded an aggregate “as stabilized” appraised value, which assumes that the borrower sponsors’ investments related to tenant buyout costs, recapture and renovation of rent regulated units, leasing costs, and in-unit renovations of market rate and rent regulated units have been completed, of $1.03 billion as of September 1, 2020. Based on the aggregate “as stabilized” appraised value and the Yorkshire & Lexington Towers Senior Loan, the Cut-off Date LTV Ratio and Maturity Date LTV Ratio are 19.4% and 19.4%, respectively. Based on the aggregate “as stabilized” appraised value and the Yorkshire & Lexington Towers Whole Loan, the Cut-off Date LTV Ratio and Maturity Date LTV Ratio are 38.8% and 38.8%, respectively. Based on the aggregate “as stabilized” appraised value and the Yorkshire & Lexington Towers Whole Loan and Yorkshire & Lexington Towers Mezzanine Loans, the Cut-off Date LTV Ratio and Maturity Date LTV Ratio are 53.4% and 53.4%, respectively. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| New York, NY 10028 | Collateral Asset Summary – Loan No. 2 Yorkshire & Lexington Towers | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 22.5% 4.28x 12.0% |

The Mortgage Loan. The second largest mortgage loan (the “Yorkshire & Lexington Towers Mortgage Loan”) is part of a whole loan (the “Yorkshire & Lexington Towers Whole Loan”) evidenced by ninepari passu promissory notes with an aggregate original principal balance of $200,000,000 (collectively, the “Yorkshire & Lexington Towers Senior Loan”) and by one subordinate companion note with an original principal balance of $200,000,000 (the “Yorkshire & Lexington Towers Subordinate Companion Loan”). The Yorkshire & Lexington Towers Whole Loan is secured by a first priority mortgage encumbering the borrowers’ fee interest in a two-property, 827-unit high rise multifamily portfolio located at 305 East 86th Street (the “Yorkshire Towers Property”) and 160 East 88th Street (the “Lexington Towers Property”) in New York, New York (collectively, the “Yorkshire & Lexington Towers Properties”). The Yorkshire & Lexington Towers Whole Loan was co-originated by UBS AG, by and through its branch office of 1285 Avenue of the Americas, New York, New York (“UBS AG”) and Natixis Real Estate Capital LLC (“Natixis”). Promissory Note A-4, with an original principal balance of $40,000,000, represents the Yorkshire & Lexington Towers Mortgage Loan and will be included in the UBS 2017-C5 Trust. Promissory Notes A-1, A-2 and A-3, with an aggregate original principal balance of $80,000,000, are currently held by Natixis, or an affiliate thereof, and are expected to be contributed to one or more future securitization transactions or may be otherwise transferred at any time. Promissory Notes A-5, A-6, A-7, A-8-1 and A-8-2, with an aggregate original principal balance of $80,000,000, are currently held by UBS AG, or an affiliate thereof, and are expected to be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The Yorkshire & Lexington Towers Subordinate Companion Loan is held by Natixis, but may be otherwise transferred at any time. The lenders provide no assurances that any of the non-securitized notes will not be split further. The Yorkshire & Lexington Towers Whole Loan will initially be serviced pursuant to the pooling and servicing agreement for the UBS 2017-C5 Trust, and from and after the securitization of Promissory Note A-1, will be serviced pursuant to the pooling and servicing agreement of such securitization trust. See “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus.

| Yorkshire & Lexington Towers Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Anticipated Note Holder | Controlling Piece |

| Note A-1 | $40,000,000 | $40,000,000 | Natixis | No |

| Note A-2 | $20,000,000 | $20,000,000 | Natixis | No |

| Note A-3 | $20,000,000 | $20,000,000 | Natixis | No |

| Note A-4 | $40,000,000 | $40,000,000 | UBS 2017-C5 | No |

| Note A-5 | $40,000,000 | $40,000,000 | UBS AG | No |

| Note A-6 | $20,000,000 | $20,000,000 | UBS AG | No |

| Note A-7 | $10,000,000 | $10,000,000 | UBS AG | No |

| Note A-8-1 | $5,000,000 | $5,000,000 | UBS AG | No |

| Note A-8-2 | $5,000,000 | $5,000,000 | UBS AG | No |

| Yorkshire & Lexington Towers Subordinate Companion Loan | $200,000,000 | $200,000,000 | Natixis | Yes |

| Total | $400,000,000 | $400,000,000 | ||

The proceeds of the Yorkshire & Lexington Towers Whole Loan, together with two mezzanine loans with an aggregate original principal balance of $150,000,000 (collectively, the “Yorkshire & Lexington Towers Mezzanine Loans”), were used to refinance the Yorkshire & Lexington Towers Properties, fund reserves, pay closing costs, and return equity to the borrower sponsors.

| (1) | Cumulative Basis Per Unit is calculated based on 827 units. |

| (2) | Based on the aggregate “as-is” appraised value of $890.0 million ($1,076,179 per unit), as of August 15, 2017. |

| (3) | Based on the UW NOI of $23,948,124. |

| (4) | Based on UW NCF of $23,764,985 and the coupon of 2.74000% on the Yorkshire & Lexington Towers Senior Loan, 4.25000% on the Yorkshire & Lexington Towers Subordinate Companion Loan, 5.45215% on the Yorkshire & Lexington Towers Mezzanine A Loan and 6.50000% on the Yorkshire & Lexington Towers Mezzanine B Loan. |

| (5) | Implied Equity is based on the “as-is” appraised value of $890.0 million, less total debt of $550.0 million. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| New York, NY 10028 | Collateral Asset Summary – Loan No. 2 Yorkshire & Lexington Towers | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | $40,000,000 22.5% 4.28x 12.0% |

The Borrowers and the Borrower Sponsors. The borrowers are CF E 88 LLC, SM E 88 LLC, CF E 86 LLC, SM E 86 LLC and LSG E 86 LLC (collectively, the “Yorkshire & Lexington Towers Borrower”), five tenants-in-common, each a single-purpose Delaware limited liability company structured to be bankruptcy remote with two independent directors. The nonrecourse carve-out guarantors of the Yorkshire & Lexington Towers Whole Loan are Jacob Chetrit and Laurence Gluck (collectively, the “Yorkshire & Lexington Towers Guarantors”). Jacob Chetrit has been involved in a prior deed in lieu of foreclosure and Laurence Gluck is currently subject to litigation, as described under “Description of the Mortgage Pool—Default History, Bankruptcy Issues and Other Proceedings” and “Description of the Mortgage Pool—Litigation and Other Considerations” in the Preliminary Prospectus, respectively.