Table of Contents

Filed Pursuant to Rule 424(b)(4)

Registration No. 333-223444

PROSPECTUS

OP Bancorp

2,000,000 Shares

Common Stock

This is the initial public offering of OP Bancorp. We are offering 2,000,000 shares of our common stock.

The initial public offering price of our common stock is $ 11.00 per share.

We have received approval to list our common stock on the Nasdaq Global Market under the symbol “OPBK.”

Our common stock was previously quoted on the OTC Market Group’s OTCQB Market under the symbol “OPBK”, and the last reported closing sale price for our common stock as reported on the OTCQB Market on March 26, 2018 was $11.90 per share.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 13.

We are an “emerging growth company” under the federal securities laws and will be subject to reduced public company reporting requirements.

| Per Share | Total | |||||||

Public offering price | $ | 11.0000 | $ | 22,000,000 | ||||

Underwriting discounts (1) | $ | 0.7535 | $ | 1,507,000 | ||||

Proceeds to us, before expenses | $ | 10.2465 | $ | 20,493,000 | ||||

| (1) | Represents a weighted average. See “Underwriting” for information regarding the calculation of the weighted average and additional information regarding underwriting compensation. |

The underwriters have an option to purchase up to an additional 300,000 shares from us at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Shares of our common stock are not savings accounts or deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

The shares of common stock will be ready for delivery on or about March 29, 2018.

Book-Running Manager

Keefe, Bruyette & Woods

A Stifel Company

Co-Manager

D.A. Davidson & Co.

The date of this prospectus is March 27, 2018.

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OPERATING INFORMATION | 11 | |||

| 13 | ||||

| 43 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

SELECTED HISTORICAL CONSOLIDATED FINANCIAL AND OPERATING INFORMATION | 49 | |||

GAAP RECONCILIATION AND MANAGEMENT EXPLANATION OFNON-GAAP FINANCIAL MEASURES | 51 | |||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 52 | |||

| 79 | ||||

| 97 | ||||

| 111 | ||||

| 121 | ||||

| 133 | ||||

| 135 | ||||

| 137 | ||||

| 141 | ||||

MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS FORNON-U.S. HOLDERS | 143 | |||

| 147 | ||||

| 152 | ||||

| 152 | ||||

| 152 | ||||

| F-1 | ||||

About this Prospectus

You should rely only on the information contained in this prospectus or in any free writing prospectus that we authorize to be delivered to you. We and the underwriters have not authorized anyone to provide you with different or additional information. We and the underwriters are not making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Unless we state otherwise or the context otherwise requires, references in this prospectus to “we”, “our”, “us,” “ourselves,” “the company” and “the Company” refer to OP Bancorp, a California corporation, and its consolidated wholly-owned subsidiary, Open Bank, a California corporation (“Open Bank” or “the Bank”), for all periods following the formation of OP Bancorp as a bank holding company under the Bank Holding Company Act of 1956, as amended, and the completion of the transactions under which Open Bank became a wholly-owned subsidiary of OP Bancorp. For all periods prior to the completion of such transactions, these terms refer to Open Bank, a California corporation.

i

Table of Contents

Market and Industry Data

Within this prospectus, we reference certain market, industry and demographic data and other statistical information. We have obtained this data and information from various independent, third party industry sources and publications. Nothing in the data or information used or derived from third party sources should be construed as advice. Some data and other information are also based on our good faith estimates, which are derived from our review of internal surveys and independent sources. We believe that these external sources and estimates are reliable, but have not independently verified them. Statements as to our market position are based on market data currently available to us. Although we are not aware of any misstatements regarding the economic, employment, industry and other market data presented herein, these estimates involve inherent risks and uncertainties and are based on assumptions that are subject to change.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

| • | we may present as few as two years of audited financial statements and two years of related management discussion and analysis of financial condition and results of operations; |

| • | we are exempt from the requirement to obtain an attestation and report from our auditors on management’s assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002; |

| • | we are permitted to provide less extensive disclosure about our executive compensation arrangements; and |

| • | we are not required to give our shareholdersnon-binding advisory votes on executive compensation or golden parachute arrangements. |

In this prospectus we have elected to take advantage of the reduced disclosure requirements relating to executive compensation, and in the future we may take advantage of any or all of these exemptions for so long as we remain an emerging growth company. We will remain an emerging growth company until the earliest of (i) the end of the fiscal year during which we have total annual gross revenues of $1.07 billion or more, (ii) the end of the fiscal year following the fifth anniversary of the completion of this offering, (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion innon-convertible debt and (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended.

In addition to the relief described above, the JOBS Act permits us an extended transition period for complying with new or revised accounting standards affecting public companies. We have elected not to take advantage of this extended transition period, which means that the financial statements included in this prospectus, as well as any financial statements that we file in the future, will be subject to all new or revised accounting standards generally applicable to public companies.

ii

Table of Contents

This summary highlights selected information contained in this prospectus. It does not contain all the information that you should consider before deciding to invest in our common stock. You should read the entire prospectus carefully, including the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections, and the historical financial statements and the accompanying notes included in this prospectus.

Our Company

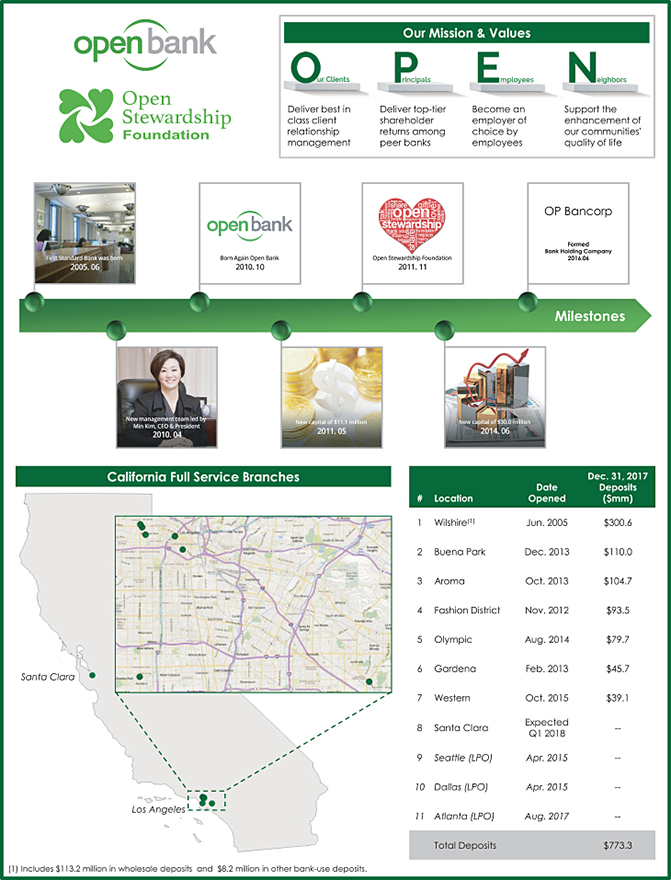

We are a bank holding company headquartered in Los Angeles, California. Our commercial banking activities are operated through Open Bank, our banking subsidiary. We offer commercial banking services to small andmedium-sized businesses, their owners and retail customers with a focus on theKorean-American community. Having grown our branch and loan production office network over the past seven years, we now operate through seven full service branches located in the greater metropolitan area of Los Angeles, California, and Orange County, California, and three loan production offices in theKorean-American communities in Atlanta, Georgia, Dallas, Texas, and Seattle, Washington. In addition, we intend to open a full service branch in Santa Clara, California in the first quarter of 2018. As of December 31, 2017, we had consolidated total assets of $901.0 million, total deposits of $773.3 million, total loans outstanding (net of allowance for loan losses) of $738.9 million, and total shareholders’ equity of $91.5 million.

We provide our customers with a high degree of service, convenience and the products they need to achieve their financial objectives, by offering a customer-oriented product mix, competitive pricing, and convenient locations. Our lending activities are diversified and include commercial real estate (“CRE”), commercial and industrial, Small Business Administration (“SBA”) guaranteed, home mortgage, and consumer loans. We generally lend in markets where we have a physical presence through our branch and loan production offices. We attract retail deposits through our branch network which offers a wide range of deposit products for business and consumer banking customers. We offer a multitude of other products and services to our customers to complement our lending and deposit business.

We have a strong, values-based corporate culture rooted in personal community-based relationship banking that permeates throughout our entire organization. We strive to provide quality customer service that exceeds our customers’ expectations. We also heavily invest in ourKorean-American communities through our annual contributions to the Open Stewardship Foundation. We believe that customers value a banking partner knowledgeable about their business needs with a willingness and commitment to reinvest back into the community. We convey to our customers that banking with us indirectly provides them an opportunity to contribute to the community. We believe our strategic approach creates opportunities for expanding our banking relationships with new and existing customers who value personalized attention, local decision making and view us as an alternative to the large consolidated Korean-American financial institutions.

We established the Open Stewardship Foundation, or the Foundation, in 2011 to actively support civic organizations, schools and other eligible charitablenon-profit organizations that provide public benefit services in the communities we serve. The Foundation operates through a board of directors that consists of individuals who are members of our board of directors and executive management team, including our President and Chief Executive Officer and our Chairman of the Board. The Foundation board of directors reviews and approves award grants. We have committed to contribute annually 10% of our consolidated net income after taxes to the Foundation. Since inception, we have donated over $2.9 million to the Foundation, aiding over 120 localnon-profits.

Our experienced executive management team has been in place since 2010 and averages more than 30 years’ experience in the banking industry. Min Kim, our President and Chief Executive Officer, has over 35 years of

1

Table of Contents

banking experience in the Korean-American banking community. Ms. Kim previously served as Chief Executive Officer of Nara Bancorp and Nara Bank (now part of Hope Bancorp and Bank of Hope). After joining us, Ms. Kim implemented her strategic vision to take advantage of the opportunities to build a Korean-American community-based bank focused on personal relationships as an alternative to the larger Korean-American financial institutions that she believed through consolidation provided an opportunity for Open Bank to better serve small tomedium-sized businesses in the Korean-American community.

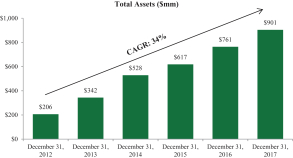

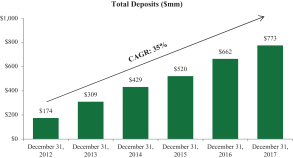

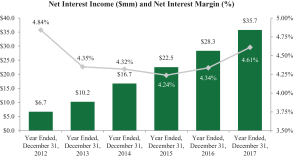

Since 2012 we have achieved significant organic growth in many of our key financial performance metrics. From December 31, 2012 through December 31, 2017, total assets have grown at a compounded annual growth rate (“CAGR”) of 34% from $206 million to $901 million, total gross loans (including loansheld-for-sale) at a CAGR of 36% from $162 million to $764 million, and total deposits at a CAGR of 35% from $174 million to $773 million. The charts below illustrate the growth in the dollar balances of our total assets, loans and deposits.

|  |

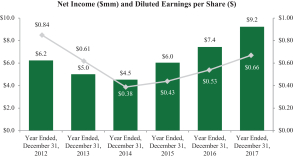

Over this same period, our profitability also significantly increased. The charts below illustrate our net income and diluted earnings per share (“EPS”) and net interest income and net interest margin (“NIM”) during this period. We believe our earnings growth during this period was primarily attributable to our organic growth initiatives, which improved our loan portfolio, our deposit mix and our efficiency ratio.

|  |

2

Table of Contents

We plan to continue to leverage our experienced management team, our personal relationship community banking focus in the attractiveKorean-American communities in which we serve, and our diversified lending approach to drive future organic growth. While other institutions frequently enter new geographies through acquisitions, we have grown our geographic footprint through de novo branches while remaining true to our business model. We intend to continue our organic growth while further diversifying our geographical concentration with the anticipated expansion in Santa Clara, California, in the first quarter of 2018, our first branch in northern California. We also are targeting markets where we have loan production offices for future expansion and development of de novo branches. Supplementing deposit products to our borrowers in those markets is expected to provide the profitability to support our investment in full service branches. Although our growth has historically been organic, we are amenable to considering opportunistic strategic acquisitions to enhance our long-term growth strategy.

Our History

We began operations in 2005 as a California chartered banking association under the name First Standard Bank. In 2010, we rebranded the bank as “Open Bank.” In 2016, we incorporated OP Bancorp as a bank holding company under the Bank Holding Company Act of 1956, as amended (“BHCA”), and Open Bank became its sole subsidiary. OP Bancorp is regulated by the Board of Governors of the Federal Reserve (“Federal Reserve”). Open Bank is regulated by the California Department of Business Oversight (“DBO”), as its primary state regulator, and the Federal Deposit Insurance Corporation (“FDIC”), as its primary federal regulator.

From our founding date through the2008-2009 financial crisis and prior to our new management team joining us in 2010, we had experienced lagging profitability, deficient credit quality and below “well capitalized” capital levels. Our management team worked through our credit quality issues bringing our nonperforming assets (“NPA”) as a percentage of total gross loans and other real estate owned (“OREO”) ratio down from its peak of 9.60% at September 30, 2009 to 0.14% as of December 31, 2017. Profitability has increased year over year for the past five years as described above. We raised $11.1 million of capital ($10.9 million net of expenses) in 2010 and 2011 from directors and accredited investors, and an additional $30.0 million ($28.3 million net of expenses) in 2014 from institutional and accredited investors through the issuance of common stock in private placement transactions. We have been “well capitalized” for bank regulatory purposes since 2010.

Our Strategies

Our vision is to be the leading Korean-American community-based commercial bank in the Korean-American communities we serve, to meet the financial needs of underserved small andmedium-sized business and individuals, and to give back to these communities.

Our more specific strategic initiatives are discussed below.

| • | Leverage our Franchise in theKorean-American Communities We Serve. The Korean-American banking landscape has seen increased consolidation of the larger Korean-American financial institutions that do business in our market areas. We believe that the customers at these larger institutions will look for an alternative banking experience that is tailored towards their specific financial objectives and we strive to be the most prominent alternative to the largerKorean-American financial institutions. We differentiate ourselves from our competitors by developing meaningful and personal relationships with our customers, combined with a superior level of service to make Open Bank an attractive choice for small tomedium-sized businesses, professionals and individuals. Our strong financial performance and growth derives in part for the desire by small andmedium-sized businesses and individuals for quality personal relationship banking, local and responsive decision making and flexible and competitive pricing of deposit |

3

Table of Contents

and loan products. Our commitment to the Open Stewardship Foundation raises our profile and reinforces our position as a community partner committed to the success of the communities we serve. We convey to our customers that banking with us provides them with an indirect opportunity to contribute to the community. In addition, we have invested in developing a distinct corporate culture guided by a core set of values. These values underlie everything we do, including the way we engage with customers, collaborate with colleagues, do business and manage our resources. We believe our commitment to our communities, culture and quality of our people have been catalysts of our success and will continue to propel our future. |

| • | Focus on Organic Growth. We intend to grow organically and believe the markets in which we operate currently provide meaningful opportunities to expand our commercial customer base and increase our market share. We believe that our overall capabilities, culture and opportunities for career growth will allow us to continue to attract talented and entrepreneurial commercial and retail bankers from larger Korean-American financial institutions. Our bankers have further capacity to penetrate the markets and communities they serve and drive loan and deposit growth as our brand awareness continues to grow. We also seek to offer our various banking products, including our deposit products, residential loan products and cash management services to our commercial loan and SBA borrowers, which we believe provides a basis for expanding our banking relationships. We believe we have built a scalable platform that will support our continual organic growth. Although we are currently focused on organic growth, we will also look for opportunistic strategic acquisitions that complement our commercial banking and the strong personal community-based relationship orientation of our franchise. |

| • | Increase our Share of Lower-Cost Deposits. We believe the quality of our deposit base and access to stable funding are key components of our success. We have a strong deposit base characterized by a high level of core deposits, high proportion ofnon-interest bearing accounts and relatively low funding costs. As of December 31, 2017, deposits accounted for 95.5% of our total liabilities. Core deposits, which we define as all deposits excluding time deposits exceeding $250,000, constituted 85.9% of our total deposits. We increased ournon-interest bearing deposits as a percentage of total deposits from 31.6% as of December 31, 2012 to 37.4% as of December 31, 2017. Our cost of total deposits was 0.62% for the year ended December 31, 2017. We employ conventional marketing initiatives and advertising and leverage our community commitment activities to generate new accounts. Deposit rates and terms are based primarily on current operating strategies and market interest rates, liquidity requirements and our deposit growth goals. Our bankers offer a full suite of products and services to our loan customers, with a specific focus on acquiring and maintaining core deposits as we depend on them to fund the majority of our loans. Small businesses are a significant source of low cost deposits and represent opportunities for future growth. We believe that small business owners value our ability to provide convenience and access to local, responsive decision makers. Commercial accounts also generally have higher deposit balances and transaction volumes than individual deposit accounts. As of December 31, 2017, commercial deposits represented 45% of our total deposits. We take specific initiatives to establish banking relationships with our SBA borrowers with the goal of securing their future banking business as they continue to grow their businesses. We typically require, depending on the circumstances and the type of relationship, our borrowers to maintain deposit accounts as a condition of granting loans. We believe that our convenient branch network, personal relationship-driven culture, diversified product offering, and flexible pricing allow us to accelerate deposit growth. We plan to continue investing in our franchise brand, our community reputation, employees, and product capabilities to further improve customer loyalty with a view toward growing our high quality deposit portfolio. |

| • | Branch Expansion. We intend to continue our strategy of opening and developing de novo branches particularly into Korean-American populated areas. We have pursued this growth strategy since the beginning of 2012 when we only had one branch location. As of December 31, 2017, we had seven branches in the greater Los Angeles and Orange County areas and anticipate opening an eighth branch in the first quarter of 2018 in Santa Clara, California. We will review future potential target areas for de novo expansion based on our ability to attract experienced bankers within such targeted regions. In addition, we currently operate three loan production offices located in Atlanta, Georgia, Dallas, Texas and Seattle, |

4

Table of Contents

Washington. We will continue to look for additional markets to expand our loan production capabilities and, if we believe there are opportunities to develop deposit business in these markets, we may expand one or more loan production offices into de novo branches. |

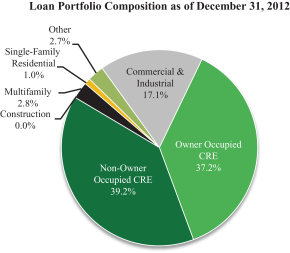

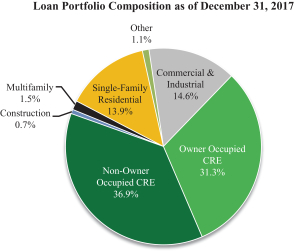

| • | Expand and Diversify our Commercial Lending. We are committed to continuing to expand and continuing to grow our commercial loan portfolios while maintaining what we believe are conservative underwriting standards. We focus our commercial lending to small andmedium-sized businesses in our market areas. Since 2012, our commercial loan portfolio has grown from $148.2 million at December 31, 2012 to $640.0 million at December 31, 2017, representing 85.6% of our total loans as of December 31, 2017. We expect to expand our commercial lending business in our expanding branch network, where we can continue to leverage our ability to develop personal community-based relationships and leverage our quality service model into new opportunities. We believe we can leverage our personalized customer service, extensive knowledge of our local markets and high visibility community activities to attract and retain customers seeking alternatives to the larger Korean-American financial institutions. We are also focused on diversifying our loan portfolio. As of December 31, 2017, total CRE loans had declined to 70.4% of our loan portfolio from 79.2% at December 31, 2012. |

|  |

| • | Preserve Our Asset Quality Through Disciplined Lending Practices. Our approach to credit management uses well-defined policies and procedures, disciplined underwriting criteria and ongoing risk management. This approach has allowed us to maintain loan growth with a diversified portfolio of high quality assets. We believe our credit culture supports accountable bankers, who maintain an ability to expand our customer base as well as make sound decisions for our company. As of December 31, 2017, our ratio of nonperforming assets to total assets was 0.12% and our ratio of nonperforming loans to total loans was 0.14%. However, as a result of the organic growth of our loan portfolio over the past five years, a large portion of our loans and lending relationships are of relatively recent origin and the current level of delinquencies and defaults may not represent the level that may prevail as the portfolio becomes more seasoned. |

| • | Leverage Public Company Status. In addition to raising capital to support our growth as further discussed under “Use of Proceeds,” we believe becoming a public reporting company, while increasing our operating costs, will provide us with additional options and better pricing to manage our cost of capital that were previously unavailable to us when our shares were quoted on the OTCQB Market. While we have not historically engaged in any merger and acquisition activity, the ability to issue publicly-traded stock as consideration may enable us to opportunistically approach potential transactions. In addition, we believe the additional liquidity provided by being listed on the Nasdaq Global Market and being a public reporting company will enhance the equity component of our compensation programs, which will enable us to better incent and retain key employees in the competitive markets in which we operate. |

5

Table of Contents

Our Competitive Strengths

Our management team has identified the following competitive strengths that we believe will allow us to continue to achieve our principal objective of increasing shareholder value and generating consistent earnings growth through the organic and strategic expansion of our commercial banking franchise:

| • | Experienced Leadership and Management Team. Our experienced executive management team and senior leaders have exhibited the ability to strengthen shareholder value by consistently growing profitably. Our Chief Executive Officer was previously the chief executive officer of a multi-billion dollar bank holding company and bank focused on the Korean-American community. The members of our executive management team have, on average, more than 30 years’ experience working for large, billion-dollar-plus financial institutions in our markets during various economic cycles. They have been with Open Bank for an average of seven years, and substantially all have known and worked with our Chief Executive Officer prior to joining Open Bank. Our executive management team has instilled a transparent and entrepreneurial culture that rewards leadership, innovation, and problem solving. Our annual compensation plan is designed to provide employees with the incentive to perform at a consistently high level and provide financial rewards for performance that meets or exceeds defined financial, strategic-related, risk-mitigating targets and individual expectations on a consistent basis. |

| • | Personal Relationship-Based Customer Service. We strive to differentiate ourselves from our competition by providing the best “relationship-based” services to small- andmedium-sized businesses and their owners and residents in our Korean-American communities. We accomplish this by striving to provide our customers with a superior level of personal and responsive service delivered by experienced bankers in a manner that timely meets our customers’ financial objectives. Our management team’s significant banking and lending experience in our markets has provided us with an understanding of the commercial banking needs of our customers, which allows us to tailor our products and services to meet our customers’ financial objectives. We believe we have also been successful in attracting customers from larger Korean-American financial institutions because of our flexible and responsive approach in providing banking solutions while maintaining disciplined underwriting standards. To enhance our relationships with our customers and to identify and meet their particular needs, each customer is assigned a relationship officer (including our SBA borrowers). Approximately 56% of our borrowers also have a deposit relationship with us, providing us with visibility into their liquidity profile and contributing to our ability to manage our asset quality. We instill in our employees the importance of delivering outstanding customer service and seeking opportunities to strengthen relationships with both customers and the communities we serve. |

| • | Strong Community Relationships. A primary mission of Open Bank is to meet the financial services needs of underserved customers in our markets, and we strive to distinguish ourselves by giving back to these communities. In October 2011, we established the Open Stewardship Foundation to actively support local civic organizations, schools, and public services. We have committed to fund the Foundation in an amount equal to 10% of our annual consolidated net income after taxes. This commitment is in the Bank’s bylaws and our annual operating budget each year. We believe that our community commitment distinguishes us from our competitors and enhances and expands business relationships within the Korean-American communities we serve. Since inception, we have donated over $2.9 million to the Foundation, aiding over 120 localnon-profits. Our President and Chief Executive Officer and our Chairman of the Board are among those who serve on the Foundation’s board of directors, enabling the Foundation to focus its awards in a manner that best comports with our overall community and business goals. Additionally, our management team has strong ties and relationships within the Korean-American communities where we operate. The Foundation and our employees and board of directors are involved in community activities that enhance our relationships with a variety of industry leadership groups, including the Korean-American Federation of Los Angeles, the Korean-American Chamber of Commerce of Los Angeles, the Korean-American Manufacturers Association, the Korean-American CPA Society of Southern California, California KAGRO |

6

Table of Contents

Association, and the Korean Real Estate Brokers Association of Southern California. Affiliation with these local organizations provide our management team with knowledge of local markets and industries, as well as market developments that may impact the evolving business environment in which we operate. |

| • | Strong Credit Quality. We have implemented policies and procedures for credit underwriting and administration which have enabled us to maintain strong asset quality while at the same time growing our banking business. As of December 31, 2017, our NPAs as a percentage of total gross loans and OREO was 0.14%. |

| • | Strong Risk Management Practices. We place significant emphasis on risk management as an integral component of our organizational culture without sacrificing growth. We believe our comprehensive risk management system is designed to ensure that we have sound policies, procedures, and practices for the management of key risks under our risk framework (which includes market, operational, liquidity, interest rate sensitivity, credit, regulatory, legal and reputational risk) and that any exceptions to written policy are reported by senior management to our board of directors or audit committee. Our risk management practices are overseen by the chairman of our audit committee and the chairman of Open Bank’s risk and compliance committees, who have more than 20 years of combined banking experience, and our chief risk officer, who has more than 35 years of banking experience. We believe that our enterprise risk management philosophy has been important in gaining and maintaining the confidence of our various constituencies and growing our business and footprint within our markets. We also believe our strong risk management practices are manifested in our asset quality metrics. |

| • | Efficient and Scalable Platform with Capacity to Support Our Growth. Our management team has built an efficient and scalable corporate infrastructure within our commercial banking franchise, including the areas of banking processes, technology, data processing, underwriting and risk management, which we believe will support our continued growth. For example, during 2016 we introduced enhanced enterprise risk software and cybersecurity monitoring software to strengthen our operations and risk culture. While expanding our infrastructure, several departmental functions have been outsourced to gain the experience of outside professionals while at the same time achieving more favorable economics and cost-effective solutions. Such outsourced areas include the internal audit function, investment securities management, select loan review, interest rate risk management and stress testing. This outsourcing strategy is designed to control costs while adding enhanced controls and/or service levels. We believe that our scalable infrastructure will continue to allow us to efficiently and effectively manage our anticipated growth. |

Market Area

We are headquartered in Los Angeles, California. We currently have one branch in the financial district of downtown Los Angeles and, directly adjacent to downtown Los Angeles, we have one branch in the fashion district and three branches in Koreatown. In addition, we operate a branch in Gardena, California and a branch in Buena Park, in Orange County, California. These branches are located in the Los Angeles-Long Beach-Anaheim, California Metropolitan Statistical Area, or MSA. With over 13 million residents, it is the largest MSA in California, the second largest MSA in the United States, and one of the most significant business markets in the world. It is estimated that the greater Los Angeles area has a gross domestic product of approximately $1 trillion, which would rank it as the 16th largest economy in the world. The economic base of the area is heavily dependent on small- andmedium-sized businesses, providing us with a market rich in potential customers. According to the U.S. Census Bureau, Asian-Americans accounted for 15.1% of the over 10.1 million residents in Los Angeles County as of July 1, 2016.

We anticipate opening a branch in Santa Clara, California in the first quarter of 2018.

We also operate loan production offices in Atlanta, Georgia, Dallas, Texas and Seattle, Washington to support our SBA lending efforts.

7

Table of Contents

Our Competition

In our primary markets in Southern California, we view the Korean-American direct banking market, including Open Bank, as comprised of nine banks divided into three segments: large publicly-traded banks (two banks), locally-owned banks (five banks), and banks that are subsidiaries of Korean banks (two banks). In addition to Open Bank, all of the locally-owned banks are based in California. As of December 31, 2017, we are the seventh-largest bank among this group of nine banks based on total assets.

The table below provides more details on the Korean-American banking landscape as of December 31, 2017.

(Dollars in millions) Institution Name | Headquarters | U.S. Offices | Total Assets | Total Loans | Total Deposits | Total Equity(1) | ||||||||||||||||

Large Publicly-Traded Korean-American Banks | ||||||||||||||||||||||

Hope Bancorp, Inc. | Los Angeles, CA | 63 | 14,207 | 11,132 | 10,847 | 1,928 | ||||||||||||||||

Hanmi Financial Corporation | Los Angeles, CA | 40 | 5,210 | 4,311 | 4,349 | 562 | ||||||||||||||||

Locally-Owned Korean-American Banks | ||||||||||||||||||||||

Pacific City Financial Corporation | Los Angeles, CA | 13 | 1,442 | 1,195 | 1,251 | 142 | ||||||||||||||||

MetroCity Bankshares, Inc. | Doraville, GA | 15 | 1,292 | 1,103 | 1,027 | 132 | ||||||||||||||||

CBB Bancorp, Inc. | Los Angeles, CA | 8 | 1,079 | 816 | 896 | 115 | ||||||||||||||||

OP Bancorp(2) | Los Angeles, CA | 8 | 901 | 764 | 773 | 91 | ||||||||||||||||

First IC Corporation | Doraville, GA | 7 | 404 | 323 | 337 | 63 | ||||||||||||||||

Noah Bank | Elkins Park, PA | 5 | 381 | 327 | 326 | 43 | ||||||||||||||||

NewBank | Flushing, NY | 5 | 349 | 214 | 297 | 44 | ||||||||||||||||

NOA Bancorp, Inc. | Duluth, GA | 5 | 327 | 240 | 273 | 42 | ||||||||||||||||

US Metro Bank | Garden Grove, CA | 4 | 325 | 218 | 269 | 49 | ||||||||||||||||

Uniti Financial Corporation | Buena Park, CA | 3 | 320 | 250 | 278 | 44 | ||||||||||||||||

U&I Financial Corp. | Lynnwood, WA | 4 | 274 | 181 | 231 | 39 | ||||||||||||||||

Ohana Pacific Bank | Honolulu, HI | 2 | 144 | 118 | 127 | 17 | ||||||||||||||||

Korean Bank Subsidiaries in the U.S. | ||||||||||||||||||||||

Woori America Bank | New York, NY | 19 | 1,817 | 1,426 | 1,544 | 249 | ||||||||||||||||

Shinhan Bank America | New York, NY | 16 | 1,337 | 1,223 | 1,167 | 162 | ||||||||||||||||

KEB Hana Bank USA, N.A. | Fort Lee, NJ | 3 | 209 | 132 | 161 | 46 | ||||||||||||||||

Source: S&P Global Market Intelligence. GAAP data when available, otherwise FR Y-9C’s and bank call reports.

| (1) | Total equity includes minority interest. |

| (2) | U.S. Offices is pro forma pending opening of the Santa Clara office in the first quarter of 2018, and does not include loan production offices. |

In addition to these Korean-American banks, we also compete with other banks in our market areas, particularly with Chinese-American banks. In certain geographic markets where we currently operate, there is overlap between Chinese-American, Korean-American and other Asian-American banks for loan and deposit business. We aim to grow both organically and potentially through acquisitions in these markets.

8

Table of Contents

Risks Related to Our Company and an Investment in Our Common Stock

An investment in our common stock involves substantial risks and uncertainties. Investors should carefully consider all of the information in this prospectus, including the detailed discussion of these and other risks under “Risk Factors” beginning on page 13, prior to investing in our common stock. Some of the more significant risks include the following:

| • | a decline in general business and economic conditions, and any regulatory responses to such conditions, could have a material adverse effect on us; |

| • | fluctuations in interest rates may reduce net interest income and otherwise negatively impact our financial condition and results of operations; |

| • | liquidity risks could affect operations and jeopardize our business, financial condition, and results of operations; |

| • | if we do not effectively manage our credit risk, we may experience increased levels of delinquencies, nonperforming loans and charge-offs, which could require increases in our provision for loan losses; |

| • | we could recognize losses on securities held in our securities portfolio, particularly if interest rates increase or economic and market conditions deteriorate; |

| • | our allowance for loan losses may prove to be insufficient to absorb potential losses in our loan portfolio; |

| • | we are subject to extensive state and federal financial regulation, and compliance with changing requirements may restrict our activities or have an adverse effect on our results of operations; |

| • | a significant portion of our loan portfolio is comprised of real estate loans, and negative changes in the economy affecting real estate values and liquidity could impair the value of collateral securing our real estate loans and result in loan and other losses; |

| • | the small andmedium-sized businesses that we lend to may have fewer resources to weather adverse business developments, which may impair a borrower’s ability to repay a loan, and such impairment could adversely affect our results of operations and financial condition; |

| • | we must effectively manage our branch growth strategy; |

| • | our ability to expand our business or make strategic acquisitions outside of California may be limited by our coexistence agreement that restricts our use of the name “Open Bank”; |

| • | system failure or breaches of our network security could subject us to increased operating costs as well as litigation and other liabilities; |

| • | severe weather, natural disasters, acts of war or terrorism and other external events could significantly impact our business; and |

| • | we are highly dependent on our management team, and the loss of our senior executive officers or other key employees could harm our ability to implement our strategic plan, impair our relationships with customers and adversely affect our business, results of operations and growth prospects. |

Corporate Information

Our principal executive office is located at 1000 Wilshire Boulevard, Suite 500, Los Angeles, California 90017, telephone number: (213)892-9999. Our website address is www.myopenbank.com. The information contained on our website is not part of, or incorporated by reference into, this prospectus.

9

Table of Contents

The Offering

Common stock offered by us | 2,000,000 shares. | |

Underwriters’ overallotment option | 300,000 shares. | |

Common stock outstanding after completion of this offering | 15,190,527 shares (or 15,490,527 shares if the underwriters exercise their overallotment option in full). | |

Use of proceeds | We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and estimated offering expenses, will be approximately $19.6 million (or approximately $22.6 million if the underwriters exercise their option to purchase 300,000 additional shares in full). We intend to use the net proceeds from this offering to support our organic growth and other general corporate purposes, which could include opportunistic strategic acquisitions. However, as of the date of this prospectus, we do not have any immediate plans, arrangements or understandings relating to any material acquisition. See “Use of Proceeds.” | |

Dividends | We have not paid dividends to holders of common stock since our inception and have no present intention to commence the payment of dividends in the future. Any future determination by our board of directors to pay dividends to holders of our common stock will depend on our results of operations, financial condition, capital requirements, regulatory restrictions and any other factors that our board of directors may deem relevant. See “Dividend Policy.” | |

Directed Share Program | At our request, the underwriters have reserved for sale, at the initial public offering price, 100,000 shares offered by this prospectus for sale to the directors, officers and employees of OP Bancorp and Open Bank. If these persons purchase reserved shares, it will reduce the number of shares available for sale to the general public. Any reserved shares that are not so purchased will be offered by the underwriters to the general public on the same terms as the other shares offered by this prospectus. | |

Risk Factors | Investing in shares of our common stock involves a high degree of risk. See “Risk Factors,” beginning on page 13, for a discussion of certain factors you should consider carefully before deciding to invest. | |

10

Table of Contents

Nasdaq symbol | We have received approval to list our common stock for trading on the Nasdaq Global Market under the trading symbol “OPBK”. | |

Unless otherwise indicated, all information in this prospectus relating to the number of shares of common stock to be outstanding immediately after the completion of this offering is based on 13,190,527 shares outstanding as of December 31, 2017 and:

| • | excludes 1,130,000 shares of common stock issuable upon exercise of stock options outstanding at December 31, 2017 at a weighted average exercise price of $4.15 per share; |

| • | excludes 218,605 shares of common stock reserved at December 31, 2017 available for future awards under our 2010 Equity Incentive Plan; and |

| • | assumes the underwriters do not exercise their overallotment option to purchase up to 300,000 additional shares from us. |

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OPERATING INFORMATION

The following table sets forth summary historical consolidated financial data as of the dates and for the periods shown. The summary balance sheet data as of December 31, 2017 and 2016 and the summary income statement data for the years ended December 31, 2017, 2016 and 2015 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary balance sheet data as of December 31, 2015 has been derived from our audited consolidated financial statements that are not included in this prospectus.

11

Table of Contents

You should read the following financial data in conjunction with the other information contained in this prospectus, including under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in the financial statements and related notes included elsewhere in this prospectus.

| As of or for the year ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (dollars in thousands, except per share data) | ||||||||||||

Income Statement Data: | ||||||||||||

Interest income | $ | 40,283 | $ | 31,701 | $ | 25,192 | ||||||

Interest expense | 4,573 | 3,371 | 2,689 | |||||||||

Net interest income | 35,710 | 28,330 | 22,503 | |||||||||

Provision for loan losses | 1,311 | 1,682 | 553 | |||||||||

Non-interest income | 8,986 | 9,007 | 7,978 | |||||||||

Non-interest expense | 26,257 | 23,334 | 19,795 | |||||||||

Income before taxes | 17,128 | 12,320 | 10,133 | |||||||||

Provision for income taxes | 7,892 | 4,894 | 4,170 | |||||||||

Net income | 9,236 | 7,425 | 5,963 | |||||||||

Per Share Data: | ||||||||||||

Basic income per share | $ | 0.68 | $ | 0.55 | $ | 0.44 | ||||||

Diluted income per share | $ | 0.66 | $ | 0.53 | $ | 0.43 | ||||||

Book value (at period end) | $ | 6.94 | $ | 6.30 | $ | 5.71 | ||||||

Shares of common stock outstanding | 13,190,527 | 12,896,548 | 12,682,510 | |||||||||

Weighted average diluted shares | 13,485,791 | 13,158,155 | 12,944,867 | |||||||||

Balance Sheet Data: | ||||||||||||

Loans held for investment | $ | 748,024 | $ | 674,227 | $ | 507,286 | ||||||

Loans held for sale | 15,739 | 1,646 | 5,579 | |||||||||

Allowance for loan losses | 9,139 | 7,910 | 6,390 | |||||||||

Total assets | 900,999 | 761,250 | 617,350 | |||||||||

Deposits | 773,306 | 661,784 | 519,721 | |||||||||

Shareholders’ equity | 91,480 | 81,284 | 72,479 | |||||||||

Performance Ratios: | ||||||||||||

Return on average assets | 1.13 | % | 1.08 | % | 1.05 | % | ||||||

Return on average equity | 10.63 | 9.69 | 8.63 | |||||||||

Yield on total loans | 5.48 | 5.20 | 5.18 | |||||||||

Yield on average earning assets | 5.20 | 4.85 | 4.70 | |||||||||

Cost of average interest bearing liabilities | 0.97 | 0.83 | 0.79 | |||||||||

Cost of deposits | 0.62 | 0.56 | 0.55 | |||||||||

Net interest margin | 4.61 | 4.34 | 4.20 | |||||||||

Efficiency ratio (1) | 58.74 | 62.50 | 64.94 | |||||||||

Asset Quality Data (at Period End): | ||||||||||||

Net charge-offs to average loans held for investment | 0.01 | % | 0.03 | % | (0.02 | )% | ||||||

Nonperforming assets to loans held for investment plus OREO | 0.14 | 0.09 | 0.20 | |||||||||

ALL to nonperforming loans | 881.29 | 1,373.26 | 615.01 | |||||||||

ALL to loans held for investment | 1.22 | 1.17 | 1.26 | |||||||||

Balance Sheet and Capital Ratios: | ||||||||||||

Loans held for investment to deposits | 96.73 | % | 101.88 | % | 97.61 | % | ||||||

Noninterest bearing deposits to deposits | 37.43 | 37.38 | 29.85 | |||||||||

Tangible common equity to tangible assets (2) | 10.15 | 10.70 | 11.74 | |||||||||

Average equity to average total assets | 10.59 | 11.18 | 12.20 | |||||||||

Leverage ratio | 10.46 | 10.89 | 11.70 | |||||||||

Common equity tier 1 ratio | 12.26 | 12.20 | 14.28 | |||||||||

Tier 1 risk-based capital ratio | 12.26 | 12.20 | 14.28 | |||||||||

Total risk-based capital ratio | 13.49 | 13.40 | 15.53 | |||||||||

Non-owner occupied CRE to total risk-based capital | 296.69 | 293.56 | 233.83 | |||||||||

| (1) | Representsnon-interest expense divided by the sum of net interest income plusnon-interest income. |

| (2) | Represents anon-GAAP financial measure. See “GAAP Reconciliation and Management Explanation ofNon-GAAP Financial Measures” for a reconciliation of ournon-GAAP measure to the most comparable financial measure. |

12

Table of Contents

Investing in our common stock involves a high degree of risk. Before you decide to invest, you should carefully consider the risks described below, together with all other information included in this prospectus. We believe the risks described below are the risks that are material to us. Any of the following risks, as well as risks that we do not know or currently deem immaterial, could have a material adverse effect on our business, financial condition, results of operations and growth prospects. In that case, you could experience a partial or complete loss of your investment.

Risks Related to Our Business

A decline in general business and economic conditions and any regulatory responses to such conditions could have a material adverse effect on our business, financial position, results of operations and growth prospects.

Our business and operations are sensitive to general business and economic conditions in the United States, generally, and particularly the state of California and the Los Angeles-Long Beach-Anaheim, California MSA. Unfavorable or uncertain economic and market conditions could lead to credit quality concerns related to borrower repayment ability and collateral protection as well as reduced demand for the products and services we offer. In recent years, there has been a gradual improvement in the U.S. economy as evidenced by a rebound in the housing market, lower unemployment and higher valuations in the equities markets. However, economic growth has been uneven, and opinions vary on the strength and direction of the economy. Uncertainties also have arisen regarding the potential for a reversal or renegotiation of international trade agreements under the administration of U.S. President Donald J. Trump, and the impact such actions and other policies of the new administration may have on economic and market conditions. In addition, concerns about the performance of international economies, especially in Europe and emerging markets, and economic conditions in Asia, particularly the economies of China, South Korea and Japan, can impact the economy and financial markets here in the United States. If the national, regional and local economies experience worsening economic conditions, including high levels of unemployment, our growth and profitability could be constrained. Weak economic conditions are characterized by, among other indicators, deflation, elevated levels of unemployment, fluctuations in debt and equity capital markets, increased delinquencies on mortgage, commercial and consumer loans, residential and commercial real estate price declines, and lower home sales and commercial activity. All of these factors are generally detrimental to our business. Our business is significantly affected by monetary and other regulatory policies of the U.S. federal government, its agencies and government-sponsored entities. Changes in any of these policies are influenced by macroeconomic conditions and other factors that are beyond our control, are difficult to predict and could have a material adverse effect on our business, financial position, results of operations and growth prospects.

Fluctuations in interest rates may reduce net interest income and otherwise negatively impact our financial condition and results of operations.

Shifts in short-term interest rates may reduce net interest income, which is the principal component of our earnings. Net interest income is the difference between the amounts received by us on our interest-earning assets and the interest paid by us on our interest-bearing liabilities. When interest rates rise, the rate of interest we receive on our assets, such as loans, rises more quickly than the rate of interest that we pay on our interest-bearing liabilities, such as deposits, which may cause our profits to increase. When interest rates decrease, the rate of interest we receive on our assets, such as loans, declines more quickly than the rate of interest that we pay on our interest-bearing liabilities, such as deposits, which may cause our profits to decrease. The impact on earnings is more adverse when the slope of the yield curve flattens, that is, when short-term interest rates increase more than long-term interest rates or when long-term interest rates decrease more than short-term interest rates.

Changes in interest rates could influence our ability to originate loans and deposits. Historically, there has been an inverse correlation between the demand for loans and interest rates. Loan origination volume usually declines

13

Table of Contents

during periods of rising or high interest rates and increases during periods of declining or low interest rates. For example, mortgage production historically, including refinancing activity, declines in rising interest rate environments. Changes in interest rates also have a significant impact on the carrying value of certain of our assets, including loans, real estate and investment securities, on our balance sheet.

Interest rate increases often result in larger payment requirements for our borrowers, which increases the potential for default. At the same time, the marketability of any underlying property that serves as collateral for such loans may be adversely affected by any reduced demand resulting from higher interest rates.

Changes in interest rates can also affect the level of loan refinancing activity, which impacts the amount of prepayment penalty income we receive on loans we hold. Because prepayment penalties are recorded as interest income when received, the extent to which they increase or decrease during any given period could have a significant impact on the level of net interest income and net income we generate during that time. A decrease in our prepayment penalty income resulting from any change in interest rates or as a result of regulatory limitations on our ability to charge prepayment penalties could therefore adversely affect our net interest income, net income or results of operations.

An increase in interest rates that adversely affects the ability of borrowers to pay the principal or interest on loans may lead to an increase in nonperforming assets and a reduction of income recognized, which could have a material adverse effect on our results of operations and cash flows. Further, when we place a loan on nonaccrual status, we reverse any accrued but unpaid interest receivable, which decreases interest income. Subsequently, we continue to have a cost to fund the loan, which is reflected as interest expense, without any interest income to offset the associated funding expense. Thus, an increase in the amount of nonperforming assets would have an adverse impact on net interest income.

Changes in interest rates also can affect the value of loans, securities and other assets. Rising interest rates will result in a decline in value of the fixed-rate debt securities we hold in our investment securities portfolio. The unrealized losses resulting from holding these securities would be recognized in accumulated other comprehensive income and reduce total shareholders’ equity. Unrealized losses do not negatively impact our regulatory capital ratios. However, tangible common equity and the associated ratios would be reduced. If debt securities in an unrealized loss position are sold, such losses become realized and will reduce our regulatory capital ratios.

If short-term interest rates remain at their historically low levels for a prolonged period, and if longer term interest rates fall, we could experience net interest margin compression as our interest earning assets would continue to reprice downward while our interest-bearing liability rates could fail to decline in tandem. This would have a material adverse effect on our net interest income and our results of operations.

We could recognize losses on securities held in our securities portfolio, particularly if interest rates increase or economic and market conditions deteriorate.

Factors beyond our control can significantly influence the fair value of securities in our portfolio and can cause potential adverse changes to the fair value of these securities. For example, fixed-rate securities acquired by us are generally subject to decreases in market value when interest rates rise. Additional factors include, but are not limited to, rating agency downgrades of the securities or our own analysis of the value of the security, defaults by the issuer or individual mortgagors with respect to the underlying securities, or instability in the credit markets. Any of the foregoing factors could cause other-than-temporary impairment in future periods and result in realized losses. The process for determining whether impairment is other-than-temporary usually requires difficult, subjective judgments about the future financial performance of the issuer and any collateral underlying the security in order to assess the probability of receiving all contractual principal and interest payments on the security. Because of changing economic and market conditions affecting interest rates, the financial condition of

14

Table of Contents

issuers of the securities and the performance of the underlying collateral, we may recognize realized and/or unrealized losses in future periods, which could have an adverse effect on our financial condition and results of operations.

Liquidity risks could affect operations and jeopardize our business, financial condition, and results of operations.

Liquidity is essential to our business. An inability to raise funds through deposits, borrowings, the sale of loans and/or investment securities and through other sources could have a substantial negative effect on our liquidity. Our most important source of funds consists of our customer deposits. Such deposit balances can decrease when customers perceive alternative investments, such as the stock market, as providing a better risk/return tradeoff. If customers move money out of bank deposits and into other investments, we could lose a relatively low cost source of funds, which would require us to seek wholesale funding alternatives in order to continue to grow, thereby increasing our funding costs and reducing our net interest income and net income.

Other primary sources of funds consist of cash from operations, investment maturities and sales, sale of loans and proceeds from the issuance and sale of our equity securities to investors. Additional liquidity is provided by our ability to borrow from the Federal Reserve Bank of San Francisco and the Federal Home Loan Bank of San Francisco. We also may borrow from third-party lenders from time to time. Our access to funding sources in amounts adequate to finance or capitalize our activities or on terms that are acceptable to us could be impaired by factors that affect us directly or the financial services industry or economy in general, such as disruptions in the financial markets or negative views and expectations about the prospects for the financial services industry.

Any decline in available funding could adversely impact our ability to continue to implement our strategic plan, including our ability to originate loans, invest in securities, meet our expenses, or to fulfill obligations such as repaying our borrowings or meeting deposit withdrawal demands, any of which could have a material adverse impact on our liquidity, business, financial condition and results of operations.

Our business depends on our ability to successfully manage credit risk.

The operation of our business requires us to manage credit risk. As a lender, we are exposed to the risk that our borrowers will be unable to repay their loans according to their terms, and that the collateral securing repayment of their loans, if any, may not be sufficient to ensure repayment. In addition, there are risks inherent in making any loan, including risks with respect to the period of time over which the loan may be repaid, risks relating to proper loan underwriting, risks resulting from changes in economic and industry conditions and risks inherent in dealing with individual borrowers. In order to successfully manage credit risk, we must, among other things, maintain disciplined and prudent underwriting standards and ensure that our bankers follow those standards. The weakening of these standards for any reason, such as an attempt to attract higher yielding loans, a lack of discipline or diligence by our employees in underwriting and monitoring loans, the inability of our employees to adequately adapt policies and procedures to changes in economic or any other conditions affecting borrowers and the quality of our loan portfolio, may result in loan defaults, foreclosures and additional charge-offs and may necessitate that we significantly increase our allowance for loan losses, each of which could adversely affect our net income. As a result, our inability to successfully manage credit risk could have a material adverse effect on our business, financial condition or results of operations.

An important feature of our credit risk management system is our use of an internal credit risk rating and control system through which we identify, measure, monitor and mitigate existing and emerging credit risk of our customers. As this process involves detailed analysis of the customer or credit risk, taking into account both quantitative and qualitative factors, it is subject to human error. In exercising their judgment, our employees may not always be able to assign an accurate credit rating to a customer or credit risk, which may result in our exposure to higher credit risks than indicated by our risk rating and control system. Although our management seeks to address possible credit risk proactively, it is possible that the credit risk rating and control system will not identify credit risk in our loan portfolio and that we may fail to manage credit risk effectively.

15

Table of Contents

Some of our tools and metrics for managing credit risk and other risks are based upon our use of observed historical market behavior and assumptions. We rely on quantitative models to measure risks and to estimate certain financial values. Models may be used in such processes as determining the pricing of various products, grading loans and extending credit, measuring interest rates and other market risks, predicting losses, assessing capital adequacy and calculating regulatory capital levels, as well as estimating the value of financial instruments and balance sheet items. Poorly designed or implemented models present the risk that our business decisions based on information incorporating such models will be adversely affected due to the inadequacy of that information. Moreover, our models may fail to predict future risk exposures if the information used in the model is incorrect, obsolete or not sufficiently comparable to actual events as they occur, or if our model assumptions prove incorrect. We seek to incorporate appropriate historical data in our models, but the range of market values and behaviors reflected in any period of historical data is not at all times predictive of future developments in any particular period and the period of data we incorporate into our models may turn out to be inappropriate for the future period being modeled. In such case, our ability to manage risk would be limited and our risk exposure and losses could be significantly greater than our models indicated.

Risks Related to Our Loans

Because a significant portion of our loan portfolio is comprised of real estate loans, negative changes in the economy affecting real estate values and liquidity could impair the value of collateral securing our real estate loans and result in loan and other losses.

At December 31, 2017, approximately 84% of our loan portfolio was comprised of loans with real estate as a primary or secondary component of collateral. As a result, adverse developments affecting real estate values in our market areas could increase the credit risk associated with our real estate loan portfolio. The market value of real estate can fluctuate significantly in a short period of time as a result of market conditions in the geographic area in which the real estate is located. Real estate values and real estate markets are generally affected by changes in national, regional or local economic conditions, the rate of unemployment, fluctuations in interest rates and the availability of loans to potential purchasers, changes in tax laws and other governmental statutes, regulations and policies and acts of nature, such as earthquakes and natural disasters. Adverse changes affecting real estate values and the liquidity of real estate in one or more of our markets could increase the credit risk associated with our loan portfolio, significantly impair the value of property pledged as collateral on loans and affect our ability to sell the collateral upon foreclosure without a loss or additional losses, which could result in losses that would adversely affect profitability. Such declines and losses would have a material adverse impact on our business, results of operations and growth prospects. In addition, if hazardous or toxic substances are found on properties pledged as collateral, the value of the real estate could be impaired. If we foreclose on and take title to such properties, we may be liable for remediation costs, as well as for personal injury and property damage. Environmental laws may require us to incur substantial expenses to address unknown liabilities and may materially reduce the affected property’s value or limit our ability to use or sell the affected property.

Many of our loans are to commercial borrowers, which have a higher degree of risk than other types of loans.

At December 31, 2017, we had $640.0 million of commercial loans, consisting of $420.8 million of commercial real estate loans, $106.9 million of SBA loans, and $103.7 million of commercial and industrial loans, including trade finance loans, for which real estate is not the primary source of collateral. Commercial loans represented 85.6% of our total loan portfolio at December 31, 2017. Commercial loans are often larger and involve greater risks than other types of lending. Because payments on such loans are often dependent on the successful operation or development of the property or business involved, repayment of such loans is often more sensitive than other types of loans to adverse conditions in the real estate market or the general business climate and economy. Accordingly, a downturn in the real estate market and a challenging business and economic environment may increase our risk related to commercial loans, particularly commercial real estate loans. Unlike home mortgage loans, which generally are made on the basis of the borrowers’ ability to make repayment from their employment and other income and which are secured by real property whose value tends to be more easily

16

Table of Contents

ascertainable, commercial loans typically are made on the basis of the borrowers’ ability to make repayment from the cash flow of the commercial venture. Our commercial and industrial loans are primarily made based on the identified cash flow of the borrower and secondarily on the collateral underlying the loans. Most often, collateral consists of accounts receivable, inventory and equipment. Inventory and equipment may depreciate over time, may be difficult to appraise and may fluctuate in value based on the success of the business. Accounts receivable may be uncollectable. If the cash flow from business operations is reduced, the borrower’s ability to repay the loan may be impaired. Due to the larger average size of each commercial loan as compared with other loans such as residential loans, as well as collateral that is generally less readily-marketable, losses incurred on a small number of commercial loans could have a material adverse impact on our financial condition and results of operations.

We have a concentration in commercial real estate lending which could cause our regulators to restrict our ability to grow.

As a part of their regulatory oversight, the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System and the Federal Deposit Insurance Corporation have issued the Commercial Real Estate (CRE) Concentration Guidance on sound risk management practices with respect to a financial institution’s concentrations in commercial real estate lending activities. These guidelines were issued in response to the agencies’ concerns that rising CRE concentrations might expose financial institutions to unanticipated earnings and capital volatility in the event of adverse changes in the commercial real estate market. Existing guidance reinforces and enhances existing regulations and guidelines for safe and sound real estate lending by providing supervisory criteria, including numerical indicators to assist in identifying institutions with potentially significant commercial real estate loan concentrations that may warrant greater supervisory scrutiny. The guidance does not limit banks’ commercial real estate lending, but rather guides institutions in developing risk management practices and levels of capital that are commensurate with the level and nature of their commercial real estate concentrations. The CRE Concentration Guidance identifies certain concentration levels that, if exceeded, will expose the institution to additional supervisory analysis with regard to the institution’s CRE concentration risk. The CRE Concentration Guidance is designed to promote appropriate levels of capital and sound loan and risk management practices for financial institutions with a concentration of CRE loans. In general, the CRE Concentration Guidance establishes the following supervisory criteria as preliminary indications of possible CRE concentration risk: (1) the institution’s total construction, land development and other land loans represent 100% or more of total risk-based capital; or (2) total CRE loans as defined in the regulatory guidelines represent 300% or more of total risk-based capital, and the institution’s CRE loan portfolio has increased by 50% or more during the prior36-month period. Pursuant to the CRE Concentration Guidelines, loans secured by owner occupied commercial real estate are not included for purposes of CRE Concentration calculation. We believe that the CRE Concentration Guidance is applicable to us. As of December 31, 2017, ournon-owner occupied CRE loans represented 296.7% of our total risk-based capital, as compared to 293.6% and 233.8% as of December 31, 2016 and 2015, respectively. Although we are actively working to manage our CRE concentration and believe that our underwriting policies, management information systems, independent credit administration process, and monitoring of real estate loan concentrations are currently sufficient to address the CRE Concentration Guidance, the FDIC or other federal regulators could become concerned about our CRE loan concentrations, and they could limit our ability to grow by, among other things, restricting their approvals for the establishment or acquisition of branches, or approvals of mergers or other acquisition opportunities.

Our single family residential loan product consists primarily ofnon-qualified single family home mortgage loans which may be considered less liquid and more risky.

As of December 31, 2017, our single family home mortgage loan portfolio amounted to $104.1 million or 13.9% of our total loan portfolio. As of December 31, 2017, all of our single family home mortgage loans werenon-qualified mortgage loans. We originated $42.1 million and $53.3 million ofnon-qualified single family home mortgage loans for the years ended December 31, 2017 and 2016, respectively. As of December 31, 2017, ournon-qualified single family home mortgage loans had an averageloan-to-value of 60%.

17

Table of Contents

Thenon-qualified single-family home mortgage loans that we originate are designed to assist Korean-Americans who have recently immigrated to the United States and those Korean-Americans without sufficient documentation to qualify for a traditional home mortgage loan and as such are willing to provide higher down payment amounts and pay higher interest rates and fees in return for reduced documentation requirements.Non-qualified single-family home mortgage loans are considered to have a higher degree of risk and are less liquid than qualified single-family home mortgage loans because non-qualified loans are not able to be securitized and can only be sold directly to other financial institutions. Qualified loans require a minimum of two years of tax returns for borrowers to demonstrate their ability to repay the loan and other standard documentation to qualify for securitization. For non-qualified loans we do not require the standard documentation required for qualified loans. For example, we will typically require only one year of tax returns and only pay-stub verification of employment. We attempt to address this enhanced risk through our underwriting process, including requiring larger down payments and, in some cases, interest reserves.

Our use of appraisals in deciding whether to make a loan on or secured by real property does not ensure the value of the real property collateral.

In considering whether to make a loan secured by real property we generally require an appraisal of the property. However, an appraisal is only an estimate of the value of the property at the time the appraisal is conducted, and an error in fact or judgment could adversely affect the reliability of an appraisal. In addition, events occurring after the initial appraisal may cause the value of the real estate to decrease. As a result of any of these factors the value of collateral securing a loan may be less than estimated, and if a default occurs we may not recover the outstanding balance of the loan.

The small andmedium-sized businesses that we lend to may have fewer resources to weather adverse business developments, which may impair a borrower’s ability to repay a loan, and such impairment could adversely affect our results of operations and financial condition.

We target our business development and marketing strategy primarily to serve the banking and financial services needs of small tomedium-sized businesses. These businesses generally have fewer financial resources in terms of capital or borrowing capacity than larger entities, frequently have smaller market shares than their competition, may be more vulnerable to economic downturns, often need substantial additional capital to expand or compete and may experience substantial volatility in operating results, any of which may impair a borrower’s ability to repay a loan. In addition, the success of a small andmedium-sized business often depends on the management talents and efforts of one or two people or a small group of people, and the death, disability or resignation of one or more of these people could have a material adverse impact on the business and its ability to repay its loan. If general economic conditions negatively impact the markets in which we operate and small tomedium-sized businesses are adversely affected or our borrowers are otherwise affected by adverse business developments, our business, financial condition and results of operations may be adversely affected.

We may suffer losses in our loan portfolio despite our underwriting practices.

We mitigate the risks inherent in our loan portfolio by adhering to sound and proven underwriting practices, managed by experienced and knowledgeable credit professionals. These practices include analysis of a borrower’s prior credit history, financial statements, tax returns, and cash flow projections, valuations of collateral based on reports of independent appraisers and verifications of liquid assets. Although we believe that our underwriting criteria is appropriate for the various kinds of loans we make, we may incur losses on loans that meet our underwriting criteria, and these losses may exceed the amounts set aside as reserves in our allowance for loan loss.

Lack of seasoning of our loan portfolio could increase risk of credit defaults in the future.

As a result of the organic growth of our loan portfolio over the past five years, a large portion of our loans and of our lending relationships are of relatively recent origin. In general, loans do not begin to show signs of credit deterioration or default until they have been outstanding for some period of time, a process referred to as “seasoning.” As a result, a portfolio of older loans will usually behave more predictably than a newer portfolio.

18

Table of Contents