ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED MAY 31, 2019

SEPTEMBER 26, 2019

SUITE 501, 543 GRANVILLE STREET

VANCOUVER, B.C. V6C 1X8

METALLA ROYALTY & STREAMING LTD.

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED MAY 31, 2019

TABLE OF CONTENTS

| SCHEDULE A – AUDIT COMMITTEE CHARTER |

-i-

INTRODUCTORY NOTES

Cautionary Note Regarding Forward-Looking Statements

This annual information form (“AIF”) contains “forward-looking information” or “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking information is provided as of the date of this AIF and Metalla Royalty & Streaming Ltd. (“Metalla” or the “Company”) does not intend to and does not assume any obligation to update forward-looking information, except as required by applicable law. For this reason and the reasons set forth below, investors should not place undue reliance on forward-looking statements.

Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. Forward-looking information is based on reasonable assumptions that have been made by Metalla as at the date of such information and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Metalla to be materially different from those expressed or implied by such forward-looking information, including but not limited to: the impact of general business and economic conditions; the absence of control over mining operations from which Metalla will purchase precious metals or from which it will receive stream or royalty payments, and risks related to those mining operations, including risks related to international operations, government and environmental regulation, delays in mine construction and operations, actual results of mining and current exploration activities, conclusions of economic evaluations and changes in project parameters as plans are refined; problems related to the ability to market precious metals or other metals; industry conditions, including commodity price fluctuations, interest and exchange rate fluctuations; interpretation by government entities of tax laws or the implementation of new tax laws; the volatility of the stock market; competition; also, those risk factors discussed under the heading “Risk Factors” in this AIF.

Forward-looking information in this AIF includes disclosure regarding the gold, silver and other metal purchase agreements (“Streams” and each individually a “Stream”) of Metalla, royalty payments to be paid to Metalla by property owners or operators of mining projects pursuant to net smelter returns (“NSR”), and other royalty agreements or interests (“Royalties” and individually a “Royalty”), the future outlook of Metalla and the mineral reserves and resource estimates for Endeavor Mine, Joaquin Mine, COSE Mine and Santa Gertrudis gold property (the “Santa Gertrudis Property”). Forward-looking statements are based on a number of material assumptions, which management of Metalla believe to be reasonable, including, but not limited to, the continuation of mining operations from which Metalla will purchase precious or other metals or in respect of which Metalla will receive Royalty payments, that commodity prices will not experience a material adverse change, mining operations that underlie Streams or Royalties will operate in accordance with disclosed parameters and such other assumptions as may be set out herein.

Although Metalla has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results to not be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. Readers of this AIF should carefully review the risk factors set out in this AIF under the heading “Risk Factors”.

- 2 -

Technical and Third-Party Information and Cautionary Note for United States Readers

Except where otherwise stated, the disclosure in this AIF relating to properties and operations in which Metalla holds Royalty, Stream or other interests, including the disclosure in this AIF under the heading “Material Assets”is based on information publicly disclosed by the owners or operators of these properties and information/data available in the public domain as at the date hereof, and none of this information has been independently verified by Metalla. Specifically, as a Royalty or Stream holder, Metalla has limited, if any, access to properties on which it holds Royalties, Streams, or other interests in its asset portfolio. The Company may from time to time receive operating information from the owners and operators of the mining properties, which it is not permitted to disclose to the public. Metalla is dependent on, (i) the operators of the mining properties and their qualified persons to provide information to Metalla, or (ii) on publicly available information to prepare disclosure pertaining to properties and operations on the properties on which the Company holds Royalty, Stream or other interests, and generally has limited or no ability to independently verify such information. Although the Company does not have any knowledge that such information may not be accurate, there can be no assurance that such third-party information is complete or accurate. Some reported public information in respect of a mining property may relate to a larger property area than the area covered by Metalla’s Royalty, Stream or other interest. Metalla’s Royalty, Stream or other interests may cover less than 100% of a specific mining property and may only apply to a portion of the publicly reported mineral reserves, mineral resources and or production from a mining property.

As at the date of this AIF the Company considers its Royalty and Stream interests in the Endeavor Mine, Joaquin Mine, COSE Mine and Santa Gertrudis Property to be its only material mineral properties for the purposes of National Instrument 43-101 –Standards of Disclosure for Mineral Projects(“NI 43-101”). Information included in this AIF with respect to these material assets have been prepared in accordance with the exemption set forth in section 9.2 of NI 43-101.

Unless otherwise noted, the disclosure contained in this AIF of a scientific or technical nature for:

| (a) | the Endeavor Mine is based on the technical report entitled “Endeavor Mine Cobar, New South Wales Australia Technical Report”having an effective date of March 28, 2013 which technical report was prepared for Coeur Mining, Inc. (“Coeur”) (formerly Coeur d’Alene Mines Corporation), and filed under Coeur’s SEDAR profile onwww.sedar.com, and on information prepared and disclosed by CBH Resources Limited (“CBH”) and their parent company TOHO Zinc Co. Ltd. (“Toho”) and can be found at http://www.toho-zinc.co.jp/. The information and data is available in the public domain as at the date hereof, and none of this information has been independently verified by the Company. |

| (b) | the Joaquin Mine is based on the technical report entitled “Technical Report for the Joaquin Property, Santa Cruz, Argentina - Pre-feasibility Study”having an effective date of November 30, 2017 which technical report was prepared for Pan American Silver Corp. (“Pan American”), and filed under Pan American’s SEDAR profile onwww.sedar.com, and information that has been provided by Pan American and/or has been sourced from their news releases with respect to the Joaquin Mine. |

| (c) | the COSE Mine is based on the technical report entitled “NI 43-101 Technical Report Preliminary Economic Assessment Cap Oeste Suroeste (COSE) Project Santa Cruz Province, Argentina”having an effective date of August 20, 2011 which technical report was prepared for Patagonia Gold Plc (“Patagonia Gold”), and filed under Patagonia Gold’s SEDAR profile onwww.sedar.com, and information that has been provided by Patagonia Gold and/or has been sourced from their news releases with respect to the COSE Mine. |

- 3 -

| (d) | the Santa Gertrudis Property is based on the technical report entitled “Technical Report, Updated Resource Estimate And Preliminary Economic Assessment On The Santa Gertrudis Gold Property, Sonora State, Mexico Latitude 30o38’ N Longitude 110o33’ W”having an effective date of August 22, 2014 which technical report was prepared for GoGold Resources Inc. (“GoGold”), and filed under GoGold’s SEDAR profile onwww.sedar.com, and information that has been provided by GoGold and/or has been sourced from their news releases with respect to the Santa Gertrudis Property. |

Unless otherwise indicated, all of the mineral reserves and mineral resources disclosed in this AIF have been prepared in accordance with NI 43-101. Canadian standards for public disclosure of scientific and technical information concerning mineral projects differ significantly from the requirements of the Industry Guide 7 (“Guide 7”) adopted by the United States Securities and Exchange Commission (the “SEC”) under the U.S. Securities Act of 1933, as amended. In particular, and without limiting the generality of the foregoing, the terms “Mineral Reserve”, “Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms as defined in accordance with NI 43-101 and CIM Standards. These definitions differ from the definitions in Guide 7, and therefore may not qualify as reserves under SEC standards. Under Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. Under Guide 7 standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

In addition, the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Accordingly, resource information contained herein may not be comparable to similar information disclosed by U.S. companies under Guide 7. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves or that they can be mined economically or legally. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Historical results or feasibility models presented herein are not guarantees or expectations of future performance. It cannot be assumed that all, or any part, of an inferred mineral resource will ever be upgraded to a higher category. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or that it can be economically or legally mined. Further, while NI 43-101 permits companies to disclose economic projections contained in pre-feasibility studies and preliminary economic assessments, which are not based on “reserves”, U.S. companies have not generally been permitted to disclose economic projections for a mineral property in their SEC filings prior to the establishment of “reserves”. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian reporting standards; however, Guide 7 normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this AIF contains descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Charles Beaudry, M.Sc., P.Geo. and géo. for Metalla and a “Qualified Person” under NI 43-101 has reviewed and approved the written scientific and technical disclosure contained in this AIF.

This AIF also contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about the projected silver production from the Company’s silver stream on the Endeavor mine which are subject to the same assumptions, risk factors, limitations and qualifications as set forth in the below paragraphs. FOFI contained in this AIF was made as of the date of this AIF and was provided for the purpose of providing further information about Metalla's anticipated future business operations. Metalla disclaims any intention or obligation to update or revise any FOFI contained in this AIF, whether as a result of new information, future events or otherwise, unless required pursuant to applicable law. FOFI contained in this AIF should not be used for purposes other than for which it is disclosed herein. Such future-oriented production information is provided for the purpose of providing information about management's current expectations and plans relating to the future. Readers are cautioned that such outlook or information should not be used for purposes other than for which it is disclosed in this AIF.

Currency Presentation

All dollar amounts referenced as “C$”, “CAD” or “CAD$” are references to Canadian dollars, all references to “US$”, “USD” or “USD$” are references to United States dollars.

The following table sets out the high and low rates of exchange for one U.S. dollar expressed in Canadian dollars in effect at the end of each of the following periods, the average rate of exchange for those periods, and the rate of exchange in effect at the end of each of those periods, each based on the rate published by the Bank of Canada.

| Year Ended May 31 | ||

| 2019 | 2018 | |

| Rate at end of period | C$1.3527 | C$1.2948 |

| Average rate during period | C$1.3224 | C$1.2718 |

| High rate for period | C$1.3642 | C$1.3504 |

| Low rate for period | C$1.2803 | C$1.2128 |

CORPORATE STRUCTURE

Metalla was incorporated on May 11, 1983 pursuant to theCompany Act (British Columbia) under the name Cactus West Explorations Ltd. The Company’s name was changed to Cimarron Minerals Ltd. and its share capital was consolidated on a five (old) for one (new) basis, on April 29, 1996. On May 1, 2000, the Company’s name was changed to DiscFactories Corporation, and its share capital was consolidated on a two (old) for one (new) basis and the Company was continued into the federal jurisdiction under theCanada Business Corporations Act. On February 20, 2007, the Company completed a change of business transaction pursuant to which it changed its name from DiscFactories Corporation to Excalibur Resources Ltd. On January 11, 2010, its share capital was consolidated on an eight (old) for one (new) basis. On December 1, 2016 it changed its name from Excalibur Resources Ltd. to Metalla, and completed a share consolidation on a three (old) for one (new) basis. On November 16, 2017, Metalla continued under theBusiness Corporations Act(British Columbia) (“BCBCA”).

The Company’s head office is located at 501-543 Granville Street, Vancouver, British Columbia, V6C 1X8, Canada. The Company’s registered and records office is located at Suite 2300, 550 Burrard Street, Vancouver, British Columbia, V6C 2B5, Canada.

The Company is a reporting issuer in British Columbia, Alberta, Manitoba, Ontario, Nova Scotia, and Newfoundland. As at the date of this AIF the Company’s common shares (the “Common Shares”) are listed on the TSX Venture Exchange (the “TSX-V”) under the symbol “MTA”, on the Frankfurt Exchange under the Symbol “X9CP”, and on Over-the-counter markets under the symbol “MTAFF”.

- 5 -

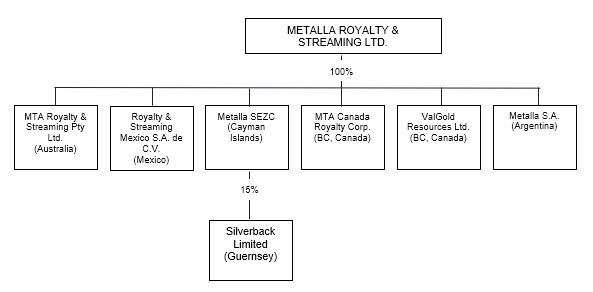

The Company has six material subsidiaries: (i) MTA Canada Royalty Corp. which was incorporated under the laws of British Columbia (ii) Valgold Resources Ltd. (“Valgold”) which was incorporated under the laws of British Columbia; (iii) MTA Royalty & Streaming Pty Ltd. which was incorporated under the laws of Australia; (iv) Metalla S.A. which was incorporated under the laws of Argentina; (v) Royalty & Streaming Mexico, S.A. de C.V. which was incorporated under the laws of Mexico; and (vi) Metalla SEZC which was incorporated under the laws of Cayman Islands.

Inter-Corporate Relationship

The chart below illustrates the Company’s material inter-corporate relationships as at the date hereof:

GENERAL DEVELOPMENT OF THE BUSINESS

Prior Business of Metalla

Prior to 2016, Metalla (operating as Excalibur Resources Ltd. at the time) was engaged in the business of exploration and development of mineral properties. Readers are referred to the public disclosure of Metalla (then referred to as Excalibur Resources Ltd.) for further information concerning the operations of Metalla prior to June 1, 2016.

Current Business of Metalla – 3 Year History

Acquisition of High Stream Corp.

On September 1, 2016, Metalla signed a binding agreement to acquire High Stream Corp., a specialty streaming and royalty finance company for 10,000,000 shares. As part of the transaction, Brett Heath, was appointed President and a director of Metalla, and subsequently was appointed Chief Executive Officer on June 19, 2017.

- 6 -

Acquisition of Royalties from International Explorers & Prospectors Inc. and Matamec Exploration Inc.

On November 15, 2016, Metalla acquired 100% of three NSRs on properties located in Timmins, Ontario for CAD$6 million in cash and CAD$4 million in Common Shares based on the achievement of various progress milestones determined by the expansion plans of the underlying operators of the mines. The acquisition included the following:

Hoyle Pond Gold Mine– 1% NSR Royalty granted by Newmont Goldcorp Corporation (“Goldcorp”) (formerly Goldcorp Inc.) on: (a) the leased mining rights located in Hoyle township, east of the Hoyle Pond Gold Mine, payable after production of 500,000 ounces gold equivalent; (b) the fee simple mining rights (patented claims) located in Hoyle township, east of the Hoyle Pond Gold Mine; and (c) the Colbert/Anglo Property mining rights located in Matheson township, east of the Hoyle Pond Gold Mine, with a right to buy back 0.375% of such NSR Royalty for an amount of CAD$500,000; and a 1% NSR Royalty on the Bint Property owned by Glencore PLC located in Matheson township, east of the Hoyle Pond Gold Mine.

West Timmins Extension– up to 1.5% NSR Royalty on the West Timmins extension properties, owned by Pan American, subject to a buyback of 0.75% for CAD$750,000. The West Timmins mine was acquired by Pan American through the takeover of Tahoe Resources in 2019. The West Timmins mine is the flagship mine in the district for Pan American. Metalla has a 1.5% NSR Royalty on the Wallingford claim which lies on the extension of the Timmins Deposit. The Timmins deposit plunges towards the NW onto Metalla Royalty Claims and will cross the boundary at depth.

DeSantis Mine Royalty– 1.5% NSR Royalty on the DeSantis properties, with a buyback of 0.5% for CAD$1 million. The DeSantis Project, which includes the past producing DeSantis Mine, covers approximately five km of strike length within the highly prospective geology of the Destor-Porcupine Deformation Zone, the main structure controlling gold deposits in the Timmins gold camp. The property is located approximately 11 km west of Goldcorp’s Dome Mine and 14 km east of Lake Shore Gold Corp.’s Timmins Mine.

On June 1, 2017, Metalla consolidated its Hoyle Pond Extension royalties by acquiring NSR Royalties from Matamec Exploration Inc. for an upfront payment of CAD$500,000 in cash and 2,000,000 (post-consolidation) Common Shares valued at CAD$0.50 each, and 1,000,000 Common Share purchase warrants each with a term of 2 years with an exercise price of CAD$0.75. The NSR Royalties included the following:

Hoyle Pond Gold Mine– 1% NSR Royalty granted by Goldcorp Inc. on: (a) the leased mining rights located in Hoyle township, east of the Hoyle Pond Gold Mine, payable after production of 500,000 ounces gold equivalent; (b) the fee simple mining rights (patented claims) located in Hoyle township, east of the Hoyle Pond Gold Mine; and (c) the Colbert/Anglo Property mining rights located in Matheson township, east of the Hoyle Pond Gold Mine, with a right to buy back 0.375% of such NSR Royalty for an amount of CAD$500,000;

Bint Property– 1% NSR Royalty on the Bint Property located in Matheson township, east of the Hoyle Pond Gold Mine; and

Montclerg Property– 1% NSR Royalty on the Montclerg Property located on the Pipestone Fault in the Timmins Gold Camp.

- 7 -

Completion of a Private Placement

On November 30, 2016, Metalla closed a non-brokered private placement for an oversubscribed total of 23,717,900 units of the Company at CAD$0.10 per unit for gross aggregate proceeds of CAD$2,371,790. Each unit consisted of one Common Share and one-half of one warrant. Each full warrant was exercisable to acquire an additional Common Share at CAD$0.15 per share for a period of two years from the closing date. These shares were issued prior to the 3 (old) for 1 (new) consolidation on December 1, 2016.

Listing on TSX-V and OTCQB

On December 2, 2016, Metalla commenced trading on the OTCQB Venture Marketplace and on February 2, 2018, Metalla commenced trading on the TSX-V as a Tier 1 issuer.

Completion of a Private Placement

On March 6, 2017, Metalla closed a non-brokered Private Placement for gross proceeds of CAD$3,216,818 for 6,433,636 units at a price of CAD$0.50 per unit. Each unit consisted of one Common Share and one half of one Common Share purchase warrant. Each full warrant was exercisable to acquire an additional Common Share at CAD$0.75 per Common Share for a period of two years from the closing date (subject to acceleration). On April 10, 2017, Metalla closed an additional tranche of 1,454,000 units for gross aggregate proceeds of CAD$727,000.

New Luika Gold Mine Stream

On May 16, 2017, Metalla acquired a 15% interest in Silverback Limited (“Silverback”). Silverback is a privately held Guernsey-based investment company that solely owns 100% of the New Luika Gold Mine silver stream which it purchased to provide the operator with construction financing for the underground mine transition. Details of the transaction include as follows: Metalla, through its ownership interest in Silverback, receives 15% of the silver produced from the New Luika Gold Mine operation under a silver streaming agreement, silver is purchased at 10% of spot (example US$1.80 per ounce at US$18 silver) upon delivery, and the stream continues through 2026. The New Luika Gold Mine is located in the Chunya Administrative District, Mbeya region in the Lupa Goldfield of southwest Tanzania, the second largest gold producing region in Tanzania in the 1900s. The property covers one prospecting license covering 49 km² and three mining licenses covering 16 km². The mine was Commissioned in August 2012 with new elution and electrowinning plant installed in the second quarter of 2014 and new crusher plant commissioned in September 2014. The processing facility uses a conventional three stage crushing, two mills in parallel and a carbon in leach operation.

Acquisition of Royalty and Streaming Portfolio from Coeur

On July 31, 2017 Metalla purchased a portfolio of 3 Royalties and 1 Stream from Coeur in exchange for a total of 14,546,597 Common Shares and an unsecured convertible debenture in the principal amount of US$6,677,475.63 (the “Convertible Debenture”). The Convertible Debenture included terms to automatically convert into Common Shares of Metalla at future financings or asset acquisitions to maintain Coeur’s 19.9% interest until the outstanding principal was either converted in full or otherwise repaid. The Convertible Debenture was unsecured and bore interest at a rate of 5% per annum. The Convertible Debenture was fully converted by Coeur on February 17, 2019.

- 8 -

The portfolio included the following:

Endeavor Silver Stream– Silver stream over the Endeavor Mine located in North-central New South Wales, Australia and once the region’s largest zinc, lead and silver producer. Commissioned in 1983 as the Elura Mine, the site has been operated by CBH since 2003 at which time the site was renamed Endeavor. The Endeavor orebody is similar to others in the Cobar Basin in that it has the form of massive vertical pillars. Extraction of some 30 million tonnes of ore has occurred with remaining reserves expected to support production out to December 2020. Metalla has the right to buy 100% of the silver production up to 20.0 million ounces from the Endeavor Mine for an operating cost contribution of USD$1.00 for each ounce of payable silver, indexed annually for inflation, plus a further increment of 50% of the silver price when the market price of silver exceeds USD $7.00 per ounce. SeeMaterial Assetssection for further information.

Joaquin Project– a 2% NSR Royalty on the Joaquin Property. The Joaquin Property was purchased by Pan American for US$25 million in January 2017. The project is composed of seven contiguous claims, totaling 28,660 hectares. It is located in the Santa Cruz Province, Argentina, approximately 145 kilometers from Pan American’s Manantial Espejo mine, where the Joaquin ore is planned to be processed. SeeMaterial Assetssection for further information.

Zaruma Gold Mine– a 1.5% NSR Royalty on the the Zaruma Gold Mine which is Core Gold’s flagship project and is located in the Zaruma-Portovelo Mining District of southern Ecuador, 3km north of the town of Zaruma. This district is a significant, high-grade goldfield, having produced over 5 million ounces of gold historically.

Puchuldiza Project– a 1.5% NSR Royalty on the Puchuldiza Project in Chile. In May of 2019, due to a failure of Regulus Resources Inc. to maintain the mining concessions in good standing, Metalla acquired 9 mining concessions underlying the 1.5% NSR Royalty for CAD$100,000 and subsequently extinguished the 1.5% NSR Royalty. Metalla currently holds 5 of the concessions in good standing and allowed 4 of the concessions to lapse.

Akasaba West Royalty

On May 14, 2018, Metalla acquired a 2% NSR Royalty on the Akasaba West Property. The Akasaba West Property is a gold-copper deposit located in the Bourlamaque and Louvicourt Townships, Val d’Or, Quebec. The Akasaba West Property is owned and operated by Agnico Eagle Mines Limited (“Agnico”). Agnico acquired the project in 2014 and has continued previous permitting and development activities, with a view to commencing mining activities in 2020.

Agnico will maintain its buy-back right of 1% for USD$7 million, and the Royalty will be payable after gold production on the claims comprising the property has exceeded 210,000 ounces.

Completion of Arrangement with ValGold Resources Ltd.

On July 31 2018, Metalla completed a plan of arrangement to acquire all outstanding common shares of ValGold which holds the Garrison Royalty (seeGarrison Royaltysection below for additional information)and an exploration and evaluation project. Under the terms of the arrangement, shareholders of ValGold received 0.1667 Common Shares for each ValGold common share. On the closing of this arrangement the following occurred:

- Metalla issued 9,659,973 Common Shares in exchange for common shares and in-the-money stock options of ValGold; and

- 9 -

- Outstanding Share purchase warrants of ValGold became exercisable to acquire up to 2,616,831 Common Shares at CAD$0.60 per Common Share, expiring October 6, 2019.

Garrison Royalty

As a result of the acquisition of ValGold, Metalla acquired a 2% NSR Royalty on a significant portion of the Garrison Project previously 100% owned by Osisko Mining Inc. (“Osisko”), including the claims which were the subject of an NI 43-101 compliant resource estimate in 2014. The Garrison Project is situated directly on the prolific Destor-Porcupine Fault Zone host to numerous gold mines. The Royalty covers the Garrcon, JonPol, and eastern portion of the 903 deposit. Osisko took over the Garrison Project in December 2015 when it acquired Northern Gold Mining Inc. and announced the start of a 20,000 metre drill program in July 2016. To-date, it has drilled 85,000 metres and made 11 announcements of drill results (the most recent on January 31, 2018) on all three main deposits on the property. On July 5, 2019, Osisko completed a plan of arrangement whereby the Garrison gold project was transferred via spin out to O3 Mining Corporation.

Loan Agreements

On November 7, 2018, Metalla entered into loan agreements with a syndicate of arm’s length lenders (the “SyndicateLenders”) for aggregate principal amount of US$1,750,000 (the “SyndicateLoan”). The proceeds from the Syndicate Loan were used to pay, in part, the US$6 million cash portion of the acquisition price for the 2% NSR Royalty on the Santa Gertrudis Property (see sections titledSanta Gertrudis RoyaltyandMaterial Assets for further information). Terms of the Syndicate Loan included interest at a rate of 5.0% per annum, calculated annually, and a term of twelve months. As an inducement for providing the Syndicate Loan, Metalla agreed to provide the Syndicate Lenders an origination discount of US$52,500 in total and, to issue an aggregate of 525,000 non-transferable Common Share purchase warrants (the “Loan Warrants”). Each Loan Warrant entitles the holder to acquire one Common Share at an exercise price of CAD$0.85 for a period of two years.

On December 11, 2018, Metalla increased the Syndicate Loan by US$250,000 (the “Syndicate Loan Increase”). In connection with this increase, Metalla agreed to issue an aggregate of 75,000 non-transferable Common Share purchase warrants with each warrant entitling the holder to one Common Share of Metalla at an exercise price of CAD$0.85 for a period of two years.

On August 7, 2019, Metalla fully paid the amounts owing under the Syndicate Loan upon the initial drawdown of the Beedie Loan (seeEstablishment of the CAD$12,000,000 Convertible Loan Facility section below) and no amounts remain outstanding under the Syndicate Loan.

Santa Gertrudis Royalty

On November 7, 2018, Metalla acquired 2% NSR Royalty over the Santa Gertrudis Property located north of Hermosillo in Sonora, Mexico, for US$12 million, 1% of which can be bought back at any time for US$7.5 million. Agnico acquired the property for US$80 million (CAD$105 million) in cash in November of 2017. The property produced over 550,000 ounces of gold in the 1990’s at an average head grade of 2.13 g/t gold. SeeMaterial Assetssectionfor further information

COSE Royalty

On December 20, 2018, Metalla acquired a 1.5% NSR Royalty on certain mining rights located on the Cap-Oeste Sur East property located in the province of Santa Cruz, Argentina for a purchase price of USD$1.5 million cash (partially funded by the Syndicate Loan Increase). Metalla also received a right of first refusal in favour of Metalla to acquire a future net smelter returns royalty that may be granted by, or received by, the seller (or an affiliate) on its Cap-Oeste mine.

- 10 -

The COSE Property is a gold and silver project located in the province of Santa Cruz, Argentina that is 100% owned by Minera Triton Argentina S.A., a wholly-owned subsidiary of Pan American. The COSE Property is a fully-permitted mine that has been developed at a total cost of USD$23.9 million, since Pan American acquired the property from Patagonia Gold for USD$15 million in May 2017. SeeMaterial Assetssection for further information.

Completion of Private Placement

Metalla completed a private placement of 8,748,808 units in two tranches on December 21, 2018 and January 4, 2019 for aggregate gross proceeds of C$6,824,070. Each unit consisted of one Common Share and one half of one Common Share purchase warrant at price of C$0.78 per unit. Each warrant entitles the holder thereof to acquire one Common Share of the Company at a price of C$1.17 for a period of 24 months from the closing date of each tranche as applicable (subject to acceleration). This offering was led by Haywood Securities Inc., on behalf of a syndicate of agents, including PI Financial Corp. and Canaccord Genuity Corp. The net proceeds from this private placement are being used to finance Royalty and Stream acquisitions and for general and working capital purposes.

Acquisition of Fifteen Mile Stream Royalty

On February 12, 2019 Metalla acquired a 1% NSR Royalty on Atlantic Gold Corporation’s (“Atlantic Gold”) Fifteen Mile Stream Project for US$4,000,000 pursuant to a Royalty purchase agreement dated February 4, 2019. On July 19, 2019, Atlantic Gold was subsequently acquired by St. Barbara Limited. (“St. Barbara”). The Fifteen Mile Stream Project is a gold project located 57km northeast of Atlantic Gold’s central milling facility at Touquoy and is readily accessible by highway. The project lies along the same geological trend as other related deposits – Touquoy, Beaver Dam and Cochrane Hill – and all are hosted within the same critical stratigraphy and structure, over a strike length of 80 km. The purchase price was satisfied by an upfront payment of US$2,200,000 in cash and 2,619,000 Common Shares. The Royalty is in connection with two claims which cover the Egerton-Maclean, Hudson, 149 East Zone, and the majority of the Plenty deposit which collectively comprise the Fifteen Mile Stream Project located in Nova Scotia, Canada. The Royalty covers all products mined or otherwise recovered from the Fifteen Mile Stream Project. For further details seeMaterial Assetssection below.

Acquisition of Alamos Royalty Portfolio – First Closing

On April 1, 2019, Metalla entered into an asset purchase agreement with Alamos Gold Inc. (together with its affiliates, “Alamos”) for the acquisition of a Royalty portfolio of up to 18 NSR Royalties or options to acquire NSR Royalties including, but not limited to, the following assets:

El Realito Royalty– 2% NSR Royalty on the El Realito Property which is owned and operated by Agnico located adjacent to its operating La India Mine. El Realito is a satellite deposit located adjacent to Agnico’s operating La India Mine in Sonora, Mexico. Agnico can buyback 1% of the Royalty for US$4 million at any time and holds a 60-day right of first refusal on the sale of the 2% Royalty. SeeMaterial Assetssection for further information.

Wasamac Royalty– 1.5% NSR Royalty on the Wasamac Mine currently under development by Monarch Gold Corporation (“Monarch”) located 15km west of Rouyn-Noranda in Quebec; Monarch has the right to buy back 0.5% of the NSR Royalty for a one-time payment of CAD$7.5 million at any time.

- 11 -

La Fortuna Royalty Option– option to purchase a 1% NSR Royalty on the La Fortuna Mine currently under development by Minera Alamos Inc. located in Durango State, Mexico. Metalla has the option to purchase the 1% NSR Royalty from Alamos for US$0.6 million payable in cash or common shares at the option of Metalla for a period of two years.

Beaufor Royalty– 1% NSR Royalty on the producing underground Beaufor Mine operated by Monarch, located 20km northeast of Val d’Or, Quebec.

San Luis Royalty– 1% NSR Royalty on the San Luis property owned by SSR Mining Inc. (“SSR”) and located in the Ancash Department, central Peru.

The first closing occurred on April 17, 2019 and Metalla issued 8,219,009 Common Shares for the initial acquisition of 13 NSR Royalties and 2 options to purchase NSR Royalties. Certain Royalties in the portfolio were subject to rights of first refusal, consents, and future options at agreed to prices were to be acquired at a second or additional closings.

Establishment of the CAD$12,000,000 Convertible Loan Facility

On April 23, 2019, Metalla announced that it had entered into a convertible loan facility (the “BeedieLoan Facility”) of up to CAD$12.0 million (the “BeedieLoan”) with Beedie Capital (“Beedie”) to fund acquisitions of new Royalties and Streams. The Beedie Loan was funded by way of an initial advance of CAD$7.0 million within 90 days from closing, and the remaining CAD$5.0 million will be available for subsequent advances in minimum tranches of CAD$1.25 million. The initial drawdown of CAD$7.0 million occurred on August 7, 2019.

The Beedie Loan Facility carries an interest rate of 8.0% on advanced funds and 2.5% on standby funds available, with the principal payment due 48 months after the date the financing is completed (the “Closing Date”) and is secured by certain assets of Metalla. The Beedie Loan can be repaid with no penalty after 18 months and carries no warrant coverage. The principal amount of the Beedie Loan will be convertible at any time at the option of Beedie into Common Shares at a conversion price of CAD$1.39 per Common Share, representing a 25% premium to the 30-day volume weighted average price as of March 15, 2019. Common Shares acquired on conversion will be subject to a four-month plus one day hold period from the date of advance.

Subsequent Events to May 31, 2019

Alamos Royalty Portfolio – Second Closing

On June 20, 2019, Metalla entered into an amended and restated asset purchase agreement and completed a second closing for the purchase of the El Realito Royalty (which was subject to a 60 day right of first refusal by Agnico) and the Biricu Royalty. As consideration for the Biricu Royalty, Metalla issued 10,299 Common Shares. Metalla also agreed to purchase from Alamos a Royalty on the Orion gold-silver project (that was not part of the existing Alamos Royalty portfolio) owned by Minera Frisco S.A.B. C.V. located in Nayarit, Mexico at a future third closing.

Additional Fifteen Mile Stream Royalty

On August 16, 2019, Metalla acquired a 3.0% NSR Royalty the Plenty project, which forms part of St. Barbara’s Fifteen Mile Stream project, for CAD$2 million from a third-party in accordance with a purchase and sale agreement. As consideration for the transaction, Metalla made an upfront payment of CAD$0.5 million in cash, with an additional payment of up to CAD$1.5 million upon the exercise of the Royalty payor’s buy-back right to purchase two-thirds of the 3.0% NSR Royalty for a period of five years.

- 12 -

Other Royalties

For a list of Royalty interests held by Metalla and not described above, see the chart below under the sectionDescription of Business – Principal Product.

DESCRIPTION OF THE BUSINESS

Metalla is a publicly traded precious metals royalty and streaming company listed on the TSX-V. In the last three years, Metalla has deployed over C$70 million across 15 transactions amassing a portfolio of 45 Royalties and Streams. Metalla's portfolio provides exposure to established counterparties, including Agnico, Goldcorp, Pan American, CBH, SSR and St Barbara.

A royalty is a non-dilutive asset level perpetual interest in the underlying project that when in production provides topline cash relative to the percentage of the royalty. Depending on the nature of a royalty interest and the laws applicable to it and the project, the royalty holder is generally not responsible for, and has no obligation to contribute to operating or capital costs or environmental liabilities. An NSR Royalty is generally based on the value of production or net proceeds received by an operator from a smelter or refinery for the minerals sold. These proceeds are usually subject to deductions or charges for transportation, insurance, smelting and refining costs as set out in the agreement governing the terms of the royalty.

Principal Product

The principal products of Metalla are: (i) precious metals that it has agreed to purchase pursuant to Stream agreements that it has entered into with mining companies; and (ii) Royalty payments pursuant to Royalty agreements acquired by Metalla or entered into with mining companies. Metalla is focused on precious metal streams and royalties for gold and silver.

The Company’s material assets are its Stream and Royalty interests in the Endeavor Mine, Joaquin Mine, COSE Mine, and Santa Gertrudis Property.

The following table summarizes the Royalty and Stream interests that Metalla owns:

| Property | Operator | Location | Stage | Metal | Terms | |

| 1 | Endeavor Mine | CBH | NSW Australia | Production | Zn, Pb, Ag | Stream on 100% of Ag |

| 2 | Joaquin Mine | Pan American | Santa Cruz, Argentina | Development | Ag, Au | 2% NSR Royalty |

| 3 | Santa Gertrudis | Agnico | Sonora, Mexico | Development | Au | 2% NSR Royalty |

| 4 | Fifteen Mile Stream | St Barbara | Nova Scotia | Development | Au | 1% NSR Royalty |

| 5 | Fifteen Mile Stream | St Barbara | Nova Scotia | Development | Au | 3% NSR Royalty |

| 6 | COSE Mine | Pan American | Santa Cruz, Argentina | Development | Ag, Au | 1.5% NSR Royalty |

- 13 -

| Property | Operator | Location | Stage | Metal | Terms | |

| 7 | Garrison Mine | O3 Mining Corporation | Kirkland Lake, ON | Development | Au | 2% NSR Royalty |

| 8 | New Luika | Shanta Gold | Lupa Goldfields, Tanzania | Production | Au | Stream on 15% of Ag |

| 9 | Hoyle Pond Extension | Goldcorp | Timmins, Canada | Development | Au | 2% NSR, subject to 500Koz exemption |

| 10 | Zaruma | Core Gold | Ecuador | Development | Au | 1.5% NSR Royalty |

| 11 | Timmins West Extension | Tahoe Resources | Timmins, Canada | Development | Au | 1.5% NSR Royalty (subject to a 0.75% buyback) |

| 12 | Akasaba West | Agnico | Val d’Or, Canada | Development | Au, Cu | 2% NSR Royalty, payable after 210Koz Au |

| 13 | TVZ Zone | Goldcorp | Timmins, Canada | Development | Au | 2% NSR Royalty |

| 14 | Dufferin East | Resource Capital | Halifax, Canada | Development | Au | 1.0 % NSR Royalty |

| 15 | El Realito | Agnico | Sonora, Mexico | Development | Au | 2.0 % NSR Royalty |

| 16 | La Fortuna | Minera Alamos Inc. | Durango, Mexico | Development | Au | Option – 1.0 % NSR Royalty |

| 17 | Wasamac | Monarch | Rouyn-Noranda, Quebec | Development | Au | 1.5% NSR Royalty |

| 18 | Beaufor Mine | Monarch | Val d’Or, Quebec | Development | Au | 1.0% NSR Royalty |

| 19 | San Luis | SSR | Peru | Development | Au | 1.0% NSR Royalty |

| 20 | DeSantis Mine | Canadian Gold Miner | Timmins, Canada | Exploration | Au | 1.5% NSR Royalty |

| 21 | Bint Property | Glencore | Timmins, Canada | Exploration | Au | 2% NSR Royalty |

| 22 | Colbert/Anglo | Goldcorp | Timmins, Canada | Exploration | Au | 2% NSR Royalty |

| 23 | Montclerg | IEP | Timmins, Canada | Exploration | Au | 1% NSR Royalty |

| 24 | Pelangio Poirier | Pelangio Exp. | Timmins, Canada | Exploration | Au | 1% NSR Royalty |

- 14 -

| Property | Operator | Location | Stage | Metal | Terms | |

| 25 | DNA | Detour Gold | Cochrane, Canada | Exploration | Au | 2% NSR Royalty |

| 26 | Beaudoin | Explor Resources | Timmins, Canada | Exploration | Au, Ag | 0.4% NSR |

| 27 | Sirola Grenfell | Golden Peak Res. | Kirkland Lake, Canada | Exploration | Au | 0.25% NSR Royalty |

| 28 | Mirado Mine | Orefinders | Kirkland Lake, Canada | Exploration | Au | 1% NSR Royalty + Option |

| 29 | Solomon’s Pillar | Sage Gold | Greenstone, Canada | Exploration | Au | 1% NSR Royalty |

| 30 | Puchuldiza | Not Applicable | Chile | Exploration | Au | 1.5% NSR Royalty1 |

| 31 | Los Patos | Private Party | Venezuela | Exploration | Au | 1.5% NSR Royalty |

| 32 | Big Island | Copper Reef Mining | Flin Flon, Manitoba | Exploration | Au | 2% NSR Royalty |

| 33 | Biricu | Guerrero Ventures | Guerrero, Mexico | Exploration | Au | 2% NSR Royalty |

| 34 | Boulevard | Independence Gold | Yukon, Ontario | Exploration | Au | 1% NSR Royalty |

| 35 | Camflo Northwest | Monarch | Val d’Or, Quebec | Exploration | Au | 1% NSR Royalty |

| 36 | Edwards Mine | Waterton | Wawa, Ontario | Exploration | Au | 1.25% NSR Royalty |

| 37 | Goodfish Kirana | War Eagle Mining | Kirkland Lake, Ontario | Exploration | Au | 1% NSR Royalty |

| 38 | Kirkland-Hudson | Kirkland Lake Gold | Kirkland Lake, Ontario | Exploration | Au | 2% NSR Royalty |

| 39 | Pucarana | Buenaventura | Peru | Exploration | Au | Option – 1.8% NSR Royalty |

| 40 | Capricho | Pucara Resources | Peru | Exploration | Au | 1% NSR Royalty |

| 41 | Lourdes | Pucara Resources | Peru | Exploration | Au | 1% NSR Royalty |

| 42 | Santo Tomas | Pucara Resources | Peru | Exploration | Au | 1% NSR Royalty |

| 43 | Guadalupe/Pararin | Pucara Resources | Peru | Exploration | Au | 1% NSR Royalty |

- 15 -

| Property | Operator | Location | Stage | Metal | Terms | |

| 44 | Tower Mountain | Private Party | Canada | Exploration | Au | 2% NSR Royalty2 |

| 45 | Orion | Minera Frisco | Mexico | Exploration | Au, Ag | 2.75% NSR Royalty2 |

11.5% Royalty has subsequently been extinguished upon acquisition of the underlying concessions by Metalla. See headingGeneral Development of the Business – Current Business of Metalla - 3 Year History - Acquisition of Royalty and Streaming Portfolio from Coeur above.

2Under contract to be acquired.

Further details regarding the purchase agreements entered into by Metalla in respect of certain Stream and Royalty acquisition agreements with respect to development or production properties can be found under the sectionGeneral Development of the Business above.

Competitive Conditions

Metalla will compete with other companies that operate in the stream and royalty market segment to acquire Streams and Royalties. Metalla will also compete with companies that provide financing to mining companies. Metalla also competes with other precious metals focused companies for capital and human resources. See sectionDescription of the Business – Risk Factors – Competition.

Components

Metalla expects to purchase or acquire Royalties or Streams as previously described above under sectionDescription of the Business.

Employees

As at the date of this AIF, Metalla has a total of 3 full time and 5 part time employees. No management functions of Metalla are performed to any substantial degree by persons other than the directors and executive officers of the Company.

Foreign Operations

Metalla currently purchases or expects to purchase precious or other metals or receives or expects to receive payments under Royalties from mines or operations in Australia, Argentina, Mexico, Canada, Tanzania, Ecuador, Peru, and Chile. Metalla may in the future purchase precious metals or receive payments under Royalties from mines or operations in other countries. Changes in legislation, regulations or governments in such countries are beyond Metalla’s control and could adversely affect the Company’s business. The effect of these factors cannot be predicted with any accuracy by Metalla or its management. See sectionDescription of the Business – Risk Factors – International Interests in this AIF.

RISK FACTORS

Investors should carefully consider all of the information disclosed in this AIF prior to investing in the securities of Metalla. In addition to the other information presented in this AIF, the following risk factors should be given special consideration when evaluating an investment in such securities. These risk factors could materially affect Metalla’s future operating results and could cause actual events to differ materially from those described in forward-looking statements relating to Metalla. The risk factors described in this AIF are not the only risks that Metalla faces. Additional risks or uncertainties that Metalla does not have any knowledge of or are currently deemed as immaterial, could also materially adversely affect Metalla.

- 16 -

Risks Relating to Metalla

Changes in Commodity Prices that underlie Royalty, Stream or Other Interests

The price of Metalla’s Common Shares may be significantly affected by declines in commodity prices. The revenue derived by Metalla from its asset portfolio will be significantly affected by changes in the market price of commodities that underlie the Royalty, Stream or other investments or interests of Metalla. Metalla’s revenue is particularly sensitive to changes in the price of gold and silver. The cash flow derived from the Endeavor Mine and New Luika Gold Mine Streams is 100% dependent on the future price of silver. The price of gold, silver and other commodities fluctuates daily and are affected by factors beyond the control of Metalla, including levels of supply and demand, industrial development, inflation and interest rates, the U.S. dollar’s strength and geo-political events. External economic factors that affect commodity prices can be influenced by changes in international investment patterns, monetary systems and political developments.

All commodities, by their nature, are subject to wide price fluctuations and future material price declines will result in a decrease in revenue and may cause a suspension or termination of production by relevant operators, which would result in a complete cessation of revenue from applicable Royalties, Streams or working interests. Even if Metalla worked to ensure a diversification of commodities that underlie its Royalties and Streams, the commodity market trends are cyclical in nature and a general downturn in commodity prices could result in a significant decrease in overall revenue.

Metalla Has No Control Over Mining Operations

Metalla is not directly involved in the operation of mines. The revenue Metalla may derive from its portfolio of Royalty and Stream assets is based entirely on production from third-party mine owners and operators. Metalla is party to precious metal purchase agreements to purchase a certain percentage of precious metals or other metals produced by certain mines and operations and Metalla expects to receive payments under Royalty agreements based on production from certain mines and operations, however, Metalla will not have a direct interest in the operation or ownership of those mines and projects. The owners and operators generally will have the power to determine the manner in which the properties are exploited, including decisions to expand, continue or reduce, suspend or discontinue production from a property, decisions about the marketing of products extracted from the property and decisions to advance exploration efforts and conduct development of non-producing properties. The interests of third-party owners and operators and those of Metalla in respect of a relevant project or property may not always be aligned. The inability of Metalla to control the operations for the properties in which it has a Royalty, Stream or other interest may result in a material adverse effect on the profitability of Metalla, the results of operations of Metalla and its financial condition. Except in a limited set of circumstances as may be specified in a specific Stream or Royalty, Metalla will not receive compensation if a specific mine or operation fails to achieve or maintain production or if the specific mine or operation is closed or discontinued. In addition, a number of mining operations in respect of which Metalla holds a Royalty or Stream interest (“Mining Operations”) are currently in exploration stage and may not commence commercial production and there can be no assurance that if such operations do commence production that they will achieve profitable and continued production levels. In addition, the owners or operators may take action contrary to policies or objectives of Metalla; be unable or unwilling to fulfill their obligations under their agreements with Metalla; have difficulty obtaining or be unable to obtain the financing necessary to move projects forward; or experience financial, operational or other difficulties, including insolvency, which could limit the owner or operator’s ability to perform its obligations under arrangements with Metalla. Metalla is also subject to the risk that a specific mine or project may be put on care and maintenance or have its operations suspended, on both a temporary or permanent basis.

- 17 -

The owners or operators of the projects or properties in which Metalla holds a Royalty or Stream interest may from time to time announce transactions, including the sale or transfer of the projects or of the operator itself, over which Metalla has little or no control. If such transactions are completed it may result in a new operator controlling the project, who may or may not operate the project in a similar manner to the current operator which may positively or negatively impact Metalla. If any such transaction is announced, there is no certainty that any such transaction will be completed, or completed as announced, and any consequences of such non-completion on Metalla may be difficult or impossible to predict.

Metalla is subject to the risk that Mining Operations may shut down on a temporary or permanent basis due to issues including but not limited to economic conditions, lack of financial capital, flooding, fire, weather related events, mechanical malfunctions, community or social related issues, social unrest, the failure to receive permits or having existing permits revoked, collapse of mining infrastructure including tailings ponds, expropriation and other risks. These issues are common in the mining industry and can occur frequently. There is a risk that the carrying values of Metalla’s assets may not be recoverable if the mining companies operating the Mining Operations cannot raise additional finances to continue to develop those assets. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in the Mining Operations becoming uneconomic resulting in their shutdown and closure. Metalla is not entitled to purchase gold, other commodities, receive royalties or other economic benefit from the Mining Operations if no gold or other commodities are produced from the Mining Operations.

Variations in Foreign Exchange Rates

The operations of Metalla are subject to foreign currency fluctuations and inflationary pressures, which may have a material adverse effect on the profitability of Metalla, its result of operations and financial condition. There can be no assurance that the steps taken by management to address such fluctuations will eliminate the adverse effects and Metalla may suffer losses due to adverse foreign currency fluctuations.

Delay Receiving or Failure to Receive Payments

Metalla is dependent to a large extent upon the financial viability and operational effectiveness of owners and operators of the relevant mines and mineral properties underlying Metalla’s Streams and Royalties. Payments from production generally flow through the operator and there is a risk of delay and additional expense in receiving such revenues. Payments may be delayed by restrictions imposed by lenders, delays in the sale or delivery of products, the ability or willingness of smelters and refiners to process mine products, recovery by the operators of expenses incurred in the operation of the Royalty or Stream properties, the establishment by the operators of reserves for such expenses or the insolvency of the operator. Metalla’s rights to payment under the Royalties/Streams must, in most cases, be enforced by contract without the protection of the ability to liquidate a property. This inhibits Metalla’s ability to collect amounts owing under its Royalties/Streams upon a default. Additionally, some agreements may provide limited recourse in particular circumstances which may further inhibit Metalla’s ability to recover or obtain equitable relief in the event of a default under such agreements. In the event of a bankruptcy of an operator or owner, it is possible that an operator may claim that Metalla should be treated as an unsecured creditor and, therefore, have a limited prospect for full recovery of revenue and a possibility that a creditor or the operator may claim that the Royalty or Stream agreement should be terminated in the insolvency proceeding. Failure to receive payments from the owners and operators of the relevant properties or termination of Metalla’s rights may result in a material and adverse effect on Metalla’s profitability, results of operations and financial condition.

- 18 -

Third-Party Reporting

Metalla relies on public disclosure and other information regarding specific mines or projects that is received from the owners or operators of the mines or other independent experts. The information received may be susceptible to being imprecise as the result of it being compiled by certain third parties. The disclosure created by Metalla may be inaccurate if the information received contains inaccuracies or omissions, which could create a material adverse effect on Metalla. Further, Metalla must rely on the accuracy and timeliness of the public disclosure and other information it receives from the owners and operators of the Mining Operations, and uses such information in its analyses, forecasts and assessments relating to its own business and to prepare its disclosure with respect to the Streams and Royalties. If the information provided by such third parties to Metalla contains material inaccuracies or omissions, the Company’s disclosure may be inaccurate and its ability to accurately forecast or achieve its stated objectives may be materially impaired, which may have a material adverse effect on Metalla.

In addition, a Royalty or Stream agreement may require an owner or operator to provide Metalla with production and operating information that may, depending on the completeness and accuracy of such information, enable Metalla to detect errors in the calculation of Royalty or Stream payments that it receives. As a result, the ability of Metalla to detect payment errors through its associated internal controls and procedures is limited, and the possibility exists that Metalla will need to make retroactive revenue adjustments. Of the Royalty or Stream agreements that Metalla enters into, some may provide Metalla the right to audit the operational calculations and production data for associated payments; however, such audits may occur many months following the recognition by Metalla of the applicable revenue and may require Metalla to adjust its revenue in later periods.

As a holder of an interest in a Royalty or Stream, Metalla will have limited access to data on the operations or to the actual properties underlying the Royalty or Stream. This limited access to data or disclosure regarding operations could affect the ability of Metalla to assess the performance of the Royalty or Stream. This could result in delays in cash flow from that which is anticipated by Metalla based on the stage of development of the properties covered by the assets within the portfolio of Metalla.

Disclosure Regarding Operations

Some Royalties or Streams may be subject to confidentiality arrangements which govern the disclosure of information with regard to the Royalty or Stream and, as such, Metalla may not be in a position to publicly disclose non-public information with respect to certain Royalties or Streams. The limited access to data and disclosure regarding the operations of the properties in which Metalla has an interest, may restrict the ability of Metalla to enhance its performance which may result in a material and adverse effect on the profitability of Metalla, results of operations for Metalla and financial condition. There can be no assurance that Metalla will be successful in obtaining these rights when negotiating the acquisition of Royalties or Streams.

Strategy for Acquisitions

As Metalla executes on its business plan it intends to seek to purchase additional Royalties and Streams from third parties. Metalla cannot offer any assurance that it can complete any acquisition or proposed business transactions on favourable terms or at all, or that any completed acquisitions or proposed transactions will benefit Metalla.

- 19 -

At any given time Metalla may have various types of transactions and acquisition opportunities in various stages of review, including submission of indications of interest and participation in discussions or negotiations in respect of such transactions. This process also involves the engagement of consultants and advisors to assist in analyzing particular opportunities. Any such acquisition or transaction could be material to Metalla and may involve the issuance of securities by Metalla to fund any such acquisition. Any such issuance of securities may result in substantial dilution to existing shareholders and may result in the creation of new control positions. In addition, any such acquisition or other Royalty or Stream transaction may have other transaction specific risks associated with it, including risks related to the completion of the transaction, the project operators or the jurisdictions in which assets may be acquired.

Additionally, Metalla may consider opportunities to restructure its Royalties or Streams where it believes such a restructuring may provide a long-term benefit to Metalla, even if such restructuring may reduce near-term revenues or result in Metalla incurring transaction related costs. Metalla may enter into one or more acquisitions, restructurings or other Royalty and Streaming transactions at any time.

Metalla Cash Flow Risk

Metalla is not directly involved in the ownership or operation of mines. Metalla’s Royalty, Stream and other interests in properties or projects are subject to most of the significant risks of the operating mining company. Metalla’s cash flow is dependent on the activities of third parties which could create risk that those third parties may, have targets inconsistent to Metalla’s targets, take action contrary to Metalla’s goals, policies or objectives, be unwilling or unable to fulfill their contractual obligations owed to Metalla, or experience financial, operational or other difficulties or setbacks, including bankruptcy or insolvency proceedings, which could limit a third-party’s ability to perform under a specific third-party arrangement. Specifically, Metalla could be negatively impacted by an operator’s ability to continue its mining operations as a going concern and have access to capital. A lack of access to capital could result in a third-party entering a bankruptcy proceeding, which would result in Metalla being unable to realize any value for its Stream, Royalty or other interest.

Rights of other Interest-Holders

Some Royalty and Stream interests are subject to: (i) buy-down right provisions pursuant to which an operator may buy-back all or a portion of the Royalty or Stream, (ii) pre-emptive rights pursuant to which certain parties have the right of first refusal or first offer with respect to a proposed sale or assignment of a Royalty or Stream to Metalla, or (iii) claw back rights pursuant to which the seller of a Royalty or Stream to Metalla has the right to re-acquire the Royalty or Stream. Holders may exercise these rights such that certain Royalty and Stream interests would no longer be held by Metalla. Any compensation received as a result may be significantly less than Metalla had budgeted receiving for the applicable Royalty or Stream and may have a material adverse effect on Metalla’s income and business.

Defects in Royalties and Streams

A defect in the Royalties and Streams and/or the underlying contract may arise to defeat or impair the claim of Metalla to such Royalty or Stream.

Change in Material Assets

As at the date of this AIF, the Endeavor Mine Stream, Joaquin Mine Royalty, COSE Mine Royalty, and Santa Gertrudis Gold Royalty are currently material assets to Metalla, although as new assets are acquired or move into production, the materiality of each of the assets of Metalla will be reconsidered. Any adverse development affecting the operation of, production from or recoverability of mineral reserves from the Endeavor Mine, Joaquin Mine, COSE Mine, and Santa Gertrudis Property, or any other significant property in the asset portfolio from time to time, such as, but not limited to, unusual and unexpected geologic formations, seismic activity, rock bursts, cave-ins, flooding and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to life or property, environmental damage, or the inability to hire suitable personnel and engineering contractors or secure supply agreements on commercially suitable terms, may have a material adverse effect on the profitability of Metalla, the financial condition of Metalla and results of its operations.

- 20 -

Dependence on Key Personnel

Metalla is dependent on the services of a small number of key management personnel. The ability of Metalla to manage its activities and its business will depend in large part on the efforts of these individuals. There can be no assurance that Metalla will be successful in engaging or retaining key personnel. The loss of the services of a member of the management of Metalla could have a material adverse effect on the Company. From time to time, Metalla may also need to identify and retain additional skilled management and specialized technical personnel to efficiently operate its business. The number of persons skilled in the acquisition of Royalties and or Streams is limited and competition for such persons is intense. Recruiting and retaining qualified personnel is critical to the success of Metalla and there can be no assurance that Metalla will be successful in recruiting and retaining the personnel it needs to successfully operate its business. If Metalla is not successful in attracting and retaining qualified personnel, the ability of Metalla to execute on its business model and strategy could be affected, which could have a material and adverse impact on its profitability, results of operations and financial condition.

Dividends

Payment of dividends on Metalla’s securities is within the discretion of Metalla’s board of directors and will depend upon Metalla’s future earnings, cash flows, acquisition capital requirements and financial condition, and other relevant factors. Although Metalla currently pays a regular dividend, there can be no assurance that it will be in a position to continue to declare dividends in the future due to the occurrence of one or more of the risks described herein.

Competition

Metalla will compete with other companies for Streams and Royalties. Other companies may have greater resources than Metalla. Any such competition may prevent Metalla from being able to secure new Streams or acquire new Royalties. Future competition in the royalty and streaming sector could materially adversely affect Metalla’s ability to conduct its business. There can be no assurance that Metalla will be able to compete successfully against other companies in acquiring new Royalty and or Stream interests. In addition, Metalla may be unable to acquire Royalties or Streams at acceptable valuations which may result in a material and adverse effect on Metalla’s profitability, results of operations and financial condition.

Project Operators may not Respect Contractual Obligations

Royalty, Stream and other interests in properties or projects are contractual in nature. Parties to contracts do not always honour contractual terms and contracts themselves may be subject to interpretation or technical defects. To the extent grantors of Royalties, Stream and other interests do not abide by their contractual obligations, Metalla may be forced to take legal action to enforce its contractual rights. Such litigation may be time consuming and costly and there is no guarantee of success. Further, any such litigation may also be required to be pursued in foreign jurisdictions. Any pending proceedings or actions or any decisions determined adversely to Metalla, may have a material and adverse effect on Metalla’s profitability, results of operations, financial condition and the trading price of the Common Shares of Metalla.

- 21 -

Enforceability

The status of Royalties at law can be uncertain and varies from jurisdiction to jurisdiction and in certain jurisdictions a Royalty may not be a registrable interest which runs with the land. As a result it may be difficult for Metalla to enforce its rights with respect to Royalties against a third party. Such a failure may result in the loss of the Company’s rights to such a Royalty in the event a third party assigns title to the underlying property.

Conflicts of Interest

Certain directors and officers of Metalla also serve as directors and/or officers of other companies that are involved in natural resource explorations, development and mining operations, including Paladin Energy Ltd., Argosy Minerals Ltd., Azarga Metals Corp., Atico Mining Corporation, Auramex Resources Corp, Mountain Boy Minerals Ltd., Romios Gold Resources Ltd., Thunderstruck Resources Ltd., Galena Mining Ltd., Crystal Lake Mining Corp., Comet Resources Limited, Tempus Resources Limited, Amwolf Capital Corp. and Palladium One Mining Inc., and consequently there exists the possibility for such directors and officers to be in a position where there is a conflict of interest. Any decision made by any such directors and officers will be made in accordance with their duties and obligations to deal in good faith and in the best interests of Metalla and its shareholders. Each director that is in a conflict of interest is required to declare such conflict and abstain from voting on a matter in which that director is conflicted in accordance with applicable law.

Global Financial Conditions

Market events and conditions, including the disruptions in the international credit markets and other financial systems, in China, Japan and Europe, along with political instability in the Middle East and Russia and falling currency prices expressed in United States dollars have resulted in commodity prices remaining volatile. These conditions have also caused a loss of confidence in global credit markets, excluding the United States, resulting in the collapse of, and government intervention in, major banks, financial institutions and insurers and creating a climate of greater volatility, tighter regulations, less liquidity, widening credit spreads, less price transparency, increased credit losses and tighter credit conditions. Notwithstanding various actions by governments, concerns about the general condition of the capital markets, financial instruments, banks and investment banks, insurers and other financial institutions caused the broader credit markets to be volatile and interest rates to remain at historical lows. These events are illustrative of the effect that events beyond the Company’s control may have on commodity prices, demand for metals, including gold, silver, copper, lead and zinc, availability of credit, investor confidence, and general financial market liquidity, all of which may adversely affect the Company’s business. Global financial conditions have always been subject to volatility. Access to public financing has been negatively impacted by sovereign debt concerns in Europe and emerging markets, as well as concerns over global growth rates and conditions.

These factors may impact the ability of Metalla to obtain both debt and equity financing in the future and, if obtained, on terms favourable to Metalla. Increased levels of volatility and market turmoil can adversely impact the operations of Metalla and the value and the price of the Common Shares of the Company could be adversely affected.

- 22 -

Future Financing; Future Securities Issuances

There can be no assurance that Metalla will be able to obtain adequate financing in the future or that the terms of such financing will be favourable. Failure to obtain such additional financing could impede the funding obligations of Metalla or result in delay or postponement of further business activities which may result in a material and adverse effect on Metalla’s profitability, results of operations and financial condition. Metalla may require new capital to continue to grow its business and there are no assurances that capital will be available when needed, if at all. It is likely that, at least to some extent, such additional capital will be raised through the issuance of additional equity, which could result in dilution to shareholders.

Repayment of Current Credit Facility

Metalla’s credit facilities and financing agreements mature on various dates. There can be no assurance that such credit facilities or financing agreements will be renewed or refinanced, or if renewed or refinanced, that the renewal or refinancing will occur on equally favourable terms to Metalla. Metalla’s ability to continue operating may be adversely affected if Metalla is not able to renew its credit facilities or arrange refinancing, or if such renewal or refinancing, as the case may be, occurs on terms materially less favorable to Metalla than at present. Metalla’s current credit facilities and financing agreements impose covenants and obligations on Metalla. There is a risk that such loans may go into default if there is a breach in complying with such covenants and obligations, which could result in the lenders realizing on their security and causing the shareholders to lose some or all of their investment.

Litigation affecting Properties

Potential litigation may arise on a property on which Metalla holds or has a Royalty or Stream interest (for example, litigation between joint venture partners or between operators and original property owners or neighbouring property owners). Metalla will not generally have any influence on the litigation and will not generally have access to data. Any such litigation that results in the cessation or reduction of production from a property (whether temporary or permanent) could have a material and adverse effect on Metalla’s profitability, results of operations, financial condition and the trading price of the Common Shares of Metalla.

Changes in Tax Laws Impacting Metalla

There can be no assurance that new tax laws, regulations, policies or interpretations will not be enacted or brought into being in the jurisdictions where Metalla has interests that could have a material adverse effect on Metalla. Any such change or implementation of new tax laws or regulations could adversely affect Metalla’s ability to conduct its business. No assurance can be given that new taxation rules or accounting policies will not be enacted or that existing rules will not be applied in a manner which could result in the profits of Metalla being subject to additional taxation or which could otherwise have a material adverse effect on the profitability of Metalla, Metalla’s results of operations, financial condition and the trading price of the Common Shares of Metalla. In addition, the introduction of new tax rules or accounting policies, or changes to, or differing interpretations of, or application of, existing tax rules or accounting policies could make Royalties, Streams or other investments by Metalla less attractive to counterparties. Such changes could adversely affect the ability of Metalla to acquire new assets or make future investments.

Credit and Liquidity Risk

Metalla is exposed to counterparty risks and liquidity risks including, but not limited to: (i) through the companies with which Metalla has Streams and Royalty agreements with; (ii) through financial institutions that hold Metalla’s cash and cash equivalents; (iii) through companies that have payables to Metalla; (iv) through Metalla’s insurance providers; and (v) through Metalla’s lenders. Metalla is also exposed to liquidity risks in meeting its operating expenditure requirements in instances where cash positions are unable to be maintained or appropriate financing is unavailable. These factors may impact the ability of Metalla to obtain loans and other credit facilities in the future and, if obtained, on terms favourable to Metalla. Also, if these risks materialize, the Company’s operations could be adversely impacted and the trading price of its securities could be adversely affected.

- 23 -

Information Systems and Cyber Security

Metalla’s information systems, and those of its counterparties under the Streams and Royalties agreements and vendors, are vulnerable to an increasing threat of continually evolving cybersecurity risks. Unauthorized parties may attempt to gain access to these systems or Metalla’s information through fraud or other means of deceiving Metalla’s counterparties. Metalla’s operations depend, in part, on how well Metalla and its suppliers, as well as counterparties under the Streams and Royalties agreements, protect networks, equipment, information technology systems and software against damage from a number of threats. The failure of information systems or a component of information systems could, depending on the nature of any such failure, adversely impact Metalla’s reputation and results of operations. Although to date Metalla has not experienced any material losses relating to cyber-attacks or other information security breaches, there can be no assurance that Metalla will not incur such losses in the future. Metalla’s risk and exposure to these matters cannot be fully mitigated because of, among other things, the evolving nature of these threats. As a result, cyber security and the continued development and enhancement of controls, processes and practices designed to protect systems, computers, software, data and networks from attack, damage or unauthorized access remain an area of attention.

Activist Shareholders