Table of Contents

As filed with the Securities and Exchange Commission on February 23, 2022

File No. 000-56270

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 5

to

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

Pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934

Bitwise 10 Crypto Index Fund

(Exact name of registrant as specified in its charter)

| DELAWARE | 82-3002349 | |

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) |

400 Montgomery Street, Suite 600

San Francisco, CA 94111

(Address of principal executive offices and Zip Code)

(415) 968-1843

(Registrant’s telephone number, including area code)

Copies to:

Robert H. Rosenblum, Esq.

Wilson Sonsini Goodrich & Rosati P.C.

1700 K St NW

Washington, D.C. 20006

Securities registered pursuant to Section 12(b) of the Act: None.

Securities to be registered pursuant to Section 12(g) of the Act: Bitwise 10 Crypto Index Fund (BITW) Shares

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Table of Contents

| Page(s) | ||||

| i | ||||

| ii | ||||

| iii | ||||

| 1 | ||||

| 40 | ||||

| 85 | ||||

| 111 | ||||

Item 4. Security Ownership of Certain Beneficial Owners and Management. | 112 | |||

| 113 | ||||

| 122 | ||||

Item 7. Certain Relationships And Related Transactions, And Director Independence. | 123 | |||

| 126 | ||||

| 126 | ||||

| 127 | ||||

Item 11. Description Of Registrant’s Securities To Be Registered. | 127 | |||

| 131 | ||||

| 132 | ||||

Item 14. Changes In And Disagreements With Accountants On Accounting And Financial Disclosure. | 132 | |||

| 133 | ||||

Table of Contents

Bitwise 10 Crypto Index Fund (hereafter, the “Trust”, “we”, “us” or “our”) is filing this Amendment No. 4 to Registration Statement on Form 10 to register its common units of fractional undivided beneficial interest (“Shares”) pursuant to Section 12(g) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Once this Registration Statement is deemed effective, the Trust will be subject to the requirements of Regulation 13A under the Exchange Act, which will require it to file annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and to comply with all other obligations of the Exchange Act applicable to issuers filing Registration Statements pursuant to Section 12(g) of the Exchange Act.

The valuation methodology used to create the financial statements herein did not identify a principal market in accordance with Financial Accounting Standards Board Accounting Standards Codification 820-10 (“ASC 820”), which outlines the application of fair value accounting under accounting principles generally accepted in the United States of America (“U.S. GAAP”). All amounts referenced within this Registration Statement pertaining to NAV per Share, NAV of the Trust, and the fair values of the Trust’s investments in digital assets approximate fair value under U.S. GAAP but were determined without identifying a principal market. The use of this valuation methodology, however, resulted in a presentation of financial statements that were determined to be presented fairly in all material aspects with U.S. GAAP. The Trust determined that the previous valuation policy, which utilized a blended average approach for calculating the price of a digital asset instead of identifying a principal market for such digital asset, was not in keeping with the proper application of U.S. GAAP, specifically ASC 820, and, therefore, resulted in an immaterial error. In accordance with the Financial Accounting Standards Board Accounting Standards Codification 250 (“ASC 250”), the Trust corrected this immaterial error by making changes to the valuation policy and the financial statements in subsequent periods. Please see Footnote 3 - Calculation of Valuation, of the Trust’s December 31, 2020 audited financial statements included herein for further information.

We are filing this Amendment No. 5 to Registration Statement on Form 10 solely for the purpose of including the city and state in which the Report of the Independent Registered Public Accounting Firm was issued and the year WithumSmith+Brown, PC began serving as our auditor. No other changes have been made.

i

Table of Contents

CAUTIONARY NOTE ON FORWARD-LOOKING STATEMENTS

This Form 10 includes forward-looking statements. All statements other than statements of historical information provided herein are forward-looking and may contain information about financial results, economic conditions, trends and known uncertainties. Some of these forward-looking statements can be identified by the use of forward-looking terminology such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates,” or “anticipates” or the negative thereof or other variations thereof or comparable terminology, or by discussions of strategy, plans, intentions or unrealized investment results.

These statements involve risks, uncertainties, assumptions and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from the information expressed or implied by these forward-looking statements. Although we believe that we have a reasonable basis for each forward-looking statement contained in this registration statement, we caution you that these statements are based on a combination of facts and factors currently known by us and our projections of the future, about which we cannot be certain. Forward-looking statements in this registration statement include, but are not limited to, statements relating to the continued quotation of the Shares on the OTCQX; our expectations regarding regulatory developments affecting the Trust; our future financial performance; and the performance of the Bitwise 10 Crypto Index (the “Index”).

Such forward-looking statements are subject to numerous risks and are necessarily dependent on assumptions, data or methods that may be incorrect or imprecise and may not be realized. The Trust cautions the reader that actual results could differ materially from those expected by the Trust depending on the outcome of certain factors, including without limitation, changes in the U.S. economy, changes in the regulation of cryptocurrencies, and other important factors described in this registration state under the Item 1.A Risk Factors. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Industry experts may disagree with such analyses, forecasts and targets, the estimations and assumptions used in preparing the analyses, forecasts and targets or the Trust’s view or understanding of current or future events. No assurance, representation or warranty is made by any person that any of such analyses, forecasts and targets will be achieved and no investor should rely on such analyses, forecasts and targets. None of the Trust’s or any of their affiliates or any of their respective directors, managers, officers, employees, partners, shareholders, advisors or agents makes any assurance, representation or warranty as to the accuracy of any of such analyses, forecasts and targets. Nothing contained in this document may be relied upon as a guarantee, promise, assurance or a representation as to the future. The Trust undertakes no obligation to release the results of any revisions to these forward-looking statements which may be made to reflect events or circumstances after the date hereof, including without limitation, changes in the Trust’s business strategy or planned expenditures, or to reflect the occurrence of unanticipated events.

ii

Table of Contents

Our business is subject to numerous risks and uncertainties, including those highlighted in the section of this form titled “Risk Factors.” These risks include the following:

| • | investing in cryptocurrencies generally is speculative, and the Portfolio Crypto Assets of the Trust are subject to volatile price fluctuations which can negatively impact Shares of the Trust; |

| • | because the Portfolio Crypto Assets of the Trust are dependent, in part, on the continued market acceptance and development of crypto assets and blockchain technology by consumers, any declines or negative trends affecting crypto assets or blockchain technology will adversely affect the value of Shares of the Trust; |

| • | our relatively limited operating history makes it difficult to evaluate the Index, which is relatively new, and the Index Methodology, which is also relatively new, and may increase the risk that we will not be successful; |

| • | our business depends on the development and commercialization of the Index, which is a highly competitive industry, and the Trust may not be commercially successful; |

| • | any actual or perceived failure of the Portfolio Crypto Assets of the Trust to block malware or prevent failures or cyber security breaches or incidents could harm the reputation of the assets, and cause the assets to be perceived as insecure, exploitable, or unreliable, and otherwise negatively impact the value of the Shares of the Trust; |

| • | our risk management efforts may not be effective to prevent fraudulent or malicious activities by third-party providers or other parties, which could expose us to material financial losses and liability and lead to theft or loss of the Portfolio Crypto Assets; |

| • | our holdings of Portfolio Crypto Assets expose us to potential risks, including exchange, security and liquidity risks, which could negatively affect the value of the Shares of the Trust; |

| • | the value of the Trust’s cryptocurrencies are dependent, directly or indirectly, on prices established by exchanges and other trading venues, which are new and, in most cases, largely unregulated; |

| • | there are uncertainties related to the regulatory regimes governing blockchain technologies, cryptocurrencies, digital assets, and new regulations, interpretations or policies may materially adversely affect the value of Portfolio Crypto Assets and the Shares; |

| • | the blockchains on which ownership of Portfolio Crypto Assets are recorded are dependent on the efforts of third parties acting in their capacity as the blockchain transaction miners or validators, and if these third parties fail to successfully perform these functions, the operation of the blockchains that record ownership of Portfolio Crypto Assets could be compromised which could lead to loss or loss of the value of the Portfolio Crypto Assets; |

| • | for a variety of factors, the long-term viability of cryptocurrencies is unknown, and this could negatively impact the value of the Portfolio Crypto Assets and the commercial success of the Trust; |

| • | shareholders are expected to rely entirely on the Sponsor to conduct and manage the affairs of the Trust and will not be able to actively participate in management; and |

| • | the Trust is a passive investment vehicle and the Sponsor will generally not actively manage the cryptocurrencies held by the Trust; instead the Trust will hold investments that track the Index regardless of current or projected performance of the Index or of the actual Portfolio Crypto Assets held. |

iii

Table of Contents

Glossary

This glossary highlights some of the industry and other terms used elsewhere in this Registration Statement but is not a complete list of all the terms used herein. Each of the following terms has the meaning set forth below:

“Airdrops” – mean a method to promote the launch and use of new digital assets by providing a small amount of such new digital assets to the private wallets or exchange accounts that support the new digital asset and that hold existing related digital assets.

“Bitcoin” or “BTC” –means a type of crypto asset based on an open source cryptographic protocol existing on the Bitcoin network, comprising one type of the crypto assets underlying the Trusts’ Shares.

“Blockchain” –means the public transaction ledger of a crypto asset’s network on which transactions are recorded.

“Consensus Algorithm” – means the algorithm at the heart of the blockchain system that enforces that all ledgers converge over time.

“Crypto assets” – means a digital asset designed to work as a medium of exchange wherein individual coin ownership records are stored in a ledger, a computerized database using cryptography to secure transaction records, to control the creation of additional coins and to verify the transfer of coin ownership.

“Crypto asset network” –means the online, end user to end user network hosting the public transaction ledger, known as the Blockchain, and the source code comprising the basis for the cryptographic and algorithmic protocols governing the crypto asset’s network.

“Crypto asset exchanges” –means a dealer market, a brokered market, principal to principal market or exchange market on which crypto assets are bought, sold, and traded.

“Custodial Account” – means a segregated custody account to store private keys, which allow for the transfer of ownership or control of the Trust’s Portfolio Crypto Assets, on the Trust’s behalf. Under the Custodian Agreement, the Custodian controls and secures the Trust’s Custodial Account.

“Custodian fee” –means an annualized fee charged monthly that is a percentage of the Trust’s monthly assets under custody.

“Custodial Services” – means the services provided by the Custodian including, (i) allowing Portfolio Crypto Assets to be deposited from a public blockchain address to the Trust’s Custodial Account and (ii) allowing the Trust or Sponsor to withdraw Portfolio Crypto Assets from the Trust’s Custodial Account to a public blockchain address the Trust or Sponsor controls.

“Custodian” – means Coinbase Custody Trust Company, LLC. On behalf of the Trust, the Custodian holds the Portfolio Crypto Assets.

“DEX” – means “decentralized” exchange, where there is no central facilitator of trade and trading rules.

“Eligible Crypto Assets” – means those crypto assets that track the Bitwise 10 Large Cap Crypto Index.

“Emissions” – mean regular awards provided to holders of crypto assets in the form of crypto asset grants, and often in the form of the “gas” that powers transactions on the relevant crypto asset network.

“Extraordinary expenses” – extraordinary expenses are expenses outside of the Trust’s normal business operations which includes, but is not limited to, any non-customary costs and expenses including indemnification and extraordinary costs of the Administrator and Auditor, costs of any litigation or investigation involving Trust activities, and financial distress and restructuring and indemnification expenses.

iv

Table of Contents

“Hard fork” – occurs when there is a change in the set of rules governing a blockchain that makes it more restrictive than the previous set of rules in place.

“Index” – means the Bitwise 10 Large Cap Crypto Index.

“Index Components” – mean the Index is comprised of the top 10 coins selected and weighted by inflation adjusted market capitalization.

“Index Provider” – means Bitwise Index Services, LLC, an affiliate of the Trust that is controlled by the same parent entity as the Sponsor. The Index Provider administers the Index.

“Market-capitalization weighted” – means the top 10 cryptocurrencies in the Bitwise 10 Crypto Index are selected and held in proportion to their valuation.

“Miners” – means stakeholders that help process transactions and ensure that the distributed ledgers that make up a blockchain network stay consistent with one another.

“Mining” – means the act of solving computational puzzles through which transactions with cryptocurrencies are verified and added to the blockchain digital ledger in exchange for a crypto asset as a reward.

“NAV” – means net asset value.

“NAV of the Trust” – means the sum of the assets and liabilities of the Trust.

“NAV per share” – means the NAV of the Trust calculated on a per Share basis.

“Oracles” – means the reliable data source used by a blockchain application whenever it needs to interact with external data.

“Portfolio Crypto Assets” – means the group of selected cryptocurrencies that are held by the Trust.

“PoS” – means proof-of-stake and is a scheme miners can operate in to provide the mining service for the blockchain network and receive payment. PoS is a newer scheme that tries to avoid the heavy energy consumption that PoW systems typically require. PoS systems require miners to lock up and put at risk (aka, “stake”) a certain amount of the crypto asset associated with a given blockchain in order to process transactions. These staked assets are lost if a miner processes a transaction in a way that is fraudulent or violates the rules of the underlying blockchain.

“PoW” – means proof-of-work and is a scheme miners can operate in to provide the mining service for the blockchain network and receive payment. PoW is the first and most established scheme and involves computers solving complicated cryptographic puzzles that require a substantial amount of energy as a way of securing the network and processing transactions.

“Soft fork” – occurs when there is a change in the set of rules governing a blockchain that makes it less restrictive than the previous set of rules in place.

v

Table of Contents

History of the Trust and the Shares

The Bitwise 10 Crypto Index Fund (the “Trust”) is a Delaware Statutory Trust that issues common units of fractional undivided beneficial interest (“Shares”), which represent ownership in the Trust. The Trust was initially formed as a Delaware limited liability company on September 18, 2017 and commenced operations on November 22, 2017. The Trust has had several name changes since it was incorporated:

| • | Bitwise HODL 10 Private Index Fund, LLC |

| • | Bitwise HOLD 10 Private Index Fund, LLC |

| • | Bitwise 10 Private Index Fund, LLC |

On May 1, 2020, the Trust was converted to a Delaware statutory trust. The Trust’s current standing in Delaware is active. The Trust was formed by the filing of a Certificate of Trust with the Delaware Secretary of State in accordance with the provisions of the Delaware Statutory Trust Act (the “DSTA”) and the adoption of a Trust Agreement (the “Trust Agreement”). The Trust operates pursuant to the Trust Agreement.

Bitwise Investment Advisers, LLC is the Sponsor of the Trust (the “Sponsor”). Bitwise Asset Management, Inc. (“Bitwise”), the parent company of the Sponsor maintains a corporate website, www.bitwiseinvestments.com, which contains general information about the Trust and the Sponsor. The reference to the Bitwise website is an interactive textual reference only, and the information contained on the Bitwise website shall not be deemed incorporated by reference herein.

The Trust issues Shares, which represent common units of fractional undivided beneficial interest in, and ownership of, the Trust, on a periodic basis to certain “accredited investors” within the meaning of Rule 501(a) of Regulation D under the Securities Act. Shares purchased directly from the Trust are restricted securities that may not be resold except in transactions exempt from registration under the Securities Act and state securities laws and any such transaction must be approved in advance by the Sponsor. In determining whether to grant approval, the Sponsor will specifically look at whether the conditions of Rule 144 under the Securities Act and any other applicable laws have been met. Any attempt to sell Shares without the approval of the Sponsor in its sole discretion will be void ab initio. See “Description of Securities—Transfer Restrictions” for more information. The Shares are quoted on OTCQX under the ticker symbol “BITW.” Shares that have become unrestricted in accordance with Rule 144 under the Securities Act may trade on OTCQX. See “Description of Securities—Transfer Restrictions” for more detail.

The Trust’s principal investment objective is to invest in a portfolio (“Portfolio”) of cryptocurrencies (each, a “Portfolio Crypto Asset” and collectively, “Portfolio Crypto Assets”) that tracks the Bitwise 10 Large Cap Crypto Index (the “Index”) as closely as possible with certain exceptions determined by the Sponsor in its sole discretion, as described more fully below in the section entitled “Business of the Trust”. In addition, in the event the Portfolio Crypto Assets being held by the Trust present opportunities to generate returns in excess of the Index (for example, airdrops, emissions, forks, or similar network events) the Sponsor may also pursue these incidental opportunities on behalf of the Trust as part of the investment objective if in its sole discretion the Sponsor deems such activities to be possible and prudent.

The Trust believes that it has met its principal investment objective, however, because the Trust does not operate a redemption program for the Shares, because the holding period required under Rule 144 for the sale of the Shares purchased from the Trust, and because the Trust may from time to time halt Share subscriptions, there can be no assurance that the value of the Shares will reflect the value of the NAV per Share, and the Shares may trade at a substantial premium over, or a substantial discount to, the value of the NAV per Share, and as such, there can be no assurance that an investor will achieve a return on investment that tracks the performance of the Index. As of March 31, 2021, there was a correlation of 99.84% between the Portfolio Crypto Assets and the assets

1

Table of Contents

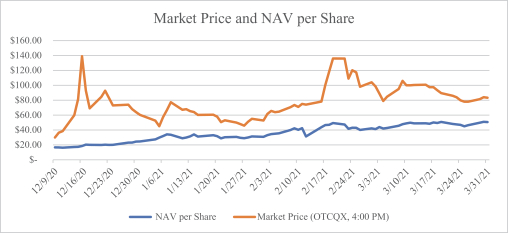

included in the Index. The Trust is aware that the market price of the Trust’s shares may deviate from the NAV of the Shares, that to date the Shares traded on the secondary market have not closely tracked the NAV of the Shares and that the market price of the Shares has been and may continue to be significantly above or below NAV per share. However, the Trust does not have control over an investor’s ability to achieve a return on investment that tracks the performance of the Index. The trading price of the Shares is determined by the market, and at times the Shares will trade at a premium or a discount to the NAV per share). Regardless of the Trust or Sponsor’s methods of managing the underlying portfolio, the price an investor will pay on the secondary market could differ significantly from the NAV per share. The Trust does not seek to track the performance of the trading of Shares on the secondary market and the trading price of Shares. The price an investor will pay on the secondary market may be significantly different from the NAV per Share. Furthermore, under Regulation M, the Trust, as the issuer of the Shares, is not legally permitted to take the types of actions that might help to reconcile the NAV per Share and the market price per Share.

The Shares may also trade at a substantial premium over, or a substantial discount to, the NAV per Share as a result of price volatility, trading volume and closings of the exchanges on which the Sponsor purchases Portfolio Crypto Assets on behalf of the Trust due to fraud, failure, security breaches or otherwise. As a result of the foregoing, the price of the Shares as quoted on OTCQX has varied significantly from the NAV per Share since the Shares were approved for quotation on December 9, 2020.

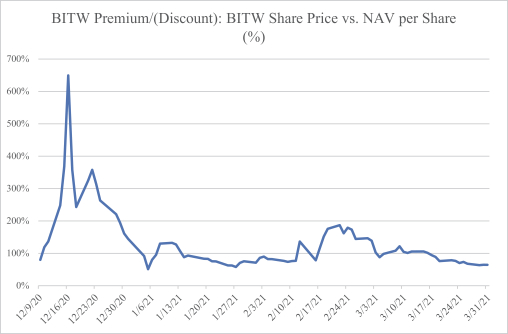

The following chart shows a comparison of the market price of the Shares as quoted on OTCQX and the NAV per share.

2

Table of Contents

From December 9, 2020 to March 31, 2021, the Shares of BITW traded at an average premium, based on closing prices at 4:00 p.m. ET New York time, and estimated, un-audited, NAV per share, of 104%. During that same period, the highest premium was 649% on December 16, 2020, and the lowest premium was 51% on January 5, 2021. The Shares have not traded at a discount, but they may do so in the future. Given the lack of an ongoing redemption program and the holding period under Rule 144, there is no arbitrage mechanism to keep the Shares closely linked to the value of the Trust’s underlying holdings which may continue to have an adverse impact on investments in the Shares.

The following chart shows a comparison of the cumulative returns of the Index compared to the NAV of the Trust:

3

Table of Contents

Emerging Growth Company Status

The Trust is an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For as long as the Trust is an emerging growth company, unlike other public companies, it will not be required to, among other things:

| • | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; or |

| • | comply with any new audit rules adopted by the PCAOB after April 5, 2012, unless the SEC determines otherwise. |

The Trust will cease to be an “emerging growth company” upon the earliest of (i) it having $1.0 billion or more in annual revenues, (ii) it becomes a “large accelerated filer,” as defined in Rule 12b-2 of the Exchange Act, (iii) it issuing more than $1.0 billion of non-convertible debt over a three-year period or (iv) the last day of the fiscal year following the fifth anniversary of its initial public offering.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. The Trust has chosen not to “opt out” of such extended transition period, and as a result, the Trust will take advantage of such extended transition period.

Business Development

The Trust has not been in, and is not in the process of, any bankruptcy, receivership or any similar proceeding since its inception.

Other than the conversion of the Trust from a Delaware limited liability company into a Delaware Statutory Trust, the Trust has not undergone any material reclassification, merger, consolidation, or purchase or sale of a significant amount of assets since its inception.

The Trust has not experienced any default of the terms of any note, loan, lease, or other indebtedness or financing arrangement requiring the Trust to make payments since its inception.

The Trust has not experienced any change of control since its inception.

The Trust has only one class of outstanding equity securities. The Trust has experienced increases of more than 10% of the Shares since inception of the Trust (date of inception). The Trust is a Delaware statutory trust that has no limit on the number of Shares that can be issued.

Other than the conversion of the Trust from a Delaware limited liability company into a Delaware Statutory Trust and the associated share split, there are no past or pending share splits, dividends, recapitalizations, mergers, acquisitions, spin-offs, or reorganizations since the Trust’s inception.

There has not been any delisting of the Shares by any securities exchange or deletion from the OTC Bulletin Board.

Competitive Business Conditions

The digital asset industry is rapidly developing, and there are significant uncertainties with respect to the development, acceptance, and success of the digital networks underlying the Portfolio Crypto Assets. See “Risk

4

Table of Contents

Factors—The further development and acceptance of the cryptographic and algorithmic protocols governing the issuance of and transactions in cryptocurrencies, which represents a new and rapidly changing industry, is subject to a variety of factors that are difficult to evaluate” for additional information. While the digital assets that are Portfolio Crypto Assets have enjoyed some acceptance and use in their limited history, it is possible that other crypto assets may grow more rapidly in acceptance and adoption for use as compared to Portfolio Crypto Assets, and while the Index may, over time, change to include more successful crypto assets, the Index may not capture the growth in value of more rapidly growing crypto assets.

Business of the Trust

The Sponsor expects the market price of the Shares to fluctuate over time in response to the market prices of Portfolio Crypto Assets. In addition, because the Shares reflect the estimated accrued but unpaid expenses of the Trust, the number of Portfolio Crypto Assets represented by a Share will gradually decrease over time as the Trust’s Portfolio Crypto Assets are used to pay the Trust’s expenses.

The Trust’s Portfolio Crypto Assets are held by Coinbase Custody Trust Company, LLC (the “Custodian“) on behalf of the Trust. The Trust’s Portfolio Crypto Assets are transferred only in the following circumstances: (i) sales made in connection with monthly rebalancing in order to more closely track the Index, (ii) sales to pay expenses of the Trust, (iii) sales on behalf of the Trust in the event the Trust terminates and liquidates its assets or as otherwise required by law or regulation, and (iv) transfers to pursue airdrops, forks, emissions, or other similar network events as deemed necessary by the Sponsor. Each delivery or sale of Portfolio Crypto Assets for purposes of rebalancing the Trust’s Portfolio Crypto Assets to track the Index will be a taxable event for Shareholders. See “Certain U.S. Federal Income Tax Considerations—Taxation of Operations.” See “The Sponsor may experience loss or theft of its Portfolio Crypto Assets during the transfer of Portfolio Crypto Assets from the Custodian to the Sponsor or to Crypto Asset trading venues.” In addition, each sale of Portfolio Crypto Assets by the Trust to pay the expenses of the Trust will be a taxable event for Shareholders.

The Trust is not registered as an investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”) and the Sponsor believes that the Trust is not required to register under the Investment Company Act. See “Risk Factors—Regulatory and Compliance Related Risks” and “Overview of Government Regulation” for additional information. In addition, the Trust will not hold or trade in commodity futures contracts or other derivative contracts regulated by the Commodity Exchange Act (the “CEA”), as administered by the Commodities Future Trading Commission (the “CFTC”). The Sponsor believes that the Trust is not a commodity pool for purposes of the CEA, and that neither the Sponsor nor the Trustee is subject to regulation as a commodity pool operator or a commodity trading adviser in connection with the operation of the Trust.

The Trust has no fixed termination date. The Trust is a passive entity with no operations, and no employees. The Sponsor administers and manages the Trust as described below. The Trust has not at any time been a “shell company.” The Trust and the Sponsor have entered into a limited, non-exclusive, revocable license agreement with Bitwise Index Services, LLC (the “Index Provider”), an affiliate of the Trust that is controlled by the same parent entity as the Sponsor, at no cost to the Trust or the Sponsor allowing the Trust to use the Index for the purpose of using as the benchmark index for the Trust (the “License Agreement”).

Activities of the Trust

The Trust seeks to make it easier for an investor to invest in the cryptocurrency market as a whole, without having to pick specific tokens, manage a portfolio, or constantly monitor ongoing news and developments. Although the Shares will not be the exact equivalent of a direct investment in cryptocurrencies, they provide investors with an alternative that constitutes a relatively cost-effective, professionally managed way to participate in cryptocurrency markets.

5

Table of Contents

The Trust notes that an indirect investment in digital assets through Shares may operate and perform differently from a direct investment in digital assets, and such differences may include, among other things: the holding period under Rule 144 for the resale of the Shares purchased from the trust, the risk that the Shares may trade at a substantial premium over or a substantial discount to the NAV per Share, the risk that over time the number of Portfolio Crypto Assets represented by a Share will gradually decrease as the Portfolio Crypto Assets are used to pay the Trust’s expenses, the ability to invest in Shares via an investor’s equity retirement accounts such as a 401(k) or individual retirement account, which do not provide the ability to invest directly in cryptocurrencies; the convenience of not having to open and maintain a cryptocurrency wallet; the potential ability to participate in decentralized finance protocols including governance, voting, staking assets and lending assets; and the ability of an investor to rely on the Bitwise Crypto Index Committee (the “Committee”) to choose the Portfolio Crypto Asset composition and balance of the assets.

In addition, the Trust must pay certain expenses which would not be charged for a direct investment in digital assets, including a Management Fee payable monthly, in arrears, in an amount equal to 2.5% per annum (1/12th of 2.5% per month) of the net asset value of the Trust’s assets at the end of each month.

To date, the only decentralized finance protocol that the Trust has participated in, including governance, voting, staking assets and lending assets, was in staking Tezos. The Index has not participated in any other decentralized finance protocols, including governance, voting and lending assets. To the extent that the Trust participates in any decentralized finance protocols, the Trust anticipates only participating in such protocols where the Trust has made a direct investment in the relevant decentralized finance digital asset. While the Trust currently does not participate in any staking activities, it may in the future engage in further staking activities if the Trust deems such activity to be in the best interests of shareholders.

In furtherance of its objective, the activities of the Trust include: (i) issuing Shares in exchange for subscriptions, (ii) selling or buying Portfolio Crypto Assets in connection with monthly rebalancing, (iii) selling Portfolio Crypto Assets as necessary to cover the Management Fee (as defined below) and/or any Organizational Expenses (as defined below), (iv) causing the Sponsor to sell Portfolio Crypto Assets upon any potential future termination of the Trust, and (v) engaging in all administrative and security procedures necessary to accomplish such activities in accordance with the provisions of the Trust Agreement, and the Custodian Agreement (as defined below). In addition, the Trust may engage in any lawful activity necessary or desirable in order to facilitate these activities, provided that such activities do not conflict with the terms of the Trust Agreement.

Digital assets are purchased from approved counterparties that include exchanges, electronic trading systems that seek liquidity from multiple trading venues, and market making firms known as “over the counter” or “OTC” trading desks with the goal of purchasing digital assets at or near the prices used to calculate the Trust’s NAV per share and used to calculate the Index while also seeking to minimize execution slippage compared to the benchmark price while simultaneously promoting operational risk management and efficient management of the Trust’s assets.

The Trust does not utilize a single principal market to convert digital assets to U.S. dollars and to purchase digital assets. The Sponsor evaluates counterparties, trading venues, and execution tools on an ongoing basis. The Trust utilizes multiple venues to acquire and dispose of digital assets, including trading venues (known as exchanges), direct trading counterparties (known as “OTC desks”), and trading technology solutions that aggregate liquidity from multiple trading venues. The Sponsor exercises judgment to determine on which venue to trade.

Calculation of Valuation

For all periods through the quarterly period ended March 31, 2021, the NAV per share, the NAV of the Trust, and the fair valuations for each Portfolio Crypto Asset were calculated by the Trust’s Administrator in reliance on the fair value of each portfolio crypto asset based on the blended average approach for calculating the price of a digital asset (the “Blended Bitwise Crypto Asset Price”), which the Sponsor was responsible for calculating.

6

Table of Contents

The Sponsor provided this price to the Administrator, and the Administrator used this price (multiplied by the Trust’s holdings) for each asset to determine the fair value of the Trust’s assets. The Administrator then subtracted the Trust’s liabilities to determine the Trust’s NAV. The administrator then divided this value by the Trust’s shares outstanding in order to determine the NAV per share. As a result of the Sponsor’s responsibility in this regard, any errors, discontinuance or changes in such valuation calculations may have had or may have an adverse effect on the value of the Shares. The Sponsor instituted this valuation policy in order to generate fair value estimates because it determined that such policy was in the best interest of shareholders, as it would avoid misstatements in valuation of the assets potentially arising from deviations in pricing across the digital asset market, and because of the fragmented nature of the digital asset trading ecosystem. As a result, management applied this valuation technique which it determined to be appropriate given the circumstances.

Following the filing of its Form 10, the Sponsor conducted a complete review of its process for determining fair valuation in the presentation of its financial statements and calculation of NAV. In this process, the Sponsor evaluated whether or not the identification of a principal market for each of the Trust’s assets for valuation purposes, during each period for which the Trust created and had audited its financial statements, would have created a material difference in the Trust’s estimated fair value or assets. In conjunction, the Sponsor began to consider a change in valuation policy for the fair valuation of cryptocurrencies held in the Trust. As a result, the Sponsor has developed a revised process for the determination of a principal market for each asset based on this consideration and intends to disclose this change in valuation policy and accounting policy when implemented, which has been implemented prior to the creation of financial statements for the period ending September 30, 2021. The Blended Bitwise Crypto Asset Price is no longer used for any calculations by the Trust, including NAV per share, NAV of the Trust or fair valuations for any Portfolio Crypto Asset.

The process that the Sponsor has developed for identifying a principal market, as described in Financial Accounting Standards Board Accounting Standards Codification 820-10, which outlines the application of fair value accounting, was to begin by identifying publicly available, well-established and reputable cryptocurrency exchanges selected by the Sponsor and its affiliates in their sole discretion, currently including BitFlyer, Binance, Bitstamp, Bittrex, Coinbase, itBit, Kraken, Gemini and Poloniex, and then calculating, on each valuation period, the highest volume exchange during the 60 minutes prior to 16:00 ET for each asset. In evaluating the markets that could be considered principal markets, the Trust considered whether or not the specific markets were accessible to the Trust, either directly or through an intermediary, at the end of each period.

In the process of this review, the Sponsor also retroactively applied this process for identifying a principal market to the prior periods of reported financial results, including the fiscal years 2018, 2019 and 2020, to determine whether or not any material or significant differences would have resulted from the application of a different valuation policy in the creation of each financial statement (e.g., comparing the fair value prices determined using the existing and previous valuation methodology to the hypothetical fair value prices using an identified principal market for each asset) and to consider whether management’s use of the existing valuation policy would have created any material departures from a valuation policy of identifying a principal market.

As set out in more detail in the tables in “Management’s Discussion and Analysis—Fair Value Measurements—Calculation of Valuation,” the Sponsor’s results conclude that there are no material or significant differences in valuation or the financial statements as presented when using the policy of identifying a principal market described above as compared to the existing valuation methodology for any period since the Trust commenced operations, as the average difference in valuation prices was in all cases less than 0.05% or five one hundredths of one percent for each asset for each period measured, and that such differences are immaterial in all cases.

While management has applied accounting standards it believes are appropriate to the circumstances, and despite these findings that the previous results are immaterially different, the Sponsor intends to change its valuation policy going forward based on the foregoing discussion and interpretation of ASC 820. The Sponsor intends to change its valuation policy for the purposes of calculating its ongoing net asset value, and processing ongoing subscriptions into the Trust and will similarly disclose this change in valuation policy, as well as the differences between the two policies. As described in the Explanatory Note, the Trust determined that the previous valuation

7

Table of Contents

policy, which utilized a blended average approach for calculating the price of a digital asset instead of identifying a principal market for such digital asset, was not in keeping with the proper application of U.S. GAAP, specifically ASC 820, and, therefore, resulted in an immaterial error. In accordance with the Financial Accounting Standards Board Accounting Standards Codification 250 (“ASC 250”), the Trust corrected this immaterial error by making changes to the valuation policy and the financial statements in subsequent periods.

Statements, Filings, and Reports

The Trust will comply with all reporting obligations required of companies with a class of securities registered under the Exchange Act, including timely filing Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other customary filings.

Shareholders will receive annual audited financial statements for the Trust and any applicable tax reports (e.g., Schedules K-1) from the Sponsor. The Sponsor or the Administrator (as defined below) will issue Schedules K-1 directly to Shareholders that hold Shares or the custodian of such Shares, as applicable, for each taxable year or portion thereof.

The Trustee will make elections, file tax returns and prepare, disseminate and file tax reports, as advised by the Sponsor, the Trust’s counsel or accountants or as required by any applicable statute, rule or regulation.

Investment strategy

The Trust holds a Portfolio that generally tracks the Index. The Index is administered by Bitwise Index Services, LLC, an affiliate of the Sponsor (the “Index Provider”). The Trust rebalances monthly alongside the Index to stay current with changes. The Sponsor strives to minimize tracking error (e.g., divergence between the performance of the Trust and the Index) by managing costs and price slippage during trade execution, and holding the assets in the Index.

The Sponsor has the discretion, when possible and prudent, to take advantage of incidental opportunities to generate additional returns in excess of the Index that arise from the Portfolio Crypto Assets held by the Trust, through, for example, airdrops, emissions, forks, staking, lending or similar network events and activities, if the Sponsor determines that any such activities are in the best interest of the Trust and its shareholders. The Sponsor does not consider these activities inconsistent with its investment objective to invest in a portfolio to track the Index or inconsistent with its disclosure that the Trust is managed as a passive investment vehicle. Accrual of additional returns through such activities may offset fees and fund expenses and allow the Trust to track the performance of the Index more closely. If the Sponsor accepts and liquidates airdrops, emissions, or hard forks or engages in staking, it will apply fair value to the assets received as described in the section “Management’s Discussion and Analysis—Significant Accounting Policies—Investments and Valuation.”

The Trust seeks to track the Index, and, therefore, to the extent that a Network Distribution Event, defined as an event that offers additional opportunities to engage with a blockchain network and generate additional capital, occurs and such Network Distribution Event impacts the composition of the Index, the Trust will undertake its usual rebalancing process. The policies of the Index in regard to Network Distribution Events are described below in “ —Index Methodology.”

It is possible that a Network Distribution Event could occur that may result in an opportunity for the Trust to generate additional returns, such as if an asset that the Trust already held were to do an airdrop that resulted in the Trust obtaining a different asset. If that were to occur, the Trust may seek to utilize the Network Distribution Event in such a way as to benefit the Shareholders of the Trust. For example, the Trust may choose to sell an airdropped asset and return the proceeds to the Shareholders.

8

Table of Contents

Price and Cost Slippage

On days when the Sponsor accepts subscriptions, the Sponsor aggregates the dollar value of subscriptions into the Trust and uses quantitative portfolio management techniques to compare the Trust’s existing holdings and weightings to the constituents and weightings of the index in order to calculate the amounts and quantities of each digital asset to purchase. On days when the Sponsor rebalances the Trust’s portfolio in order to pursue its investment objective of tracking the benchmark index, the Sponsor uses quantitative portfolio management techniques to compare the Trust’s existing holdings and weightings to the new and updated constituents and weightings of the index in order to calculate the amounts and quantities of each digital asset to purchase so that the Trust’s holdings and weightings will, after trade execution, be closely aligned with the constituents and weightings of the benchmark index. In each case, the Sponsor has at its disposal multiple venues to acquire and dispose of digital assets, including trading venues (known as exchanges), direct trading counterparties (known as “OTC desks”), and trading technology solutions that aggregate liquidity from multiple trading venues.

Trade execution and portfolio management is dynamic and complex, and the Sponsor must exercise judgement, assess multiple factors including recent experience and market conditions, as well as the size of the trades, settlement procedures at each venue, types of assets that need to be executed, as well as their availability on such platforms, prior to determining the best venue to execute each trade. The Sponsor attempts to purchase or sell each asset in each instance at a price that is close to the price used for calculating the Trust’s NAV (and the Index’s daily price) at 4pm ET, while also minimizing market impact and reducing operational and settlement risk. The Trust may choose to algorithmically execute a trade over time (for example, to execute a trade while only participating in a certain amount of volume), to execute a trade using a market order (e.g., purchasing or selling a digital asset immediately at whatever price the entire order can be filled at), or by putting multiple OTC desks into competition to provide the best price possible for a given amount and quantity of a digital asset. Often, OTC desks may be able to provide better prices than trading venues, and can also streamline and minimize operational complexity and settlement risk. There is no guarantee that the Sponsor will be able to trade digital assets at or near the benchmark price, there are a number of other factors aside from price slippage that inform best practices in trade execution, and market conditions change rapidly. Such factors include, but are not limited to, reputation of the trading venue, availability and support of personnel and coverage at the trading venue, settlement consistency or procedures, availability of assets and coin coverage, understanding of market dynamics, and perceived, disclosed, or reported regulatory compliance of the platform.

Index

The following is a materially complete description of the Index methodology (“Index Methodology”). The full Index Methodology is publicly available at https://www.bitwiseinvestments.com/indexes/methodology. Should any material change be made to the Index Methodology that results in a material change to the composition of the Index and, as part of the Trust’s monthly rebalancing process, results in a material change to the composition of the Trust the Trust will notify Shareholders of such material change by filing a Form 8-K with the Securities and Exchange Commission (the “SEC”). The Trust defines a material change as any change of 10% or more to the composition of the Index, and that also results in a corresponding change to the Trust. If not required by applicable law, the Trust may or may not file a Form 8-K with the SEC to disclose changes to the Index Methodology that do not result in a material change.

Purpose of the Index

The purpose of the Index is to track a basket of cryptocurrencies that represents the majority of cryptocurrencies by market capitalization. At its inception on October 1, 2017, the cryptocurrencies in the Index represented about 83% of all cryptocurrencies by market capitalization, and now represent approximately 76% as of March 31, 2021. The Index is comprised of the top 10 coins selected and weighted by free-float-adjusted market capitalization. The Index is rebalanced monthly. Additional eligibility criteria are applied to screen coins for investment feasibility (as defined below), to ensure the integrity of the coins selected to comprise the Index, and

9

Table of Contents

to appropriately account for one-off events. As a result, the 10 coins in the Index may not always completely match the top 10 coins on popular websites like CoinMarketCap.com that do not include such screening.

Index Methodology

The Index, designed by the Index Provider, an affiliate of the Sponsor, is comprised of the top ten largest cryptocurrencies in the world based on free-float-adjusted market capitalizations. The market capitalizations of cryptocurrencies are calculated using data sources from multiple publicly available, well-established and reputable cryptocurrency exchanges. The selection of cryptocurrency exchanges used to calculate market capitalization is made by the Committee, as defined below, in its sole discretion. Currently, the list of exchanges used to calculate the value of cryptocurrency in the Index include: BitFlyer, Binance, Bitstamp, Bittrex, Coinbase, itBit, Kraken, Gemini and Poloniex.

The market capitalization of a cryptocurrency is calculated by multiplying its price times its free-float-adjusted or “circulating” supply. The proportion of each cryptocurrency in the Index is based on this adjusted market capitalization. Public exchanges used for calculating the Index are selected using criteria which may include factors such as trading volume, availability, regulatory compliance, security, and reliability of real-time price and trade volume information and absence of abnormal withdrawal restrictions of crypto and fiat currencies. Regulatory compliance is defined as the exchange having no public evidence, such as statements by a relevant regulator, that it is not in compliance with the local regulations of the exchange’s domicile and not being subject to publicly disclosed legal or regulatory action. The Committee, as defined below, monitors company web sites, news flow, social media, and API-level data feeds to determine the regulatory compliance, security and reliability of real-time price and trade volume information and the absence of abnormal withdrawal restrictions of crypto and fiat currencies.

The Index is actively researched and evaluated and, therefore, the Index Methodology’s eligibility criteria, constituents and overall strategy may be adjusted over time. The Index is calculated by the Sponsor and its affiliates on a daily basis and published on the Sponsor’s website. Since the Trust’s investment strategy is to invest its assets to track the Index, a change in Index Methodology or composition will not automatically warrant a notice or consent requirement to Shareholders. Should any material change be made to the Index Methodology that results in a material change to the composition of the Index and, as part of the Trust’s monthly rebalancing process, results in a material change to the composition of the Trust the Trust will notify Shareholders of such material change by filing a Form 8-K with the SEC. The Trust defines material change as any change of 10% or more to the composition of the Index.

To screen, select and weight the top 10 coins, the Index uses a free-float-adjusted market capitalization which is calculated as follows:

(composite price) x (free-float-adjusted or circulating supply)

A coin’s composite price is derived from the real-time price data pulled from multiple exchanges. The individual exchange price data is combined using a trade volume weighting technique. The price on the exchange with more trade volume has more influence on the composite price while the exchange with the price that deviates more from the prices of the other exchanges has less influence on the composite price. This normalization produces a more accurate composited price which is then used in the market capitalization calculation.

In calculating the available supply of a coin, the Index looks at circulating supply. Circulating supply is the best approximation of the number of coins available on public markets. Circulating supply is derived by taking the total number of existing coins from the blockchain and subtracting the number of coins verifiably burned, locked, or reserved (for example, by a foundation.

The top 10 cryptocurrencies in the Index are selected and held in proportion to their valuation, often referred to as “market-capitalization weighted.”

10

Table of Contents

Composite Price Determination by the Index

Broadly speaking, the Index intends to reflect the price at which an institutionally oriented investor can trade any given crypto asset. This price is called the Index Crypto Asset Price (“Index CAP”). The Index CAP is used solely by the Index and is not used by the Trust or the Sponsor. The default denomination of an Index CAP is the U.S. dollar, and the methodology is as follows:

Calculating Crypto Asset Prices In U.S. Dollars: The crypto asset world has two modalities of trading: crypto-to-fiat trading and crypto-to-crypto trading. To create a single unified price for every crypto asset, all trading pairs must be standardized to price that asset in a single currency (for the Index, this currency is the U.S. dollar). The steps to do that are listed below in the order that they are followed:

| 1. | Select Quote Crypto Assets: To avoid circular pricing when standardizing crypto-to-crypto trading pairs, the Committee must select a group of “Quote Crypto Assets.” Quote Crypto Assets are determined on an annual basis at the Committee meeting that precedes the start of a new calendar year. |

| a. | Quote Crypto Assets are those that: |

| i. | Have crypto-to-fiat trading on at least two eligible crypto asset trading venues that allow for institutional deposits and withdrawals in a noncapital-controlled fiat currency (an “Eligible Fiat Currency”). |

| ii. | Are the largest crypto trading pair (measured by trailing 30-day dollar trading volume) for at least one of the top 100 Eligible Crypto Assets in each of the past three months. |

| iii. | As of March 31, 2021, Quote Crypto Assets were Bitcoin (BTC) and Ethereum (ETH). |

| 2. | Calculate Quote Crypto Assets Index CAPs: Quote Crypto Assets are unique in that the Index only considers fiat-to-crypto trades when calculating their Index CAPs, as the goal is to calculate the fiat-convertible price of Eligible Crypto Assets that have crypto-to-crypto trading pairs. |

| a. | The Index CAP for a Quote Crypto Asset is calculated as follows: |

| i. | Aggregate all crypto-to-fiat trading pairs for Eligible Fiat Currencies that take place on eligible crypto asset trading venues, removing any pairs that face withdrawal issues. |

| ii. | Transform all non-U.S.-dollar fiat trading pairs into U.S. dollar prices using synchronous data from an established foreign exchange reference data provider. |

| iii. | Calculate the U.S. dollar volume over the previous hour for each crypto-to-fiat trading pair. |

| iv. | Assign each trading pair a contribution weight based on its share of total dollar trading volume in a given asset over the previous hour. |

| v. | Multiply the last traded price (adjusted into U.S. dollars) for each trading venue pair by its contribution weight. In the event that no trading price is pulled for a particular trading pair either due to technical reasons or to a lack of trading volume, the Committee may substitute a fair market value estimate for that price or eliminate that price from consideration. |

| vi. | Sum to find the Index CAP. |

| 3. | Calculate the Index CAP for Non-Quote Crypto Assets: Many crypto assets trade (sometimes exclusively) in pairs with other crypto assets. |

| a. | The process for translating these crypto-to-crypto pairs along with crypto-to-fiat pairs into an aggregate Index CAP is as follows: |

| i. | Consider both crypto-to-fiat trading pairs and crypto-to-crypto trading pairs on eligible crypto asset trading venues, excluding any trading venue pairs that have withdrawal issues. |

| ii. | Exclude all trading pairs that are not denominated in either Eligible Fiat Currencies or Quote Crypto Assets. |

11

Table of Contents

| iii. | Transform all non-U.S.-dollar fiat trading pairs into U.S. dollars using synchronous foreign exchange data from an established foreign exchange data supplier. |

| iv. | For Quote Crypto Assets, use the synchronous Index CAP to translate the crypto-to-crypto pair into a crypto-to-U.S.-dollar equivalent. The synchronous Index CAP is used to establish a conversion rate for non-fiat denominated crypto pairs. Non-quote crypto assets are usually priced relative to a Quote Crypto Asset; therefore, the price can be converted into U.S. dollar price by multiplying by the U.S. dollar Index CAP of the Quote Crypto Asset. For example, a non-quote crypto asset can be priced in Bitcoin, which is a Quote Crypto Asset. Therefore, you would convert the price of the non-quote crypto asset to its price in Bitcoin, and then convert that price to U.S. dollars. In either scenario, the crypto-to-crypto price is converted or “translated” into a crypto-to-U.S. dollar equivalent. This process is similar to how a foreign exchange rate would be used to convert or “translate” a crypto-to-forex price into a crypto-to-U.S. dollar equivalent. |

| v. | Calculate the U.S. dollar volume for each trading pair and assign each pair a contribution weight based on its share of total U.S. dollar trading volume in a given crypto asset over the past hour. |

| vi. | Multiply the last traded price (adjusted into U.S. dollars) by its contribution weight. Note: In the event that no trading price is pulled for a particular trading pair either due to technical reasons or a lack of trading volume, the Committee may substitute a fair market value estimate for that price or eliminate that price from consideration. |

| vii. | Sum to find the Index CAP. |

Changes in Index Methodology

The Index Methodology is subject to change, though changes are expected to be infrequent and consistent with the Index’s goal of including the most valuable coins that cover the majority of the cryptocurrency market based on market capitalization, while meeting criteria relating to liquidity, access to markets, available pricing, available custody options, and other criteria included within the Index’s rules, which we collectively refer to as meeting an “investment feasibility” standard. See “Eligibility of Cryptocurrencies” for additional information.

Given the speed at which the crypto asset market has been changing over the past few years, some adjustments to the methodology have been made in order for the Index to better reflect its target market. Examples of such changes include the method followed to determine which exchanges or custodians are needed to support a crypto asset in order to make it eligible, the method to calculate a crypto asset’s free-float-adjusted market capitalization, and the specifics of how to screen out assets for non-compensated regulatory or technical risks.

Since the inception of the Index on October 1, 2017, the Committee approved the following changes to the methodology:

| • | Meeting of September, 30, 2020: Adopted a new rule concerning the risk, given present facts and circumstances, of a crypto asset being deemed a security under U.S. Federal Securities laws. |

| • | Meeting of December, 29, 2020: Adopted a change to Rule V.B, which defines the calculation methodology of market capitalization to exclude the five-year inflation adjustment that was in place up until that time. |

| • | Meeting of January 25, 2021: Adopted an amendment to Rule III.B.3.i.e, the custody rule, to require inclusion of additional factors related to the regulatory standing of approved custodians requiring that such custodians follow industry best practices. |

| • | Meeting of June 30, 2021: Adopted an amendment to Rule III.B.i.g. to state that cryptoassets will be screened for undue risk “of being in violation of U.S. federal securities laws” rather than being screened for undue risk “of being deemed a security under U.S. federal securities laws.” |

12

Table of Contents

Since the Trust’s principal investment objectives is to invest in a portfolio of cryptocurrencies that tracks the Index as closely as possible, the Trust relies on the Index Methodology when the Trust determines in which digital assets it should invest. The Trust does not intend for its holdings to deviate from the digital assets as determined by the Index, and the Trust anticipates that such deviation would likely occur only if the Trust was unable to hold a particular digital asset that was included in the Index or if the Trust determined that holding a particular asset would result in significant harm to Shareholders.

Eligibility of Cryptocurrencies

The Index is comprised of the top 10 coins measured by free-float-adjusted market capitalization. The Index is rebalanced monthly. Additional eligibility criteria are applied to screen coins for investment feasibility (as defined below), to ensure the integrity of the coins selected to comprise the Index, and to appropriately account for one-off events. As a result, the 10 coins that comprise the Index may not always completely correlate with the top 10 coins posted on popular websites like CoinMarketCap.com to the extent that such coins do not also meet the Index’s eligibility criteria. The Index will only consider for eligibility cryptocurrencies that satisfy the following conditions as established by the Committee for each coin:

| 1. | Is a cryptographically secured digital bearer instrument |

| 2. | Has a price that is not pegged to another crypto asset, fiat currency, group of those currencies, or hard asset |

| 3. | Is freely traded and can be freely held for the foreseeable future |

| 4. | Trades on two or more eligible crypto asset trading venues, without withdrawal issues specific to that crypto asset |

| 5. | Is custodied by a third-party custodian regulated as a federally chartered bank or as a state trust company, and meets additional security practices, insurance requirements and business practice requirements as determined by the Committee. The list of approved custodians is reviewed and updated on an annual basis, or at the discretion of the Committee. As of January 25, 2021, the date that the Committee performed its 2021 annual review of eligible custodians, the list of approved custodians was as follows: |

| i. | Anchorage |

| ii. | Bakkt Warehouse |

| iii. | BitGo |

| iv. | Coinbase Custody |

| v. | Fidelity Digital Assets |

| vi. | Gemini Custody |

| 6. | Has no known security vulnerabilities, including critical bugs, undue exposure to 51% attacks, or other factors, as determined by the Committee. |

| 7. | Does not face undue risk of being in violation of U.S. federal securities laws in the opinion of the Committee, given present knowable facts and circumstances. This is a risk-based assessment that considers whether the digital asset may be deemed a security under U.S. federal securities laws and whether it is subject to regulatory action that may imperil the value of the digital asset. Such assessment does not preclude legal or regulatory action based on the presence of a security. The Committee does not engage in legal analysis of any digital assets or perform any analysis of digital assets based upon any legal standards. |

The Committee reviews the following information to make this determination: 1) public information to determine if the SEC, any other US regulatory agency or any court has made any statements regarding

13

Table of Contents

the digital asset, 2) public information regarding how the digital asset markets view the digital asset, including whether the digital asset has been listed on entities such as Coinbase or other US exchanges that would have had access to a reasonable amount of information when making their determinations to list the digital asset, 3) public information to undertake reasonable diligence into the structure and technology of the digital asset, including reviewing the digital asset’s whitepaper if available and speaking with the sponsor of the digital asset, and 4) any other information gained from reputable sources that may impact the Committee’s view of digital asset.

Any legal test utilized to determine whether a digital asset is a security would differ from the analysis performed by the Committee. If the Committee adds a digital asset to the Index, but later becomes aware of new information that causes the Committee to revalue the risk profile of such digital asset, the Committee will review such information and determine whether the digital asset should be removed from the Index.

| 8. | Has traded more than 10% of its free-float-adjusted market capitalization on eligible crypto asset trading venues over the past 30 days. |

The following table sets forth all of the digital assets included in the Index as of March 31, 2021, as well as digital assets that were included in the list of the top 10 coins measured by market capitalization on CoinMarketCap.com as of March 31, 2021, but were deemed by the Committee not to satisfy each of the above-described eligibility requirements and were therefore not included in the Index:

Digital Assets | Included in / | If excluded, reason for exclusion | ||

Bitcoin BTC | Included | — | ||

Ethereum ETH | Included | — | ||

Binance Coin BNB | Excluded | Because it does not trade on two or more eligible crypto asset trading venues | ||

Tether USDT | Excluded | Because it is pegged to a fiat currency | ||

Cardano ADA | Excluded | Because it was not able to be custodied by a third-party custodian regulated as a federally chartered bank or as a state trust company | ||

Polkadot DOT | Excluded | Because the Committee believes it may face undue risk of being in violation of U.S. federal securities laws | ||

XRP XRP | Excluded | Because the Committee believes it may face undue risk of being in violation of U.S. federal securities laws | ||

Uniswap UNI | Included | — | ||

Litecoin LTC | Included | — | ||

THETA | Excluded | Because it did not trade on two or more eligible crypto asset trading venues | ||

ChainLink LINK | Included | — | ||

Bitcoin Cash BCH | Included | — | ||

Stellar Lumens XLM | Included | — | ||

AAVE | Included | — | ||

EOS | Included | — | ||

Cosmos ATOM | Included | — |

To the extent that any such coin meets the Index’s eligibility requirements at a future date, it would be considered for inclusion in the Index in connection with a future rebalancing. Assets will lose eligibility and be removed from the Index at the next monthly reconstitution event if they violate any of the listed Eligibility Requirements for 30-consecutive days. Under extraordinary circumstances, assets may lose eligibility and be removed on a same-day basis by a unanimous vote of the quorum of members of the Bitwise Crypto Index Committee. Such

14

Table of Contents

emergency removals will take place at 4:00 p.m. ET following the conclusion of the meeting and public posting of that notice on the Sponsor’s web site. In either case, if the Sponsor determines that the change is material (which the Sponsor generally considers to be a change of 10% or more to the Trust or the Index holdings, but in any event, is also determined at the Trust’s discretion) the Sponsor will disclose such change on Form 8-K. The Committee relies on the analysis conducted by the Sponsor as described in “Certain Legal and Regulatory Considerations” and “Overview of Government Regulation.” The Trust, in the Sponsor’s sole discretion, may choose to immediately liquidate its position in any Portfolio Crypto Asset that it determines may be at increased risk of being in violation of U.S. federal securities laws or based on consideration of new public information available regarding the asset. The Sponsor makes its determination using the same process as that used by the Committee as set forth above. In certain circumstances, the Sponsor may cause the Trust to differ from the Index in the coins that it holds if the Sponsor causes the Trust to exclude a coin based on these or similar circumstances, and this may lead to tracking differences between the Trust and the Index.

One-Off Events

The Index has provisions for handling one-off events in a basket cryptocurrency or the cryptocurrency market generally, such as trade suspensions and hard forks. One-off events are events that are not expected to occur during the normal functioning of a cryptocurrency network and that significantly impact the operation of the network or the ability for market players to trade in or out of the cryptocurrency. Examples of these are hard-forks, which can lead to a network split and therefore two versions of the same asset circulating in the market, or significant liquidity reductions, such as in the event of trading suspensions or delistings from exchanges. If new types of important one-off events become common, the Index may adopt additional policies to address them as determined in the sole discretion of the Sponsor. With regard to trade suspensions, if an exchange suspends the trading of a given coin for any reason, the Index may remove that individual exchange from consideration. In the event of delisting of such coin from all public exchanges, then the coin will be removed from the Index during the next rebalancing regardless of what the assumed market capitalization might have been. The Committee may convene ad hoc to consider appropriate actions should there be a sudden and extenuating event.

The Index views hard forks similarly to how company spinoffs are viewed in US equity markets. A hard fork is when a cryptocurrency is split because portions of the consensus nodes adopt different policies. In such an event, often a private key holder ends up with ownership on both chains. Often there is a primary chain that is adopted by the majority. When a hard fork occurs, the forked coin will be held in the Index until the next rebalancing. This embodies the idea that the value of the forked coin stems from that of the original coin. Thus, the Index will hold the two coins as if they were one until the next opportunity to treat them as separate. The new forked coin will then be removed from the Index upon the next rebalancing unless it meets all the eligibility requirements (except the requirement to have a three-month trade history) and has an inflation adjusted market capitalization of its own to warrant being included in the Index.

The Index also has provisions for other Network Distribution Events. Network Distribution Events include emissions, airdrops, and staking. To the extent that Network Distribution Events occur that impact the Index and, due to the Trust’s goal of tracking the Index, thereby impact the Trust as well, the Trust will notify shareholders of such Network Distribution Events by filing a Form 8-K with the SEC.

| • | Emissions: Certain crypto assets provide regular awards to holders in the form of crypto asset grants, often in the form of “gas” that powers transactions on the network itself, which are referred to as “emissions.” Such emissions are a native development for the crypto assets that provide them. Currently, there are no assets in the Index that produce emissions, and historically, there has been just one asset (NEO) that did so. To date, the daily value of distributed emissions has been de minimis for any given crypto asset. Given the small values involved, it would not be practical for investment funds handling regular inflows and outflows to accurately track the Index if it accrued emissions on a daily basis, regardless of whether the Index collected those emissions over time or liquidated them daily. As a result, the Index ignores emissions for index calculation purposes It is possible that the Trust may |

15

Table of Contents

choose to periodically liquidate emissions and return the proceeds of such liquidation to Shareholders. The Trust will only do so if it has a good faith belief that such liquidation would result in a benefit to Shareholders. In the period ended December 31, 2018, the Trust received approximately 311 ONT tokens and 219 GAS tokens as a result of its holdings in NEO, resulting in approximately $6,000 USD in investment income. The Trust sold its positions in these tokens during the period and reinvested the proceeds in the Trust’s Portfolio Crypto Assets.” |

| • | Airdrops: An airdrop occurs when a new or emergent crypto asset is granted to holders of an existing crypto asset on a one-off or occasional basis. Airdrops are not native to the internal return drivers of any given crypto asset. Importantly, they also require agency on the part of crypto asset holders to claim, and the act of claiming an airdropped crypto asset can potentially put holders of a given crypto asset at risk. As such, the Index does not incorporate the value of airdropped crypto assets into the Index It is possible that the Trust may choose to periodically liquidate airdropped assets and return the proceeds of such liquidation to Shareholders. The Trust will only do so if it has a good faith belief that such liquidation would result in a benefit to Shareholders. |

When considering whether or not to accept and/or sell an airdrop of digital assets, the Trust primarily considers whether or not the Trust’s custodian will support such activities related to the airdropped asset. If the Trust’s custodian does not support the airdrop, it is unlikely that the Trust will participate in the acceptance and sale of the airdropped asset. If the Trust’s custodian does support the airdropped asset, it is likely, though not necessary, that the Trust will participate in the acceptance and sale of the airdropped asset. However, as airdrops may provide opportunities to generate incremental return, the Sponsor retains discretion to pursue receipt of any airdropped asset, even if not supported by the custodian, which may require putting a related portfolio crypto asset at risk. There may be operational, securities law, regulatory, legal and practical issues with accepting such assets.

Additionally, laws, regulation or other factors may prevent Shareholders from benefiting from such airdrops. For example, it may be illegal to sell or otherwise dispose of such assets, or there may not be a suitable market into which such assets can be sold (immediately after the airdrop, or ever). There were no “airdrops” or emissions recognized or not recognized during the fiscal quarter ended March 31, 2021 or the fiscal year ended December 31, 2020.