Exhibit 99.2

BM Technologies, Inc. created by the Business Combination of BankMobile Technologies & Megalith FinancialAcquisition A Banking-as-a-Service pioneer, enabling non-banks to build financial services for their customers August2020

This presentation (the “Presentation”) contemplates the purchase by Megalith Financial Acquisition (“MFAC”) of BankMobile Technologies, Inc. (“BankMobile” or the “Company”) from Customers Bank, by which BankMobile will become a subsidiary of MFAC (“theTransaction”). BankMobile is Not aBank BM Technologies is Not a Bank and it does not provide banking services. BankMobile is a technology provider that facilitates deposits and banking services between a customer and an FDIC insured partner bank. Any reference in this presentation to “banking” or “banking services” is in reference to BankMobile providing services between customers and a partner bank. The BankMobile brand and trademark is only used in reference to services being provided between a customer and an FDICinsured partner bank No Offer orSolicitation This Presentation is for informational purposes only and is neither an offer to sell or purchase, nor a solicitation of an offer to sell, buy or subscribe for any securities, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law. No offering of securities shall be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended (the “Securities Act”), or an exemptiontherefrom. Forward-LookingStatements This Presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended. This information is, where applicable, based on estimates, assumptions and analysis that management believes, as of the date hereof, provide a reasonable basis for the information contained herein. Forward-looking statements can generally be identified by the use of forward-looking words such as “may”, “will”, “would”, “could”, “expect”, “intend”, “plan”, “aim”, “estimate”, “target”, “anticipate”, “believe”, “continue”, “objectives”, “outlook”, “guidance” or other similar words, and include statements regarding plans, strategies, objectives, targets, estimates, projections, and expected financial performance. These forward-looking statements involve known and unknown risks, uncertainties and other factors. Actual results, performance or achievements may differ materially, and potentially adversely, from any projections and forward-looking statements and the assumptions on which those projections and forward-looking statements are based. There can be no assurance that the data contained herein is reflective of future performance to any degree. You are cautioned not to place undue reliance on forward-looking statements as a predictor of future performance as projected financial information, cost savings, synergies and other information are based on estimates and assumptions that are inherently subject to various significant risks, uncertainties and other factors. There can be no assurance that the estimates and assumptions made in preparing the financial projections and forecasts will prove accurate, that the projected results will be realized or that actual results will not be significantly higher or lower than projected. The Company's financial performance and results of operations will be subject to a variety of risks, including but not limited to general economic conditions, consumer adoption, and the operations and performance of its partners, including white-label partners. All information herein speaks only as of the date hereof unless otherwise specified. Management undertakes no duty to update, add to or otherwise revise or correct any of the information contained herein, whether as a result of new information supplied, future events, inaccuracies that become apparent after the date hereof or otherwise. Forecasts and estimates regarding industry and end markets are based on sources believed to be reliable, however, there can be no assurance these forecasts and estimates will prove accurate in whole or inpart. Use ofProjections This Presentation contains financial forecasts with respect to, among other things, income sources, revenue growth, and equity values. These unaudited financial projections should not be relied upon as being necessarily indicative of future results. The inclusion of the unaudited financial projections in this Presentation is not an admission or representation that such information is material. The assumptions and estimates underlying the unaudited financial projections are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the unaudited financial projections. There can be no assurance that the prospective results are indicative of future performance or that actual results will not differ materially from those presented in the unaudited financial projections. Inclusion of the unaudited financial projections in this Presentation should not be regarded as a representation by any person that the results contained in the unaudited financial projections will beachieved. IndustryandMarketData Theinformationcontainedherealsoincludesinformationprovidedbythirdparties,suchamarketresearchfirms.Inparticular,BankMobilehasrelieduponindependentresearchfromAccenture,ARKInvestmentManagementLLC,FactSetResearchSystems,FT PartnersResearch,PWC&S&PGlobalMarketIntelligenceformarketandindustryinformationtobeusedbyBankMobile.NoneofMFAC,thesponsorofMFAC,BankMobile,BMT,CustomersBankanditsaffiliatesandanythirdpartiesthatprovidedinformation toMFACorBankMobile,provideguaranteesoftheaccuracy,completenessandtimelinessoravailabilityoftheinformation.NoneofMFAC,BankMobile,CustomersBanknoranyoftheirrespectiveaffiliates,noranyoftheresearchproviders,areresponsiblefor anyerrorsoromissionsorconclusionsformtheuseofsuchcontent. Non-GAAP FinancialMeasures This Presentation includes certain non-GAAP financial measures that management reviews to evaluate its business, measure its performance and make strategic decisions. Management believes that such non-GAAP financial measures provide useful information to investors and others in understanding and evaluating its operating results in the same manner as management. EBITDA is a non-GAAP financial measure that represents net income prior to interest expense, net, other expense, net, income taxes, and depreciation and amortization, as adjusted to add back certain non-cash and non-recurring charge. EBITDA and any other ratio or metrics derived therefrom are financial measures not calculated in accordance with GAAP and should not be considered as substitutes for revenue, net income, operating profit, or any other operating performance measure calculated in accordance with GAAP. Using these non-GAAP financial measures to analyze the business would have material limitations because their calculations are based on the subjective determination of management regarding the nature and classification of events and circumstances that investors may find significant. In addition, although other companies in its industry may report measures titled EBITDA or similar measures, such non-GAAP financial measures may be calculated differently from how management calculates its non-GAAP financial measures, which reduces their overall usefulness as comparative measures. Because of these limitations, you should consider EBITDA alongside other financial performance measures, including net income and other financial results presented in accordance withGAAP. |2 Disclaimer

Table ofContents I. Introduction II. TransactionSummary III. BankMobileOverview IV. FinancialInformation V. Appendix

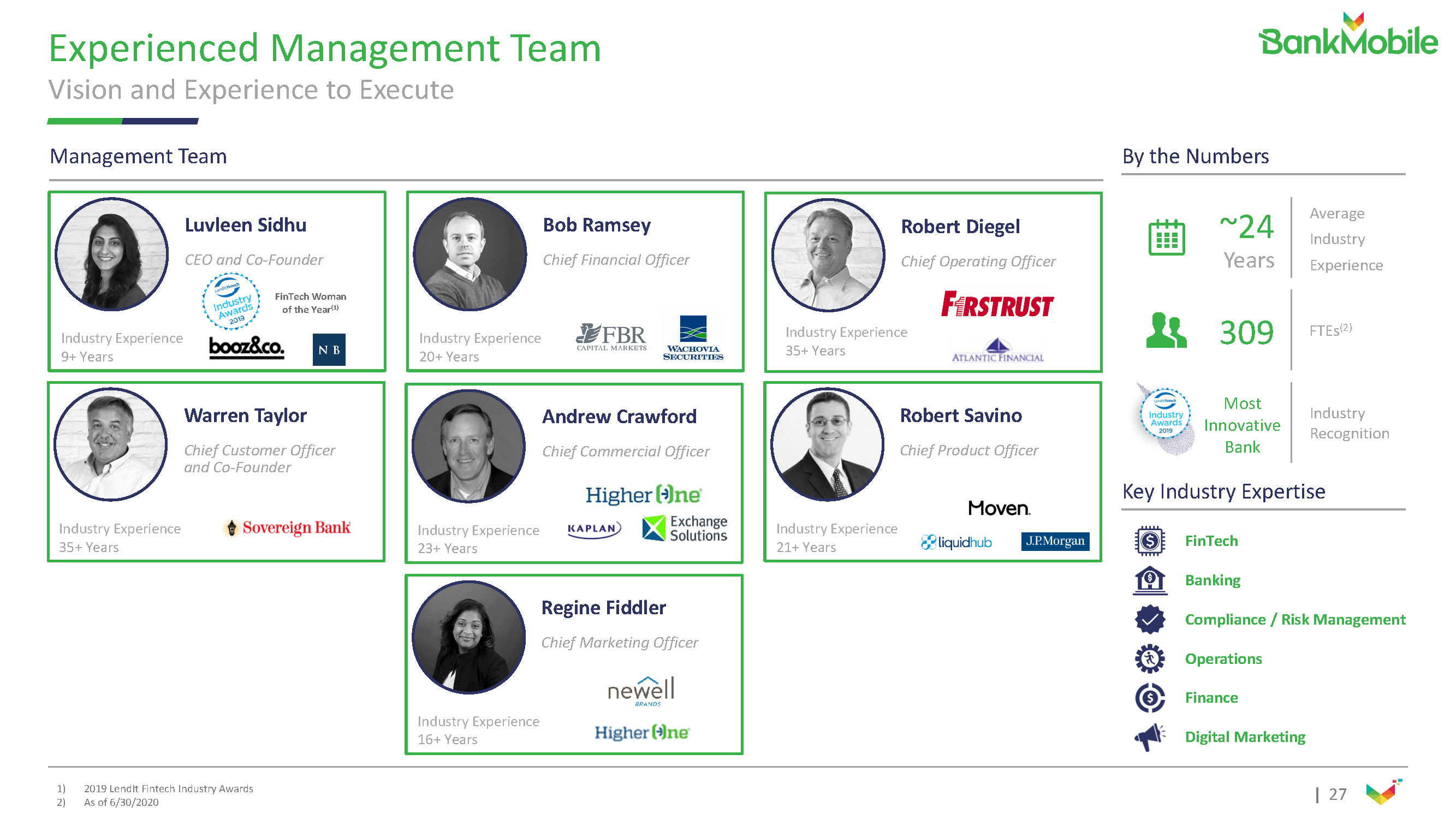

|4 Management PresentingToday LuvleenSidhu CEO andCo-Founder BobRamsey Chief FinancialOfficer IndustryExperience 9+Years IndustryExperience 20+ Years • As BankMobile's Chief Financial Officer, Bob Ramsey oversees the bank’s financial operations, including planning, risk, andreporting • Prior to joining BankMobile, Ramsey served as senior equity research analyst at FBR Capital Markets, where he covered community banks, regional banks, super- regional banks, consumer finance and fintech companies during his 13-yeartenure • Ramsey is a Chartered Financial Analyst (CFA). He holds a Bachelor of Arts degree in Managerial economics from Hampden-Sydney College and a Master of Business Administration degree from the College of William and Mary FinTechWoman of theYear (1) Expertise in Scaling andBuilding Billion Dollar Companies in RelatedIndustries Total Board Experience of50+ Years in RelatedIndustries Track Record of CreativeDeal Structuring and Partnership Development A.J.Dunklau CEO The MFAC Board is aValue-Add Partner toBankMobile • LuvleenSidhuistheChiefExecutiveOfficerandCo- FounderofBankMobile • AftergraduatingfromHarvardandWhartonshewasa managementconsultantatBooz&co.intheirfinancial servicespractice • Sidhu is a recognized leader in the industry and wasnamed one of Crain’s New York Business 2020 40 Under 40 and a “Rising Star in Banking & Finance” in2020 • Before attending business school at Wharton, she was analyst at Neuberger Berman and also worked as adirector of corporate development at Customers Bank. While at the company, Sidhu introduced several growth projects, including partnering with a New York City-based start-up to improve the banking experience through innovative technology • Sidhu has been featured regularly in the media including on CNBC, Bloomberg Radio, Yahoo Finance, Fox News Radio and in The Wall Street Journal,Forbes.com, American Banker, Crain’s New York, FoxNews.com,among others P P P MFAC Board Leadership orBoard Experience 1) 2019 LendIt Fintech Industry Awards

|5 Where Does BankMobile Technologies StandToday? Delivering Full-Featured Digital Banking Platform to Large Scale Non-BankPartners …Award Winning BankingTechnology, Focused on Banking Services for Millennials& Middle IncomeAmericans… xCustomer-centricapproach xProvides an affordable, easy-to-useproduct xSimplifies banking for theconsumer xCreates customers for life with full suite of banking products, including checking, savings, personal loans, credit cards and studentrefinancing xCreates attractivereturns xProprietary Banking-as-a-Service(“BaaS”) technology xAllows for greater speed and cost effectiveness in bank roll out forpartners xHigh-volume, low-cost customer acquisition model xServes ~1 in 3 U.S. students on 722 campuses (4) xLaunched partnership with T-Mobile via the T- Mobile MONEY checkingaccount xPlanned 2021 launch of digital bank account with GooglePay xOver 2M accounts (1) x~300K accounts opened annually (2) x~$812M in 2020EDeposits x$72M in 2020ERevenue x$6M in 2020E Adjusted EBITDA (3) One of America’s LargestDigital BankingPlatforms… Expert in B2B2CBanking… 1) Data as of6/30/2020 2) Per BankMobilemanagement 3) EBITDA is a Non-GAAP financial measure; see page 39 for reconciliations to Non- GAAP financial measures and disclaimers on forward lookingfinancials 4) Based on market share for Signed Student Enrollments (“SSEs”) (the number of students enrolled at higher-ed institutions); Assumes ~3M SSEs are considered non- addressable (beauty schools, trucking schools, etc.); Data per BankMobile’s internal sales database and estimated student market size and National Center for EducationStatistics“EnrollmentandEmployeesinPostsecondaryInstitutions,Fall2015; FinancialStatisticsAcademicLibraries,FiscalYear2015”, February2017

|6 Consumers Are Recalibrating Their BankingNeeds New Digital Options, Remote Necessities and Poor Customer Experiences Are DrivingChange 1) Accenture Consumer Retail Banking Survey Summary, July2017 2) PWC Consumer Banking Survey,2019 3) Forbes, “Consumers Shelled Out $1B in Monthly Bank Maintenance Fees”,2019 1 in2 consumers switch theirprimary banks due to discounts and promotions onfees (1) 1 in3 consumers switch primary banks for a better interestrate on theirdeposits (2) 50% of consumers likely will notopen their next account with the bank they currentlyuse (2) 63% of consumers areusing mobile channels more frequently (2) 59% of employees claim financial or money challenges as the #1cause of stress in theirlives (4) 10% of income spent on feescharged by payday lenders and other financial serviceproviders (5) Consumers are Looking for an Affordable Banking Alternative (3)(5) x 1 in 3 Americans live paycheck topaycheck x Americans pay $34B a year in overdraftfees x The average overdraft fee is$33.36 x Big banks require at least $1,500 in a basic checking account to waive their monthly maintenance fee, which averages$10.99 x Women pay 18% more in overdraft fees than men (five per year) dueto lower-than-averageearnings x The average fee to withdraw money from an out-of-network ATM has hit a record high of $4.72, up 33% over the pastdecade Consumer Preferences are Changing, with Banks Slow toAdapt 4) PWC Employee Wellness Survey,2019 5) The Cornerstone Performance Report,2017

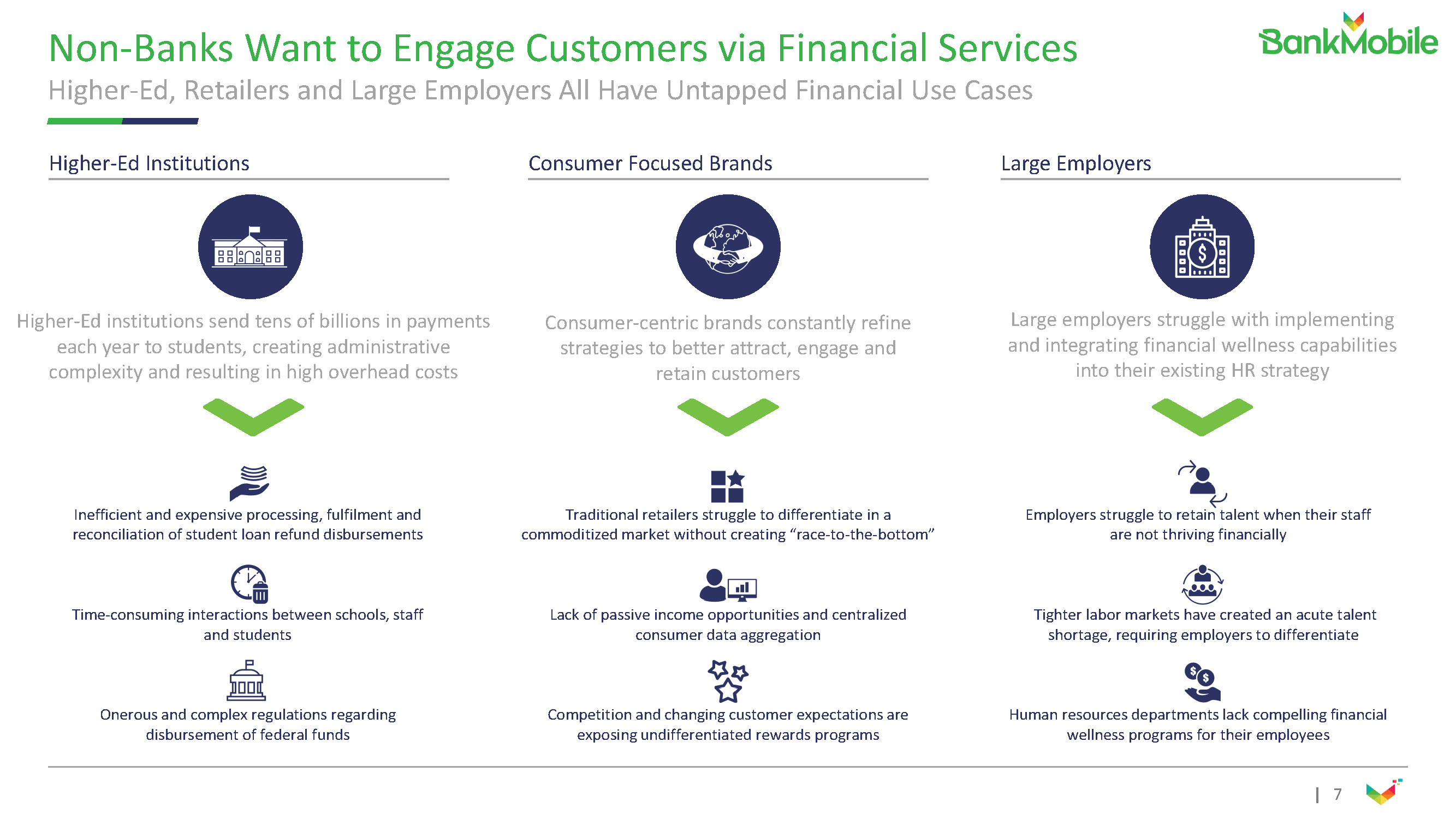

|7 Non-Banks Want to Engage Customers via FinancialServices Higher-Ed, Retailers and Large Employers All Have Untapped Financial UseCases Higher-Ed institutions send tens of billions in payments each year to students, creating administrative complexity and resulting in high overheadcosts Large employers struggle with implementing and integrating financial wellness capabilities into their existing HRstrategy Onerous and complex regulations regarding disbursement of federalfunds Inefficient and expensive processing, fulfilment and reconciliation of student loan refunddisbursements Time-consuming interactions between schools, staff andstudents Employers struggle to retain talent when their staff are not thrivingfinancially Human resources departments lack compelling financial wellness programs for theiremployees Tighter labor markets have created an acute talent shortage, requiring employers todifferentiate Consumer-centric brands constantly refine strategies to better attract, engage and retaincustomers Higher-EdInstitutions ConsumerFocusedBrands LargeEmployers Traditional retailers struggle to differentiate ina commoditized market without creating“race-to-the-bottom” Lack of passive income opportunities and centralized consumer dataaggregation Competition and changing customer expectations are exposing undifferentiated rewardsprograms

|8 BankMobile Solves Multiple Parties’ Pain Points in OneSolution Resulting in High-Volume, Low-Cost CustomerAcquisition B2B2CApproach Examples of BankMobile Solutions within 3Verticals Higher-EdBanking x Distribute financial aid refunds and otherdisbursements x Eliminate administrative burden andcomplexity x Offer students access to bankingservices x Reduce processing costs annually by ~$125K /year (1) White-Label Banking x Offer financial services through white-label partnerships (2) x Attract customers by improving banking experience in historically- underserved segments x Deliver customizable, partner branded rewards and special offers to further driveloyalty x Create net-new, passive revenue streams for partners with lower customerattrition WorkplaceBanking x Deploy differentiated financial services in conjunction with financial wellness strategy x Represents the first benefit that earns employee's money via interest-bearing accounts, no fees and unique cost-saving opportunities x Easily accessible benefits through HRportal 1) Compared to existing campus processing costs; Approximation based on internal BankMobileestimates 2) Deposits are held with bankpartner BankPartners Planned Launchin 2021

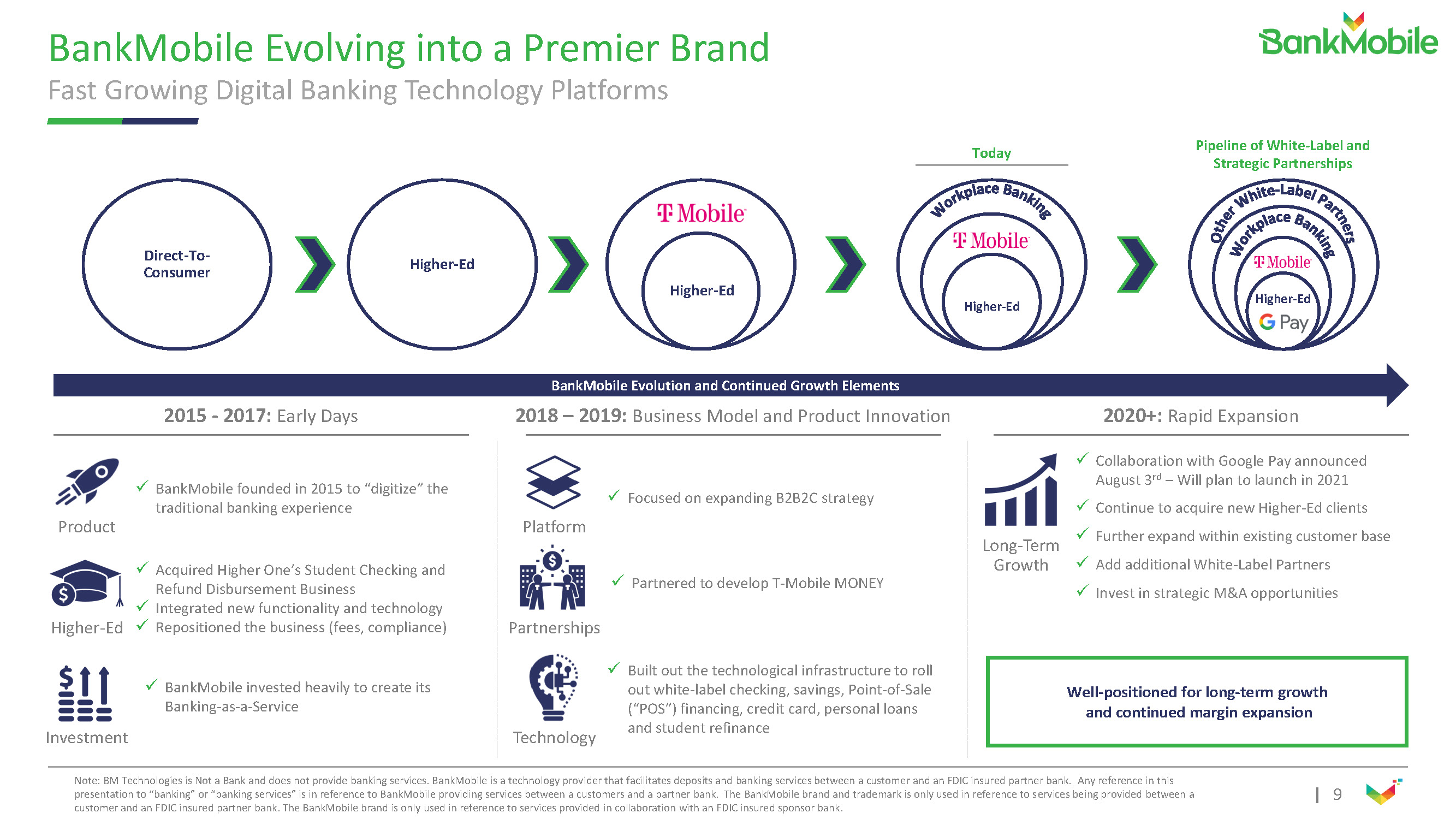

|9 BankMobile Evolving into a PremierBrand Fast Growing Digital Banking TechnologyPlatforms 2020+: RapidExpansion2015 -2017: EarlyDays xBankMobile founded in 2015 to “digitize”the traditional bankingexperience Product Higher-Ed xAcquired Higher One’s Student Checking and Refund DisbursementBusiness xIntegrated new functionality andtechnology xRepositioned the business (fees,compliance) Well-positioned for long-term growth and continued marginexpansion BankMobile Evolution and Continued GrowthElements 2018 –2019: Business Model and ProductInnovation xPartnered to develop T-MobileMONEY Partnerships Platform xFocused on expanding B2B2Cstrategy xCollaboration with Google Payannounced August 3 rd –Will plan to launch in2021 xContinue to acquire new Higher-Edclients xFurther expand within existing customerbase xAdd additional White-LabelPartners xInvest in strategic M&Aopportunities Long-Term Growth xBankMobile invested heavily to create its Banking-as-a-Service xBuilt out the technological infrastructure to roll out white-label checking, savings, Point-of-Sale (“POS”) financing, credit card, personal loans and studentrefinance Investment Technology Direct-To- Consumer Higher-Ed Higher-Ed Higher-Ed Higher-Ed Pipeline of White-Label and StrategicPartnerships Today Note:BMTechnologiesisNotaBankanddoesnotprovidebankingservices.BankMobileisatechnologyproviderthatfacilitatesdepositsandbankingservices betweenacustomerandanFDICinsuredpartnerbank.Anyreferenceinthis presentation to “banking” or “banking services” is in reference to BankMobile providing services between a customers and a partner bank. The BankMobile brand and trademark is only used in reference to services being provided between a customerandanFDICinsuredpartnerbank.TheBankMobilebrandisonlyusedinreferencetoservicesprovidedincollaborationwithanFDICinsuredsponsorbank.

|10 ▪ Megalith Financial Acquisition Corp (NYSE: MFAC) has entered into a definitive agreement to acquire BankMobile Technologies ▪ This transaction is subject to customary regulatoryapprovals Transaction Structure (1) ▪ Transaction valued at an implied post-money enterprise value of $140mm (2) , which equates to 1.3x multiple on 2021E Revenue of $104.0mm (3) 6.5x multiple on 2021E EBITDA of $21.5mm (3) Valuation ▪ Transaction to be funded through a combination of MFAC common stock, cash held in the MFAC trust account, proceeds received from newly issued shares through a PIPE transaction and assumed debt of $40mm (2) ▪ Pro forma net leverage of 2.1x based upon 2020E Adjusted EBITDA of $6.3mm (3)(4) Cap Structure &Leverage ▪ MFAC public equity investors (original SPAC investors) are expected to own 28.3% of the combined (5) ▪ Shares issued to PIPE Investors are expected to own 25.0% (5) ▪ Customers Bank is expected to own 46.7% (5) Pro FormaOwnership ▪ MFAC will remain a Delaware corporation, and as the post-closing company will remain listed on theNYSE ▪ The public company will be renamed BM Technologies,Inc. Listing 1) 2) 3) See “Proposed Transaction Structure” on slide 38 and “Proposed Capitalization and Ownership” on slide37 4) See “Proposed Capitalization and Ownership” on slide 37 for calculation; Reflects debt prior to partial paydown from cash in MFAC’s trustaccount 5) Forecasted Revenue, EBITDA and Adjusted EBITDA set forth on “Income Statement History and Forecast“ and “Reconciliation to Non-GAAP Financial Measures” on slides 22, 30 and 39,respectively Net leverage defined as net debt at closing / 2020E forecasted adjusted EBITDA; See “Reconciliation to Non-GAAP Financial Measures” on slides 39 and 40 See ownership table on slide 37 “Proposed Capitalization and Ownership”; Assumes the full $33.2 million cash held in the trust account by MFAC related to existing MFAC public stockholders will not be redeemed upon Transaction closing, shares will remain outstanding and cash willbeavailable for use in the Transaction; Assumes aggregate PIPE investment of $20.0mm; See slide 37 for materialassumptions BankMobile Evolving into a PremierBrand

|11 TransactionBackground Why is BankMobile Technologies (“BMT”) Being Divested? Why is BMT Positioned as an IndependentCompany? BMT -A standalone subsidiary of CustomersBank Banking-as-a-Service ▪Remove Growth Constraints overlaid byparent ▪Aligns management, board and investors primary focus without distraction of otherbusinesses ▪As independent entity, BMT will more easily establish new bank partners who will enable BMT to offer credit and other financial products to existingcustomers. ▪The legacy of being owned by a bank provides the core expertise and systems to safely, securely plug into new BaaS users that require such expertise without the limitations imposed by being owned by a regulatedentity ▪BMTbecomesastandaloneFinTechcompanywithits owncapitalsourcesandsectorvaluationmetrics;and notgovernedbybankvaluations Reasons forDivestment A.BankMobile Technologies (“BMT”), a subsidiary of Customers Bank (“Customers”), will be subject to reduced interchange income if it remains wholly-owned by CUBI, due to the Durbin Amendment (part of Dodd- Frank banking reform of 2011). When a bankcrosses $10b in assets on December 31 st , it becomes subject to the Durbin Amendment, and interchange income is significantly reduced. Customers is now subject to the DurbinAmendment. B.Customers Bancorp (“CUBI”) has made recent strategic decisions to focus on its largest commercial lending lines of business. BMT is a smaller operating unit which focuses on retail deposit customers and retail banking- as-a-service (BaaS); BMT does not fit CUBI’s core commercial banking focus and is beingdivested. C.From a regulatory and business focus point of view,CUBI wishes to be a “Business oriented Community Bank.” . A. “Durbin Fee Challenge” B. Realigned Priorities &Focus C.Regulation 1) Customers is divesting BankMobile Technologies 2) BMT will also have debt outstanding held by CUBI in amount of $40 (1) million; which is also part of the purchase price paid (it is BM Technologies Inc.’s intention to pay off the debt as soon aspossible) 3) Customers will contractually agree to provide the same Deposit Related Fees and Durbin Exempt Interchange Rate (Fees) through 2022 to enable BMT a stable “runway” of revenue while BMT establishes additional bank partnerships to replaceCUBI See Proposed Capitalization and Ownership and Proposed Transaction Structure on pages 37 and 38, respectively ▪BMT can more easily delivers a full-service, centralized and customer-centric experience while alleviating the back-office and administrative burden for white-label partners ▪Better positioned to capitalize on trends away from branch basedbanking Transaction Related Independent Platform BetterPositioned Customers Bank (“CUBI”) is divestingBMT 1 2 3 Note: Framework based on full divestiture from the parentbank 1) Reflects debt prior to partial paydown from cash in MFAC’s trustaccount

Business Overview

|13 Key InvestmentHighlights High-Volume, Low-Cost, Customer AcquisitionStrategy 2 Our “Bank-as-a-Service” Delivers a Full-Featured Digital Banking Platform toPartners 4 Opportunity to Disrupt Massive U.S. BankingMarket 1 Highly-Attractive BusinessModel 7 Attractive Distribution Channel Through Market Leadership Position in HigherEducation 6 5 Unique CompetitivePosition 3 Collaborations with Large, Highly AttractiveBrands

|14 Opportunity to Disrupt Massive U.S. BankingMarket 1) Source: USBL “Banks Ranked by Total Assets”, June2019. BankMobile is able to capture deposits for Partner Banks from the dissatisfied customers of big banks and undercut smaller banks struggling with customeracquisition COMMUNITYBANKS (<$1B ASSETS) MEGA BANKS ($1T+ASSETS) SUPER-REGIONAL BANKS ($250B-$1TASSETS) CORE REGIONAL BANKS ($50B-$250BASSETS) SMALL REGIONAL BANKS ($10B-$50BASSETS) MICROBANKS ($1B-$10BASSETS) TOP ~0.2%OF BANKS COVER ~50%OF ASSETS ALL OTHER BANKS COVER REMAINING ~50% 1 Banks Have Consolidated, but Fragmentation RemainsHigh Industry-wide headwinds have driven significant asset consolidation, with big banks holding 50% of deposits and struggling with customer satisfaction while the 99.8% of other banks hold the other 50% of deposits, yet struggle to acquire customers at a lowcost Asset Concentration in Banking,June2019 (1) The BankMobileSolution BankMobile is pairing with white-label partners and partner banks to beat large and small banks through high-volume, low-cost customer acquisition driven by its full-featured BaaSplatform

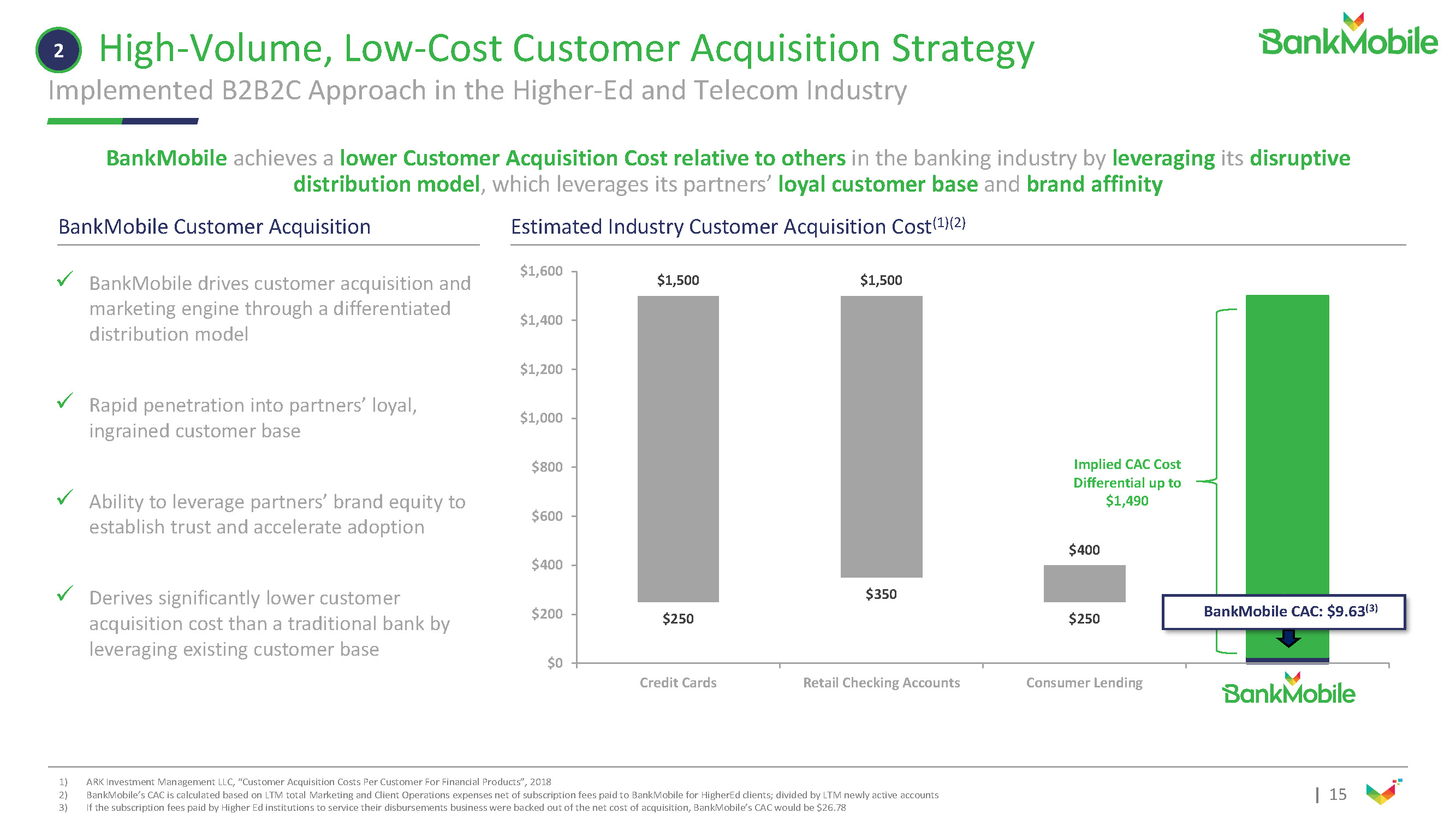

|15 $250 $350 $250 $1,500 $1,500 $400 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 CreditCards Retail CheckingAccounts ConsumerLending High-Volume, Low-Cost Customer AcquisitionStrategy Implemented B2B2C Approach in the Higher-Ed and TelecomIndustry BankMobile achieves a lower Customer Acquisition Cost relative to others in the banking industry by leveraging itsdisruptive distribution model, which leverages its partners’ loyal customer base and brandaffinity BankMobileCustomerAcquisition Estimated Industry Customer AcquisitionCost (1)(2) 1) ARK Investment Management LLC, “Customer Acquisition Costs Per Customer For Financial Products”,2018 2) BankMobile’sCACiscalculatedbased onLTMtotalMarketingandClientOperationsexpensesnetofsubscriptionfeespaidtoBankMobileforHigherEdclients;divided byLTMnewly activeaccounts 3) If the subscription fees paid by Higher Ed institutions to service their disbursements business were backed out of the net cost of acquisition, BankMobile’s CAC wouldbe $26.78 x BankMobile drives customer acquisition and marketing engine through a differentiated distributionmodel x Rapid penetration into partners’loyal, ingrained customerbase x Ability to leverage partners’ brand equityto establish trust and accelerateadoption x Derives significantly lower customer acquisition cost than a traditional bank by leveraging existing customerbase 2 Implied CACCost Differential upto $1,490 BankMobile CAC:$9.63 (3)

|16 • BankMobile and T-Mobile partnered to launch T-Mobile MONEY in2019 • Offers no account fees and 4% interest on balances up to $3k for T-Mobilecustomers RelationshipOverview Win –WinRelationship x Strong customer retention program forT-Mobile x New BankMobile customers (deposits for PartnerBanks) PartnershipHighlights “Traditional banks aren’t mobile-first, and they’re definitely not customer-first. As more and more people use their smartphones to manage money, we saw an opportunity to address another customer pain point,” said John Legere, former CEO of T-Mobile (April 2019) (1) 1) PerT-Mobilepressrelease;Bye,“BigBanks.Hello,T-MobileMONEYIntroducingYourNo-Fee,Interest-Earning,Mobile-FirstCheckingAccount”–April18 th ,2019 3a Collaborations with Large, Highly AttractiveBrands White-Label Banking Case Study: T-MobileMONEY

|17 On August 3 rd 2020, BankMobile announced an execution of an agreement with Google to introduce digital bankaccounts Highlights x Google Pay will provide the front-end userexperience x The product will be built upon BankMobile’s existing bankinginfrastructure x Product will be offered through BankMobile’s existing higher education distribution channel which serves approximately one in three college students through relationships with 722campuses x Planned launch in2021 Win –WinRelationship x Increase the percentage of college students that choose to receive a disbursement through the opening of a BankMobileaccount x Provide students new tools that will assist in budgeting and offer personal financialinsights PartnershipHighlights “Google is excited to partner with BankMobile in enabling a digital experience that is equitable for all and meets the evolving needs of a new generation of customers. We believe that we can use our technology expertise to benefit users, banks and the entire financial ecosystem.” -Felix Lin, Vice President at Google (August 2020) (1) “We are thrilled to be collaborating with Google to offer our student customers enhanced digital bank accounts. Many of our student customers today are struggling to manage their money as they work part-time and attend school. Through our collaboration with Google we believe we can provide these students with the appropriate financial tools to helpthem navigate through these difficult situations successfully” –Luvleen Sidhu, CEO, BankMobile (August 2020) (1) 3b Collaborations with Large, Highly AttractiveBrands Recently Announced Collaboration with GooglePay Relationship Overview 1) Source per PressRelease: BankMobile Announces a Collaboration to Offer Digital Bank Accounts –8/3/2020

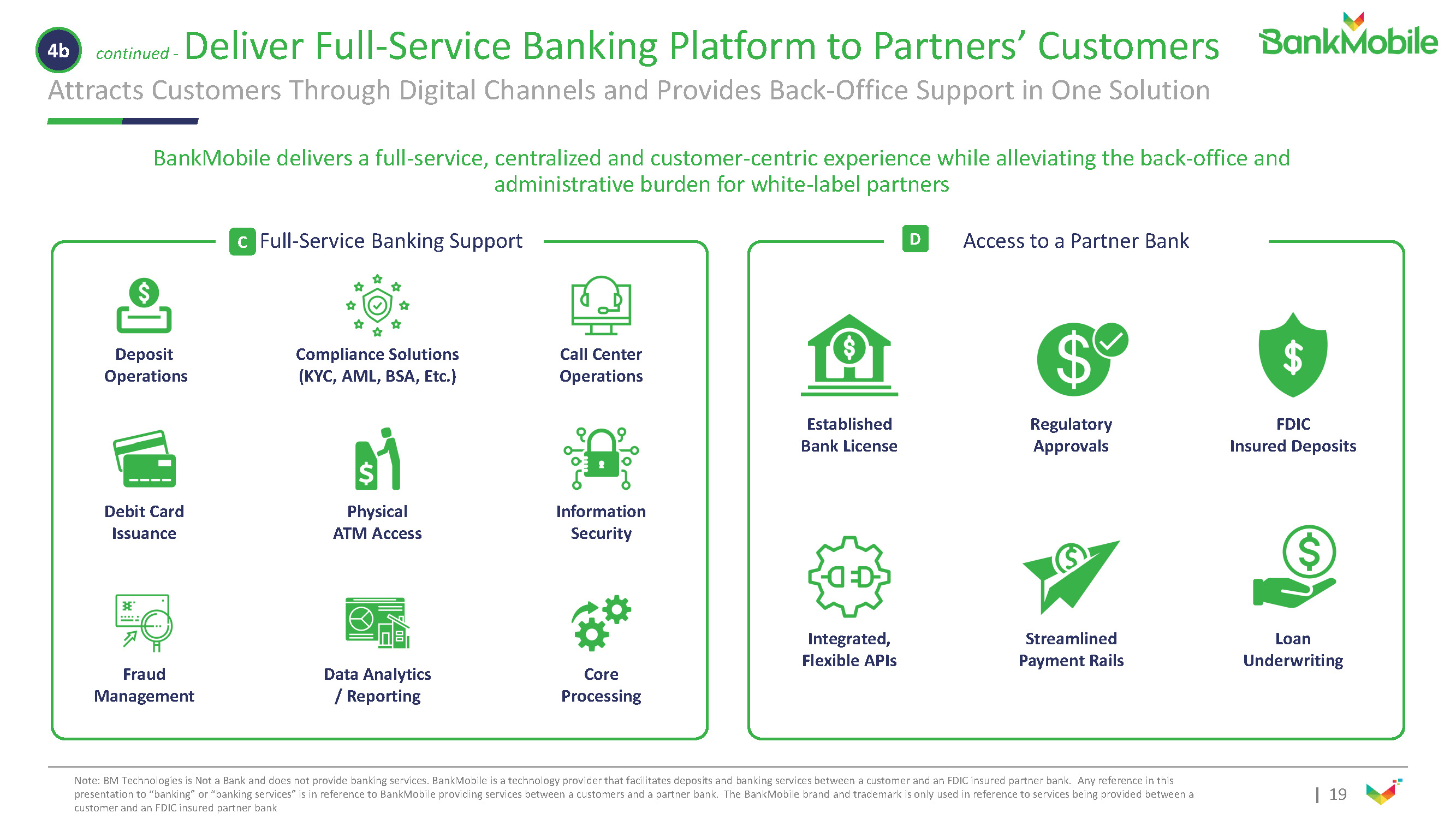

|18 Core BankingSystems Payments Checking Savings Credit AzureCloud Digital Activity Data Partner Data Bank Product Data x Alldigitalchannelsandbanktechnologiesdelivered includingmobile,web,Alexa,APIsandUSpayment systems x Out of the box capabilities supported including customer care, compliance, fraud mgmt., deposit / loan operations and debit cardprinting x Flexible connections to banks via partner-specific bankingAPIs “Bank as a ServiceOffering” Omni-Channel DigitalBanking Modern TechnologyPlatform Full-Service BankingSupport BankPartnerships x Frictionless onboarding and omni-channelapps x Full primary bank relationship support, including transfers, remote deposit capture, P2P, bill pay, ATMs, cash-in and physical/digital debitcards x Gamified cross-industry offers andperks x Near-real-time APIs with aggregated data enables partner-specialized, customer-centric experiences x Core banking systems provide primary account features at ultra-highreliability x Modern cloud enables consistent re-use across multiple partners, tested on millions ofaccounts 4a BankMobile Technologies Delivers a Full-Service Digital BankingPlatform Key Capabilities, Products and TechnologyPlatform A B C D BaaSOffering A A . Branded DigitalBanking Apps B B . Modern Cloud-Based TechnologyPlatform BankMobile brings the whole banktopartners… … with a tailored signup and brandedbankUX… … enabled by tech designed for partnerintegration Partner BaaS Customer HubAPIs Note:BMTechnologiesisNotaBankanddoesnotprovidebankingservices.BankMobileisatechnologyproviderthatfacilitates depositsandbankingservices betweenacustomerandanFDICinsuredpartnerbank.Anyreferenceinthis presentation to “banking” or “banking services” is in reference to BankMobile providing services between a customers and a partner bank. The BankMobile brand and trademark is only used in reference to services being provided between a customer and an FDIC insured partnerbank

|19 continued -Deliver Full-Service Banking Platform to Partners’Customers Attracts Customers Through Digital Channels and Provides Back-Office Support in OneSolution BankMobile delivers a full-service, centralized and customer-centric experience while alleviating the back-office and administrative burden for white-labelpartners Deposit Operations Compliance Solutions (KYC, AML, BSA,Etc.) Call Center Operations Physical ATMAccess DebitCard Issuance Information Security Fraud Management DataAnalytics /Reporting Core Processing Loan Underwriting Regulatory Approvals Established BankLicense Streamlined PaymentRails Integrated, FlexibleAPIs FDIC InsuredDeposits C C . Full-Service BankingSupport Access to a PartnerBank D 4b Note:BMTechnologiesisNotaBankanddoesnotprovidebankingservices.BankMobileisatechnologyproviderthatfacilitates depositsandbankingservices betweenacustomerandanFDICinsuredpartnerbank.Anyreferenceinthis presentation to “banking” or “banking services” is in reference to BankMobile providing services between a customers and a partner bank. The BankMobile brand and trademark is only used in reference to services being provided between a customer and an FDIC insured partnerbank

Deep experience in B2B2C banking Modern digital banking platform with customer- centric approach Ability to roll-out a bank to partners in months, notyears Providefullback-office supportforwhite-label partners Extreme partner tailoring to allow for seamless onboarding and customized perks Durbin advantage provides attractive interchange revenue sharepotential |20 RepresentativeFirms Competitive Differentiation TraditionalBanks “NeoBanks” Banking-as-a- Service Full-BaaS Model Complete digital banking platform including back office support (compliance, deposit operations, fraud management, customer care,etc.) 4 0 0 2 Revenue Share / Great ConsumerPrices Small bank interchange/big bankmaturity 4 0 0 3 Extreme PartnershipTailoring Deep customer experienceintegration 4 0 1 2 Fintech with Heavy BankingExperience Blend of innovation and strong bankingdiscipline 4 2 2 Speed toMarket Months to deploy full feature digital bankplatform 4 0 1 2 Complete Digital BankingPlatform Illustrative CompetitiveLandscape The BankMobileAdvantage 5 CompetitivePositioning

|21 Distribution Through Market Leadership Position inHigher-Ed Deeply Embedded Campus Relationships Allow for Customer Acquisition and “Customer for Life”Strategy U.S. Higher-Ed Student DisbursementMarketShare (1) Benefit of the Higher-EdBusiness x Access to ~1 in every 3 college students in theU.S. x Ability to create “customer for life” through selling additional financial services products as studentsgraduate x Proven scale generating $60M+ in annual revenues with ~2M accounts currently on the platform x Scalable technology distributing more than $10B of payments ayear Note: SSEs refers to Signed StudentEnrollment 1) 2) Per BankMobile’sinternalsalesdatabaseandestimatedstudentmarketsizebasedonSSEs NationalCenterforEducationStatistics.“EnrollmentandEmployeesinPostsecondaryInstitutions,Fall 2015;FinancialStatisticsAcademic Libraries, Fiscal Year 2015”, February2017 3) 4) 5) ~3M SSEs are considered non-addressable (beauty schools, trucking schools, etc.) RepresentsoneminustheannualSSEattritionoverbeginningoftheyearSSEcount Includescreditunions,regionalbanks,othersoftwareproviders,unknown,etc. Total Addressable Market is 20M students and replenishes everyyear (2)(3) 31% Software 19% Other (5) 18% 2% In-HouseCapabilities 30% Regionaland National Banks Payment Providers Exclusive, Long-Term and Contractual CampusRelationships x Long-term embedded university client base of 722campuses x SSE retention rate of over98% (4) x Average client tenure > 5years x Typical new contract term is 3 –5 years with auto-renewal periods of variouslengths x Active pipeline of ~1Mstudents x Expect prepaid providers to be a minimal threat as regulations have made it more difficult for prepaidoperators x BMT is in active implementation and negotiations on 2 new Partnerships that are intended to increase product offerings to schools and increase adoption of BMT products bySSEs. x BMT’s mix of SSE’s is weighted towards local, two-yearinstitutions x Management believes BMT’s segment exposure could perform better than more expensive, private, four-year schools, by offering a better value proposition particularly if remote learning becomes more common orrequired ? 87% of SSE at better value “public”schools ? Active pipeline of schools with ~1MSSEs RecentDevelopments 6

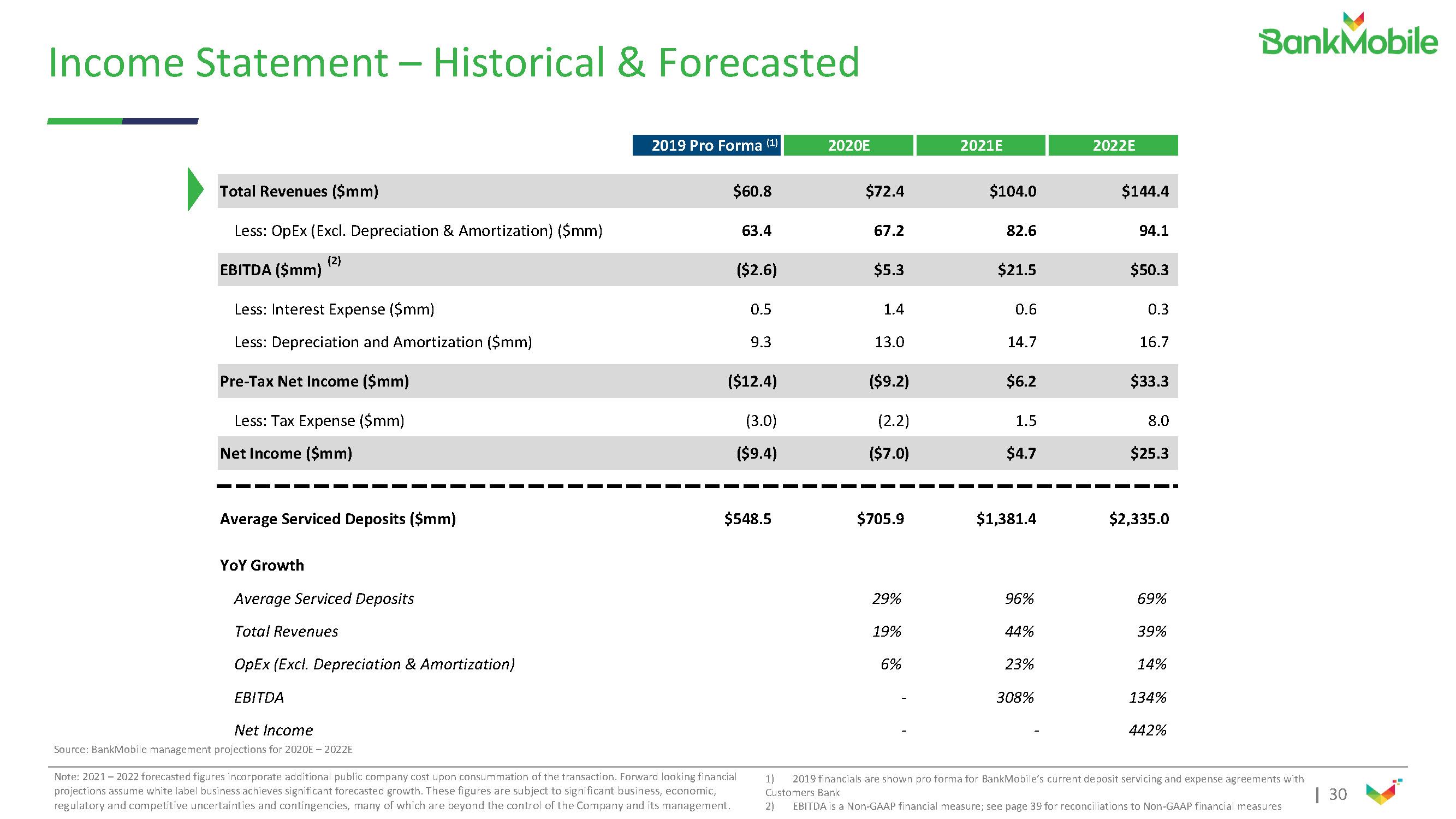

|22 Income Statement –Historical &Forecasted Source: BankMobile management projections for 2020E –2022E Note: 2021 –2022 forecasted figures incorporate additional public company cost upon consummation of the transaction. Forward looking financial projections assume white label business achieves significant forecasted growth. These figures are subject to significant business, economic, regulatoryandcompetitiveuncertaintiesandcontingencies,manyofwhicharebeyondthecontroloftheCompanyandits management. 1)2019 financials are shown pro forma for BankMobile’s current deposit servicing and expense agreements with Customers Bank 2) EBITDAisaNon-GAAPfinancialmeasure;seepage39forreconciliationstoNon-GAAPfinancialmeasures 2019 Pro Forma (1) 2020E 2021E 2022E Less: OpEx (Excl. Depreciation & Amortization)($mm) 63.4 67.2 82.6 94.1 (2) EBITDA($mm) ($2.6) $5.3 $21.5 $50.3 Less: Interest Expense($mm) 0.5 1.4 0.6 0.3 Less: Depreciation and Amortization($mm) 9.3 13.0 14.7 16.7 TotalRevenues($mm) $60.8 $72.4 $104.0 $144.4 Average ServicedDeposits 29% 96% 69% TotalRevenues 19% 44% 39% OpEx (Excl. Depreciation &Amortization) 6% 23% 14% EBITDA - 308% 134% Net Income - - 442% Historical & Projected IncomeStatementRevenue Breakout by MajorCategories CardRevenue OtherFees UniversityFees DepositServicing Fees Pre-Tax Net Income($mm) ($12.4) ($9.2) $6.2 $33.3 Less: Tax Expense($mm) (3.0) (2.2) 1.5 8.0 Net Income($mm) ($9.4) ($7.0) $4.7 $25.3 AccountFees Monthly account fees, wire fees andcard replacementfees Average Serviced Deposits($mm) $548.5 $705.9 $1,381.4 $2,335.0 YoY Growth Interchange and MasterCard incentive incomebased on card activity and out-of-network ATMfees Various nominal other fees, including fees associated with cashdeposits Subscription and transactional fees charged to colleges based on enrollment size, competitive marketplace and disbursement channels andoptions Fee charged to partner bank(s) based onaverage balances of serviceddeposits Highly Attractive BusinessModel 7

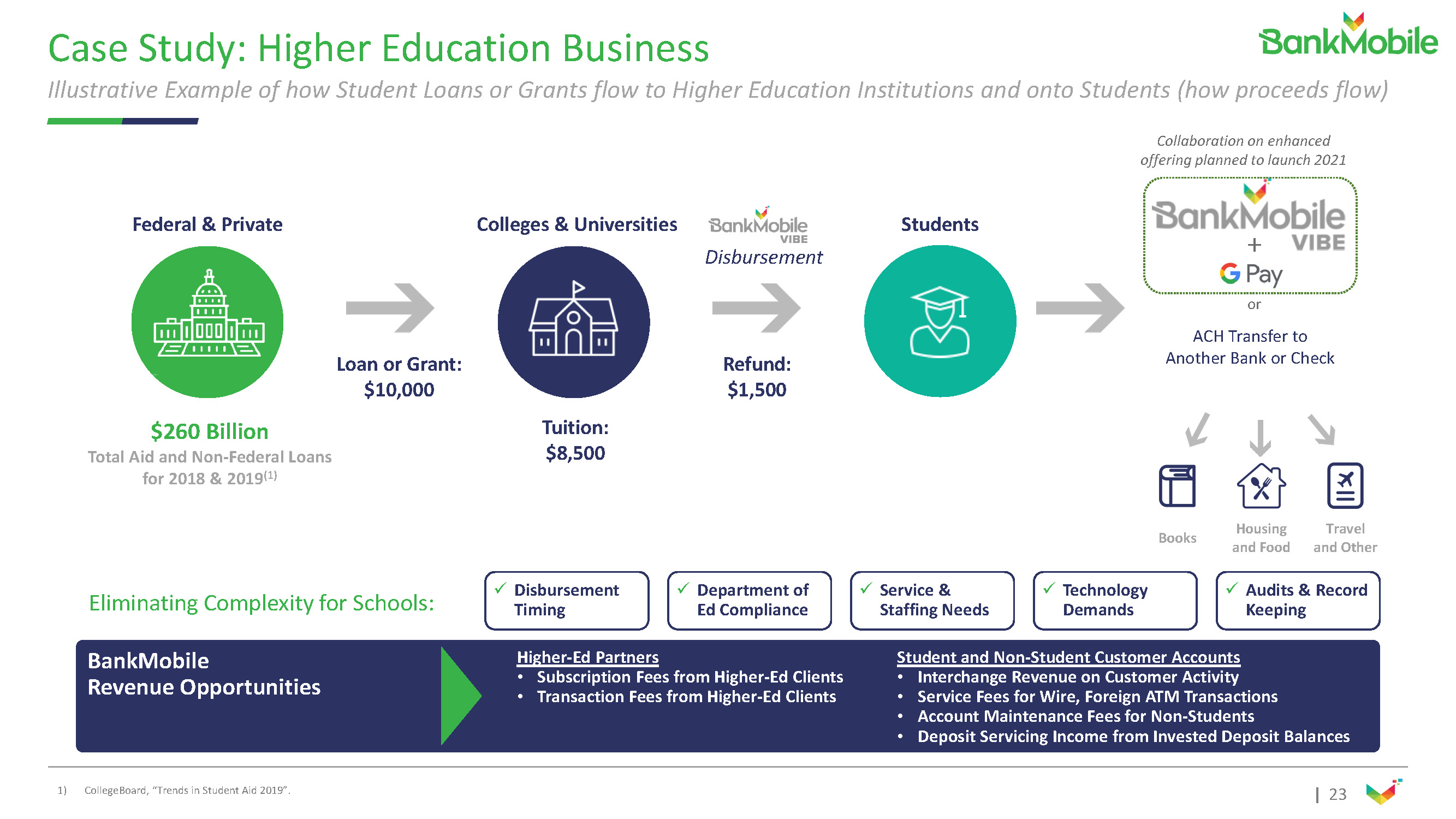

|23 Federal &Private Colleges &Universities Loan orGrant: $10,000 Refund: $1,500 $260Billion Total Aid and Non-Federal Loans for 2018 &2019 (1) Disbursement Tuition: $8,500 BankMobile RevenueOpportunities Higher-EdPartners • Subscription Fees from Higher-EdClients • Transaction Fees from Higher-EdClients Student and Non-Student CustomerAccounts • Interchange Revenue on CustomerActivity • Service Fees for Wire, Foreign ATMTransactions • Account Maintenance Fees forNon-Students • Deposit Servicing Income from Invested DepositBalances ACH Transfer to Another Bank orCheck Students 1) CollegeBoard, “Trends in Student Aid2019”. Travel andOther Housing andFood Books Eliminating Complexity forSchools: xDisbursement Timing xService & StaffingNeeds xDepartment of EdCompliance xAudits &Record Keeping xTechnology Demands or Collaboration on enhanced offering planned to launch2021 + Case Study: Higher EducationBusiness Illustrative Example of how Student Loans or Grants flow to Higher Education Institutions and onto Students (how proceedsflow)

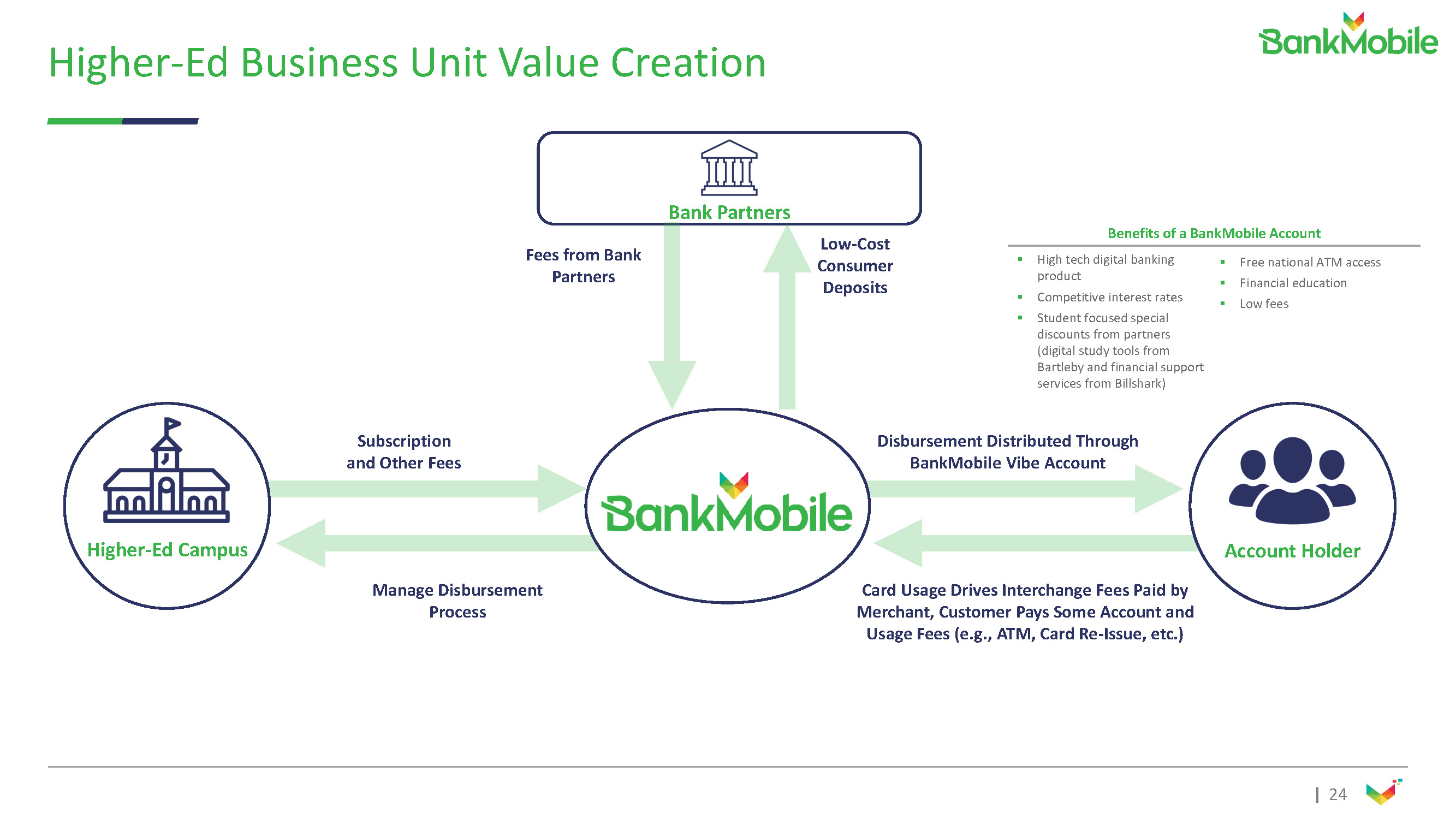

|24 Higher-Ed Business Unit ValueCreation Subscription and OtherFees Low-Cost Consumer Deposits ManageDisbursement Process Card Usage Drives Interchange Fees Paid by Merchant, Customer Pays Some Account and Usage Fees (e.g., ATM, Card Re-Issue,etc.) AccountHolder BankPartners Higher-EdCampus Fees fromBank Partners Benefits of a BankMobileAccount ▪ High tech digital banking product ▪ Competitive interestrates ▪ Student focused special discounts from partners (digital study tools from Bartleby and financial support services from Billshark) ▪ Free national ATMaccess ▪ Financialeducation ▪ Lowfees Disbursement Distributed Through BankMobile VibeAccount

|25 White-Label BaaS MarketOpportunity Key Market Attributes of TargetPartners Established Brand Equity Ability to leverage market-trusted image in co-branded marketing materials, as well as UX andApp Immense, Captive CustomerBase Massive, underserved customer bases provide a deep pipeline of sticky customers to marketto Diverse MarketingChannels Deeply ingrained marketing channels to promote co-branded platform and increaseawareness Numerous Natural CheckoutMoments Effortless, omni-channel checkout points retain customer dollars within the Banking-as-a-Serviceecosystem Strong Customer Loyalty Immensely loyal, existing customer base in need of financial and digitalbanking solutions 1) RepresentscustomerreachofidentifiedWhite-LabelprospectsinitiatedinpartnershipconversationswithBankMobile;BankMobileacknowledgesthatthereislikelytobecustomeroverlapamongstwhite-labelcustomersandindustryverticals >50Million Prospects ~150Million Prospects >200Million Prospects Massive Identified AddressableMarket ExistingIdentified Market Customer Pipeline related to New White- LabelPartners (1) TotalIdentified Market

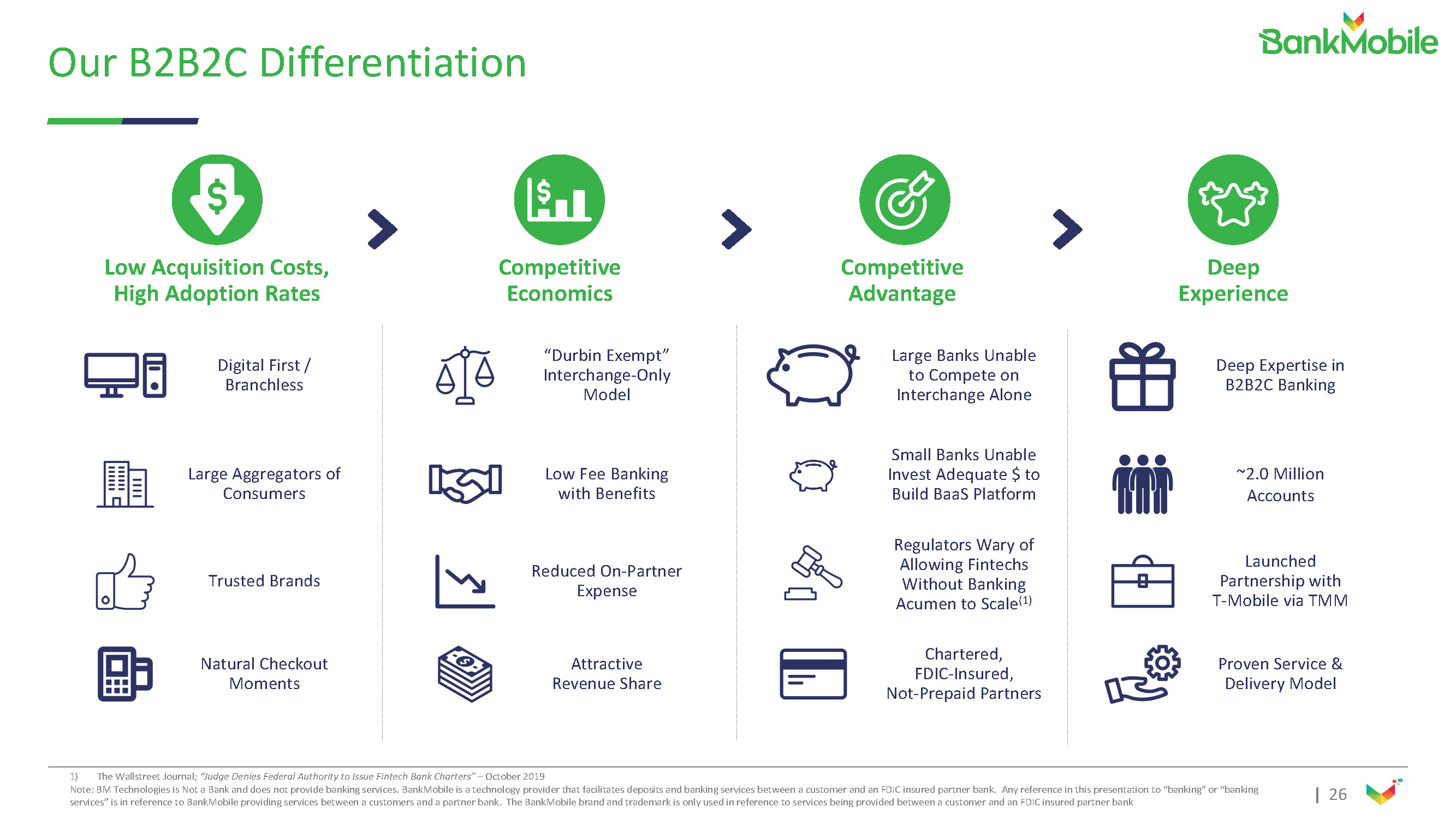

|26 Competitive Economics Deep Experience Launched Partnershipwith T-Mobile viaTMM Proven Service& DeliveryModel ~2.0Million Accounts Competitive Advantage Large BanksUnable to Compete on InterchangeAlone SmallBanksUnable InvestAdequate$to BuildBaaSPlatform Regulators Waryof Allowing Fintechs Without Banking Acumen toScale (1) Chartered, FDIC-Insured, Not-PrepaidPartners Low AcquisitionCosts, High AdoptionRates Digital First/ Branchless NaturalCheckout Moments Large Aggregatorsof Consumers Deep Expertisein B2B2CBanking TrustedBrands Our B2B2CDifferentiation “DurbinExempt” Interchange-Only Model Attractive RevenueShare Low FeeBanking withBenefits ReducedOn-Partner Expense 1) The Wallstreet Journal; “Judge Denies Federal Authority to Issue Fintech Bank Charters” –October2019 Note: BM Technologies is Not a Bank and does not provide banking services. BankMobile is a technology provider that facilitates deposits and banking services between a customer and an FDIC insured partner bank. Any reference in this presentation to “banking” or “banking services”isinreferencetoBankMobileproviding servicesbetweenacustomersand apartnerbank.TheBankMobilebrandand trademarkisonlyused in referencetoservicesbeingprovided betweenacustomerand anFDICinsured partnerbank

|27 Experienced ManagementTeam Vision and Experience toExecute ~24 Years Average Industry Experience ManagementTeam By theNumbers 309 FTEs (2) 1) 2019 LendIt Fintech Industry Awards 2) As of6/30/2020 BobRamsey Chief Financial Officer IndustryExperience 20+ Years RobertDiegel Chief OperatingOfficer Industry Experience 35+ Years WarrenTaylor Chief Customer Officer andCo-Founder Industry Experience 35+ Years RobertSavino Chief ProductOfficer Industry Experience 21+ Years Industry Recognition Most Innovative Bank LuvleenSidhu CEO andCo-Founder FinTechWoman of theYear (1) Industry Experience 9+Years AndrewCrawford Chief CommercialOfficer IndustryExperience 23+ Years RegineFiddler Chief MarketingOfficer Industry Experience 16+ Years Key IndustryExpertise FinTech Banking Compliance / Risk Management Operations Finance DigitalMarketing

CONFIDENTIAL|28 Tremendous Platform GrowthOpportunity Multiple Levers to AccelerateGrowth Expand Student Adoption and Create Long-Term Customer Relationships by Expanding Access to Credit Products Add New White-LabelPartners Strategic M&A Expand Distribution Channels and ProductOfferings x Drive strong organic growth by successfully executing on our customer acquisition and engagementstrategies x Continue RFP process and strategic discussions with vetted blue-chip, white-label partners to tap into their loyal customerbases x Distribute the platform through new channels to open up incrementalTAM x Capitalize on robust universe of marketplace lenders, Personal Financial Management (“PFM”) players, and vertical higher-ed software acquisitiontargets Further Expand Within Existing White-Label Partnerships x Continue to add newSSEs x Increase adoption rates through newpartnerships x Expand bank partnerships to expand access tocredit

Financial Information

|30 2019 Pro Forma (1) 2020E 2021E 2022E Total Revenues($mm) $60.8 $72.4 $104.0 $144.4 Less: OpEx (Excl. Depreciation & Amortization)($mm) 63.4 67.2 82.6 94.1 (2) EBITDA($mm) ($2.6) $5.3 $21.5 $50.3 Less: Interest Expense($mm) 0.5 1.4 0.6 0.3 Less: Depreciation and Amortization($mm) 9.3 13.0 14.7 16.7 Pre-Tax Net Income($mm) ($12.4) ($9.2) $6.2 $33.3 Less: Tax Expense($mm) (3.0) (2.2) 1.5 8.0 Net Income($mm) ($9.4) ($7.0) $4.7 $25.3 Average Serviced Deposits ($mm) $548.5 $705.9 $1,381.4 $2,335.0 YoYGrowth Average ServicedDeposits 29% 96% 69% TotalRevenues 19% 44% 39% OpEx (Excl. Depreciation & Amortization) 6% 23% 14% EBITDA - 308% 134% NetIncome Source: BankMobile management projections for 2020E –2022E - - 442% Income Statement –Historical &Forecasted 1)2019 financials are shown pro forma for BankMobile’s current deposit servicing and expense agreements with Customers Bank 2) EBITDAisaNon-GAAPfinancialmeasure;seepage39forreconciliationstoNon-GAAPfinancialmeasures Note: 2021 –2022 forecasted figures incorporate additional public company cost upon consummation of the transaction. Forward looking financial projections assume white label business achieves significant forecasted growth. These figures are subject to significant business, economic, regulatoryandcompetitiveuncertaintiesandcontingencies,manyofwhicharebeyondthecontroloftheCompanyandits management.

|31 Revenue 21% 2021E (4) • Signed Student Enrollments(“SSEs”) Source: BankMobilemanagement 1) Data as of the period end6/30/2020 2) Represents one minus the annual SSE attrition over beginning of the year SSEcount 3) Reflects last twelve-month data for the period end6/30/2020 $10.8bn Total Student Refund Dollars Processed (3) $663mm EoPServiced Deposits (1) $2.5bn Debit Spend (3) 4) Reflects forecasted full year 2021 data; Forecasted Revenue and EBITDA set forth on “Income Statement History and Forecast“ on slide 22 & 30; EBITDA is a Non- GAAP financial measure which can be reconciled on page 39; Forward looking financial projections assume white label business achieves significant forecasted growth. These figures are subject to significant business, economic, regulatory and competitive uncertainties and contingencies, many of which are beyond the control of the Company and itsmanagement >5mm * SSEs (1) BankMobile ServesApproximately 1 in 3 of all US CollegeStudents $61mm >2mm Accounts (1) 98% Higher-Ed Client Retention (by SSEs) (1)(2) LTM as of6/30/20 Revenue $104mm 2021E (4) EBITDAMargin Financial & OperatingHighlights BankMobile (BMT)’s Model has enabled it to establish a highly attractive financial & operatingprofile

|32 $401 $812 $1,601 $2,632 2019 ProForma (2) 2020E 2021E 2022E $60.8 $72.4 $104.0 $144.4 2019 ProForma (2) 2020E 2021E 2022E $525 $693 Q22019 Q22020 FinancialOverview Significant Growth and Scale Growth Drivers (1) Forecasted DepositGrowth ($ inmillions) $663 Q22019 Q22020 ($ inmillions) 33%CAGR RevenueProjection 45% $456 32% End of Period ServicedDeposits DebitSpend Projected End of Period ServicedDeposits ($ inmillions) ($ inmillions) 1) Data as of the quarter ended6/30/2020 2) 2019 financials are shown pro forma for BankMobile’s current deposit servicing and expense agreements with CustomersBank Projected AnnualRevenue 87%CAGR Note: 2021 –2022 forecasted figures incorporate additional public company cost upon consummation of the transaction. Forward looking financial projections assume white label business achieves significant forecasted growth. These figures are subject to significant business, economic, regulatory and competitive uncertainties and contingencies, many of which are beyond the control of the Company and itsmanagement.

|33 $69 $725 $209 $178 $400 $700 $550 $375 BankMobile Chime Varo Stash NuBank N26 Revolut Monzo 1.3x 7.4x 9.2x 6.2x 6.5x 18.7x 25.3x 13.0x Mobile & online B2B Payments& Prepaid ValuationOverview ▪ Enterprise Value multiples are valued at a significant discount when looking at 2021E EBITDAand revenue Public ComparableCompanies (1) Public Comparable Companies (1) EV / 2021E EBITDAMultiples B2B Payments & PrepaidComparables FleetCor 9.3x 16.8x Edenred 7.5x 18.5x WEX 4.9x 11.1x Bill.com 33.9x NM GreenDot 1.3x 6.4x EMLPayments 4.0x 13.0x Median 6.2x 13.0x EnterpriseValue/ 2021ERev. 2021EEBITDA Bank TechComparables FIS 8.0x 17.6x Intuit 9.3x 23.3x Fiserv 5.6x 14.4x ADP 4.0x 17.0x JackHenry 7.4x 24.0x Temenos 11.0x 26.7x Q2 11.3x NM ACIWorldwide 3.0x 11.0x Bottomline Tech. 4.4x 19.7x Median 7.4x 18.7x Mobile & OnlineComparables PayPal 9.0x 31.5x Shopify 37.2x NM Square 9.2x NM AdyenNV 45.9x NM Pagseguro 7.6x 19.2x Median 9.2x 25.3x EV / 2021E RevenueMultiples Source: Capital IQ & FactSet Research Systems, Inc.; Market data as of8/4/2020 Note: Multiples exclude valuations less than 0.0x and greater than 50.0x; Peer data reflects consensusestimates 1) 2) Reflects median values for comparable companies in each respective industry ForecastedRevenueandEBITDAaresetforthon“IncomeStatementHistoryandForecast“onslide22&30;EBITDA isaNon-GAAPfinancialmeasurewhichcanbereconciled onpage39 Mobile & online B2BPayments& BankMobile (2) BankTech Prepaid BankMobile (2) BankTech Average:$448mm Valuation ($mm) Accounts (3) (millions) $140mm $5,800mm $418mm $800mm $10,000mm $3,500mm $5,500mm $1,500mm 2mm 8mm 2mm 5mm 25mm 5mm 10mm 4mm ▪ Private market valuations for US and Int’l Neobanks using disclosed valuations and number of accounts (3) Valuation / Customers($mm) 3) FT Partners Research, “The Rise of Challenger Banks”, Business Insider, TechCrunch and Bloomberg; References to number of customers is assumed to applyaccounts

|34 InvestmentThesis Unique Opportunity to Invest in a Premier Brand Positioned for SignificantGrowth Strong FinancialProfile ~$72M 2020ERevenue 19% 2020E RevenueGrowth RapidMarket Expansion Positioned For SignificantGrowth New White-Label PartnerAdditions Distribution Channel and ProductOffering Expansion Best-in-Class DigitalBank Sophisticated Capabilities Dynamic ConsumerData Frictionless Onboarding Powerful CustomerAcquisition Proprietary Infrastructure Recognized MarketLeader Among theLargest Digital Banking Platforms Full Suite ofBanking Products Through PartnerBanks Proprietary“BaaS” Technology Planned 2021Launch of Collaboration with GooglePay High Volume, Low Cost AcquisitionModel ~$812M 2020E EoPDeposits 29% 2020E Avg. DepositGrowth 27% 2020E Debit SpendGrowth StrategicM&A White-LabelPartner Expansion Higher-Ed White-Label Partnerships Workplace Banking

Appendix

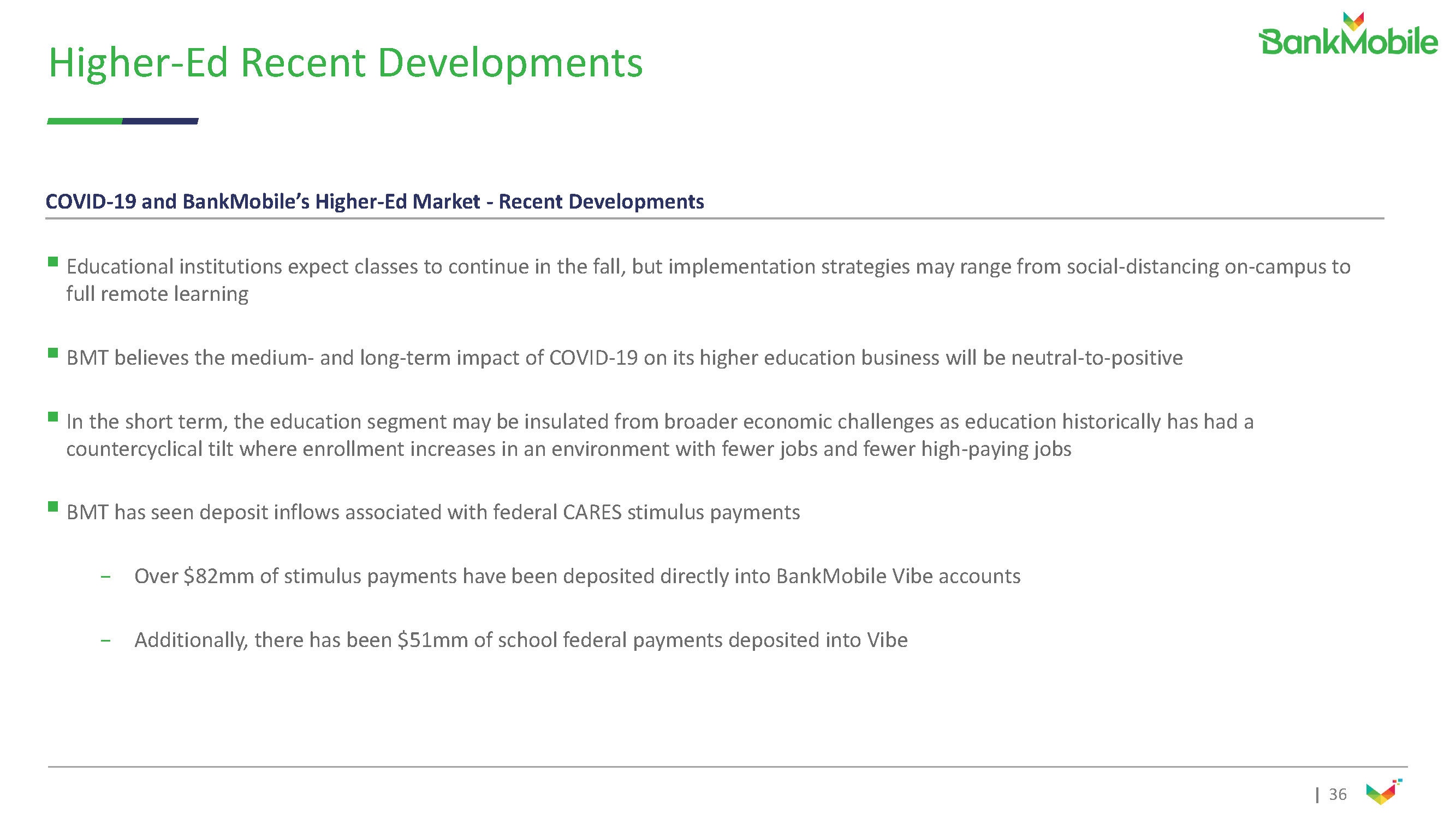

|36 Higher-Ed RecentDevelopments COVID-19 and BankMobile’s Higher-Ed Market -RecentDevelopments ▪Educational institutions expect classes to continue in the fall, but implementation strategies may range from social-distancing on-campus to full remotelearning ▪BMT believes the medium-and long-term impact of COVID-19 on its higher education business will beneutral-to-positive ▪In the short term, the education segment may be insulated from broader economic challenges as education historically has had a countercyclical tilt where enrollment increases in an environment with fewer jobs and fewer high-payingjobs ▪BMT has seen deposit inflows associated with federal CARES stimuluspayments - Over $82mm of stimulus payments have been deposited directly into BankMobile Vibeaccounts - Additionally, there has been $51mm of school federal payments deposited intoVibe

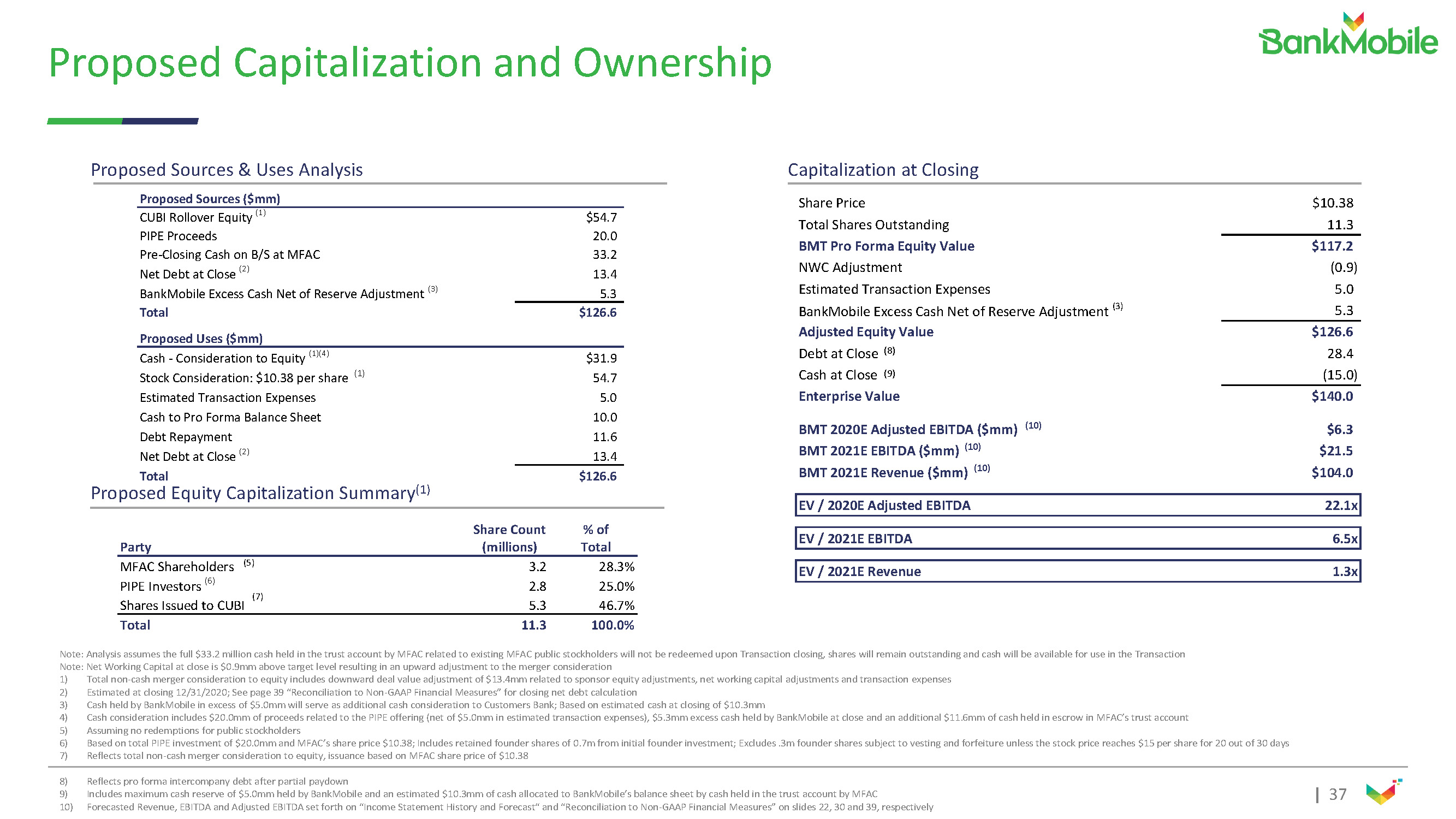

|37 Proposed Capitalization andOwnership 8) Reflects pro forma intercompany debt after partialpaydown 9) Includes maximum cash reserve of $5.0mm held by BankMobile and an estimated $10.3mm of cash allocated to BankMobile’sbalance sheet by cash held in the trust account by MFAC 10) ForecastedRevenue, EBITDAand Adjusted EBITDA setforthon“IncomeStatementHistoryandForecast“and“ReconciliationtoNon-GAAPFinancialMeasures”onslides22,30 and39,respectively Proposed Sources & UsesAnalysis Total Proposed Equity CapitalizationSummary (1) Capitalization atClosing SharePrice $10.38 Total SharesOutstanding 11.3 BMT Pro Forma EquityValue $117.2 NWCAdjustment (0.9) Estimated Transaction Expenses 5.0 Proposed Sources($mm) CUBI Rollover Equity (1) $54.7 PIPE Proceeds 20.0 Pre-Closing Cash on B/S atMFAC 33.2 Net Debt at Close (2) 13.4 BankMobile Excess Cash Net of Reserve Adjustment (3) Total 5.3 $126.6 Proposed Uses($mm) $31.9 54.7 5.0 Cash -Consideration to Equity (1)(4) Stock Consideration: $10.38 per share (1) Estimated TransactionExpenses Cash to Pro Forma BalanceSheet 10.0 DebtRepayment 11.6 Net Debt at Close (2) 13.4 $126.6 BankMobile Excess Cash Net of Reserve Adjustment (3) Adjusted EquityValue Debt at Close (8) Cash at Close (9) EnterpriseValue 5.3 $126.6 28.4 (15.0) $140.0 BMT 2020E Adjusted EBITDA ($mm) (10) BMT 2021E EBITDA ($mm) (10) BMT 2021E Revenue ($mm) (10) $6.3 $21.5 $104.0 EV / 2020EAdjustedEBITDA 22.1x EV /2021EEBITDA 6.5x EV /2021ERevenue 1.3x ShareCount %of Party (millions) Total 3.2 2.8 28.3% 25.0% SharesIssuedtoCUBI 5.3 46.7% Total 11.3 100.0% Note: Analysis assumes the full $33.2 million cash held in the trust account by MFAC related to existing MFAC public stockholders will not be redeemed upon Transaction closing, shares will remain outstanding and cash will be available for use in the Transaction Note: Net Working Capital at close is $0.9mm above target level resulting in an upward adjustment to the mergerconsideration 1) Total non-cash merger consideration to equity includes downward deal value adjustment of $13.4mm related to sponsor equity adjustments, net working capital adjustments andtransaction expenses 2) Estimated at closing 12/31/2020; See page 39 “Reconciliation to Non-GAAP Financial Measures” for closing net debtcalculation 3) Cash held by BankMobile in excess of $5.0mm will serve as additional cash consideration to Customers Bank; Based on estimated cash at closing of$10.3mm 4) Cashconsiderationincludes$20.0mmofproceedsrelatedtothePIPEoffering(netof$5.0mminestimatedtransactionexpenses),$5.3mmexcesscashheldby BankMobileatcloseand anadditional$11.6mm ofcashheld in escrowinMFAC’strustaccount 5) Assuming no redemptions for publicstockholders 6) BasedontotalPIPEinvestmentof$20.0mm andMFAC’sshareprice$10.38;Includesretainedfoundersharesof0.7m frominitialfounderinvestment;Excludes.3m foundersharessubjecttovestingandforfeitureunlessthestockpricereaches$15persharefor20 outof30 days 7) Reflects total non-cash merger consideration to equity, issuance based on MFAC share price of$10.38 MFAC Shareholders (5) PIPE Investors (6) (7)

|38 Proposed TransactionStructure MFAC Public shareholders have the optionto: (a) continue to own, in connection withthe closing, MFAC sharesor (b) redeem shares for a portion ofthe $33.2mm intrust Megalith Financial AcquisitionCorp. (“Purchaser” or“MFAC”) (NYSE listed company to berenamed BM Technologies,Inc.) (“MFACSponsor”) MFAC Public Shareholders MFACSponsor Members (1) PIPEInvestment PIPEInvestors BankMobileTechnologies, Inc. (“TheCompany”) MFAC Sponsor and Investors contribute capital to single PIPE investment; MFACSponsor relinquishes “Class B”shares Customers Bancorp,Inc (“CUBI”) CustomersBank (“Seller of Company”;“Lender toCompany”) CUBI owns 100% of CustomersBank MFAC issues shares and cash to Customers Bank, the sole stockholder ofBankMobile Shares in theCompany Obligation ona $40mmCredit Facility (1) MFAC Sponsor transfers additional “Class B” shares to CUBI as part of the aggregatedconsideration BankMobile merges into MFAC Merger SubInc. Shares inMFAC issued forcash Prior to Transaction closing, 100% ownership of BankMobile Technologies,Inc. MFAC Merger SubInc. MFAC Merger Sub Inc. established as a wholly- owned subsidiary ofMFAC

|39 Reconciliation to Non-GAAP Financial Measures Source: BankMobile managementprojections Note: 2021 –2022 forecasted figures incorporate additional public company cost upon consummation of the transaction. Forward looking financial projections assume white label business achieves significant forecasted growth. These figures are subject to significant business, economic, regulatory and competitive uncertainties and contingencies, many of which are beyond the control of the Company and itsmanagement. ($ shown inmillions) 2019 Pro Forma (1) 2020E 2021E 2022E Pre-Tax NetIncome ($12.4) ($9.2) $6.2 $33.3 Addback of Interest Expense (2) 0.5 1.4 0.6 0.3 Addback of Depreciation &Amortization 9.3 13.0 14.7 16.7 EBITDA ($2.6) $5.3 $21.5 $50.3 Addback of Merger RelatedExpenses 0.1 0.1 0.0 0.0 Addback of DOESettlement 1.0 1.0 0.0 0.0 Adjusted EBITDA ($1.5) $6.3 $21.5 $50.3 EBITDA ($2.6) $5.3 $21.9 $50.7 Revenue 60.8 72.4 104.0 144.4 EBITDAMargin (4%) 7% 21% 35% 1) 2019 financials are shown pro forma for BankMobile’s current deposit servicing and expense agreements with CustomersBank 2) Reflects cost of intercompanydebt .

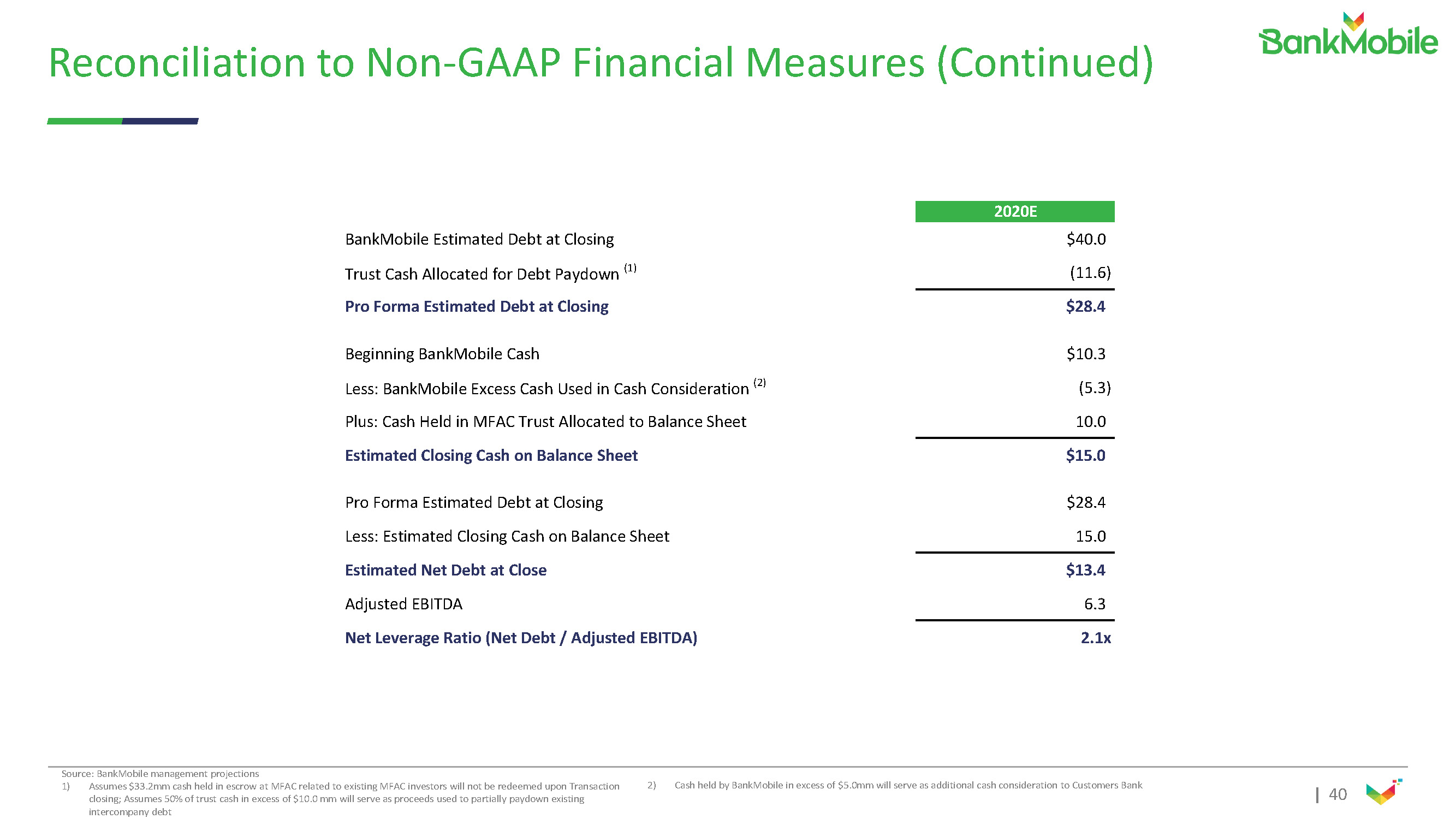

|40 Reconciliation to Non-GAAP Financial Measures(Continued) Source: BankMobile managementprojections 1) Assumes $33.2mm cash held in escrow at MFAC related to existing MFAC investors will not be redeemed upon Transaction closing; Assumes 50% of trust cash in excess of $10.0 mm will serve as proceeds used to partially paydown existing intercompanydebt 2020E BankMobile Estimated Debt atClosing $40.0 Trust Cash Allocated for Debt Paydown (1) (11.6) Pro Forma Estimated Debt atClosing $28.4 Beginning BankMobileCash $10.3 Less: BankMobile Excess Cash Used in Cash Consideration (2) (5.3) Plus: Cash Held in MFAC Trust Allocated to BalanceSheet 10.0 Estimated Closing Cash on BalanceSheet $15.0 Pro Forma Estimated Debt atClosing $28.4 Less: Estimated Closing Cash on BalanceSheet 15.0 Estimated Net Debt atClose $13.4 AdjustedEBITDA 6.3 Net Leverage Ratio (Net Debt / AdjustedEBITDA) 2.1x 2) Cash held by BankMobile in excess of $5.0mm will serve as additional cash consideration to CustomersBank