Table of Contents

Exhibit 99.3

2019 Annual Audited

Financial Statements

Table of Contents

Statements

| 76 | ||||||||

| 77 | ||||||||

| 77 | ||||||||

| 78 | ||||||||

| 79 | ||||||||

| 80 | ||||||||

| 81 | Note 1 | |||||||

| 81 | Note 2 | |||||||

| P,E | 82 | Note 3 | ||||||

| P,E | 86 | Note 4 | ||||||

| 90 | Note 5 | |||||||

| P,E | 90 | Note 6 | ||||||

| 92 | Note 7 | |||||||

| 93 | Note 8 | |||||||

| P,E | 93 | Note 9 | ||||||

| P | 97 | Note 10 | ||||||

| 97 | Note 11 | |||||||

| P | 98 | Note 12 | ||||||

| P,E | 103 | Note 13 | ||||||

| P,E | 104 | Note 14 | ||||||

| P,E | 105 | Note 15 | ||||||

| P,E | 109 | Note 16 | ||||||

| P,E | 111 | Note 17 | ||||||

| 113 | Note 18 | |||||||

| 113 | Note 19 | |||||||

| 114 | Note 20 | |||||||

| 115 | Note 21 | |||||||

| 116 | Note 22 | |||||||

| P,E | 116 | Note 23 | ||||||

P,E | 121 | Note 24 | Asset Retirement Obligations and Accrued Environmental Costs | |||||

| 123 | Note 25 | |||||||

| 124 | Note 26 | |||||||

| 125 | Note 27 | |||||||

| P | 126 | Note 28 | ||||||

| 127 | Note 29 | |||||||

| E | 127 | Note 30 | ||||||

| P,E | 129 | Note 31 | ||||||

| P | Includes Accounting Policies |

| E | Includes Accounting Estimates and Judgments |

Table of Contents

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Management’s

Responsibility

Management’s Responsibility for Financial Reporting

Management’s Report on Financial Statements

The accompanying consolidated financial statements and related financial information are the responsibility of the management of Nutrien Ltd. (the “Company”). They have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”) and include amounts based on estimates and judgments. Financial information included elsewhere in this report is consistent with the consolidated financial statements.

The consolidated financial statements are approved by the Board of Directors on the recommendation of the audit committee. The audit committee of the Board of Directors is composed entirely of independent directors. The audit committee discusses and analyzes Nutrien’s interim condensed consolidated financial statements and Management’s Discussion and Analysis (“MD&A”) with management before such information is approved by the committee and submitted to securities commissions or other regulatory authorities. The audit committee and management also analyze the annual consolidated financial statements and MD&A prior to their approval by the Board of Directors.

The audit committee duties also include reviewing critical accounting policies and significant estimates and judgments underlying the consolidated financial statements as presented by management and approving the fees of our independent registered public accounting firm.

Our independent registered public accounting firm, KPMG LLP, performs an audit of the consolidated financial statements, the results of which are reflected in their report for 2019 included on Page 74. KPMG LLP have full and independent access to the audit committee to discuss their audit and related matters.

Management’s Annual Report on Internal Control over Financial Reporting

Management is responsible for establishing and maintaining adequate internal control over financial reporting, as defined in Rules13a-15(f) and15d-15(f) of the Exchange Act, as amended, and National Instrument52-109 – Certification of Disclosure in Issuers’ Annual and Interim Filings. Internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and preparation of financial statements for external purposes in accordance with IFRS.

Under our supervision and with the participation of management, the Company conducted an evaluation of the design and effectiveness of our internal control over financial reporting as of the end of the fiscal year covered by this report, based on the framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”) in Internal Control – Integrated Framework (2013). Based on this evaluation, management concluded that, as of December 31, 2019, the Company did maintain effective internal control over financial reporting.

We completed the Ruralco acquisition on September 30, 2019 as more fully described in Note 4 of the Notes to the Consolidated Financial Statements. This business was excluded from management’s evaluation of the effectiveness of the Company’s internal controls over financial reporting as of December 31, 2019 due to the proximity of the acquisition toyear-end. The associated total assets represent approximately 2 percent of consolidated total assets and total revenues represent approximately 1 percent of consolidated revenues included in Nutrien’s 2019 consolidated financial statements.

The effectiveness of the Company’s internal control over financial reporting as at December 31, 2019 has been audited by KPMG LLP, as reflected in their report for 2019 included on page 73.

|  | |

Chuck Magro President and Chief Executive Officer February 19, 2020 | Pedro Farah Chief Financial Officer February 19, 2020 |

| 72 | Nutrien Annual Report 2019 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Report of Independent

Registered Public

Accounting Firm

To the Shareholders and Board of Directors of Nutrien Ltd.

Opinion on Internal Control Over Financial Reporting

We have audited Nutrien Ltd. and subsidiaries’ (the “Company”) internal control over financial reporting as of December 31, 2019, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission. In our opinion, the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2019, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (“PCAOB”), the consolidated balance sheets of the Company as of December 31, 2019 and 2018, the related consolidated statements of earnings, comprehensive income, changes in shareholders’ equity, and cash flows for the years then ended, and the related notes (collectively, the “consolidated financial statements”), and our report dated February 19, 2020 expressed an unqualified opinion on those consolidated financial statements.

The Company acquired Ruralco Holdings Limited (“Ruralco”) during 2019, and management excluded from its assessment of the effectiveness of the Company’s internal control over financial reporting as of December 31, 2019, Ruralco’s internal control over financial reporting associated with 2 percent of total assets and 1 percent of total revenues included in the consolidated financial statements of the Company as of and for the year ended December 31, 2019. Our audit of internal control over financial reporting of the Company also excluded an evaluation of the internal control over financial reporting of Ruralco.

Basis for Opinion

The Company’s management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying Management’s Responsibility report. Our responsibility is to express an opinion on the Company’s internal control over financial reporting based on our audit. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the US federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. Our audit also included performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion.

Definition and Limitations of Internal Control Over Financial Reporting

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Chartered Professional Accountants

Calgary, Canada

February 19, 2020

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 73 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Report of Independent

Registered Public

Accounting Firm

To the Shareholders and Board of Directors of Nutrien Ltd.

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated balance sheets of Nutrien Ltd. and subsidiaries (the “Company”) as of December 31, 2019 and 2018, the related consolidated statements of earnings, comprehensive income, changes in shareholders’ equity, and cash flows for the years then ended, and the related notes (collectively, the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2019 and 2018, and the results of its operations and its cash flows for the years then ended, in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (“PCAOB”), the Company’s internal control over financial reporting as of December 31, 2019, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission, and our report dated February 19, 2020 expressed an unqualified opinion on the effectiveness of the Company’s internal control over financial reporting.

Change in Accounting Principle

As discussed in Note 31 to the consolidated financial statements, the Company has changed its method of accounting for leases as of January 1, 2019 due to the adoption of International Financial Reporting Standard 16, Leases.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical Audit Matters

The critical audit matters communicated below are matters arising from the current period audit of the consolidated financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the consolidated financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate.

Assessment of the carrying amount of goodwill for the Retail North America cash-generating unit

As discussed in Note 16 to the consolidated financial statements, the carrying amount of goodwill as of December 31, 2019 was $11,986 million, of which $6,826 million of goodwill has been allocated to the Retail North America cash-generating unit. The Retail North Americacash-generating unit is tested for impairment annually, and whenever events or changes in circumstances indicate that the carrying amount of the cash-generating unit, including goodwill, exceeds its estimated recoverable amount. The

| 74 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

assessment of the carrying amount of the Retail North America cash-generating unit involves a number of estimates including forecasted earnings before tax, interest, depreciation and amortization (“EBITDA”), terminal growth rate and the discount rate assumptions used to calculate the recoverable amount of the Retail North America cash-generating unit.

We identified the assessment of the carrying amount of goodwill for the Retail North America cash-generating unit as a critical audit matter. Complex auditor judgment was required to evaluate the Company’s forecasted EBITDA, terminal growth rate and discount rate, which were used to calculate the recoverable amount of the Retail North Americacash-generating unit. Minor changes to these assumptions have a significant effect on the Company’s assessment of the carrying amount of the goodwill.

The primary procedures we performed to address this critical audit matter included the following. We tested certain internal controls over the Company’s goodwill impairment assessment process, including controls related to the determination of the recoverable amount of the Retail North Americacash-generating unit, and the forecasted EBITDA, terminal growth rate and discount rate. We performed sensitivity analyses over the terminal growth rate and discount rate to assess their impact on the Company’s determination that the recoverable amount of the Retail North America cash-generating unit exceeded its carrying amount. We evaluated the Company’s forecasted EBITDA for the Retail North America

cash-generating unit by comparing to historical results and forecasted planted acreage in the United States. We compared the terminal growth rate to historical growth of the Retail North America cash-generating unit and to market information, including forecasted inflation and forecasted gross domestic product in the United States. We compared the Company’s historical forecasts of EBITDA to actual results to assess the Company’s ability to accurately forecast. In addition, we involved valuation professionals with specialized skills and knowledge, who assisted in:

| • | Evaluating the Company’s method for estimating its discount rate, and testing assumptions used to estimate the discount rate to publicly available market data for comparable companies; and |

| • | Evaluating the Company’s method for estimating the recoverable amount of the Retail North Americacash-generating unit and comparing the results of the Company’s estimate to publicly available market data and valuation metrics for comparable companies. |

Chartered Professional Accountants

We have served as the Company’s auditor since 2018.

Calgary, Canada

February 19, 2020

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 75 |

Table of Contents

Find out more at nutrien.com

Find out more at nutrien.comTable of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Consolidated Financial Statements

Consolidated Statements of Earnings

For the years ended December 31 | Note | 2019 | 2018 | |||||||||

| Note 2 | ||||||||||||

| Sales | 3 | 20,023 | 19,636 | |||||||||

| Freight, transportation and distribution | 5 | 768 | 864 | |||||||||

| Cost of goods sold | 5 | 13,814 | 13,380 | |||||||||

|

|

|

|

|

|

| ||||||

| Gross Margin | 5,441 | 5,392 | ||||||||||

| Selling expenses | 5 | 2,505 | 2,337 | |||||||||

| General and administrative expenses | 5 | 404 | 423 | |||||||||

| Provincial mining and other taxes | 5 | 292 | 250 | |||||||||

| Share-based compensation | 6 | 104 | 116 | |||||||||

| Impairment of assets | 15, 16 | 120 | 1,809 | |||||||||

| Other expenses | 7 | 154 | 43 | |||||||||

|

|

|

|

|

|

| ||||||

| Earnings Before Finance Costs and Income Taxes | 1,862 | 414 | ||||||||||

| Finance costs | 8 | 554 | 538 | |||||||||

|

|

|

|

|

|

| ||||||

| Earnings (Loss) Before Income Taxes | 1,308 | (124) | ||||||||||

| Income tax expense (recovery) | 9 | 316 | (93) | |||||||||

|

|

|

|

|

|

| ||||||

| Net Earnings (Loss) from Continuing Operations | 992 | (31) | ||||||||||

| Net earnings from discontinued operations | 10 | – | 3,604 | |||||||||

|

|

|

|

|

|

| ||||||

| Net Earnings | 992 | 3,573 | ||||||||||

|

|

|

|

|

|

| ||||||

| Net Earnings (Loss) per share from Continuing Operations | 11 | |||||||||||

| Basic | 1.70 | (0.05) | ||||||||||

| Diluted | 1.70 | (0.05) | ||||||||||

|

|

|

|

|

|

| ||||||

| Net Earnings per share from Discontinued Operations | 11 | |||||||||||

| Basic | – | 5.77 | ||||||||||

| Diluted | – | 5.77 | ||||||||||

|

|

|

|

|

|

| ||||||

| Net Earnings per share (“EPS”) | 11 | |||||||||||

| Basic | 1.70 | 5.72 | ||||||||||

| Diluted | 1.70 | 5.72 | ||||||||||

|

|

|

|

|

|

| ||||||

| Weighted average shares outstanding for basic EPS | 11 | 582,269,000 | 624,900,000 | |||||||||

| Weighted average shares outstanding for diluted EPS | 11 | 583,102,000 | 624,900,000 | |||||||||

|

|

|

|

|

|

| ||||||

Consolidated Statements of Comprehensive Income

For the years ended December 31 (net of related income taxes) | 2019 | 2018 | ||||||

| Net Earnings | 992 | 3,573 | ||||||

| Other comprehensive income (loss) | ||||||||

Items that will not be reclassified to net earnings: | ||||||||

Net actuarial gain on defined benefit plans | 7 | 54 | ||||||

Net fair value loss on investments | (25) | (99) | ||||||

Items that have been or may be subsequently reclassified to net earnings: | ||||||||

Gain (loss) on currency translation of foreign operations | 47 | (249) | ||||||

Other | 7 | (8) | ||||||

|

|

|

|

| ||||

| Other Comprehensive Income (Loss) | 36 | (302) | ||||||

|

|

|

|

| ||||

| Comprehensive Income | 1,028 | 3,271 | ||||||

|

|

|

|

| ||||

(See Notes to the Consolidated Financial Statements)

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 77 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Consolidated Statements of Cash Flows

For the years ended December 31 | Note | 2019 | 2018 | |||||||||

| Note 2 | ||||||||||||

| Operating Activities | ||||||||||||

| Net earnings | 992 | 3,573 | ||||||||||

| Adjustments for: | ||||||||||||

Depreciation and amortization | 1,799 | 1,592 | ||||||||||

Share-based compensation | 6 | 104 | 116 | |||||||||

Impairment of assets | 15, 16 | 120 | 1,809 | |||||||||

Provision for (recovery of) deferred income tax | 177 | (290) | ||||||||||

Gain on sale of investments in Sociedad Quimica y Minera de Chile S.A. (“SQM”) and Arab Potash Company (“APC”) | – | (4,399) | ||||||||||

Income tax related to the sale of the investment in SQM | – | 977 | ||||||||||

Other long-term liabilities and miscellaneous | (17) | (188) | ||||||||||

|

|

|

|

|

|

| ||||||

| Cash from operations before working capital changes | 3,175 | 3,190 | ||||||||||

| Changes innon-cash operating working capital: | ||||||||||||

Receivables | (64) | (153) | ||||||||||

Inventories | 190 | (887) | ||||||||||

Prepaid expenses and other current assets | (238) | 561 | ||||||||||

Payables and accrued charges | 602 | (659) | ||||||||||

|

|

|

|

|

|

| ||||||

| Cash Provided by Operating Activities | 3,665 | 2,052 | ||||||||||

|

|

|

|

|

|

| ||||||

| Investing Activities | ||||||||||||

| Additions to property, plant and equipment | 15 | (1,728) | (1,405) | |||||||||

| Additions to intangible assets | 16 | (163) | (102) | |||||||||

| Business acquisitions, net of cash acquired | 4 | (911) | (433) | |||||||||

| Proceeds from disposal of discontinued operations, net of tax | 10 | 55 | 5,394 | |||||||||

| Purchase of investments | (198) | (135) | ||||||||||

| Cash acquired in Merger | 4 | – | 466 | |||||||||

| Other | 147 | 102 | ||||||||||

|

|

|

|

|

|

| ||||||

| Cash (Used in) Provided by Investing Activities | (2,798) | 3,887 | ||||||||||

|

|

|

|

|

|

| ||||||

| Financing Activities | ||||||||||||

| Transaction costs on long-term debt | (29) | (21) | ||||||||||

| Proceeds from (repayment of) short-term debt, net | 19 | 216 | (927) | |||||||||

| Proceeds from long-term debt | 20 | 1,510 | – | |||||||||

| Repayment of long-term debt | 20 | (1,010) | (12) | |||||||||

| Repayment of principal portion of lease liabilities | 20 | (234) | – | |||||||||

| Dividends paid | 25 | (1,022) | (952) | |||||||||

| Repurchase of common shares | 25 | (1,930) | (1,800) | |||||||||

| Issuance of common shares | 25 | 20 | 7 | |||||||||

|

|

|

|

|

|

| ||||||

| Cash Used in Financing Activities | (2,479) | (3,705) | ||||||||||

|

|

|

|

|

|

| ||||||

| Effect of Exchange Rate Changes on Cash and Cash Equivalents | (31) | (36) | ||||||||||

|

|

|

|

|

|

| ||||||

| (Decrease) Increase in Cash and Cash Equivalents | (1,643) | 2,198 | ||||||||||

| Cash and Cash Equivalents – Beginning of Year | 2,314 | 116 | ||||||||||

|

|

|

|

|

|

| ||||||

| Cash and Cash Equivalents – End of Year | 671 | 2,314 | ||||||||||

|

|

|

|

|

|

| ||||||

| Cash and cash equivalents1 comprised of: | ||||||||||||

| Cash | 532 | 1,506 | ||||||||||

| Short-term investments | 139 | 808 | ||||||||||

|

|

|

|

|

|

| ||||||

| 671 | 2,314 | |||||||||||

|

|

|

|

|

|

| ||||||

| Supplemental Cash Flows Information | ||||||||||||

| Interest paid | 505 | 507 | ||||||||||

| Income taxes paid | 29 | 1,155 | ||||||||||

| Total cash outflow for leases | 345 | – | ||||||||||

|

|

|

|

|

|

| ||||||

| 1 | Highly liquid investments with a maturity of three months or less from the date of purchase are considered to be cash equivalents. |

(See Notes to the Consolidated Financial Statements)

| 78 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Consolidated Statements of Changes in

Shareholders’ Equity

| Share Capital | Contributed Surplus | Accumulated Other Comprehensive (Loss) Income (“AOCI”) | Retained Earnings | Total Equity 2 | ||||||||||||||||||||||||||||||||

| Net Fair Value Gain (Loss) on Investments | Net Actuarial Gain on Defined Benefit Plans 1 | Loss on Currency Translation of Foreign Operations | Other | Total AOCI | |||||||||||||||||||||||||||||||

Balance – | 1,806 | 230 | 73 | – | (2) | (46) | 25 | 6,242 | 8,303 | |||||||||||||||||||||||||||

Merger impact (Note 4) | 15,898 | 7 | – | – | – | – | – | (1) | 15,904 | |||||||||||||||||||||||||||

Net earnings | – | – | – | – | – | – | – | 3,573 | 3,573 | |||||||||||||||||||||||||||

Other comprehensive (loss) income | – | – | (99) | 54 | (249) | (8) | (302) | – | (302) | |||||||||||||||||||||||||||

Shares repurchased (Note 25) | (998) | (23) | – | – | – | – | – | (831) | (1,852) | |||||||||||||||||||||||||||

Dividends declared | – | – | – | – | – | – | – | (1,273) | (1,273) | |||||||||||||||||||||||||||

Effect of share-based compensation including issuance of common shares | 34 | 17 | – | – | – | – | – | – | 51 | |||||||||||||||||||||||||||

Transfer of net actuarial gain on defined benefit plans | – | – | – | (54) | – | – | (54) | 54 | – | |||||||||||||||||||||||||||

Transfer of net loss on sale of investment | – | – | 19 | – | – | – | 19 | (19) | – | |||||||||||||||||||||||||||

Transfer of net loss on cash flow hedges | – | – | – | – | – | 21 | 21 | – | 21 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Balance – | 16,740 | 231 | (7) | – | (251) | (33) | (291) | 7,745 | 24,425 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Net earnings | – | – | – | – | – | – | – | 992 | 992 | |||||||||||||||||||||||||||

Other comprehensive (loss) income | – | – | (25) | 7 | 47 | 7 | 36 | – | 36 | |||||||||||||||||||||||||||

Shares repurchased (Note 25) | (992) | – | – | – | – | – | – | (886) | (1,878) | |||||||||||||||||||||||||||

Dividends declared | – | – | – | – | – | – | – | (754) | (754) | |||||||||||||||||||||||||||

Effect of share-based compensation including issuance of common shares | 23 | 17 | – | – | – | – | – | – | 40 | |||||||||||||||||||||||||||

Transfer of net actuarial gain on defined benefit plans | – | – | – | (7) | – | – | (7) | 7 | – | |||||||||||||||||||||||||||

Transfer of net loss on sale of investment | – | – | 3 | – | – | – | 3 | (3) | – | |||||||||||||||||||||||||||

Transfer of net loss on cash flow hedges | – | – | – | – | – | 8 | 8 | – | 8 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Balance – | 15,771 | 248 | (29) | – | (204) | (18) | (251) | 7,101 | 22,869 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

| 1 | Any amounts incurred during a period were closed out to retained earnings at eachperiod-end. Therefore, no balance exists at the beginning or end of period. |

| 2 | All equity transactions were attributable to common shareholders. |

(See Notes to the Consolidated Financial Statements)

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 79 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

As at December 31 | Note | 2019 | 2018 | |||||||||

| Assets | ||||||||||||

| Current assets | ||||||||||||

Cash and cash equivalents | 671 | 2,314 | ||||||||||

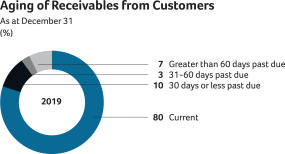

Receivables | 13 | 3,542 | 3,342 | |||||||||

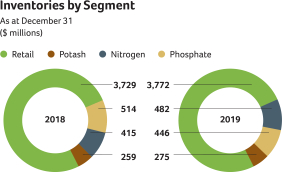

Inventories | 14 | 4,975 | 4,917 | |||||||||

Prepaid expenses and other current assets | 1,477 | 1,089 | ||||||||||

|

|

|

|

|

|

| ||||||

| 10,665 | 11,662 | |||||||||||

| Non-current assets | ||||||||||||

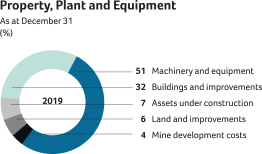

Property, plant and equipment | 15 | 20,335 | 18,796 | |||||||||

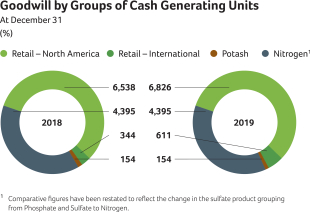

Goodwill | 16 | 11,986 | 11,431 | |||||||||

Other intangible assets | 16 | 2,428 | 2,210 | |||||||||

Investments | 17 | 821 | 878 | |||||||||

Other assets | 18 | 564 | 525 | |||||||||

|

|

|

|

|

|

| ||||||

| Total Assets | 46,799 | 45,502 | ||||||||||

|

|

|

|

|

|

| ||||||

| Liabilities | ||||||||||||

| Current liabilities | ||||||||||||

Short-term debt | 19 | 976 | 629 | |||||||||

Current portion of long-term debt | 20 | 502 | 995 | |||||||||

Current portion of lease liabilities | 21 | 214 | 8 | |||||||||

Payables and accrued charges | 22 | 7,437 | 6,703 | |||||||||

|

|

|

|

|

|

| ||||||

| 9,129 | 8,335 | |||||||||||

| Non-current liabilities | ||||||||||||

Long-term debt | 20 | 8,553 | 7,579 | |||||||||

Lease liabilities | 21 | 859 | 12 | |||||||||

Deferred income tax liabilities | 9 | 3,145 | 2,907 | |||||||||

Pension and other post-retirement benefit liabilities | 23 | 433 | 395 | |||||||||

Asset retirement obligations and accrued environmental costs | 24 | 1,650 | 1,673 | |||||||||

Othernon-current liabilities | 161 | 176 | ||||||||||

|

|

|

|

|

|

| ||||||

| Total Liabilities | 23,930 | 21,077 | ||||||||||

|

|

|

|

|

|

| ||||||

| Shareholders’ Equity | ||||||||||||

Share capital | 25 | 15,771 | 16,740 | |||||||||

Contributed surplus | 248 | 231 | ||||||||||

Accumulated other comprehensive loss | (251) | (291) | ||||||||||

Retained earnings | 7,101 | 7,745 | ||||||||||

|

|

|

|

|

|

| ||||||

| Total Shareholders’ Equity | 22,869 | 24,425 | ||||||||||

|

|

|

|

|

|

| ||||||

| Total Liabilities and Shareholders’ Equity | 46,799 | 45,502 | ||||||||||

|

|

|

|

|

|

| ||||||

| (See Notes to the Consolidated Financial Statements) | ||||||||||||

Approved by the Board of Directors,

| ||||||||||||

|  | |||||

| Director | Director |

| 80 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 1 Description of Business

Nutrien Ltd. (collectively with its subsidiaries, “Nutrien”, “we”, “us”, “our” or “the Company”) is the world’s largest provider of crop inputs and services. Nutrien plays a critical role in helping growers around the globe increase food production in a sustainable manner.

The Company is a corporation organized under the laws of Canada with its registered head office located at Suite 500, 122 – 1st Avenue South, Saskatoon, Saskatchewan, Canada. As at December 31, 2019, the Company had assets as follows:

Retail

| • | various retail facilities across the US, Canada, Australia and South America |

| • | private label and proprietary crop protection products and nutritionals |

| • | an innovative integrated digital platform for growers and crop consultants |

Potash

| • | six operations in the province of Saskatchewan |

Nitrogen

| • | eight production facilities in North America: four in Alberta and one each in Georgia, Louisiana, Ohio and Texas |

| • | one large-scale operation in Trinidad |

| • | seven upgrade facilities in North America: three in Alberta and one each in Alabama, Georgia, Missouri, and Washington |

| • | 50 percent investment in Profertil S.A. (“Profertil”), a nitrogen producer based in Argentina |

| • | 26 percent investment in Misr Fertilizers Production Company S.A.E. (“MOPCO”), a nitrogen producer based in Egypt |

Phosphate

| • | two mines and processing plants: one in Florida and one in North Carolina |

| • | phosphate feed plants in Illinois, Missouri and Nebraska |

| • | an industrial phosphoric acid plant in Ohio |

Corporate and Others

| • | investment in Canpotex Limited (“Canpotex”), a Canadian potash export, sales and marketing company owned in equal shares by Nutrien and another potash producer |

| • | 22 percent investment in Sinofert Holdings Limited (“Sinofert”), a fertilizer supplier and distributor in China |

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). We have consistently applied the same accounting policies throughout all periods presented, as if these policies had always been in effect, with the exception of IFRS 16, “Leases” (“IFRS 16”), which was adopted effective January 1, 2019, the impacts of which are disclosed in Note 31.

Certain immaterial 2018 figures have been reclassified or grouped together in the consolidated statements of earnings, consolidated statements of cash flows, segment information and nature of expenses.

These consolidated financial statements were authorized for issue by the Board of Directors on February 19, 2020.

Where an accounting policy is applicable to a specific note to the consolidated financial statements, the policy is described within that note, with the related financial disclosures by major caption as noted in the table of contents. Certain of our accounting policies that relate to the consolidated financial statements as a whole, as well as estimates and judgments we have made and how they affect the amounts reported in the consolidated financial statements, are disclosed in Note 31. Sensitivity analyses included throughout the notes should be used with caution as the changes are hypothetical and not reflective of future performance. The sensitivities have been calculated independently of changes in other key variables. Changes in one factor may result in changes in another, which could increase or reduce certain sensitivities. These consolidated financial statements were prepared under the historical cost basis, except for items that IFRS requires to be measured at fair value.

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 81 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

The Company has four reportable operating segments: Retail, Potash, Nitrogen and Phosphate. The Retail segment distributes crop nutrients, crop protection products, seed and merchandise, and provides services directly to growers through a network of farm centers in North and South America and Australia. The Potash, Nitrogen and Phosphate segments are differentiated by the chemical nutrient contained in the products that each produces.

Accounting Policies, Estimates and Judgments

Operating Segments

We identified the Executive Leadership Team (“ELT”), comprised of officers at the Executive Vice President level and above, as the Chief Operating Decision Maker (“CODM”). The CODM uses net earnings (loss) before finance costs, income taxes, and depreciation and amortization (“EBITDA”) to measure performance and allocate resources to the operating segments. The CODM considers EBITDA a meaningful measure because it is not impacted by long-term investment and financing decisions, but rather focuses on the performance of ourday-to-day operations.

In 2019, the CODM reassessed our product groupings and decided to evaluate the performance of ammonium sulfate as part of the Nitrogen segment, rather than the Phosphate and Sulfate segment, as previously reported in our 2018 annual

consolidated financial statements. Comparative amounts for the Nitrogen and Phosphate segments were restated. For the year ended December 31, 2018, Nitrogen reflected increases of $121, $40, and $53 in sales, gross margin and EBITDA, respectively, and $377 in assets, with corresponding decreases in Phosphate. In addition, the “Others” segment was renamed to “Corporate and Others”.

Judgment is used in determining the composition of the reportable segments based on factors including risks and returns, internal organization, and internal reports reviewed by the CODM.

Certain expenses are allocated across segments based on reasonable considerations such as production capacities or historical trends.

Revenue

We recognize revenue when we transfer control over a good or service to a customer.

Transfer of Control for | Retail | Potash, Nitrogen and Phosphate | ||

Sale of Goods | At the point in time when the product is

• purchased at our Retail farm center or

• delivered and accepted by customers at their premises. | At the point in time when the product is

• loaded for shipping or

• delivered to the customer. | ||

|

|

| ||

Services | Over time as the promised service is rendered. | Over time as the promised service is rendered. | ||

|

|

|

For transactions in which we act as an agent rather than the principal, revenue is recognized net of any commissions earned. The relating commissions are recognized as the sales occurred or as unconditional contracts are signed.

Retail

Retail revenue is generated primarily from sales of the following:

|

| |

Crop nutrients | Dry and liquid macronutrient products including potash, nitrogen and phosphate, proprietary liquid micronutrient products and nutrient application services. | |

|

| |

Crop protection products | Various third-party supplier and proprietary products designed to maintain crop quality and manage plant diseases, weeds, and other pests. | |

|

| |

Seed | Various third-party supplier seed brands and proprietary seed product lines. | |

|

| |

Merchandise | Fencing, feed supplements, livestock-related animal health products, storage and irrigation equipment, and other products. | |

|

| |

Services and other revenues | Product application, soil and leaf testing, crop scouting and precision agriculture services, water services, financial services and livestock marketing. | |

|

|

Provisions for returns, trade discounts and rebates are deducted from sales revenue.

| 82 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 3Segment Information Continued

Potash, Nitrogen and Phosphate

Our sales revenue is recorded and measured based on the “freight on board” mine, plant, warehouse or terminal price specified in the contract (except for certain vessel sales or specific product sales that are shipped and recorded on a delivered basis), which reflects the consideration we expect to be entitled to in exchange for the goods or services, net of any variable consideration (e.g., any trade discounts or estimated volume rebates). Where customer contracts include volume rebates, we estimate revenue at the earlier of the most likely

amount of consideration we expect to receive or when it is highly probable that a significant reversal will not occur. Our customer contracts may provide certain product quality specification guarantees but do not generally provide for refunds or returns.

Sales prices are based on North American and International benchmark market prices which are variable and subject to global supply and demand and other market factors.

| Potash | Nitrogen | Phosphate | |||

Products | • North American – primarily granular

• Offshore (international) – primarily granular and standard | • Ammonia, urea, urea ammonium nitrate, industrial grade ammonium nitrate and ammonium sulfate | • Solid fertilizer, liquid fertilizer, industrial products and feed products | |||

|

|

|

| |||

Sales prices impacted by | • North American prices referenced at delivered prices (including transportation and distribution costs)

• International prices referenced at the mine site (excluding transportation and distribution costs) | • Global energy costs and supply | • Global prices and supplies of ammonia and sulfur | |||

|

|

|

|

Other

We do not provide general warranties. Intersegment sales are made under terms that approximate market value. Transportation costs are generally recovered from the customer through sales pricing.

We elected to use the practical expedient related to the adjustment of the promised consideration for the effects of a significant financing component as the expected period between when control over a promised good or service is transferred and when the customer pays for that good or service is less than 12 months.

Seasonality in our business results from increased demand for products during planting season. Crop input sales are generally higher in spring and fall crop input application seasons. Crop nutrient inventories are normally accumulated leading up to each application season. Our cash collections generally occur

after the application season is complete, while customer prepayments made to us are typically concentrated in December and January and inventory prepayments paid to our vendors are typically concentrated in the period from November to January. Feed and industrial sales are more evenly distributed throughout the year.

For product sales with volume rebates, revenue is recognized to the extent that it is highly probable that significant reversals will not occur using the most likely method and accumulated experience.

Returns and incentives are estimated based on historical and forecasted data, contractual terms and current conditions. Due to the nature of goods and services sold, any single estimate would have only a negligible impact on revenue.

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 83 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 3Segment Information Continued

Supporting Information

Financial information on each of these segments is summarized in the following tables:

2019 | Retail | Potash | Nitrogen | Phosphate | Corporate and Others | Eliminations | Consolidated | |||||||||||||||||||||||

| Sales | – third party | 13,183 | 2,702 | 2,608 | 1,397 | 133 | – | 20,023 | ||||||||||||||||||||||

– intersegment | 38 | 207 | 612 | 203 | – | (1,060) | – | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Sales | – total | 13,221 | 2,909 | 3,220 | 1,600 | 133 | (1,060) | 20,023 | ||||||||||||||||||||||

| Freight, transportation and distribution | – | 305 | 372 | 232 | – | (141) | 768 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Net sales | 13,221 | 2,604 | 2,848 | 1,368 | 133 | (919) | 19,255 | |||||||||||||||||||||||

| Cost of goods sold | 9,981 | 1,103 | 2,148 | 1,373 | 133 | (924) | 13,814 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Gross margin | 3,240 | 1,501 | 700 | (5) | – | 5 | 5,441 | |||||||||||||||||||||||

| Selling expenses | 2,484 | 9 | 25 | 5 | (18) | – | 2,505 | |||||||||||||||||||||||

| General and administrative expenses | 112 | 6 | 15 | 7 | 264 | – | 404 | |||||||||||||||||||||||

| Provincial mining and other taxes | – | 287 | 2 | 1 | 2 | – | 292 | |||||||||||||||||||||||

| Share-based compensation expense | – | – | – | – | 104 | – | 104 | |||||||||||||||||||||||

| Impairment of assets (Note 15 and 16) | – | – | – | – | 120 | – | 120 | |||||||||||||||||||||||

| Other expenses (income) | 8 | (4 | ) | (46) | 25 | 171 | – | 154 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Earnings (loss) before finance costs | 636 | 1,203 | 704 | (43) | (643) | 5 | 1,862 | |||||||||||||||||||||||

| Depreciation and amortization | 595 | 390 | 535 | 237 | 42 | – | 1,799 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| EBITDA | 1,231 | 1,593 | 1,239 | 194 | (601) | 5 | 3,661 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Assets 1 | 19,990 | 11,696 | 10,991 | 2,198 | 2,129 | (205) | 46,799 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| 1 | Included in the Retail and Nitrogen segments are $126 and $482, respectively, relating to equity-accounted investees as described in Note 17. |

2018 | Retail | Potash | Nitrogen 1 | Phosphate 1 | Corporate and Others | Eliminations | Consolidated | |||||||||||||||||||||||

| Sales | – third party | 12,470 | 2,796 | 2,712 | 1,508 | 150 | – | 19,636 | ||||||||||||||||||||||

– intersegment | 50 | 220 | 626 | 268 | – | (1,164) | – | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Sales | – total | 12,520 | 3,016 | 3,338 | 1,776 | 150 | (1,164) | 19,636 | ||||||||||||||||||||||

| Freight, transportation and distribution | – | 349 | 373 | 215 | – | (73) | 864 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Net sales | 12,520 | 2,667 | 2,965 | 1,561 | 150 | (1,091) | 18,772 | |||||||||||||||||||||||

| Cost of goods sold | 9,485 | 1,183 | 2,145 | 1,473 | 150 | (1,056) | 13,380 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Gross margin | 3,035 | 1,484 | 820 | 88 | – | (35) | 5,392 | |||||||||||||||||||||||

| Selling expenses | 2,303 | 14 | 32 | 10 | (22) | – | 2,337 | |||||||||||||||||||||||

| General and administrative expenses | 100 | 10 | 20 | 9 | 284 | – | 423 | |||||||||||||||||||||||

| Provincial mining and other taxes | – | 244 | 3 | 1 | 2 | – | 250 | |||||||||||||||||||||||

| Share-based compensation expense | – | – | – | – | 116 | – | 116 | |||||||||||||||||||||||

| Impairment of assets (Note 15) | – | 1,809 | – | – | – | – | 1,809 | |||||||||||||||||||||||

| Other (income) expenses | (75 | ) | 14 | (8) | 6 | 106 | – | 43 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Earnings (loss) before finance costs | 707 | (607 | ) | 773 | 62 | (486) | (35) | 414 | ||||||||||||||||||||||

| Depreciation and amortization | 499 | 404 | 442 | 193 | 54 | – | 1,592 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| EBITDA | 1,206 | (203 | ) | 1,215 | 255 | (432) | (35) | 2,006 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Assets 2 | 17,964 | 11,710 | 10,386 | 2,406 | 3,678 | (642) | 45,502 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| 1 | Comparative figures have been restated to reflect the change in the sulfate product grouping from Phosphate and Sulfate to Nitrogen. |

| 2 | Included in the Retail and Nitrogen segments are $208 and $428, respectively, relating to equity-accounted investees as described in Note 17. |

| 84 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 3Segment Information Continued

Financial information by geographic area is summarized in the following tables:

Sales – Third Party | 2019 | 2018 | ||||||

| United States | 12,522 | 11,891 | ||||||

| Canada | 2,504 | 2,790 | ||||||

| Australia | 1,955 | 1,681 | ||||||

| Canpotex1 | 1,625 | 1,657 | ||||||

| Trinidad | 113 | 190 | ||||||

| Argentina | 388 | 387 | ||||||

| Europe | 210 | 312 | ||||||

| Other | 706 | 728 | ||||||

|

|

|

|

| ||||

| 20,023 | 19,636 | |||||||

|

|

|

|

| ||||

| 1 | As described in Note 1, Canpotex executed offshore marketing, sales and distribution functions for certain of our products. Canpotex’s 2019 sales volumes were made to: Latin America 31 percent, China 22 percent, India 10 percent, Other Asian markets 27 percent, Other markets 10 percent (2018 – Latin America 33 percent, China 18 percent, India 10 percent, Other Asian markets 31 percent, Other markets 8 percent) (Note 29). |

Non-Current Assets1 | 2019 | 2018 | ||||||

| United States | 15,685 | 14,501 | ||||||

| Canada | 17,503 | 17,100 | ||||||

| Australia | 1,172 | 607 | ||||||

| Trinidad | 691 | 570 | ||||||

| Other | 639 | 621 | ||||||

|

|

|

|

| ||||

| 35,690 | 33,399 | |||||||

|

|

|

|

| ||||

| 1 | Excludes financial instruments (other than equity-accounted investees), deferred tax assets and post-employment benefit assets. |

We disaggregated revenue from contracts with customers by product line or geographic location for each reportable segment to show how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors. Sales reported under our Corporate and Others segment primarily relates to our non-core Canadian business.

| 2019 | 2018 | ||||||

| Retail sales by product line | ||||||||

Crop nutrients | 4,989 | 4,577 | ||||||

Crop protection products | 4,983 | 4,862 | ||||||

Seed | 1,712 | 1,687 | ||||||

Merchandise | 598 | 584 | ||||||

Services and other | 939 | 810 | ||||||

|

|

|

|

| ||||

| 13,221 | 12,520 | |||||||

|

|

|

|

| ||||

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 85 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 3Segment Information Continued

| 2019 | 2018 | ||||||

| Potash sales by geography | ||||||||

Manufactured product | ||||||||

North America | 1,283 | 1,356 | ||||||

Offshore1 | 1,625 | 1,657 | ||||||

Other potash and purchased products | 1 | 3 | ||||||

|

|

|

|

| ||||

| 2,909 | 3,016 | |||||||

|

|

|

|

| ||||

| Nitrogen sales by product line2 | ||||||||

Manufactured product | ||||||||

Ammonia | 884 | 1,061 | ||||||

Urea | 1,019 | 979 | ||||||

Solutions, nitrates and sulfates | 812 | 825 | ||||||

Other nitrogen and purchased products | 505 | 473 | ||||||

|

|

|

|

| ||||

| 3,220 | 3,338 | |||||||

|

|

|

|

| ||||

| Phosphate sales by product line2 | ||||||||

Manufactured product | ||||||||

Fertilizer | 944 | 1,141 | ||||||

Industrial and feed | 475 | 469 | ||||||

Other phosphate and purchased products | 181 | 166 | ||||||

|

|

|

|

| ||||

| 1,600 | 1,776 | |||||||

|

|

|

|

| ||||

| 1 | Relates to Canpotex. |

| 2 | Comparative figures have been restated to reflect the change in the sulfate product grouping from Phosphate and Sulfate to Nitrogen. |

The Company’s business combinations include the merger between Potash Corporation of Saskatchewan Inc. (“PotashCorp”) and Agrium Inc. (“Agrium”) (the “Merger”), the acquisition of Retail businesses, including Ruralco Holdings Limited (“Ruralco”), and various digital agriculture, proprietary products and agricultural services.

Accounting Policies, Estimates and Judgments

| • | Consideration is measured at the aggregate of the fair values of assets transferred, liabilities incurred or assumed, and equity instruments issued in exchange for control of the acquiree at the acquisition date. |

| • | Identifiable assets acquired and liabilities assumed are generally measured at fair value. |

| • | The excess of total consideration for each acquisitionplus non-controlling interest in the acquiree, over the fair value of the identifiable net assets acquired, is recorded as goodwill. |

| • | For each business combination, we elect to measure thenon-controlling interest in the acquired entity either at fair value or at the proportionate share of the acquiree’s identifiable net assets. |

| 86 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 4Business Combinations Continued

Judgment is required to determine which entity is the acquirer in a merger of equals. In identifying PotashCorp as the acquirer in the Merger, we considered the voting rights of all equity instruments, the intended corporate governance structure of the combined company, the intended composition of senior management of the combined company and the size of each of the companies. In assessing the size of each of the companies, we evaluated various metrics. No single factor was the sole determinant in the overall conclusion that PotashCorp was the acquirer for accounting purposes in the Merger; rather, all factors were considered in arriving at the conclusion.

Purchase price allocation involves judgment in identifying assets acquired and liabilities assumed, and estimation of their fair values. To determine fair values, we used quoted market prices or widely accepted valuation techniques as described below. Key assumptions include discount rates and revenue growth rates specific to the acquired assets or liabilities assumed. We performed a thorough review of all internal and external sources of information available on circumstances that existed at the acquisition date. We also engaged independent valuation experts on certain acquisitions to assist in determining the fair value of certain assets acquired and liabilities assumed and related deferred income tax impacts.

Asset | Ruralco | Merger | Other | Valuation Technique and Judgments Applied | ||||

Property, plant and equipment | X | X | X | Market approach for land and certain types of personal property: sales comparison that measures the value of an asset through an analysis of sales and offerings of comparable assets.

Replacement costs for all other depreciable property, plant and equipment: measures the value of an asset by estimating the costs to acquire or construct comparable assets and adjusts for age and condition of the asset. | ||||

|

|

|

|

| ||||

Other intangible assets | X | X | X | Income approach – multi-period excess earnings method: measures the value of an asset based on the present value of the incrementalafter-tax cash flows attributable to the asset after deducting contributory asset charges (“CACs”). Allocation of CACs is a matter of judgment and based on the nature of the acquired businesses’ operations and historical trends.

We considered several factors in determining the fair value of customer relationships, such as customers’ relationships with the acquired company and its employees, the segmentation of customers, historical customer attrition rates and revenue growth. Segmenting customers is a matter of judgment and includes factors such as the size of the customer and customer behavior patterns. | ||||

|

|

|

|

| ||||

Long-term debt | X | Comparable debt instruments with similar maturities, adjusted where necessary to the acquired company’s credit spread, based on information published by financial institutions. | ||||||

|

|

|

|

| ||||

Asset retirement obligations and accrued environmental costs | X | Decision-tree approach of future costs and a risk premium to capture the compensation sought by risk-averse market participants for bearing the uncertainty inherent in the cash flows of the liability. We expect asset retirement obligations for phosphate sites to be paid over the next 68 years, while we expect asset retirement obligations for potash and nitrogen sites to be paid subsequently.

We expect accrued environmental costs – discounted using a credit adjusted risk-free rate – to be paid over the next 30 years. | ||||||

|

|

|

|

|

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 87 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 4Business Combinations Continued

Supporting Information

| Ruralco | Merger | Other Acquisitions | |||

Acquisition date | September 30, 2019 | January 1, 2018 | Various | |||

|

|

|

| |||

Purchase price, net of cash and cash equivalents acquired | $330

On the acquisition date, we acquired 100% of the Ruralco stock that was issued and outstanding.

Also included in the total consideration, net of cash and cash equivalents acquired, is the impact of $18 relating to a foreign exchange hedge loss which we designated a cash flow hedge.

Transaction costs are recorded in acquisition and integration related costs in other expenses. | $16,010

We determined the purchase price based on the number of Agrium shares outstanding

On the acquisition date, shareholders of PotashCorp received 0.400 common shares of Nutrien for each PotashCorp share held, and shareholders of Agrium received 2.230 common shares of Nutrien for each Agrium share held.

Merger and related costs are included in other expenses. | 2019 – $581, net of $100 previously held equity-accounted interest in Agrichem. We acquired the remaining 20 percent interest in Agrichem in the first nine months of 2019, making Agrichem a wholly owned consolidated subsidiary of the Company.

(2018 – $433) | |||

|

|

|

| |||

Goodwill and expected benefits of the acquisition | $202 | $11,185, none of which is deductible for income tax purposes. | $341 (2018 – $197) | |||

|

|

| ||||

The expected benefits of the acquisitions resulting in goodwill include:

• synergies from expected reduction in operating costs;

• wider distribution channel for selling products of acquired businesses;

• a larger assembled workforce;

• potential increase in customer base;

• enhanced ability to innovate;

• production and expense optimization, including procurement savings (specific to Merger); and

• closer proximity of nitrogen operations to sources oflow-cost natural gas (specific to Merger). | ||||||

|

|

|

| |||

Description | An agriservices business in Australia with approximately 250 operating locations. | A major global producer and distributor of agricultural products, services and solutions. | 68 Retail locations in North and South America and Australia, including companies operating in the proprietary products business, such as Actagro, LLC, a developer, manufacturer and marketer of environmentally sustainable soil and plant health products and technologies (2018 – 53 Retail locations in North America and Australia and companies operating within the digital agriculture, proprietary products and agricultural services businesses). | |||

|

|

|

| |||

| 88 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 4Business Combinations Continued

We allocated the following values to the acquired assets and assumed liabilities based upon fair values at their respective acquisition date:

| 2019 | 2018 | |||||||||||||||||||||||

| Ruralco (Estimate) | ||||||||||||||||||||||||

| Preliminary 1 | Adjustments 2 | Revised Fair Value | Other Acquisitions 3 | Merger (Final) | Other Acquisitions 3 | ||||||||||||||||||

Cash and cash equivalents | – | – | – | – | 466 | – | ||||||||||||||||||

Receivables | 250 | 39 | 289 | 4 | 68 | 2,600 | 4 | 20 | ||||||||||||||||

Inventories | 116 | 1 | 117 | 145 | 3,303 | 146 | ||||||||||||||||||

Prepaid expenses and other current assets | 11 | (3 | ) | 8 | 38 | 1,124 | 2 | |||||||||||||||||

Property, plant and equipment | 70 | 66 | 136 | 115 | 7,459 | 107 | ||||||||||||||||||

Goodwill | 272 | (70 | ) | 202 | 341 | 11,185 | 197 | |||||||||||||||||

Other intangible assets | 55 | 110 | 165 | 179 | 2,348 | 8 | ||||||||||||||||||

Investments | 15 | – | 15 | – | 528 | 11 | ||||||||||||||||||

Other assets | 16 | – | 16 | 5 | 2 | 293 | 5 | 3 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Total assets | 805 | 143 | 948 | 888 | 29,306 | 494 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Short-term debt | 112 | – | 112 | 25 | 867 | – | ||||||||||||||||||

Payables and accrued charges | 299 | 46 | 345 | 156 | 5,239 | 52 | ||||||||||||||||||

Long-term debt, including current portion | – | – | – | 11 | 4,941 | – | ||||||||||||||||||

Lease liabilities, including current portion | 44 | 66 | 110 | 1 | – | – | ||||||||||||||||||

Deferred income tax liabilities | 7 | 31 | 38 | 7 | 934 | – | ||||||||||||||||||

Pension and other post-retirement benefit liabilities | – | – | – | – | 142 | – | ||||||||||||||||||

Asset retirement obligations and accrued environmental costs | – | – | – | – | 1,094 | – | ||||||||||||||||||

Othernon-current liabilities | 13 | – | 13 | 7 | 79 | 9 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Total liabilities | 475 | 143 | 618 | 207 | 13,296 | 61 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Total consideration | 330 | – | 330 | 681 | 16,010 | 433 | ||||||||||||||||||

Previously held equity-accounted interest in Agrichem | – | – | – | 100 | – | – | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Total consideration, net of cash and cash equivalents acquired | 330 | – | 330 | 581 | 16,010 | 433 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

| 1 | Preliminary value as previously reported in our third quarter 2019 unaudited financial statements. The purchase price allocation is not final as we continue to obtain and verify information required to determine the fair value of certain assets and liabilities and the amount of deferred income taxes arising on their recognition. We estimated the preliminary purchase price allocation as of the date of the acquisition based on information that was available and continue to adjust those estimates as new information that existed at the date of acquisition becomes available. We expect to finalize the amounts recognized when we obtain the information necessary to complete the analysis, and in any event, not later than September 30, 2020. |

| 2 | We recorded adjustments to the preliminary fair value to reflect facts and circumstances in existence as of the date of acquisition. These adjustments primarily related to changes in the preliminary valuation assumptions, including refinement of intangible assets. All measurement period adjustments were offset against goodwill. |

| 3 | This represents preliminary fair values. For certain acquisitions, we finalized the purchase price with no material change to the fair values disclosed in prior periods. |

| 4 | Includes receivables from customers with gross contractual amounts of $247, of which $5 are considered to be uncollectible relating to Ruralco (2018 – $2,247 and $80 respectively relating to the Merger). |

| 5 | Includes deferred income tax assets of $14 relating to Ruralco (2018 – $158 relating to the Merger). |

Financial Information Related to the Acquired Operations

| 2019 Proforma1 | Ruralco | Other Acquisitions | ||||||

Sales | 1,090 | 480 | ||||||

EBITDA | 50 | 40 | ||||||

|

|

|

|

| ||||

1 Estimated annual sales and EBITDA if acquisitions occurred at the beginning of the year. Net earnings before income taxes is not available. |

| |||||||

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 89 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 4Business Combinations Continued

| 2019 Actuals | 2018 Actuals | |||||||||||||||

From date of acquisition | Ruralco | Other Acquisitions | Merger | Other Acquisitions | ||||||||||||

| Sales | 249 | 312 | 14,551 | 213 | ||||||||||||

| Net earnings (loss) before income taxes | (2 | ) | (1 | ) | 546 | 10 | ||||||||||

|

|

|

|

|

|

|

|

| ||||||||

| 2019 | 2018 | ||||||

| Purchased and produced raw materials and product for resale1 | 11,335 | 10,881 | ||||||

| Depreciation and amortization | 1,799 | 1,592 | ||||||

| Employee costs2 | 2,268 | 1,949 | ||||||

| Freight | 845 | 934 | ||||||

| Impairment of assets (Note 15 and 16) | 120 | 1,809 | ||||||

| Provincial mining and other taxes3 | 292 | 250 | ||||||

| Offsite warehouse costs4 | 51 | 68 | ||||||

| Railcar and vessel costs4 | 5 | 128 | ||||||

| Merger and related costs | 82 | 170 | ||||||

| Acquisition and integration related costs | 16 | – | ||||||

| Contract services | 504 | 469 | ||||||

| Lease expense 5 | 66 | 148 | ||||||

| Fleet fuel, repairs and maintenance | 202 | 183 | ||||||

| Other | 576 | 641 | ||||||

|

|

|

|

| ||||

| Total cost of goods sold and expenses | 18,161 | 19,222 | ||||||

|

|

|

|

| ||||

| 1 | Significant expenses include: supplies, energy, fuel, purchases of raw material (natural gas – feedstock, sulfur, ammonia and reagents) and product for resale (crop nutrients and protection products, and seed). |

| 2 | Includes employee benefits and share–based compensation. In 2018, employee costs also include a $157 gain on curtailment of defined benefit pension and other post-retirement benefit plans (“Defined Benefit Plans Curtailment Gain”) as described in Note 23. |

| 3 | Includes $190 and $102 (2018 – $160 and $90) relating to Saskatchewan potash production tax and Saskatchewan resource surcharge and other, respectively, as required under Saskatchewan provincial legislation. |

| 4 | Includes expenses relating to operating leases in 2018. |

| 5 | In 2019, includes lease expense relating to short-term leases, leases oflow-value and variable lease payments. |

Note 6 Share-Based Compensation

We have share-based compensation plans (including those assumed from PotashCorp and Agrium) for eligible employees and directors as part of their remuneration package, including Stock Options, Performance Share Units (“PSUs”), Restricted Share Units (“RSUs”) and Deferred Share Units (“DSUs”).

Accounting Policies, Estimates and Judgments

For awards with performance conditions that determine the number of options or units to which employees are entitled, measurement of compensation cost is based on our best estimate of the outcome of the performance conditions. Changes to vesting assumptions are reflected in earnings immediately for compensation cost already recognized.

For plans settled through the issuance of equity

| • | fair value for stock options is determined on grant date using the Black-Scholes-Merton option-pricing model, and |

| • | fair value for PSUs is determined on grant date by projecting the outcome of performance conditions. |

For plans settled through cash, a liability is recorded based on the fair value of the awards each period.

| 90 | Nutrien Annual Report 2019 | In millions of US dollars except as otherwise noted |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 6Share-Based Compensation Continued

Estimation involves determining:

| • | stock option-pricing model assumptions as described in the weighted average assumptions table; |

| • | forfeiture rate for options granted based on past experience and future expectations, and adjusted upon actual vesting; |

| • | projected outcome of performance conditions for PSUs, including the relative ranking of our total shareholder |

return, including expected dividends, compared with a specified peer group using a Monte Carlo simulation option-pricing model and the outcome of our synergies relative to the target; and |

| • | the number of dividend equivalent units expected to be earned. |

Supporting Information

The following summarizes the Nutrien share-based compensation plans, under which we have awards available to be granted, and the assumed legacy plans of PotashCorp and Agrium, under which no awards will be granted.

Plan Features | Stock Options | PSUs | RSUs | DSUs | SARs/TSARs 4 | |||||

Eligibility | Officers and eligible employees | Officers and eligible employees | Eligible employees | Non-executive directors | Awards no longer granted; legacy awards only | |||||

|

|

|

|

|

| |||||

Granted | Annually | Annually | Annually | At the discretion of the Board of Directors | Awards no longer granted; legacy awards only | |||||

|

|

|

|

|

| |||||

Vesting Period | 25% per year over four years 1 | On third anniversary of grant date based on total shareholder return over a three-year performance cycle, compared to average total shareholder return of a peer group of companies over the same period | On third anniversary of grant date and are not subject to performance conditions | Fully vest upon grant | 25% per year over four years | |||||

|

|

|

|

|

| |||||

Maximum Term | 10 years | Not applicable | Not applicable | Not applicable | 10 years | |||||

|

|

|

|

|

| |||||

Settlement | Shares | Cash / Shares2 | Cash | Cash3 | Cash | |||||

|

|

|

|

|

|

| 1 | Under the assumed legacy PotashCorp long-term incentive and performance option plan, stock options vest on the third anniversary of the grant date. |

| 2 | Under the assumed legacy PotashCorp long-term incentive plan, PSUs will be settled in shares for grantees who are subject to our share ownership guidelines and in cash for all other grantees. |

| 3 | Based on the common share price at the time of the director’s departure from the Board of Directors. |

| 4 | Under the assumed legacy Agrium stock appreciation rights (“SARs”) plan, holders of tandem stock appreciation rights (“TSARs”) have the ability to choose between (a) receiving in cash the price of our shares on the date of exercise in excess of the exercise price of the right or (b) receiving common shares by paying the exercise price of the right. Our past experience and future expectation is that substantially all TSAR holders will elect to choose the first option. |

The weighted average fair value of stock options granted was estimated as of the date of the grant using the Black-Scholes-Merton option-pricing model. The weighted average grant date fair value of stock options per unit granted in 2019 was $11.27 (2018 – $9.71). The weighted average assumptions by year of grant that impacted current year results are as follows:

| Year of Grant | ||||||||||

Assumptions | Based On | 2019 | 2018 | |||||||

| Exercise price per option | Quoted market closing price 1 | 53.54 | 44.50 | |||||||

| Expected annual dividend yield (%) | Annualized dividend rate2 | 3.22 | 3.58 | |||||||

| Expected volatility (%) | Historical volatility3 | 27 | 29 | |||||||

| Risk-free interest rate (%) | Zero-coupon government issues4 | 2.55 | 2.79 | |||||||

| Average expected life of options (years) | Historical experience | 7.5 | 7.5 | |||||||

|

|

|

|

|

| |||||

| 1 | Of common shares on the last trading day immediately preceding the date of the grant. |

| 2 | As of the date of grant. |

| 3 | Of the Company’s share over a period commensurate with the expected life of the option. |

| 4 | Implied yield available on equivalent remaining term at the time of the grant. |

| In millions of US dollars except as otherwise noted | Nutrien Annual Report 2019 | 91 |

Table of Contents

| Overview | Management’s Discussion & Analysis | Two Year Highlights | Financial Statements | Other Information |

Note 6Share-Based Compensation Continued

A summary of the status of our stock option plans as at December 31, 2019 and 2018 and changes during the years ending on those dates is as follows:

| Number of Shares Subject to Option | Weighted Average Exercise Price | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||||