Filed Pursuant to Rule 424(b)(3)

Registration No. 333-268335

Prospectus Supplement No. 1

to Prospectus dated February 3, 2023

CHILEAN COBALT CORP.

13,000,000 Shares of Common Stock

$4.00 per Share

This prospectus supplement No. 1 amends and supplements the prospectus dated February 3, 2023, relating to the resale of up to 13,000,000 shares of common stock of Chilean Cobalt Corp. (the “Company,” “C3,” “we,” “our” and “us”) by the selling stockholders named in the prospectus. The foregoing prospectus and this prospectus supplement are collectively referred to as the “prospectus.” Please keep this prospectus supplement with your prospectus for future reference.

This prospectus supplement incorporates into the prospectus the attached Annual Report on Form 10-K for the fiscal year ended December 31, 2022, filed with the Securities and Exchange Commission (“SEC”) on March 24, 2023.

This prospectus supplement is not complete without the prospectus, including any supplements and amendments thereto. This prospectus supplement should be read in conjunction with the prospectus which is to be delivered with this prospectus supplement. This prospectus supplement is qualified by reference to the prospectus, except to the extent that the information in this prospectus supplement updates or supersedes the information contained in the prospectus, including any supplements and amendments thereto.

Investing in our common stock should be considered speculative and involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” section of the prospectus to read about the risks you should consider before buying shares of our common stock.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Capitalized terms contained in this prospectus supplement have the same meanings as in the prospectus unless otherwise stated herein.

The date of this prospectus supplement is March 24, 2023

Index of SEC Filings

The following report listed below is filed as a part of this prospectus supplement No. 1.

Appendix No. | Description | |

| Appendix 1 | Annual Report on Form 10-K for the year ended December 31, 2022, filed with the Securities and Exchange Commission on March 24, 2023. |

Appendix 1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to _____

Commission File Number 333-268335

CHILEAN COBALT CORP.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 82-3590294 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

1199 Lancaster Ave, Suite 107 Berwyn, Pennsylvania | 19312 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(484) 580-8697

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class |

| N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☒ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on an attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, there were 4,899,530 shares of common stock, $0.0001 value per share, outstanding that were held by non-affiliates. The Registrant’s common stock has not traded on the OTC Markets or elsewhere and, accordingly, there is no aggregate “market value” to be indicated for such shares that is based on any market price.

There were 13,000,000 shares of the registrant’s common stock, $0.0001 par value per share, outstanding as of March 24, 2023.

Documents Incorporated by Reference

None

CHILEAN COBALT CORP.

Contents

| 5 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the documents incorporated herein by reference contain forward-looking statements. Such forward-looking statements are based on current expectations, estimates and projections about Chilean Cobalt Corp.’s industry, management beliefs, and assumptions made by management. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict; therefore, actual results and outcomes may differ materially from what is expressed or forecasted in any such forward-looking statements. Although we believe the expectations reflected in our forward-looking statements are based upon reasonable assumptions, it is not possible to foresee or identify all factors that could have a material effect on the future financial performance of the Company. The forward-looking statements in this Annual Report on Form 10-K are made on the basis of management’s assumptions and analyses, as of the time the statements are made, in light of their experience and perception of historical conditions, expected future developments and other factors believed to be appropriate under the circumstances. Except as otherwise required by the federal securities laws, we disclaim any obligation or undertaking to publicly release any updates or revisions to any forward-looking statement contained in this Annual Report on Form 10-K and the information incorporated by reference in this Annual Report on Form 10-K to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any statement is based.

| 6 |

PART I

ITEM 1. BUSINESS

Our Company

Chilean Cobalt Corp. (“C3,” the “Company,” “we,” “our,” “ours” or “us”) is a critical materials exploration and development company focused on developing the La Cobaltera project located in Chile’s historic San Juan cobalt district. C3 is mission-driven as an innovator and leader that strives to be the most responsible supplier of critical mineral resources for the development of advanced materials and cleaner energy technologies that address the most pressing environmental and development issues. In this Annual Report on Form 10-K, unless the context indicates otherwise, “C3,” the “Company,” “we,” “our,” “ours” or “us” refer to Chilean Cobalt Corp., a Nevada corporation, and its sole subsidiary, Baltum Mineria SpA.

Given the transformational shift from internal combustion engines to electric vehicles (EVs), there has been an increase in demand for cobalt, a critical battery material in lithium-ion batteries that EVs use, along with copper as well. The Company’s wholly-owned subsidiary Baltum Mineria SpA (“Baltum”) has acquired 2,635 hectares of fully exploitable mining concessions in northern Chile’s Atacama region in the San Juan District. The Company continues to seek opportunities to further consolidate mining rights in the district. The San Juan mining district, which includes the La Cobaltera area, has been identified by CORFO, the Chilean governmental agency responsible for the country’s economic development, as likely containing the highest quality cobalt assets in Chile. Chile already being the leading copper-producing country in the world with the La Cobaltera area historically supporting the existence of established and high-quality copper assets. Being strategically located near roads, electricity, water, and ports, the site is in close proximity to robust mining infrastructure. The Company’s principal business activities since incorporation have been the assessment, acquisition and consolidation of mining concessions; the exploration of the potential cobalt-copper resources within the concessions; and developing an accelerated phased implementation plan to generate revenue as quickly as possible.

We have not generated revenues to date. Our limited operations have included the formation of the Company and its wholly-owned subsidiary Baltum Mineria SpA, oversight of cobalt exploration activities, and business development activities. These limited operations have been funded by capital raised through the issuance of our common stock, preferred stock, and debt. From December 4, 2017 through March 24, 2023, we raised a total of $29,209,536 from accredited investors through the issuance of our common stock, preferred stock, and debt.

We have limited business operations and have achieved losses since inception. We have been issued a going concern opinion from our auditors as a result of not generating sufficient business to date.

Our monthly “burn rate,” the amount of expenses we expect to incur on a monthly basis, is approximately $79,000 for a total of $948,000 for the following 12 months. We have relied and will continue to rely on capital raised from third parties to fund operations during the following 12 months.

In order to complete our plan of operations, we estimate that approximately $160 million in funds will be required.

Our management has concluded that our historical recurring losses from operations and negative cash flows from operations as well as our dependence on securing private equity and other financings raise substantial doubt about our ability to continue as a going concern and our auditor has included an explanatory paragraph relating to our ability to continue as a going concern in its audit reports for the fiscal years ended December 31, 2022 and 2021. As noted in our financial statements, we had an accumulated stockholders’ deficit of approximately $31,207,496 and recurring losses from operations as of December 31, 2022. See “Risk Factors - We have a history of operating losses and our management has concluded that factors raise substantial doubt about our ability to continue as a going concern and our auditor has included an explanatory paragraph relating to our ability to continue as a going concern in its audit report for the fiscal years ended December 31, 2022 and 2021.”

| 7 |

Our Market Opportunity

Our market opportunity is driven by the generational opportunity emerging from the rapidly changing ways that the world produces, stores, and consumes energy. As adoption rates of electric vehicles across the entire transportation spectrum increase, and efficient battery-based renewable energy generation storage becomes more mainstream, thereby causing the demand for critical materials to increase dramatically, we believe that the scope of our market opportunity becomes materially more meaningful and global.

Electric Vehicle (“EV”) market penetration is expected to be a major driver of growth, as specifically indicated in the following chart for passenger vehicles in the BloombergNEF (“BNEF” or “Bloomberg”) EV Outlook 2022 forecast of greater than 40% global (dashed line in the chart) penetration by 2030 for share of sales under its economic transition scenario. Benchmark Mineral Intelligence (“BMI” or “Benchmark”) forecasts the EV battery market to grow at a 26% CAGR at the tier 3 level and higher growth rates on average across all tiers through 2031, reaching an annual sales volume of approximately 36.7 million vehicles per BNEF Aug 2021 estimates. In the long term, BNEF forecasts the global EV penetration in the passenger vehicle space to exceed 70% market share by 2040, which given projections on expansion of overall annual passenger vehicle sales between now and 2040 is projected to represent sales of around 66.2 million passenger EV units per year by that point in time per BNEF August 2021 estimates.

| 8 |

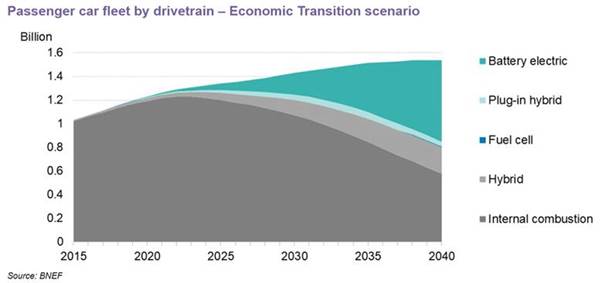

More importantly, as shown in the chart below, BNEF believes we are at or near an inflection point in the overall passenger vehicle fleet, where the internal combustion engine (“ICE”) numbers have peaked and will only begin to steadily decline over time as sales of alternative drivetrain light-duty vehicles take an increasingly larger cut of the future annual sales volume and annual fleet retirements reduce the volume of older, obsolete and damaged vehicles, which are predominantly ICE-based.

| 9 |

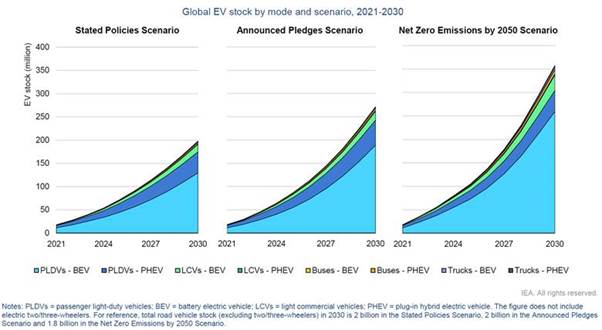

The International Energy Agency (“IEA”) has projected unit volumes of EV’s produced by year under discreet scenarios for various types of vehicles. These projections go beyond the passenger vehicle projections, as depicted in the following chart.

The IEA projects a 200 million EV fleet by 2030, under its most conservative and not necessarily global climate goals achieving scenario and this excludes the 2-wheel and 3-wheel segments. Passenger light-duty EV sales dominate this estimate in excess of 85% of the overall volume. These EV sales require a corresponding volume of battery or fuel cell production to accommodate EV production. If governments and other stakeholders were to incentivize meeting the net zero emissions by 2050 targets, the overall EV fleet would be projected to increase by about 75% to in excess of a 350 million EV fleet. IEA in the chart that follows later in the Industry Demand section of this Annual Report on Form 10-K on page 9, indicated that there is a 15% reduction in cobalt demand equivalent to approximately 35 kilo-tonnes per year between their 2030 base versus constrained methodologies. From this it can be deduced that they project over 233 kilo-tonnes per year base-case and 198 kilo-tonnes per year constrained. To put that in perspective, Statista indicates that there was 170,000 kilo-tonnes of cobalt produced in 2021. Therefore, as it pertains to light-duty vehicles only, albeit the behemoth in the EV sector, by 2030, it is projected that at least 16% or more in cobalt production will be needed than at present. Add to that uses of cobalt for battery applications outside of light-duty vehicles and materials and other technology applications outside the EV spectrum, there will absolutely be a need for expansion of cobalt sourcing to meet demand. Given environmental and global climate considerations, there will be an even bigger demand for responsibly sourced cobalt, given that over 70% of current production comes from the Democratic Republic of Congo (“DRC”), as discussed later in the Quality of Primary Cobalt Project and Potential Producer of Cobalt outside of the DRC section of this Annual Report on Form 10-K on page 5. Demand for copper is expected to increase as well, albeit not quite to the extent of Cobalt, given that copper sources aren’t nearly as constrained.

| 10 |

Government policies around the world have been accommodating and supportive of EV adoption. The U.S., for example, recently signed into law the Inflation Reduction Act, which has environmental provisions targeted at providing credits toward the purchase of EV’s meeting certain favorable trade criteria. While there is concern over the ability for companies to meet the favorable trade criteria and for end-consumers to qualify for the credits, we believe that it is an indication of the commitment to incentivizing the transition process at the highest levels of government. In addition to penetration targets, other countries have proposed banning sales of internal combustion engine (“ICE”) vehicles by various deadlines, with 2030 being a common goal year for such policies.

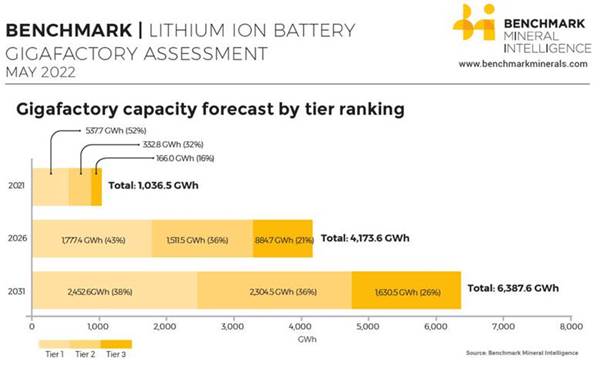

Battery cell manufacturing has also been the beneficiary of billions in investment, with currently planned “gigafactories” totaling a capacity of 6,388 GWh projected to be deployed by 2031 per the BMI chart presented previously. If all of the planned plants were realized and produced at 100% capacity, the impact on battery raw materials markets would be extraordinary, causing demand for cobalt to expand to over 6X its current level.

Although the growth of EVs has given market fundamentals strength in the near term, energy storage provides a whole new source of growing battery material demand over the longer term. Renewable Grid Storage is a collection of methods used to store electrical energy on a large scale within an electric power grid. Electrical energy is stored during times when production, particularly from select alternative sources like wind, tidal, and solar, exceeds consumption and is activated when electricity production falls below consumption. In an electrical power grid without battery energy storage, energy sources that rely on fossil fuels must be scaled up and down to match the rise and fall of energy production from intermittent energy sources. As in EVs, batteries in a grid storage system can store excess energy, mitigating peak-power demand pricing, and decouple intermittent power generation from demand. The capital cost of a utility-scale lithium-ion battery storage system is expected to decrease another 27 – 57% by 2030 per the National Renewable Energy Laboratory (“NREL”). NREL projects that cost decreases could range from 0 – 38% additional between 2030 and 2050. Moreover, BNEF forecasts call for Renewable Grid Storage to grow at a 30% CAGR through 2030, while Brandessence Market Research projected a 27.68% CAGR in taking the Battery Storage Market to nearly 50 billion by 2028.

Our Planned Products

We are a primary cobalt and secondary copper resource exploration and development company with operations in northern Chile. Chile is the leading copper-producing country in the world.

Our Strengths

Experienced, Proven Management Team

The C3’s management team and partner network have extensive industry, process, and financial expertise and a proven track record of financing, developing, building, and operating projects within the junior mining and exploration space.

Positive Jurisdiction for Investments

C3’s operations are located in Chile. Chile is a country that is a mining-friendly jurisdiction and presently has free trade agreements, economic association and cooperation agreements in place with many Western countries, including the US. The Company has fostered good industry and Government relations and has received Government support at all levels. Due to Chile’s longstanding mining history, C3 has access to very good infrastructure in terms of roads, water and electricity.

| 11 |

Quality of Primary Cobalt Project and Potential Producer of Cobalt outside of the DRC

C3’s management believes that C3 holds a potentially world-class, scarce mining project with a robust demand profile. Only one primary cobalt mine operates globally, and in 2021 an estimated 70.6% of global cobalt supply was sourced from the Democratic Republic of the Congo by USGS statistics. Security and reliability of supply is critically important for EV battery and car manufacturers, and supply risk is high due to the concentration of cobalt coming from one source. Historical mine operations and production data associated with this mining jurisdiction lowers the risk that would be associated with a greenfield project and likely increases the speed of execution. The resource has the potential to be a Tier-1 asset, and the unique characteristics of the spatial layout of the resource allow for effective use of multiple mining techniques and processing technologies.

Low-Cost Provider, Extensive Process Technology and Know-How

The C3 operating team, including its outside consultants, is comprised of a host of professionals with decades of financial, geological and mining experience and expertise. As the Company adds sub-projects to the overall La Cobaltera strategic plan, the scope of our services and materials will expand, providing low-cost benefits and opportunities to increase the pipeline.

Culture of Safety and Sustainability

Safety and sustainability are core values of our business and a critical part of our value proposition. C3 is developing ESG-focused goals, measures, and targets that are aligned with leading standards from the Global Reporting Initiative (“GRI”), the International Sustainability Standards Board (“ISSB”), and the initiative for Responsible Mining Assurance (“IRMA”) initiatives, in addition to the European Sustainability Reporting Standards under development in the European Union (“EU”) and the United States Securities and Exchange Commission’s (“SEC”) Climate-Related Disclosures. We believe our commitment to safety and sustainability is part of what will make us a preferred supplier and customer within the lithium-ion battery ecosystem.

Management Experience

Our management team, including management advisory consultants, has extensive experience in financial asset management, energy materials, water infrastructure and infrastructure. Specifically, we have significant experience in energy materials, from resource exploration and development through commercialization and closure.

Duncan T. Blount, Chief Executive Officer of C3, is responsible for Company leadership and all strategic aspects of the business. Mr. Blount has over 15 years of experience focused on global natural resources. From 2017 until joining C3, he was CEO and Director of Decklar Resources, Inc. (“DKL.V”), a TSX-V listed Nigeria-focused independent oil & gas exploration and development company. Prior to DKL.V’s focus on Nigeria, it was named Asian Mineral Resources Ltd. And was focused on a nickel-copper-cobalt mine in Vietnam. Prior to these corporate executive roles, Mr. Blount spent a decade in the investment management industry focused on natural resources in emerging markets. During this time, he held roles at RWC Partners Ltd. And Everest Capital Ltd., where he was responsible for developing commodity and natural resources portfolio strategy. Duncan presently serves as a Non-Executive Director for Decklar Resources, Inc. and, Ponce de Leon Mining LLC. He also serves on the Advisory Board of Ocean Minerals LLC and on the Index Committee of the EQM Lithium & Battery Technology Index (BATTIDX). In addition, he previously served on the boards for Kuscan Minerals SA and AMR Nickel Ltd. Duncan graduated with an MBA from the Thunderbird School of Global Management in Glendale, Arizona and a BA in Language and World Trade from Samford University in Birmingham, Alabama.

Jeremy McCann Chief Operating Officer of C3, is the Chief Operating Officer and a Founder of both Genlith Inc., a venture holdings company focused on the transformational shift in the way the world produces, stores, distributes and consumes energy, and C3. He has held these roles since inception in 2017. He is responsible for all operational aspects of C3 business. Prior to his current role, from 2008-2017 he was COO of Schooner Investment Group LLC., a registered investment advisor to multiple registered mutual funds. Jeremy graduated with a B.S. in Finance from McGill University in Montreal, Canada.

| 12 |

Jim Van Horn, Chief Financial Officer of C3, is responsible for all financial aspects of the business. Prior positions include Interim Chief Financial Officer and Chief Compliance Officer, Sigma for Mercer Global Advisors and Chief Financial Officer and Chief Compliance Officer for Sigma Investment Management Company. Jim received a post-baccalaureate in Accounting from Portland State University in Portland, Oregon and graduated with a B.S. in Chemical Engineering from Oregon State University in Corvallis, Oregon. Jim has maintained his Certified Public Accounting license with the State Board of Accountancy for the State of Oregon since May 1999.

Ignacio Moreno, Chile Country Manager of C3, has over 20 years of experience working in the public & private sectors of the mining industry. Between 2014 and 2016, he was appointed Undersecretary of Mining for the Chilean government. Previous to that he was the head of the Development division of ENAMI (Empresa Nacional de Minería), a Chilean state-run mining company. Ignacio also served several years as General Manager of Minera Cerro Dominador, a private mining company producing copper in Northern Chile. Ignacio started his career in banking for Banque Nationale de Paris in Chile. He holds a Maitrise de Gestion (Master I in the European Standard) from the University of Montpellier (France) and a Graduate Diploma in Management Sciences from the University of Bradford (UK).

Our Industry

Electric Vehicles

Spurred by the necessity to aggressively reduce carbon dioxide emissions to preserve the environment and reverse negative effects that have occurred to date, the shift from a global economy mobilized by fossil fuels to one powered by electricity is underway. This transition is no less than revolutionary in terms of the ongoing effects it will have on global civilization. Like the industrial revolution and the rise of the internet in the 1990’s, this is the next major transformative event to shape global economics and everyday human life. Consumer electronics was the first major industry to experience the trend toward electrification. Being in the early stages of the shift from internal combustion engines (“ICE”) to electric vehicles (“EV”), EVs are the segment that is currently receiving the most attention and exponential growth is expected in the near term. Energy grid storage will also become part of the trend to enable scaling of renewable energy like solar and wind. The world is going electric and green. This will require large-scale expansion in energy storage capacity. The best available technology for doing this now and for the foreseeable future is the lithium-ion battery (“LIB”), especially when weight and size are major considerations. This is why LIB technology is the energy storage of choice when it comes to e-mobility. Next-generation EV battery technology is still going to be LIB based, with innovation likely centering on the anode and electrolyte solution. The cathode has seen most of the innovation to date.

In the future, we envision a world where everyday life runs on batteries, and ipso facto, materials critical to the manufacture of batteries will see substantial increases in demand. These materials include lithium, cobalt, graphite, nickel and copper, among others. For a company to maximize shareholder value and capitalize on the creation of incremental demand for these materials, the technology and expertise to extract, process, combine, and recycle the materials is required.

Cobalt

Cobalt, a transition metal found between iron and nickel on the periodic table, is a hard, lustrous, grayish-silver metallic element with low thermal and electrical conductivity. The unique properties of cobalt and cobalt products are responsible for its extensive applications in energy storage, industrial and other areas. These characteristics include its high energy density, ability to alloy and impart strength at high temperatures, and ferromagnetic properties.

Cobalt naturally occurs in three mineral ore forms: cobaltite, smaltite, and erythrite. Concentration levels of the metal are often too low to be extracted economically, so it is usually mined as a byproduct of copper or nickel mining, with economically viable concentration levels usually observed between 0.1% and 0.5%. Ore is extracted, processed and converted into either cobalt metal or a cobalt chemical compound and delivered to chemical manufacturers. Potential chemical compounds include cobalt carbonate, cobalt sulfate, and cobalt salt derivatives. The vast majority of demand for these compounds comes from the rechargeable battery segment.

| 13 |

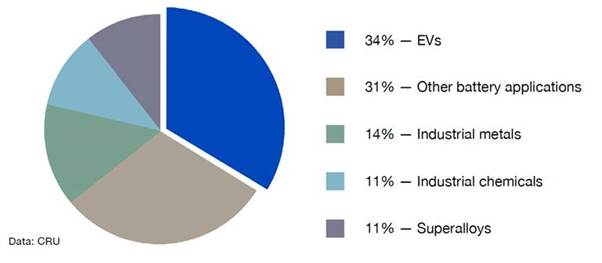

Cobalt applications can be divided into two primary categories: chemical and metallurgical. Based on research by the CRU Group on behalf of the Cobalt Institute for 2021, the batteries market, including consumer batteries (smartphones, tablets, other electronic devices) and EVs, currently accounts for approximately 87% of cobalt chemical demand and about 65% of overall cobalt demand. Metallurgical cobalt is the second largest cobalt consuming market at approximately 25% of overall cobalt demand. This is used primarily to produce superalloys consisting of cobalt combined with other metals such as nickel and/or iron. These alloys are surface stable and resistant to heat, corrosion and oxidation, which makes them valuable to and widely used by the aerospace, electricity generation, aircraft, medical, automotive, and military-related industries. Other applications for metallurgical cobalt include hard metals and diamond tools, catalysts in oil and gas refinement, and pigments.

Cobalt in Lithium-ion Batteries

Lithium-ion batteries that contain cobalt have high energy density, making them lightweight and efficient in terms of energy delivered relative to size, which helps to maximize EV driving range. Cobalt’s properties also give it distinct advantages in improving the longevity and safety of lithium-ion batteries, as its tight molecular compound structure allows for a high cycling ability – shorter recharge times and more charging and recharging cycles, and its high heat capacity provides good thermal stability to battery chemistries.

Lithium-ion battery cathodes come in a variety of chemistries, some of which contain cobalt and others that do not contain cobalt. The main cobalt containing chemistries are: lithium cobalt oxide (“LCO”) – LiCoO2, lithium nickel manganese cobalt oxide (“NMC”) – LiNiMnCoO2, and lithium nickel cobalt aluminum oxide (“NCA”) – LiNiCoAlO2. The NMC chemistry is the dominant chemistry of the cobalt-containing configurations.

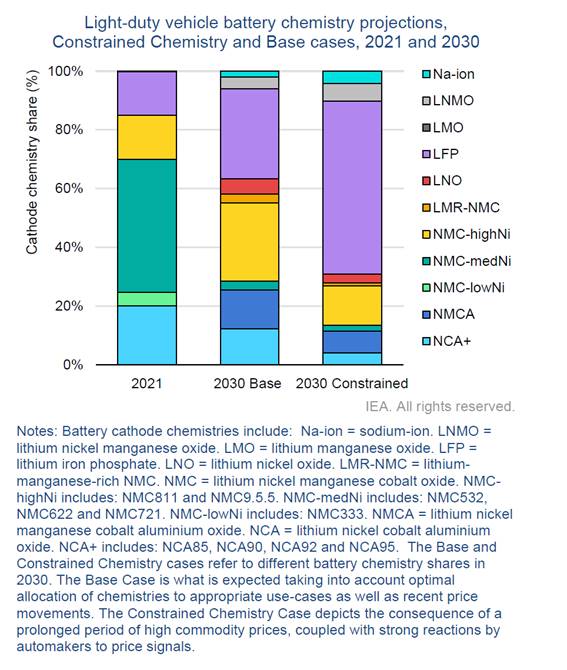

In the chart that follows in the “Industry Demand” section from the International Energy Agency (“IEA”), it can be seen that by 2030, cobalt-containing chemistries are expected to have somewhere in the range of 28% (constrained case) to 59% (base case) of the overall light-duty vehicle battery chemistry demand, while non-cobalt-containing substitutes, such as lithium iron phosphate (“LFP”) are expected to hold the balance of the market. The constrained case is where a prolonged period of higher battery metal prices pushes automakers toward alternatives.

Within the NMC chemistry is the question of what ratio of cobalt to other metals is optimal. NMC532, NMC622, NMC811 and NMC 9.5.5. NMC 811 or NMC 9.5.5 appear to be the most likely NMC chemistry sub-types to become the cobalt-containing battery cathode market leader. However, projections suggest that LFP will become the overall market leader for battery cathodes (i.e., overall for cobalt and non-cobalt containing cathodes). The emergence of chemistries with less cobalt or no cobalt are a definite consideration for long-term cobalt demand. Scientists, however, continue to lament the technical difficulties of implementing low- or no-cobalt configurations, such as the 811 chemistry, for large-scale applications. The bottom line is cobalt is a necessary element to produce lithium-ion batteries with high energy densities coupled with favorable thermal stability profiles. The most likely scenario is that the rate of decrease of cobalt content in batteries will be far outstripped by the rapid increase in demand for lithium-ion batteries due to the exponential growth in the adoption of EVs, as depicted in the following chart.

| 14 |

Industry Demand

The growth forecasted in the EV market has resulted in a significant increase in current and expected future demand for battery-grade cobalt compounds. AllianceBernstein (“AB”) as presented in The Economist projected EV battery capacity to increase from approximately 460 Gwh in 2022 to around 2.7TWh in 2030. This has EV battery capacity tracking at more than 40% of the overall LIB demand as depicted in the BMI gigafactory projections presented earlier. In the Cobalt Market Report 2021, released in May 2022, the Cobalt Institute projected medium term increases in cobalt demand from 175 kilotonnes in 2021 to around 320 kilotonnes by 2026, rising at a CAGR of 12.7% over that period. IEA projections are more cautious, expecting the market for EV-related uses of cobalt will increase by 2030 to somewhere between 250 kilotonnes to as much as 295 kilotonnes of annual cobalt demand, unless countries align with a net zero emissions by 2050 (“NZE”) standard, in which case annual demand for cobalt could be expected to reach as much as 410 kilotonnes by the end of that period.

| 15 |

In 2021 EV applications were the largest end-use sector for cobalt as depicted in the following chart compiled by CRU on behalf of the Cobalt Institute. This was the first year ever that EV applications were the predominant end-use sector and expectations are that this sector will only continue to increase its spread compared to other end use applications in the coming years.

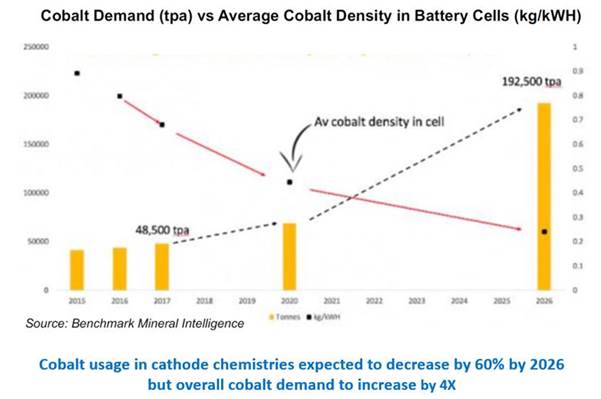

As of forecasts prepared in late 2020, BMI projected cobalt demand for battery applications to increase from 66,000 tonnes in 2020 to just over 1.1 million tonnes in 2040. Adding in the cobalt demand forecast for non-battery applications, total cobalt demand is expected to reach 1.2 million mt in 2040 from a current level of ~159,000 tonnes, for a predicted CAGR of 11.9%.

Additionally, IEA forecasts that by 2030, demand for the NMC-High Nickel type of batteries, which includes the NMC811 cathode chemistry, will range from approximately 13% (constrained) to 27% (base) across all battery chemistries, as depicted in the following chart. As indicated in the earlier BMI chart, while cobalt usage is expected to decrease through 2026, the annual demand is expected to increase substantially through that same period. Therefore, even using relatively conservative assumptions for cobalt-containing battery chemistries, this illustrates that the rapid growth of EV market penetration is likely to still create a substantial increase in cobalt demand in the EV space and overall. This expectation aligns well with the earlier projections that have total annual cobalt demand close to or more than doubling by 2030, depending on the scenario and underlying assumptions. These estimates are roughly in line with a 2022 BNEF projection for a 1.5X increase in demand for cobalt from lithium-ion batteries for 2030 compared to 2021.

| 16 |

| 17 |

Industry Supply

Cobalt is a fairly rare metal, comprising only 0.001% of the earth’s crust, though widely dispersed and commonly found and obtained in association with other mining activities. More commonly, cobalt is found in ores of iron, nickel, copper, silver, manganese, zinc, and arsenic. Cobalt is usually mined as a by-product of either nickel, copper, or other more abundant metals. Most cobalt production is ultimately dependent on the production of copper and nickel, and the mined ore often contains only 0.1% - 0.5% elemental cobalt. Global cobalt reserves are estimated by the United States Geological Survey as of January 2021 to be about 7.1 million tonnes with just over 50% of these reserves located in the DRC.

Per USGS estimates, mined cobalt production for 2021 was estimated at roughly 170,000 tonnes of mined supply produced. As stated earlier in the “Quality of Primary Cobalt Project and Potential Producer of Cobalt outside of the DRC” section, approximately 70.6% of the current supply comes from the DRC. The next largest mining producer of cobalt is Russia, with around a 4.5% market share.

IEA projects that annual cobalt supply will just exceed approximately 300 kilotonnes by 2030 and this will approximately pace the overall demand as referenced earlier in the “Industry Demand” section. This balancing presumes that NZE models aren’t the prevailing scenario, as that would predict much higher demands and imbalances with supply. The following chart is IEA’s long-term cobalt supply forecast, which shows a substantial ramp-up in the quantity of cobalt supplied to the market, particularly over the next few years. IEA expected a CAGR of approximately 12% over the period from 2020 to 2025. In the chart, the y axis represents quantity in kilotonnes, the supply is represented by the light blue highlighted bars, whereas, the green and gold lines and red shaded bars, represent demand for the stated policies scenario (status quo), announced pledges scenario (greater action taken) and NZE scenario, respectively. It should be noted that the supply forecasts by IEA were derived from BMI information and as such, the forecast is likely to include mined production from expected and potential future producers who have a quantifiable probability of bringing supply to market over the projection timeframe, which is a characteristic attribute of BMI projections.

| 18 |

Industry Supply, Demand, and Pricing Dynamics

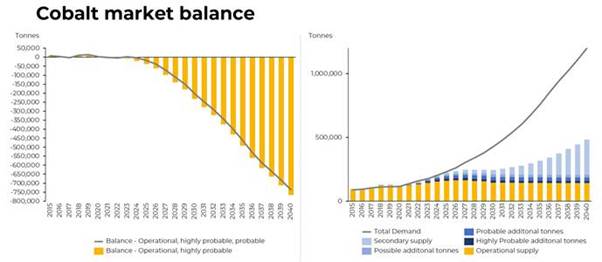

Cobalt is presently in a state of surplus, as more material is being supplied to the market than there is demand. However, as depicted in the side-by-side charts from BMI that follow, annual shortages compared to current and projected sources of supply are expected to begin within the next few years and only get more pronounced with each successive year. By 2040 this shortfall is anticipated to be as drastic as 800 kilotonnes, unless presently unknown sources of potential or proven reserves come online, are exploited and add to the anticipated supply volumes. This shortfall is nearly 5X the 2021 overall global cobalt production. The charts show the situation from a balance of supply and demand to a gap in supply and demand perspective and vary the presentation by showing highly probable supply apart from probable, possible and secondary sources.

By observing any trailing 5-year historical charts, it is evident that Cobalt pricing suffered from the second half of 2018 through early 2019. This was primarily due to negative sentiment and increased short-term supply. The price remained fairly flat from its low in early 2019 until around mid-2020, where squeezed supply from the Covid-19 pandemic along with increasing demand, due to the EV transition needs caused prices to start climbing toward their peak around $82,000USD per tonne in early-March 2022 through mid-May 2022. Prices have receded to a more balanced supply-demand state around $50,000USD per tonne from mid-July 2022 to present.

The cobalt market is a relatively small niche market compared to other metals and commodities, and much of the supply is tied up in long term contracts between producers and their offtake partners, among others. Companies that are increasingly concerned about being socially responsible within their supply chains enter into these contracts to obtain a reliable and clean supply of cobalt. Market perception of price moves in cobalt is often influenced by cobalt futures pricing published by the London Metals Exchange (LME). Because most cobalt supply is tied up in long-term contracts, the relatively small percentage of supply that trades on the LME does not necessarily originate from the highest quality sources, and due to the small size of the market, pricing is susceptible to increased volatility on low trading volume.

| 19 |

Property Disclosures

As it relates to the material property details for the La Cobaltera Project, C3 and Baltum, are exploration-stage companies and all areas described are exploration-stage areas of the overall property.

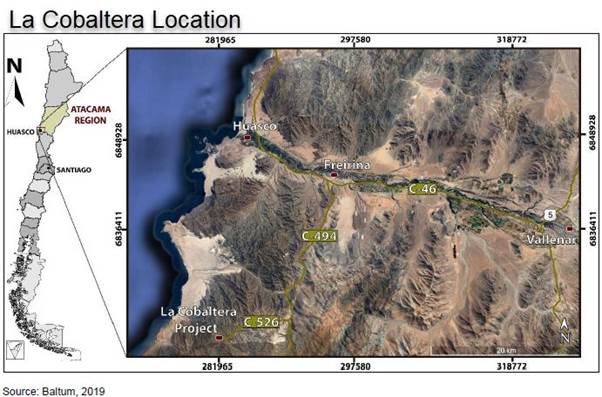

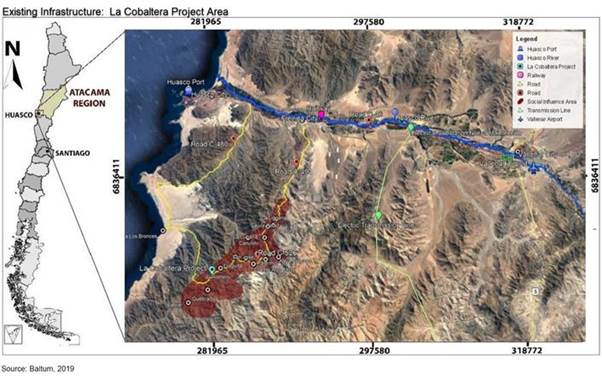

Descriptively, La Cobaltera is located in northern Chile, 48 kilometers (approximately 30 miles) south of Huasco, Huasco Province, Atacama Region. The property is located approximately 700 kilometers north of Santiago. The UTM coordinates are E 285,170 longitude and N 6,823,000 latitude with a variable elevation between 700 – 1,100 meters above sea level.

The following map depicts the existing infrastructure near the La Cobaltera Project.

For roads, see the yellow lines and orange with black dot markers in the preceding map, which show the primary routes in the area which are: Hwy 5, C-46, C-494 and C-526.

| 20 |

For railroads, see the pink marker in the following map. The freight train carrier, Ferronor, owns lines throughout Chile, including the one depicted, which is a 49 kilometer branch line between the port of Huasco and Vallenar. At Vallenar, there is a junction with the main line that runs north and south in Chile and allows for freight connections to other major regions of Chile.

For airports, see the plane icon in the following map, which references Vallenar Airport. The Vallenar Airport is a smaller regional airport that doesn’t serve commercial flights. It has an asphalt runway of 4,521 feet in length. Most commercial flights are routed through either La Serena, Chile to the South or Copiapo, Chile to the North with bus or other means of transportation to get to Vallenar and the surrounding areas.

The towns of Huasco City, Freirina City, Vallenar City are labeled in the following map and are the primary population centers in the area.

For ports, see the lighthouse icon in the following map, which references Huasco Port. This is a medium-sized port, with the maximum length of vessels recorded entering the port of 300 meters, maximum draught of 14 meters and maximum deadweight of 209,537 tonnes.

Water sources are generally from onsite wells, when available for smaller needs, trucked into the area for employee use and consumption, or derived from seawater for direct processing use or after first being desalinated, if a pipeline is constructed for transporting the water from the nearby ocean to the site. Both C3 and Baltum are highly sensitive to the social impact of water usage in a dry, drought-prone area and strives to leverage sources that minimize the impact to the local population and the environment.

| 21 |

The previous map depicts an electric transmission line in green. It should be noted that the grid in the area is supplied by electricity generation from a variety of sources, such as solar, wind, hydroelectric and coal.

Personnel will typically be sourced from nearby towns for general mining labor once that occurs. Experts, such as geologists, engineers, independent consultants and onsite management are typically sourced from major Chilean cities, such as Santiago, or from non-Chilean labor.

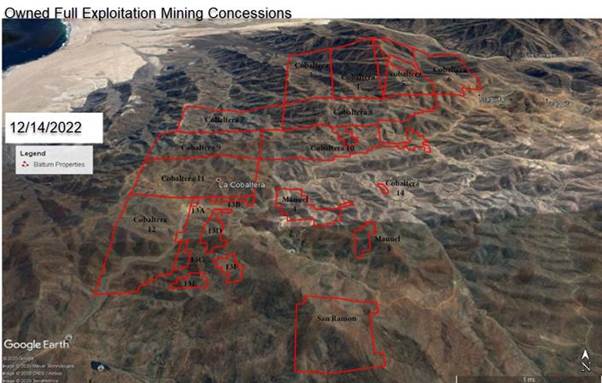

The mining concessions that comprise the La Cobaltera Project are depicted in the following map:

COBALTERA 3, 1 to 300 (300 hectares); COBALTERA 4, 1 to 300 (300 hectares); COBALTERA 5, 1 to 264 (264 hectares); COBALTERA 6, 1 to 270 (270 hectares); COBALTERA 7, 1 to 200 (200 hectares); COBALTERA 8, 1 to 269 (269 hectares); COBALTERA 9, 1 to 200 (200 hectares); COBALTERA 10, 1 to 207 (207 hectares); COBALTERA 11, 1 to 200 (200 hectares); COBALTERA 12, 1 to 189 (189 hectares); COBALTERA 13A, 1 to 2 (2 hectares); COBALTERA 13B, 1 to 8 (8 hectares); COBALTERA 13C, 1 to 9 (9 hectares); COBALTERA 13D, 1 to 23 (23 hectares); COBALTERA 13E, 1 to 11 (11 hectares); COBALTERA 13F, 1 to 14 (14 hectares); COBALTERA 14, 1 to 3 (3 hectares); MANUEL TRES [3] 1 to 13 (13 hectares); MANUEL 4 1/60 (60 hectares); SAN RAMON 1 to 10 (93 hectares). In aggregate, the material mining property is 2,635 hectares. To retain the full exploitation status properties described above, Baltum must pay the Chilean Treasury Department annual patent fees (estimated to be approximately $6.30USD per hectare).

| 22 |

The condition of the mining concession areas within the La Cobaltera Project is generally in their natural state, as little to no exploration has yet to be conducted onsite. What has been completed is GeoMagDrone imaging of magnetic field variances (including Total Magnetic Intensity, Magnetic Intensity Reduction to Pole and Magnetic Analytical Signal) in areas that include COBALTERA 13C, COBALTERA 13E, COBALTERA 13F, COBALTERA 14, MANUEL TRES and MANUEL 4 in their entirety and varying portions of COBALTERA 6 (SE Corner, approximately 15 – 20% by area), COBALTERA 8 (South sliver, approximately 5% or less by area), COBALTERA 10 (Eastern half, approximately 40 – 45% by area), COBALTERA 11 (SE Corner, approximately 5% or less by area), COBALTERA 12 (lower ¾, approximately 70 – 75% by area), COBALTERA 13B (Eastern half, approximately 50 – 55% by area), COBALTERA 13D (lower ¾, approximately 75 – 80% by area) and SAN RAMON (NE Corner, approximately 10 – 15% by area). To reiterate, at present this is an exploration-stage material property as are each of the areas outlined previously.

The Company exploration program is focused on the continuance of widespread use of any and all non-destructive means of exploration, such as GeoMagDrone, GeoPhysics, Drone surveys, Robotic fieldwork and other non-invasive or less-invasive methods that we can devise or that become available to us through technological advances. Once this preliminary data is obtained, our geologists will use the data to determine the best target sites for core sample drilling in order to maximum the coverage for higher probability areas and achieving overall minimization of the use of drilling while scoping for resources and/or reserves that could lead toward development and production. There are no existing mines in these areas and the proposed program is exploratory in nature. Furthermore, there is no equipment, facilities, mine infrastructure or underground development on this overall material property. The carrying book value of the La Cobaltera Property for accounting purposes is $0. As none of the areas described have been previously developed, there is no history of previous operations on the material property. There are no significant encumbrances to the material property, as exploitation-level mining concessions in Chile have an indefinite life, as long as the annual patent fees are paid each year, as discussed previously. To do any core sample drilling or more invasive development beyond that would require submittal of an Environmental Assessment and Plan of Work for approval. There is no permitting required to perform the type of non-invasive exploration that is outlined earlier in the paragraph with regard to the exploration program.

Baltum may be subject to a fine imposed by the National Forestry Corporation of the Atacama Region ("CONAF"), which is currently being negotiated by Baltum’s counsel and CONAF, of up to $4,000, which may be reduced by as much as 50%. This is in connection with a self-report made by Baltum to CONAF on May 13, 2019, reporting the involuntary cutting of certain vegetation species in the La Cobaltera sector. Since Baltum made a self-report to CONAF, the applicable fine may be reduced by as much as 50%. We do not believe that this fine, even if imposed in the full amount, will have any material effect on the Company’s business, financial position or results of operations.

Exploration Program Internal Controls

There are no internal controls in place at this time with regard to the Company’s exploration program as there are currently no exploration and mineral resource reserve estimation efforts by the Company at this time. As there are presently no mineral resource and reserve estimation efforts on the Company’s material property, related to any of its mining concession areas, there are no applicable internal controls or quality control and quality assurance programs for their estimation in place at this time. However, when it is appropriate to make mineral resource and reserve estimations, the Company intends to engage industry-respected, independent geological consultants to oversee and provide assurance to this process of estimating mineral resources and reserves.

COVID-19

In March 2020, the World Health Organization declared the outbreak of a novel coronavirus (“COVID-19”) as a pandemic. Variants of this virus continues to spread throughout the United States and the world. Efforts implemented by local and national governments, as well as businesses, including temporary closures, have had adverse impacts on local, national and global economies. The extent of the impact of COVID-19 on C3 operational and financial performance going forward will depend on certain developments, including but not limited to the duration and continued spread of the outbreak and strand mutations, the availability and use of vaccines, the development of therapeutic drugs and treatments, and the direct and indirect impacts on our employees, vendors, and customers, all of which are uncertain and cannot be fully anticipated or predicted.

| 23 |

We have experienced material disruptions to our business because of COVID-19. For example, as discussed below, due in part to complications from COVID-19, the inability to raise capital and maintain operations necessitated the decision on the Company’s part to let the installment options to purchase both La Cobaltera and Carrizal Alto lapse in 2020.

As such, we can provide no assurance that our operations will not be materially and/or adversely affected by the COVID-19 pandemic in the future that could result from any worsening of the pandemic, the effect of mutating strains, additional outbreaks of the pandemic, actions taken to contain the pandemic’s spread or treat its impact, continued availability of vaccines, and their distribution, acceptance and efficacy, and governmental, business and individual actions taken in response to the pandemic including government-imposed regulations regarding, among other things, COVID-19 testing, vaccine mandates and related workplace restrictions.

Corporate History

On December 4, 2017, Chilean Cobalt Corp. (“C3”) was incorporated in the state of Nevada.

On January 3, 2018, C3 formed a direct, wholly-owned Chilean operating subsidiary, named Baltum Mineria SpA (“Baltum”).

Founder Shares

On December 4, 2017, in connection with the incorporation of C3 on December 4, 2017, C3 issued 11,666,667 shares (pre-reverse split) of common stock at a purchase price of $0.0001 per share (for an aggregate of $1,166.67 of proceeds) to Genlith, Inc. in a private placement under Rule 506(b) of Regulation D of the Securities Act.

Acquisition of Mining Concessions in Northern Chile's Atacama region

In January 2018, C3 entered into a stock purchase agreement pursuant to which C3 agreed to sell to investors 5,000,000 shares of Series A Convertible Preferred Stock (“Preferred Stock”) at $1.00 per share for gross proceeds of $5,000,000. The proceeds from this stock purchase agreement funded the acquisition of mining concessions to develop premier cobalt and copper projects in Northern Chile's Atacama region.

| (i) | On January 19, 2018, the Company’s subsidiary Baltum signed a unilateral option contract for the purchase of mining concessions with Sociedad Legal Minera Soledad Uno de la Sierra Arenillas Atlas and Homero Eduardo Callejas Molina. |

| (ii) | On March 16, 2018, the Company’s subsidiary Baltum signed unilateral option contract for the purchase of additional mining concessions with Sociedad Minera Contractual Carrizal Alto. |

However, due to complications from COVID-19 and Chilean Unrest at the end of 2019 and into 2020, the inability to raise capital and maintain operations necessitated the decision to let the installment options to purchase both La Cobaltera and Carrizal Alto lapse in 2020.

Land Consolidation Package

On April 2, 2019, Baltum entered into a land consolidation package with Cobalta Chile SpA which included mining exploration and exploitation concessions in the La Cobaltera District, Chile. The total consideration paid to Cobalta Chile SpA was $600,000, of which $550,000 went towards acquisition of exploitation and exploration claims, the other $50,000 went towards an option on three additional exploitation claims of which one was eventually purchased on November 6, 2020 for an additional $116,666. Overall acquisition costs paid to Cobalta Chile SpA were $716,666.

| 24 |

Private Placement in 2019– Common Stock

During the period from March 2019 through June 2019, C3 issued 2,900,000 shares (pre-reverse split) of common stock at a purchase price of $4.00 per share (for an aggregate of $11,600,000 of proceeds) to accredited investors in a private placement under Rule 506(b) of Regulation D of the Securities Act. On June 26, 2019, Genlith, Inc. retired $400,000 of debt for 100,000 shares (pre-reverse split) of common stock at a valuation of $4.00 per share. Genlith, Inc. also exchanged share-for-share 100,000 shares of Genlith, Inc. for 100,000 shares of C3 with four separate shareholders of C3.

During September 2019, C3 issued 3,383,625 shares (pre-reverse split) of common stock at a purchase price of $1.45 per share (for an aggregate of $4,906,250 of proceeds) to accredited investors in a private placement under Rule 506(b) of Regulation D of the Securities Act. Also on September 3, 2019, Genlith, Inc. retired $1,500,000 of debt for 1,034,485 shares (pre-reverse split) of common stock at a valuation of $1.45 per share.

Anti-dilution Shares Issued

This issuance was made to the thirteen shareholders who acquired shares in September 2019 at $1.45 per share signing agreements to waive their anti-dilution rights. These thirteen shareholders received an additional 4.8 shares to each of their shares giving them an effective 5.8 shares for every share, totaling 21,206,892 shares issued. Only par was paid, which was paid by Genlith, Inc. on behalf of all shareholders, for accounting purposes, this created a non-cash loss on the independently valued price of $0.09 per share on July 24, 2020 compared to par paid – a $1,906,500 non-cash loss. This issuance was made in reliance on Rule 506(b) of Regulation D of the Securities Act.

1-for-13.430605 Reverse Stock Split

Our board of directors and shareholders approved on July 23, 2020 and July 24, 2020, respectively, a 1-for-13.430605 reverse split of our common stock, which was effected on August 10, 2020. The reverse split combined each 13.430605 shares of our outstanding common stock into one share of common stock. No fractional shares were issued in connection with the reverse split, and any fractional shares resulting from the reverse split were rounded to the nearest whole share. All references to common stock, share data, per share data and related information have been retroactively adjusted, where applicable, in this Annual Report on Form 10-K to reflect the reverse split of our common stock as if it had occurred at the beginning of the earliest period presented. As a result of the reverse stock split, the number of shares of common stock issued and outstanding decreased from 40,291,669 shares as of August 10, 2020, to approximately 3,000,000 shares. In connection with the reverse stock split, we filed a Certificate of Change to effect the reverse stock split with the Secretary of State of Nevada on August 10, 2020.

Share Exchange in 2020 – Common Stock

On August 10, 2020, C3 issued 4,000,000 shares of common stock to holders of Series A Convertible Preferred Stock in exchange for 5,151,125 shares of Series A Convertible Preferred Stock (including 151,125 received as dividends paid-in-kind) held by such holders in reliance upon the exemption from registration provided by Section 3(a)(9) of the Securities Act.

Share Exchange in 2020 – Common Stock for Convertible Debt

On August 18, 2020, C3 issued 3,000,000 shares of common stock to Genlith, Inc. in exchange for complete extinguishment of $4,100,000 of principal debt and all accrued interest on such debt in reliance upon the exemption from registration provided by Section 3(a)(9) of the Securities Act.

| 25 |

Rights Issuance in 2020 – Common Stock

During the period from August 24, 2020 through September 17, 2020, C3 issued 1,000,000 shares of common stock at a purchase price of $0.50 per share (for an aggregate of $500,000 of proceeds) to existing shareholders in reliance upon the exemption from registration provided by Section 506(b) of Regulation D of the Securities Act.

Private Placement in 2021 – Common Stock

On December 31, 2021, C3 issued 41,667 shares of common stock at a purchase price of $0.60 per share (for an aggregate of $25,000 of proceeds) to an accredited investor in a private placement under Rule 506(b) of Regulation D of the Securities Act.

Recent Developments

Private Placements in 2022 – Common Stock

During the period from January 2022 through April 2022, C3 issued 1,958,333 shares of common stock at a purchase price of $0.60 per share (for an aggregate of $1,175,000 of proceeds) to accredited investors in a private placement under Rule 506(b) of Regulation D of the Securities Act.

Approval of Chilean Cobalt Corp. 2022 Equity Incentive Plan

Our board of directors and shareholders adopted and approved on April 26, 2022 and April 29, 2022, respectively, the Chilean Cobalt Corp. 2022 Equity Incentive Plan, effective April 29, 2022, under which incentive stock options, non-statutory stock options, stock appreciation rights, restricted stock, restricted stock units, performance awards, cash-based awards and other stock-based awards may be granted to officers, directors, employees and consultants, as applicable. Under the Plan, 1,950,000 of common stock, par value $0.0001 per share, are reserved for issuance.

Genlith, Inc. Distribution of C3 Shares of Common Stock to Shareholders of Genlith, Inc.

On May 12, 2022, Genlith, Inc. distributed to the shareholders of Genlith, Inc. on a pro rata basis 4,786,727 shares of common stock of C3 held by Genlith, Inc., representing Genlith, Inc.’s entire holdings of capital stock of C3.

Appointment of VStock Transfer, LLC as Transfer Agent

On May 20, 2022, C3 entered into that certain Transfer Agent and Registrar Agreement with VStock Transfer, LLC, whereby VStock Transfer, LLC agreed to act as the transfer agent of C3.

Issuance of Stock Options under 2022 Equity Incentive Plan

On May 24, 2022, the Company granted options to purchase an aggregate of 825,000, 400,000, and 450,000 shares of common stock at an exercise price of $0.60 per share to officers/management, advisors, and directors, respectively, of the Company in recognition of their services to the Company. Such granted options are subject to graduated vesting in the following installments on each of the following dates: options to purchase 25% of granted shares on June 30, 2022 and options to purchase 12.5% of granted shares on September 30, 2022, December 31, 2022, March 31, 2023, June 30, 2023, September 30, 2023, and December 31, 2023.

| 26 |

On June 1, 2022, the Company granted options to purchase an aggregate of 26,668 shares of common stock at an exercise price of $0.60 per share to an advisor of the Company in recognition of his services to the Company. Such granted options are subject to graduated vesting in the following installments on each of the following dates: options to purchase 25% of granted shares on August 31, 2022, November 30, 2022, February 28, 2023, and May 31, 2023.

On July 15, 2022, the Company granted options to purchase an aggregate of 150,000 shares of common stock at an exercise price of $0.60 per share to an officer and director of the Company in recognition of his services to the Company. Such granted options are subject to graduated vesting in the following installments on each of the following dates: options to purchase 25% of granted shares on September 30, 2022, December 31, 2022, March 31, 2023 and June 30, 2023.

On July 28, 2022, the Company granted options to purchase an aggregate of 50,000 shares of common stock at an exercise price of $0.60 per share to an officer and director of the Company in recognition of his services to the Company. Such granted options are subject to graduated vesting in the following installments on each of the following dates: options to purchase 12.5% of granted shares on September 30, 2022, December 31, 2022, March 31, 2023, June 30, 2023, September 30, 2023, December 31, 2023, March 31, 2024 and June 30, 2024.

Kevin Russell resigned as director of the Company effective November 3, 2022, and on the same date forfeited to the Company options to purchase 31,250 shares of the Company’s common stock held by Mr. Russell, which were part of the options to purchase 450,000 shares of the Company’s common stock granted to directors on May 24, 2022 as described above.

Current Private Placement of Common Stock

The Company is currently engaged in a private placement under Rule 506(c) of Regulation D of the Securities Act (“Current Private Placement”) of up to 1,558,442 of its shares of common stock for $0.77 per share, for an aggregate of gross proceeds in the amount of up to approximately $1,200,000. However, the Company may not be able to raise this amount and may have to close the private placement at a lower amount. Additionally, there can be no assurance that the Company will be able to raise any funds in this private placement.

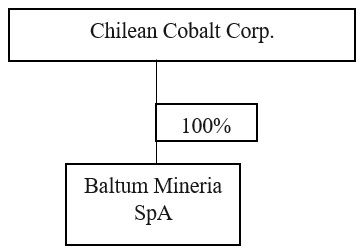

Organizational Structure

The following is a current organizational chart of our Company:

| 27 |

Employees

As of March 24, 2023, we had 3 full-time employees. None of our employees is represented by a union. We consider our relations with our employees to be good.

Legal Proceedings

From time to time, we are involved in various claims and legal actions arising in the ordinary course of business. There are no legal proceedings currently pending against us which we believe would have a material effect on our business, financial position or results of operations and, to the best of our knowledge, there are no such legal proceedings contemplated or threatened.

We may be subject to a fine imposed by the National Forestry Corporation of the Atacama Region ("CONAF"), on our subsidiary Baltum Mineria SpA (“Baltum”), which is currently being negotiated by Baltum’s counsel and CONAF, of up to $4,000, which may be reduced by as much as 50%. This is in connection with a self-report made by Baltum to CONAF on May 13, 2019, reporting the involuntary cutting of certain vegetation species in the La Cobaltera sector. Since Baltum made a self-report to CONAF, the applicable fine may be reduced by as much as 50%. We do not believe that this fine, even if imposed in the full amount, will have any material effect on the Company’s business, financial position or results of operations.

Description of Properties

Our corporate offices are located at 1199 Lancaster Ave, Suite 107, Berwyn, Pennsylvania 19312. Genlith, Inc. founder of the Company and former shareholder, allows the Company to share this office at no cost by verbal agreement among the two entities.

Baltum’s corporate offices are located at Rosario Norte 100, of. 1401, Las Condes, Santiago, Chile. Gestion Ambiental S.A. (“SGA”), an affiliate of Genlith, Inc. and provider of certain accounting and administrative services to Baltum, SGA allows Baltum to use this office for address-purposes and as necessary at no cost by verbal agreement among the two entities.

Competition

We expect to compete globally against a number of other cobalt and copper producers. Competition is based on several key criteria, including technological capabilities, service, product performance and quality, ESG factors and price. Some of our competitors are larger than we are and may have greater financial resources. These competitors may also be able to maintain greater operating and financial flexibility. If we fail to compete effectively, we may be unable to retain or expand our market share, which could have a material adverse effect on our business, results of operations and financial condition.

| 28 |

Government and Environmental Regulations

In the ordinary course of business we are required to obtain and renew governmental permits for our current limited operations at our projects. We will also need additional governmental permits to accomplish our long-term plans to mine cobalt under plans yet to be developed. Obtaining or renewing the necessary governmental permits is a complex and time-consuming process involving costly undertakings by us. The duration and success of our efforts to obtain and renew permits are contingent upon many variables not within our control, including the interpretation of applicable requirements implemented by the permitting authority and intervention by third parties in any required environmental review. We may not be able to obtain or renew permits that are necessary on a timely basis or at all, and the cost to obtain or renew permits may exceed our estimates. Failure to comply with the terms of our permits may result in injunctions, fines, suspension or revocation of permits and other penalties. We can provide no assurance that we have been, or will at all times be, in full compliance with all of the terms of our permits or that we have all required permits. The costs and delays associated with compliance with these permits and with the permitting process could alter all or a portion of any mine plan we may propose in the future, delay or stop us from proceeding with the development of our projects or increase the costs of development or production, any or all of which may materially and/or adversely affect our business, prospects, results of operations, financial condition and liquidity.

We are subject to extensive federal, state, local, and foreign environmental and safety laws, regulations, directives, rules and ordinances concerning, among other things, employee health and safety, the composition of our planned products, the discharge of pollutants into the air and water, the management and disposal of hazardous substances and wastes, the usage and availability of water, the cleanup of contaminated properties (including the federal Comprehensive Environmental Response, Compensation and Liability Act, commonly known as CERCLA or Superfund, in the U.S., and similar foreign and state laws) and the reclamation of our future mine extraction operations and certain other assets at the end of their useful life. In addition, our future production facilities will require numerous operating permits. Due to the nature of these requirements and changes in our planned operations, we may incur substantial capital and operating costs, which may have a material adverse effect on our results of operations. The Company does not currently have any production facilities in place as these are all in the future planning stages at this time and accordingly, the Company has not yet started the permit process in respect to such planned production facilities.

We may also incur substantial costs, including fines, damages, criminal or civil sanctions and remediation costs, or experience interruptions in our operations, for violations arising under these laws and regulations or permit requirements. In addition, we may be required to either modify existing or obtain new permits to meet our capacity expansion plans. We may be unable to modify or obtain such permits or if we can, it may be costly to do so. Furthermore, environmental, health and safety laws and regulations are subject to change and have become increasingly stringent in recent years. Future environmental, health and safety laws and regulations could require us to alter our production processes, acquire pollution abatement or remediation equipment, modify our planned products or incur other expenses, which could harm our business and results of operations.

If we violate environmental, health and safety laws or regulations, in addition to being required to correct such violations, we can be held liable in administrative, civil or criminal proceedings for substantial fines and other sanctions could be imposed that could disrupt or limit our operations. Liabilities associated with the investigation and cleanup of hazardous substances, as well as personal injury, property damages or natural resource damages arising from the release of, or exposure to, such hazardous substances, may be imposed without regard to violations of laws or regulations or other fault, and may also be imposed jointly and severally. Such liabilities may also be imposed on many different entities, including, for example, current and prior property owners or operators, as well as entities that arranged for the disposal of the hazardous substances.

| 29 |

ITEM 1A. RISK FACTORS

Our business is subject to numerous risks and uncertainties. These risks represent challenges to the successful implementation of our strategy and to the growth and future profitability of our business. These risks include, but are not limited to, the following :

| · | We are in the early stages of our operations; | |

| · | We have a history of operating losses and our management has concluded that factors raise substantial doubt about our ability to continue as a going concern and our auditor has included an explanatory paragraph relating to our ability to continue as a going concern in its audit report for the fiscal years ended December 31, 2022 and 2021; | |

| · | Our current cash resources will not allow us to become profitable and will only allow us to fund operations for a limited period of time; | |

| · | We will need additional capital to fund our operations, which, if obtained, could result in substantial dilution or significant debt service obligations. We may not be able to obtain additional capital on commercially reasonable terms, which could adversely affect our liquidity and financial position; | |

| · | The COVID-19 pandemic may adversely impact our business and financial condition; | |

| · | Our growth depends upon the continued growth in demand for end-products utilizing rechargeable storage batteries, particularly electric vehicles; | |

| · | Adverse conditions in the economy and volatility and disruption of financial markets can negatively impact our prospective customers, and downturns in our prospective customers’ end-markets could adversely affect our prospective sales and profitability; | |

| · | Our research and development efforts may not succeed, and our competitors may develop more effective or successful products; | |

| · | Cobalt and copper prices can be volatile, especially due to changes in supply; | |

| · | We face competition in our business; | |

| · | Our planned production development efforts are complex projects that will require significant capital expenditures and are subject to significant risks and uncertainties; | |

| · | We may make future acquisitions which may be difficult to integrate, divert management and financial resources and result in unanticipated costs; | |

| · | The development and adoption of new battery technologies that rely on inputs other than cobalt compounds could significantly impact our prospects and future revenues; | |

| · | We have substantial international operations, and the risks of doing business in foreign countries could adversely affect our business, financial condition and results of operations; |

| 30 |

| · | Our planned cobalt and copper extraction and planned production operations in Chile will expose us to specific political, financial and operational risks; | |

| · | Our planned operations will be subject to hazards and other disruptions, which could adversely affect our reputation and results of operations; | |

| · | We may not satisfy prospective customers’ or governments’ quality standards, and we could be subject to damages based on claims brought against us or lose customers as a result of the failure of our planned products to meet certain quality standards; | |

| · | Fluctuations in the price of energy and certain raw materials, and our inability to obtain raw materials and products under contract sourcing arrangements, could have an adverse effect on the margins of our planned products, our business, financial condition and our results of operations; | |

| · | Our success depends upon our ability to attract and retain key employees and the identification and development of talent to succeed senior management; | |

| · | Some of our employees will be unionized or will be employed subject to local laws that are less favorable to employers than the laws of the United States; | |

| · | Our business and operations could suffer in the event of cybersecurity breaches or disruptions to our information technology environment; | |

| · | Our inability to protect our intellectual property rights could have a material adverse effect on our business, financial condition and results of operations; | |

| · | We have not established “proven” or “probable” reserves, as defined by the SEC under Industry Guide 7, through the completion of a feasibility study for the minerals that we produce; | |

| · | Our reliance on third-party contractors and consultants to conduct our exploration and development projects exposes us to risks; | |

| · | A shortage of equipment and supplies and/or the time it takes such items to arrive at our projects could adversely affect our ability to operate our business; | |

| · | Mining development and processing operations pose inherent risks and costs that may negatively impact our business; | |

| · | Failure to adequately manage our growth may seriously harm our business; | |

| · | If we cannot maintain our corporate culture as we grow, we could lose the innovation, teamwork and focus that contribute crucially to our business; |

| 31 |

| · | Our future operating results may fluctuate, which makes our results difficult to predict and could cause our results to fall short of expectations; | |

| · | The requirements of being a public company may strain our resources, divert management’s attention, and affect our ability to attract and retain executive management and qualified board members; | |

| · | Our business and financial results may be adversely affected by various legal and regulatory proceedings; | |

| · | We, our future operations, planned facilities, prospective products and raw materials are subject to environmental, health and safety laws and regulations, and costs to comply with, and liabilities related to, these laws and regulations could adversely affect our business; | |

| · | Environmental regulations could require us to make significant expenditures or expose us to potential liability; | |

| · | We are subject to numerous governmental permits that are difficult to obtain and we may not be able to obtain or renew all of the permits we require, or such permits may not be timely obtained or renewed; | |

| · | An active trading market for our common stock may not develop and you may not be able to resell your shares at or above the price which you paid; and | |

| · | The Company’s stock price may be volatile. |

Risks Related to Our Business and Industry

We are in the early stages of our operations.

We were incorporated on December 4, 2017 and have had limited operations to date. We have not received revenue from our operations since the date of incorporation. As we are in the early stages of our operating history, it is difficult for an investor to make a determination as to the possible success or failure of our business. We are subject to all of the risks associated with a start-up company in the cobalt production business, including the risks set forth herein.

We have a history of operating losses and our management has concluded that factors raise substantial doubt about our ability to continue as a going concern and our auditor has included an explanatory paragraph relating to our ability to continue as a going concern in its audit report for the fiscal years ended December 31, 2022 and 2021.