| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207340-09 | ||

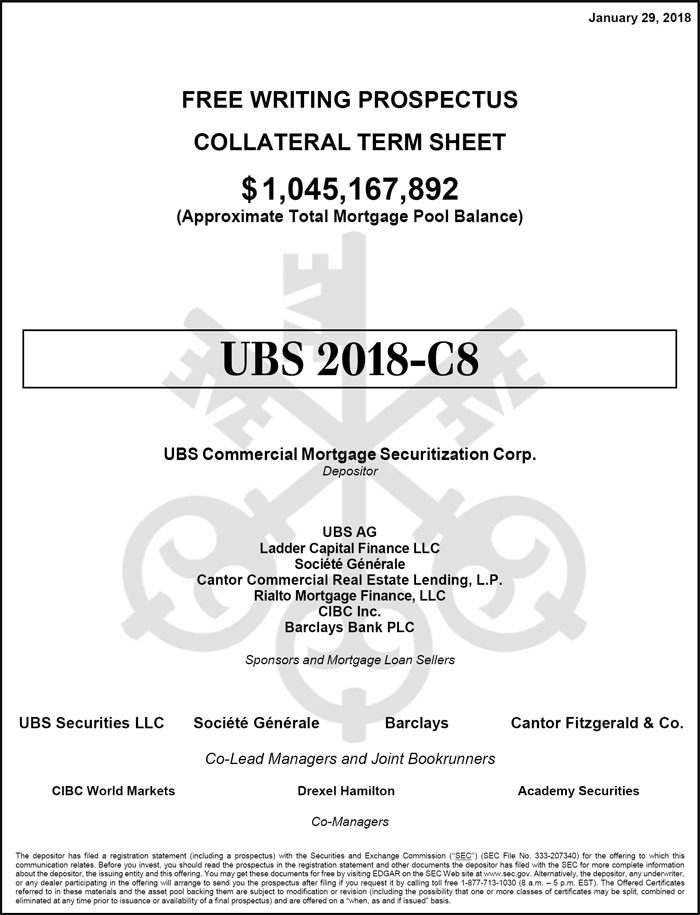

January 29, 2018 FREE WRITING PROSPECTUS COLLATERAL TERM SHEET $ 1,045,167,892 (Approximate Total Mortgage Pool Balance) UBS 2018-C8 UBS Commercial Mortgage Securitization Corp. Depositor UBS AG Ladder Capital Finance LLC Société Générale Cantor Commercial Real Estate Lending, L.P. Rialto Mortgage Finance, LLC CIBC Inc. Barclays Bank PLC Sponsors and Mortgage Loan Sellers UBS Securities LLC Société Générale Barclays Cantor Fitzgerald & Co. Co-Lead Managers and Joint Bookrunners CIBC World Markets Drexel Hamilton Academy Securities Co-Managers The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-207340) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-877-713-1030 (8 a.m. – 5 p.m. EST). The Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale and ultimately by the final prospectus relating to the offered certificates. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward- looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) that have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of the offered certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the offered certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of UBS Securities LLC, SG Americas Securities, LLC, Barclays Capital Inc., Cantor Fitzgerald & Co., CIBC World Markets Corp., Drexel Hamilton, LLC or Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the offered certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The offered certificates described herein are not suitable investments for all investors. In particular, you should not purchase any class of offered certificates unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with such class of certificates. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity and the aggregate amount and timing of distributions on the offered certificates are subject to material variability from period to period and give rise to the potential for significant loss over the life of such certificates. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered certificates involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the certificates. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered certificates described in this free writing prospectus.

This free writing prospectus is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this free writing prospectus may not pertain to any securities that will actually be sold. The information contained in this free writing prospectus may be based on assumptions regarding market conditions and other matters as reflected in this free writing prospectus. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this free writing prospectus should not be relied upon for such purposes. The Underwriters and their respective affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this free writing prospectus may, from time to time, have long or short positions in, and buy or sell, the offered certificates mentioned in this free writing prospectus or derivatives thereof (including options). Information contained in this free writing prospectus is current as of the date appearing on this free writing prospectus only. None of UBS Securities LLC, SG Americas Securities, LLC, Barclays Capital Inc., Cantor Fitzgerald & Co., CIBC World Markets Corp., Drexel Hamilton, LLC or Academy Securities, Inc. provides accounting, tax or legal advice.

2

The issuing entity will be relying upon an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Other Risks Relating to the Certificates—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

3

UBS 2018-C8

Capitalized terms used but not defined herein have the meanings assigned to them in the preliminary prospectus expected to be dated January 31, 2018 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | |

| Co-Lead Managers and Joint Bookrunners: | UBS Securities LLC SG Americas Securities, LLC Barclays Capital Inc. Cantor Fitzgerald & Co. |

| Co-Managers: | CIBC World Markets Corp. Drexel Hamilton, LLC Academy Securities, Inc. |

| Mortgage Loan Sellers: | UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS AG”) (17.8%), Ladder Capital Finance LLC (“LCF”) (23.1%), Société Générale (“SG”) (17.3%), Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (12.9%), Rialto Mortgage Finance, LLC (“RMF”) (10.8%), CIBC Inc. (“CIBC”) (9.4%), and Barclays Bank PLC (“Barclays”) (8.9%) |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Trustee: | Wells Fargo Bank, National Association |

| Certificate Administrator: | Wells Fargo Bank, National Association |

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc. and Moody’s Investors Service, Inc. |

| U.S. Credit Risk Retention: | UBS AG is expected to act as the “retaining sponsor” for this securitization and intends to satisfy the U.S. credit risk retention requirement through the purchase by KKR Real Estate Credit Opportunity Partners AIV Aggregator I L.P., as a third party purchaser (as defined in Regulation RR), from the initial purchasers, on the Closing Date, of an “eligible horizontal residual interest”. The aggregate estimated fair value of the “eligible horizontal residual interest” will equal at least 5% of the estimated fair value of all of the certificates issued by the issuing entity. The pooling and servicing agreement will include the required provisions applicable to an operating advisor necessary for the securitization to comply with the credit risk retention rules utilizing the “third party purchaser” option. See “Operating Advisor” below. For additional information, see “Credit Risk Retention” in the Preliminary Prospectus. |

| EU Credit Risk Retention: | The transaction isnot structured to satisfy the EU risk retention and due diligence requirements. |

| Cut-off Date: | The mortgage loans will be considered part of the trust fund as of their respective cut-off dates. The cut-off date with respect to each mortgage loan is the respective due date for the monthly debt service payment that is due in February 2018 (or, in the case of any mortgage loan that has its first due date after February 2018, the date that would have been its due date in February 2018 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). |

| Closing Date: | On or about February 27, 2018 |

| Clean-up Call: | 1.0% |

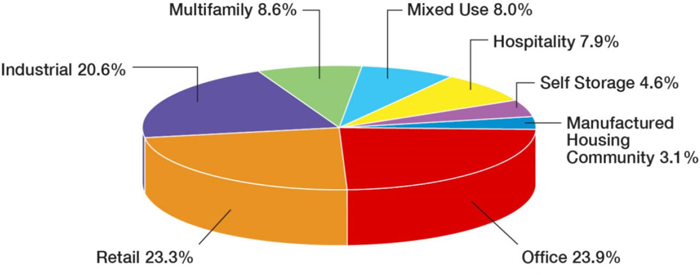

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

UBS 2018-C8

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance(1) |

| Ladder Capital Finance LLC | 18 | 31 | $240,914,103 | 23.1% |

| UBS AG(2) | 13 | 31 | $185,760,271 | 17.8% |

| Société Générale(2) | 7 | 23 | $180,386,589 | 17.3% |

| Cantor Commercial Real Estate Lending, L.P.(2) | 7 | 8 | $134,620,128 | 12.9% |

| Rialto Mortgage Finance | 8 | 8 | $112,425,000 | 10.8% |

| CIBC Inc. | 9 | 10 | $98,083,420 | 9.4% |

| Barclays Bank PLC | 7 | 28 | $92,978,380 | 8.9% |

| Total | 67 | 126 | $1,045,167,892 | 100.0% |

| Pooled Collateral Facts: | |

| Initial Outstanding Pool Balance: | $1,045,167,892 |

| Number of Mortgage Loans: | 67 |

| Number of Mortgaged Properties: | 126 |

| Average Mortgage Loan Cut-off Date Balance: | $15,599,521 |

| Average Mortgaged Property Cut-off Date Balance: | $8,294,983 |

| Weighted Average Mortgage Rate: | 4.724% |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months)(3): | 116 |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months)(3): | 115 |

| Weighted Average Mortgage Loan Seasoning (months): | 1 |

| % of Mortgaged Properties Leased to a Single Tenant: | 23.1% |

| % of Mortgage Loans Secured by a Property or a Portfolio of Mortgaged Properties Leased to a Single Tenant: | 14.3% |

| Credit Statistics | |

| Weighted Average Mortgage Loan U/W NCF DSCR(4): | 1.92x |

| Weighted Average Mortgage Loan Cut-off Date LTV(4)(5): | 59.5% |

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(4)(5): | 55.4% |

| Weighted Average U/W NOI Debt Yield(4): | 10.8% |

| Amortization Overview | |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD(3): | 57.1% |

| % Mortgage Loans with Amortization through Maturity Date or ARD(3): | 23.7% |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD(3): | 19.2% |

| Weighted Average Remaining Amortization Term (months)(6): | 356 |

| Loan Structural Features | |

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 73.4% |

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(7): | 73.3% |

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 62.2% |

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(8): | 83.2% |

| % Mortgage Loans with Upfront Engineering Reserves: | 51.4% |

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 64.0% |

| % Mortgage Loans with In Place Hard Lockboxes: | 50.6% |

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.05x(9): | 88.8% |

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 75.9% |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge Only After a Lockout Period and Prior to an Open Period: | 20.7% |

| % Mortgage Loans with a Period of Prepayment with a Yield Maintenance Charge Followed by a Period of Prepayment with a Yield Maintenance Charge or Defeasance Followed by an Open Period: | 3.5% |

Please see footnotes on the following page.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

UBS 2018-C8

| TRANSACTION HIGHLIGHTS |

| (1) | Unless otherwise indicated, all references to “% of Outstanding Pool Balance” in this Term Sheet reflect a percentage of the aggregate principal balance of the mortgage pool as of the Cut-off Date, after application of all payments of principal due during or prior to February 2018. |

| (2) | The UBS AG and Société Générale allocations each include the AFIN Portfolio mortgage loan (1 loan and 12 properties), and the UBS AG and CCRE allocations each include the Tryad Industrial & Business Center mortgage loan (1 loan and 1 property). |

| (3) | For any mortgage loan with an anticipated repayment date, calculated to or as of, as applicable, that anticipated repayment date. |

| (4) | With respect to any mortgage loan that is part of a whole loan, unless otherwise indicated, LTV, DSCR and Debt Yield calculations in this Term Sheet include any relatedpari passu companion loans and exclude any subordinate companion loans, as applicable. Additionally, LTV, DSCR and Debt Yield figures in this Term Sheet are calculated for mortgage loans without regard to any additional indebtedness that may be incurred at a future date. |

| (5) | With respect to the whole loan secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Park Place at Florham Park, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the alternate market “As-Is” appraised value of $96,000,000 as of December 4, 2017, which assumes that outstanding landlord obligations for free rent, tenant improvements, and leasing commissions are fully funded and escrowed by the lender through a title company. At origination, landlord obligations of $5,044,401 were escrowed. The Cut-off Date LTV and Maturity Date or ARD LTV assuming the “As-Is” appraised value of $91,200,000 for the Park Place at Florham Park Mortgaged Properties are 68.5% and 68.5%, respectively. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as The Village at La Orilla, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the “As-Stabilized” appraised value of $22,050,000 as of January 1, 2018, which assumes certain tenants are in occupancy who have signed leases but have not yet taken their space. At origination, $622,968 was reserved with respect to these tenants. The Cut-off Date LTV and Maturity Date or ARD LTV assuming the “As-Is” appraised value of $21,450,000 as of August 2, 2017 are 71.7% and 58.8%, respectively. For additional information, see “Description of the Mortgage Pool—Mortgage Pool Characteristics – Appraised Value” in the Preliminary Prospectus and the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (6) | Excludes mortgage loans that are interest-only for the full loan term. |

| (7) | Includes FF&E Reserves. |

| (8) | Represents the percent of the allocated aggregate principal balance of the mortgage pool as of the Cut-off Date of retail, office, industrial, and mixed use, and the Yorkshire & Lexington Towers properties only. |

| (9) | The Yorkshire & Lexington Towers Whole Loan has a cash trap trigger that, among other trigger events requires that the debt service coverage ratio for the trailing twelve-month period must not fall below 1.05x and, after the second anniversary of the first payment date, the debt service coverage ratio based on the trailing twelve-month must not fall below 1.10x. If the Yorkshire & Lexington Towers Whole Loan was included in this calculation the % of Mortgage Loans with Cash Traps Triggered at DSCR Levels greater than and equal to 1.05x would be 90.0% of the Initial Pool Balance. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date Balances | |||||||||||

| Weighted Averages | |||||||||||

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | |||

| $896,000 | - | $10,000,000 | 33 | $190,119,922 | 18.2% | 5.050% | 112 | 1.66x | 62.2% | 55.8% | |

| $10,000,001 | - | $15,000,000 | 13 | $166,574,611 | 15.9% | 4.566% | 113 | 1.99x | 57.9% | 52.2% | |

| $15,000,001 | - | $20,000,000 | 5 | $80,633,103 | 7.7% | 4.963% | 120 | 1.64x | 62.9% | 56.7% | |

| $20,000,001 | - | $25,000,000 | 3 | $67,300,000 | 6.4% | 4.475% | 119 | 1.51x | 67.4% | 59.0% | |

| $25,000,001 | - | $30,000,000 | 2 | $53,950,000 | 5.2% | 4.503% | 88 | 2.19x | 62.5% | 62.5% | |

| $30,000,001 | - | $35,000,000 | 4 | $133,650,000 | 12.8% | 4.430% | 118 | 2.54x | 56.2% | 56.2% | |

| $35,000,001 | - | $45,000,000 | 2 | $90,000,000 | 8.6% | 4.905% | 120 | 1.78x | 57.4% | 57.4% | |

| $45,000,001 | - | $50,000,000 | 3 | $146,500,000 | 14.0% | 4.804% | 120 | 1.98x | 59.5% | 56.1% | |

| $50,000,001 | - | $60,000,000 | 2 | $116,440,256 | 11.1% | 4.593% | 119 | 1.89x | 54.6% | 50.1% | |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | |||

| Distribution of Mortgage Rates | ||||||||||

| Weighted Averages | ||||||||||

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | ||

| 2.7400% | - | 4.0000% | 1 | $15,000,000 | 1.4% | 2.740% | 56 | 4.28x | 22.5% | 22.5% |

| 4.0001% | - | 4.2500% | 3 | $97,400,000 | 9.3% | 4.141% | 119 | 2.50x | 54.5% | 54.5% |

| 4.2501% | - | 4.5000% | 7 | $133,900,000 | 12.8% | 4.390% | 107 | 2.21x | 60.5% | 56.2% |

| 4.5001% | - | 4.7500% | 16 | $359,612,500 | 34.4% | 4.639% | 119 | 1.98x | 59.0% | 57.5% |

| 4.7501% | - | 5.0000% | 18 | $155,328,844 | 14.9% | 4.884% | 119 | 1.71x | 63.1% | 56.1% |

| 5.0001% | - | 5.2500% | 16 | $240,536,073 | 23.0% | 5.105% | 119 | 1.52x | 61.1% | 53.9% |

| 5.2501% | - | 5.5000% | 2 | $12,740,475 | 1.2% | 5.320% | 119 | 1.27x | 72.1% | 60.7% |

| 5.5001% | - | 6.1600% | 4 | $30,650,000 | 2.9% | 5.948% | 75 | 1.53x | 59.4% | 53.3% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | ||

| Property Type Distribution(1) | |||||||||||

| Weighted Averages | |||||||||||

| Property Type | Number of Mortgage Properties | Aggregate Cut-Off Date Balance | % of Initial Outstanding Pool Balance(1) | Number of Units/Rooms/Pads/ NRA/Beds | Cut-off Date Balance per Unit/Room/Pads NRA(1)(2) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | Occupancy | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) |

| Office | 15 | $249,950,000 | 23.9% | 2,878,585 | $151 | 4.759% | 120 | 94.7% | 1.86x | 63.0% | 59.5% |

| Suburban | 11 | $206,000,000 | 19.7% | 2,618,684 | $135 | 4.731% | 120 | 95.5% | 1.95x | 62.8% | 60.5% |

| Medical | 3 | $31,200,000 | 3.0% | 121,880 | $280 | 4.892% | 119 | 93.7% | 1.53x | 61.1% | 55.2% |

| CBD | 1 | $12,750,000 | 1.2% | 138,021 | $92 | 4.885% | 119 | 83.1% | 1.32x | 69.7% | 53.4% |

| Retail | 49 | $243,124,044 | 23.3% | 3,849,338 | $141 | 4.570% | 119 | 96.8% | 2.00x | 62.0% | 58.3% |

| Anchored | 20 | $171,923,773 | 16.4% | 3,354,028 | $123 | 4.527% | 119 | 95.5% | 2.06x | 61.6% | 58.9% |

| Free-Standing | 23 | $47,209,796 | 4.5% | 399,939 | $119 | 4.465% | 119 | 100.0% | 2.08x | 59.7% | 55.9% |

| Shadow Anchored | 4 | $16,983,709 | 1.6% | 56,671 | $335 | 5.039% | 119 | 100.0% | 1.39x | 66.8% | 56.8% |

| Unanchored | 2 | $7,006,765 | 0.7% | 38,700 | $253 | 5.190% | 120 | 100.0% | 1.42x | 74.1% | 61.3% |

| Industrial | 25 | $215,791,708 | 20.6% | 8,985,497 | $46 | 4.760% | 112 | 90.4% | 1.88x | 56.6% | 50.5% |

| Warehouse/Distribution | 21 | $139,244,652 | 13.3% | 5,348,752 | $51 | 4.718% | 108 | 98.1% | 1.94x | 58.8% | 53.2% |

| Flex | 1 | $56,440,256 | 5.4% | 3,353,230 | $33 | 5.021% | 119 | 68.1% | 1.42x | 52.6% | 43.3% |

| Flex/R&D | 1 | $13,341,000 | 1.3% | 127,105 | $52 | 4.320% | 120 | 100.0% | 2.76x | 52.3% | 52.3% |

| Light Industrial | 1 | $4,098,300 | 0.4% | 58,546 | $52 | 4.320% | 120 | 100.0% | 2.76x | 52.3% | 52.3% |

| Manufacturing | 1 | $2,667,500 | 0.3% | 97,864 | $52 | 4.320% | 120 | 100.0% | 2.76x | 52.3% | 52.3% |

| Multifamily | 13 | $90,100,000 | 8.6% | 1,955 | $123,024 | 4.511% | 103 | 96.5% | 2.13x | 54.0% | 51.6% |

| Garden | 9 | $38,287,500 | 3.7% | 780 | $68,630 | 5.012% | 109 | 95.5% | 1.51x | 61.5% | 55.9% |

| Student Housing | 1 | $34,500,000 | 3.3% | 342 | $100,877 | 4.690% | 115 | 99.7% | 1.95x | 58.8% | 58.8% |

| High Rise | 2 | $15,000,000 | 1.4% | 827 | $241,838 | 2.740% | 56 | 92.0% | 4.28x | 22.5% | 22.5% |

| Mid Rise | 1 | $2,312,500 | 0.2% | 6 | $583,333 | 5.023% | 119 | 95.1% | 1.35x | 62.5% | 62.5% |

| Mixed Use | 7 | $83,725,522 | 8.0% | 508,199 | $32,924 | 4.773% | 120 | 91.4% | 1.71x | 54.3% | 51.7% |

| Office/Garage/Retail | 1 | $45,000,000 | 4.3% | 246,136 | $366 | 4.728% | 120 | 94.2% | 1.76x | 49.7% | 49.7% |

| Retail/Office | 2 | $22,988,022 | 2.2% | 143,333 | $183 | 4.803% | 118 | 84.8% | 1.71x | 58.6% | 53.1% |

| Medical/Office/Retail | 1 | $6,550,000 | 0.6% | 33,056 | $198 | 4.805% | 120 | 92.0% | 1.69x | 61.5% | 55.4% |

| Multifamily/Retail | 2 | $4,687,500 | 0.4% | 6 | $583,333 | 5.023% | 119 | 95.1% | 1.35x | 62.5% | 62.5% |

| Office/Retail | 1 | $4,500,000 | 0.4% | 85,668 | $53 | 4.768% | 120 | 91.6% | 1.60x | 58.4% | 47.7% |

| Hospitality | 9 | $82,392,296 | 7.9% | 886 | $141,303 | 5.011% | 114 | 79.0% | 2.19x | 62.4% | 55.6% |

| Limited Service | 6 | $41,892,296 | 4.0% | 470 | $122,963 | 5.139% | 119 | 72.9% | 1.91x | 65.9% | 53.5% |

| Extended Stay | 3 | $40,500,000 | 3.9% | 416 | $160,273 | 4.879% | 109 | 85.3% | 2.49x | 58.7% | 57.8% |

| Self Storage | 6 | $47,584,320 | 4.6% | 662,596 | $79 | 4.787% | 119 | 87.9% | 1.97x | 53.6% | 52.7% |

| Manufactured Housing Community | 2 | $32,500,000 | 3.1% | 578 | $61,215 | 5.007% | 103 | 93.6% | 1.26x | 64.6% | 59.8% |

| Total/Weighted Average | 126 | $1,045,167,892 | 100.0% | 4.724% | 115 | 92.6% | 1.92x | 59.5% | 55.4% | ||

Please see footnotes on page 10.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Geographic Distribution(1) | ||||||||

| Weighted Averages | ||||||||

| State/Location | Number of Mortgage Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) |

| California | 10 | $162,300,000 | 15.5% | 4.811% | 116 | 1.87x | 55.1% | 53.9% |

| California - Southern(4) | 6 | $98,800,000 | 9.5% | 4.895% | 114 | 1.91x | 57.7% | 55.7% |

| California - Northern(4) | 4 | $63,500,000 | 6.1% | 4.680% | 120 | 1.81x | 51.0% | 51.0% |

| Texas | 7 | $136,442,813 | 13.1% | 4.826% | 117 | 1.80x | 59.9% | 54.4% |

| New York | 15 | $92,564,319 | 8.9% | 4.565% | 109 | 1.96x | 50.3% | 43.9% |

| Indiana | 5 | $60,350,000 | 5.8% | 4.833% | 117 | 1.73x | 62.3% | 57.7% |

| Massachusetts | 2 | $59,327,500 | 5.7% | 4.692% | 111 | 2.27x | 60.7% | 60.7% |

| Other | 87 | $534,183,258 | 51.1% | 4.690% | 116 | 1.94x | 61.9% | 57.3% |

| Total/Weighted Average | 126 | 1,045,167,890 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% |

| Distribution of Cut-off Date LTV Ratios(1)(2)(3) | ||||||||||

| Weighted Averages | ||||||||||

| Range of Cut-off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | ||

| 22.5% | - | 35.0% | 2 | $19,000,000 | 1.8% | 3.010% | 69 | 3.87x | 25.0% | 25.0% |

| 35.1% | - | 45.0% | 1 | $6,000,000 | 0.6% | 4.374% | 120 | 3.42x | 39.3% | 39.3% |

| 45.1% | - | 55.0% | 11 | $234,474,576 | 22.4% | 4.728% | 116 | 1.95x | 52.0% | 49.0% |

| 55.1% | - | 60.0% | 13 | $284,642,750 | 27.2% | 4.652% | 119 | 2.04x | 58.2% | 55.6% |

| 60.1% | - | 65.0% | 19 | $283,368,671 | 27.1% | 4.767% | 112 | 1.93x | 62.1% | 58.6% |

| 65.1% | - | 70.0% | 12 | $140,963,250 | 13.5% | 4.974% | 119 | 1.54x | 67.5% | 59.9% |

| 70.1% | - | 75.0% | 9 | $76,718,645 | 7.3% | 4.808% | 119 | 1.47x | 73.2% | 63.3% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | ||

| Distribution of Maturity Date or ARD LTV Ratios(1)(2)(3) | ||||||||||

| Weighted Averages | ||||||||||

| Range of LTV Ratios at Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | ||

| 22.5% | - | 45.0% | 6 | $97,274,576 | 9.3% | 4.548% | 109 | 2.06x | 46.1% | 39.6% |

| 45.1% | - | 55.0% | 20 | $316,318,671 | 30.3% | 4.769% | 117 | 1.89x | 56.4% | 51.0% |

| 55.1% | - | 60.0% | 19 | $340,203,170 | 32.6% | 4.673% | 119 | 1.92x | 61.3% | 57.9% |

| 60.1% | - | 65.0% | 16 | $224,090,475 | 21.4% | 4.730% | 110 | 1.98x | 64.6% | 61.8% |

| 65.1% | - | 70.0% | 6 | $67,281,000 | 6.4% | 5.002% | 120 | 1.68x | 67.6% | 65.7% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | ||

| Distribution of Underwritten NCF Debt Service Coverage Ratios(1)(2) | |||||||||||

| Weighted Averages | |||||||||||

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | |||

| 1.25x | - | 1.35x | 8 | $90,565,475 | 8.7% | 5.055% | 113 | 1.28x | 66.6% | 58.8% | |

| 1.36x | - | 1.45x | 8 | $169,673,349 | 16.2% | 5.053% | 119 | 1.41x | 59.9% | 50.3% | |

| 1.46x | - | 1.55x | 7 | $52,575,522 | 5.0% | 4.812% | 118 | 1.51x | 65.8% | 56.9% | |

| 1.56x | - | 1.65x | 8 | $67,944,060 | 6.5% | 4.908% | 114 | 1.59x | 62.6% | 53.9% | |

| 1.66x | - | 1.75x | 9 | $82,268,500 | 7.9% | 4.599% | 120 | 1.70x | 59.6% | 53.4% | |

| 1.76x | - | 1.85x | 4 | $110,500,000 | 10.6% | 4.971% | 116 | 1.79x | 56.9% | 56.6% | |

| 1.86x | - | 1.95x | 8 | $108,111,647 | 10.3% | 4.723% | 118 | 1.91x | 60.7% | 59.0% | |

| 1.96x | - | 2.05x | 2 | $11,092,750 | 1.1% | 4.524% | 119 | 2.01x | 59.1% | 59.1% | |

| 2.06x | - | 2.30x | 3 | $109,886,589 | 10.5% | 4.667% | 120 | 2.26x | 60.6% | 59.3% | |

| 2.31x | - | 2.55x | 4 | $108,900,000 | 10.4% | 4.367% | 104 | 2.40x | 58.3% | 58.3% | |

| 2.56x | - | 4.28x | 6 | $133,650,000 | 12.8% | 4.180% | 113 | 2.93x | 51.5% | 51.5% | |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | |||

Please see footnotes on page 10.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Original Terms to Maturity or ARD | ||||||||

| Weighted Averages | ||||||||

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) |

| 60 | 5 | $66,350,000 | 6.3% | 4.623% | 59 | 2.55x | 52.1% | 51.2% |

| 120 | 62 | $978,817,892 | 93.7% | 4.731% | 119 | 1.88x | 60.0% | 55.7% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% |

| Distribution of Remaining Terms to Maturity or ARD | ||||||||||

| Weighted Averages | ||||||||||

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | ||

| 56 | - | 118 | 13 | $158,224,990 | 15.1% | 4.722% | 92 | 2.04x | 57.0% | 54.5% |

| 119 | - | 120 | 54 | $886,942,901 | 84.9% | 4.724% | 120 | 1.90x | 60.0% | 55.6% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | ||

| Distribution of Underwritten NOI Debt Yields(1)(2)(3) | ||||||||||

| Weighted Averages | ||||||||||

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) | ||

| 7.0% | - | 8.5% | 6 | $69,475,000 | 6.6% | 4.915% | 111 | 1.39x | 62.4% | 59.1% |

| 8.6% | - | 9.0% | 9 | $112,192,077 | 10.7% | 4.921% | 120 | 1.54x | 59.6% | 55.1% |

| 9.1% | - | 9.5% | 6 | $52,246,820 | 5.0% | 4.675% | 118 | 1.75x | 60.0% | 56.8% |

| 9.6% | - | 10.0% | 11 | $124,142,750 | 11.9% | 4.788% | 118 | 1.72x | 61.3% | 56.8% |

| 10.1% | - | 10.5% | 7 | $123,480,926 | 11.8% | 4.822% | 119 | 1.53x | 58.6% | 51.0% |

| 10.6% | - | 11.0% | 4 | $109,688,022 | 10.5% | 5.102% | 120 | 1.60x | 62.3% | 56.1% |

| 11.1% | - | 11.5% | 6 | $145,094,060 | 13.9% | 4.410% | 119 | 2.14x | 61.1% | 58.5% |

| 11.6% | - | 12.0% | 2 | $65,000,000 | 6.2% | 4.274% | 105 | 2.71x | 51.3% | 51.3% |

| 12.1% | - | 12.5% | 6 | $128,900,000 | 12.3% | 4.386% | 104 | 2.51x | 56.7% | 55.3% |

| 12.6% | - | 16.2% | 10 | $114,948,236 | 11.0% | 4.931% | 116 | 2.26x | 59.5% | 54.2% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% | ||

| Amortization Types | ||||||||

| Weighted Averages | ||||||||

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) |

| Full IO | 28 | $593,792,750 | 56.8% | 4.569% | 114 | 2.24x | 56.9% | 56.9% |

| Amortizing | 19 | $248,144,142 | 23.7% | 5.080% | 116 | 1.54x | 60.8% | 50.2% |

| Partial IO | 17 | $200,462,500 | 19.2% | 4.733% | 119 | 1.46x | 65.4% | 57.3% |

| Full IO, ARD | 3 | $2,768,500 | 0.3% | 5.200% | 120 | 1.69x | 70.0% | 70.0% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% |

| Loan Purposes | ||||||||

| Weighted Averages | ||||||||

| Loan Purpose | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | Mortgage Rate | Stated Remaining Term (Mos.)(6) | U/W NCF DSCR(1)(2) | Cut-off Date LTV Ratio(1)(2)(3) | Maturity Date or ARD LTV Ratio(1)(2)(3) |

| Refinance | 36 | $515,571,417 | 49.3% | 4.813% | 115 | 1.80x | 58.8% | 54.0% |

| Acquisition | 29 | $420,596,475 | 40.2% | 4.642% | 116 | 2.07x | 61.0% | 57.9% |

| Recapitalization(5) | 2 | $109,000,000 | 10.4% | 4.618% | 119 | 1.94x | 57.3% | 52.8% |

| Total/Weighted Average | 67 | $1,045,167,892 | 100.0% | 4.724% | 115 | 1.92x | 59.5% | 55.4% |

Please see footnotes on page 10.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| (1) | All numerical information concerning the mortgage loans is approximate and, in the case of mortgage loans secured by multiple properties, is based on allocated loan amounts with respect to such properties. All weighted average information regarding the mortgage loans reflects the weighting of the mortgage loans based on their outstanding principal balances as of the Cut-off Date or, in the case of mortgage loans secured by multiple properties, allocated loan amounts. The sum of numbers and percentages in columns may not match the “Total” due to rounding. |

| (2) | With respect to any mortgage loan that is part of a whole loan, unless otherwise indicated, Balance per Unit/Room/Pad/NRA, LTV, DSCR and Debt Yield calculations in this Term Sheet include any relatedpari passu companion loans and exclude any subordinate companion loans, as applicable. Additionally, Balance per Unit/Room/Pad/NRA, LTV, DSCR and Debt Yield figures in this Term Sheet are calculated for mortgage loans without regard to any additional indebtedness that may be incurred at a future date. |

| (3) | With respect to the whole loan secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Park Place at Florham Park, the Cut-off Date LTV Ratio, Maturity Date or ARD LTV Ratio, and appraised value are based on the alternate market “As-Is” appraised value of $96,000,000 as of December 4, 2017, which assumes that outstanding landlord obligations for free rent, tenant improvements, and leasing commissions are fully funded and escrowed by the lender through a title company. At origination, landlord obligations of $5,044,401 were escrowed. The Cut-off Date LTV Ratio and Maturity Date or ARD LTV Ratio assuming the “As-Is” appraised value of $91,200,000 for the Park Place at Florham Park Mortgaged Properties are 68.5% and 68.5%, respectively. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as The Village at La Orilla, the Cut-off Date LTV Ratio, Maturity Date or ARD LTV Ratio, and appraised value are based on the "As-Stabilized" appraised value of $22,050,000 as of January 1, 2018, which assumes certain tenants are in occupancy who have signed leases but have not yet taken their space. At origination, $622,968 was reserved with respect to these tenants. The Cut-off Date LTV Ratio and Maturity Date or ARD LTV Ratio assuming the “As-Is” appraised value of $21,450,000 as of August 2, 2017 are 71.7% and 58.8%, respectively. For additional information, see “Description of the Mortgage Pool—Mortgage Pool Characteristics – Appraised Value” in the Preliminary Prospectus and the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (4) | “California—Northern” includes zip codes above 93600, and “California—Southern” includes zip codes at or below 93600. |

| (5) | With respect to the whole loan secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as AFIN Portfolio, loan proceeds were used to refinance existing debt of approximately $18.0 million encumbering the San Pedro Crossing Mortgaged Property and recapitalize the borrower sponsors recent acquisition of the remaining 11 AFIN Portfolio Mortgaged Properties. With respect to the mortgage loan secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as AFIN Industrial and Retail Net-Leased Portfolio, loan proceeds were used to recapitalize the borrower sponsor after the purchase the AFIN Industrial and Retail Net-Leased Portfolio Mortgaged Properties between March 31, 2017 and November 7, 2017. |

| (6) | With respect to an ARD loan, refers to the term through the related anticipated repayment date. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Ten Largest Mortgage Loans | |||||||||

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Cut-off Date Balance | % of Initial Outstanding Pool Balance | Cut-off Date Balance per Unit/Room/ Pad/NRA(1) | Cut-off Date LTV Ratio(1) | U/W NCF DSCR(1) | U/W NOI Debt Yield(1) |

| AFIN Portfolio | SG; UBS AG | Various | Retail | $60,000,000 | 5.7% | $87 | 56.5% | 2.34x | 11.1% |

| Tryad Industrial & Business Center | CCRE; UBS AG | Rochester, NY | Industrial | $56,440,256 | 5.4% | $33 | 52.6% | 1.42x | 10.5% |

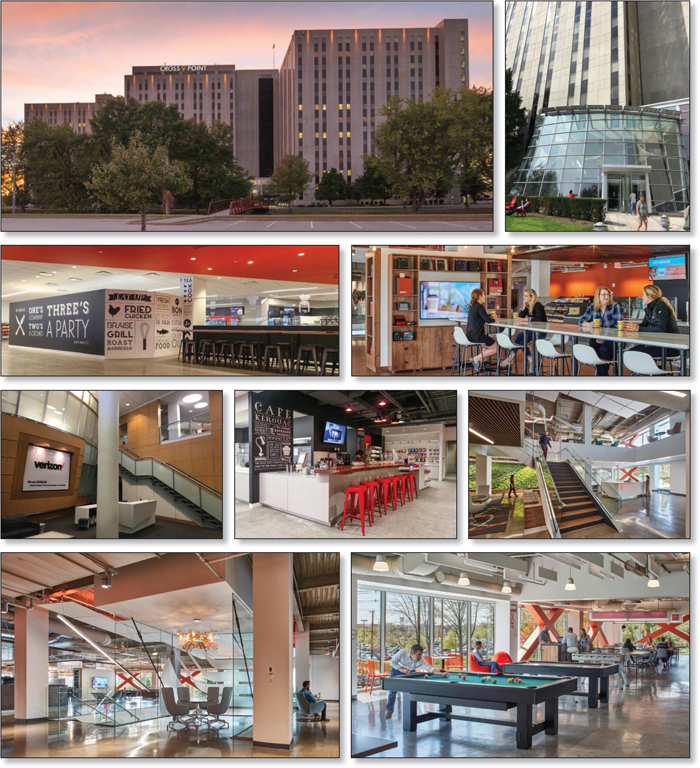

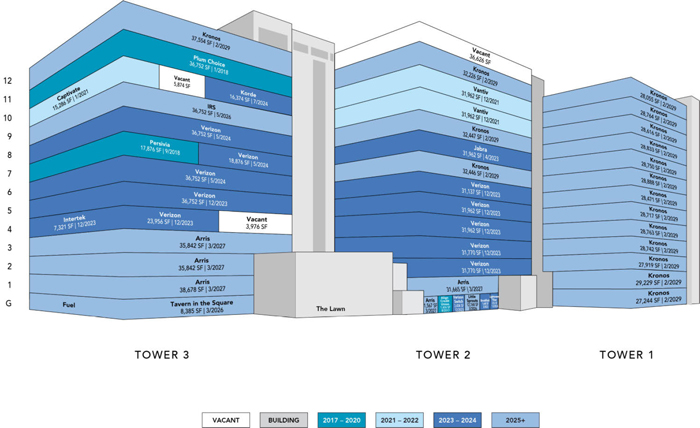

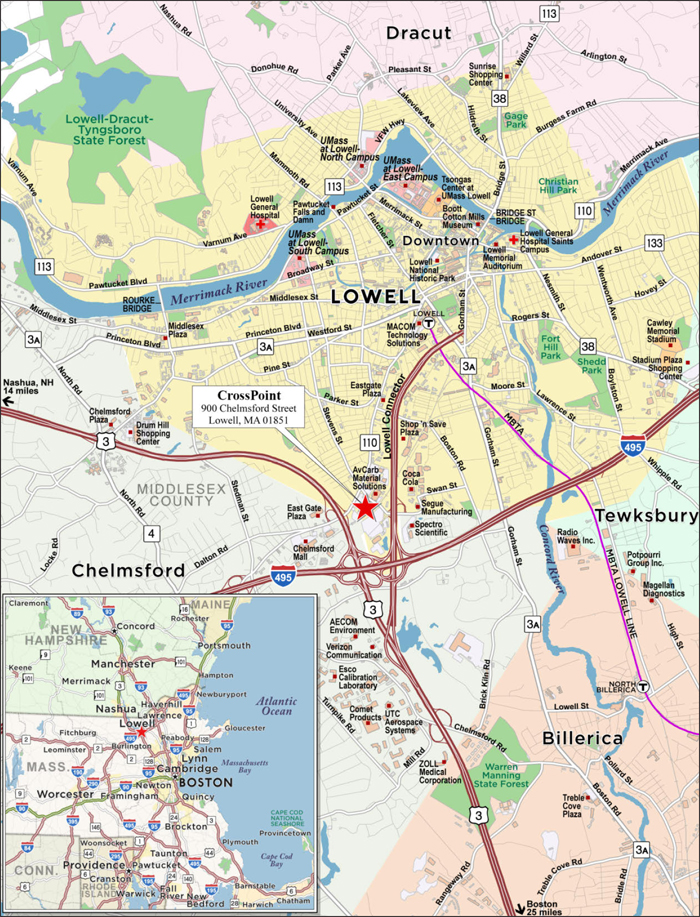

| CrossPoint | CCRE | Lowell, MA | Office | $50,000,000 | 4.8% | $114 | 60.0% | 2.24x | 11.8% |

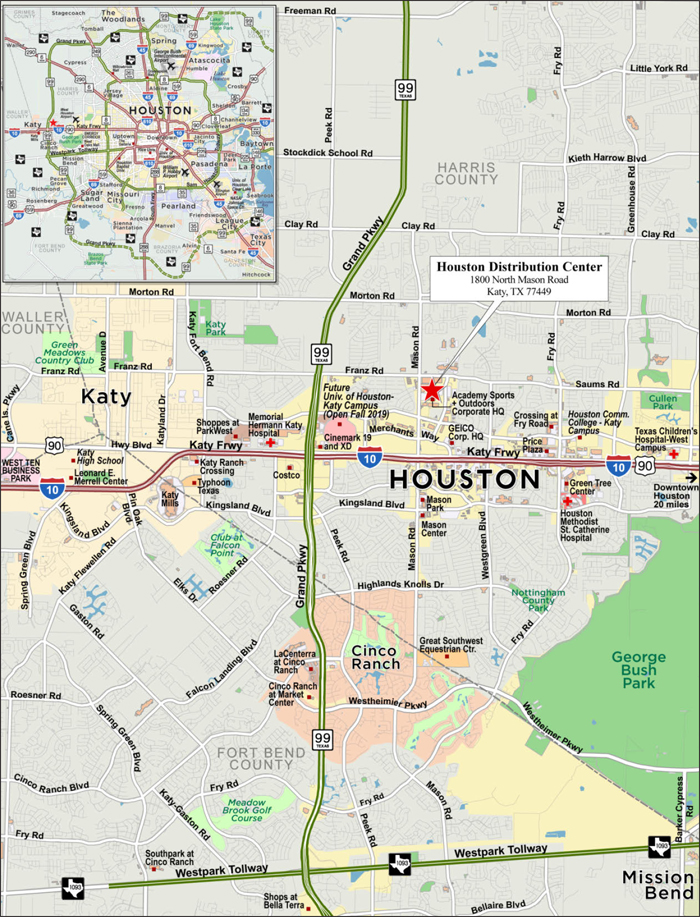

| Houston Distribution Center | SG | Katy, TX | Industrial | $49,000,000 | 4.7% | $56 | 58.3% | 1.44x | 10.6% |

| Moore Plaza | RMF | Corpus Christi, TX | Retail | $47,500,000 | 4.5% | $126 | 60.2% | 2.27x | 11.4% |

| Park Place at Florham Park(2) | UBS AG | Florham Park, NJ | Office | $45,000,000 | 4.3% | $176 | 65.1% | 1.80x | 10.6% |

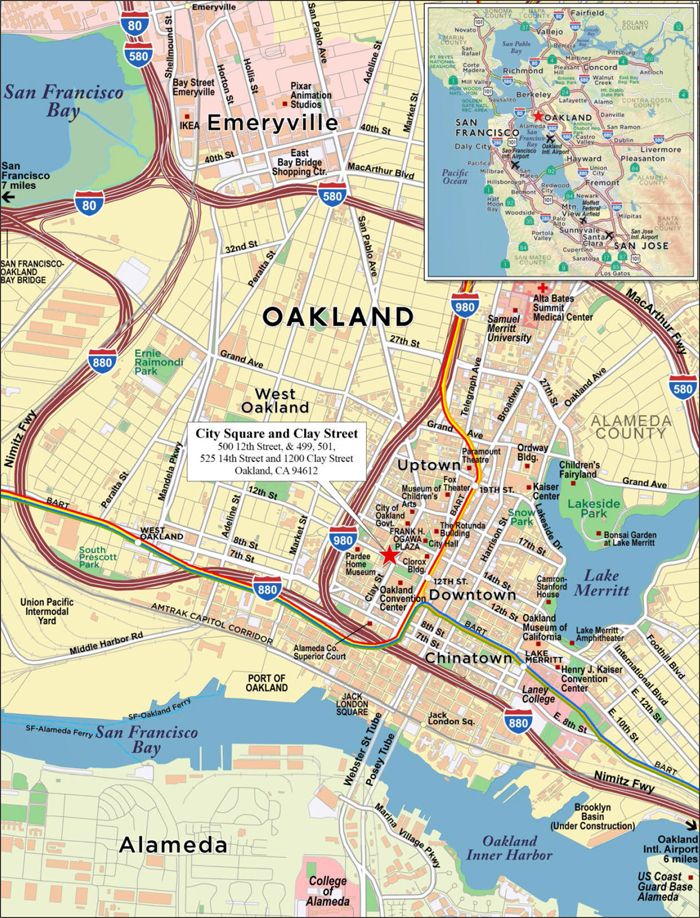

| City Square and Clay Street | LCF | Oakland, CA | Mixed Use | $45,000,000 | 4.3% | $366 | 49.7% | 1.76x | 8.9% |

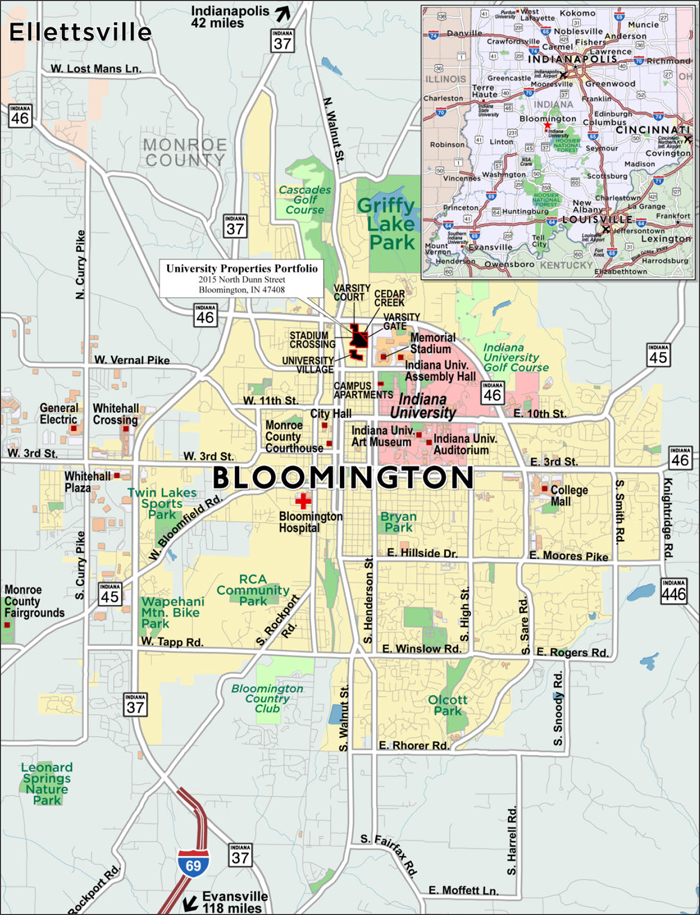

| University Properties Portfolio | CIBC | Bloomington, IN | Multifamily | $34,500,000 | 3.3% | $100,877 | 58.8% | 1.95x | 9.6% |

| AFIN Industrial and Retail Net-Leased Portfolio | Barclays Bank PLC | Various | Various | $33,400,000 | 3.2% | $73 | 53.4% | 2.81x | 12.4% |

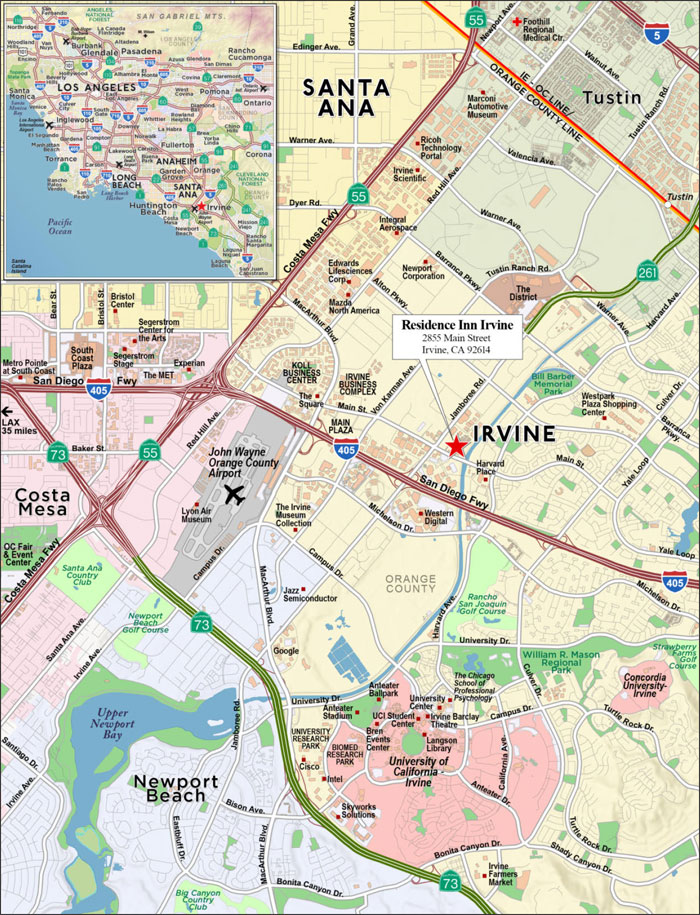

| Residence Inn Irvine | SG | Irvine, CA | Hospitality | $33,000,000 | 3.2% | $189,655 | 60.0% | 2.65x | 14.0% |

| Total/Weighted Average | $453,840,256 | 43.4% | 57.4% | 2.03x | 11.0% | ||||

| (1) | With respect to any mortgage loan that is part of a whole loan, unless otherwise indicated, all LTV Ratio, U/W NCF DSCR, Debt Yield and Balance per Unit/Room/Pad/NRA calculations in this Term Sheet include any relatedpari passu companion loans and exclude any subordinate companion loans, as applicable. Additionally, LTV Ratio, U/W NCF DSCR, Debt Yield and Balance per Unit/Room/Pad/NRA figures in this Term Sheet are calculated for mortgage loans without regard to any additional indebtedness that may be incurred at a future date. |

| (2) | With respect to the whole loan secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Park Place at Florham Park, the Cut-off Date LTV Ratio and appraised value are based on the alternate market “As-Is” appraised value of $96,000,000 as of December 4, 2017, which assumes that outstanding landlord obligations for free rent, tenant improvements, and leasing commissions are fully funded and escrowed by the lender through a title company. At origination, landlord obligations of $5,044,401 were escrowed. The Cut-off Date LTV Ratio assuming the “As-Is” appraised value of $91,200,000 for the Park Place at Florham Park Mortgaged Properties is 68.5%. |

| Existing Mezzanine Debt Summary | ||||||||

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR(1) | Total Debt U/W NCF DSCR(2) | Trust Cut-off Date LTV Ratio(1) | Total Debt Cut-off Date LTV Ratio(2) | Trust U/W NOI Debt Yield(1) | Total Debt U/W NOI Debt Yield(2) |

| Tryad Industrial & Business Center | $56,440,256 | $19,500,000 | 1.42x | 1.09x | 52.6% | 61.8% | 10.5% | 8.9% |

| Park Place at Florham Park | $45,000,000 | $12,500,000 | 1.80x | 1.18x | 65.1% | 78.1% | 10.6% | 8.8% |

| University Properties Portfolio | $34,500,000 | $5,000,000 | 1.95x | 1.43x | 58.8% | 67.3% | 9.6% | 8.3% |

| Yorkshire & Lexington Towers | $15,000,000 | $150,000,000 | 4.28x | 1.04x | 22.5% | 61.8% | 12.0% | 4.4% |

| (1) | With respect to any mortgage loan that is part of a whole loan, the Trust U/W NCF DSCR, Trust Cut-off Date LTV Ratio and Trust U/W NOI Debt Yield include the relatedpari passucompanion loan(s) and exclude any related subordinate companion loan(s) and the related mezzanine loan(s). |

| (2) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV Ratio and Total Debt U/W NOI Debt Yield calculations include any relatedpari passu companion loan(s), related subordinate companion loan(s) and/or related mezzanine loan(s). |

| Subordinate Debt Summary | |||||||||

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Pari Passu Companion Loan(s) Cut-off Date Balance | Subordinate Debt Cut-off Date Balance | Trust U/W NCF DSCR | Total Mortgage Debt U/W NCF DSCR(1) | Trust Cut-off Date LTV Ratio | Total Mortgage Debt Cut-off Date LTV Ratio(1) | Trust U/W NOI Debt Yield | Total Mortgage Debt U/W NOI Debt Yield(1) |

| Yorkshire & Lexington Towers | $15,000,000 | $185,000,000 | $200,000,000 | 4.28x | 1.68x | 22.5% | 44.9% | 12.0% | 6.0% |

| (1) | Total Mortgage Debt U/W NCF DSCR, Total Mortgage Debt Cut-off Date LTV, Total Mortgage Debt U/W NOI Debt Yield calculations include any relatedpari passu companion loan(s), relate subordinate companion loan(s) and excludes related mezzanine loan(s), if any. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Pari Passu Companion Loan Summary | ||||||

| Mortgage Loan | Note(s) | Original Balance | Holder of Note(1) | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| AFIN Portfolio | A-1, A-5, A-10, A-15 | $60,000,000 | UBS 2018-C8(2) | No | Wells Fargo Bank, National Association(2) | KeyBank Real Estate Capital(2) |

| A-3, A-4, A-9, A-14 | $60,000,000 | UBS 2017-C7 | No | |||

| A-2, A-6, A-7, A-8 (controlling) | $45,000,000 | Société Générale | Yes | |||

| A-11, A-12, A-13, A-16 | $25,000,000 | UBS AG | No | |||

| Tryad Industrial & Business Center | A-1-2 (controlling), A-1-3, A-1-4, A-2-2, A-2-3, A-2-4 | $56,500,000 | UBS 2018-C8 | Yes | Midland Loan Services | Midland Loan Services |

| A-1-1, A-2-1 | $54,000,000 | UBS 2017-C7 | No | |||

| CrossPoint | A-2, A-3, A-9 | $50,000,000 | UBS 2018-C8(3) | No | Midland Loan Services(3) | Midland Loan Services(3) |

| A-1 (controlling), A-4, A-7, A-8, A-10 | $75,000,000 | CCRE | Yes | |||

| A-5, A-6 | $25,000,000 | Starwood Mortgage Capital LLC | No | |||

| Houston Distribution Center | A-1 (controlling), A-2 | $49,000,000 | UBS 2018-C8 | Yes | Midland Loan Services | Midland Loan Services |

| A-3 | $35,000,000 | Barclays Bank, PLC | No | |||

| Park Place at Florham Park | A-1 (controlling), A-2, A-5 | $45,000,000 | UBS 2018-C8 | Yes | Midland Loan Services | Midland Loan Services |

| A-3, A-4 | $17,500,000 | UBS AG | No | |||

| City Square and Clay Street | A-2, A-4 | $45,000,000 | UBS 2018-C8(4) | No | Midland Loan Services(4) | Midland Loan Services(4) |

| A-1 (controlling) | $30,000,000 | LCF or an affiliate | Yes | |||

| A-3 | $15,000,000 | LCF or an affiliate | No | |||

| BlueLinx Portfolio | A-3, A-4 | $28,600,000 | UBS 2018-C8 | No | (5) | (5) |

| A-1 (controlling), A-2 | $42,900,000 | (5) | Yes | |||

| Yorkshire & Lexington Towers | A-7, A-8-2 | $15,000,000 | UBS 2018-C8 | No | KeyBank Real Estate Capital | CWCapital Asset Management LLC |

| A-1 (controlling)(6), A-2 | $60,000,000 | CSAIL 2017-CX10 | Yes | |||

| A-4 | $40,000,000 | UBS 2017-C5 | No | |||

| A-5 | $40,000,000 | UBS 2017-C6 | No | |||

| A-6, A-8-1 | $25,000,000 | CCUBS 2017-C1 | No | |||

| A-3 | $20,000,000 | Natixis | No | |||

| (1) | Identifies the expected holder as of the Closing Date. |

| (2) | The AFIN Portfolio Whole Loan is currently serviced under the UBS 2017-C7 pooling and servicing agreement until the securitization of the related controllingpari passu Note A-8 (the date thereof, the “AFIN Portfolio Servicing Shift Securitization Date”), after which the AFIN Portfolio Whole Loan will be serviced under the pooling and servicing agreement related to the securitization of the related controllingpari passu Note A-8 (the “AFIN Portfolio Servicing Shift PSA”). The master servicer and the special servicer under the AFIN Portfolio Servicing Shift PSA will be identified in a notice, report or statement to holders of the UBS 2018-C8 certificates after the securitization of the related controllingpari passu Note A-8. |

| (3) | The CrossPoint Whole Loan is expected to initially be serviced under the UBS 2018-C8 pooling and servicing agreement until the securitization of the related controllingpari passuNote A-1 (the date thereof, the “CrossPoint Servicing Shift Securitization Date”), after which the CrossPoint Whole Loan will be serviced under the pooling and servicing agreement related to the securitization of the related controllingpari passu Note A-1 (the “CrossPoint Servicing Shift PSA”). The master servicer and the special servicer under the CrossPoint Servicing Shift PSA will be identified in a notice, report or statement to holders of the UBS 2018-C8 certificates after the securitization of the related controlling pari passu Note A-1. |

| (4) | The City Square and Clay Street Whole Loan is expected to initially be serviced under the UBS 2018-C8 pooling and servicing agreement until the securitization of the related controllingpari passu Note A-1 (the date thereof, the “City Square and Clay Street Servicing Shift Securitization Date”), after which the City Square and Clay Street Whole Loan will be serviced under the pooling and servicing agreement related to the securitization of the related controllingpari passu Note A-1 (the “City Square and Clay Street Servicing Shift PSA”). The master servicer and the special servicer under the City Square and Clay Street Servicing Shift PSA will be identified in a notice, report or statement to holders of the UBS 2018-C8 certificates after the securitization of the related controlling pari passu Note A-1. |

| (5) | The BlueLinx Portfolio Whole Loan is expected to be serviced by the related master servicer and special servicer pursuant to the pooling and servicing agreement governing the public conduit securitization in which the controlling Note A-1 will be deposited. |

| (6) | The related whole loan will be serviced pursuant to the indicated pooling and servicing agreement or trust and servicing agreement, as applicable. However, so long as no “control appraisal period” (or similar term) has occurred and is continuing, the holder of the related subordinate companion loan will be the controlling noteholder and will have the right to approve certain modifications and consent to certain actions taken with respect to the related whole loan. If a control appraisal period has occurred and is continuing, the holder of the note indicated as the “controlling” note will be the controlling noteholder. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

UBS 2018-C8

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Previous Securitization History(1) | ||||||

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Cut-off Date Balance | % of Initial Outstanding Pool Balance | Previous Securitization(s) |

| University Properties Portfolio | CIBC | Bloomington, IN | Multifamily | $34,500,000 | 3.3% | MSC 2007-IQ16 |

| Residence Inn Irvine | SG | Irvine, CA | Hospitality | $33,000,000 | 3.2% | BACM 2008-1 |

| City Square & Clay Street | LCF | Oakland, CA | Mixed Use | $45,000,000 | 4.3% | COMM 2014-CCRE14 |

| BlueLinx Portfolio | SG | Various | Industrial | $28,600,000 | 2.7% | WBCMT 2006-C27 |

| South Bend Medical Office | CCRE | South Bend, IN | Office | $15,200,000 | 1.5% | MSC 2006-HQ10 |

| Storage Direct Roseville | RMF | Roseville, CA | Self Storage | $8,350,000 | 0.8% | BACM 2006-3 |

| WoodSpring Suites Baton Rouge Portfolio | CIBC | Baton Rouge, LA | Hospitality | $7,500,000 | 0.7% | CGCMT 2013-GC11 |

| Brooklyn Multifamily Portfolio | LCF | Brooklyn, NY | Various | $7,000,000 | 0.7% | COMM 2014-UBS4 |

| San Pedro Crossing(2) | SG; UBS AG | San Antonio, TX | Retail | $4,477,143 | 0.4% | COMM 2013-LC6 |

| Walgreens - Harlingen, TX | CIBC | Harlingen, TX | Retail | $3,250,000 | 0.3% | LBUBS 2008-C1 |

| Walgreens - Dallas, GA | CIBC | Dallas, GA | Retail | $2,800,000 | 0.3% | LBUBS 2008-C1 |

| Walgreens - Guthrie, OK | CIBC | Guthrie, OK | Retail | $2,742,750 | 0.3% | LBUBS 2008-C1 |

| (1) | Includes mortgage loans for which all or a portion of the previously existing debt was most recently securitized in one or more conduit securitizations, based on information provided by the related borrower or obtained through searches of a third-party database. The information has not otherwise been confirmed by the mortgage loan sellers. |

| (2) | Part of the collateral for the AFIN Portfolio Mortgage Loan |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

| Mortgage Loan Information | Property Information | ||||||

| Mortgage Loan Seller(1): | Société Générale; UBS AG | Single Asset/Portfolio: | Portfolio | ||||

| Original Balance(2): | $60,000,000 | Location: | Various | ||||

| Cut-off Date Balance(2): | $60,000,000 | General Property Type: | Retail | ||||

| % of Initial Pool Balance: | 5.7% | Detailed Property Type: | Anchored | ||||

| Loan Purpose(3): | Recapitalization | Title Vesting: | Fee | ||||

| Borrower Sponsor: | American Finance Operating Partnership, L.P. | Year Built/Renovated: | Various | ||||

| Size: | 2,418,910 SF | ||||||

| Mortgage Rate: | 4.1910% | Cut-off Date Balance per SF(2): | $87 | ||||

| Note Date: | 12/8/2017 | Maturity Date Balance per SF(2): | $87 | ||||

| First Payment Date: | 2/1/2018 | Property Manager: | American Finance Properties, LLC | ||||

| Maturity Date: | 1/1/2028 | ||||||

| Original Term to Maturity: | 120 months | ||||||

| Original Amortization Term: | 0 months | ||||||

| IO Period: | 120 months | ||||||

| Seasoning: | 1 month | ||||||

| Prepayment Provisions(4): | LO (11); YM1 (107); O (2) | Underwriting and Financial Information | |||||

| Lockbox/Cash Mgmt Status: | Hard/Springing | UW NOI: | $23,341,476 | ||||

| Additional Debt Type(2): | Pari Passu | UW NOI Debt Yield(2): | 11.1% | ||||

| Additional Debt Balance(2): | $150,000,000 | UW NOI Debt Yield at Maturity(2): | 11.1% | ||||

| Future Debt Permitted (Type): | No (N/A) | UW NCF DSCR(2): | 2.34x | ||||

| Reserves(5) | Most Recent NOI: | $26,006,908 (9/30/2017 TTM) | |||||

| Type | Initial | Monthly | Cap | 2nd Most Recent NOI: | $27,004,951 (12/31/2016) | ||

| RE Tax: | $832,502 | $355,956 | N/A | 3rd Most Recent NOI: | N/A | ||

| Insurance: | $203,509 | $43,761 | N/A | Most Recent Occupancy: | 90.3% (11/28/2017) | ||

| Replacements: | $0 | Springing | N/A | 2nd Most Recent Occupancy: | 97.6% (12/31/2016) | ||

| Deferred Maintenance: | $101,926 | $0 | N/A | 3rd Most Recent Occupancy: | N/A | ||

| TI/LC: | $798,196 | Springing | N/A | Appraised Value (as of): | $371,735,000 (Various) | ||

| Environmental: | $9,827 | $0 | N/A | Cut-off Date LTV Ratio(2): | 56.5% | ||

| Free Rent: | $154,430 | $0 | N/A | Maturity Date LTV Ratio(2): | 56.5% | ||

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Loan Amount(2): | $210,000,000 | 100.0% | Loan Payoff(3): | $17,985,000 | 8.6% | |

| Reserves: | $2,100,391 | 1.0% | ||||

| Closing Costs: | $4,431,142 | 2.1% | ||||

| Return of Equity: | $185,483,468 | 88.3% | ||||

| Total Sources: | $210,000,000 | 100.0% | Total Uses: | $210,000,000 | 100.0% | |

| (1) | The AFIN Portfolio Whole Loan was co-originated by Société Générale and UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS AG”). |

| (2) | The AFIN Portfolio Mortgage Loan (as defined below) is part of the AFIN Portfolio Whole Loan, which is comprised of sixteenpari passusenior promissory notes with an aggregate principal balance of $210,000,000. The Cut-off Date Balance per SF, Maturity Date Balance per SF, UW NOI Debt Yield, UW NOI Debt Yield at Maturity, UW NCF DSCR, Cut-off Date LTV Ratio and Maturity Date LTV Ratio numbers presented above are based on the aggregate principal balance of the AFIN Portfolio Whole Loan. |

| (3) | Loan proceeds were used to refinance existing debt of approximately $18.0 million encumbering the San Pedro Crossing Property and recapitalize the borrower sponsor’s recent acquisition of the remaining 11 AFIN Portfolio Properties. |

| (4) | Prior to the open prepayment date occurring in December 2027, the AFIN Portfolio Whole Loan can be prepaid with yield maintenance. Partial release is permitted. See “Release of Property” below for further discussion of release requirements. |

| (5) | See “Escrows and Reserves” below for further discussion of reserve requirements. |

The Mortgage Loan. The largest mortgage loan (the “AFIN Portfolio Mortgage Loan”) is part of a whole loan (the “AFIN Portfolio Whole Loan”) evidenced by sixteenpari passu promissory notes with an aggregate original principal balance of $210,000,000. The AFIN Portfolio Whole Loan is secured by a first priority fee mortgage encumbering a 2,418,910 SF, 12-property portfolio of anchored retail properties located in North Carolina (three properties), Florida (two properties), Nevada (two properties), Kentucky (one property), Ohio (one property), Oklahoma (one property), Texas (one property) and South Carolina (one property) (collectively, the “AFIN Portfolio Properties”). The AFIN Portfolio Whole Loan was co-originated by Société Générale and UBS AG. Promissory Notes A-1, A-5, A-10 and A-15, with an aggregate original principal balance of $60,000,000, collectively represent the AFIN Portfolio Mortgage Loan and will be included in the UBS 2018-C8 Trust. The below table summarizes the remaining promissory notes, which were either previously securitized or are currently held by Société Générale and UBS AG and are expected to be contributed to one or more future securitization transactions or may be otherwise transferred at any time.

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

| AFIN Portfolio Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Anticipated Note Holder | Controlling Piece |

| Note A-1 | $25,000,000 | $25,000,000 | UBS 2018-C8 | No |

| Note A-2 | $25,000,000 | $25,000,000 | Société Générale | No |

| Note A-3 | $20,000,000 | $20,000,000 | UBS 2017-C7 | No |

| Note A-4 | $12,000,000 | $12,000,000 | UBS 2017-C7 | No |

| Note A-5 | $10,000,000 | $10,000,000 | UBS 2018-C8 | No |

| Note A-6 | $10,000,000 | $10,000,000 | Société Générale | No |

| Note A-7 | $5,000,000 | $5,000,000 | Société Générale | No |

| Note A-8 | $5,000,000 | $5,000,000 | Société Générale | Yes |

| Note A-9 | $20,000,000 | $20,000,000 | UBS 2017-C7 | No |

| Note A-10 | $20,000,000 | $20,000,000 | UBS 2018-C8 | No |

| Note A-11 | $15,000,000 | $15,000,000 | UBS AG | No |

| Note A-12 | $15,000,000 | $15,000,000 | UBS AG | No |

| Note A-13 | $10,000,000 | $10,000,000 | UBS AG | No |

| Note A-14 | $8,000,000 | $8,000,000 | UBS 2017-C7 | No |

| Note A-15 | $5,000,000 | $5,000,000 | UBS 2018-C8 | No |

| Note A-16 | $5,000,000 | $5,000,000 | UBS AG | No |

| Total | $210,000,000 | $210,000,000 | ||

The proceeds of the AFIN Portfolio Whole Loan were used to refinance existing debt of approximately $18.0 million encumbering the San Pedro Crossing Property, recapitalize the borrower sponsor’s investment in the remaining 11 AFIN Portfolio Properties, fund reserves, and pay closing costs.

The Borrowers and the Borrower Sponsor. The borrowers are ARC CPOKCOK001, LLC; ARC SMWMBFL001, LLC; ARC CPFAYNC001, LLC; ARC SPSANTX001, LLC; ARC JCLOUKY001, LLC; ARC NPHUBOH001, LLC; ARC ASANDSC001, LLC; ARC NLLKLFL001, LLC; ARC RBASHNC001, LLC; ARC MCLVSNV001, LLC; ARC BBLVSNV001, LLC; and ARC RGCHRNC001, LLC (collectively, the “AFIN Portfolio Borrowers”), all single-purpose Delaware limited liability companies structured to be bankruptcy remote with two independent directors. The AFIN Portfolio Borrowers are 100.0% owned by the borrower sponsor and nonrecourse carve-out guarantor, American Finance Operating Partnership, L.P. (the “Guarantor”).

American Finance Trust, Inc. (“AFIN”) is a public non-traded real estate investment trust that acquires and manages a diversified portfolio of commercial properties, which are net leased primarily to investment grade and national tenants, as well as a portfolio of stabilized core retail properties consisting primarily of power centers and lifestyle centers. As of the second quarter 2017, the borrower sponsor had a portfolio of 516 properties totaling approximately 19.2 million square feet. AFIN is externally managed by AR Global Investments, LLC, which has raised and invested over $30.0 billion in capital, served over 150,000 shareholders, and grown to one of the largest external managers of direct investment programs in the United States. See “Description of the Mortgage Pool—Litigation and Other Considerations” in the Preliminary Prospectus.

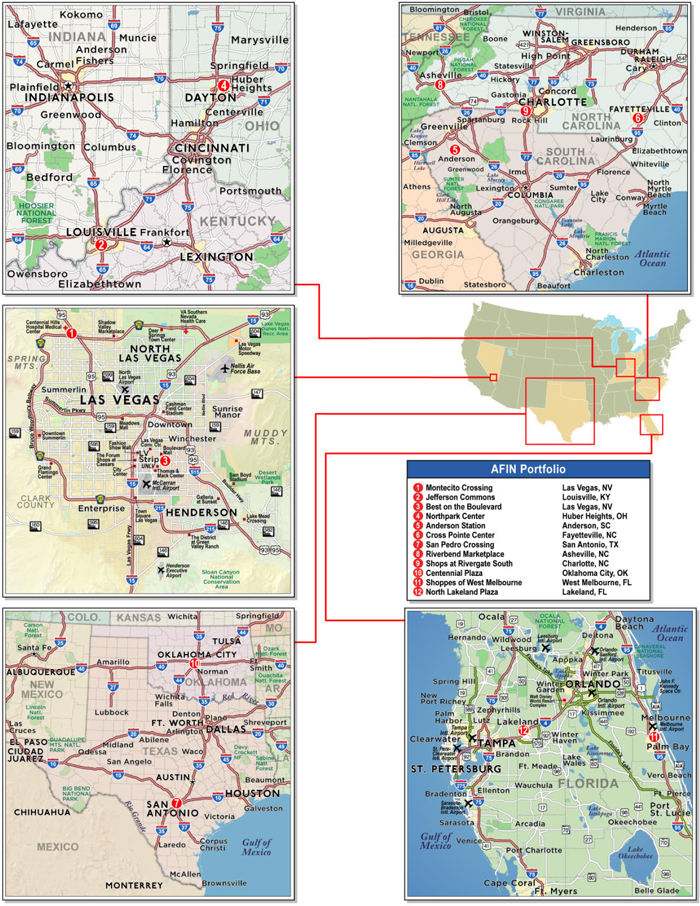

The Properties.The following table describes each property comprising the AFIN Portfolio Properties by descending Allocated Whole Loan Cut-off Date Balance.

| Portfolio Summary | |||||||||

| Property Name | Location | Year Built/ Renovated | Net Rentable Area (SF)(1) | UW NCF | % of UW NCF | Allocated Whole Loan Cut-off Date Balance(2) | % of Whole Loan Cut-off Date Balance | Appraised Value | Allocated Cut-off Date LTV Ratio(2) |

| Montecito Crossing | Las Vegas, NV | 2005/N/A | 179,721 | $3,101,756 | 14.9% | $33,040,000 | 15.7% | $52,450,000 | 63.0% |

| Jefferson Commons | Louisville, KY | 2014/N/A | 205,918 | $2,424,762 | 11.6% | $24,440,000 | 11.6% | $38,800,000 | 63.0% |

| Best on the Boulevard | Las Vegas, NV | 1996/2000 | 204,568 | $2,260,490 | 10.8% | $24,350,000 | 11.6% | $38,650,000 | 63.0% |

| Northpark Center | Huber Heights, OH | 1994/2017 | 318,330 | $2,394,795 | 11.5% | $20,350,000 | 9.7% | $36,330,000 | 56.0% |

| Anderson Station | Anderson, SC | 2001/N/A | 244,171 | $1,864,006 | 8.9% | $15,860,000 | 7.6% | $28,000,000 | 56.6% |

| Cross Pointe Center | Fayetteville, NC | 1986/2003 | 226,089 | $1,686,633 | 8.1% | $15,730,000 | 7.5% | $27,675,000 | 56.8% |

| San Pedro Crossing | San Antonio, TX | 1995-1999/N/A | 207,121 | $1,398,161 | 6.7% | $15,670,000 | 7.5% | $39,800,000 | 39.4% |

| Riverbend Marketplace | Asheville, NC | 2004/N/A | 142,617 | $1,237,445 | 5.9% | $14,120,000 | 6.7% | $22,580,000 | 62.5% |

| Shops at RiverGate South | Charlotte, NC | 2014/N/A | 140,697 | $1,081,973 | 5.2% | $14,090,000 | 6.7% | $25,000,000 | 56.4% |

| Centennial Plaza | Oklahoma City, OK | 1992-1994/N/A | 233,797 | $1,209,463 | 5.8% | $13,360,000 | 6.4% | $25,600,000 | 52.2% |

| Shoppes of West Melbourne | West Melbourne, FL | 1984/N/A | 144,484 | $1,529,708 | 7.3% | $12,480,000 | 5.9% | $21,900,000 | 57.0% |

| North Lakeland Plaza | Lakeland, FL | 1986/N/A | 171,397 | $649,325 | 3.1% | $6,510,000 | 3.1% | $14,950,000 | 43.5% |

| Total/Wtd. Avg. | 2,418,910 | $20,838,518 | 100.0% | $210,000,000 | 100.0% | $371,735,000 | 56.5% | ||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Based on the AFIN Portfolio Whole Loan allocated loan amounts. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

The AFIN Portfolio Properties benefit from nine distinct retailers (23.8% of underwritten base rent), representing investment grade tenants, including Kohl’s (rated BBB/Baa2/BBB- by Fitch/Moody’s/S&P), Best Buy (rated BBB-/Baa1/BBB- by Fitch/Moody’s/S&P), The Home Depot (rated A/A2/A by Fitch/Moody’s/S&P), Bed Bath & Beyond (rated NR/Baa1/BBB by Fitch/Moody’s/S&P), Ross Dress For Less (rated NR/A3/A- by Fitch/Moody’s/S&P), The TJX Companies, Inc. (parent company of TJ Maxx and Marshalls, rated NR/A2/A+ by Fitch/Moody’s/S&P), and Gap, Inc. (parent company of Old Navy, rated BB+/Baa2/BB+ by Fitch/Moody’s/S&P), among others.

The AFIN Portfolio Properties have a weighted average tenant tenure of 14.4 years and a weighted average remaining lease term of 5.7 years. Additionally, 59.1% of tenants by NRA have been in occupancy for more than 11 years.

The following table presents certain information relating the tenants at the AFIN Portfolio Properties:

| Tenant Summary(1) | ||||||||

| Tenant Name | Portfolio Locations | Credit Rating (Fitch/Moody’s/S&P)(2) | Tenant SF | Approximate % of SF | Annual UW Base Rent(3) | % of Total Annual UW Base Rent | Annual UW Base Rent PSF(3) | Lease Expiration |

| Kohl’s | 2 | BBB/Baa2/BBB- | 169,139 | 7.0% | $1,353,380 | 5.0% | $8.00 | Various |

| Best Buy | 3 | BBB-/Baa1/BBB- | 155,347 | 6.4% | $1,529,407 | 5.6% | $9.85 | Various |

| Home Depot | 1 | A/A2/A | 102,962 | 4.3% | $854,585 | 3.1% | $8.30 | 1/31/2019 |

| Elder Beerman | 1 | NR/NR/NR | 101,840 | 4.2% | $407,360 | 1.5% | $4.00 | 10/31/2019 |

| Bealls | 1 | NR/NR/NR | 84,146 | 3.5% | $483,839 | 1.8% | $5.75 | 4/30/2020 |

| Bed Bath & Beyond | 3 | NR/Baa1/BBB | 77,986 | 3.2% | $770,152 | 2.8% | $9.88 | Various |

| Academy Sports + Outdoors | 1 | NR/B3/NR | 71,914 | 3.0% | $701,162 | 2.6% | $9.75 | 2/28/2030 |

| PetSmart | 3 | NR/B1/B | 66,351 | 2.7% | $899,498 | 3.3% | $13.56 | Various |

| Ross Dress For Less | 2 | NR/A3/A- | 62,034 | 2.6% | $707,021 | 2.6% | $11.40 | Various |

| Toys R Us(4) | 1 | NR/NR/NR | 60,687 | 2.5% | $0 | 0.0% | $0.00 | 1/31/2021 |

| Office Depot | 3 | NR/B1/B | 57,262 | 2.4% | $589,295 | 2.2% | $10.29 | Various |

| Shoe Carnival | 4 | NR/NR/NR | 56,287 | 2.3% | $730,967 | 2.7% | $12.99 | Various |

| Hobby Lobby | 1 | NR/NR/NR | 55,000 | 2.3% | $426,240 | 1.6% | $7.75 | 8/31/2019 |

| Jo-Ann Fabric | 2 | NR/B1/B | 54,859 | 2.3% | $566,586 | 2.1% | $10.33 | Various |

| Party City | 3 | NR/NR/NR | 52,427 | 2.2% | $616,513 | 2.3% | $11.76 | Various |

| HomeGoods | 2 | NR/A2/A+ | 49,000 | 2.0% | $370,894 | 1.4% | $7.57 | Various |

| Seafood City Supermarket | 1 | NR/NR/NR | 42,618 | 1.8% | $500,369 | 1.8% | $11.74 | 2/28/2022 |

| Barnes & Noble | 1 | NR/NR/NR | 35,475 | 1.5% | $645,000 | 2.4% | $18.18 | 2/28/2021 |

| Michaels | 2 | NR/NR/NR | 34,502 | 1.4% | $412,785 | 1.5% | $11.96 | Various |

| ULTA Beauty | 3 | NR/NR/NR | 30,415 | 1.3% | $595,426 | 2.2% | $19.58 | Various |

| Pier 1 Imports | 3 | NR/NR/B | 30,300 | 1.3% | $533,550 | 2.0% | $17.61 | Various |

| TJ Maxx | 1 | NR/A2/A+ | 30,000 | 1.2% | $330,000 | 1.2% | $11.00 | 10/31/2026 |

| Marshalls | 1 | NR/A2/A+ | 29,500 | 1.2% | $309,750 | 1.1% | $10.50 | 5/31/2026 |

| Aldi | 1 | NR/NR/NR | 24,067 | 1.0% | $264,737 | 1.0% | $11.00 | 5/31/2028 |

| The Container Store | 1 | NR/NR/NR | 22,817 | 0.9% | $607,389 | 2.2% | $26.62 | 1/31/2023 |

| Liquor Barn | 1 | NR/NR/NR | 22,000 | 0.9% | $302,500 | 1.1% | $13.75 | 5/31/2025 |

| Dollar Tree | 2 | NR/Ba1/BB+ | 21,563 | 0.9% | $192,530 | 0.7% | $8.93 | Various |

| Old Navy | 1 | BB+/Baa2/BB+ | 20,000 | 0.8% | $260,000 | 1.0% | $13.00 | 1/31/2022 |

| Five Below | 2 | NR/NR/NR | 15,815 | 0.7% | $243,364 | 0.9% | $15.39 | Various |

| Guitar Center | 1 | NR/NR/NR | 15,200 | 0.6% | $149,720 | 0.6% | $9.85 | 10/31/2025 |

| Kirkland’s | 2 | NR/NR/NR | 13,661 | 0.6% | $227,784 | 0.8% | $16.67 | Various |

| Cavender’s Boot City | 1 | NR/NR/NR | 13,548 | 0.6% | $270,960 | 1.0% | $20.00 | 6/30/2022 |

| Big 5 Sports | 1 | NR/NR/NR | 10,080 | 0.4% | $157,308 | 0.6% | $15.61 | 1/31/2021 |

| Tuesday Morning | 1 | NR/NR/NR | 10,000 | 0.4% | $115,000 | 0.4% | $11.50 | 7/31/2021 |

| Subtotal/Wtd. Avg. | 59 | 1,698,802 | 70.2% | $17,125,071 | 62.9% | $10.45 | ||

| Remaining Tenants | 145 | 484,411 | 20.0% | $10,096,411 | 37.1% | $20.84 | ||

| Vacant Space | 0 | 235,697 | 9.7% | $0 | 0.0% | $0.00 | ||

| Total/Wtd. Avg. | 204 | 2,418,910 | 100.0% | $27,221,482 | 100.0% | $12.83 | ||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Ratings provided are for the parent company of the entity listed in the Tenant Name field whether or not the parent company guarantees the lease. |

| (3) | Annual UW Base Rent and Annual UW Base Rent PSF exclude vacant space and Toys R Us, which was underwritten as vacant. |

| (4) | Toys R Us was underwritten as vacant; however, it is currently in occupancy and paying annual base rent of $910,305. |

THE INFORMATION IN THIS COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| Various | Collateral Asset Summary – Loan No. 1 AFIN Portfolio | Cut-off Date Balance: Cut-off Date LTV Ratio: UW NCF DSCR: UW NOI Debt Yield: | 11.1% |

The following table presents certain information relating to the lease rollover schedule at the AFIN Portfolio Properties:

| Lease Rollover Schedule(1)(2) | ||||||||

| Year | # of Leases Rolling | SF Rolling | Approx. % of Total SF Rolling | Approx. Cumulative % of SF Rolling | UW Base Rent PSF Rolling(3) | Total UW Base Rent Rolling | Approx. % of Total Rent Rolling | Approx. Cumulative % of Total Rent Rolling |

| MTM | 3 | 1,200 | 0.0% | 0.0% | $13.00 | $15,600 | 0.1% | 0.1% |

| 2017 | 1 | 6,450 | 0.3% | 0.3% | $17.05 | $110,000 | 0.4% | 0.5% |

| 2018 | 12 | 30,119 | 1.2% | 1.6% | $23.72 | $714,319 | 2.6% | 3.1% |

| 2019 | 37 | 385,633 | 15.9% | 17.5% | $10.43 | $4,021,681 | 14.8% | 17.9% |

| 2020 | 40 | 305,740 | 12.6% | 30.1% | $11.70 | $3,575,705 | 13.1% | 31.0% |

| 2021 | 24 | 304,056 | 12.6% | 42.7% | $16.52 | $4,020,214 | 14.8% | 45.8% |

| 2022 | 20 | 209,122 | 8.6% | 51.4% | $13.25 | $2,770,175 | 10.2% | 55.9% |

| 2023 | 15 | 147,255 | 6.1% | 57.4% | $15.59 | $2,295,977 | 8.4% | 64.4% |

| 2024 | 10 | 107,970 | 4.5% | 61.9% | $13.97 | $1,508,345 | 5.5% | 69.9% |

| 2025 | 22 | 375,206 | 15.5% | 77.4% | $13.66 | $5,126,583 | 18.8% | 88.7% |

| 2026 | 5 | 80,723 | 3.3% | 80.8% | $13.24 | $1,068,564 | 3.9% | 92.7% |

| 2027 | 3 | 13,563 | 0.6% | 81.3% | $28.03 | $380,233 | 1.4% | 94.1% |

| 2028 & Beyond | 12 | 216,176 | 8.9% | 90.3% | $7.47 | $1,614,086 | 5.9% | 100.0% |

| Vacant | 0 | 235,697 | 9.7% | 100.0% | $0.00 | $0 | 0.0% | 100.0% |

| Total/Wtd. Avg. | 204 | 2,418,910 | 100.0% | $12.83 | $27,221,482 | 100.0% | ||

| (1) | Information is based on the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the originally stated expiration date of the subject lease and that are not considered in the lease rollover schedule. |

| (3) | Wtd. Avg. UW Base Rent PSF Rolling excludes vacant space. |

The Market.

The following table presents certain market information relating to the AFIN Portfolio Properties:

| Market Overview(1) | |||||||

| Property Name | Location | Market | Submarket | Estimated 2017 Population(2) | Estimated 2017 Average Household Income(2) | Rental Rate PSF | |

| Actual(3) | Submarket(4) | ||||||

| Montecito Crossing | Las Vegas, NV | Las Vegas | Northwest | 233,930 | $86,121 | $21.10 | $19.80 |

| Jefferson Commons | Louisville, KY | Louisville | South Central | 176,569 | $59,649 | $14.29 | $9.67 |

| Best on the Boulevard | Las Vegas, NV | Las Vegas | Central East | 448,909 | $50,073 | $14.33 | $15.48 |

| Northpark Center | Huber Heights, OH | Dayton | NE Central Dayton | 83,316 | $71,020 | $8.74 | $7.42 |

| Anderson Station | Anderson, SC | Greenville/Spartanburg | Anderson | 56,860 | $64,691 | $11.61 | $8.73 |

| Cross Pointe Center | Fayetteville, NC | Fayetteville | N/A(5) | 151,777 | $58,794 | $9.55 | $10.26(5) |

| San Pedro Crossing | San Antonio, TX | San Antonio | North Central | 322,165 | $78,955 | $17.34 | $18.72 |

| Riverbend Marketplace | Asheville, NC | Asheville | East Asheville | 87,541 | $66,334 | $12.13 | $13.57 |

| Shops at RiverGate South | Charlotte, NC | Charlotte | Southwest | 99,238 | $95,171 | $17.44 | $20.75 |

| Centennial Plaza | Oklahoma City, OK | Oklahoma City | Penn Square | 243,184 | $63,794 | $9.31 | $12.72 |

| Shoppes of West Melbourne | West Melbourne, FL | Orlando | Brevard County | 132,623 | $61,786 | $12.34 | $11.85 |