Filed Pursuant to Rule 424(b)(3)

Registration No. 333-254251

$73,298,000

Cleveland-Cliffs Inc.

Offer to Exchange

All of the Outstanding Restricted 7.00% Senior Guaranteed Notes due 2027

Issued on March 16, 2020

for

Newly Issued and Registered 7.00% Senior Guaranteed Notes due 2027

On March 16, 2020, we issued $335,376,000 aggregate principal amount of restricted 7.00% senior guaranteed notes due 2027, which we refer to herein as the Original Notes. The Original Notes were issued in a private transaction exempt from the registration requirements of the Securities Act of 1933, as amended, or the Securities Act. As of March 12, 2021, there was $73,298,000 aggregate principal amount of Original Notes outstanding.

We are offering to exchange up to $73,298,000 aggregate principal amount of new 7.00% senior guaranteed notes due 2027, which we refer to herein as the Exchange Notes, for the outstanding Original Notes. We refer herein to the Original Notes and the Exchange Notes, collectively, as the Notes. We refer to the offer to exchange as the Exchange Offer.

The terms of the Exchange Notes will be substantially identical to the terms of the Original Notes, except that the Exchange Notes will be registered under the Securities Act and the transfer restrictions and registration rights and related additional interest provisions applicable to the Original Notes will not apply to the Exchange Notes. The Exchange Notes will be part of the same series as the Original Notes and will be issued under the same indenture. The Exchange Notes will be exchanged for Original Notes in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. We will not receive any proceeds from the issuance of Exchange Notes in the Exchange Offer.

You may withdraw tenders of Original Notes at any time prior to the expiration of the Exchange Offer.

The Exchange Offer expires at 5:00 p.m. New York City time on April 22, 2021 unless extended, which we refer to as the Expiration Date.

We do not intend to list the Exchange Notes on any securities exchange or to seek approval through any automated quotation system, and no active public market for the Exchange Notes is anticipated.

You should consider carefully the risk factors beginning on page 18 of this prospectus before deciding whether to participate in the Exchange Offer. Neither the Securities and Exchange Commission, which we refer to herein as the SEC, nor any state securities commission has approved or disapproved of the Exchange Notes or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is March 25, 2021.

Rather than repeat certain information in this prospectus that we have already included in reports filed with the SEC, this prospectus incorporates important business and financial information about us that is not included in or delivered with this prospectus. We will provide this information to you at no charge upon written or oral request directed to: Cleveland-Cliffs Inc., 200 Public Square, Suite 3300, Cleveland, Ohio, 44114-2315, Attention: Investor Relations; Telephone: (216) 694-5700. In order to receive timely delivery of any requested documents in advance of the Expiration Date, you should make your request no later than April 15, 2021, which is five full business days before you must make a decision regarding the Exchange Offer.

Table of Contents

| | | | | |

| Page |

| NOTICE TO INVESTORS | |

| WHERE YOU CAN FIND MORE INFORMATION | |

| INFORMATION WE INCORPORATE BY REFERENCE | |

| NON-GAAP FINANCIAL MEASURES | |

| DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS | |

| SUMMARY | |

| RISK FACTORS | |

| USE OF PROCEEDS | |

| THE EXCHANGE OFFER | |

| DESCRIPTION OF OTHER INDEBTEDNESS | |

| DESCRIPTION OF THE NOTES | |

| CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS | |

| CERTAIN ERISA CONSIDERATIONS | |

| PLAN OF DISTRIBUTION | |

| LEGAL MATTERS | |

| EXPERTS | |

NOTICE TO INVESTORS

This prospectus may only be used where it is legal to make the Exchange Offer and by a broker-dealer for resales of Exchange Notes acquired in the Exchange Offer where it is legal to do so.

This prospectus and the information incorporated by reference summarize documents and other information in a manner we believe to be accurate, but we refer you to the actual documents for a more complete understanding of the information we discuss in this prospectus and the information incorporated by reference. In deciding to exchange your Original Notes, you must rely on your own examination of such documents, our business and the terms of the Exchange Offer and the Exchange Notes, including the merits and risks involved.

We make no representation to you that the Exchange Notes will be a legal investment for you. You should not consider any information in this prospectus to be legal, business or tax advice. You should consult your own attorney, business advisor and tax advisor for legal, business and tax advice regarding an investment in the Exchange Notes. Neither the delivery of the prospectus nor any exchange made pursuant to this prospectus implies that any information set forth in or incorporated by reference in this prospectus is correct as of any date after the date of this prospectus.

Each broker-dealer that receives Exchange Notes for its own account pursuant to the Exchange Offer must acknowledge that it will deliver a prospectus in connection with any resale of Exchange Notes. The letter of transmittal accompanying this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of Exchange Notes received in exchange for Original Notes where the Original Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period ending on the date on which a broker-dealer is no longer required to deliver a prospectus in connection with market-making or other trading activities, we will make this prospectus available to any broker-dealer for use in connection with these resales. See “Plan of Distribution.”

Except as otherwise indicated or the context otherwise requires, references in this prospectus to the terms “we,” “us,” “our,” “the Company” or “Cliffs” or other similar terms mean Cleveland-Cliffs Inc. and its consolidated subsidiaries, including (i) Cleveland-Cliffs Steel Holding Corporation (f/k/a AK Steel Holding Corporation), or AK Steel, and (ii) entities acquired in connection with the AM USA Transaction (as defined below), which include substantially all of the operations of the former ArcelorMittal USA LLC, a Delaware limited liability company, its subsidiaries and certain affiliates. In connection with the AM USA Transaction, Cliffs also acquired I/N Kote L.P., or I/N Kote, and I/N Tek L.P., or I/N Tek, which are former joint ventures between subsidiaries of the former ArcelorMittal USA LLC and Nippon Steel Corporation. We refer to the former ArcelorMittal USA LLC, its subsidiaries and certain of its affiliates, I/N Kote and I/N Tek, collectively, as ArcelorMittal USA. As used in this prospectus, the term “long ton” means a long ton (equal to 2,240 pounds) and the term “net ton” means a net ton (equal to 2,000 pounds).

WHERE YOU CAN FIND MORE INFORMATION

We are subject to the informational reporting requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act. We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available over the Internet at the SEC’s website at www.sec.gov.

We make available, free of charge, on our website at www.clevelandcliffs.com, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and amendments to those reports and statements as soon as reasonably practicable after they are filed with

the SEC. The information contained on or accessible through our website is not part of this prospectus, other than the documents that we file with the SEC that are specifically incorporated by reference into this prospectus.

INFORMATION WE INCORPORATE BY REFERENCE

We are incorporating by reference certain information that we file with the SEC, which means:

•incorporated documents are considered part of this prospectus;

•we can disclose important information to you by referring you to those documents; and

•information that we file with the SEC after the date of this prospectus will automatically update and supersede the information contained in this prospectus and incorporated filings.

We incorporate by reference the documents listed below that we filed with the SEC under the Exchange Act:

•Annual Report on Form 10-K for the year ended December 31, 2020 (filed with the SEC on February 26, 2021); and •Current Reports on Form 8-K filed with the SEC on December 9, 2020 (as to Items 1.01, 2.01, 2.03, 3.02, 3.03, 5.03 and 9.01(a) and (b) and related exhibits only), as amended by Amendment No. 1 to Current Report on Form 8-K/A filed with the SEC on February 8, 2021 (excluding Exhibit 99.7), February 9, 2021, February 11, 2021, February 17, 2021 and March 12, 2021. We also incorporate by reference each of the documents that we file with the SEC under Section 13(a), 13(c), 14 or 15(d) of the Exchange Act on or after the date of this prospectus and until the completion of the Exchange Offer. We do not and will not, however, incorporate by reference in this prospectus any documents or portions thereof that are not deemed “filed” with the SEC, including any information furnished pursuant to Item 2.02 or Item 7.01 of our Current Reports on Form 8-K after the date of this prospectus unless, and except to the extent, specified in such Current Reports.

We will provide you with a copy of any of these filings (other than an exhibit to these filings, unless the exhibit is specifically incorporated by reference into the filing requested) at no cost, if you submit a request to us by writing or telephoning us at the following address or telephone number:

Cleveland-Cliffs Inc.

200 Public Square, Suite 3300

Cleveland, Ohio 44114

Attention: Investor Relations

Telephone: 1-216-694-5700

NON-GAAP FINANCIAL MEASURES

We believe that the financial statements and the other financial data included in, or incorporated by reference into, this prospectus have been prepared in a manner that complies, in all material respects, with generally accepted accounting principles in the United States, or GAAP, and the regulations published by the SEC and are consistent with current practice with the exception of the presentation of earnings before interest, taxes, depreciation and amortization, or EBITDA, as adjusted, with respect to each of Cliffs; the former ArcelorMittal USA LLC, its subsidiaries and certain affiliates; I/N Kote; and I/N Tek.

Adjusted EBITDA is a non-GAAP financial measure and is not calculated in the same manner by all companies or the entities presented herein, and, accordingly, is not necessarily comparable to similarly titled measures of other companies and may not be an appropriate measure for comparing performance relative to other companies. While we believe that the presentation of adjusted EBITDA will (1) enhance an investor’s understanding of our operating performance and how it compares to other producers and (2) provide a more accurate view of the cash outflows related to the sale of steel and iron ore, the use of the non-GAAP financial measures as analytical tools has limitations and you should not consider them in isolation, or as substitutes for an analysis of our results of operations as reported in accordance with GAAP. Adjusted EBITDA is not a measurement of financial performance or condition under GAAP and should not be considered as alternatives to net income, operating income, or any other financial performance measure derived in accordance with GAAP.

Cliffs

Cliffs evaluates performance based on adjusted EBITDA, which is defined as EBITDA, excluding certain items such as EBITDA of noncontrolling interest, impacts of discontinued operations, extinguishment of debt, severance, acquisition-related costs, amortization of inventory step-up, foreign exchange remeasurement, and impairment of other long-lived assets, or Cliffs Adjusted EBITDA.

This measure is used by management, investors, lenders and other external users of our financial statements to assess our operating performance and to compare operating performance to other companies in the steel and iron ore industries, although it is not necessarily comparable to similarly titled measures used by other companies. In addition, management believes Cliffs Adjusted EBITDA is a useful measure to assess the earnings power of the business without the impact of capital structure and can be used to assess our ability to service debt and fund future capital expenditures in the business.

For additional information about Cliffs Adjusted EBITDA, including a reconciliation to the most directly comparable GAAP financial measure, see the section titled “Summary—Summary Historical Consolidated Financial Data of Cliffs” of this prospectus.

ArcelorMittal USA LLC and Affiliates, I/N Kote and I/N Tek

Adjusted EBITDA is presented in this prospectus with respect to each of the former ArcelorMittal USA LLC, its subsidiaries and certain affiliates; I/N Kote; and I/N Tek and is defined as EBITDA, excluding certain items such as the effect of derivative timing adjustments, Industrial Franchise Agreement (as defined herein) fee and miscellaneous corporate chargebacks, asset impairments and impacts of onerous contracts, as applicable, or ArcelorMittal USA Adjusted EBITDA Measures.

Management believes that reporting the ArcelorMittal USA Adjusted EBITDA Measures more clearly reflects these entities’ respective operating results for the periods presented and provides investors with a better understanding of their respective overall financial performance.

For additional information about the ArcelorMittal USA Adjusted EBITDA Measures, including a reconciliation to the most directly comparable GAAP financial measure, see the sections titled “Summary—Summary Historical Financial Data of ArcelorMittal USA LLC and Affiliates,” “Summary—Summary Historical Financial Data of I/N Kote” and “Summary—Summary Historical Financial Data of I/N Tek” of this prospectus.

Unaudited Pro Forma Condensed Combined Financial Data

Adjusted EBITDA is presented in this prospectus with respect to the unaudited pro forma condensed combined financial statements and is defined as EBITDA, excluding certain items such as the effects of the EBITDA of noncontrolling interests, charges associated with asset impairments, acquisition-related costs, inventory step-up, impact of discontinued operations, impact of extinguishment of debt,

severance costs, impact of onerous contracts and certain expected synergies, or Pro Forma Adjusted EBITDA.

This measure is used by management, investors, lenders and other external users of our financial statements to assess our operating performance and to compare operating performance to other companies in the steel industry, although it is not necessarily comparable to similarly titled measures used by other companies. In addition, management believes Pro Forma Adjusted EBITDA is a useful measure to assess the earnings power of the business without the impact of capital structure and can be used to assess our ability to service debt and fund future capital expenditures in the business.

For additional information about Pro Forma Adjusted EBITDA, including a reconciliation to the most directly comparable GAAP financial measure, see the section titled “Summary—Unaudited Pro Forma Condensed Combined Financial Data” of this prospectus.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus, including the documents incorporated by reference, contains, and any prospectus supplement may contain, statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements may be identified by the use of predictive, future-tense or forward-looking terminology, such as “anticipate,” “assume,” “believe,” “build,” “continue,” “create,” “design,” “estimate,” “expect,” “focus,” “forecast,” “future,” “goal,” “guidance,” “imply,” “intend,” “look,” “objective,” “opportunity,” “outlook,” “plan,” “position,” “potential,” “predict,” “project,” “prospective,” “pursue,” “seek,” “strategy,” “target,” “work,” “could,” “may,” “should,” “will,” “would” or the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion of future plans, actions or events identify forward-looking statements with respect to our business, strategy and plans, expectations relating to the Acquisitions (as defined herein) and future financial condition and performance. These statements speak only as of the date of this prospectus or the date of the document incorporated by reference, as applicable, and we undertake no ongoing obligation, other than that imposed by law, to update these statements. These statements appear in a number of places in this prospectus, including the documents incorporated by reference, and relate to, among other things, our intent, belief or current expectations of our directors or our officers with respect to: our future financial condition; results of operations or prospects; estimates of our economic mineral reserves; our business and growth strategies; and our financing plans and forecasts. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve significant risks and uncertainties, and that actual results may differ materially from those contained in or implied by the forward-looking statements as a result of various factors, some of which are unknown, including, without limitation:

•disruptions to our operations relating to the COVID-19 pandemic, including the heightened risk that a significant portion of our workforce or on-site contractors may suffer illness or otherwise be unable to perform their ordinary work functions;

•continued volatility of steel and iron ore market prices, which directly and indirectly impact the prices of the products that we sell to our customers;

•uncertainties associated with the highly competitive and cyclical steel industry and our reliance on the demand for steel from the automotive industry, which has been experiencing a trend toward light weighting that could result in lower steel volumes being consumed;

•potential weaknesses and uncertainties in global economic conditions, excess global steelmaking capacity, oversupply of iron ore, prevalence of steel imports and reduced market demand, including as a result of the COVID-19 pandemic;

•severe financial hardship, bankruptcy, temporary or permanent shutdowns or operational challenges, due to the COVID-19 pandemic or otherwise, of one or more of our major customers, including customers in the automotive market, key suppliers or contractors, which, among other adverse effects, could lead to reduced demand for our products, increased difficulty collecting receivables, and customers and/or suppliers asserting force majeure or other reasons for not performing their contractual obligations to us;

•risks related to U.S. government actions with respect to Section 232 of the Trade Expansion Act (as amended by the Trade Act of 1974), or Section 232, the United States-Mexico-Canada Agreement, or USMCA, and/or other trade agreements, tariffs, treaties or policies, as well as the uncertainty of obtaining and maintaining effective antidumping and countervailing duty orders to counteract the harmful effects of unfairly traded imports;

•impacts of existing and increasing governmental regulation, including climate change and other environmental regulation that may be proposed under the Biden Administration, and related costs and liabilities, including failure to receive or maintain required operating and environmental permits, approvals, modifications or other authorizations of, or from, any governmental or regulatory authority and costs related to implementing improvements to ensure compliance with regulatory changes, including potential financial assurance requirements;

•potential impacts to the environment or exposure to hazardous substances resulting from our operations;

•our ability to maintain adequate liquidity, our level of indebtedness and the availability of capital could limit cash flow necessary to fund working capital, planned capital expenditures, acquisitions, and other general corporate purposes or ongoing needs of our business;

•adverse changes in credit ratings, interest rates, foreign currency rates and tax laws;

•limitations on our ability to realize some or all of our deferred tax assets, including our net operating loss carryforwards, or NOLs;

•our ability to realize the anticipated synergies and benefits of the Acquisitions and to successfully integrate the businesses of AK Steel and ArcelorMittal USA into our existing businesses, including uncertainties associated with maintaining relationships with customers, vendors and employees;

•additional debt we assumed, incurred or issued in connection with the Acquisitions, as well as additional debt we incurred in connection with enhancing our liquidity during the COVID-19 pandemic, may negatively impact our credit profile and limit our financial flexibility;

•known and unknown liabilities we assumed in connection with the Acquisitions, including significant environmental, pension and other postretirement benefits, or OPEB, obligations;

•the ability of our customers, joint venture partners and third-party service providers to meet their obligations to us on a timely basis or at all;

•supply chain disruptions or changes in the cost or quality of energy sources or critical raw materials and supplies, including iron ore, industrial gases, graphite electrodes, scrap, chrome, zinc, coke and coal;

•liabilities and costs arising in connection with any business decisions to temporarily idle or permanently close a mine or production facility, which could adversely impact the carrying value of associated assets and give rise to impairment charges or closure and reclamation obligations, as well as uncertainties associated with restarting any previously idled mine or production facility;

•problems or disruptions associated with transporting products to our customers, moving products internally among our facilities or suppliers transporting raw materials to us;

•uncertainties associated with natural or human-caused disasters, adverse weather conditions, unanticipated geological conditions, critical equipment failures, infectious disease outbreaks, tailings dam failures and other unexpected events;

•our level of self-insurance and our ability to obtain sufficient third-party insurance to adequately cover potential adverse events and business risks;

•disruptions in, or failures of, our information technology, or IT, systems, including those related to cybersecurity;

•our ability to successfully identify and consummate any strategic investments or development projects, cost-effectively achieve planned production rates or levels, and diversify our product mix and add new customers;

•our actual economic iron ore and coal reserves or reductions in current mineral estimates, including whether we are able to replace depleted reserves with additional mineral bodies to support the long-term viability of our operations;

•the outcome of any contractual disputes with our customers, joint venture partners, lessors, or significant energy, raw material or service providers, or any other litigation or arbitration;

•our ability to maintain our social license to operate with our stakeholders, including by fostering a strong reputation and consistent operational and safety track record;

•our ability to maintain satisfactory labor relations with unions and employees;

•availability of workers to fill critical operational positions and potential labor shortages caused by the COVID-19 pandemic, as well as our ability to attract, hire, develop and retain key personnel, including within the acquired AK Steel and ArcelorMittal USA businesses;

•unanticipated or higher costs associated with pension and OPEB obligations resulting from changes in the value of plan assets or contribution increases required for unfunded obligations;

•potential significant deficiencies or material weaknesses in our internal control over financial reporting; and

•other risks described in our Annual Report on Form 10-K for the year ended December 31, 2020, and in the “Risk Factors” section of this prospectus.

These factors and the other risk factors described in this prospectus, including the documents incorporated by reference, are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors also could harm our results. Consequently, there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, us. Given these uncertainties, prospective investors are cautioned not to place undue reliance on such forward-looking statements.

SUMMARY

This summary highlights information about us, the Exchange Offer and the Exchange Notes. This summary is not complete and may not contain all of the information that you should consider prior to deciding whether to participate in the Exchange Offer. For a more complete understanding of us, we encourage you to read this prospectus, including the information incorporated by reference into this prospectus and the other documents to which we have expressly referred you. In particular, we encourage you to read the historical financial statements, and the related notes, incorporated by reference into this prospectus. Investing in the Exchange Notes involves significant risks, as described in the “Risk Factors” section.

Our Company

Cliffs is the largest flat-rolled steel producer in North America. Founded in 1847 as a mine operator, we are also the largest supplier of iron ore pellets in North America. In 2020, we acquired two major steelmakers, AK Steel and ArcelorMittal USA, vertically integrating our legacy iron ore business with quality-focused steel production and emphasis on the automotive end market. Our fully integrated portfolio includes custom-made pellets and hot briquetted iron; flat-rolled carbon steel, stainless, electrical, plate, tinplate and long steel products; as well as carbon and stainless steel tubing, hot and cold stamping and tooling. Headquartered in Cleveland, Ohio, we employ approximately 25,000 people across our mining, steel and downstream manufacturing operations in the United States and Canada.

On March 13, 2020, we completed the acquisition of AK Steel, or the AK Steel Merger, a leading producer of flat-rolled carbon, stainless and electrical steel products. These operations consist primarily of seven steelmaking and finishing plants, two cokemaking operations, three tube manufacturing plants and ten tooling and stamping operations. The businesses of Cleveland-Cliffs Tubular Components LLC (f/k/a AK Tube LLC) and PPHC Holdings, LLC and its subsidiaries acquired in the AK Steel Merger provide customer solutions with carbon and stainless steel tubing products, die design and tooling, and hot- and cold-stamped components.

On December 9, 2020, we completed the acquisition of ArcelorMittal USA pursuant to the terms of the Transaction Agreement, dated as of September 28, 2020, between Cleveland-Cliffs Inc. and ArcelorMittal S.A., a company organized under the laws of Luxembourg, or ArcelorMittal, and the former ultimate parent company of ArcelorMittal USA, and the associated ABL Amendment (as defined below), together, the AM USA Transaction. These operations include six steelmaking facilities, eight finishing facilities, two iron ore mining and pelletizing operations, one coal mining complex and three cokemaking operations. These assets build upon our existing high-end steelmaking and raw material capabilities, and also open up new markets to us. The combination provides us additional scale and technical capabilities necessary in a competitive and increasingly quality-focused marketplace.

We refer to the AK Steel Merger and AM USA Transaction, together, as the “Acquisitions.”

Recent Developments

On February 11, 2021, we sold 20 million of our common shares and the indirect, wholly owned subsidiary of ArcelorMittal to which approximately 78 million common shares were issued as part of the consideration paid by us in connection with the closing of the AM USA Transaction, as a selling shareholder, sold 40 million common shares, in each case at a price per share to the underwriter of $16.12, in an underwritten public offering, or the Equity Offering. We did not receive any proceeds from the sale of the common shares by the selling shareholder in the Equity Offering. On March 11, 2021, we used the net proceeds to us from the Equity Offering, plus cash on hand, to redeem $322 million aggregate principal amount of our outstanding 9.875% senior secured notes due 2025, or the 9.875% 2025 Senior Secured Notes.

On February 17, 2021, we issued $500 million aggregate principal amount of our 4.625% senior guaranteed notes due 2029, or the 4.625% 2029 Senior Notes, and $500 million aggregate principal amount of our 4.875% senior guaranteed notes due 2031, or the 4.875% 2031 Senior Notes, in an offering that was exempt from the registration requirements of the Securities Act, or the Notes Offering. On March 12, 2021, we used a portion of the net proceeds from the Notes Offering to redeem all of the outstanding 4.875% senior secured notes due 2024, or the 4.875% 2024 Senior Secured Notes, and 6.375% senior guaranteed notes due 2025, or the 6.375% 2025 Senior Notes, issued by Cleveland-Cliffs Inc. and all of the outstanding 7.625% senior notes due 2021, or the 7.625% 2021 AK Senior Notes, 7.50% senior notes due 2023, or the 7.50% 2023 AK Senior Notes, and 6.375% senior notes due 2025, or the 6.375% 2025 AK Senior Notes, issued by AK Steel Corporation (n/k/a Cleveland-Cliffs Steel Corporation), and pay fees and expenses in connection with such redemptions. We intend to use the remaining net proceeds from the Notes Offering to reduce borrowings under our ABL Facility (as defined herein).

We refer to the Equity Offering, the use of the net proceeds to us from the Equity Offering, plus cash on hand, to redeem $322 million aggregate principal amount of our 9.875% Senior Secured Notes on March 11, 2021, the Notes Offering and the use of the net proceeds from the Notes Offering to redeem all of the outstanding 4.875% 2024 Senior Secured Notes, 6.375% 2025 Senior Notes, 7.625% 2021 AK Senior Notes, 7.50% 2023 AK Senior Notes and 6.375% 2025 AK Senior Notes on March 12, 2021, and pay fees and expenses in connection with such redemptions, and reduce borrowings under our ABL Facility, collectively, as the “February 2021 Financing Transactions.”

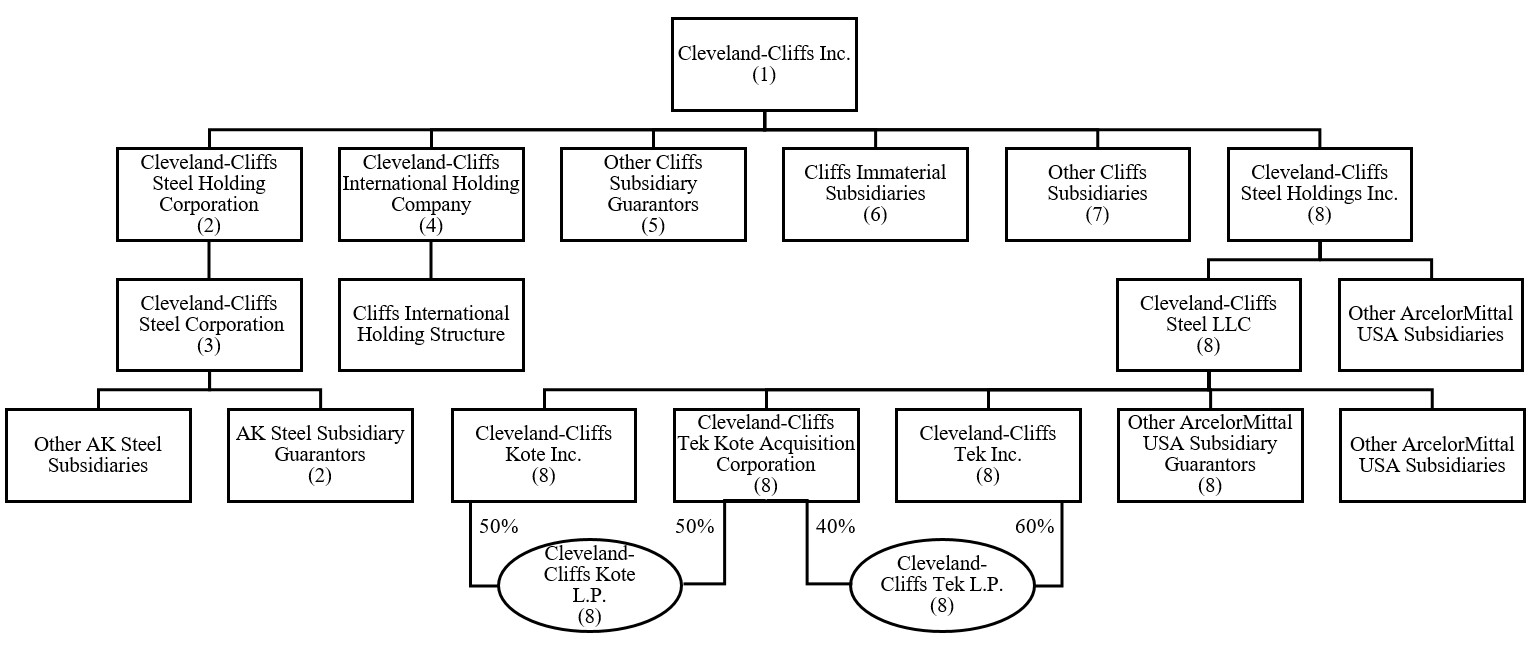

Our Structure

The following diagram illustrates Cliffs’ organizational structure as of the date of this prospectus. This diagram is provided for illustrative purposes only and does not show all legal entities or obligations of such entities.

(1) Issuer of the existing secured and unsecured senior notes issued by Cliffs, including the Original Notes, borrower under the ABL Facility and future issuer of the Exchange Notes. Cliffs’ 6.25% senior notes due 2040, or the 6.25% 2040 Senior Notes, and 1.50% convertible senior notes due 2025, or the 1.50% 2025 Convertible Senior Notes, are unsecured and are not guaranteed by any of Cliffs’ subsidiaries.

Cliffs’ 5.75% senior notes due 2025, or the 5.75% 2025 Senior Notes, the 9.875% 2025 Senior Secured Notes, Cliffs’ 6.75% senior secured notes due 2026, or the 6.75% 2026 Senior Secured Notes, Cliffs’ 5.875% senior guaranteed notes due 2027, or the 5.875% 2027 Senior Notes, the 4.625% 2029 Senior Notes, the 4.875% 2031 Senior Notes and the Original Notes are, and the Exchange Notes will be, guaranteed on a senior basis by each of Cliffs’ material direct and indirect wholly owned domestic subsidiaries, subject to certain exceptions. The ABL Facility is guaranteed by Cliffs’ material direct and indirect wholly owned domestic subsidiaries, subject to certain exceptions. See “Description of Other Indebtedness.”

(2) AK Steel and the following subsidiaries of AK Steel are guarantors of the 5.75% 2025 Senior Notes, the 9.875% 2025 Senior Secured Notes, the 6.75% 2026 Senior Secured Notes, the 5.875% 2027 Senior Notes, the 4.625% 2029 Senior Notes, the 4.875% 2031 Senior Notes, the Original Notes and the ABL Facility and will be guarantors of the Exchange Notes: Cleveland-Cliffs Steel Corporation (f/k/a AK Steel Corporation), Cleveland-Cliffs Steel Management Inc. (f/k/a AH Management, Inc.), Cleveland-Cliffs Investments Inc. (f/k/a AKS Investments, Inc.), Cleveland-Cliffs Steel Properties Inc. (f/k/a AK Steel Properties, Inc.), Cleveland-Cliffs Tubular Components LLC (f/k/a AK Tube LLC), Mountain State Carbon, LLC, PPHC Holdings, LLC, SNA Carbon, LLC, Cannon Automotive Solutions – Bowling Green, Inc., Fleetwood Metal Industries, LLC and Precision Partners Holding Company.

(3) Issuer of Cleveland-Cliffs Steel Corporation’s (f/k/a AK Steel Corporation) 7.00% senior notes due 2027, or the 7.00% 2027 AK Senior Notes, and guarantor of the 5.75% 2025 Senior Notes, the 9.875% 2025 Senior Secured Notes, the 6.75% 2026 Senior Secured Notes, the 5.875% 2027

Senior Notes, the 4.625% 2029 Senior Notes, the 4.875% 2031 Senior Notes, the Original Notes and the ABL Facility and will be a guarantor of the Exchange Notes.

(4) Cliffs’ foreign subsidiaries do not guarantee any of Cliffs’ existing notes, including the Original Notes, or the ABL Facility and will not guarantee the Exchange Notes. Cliffs’ main holding company for these foreign subsidiaries, Cleveland-Cliffs International Holding Company, will also not provide a guarantee so long as substantially all of its assets consist of equity interests in one or more foreign subsidiaries. Also, any pledge of Cleveland-Cliffs International Holding Company voting stock will be limited to 65% of the voting equity interests in Cleveland-Cliffs International Holding Company.

(5) The following subsidiaries of Cliffs are guarantors of the 5.75% 2025 Senior Notes, the 9.875% 2025 Senior Secured Notes, the 6.75% 2026 Senior Secured Notes, the 5.875% 2027 Senior Notes, the 4.625% 2029 Senior Notes, the 4.875% 2031 Senior Notes, the Original Notes and the ABL Facility and will be guarantors of the Exchange Notes: Cliffs Mining Company, Cliffs Minnesota Mining Company, Cliffs TIOP Holding, LLC, Cliffs TIOP, Inc., Cliffs TIOP II, LLC, Cliffs UTAC Holding LLC, IronUnits LLC, Lake Superior & Ishpeming Railroad Company, Metallics Sales Company, Northshore Mining Company, Silver Bay Power Company, The Cleveland-Cliffs Iron Company, Tilden Mining Company L.C. and United Taconite LLC. Each of the foregoing subsidiaries of Cliffs are included in Cliffs’ historical consolidated financial data for all periods presented within this prospectus and in the documents incorporated by reference herein.

(6) Immaterial subsidiaries are limited to Cliffs’ direct and indirect subsidiaries that do not have consolidated total assets or consolidated total revenues in excess of 3.0% (5.0% with respect to the 4.625% 2029 Senior Notes and the 4.875% 2031 Senior Notes) of the consolidated total assets or consolidated total revenues of Cliffs and its subsidiaries as of the most recent balance sheet date or for the most recent four-quarter period, respectively, provided that all immaterial subsidiaries taken together may not have consolidated total assets or consolidated total revenues in excess of 7.5% (10.0% with respect to the 4.625% 2029 Senior Notes and the 4.875% 2031 Senior Notes) of the consolidated total assets or consolidated total revenues, respectively, of Cliffs and its subsidiaries. Immaterial subsidiaries do not guarantee any of Cliffs’ existing notes, including the Original Notes, or the ABL Facility and will not guarantee the Exchange Notes.

(7) Other non-guarantor subsidiaries are limited to (a) Cliffs’ non-wholly owned subsidiaries to the extent the organizational documents (e.g., joint venture or shareholder agreements) of such subsidiaries prohibit such guarantee and (b) Cliffs’ indirect subsidiary, Wabush Iron Co. Limited.

(8) Cleveland-Cliffs Steel Holdings Inc., which was formed in connection with the AM USA Transaction to be Cliffs’ main holding company for the entities that compose ArcelorMittal USA, and the following subsidiaries of Cleveland-Cliffs Steel Holdings Inc. are guarantors of the 5.75% 2025 Senior Notes, the 9.875% 2025 Senior Secured Notes, the 6.75% 2026 Senior Secured Notes, the 5.875% 2027 Senior Notes, the 4.625% 2029 Senior Notes, the 4.875% 2031 Senior Notes, the Original Notes and the ABL Facility and will be guarantors of the Exchange Notes: Cleveland-Cliffs Steel LLC (f/k/a ArcelorMittal USA LLC), Cleveland-Cliffs Burns Harbor LLC (f/k/a ArcelorMittal Burns Harbor LLC), Cleveland-Cliffs Cleveland Works LLC (f/k/a ArcelorMittal Cleveland LLC), Cleveland-Cliffs Columbus LLC (f/k/a ArcelorMittal Columbus LLC), Cleveland-Cliffs Kote Inc. (f/k/a ArcelorMittal Kote Inc.), Cleveland-Cliffs Kote L.P. (f/k/a I/N Kote L.P.), Cleveland-Cliffs Minorca Mine Inc. (f/k/a ArcelorMittal Minorca Mine Inc.), Cleveland-Cliffs Monessen Coke LLC (f/k/a ArcelorMittal Monessen LLC), Cleveland-Cliffs Plate LLC (f/k/a ArcelorMittal Plate LLC), Cleveland-Cliffs Railways Inc. (f/k/a Mittal Steel USA — Railways Inc.), Cleveland-Cliffs Riverdale LLC (f/k/a ArcelorMittal Riverdale LLC), Cleveland-Cliffs South Chicago & Indiana Harbor Railway Inc. (f/k/a ArcelorMittal South Chicago & Indiana Harbor Railway Inc.), Cleveland-Cliffs Steelton LLC (f/k/a ArcelorMittal Steelton LLC), Cleveland-Cliffs Steelworks Railway Inc. (f/k/a ArcelorMittal Cleveland Works Railway Inc.), Cleveland-Cliffs Tek Inc. (f/k/a ArcelorMittal Tek Inc.), Cleveland-Cliffs Tek Kote Acquisition Corporation (f/k/a Tek Kote

Acquisition Corporation), Cleveland-Cliffs Tek L.P. (f/k/a I/N Tek L.P.), Cleveland-Cliffs Weirton LLC (f/k/a ArcelorMittal Weirton LLC) and Mid-Vol Coal Sales, Inc. For summarized financial information regarding the entities that compose ArcelorMittal USA, see Cliffs’ Current Report on Form 8-K/A filed with the SEC on February 8, 2021, which is incorporated by reference herein.

Corporate Information

Our principal executive offices are located at 200 Public Square, Suite 3300, Cleveland, Ohio 44114-2315. Our main telephone number is (216) 694-5700, and our website address is www.clevelandcliffs.com. The information contained on or accessible through our website is not part of this prospectus, other than the documents that we file with the SEC that are specifically incorporated by reference into this prospectus.

The Exchange Offer

The following summary contains basic information about the Exchange Offer and is not intended to be complete. It does not contain all the information that may be important to you. For a more complete understanding of the Exchange Offer, including for the meanings of capitalized terms not otherwise defined below, please refer to “The Exchange Offer.”

| | | | | |

| The Exchange Offer | We are offering to exchange up to $73,298,000 aggregate principal amount of our registered 7.00% senior guaranteed notes due 2027, which we refer to herein as the Exchange Notes, for an equal principal amount of our outstanding restricted 7.00% senior guaranteed notes due 2027 issued in a private transaction exempt from the registration requirements of the Securities Act on March 16, 2020, which we refer to herein as the Original Notes. We refer herein to the Original Notes and the Exchange Notes, collectively, as the Notes. We refer herein to the offer to exchange as the Exchange Offer. The terms of the Exchange Notes will be substantially identical to the terms of the Original Notes, except that the Exchange Notes will be registered under the Securities Act and the transfer restrictions and registration rights and related additional interest provisions applicable to the Original Notes will not apply to the Exchange Notes. The Exchange Notes will be part of the same series as the Original Notes and will be issued under the same indenture. Holders of Original Notes do not have any appraisal or dissenters’ rights in connection with the Exchange Offer. |

| Purpose of the Exchange Offer | The Exchange Notes are being offered to satisfy our obligations under the registration rights agreement entered into at the time we issued and sold the Original Notes. |

| Expiration Date; Withdrawal of Tenders; Return of Original Notes Not Accepted for Exchange | The Exchange Offer will expire at 5:00 p.m., New York City time, on April 22, 2021 or on a later date and time to which we extend it. We refer to such time and date as the Expiration Date. Tenders of Original Notes in the Exchange Offer may be withdrawn at any time prior to the Expiration Date. We will exchange the Exchange Notes for validly tendered Original Notes promptly following the Expiration Date. We refer to such date of exchange as the Exchange Date. Any Original Notes that are not accepted for exchange for any reason will be returned by us, at our expense, to the tendering holder promptly after the expiration or termination of the Exchange Offer. |

| | | | | |

| Procedures for Tendering Original Notes | Each holder of Original Notes wishing to participate in the Exchange Offer must follow procedures of The Depository Trust Company’s, or DTC, Automated Tender Offer Program, or ATOP, subject to the terms and procedures of that program. The ATOP procedures require that the exchange agent receives, prior to the Expiration Date, a computer-generated message known as an “agent’s message” that is transmitted through ATOP and pursuant to which DTC confirms that: •DTC has received instructions to exchange your Original Notes; and •you agree to be bound by the terms of the letter of transmittal. See “The Exchange Offer—Procedures for Tendering Original Notes.” |

| Consequences of Failure to Exchange Original Notes | You will continue to hold Original Notes, which will remain subject to their existing transfer restrictions, if you do not validly tender your Original Notes or you tender your Original Notes and they are not accepted for exchange. With some limited exceptions, we will have no obligation to register the Original Notes after we consummate the Exchange Offer. See “The Exchange Offer—Terms of the Exchange Offer” and “The Exchange Offer—Consequences of Failure to Exchange.” |

| Conditions to the Exchange Offer | The Exchange Offer is not conditioned upon any minimum aggregate principal amount of Original Notes being tendered or accepted for exchange. The Exchange Offer is subject to customary conditions, which may be waived by us in our discretion. We currently expect that all of the conditions will be satisfied and that no waivers will be necessary. See “The Exchange Offer—Conditions to the Exchange Offer.” |

| Exchange Agent | U.S. Bank National Association |

| Certain U.S. Federal Income Tax Considerations | As described in “Certain U.S. Federal Income Tax Considerations,” the exchange of an Original Note for an Exchange Note pursuant to the Exchange Offer will not constitute a taxable exchange and will not result in any taxable income, gain or loss for U.S. federal income tax purposes, and immediately after the exchange, a holder will have the same adjusted tax basis and holding period in each Exchange Note received as such holder had immediately prior to the exchange in the corresponding Original Note surrendered. |

| Risk Factors | You should carefully read and consider the risk factors beginning on page 18 of this prospectus before deciding whether to participate in the Exchange Offer. |

The Exchange Notes

The following is a brief summary of the principal terms of the Exchange Notes and is provided solely for your convenience. It is not intended to be complete. For a more detailed description of the Exchange Notes, see “Description of the Notes.”

| | | | | |

| Issuer | Cleveland-Cliffs Inc. |

| Securities Offered | Up to $73,298,000 aggregate principal amount of Exchange Notes. |

| Maturity Date | March 15, 2027. |

| Interest Rate | The Exchange Notes will bear interest at 7.00% per year. |

| Accrual of Interest | The Exchange Notes will accrue interest from (and including) the most recent date on which interest has been paid on the Original Notes accepted in the Exchange Offer. |

| Interest Payment Dates | Interest will be payable in cash on March 15 and September 15 of each year, commencing on September 15, 2021. If the record date for the first interest payment date occurs on or prior to the Exchange Date, the record date for the first interest payment date will be deemed the close of business on the business day immediately prior to such interest payment date. |

| Optional Redemption | We may redeem any of the Notes beginning on March 15, 2022. The initial redemption price is 103.500% of their principal amount, plus accrued and unpaid interest, if any, to, but excluding, the redemption date. The redemption price will decline each year after 2022 and will be 100% of their principal amount, plus accrued interest, beginning on March 15, 2025. We may also redeem some or all of the Notes at any time and from time to time prior to March 15, 2022 at a redemption price equal to 100% of the principal amount thereof plus a “make-whole” premium, plus accrued and unpaid interest, if any, to, but excluding, the redemption date. See “Description of the Notes—Optional Redemption.” |

| Change of Control | Upon certain change of control triggering events, we will be required to make an offer to purchase the Notes. The purchase price will equal 101% of the principal amount of the Notes on the date of purchase plus accrued and unpaid interest, if any, to, but excluding, the date of repurchase. We may not have sufficient funds available at the time of any change of control triggering event to make any required debt repayment (including repurchases of the Notes). See “Risk Factors—Risks Relating to the Notes—We may not be able to repurchase the Notes upon a change of control triggering event.” |

| | | | | |

| Ranking | The Exchange Notes and the related guarantees: •will be general unsecured senior obligations of Cliffs and the Guarantors; •will rank equally in right of payment with all existing and future senior unsecured indebtedness of Cliffs and the Guarantors (including the Original Notes), and any guarantees thereof by the Guarantors; •will rank senior in right of payment to all existing and future subordinated indebtedness of Cliffs and the Guarantors; •will be effectively subordinated to Cliffs’ and the Guarantors’ existing and future secured indebtedness to the extent of the value of the assets securing such indebtedness; •will be structurally senior to existing and future indebtedness of Cliffs that is not guaranteed by each Guarantor; and •will be structurally subordinated to all existing and future indebtedness and other liabilities of subsidiaries of Cliffs that do not guarantee the Notes. On a pro forma basis, after giving effect to the Acquisitions, and on a continuing operations basis, our non-Guarantor subsidiaries would have accounted for 3% of our consolidated revenue and approximately 15% of our consolidated net loss for the year ended December 31, 2020. As of December 31, 2020, on an as adjusted basis, after giving effect to the February 2021 Financing Transactions and our borrowing of an additional $260 million under our ABL Facility since December 31, 2020 in connection with the termination of ArcelorMittal USA’s accounts receivable factoring arrangement, our non-Guarantor subsidiaries would have accounted for approximately 9% of our consolidated assets and less than 1% of our consolidated long-term debt. |

| Certain Covenants | The indenture governing the Notes contains covenants that, among other things, limit Cliffs’ and its subsidiaries’ ability to: •create liens on our property that secure indebtedness; •enter into certain sale and leaseback transactions; and •merge, consolidate or amalgamate with another company. These covenants are subject to a number of important limitations and exceptions. See “Description of the Notes—Certain Covenants.” |

| Use of Proceeds | We will not receive any cash proceeds from the issuance of the Exchange Notes. See “Use of Proceeds.” |

| Governing Law | The Notes, the guarantees thereof and the indenture governing the Notes are governed by the laws of the State of New York. |

| Trustee, Registrar and Paying Agent | U.S. Bank National Association. |

| Risk Factors | See “Risk Factors” and other information in this prospectus for a discussion of factors that should be carefully considered by the holders of the Original Notes before tendering their Original Notes in the Exchange Offer and investing in the Exchange Notes. |

Summary Historical Consolidated Financial Data of Cliffs

The table below sets forth our summary historical consolidated financial and other statistical data for the periods presented. We derived the summary historical consolidated financial data and other statistical data as of December 31, 2020 and 2019 and for the years ended December 31, 2020, 2019 and 2018 from our audited consolidated financial statements, which are incorporated by reference into this prospectus. The summary historical consolidated financial data and other statistical data as of December 31, 2018 are derived from our audited consolidated financial statements, which are not incorporated by reference into this prospectus. Summary historical consolidated financial and other statistical data should be read in conjunction with our consolidated financial statements, the related notes and other financial information incorporated by reference into this prospectus.

The information set forth below is not necessarily indicative of future results and should be read together with the other information contained in Cliffs’ Annual Report on Form 10-K for the year ended December 31, 2020, including the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the consolidated financial statements and accompanying notes included in the reports incorporated by reference into this prospectus.

| | | | | | | | | | | | | | | | | |

| (In Millions, except per share amounts) |

| Year Ended December 31, |

| 2020(a) | | 2019 | | 2018(b) |

| Financial data | | | | | |

| Revenues | $ | 5,319 | | | $ | 1,990 | | | $ | 2,332 | |

| Realization of deferred revenue | $ | 35 | | | $ | — | | | $ | — | |

| Income (loss) from continuing operations | $ | (82) | | | $ | 295 | | | $ | 1,040 | |

| Income (loss) from discontinued operations, net of tax | $ | 1 | | | $ | (2) | | | $ | 88 | |

| Earnings (loss) per common share attributable to Cliffs common shareholders – basic | | | | | |

| Continuing operations | $ | (0.32) | | | $ | 1.07 | | | $ | 3.50 | |

| Discontinued operations | — | | | (0.01) | | | 0.30 | |

Earnings (loss) per common share

attributable to Cliffs common

shareholders – basic | $ | (0.32) | | | $ | 1.06 | | | $ | 3.80 | |

| Earnings (loss) per common share attributable to Cliffs common shareholders – diluted | | | | | |

| Continuing operations | $ | 0.32 | | | $ | 1.04 | | | $ | 3.42 | |

| Discontinued operations | — | | | (0.01) | | | 0.29 | |

Earnings (loss) per common share

attributable to Cliffs common

shareholders – diluted | $ | 0.32 | | | $ | 1.03 | | | $ | 3.71 | |

| Total assets | $ | 16,771 | | | $ | 3,504 | | | $ | 3,530 | |

Long-term debt obligations

(including finance leases) | $ | 5,634 | | | $ | 2,145 | | | $ | 2,105 | |

| | | | | | | | | | | | | | | | | |

| (In Millions, except per share amounts) |

| Year Ended December 31, |

| 2020(a) | | 2019 | | 2018(b) |

| Financial data (continued) | | | | | |

| Cash dividends declared to common shareholders | | | | | |

| - Per share | $ | 0.06 | | | $ | 0.27 | | | $ | 0.05 | |

| - Total | $ | 25 | | | $ | 75 | | | $ | 15 | |

| Repurchases of common shares | $ | — | | | $ | (253) | | | $ | (48) | |

| Common shares outstanding – basic (millions) | | | | | |

| - Average for period | 379 | | 277 | | 297 |

| - At period-end | 478 | | 270 | | 293 |

| | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, |

| 2020(a) | | 2019 | | 2018(b) |

| Sales statistics | | | | | |

| Third-Party Sales tonnage | | | | | |

| - Steel (net tons) | 3.8 | | — | | — |

| - Iron Ore (long tons) | 11.7 | | 18.6 | | 20.6 |

| | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, |

| 2020(a) | | 2019 | | 2018(b) |

| Reconciliation of Net Income to EBITDA to Total Cliffs Adjusted EBITDA | | | | | |

| Net income (loss) | $ | (81) | | | $ | 293 | | | $ | 1,128 | |

| Less: | | | | | |

| Interest expense, net | (238) | | | (101) | | | (121) | |

| Income tax benefit (expense) | 111 | | | (18) | | | 460 | |

| Depreciation, depletion and amortization | (308) | | | (85) | | | (89) | |

| Total EBITDA | $ | 354 | | | $ | 497 | | | $ | 878 | |

| Less: | | | | | |

| EBITDA of noncontrolling interests | $ | 56 | | | $ | — | | | $ | — | |

| Impact of discontinued operations | 1 | | | (1) | | | 121 | |

| Gain (loss) on extinguishment of debt | 130 | | | (18) | | | (7) | |

| Severance costs | (38) | | | (2) | | | — | |

| Acquisition-related costs | (52) | | | (7) | | | — | |

| Amortization of inventory step-up | (96) | | | — | | | — | |

| Foreign exchange remeasurement | — | | | — | | | (1) | |

| Impairment of long-lived assets | — | | | — | | | (1) | |

| Total Cliffs Adjusted EBITDA | $ | 353 | | | $ | 525 | | | $ | 766 | |

(a)During 2020, Cliffs completed the AK Steel Merger on March 13, 2020 and the AM USA Transaction on December 9, 2020. Results for 2020 include the results subsequent to the respective acquisition dates.

(b)During 2018, Cliffs recorded an income tax benefit of $475 million, primarily related to the release of the valuation allowance in the U.S. Additionally, on January 1, 2018, Cliffs adopted Accounting Standards Codification, or ASC, Topic 606, Revenue from Contracts with Customers, or ASC Topic 606, and applied it to all contracts that were not completed using the modified retrospective method. Cliffs recognized the cumulative effect of initially applying ASC Topic 606 as an adjustment of $34 million to the opening balance of retained deficit.

Summary Historical Financial Data of ArcelorMittal USA LLC and Affiliates

The table below sets forth summary historical financial data of ArcelorMittal USA LLC and other former wholly owned subsidiaries of ArcelorMittal that were acquired by Cliffs in connection with the AM USA Transaction as of and for (i) the years ended December 31, 2019 and 2018 and (ii) the nine months ended September 30, 2020 and 2019. The summary historical condensed combined consolidated financial data as of and for each of the years ended December 31, 2019 and 2018 have been derived from audited combined consolidated financial statements for “ArcelorMittal USA LLC and Affiliates,” which are incorporated by reference into this prospectus. The summary historical condensed combined consolidated financial data as of September 30, 2020 and for the nine months ended September 30, 2020 and 2019 have been derived from unaudited condensed combined consolidated financial statements for “ArcelorMittal USA LLC and Affiliates,” which are incorporated by reference herein. The interim unaudited financial data have been prepared on the same basis as the audited financial data and include, in the opinion of management, all adjustments, consisting of normal and recurring adjustments, necessary to present fairly the data for such periods and may not necessarily be indicative of full-year results.

The information set forth below is not necessarily indicative of future results and should be read together with the consolidated financial statements and accompanying notes included in the reports incorporated by reference into this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions, except as otherwise noted) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Statement of Operations Data | | | | | | | |

| Net sales | $ | 10,169 | | | $ | 11,334 | | | $ | 5,629 | | | $ | 8,001 | |

| Operating income (loss) | (126) | | | 613 | | | (725) | | | 63 | |

| Net income (loss) | (79) | | | 585 | | | (702) | | | 54 | |

| | | | | | | |

| Other Data | | | | | | | |

| Total flat-rolled shipments (in thousands of net tons) | 11,220 | | | 12,040 | | | 7,234 | | | 8,588 | |

| Selling price per flat-rolled net ton (in dollars) | $ | 774 | | | $ | 828 | | | $ | 662 | | | $ | 800 | |

| Total other steel shipments (in thousands of net tons) | 1,310 | | | 1,128 | | | 837 | | | 990 | |

| | | | | | | |

| Balance Sheet Data | | | | | | | |

| Total assets | $ | 9,398 | | | $ | 9,703 | | | $ | 8,380 | | | |

| Long-term debt | — | | | — | | | — | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Reconciliation of Adjusted EBITDA | | | | | | | |

| Net income attributable to ArcelorMittal USA | $ | (79) | | | $ | 585 | | | $ | (702) | | | $ | 54 | |

| Less: | | | | | | | |

| Interest and other financing expense, third party | (100) | | | (104) | | | (50) | | | (81) | |

| Interest income, related party | 146 | | | 137 | | | 103 | | | 110 | |

| Interest income, third party | 7 | | | 4 | | | 1 | | | 6 | |

| Benefit (provision) for income taxes | 53 | | | (2) | | | 3 | | | — | |

| Depreciation and amortization | (359) | | | (356) | | | (309) | | | (262) | |

| EBITDA | 174 | | | 906 | | | (450) | | | 281 | |

| Less: | | | | | | | |

| Derivative timing adjustment | 37 | | | 77 | | | 10 | | | 26 | |

| IFA fee & misc. corporate chargebacks (a) | (129) | | | (154) | | | (98) | | | (104) | |

| Asset impairments | (21) | | | — | | | (26) | | | — | |

| Onerous contracts | (21) | | | 2 | | | (3) | | | (59) | |

| Adjusted EBITDA | $ | 308 | | | $ | 981 | | | $ | (333) | | | $ | 418 | |

(a)The impact of reversal of the fees charged for management, financial and legal services, and research and development under the Industrial Franchise Agreement, dated January 1, 2015, between ArcelorMittal USA LLC and its former parent, or the Industrial Franchise Agreement, net of income from right to use intellectual property.

Summary Historical Financial Data of I/N Kote

The table below sets forth summary historical financial data of I/N Kote as of and for (i) the years ended December 31, 2019 and 2018 and (ii) the nine months ended September 30, 2020 and 2019. The summary historical financial data as of and for each of the years ended December 31, 2019 and 2018 have been derived from audited financial statements for “I/N Kote,” which are incorporated by reference into this prospectus. The summary historical financial data as of September 30, 2020 and for the nine months ended September 30, 2020 and 2019 have been derived from unaudited condensed financial statements for “I/N Kote,” which are incorporated by reference herein. The interim unaudited financial data have been prepared on the same basis as the audited financial data and include, in the opinion of management, all adjustments, consisting of normal and recurring adjustments, necessary to present fairly the data for such periods and may not necessarily be indicative of full-year results.

The information set forth below is not necessarily indicative of future results and should be read together with the financial statements and accompanying notes included in the reports incorporated by reference into this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions, except as otherwise noted) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Statement of Operations Data | | | | | | | |

| Net sales | $ | 498 | | | $ | 553 | | | $ | 265 | | | $ | 365 | |

| Operating income | 38 | | | 41 | | | 21 | | | 30 | |

| Net income | 38 | | | 41 | | | 21 | | | 29 | |

| | | | | | | |

| Other Data | | | | | | | |

| Total flat-rolled shipments (in thousands of net tons) | 490 | | | 567 | | | 288 | | | 375 | |

| Selling price per flat-rolled net ton (in dollars) | $ | 1,017 | | | $ | 976 | | | $ | 920 | | | $ | 973 | |

| | | | | | | |

| Balance Sheet Data | | | | | | | |

| Total assets | $ | 210 | | | $ | 221 | | | $ | 248 | | | |

| Long-term debt (a) | 15 | | | 17 | | | 10 | | | |

(a)Includes the current portion of long-term debt.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Reconciliation of Adjusted EBITDA | | | | | | | |

| Net income attributable to I/N Kote | $ | 38 | | | $ | 41 | | | $ | 21 | | | $ | 29 | |

| Less: | | | | | | | |

| Interest expense, net | — | | | — | | | — | | | — | |

| Income tax expense | — | | | — | | | — | | | — | |

| Depreciation and amortization | (6) | | | (7) | | | (4) | | | (4) | |

| EBITDA | $ | 44 | | | $ | 48 | | | $ | 25 | | | $ | 33 | |

| Adjusted EBITDA (a) | $ | 44 | | | $ | 48 | | | $ | 25 | | | $ | 33 | |

(a)All adjustments to EBITDA are nil.

Summary Historical Financial Data of I/N Tek

The table below sets forth summary historical financial data of I/N Tek as of and for (i) the years ended December 31, 2019 and 2018 and (ii) the nine months ended September 30, 2020 and 2019. The summary historical financial data as of and for each of the years ended December 31, 2019 and 2018 have been derived from audited financial statements for “I/N Tek,” which are incorporated by reference into this prospectus. The summary historical financial data as of September 30, 2020 and for the nine months ended September 30, 2020 and 2019 have been derived from unaudited condensed financial statements for “I/N Tek,” which are incorporated by reference herein. The interim unaudited financial data have been prepared on the same basis as the audited financial data and include, in the opinion of management, all adjustments, consisting of normal and recurring adjustments, necessary to present fairly the data for such periods and may not necessarily be indicative of full-year results.

The information set forth below is not necessarily indicative of future results and should be read together with the financial statements and accompanying notes included in the reports incorporated by reference into this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions, except as otherwise noted) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Statement of Operations Data | | | | | | | |

| Net sales | $ | 167 | | | $ | 168 | | | $ | 108 | | | $ | 124 | |

| Operating income | 68 | | | 65 | | | 44 | | | 50 | |

| Net income | 66 | | | 63 | | | 44 | | | 49 | |

| | | | | | | |

| Other Data | | | | | | | |

| Total flat-rolled shipments (in thousands of net tons) | 1,319 | | | 1,428 | | | 733 | | | 1,003 | |

| Selling price per flat-rolled net ton (in dollars) | $ | 127 | | | $ | 117 | | | $ | 147 | | | $ | 123 | |

| | | | | | | |

| Balance Sheet Data | | | | | | | |

| Total assets | $ | 169 | | | $ | 160 | | | $ | 166 | | | |

| Long-term debt (a) | 38 | | | 42 | | | 26 | | | |

(a)Includes the current portion of long-term debt.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, | | Nine Months Ended September 30, |

| 2019 | | 2018 | | 2020 | | 2019 |

| Reconciliation of Adjusted EBITDA | | | | | | | |

| Net income attributable to I/N Tek | $ | 66 | | | $ | 63 | | | $ | 44 | | | $ | 49 | |

| Less: | | | | | | | |

| Interest expense, net | (1) | | | (1) | | | — | | | (1) | |

| Income tax benefit (expense) | — | | | — | | | — | | | — | |

| Depreciation and amortization | (9) | | | (9) | | | (6) | | | (6) | |

| EBITDA | 76 | | | 73 | | | 50 | | | 56 | |

| Adjusted EBITDA (a) | $ | 76 | | | $ | 73 | | | $ | 50 | | | $ | 56 | |

(a)All adjustments to EBITDA are nil.

Summary Unaudited Pro Forma Condensed Combined Financial Data

The following table presents summary unaudited pro forma condensed combined financial data of Cliffs after giving effect to the Acquisitions, which is referred to as the “summary pro forma financial data.” The information under “Pro Forma Statements of Income Data” and “Pro Forma Adjusted EBITDA” in the tables below gives effect to the Acquisitions as if they had been consummated on January 1, 2020, the beginning of the earliest period for which unaudited pro forma condensed combined financial data have been presented. This pro forma financial data was prepared using the acquisition method of accounting with Cliffs considered the accounting acquirer in each of the Acquisitions.

The summary pro forma financial data reflects preliminary pro forma adjustments that have been made solely for the purpose of providing the summary pro forma financial data presented in this prospectus. Cliffs estimated the fair value of AK Steel’s and ArcelorMittal USA’s assets and liabilities based on discussions with AK Steel’s and ArcelorMittal USA’s management, due diligence information, preliminary valuation analyses performed by a third-party specialist and reviewed by Cliffs, information presented in AK Steel’s SEC filings and other publicly available information. As a result of the foregoing, the pro forma adjustments are preliminary and are subject to change as additional information becomes available and as additional analysis is performed.

Any changes in the fair values of the net assets or total purchase consideration as compared with the information shown in the pro forma financial data may change the amount of the total purchase consideration allocated to goodwill and other assets and liabilities and may impact the combined company statements of income due to adjustments in depreciation and amortization of the adjusted assets or liabilities and related deferred income tax effects. The final purchase consideration allocation may be materially different than the preliminary purchase consideration allocation presented in the pro forma financial data.

The information presented below should be read in conjunction with the historical financial statements and related notes incorporated by reference into this prospectus, and with the unaudited pro forma condensed combined financial statements of Cliffs, including the related notes, incorporated by reference into this prospectus. The unaudited pro forma condensed combined financial statements are presented for illustrative purposes only and are not necessarily indicative of results that actually would have occurred or that may occur in the future had the Acquisitions been completed on the dates indicated, or of the future operating results or financial position of the combined company following the Acquisitions. Future results may vary significantly from the results reflected because of various factors, including those discussed in the section entitled “Risk Factors.”

| | | | | |

| (In Millions, except per share amounts) |

| Year Ended December 31, 2020 |

| Pro Forma Statements of Income Data: | |

| Revenues from product sales and services | $ | 12,837 | |

| Loss from continuing operations | $ | (820) | |

| Income from discontinued operations, net of tax | $ | 1 | |

| Earnings (loss) per common share attributable to common shareholders | |

| Basic | $ | (1.82) | |

| Diluted | $ | (1.82) | |

| Cash dividends declared to common shareholders (a) | N/A |

| Cash dividends declared to preferred shareholders (a) | N/A |

(a)Pro forma dividends per share data is not presented, as the dividend per share for the combined company will be determined by the board of directors of the combined company.

The following table reconciles pro forma net income to Pro Forma Adjusted EBITDA.

| | | | | |

| (In Millions) |

| Pro Forma Year Ended December 31, 2020 |

| Pro Forma Adjusted EBITDA: | |

| Net income (loss) | $ | (819) | |

| Less: | |

| Interest expense, net | (317) | |

| Income tax benefit | 439 | |

| Depreciation, depletion and amortization | (593) | |

| EBITDA | (348) | |

| Less: | |

| EBITDA of noncontrolling interests | 65 | |

| Asset impairments | (26) | |

| Impact of discontinued operations | 1 | |

| Gain (loss) on extinguishment of debt | 130 | |

| Inventory step-up | (362) | |

| Onerous contracts | (42) | |

| Acquisition-related costs | (55) | |

| Severance costs | (50) | |

| Pro Forma Adjusted EBITDA | (9) | |

| Expected synergies not already realized | 242 | |

| Pro Forma Adjusted EBITDA (inclusive of expected synergies) | $ | 233 | |

RISK FACTORS

The terms of the Exchange Notes will be identical in all material respects to those of the Original Notes, except for the transfer restrictions and registration rights and related additional interest provisions relating to the Original Notes that will not apply to the Exchange Notes. You should carefully consider the risks described below and all of the information contained in and incorporated by reference into this prospectus before making a decision on whether or not to participate in the Exchange Offer. In addition, you should carefully consider, among other things, the matters discussed under “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2020. If any of those risks actually occurs, our business, financial condition and results of operations could suffer. The risks discussed below also include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements. See “Disclosure Regarding Forward-Looking Statements” in this prospectus.

Risks Relating to the Notes

Our existing and future indebtedness may limit cash flow available to invest in the ongoing needs of our business, which could prevent us from fulfilling our obligations under the Notes.

As of December 31, 2020, on an as adjusted basis, after giving effect to the February 2021 Financing Transactions and our borrowing of an additional $260 million under our ABL Facility since December 31, 2020 in connection with the termination of ArcelorMittal USA’s accounts receivable factoring arrangement, we would have had approximately $5.4 billion of indebtedness outstanding, approximately $2.8 billion of which would have been secured indebtedness (excluding $247 million of outstanding letters of credit and $335 million of finance leases), and approximately $79 million of cash on our balance sheet. In addition, on an as adjusted basis, after giving effect to the February 2021 Financing Transactions and our borrowing of an additional $260 million under our ABL Facility since December 31, 2020 in connection with the termination of ArcelorMittal USA’s accounts receivable factoring arrangement, we would have had up to $1.3 billion of committed borrowing capacity, subject to a borrowing base limitation and less letters of credit expected to be outstanding, under our ABL Facility. Our level of indebtedness could have important consequences to you. For example, it could:

•require us to dedicate a substantial portion of our cash flow from operations to the payment of debt service, reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes;

•increase our vulnerability to adverse economic or industry conditions;

•limit our ability to obtain additional financing in the future to enable us to react to changes in our business;

•place us at a competitive disadvantage compared to businesses in our industry that have less indebtedness; or

•limit our ability to pay dividends on or purchase or redeem our capital stock.

Our liquidity needs could vary significantly and may be affected by general economic conditions, industry trends, performance and many other factors not within our control. If we are unable to generate sufficient cash flow from operations in the future to service our debt, we may be required to refinance all or a portion of our existing debt. However, we may not be able to obtain any such new or additional debt on favorable terms or at all.

Additionally, any failure to comply with covenants in the instruments governing our debt could result in an event of default, which, if not cured or waived, would have a material adverse effect on us.

Despite our current debt levels, we and our subsidiaries may still incur significant additional debt, and the indenture governing the Notes does not restrict our ability to engage in other transactions that may adversely affect holders of the Notes.

The indenture governing the Notes does not limit the amount of unsecured debt that we may incur and only limits the amount of secured debt that we may incur. Accordingly, we and our subsidiaries may be able to incur substantial additional debt, including a limited amount of secured debt, in the future. The indenture also does not prevent us from incurring certain other liabilities that do not constitute debt (as defined in the indenture). Non-Guarantor subsidiaries, which include our foreign subsidiaries and certain excluded domestic subsidiaries, may incur additional debt in accordance with the indenture, which debt (as well as other liabilities at any such subsidiary) would be structurally senior to the Notes. As of December 31, 2020, on an as adjusted basis, after giving effect to the February 2021 Financing Transactions and our borrowing of an additional $260 million under our ABL Facility since December 31, 2020 in connection with the termination of ArcelorMittal USA’s accounts receivable factoring arrangement, the non-Guarantor subsidiaries would have accounted for approximately 9% of our consolidated assets and less than 1% of our consolidated long-term debt. On an as adjusted basis, after giving effect to the February 2021 Financing Transactions and our borrowing of an additional $260 million under our ABL Facility since December 31, 2020 in connection with the termination of ArcelorMittal USA’s accounts receivable factoring arrangement, we would have had approximately $2.8 billion of secured indebtedness and $1.9 billion of availability under the ABL Facility based on a maximum borrowing base capacity of $3.5 billion, all of which would be secured indebtedness if drawn, as of December 31, 2020. If new debt or other liabilities are added to our current debt levels, the related risks that we and our subsidiaries now face could intensify. In addition, the indenture does not contain any financial covenants or other provisions that would afford the holders of the Notes any substantial protection in the event we participate in a highly leveraged transaction. The indenture also does not limit our ability to pay dividends, make distributions, repurchase our common shares or redeem our preferred shares. Any such transaction could adversely affect you.

Restrictive covenants in the indenture governing the Notes and the agreements governing our other indebtedness restrict our ability to operate our business.

The indenture governing the Notes and agreements governing our other outstanding indebtedness and indebtedness we may incur in the future contain or may contain covenants that restrict our ability to, among other things, incur additional debt, pay dividends, make investments, enter into transactions with affiliates, merge or consolidate with other entities or sell all or substantially all of our assets.

For example, the restrictions in the agreements governing our other indebtedness limit our ability, among other things, to:

•pay dividends on or purchase or redeem our capital stock;

•incur debt;

•prepay and modify certain debt;

•merge, acquire other entities, enter into joint ventures and partnerships;

•sell assets;

•make investments in other persons;

•change the nature of the business;

•incur liens or encumbrances; and

•enter into certain transactions with affiliates.

Additionally, the restrictions in the indenture governing the Notes limit our ability, among other things, to: incur certain secured indebtedness; enter into certain sale and leaseback transactions; and merge, consolidate or amalgamate with another company.