UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-23330 |

| | |

| | BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. | |

| | (Exact name of Registrant as specified in charter) | |

| | | |

| | c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 | |

| | (Address of principal executive offices) (Zip code) | |

| | | |

| | Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 | |

| | (Name and address of agent for service) | |

| |

| Registrant's telephone number, including area code: | (212) 922-6400 |

| | |

Date of fiscal year end: | 03/31 | |

| Date of reporting period: | 03/31/2022 | |

| | | | | | | |

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc.

| |

ANNUAL REPORT March 31, 2022 |

| |

|

| |

BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. Protecting Your Privacy

Our Pledge to You THE FUND IS COMMITTED TO YOUR PRIVACY. On this page, you will find the fund’s policies and practices for collecting, disclosing, and safeguarding “nonpublic personal information,” which may include financial or other customer information. These policies apply to individuals who purchase fund shares for personal, family, or household purposes, or have done so in the past. This notification replaces all previous statements of the fund’s consumer privacy policy, and may be amended at any time. We’ll keep you informed of changes as required by law. YOUR ACCOUNT IS PROVIDED IN A SECURE ENVIRONMENT. The fund maintains physical, electronic and procedural safeguards that comply with federal regulations to guard nonpublic personal information. The fund’s agents and service providers have limited access to customer information based on their role in servicing your account. THE FUND COLLECTS INFORMATION IN ORDER TO SERVICE AND ADMINISTER YOUR ACCOUNT. The fund collects a variety of nonpublic personal information, which may include: • Information we receive from you, such as your name, address, and social security number. • Information about your transactions with us, such as the purchase or sale of fund shares. • Information we receive from agents and service providers, such as proxy voting information. THE FUND DOES NOT SHARE NONPUBLIC PERSONAL INFORMATION WITH ANYONE, EXCEPT AS PERMITTED BY LAW. Thank you for this opportunity to serve you. |

| |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

FOR MORE INFORMATION

Back Cover

| |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period from April 1, 2021, through March 31, 2022, as provided by the fund’s primary portfolio managers, Chris Barris, Kevin Cronk, Jonathan Desimone, Hiram Hamilton and Suhail A. Shaikh, of Alcentra NY, LLC, Sub-adviser

Market and Fund Performance Overview

For the 12-month period ended March 31, 2022, BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. (the “fund”) produced a total return of 2.78% on a net-asset-value basis. Over the same time period, the fund paid dividends of $7.82 per share.1 In comparison, the ICE BofA Merrill Lynch Global High Yield Index (the “Index”), the fund’s benchmark, posted a total return of −4.65% for the same period.2

Most global, fixed-income prices declined over the 12 months under pressure from rising interest rates and increasingly hawkish rhetoric from the U.S. Federal Reserve (the “Fed”). The fund outperformed the Index primarily due to advantageous asset class, credit quality, sector and duration positioning.

The Fund’s Investment Approach

The fund seeks to provide total return consisting of high current income and capital appreciation. The fund normally will invest at least 80% of its “Managed Assets”3 in credit instruments and other investments with similar economic characteristics, including: first and second lien, senior secured loans, as well as investments in participations and assignments of such loans; senior unsecured, mezzanine and other collateralized and uncollateralized subordinated loans; unitranche loans; corporate debt obligations other than loans; and structured products, including collateralized bond, loan and other debt obligations, structured notes and credit-linked notes. The fund’s assets will be allocated to certain credit strategies, focusing on (i) senior structured loans; (ii) direct lending and subordinated loans; (iii) special situations; (iv) structured credit; and (v) corporate debt. The fund expects to invest a substantial portion of its Managed Assets, and may invest without limit, in credit instruments that, at the time of investment, are rated below investment grade, or, if unrated, determined to be of comparable quality by Alcentra NY, LLC, the fund’s sub-adviser and an affiliate of BNY Mellon Investment Adviser, Inc.

Floating Rate and High Yield Outperform as Inflation Rises

The period began with economies emerging from pandemic-related lockdowns, supported by vaccine deployment, aggressive government stimulus programs and accommodative monetary policies. At the same time, inflationary pressures began to climb, fueled by high levels of consumer spending, pandemic-related, supply-chain bottlenecks and improvements in housing and labor. Initially expected to be transitory, inflation proved more persistent than expected, gradually leading to a more hawkish stance from developed market central banks. Bond yields proved volatile in this environment of uncertainty, easing somewhat during the spring and early summer, rising from September through November, trending sideways in December 2021 and January 2022, then rising sharply in February and March. On average, long-bond yields rose substantially during the period, putting downward pressure on bond prices, which generally move in the opposite direction of yields. The first quarter of 2022 proved particularly challenging for the fixed-income market as yields peaked

2

in reaction to hawkish comments from the Fed, regarding prospective interest-rate increases, with domestic inflation reaching a 40-year high of nearly 8%.

While bond prices across the board were challenged by rising yields, floating-rate credits performed relatively well as their variable interest rates increase as their benchmark rate rises. Among fixed-rate instruments, investors favored riskier assets in the prevailing environment of strong economic growth and accommodative monetary policy. High yield corporate bonds produced stronger returns than investment-grade corporates, supported by better-than-expected corporate earnings and historically low default rates. Initially, securities issued by companies in cyclical industries benefited from economic reopenings. However, as economic and geopolitical uncertainties mounted, and commodity prices spiked with Russia’s invasion of Ukraine, more defensive sectors, such as broadcasting and cable, outperformed. Rising commodity prices also bolstered returns for energy and some natural resources credits. Short duration credits outperformed long-duration instruments.

Allocation and Selection Enhance Returns

Several allocation decisions bolstered the fund’s returns relative to the Index during the period. Most significantly, the fund emphasized floating-rate assets, with its largest holdings in the structured credit arena, along with smaller holdings of global loans, direct lending and special situations. The fund also held a position in high yield bonds, with an emphasis on lower-rated B and select CCC corporate credits. Among high yield corporate sectors, the fund benefited from good security selection in the chemicals and finance sectors. Relatively short average duration further enhanced returns.

Conversely, relative returns were constrained by disappointing performance in the technology and metals & mining sectors. The fund also held modest exposure to credits issued by European cyclical firms, some of which were negatively affected in terms of revenues, costs and margins by sharply higher commodity prices.

Maintaining a Long-Term Focus in an Uncertain Environment

With the market’s focus having moved away from the pandemic at the start of 2022 toward a shift in monetary policy in the face of surging inflation, Russia’s full-scale invasion of Ukraine has presented yet another major concern for investors, while exacerbating inflationary pressures. The broad scope of sanctions imposed against Russia by most developed nations and increases in energy costs have the potential to derail the emerging economic recovery as parts of the world exit from pandemic-related restrictions. How policymakers respond to such a change in the outlook, particularly as the squeeze on consumer disposable incomes intensifies against the backdrop of higher inflation, will be important for valuations and yields. Geopolitical tensions will likely cast a cloud over financial markets in the shorter term, with the threat of military escalation and financial market instability heightening uncertainties.

In light of these challenges, we take a positive view of the underlying fundamentals of floating rate assets and have been increasing the fund’s exposure to the asset class while reducing exposure to high yield securities. Within the remaining fixed-rate, high yield component, the fund continues to emphasize lower-rated B and select CCC credits that we believe offer attractive opportunities for high distribution income, and has been reducing duration. As of the end of the period, the fund holds overweight exposure to sectors

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

somewhat insulated from macroeconomic conditions, such as cable and health care. Conversely, the fund continues to hold underweight exposure to cyclical sectors, such as chemicals and metals & mining.

April 15, 2022

1 Total return includes reinvestment of dividends and any capital gains paid, based upon net asset value per share. Past performance is no guarantee of future results. Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: FactSet — The ICE BofA Merrill Lynch Global High Yield Index is a measure of the global high-yield debt market. The Index represents the union of the U.S. high yield, the pan-European high yield and emerging-markets, hard currency, high yield indices. Investors cannot invest directly in any index.

3 “Managed Assets” of the fund means the total assets of the fund, including any assets attributable to leverage (i.e., any loans from certain financial institutions and/or the issuance of debt securities (collectively, “Borrowings”), preferred stock or other similar preference securities (“Preferred Shares”), or the use of derivative instruments that have the economic effect of leverage), minus the fund’s accrued liabilities, other than any liabilities or obligations attributable to leverage obtained through (i) indebtedness of any type (including, without limitation, Borrowings), (ii) the issuance of Preferred Shares, and/or (iii) any other means, all as determined in accordance with generally accepted accounting principles.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

High yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity. The use of leverage may magnify the fund’s gains or losses. For derivatives with a leveraging component, adverse changes in the value or level of the underlying asset can result in a loss that is much greater than the original investment in the derivative.

Credit risk is the risk that one or more credit instruments in the fund’s portfolio will decline in price or fail to pay interest or principal when due because the issuer of the instrument experiences a decline in its financial status.

Collateralized Loan Obligations (“CLOs”) and other types of Collateralized Debt Obligations (“CDOs”) are typically privately offered and sold, and thus are not registered under the securities laws. As a result, investments in CLOs and other types of CDOs may be characterized by the fund as illiquid securities. In addition to the general risks associated with credit instruments, CLOs and other types of CDOs carry additional risks, including, but not limited to: (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) the possibility that the CLO or CDO is subordinate to other classes; and (iv) the complex structure of the security may not be fully understood at the time of investment and may produce disputes with the issuer or unexpected investment results.

The Senior Secured Loans in which the fund invests typically will be below-investment-grade quality. Although, in contrast to other below-investment-grade instruments, Senior Secured Loans hold senior positions in the capital structure of a business entity, are secured with specific collateral and have a claim on the assets and/or stock of the borrower that is senior to that held by unsecured creditors, subordinated debt holders and stockholders of the borrower, the risks associated with Senior Secured Loans are similar to the risks of below-investment-grade instruments. Although the Senior Secured Loans in which the fund invests will be secured by collateral, there can be no assurance that such collateral can be readily liquidated or that the liquidation of such collateral would satisfy the borrower’s obligation in the event of non-payment of scheduled interest or principal. Additionally, if a borrower under a Senior Secured Loan defaults, becomes insolvent or goes into bankruptcy, the fund may recover only a fraction of what is owed on the Senior Secured Loan or nothing at all. In general, the secondary trading market for Senior Secured Loans is not fully developed. Illiquidity and adverse market conditions may mean that the fund may not be able to sell certain Senior Secured Loans quickly or at a fair price.

Subordinated Loans generally are subject to similar risks as those associated with investments in Senior Secured Loans, except that such loans are subordinated in payment and/or lower in lien priority to first lien holders. Subordinated Loans are subject to the additional risk that the cash flow of the borrower and collateral securing the loan or debt, if any, may be insufficient to meet scheduled payments after giving effect to the senior unsecured or senior secured obligations of the borrower. This risk is generally higher for subordinated, unsecured loans or debt, which are not backed by a security interest in any specific collateral. Subordinated Loans generally have greater price volatility than Senior Secured Loans and may be less liquid.

The use of leverage magnifies the fund’s investment, market and certain other risks. For derivatives with a leverage component, adverse changes in the value or level of the underlying asset, reference rate or index can result in a loss substantially greater than the amount invested in the derivative itself.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

Recent market risks include pandemic risks related to COVID-19. The effects of COVID-19 have contributed to increased volatility in global markets and will likely affect certain countries, companies, industries and market sectors more dramatically than others. To the extent the fund may overweight its investments in certain countries, companies, industries or market sectors, such positions will increase the fund’s exposure to risk of loss from adverse developments affecting those countries, companies, industries or sectors.

4

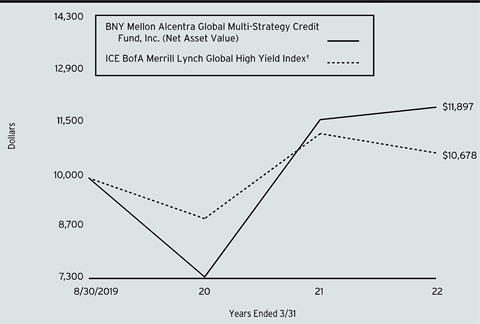

FUND PERFORMANCE AND DISTRIBUTION INFORMATION (Unaudited)

Comparison of change in value of a $10,000 investment in BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. with a hypothetical investment of $10,000 in the ICE BofA Merrill Lynch Global High Yield Index (the “Index”).

† Source: FactSet.

Past performance is not predictive of future performance.

The above graph compares a hypothetical investment of $10,000 made in BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. on 08/30/2019 to a hypothetical investment of $10,000 made in the Index on that date. All figures for the fund are based net asset value price. All dividends and capital gain distributions are reinvested.

The fund invests primarily in fixed-income securities and its performance shown in the line graph takes into account fees and expenses. The Index is a measure of the global high yield debt market. It represents the union of the U.S. high yield, the pan-European high yield and emerging-markets, hard currency, high yield indices. Investors cannot invest directly in any index.

| | | | |

Average Annual Total Returns as of 3/31/2022 | |

| Inception

Date | 1 Years | From

Inception |

BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc. | 8/30/19 | 2.78% | 6.96% |

ICE BofA Merrill Lynch Global High Yield Index | | -4.65% | 2.57% |

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon sale of the shares. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the sale of fund shares.

5

FUND PERFORMANCE AND DISTRIBUTION INFORMATION (Unaudited) (continued)

The following information regarding the fund’s distributions is current as of March 31, 2022, the fund’s fiscal year end. The fund’s returns during the period were sufficient to meet fund distributions.

The fund’s distribution policy is intended to provide shareholders with stable, but not guaranteed, cash flow, independent of the amount or timing of income earned or capital gains realized by the fund. The fund intends to distribute all or substantially all of its net investment income through its regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, in order to try to maintain a level distribution amount, the fund may pay out more or less than its net investment income during the period. As a result, distributions sources may include net investment income, realized gains and return of capital. You should not draw any conclusions about the fund’s investment performance from the amount of the distribution or from the terms of the level distribution program. A return of capital is a non-taxable distribution of a portion of a fund’s capital. A return of capital distribution does not necessarily reflect a fund’s investment performance and should not be confused with “yield” or “income.”

The amounts and sources of distributions reported below are for financial reporting purposes and are not being provided for tax reporting purposes. The actual amounts and character of the distributions for tax reporting purposes will be reported to shareholders on Form 1099-DIV, which will be sent to shareholders shortly after calendar year-end. Because distribution source estimates are updated throughout the current fiscal year based on the fund’s performance, those estimates may differ from both the tax information reported to you in your fund’s 1099 statement, as well as the ultimate economic sources of distributions over the life of your investment. The figures in the table below provide the sources of distributions and may include amounts attributed to realized gains and/or returns of capital.

| | | | | | | | |

Distributions | |

| | Current Month

Percentage of Distributions | Fiscal Year Ended

Per Share Amounts |

| Net Investment Income | Realized Gains | Return of Capital | Total Distributions | Net Investment Income | Realized Gains | Return of Capital |

BNY Mellon Alcentra Global Multi-Strategy Credit Fund, Inc | 100.00% | .00% | .00% | $7.82 | $7.82 | $.00 | $.00 |

6

STATEMENT OF INVESTMENTS

March 31, 2022

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% | | | | | |

Advertising - .7% | | | | | |

Advantage Sales & Marketing, Sr. Scd. Notes | | 6.50 | | 11/15/2028 | | 685,000 | c | 649,640 | |

Clear Channel Outdoor Holdings, Sr. Scd. Notes | | 5.13 | | 8/15/2027 | | 415,000 | c | 411,265 | |

Terrier Media Buyer, Gtd. Notes | | 8.88 | | 12/15/2027 | | 586,000 | c | 596,970 | |

| | 1,657,875 | |

Aerospace & Defense - .1% | | | | | |

TransDigm, Gtd. Notes | | 4.88 | | 5/1/2029 | | 286,000 | | 268,640 | |

Airlines - .1% | | | | | |

American Airlines Group, Gtd. Notes | | 3.75 | | 3/1/2025 | | 271,000 | c | 247,549 | |

Automobiles & Components - .9% | | | | | |

Clarios Global, Gtd. Notes | | 8.50 | | 5/15/2027 | | 375,000 | c | 389,569 | |

Dealer Tire, Sr. Unscd. Notes | | 8.00 | | 2/1/2028 | | 960,000 | c | 963,542 | |

Real Hero Merger Sub 2, Sr. Unscd. Notes | | 6.25 | | 2/1/2029 | | 240,000 | c | 219,146 | |

Standard Profil Automotive GmbH, Sr. Scd. Bonds | EUR | 6.25 | | 4/30/2026 | | 490,000 | c | 407,060 | |

| | 1,979,317 | |

Building Materials - .7% | | | | | |

CP Atlas Buyer, Sr. Unscd. Notes | | 7.00 | | 12/1/2028 | | 745,000 | c | 636,670 | |

Eco Material Technologies, Sr. Scd. Notes | | 7.88 | | 1/31/2027 | | 202,000 | c | 201,194 | |

MIWD Finance, Gtd. Notes | | 5.50 | | 2/1/2030 | | 280,000 | c | 261,947 | |

PCF GmbH, Sr. Scd. Bonds | EUR | 4.75 | | 4/15/2026 | | 405,000 | c | 431,871 | |

| | 1,531,682 | |

Chemicals - 2.0% | | | | | |

ASP Unifrax Holdings, Sr. Scd. Notes | | 5.25 | | 9/30/2028 | | 380,000 | c | 353,487 | |

Consolidated Energy Finance, Gtd. Notes | | 5.63 | | 10/15/2028 | | 344,000 | c | 318,879 | |

Consolidated Energy Finance, Gtd. Notes | | 6.50 | | 5/15/2026 | | 445,000 | c | 454,708 | |

Herens Midco, Gtd. Notes | EUR | 5.25 | | 5/15/2029 | | 890,000 | c | 846,025 | |

Innophos Holdings, Sr. Unscd. Notes | | 9.38 | | 2/15/2028 | | 625,000 | c | 664,559 | |

Iris Holdings, Sr. Unscd. Notes | | 8.75 | | 2/15/2026 | | 311,000 | c,d | 311,390 | |

Italmatch Chemicals, Sr. Scd. Notes, 3 Month EURIBOR +4.75% | EUR | 4.75 | | 9/30/2024 | | 450,000 | c,e | 475,411 | |

Olympus Water US Holding, Sr. Unscd. Notes | | 6.25 | | 10/1/2029 | | 380,000 | c | 337,030 | |

Polar US Borrower, Sr. Unscd. Notes | | 6.75 | | 5/15/2026 | | 261,000 | c | 222,812 | |

Venator Finance, Gtd. Notes | | 5.75 | | 7/15/2025 | | 520,000 | c | 418,655 | |

| | 4,402,956 | |

7

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Collateralized Loan Obligations Debt - 50.3% | | | | | |

Adagio VIII CLO, Ser. 8A, Cl. E, 3 Month EURIBOR +6.03% | EUR | 6.03 | | 4/15/2032 | | 3,000,000 | c,e | 3,181,602 | |

Barings CLO, Ser. 2019-4A, CI. E, 3 Month LIBOR +7.39% | | 7.63 | | 1/15/2033 | | 3,000,000 | c,e | 2,969,328 | |

Barings Euro CLO, Ser. 2015-1A, CI. ERR, 3 Month EURIBOR +6.86% | EUR | 6.86 | | 7/25/2035 | | 1,500,000 | c,e | 1,560,061 | |

Barings Euro CLO, Ser. 2018-3A, Cl. E, 3 Month EURIBOR +5.79% | EUR | 5.79 | | 7/27/2031 | | 2,150,000 | c,e | 2,252,208 | |

Barings Euro CLO, Ser. 2019-1A, CI. ER, 3 Month EURIBOR +7.21% | EUR | 7.21 | | 4/15/2036 | | 1,500,000 | c,e | 1,626,256 | |

Birch Grove 2 CLO, Ser. 2021-2A, Cl. E, 3 Month LIBOR +6.95% | | 7.20 | | 10/19/2034 | | 1,250,000 | c,e | 1,176,881 | |

Birch Grove 3 CLO, Ser. 2021-3A, Cl. E, 1 Month LIBOR +6.98% | | 7.18 | | 1/19/2035 | | 2,000,000 | c,e | 1,904,280 | |

BlueMountain CLO, Ser. 2016-2A, CI. DR, 3 Month LIBOR +7.79% | | 8.27 | | 8/20/2032 | | 2,250,000 | c,e | 2,217,600 | |

Cairn VI CLO, Ser. 2016-6A, CL. FR, 3 Month EURIBOR +8.25% | EUR | 8.25 | | 7/25/2029 | | 2,700,000 | c,e | 2,906,869 | |

Carlyle Euro CLO, Ser. 2019-1A, CI. D, 3 Month EURIBOR +6.12% | EUR | 6.12 | | 3/15/2032 | | 4,200,000 | c,e | 4,408,269 | |

Carlyle Global Market Strategies Euro CLO, Ser. 2014-2A, Cl. DRR, 3 Month EURIBOR +5.70% | EUR | 5.70 | | 11/17/2031 | | 2,034,000 | c,e | 2,141,230 | |

Carlyle Global Market Strategies Euro CLO, Ser. 2015-1A, CI. ER, 3 Month EURIBOR +8.03% | EUR | 8.03 | | 1/16/2033 | | 1,000,000 | c,e | 1,016,399 | |

Contego VII CLO, Ser. 7A, Cl. F, 3 Month EURIBOR +8.76% | EUR | 8.76 | | 5/14/2032 | | 3,500,000 | c,e | 3,656,432 | |

Crown Point 8 CLO, Ser. 2019-8A, Cl. ER, 3 Month LIBOR +7.13% | | 7.38 | | 10/20/2034 | | 3,000,000 | c,e | 2,841,342 | |

CVC Cordatus Loan Fund XIV CLO, Ser. 14A, Cl. E, 3 Month EURIBOR +5.90% | EUR | 5.90 | | 5/22/2032 | | 3,000,000 | c,e | 3,213,917 | |

CVC Cordatus Loan Fund XVIII CLO, Ser. 18A, Cl. FR, 3 Month EURIBOR +8.85% | EUR | 8.85 | | 7/29/2034 | | 2,000,000 | c,e | 2,046,618 | |

Dryden 66 Euro CLO, Ser. 2018-66A, CI. E, 3 Month EURIBOR +5.41% | EUR | 5.41 | | 1/18/2032 | | 2,000,000 | c,e | 2,098,984 | |

Dryden 69 Euro CLO, Ser. 2019-69A, Cl. ER, 3 Month EURIBOR +6.37% | EUR | 6.37 | | 10/18/2034 | | 1,900,000 | c,e | 2,043,310 | |

Elevation CLO, Ser. 2013-1A, Cl. D1R2, 3 Month LIBOR +7.65% | | 8.16 | | 8/15/2032 | | 2,500,000 | c,e | 2,393,370 | |

Elm Park CLO, Ser. 1A, CI. DRR, 3 Month EURIBOR +6.16% | EUR | 6.16 | | 4/15/2034 | | 1,167,000 | c,e | 1,222,353 | |

Fidelity Grand Harbour CLO, Ser. 2021-1A, Cl. E, 3 Month EURIBOR +6.22% | EUR | 6.22 | | 10/15/2034 | | 1,000,000 | c,e | 1,022,588 | |

8

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Collateralized Loan Obligations Debt - 50.3% (continued) | | | | | |

Fidelity Grand Harbour CLO, Ser. 2021-1A, Cl. F, 3 Month EURIBOR +9.15% | EUR | 9.15 | | 10/15/2034 | | 1,000,000 | c,e | 1,040,196 | |

Franklin Park Place I CLO, Ser. 2022-1A, Cl. E, 3 Month TSFR +7.50% | | 8.27 | | 4/14/2035 | | 1,300,000 | c,e | 1,245,478 | |

GoldenTree Loan Management EUR 4 CLO, Ser. 4A, Cl. ER, 3 Month EURIBOR +6.07% | EUR | 6.07 | | 7/20/2034 | | 1,500,000 | c,e | 1,564,792 | |

Greywolf II CLO, Ser. 2013-1A, Cl. DRR, 3 Month LIBOR +7.05% | | 7.29 | | 4/15/2034 | | 2,000,000 | c,e | 1,916,228 | |

ICG Euro CLO, Ser. 2021-1A, Cl. E, 3 Month EURIBOR +6.46% | EUR | 6.46 | | 10/15/2034 | | 1,000,000 | c,e | 1,059,388 | |

KKR 24 CLO, Ser. 24, CI. E, 3 Month LIBOR +6.38% | | 6.63 | | 4/20/2032 | | 2,690,000 | c,e | 2,584,673 | |

KKR 27 CLO, Ser. 27A, CI. ER, 3 Month TSFR +6.50% | | 6.73 | | 10/15/2032 | | 3,000,000 | c,e | 2,960,568 | |

MidOcean Credit X CLO, Ser. 2019-10A, Cl. ER, 3 Month LIBOR +7.16% | | 7.42 | | 10/23/2034 | | 4,000,000 | c,e | 3,728,052 | |

Northwoods Capital 20 CLO, Ser. 2019-20A, Cl. ER, 3 Month LIBOR +7.85% | | 8.11 | | 1/25/2032 | | 2,437,500 | c,e | 2,331,856 | |

Northwoods Capital 25 CLO, Ser. 2021-25A, CI. E, 3 Month LIBOR +7.14% | | 7.39 | | 7/20/2034 | | 3,000,000 | c,e | 2,902,398 | |

Northwoods Capital 27 CLO, Ser. 2021-27A, Cl. E, 3 Month LIBOR +7.04% | | 7.16 | | 10/17/2034 | | 1,150,000 | c,e | 1,092,154 | |

Octagon Investment Partners 20-R CLO, Ser. 2019-4A, Cl. E, 3 Month LIBOR +6.80% | | 7.19 | | 5/12/2031 | | 4,000,000 | c,e | 3,800,676 | |

Purple Finance 2 CLO, Ser. 2A, Cl. E, 3 Month EURIBOR +6.40% | EUR | 6.40 | | 4/20/2032 | | 2,600,000 | c,e | 2,708,568 | |

Purple Finance 2 CLO, Ser. 2A, Cl. F, 3 Month EURIBOR +8.84% | EUR | 8.84 | | 4/20/2032 | | 2,300,000 | c,e | 2,342,768 | |

Rockford Tower Europe CLO, Ser. 2019-1A, Cl. E, 3 Month EURIBOR +6.03% | EUR | 6.03 | | 1/20/2033 | | 2,000,000 | c,e | 2,139,341 | |

Sound Point XXIII CLO, Ser. 2019-2A, Cl. ER, 3 Month LIBOR +6.47% | | 6.71 | | 7/15/2034 | | 4,750,000 | c,e | 4,427,537 | |

Toro European 2 CLO, Ser. 2A, Cl. ERR, 3 Month EURIBOR +6.47% | EUR | 6.47 | | 7/25/2034 | | 2,000,000 | c,e | 2,106,214 | |

Toro European 3 CLO, Ser. 3A, Cl. ERR, 3 Month EURIBOR +6.30% | EUR | 6.30 | | 7/15/2034 | | 2,000,000 | c,e | 2,102,494 | |

Toro European 6 CLO, Ser. 6A, Cl. E, 3 Month EURIBOR +6.49% | EUR | 6.49 | | 1/12/2032 | | 1,385,000 | c,e | 1,445,944 | |

9

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Collateralized Loan Obligations Debt - 50.3% (continued) | | | | | |

Toro European 6 CLO, Ser. 6A, Cl. F, 3 Month EURIBOR +8.49% | EUR | 8.49 | | 1/12/2032 | | 2,745,000 | c,e | 2,831,112 | |

Trimaran CAVU CLO, Ser. 2019-1A, CI. E, 3 Month LIBOR +7.04% | | 7.29 | | 7/20/2032 | | 2,100,000 | c,e | 2,012,317 | |

Trimaran CAVU CLO, Ser. 2019-2A, Cl. D, 3 Month LIBOR +6.95% | | 7.19 | | 11/26/2032 | | 1,750,000 | c,e | 1,653,444 | |

Trimaran CAVU CLO, Ser. 2021-2A, CI. E, 3 Month LIBOR +7.20% | | 7.33 | | 10/25/2034 | | 2,000,000 | c,e | 1,901,364 | |

Trimaran CAVU CLO, Ser. 2021-3A, Cl. E, 3 Month LIBOR +7.37% | | 7.47 | | 1/18/2035 | | 2,000,000 | c,e | 1,912,388 | |

Trinitas XI CLO, Ser. 2019-11A, CI. ER, 3 Month LIBOR +7.27% | | 7.51 | | 7/15/2034 | | 2,000,000 | c,e | 1,954,690 | |

Venture 39 CLO, Ser. 2021-39A, Cl. E, 3 Month LIBOR +7.63% | | 7.87 | | 4/15/2033 | | 2,350,000 | c,e | 2,259,854 | |

Venture 41 CLO, Ser. 2021-41A, Cl. E, 3 Month LIBOR +7.71% | | 7.96 | | 1/20/2034 | | 2,000,000 | c,e | 1,928,356 | |

Wellfleet CLO, Ser. 2021-3A, Cl. E, 3 Month LIBOR +7.10% | | 7.21 | | 1/15/2035 | | 1,000,000 | c,e | 967,330 | |

Wellfleet X CLO, Ser. 2019-XA, Cl. DR, 3 Month LIBOR +6.61% | | 6.86 | | 7/20/2032 | | 4,000,000 | c,e | 3,689,752 | |

| | 112,509,829 | |

Collateralized Loan Obligations Equity - 4.0% | | | | | |

Blackrock European VIII CLO, Ser. 8A, Cl. SUB | EUR | 12.08 | | 7/20/2032 | | 1,425,000 | c,f | 1,065,931 | |

BlueMountain Fuji III CLO, Ser. 3A, CI. SUB | EUR | 8.59 | | 1/15/2031 | | 3,000,000 | c,f | 1,950,200 | |

Madison Park Funding X CLO, Ser. 2012-10A, Cl. SUB | | 0.00 | | 1/20/2029 | | 5,000,000 | c,f | 250,000 | |

Providus II CLO, Ser. 2A, Cl. SUB | EUR | 13.25 | | 7/15/2031 | | 1,000,000 | c,f | 672,629 | |

Wind River CLO, Ser. 2016-1A, CI. SUB | | 16.56 | | 1/15/2029 | | 11,350,000 | c,f | 5,038,163 | |

| | 8,976,923 | |

Commercial & Professional Services - 3.7% | | | | | |

Adtalem Global Education, Sr. Scd. Notes | | 5.50 | | 3/1/2028 | | 640,000 | c | 620,502 | |

Albion Financing 1, Sr. Scd. Notes | EUR | 5.25 | | 10/15/2026 | | 410,000 | c | 448,420 | |

APX Group, Gtd. Notes | | 5.75 | | 7/15/2029 | | 512,000 | c | 468,160 | |

APX Group, Sr. Scd. Notes | | 6.75 | | 2/15/2027 | | 294,000 | c | 301,062 | |

BCP V Modular Services Finance II, Sr. Scd. Bonds | EUR | 4.75 | | 11/30/2028 | | 260,000 | c | 276,227 | |

Castor, Sr. Scd. Bonds, 3 Month EURIBOR +5.25% | EUR | 5.25 | | 2/15/2029 | | 380,000 | c,e | 419,219 | |

HealthEquity, Gtd. Notes | | 4.50 | | 10/1/2029 | | 421,000 | c | 399,424 | |

Kapla Holding, Sr. Scd. Bonds | EUR | 3.38 | | 12/15/2026 | | 260,000 | c | 276,051 | |

La Financiere Atalian, Gtd. Bonds | EUR | 4.00 | | 5/15/2024 | | 330,000 | c | 332,188 | |

La Financiere Atalian, Gtd. Bonds | EUR | 5.13 | | 5/15/2025 | | 640,000 | c | 633,249 | |

10

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Commercial & Professional Services - 3.7% (continued) | | | | | |

La Financiere Atalian, Gtd. Notes | GBP | 6.63 | | 5/15/2025 | | 600,000 | | 731,391 | |

PECF USS Intermediate Holding III, Sr. Unscd. Notes | | 8.00 | | 11/15/2029 | | 619,000 | c | 598,542 | |

Prime Security Services Borrower, Scd. Notes | | 6.25 | | 1/15/2028 | | 525,000 | c | 514,616 | |

Team Health Holdings, Gtd. Notes | | 6.38 | | 2/1/2025 | | 861,000 | c | 774,172 | |

The Hertz, Gtd. Notes | | 4.63 | | 12/1/2026 | | 392,000 | c | 366,606 | |

The Hertz, Gtd. Notes | | 5.00 | | 12/1/2029 | | 70,000 | c | 63,441 | |

The House of Finance, Sr. Scd. Notes | EUR | 4.38 | | 7/15/2026 | | 100,000 | c | 108,703 | |

Verisure Midholding, Gtd. Notes | EUR | 5.25 | | 2/15/2029 | | 665,000 | c | 680,993 | |

WW International, Sr. Scd. Notes | | 4.50 | | 4/15/2029 | | 294,000 | c | 238,630 | |

| | 8,251,596 | |

Consumer Discretionary - 3.5% | | | | | |

Allen Media, Gtd. Notes | | 10.50 | | 2/15/2028 | | 935,000 | c | 923,027 | |

Ashton Woods USA, Sr. Unscd. Notes | | 4.63 | | 8/1/2029 | | 317,000 | c | 280,128 | |

Ashton Woods USA, Sr. Unscd. Notes | | 6.63 | | 1/15/2028 | | 435,000 | c | 446,188 | |

Banijay Group, Sr. Unscd. Notes | EUR | 6.50 | | 3/1/2026 | | 400,000 | c | 444,672 | |

Caesars Entertainment, Sr. Unscd. Notes | | 8.13 | | 7/1/2027 | | 465,000 | c | 498,861 | |

Carnival, Gtd. Bonds | EUR | 7.63 | | 3/1/2026 | | 365,000 | c | 414,916 | |

Carnival, Sr. Unscd. Notes | | 5.75 | | 3/1/2027 | | 112,000 | c | 106,960 | |

Carnival, Sr. Unscd. Notes | | 7.63 | | 3/1/2026 | | 565,000 | c | 569,351 | |

Deuce Finco, Sr. Scd. Bonds | GBP | 5.50 | | 6/15/2027 | | 330,000 | c | 415,534 | |

Lions Gate Capital Holdings, Gtd. Notes | | 5.50 | | 4/15/2029 | | 110,000 | c | 106,153 | |

Melco Resorts Finance, Sr. Unscd. Notes | | 4.88 | | 6/6/2025 | | 240,000 | c | 220,202 | |

NCL, Gtd. Notes | | 5.88 | | 3/15/2026 | | 375,000 | c | 356,749 | |

NCL, Sr. Scd. Notes | | 5.88 | | 2/15/2027 | | 288,000 | c | 284,047 | |

NCL Finance, Gtd. Notes | | 6.13 | | 3/15/2028 | | 168,000 | c | 156,135 | |

Royal Caribbean Cruises, Sr. Unscd. Notes | | 5.38 | | 7/15/2027 | | 310,000 | c | 298,299 | |

Royal Caribbean Cruises, Sr. Unscd. Notes | | 5.50 | | 8/31/2026 | | 240,000 | c | 233,572 | |

Royal Caribbean Cruises, Sr. Unscd. Notes | | 5.50 | | 4/1/2028 | | 495,000 | c | 472,559 | |

Scientific Games Holdings, Sr. Unscd. Notes | | 6.63 | | 3/1/2030 | | 234,000 | c | 230,958 | |

Scientific Games International, Gtd. Notes | EUR | 5.50 | | 2/15/2026 | | 260,000 | c | 295,565 | |

Scientific Games International, Gtd. Notes | | 7.25 | | 11/15/2029 | | 237,000 | c | 248,766 | |

Scientific Games International, Gtd. Notes | | 8.25 | | 3/15/2026 | | 365,000 | c | 380,056 | |

11

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Consumer Discretionary - 3.5% (continued) | | | | | |

TUI Cruises GmbH, Sr. Unscd. Notes | EUR | 6.50 | | 5/15/2026 | | 486,000 | c | 510,756 | |

| | 7,893,454 | |

Consumer Staples - .2% | | | | | |

Kronos Acquisition Holdings, Sr. Scd. Notes | | 5.00 | | 12/31/2026 | | 510,000 | c | 469,430 | |

Diversified Financials - 2.2% | | | | | |

Compass Group Diversified Holdings, Gtd. Notes | | 5.25 | | 4/15/2029 | | 360,000 | c | 338,845 | |

Compass Group Diversified Holdings, Sr. Unscd. Notes | | 5.00 | | 1/15/2032 | | 49,000 | c | 44,432 | |

Garfunkelux Holdco 3, Sr. Scd. Bonds | GBP | 7.75 | | 11/1/2025 | | 455,000 | c | 594,722 | |

Garfunkelux Holdco 3, Sr. Scd. Notes | EUR | 6.75 | | 11/1/2025 | | 500,000 | c | 552,483 | |

Icahn Enterprises, Gtd. Notes | | 6.25 | | 5/15/2026 | | 635,000 | | 648,516 | |

Nationstar Mortgage Holdings, Gtd. Notes | | 5.50 | | 8/15/2028 | | 790,000 | c | 760,217 | |

Nationstar Mortgage Holdings, Gtd. Notes | | 6.00 | | 1/15/2027 | | 235,000 | c | 239,540 | |

Navient, Sr. Unscd. Notes | | 5.00 | | 3/15/2027 | | 480,000 | | 458,066 | |

Navient, Sr. Unscd. Notes | | 5.50 | | 3/15/2029 | | 453,000 | | 422,459 | |

PennyMac Financial Services, Gtd. Notes | | 5.38 | | 10/15/2025 | | 230,000 | c | 228,067 | |

PennyMac Financial Services, Gtd. Notes | | 5.75 | | 9/15/2031 | | 622,000 | c | 553,922 | |

| | 4,841,269 | |

Electronic Components - .1% | | | | | |

Energizer Gamma Acquisition, Gtd. Bonds | EUR | 3.50 | | 6/30/2029 | | 260,000 | c | 254,201 | |

Energy - 4.0% | | | | | |

Antero Midstream Partners, Gtd. Notes | | 5.75 | | 1/15/2028 | | 320,000 | c | 327,355 | |

Antero Midstream Partners, Gtd. Notes | | 5.75 | | 3/1/2027 | | 545,000 | c | 555,911 | |

Antero Midstream Partners, Gtd. Notes | | 7.88 | | 5/15/2026 | | 200,000 | c | 216,746 | |

Antero Resources, Gtd. Notes | | 5.38 | | 3/1/2030 | | 160,000 | c | 163,641 | |

Antero Resources, Gtd. Notes | | 7.63 | | 2/1/2029 | | 274,000 | c | 296,705 | |

Archrock Partners, Gtd. Notes | | 6.25 | | 4/1/2028 | | 779,000 | c | 769,263 | |

Blue Racer Midstream, Sr. Unscd. Notes | | 6.63 | | 7/15/2026 | | 960,000 | c | 976,291 | |

Blue Racer Midstream, Sr. Unscd. Notes | | 7.63 | | 12/15/2025 | | 185,000 | c | 193,788 | |

Centennial Resource Production, Gtd. Notes | | 6.88 | | 4/1/2027 | | 349,000 | c | 351,446 | |

Colgate Energy Partners III, Sr. Unscd. Notes | | 5.88 | | 7/1/2029 | | 240,000 | c | 247,853 | |

12

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Energy - 4.0% (continued) | | | | | |

CQP Holdco, Sr. Scd. Notes | | 5.50 | | 6/15/2031 | | 500,000 | c | 491,875 | |

Crestwood Midstream Partners, Gtd. Notes | | 5.63 | | 5/1/2027 | | 25,000 | c | 24,823 | |

Crestwood Midstream Partners, Gtd. Notes | | 6.00 | | 2/1/2029 | | 715,000 | c | 713,806 | |

CrownRock, Sr. Unscd. Notes | | 5.00 | | 5/1/2029 | | 285,000 | c | 285,606 | |

EQM Midstream Partners, Sr. Unscd. Notes | | 5.50 | | 7/15/2028 | | 396,000 | | 398,253 | |

EQM Midstream Partners, Sr. Unscd. Notes | | 6.50 | | 7/1/2027 | | 205,000 | c | 214,449 | |

Genesis Energy, Gtd. Notes | | 6.25 | | 5/15/2026 | | 250,000 | | 242,345 | |

Genesis Energy, Gtd. Notes | | 6.50 | | 10/1/2025 | | 188,000 | | 185,722 | |

Genesis Energy, Gtd. Notes | | 8.00 | | 1/15/2027 | | 220,000 | | 226,560 | |

Matador Resources, Gtd. Notes | | 5.88 | | 9/15/2026 | | 160,000 | | 163,144 | |

Rockcliff Energy II, Sr. Unscd. Notes | | 5.50 | | 10/15/2029 | | 655,000 | c | 656,690 | |

Southwestern Energy, Gtd. Notes | | 5.38 | | 3/15/2030 | | 110,000 | | 111,943 | |

Southwestern Energy, Gtd. Notes | | 8.38 | | 9/15/2028 | | 155,000 | | 170,302 | |

USA Compression Partners, Gtd. Notes | | 6.88 | | 9/1/2027 | | 732,000 | | 735,942 | |

USA Compression Partners, Gtd. Notes | | 6.88 | | 4/1/2026 | | 210,000 | | 212,243 | |

| | 8,932,702 | |

Environmental Control - .3% | | | | | |

Harsco, Gtd. Notes | | 5.75 | | 7/31/2027 | | 500,000 | c | 485,120 | |

Verde Bidco, Sr. Scd. Notes | EUR | 4.63 | | 10/1/2026 | | 164,000 | c | 174,508 | |

| | 659,628 | |

Health Care - 2.8% | | | | | |

Air Methods, Sr. Unscd. Notes | | 8.00 | | 5/15/2025 | | 196,000 | c | 169,779 | |

Bausch Health, Gtd. Notes | | 5.25 | | 1/30/2030 | | 115,000 | c | 90,522 | |

Bausch Health, Gtd. Notes | | 6.25 | | 2/15/2029 | | 55,000 | c | 45,188 | |

Bausch Health, Gtd. Notes | | 7.25 | | 5/30/2029 | | 660,000 | c | 564,168 | |

Bausch Health, Sr. Scd. Notes | | 4.88 | | 6/1/2028 | | 158,000 | c | 151,499 | |

CHEPLAPHARM Arzneimittel GmbH, Sr. Scd. Notes | | 5.50 | | 1/15/2028 | | 260,000 | c | 252,056 | |

Chrome Holdco, Gtd. Notes | EUR | 5.00 | | 5/31/2029 | | 240,000 | c | 247,413 | |

Cidron Aida Finco, Sr. Scd. Bonds | EUR | 5.00 | | 4/1/2028 | | 760,000 | c | 790,885 | |

Cidron Aida Finco, Sr. Scd. Bonds | GBP | 6.25 | | 4/1/2028 | | 480,000 | c | 590,354 | |

Community Health Systems, Scd. Notes | | 6.13 | | 4/1/2030 | | 480,000 | c | 447,586 | |

Community Health Systems, Scd. Notes | | 6.88 | | 4/15/2029 | | 405,000 | c | 398,471 | |

Community Health Systems, Sr. Scd. Notes | | 4.75 | | 2/15/2031 | | 230,000 | c | 217,670 | |

Grifols Escrow Issuer, Sr. Unscd. Notes | | 4.75 | | 10/15/2028 | | 207,000 | c | 195,119 | |

13

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Health Care - 2.8% (continued) | | | | | |

Mozart Debt Merger Sub, Sr. Unscd. Notes | | 5.25 | | 10/1/2029 | | 615,000 | c | 572,534 | |

Organon & Co., Sr. Unscd. Notes | | 5.13 | | 4/30/2031 | | 590,000 | c | 570,146 | |

Ortho-Clinical Diagnostics, Sr. Unscd. Notes | | 7.25 | | 2/1/2028 | | 381,000 | c | 392,916 | |

Prime Healthcare Services, Sr. Scd. Notes | | 7.25 | | 11/1/2025 | | 516,000 | c | 529,542 | |

| | 6,225,848 | |

Industrial - 1.1% | | | | | |

Husky III Holding, Sr. Unscd. Notes | | 13.00 | | 2/15/2025 | | 595,000 | c,d | 619,559 | |

Norican A/S, Sr. Scd. Bonds | EUR | 4.50 | | 5/15/2023 | | 315,000 | | 339,757 | |

Promontoria Holding 264, Sr. Scd. Bonds | EUR | 6.38 | | 3/1/2027 | | 323,000 | c | 350,932 | |

Titan Acquisition, Sr. Unscd. Notes | | 7.75 | | 4/15/2026 | | 1,205,000 | c | 1,199,156 | |

| | 2,509,404 | |

Information Technology - .2% | | | | | |

Minerva Merger Sub, Sr. Unscd. Notes | | 6.50 | | 2/15/2030 | | 359,000 | c | 348,725 | |

Insurance - .8% | | | | | |

AmWINS Group, Sr. Unscd. Notes | | 4.88 | | 6/30/2029 | | 470,000 | c | 451,811 | |

AssuredPartners, Sr. Unscd. Notes | | 5.63 | | 1/15/2029 | | 335,000 | c | 308,979 | |

GTCR AP Finance, Sr. Unscd. Notes | | 8.00 | | 5/15/2027 | | 985,000 | c | 997,647 | |

| | 1,758,437 | |

Internet Software & Services - .8% | | | | | |

Endurance International Group Holdings, Sr. Unscd. Notes | | 6.00 | | 2/15/2029 | | 695,000 | c | 600,880 | |

Northwest Fiber, Sr. Scd. Notes | | 4.75 | | 4/30/2027 | | 221,000 | c | 210,310 | |

Northwest Fiber, Sr. Unscd. Notes | | 6.00 | | 2/15/2028 | | 695,000 | c | 611,500 | |

United Group, Sr. Scd. Bonds | EUR | 5.25 | | 2/1/2030 | | 310,000 | c | 321,729 | |

| | 1,744,419 | |

Materials - 2.0% | | | | | |

ARD Finance, Sr. Scd. Notes | EUR | 5.00 | | 6/30/2027 | | 220,000 | c,d | 221,876 | |

ARD Finance, Sr. Scd. Notes | | 6.50 | | 6/30/2027 | | 410,000 | c,d | 375,638 | |

Clydesdale Acquisition Holdings, Gtd. Notes | | 8.75 | | 4/15/2030 | | 98,000 | c,g | 92,365 | |

Graham Packaging, Gtd. Notes | | 7.13 | | 8/15/2028 | | 490,000 | c | 445,631 | |

Kleopatra Finco, Sr. Scd. Bonds | EUR | 4.25 | | 3/1/2026 | | 520,000 | c | 513,411 | |

LABL, Sr. Scd. Notes | | 5.88 | | 11/1/2028 | | 151,000 | c | 141,846 | |

LABL, Sr. Scd. Notes | | 6.75 | | 7/15/2026 | | 239,000 | c | 236,682 | |

LABL, Sr. Unscd. Notes | | 8.25 | | 11/1/2029 | | 607,000 | c | 536,816 | |

LABL, Sr. Unscd. Notes | | 10.50 | | 7/15/2027 | | 74,000 | c | 74,252 | |

Mauser Packaging Solutions Holding, Sr. Unscd. Notes | | 7.25 | | 4/15/2025 | | 1,264,000 | c | 1,254,267 | |

14

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Materials - 2.0% (continued) | | | | | |

Titan Holdings II, Sr. Unscd. Notes | EUR | 5.13 | | 7/15/2029 | | 480,000 | c | 490,007 | |

| | 4,382,791 | |

Media - 2.9% | | | | | |

Altice Financing, Sr. Scd. Bonds | | 5.75 | | 8/15/2029 | | 490,000 | c | 446,140 | |

Altice Finco, Scd. Notes | EUR | 4.75 | | 1/15/2028 | | 970,000 | c | 943,328 | |

CSC Holdings, Gtd. Notes | | 5.38 | | 2/1/2028 | | 400,000 | c | 388,928 | |

CSC Holdings, Gtd. Notes | | 6.50 | | 2/1/2029 | | 280,000 | c | 282,764 | |

CSC Holdings, Sr. Unscd. Notes | | 5.75 | | 1/15/2030 | | 710,000 | c | 633,125 | |

DISH DBS, Gtd. Notes | | 5.88 | | 11/15/2024 | | 430,000 | | 429,512 | |

DISH DBS, Sr. Scd. Bonds | | 5.25 | | 12/1/2026 | | 169,000 | c | 161,289 | |

DISH DBS, Sr. Scd. Notes | | 5.75 | | 12/1/2028 | | 169,000 | c | 160,233 | |

Radiate Holdco, Sr. Unscd. Notes | | 6.50 | | 9/15/2028 | | 608,000 | c | 576,080 | |

Scripps Escrow II, Sr. Unscd. Notes | | 5.38 | | 1/15/2031 | | 523,000 | c | 501,494 | |

Sinclair Television Group, Gtd. Notes | | 5.13 | | 2/15/2027 | | 90,000 | c | 81,864 | |

Sinclair Television Group, Gtd. Notes | | 5.50 | | 3/1/2030 | | 460,000 | c | 398,995 | |

Summer Bidco, Sr. Unscd. Bonds | EUR | 9.00 | | 11/15/2025 | | 178,288 | c,d | 197,113 | |

Summer BidCo, Sr. Unscd. Bonds | EUR | 9.00 | | 11/15/2025 | | 328,580 | c,d | 363,275 | |

Townsquare Media, Sr. Scd. Notes | | 6.88 | | 2/1/2026 | | 270,000 | c | 278,537 | |

UPC Broadband Finco, Sr. Scd. Notes | | 4.88 | | 7/15/2031 | | 380,000 | c | 357,306 | |

Virgin Media Finance, Gtd. Notes | | 5.00 | | 7/15/2030 | | 330,000 | c | 312,147 | |

| | 6,512,130 | |

Metals & Mining - .3% | | | | | |

Arconic, Scd. Notes | | 6.13 | | 2/15/2028 | | 235,000 | c | 236,222 | |

Hudbay Minerals, Gtd. Notes | | 6.13 | | 4/1/2029 | | 353,000 | c | 364,127 | |

| | 600,349 | |

Real Estate - .6% | | | | | |

Flamingo Lux II, Sr. Unscd. Notes | EUR | 5.00 | | 3/31/2029 | | 672,000 | c | 681,958 | |

Iron Mountain, Gtd. Notes | | 5.25 | | 7/15/2030 | | 450,000 | c | 441,612 | |

Park Intermediate Holdings, Sr. Scd. Notes | | 4.88 | | 5/15/2029 | | 240,000 | c | 225,475 | |

| | 1,349,045 | |

Retailing - 3.1% | | | | | |

Asbury Automotive Group, Gtd. Notes | | 4.63 | | 11/15/2029 | | 100,000 | c | 93,248 | |

Asbury Automotive Group, Gtd. Notes | | 4.75 | | 3/1/2030 | | 190,000 | | 179,559 | |

BCPE Ulysses Intermediate, Sr. Unscd. Notes | | 7.75 | | 4/1/2027 | | 1,135,000 | c,d | 1,031,329 | |

eG Global Finance, Sr. Scd. Notes | EUR | 4.38 | | 2/7/2025 | | 160,000 | c | 172,664 | |

Fertitta Entertainment, Gtd. Notes | | 6.75 | | 1/15/2030 | | 370,000 | c | 340,857 | |

Foundation Building Materials, Gtd. Notes | | 6.00 | | 3/1/2029 | | 280,000 | c | 252,543 | |

LBM Acquisition, Gtd. Notes | | 6.25 | | 1/15/2029 | | 231,000 | c | 216,656 | |

15

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Bonds and Notes - 90.3% (continued) | | | | | |

Retailing - 3.1% (continued) | | | | | |

Macy's Retail Holdings, Gtd. Notes | | 4.50 | | 12/15/2034 | | 505,000 | | 431,512 | |

Macy's Retail Holdings, Gtd. Notes | | 5.88 | | 3/15/2030 | | 170,000 | c | 167,904 | |

Park River Holdings, Gtd. Notes | | 5.63 | | 2/1/2029 | | 219,000 | c | 177,318 | |

Park River Holdings, Sr. Unscd. Notes | | 6.75 | | 8/1/2029 | | 463,000 | c | 387,272 | |

Shiba Bidco, Sr. Scd. Bonds | EUR | 4.50 | | 10/31/2028 | | 354,000 | c | 377,733 | |

Staples, Sr. Scd. Notes | | 7.50 | | 4/15/2026 | | 560,000 | c | 544,432 | |

Staples, Sr. Unscd. Notes | | 10.75 | | 4/15/2027 | | 373,000 | c | 332,356 | |

The Michaels Companies, Sr. Scd. Notes | | 5.25 | | 5/1/2028 | | 330,000 | c | 303,395 | |

The Michaels Companies, Sr. Unscd. Notes | | 7.88 | | 5/1/2029 | | 460,000 | c | 394,448 | |

The Very Group Funding, Sr. Scd. Bonds | GBP | 6.50 | | 8/1/2026 | | 469,000 | c | 585,297 | |

White Cap Buyer, Sr. Unscd. Notes | | 6.88 | | 10/15/2028 | | 495,000 | c | 469,654 | |

White Cap Parent, Sr. Unscd. Notes | | 8.25 | | 3/15/2026 | | 498,000 | c,d | 489,875 | |

| | 6,948,052 | |

Technology Hardware & Equipment - .2% | | | | | |

Banff Merger Sub, Sr. Unscd. Notes | EUR | 8.38 | | 9/1/2026 | | 380,000 | c | 420,433 | |

Telecommunication Services - 2.0% | | | | | |

Altice France, Sr. Scd. Notes | | 5.13 | | 7/15/2029 | | 250,000 | c | 224,400 | |

Altice France, Sr. Scd. Notes | | 5.50 | | 10/15/2029 | | 532,000 | c | 478,077 | |

Altice France, Sr. Scd. Notes | | 5.50 | | 1/15/2028 | | 200,000 | c | 185,746 | |

Altice France Holding, Gtd. Notes | EUR | 4.00 | | 2/15/2028 | | 140,000 | c | 133,390 | |

Altice France Holding, Gtd. Notes | | 6.00 | | 2/15/2028 | | 420,000 | c | 363,084 | |

CommScope, Gtd. Notes | | 7.13 | | 7/1/2028 | | 550,000 | c | 497,475 | |

CommScope, Gtd. Notes | | 8.25 | | 3/1/2027 | | 215,000 | c | 209,336 | |

Connect Finco, Sr. Scd. Notes | | 6.75 | | 10/1/2026 | | 985,000 | c | 1,003,415 | |

Embarq, Sr. Unscd. Notes | | 8.00 | | 6/1/2036 | | 340,000 | | 328,154 | |

ViaSat, Sr. Unscd. Notes | | 5.63 | | 9/15/2025 | | 300,000 | c | 293,501 | |

WP/AP Telecom Holdings III, Sr. Unscd. Notes | EUR | 5.50 | | 1/15/2030 | | 420,000 | c | 438,144 | |

Zoncolan Bidco, Sr. Scd. Bonds | EUR | 4.88 | | 10/21/2028 | | 228,000 | c | 236,997 | |

| | 4,391,719 | |

Utilities - .7% | | | | | |

Energia Group Ni Financeco, Sr. Scd. Notes | GBP | 4.75 | | 9/15/2024 | | 630,000 | c | 804,841 | |

Energia Group ROI Holdings, Sr. Scd. Notes | GBP | 4.75 | | 9/15/2024 | | 380,000 | | 485,459 | |

Pike, Gtd. Notes | | 5.50 | | 9/1/2028 | | 415,000 | c | 391,855 | |

| | 1,682,155 | |

Total Bonds and Notes

(cost $207,968,390) | | 201,750,558 | |

16

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% | | | | | |

Advertising - 1.0% | | | | | |

ABG Intermediate Holdings 2, 2021 Refinancing Term Loan, 3 Month LIBOR +3.25% | | 3.76 | | 12/4/2024 | | 354,905 | e | 352,613 | |

ABG Intermediate Holdings 2, Second Lien Initial Term Loan, 3 Month Term SOFR +6.00% | | 6.50 | | 12/20/2029 | | 80,000 | e | 79,500 | |

Advantage Sales & Marketing, Term Loan B-1, 3 Month LIBOR +4.50% | | 5.25 | | 10/28/2027 | | 422,569 | e | 419,399 | |

Clear Channel Outdoor Holdings, Term Loan B, 3 Month LIBOR +3.50% | | 3.80 | | 8/21/2026 | | 392,731 | e | 386,718 | |

Polyconcept North America, First Lien Closing Date Term Loan, 6 Month LIBOR +4.50% | | 6.00 | | 8/16/2023 | | 255,107 | e | 253,937 | |

Red Ventures, First Lien Term Loan B-3, 1 Month LIBOR +3.50% | | 4.25 | | 11/8/2024 | | 105,185 | e | 104,440 | |

Summer BC Holdco B, USD Additional Facility Term Loan B-2, 3 Month LIBOR +4.50% | | 5.51 | | 12/25/2026 | | 567,752 | e | 565,387 | |

| | 2,161,994 | |

Airlines - .1% | | | | | |

AAdvantage Loyalty, Initial Term Loan, 3 Month LIBOR +4.75% | | 5.50 | | 4/20/2028 | | 189,805 | e | 192,653 | |

Building Materials - 1.0% | | | | | |

BME Group Holding, Facility Term Loan B, 3 Month EURIBOR +3.75% | EUR | 3.75 | | 10/31/2026 | | 1,000,000 | e | 1,094,430 | |

LSF10 XL Bidco, Facility Term Loan B-4, 1-3 Month EURIBOR +4.00% | EUR | 4.00 | | 4/9/2028 | | 1,000,000 | e | 1,091,421 | |

| | 2,185,851 | |

Chemicals - 2.9% | | | | | |

Albaugh, Term Loan B, 1 Month Term SOFR +3.75% | | 4.75 | | 2/18/2029 | | 278,311 | e | 277,848 | |

Aruba Investment Holding, Euro Term Loan B, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 11/24/2027 | | 990,000 | e | 1,085,605 | |

Aruba Investment Holding, First Lien Initial Dollar Term Loan, 6 Month LIBOR +3.75% | | 4.50 | | 11/24/2027 | | 119,120 | e | 117,879 | |

ColourOZ Investment 1 GmbH, Second Lien Initial Euro Term Loan, 3 Month EURIBOR +4.25% | EUR | 5.25 | | 9/7/2022 | | 127,702 | e | 143,743 | |

ColourOZ Investment 2, First Lien Initial Term Loan B-2, 3 Month LIBOR +4.25% | | 5.25 | | 9/7/2023 | | 1,159,724 | e | 1,107,537 | |

ColourOZ Investment 2, First Lien Initial Term Loan C, 3 Month LIBOR +4.25% | | 5.25 | | 9/7/2023 | | 191,716 | e | 183,089 | |

17

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Chemicals - 2.9% (continued) | | | | | |

ColourOZ Investment 2, Second Lien Initial Term Loan B-2, 3 Month LIBOR +4.25% | | 5.25 | | 9/7/2022 | | 2,173,995 | e | 2,119,645 | |

Flexsys Holdings, Initial Term Loan, 3 Month LIBOR +5.25% | | 6.00 | | 11/1/2028 | | 340,000 | e | 337,025 | |

Flint Group GmbH, First Lien Initial Term Loan B-8, 3 Month LIBOR +4.25% | | 5.25 | | 9/21/2023 | | 337,601 | e | 322,409 | |

LSF11 Skyscraper Holdco, USD Facility Term Loan B-3, 3 Month LIBOR +3.50% | | 4.51 | | 9/30/2027 | | 309,889 | e | 309,116 | |

Polar US Borrower, Initial Term Loan, 3 Month LIBOR +4.75% | | 4.99 | | 10/16/2025 | | 395,893 | e | 385,006 | |

Sparta US HoldCo, First Lien Initial Term Loan, 1 Month LIBOR +3.50% | | 4.25 | | 8/2/2028 | | 194,377 | e | 192,433 | |

| | 6,581,335 | |

Commercial & Professional Services - 6.6% | | | | | |

Adtalem Global Education, Term Loan B, 1 Month LIBOR +4.50% | | 5.25 | | 8/12/2028 | | 337,591 | e | 336,905 | |

Albion Acquisitions, Term Loan B, 3 Month EURIBOR +5.25% | EUR | 5.25 | | 7/31/2026 | | 1,000,000 | e | 1,105,470 | |

American Auto Auction, First Lien Tranche Term Loan B, 3 Month Term SOFR +5.00% | | 5.80 | | 12/30/2027 | | 389,025 | e | 383,676 | |

APX Group, Initial Term Loan, 1 Month LIBOR +3.50% and 3 Month PRIME +3.50% | | 5.00 | | 7/9/2028 | | 266,656 | e | 263,419 | |

Avis Budget Car Rental, Tranche Term Loan C, 1 Month Term SOFR +3.50% | | 4.00 | | 3/16/2029 | | 311,348 | e | 309,597 | |

AVSC Holding, Term Loan B-1, 3 Month LIBOR +3.50% | | 4.50 | | 3/1/2025 | | 220,229 | e | 208,499 | |

Axiom Global, Initial Term Loan, 3 Month LIBOR +4.75% | | 5.50 | | 10/1/2026 | | 4,887,500 | e | 4,777,531 | |

Boels Topholding, Facility Term Loan B-2, 3 Month EURIBOR +3.25% | EUR | 3.25 | | 2/5/2027 | | 1,000,000 | e | 1,086,072 | |

Cast & Crew, First Lien Incremental Facility No. 2 Incremental Term Loan, 1 Month Term SOFR +3.75% | | 4.25 | | 12/30/2028 | | 28,053 | e | 27,939 | |

Cast & Crew, First Lien Initial Term Loan, 1 Month LIBOR +3.50% | | 3.96 | | 2/7/2026 | | 67,273 | e | 66,955 | |

CIBT Global, First Lien Term Loan, 3 Month LIBOR +1.00% | | 2.00 | | 6/1/2024 | | 1,000,000 | e | 806,070 | |

Electro Rent, First Lien Initial Term Loan, 3 Month LIBOR +5.00% | | 6.00 | | 1/31/2024 | | 197,396 | e | 197,520 | |

18

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Commercial & Professional Services - 6.6% (continued) | | | | | |

Employbridge, Term Loan B, 3 Month LIBOR +4.75% | | 5.76 | | 7/19/2028 | | 207,414 | e | 205,599 | |

Infinitas Learning Finco, Term Loan B, 6 Month EURIBOR +4.50% | EUR | 4.50 | | 9/30/2028 | | 999,957 | e | 1,102,938 | |

PECF USS Intermediate Holding, Initial Term Loan, 3 Month LIBOR +4.25% | | 4.75 | | 12/15/2028 | | 294,740 | e | 292,504 | |

Praesidiad, Facility Term Loan B, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 10/4/2024 | | 1,000,000 | e | 989,817 | |

Pre-Paid Legal Services, First Lien Initial Term Loan, 1 Month LIBOR +3.75% | | 4.25 | | 12/15/2028 | | 173,982 | e | 172,115 | |

RLG Holdings, First Lien Closing Date Initial Term Loan, 3 Month LIBOR +4.25% | | 5.00 | | 7/8/2028 | | 410,369 | e | 407,805 | |

Team Health Holdings, Extended Term Loan, 1 Month Term SOFR +5.25% | | 6.25 | | 2/17/2027 | | 187,823 | e | 179,449 | |

Vaco Holdings, Initial Term Loan, 3 Month Term SOFR +5.00% | | 5.75 | | 1/21/2029 | | 194,041 | e,h | 193,192 | |

Verscend Holding, New Term Loan B, 1 Month LIBOR +4.00% | | 4.46 | | 8/27/2025 | | 487,498 | e | 486,888 | |

WP/AP Holdings, Facility Term Loan B, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 11/18/2028 | | 1,000,000 | e | 1,103,484 | |

| | 14,703,444 | |

Consumer Discretionary - 5.6% | | | | | |

Allen Media, Term Loan B, 3 Month LIBOR +5.50% | | 5.72 | | 2/10/2027 | | 364,669 | e | 362,298 | |

AP Gaming I, Term Loan B, 3 Month Term SOFR +4.00% | | 4.75 | | 2/15/2029 | | 265,795 | e | 261,476 | |

Caesars Resort Collection, Term Loan B-1, 1 Month LIBOR +3.50% | | 3.96 | | 7/20/2025 | | 271,860 | e | 271,316 | |

Center Parcs Europe, Facility Term Loan B-1, 3 Month EURIBOR +2.00% | EUR | 2.00 | | 9/23/2022 | | 2,096,068 | e | 2,318,775 | |

Center Parcs Europe, Facility Term Loan B-2, 3 Month EURIBOR +2.00% | EUR | 2.00 | | 9/23/2022 | | 1,240,879 | e | 1,372,723 | |

Dealer Tire, Term Loan B-1, 1 Month LIBOR +4.25% | | 4.71 | | 12/12/2025 | | 403,841 | e | 402,494 | |

Freshworld Holding IV GmbH, Facility Term Loan B-2, 6 Month EURIBOR +3.75% | EUR | 3.75 | | 10/2/2026 | | 1,000,000 | e | 1,097,522 | |

Great Canadian Gaming, Term Loan B, 3 Month LIBOR +4.00% | | 4.93 | | 11/1/2026 | | 261,314 | e | 260,417 | |

19

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Consumer Discretionary - 5.6% (continued) | | | | | |

Scientific Games Holdings, Term Loan B-2, 1 Month Term SOFR +3.50% | | 4.00 | | 2/4/2029 | | 303,047 | e | 300,719 | |

Silk Bidco, Facility Term Loan B, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 2/22/2025 | | 2,000,000 | e | 1,999,857 | |

Stage Entertainment, Facility Term Loan B-2, 6 Month EURIBOR +3.25% | EUR | 3.25 | | 5/2/2026 | | 1,000,000 | e | 1,063,383 | |

Tecta America, First Lien Initial Term Loan, 1 Month LIBOR +4.25% | | 5.00 | | 4/9/2028 | | 754,001 | e | 748,346 | |

Travel Leaders Group, 2018 Refinancing Term Loan, 1 Month LIBOR +4.00% | | 4.46 | | 1/25/2024 | | 137,927 | e | 130,643 | |

Vacalians Holding, Facility Term Loan B, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 11/30/2025 | | 1,000,000 | e | 1,085,508 | |

Varsity Brands Holding, First Lien Initial Term Loan, 1 Month LIBOR +3.50% | | 4.50 | | 12/15/2024 | | 672,571 | e | 646,579 | |

William Morris Endeavor, New Term Loan B-1, 1 Month LIBOR +2.75% | | 3.02 | | 5/18/2025 | | 255,846 | e | 251,956 | |

| | 12,574,012 | |

Consumer Staples - .2% | | | | | |

Kronos Acquisition Holdings, Tranche Term Loan B-1, 3 Month LIBOR +3.75% | | 4.25 | | 12/22/2026 | | 569,438 | e | 534,324 | |

Diversified Financials - .6% | | | | | |

Polystorm Bidco, Delayed Draw Term Loan, 3-4 Month EURIBOR +2.50% | EUR | 2.50 | | 10/1/2028 | | 113,402 | e,h | 124,667 | |

Polystorm Bidco, Facility Term Loan B-1, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 10/1/2028 | | 886,598 | e | 974,669 | |

Tegra118 Wealth Solutions, Initial Term Loan, 3 Month LIBOR +4.00% | | 4.49 | | 2/18/2027 | | 275,100 | e | 273,954 | |

| | 1,373,290 | |

Electronic Components - .5% | | | | | |

IDEMIA Identity & Security France, Term Loan B-3, 3 Month EURIBOR +4.50% | EUR | 4.50 | | 1/10/2026 | | 1,000,000 | e | 1,107,522 | |

Energy - .8% | | | | | |

BCP Renaissance Parent, Term Loan B-3, 1 Month Term SOFR +3.50% | | 4.50 | | 10/31/2026 | | 229,726 | e | 227,045 | |

GIP III Stetson I, Initial Term Loan, 1 Month LIBOR +4.25% | | 4.71 | | 7/18/2025 | | 198,909 | e | 193,414 | |

20

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Energy - .8% (continued) | | | | | |

Lucid Energy Group II, First Lien Term Loan, 1 Month LIBOR +4.25% | | 5.00 | | 11/22/2028 | | 310,000 | e | 307,838 | |

Traverse Midstream Partners, Advance Term Loan, 3 Month Term SOFR +4.25% | | 5.25 | | 9/27/2024 | | 641,684 | e | 640,079 | |

WaterBridge Midstream Operating, Initial Term Loan, 3 Month LIBOR +5.75% | | 6.75 | | 6/21/2026 | | 341,776 | e | 330,402 | |

| | 1,698,778 | |

Environmental Control - .5% | | | | | |

Northstar Group Services, Term Loan B, 1 Month LIBOR +5.50% | | 6.50 | | 11/12/2026 | | 254,968 | e | 254,011 | |

Packers Holdings, Initial Term Loan, 6 Month LIBOR +3.25% | | 4.00 | | 3/9/2028 | | 158,091 | e | 155,996 | |

Waterlogic USA Holdings, Facility Term Loan B-2, 3 Month LIBOR +4.75% | | 5.76 | | 8/12/2028 | | 627,796 | e | 626,880 | |

| | 1,036,887 | |

Food Products - 1.7% | | | | | |

CJ Foods, Term Loan, 3 Month LIBOR +6.00% | | 7.00 | | 3/5/2027 | | 2,456,140 | e | 2,349,716 | |

Sovos Brands Intermediate, First Lien Initial Term Loan, 3 Month LIBOR +3.75% | | 4.50 | | 6/8/2028 | | 380,518 | e | 377,460 | |

ZF Invest, Term Loan B, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 7/12/2028 | | 1,000,000 | e | 1,078,710 | |

| | 3,805,886 | |

Food Service - .1% | | | | | |

TKC Holdings, Term Loan, 6 Month LIBOR +5.50% | | 7.00 | | 5/14/2028 | | 207,225 | e | 204,738 | |

Forest Products & Paper - .1% | | | | | |

SPA US HoldCo, USD Facility Term Loan B, 3 Month LIBOR +3.75% | | 4.50 | | 2/4/2028 | | 258,675 | e | 251,562 | |

Health Care - 7.9% | | | | | |

Air Methods, Initial Term Loan, 3 Month LIBOR +3.50% | | 4.51 | | 4/21/2024 | | 302,072 | e | 290,241 | |

Auris Luxembourg III, Facility Term Loan B-1, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 2/21/2026 | | 1,000,000 | e | 1,102,798 | |

Auris Luxembourg III, Facility Term Loan B-2, 1 Month LIBOR +3.75% | | 4.21 | | 2/21/2026 | | 351,733 | e | 343,490 | |

Baart Programs, Delayed Draw Term Loan, 3 Month LIBOR +5.00% | | 5.29 | | 6/11/2027 | | 924,364 | e,h | 912,809 | |

Baart Programs, Term Loan, 3 Month LIBOR +5.00% | | 6.01 | | 6/11/2027 | | 1,067,125 | e | 1,053,786 | |

21

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Health Care - 7.9% (continued) | | | | | |

Cerebro Bidco GmbH, Facility Term Loan B-1, 6 Month EURIBOR +4.25% | EUR | 4.25 | | 12/11/2027 | | 633,857 | e | 699,834 | |

Cerebro BidCo GmbH, Facility Term Loan B-2, 6 Month EURIBOR +4.25% | EUR | 4.25 | | 12/11/2027 | | 366,143 | e | 404,254 | |

eResearchTechnology, First Lien Initial Term Loan, 3 Month LIBOR +4.50% | | 5.50 | | 2/4/2027 | | 154,010 | e | 153,674 | |

Financiere Verdi I, Facility Term Loan B, 12 Month SONIA +4.50% | GBP | 5.19 | | 4/15/2028 | | 1,500,000 | e | 1,896,582 | |

Finthrive Software Intermediate, Term Loan, 6 Month LIBOR +4.00% | | 4.50 | | 12/17/2028 | | 235,786 | e | 233,796 | |

Gainwell Acquisition, Term Loan B, 3 Month LIBOR +4.00% | | 5.01 | | 10/1/2027 | | 341,836 | e | 341,836 | |

Global Medical Response, 2017-2 New Term Loan, 3 Month LIBOR +4.25% | | 5.25 | | 3/14/2025 | | 104,795 | e | 104,327 | |

Global Medical Response, 2020 Term Loan, 3 Month LIBOR +4.25% | | 5.25 | | 10/2/2025 | | 177,750 | e | 176,834 | |

Hera, Facility Term Loan B, 1 Month EURIBOR +3.50% | EUR | 3.50 | | 9/20/2024 | | 2,000,000 | e | 2,204,203 | |

Inovie, Senior Facility Term Loan B, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 12/15/2028 | | 1,000,000 | e | 1,100,636 | |

Inula Natural Health Group, Senior Facility Term Loan B, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 12/11/2025 | | 903,382 | e | 949,398 | |

IWH UK Midco, Facility Term Loan B, 1 Month EURIBOR +4.00% | EUR | 4.00 | | 2/1/2025 | | 1,500,000 | e | 1,651,767 | |

MED ParentCo, First Lien Initial Term Loan, 1 Month LIBOR +4.25% | | 4.71 | | 8/31/2026 | | 603,520 | e | 598,239 | |

One Call, First Lien Term Loan B, 3 Month LIBOR +5.50% | | 6.25 | | 4/22/2027 | | 794,000 | e | 746,360 | |

Pathway Vet Alliance, 2021 Replacement Term Loan, 1 Month LIBOR +3.75% | | 4.21 | | 3/31/2027 | | 171,912 | e | 170,516 | |

PetVet Care Centers, Second Lien Initial Term Loan, 1 Month LIBOR +6.25% | | 6.71 | | 2/15/2026 | | 301,948 | e | 301,006 | |

Pluto Acquisition I, 2021 First Lien Term Loan, 3 Month LIBOR +4.00% | | 4.21 | | 6/20/2026 | | 86,983 | e | 85,896 | |

Resonetics, First Lien Initial Term Loan, 3 Month LIBOR +4.00% | | 4.75 | | 4/28/2028 | | 58,962 | e | 58,483 | |

22

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Health Care - 7.9% (continued) | | | | | |

Sharp Midco, First Lien Initial Term Loan, 3 Month LIBOR +4.00% | | 5.01 | | 12/14/2028 | | 152,986 | e | 152,412 | |

Sirona BidCo, Facility Term Loan B, 3 Month EURIBOR +4.50% | EUR | 4.50 | | 12/17/2028 | | 1,000,000 | e | 1,091,963 | |

Surgery Center Holdings, 2021 New Term Loan, 1 Month LIBOR +3.75% | | 4.50 | | 8/31/2026 | | 439,282 | e | 436,594 | |

WCG Purchaser, First Lien Initial Term Loan, 3 Month LIBOR +4.00% | | 5.01 | | 1/8/2027 | | 383,832 | e | 383,032 | |

| | 17,644,766 | |

Industrial - 3.2% | | | | | |

Osmose Utilities Services, First Lien Initial Term Loan, 1 Month LIBOR +3.25% | | 3.75 | | 6/22/2028 | | 232,790 | e | 230,316 | |

Pro Mach Group, Delayed Draw Term Loan, 3 Month LIBOR +4.00% | | 5.00 | | 8/31/2028 | | 12,370 | e,h | 12,331 | |

Pro Mach Group, Initial Term Loan, 3 Month LIBOR +4.00% | | 5.00 | | 8/31/2028 | | 179,719 | e | 179,157 | |

Qualtek USA, Tranche Term Loan B, 3 Month LIBOR +6.25% | | 7.25 | | 7/18/2025 | | 4,844,326 | e | 4,698,996 | |

Radar Bidco, Initial Term Loan, 6 Month EURIBOR +10.00% | EUR | 10.00 | | 12/16/2024 | | 1,109,299 | e | 1,244,392 | |

SPX FLOW, Term Loan, 1 Month Term SOFR +4.50% | | 5.00 | | 3/18/2029 | | 242,006 | e | 236,056 | |

Titan Acquisition, Initial Term Loan, 3 Month LIBOR +3.00% | | 3.35 | | 3/28/2025 | | 344,672 | e | 337,964 | |

VAC Germany Holding GmbH, Term Loan B, 3 Month LIBOR +4.00% | | 5.01 | | 3/8/2025 | | 263,147 | e | 252,950 | |

| | 7,192,162 | |

Information Technology - 3.6% | | | | | |

Boxer Parent, 2021 Replacement Dollar Term Loan, 3 Month LIBOR +3.75% | | 4.76 | | 10/2/2025 | | 649,326 | e | 646,352 | |

Boxer Parent, 2021 Replacement EURO Term Loan, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 10/2/2025 | | 990,329 | e | 1,094,784 | |

Camelia Bidco, Facility Term Loan B-1, 3 Month GBPLIBOR +4.75% | GBP | 4.77 | | 10/5/2024 | | 1,500,000 | e | 1,936,455 | |

Concorde Lux, Term Loan B, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 3/1/2028 | | 1,000,000 | e | 1,098,871 | |

CT Technologies, 2021 Reprice Term Loan, 1 Month LIBOR +4.25% | | 5.00 | | 12/16/2025 | | 152,110 | e | 151,227 | |

DCert Buyer, First Lien Initial Term Loan, 1 Month LIBOR +4.00% | | 4.46 | | 10/16/2026 | | 427,190 | e | 424,727 | |

23

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Information Technology - 3.6% (continued) | | | | | |

DCert Buyer, Second Lien Initial Term Loan, 1 Month LIBOR +7.00% | | 7.46 | | 2/16/2029 | | 200,000 | e | 198,208 | |

ECL Entertainment, Term Loan B, 3 Month LIBOR +7.50% | | 8.25 | | 4/30/2028 | | 168,725 | e | 170,623 | |

EP Purchaser, Closing Date Term Loan, 3 Month LIBOR +3.50% | | 4.51 | | 11/4/2028 | | 320,000 | e | 318,334 | |

Finastra USA, First Lien Dollar Term Loan, 6 Month LIBOR +3.50% | | 4.50 | | 6/13/2024 | | 719,725 | e | 711,711 | |

Greeneden US Holdings II, Dollar Term Loan B-4, 1 Month LIBOR +4.00% | | 4.87 | | 12/1/2027 | | 175,188 | e | 175,133 | |

Ivanti Software, First Amendment Term Loan, 3 Month LIBOR +4.00% | | 4.75 | | 12/1/2027 | | 173,041 | e | 170,446 | |

Ivanti Software, First Lien Term Loan B, 3 Month LIBOR +4.25% | | 5.00 | | 12/1/2027 | | 479,181 | e | 473,491 | |

Mitchell International, Second Lien Initial Term Loan, 3 Month LIBOR +6.50% | | 7.00 | | 10/15/2029 | | 107,692 | e | 106,919 | |

TIBCO Software, Term Loan B-3, 1 Month LIBOR +3.75% | | 3.96 | | 7/3/2026 | | 253,643 | e | 252,691 | |

| | 7,929,972 | |

Insurance - 3.7% | | | | | |

Asurion, New Term Loan B-4, 1 Month LIBOR +5.25% | | 5.71 | | 1/15/2029 | | 71,244 | e | 69,752 | |

Asurion, Second Lien Term Loan B-3, 1 Month LIBOR +5.25% | | 5.71 | | 2/3/2028 | | 1,083,367 | e | 1,063,866 | |

BidCo SB, Term Loan, 6 Month EURIBOR +4.00% | EUR | 4.00 | | 11/16/2028 | | 1,000,000 | e | 1,103,717 | |

Hestia Holding, Facility Term Loan B-1, 3 Month EURIBOR +4.00% | EUR | 4.00 | | 6/1/2027 | | 1,000,000 | e | 1,104,640 | |

Mayfield Agency Borrower, First Lien Term Loan B, 1 Month LIBOR +4.50% | | 4.96 | | 2/28/2025 | | 571,723 | e | 567,078 | |

Sedgwick Claims Management Services, 2019 New Term Loan, 1 Month LIBOR +3.75% | | 4.21 | | 9/3/2026 | | 767,394 | e | 763,557 | |

Sedgwick Claims Management Services, 2020 Term Loan, 1 Month LIBOR +4.25% | | 5.25 | | 9/3/2026 | | 6,978 | e | 6,951 | |

Selectquote, Initial Term Loan, 1 Month LIBOR +5.00% | | 5.75 | | 11/5/2024 | | 3,813,971 | e,i | 3,661,412 | |

| | 8,340,973 | |

Internet Software & Services - 1.8% | | | | | |

Endure Digital, Initial Term Loan, 3 Month LIBOR +3.50% | | 4.25 | | 2/10/2028 | | 406,925 | e | 396,243 | |

24

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Internet Software & Services - 1.8% (continued) | | | | | |

ION Trading Finance, Initial Dollar Term Loan, 1 Month LIBOR +4.75% | | 5.21 | | 4/1/2028 | | 129,025 | e | 128,261 | |

ION Trading Finance, Initial Euro Term Loan, 3 Month EURIBOR +4.25% | EUR | 4.25 | | 4/1/2028 | | 1,985,000 | e | 2,189,955 | |

Proofpoint, Initial Term Loan, 3 Month LIBOR +3.25% | | 3.76 | | 8/31/2028 | | 487,465 | e | 482,827 | |

Trader, Senior Secured First Lien Term Loan, 3 Month LIBOR +3.00% | | 4.00 | | 9/28/2023 | | 170,000 | e | 169,150 | |

Weddingwire, Ammendment No. 3 Term Loan, 1 Month Term SOFR +4.50% | | 4.67 | | 12/19/2025 | | 731,156 | e | 729,785 | |

| | 4,096,221 | |

Materials - 1.3% | | | | | |

Berlin Packaging, Tranche Term Loan B-5, 1 Month LIBOR +3.75% | | 4.25 | | 3/11/2028 | | 207,985 | e | 206,373 | |

Charter Nex US, 2021 Refinancing Term Loan, 1 Month LIBOR +3.75% | | 4.50 | | 12/1/2027 | | 78,971 | e | 78,638 | |

Clydesdale Acquisition, Term Loan, 1 Month Term SOFR +4.25% | | 4.75 | | 3/30/2029 | | 286,979 | e | 282,674 | |

Grinding Media, First Lien Initial Term Loan, 1 Month LIBOR +4.00% | | 4.75 | | 10/12/2028 | | 294,242 | e | 292,219 | |

IFCO Management GmbH, Facility Term Loan B-1A, 6 Month EURIBOR +3.25% | EUR | 3.25 | | 5/31/2026 | | 1,000,000 | e | 1,086,028 | |

MAR Bidco, USD Facility Term Loan B, 3 Month LIBOR +4.25% | | 4.75 | | 6/28/2028 | | 109,778 | e | 108,543 | |

Mauser Packaging Solutions, Initial Term Loan, 3 Month LIBOR +3.25% | | 3.48 | | 4/3/2024 | | 110,961 | e | 109,632 | |

Proampac PG Borrower, 2020-1 Term Loan, 3 Month LIBOR +3.75% | | 4.50 | | 11/3/2025 | | 335,062 | e | 328,445 | |

Tecostar Holdings, 2017 First Lien Term Loan, 3 Month LIBOR +3.50% | | 4.50 | | 5/1/2024 | | 225,357 | e | 211,836 | |

Tosca Services, 2021 Refinancing Term Loan, 1 Month LIBOR +3.50% | | 4.25 | | 8/18/2027 | | 54,453 | e | 53,295 | |

Valcour Packaging, Second Lien Initial Term Loan, 3 Month LIBOR +7.00% | | 7.50 | | 9/30/2029 | | 240,000 | e | 229,200 | |

| | 2,986,883 | |

25

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Media - 1.4% | | | | | |

Banijay Group US Holding, USD Facility Term Loan B, 1 Month LIBOR +3.75% | | 3.99 | | 3/1/2025 | | 210,138 | e | 208,562 | |

DIRECTV Financing, Closing Date Term Loan, 1 Month LIBOR +5.00% | | 5.75 | | 8/2/2027 | | 738,438 | e | 738,582 | |

NEP Europe Finco, Initial Euro Term Loan, 3 Month EURIBOR +3.50% | EUR | 3.50 | | 10/20/2025 | | 1,944,724 | e | 2,117,746 | |

| | 3,064,890 | |

Retailing - .9% | | | | | |

Academy, Refinancing Term Loan, 1 Month LIBOR +3.75% | | 4.50 | | 11/6/2027 | | 253,083 | e | 251,819 | |

Great Outdoors Group, Term Loan B-2, 1 Month LIBOR +3.75% | | 4.50 | | 3/5/2028 | | 589,982 | e | 588,599 | |

LBM Acquisition, First Lien Initial Term Loan, 1 Month LIBOR +3.75% | | 4.50 | | 12/18/2027 | | 395,445 | e | 386,550 | |

Park River Holdings, Initial Term Loan, 3 Month LIBOR +3.25% | | 4.00 | | 12/28/2027 | | 201,651 | e | 197,528 | |

PetSmart, Initial Term Loan, 3 Month LIBOR +3.75% | | 4.50 | | 2/12/2028 | | 124,972 | e | 124,738 | |

Staples, 2019 Refinancing New Term Loan B-1, 3 Month LIBOR +5.00% | | 5.32 | | 4/12/2026 | | 193,981 | e | 183,757 | |

Woof Holdings, First Lien Initial Term Loan, 3 Month LIBOR +3.75% | | 4.68 | | 12/21/2027 | | 357,613 | e | 355,378 | |

| | 2,088,369 | |

Semiconductors & Semiconductor Equipment - .4% | | | | | |

Natel Engineering, Initial Term Loan, 1-6 Month LIBOR +6.25% | | 7.50 | | 4/30/2026 | | 668,480 | e | 655,946 | |

Ultra Clean Holdings, Second Amendment Term Loan B, 1 Month LIBOR +3.75% | | 4.21 | | 8/27/2025 | | 237,339 | e | 237,140 | |

| | 893,086 | |

Technology Hardware & Equipment - .6% | | | | | |

Access CIG, First Lien Term Loan B, 1 Month LIBOR +3.75% | | 4.21 | | 2/27/2025 | | 170,967 | e | 168,700 | |

Atlas CC Acquisition, First Lien Term Loan B, 3 Month LIBOR +4.25% | | 5.00 | | 5/25/2028 | | 722,021 | e | 720,104 | |

Atlas CC Acquisition, First Lien Term Loan C, 3 Month LIBOR +4.25% | | 5.00 | | 5/25/2028 | | 146,852 | e | 146,462 | |

Marnix SAS, Additional Term Loan B, 3 Month SOFR +4.00% | | 4.50 | | 8/2/2028 | | 92,392 | e | 91,150 | |

26

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a,b | Value ($) | |

Floating Rate Loan Interests - 47.4% (continued) | | | | | |

Technology Hardware & Equipment - .6% (continued) | | | | | |

VeriFone Systems, First Lien Initial Term Loan, 3 Month LIBOR +4.00% | | 4.50 | | 8/20/2025 | | 200,563 | e | 198,056 | |

| | 1,324,472 | |

Telecommunication Services - .7% | | | | | |

CCI Buyer, First Lien Initial Term Loan, 3 Month Term SOFR +4.00% | | 4.75 | | 12/17/2027 | | 667,540 | e | 659,753 | |

Connect Finco, Amendment No. 1 Refinancing Term Loan, 1 Month LIBOR +3.50% | | 4.50 | | 12/12/2026 | | 261,202 | e | 259,439 | |

Crown Subsea Communications, Initial Term Loan, 1 Month LIBOR +4.75% | | 5.50 | | 4/27/2027 | | 270,264 | e | 269,812 | |

Cyxtera DC Holdings, First Lien Initial Term Loan, 3 Month LIBOR +3.00% | | 4.00 | | 5/1/2024 | | 161,572 | e | 160,260 | |

West, Initial Term Loan B, 3 Month LIBOR +4.00% | | 5.00 | | 10/10/2024 | | 159,797 | e | 146,505 | |

| | 1,495,769 | |

Transportation - .1% | | | | | |

OLA Netherlands, Term Loan, 3 Month Term SOFR +6.25% | | 7.00 | | 12/3/2026 | | 148,358 | e | 144,092 | |

Worldwide Express, First Lien Initial Term Loan, 3 Month LIBOR +4.25% | | 5.26 | | 7/26/2028 | | 94,819 | e | 94,034 | |

| | 238,126 | |

Utilities - .1% | | | | | |

Eastern Power, Term Loan B, 3 Month LIBOR +3.75% | | 4.76 | | 10/2/2025 | | 299,983 | e | 214,881 | |

Total Floating Rate Loan Interests

(cost $108,575,205) | | 105,922,846 | |

27

STATEMENT OF INVESTMENTS (continued)