American Beacon Sound Point Enhanced Income Fund (SPEYX)

Filed: 5 Nov 20, 1:27pm

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23326

AMERICAN BEACON SOUND POINT ENHANCED INCOME FUND

(Exact name of registrant as specified in charter)

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(Address of principal executive offices)-(Zip code)

GENE L. NEEDLES, JR., PRESIDENT

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(Name and address of agent for service)

Registrant’s telephone number, including area code: (817) 391-6100

Date of fiscal year end: August 31, 2020

Date of reporting period: August 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

About American Beacon Advisors, Inc.

Since 1986, American Beacon Advisors, Inc. has offered a variety of products and investment advisory services to numerous institutional and retail clients, including a variety of mutual funds, corporate cash management, and separate account management.

Our clients include defined benefit plans, defined contribution plans, foundations, endowments, corporations, financial planners, and other institutional investors. With American Beacon Advisors, Inc., you can put the experience of a multi-billion dollar asset management firm to work for your company.

SOUND POINT ENHANCED INCOME FUND

All investing involves risk including the possible loss of principal. The Fund is a non-diversified, closed-end fund structured as an “interval fund” and designed primarily for long-term investors. The Fund’s use of fixed-income and variable-rate securities, such as loans and related instruments of varying levels of seniority, corporate debt and notes, high-yield securities, CLOs, CLNs and derivatives entails interest rate, liquidity, market and credit risks. The Fund’s ability to borrow for investment purposes and otherwise use leverage can magnify these risks. There is no secondary market for the Fund’s shares, and the Fund expects that no secondary market will develop. Even though the Fund will make quarterly repurchase offers for its outstanding shares, investors should consider shares of the Fund to be an illiquid investment. Investing in foreign securities may involve heightened risk due to currency fluctuations and economic and political risks. There is no guarantee that investors will be able to sell their shares at any given time or in the quantity desired.

Please see the prospectus for a complete discussion of the Fund’s risks. There can be no assurances that the investment objectives of this Fund will be met.

The American Beacon Interval Funds are comprised of the American Beacon Sound Point Enhanced Income Fund and the American Beacon Apollo Total Return Fund.

Any opinions herein, including forecasts, reflect our judgment as of the end of the reporting period and are subject to change. Each advisor’s strategies and the Fund’s portfolio composition will change depending on economic and market conditions. This report is not a complete analysis of market conditions and therefore, should not be relied upon as investment advice. Although economic and market information has been compiled from reliable sources, American Beacon Advisors, Inc. makes no representation as to the completeness or accuracy of the statements contained herein.

American Beacon Advisors | August 31, 2020 |

Contents

| 1 | ||||

| 4 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 15 | ||||

| 18 | ||||

| 43 | ||||

| 45 | ||||

Disclosures Regarding the Approval of the Management and Investment Advisory Agreements | 46 | |||

| 50 | ||||

| 56 | ||||

| Back Cover |

| Dear Shareholders,

Unlike anything we’ve experienced in our lifetimes, the COVID-19 pandemic continues to have an overwhelming effect on the world’s population, economies and markets. While news reports in the first half of this reporting period highlighted the many headwinds affecting the global economy and contributing to market volatility – including the U.S. trade war with China, Brexit, disruptions in the Middle East and protests in Hong Kong – the second half of this reporting period has been dominated by headlines related to the virus:

u On March 15, the Federal Reserve cut the federal funds rate by 100 basis points (1%) to a range of 0% to 0.25%, and announced quantitative easing would be unlimited. |

| u | Also in March, the U.S. government passed a stimulus package in three phases: phase one for approximately $8.3 billion, phase two for approximately $100 billion, and phase three for approximately $2 trillion. |

| u | On April 20, the price of U.S. oil turned negative for the first time in history, closing at -$37.60 per barrel for oil deliveries in May. However, by the end of August, the average crude oil spot price – which calculates an equally weighted price for West Texas Intermediate, Brent and Dubai crude oils – was $43.44 per barrel. |

| u | Although equity markets around the world have rebounded since the lows experienced earlier this year, uncertainty and volatility remain while economies continue to feel the effects of the pandemic. In the U.S., real gross domestic product had an annualized decline of 31.7% for the second quarter – reflecting the sharpest economic contraction in modern history, although slightly less than the 32.9% initially estimated. |

| u | As of August 30, the virus had infected more than 24.8 million individuals around the world, resulting in more than 838,000 deaths. The U.S. alone accounted for more than 5.8 million confirmed cases and more than 180,000 deaths. |

Now more than ever, we recognize that fear of loss can be a powerful emotion, leading many investors to make short-term decisions subject to a variety of potential error-leading biases. Unfortunately, short-term investment decisions may derail future plans. We encourage investors to maintain focus on their long-term financial goals, working with financial professionals to make thoughtful adjustments to their changing needs.

The three Ds – direction, discipline and diversification – may help frame this conversation.

| u | Direction: Achieving your long-term financial goals requires an individualized plan of action. You may want your plan to provide some measure of protection against periods of geopolitical turmoil, economic uncertainty, market volatility and job insecurity. Your plan should be reviewed annually and be adjusted in the event your long-range needs change. |

| u | Discipline: Long-term, systematic participation in an investment portfolio requires your resolution to stay the course. Spending time in the market – rather than trying to time the market – may place you in a better position to reach your long-term financial goals. |

| u | Diversification: By investing in different investment styles and asset classes, you may be able to help mitigate financial risks across your investment portfolio. By allocating your investment portfolio according to your risk-tolerance level, you may be better positioned to weather storms and achieve your long-term financial goals. |

1

President’s Message

American Beacon has endeavored to provide investors with a disciplined approach to realizing long-term financial goals since 1986. As a manager of managers, we strive to provide investment products that may enable investors to participate during market upswings while potentially insulating against market downswings. The investment teams behind our mutual funds seek to produce consistent, long-term results rather than focus only on short-term movements in the markets. In managing our investment products, we emphasize identifying opportunities that offer the potential for long-term rewards.

Thank you for staying the course with American Beacon. For additional information about our investment products or to access your account information, please visit our website at www.americanbeaconfunds.com.

Best Regards,

Gene L. Needles, Jr.

President

American Beacon Sound Point Enhanced Income Fund

2

Global Bond Market Overview

August 31, 2020 (Unaudited)

The period began with the credit markets grinding steadily tighter through the end of calendar year 2019. U.S. investment-grade and high-yield bonds fared particularly well as the Federal Reserve’s concerns around potentially slower global growth, low inflation and lingering trade uncertainty resulted in three interest rate cuts in 2019 and provided a meaningful tailwind for risk assets. From August 31, 2019 through December 31, 2019, the ICE BofA U.S. Corporate Index (“Investment Grade”) returned 0.5%, the ICE BofA U.S. High Yield Index (“High Yield”) returned 2.9%, the S&P/LSTA Leveraged Loan Index (“Loans”) returned 2.2% and the JP Morgan Emerging Market Bond Global Diversified Index (“Emerging Market Debt”) returned 1.4%. By comparison, the ICE BofA U.S. Treasury Index (“Treasuries”) returned -1.8%.

Markets entered 2020 with a flurry of tense global headlines, which muted gains in various credit sectors. Escalating tensions between the U.S. and Iran, the initial outbreak of COVID-19 and a ramp up of U.S. presidential election rhetoric caused investors to look for the sidelines as concerns mounted. By mid-March, virus lockdowns were in place in many countries around the world, and the stampede into safe-haven assets had begun. Unlike the slow-building correction during the 2008 financial crisis, this crisis took place seemingly overnight.

In February 2020, the S&P 500 Index closed at an all-time high. However, by the end of March, it was down nearly 20% year to date and had officially entered bear-market territory. March registered declines across the board: the CBOE Volatility Index registered the highest reading since 2009; oil markets had their worst month since futures started trading in 1983 and West Texas Intermediate (“WTI”) crude oil benchmark fell 55%; the 10-year Treasury briefly traded at a record low 0.32%; Investment Grade fell 7.5%, its worst monthly performance in history; and High Yield declined nearly 12%. Spreads and yields in the high-yield and loan markets reached their widest levels since the financial crisis in 2008.

In response, the Fed implemented a far-reaching set of programs measuring in the trillions of dollars that dwarfed all previous policy accommodations. The huge wave of money led to a rapid turnaround in investor sentiment and a rebound in the markets. Congress also did its part by expanding unemployment benefits and providing financing to cash-starved companies, among other programs.

In the second quarter of 2020, High Yield was up 9.6%, Investment Grade returned 9.3% and the S&P 500 Index gained 20.5%. Several countries made progress re-opening their economies, and the corporate bond market opened with immense volume allowing issuers to raise large amounts of liquidity. Despite investors’ initial concern about the economic impact of the virus, the sheer volume of money injected into the system by the U.S. government brought risk markets back to life. Unfortunately, not all companies could be saved from the economic fallout. By period end, markets began to witness an uptick in distressed credit. As such, caution remained as periodic episodes of volatility were expected to surface in the foreseeable future.

For the 12-month period ended August 31, 2020, Investment Grade returned 7.4%, High Yield returned 3.7%, Loans returned 0.9% and Emerging Market Debt returned 2.7%. Given the record-low interest rates, Treasuries also performed well with a 7.0% return.

3

American Beacon Sound Point Enhanced Income FundSM

August 31, 2020 (Unaudited)

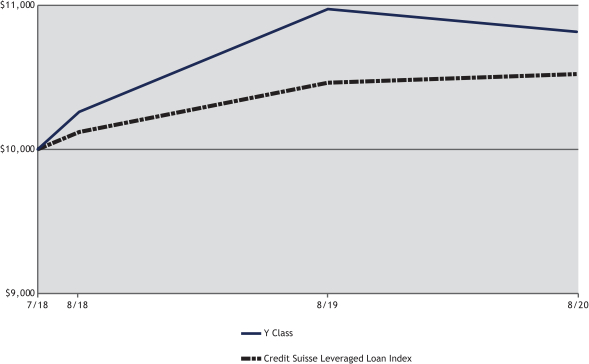

The Y Class of the American Beacon Sound Point Enhanced Income Fund (the “Fund”) returned -1.45% for the twelve months ended August 31, 2020. The Fund underperformed the Credit Suisse Leveraged Loan Index (the “Index”) return of 0.57% for the same period. For further comparison, the Fund has returned 3.68%, annualized, since inception compared to the Index return of 2.37% for the same period.

Comparison of Change in Value of a $10,000 Investment for the period from 07/02/2018 through 08/31/2020

| Total Returns for the Period ended August 31, 2020 |

| |||||||||||||||||||||

Ticker | 1 Year | Since Inception | Value of $10,000 08/31/2020 | |||||||||||||||||||

Y Class (1,2,4) | SPEYX | (1.45 | )% | 3.68 | % | $ | 10,814 | |||||||||||||||

T Class with sales charge (1,2,4) | SPETX | (5.38 | )% | 1.76 | % | $ | 10,385 | |||||||||||||||

T Class without sales charge (1,2,4) | SPETX | (2.42 | )% | 3.21 | % | $ | 10,707 | |||||||||||||||

Credit Suisse Leveraged Loan Index (3) | 0.57 | % | 2.37 | % | $ | 10,521 | ||||||||||||||||

| 1. | Performance shown is historical and is not indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is calculated based on the published end of day net asset values as of the date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month end, please visit www.americanbeaconfunds.com or call 1-800-967-9009. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights. T Class shares have a maximum sales charge of 3.00%. |

| 2. | A portion of the fees charged to both of the Classes has been waived since Fund inception. Performance prior to waiving fees was lower than actual returns shown. |

| 3. | The Credit Suisse Leveraged Loan Index is an index designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market. One cannot directly invest in an index. |

| 4. | The Total Annual Fund Operating Expense ratios set forth in the most recent Fund prospectus for the Y and T Class shares were 9.65% and 10.25%, respectively. (The ratios include estimated expenses related to interest payments on borrowed funds.) The expense ratios above may vary from the expense ratios presented in other sections of this report that are based on expenses incurred during the period covered by this report. |

4

American Beacon Sound Point Enhanced Income FundSM

Performance Overview

August 31, 2020 (Unaudited)

The Fund’s overweight positions in smaller and lower-rated issuers were the primary causes of its underperformance during the period. Within the Index, low-rated issuers were the most severely impacted by the coronavirus as industries shuttered and unemployment surged. In particular, the Fund’s overweight position in triple-C rated issues was the most adversely affected.

The Fund did, however, benefit from its traditional underweight position in the energy, commodity, and retail sectors as they were severely impacted by the virus shutdowns. Conversely, the Fund also typically avoids segments within the health care industry given their low relative value; however, they performed well during this period given the focus on healthcare services and vaccine development.

The Fund also benefitted from its exposure to fixed-rate high-yield bonds. While the Fund was primarily invested in floating-rate bank loan instruments, it held approximately 13% exposure to traditional high yield at period end, which outperformed as yields declined.

To a lesser extent, the Fund also experienced certain credit events during the period which weighed on performance. Disruptions in company transactions, such as selling or merging business segments, and contractions in consumer activity led issuers to engage in debt restructurings or negotiate with creditors for financial flexibility. While the Fund’s holdings are generally well secured by collateral of the issuer, the process of restructuring can lead to volatility, especially in unsettled markets.

The Fund’s exposure to smaller issuers also hindered performance as such companies generally have less financial flexibility during periods of market stress. While they may offer attractive risk-adjusted returns and are overlooked by investors in calm markets, they tend to lag during periods of volatility. Investors gravitated toward the largest and most-liquid issues in the Index, and relative value considerations were temporarily put on hold.

The U.S. Government’s extraordinary support for the economy helped to mitigate the impact of the virus and produced a rapid recovery by period end. The large issues that investors sold for liquidity when the crisis hit were the first to recover as markets stabilized. Additionally, the new-issue market surged as markets opened for companies to raise much-needed cash at very attractive levels for investors. The Fund sought to take advantage of these opportunities in the new-issue market as cash flows and trading allowed. By period end, the largest issuers had produced the highest total returns in the Index.

While the period was unusual, the Fund maintained its focus on generating higher yield and lower volatility than the Index over a market cycle. The sub-advisor continued to build a defensive portfolio with attractive risk/reward opportunities in issuers that they believe were oversold, well-capitalized and less correlated to the pandemic.

5

American Beacon Sound Point Enhanced Income FundSM

Performance Overview

August 31, 2020 (Unaudited)

| Top Ten Holdings (% Net Assets) |

| |||||||

| LogMeIn, Inc., Due 8/14/2027, Term Loan B |

| 4.2 | ||||||

| Informatica LLC, 7.125%, Due 2/25/2025, 2020 USD 2nd Lien Term Loan |

| 2.9 | ||||||

| EIG Investors Corp., 10.875%, Due 2/1/2024 |

| 2.2 | ||||||

| Mileage Plus Holdings LLC, 6.250%, Due 6/25/2027, 2020 Term Loan B, (3-mo. LIBOR + 5.250%) |

| 2.2 | ||||||

| G-III Apparel Group Ltd., 7.875%, Due 8/15/2025 |

| 2.1 | ||||||

| AqGen Ascensus, Inc., 5.000%, Due 12/13/2026, 2020 Term Loan, (1-mo. LIBOR + 4.000%) |

| 2.1 | ||||||

| WP CityMD Bidco LLC, 5.500%, Due 8/13/2026, 2019 Term Loan B, (3-mo. LIBOR + 4.500%, 6-mo. LIBOR + 4.500%) |

| 2.1 | ||||||

| Tutor Perini Corp., Due 8/13/2027, Term Loan B |

| 2.1 | ||||||

| Ivanti Software, Inc., 10.000%, Due 1/20/2025, 2017 2nd Lien Term Loan, (1-mo. LIBOR + 9.000%) |

| 1.9 | ||||||

| JetBlue Airways Corp., 6.250%, Due 6/17/2024, Term Loan, (3-mo. LIBOR + 5.250%) |

| 1.9 | ||||||

| Total Fund Holdings | 94 | |||||||

| Sector Allocation (% Investments) |

| |||||||

| Technology | 34.6 | |||||||

| Consumer, Non-Cyclical | 17.2 | |||||||

| Consumer, Cyclical | 17.1 | |||||||

| Communications | 15.8 | |||||||

| Financial | 7.9 | |||||||

| Industrial | 4.0 | |||||||

| Utilities | 3.3 | |||||||

| Diversified | 0.1 | |||||||

6

American Beacon Sound Point Enhanced Income FundSM

August 31, 2020 (Unaudited)

| American Beacon Sound Point Enhanced Income Fund |

| ||||||||||||||

| Beginning Account Value 3/1/2020 | Ending Account Value 8/31/2020 | Expenses Paid During Period 3/1/2020-8/31/2020* | |||||||||||||

| Y Class | |||||||||||||||

| Actual | $1,000.00 | $998.40 | $7.33 | ||||||||||||

| Hypothetical** | $1,000.00 | $1,017.80 | $7.41 | ||||||||||||

| T Class | |||||||||||||||

| Actual | $1,000.00 | $990.40 | $16.11 | ||||||||||||

| Hypothetical** | $1,000.00 | $1,008.95 | $16.26 | ||||||||||||

| * | Expenses are equal to the Fund’s annualized expense ratios for the six-month period of 1.46% and 3.22% for the Y and T Classes, respectively, multiplied by the average account value over the period, multiplied by the number derived by dividing the number of days in the most recent fiscal half-year (184) by days in the year (366) to reflect the half-year period. |

| ** | 5% return before expenses. |

7

American Beacon Sound Point Enhanced Income FundSM

Report of Independent Registered Public Accounting Firm

To the Shareholders and the Board of Trustees of American Beacon Sound Point Enhanced Income Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of American Beacon Sound Point Enhanced Income Fund (the “Fund”), including the schedule of investments, as of August 31, 2020, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the two years in the period then ended and the period from July 2, 2018 (commencement of operations) to August 31, 2018, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund at August 31, 2020, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the two years in the period then ended and the period from July 2, 2018 (commencement of operations) to August 31, 2018, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of August 31, 2020, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more American Beacon investment companies since 1987.

Dallas, Texas

October 28, 2020

8

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

| Shares | Fair Value | ||||||||||||||

| COMMON STOCKS - 0.00% | |||||||||||||||

| Consumer Discretionary - 0.00% | |||||||||||||||

| Commercial Services & Supplies - 0.00% | |||||||||||||||

| Constellis Holdings LLCA | 72 | $ | 54 | ||||||||||||

|

| ||||||||||||||

| Entertainment - 0.00% | |||||||||||||||

| Deluxe EntertainmentA | 726 | 309 | |||||||||||||

|

| ||||||||||||||

Total Consumer Discretionary | 363 | ||||||||||||||

|

| ||||||||||||||

Total Common Stocks (Cost $3,714) | 363 | ||||||||||||||

|

| ||||||||||||||

| Principal Amount | |||||||||||||||

| BANK LOAN OBLIGATIONSB - 75.46% | |||||||||||||||

| Communications - 10.41% | |||||||||||||||

| Advertising - 0.79% | |||||||||||||||

| ABG Intermediate Holdings LLC, 6.250%, Due 9/27/2024, 2020 Incremental Term Loan, (2-mo. LIBOR + 5.250%) | $ | 75,000 | 73,875 | ||||||||||||

|

| ||||||||||||||

| Internet - 3.03% | |||||||||||||||

| Airbnb, Inc., 8.500%, Due 4/17/2025, Term Loan, (1-mo. LIBOR + 7.500%, 3-mo. LIBOR + 7.500%) | 44,000 | 46,420 | |||||||||||||

| ION Trading Technologies SARL, 5.072%, Due 11/21/2024, USD Incremental Term Loan B, (3-mo. LIBOR + 4.000%) | 149,740 | 146,130 | |||||||||||||

| WeddingWire, Inc., 4.808%, Due 12/19/2025, 1st Lien Term Loan, (3-mo. LIBOR + 4.500%) | 96,630 | 92,281 | |||||||||||||

|

| ||||||||||||||

| 284,831 | |||||||||||||||

|

| ||||||||||||||

| Media - 1.57% | |||||||||||||||

| Cengage Learning, Inc., 5.250%, Due 6/7/2023, 2016 Term Loan B, (3-mo. LIBOR + 4.250%) | 21,666 | 17,793 | |||||||||||||

| NEP/NCP Holdco, Inc., 3.406%, Due 10/20/2025, 2018 1st Lien Term Loan, (1-mo. LIBOR + 3.250%) | 99,747 | 83,645 | |||||||||||||

| Univision Communications, Inc., 4.750%, Due 3/13/2026, 2020 Replacement Term Loan, (1-mo. LIBOR + 3.750%) | 47,047 | 45,929 | |||||||||||||

|

| ||||||||||||||

| 147,367 | |||||||||||||||

|

| ||||||||||||||

| Telecommunications - 5.02% | |||||||||||||||

| Global Tel*Link Corp., 4.406%, Due 11/29/2025, 2018 1st Lien Term Loan, (1-mo. LIBOR + 4.250%) | 9,317 | 8,086 | |||||||||||||

| LogMeIn, Inc., Due 8/14/2027, Term Loan BC | 400,000 | 389,832 | |||||||||||||

| West Corp., 5.000%, Due 10/10/2024, 2017 Term Loan, (3-mo. LIBOR + 4.000%) | 81,702 | 72,911 | |||||||||||||

|

| ||||||||||||||

| 470,829 | |||||||||||||||

|

| ||||||||||||||

Total Communications | 976,902 | ||||||||||||||

|

| ||||||||||||||

| Consumer, Cyclical - 11.11% | |||||||||||||||

| Airlines - 4.01% | |||||||||||||||

| JetBlue Airways Corp., 6.250%, Due 6/17/2024, Term Loan, (3-mo. LIBOR + 5.250%) | 175,000 | 174,256 | |||||||||||||

| Mileage Plus Holdings LLC, 6.250%, Due 6/25/2027, 2020 Term Loan B, (3-mo. LIBOR + 5.250%) | 200,000 | 202,126 | |||||||||||||

|

| ||||||||||||||

| 376,382 | |||||||||||||||

|

| ||||||||||||||

| Auto Manufacturers - 0.20% | |||||||||||||||

| OEConnection LLC, | |||||||||||||||

Due 9/25/2026, 2019 Delayed Draw Term LoanC D | 1,173 | 1,127 | |||||||||||||

4.155% - 5.072%, Due 9/25/2026, 2019 Term Loan B, (1-mo. LIBOR + 4.000%, | 18,586 | 17,842 | |||||||||||||

|

| ||||||||||||||

| 18,969 | |||||||||||||||

|

| ||||||||||||||

See accompanying notes

9

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

| Principal Amount | Fair Value | ||||||||||||||

| Consumer, Cyclical - 11.11% (continued) | |||||||||||||||

| Auto Parts & Equipment - 0.05% | |||||||||||||||

| Trico Group LLC, 8.500%, Due 2/2/2024, 2020 Term Loan B, (2-mo. LIBOR + 7.500%) | $ | 4,808 | $ | 4,711 | |||||||||||

|

| ||||||||||||||

| Entertainment - 1.62% | |||||||||||||||

| Deluxe Entertainment Services Group, Inc., | |||||||||||||||

6.000%, Due 3/25/2024, 2019 1st Lien Term Loan, PIK (in-kind rate 1.500%)E F | 3,576 | 3,218 | |||||||||||||

7.000%, Due 9/25/2024, 2019 2nd Lien Term Loan, PIK (in-kind rate 2.500%)E F | 7,499 | 5,624 | |||||||||||||

| William Morris Endeavor Entertainment LLC, | |||||||||||||||

2.910%, Due 5/18/2025, 2018 1st Lien Term Loan, (1-mo. LIBOR + 2.750%) | 32,891 | 26,560 | |||||||||||||

9.500%, Due 5/18/2025, 2020 Term Loan B2, (1-mo. LIBOR + 8.500%) | 119,700 | 116,109 | |||||||||||||

|

| ||||||||||||||

| 151,511 | |||||||||||||||

|

| ||||||||||||||

| Leisure Time - 1.85% | |||||||||||||||

| TopGolf International, Inc., 5.808%, Due 2/8/2026, Term Loan B, (3-mo. LIBOR + 5.500%) | 97,254 | 91,804 | |||||||||||||

| Varsity Brands, Inc., 4.500%, Due 12/15/2024, 2017 Term Loan B, (1-mo. LIBOR + 3.500%) | 99,745 | 81,416 | |||||||||||||

|

| ||||||||||||||

| 173,220 | |||||||||||||||

|

| ||||||||||||||

| Lodging - 0.77% | |||||||||||||||

| Caesars Resort Collection LLC, 4.703% - 4.772%, Due 7/21/2025, 2020 Term Loan B1, (3-mo. LIBOR + 4.500%) | 75,000 | 72,610 | |||||||||||||

|

| ||||||||||||||

| Office Furnishings - 0.00% | |||||||||||||||

| VIP Cinema Holdings, Inc., | |||||||||||||||

10.250%, Due 6/26/2020, 2020 New Money Term Loan, (3-mo. LIBOR + 8.000%)E F | 795 | 118 | |||||||||||||

10.250%, Due 2/24/2021, 2020 DIP Exit Term Loan, (3-mo. LIBOR + 8.000%)E F | 23 | 23 | |||||||||||||

10.250%, Due 3/1/2023, USD Term Loan B, (3-mo. PRIME + 7.000%) | 2,044 | 82 | |||||||||||||

|

| ||||||||||||||

| 223 | |||||||||||||||

|

| ||||||||||||||

| Retail - 2.61% | |||||||||||||||

| Bass Pro Group LLC, 6.072%, Due 9/25/2024, Term Loan B, (3-mo. LIBOR + 5.000%) | 98,885 | 98,483 | |||||||||||||

| NPC International, Inc., | |||||||||||||||

3.000%, Due 1/21/2021, 2020 Incremental Priority Term Loan, (1-mo. LIBOR + 1.500%)C D | 6,768 | 6,735 | |||||||||||||

4.500%, Due 4/19/2024, 1st Lien Term Loan, (3-mo. LIBOR + 3.500%) | 29,847 | 20,930 | |||||||||||||

| SP PF Buyer LLC, 4.656%, Due 12/22/2025, Term Loan, (1-mo. LIBOR + 4.500%) | 107,881 | 96,733 | |||||||||||||

| Staples, Inc., 5.251%, Due 4/16/2026, 7 Year Term Loan, (3-mo. LIBOR + 5.000%) | 25,869 | 21,903 | |||||||||||||

|

| ||||||||||||||

| 244,784 | |||||||||||||||

|

| ||||||||||||||

Total Consumer, Cyclical | 1,042,410 | ||||||||||||||

|

| ||||||||||||||

| Consumer, Non-Cyclical - 11.57% | |||||||||||||||

| Commercial Services - 1.13% | |||||||||||||||

| APX Group, Inc., 5.156% - 7.250%, Due 12/31/2025, 2020 Term Loan, (1-mo. LIBOR + 5.000%, 3-mo. PRIME + 4.000%) | 1,970 | 1,942 | |||||||||||||

| New Constellis Borrower LLC, 11.000%, Due 6/30/2021, 2020 Priority Term Loan, (1-mo. LIBOR + 10.000%) | 2,196 | 2,152 | |||||||||||||

| PAE Holding Corp., 6.500%, Due 10/20/2022, 1st Lien Term Loan, (1-mo. LIBOR + 5.500%) | 97,059 | 96,250 | |||||||||||||

| Travelport Finance SARL, 6.072%, Due 5/29/2026, 2019 Term Loan, (3-mo. LIBOR + 5.000%) | 3,980 | 2,651 | |||||||||||||

| USS Ultimate Holdings, Inc., 4.750%, Due 8/25/2024, 1st Lien Term Loan, (3-mo. LIBOR + 3.750%) | 2,940 | 2,853 | |||||||||||||

|

| ||||||||||||||

| 105,848 | |||||||||||||||

|

| ||||||||||||||

| Food - 1.04% | |||||||||||||||

| Snacking Investments Bidco Pty Ltd., 5.000%, Due 12/18/2026, Term Loan, (1-mo. LIBOR + 4.000%) | 98,734 | 97,418 | |||||||||||||

|

| ||||||||||||||

See accompanying notes

10

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

| Principal Amount | Fair Value | ||||||||||||||

| Consumer, Non-Cyclical - 11.57% (continued) | |||||||||||||||

| Health Care - Products - 1.05% | |||||||||||||||

| Athenahealth, Inc., 4.818%, Due 2/11/2026, 2019 Term Loan B, (3-mo. LIBOR + 4.500%) | $ | 99,747 | $ | 98,813 | |||||||||||

|

| ||||||||||||||

| Health Care - Services - 7.32% | |||||||||||||||

| Compassus Intermediate, Inc., 6.072%, Due 12/31/2026, Term Loan B, (3-mo. LIBOR + 5.000%) | 99,375 | 98,133 | |||||||||||||

| Da Vinci Purchaser Corp., 5.238%, Due 1/8/2027, 2019 Term Loan, (3-mo. LIBOR + 4.000%) | 100,000 | 99,292 | |||||||||||||

| Envision Healthcare Corp., 3.906%, Due 10/10/2025, 2018 1st Lien Term Loan, (1-mo. LIBOR + 3.750%) | 86,720 | 62,586 | |||||||||||||

| Global Medical Response, Inc., 4.250%, Due 4/28/2022, 2018 Term Loan B1, (3-mo. LIBOR + 3.250%) | 99,744 | 98,711 | |||||||||||||

| US Renal Care, Inc., 5.188%, Due 6/26/2026, 2019 Term Loan B, (1-mo. LIBOR + 5.000%) | 134,372 | 130,956 | |||||||||||||

| WP CityMD Bidco LLC, 5.500% - 5.572%, Due 8/13/2026, 2019 Term Loan B, (3-mo. LIBOR + 4.500%, 6-mo. LIBOR + 4.500%) | 199,000 | 197,476 | |||||||||||||

|

| ||||||||||||||

| 687,154 | |||||||||||||||

|

| ||||||||||||||

| Pharmaceuticals - 1.03% | |||||||||||||||

| US Renal Care, Inc., 7.906%, Due 9/26/2025, 2017 2nd Lien Term Loan, (1-mo. LIBOR + 7.750%) | 100,000 | 96,375 | |||||||||||||

|

| ||||||||||||||

Total Consumer, Non-Cyclical | 1,085,608 | ||||||||||||||

|

| ||||||||||||||

| Diversified - 0.12% | |||||||||||||||

| Holding Companies - Diversified - 0.12% | |||||||||||||||

| Genesis Specialist Care Finance Ltd., 6.000%, Due 5/14/2027, 2020 USD Term Loan B, (3-mo. LIBOR + 5.000%) | 11,970 | 11,342 | |||||||||||||

|

| ||||||||||||||

| Energy - 0.01% | |||||||||||||||

| Oil & Gas - 0.01% | |||||||||||||||

| McDermott Technology Americas, Inc., 3.156%, Due 6/30/2024, 2020 Make Whole Term Loan, (1-mo. LIBOR + 3.000%) | 807 | 718 | |||||||||||||

|

| ||||||||||||||

| Financial - 7.04% | |||||||||||||||

| Diversified Financial Services - 5.93% | |||||||||||||||

| AqGen Ascensus, Inc., 5.000%, Due 12/13/2026, 2020 Term Loan, (1-mo. LIBOR + 4.000%) | 200,000 | 198,500 | |||||||||||||

| Aretec Group, Inc., 4.406%, Due 10/1/2025, 2018 Term Loan, (1-mo. LIBOR + 4.250%) | 10,775 | 9,994 | |||||||||||||

| Blucora, Inc., 5.000%, Due 5/22/2024, 2017 Term Loan B, (6-mo. LIBOR + 4.000%) | 100,000 | 98,250 | |||||||||||||

| GreenSky Holdings LLC, 3.438%, Due 3/31/2025, 2018 Term Loan B, (1-mo. LIBOR + 3.250%) | 4,949 | 4,751 | |||||||||||||

| Hudson River Trading LLC, Due 2/18/2027, 2020 Term Loan BC | 100,000 | 98,875 | |||||||||||||

| IG Investment Holdings LLC, 5.000%, Due 5/23/2025, 2018 1st Lien Term Loan, (3-mo. LIBOR + 4.000%) | 150,000 | 145,688 | |||||||||||||

|

| ||||||||||||||

| 556,058 | |||||||||||||||

|

| ||||||||||||||

| Insurance - 1.11% | |||||||||||||||

| AssuredPartners Capital, Inc., 5.500%, Due 2/12/2027, 2020 Incremental Term Loan B, (1-mo. LIBOR + 4.500%) | 99,750 | 99,418 | |||||||||||||

| Asurion LLC, 6.656%, Due 8/4/2025, 2017 2nd Lien Term Loan, (1-mo. LIBOR + 6.500%) | 4,697 | 4,704 | |||||||||||||

|

| ||||||||||||||

| 104,122 | |||||||||||||||

|

| ||||||||||||||

Total Financial | 660,180 | ||||||||||||||

|

| ||||||||||||||

| Industrial - 3.61% | |||||||||||||||

| Electronics - 1.51% | |||||||||||||||

| NorthPole Newco SARL, 7.308%, Due 3/18/2025, Term Loan, (3-mo. LIBOR + 7.000%) | 157,242 | 141,911 | |||||||||||||

|

| ||||||||||||||

| Engineering & Construction - 2.10% | |||||||||||||||

| Tutor Perini Corp., Due 8/13/2027, Term Loan BC | 200,000 | 196,750 | |||||||||||||

|

| ||||||||||||||

Total Industrial | 338,661 | ||||||||||||||

|

| ||||||||||||||

See accompanying notes

11

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

| Principal Amount | Fair Value | ||||||||||||||

| Technology - 28.69% | |||||||||||||||

| Computers - 5.07% | |||||||||||||||

| Corsair Components, Inc., 4.750%, Due 8/28/2024, 2017 1st Lien Term Loan B, (1-mo. LIBOR + 3.750%) | $ | 100,000 | $ | 99,250 | |||||||||||

| Electronics for Imaging, Inc., 5.155%, Due 7/23/2026, Term Loan, (1-mo. LIBOR + 5.000%) | 99,126 | 78,309 | |||||||||||||

| McAfee LLC, | |||||||||||||||

3.906%, Due 9/30/2024, 2018 USD Term Loan B, (1-mo. LIBOR + 3.750%) | 101,237 | 100,188 | |||||||||||||

9.500%, Due 9/29/2025, 2017 2nd Lien Term Loan, (1-mo. LIBOR + 8.500%) | 100,000 | 100,688 | |||||||||||||

| Perforce Software, Inc., 3.906%, Due 7/1/2026, 2020 Term Loan B, (1-mo. LIBOR + 3.750%) | 100,642 | 97,718 | |||||||||||||

|

| ||||||||||||||

| 476,153 | |||||||||||||||

|

| ||||||||||||||

| Software - 23.62% | |||||||||||||||

| Cvent, Inc., 3.906%, Due 11/29/2024, 1st Lien Term Loan, (1-mo. LIBOR + 3.750%) | 74,809 | 64,570 | |||||||||||||

| DCert Buyer, Inc., 4.156%, Due 10/16/2026, 2019 Term Loan B, (1-mo. LIBOR + 4.000%) | 100,685 | 99,364 | |||||||||||||

| DTI Holdco, Inc., 5.750%, Due 9/30/2023, 2018 Term Loan B, (2-mo. LIBOR + 4.750%, 3-mo. LIBOR + 4.750%) | 149,611 | 123,273 | |||||||||||||

| Finastra USA, Inc., 4.500%, Due 6/13/2024, USD 1st Lien Term Loan, (6-mo. LIBOR + 3.500%) | 117,394 | 110,372 | |||||||||||||

| Helios Software Holdings, Inc., 5.322%, Due 10/24/2025, USD Term Loan, (6-mo. LIBOR + 4.250%) | 118,544 | 117,358 | |||||||||||||

| Informatica LLC, 7.125%, Due 2/25/2025, 2020 USD 2nd Lien Term LoanG | 272,000 | 274,494 | |||||||||||||

| Ivanti Software, Inc., | |||||||||||||||

5.250%, Due 1/20/2024, 2017 Term Loan B, (1-mo. LIBOR + 4.250%) | 140,595 | 136,026 | |||||||||||||

10.000%, Due 1/20/2025, 2017 2nd Lien Term Loan, (1-mo. LIBOR + 9.000%) | 200,000 | 180,750 | |||||||||||||

| MA FinanceCo. LLC, 5.250%, Due 6/5/2025, 2020 USD Term Loan B, (3-mo. LIBOR + 4.250%) | 150,000 | 149,438 | |||||||||||||

| Navicure, Inc., 4.156%, Due 10/22/2026, 2019 Term Loan B, (1-mo. LIBOR + 4.000%) | 100,000 | 97,125 | |||||||||||||

| Netsmart, Inc., 4.750%, Due 4/19/2023, Term Loan D1, (3-mo. LIBOR + 3.750%) | 169,558 | 166,167 | |||||||||||||

| Particle Investments SARL, 5.750%, Due 5/14/2027, Term Loan, (1 Week LIBOR + 5.250%) | 150,000 | 145,875 | |||||||||||||

| Project Alpha Intermediate Holding, Inc., 4.500%, Due 4/26/2024, 2017 Term Loan B, (3-mo. LIBOR + 3.500%) | 99,679 | 98,931 | |||||||||||||

| Riverbed Technology, Inc., 4.250%, Due 4/24/2022, 2016 Term Loan, (2-mo. LIBOR + 3.250%, 3-mo. LIBOR + 3.250%) | 149,605 | 132,101 | |||||||||||||

| S2P Acquisition Borrower, Inc., 5.072%, Due 8/14/2026, Term Loan, (3-mo. LIBOR + 4.000%) | 99,435 | 97,882 | |||||||||||||

| Ultimate Software Group, Inc., 4.750%, Due 5/4/2026, 2020 Incremental Term Loan B, (3-mo. LIBOR + 4.000%) | 100,000 | 99,813 | |||||||||||||

| Zelis Healthcare Corp., 4.906%, Due 9/30/2026, Term Loan B, (1-mo. LIBOR + 4.750%) | 122,385 | 122,258 | |||||||||||||

|

| ||||||||||||||

| 2,215,797 | |||||||||||||||

|

| ||||||||||||||

Total Technology | 2,691,950 | ||||||||||||||

|

| ||||||||||||||

| Utilities - 2.90% | |||||||||||||||

| Electric - 2.90% | |||||||||||||||

| Hamilton Projects Acquiror LLC, 5.750%, Due 6/17/2027, Term Loan B, (3-mo. LIBOR + 4.750%) | 100,000 | 99,750 | |||||||||||||

| Pacific Gas & Electric Co., 5.500%, Due 6/23/2025, 2020 Exit Term Loan B, (3-mo. LIBOR + 4.500%) | 175,000 | 172,048 | |||||||||||||

|

| ||||||||||||||

| 271,798 | |||||||||||||||

|

| ||||||||||||||

Total Utilities | 271,798 | ||||||||||||||

|

| ||||||||||||||

Total Bank Loan Obligations (Cost $7,075,612) | 7,079,569 | ||||||||||||||

|

| ||||||||||||||

| CORPORATE OBLIGATIONS - 13.84% | |||||||||||||||

| Communications - 3.69% | |||||||||||||||

| Internet - 2.21% | |||||||||||||||

| EIG Investors Corp., 10.875%, Due 2/1/2024 | 200,000 | 207,000 | |||||||||||||

|

| ||||||||||||||

| Media - 1.21% | |||||||||||||||

| Univision Communications, Inc., 6.625%, Due 6/1/2027H | 113,000 | 113,283 | |||||||||||||

|

| ||||||||||||||

See accompanying notes

12

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

| Principal Amount | Fair Value | ||||||||||||||

| CORPORATE OBLIGATIONS - 13.84% (continued) | |||||||||||||||

| Communications - 3.69% (continued) | |||||||||||||||

| Telecommunications - 0.27% | |||||||||||||||

| Plantronics, Inc., 5.500%, Due 5/31/2023H | $ | 27,000 | $ | 25,488 | |||||||||||

|

| ||||||||||||||

Total Communications | 345,771 | ||||||||||||||

|

| ||||||||||||||

| Consumer, Cyclical - 4.12% | |||||||||||||||

| Airlines - 0.30% | |||||||||||||||

| Mileage Plus Holdings LLC / Mileage Plus Intellectual Property Assets Ltd., 6.500%, Due 6/20/2027H | 26,996 | 28,076 | |||||||||||||

|

| ||||||||||||||

| Auto Parts & Equipment - 1.70% | |||||||||||||||

| Clarios Global LP / Clarios US Finance Co, 8.500%, Due 5/15/2027H | 150,000 | 159,268 | |||||||||||||

|

| ||||||||||||||

| Distribution/Wholesale - 2.12% | |||||||||||||||

| G-III Apparel Group Ltd., 7.875%, Due 8/15/2025H | 200,000 | 198,750 | |||||||||||||

|

| ||||||||||||||

Total Consumer, Cyclical | 386,094 | ||||||||||||||

|

| ||||||||||||||

| Consumer, Non-Cyclical - 3.79% | |||||||||||||||

| Commercial Services - 2.21% | |||||||||||||||

| APX Group, Inc., | |||||||||||||||

7.625%, Due 9/1/2023 | 100,000 | 102,250 | |||||||||||||

6.750%, Due 2/15/2027H | 100,000 | 105,000 | |||||||||||||

|

| ||||||||||||||

| 207,250 | |||||||||||||||

|

| ||||||||||||||

| Health Care - Services - 1.58% | |||||||||||||||

| Air Medical Group Holdings, Inc., 6.375%, Due 5/15/2023H | 25,000 | 24,750 | |||||||||||||

| US Renal Care, Inc., 10.625%, Due 7/15/2027H | 115,000 | 123,912 | |||||||||||||

|

| ||||||||||||||

| 148,662 | |||||||||||||||

|

| ||||||||||||||

Total Consumer, Non-Cyclical | 355,912 | ||||||||||||||

|

| ||||||||||||||

| Technology - 2.24% | |||||||||||||||

| Software - 2.24% | |||||||||||||||

| Granite Merger Sub 2, Inc., 11.000%, Due 7/15/2027H | 101,000 | 105,710 | |||||||||||||

| Solera LLC / Solera Finance, Inc., 10.500%, Due 3/1/2024H | 100,000 | 104,875 | |||||||||||||

|

| ||||||||||||||

| 210,585 | |||||||||||||||

|

| ||||||||||||||

Total Technology | 210,585 | ||||||||||||||

|

| ||||||||||||||

Total Corporate Obligations (Cost $1,267,336) | 1,298,362 | ||||||||||||||

|

| ||||||||||||||

| Shares | |||||||||||||||

| SHORT-TERM INVESTMENTS - 16.94% (Cost $1,589,262) | |||||||||||||||

| Investment Companies - 16.94% | |||||||||||||||

| American Beacon U.S. Government Money Market Select Fund, 0.01%I J | 1,589,262 | 1,589,262 | |||||||||||||

|

| ||||||||||||||

TOTAL INVESTMENTS - 106.24% (Cost $9,935,924) | 9,967,556 | ||||||||||||||

LIABILITIES, NET OF OTHER ASSETS - (6.24%) | (585,645 | ) | |||||||||||||

|

| ||||||||||||||

TOTAL NET ASSETS - 100.00% | $ | 9,381,911 | |||||||||||||

|

| ||||||||||||||

| Percentages are stated as a percent of net assets. | |||||||||||||||

A Non-income producing security.

B Bank loan obligations, unless otherwise stated, carry a floating rate of interest. The coupon rate shown on floating or adjustable rate securities represents the rate at period end.

See accompanying notes

13

American Beacon Sound Point Enhanced Income FundSM

Schedule of Investments

August 31, 2020

C Coupon rates may not be available for all or a portion of bank loans that are unsettled and/or unfunded as of August 31, 2020.

D All or a portion of the security is an Unfunded Loan Commitment. At period end, the amount of unfunded loan commitments was $4,537 or 0.05% of net assets. Of this amount, $1,173 and $3,364 relate to OEConnection LLC and NPC International, Inc., respectively.

E Fair valued pursuant to procedures approved by the Board of Trustees. At period end, the value of these securities amounted to $8,983 or 0.10% of net assets.

F Value was determined using significant unobservable inputs.

G Fixed Rate.

H Security exempt from registration under the Securities Act of 1933. These securities may be resold to qualified institutional buyers pursuant to Rule 144A. At the period end, the value of these securities amounted to $989,112 or 10.54% of net assets. The Fund has no right to demand registration of these securities.

I 7-day yield.

J The Fund is affiliated by having the same investment advisor.

DIP - Debtor-in-possession.

LIBOR - London Interbank Offered Rate.

LLC - Limited Liability Company.

LP - Limited Partnership.

PIK - Payment in Kind.

PRIME - A rate, charged by banks, based on the U.S. Federal Funds rate.

Pty Ltd. - Proprietary Limited.

USD - United States Dollar.

The Fund’s investments are summarized by level based on the inputs used to determine their values. As of August 31, 2020, the investments were classified as described below:

Sound Point Enhanced Income Fund | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||||||

Assets |

| |||||||||||||||||||||||||||

Common Stocks | $ | 363 | $ | - | $ | - | $ | 363 | ||||||||||||||||||||

Bank Loan Obligations(1) | - | 7,070,586 | 8,983 | 7,079,569 | ||||||||||||||||||||||||

Corporate Obligations | - | 1,298,362 | - | 1,298,362 | ||||||||||||||||||||||||

Short-Term Investments | 1,589,262 | - | - | 1,589,262 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||||||

Total Investments in Securities - Assets | $ | 1,589,625 | $ | 8,368,948 | $ | 8,983 | $ | 9,967,556 | ||||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||||||

| (1) | Unfunded loan commitments represent $4,537 at year end. |

U.S. GAAP requires transfers between all levels to/from level 3 be disclosed. During the year ended August 31, 2020, there were no transfers into or out of Level 3.

The following table is a reconciliation of Level 3 assets within the Fund for which significant unobservable inputs were used to determine fair value. Transfers in or out of Level 3 represent the ending value of any security or instrument where a change in the level has occurred from the beginning to the end of the period:

| Security Type | Balance as of 8/31/2019 | Purchases | Sales | Accrued Discounts (Premiums) | Realized Gain (Loss) | Change in Unrealized Appreciation (Depreciation) | Transfer into Level 3 | Transfer out of Level 3 | Balance as of 8/31//2020 | Unrealized Appreciation (Depreciation) at Year End** | ||||||||||||||||||||||||||||||

| Bank Loan Obligations | $ | 31,382 | $ | 12,947 | $ | 23,350 | $ | 461 | $ | (14,455 | ) | $ | 1,998 | $ | - | $ | - | $ | 8,983 | $ | (1,697 | ) | ||||||||||||||||||

| ** | Change in unrealized appreciation (depreciation) attributable to Level 3 securities held at year end. This balance is included in the change in unrealized appreciation (depreciation) on the Statement of Operations. |

For the year ended August 31, 2020, bank loan obligations valued at $8,983 have been classified as Level 3 due to the use of significant unobservable inputs.

See accompanying notes

14

American Beacon Sound Point Enhanced Income FundSM

Statement of Assets and Liabilities

August 31, 2020

Assets: | ||||

Investments in unaffiliated securities, at fair value† | $ | 8,378,294 | ||

Investments in affiliated securities, at fair value‡ | 1,589,262 | |||

Cash | 129,808 | |||

Dividends and interest receivable | 65,476 | |||

Receivable for investments sold | 1,050,725 | |||

Other assets | 107 | |||

Prepaid expenses | 20,163 | |||

|

| |||

Total assets | 11,233,835 | |||

|

| |||

Liabilities: | ||||

Payable for investments purchased | 1,569,166 | |||

Payable for expense reimbursement (Note 2) | 61,424 | |||

Dividends payable | 72,592 | |||

Unfunded loan commitments | 4,537 | |||

Management and sub-advisory fees payable (Note 2) | 9,540 | |||

Service fees payable (Note 2) | 606 | |||

Transfer agent fees payable (Note 2) | 3,356 | |||

Custody and fund accounting fees payable | 14,184 | |||

Professional fees payable | 108,859 | |||

Payable for prospectus and shareholder reports | 7,051 | |||

Other liabilities | 609 | |||

|

| |||

Total liabilities | 1,851,924 | |||

|

| |||

Net assets | $ | 9,381,911 | ||

|

| |||

Analysis of net assets: | ||||

Paid-in-capital | $ | 10,238,081 | ||

Total distributable earnings (deficits)A | (856,170 | ) | ||

|

| |||

Net assets | $ | 9,381,911 | ||

|

| |||

Shares outstanding at no par value (unlimited shares authorized): | ||||

Y Class | 1,005,622 | |||

|

| |||

T ClassB | 10,493 | |||

|

| |||

Net assets: | ||||

Y Class | $ | 9,285,372 | ||

|

| |||

T ClassB | $ | 96,539 | ||

|

| |||

Net asset value, offering and redemption price per share: | ||||

Y Class | $ | 9.23 | ||

|

| |||

T ClassB | $ | 9.20 | ||

|

| |||

† Cost of investments in unaffiliated securities | $ | 8,346,662 | ||

‡ Cost of investments in affiliated securities | $ | 1,589,262 | ||

A The Fund’s investments in affiliated securities did not have unrealized appreciation (depreciation) at year end. | ||||

B The T Class became effective on December 27, 2019 and commenced operations on December 30, 2019 (Note 1). | ||||

See accompanying notes

15

American Beacon Sound Point Enhanced Income FundSM

Statement of Operations

For the year ended August 31, 2020

| Sound Point Enhanced Income Fund | ||||

Investment income: | ||||

Dividend income from affiliated securities (Note 2) | $ | 13,725 | ||

Interest income (net of foreign taxes) | 565,831 | |||

|

| |||

Total investment income | 579,556 | |||

|

| |||

Expenses: |

| |||

Management and sub-advisory fees (Note 2) | 114,656 | |||

Transfer agent fees: | ||||

Y Class (Note 2) | 54,730 | |||

T ClassA | 13,528 | |||

Custody and fund accounting fees | 83,334 | |||

Professional fees | 232,673 | |||

Registration fees and expenses | 21,835 | |||

Distribution fees (Note 2): | ||||

T ClassA | 478 | |||

Prospectus and shareholder report expenses | 26,529 | |||

Trustee fees (Note 2) | 796 | |||

Other expenses | 66,245 | |||

|

| |||

Total expenses | 614,804 | |||

|

| |||

Net fees waived and expenses (reimbursed) (Note 2) | (478,492 | ) | ||

|

| |||

Net expenses | 136,312 | |||

|

| |||

Net investment income | 443,244 | |||

|

| |||

Realized and unrealized gain (loss) from investments: |

| |||

Net realized gain (loss) from: | ||||

Investments in unaffiliated securitiesB | (872,736 | ) | ||

Change in net unrealized appreciation of: | ||||

Investments in unaffiliated securitiesC | 276,550 | |||

|

| |||

Net (loss) from investments | (596,186 | ) | ||

|

| |||

Net (decrease) in net assets resulting from operations | $ | (152,942 | ) | |

|

| |||

A The T Class became effective on December 27, 2019 and commenced operations on December 30, 2019 (Note 1). | ||||

B The Fund did not recognize net realized gains (losses) from the sale of investments in affiliated securities. | ||||

C The Fund’s investments in affiliated securities did not have a change in unrealized appreciation (depreciation) at year end. | ||||

See accompanying notes

16

American Beacon Sound Point Enhanced Income FundSM

Statement of Changes in Net Assets

| Year Ended August 31, 2020 | Year Ended August 31, 2019 | |||||||||||

Increase (decrease) in net assets: | ||||||||||||

Operations: | ||||||||||||

Net investment income | $ | 443,244 | $ | 507,703 | ||||||||

Net realized gain (loss) from investments in unaffiliated securities | (872,736 | ) | 376,725 | |||||||||

Change in net unrealized appreciation (depreciation) of investments in unaffiliated securities | 276,550 | (258,134 | ) | |||||||||

|

|

|

| |||||||||

Net increase (decrease) in net assets resulting from operations | (152,942 | ) | 626,294 | |||||||||

|

|

|

| |||||||||

Distributions to shareholders: | ||||||||||||

Total retained earnings: | ||||||||||||

Y Class | (844,829 | ) | (583,247 | ) | ||||||||

T ClassA | (2,006 | ) | - | |||||||||

|

|

|

| |||||||||

Net distributions to shareholders | (846,835 | ) | (583,247 | ) | ||||||||

|

|

|

| |||||||||

Capital share transactions (Note 8): | ||||||||||||

Proceeds from sales of shares | 124,870 | 5,608,524 | ||||||||||

Reinvestment of dividends and distributions | 372,628 | 426,808 | ||||||||||

Cost of shares redeemed | (520,578 | ) | (864,373 | ) | ||||||||

|

|

|

| |||||||||

Net increase (decrease) in net assets from capital share transactions | (23,080 | ) | 5,170,959 | |||||||||

|

|

|

| |||||||||

Net increase (decrease) in net assets | (1,022,857 | ) | 5,214,006 | |||||||||

|

|

|

| |||||||||

Net assets: | ||||||||||||

Beginning of period | 10,404,768 | 5,190,762 | ||||||||||

|

|

|

| |||||||||

End of period | $ | 9,381,911 | $ | 10,404,768 | ||||||||

|

|

|

| |||||||||

A The T Class became effective on December 27, 2019 and commenced operations on December 30, 2019 (Note 1). |

| |||||||||||

See accompanying notes

17

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

1. Organization and Significant Accounting Policies

The American Beacon Sound Point Enhanced Income Fund (the “Fund”) is a series of a non-diversified, closed-end management investment company of the same name (the “Trust”) that continuously offers two classes of shares of beneficial interest (“Shares”), Y Class and T Class Shares, and is operated as an “interval fund” (as defined below). The Trust was formed on January 12, 2018 as a Delaware statutory trust. The Fund commenced operations on July 2, 2018. American Beacon Advisors, Inc. (the “Manager”) is a Delaware corporation and a wholly-owned subsidiary of Resolute Investment Managers, Inc. (“RIM”) organized in 1986 to provide business management, advisory, administrative, and asset management consulting services to the Trust and other investors. The Manager is registered as an investment advisor under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). RIM is, in turn, a wholly-owned subsidiary of Resolute Acquisition, Inc., which is a wholly-owned subsidiary of Resolute Topco, Inc., a wholly-owned subsidiary of Resolute Investment Holdings, LLC (“RIH”). RIH is owned primarily by Kelso Investment Associates VIII, L.P., KEP VI, LLC and Estancia Capital Partners L.P., investment funds affiliated with Kelso & Company, L.P. (“Kelso”) or Estancia Capital Management, LLC (“Estancia”), which are private equity firms.

The Fund’s Shares are offered on a continuous basis at net asset value (“NAV”) per share. The Fund may close at any time to new investors or new investments and, during such closings, only purchases of Shares by existing shareholders of the Fund (“Shareholders”) or the reinvestment of distributions by existing Shareholders, as applicable, will be permitted. The Fund may re-open to new investments and subsequently close again to new investors or new investments at any time at the discretion of the Manager. Any such opening and closing of the Fund will be disclosed to investors via a supplement to the Prospectus.

The Fund’s Shares are offered through Resolute Investment Distributors, Inc. (the “Distributor”), which is the exclusive distributor of Shares, on a best-efforts basis. The minimum investment is $100,000 for Y Class and $2,500 for T Class, subject to certain exceptions. The Fund reserves the right to reject a purchase order for any reason. Shareholders will not have the right to redeem their Shares. However, as described below, in order to provide liquidity to Shareholders, the Fund will conduct periodic offers to repurchase a portion of its outstanding Shares.

The Fund is an “interval fund,” a type of fund which, in order to provide liquidity to shareholders, has adopted a fundamental investment policy to make quarterly offers to repurchase at least 5% and not more than 25% of its outstanding Shares at NAV per share, reduced by any applicable repurchase fee. Subject to applicable law and approval of the Trust’s Board of Trustees (the “Board”), the Fund will seek to conduct such quarterly repurchase offers typically in the amount of 8% of its outstanding Shares at NAV per share, which is the minimum amount permitted. Quarterly repurchase offers will occur in the months of January, April, July, and October. Written notification of each quarterly repurchase offer (the “Repurchase Offer Notice”) is sent to Shareholders of record at least 21 calendar days before the repurchase request deadline (i.e., the latest date on which Shareholders can tender their Shares in response to a repurchase offer) (the “Repurchase Request Deadline”). If you invest in the Fund through a financial intermediary, the Repurchase Offer Notice will be provided to you by your financial intermediary. The Fund’s Shares are not listed on any national securities exchange, and the Fund anticipates that no secondary market will develop for its Shares. Accordingly, you may not be able to sell Shares when and/or in the amount that you desire. Thus, the Shares are appropriate only as a long-term investment. In addition, the Fund’s repurchase offers may subject the Fund and Shareholders to special risks. See “Repurchase Offers Risk/Interval Fund Risk” in Footnote 5 – Principal Risks.

The Fund’s investment objective seeks to provide high current income and, secondarily, capital appreciation. The Fund seeks to achieve its investment objectives by investing primarily in a variety of credit related instruments, including corporate obligations and securitized and structured issues of varying maturities. The mix of assets in which the Fund may invest will be flexible and responsive to market conditions; however, under normal circumstances, bank loans are expected to constitute at least 40% of the Fund’s managed assets. The Fund expects to utilize leverage, as discussed below. To the extent consistent with the applicable liquidity

18

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

requirements for interval funds operating pursuant to Rule 23c-3 under the Investment Company Act of 1940, as amended (“Investment Company Act”), the Fund may invest without limit in illiquid securities.

The Fund may seek to use leverage directly or indirectly to enhance the return to Shareholders, subject to any applicable restrictions of the Investment Company Act; however, there can be no assurance that a leveraging strategy will be successful during any period in which it is employed. The Fund currently expects to borrow through a credit facility in an amount that would typically be up to 20% of the Fund’s total assets (which include any assets attributable to leverage) under normal market conditions. However, the Fund may borrow up to the maximum amount permitted by the Investment Company Act, which, for debt leverage such as borrowings under the credit facility, is 331⁄3% of the Fund’s total assets (reduced by liabilities and indebtedness except for indebtedness representing senior securities); this represents 50% of the Fund’s net assets. The Fund currently does not expect to engage in such borrowings for investment purposes until its assets reach approximately $25 million.

Recently Adopted Accounting Pronouncements

In March 2020, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2020-04, which provides optional expedients and exceptions for contracts, hedging relationships and other transactions affected by the transitioning away from the London Interbank Offered Rate (LIBOR) and other reference rates that are expected to be discontinued. The amendments in this Update are effective for all entities as of March 12, 2020 through December 31, 2022. At this time, management is evaluating the implications of these changes on the financial statements.

Class Disclosure

On December 27, 2019, the Fund created the T Class, a new class made available for sale pursuant to the Fund’s registration statement filed with the U.S. Securities and Exchange Commission (“SEC”). The T Class commenced operations on December 30, 2019. Refer to the Fund’s Prospectus for more details.

The Fund has multiple classes of shares designed to meet the needs of different groups of investors. The following table sets forth the differences amongst the classes:

Class | Eligible Investors | Minimum Initial Investments | ||||

| Y Class | All Investors who can meet the minimum investment amount - sold directly or through intermediary channels. | $ | 100,000 | |||

| T Class | Sold to retail investors by broker-dealers that are members of Financial Industry Regulatory Authority (“FINRA”) and have agreements with the Distributor, but may be made available through other financial firms, including banks and trust companies, and to specified benefit plans and other retirement accounts. | $ | 2,500 | |||

Each class offered by the Trust has equal rights as to assets and voting privileges. Income and non-class specific expenses are allocated daily to each class based on the relative net assets. Realized and unrealized capital gains and losses of each class are allocated daily based on the relative net assets of each class of the respective Fund. Class specific expenses, where applicable, currently include service, distribution, transfer agent fees, and sub-transfer agent fees that vary amongst the classes as described more fully in Note 2.

Significant Accounting Policies

The following is a summary of significant accounting policies, consistently followed by the Fund in preparation of the financial statements. The Fund is considered an investment company and accordingly, follows the investment company accounting and reporting guidance of the FASB Accounting Standards Codification Topic 946, Financial Services – Investment Companies, a part of Generally Accepted Accounting Principles (“U.S. GAAP”).

19

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

Security Transactions and Investment Income

Security transactions are recorded as of the trade date for financial reporting purposes. Securities purchased or sold on a when-issued or delayed-delivery basis may be settled beyond a standard settlement period for the security after the trade date.

Dividend income, net of foreign taxes, is recorded on the ex-dividend date, except certain dividends from foreign securities which are recorded as soon as the information is available to the Fund. Interest income, net of foreign taxes, is earned from settlement date, recorded on the accrual basis, and adjusted, if necessary, for accretion of discounts and amortization of premiums. Realized gains (losses) from securities sold are determined based on specific lot identification.

Currency Translation

All assets and liabilities initially expressed in foreign currency values are converted into U.S. dollar values at the mean of the bid and ask prices of such currencies against U.S. dollars as last quoted by a recognized dealer. Income, expenses, and purchases and sales of investments are translated into U.S. dollars at the rate of the exchange prevailing on the respective dates of such transactions. The effect of changes in foreign currency exchange rates on investments is separately identified from the fluctuations arising from changes in market values of securities held and is reported with all other foreign currency gains and losses on the Fund’s Statement of Operations.

Distributions to Shareholders

Effective October 1, 2020, the Fund’s distribution policy changed to declare income distributions quarterly and to distribute them to shareholders quarterly. Prior to October 1, 2020, the Fund declared income distributions daily and distribute them to Shareholders quarterly. The Fund’s final distribution for each taxable (fiscal) year will include any remaining investment company taxable income undistributed during the year, as well as all net capital gain realized during the year. Dividends to shareholders are determined in accordance with federal income tax regulations, which may differ in amount and character from net investment income and realized gains recognized for purposes of U.S. GAAP. If all or a portion of any Fund distribution exceeds the sum of the Fund’s investment company taxable income and realized net capital gain for a taxable year, the excess would be treated (i) first, as dividend income to the extent of the Fund’s current or accumulated earnings and profits, as calculated for federal income tax purposes (“E&P”), (ii) then as a tax-free “return of capital,” reducing a Shareholder’s adjusted tax basis in his or her Shares (which would result in a higher tax liability when the Shares are sold, even if they had not increased in value, or, in fact, had lost value), and (iii) then, after that basis is reduced to zero, as realized capital gain (assuming the Shares are held as capital assets), long-term or short-term, depending on the Shareholder’s holding period for the Shares.

The Board reserves the right to change the quarterly distribution policy from time to time.

Allocation of Income, Trust Expenses, Gains, and Losses

Investment income, realized and unrealized gains and losses from investments of the Fund is allocated daily to each class of shares based upon the relative proportion of net assets of each class to the total net assets of the Fund. Expenses directly charged or attributable to the Fund will be paid from the assets of the Fund. Generally, expenses of the Trust will be allocated among and charged to the assets of the Fund on a basis that the Board deems fair and equitable, which may be based on the relative net assets of the Fund or nature of the services performed and relative applicability to the Fund.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results may differ from those estimated.

20

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

Other

Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In the normal course of business, the Trust enters into contracts that provide indemnification to the other party or parties against potential costs or liabilities. The Trust’s maximum exposure under these arrangements is dependent on claims that may be made in the future and, therefore, cannot be estimated. The Trust has had no prior claims or losses pursuant to any such agreement.

2. Transactions with Affiliates

Management and Investment Sub-Advisory Agreements

The Fund and the Manager are parties to a Management Agreement that obligates the Manager to provide the Fund with investment advisory and administrative services. As compensation for performing the duties under the Management Agreement, the Manager will receive an annualized management fee based on a percentage of the Fund’s average daily net assets that is calculated and accrued daily according to the following schedule:

First $1 billion | 0.40 | % | ||

Next $4 billion | 0.375 | % | ||

Next $5 billion | 0.35 | % | ||

Over $10 billion | 0.325 | % |

The Trust, on behalf of the Fund, and the Manager have entered into an Investment Advisory Agreement with Sound Point Capital Management, LP, (the “Sub-Advisor”) pursuant to which the Fund has agreed to pay an annualized sub-advisory fee that is calculated and accrued daily based on the Fund’s average daily managed net assets according to the following schedule:

First $1 billion | 0.80 | % | ||

Over $1 billion | 0.75 | % |

The Management and Sub-Advisory Fees paid by the Fund for the year ended August 31, 2020 were as follows:

| Effective Fee Rate | Amount of Fees Paid | |||||||||||

Management Fees | 0.40 | % | $ | 38,137 | ||||||||

Sub-Advisor Fees | 0.80 | % | 76,519 | |||||||||

|

|

|

| |||||||||

Total | 1.20 | % | $ | 114,656 | ||||||||

|

|

|

| |||||||||

Distribution Plans

The Trust has adopted a distribution plan for its T Class Shares (“Distribution Plan”). Although the Fund is not an open-end management investment company, it has undertaken to comply with the terms of Rule 12b-1 under the Investment Company Act, which regulates the manner in which an open-end management investment company may directly or indirectly bear the expenses of distributing its shares, as a condition of an exemptive order under the Investment Company Act which permits it to have, among other things, a multi-class structure and distribution fees. The Distribution Plan allows the T Class Shares to pay distribution and other fees for the sale and distribution of Fund Shares and for other services provided to Shareholders, including expenses relating to selling efforts of various broker-dealers, shareholder servicing fees and the preparation and distribution of T Class advertising material and sales literature. The Distribution Plan also authorizes the use of any fees received by the Manager in accordance with the Management Agreement, and any fees received by the Sub-Advisor pursuant to the Investment Advisory Agreement, to be used for the sale and distribution of Fund Shares. The Distribution Plan provides that the T Class Shares of the Fund will pay up to 0.75% per annum of the average daily net assets attributable to the T Class to the Manager (or another entity approved by the Board). The Manager or other

21

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

approved entity will receive Rule 12b-1 fees from the T Class regardless of the amount of the actual expenses incurred by the Manager or other approved entity related to distribution and shareholder servicing efforts on behalf of the T Class. Thus, the Manager or other approved entity may realize a profit or a loss based upon its actual distribution and shareholder servicing related expenditures for the T Class. The Manager anticipates that the Distribution Plan will benefit Shareholders by providing broader access to the Fund through broker-dealers and other financial intermediaries who require compensation for their expenses in order to offer Shares of the Fund. Because Rule 12b-1 fees are paid out of the Fund’s T Class assets on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges.

Service Plans

The Trust has adopted a Service Plan for its Y Class Shares (the “Service Plan”) that authorizes the payment to the Manager and/or to such other entities as approved by the Board of an aggregate fee at the rate of up to 0.25% on an annualized basis of the average daily net assets of the Y Class Shares, payable monthly in arrears. The Manager or other approved entity may spend such amounts as it deems appropriate on any activities or expenses primarily intended to result in or relate to the servicing of Y Class Shares, including, but not limited to, the payment to third parties of shareholder service, transfer agency or sub-transfer agency fees or expenses. The primary expenses expected to be incurred are for shareholder servicing, record keeping fees and servicing fees paid to financial intermediaries such as plan sponsors and broker-dealers.

Investments in Affiliated Funds

The Fund may invest in the American Beacon U.S. Government Money Market Select Fund (the “USG Select Fund”). The Fund held the following shares with an August 31, 2020 fair value and dividend income earned from the investment in the USG Select Fund:

Affiliated Security | Type of Transaction | Fund | August 31, 2020 Shares/ Principal | Change in Unrealized Gain (Loss) | Realized Gain (Loss) | Dividend Income | August 31, 2020 Fair Value | |||||||||||||||||||||||||||||||||||||||||

| U.S. Government Money Market Select Fund | Direct | Sound Point Enhanced Income | $ | 1,589,262 | $ | - | $ | - | $ | 13,725 | $ | 1,589,262 | ||||||||||||||||||||||||||||||||||||

The Fund and the USG Select Fund have the same investment advisor and therefore, are considered to be affiliated. The Manager serves as investment advisor to the USG Select Fund and receives management fees and administrative fees totaling 0.10% of the average daily net assets of the USG Select Fund. During the year ended August 31, 2020, the Manager earned fees on the Fund’s direct investments in the USG Select Fund as shown below:

Fund | Direct Investments in USG Select Fund | |||

Sound Point Enhanced Income | $ | 1,378 | ||

Expense Reimbursement Plan

The Manager contractually agreed to reduce fees and/or reimburse expenses for the Y Class Shares and T Class Shares of the Fund to the extent that total operating expenses exceed 0.25% of average daily net assets for the Y Class and 1.00% of average daily net assets for the T Class (excluding management fees, shareholder service fees, taxes, interest including interest on borrowings, brokerage commissions, securities lending fees, expenses

22

American Beacon Sound Point Enhanced Income FundSM

Notes to Financial Statements

August 31, 2020

associated with securities sold short and the Fund’s use of leverage, litigation, and other extraordinary expenses). During the year ended August 31, 2020, the Manager waived and/or reimbursed expenses as follows:

| Expense Cap | Expiration of Reimbursed Expenses | |||||||||||||||

Fund Class | 9/1/2019 - 8/31/2020 | Reimbursed Expenses | (Recouped) Expenses | |||||||||||||

Sound Point Enhanced Income Y | 0.25 | % | $ | 463,446 | $ | (64,690 | )** | 2022 - 2023 | ||||||||

Sound Point Enhanced Income T* | 1.00 | % | 15,046 | - | 2022 - 2023 | |||||||||||

* Class commenced operations on December 30, 2019.

** This amount represents Recouped Expenses from prior fiscal years and is reflected in Total Expenses on the Statements of Operations.

Of these amounts, $61,424 was disclosed as a payable to the Manager on the Statement of Assets and Liabilities at August 31, 2020.

The Fund has adopted an Expense Reimbursement Plan whereby the Manager may seek repayment of such fee or voluntary reductions and expense reimbursements. Under the policy, the Manager can be reimbursed by the Fund for any contractual or voluntary fee reductions or expense reimbursements if reimbursement to the Manager (a) occurs within three years from the date of the Manager’s waiver/reimbursement and (b) does not cause the Fund’s annual operating expenses to exceed the lesser of the contractual percentage limit in effect at the time of the waiver/reimbursement or time of recoupment. The reimbursed expenses listed above will expire in 2022 and 2023. The carryover of excess expenses potentially reimbursable to the Manager, but not recorded as a liability are as follows:

Fund | Recouped Expenses | Excess Expense Carryover | Expired Expense Carryover | Expiration of Reimbursed Expenses | ||||||||||||

Sound Point Enhanced Income | $ | 64,690 | $ | 423,161 | $ | - | 2021 | |||||||||

Sound Point Enhanced Income | - | 996,044 | - | 2021 - 2022 | ||||||||||||

Concentration of Ownership