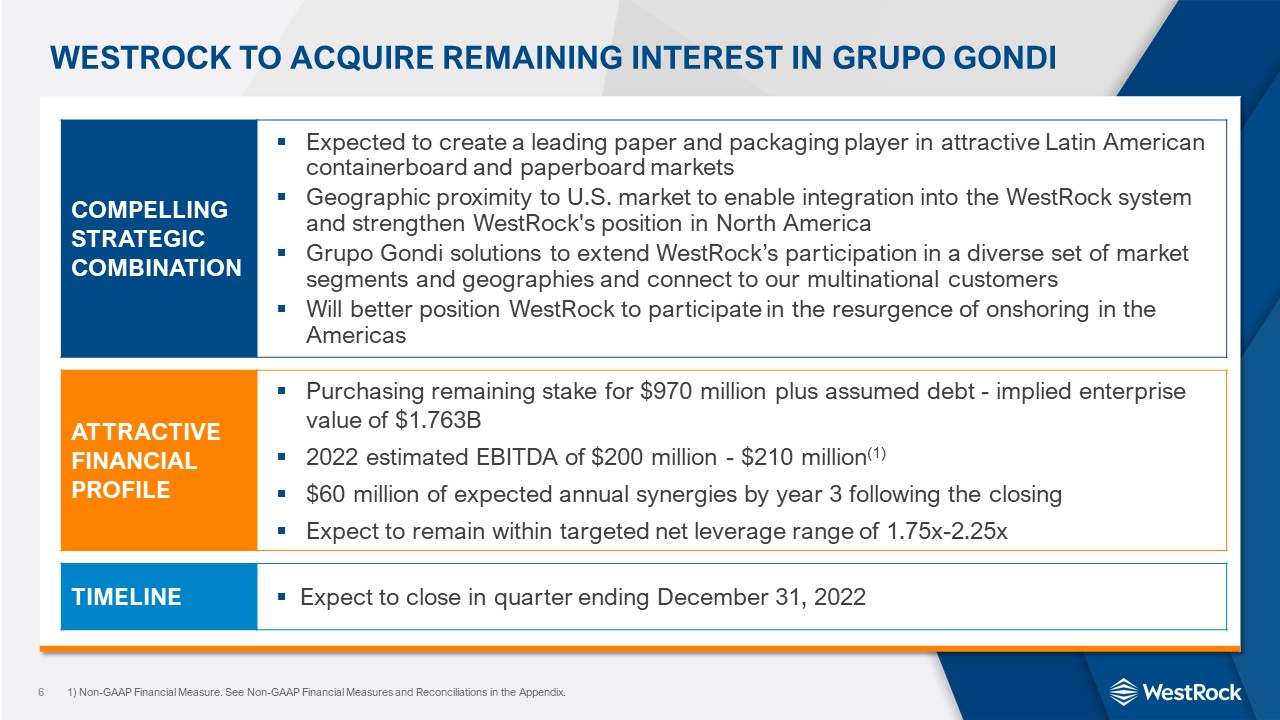

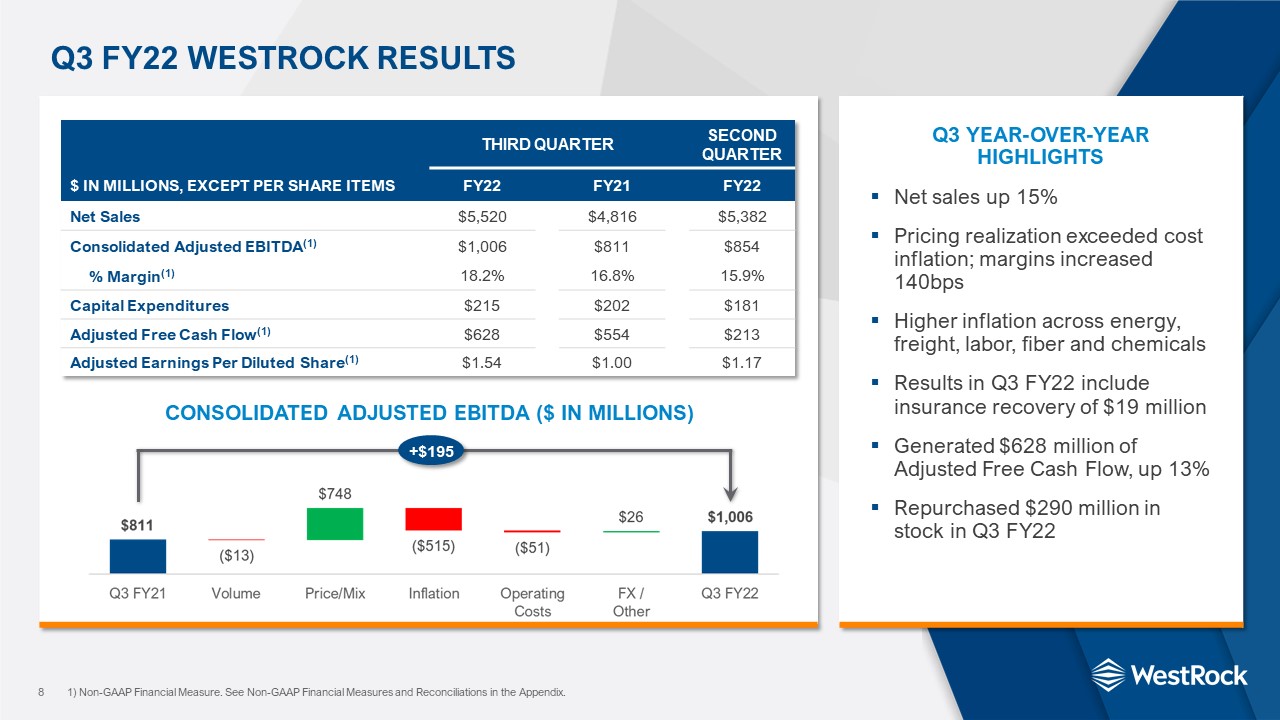

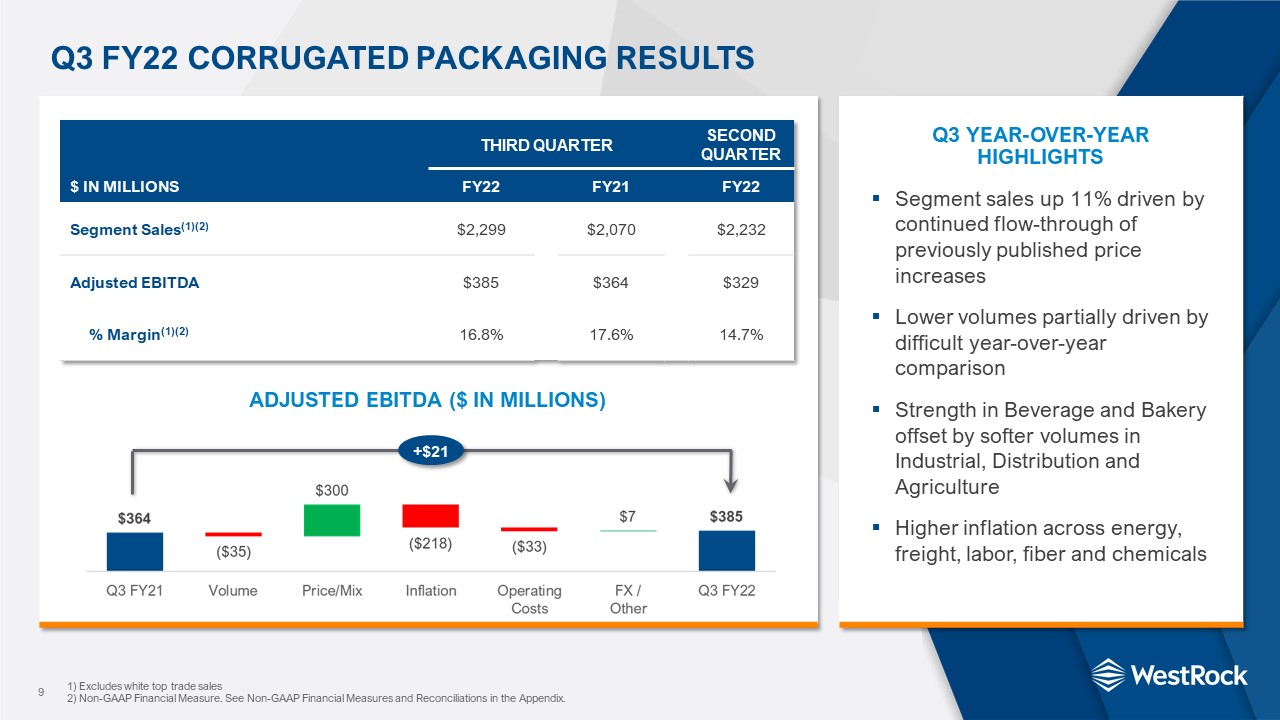

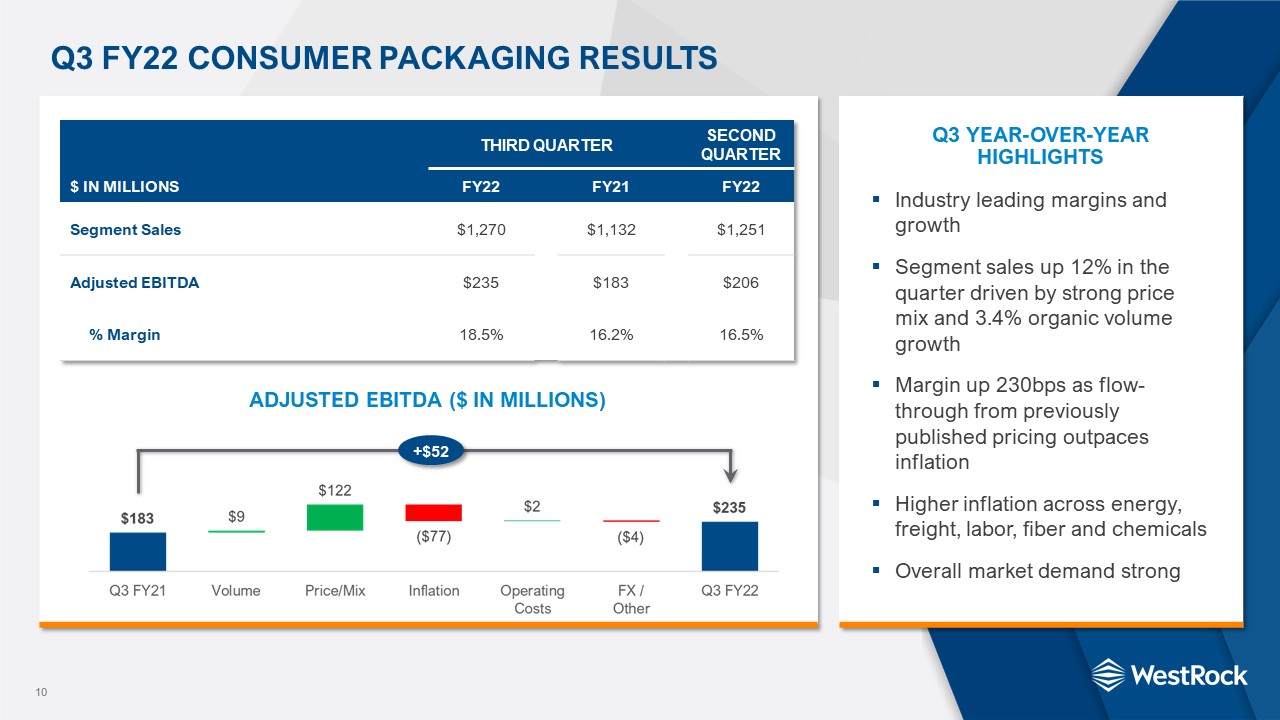

Forward Looking Statements: This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including but not limited to the statements on the slides entitled “Transformation Update”, “Pricing and Mix Management Outpacing Inflation Year-over-Year”, “WestRock to Acquire Remaining Interest in Grupo Gondi”, “Strategic Fit with Strong Growth Potential”, “Q4 FY22 Guidance”, “Additional Guidance”, and “Key Commodity Annual Consumption Volumes” that give guidance or estimates for future periods. Forward-looking statements are based on our current expectations, beliefs, plans or forecasts and are typically identified by words or phrases such as "may," "will," "could," "should," "would," "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "target," "prospects," "potential" and "forecast," and other words, terms and phrases of similar meaning. Forward-looking statements involve estimates, expectations, projections, goals, forecasts, assumptions, risks and uncertainties. A forward-looking statement is not a guarantee of future performance, and actual results could differ materially from those contained in the forward-looking statement. Forward-looking statements are subject to a number of assumptions, risks and uncertainties, such as developments related to the COVID-19 pandemic, including the severity, magnitude and duration of the pandemic, negative global economic conditions arising from the pandemic, impacts of governments' responses to the pandemic on operations, and impacts of the pandemic on commercial activity, customer and consumer preferences and demand; supply chain disruptions; disruptions in the credit or financial markets; results and impacts of acquisitions, including timing and operational and financial effects from our recently announced acquisition of Grupo Gondi; economic, competitive and market conditions generally, including the impact of inflation and increases in energy, raw materials, shipping, labor and capital equipment costs; reduced supply of raw materials; our ability to successfully identify and make performance and productivity improvements and risks associated with completing strategic projects on the anticipated timelines and realizing anticipated financial improvements; adverse legal, reputational and financial effects resulting from cyber incidents and the effectiveness of business continuity plans during a ransomware or other cyber incident; fluctuations in selling prices and volumes; intense competition; the potential loss of certain customers; the scope, costs, timing and impact of any restructuring of our operations and corporate and tax structure; the occurrence of severe weather or a natural disaster or other unanticipated problems, such as labor difficulties, equipment failure or unscheduled maintenance and repair; our desire or ability to continue to repurchase company stock; and the scope, timing and outcome of any litigation, claims or other proceedings or dispute resolutions and the impact of any such litigation. Such risks and other factors that may impact management's assumptions are more particularly described in our filings with the Securities and Exchange Commission, including in Part I, Item 1A “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended September 30, 2021. The information contained herein speaks as of the date hereof, and we do not have or undertake any obligation to update or revise our forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent required by law. Non-GAAP Financial Measures and other matters: We report our financial results in accordance with accounting principles generally accepted in the United States (“GAAP”). However, management believes certain non-GAAP financial measures provide users with additional meaningful financial information that should be considered when assessing our ongoing performance. Management also uses these non-GAAP financial measures in making financial, operating and planning decisions and in evaluating our performance. Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, our GAAP results. The non-GAAP financial measures we present may differ from similarly captioned measures presented by other companies. For additional information, see the Appendix. This presentation shall not be considered to be part of any solicitation of an offer to buy or sell the Company’s securities. This presentation also may not include all of the information regarding the Company that you may need to make an investment decision regarding the Company’s securities. Any investment decision should be made on the basis of the total mix of information regarding the Company that is publicly available as of the date of the investment decision. Cautionary Language 2