In addition, pursuant to Circular 6 and the Ministry of Commerce (the “MOFCOM”) Security Review Rules, a security review is required for mergers and acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign investors may acquire “de facto control” of domestic enterprises with “national security” concerns and prohibit foreign investors from bypassing the security review requirement by structuring transactions through proxies, trusts, indirect investments, leases, loans, control through contractual arrangements or Offshore transactions. These national security review-related regulations are relatively new and there is a lack of clear statutory interpretation regarding the implementation of the rules, and PRC authorities may interpret these regulations to mean that the transactions implementing our VIE structures should have been submitted for review. For a discussion of these PRC national security review requirements, see “Government Regulation and Legal Uncertainties—Specific Statues and Regulations—Miscellaneous—Regulation of M&A and Overseas Listings”

If we were found to be in violation of any existing or future PRC law or regulations relating to foreign ownership of value-added telecommunications businesses and security reviews of foreign investments in such businesses, including online games businesses, regulatory authorities with jurisdiction over the operation of our business would have broad discretion in dealing with such a violation, including levying fines, confiscating our income, revoking the business or operating licenses of PRC subsidiaries and/or VIEs, requiring us to restructure our ownership structure or operations, requiring us to discontinue or divest ourselves of all or any portion of our operations or assets, restricting our right to collect revenues, blocking our Internet platforms, or imposing additional conditions or requirements with which we may not be able to comply. Any of these actions could cause significant disruption to our business operations and have an adverse impact on our business, financial condition and results of operations. Further, if changes were required to be made to our ownership structure, our ability to consolidate our VIEs could be adversely affected.

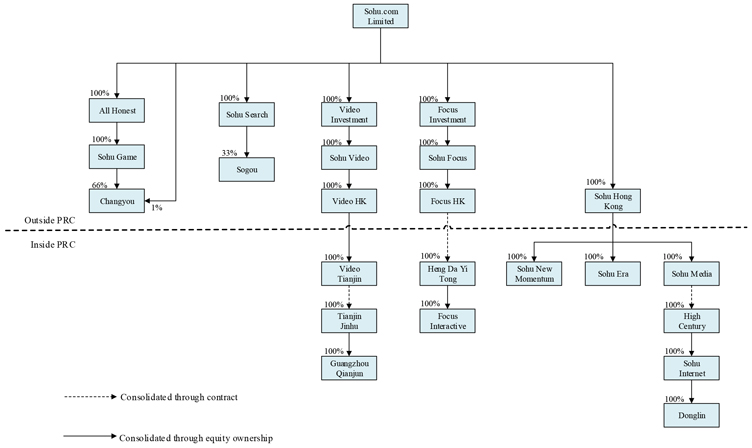

We may be unable to collect long-term loans to officers and employees or exercise management influence associated with High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace.

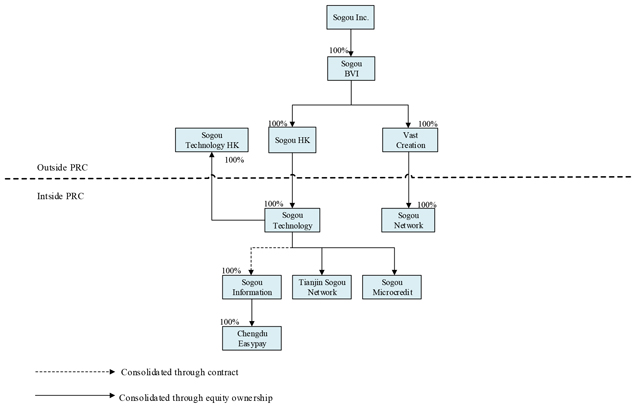

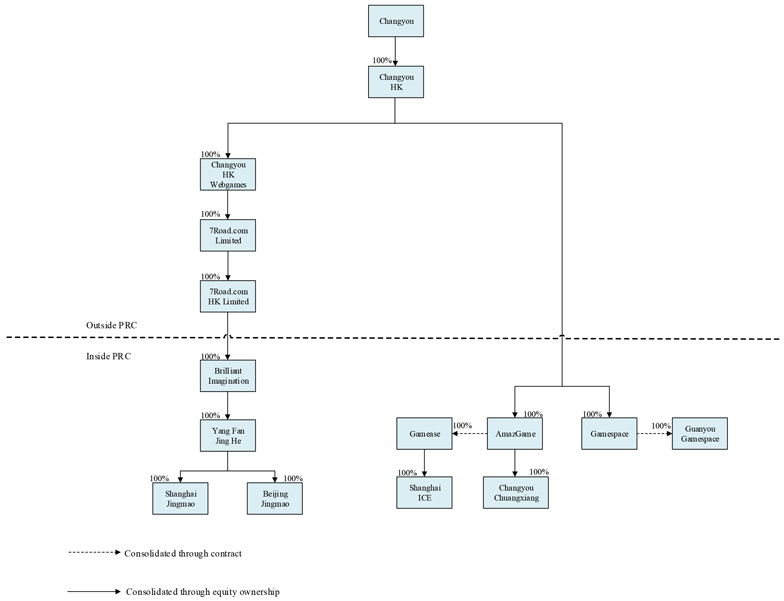

As of December 31, 2018, Sohu had outstanding long-term loans of $7.7 million to Dr. Charles Zhang and to certain PRC entities owned by Dr. Zhang and/or certain other employees. These long-term loans were used to finance investments in our VIEs Beijing Century High-Tech Investment Co., Ltd. (“High Century”), Beijing Heng Da Yi Tong Information Technology Co., Ltd. (“Heng Da Yi Tong”), Tianjin Jinhu Culture Development Co., Ltd. (“Tianjin Jinhu”), Beijing Sogou Information Service Co., Ltd. (“Sogou Information”), Beijing Gamease Age Digital Technology Co., Ltd. (“Gamease”), and Beijing Guanyou Gamespace Digital Technology Co., Ltd. (“Guanyou Gamespace”), which are used to facilitate our participation in telecommunications, Internet content, online games and certain other businesses in China where foreign ownership is either prohibited or restricted.

The loan agreements contain provisions that, subject to PRC laws, (i) the loans can only be repaid to us by transferring the shares of High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace to us; (ii) the shares of High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace cannot be transferred by the borrowers without our approval; and (iii) we have the right to appoint all directors and senior management personnel of High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace. Under the loan agreements the borrowers have pledged all of their shares in High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace collateral for the loans, and the loans bear no interest and are due on the earlier of a demand or such time as Dr. Charles Zhang or one of the other employee borrowers, as the case may be, is not an employee of Sohu. Sohu does not intend to request repayment of the loans as long as PRC regulations prohibit it from directly investing in businesses engaged in by the VIEs.

Because these loans can only be repaid by the borrowers’ transferring the shares of the various entities, our ability to ultimately realize the effective return of the amounts advanced under these loans will depend on the profitability of High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace and is therefore uncertain.

Furthermore, because of uncertainties associated with PRC law, ultimate enforcement of the loan agreements is uncertain. Accordingly, we may never be able to collect these loans and we may not be able to continue to exercise influence over High Century, Heng Da Yi Tong, Tianjin Jinhu, Sogou Information, Gamease and Guanyou Gamespace.

We depend upon contractual arrangements with our VIEs for the success of our business and these arrangements may not be as effective in providing operational control as direct ownership of these businesses and may be difficult to enforce.

Because we conduct our Internet operations mainly in the PRC, and are restricted or prohibited by the PRC government from owning Internet content, telecommunication, online games operations and certain other operations in the PRC, we are dependent on our VIEs in which we have no direct ownership interest, to provide those services through contractual agreements among the parties and to hold some of our assets, including some of the domain names and trademarks relating to our business. These arrangements may not be as effective in providing control over our Internet content, telecommunications operations, online games operations and certain other as direct ownership of these businesses. For example, if we had direct ownership of our VIEs, we would be able to exercise our rights as a shareholder to effect changes in their boards of directors, which in turn could effect changes at the management level. Due to our VIE structure, we have to rely on contractual rights to effect control and management of our VIEs, which exposes us to the risk of potential breach of contract by the VIEs or their shareholders, such as their failing to use the domain names and trademarks held by them, or failing to maintain our Internet platforms, in an acceptable manner or taking other actions that are detrimental to our interests. In addition, as each of our VIEs is jointly owned by its shareholders, it may be difficult for us to change our corporate structure if such shareholders refuse to cooperate with us. In addition, some of our subsidiaries and VIEs could fail to take actions required for our business, such as entering into content development contracts with potential content suppliers or failing to maintain the necessary permits for the content servers. Furthermore, if the shareholders of any of our VIEs were involved in proceedings that had an adverse impact on their shareholder interests in such VIE or on our ability to enforce relevant contracts related to the VIE structure, our business would be adversely affected.

18