As filed with the United States Securities and Exchange Commission on March 31, 2020

Registration No. 333-236079

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NEW FRONTIER HEALTH CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| Cayman Islands | 8062 | N/A |

(State or Other Jurisdiction of

Incorporation or Organization) | (Primary Standard Industrial

Classification Code Number) | (I.R.S. Employer

Identification No.) |

10 Jiuxianqiao Road,

Hengtong Business Park

B7 Building, 1/F

Chaoyang District, 100015,

Beijing, China

Tel: 86-10-59277000

(Address and Telephone Number of Registrant’s Principal Executive Offices)

Edward Truitt

Maples Fiduciary Services (Delaware) Inc.

4001 Kennett Pike, Suite 302

Wilmington, Delaware 19807

(Name, Address, and Telephone Number of Agent for Service)

Copies to:

Joel L. Rubinstein

Jonathan P. Rochwarger

Elliott M. Smith

Winston & Strawn LLP

200 Park Avenue

New York, New York 10166

Tel: (212) 294-6700

Fax: (212) 294-4700

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth companyx

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards1provided pursuant to Section 7(a)(2)(B) of the Securities Act.¨

| 1 | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | | Amount

to be

Registered(1) | | | Proposed

Maximum

Offering Price

Per Share | | | Proposed

Maximum

Aggregate

Offering Price | | | Amount of

Registration

Fee(2) | |

| Primary Offering: | | | | | | | | | | | | | | | | |

| Ordinary shares, par value $0.0001 per share (“ordinary shares”) underlying warrants | | | 26,875,000 | (3) | | | 11.50 | (4) | | | 309,062,500 | | | | 40,116.31 | |

| Secondary Offering: | | | | | | | | | | | | | | | | |

| Ordinary shares | | | 114,841,048 | (5) | | | 10.17 | (6) | | | 1,167,933,458 | (6) | | | 151,597.76 | |

| Ordinary shares underlying warrants | | | 12,500,000 | (7) | | | 11.50 | (4) | | | 143,750,000 | | | | 18,658.75 | |

| Warrants to purchase ordinary shares | | | 12,500,000 | (8) | | | — | | | | — | | | | — | (9) |

| Totals | | | | | | | | | | | 1,620,745,958 | | | | 210,372.83 | (10) |

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the registrant is also registering an indeterminate number of additional securities as may be issued to prevent dilution resulting from share dividends, share splits or similar transactions. |

| (2) | Calculated by multiplying the estimated aggregate offering price of the securities being registered by 0.0001298. |

| (3) | Includes (i) 14,375,000 ordinary shares issuable upon the exercise of redeemable warrants included as part of the units (the “public warrants”) issued in the registrant’s initial public offering (the “IPO”), (ii) 4,750,000 ordinary shares issuable upon the exercise of redeemable warrants issued to certain institutions and accredited investors upon the closing of the registrant’s initial business combination with Healthy Harmony Holdings, L.P. (“Healthy Harmony”) and Healthy Harmony GP, Inc. (together with Healthy Harmony, “UFH”) (the “business combination”) pursuant to Forward Purchase Agreements (the “forward purchase warrants”) and (iii) 7,750,000 ordinary shares issuable upon exercise of warrants the registrant issued to New Frontier Public Holding Ltd. (the “Sponsor”) in a private placement simultaneously with the closing of the IPO (the “private placement warrants”). |

| (4) | Estimated solely for the purpose of the calculation of the registration fee pursuant to Rule 457(g), based on the exercise price of the warrants. |

| (5) | Includes the resale of (i) 69,246,187 ordinary shares issued to certain institutions and accredited investors in private placements at the closing of the business combination, (ii) 19,000,000 ordinary shares issued to certain institutions and accredited investors upon the closing of the business combination pursuant to Forward Purchase Agreements (the “forward purchase shares”), (iii) 14,657,361 ordinary shares issued to certain sellers and members of UFH management in connection with the business combination and (iv) 11,937,500 ordinary shares issued upon the redesignation of the registrant’s outstanding Class B ordinary shares (the “founder shares”) at the closing of the business combination. |

| (6) | Pursuant to Rule 457(c) under the Securities Act, and solely for the purpose of calculating the registration fee, the proposed maximum offering price is $10.17, which is the average of the high and low prices of the registrant’s ordinary shares on December 18, 2019 (such date being within five business days of the date that this registration statement was first filed with the Securities and Exchange Commission (the “SEC”)) on The New York Stock Exchange. |

| (7) | Includes the resale of (i) 4,750,000 ordinary shares issuable upon the exercise of forward purchase warrants and (iii) 7,750,000 ordinary shares issuable upon exercise of private placement warrants. |

| (8) | Includes the resale of (i) 4,750,000 forward purchase warrants and (ii) 7,750,000 private placement warrants. |

| (9) | In accordance with Rule 457(g), the entire registration fee for the warrants is allocated to the ordinary shares underlying the warrants, and no separate fee is payable for the warrants. |

| (10) | Registration fee previously calculated in respect of the registration statement filed with the SEC on December 26, 2019 and previously paid. No further registration fee is due. There has been no increase in the securities being registered pursuant to this registration statement since the date that this registration statement was first filed with the SEC. |

Pursuant to Rule 429 under the Securities Act of 1933, the prospectus included in this registration statement is a combined prospectus relating also to Registration Statement No. 333-236079 previously filed by the registrant on Form F-1 and declared effective by the Securities and Exchange Commission on January 28, 2020. This Registration Statement, which is a new Registration Statement, upon effectiveness, also constitutes Post-Effective Amendment No. 1 to Registration Statement No. 333-236079, and such post-effective amendment shall hereafter become effective concurrently with the effectiveness of this Registration Statement and in accordance with Section 8(c) of the Securities Act of 1933.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

On January 24, 2020, the registrant filed a Registration Statement on Form F-1 (Registration No. 333- 236079), which was subsequently declared effective by the U.S. Securities and Exchange Commission (the “SEC”) on January 28, 2020 (the “Registration Statement”).

This post-effective amendment is being filed to update the Registration Statement to include the audited consolidated financial statements and the notes thereto included in the registrant’s Annual Report on Form 20-F for the fiscal year ended December 31, 2019, filed with the SEC on March 31, 2020, and certain other information in such Registration Statement.

No additional securities are being registered under this post-effective amendment. All applicable registration fees were paid at the time of the original filing of the Registration Statement.

The information in this prospectus is not complete and may be changed. Neither we nor the selling securityholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION — DATED MARCH 31, 2020

PRELIMINARY PROSPECTUS

NEW FRONTIER HEALTH CORPORATION

Primary Offering of

26,875,000 Ordinary Shares

Secondary Offering of

127,341,048 Ordinary Shares

12,500,000 Warrants

This prospectus relates to the issuance from time to time by us of up to 26,875,000 of our ordinary shares, par value $0.0001 per share (the “ordinary shares”), including (i) 14,375,000 ordinary shares issuable upon the exercise of redeemable warrants (the “public warrants”) that were issued as part of the units in our initial public offering (our “IPO”), (ii) 4,750,000 ordinary shares issuable upon the exercise of redeemable warrants that we issued in private placements (the “forward purchase warrants”) to certain institutions and accredited investors upon the closing of our initial business combination with Healthy Harmony Holdings, L.P. (“Healthy Harmony”) and Healthy Harmony GP, Inc. (together with Healthy Harmony, “UFH”) (the “business combination”) pursuant to certain Forward Purchase Agreements entered into in connection with our IPO (the “Forward Purchase Agreements”) and (iii) 7,750,000 ordinary shares issuable upon the exercise of warrants we issued to New Frontier Public Holding Ltd. (the “Sponsor”) in a private placement simultaneously with the closing of our IPO (the “private placement warrants” and, collectively with the public warrants and the forward purchase warrants, the “warrants”).

This prospectus also relates to the resale from time to time by the selling securityholders named in this prospectus or their permitted transferees (collectively, the “Selling Securityholders”) of up to (i) 127,341,048 ordinary shares and (ii) 12,500,000 warrants to purchase ordinary shares, consisting of 4,750,000 forward purchase warrants and 7,750,000 private placement warrants.

The ordinary shares covered by this prospectus that may be offered and sold by the Selling Securityholders include (i) 69,246,187 ordinary shares issued to certain institutions and accredited investors, including certain of our directors and/or entities controlled by them, in private placements at the closing of the business combination, (ii) 19,000,000 ordinary shares issued to certain institutions and accredited investors upon the closing of the business combination pursuant to Forward Purchase Agreements (the “forward purchase shares”), (iii) 14,657,361 ordinary shares issued to certain sellers and members of UFH management in connection with the business combination, (iv) 11,937,500 ordinary shares issued upon the redesignation of our outstanding Class B ordinary shares, par value $0.0001 per share (the “founder shares”), at the closing of the business combination, which ordinary shares are subject to varying transfer restrictions as described herein, (v) 4,750,000 ordinary shares issuable upon the exercise of the forward purchase warrants and (vi) 7,750,000 ordinary shares issuable upon the exercise of the private placement warrants.

Each whole warrant entitles the holder to purchase one ordinary share at an exercise price of $11.50 per share commencing on January 17, 2020 and will expire on December 18, 2024, at 5:00 p.m., New York City time, or earlier upon redemption or liquidation. Once the warrants are exercisable, we may redeem the outstanding public warrants and forward purchase warrants at a price of $0.01 per warrant if the last reported sales price of the ordinary shares equals or exceeds $18.00 per share (as adjusted for share splits, share capitalizations, reorganizations, recapitalizations and the like) for any 20 trading days within a 30-trading day period ending on the third trading day prior to the date on which we send the notice of redemption to the warrant holders, as described herein. The private placement warrants have terms and provisions that are identical to those of the public warrants, except as described herein. If the private placement warrants are held by holders other than the Sponsor or its permitted transferees, the private placement warrants will be redeemable by us and exercisable by the holders on the same basis as the public warrants.

We are registering the offer and sale of these securities to satisfy certain registration rights we have granted. The Selling Securityholders may sell the securities covered by this prospectus in a number of different ways and at varying prices. We will not receive any of the proceeds from the sale of the securities by the Selling Securityholders. We will receive proceeds from warrants exercised in the event that such warrants are exercised for cash. We will pay certain expenses associated with the registration of the securities covered by this prospectus, as described in the section titled “Plan of Distribution.”

Our ordinary shares and public warrants trade on the New York Stock Exchange (“NYSE”) under the symbols “NFH” and “NFH WS,” respectively. On March 30, 2020, the closing prices of the ordinary shares and public warrants were $7.87 per share and $0.90 per warrant, respectively.

An investment in our securities involves risks. See “Risk Factors” beginning on page 12 of this prospectus.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2020.

TABLE OF CONTENTS

Page

You should rely only on the information provided in this prospectus and any applicable prospectus supplement. Neither we nor the Selling Securityholders have authorized anyone to provide you with different information. Neither we nor the Selling Securityholders are making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information in this prospectus and any applicable prospectus supplement is accurate as of any date other than the date of the applicable document. Since the respective dates of this prospectus, our business, financial condition, results of operations and prospects may have changed.

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form F-1 that we filed with the SEC using a “shelf” registration process. Under this shelf registration process, the Selling Securityholders may, from time to time, offer and sell any combination of the securities described in this prospectus in one or more offerings. The Selling Securityholders may use the shelf registration statement to sell up to an aggregate of 127,341,048 ordinary shares and 12,500,000 warrants from time to time as described in the section entitled “Plan of Distribution.” This prospectus also relates to the issuance by us of up to 26,875,000 ordinary shares that are issuable upon the exercise of the warrants.

We will not receive any proceeds from the sale of ordinary shares or warrants to be offered by the Selling Securityholders pursuant to this prospectus, but we will receive proceeds from warrants exercised in the event that such warrants are exercised for cash. We will pay the expenses, other than underwriting discounts and commissions, if any, associated with the sale of ordinary shares and warrants pursuant to this prospectus. To the extent required, we and the Selling Securityholders, as applicable, will deliver a prospectus supplement with this prospectus to update the information contained in this prospectus. The prospectus supplement may also add, update or change information included in this prospectus. You should read both this prospectus and any applicable prospectus supplement, together with additional information described below under the caption “Where You Can Find More Information.” We have not, and the Selling Securityholders have not authorized anyone to provide you with information different from that contained in this prospectus. The information contained in this prospectus is accurate only as of the date on the front cover of the prospectus. You should not assume that the information contained in this prospectus is accurate as of any other date.

No offer of these securities will be made in any jurisdiction where the offer is not permitted.

Unless the context indicates otherwise, the terms “New Frontier Health Corporation,” the “Company,” “we,” “us” and “our” refer to New Frontier Health Corporation (formerly known as New Frontier Corporation or “NFC”), a Cayman Islands exempted company. References in this prospectus to the “business combination” refer to the consummation of the transactions contemplated by that certain Transaction Agreement, dated as of July 30, 2019, which transactions were consummated on December 18, 2019.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. These forward-looking statements relate to expectations for future financial performance, business strategies or expectations for our business. Specifically, forward-looking statements may include statements relating to:

| · | the benefits of the business combination; |

| · | the future financial performance of the Company following the business combination; |

| · | changes in the market for our services; |

| · | expansion plans and opportunities; and |

other statements preceded by, followed by or that include the words “may,” “can,” “should,” “will,” “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target” or similar expressions.

You should not place undue reliance on these forward-looking statements in deciding whether to invest in our securities. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

| · | the risk that the business combination disrupts current plans and operations; |

| · | the ability to recognize the anticipated benefits of the business combination, which may be affected by, among other things, competition and the ability of the combined business to grow and manage growth profitably; |

| · | costs related to the business combination; |

| · | changes in applicable laws or regulations; and |

| · | the possibility that we may be adversely affected by other economic, business, and/or competitive factors, including but not limited to the economic, social and political climate in China and the impact of regulations on the Company’s business; and |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. In particular, you should consider the risks provided under “Risk Factors” in this prospectus. Our forward-looking statements speak only as of the time that they are made and do not necessarily reflect our outlook at any other point in time, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date. We do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

FREQUENTLY USED TERMS

“anchor investors” means the accredited investors with whom the Company entered into the Forward Purchase Agreements, including certain entities controlled by certain of the Company’s directors.

“business combination” means the transactions contemplated by the Transaction Agreement consummated on December 18, 2019, whereby the Company indirectly acquired all of the issued and outstanding equity interests of UFH and changed its name to New Frontier Health Corporation.

“Charter” means our amended and restated memorandum and articles of incorporation as currently in effect.

“Class A ordinary shares” means the Class A ordinary shares, par value $0.0001 per share, that were redesignated as ordinary shares at the Closing.

“Class B ordinary shares” means the Class B ordinary shares, par value $0.0001 per share, that were redesignated as ordinary shares at the Closing.

“Closing” means the closing of the business combination.

“Closing Date” means December 18, 2019, the closing date of the business combination.

“Companies Law” means the Companies Law (2018 Revision) of the Cayman Islands, as amended.

“Forward Purchase Agreements” means the forward purchase agreements, dated as of June 4, 2018 and June 29, 2018, as amended from time to time, pursuant to which the anchor investors agreed to purchase an aggregate of 19,000,000 forward purchase shares, plus 4,750,000 forward purchase warrants, for a purchase price of $10.00 per forward purchase share, or $190,000,000 in the aggregate, which aggregate purchase price includes purchases by entities controlled Antony Leung and Carl Wu, two of the Company’s directors, for an aggregate of $21,000,000, in a private placement that occurred immediately prior to the closing of the business combination.

“forward purchase shares” means the 19,000,000 ordinary shares issued to the anchor investors pursuant to the Forward Purchase Agreements.

“forward purchase warrants” means the 4,750,000 redeemable warrants issued to the anchor investors pursuant to the Forward Purchase Agreements, each of which is exercisable for one ordinary share at an exercise price of $11.50 per share, in accordance with its terms.

“Fosun” means Fosun Industrial Co., Limited, a company incorporated in Hong Kong.

“Fosun Director Nomination Agreement” means the Fosun Director Nomination Agreement, dated as of December 18, 2019, by and among the Company, the Sponsor and Fosun.

“Fosun Rollover Agreement” means the Fosun Rollover Agreement, dated as of July 30, 2019, by and between the Company and Fosun.

“founder shares” means the 11,937,500 Class B ordinary shares that were redesignated as ordinary shares at the Closing, of which 9,805,000 are held by the initial purchasers and 2,132,500 are held by the anchor investors.

“founders” means the Sponsor, Antony Leung and Carl Wu and their affiliates.

“Healthy Harmony” means Healthy Harmony Holdings, L.P., a Cayman Islands exempted limited partnership.

“HH GP” means Healthy Harmony GP, Inc., a Cayman Islands exempted company and the sole general partner of Healthy Harmony.

“initial shareholders” means our Sponsor, anchor investors and certain of our current and former directors (and their assignees) who purchased shares in connection with the Company’s IPO.

“IPO” means the Company’s initial public offering of units, which closed on July 3, 2018.

“Lipson Employment Agreement” means the employment agreement entered into on December 17, 2019 between the Company and Roberta Lipson.

“Lipson Parties” means Roberta Lipson, the Benjamin Lipson Plafker Trust, the Daniel Lipson Plafker Trust, the Jonathan Lipson Plafker Trust and the Ariel Benjamin Lee Trust.

“Lipson Registration Rights Agreement” means the Registration Rights Agreement, dated as of December 17, 2019, by and between the Company and the Lipson Parties.

“Lipson Reinvestment Agreement” means the Founder Reinvestment Agreement, dated as of July 30, 2019, by and between the Company and the Lipson Parties, as amended by the Amendment to Founder Reinvestment Agreement on December 17, 2019.

“Management Reinvestment Agreements” means those certain Management Reinvestment Agreements, dated as of December 17, 2019, between the Company and the Management Sellers.

“Management Sellers” means certain members of management of UFH who held equity interests in UFH, other than Roberta Lipson.

“NFC Buyer Sub” means NF Unicorn Acquisition L.P., a Cayman Islands exempted limited partnership and wholly owned indirect subsidiary of the Company.

“NFG” means New Frontier Group Ltd., an affiliate of the Company and the Sponsor.

“NYSE” means the New York Stock Exchange

“ordinary shares” means the ordinary shares of the Company, par value $0.0001 per share.

“PIPE Investors” means the accredited investors with whom the Company entered into Subscription Agreements.

“preference shares” means the preference shares of the Company, par value $0.0001 per share.

“private placement warrants” means the 7,750,000 warrants issued to our Sponsor in a private placement simultaneously with the closing of our IPO, each of which is exercisable for one ordinary share at an exercise price of $11.50 per share, in accordance with its terms.

“Proxy Statement” means the definitive proxy statement on Schedule 14A, filed with the SEC by the Company on November 27, 2019.

“public warrants” means the 14,375,000 redeemable warrants included in the units issued in the IPO, each of which is exercisable for one ordinary share at an exercise price of $11.50 per share, in accordance with its terms.

“Registration Rights Agreement” means the Registration Rights Agreement, dated as of June 27, 2018, by and between the Company and the Sponsor.

“Sellers” means Fosun, the Lipson Parties, TPG Healthy, L.P., a Cayman Islands exempted limited partnership, and Plenteous Flair Limited, a Cayman Islands company.

“Selling Securityholders” means the persons listed in the table in the “Selling Securityholders” section of this prospectus, and the pledgees, donees, transferees, assignees, successors and others who later come to hold any of the Selling Securityholders’ interest in our securities after the date of this prospectus.

“Sponsor” means New Frontier Public Holding Ltd., a Cayman Islands exempted company.

“Subscription Agreements” means the subscription agreements entered into with the PIPE Investors, pursuant to which the Company issued an aggregate of 69,248,187 Class A ordinary shares for a purchase price of $10.00 per Class A ordinary share, or $692,461,870 in the aggregate.

“Transaction Agreement” means that certain Transaction Agreement, dated as of July 30, 2019, by and among the Company, NFC Buyer Sub, Healthy Harmony, HH GP and the Sellers, pursuant to which, on the terms and conditions contained therein, indirectly acquired UFH.

“UFH” means United Family Healthcare, the brand name under which the business operations of Healthy Harmony are conducted.

“units” means the 28,750,000 units of the Company sold in the IPO, each consisting of one Class A ordinary share and one-half of one public warrant.

“Vivo Director Nomination Agreement” means the Director Nomination Agreement, dated as of December 17, 2019, by and among the Company, the Sponsor and Vivo Capital Fund IX (Cayman), L.P. (“Vivo”).

“warrants” are to the public warrants, the private placement warrants and the forward purchase warrants.

SUMMARY

This summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information that is important to you. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Operating and Financial Review and Prospects” and our combined financial statements included elsewhere in this prospectus.

Unless the context indicates otherwise, the terms “New Frontier Health Corporation,” the “Company,” “we,” “us” and “our” refer to New Frontier Health Corporation (formerly known as New Frontier Corporation), a Cayman Islands exempted company.

The Company

Our subsidiary, UFH, is a leading internationally accredited healthcare provider committed to providing comprehensive and integrated healthcare services in urban centers in China, and is one of the only comprehensive hospital and clinic operators in the country with a nationwide network. UFH’s patient base includes China’s rapidly growing upper middle class and expatriate communities. Since the opening of its first hospital in Beijing, Beijing United Family Hospital (“BJU”), in 1997, UFH has expanded into several other Chinese markets including Shanghai, Guangzhou, Tianjin, Qingdao, and Hangzhou as described below, and its patient base has expanded from predominantly expatriate to an increasingly local Chinese population.

UFH offers comprehensive, premium quality healthcare services through a network of hospital inpatient departments and integrated outpatient clinics, including satellite feeder clinics. UFH’s facilities include 24/7 emergency rooms, intensive care units, neonatal intensive care units, operating rooms, clinical laboratories, radiology and blood banking services. UFH operates its network of hospitals and clinics in a “hub and spoke” model featuring a central hospital with several nearby clinics. Utilizing this model, UFH is able to leverage its extensive network by enabling patients to visit physicians at conveniently located outpatient clinics and, if necessary, they are then referred to one of UFH’s hospitals for more specialized care, and returned to the care of the primary care provider when appropriate. This integrated network enables patients to receive a full range of healthcare services without the need to find a new doctor or move patient records from one facility to another, and allows UFH to care for more patients. As such, our management believes this model results in several benefits and competitive advantages including increasing patient loyalty by providing a wide range of services within a single network, enhancing service quality through cross-departmental training, quality control and referral, and raising barriers to entry to competition by expanding its services and locations. By comparison, other private healthcare facilities in China generally consist of standalone hospitals or clinics.

Furthermore, UFH’s hub and spoke business model enables it to offer a comprehensive healthcare services platform with multiple patient touch points that serve patient needs from birth throughout a patient’s lifetime, also known as a “life-cycle” model. Specifically, UFH intends to initially attract patients through its focus on primary care with its prenatal, OB/GYN and pediatrics practices, and then naturally transition the patient to its family medicine practice and adult and geriatric medical and surgical care, with the intention that these services will become gateways for other higher margin specialties within the UFH network over time. Other specialties that UFH expects to be drivers of current and future business growth as part of the life-cycle model include emergency medicine, ophthalmology, ear nose and throat (“ENT”), dermatology, and other high acuity services including orthopedics and surgery. Differentiated services, including general rehabilitation, postpartum rehabilitation, dental and home health complete the “lifecycle” of coverage provided by UFH. By providing these all-inclusive services, we believe we are able to differentiate ourselves from other private healthcare providers in China who only generally provide either specialized services or primary care, but not both.

Background

We were originally incorporated on March 28, 2018 as a Cayman Islands exempted company for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. On December 18, 2019, we consummated the acquisition of UFH and related transactions. As of result of the business combination, we became the holding company of UFH and we changed our name from “New Frontier Corporation” to “New Frontier Health Corporation.”

Our results are separated into two distinct periods as follows: (1) up to and including the business combination closing date (labeled “Predecessor”) and (2) the period after that date (labeled “Successor”). The period presented from December 19, 2019 through December 31, 2019 is the “Successor” period. The periods presented from January 1 through December 18, 2019 and January 1, 2018 through December 31, 2018 are the “Predecessor” periods. The Predecessor and Successor periods reflect the application of different bases of accounting as a result of the business combination, and are therefore not comparable.

The historical financial information of NFC (a special purpose acquisition company, or SPAC) prior to the business combination has not been reflected in the Predecessor financial statements as these historical amounts have been determined to be not useful information to a user of the financial statements. SPACs deposit the proceeds from their initial public offerings into a segregated trust account until a business combination occurs, where such funds are then used to either pay consideration for the acquiree or stockholders who elect to redeem their shares of common stock in connection with the business combination. SPACs will operate until the closing of a business combination, and the SPAC’s operations until the closing of a business combination, other than income from the trust account investments and transaction expenses, are nominal. Accordingly, no other activity in the Company was reported for periods prior to December 19, 2019 besides UFH’s operations as Predecessor.

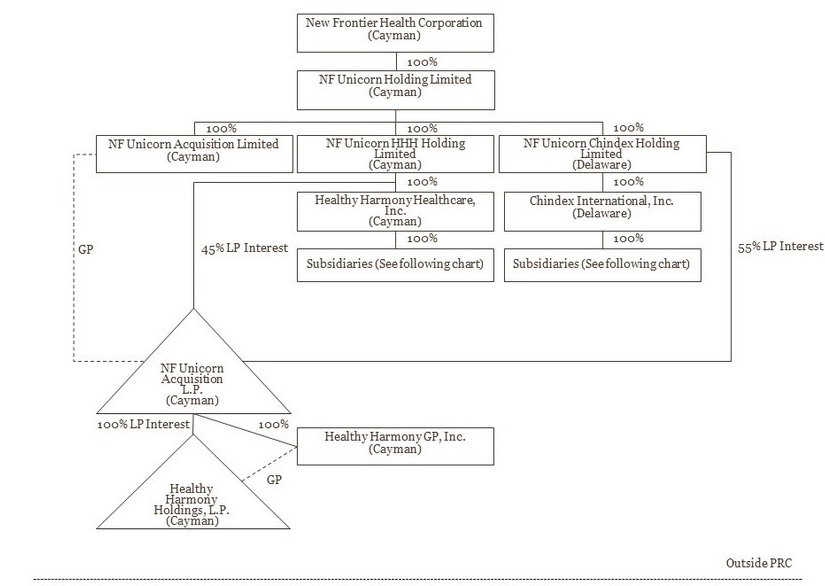

Organizational Structure

New Frontier Health Corporation is a Cayman Islands exempted company. The following diagram depicts our current organizational structure:

NF Unicorn Holding Limited (Cayman) New Frontier Health Corporation (Cayman) NF Unicorn HHH Holding Limited (Cayman) NF Unicorn Acquisition Limited (Cayman) NF Unicorn Chindex Holding Limited (Delaware) Healthy Harmony Healthcare, Inc. (Cayman) Subsidiaries (See following chart ) Chindex International, Inc. (Delaware) Subsidiaries (See following chart ) NF Unicorn Acquisition L.P. (Cayman) Healthy Harmony Holdings, L.P. (Cayman) Healthy Harmony GP, Inc . (Cayman) 100% 100% 100% 100% 100% 100% 100% 100% 45% LP Interest 55% LP Interest GP 100% LP Interest 100% GP Outside PRC

United Family Healthcare (Hong Kong) Limited (Hong Kong) NF Unicorn HHH Holding Limited (Cayman) NF Unicorn Chindex Holding Limited (Delaware) 100 % 100 % New Frontier Health Corporation (Cayman ) Healthy Harmony Healthcare, Inc. (Cayman) Healthy Harmony Limited (BVI) United Family Healthcare Limited (Hong Kong) Chindex International, Inc. (Delaware) 100 % 100 % 100 % 100 % Outside PRC Inside PRC Guangzhou United Family Hospital Co., Ltd ( GZU ) Shanghai Xincheng United Family Hospital Co., Ltd. ( PDU ) Beijing Jingbei Women & Children United Family Hospital Co., Ltd. ( DT U ) 70 % 70 % 70 % 30 % NF Unicorn Holding Limited (Cayman) 100 % 100 % (See following chart) (See following chart) 100 %

100 % 55% Qingdao United Family Qiji Hospital Management Co., Ltd Hangzhou Pumai Hospital Manageme nt Co., Ltd. Hangzhou United Family Clinic Co., Ltd. NF Unicorn Chindex Holding Limited (Delaware) Chindex International, Inc. (Delaware) United Family Hospitals and Clinics Limited (HK) United Family Healthcare Holdings Ltd. ( HK) United Family Healthcare Holdings (Mauritius) United Family American Hospital Ventures (Mauritius) United Family Healthcare Management Consulting (Beijing) Co., Ltd. ( UFH ( WFOE )) Qingdao United Family Hospital Co., Ltd . (QDU ) Beijing United Family Hospital Co., Ltd . ( BJU ) Beijing United Family Rehabilitation Hospital Co., Ltd . (Rehab ) Tianjin United Family Hospital Co., Ltd . (TJU) Beijing United Family Health Center Co., Ltd . (NH) Shanghai United Family Hospital Co., Ltd. (SHU) Beijing United Family Guangqum en Clinic Co., Ltd. (GQM) Beijing United Family Wudaokou Clinic Co., Ltd. (WDK ) Beijing United Family Jian Guo Men Clinic Co., Ltd. (JGM ) Beijing United Family Liang Ma Clinic Co., Ltd. (BLC) Beijing United Family Chao Wai Clinic Co., Ltd. (CBD) Beijing United Family Fu Xing Men Clinic Co., Ltd. (JRJ) Shanghai He Mei Jia Clinic Co., Ltd. (SRC) Shanghai He Man Jia Clinic Co., Ltd. (SHD ) Guangzhou United Family Yue Xiu Clinic Co., Ltd . ( GZC ) Shanghai United Family Hospital Fengshang Clinic Co., Ltd . (FSC) Hainan Boao United Family Medical Center Co., Ltd. (BAC ) Beijing Youhujia Healthcare Manageme nt Co., Ltd . (YHJ) Beijing Access Health Hospital Management Co., Ltd . (Access) Beijing United Family Hospital Management Co., Ltd. (S HY ) To DTU on the diagram above Outside PRC Inside PRC 100 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % 30 % 70 % 70 % 70 % 70 % 67.5% 20 % 30 % 20 % 30 % 70 % 70 % 30 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % 100 % NF Unicorn Holding Limited (Cayman) New Frontier Health Corporation (Cayman) 100 % 100 % 100 % Shanghai United Family Kangqiao Clinic Co., Ltd (KQC) 100 % Shareholding ownership Contractual ownership

| (1) | New Frontier Health Corporation is a holding company with no direct operations. |

| (2) | United Family Healthcare Management Consulting (Beijing) Co., Ltd is a wholly foreign-owned enterprise. |

| (3) | The shareholders of Beijing Access Health Hospital Management Co., Ltd. are United Family Healthcare Management Consulting (Beijing) Co., Ltd., Mr. Ming Xie and Ms. Xiaoyan Shen, owning 70%, 15% and 15% of the equity interests of Beijing Access Health Hospital Management Co., Ltd., respectively. Mr. Ming Xie is a senior executive and director of both Access and SHY, and Ms. Xiaoyan Shen is the supervisor of both Access and SHY; both act as nominee shareholders on behalf of United Family Healthcare Management Consulting (Beijing) Co., Ltd. |

| (4) | The shareholders of Beijing United Family Hospital Management Co., Ltd. are Beijing Access Health Hospital Management Co., Ltd. and Mr. Ming Xie, owning 70% and 30% of the equity interests of Beijing United Family Hospital Management Co., Ltd., respectively. Mr. Ming Xie is a senior executive and director of both Access and SHY and acts as a nominee shareholder on behalf of United Family Healthcare Management Consulting (Beijing) Co., Ltd. |

| (5) | Qingdao United Family Hospital Co., Ltd. is a wholly foreign-owned enterprise and was established as such under an exception to the Interim Measures for Administration of China — Foreign Joint Venture and Cooperative Medical Institutions, as further described in the section entitled “Business — Regulatory Matters — Regulations Relating to Foreign Investment in Our Industry.” |

| (6) | Shanghai Xincheng United Family Hospital Co., Ltd. is a China-Foreign Equity Joint Venture. |

| (7) | Guangzhou United Family Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (8) | Beijing Jingbei Women & Children United Family Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (9) | Beijing United Family Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (10) | Beijing United Family Rehabilitation Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (11) | Tianjin United Family Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (12) | Beijing United Family Health Center Co., Ltd. is a China-Foreign Contractual Joint Venture. |

| (13) | Shanghai United Family Hospital Co., Ltd. is a China-Foreign Contractual Joint Venture. |

As shown in the above diagrams, two of our subsidiaries in China are organized as partial variable interest entities to comply with Chinese laws and regulations generally limiting foreign ownership of companies in the healthcare industry to no more than 70%. As shown in the second diagram above, United Family Healthcare Management Consulting (Beijing) Co., Ltd. (“UFH (WFOE)”), which is one of our indirect, wholly-owned subsidiaries, owns 70% of the equity interests in Beijing Access Health Hospital Management Co., Ltd (“Access”), and the remaining 30% of the equity interests are held by certain senior executives of UFH, who are serving as nominee shareholders in accordance with and subject to various variable interest entity arrangements in favor of UFH (WFOE). Similarly, Access holds 70% of the equity interests in Beijing United Family Hospital Management Co., Ltd. (“SHY”, and together with Access, each a “Relevant Entity”), and the remaining 30% of the equity interests are held by a senior executive of UFH who is serving as a nominee shareholder in accordance with and subject to various variable interest entity arrangements in favor of UFH (WFOE). These variable interest entity arrangements consist of a series of contractual arrangements among UFH (WFOE), the Relevant Entities, their respective nominee shareholders and the respective nominee shareholders’ spouses, and include exclusive operation services agreements, spousal consent letters, entrustment agreements of shareholder’s rights and equity interest pledge agreements, and exclusive call option agreements, in each case, in favor of UFH (WFOE). As a result of these contractual arrangements, we are able to control 100% of the Relevant Entities (including the 30% held by the nominee shareholder(s)) and receive all of the economic benefits of the operations of the Relevant Entities.

Additional Information

Our principal executive offices are located at 10 Jiuxianqiao Road, Hengtong Business Park, B7 Building, 1/F Chaoyang District, 100015, Beijing, China. Our telephone number is 86-10-59277000. Our website is located at www.nfh.com.cn. The information contained on, or that may be accessed through, our website is not part of, and is not incorporated into, this prospectus or the registration statement of which it forms a part.

THE OFFERING

| Issuer | | New Frontier Health Corporation |

| | | |

| Shares issuable by us upon exercise of warrants | | 26,875,000 |

| | | |

| Securities that may be offered and sold from time to time by the Selling Securityholders named herein: | | |

| | | |

| Ordinary shares | | 127,341,048 (including 12,500,000 ordinary shares issuable upon exercise of the 4,750,000 forward purchase warrants and 7,750,000 private placement warrants) |

| | | |

| Forward purchase warrants | | 4,750,000 |

| | | |

| Private placement warrants | | 7,750,000 |

| | | |

| Ordinary shares issued and outstanding prior to any exercise of warrants | | 131,356,980 |

| | | |

| Shares to be issued and outstanding assuming exercise of all warrants | | 158,231,980 |

| | | |

| Transfer restrictions on 2,132,500 founder shares held by the initial shareholders other than the founders | | Under the Forward Purchase Agreements and the letter agreement entered into in connection with the IPO, the initial shareholders (other than the founders) agreed not to transfer, assign or sell any founder shares held by them until the earlier to occur of: (i) one year after the closing of the business combination or (ii) the date following the closing of the business combination on which we complete a liquidation, merger, share exchange or other similar transaction that results in all of our shareholders having the right to exchange their ordinary shares for cash, securities or other property, subject to certain exceptions. Any permitted transferees will be subject to the same restrictions and other agreements of the holders of the founder shares prior to the IPO with respect to any founder shares. Notwithstanding the foregoing, if the closing price of the ordinary shares equals or exceeds $12.00 per share (as adjusted for share splits, share capitalizations, reorganizations, recapitalizations and the like) for any 20 trading days within any 30-trading day period commencing at least 150 days after the business combination closing, the founder shares held by such investors and their permitted transferees will be released from the lock-up. |

| Transfer restrictions on 9,805,000 founder shares held by the founders | | Under the letter agreement entered into in connection with the IPO, the founders agreed that they will not transfer any founder shares held by them until the earlier of (A) with respect to 50% of such shares, one year after the completion of the business combination, (B) with respect to the remaining 50% of such shares, two years after the completion of the business combination, and (C) with respect to 100% of such shares, the date following the completion of a business combination on which the Company completes a liquidation, merger, share exchange or other similar transaction that results in all of the Company’s shareholders having the right to exchange their ordinary shares for cash, securities or other property. |

| | | |

| Transfer restrictions on 3,590,799 ordinary shares held by the Lipson Parties | | Under the Lipson Reinvestment Agreement, the Lipson Parties agreed that (i) they will not transfer any of the ordinary shares received by them at Closing at any time prior to six months from the date of Closing and (ii) at any time prior to the first anniversary of the Closing, such holder’s beneficial ownership of the ordinary shares held by them will not fall below 90% of such holder’s beneficial ownership as of immediately after the Closing; except in each case for (a) transfers among the Lipson Parties, (b) transfers as a gift to such person’s immediate family or to a trust, the beneficiary of which is a member of such person’s immediate family, an affiliate of such person or to a charitable organization, (c) by virtue of the laws of descent and distribution upon the death of such person, (d) pursuant to a qualified domestic relations order, or (e) in the event that the Company completes a liquidation, merger, share exchange or other similar transaction which results in all of its shareholders having the right to exchange their ordinary shares for cash, securities or other property; provided, however, that in the case of clauses (a) through (d) these permitted transferees must enter into a written agreement with the Company agreeing to be bound by these transfer restrictions. |

| | | |

| Transfer restrictions on 1,666,562 ordinary shares held by the Management Sellers | | Under the Management Reinvestment Agreements entered into in connection with the Closing, certain of the Management Sellers agreed that, prior to the first anniversary of the Closing, they will not transfer (i) more than the number of Unrestricted Executive NFC Shares (as defined in such Management Seller’s Management Reinvestment Agreement) held by them and (ii) any ordinary shares received by such Management Seller upon exercise or settlement, as applicable, of any of the Company’s options or RSUs issued to them at Closing; except in each case for (a) transfers as a gift to such person’s immediate family or to a trust, the beneficiary of which is a member of such person’s immediate family, an affiliate of such person or to a charitable organization, (b) by virtue of the laws of descent and distribution upon the death of such person, (c) pursuant to a qualified domestic relations order, or (d) in the event that the Company completes a liquidation, merger, share exchange or other similar transaction which results in all of its shareholders having the right to exchange their ordinary shares for cash, securities or other property; provided, however, that in the case of clauses (a) through (d) these permitted transferees must enter into a written agreement with the Company agreeing to be bound by these transfer restrictions. |

| Transfer restrictions on private placement warrants | | The private placement warrants and the ordinary shares underlying such warrants are not transferable or salable until 30 days after the completion of the business combination, except in each case (a) to our officers or directors, any affiliate or family members of any of our officers or directors, any affiliate of the Sponsor or to any member of the Sponsor or any of their affiliates or shareholders, (b) in the case of an individual, as a gift to such person’s immediate family or to a trust, the beneficiary of which is a member of such person’s immediate family, an affiliate of such person or to a charitable organization; (iii) in the case of an individual, by virtue of laws of descent and distribution upon death of such person; (iv) in the case of an individual, pursuant to a qualified domestic relations order; (v) by private sales or transfers made in connection with any Forward Purchase Agreement or similar arrangement or in connection with the consummation of the business combination at prices no greater than the price at which the shares or warrants were originally purchased; (vi) by virtue of the laws of the Cayman Islands upon dissolution of the Sponsor, or (vii) in the event that, subsequent to its consummation of the business combination, the Company completes a liquidation, merger, share exchange or other similar transaction which results in all of its shareholders having the right to exchange their ordinary shares for cash, securities or other property; provided, however, that in the case of clauses (i) through (vi) these permitted transferees must enter into a written agreement with the Company agreeing to be bound by these transfer restrictions. |

| | | |

| Use of proceeds | | All of the ordinary shares and warrants (including shares underlying such warrants) offered by the Selling Securityholders pursuant to this prospectus will be sold by the Selling Securityholders for their respective accounts. We will not receive any of the proceeds from these sales. We will receive up to an aggregate of approximately $165,312,500 from the exercise of public warrants, approximately $54,625,000 from the exercise of the forward purchase warrants and approximately $89,125,000 from the exercise of private placement warrants, assuming the exercise in full of all the warrants for cash. The private placement warrants may be exercised on a “cashless basis” so long as they are held by their initial purchasers or their permitted transferees. We expect to use the net proceeds from the exercise of the warrants for general corporate purposes, which may include acquisitions and other business opportunities and the repayment of indebtedness. Our management will have broad discretion over the use of proceeds from the exercise of the warrants. |

| Market for our ordinary shares and warrants | | Our ordinary shares and public warrants are currently listed on NYSE and, after resale, the forward purchase warrants and the private placement warrants will also trade under the same CUSIP and ticker symbol as the public warrants. |

| | | |

| NYSE Ticker Symbols | | “NFH” and “NFH WS” |

| | | |

| Risk Factors | | Any investment in the securities offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” on page 12 of this prospectus. |

SELECTED HISTORICAL FINANCIAL INFORMATION

The following tables set forth, for the periods and dates indicated, certain selected historical financial information. You should read the following selected combined financial and other data in conjunction with “Operating and Financial Review and Prospects” and the audited financial statements and respective notes included elsewhere in this prospectus. Historical results are not necessarily indicative of the results that may be expected in the future.

Prior to the business combination, NFC was a blank check company with nominal operations. On December 18, 2019, we completed the business combination, whereby we acquired UFH. In the business combination, NFC was deemed the accounting acquirer and UFH was deemed the acquiree, and our accounting predecessor. As a result of the application of the acquisition method of accounting as of the effective time of the business combination, the accompanying summary historical financial information includes a black line division which indicates that the Predecessor and Successor reporting entities shown are presented on a different basis and are, therefore, not comparable. The period presented from December 19, 2019 through December 31, 2019 is the “Successor” period. The periods presented from January 1, 2019 through December 18, 2019, the year ended December 31, 2018 and the year ended December 31, 2017 are the “Predecessor” periods.

The following tables set forth summary consolidated financial information as of December 31, 2019 (Successor) and December 31, 2018 (Predecessor), from December 19, 2019 through December 31, 2019 (Successor), from January 1, 2019 through December 18, 2019 (Predecessor) and each of the two years ended December 31, 2018 (Predecessor). The consolidated financial information is derived from the audited consolidated financial statements included elsewhere in this prospectus.

The historical financial information of NFC (a special purpose acquisition company, or SPAC) prior to the business combination has not been reflected in the Predecessor financial statements as these historical amounts have been determined to be not useful information to a user of the financial statements. SPACs deposit the proceeds from their initial public offerings into a segregated trust account until a business combination occurs, where such funds are then used to either pay consideration for the acquiree or stockholders who elect to redeem their shares of common stock in connection with the business combination. SPACs will operate until the closing of a business combination, and the SPAC’s operations until the closing of a business combination, other than income from the trust account investments and transaction expenses, are nominal. Accordingly, no other activity in the Company was reported for periods prior to December 19, 2019 besides UFH’s operations as Predecessor. The financial information has been prepared in accordance with International Financial Reporting Standards, which we refer to as IFRS, as issued by the International Accounting Standards Board.

The consolidated financial statements are stated in thousands of Renminbi (“RMB”).

| | | Predecessor | | | Successor | |

| | | Year Ended

December 31

2017 | | | Year Ended

December 31

2018 | | | Period from

January 1 to

December 18

2019 | | | Period from

December 19

to December 31

2019 | |

| (in thousands) | | RMB | | | RMB | | | RMB | | | RMB | |

| | | | | | | | | | | | | |

| Statement of Profit or Loss and Other Comprehensive Income Data: | | | | | | | | | | | | | | | | |

| Revenues | | | 1,827,880 | | | | 2,058,779 | | | | 2,369,167 | | | | 80,035 | |

| Net profit/(loss) | | | 1,591 | | | | (154,046 | ) | | | (228,378 | ) | | | (230,297 | ) |

| | | | | | | | | | | | | | | | | |

| Statement of Cash Flows Data: | | | | | | | | | | | | | | | | |

| Net cash provided by operating activities | | | 191,220 | | | | 130,980 | | | | 316,639 | | | | (80,432 | ) |

| Net cash used in investing activities | | | (129,850 | ) | | | (534,948 | ) | | | (341,771 | ) | | | (45,671 | ) |

| Net cash provided by/(used in) financing activities | | | 233,681 | | | | 103,635 | | | | (189,961 | ) | | | (9,702 | ) |

| | | Predecessor | | | Successor | |

| | | December 31

2018 | | | December 31

2019 | |

| | | RMB | | | RMB | |

| Statement of Financial Position Data: | | | | | | | | |

| Total assets | | | 5,172,462 | | | | 14,649,635 | |

| Total liabilities | | | 1,832,814 | | | | 6,242,666 | |

| Total equity | | | 3,339,648 | | | | 8,406,969 | |

RISK FACTORS

An investment in our securities involves a high degree of risk. You should consider carefully the following risks, together with all the other information in this prospectus, including our financial statements and notes thereto before you invest in our ordinary shares. If any of the following risks actually materializes our operating results financial condition and liquidity could be materially adversely affected. As a result, the trading price of our ordinary shares could decline and you could lose all or part of your investment.

Risks Relating to Our Business and Financial Condition

If our existing facilities fail to perform as expected, our overall business could be negatively impacted.

Our existing facilities are all strategic investments which have expected growth rates. These growth rates are based on many factors, including, but not limited to, a baseline expected ramp-up based on previously opened and ramped-up businesses, our management’s opinion and publicly available data on market capacity, planned capital investment in the Company, and our management’s best estimates and projections of macroeconomic, cultural, and regulatory factors based on publicly available data and information. Several of these factors make necessary assumptions and judgments based on management’s experience and expertise, and as such may be imperfect or subject to error. If these factors, assumptions, or judgments prove to be inaccurate or incomplete, the ramp-up of existing facilities could be negatively impacted and adversely affect our business. Furthermore, our management uses the cash flow expectations of its existing facilities, which take into account projected ramp-ups and growth trends, as inputs for certain of our financing and timing decisions relating to potential expansion projects and capital investments. Therefore, if existing facilities do not ramp up as expected, our future expansions and capital investments may have to be reassessed, or even delayed or canceled, which could adversely impact the overall business.

We may experience difficulties executing our expansion plans.

Our long-term expansion plans include targeted expansion into highly populated markets through the development of new facilities in cities such as Shenzhen, among others, as well as expanding current facilities and opening additional facilities in our existing markets, namely Beijing, Shanghai, Tianjin, Qingdao and Guangzhou. In addition, we plan to continue expanding the number and variety of services we offer at such facilities. As a result, we expect to continue to make capital expenditures over the coming years.

The profitability or success of our current and future projects and investments are subject to numerous factors, conditions and assumptions, many of which are beyond our control. Unfavorable outcomes could reduce our available cash and limit our ability to make cash investments in the future. This could result in lower investment interest or earnings which could result in net losses, and reduce our ability to service current or future indebtedness, which might require us to take on additional borrowings at higher costs. Any of these could have a material adverse effect on our future financial condition or results of operations. Further, any additional financing necessary to complete our expansion plans may not be available on favorable terms, or at all.

Commencement of facility construction is subject to governmental approval and permitting processes, which could materially affect the ultimate cost and timing of construction. Numerous factors, many of which are beyond our control, may influence the ultimate costs and timing of various projects or capital improvements at our facilities, including:

| · | delays in mandatory governmental approvals; |

| · | additional land or facilities acquisition costs; |

| · | increases in the budgeted costs, including increases in the costs of construction materials and labor; |

| · | unforeseen changes in design or delays in construction permits; |

| · | litigation, accidents or natural disasters affecting the construction site; and |

| · | national or regional economic, regulatory or geopolitical changes. |

| · | future outbreaks of infectious diseases like the recent coronavirus (or COVID-19), or the previous SARS virus, which could delay the progress of construction projects due to the possible unavailability of construction workers, or government mandated work stoppages on construction sites. |

In addition, actual costs could vary materially from our estimates if those factors or our assumptions about the quality of materials or labor required, or the cost of financing were to change. Should healthcare facility projects be abandoned or substantially decreased in scope due to the inability to obtain necessary permits or other governmental approvals or other unforeseen negative factors, we could be required to expense some or all previously capitalized costs, which could have a material adverse effect on our future financial condition or results of operations.

We may not be able to manage our expected growth and enlarged business.

We plan to make capital expenditures over the coming years to implement our expansion strategy. This growth strategy may not be successful for the following reasons:

| · | Our ability to obtain additional capital for growth is subject to a variety of uncertainties, including our operating results, financial condition, capital market perception, general market conditions for capital raising activities by healthcare companies, and economic conditions in China. |

| · | Our profitability may be adversely affected by the additional costs and expenses associated with the operation of new facilities, increased marketing and sales support activities, technological improvement projects, the recruitment of new employees, the upgrading of our managerial, operational and financial systems, procedures and controls, and the training and management of our growing employee base. |

| · | The increased scale of operation will present our management with challenges associated with operating an enlarged business, including dedication of substantially more time and resources in operating and managing facilities in new geographic locations in China, ensuring regulatory compliance and continuing to manage and grow our business. |

We cannot be certain that our cash flows will grow at all or grow rapidly enough to satisfy the capital and expenses necessary for our growth. It is difficult to assess the extent of capital and expenditure necessary for our growth and their impact on our operating results. Failure to manage growth and enlarged business effectively could have a material adverse effect on our business, financial condition and results of operations.

Our business is capital intensive and we may not be able to secure additional capital financing for new projects or execute new business strategies.

We currently have adequate capital to fund our current expansion projects. However, we may not be able to raise sufficient capital to complete some or all of our business strategies in the future, including new projects or acquisitions, or to react rapidly enough to changes in technology, products, services or the competitive landscape. Healthcare service providers often face high capital requirements in order to take advantage of new market opportunities, respond to rigorous competitive pressure and react quickly to changes in technology and as such, there can be no assurance that we will be able to satisfy our capital requirements in the future. In particular, our expansion strategy requires the construction and maintenance of new and existing healthcare facilities, which requires and depends upon the availability of significant capital, not all of which may be available at the time such project is considered or commenced. In the absence of sufficient available or obtainable capital, we would likely be unable to establish new facilities or maintain growth at our existing facilities as planned. In addition, we may incur costs for projects that may not be completed as projected, if at all, and we may be required to seek capital in financings under circumstances and at times that limit the optimization of the terms of such financings.

If leases at our existing facilities are not renewed or are cancelled, our overall business could be materially impacted.

Our premises are all leased from third parties, and in general have fixed terms. Approximately 9% of our leases in terms of the lease contract value are up for renewal in the next five years. If we are unable to renew our leases, or our leases are terminated before the lease ends, our existing operations may need to be relocated and we would have to pay the associated expenses of relocation, which could be significant. Operation relocation may have negative impacts on our business, including but not limited to: reduced patient volumes if a new location is inconvenient for existing patients; pressure on physician or administration teams if a new location is inconvenient for existing staff; reductions in available space for operations at a new location; less attractive lease terms at a new location; unanticipated capital expenditures to renovate a new location; and possible extra rent expense as we pay rent for a new location during construction and fit-out while a previous location continues operations. For example, the lease of one of the buildings of Beijing United Family Hospital (“BJU”), which covers a total of 6,184 square meters of leased area, is up for renewal by December 31, 2020. Our management team is in active discussions with the landlord to renew the lease. If we are unable to renew this lease, the existing operations of BJU may need to be relocated to the clinics and other UFH facilities in Beijing. The relocation may cause disruption of the operations and business of BJU and cause significant relocation expenses. In addition, BJU's operations and financial performance may be temporarily materially impacted. Any of these factors may have an adverse effect on our business and results of operations.

Expansion of private healthcare services to reach the Chinese population depends to some extent on the development of insurance products that are not widely available or used.

Expected growth of commercial medical insurance products availability and consumption by the Chinese population is an assumption for our growth and investment decisions. Currently, commercial medical insurance is not generally purchased by the majority of the Chinese population; however, according to the China Insurance Yearbook, gross written commercial health insurance premiums sold in China increased from approximately $12 billion in 2012 to approximately $76 billion in 2018 and, according to the EY White Paper on China Commercial Health Insurance, is expected to reach $181 billion by 2020. This rapid growth is anticipated to continue in the future. Furthermore, reimbursement under Chinese government public healthcare insurance is either not enough to cover the entire cost or partial cost of services at private healthcare facilities like ours, consequently, our patients often have to pay for their procedures themselves. This limitation may impede the attractiveness of our services as compared to services at public hospitals for which government benefits provide coverage, especially during economic downturns. As part of our expansion plans, we intend to implement initiatives to increase the number of our local Chinese patients, including increasing marketing outreach and piloting new commercial insurance products primarily targeted at local Chinese patients. If we are not able to achieve success with these initiatives or the commercial insurance industry does not grow as expected, our ability to continue to grow our business may be materially adversely affected.

Our financial performance may be affected by seasonal and annual fluctuations.

Our revenues are impacted by seasonal and annual fluctuations related to epidemiological, cultural, and lifestyle factors. For example, many expatriate and affluent Chinese families traditionally travel outside of China for spring and summer festival vacations, so our revenue typically decreases during those times of year. There are also regular seasonal epidemiological factors where certain medical conditions and patient volumes fluctuate over the course of the year, such as the annual flu season which typically boosts primary care volume during the winter months. In addition, there are often variations in demand year to year for obstetrics services depending on the relative attractiveness of any particular Chinese zodiac calendar year, with certain years being considered particularly attractive, boosting volume, and some considered particularly negative, with ensuing volume, revenue, and referral impacts. As a result of these and other unpredictable seasonal factors, our operating results may fluctuate and adversely impact our business.

New or ongoing health epidemics could adversely affect our operations.

An epidemic outbreak could significantly disrupt our ability to adequately staff our facilities and may generally disrupt operations. For example, in March 2003, several countries, including China, experienced an outbreak of a new and highly contagious form of atypical pneumonia now commonly known as Severe Acute Respiratory Syndrome, or “SARS.” The severity of the outbreak in certain municipalities, such as Beijing, and provinces, such as the Guangdong Province, materially affected general commercial activity. In particular, a large percentage of the expatriate community that uses our healthcare services left China during the height of the SARS epidemic and could be expected to do so again under similar circumstances. The SARS epidemic in China had a significantly negative impact on our healthcare business, and the extent of any adverse impact that any future SARS outbreak or similar epidemic, such as Avian flu or Swine flu, could have on the Chinese economy and on our business cannot be predicted at this time.

More recently, in December 2019, a novel strain of coronavirus, or COVID-19, was first identified in Wuhan, China, and subsequently spread throughout China and the rest of the world. The Chinese central government and local government in Wuhan and other cities in China introduced various temporary measures to contain the coronavirus outbreak, such as extension of the Lunar New Year holiday, travel restrictions, and voluntary and involuntary quarantines, which have impacted national and local economies to varying degrees. As a result, our operations have been impacted by temporary delays in business activities, commercial transactions and general uncertainties surrounding the duration of the government’s extended business and travel restrictions. In addition, our business operations could be disrupted if any of our employees contracts or is suspected of contracting the coronavirus or any other epidemic disease, since our employees could be quarantined and/or our offices be shut down for disinfection. Also, changes in patient healthcare consumption habits as a result of the epidemic, or patients voluntarily leaving China temporarily or permanently in response to this epidemic, could materially impact our business. The potential downturn brought by and the duration of the coronavirus outbreak are difficult to assess or predict and the actual effects on our business and the global economy will depend on many factors beyond our control. The extent to which the coronavirus impacts our results remains uncertain, and we are closely monitoring its impact. Our business, results of operations, financial conditions and prospects could be directly adversely affected, as well as indirectly, to the extent that the coronavirus or any other epidemic harms the Chinese and global economies in general.

As of March 2020, the number of COVID-19 cases in China has been significantly reduced, but the number of cases are increasing globally, the effects of which may materially and negatively impact our business, through lower international travel and commerce, interrupted supply chains, international recruiting difficulty, general international economic softness leading to lower consumer sentiment and spending, as well as numerous other unknown and unforeseeable negative consequences which could negatively impact our operations and business. In addition, any future health pandemic or similar outbreak could severely restrict the level of economic activity in affected areas, which could have a material adverse effect on our business and results of operations.

If we fail to manage our growth or maintain adequate internal accounting, disclosure, data security, and other controls, our business could be adversely affected.

We have expanded our operations rapidly in recent years and continue to explore ways to extend our service and product offerings. Our growth may place a strain on our management systems, information technology systems, resources, internal control over financial reporting and disclosure controls. Our ability to operate our business requires adequate information systems and resources as well as sufficient oversight from senior management. As such, our ability to manage our operations and future growth will require us to continue to improve our operational, financial, data, and management controls, including our internal control over financial reporting and disclosure controls, reporting systems and procedures. As a result of our expansion, we may not be able to maintain adequate controls and procedures or implement improvements to our management, information technology, and control systems in an efficient or timely manner and may discover deficiencies in our existing systems and controls. Our inability to successfully manage our growth and expand our operations could have a material and adverse effect on our business, financial condition, results of operations and prospects.

We face competition that could adversely affect our results of operations.

Our Beijing, Shanghai, Tianjin, Qingdao, Guangzhou, and Hangzhou healthcare facilities compete with a large number and variety of healthcare facilities in their respective markets. There are many public Chinese hospitals and many of these offer so called “VIP” services, which cater mostly to the affluent Chinese market as well as some foreign residents, and also international clinics serving the expatriate and diplomatic communities and affluent Chinese population. There can be no assurance that these or other hospitals, clinics or facilities will not commence or expand their operations, which could increase competition and potentially affect our market position. Further, there can be no assurance that a qualified Western-style or other healthcare organization, having greater resources in the provision or management of healthcare services, will not enter the market and provide similar services to those being provided by us in any of the cities in which we currently operate or plan to expand. Any shift in the competitive landscape could adversely affect our business, such as driving down market perception on prices for private healthcare services.

Competition in payor systems may also emerge in the Chinese private healthcare industry. Managed care or HMO models, innovative payor contract models, or new or reformed government payor systems could change our payor mix, putting pressure on prices as we seek to attract patients from managed care networks, sign payor contracts, or be eligible for new or reformed government reimbursement systems.

If our management decides or is compelled to lower prices as a competitive strategy or reaction for these or other reasons, revenues may be negatively impacted and overall profitability and growth may be adversely affected.

Our business may be adversely affected by inflation or foreign currency fluctuation.

We generate 100% of our revenue and incur approximately 99% of our expenses in Chinese Yuan (“RMB”) within China. The RMB is not freely traded and is closely controlled by the Chinese government and so the value of the RMB against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, the political situation as well as economic policies and conditions. In addition, it is difficult to predict how market forces or Chinese or U.S. government policy may impact the exchange rate between RMB and the U.S. dollar in the future.