UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________

FORM N-CSR/A

________

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23348

City National Rochdale Strategic Credit Fund

(Exact name of registrant as specified in charter)

________

400 Park Avenue

New York, New York 10022

(Address of principal executive offices) (Zip code)

Rochelle Levy

City National Rochdale, LLC

400 Park Avenue

New York, New York 10022

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-888-889-0799

Date of fiscal year end: May 31, 2024

Date of reporting period: May 31, 2024

Explanatory Note: This Form N-CSR/A is filed to correct the title of the signatory of the “Investment Advisory’s Report” and to add biographical information to the Trustee and Officer table of the Fund’s new Interim President.” Other than the aforementioned changes, no other information or disclosures contained in the Form are amended by this Form N-CSR/A.

Item 1. Reports to Stockholders.

| (a) | A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto. |

TABLE OF CONTENTS

City National Rochdale Strategic Credit Fund |

2 | Investment Adviser’s Report |

4 | Fund Overview |

5 | Schedule of Investments |

10 | Statement of Assets and Liabilities |

11 | Statement of Operations |

12 | Statements of Changes in Net Assets |

13 | Statement of Cash Flows |

14 | Financial Highlights |

15 | Notes to Financial Statements |

30 | Report of Independent Registered Public Accounting Firm |

31 | Trustees and Officers |

34 | Notice to Shareholders |

35 | Disclosure of Fund Expenses |

36 | Board Approval of Advisory and Sub-Advisory Agreements |

The Fund files its complete schedule of investments with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT within 60 days after the end of the period. The Fund’s Form N-PORT reports are available on the Commission’s website at https://www.sec.gov. The most current Schedule of Investments is available on the Fund’s website at www.citynationalrochdalefunds.com and without charge, upon request, by calling 1-888-889-0799.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to the Fund’s portfolio securities is available, and information on how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available (1) without charge, upon request, by calling 1-888-889-0799, (2) on the Fund’s website at www.citynationalrochdalefunds.com, and (3) on the Commission’s website at https://www.sec.gov.

City National Rochdale Strategic Credit Fund | PAGE 1

investment adviser’s report (Unaudited) |

May 31, 2024 |

City National Rochdale Strategic Credit Fund |

Dear Fellow Shareholders,

The primary objective of the City National Rochdale Strategic Credit Fund (the “Fund”) is to generate current income, and its secondary objective is long-term capital appreciation. The Fund pursues its investment objectives by investing mainly in debt securities and other credit related investments, primarily sourcing opportunities in collateralized loan obligations (“CLOs”). We view the Fund as a complement to other liquid opportunistic income portfolios and appropriate for sophisticated investors that seek diversification and income potential over a longer time horizon.

For the year ended May 31, 2024, the Fund posted a return of +29.29%, underperforming the Palmer Square CLO BB Total Return Index (+30.56%), and outperforming the Palmer Square CLO BBB Total Return Index (+19.34%). Due to the Fund’s ability to invest in all segments of the CLO market, the Fund compares its performance to a 50/50 blend of the BB/BBB indices (the “50/50 Blended Benchmark”), which the Fund outperformed by +4.34% (+29.29% for the Fund vs. +24.95% for the 50/50 Blended Benchmark). Over the past 12 months, the Fund distributed $1.69 per share in income, resulting in a 12-month yield of 22.03% with the Fund’s net asset value per share priced at $7.67.

Strong performance for the past 12 months is a result of higher leveraged loan prices and positive market sentiment impacting CLOs broadly. The threat of higher defaults with higher interest rate costs did not materialize in the loan market. While the Fund does have exposure to multiple segments of CLOs, the equity positions bear the first loss arising out of default, and they generally have higher expected returns. We continue to believe that barring any significant default cycles, there are significant opportunities in the CLO equity segments of a client portfolio, and we see current levels of cash flow continuing even with potential rate cuts on the horizon. Over the three years ended May 31, 2024, the Fund has annualized +9.34% returns and outperformed the 50/50 Blended Benchmark by +0.62% (+9.34% vs. 8.72% annualized).

Markets rallied significantly over the past 12 months, but few income markets provided the return exposure like CLOs. For comparison, the Bloomberg US High Yield Index returned +11.24%, and the Bloomberg US Aggregate Index returned +1.31%. This was driven by reduced recession risk and resilient corporate earnings, while inflation continued to come down from the previous year’s highs.

As mentioned in prior letters, our investment thesis for the Fund (and CLO markets in general) is that market dislocations will occur, and we expect recoveries to allow for large recoupments of losses when there is market volatility. We saw that play out in the year ended May 31, 2024, and believe our investor base was rewarded.

While we do see some challenges, many things bode well for CLOs during these times. Underlying investments are naturally hedged against changing interest rates, higher yield levels that we currently see in the market can offset potential volatility, and there are structural benefits in the underlying market that are used to preserve investors’ capital over the long term (e.g., collateral managers are usually not forced sellers).

Given the environment, the Fund is currently maintaining allocations to segments of the market with the potential for higher risk/higher return, but the Fund continues to be diversified across different risk segments. We do believe that there will be continued bouts of volatility in the market over the near term, and we see managers taking advantage of this potential instability.

Thank you for your support and confidence in the Fund.

Sincerely,

Tom Ehrlein

Director, Investment Solutions

Co-Portfolio Manager, City National Rochdale Strategic Credit Fund

This information must be preceded or accompanied by a current prospectus. Please read the prospectus carefully before investing.

This material represents the investment adviser’s assessment of the portfolio and market environment at a specific point

City National Rochdale Strategic Credit Fund | PAGE 2

investment adviser’s report (Unaudited) |

May 31, 2024 |

City National Rochdale Strategic Credit Fund (continued) |

in time and should not be relied upon by the reader as research or investment advice. These views are as of the date of this report and subject to change based on market conditions.

Performance data quoted represents past performance and does not guarantee similar future results.

Diversification does not ensure a profit or guarantee against a loss.

Risk Disclosures:

The Fund is a non-diversified, closed-end management investment company. The Fund’s shares have no history of public trading and the Fund does not currently intend to list its shares for trading on any national securities exchange. There currently is no secondary market for the Fund’s shares and the Fund expects that no secondary market will develop. The shares are, therefore, not readily marketable. Even if such a market were to develop, shares of closed-end funds frequently trade at prices lower than their net asset value.

This Fund is a closed-end interval fund. Investors may only redeem shares on a quarterly basis. Even though the Fund will make quarterly repurchase offers to repurchase a portion of the shares to provide some liquidity to shareholders, you should consider the shares to be an illiquid investment. There is no assurance that every investor will be able to tender their respective shares when or in the amount that the investor desires. An investment in the Fund is suitable only for long term investors who can bear the risks associated with the limited liquidity of the shares. The amount of distributions that the Fund may pay, if any, is uncertain. Investing involves risk, including possible loss of principal. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Bonds and bond funds are subject to interest rate risks and will decline in value as interest rates rise. Investing in securities that are not investment grade generally offers a higher yield but also carries a greater degree of risk of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments.

Risks associated with bank loans include (i) prepayment risk which could cause the Fund to reinvest prepayment proceeds in lower- yielding investments; (ii) credit risk; and (iii) price volatility due to such factors as interest rate sensitivity and liquidity. The quality of the collateral underlying the CLOs may decline in value or default. Investments in CLO equity and junior debt tranches will likely be subordinate in right of payment to other senior classes of CLO debt. The complex structure of a particular CLO may not be fully understood at the time of investment and may produce disputes with the issuer or unexpected investment results. The value of any collateral or distributions from collateral assets can decline or be insufficient to meet the issuer’s obligations. The Fund may invest in floating rate loans and similar instruments which may be illiquid or less liquid than other investments. The Fund may invest in distressed investments, which tend to be more volatile and sensitive to changing interest rates and adverse economic conditions than other securities. The Fund may not be able to divest itself of these securities.

The Fund or its underlying investments may utilize derivatives. The market value of the underlying securities and of the derivative instruments relating to those securities may not be proportionate. Derivatives are subject to illiquidity and counterparty risk. The use of leverage by the Fund’s manager may accelerate the velocity of potential losses.

The Fund is subject to the risk that one or more of the securities in which the Fund invests are priced incorrectly, due to factors such as incomplete data, market instability, lack of a liquid secondary market or human error. Restricted and illiquid securities may be difficult to sell for the value at which they are carried, if at all, or at any price within the desired time frame. Investing in restricted and illiquid securities may subject a portfolio to higher costs and liquidity risk.

City National Rochdale Strategic Credit Fund | PAGE 3

fund overview (Unaudited) |

May 31, 2024 |

City National Rochdale Strategic Credit Fund |

The Fund’s primary objective is to generate current income; its secondary objective is long-term capital appreciation.

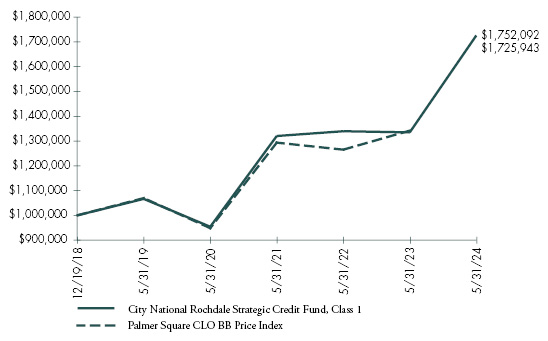

Comparison of Change in the Value of a $1,000,000 Investment in the City National Rochdale Strategic Credit Fund, Class 1, versus the Palmer Square CLO BB Price Index(1)

(1) | The performance in the above graph does not reflect the deduction of taxes the shareholder will pay on Fund distributions or the redemptions of Fund shares. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. |

Past performance is no indication of future performance. |

The Fund’s comparative benchmark does not include the annual operating expenses incurred by the Fund. Please note that one cannot invest directly in an unmanaged index. |

AVERAGE ANNUAL TOTAL RETURNS | |||||

| Ticker | One Year | Three Year | Five Year | Since |

City National Rochdale Strategic Credit Fund, Class 1(1) | CNROX | 29.29% | 9.34% | 10.11% | 10.53% |

Palmer Square CLO BB Total Return Index | PCLOBBTR | 30.56% | 10.63% | 10.36% | 11.14% |

Palmer Square CLO BBB Total Return Index | PCLOBBBT | 19.34% | 6.80% | 6.33% | 6.97% |

(1) | Commenced operations on December 19, 2018. |

City National Rochdale Strategic Credit Fund | PAGE 4

schedule of investments |

May 31, 2024 |

City National Rochdale Strategic Credit Fund |

Description | Face Amount (000) | Value (000) | ||||||||||

Asset-Backed Securities [96.7%] | ||||||||||||

Other Asset-Backed Securities [96.7%] | ||||||||||||

AIMCO CLO 17 Equity, Ser 2022-17A, Cl SUB | ||||||||||||

12.010%, 07/20/35(A) | $ | 10,250 | $ | 7,881 | ||||||||

AIMCO CLO 21, Ser 2024-21A, Cl F | ||||||||||||

11.826%, TSFR3M + 6.500%, 04/18/37(B)(C) | 1,250 | 1,127 | ||||||||||

AIMCO CLO Equity, Ser 2021-15A, Cl SUB | ||||||||||||

15.270%, 10/17/34(A)(C) | 9,750 | 5,904 | ||||||||||

ALM 2020 CLO Equity, Ser 2020-1A, Cl SUB | ||||||||||||

11.760%, 10/15/29(A)(C) | 5,025 | 2,331 | ||||||||||

Apidos CLO XL Equity, Ser 2022-40A, Cl SUB | ||||||||||||

12.180%, 07/15/35(A) | 2,250 | 1,570 | ||||||||||

Apidos CLO XXVIII Equity, Ser 2017-28A, Cl SUB | ||||||||||||

19.060%, 01/20/31(A)(C) | 2,000 | 640 | ||||||||||

Apidos CLO XXXII Equity, Ser 2019-32A, Cl SUB | ||||||||||||

12.830%, 01/20/33(A)(C) | 4,400 | 3,064 | ||||||||||

Apidos CLO XXXV Equity, Ser 2021-35A, Cl SUB | ||||||||||||

19.440%, 04/20/34(A)(C) | 500 | 284 | ||||||||||

Ares LXII CLO Equity, Ser 2021-62A, Cl SUB | ||||||||||||

16.530%, 01/25/34(A)(C) | 1,500 | 1,029 | ||||||||||

Barings CLO, Ser 2015-2A, Cl ER | ||||||||||||

12.036%, TSFR3M + 6.712%, 10/20/30(B)(C) | 2,500 | 2,490 | ||||||||||

Barings CLO Equity, Ser 2018-2, Cl SUB | ||||||||||||

11.730%, 04/15/30(A) | 1,000 | 406 | ||||||||||

Barings CLO Equity, Ser 2020-4A, Cl SUB | ||||||||||||

18.740%, 01/20/32(A)(C) | 6,500 | 3,059 | ||||||||||

Battalion CLO XVI Equity, Ser 2019-16A, Cl SUB | ||||||||||||

30.770%, 12/19/32(A)(C) | 2,500 | 940 | ||||||||||

BlueMountain CLO, Ser 2018-3A, Cl E | ||||||||||||

11.535%, TSFR3M + 6.212%, 10/25/30(B)(C) | 750 | 720 | ||||||||||

BlueMountain CLO XXII Equity, Ser 2018-22A, Cl SUB | ||||||||||||

33.260%, 07/15/31(A)(C) | 3,500 | 805 | ||||||||||

BlueMountain CLO XXIII Equity, Ser 2018-23A, Cl SUB | ||||||||||||

25.200%, 10/20/31(A)(C) | 9,500 | 3,535 | ||||||||||

BlueMountain Fuji US CLO I, Ser 2017-1A, Cl E | ||||||||||||

11.586%, TSFR3M + 6.262%, 07/20/29(B)(C) | 1,500 | 1,436 | ||||||||||

BlueMountain Fuji US CLO II Equity, Ser 2017-2A, Cl SUB | ||||||||||||

69.290%, 10/20/30(A)(C) | 1,500 | 210 | ||||||||||

BlueMountain Fuji US CLO III Equity, Ser 2017-3A, Cl SUB | ||||||||||||

29.050%, 01/15/30(A)(C) | 4,225 | 955 | ||||||||||

Burnham Park CLO Equity, Ser 2016-1A, Cl SUB | ||||||||||||

0.000%, 10/20/29(A)(E)(F) | 16,576 | 787 | ||||||||||

Carlyle Global Market Strategies CLO, Ser 2013-3A, Cl DR | ||||||||||||

11.090%, TSFR3M + 5.762%, 10/15/30(B)(C) | 400 | 387 | ||||||||||

Carlyle Global Market Strategies CLO, Ser 2014-1A, Cl ER | ||||||||||||

10.979%, TSFR3M + 5.662%, 04/17/31(B)(C) | 3,400 | 3,223 | ||||||||||

Carlyle Global Market Strategies CLO Equity, Ser 2014-1A, Cl INC | ||||||||||||

43.610%, 04/17/31(A)(C) | 500 | 65 | ||||||||||

Carlyle Global Market Strategies CLO Equity, Ser 2015-1A, Cl SUB | ||||||||||||

0.000%, 07/20/31(A)(C)(F) | 613 | 19 | ||||||||||

Carlyle Global Market Strategies CLO Equity, Ser 2021-5A, Cl SUB | ||||||||||||

16.660%, 07/20/34(A) | 7,250 | 4,426 | ||||||||||

Carlyle US CLO Equity, Ser 2017-2A, Cl SUB | ||||||||||||

16.350%, 07/20/31(A)(C) | 12,750 | 2,744 | ||||||||||

Carlyle US CLO Equity, Ser 2018-1A, Cl SUB | ||||||||||||

0.000%, 04/20/31(A)(C)(E)(F) | 600 | 24 | ||||||||||

Carlyle US CLO Equity, Ser 2017-5A, Cl SUB | ||||||||||||

25.800%, 01/20/30(A)(C) | 13,500 | 2,766 | ||||||||||

Clover CLO Equity, Ser 2019-2A, Cl SUB | ||||||||||||

14.870%, 10/25/33(A)(C) | 3,000 | 2,012 | ||||||||||

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 5

schedule of investments |

May 31, 2024 |

City National Rochdale Strategic Credit Fund (continued) |

Description | Face Amount (000) | Value (000) | ||||||||||

Crown Point CLO IV, Ser 2018-4A, Cl E | ||||||||||||

11.086%, TSFR3M + 5.762%, 04/20/31(B)(C) | $ | 1,000 | $ | 888 | ||||||||

Dryden 40 Senior Loan Fund CLO, Ser 2018-40A, Cl FR | ||||||||||||

13.444%, TSFR3M + 8.122%, 08/15/31(B)(C) | 500 | 367 | ||||||||||

Dryden 75 CLO Equity, Ser 2019-75A, Cl SUB | ||||||||||||

15.420%, 04/14/34(A)(C) | 500 | 290 | ||||||||||

Dryden 93 CLO Equity, Ser 2021-93A, Cl SUB | ||||||||||||

13.960%, 01/15/34(A)(C) | 13,250 | 6,184 | ||||||||||

Dryden 95 CLO Equity, Ser 2021-95A, Cl SUB | ||||||||||||

19.650%, 08/20/34(A)(C) | 2,000 | 1,092 | ||||||||||

Eaton Vance CLO Equity, Ser 2020-1A, Cl SUB | ||||||||||||

17.810%, 10/15/34(A)(C) | 5,640 | 3,556 | ||||||||||

Eaton Vance CLO Equity, Ser 2022-1A, Cl SUB | ||||||||||||

22.850%, 04/22/33(A)(C) | 2,000 | 993 | ||||||||||

Eaton Vance CLO Equity, Ser 2024-21A, Cl SUB | ||||||||||||

14.340%, 04/18/37(A)(C) | 10,750 | 9,309 | ||||||||||

Elmwood IX CLO Equity, Ser 2021-2A, Cl SUB | ||||||||||||

13.210%, 07/20/34(A)(C) | 9,650 | 7,408 | ||||||||||

Flatiron CLO 18 Equity, Ser 2018-1A, Cl SUB | ||||||||||||

12.790%, 04/17/31(A)(C) | 750 | 367 | ||||||||||

Flatiron CLO 23 CLO Equity, Ser 2023-1A, Cl SUB | ||||||||||||

9.390%, 04/17/36(A)(C) | 1,100 | 960 | ||||||||||

Flatiron RR CLO 22 Equity, Ser 2021-2A, Cl SUB | ||||||||||||

15.690%, 10/15/34(A)(C) | 8,750 | 6,712 | ||||||||||

Flatiron Warehouse CLO 25 Equity, Ser 02/24/2022 | ||||||||||||

0.000%, 11/23/25(A)(D)(F) | 2,579 | 3,317 | ||||||||||

Flatiron Warehouse CLO 25 Equity, Ser 03/05/2024 | ||||||||||||

0.000%, 11/23/25(A)(D)(F) | 1,600 | 1,655 | ||||||||||

Flatiron Warehouse CLO 25 Equity, Ser 04/18/2024 | ||||||||||||

0.000%, 11/23/25(A)(D)(F) | 1,600 | 1,627 | ||||||||||

Flatiron Warehouse CLO 25 Equity, Ser 07/13/2022 | ||||||||||||

0.000%, 11/23/25(A)(D)(F) | 2,450 | 3,061 | ||||||||||

Flatiron Warehouse CLO 25 Equity, Ser 12/13/2021 | ||||||||||||

0.000%, 11/23/25(A)(D)(F) | 2,450 | 3,178 | ||||||||||

Greenwood Park CLO Equity, Ser 2018-1A, Cl SUB | ||||||||||||

26.290%, 04/15/31(A)(C) | 12,075 | 2,777 | ||||||||||

Grippen Park CLO Equity, Ser 2017-1A, Cl SUB | ||||||||||||

8.150%, 01/20/30(A)(C) | 500 | 105 | ||||||||||

LCM XV CLO, Ser 2014-15, Cl ER | ||||||||||||

12.086%, TSFR3M + 6.762%, 07/20/30(B)(C) | 4,250 | 3,876 | ||||||||||

LCM XXII CLO, Ser 2018-22A, Cl DR | ||||||||||||

11.086%, TSFR3M + 5.762%, 10/20/28(B)(C) | 1,250 | 1,115 | ||||||||||

LCM XXIII CLO, Ser 2016-23A, Cl D | ||||||||||||

12.636%, TSFR3M + 7.312%, 10/20/29(B)(C) | 500 | 388 | ||||||||||

LCM XXV CLO, Ser 2017-25A, Cl E | ||||||||||||

11.986%, TSFR3M + 6.662%, 07/20/30(B)(C) | 750 | 562 | ||||||||||

Magnetite XL CLO, Ser 2024-40A, Cl F | ||||||||||||

11.843%, TSFR3M + 6.500%, 07/15/37(B)(C) | 500 | 452 | ||||||||||

Magnetite XL CLO Equity, Ser 2024-40A, Cl SUB | ||||||||||||

12.500%, 07/15/37(A)(C) | 20,136 | 17,551 | ||||||||||

Magnetite XVI CLO Equity, Ser 2015-16A, Cl SUB | ||||||||||||

0.000%, 01/18/28(A)(C)(E)(F) | 750 | 25 | ||||||||||

Midocean Credit CLO IX, Ser 2018-9A, Cl INC | ||||||||||||

57.830%, 07/20/31(A)(C) | 750 | 71 | ||||||||||

Morgan Stanley Eaton Vance CLO Equity, Ser 2021-1A, Cl SUB | ||||||||||||

19.520%, 10/23/34(A)(C) | 12,000 | 6,944 | ||||||||||

Morgan Stanley Eaton Vance CLO Equity, Ser 2022-16A, Cl SUB | ||||||||||||

17.420%, 04/15/35(A)(C) | 8,750 | 6,219 | ||||||||||

Neuberger Berman CLO Equity, Ser 2021-42A, Cl SUB | ||||||||||||

16.860%, 07/16/35(A) | 2,000 | 1,366 | ||||||||||

Neuberger Berman Loan Advisers CLO 26 Equity, Ser 2017-26A, Cl INC | ||||||||||||

21.240%, 10/18/30(A)(C) | 800 | 288 | ||||||||||

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 6

schedule of investments |

May 31, 2024 |

City National Rochdale Strategic Credit Fund (continued) |

Description | Face Amount (000) | Value (000) | ||||||||||

Neuberger Berman Loan Advisers CLO 27 Equity, Ser 2018-27A, Cl INC | ||||||||||||

14.870%, 01/15/30(A)(C) | $ | 500 | $ | 170 | ||||||||

Neuberger Berman Loan Advisers CLO 40 Equity, Ser 2021-40A, Cl SUB | ||||||||||||

17.420%, 04/16/33(A)(C) | 500 | 266 | ||||||||||

Neuberger Berman Loan Advisers CLO 46 Equity, Ser 2021-46A, Cl SUB | ||||||||||||

15.580%, 01/20/36(A)(C) | 9,250 | 6,139 | ||||||||||

Octagon 55 CLO Equity, Ser 2021-1A, Cl SUB | ||||||||||||

20.100%, 07/20/34(A)(C) | 1,250 | 673 | ||||||||||

Octagon Investment Partners 26 CLO, Ser 2016-1A, Cl ER | ||||||||||||

10.990%, TSFR3M + 5.662%, 07/15/30(B)(C) | 3,125 | 2,931 | ||||||||||

Octagon Investment Partners 31 CLO, Ser 2017-1A, Cl F | ||||||||||||

13.786%, TSFR3M + 8.462%, 07/20/30(B)(C) | 700 | 643 | ||||||||||

Octagon Investment Partners CLO, Ser 2018-18A, Cl D | ||||||||||||

11.099%, TSFR3M + 5.772%, 04/16/31(B)(C) | 1,200 | 1,138 | ||||||||||

Octagon Investment Partners CLO 30 Equity, Ser 2017-1A, Cl SUB | ||||||||||||

36.090%, 03/17/30(A)(C) | 3,000 | 358 | ||||||||||

Octagon Investment Partners CLO 47 Equity, Ser 2020-1A, Cl SUB | ||||||||||||

20.240%, 07/20/34(A)(C) | 2,000 | 978 | ||||||||||

Octagon Investment Partners CLO Equity, Ser 2018-1A, Cl SUB | ||||||||||||

45.870%, 01/20/31(A)(C) | 2,250 | 294 | ||||||||||

Octagon Investment Partners XVII CLO, Ser 2013-1A, Cl ER2 | ||||||||||||

10.735%, TSFR3M + 5.412%, 01/25/31(B)(C) | 1,081 | 1,004 | ||||||||||

Octagon Investment Partners XXII CLO, Ser 2014-1A, Cl ERR | ||||||||||||

11.036%, TSFR3M + 5.712%, 01/22/30(B)(C) | 2,500 | 2,419 | ||||||||||

Race Point VIII CLO, Ser 2013-8A, Cl ER | ||||||||||||

12.437%, TSFR3M + 7.112%, 02/20/30(B)(C) | 5,000 | 4,676 | ||||||||||

Regatta XI Funding CLO Equity, Ser 2018-1A, Cl SUB | ||||||||||||

13.350%, 07/17/31(A)(C) | 500 | 165 | ||||||||||

Rockford Tower CLO Equity, Ser 2018-1A, Cl SUB | ||||||||||||

26.640%, 05/20/31(A)(C) | 2,500 | 625 | ||||||||||

Rockford Tower CLO Equity, Ser 2021-1A, Cl SUB | ||||||||||||

17.020%, 07/20/34(A)(C) | 4,100 | 2,624 | ||||||||||

Rockford Tower CLO Equity, Ser 2021-2A, Cl SUB | ||||||||||||

20.320%, 07/20/34(A)(C) | 4,750 | 2,983 | ||||||||||

RR 3 CLO, Ser 2018-3A, Cl DR2 | ||||||||||||

10.990%, TSFR3M + 5.662%, 01/15/30(B)(C) | 1,546 | 1,527 | ||||||||||

RR 3 CLO Equity, Ser 2018-3A, Cl PREF | ||||||||||||

31.270%, 01/15/30(A) | 3,750 | 561 | ||||||||||

Shackleton CLO, Ser 2013-3A, Cl ER | ||||||||||||

11.470%, TSFR3M + 6.142%, 07/15/30(B)(C) | 3,000 | 2,891 | ||||||||||

Shackleton CLO, Ser 2014-5RA, Cl E | ||||||||||||

11.739%, TSFR3M + 6.412%, 05/07/31(B)(C) | 2,100 | 2,006 | ||||||||||

Shackleton CLO, Ser 2017-11A, Cl E | ||||||||||||

11.884%, TSFR3M + 6.562%, 08/15/30(B)(C) | 3,250 | 2,987 | ||||||||||

Shackleton CLO Equity, Ser 2019-14A, Cl SUB | ||||||||||||

17.750%, 07/20/34(A)(C) | 3,000 | 2,217 | ||||||||||

Sound Point CLO II, Ser 2013-1A, Cl B2R | ||||||||||||

11.086%, TSFR3M + 5.762%, 01/26/31(B)(C) | 599 | 504 | ||||||||||

Sound Point CLO III-R, Ser 2013-2RA, Cl E | ||||||||||||

11.590%, TSFR3M + 6.262%, 04/15/29(B)(C) | 3,800 | 3,355 | ||||||||||

Sound Point CLO IV-R Equity, Ser 2013-3RA, Cl SUB | ||||||||||||

0.000%, 04/18/31(A)(C)(F) | 3,750 | 37 | ||||||||||

SOUND POINT CLO VIII-R, Ser 2019-1RA, Cl E | ||||||||||||

12.190%, TSFR3M + 6.862%, 04/15/30(B)(C) | 1,250 | 809 | ||||||||||

Sound Point CLO XIX, Ser 2018-1A, Cl E | ||||||||||||

11.240%, TSFR3M + 5.912%, 04/15/31(B)(C) | 3,900 | 3,154 | ||||||||||

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 7

schedule of investments |

May 31, 2024 |

City National Rochdale Strategic Credit Fund (continued) |

Description | Face Amount (000) | Value (000) | ||||||||||

Sound Point CLO XIX Equity, Ser 2018-1A, Cl SUB | ||||||||||||

0.000%, 04/15/31(A)(C)(F) | $ | 4,500 | $ | 135 | ||||||||

Sound Point CLO XVI, Ser 2017-2A, Cl E | ||||||||||||

11.685%, TSFR3M + 6.362%, 07/25/30(B)(C) | 2,063 | 1,719 | ||||||||||

Sound Point CLO XVII, Ser 2017-3A, Cl D | ||||||||||||

12.086%, TSFR3M + 6.762%, 10/20/30(B)(C) | 500 | 442 | ||||||||||

Sound Point CLO XVII Equity, Ser 2017-3A, Cl SUB | ||||||||||||

93.760%, 10/20/30(A)(C) | 3,250 | 199 | ||||||||||

Sound Point CLO XVIII, Ser 2017-4A, Cl D | ||||||||||||

11.086%, TSFR3M + 5.762%, 01/21/31(B)(C) | 3,500 | 2,716 | ||||||||||

Sound Point CLO XX, Ser 2018-2A, Cl E | ||||||||||||

11.586%, TSFR3M + 6.262%, 07/26/31(B)(C) | 3,000 | 2,262 | ||||||||||

Sound Point CLO XXI Equity, Ser 2018-3A, Cl SUB | ||||||||||||

57.730%, 10/26/31(A)(C) | 1,000 | 80 | ||||||||||

Sounds Point CLO IV-R, Ser 2013-3RA, Cl E | ||||||||||||

11.839%, TSFR3M + 6.512%, 04/18/31(B)(C) | 1,000 | 581 | ||||||||||

Southwick Park CLO Equity, Ser 2019-4A, Cl SUB | ||||||||||||

18.460%, 07/20/32(A)(C) | 2,000 | 1,214 | ||||||||||

Steele Creek CLO, Ser 2016-1A, Cl ER | ||||||||||||

11.341%, TSFR3M + 6.012%, 06/15/31(B)(C) | 1,500 | 1,223 | ||||||||||

Steele Creek CLO, Ser 2017-1A, Cl E | ||||||||||||

11.790%, TSFR3M + 6.462%, 10/15/30(B)(C) | 1,900 | 1,642 | ||||||||||

Steele Creek CLO, Ser 2018-1A, Cl E | ||||||||||||

11.340%, TSFR3M + 6.012%, 04/15/31(B)(C) | 4,000 | 3,263 | ||||||||||

Steele Creek CLO Equity, Ser 2014-1RA, Cl SUB | ||||||||||||

27.510%, 04/21/31(A)(C) | 21,168 | 187 | ||||||||||

Steele Creek CLO Equity, Ser 2017-1A, Cl SUB | ||||||||||||

0.000%, 10/15/30(A)(C)(F) | 2,500 | 125 | ||||||||||

Steele Creek CLO Equity, Ser 2018-2A, Cl SUB | ||||||||||||

35.160%, 08/18/31(A)(C) | 2,500 | 309 | ||||||||||

Symphony CLO XXVI Equity, Ser 2021-26A, Cl SUB | ||||||||||||

31.730%, 04/20/33(A)(C) | 6,500 | 1,773 | ||||||||||

Tallman Park CLO Equity, Ser 2021-1A, Cl SUB | ||||||||||||

14.760%, 04/20/34(A)(C) | 12,765 | 8,491 | ||||||||||

TCW CLO Equity, Ser 2021-1A, Cl SUB | ||||||||||||

19.890%, 03/18/34(A)(C) | 9,350 | 5,279 | ||||||||||

THL Credit Wind River CLO, Ser 2018-1A, Cl E | ||||||||||||

11.090%, TSFR3M + 5.762%, 07/15/30(B)(C) | 2,500 | 2,420 | ||||||||||

Upland CLO Equity, Ser 2016-1A, Cl SUB | ||||||||||||

23.520%, 04/20/31(A) | 2,500 | 796 | ||||||||||

Voya CLO, Ser 2015-1A, Cl DR | ||||||||||||

11.239%, TSFR3M + 5.912%, 01/18/29(B)(C) | 750 | 745 | ||||||||||

Voya CLO, Ser 2017-1A, Cl D | ||||||||||||

11.679%, TSFR3M + 6.362%, 04/17/30(B)(C) | 1,500 | 1,440 | ||||||||||

Voya CLO, Ser 2018-2A, Cl E | ||||||||||||

10.840%, TSFR3M + 5.512%, 07/15/31(B)(C) | 1,625 | 1,527 | ||||||||||

Wehle Park CLO Equity, Ser 2014-1RA, Cl SUB | ||||||||||||

13.680%, 04/21/35(A) | 17,250 | 13,110 | ||||||||||

Wellfleet CLO, Ser 2015-1A, Cl ER3 | ||||||||||||

12.636%, TSFR3M + 7.312%, 07/20/29(B)(C) | 1,000 | 643 | ||||||||||

Wellfleet CLO, Ser 2017-1A, Cl D | ||||||||||||

13.786%, TSFR3M + 6.312%, 04/20/29(B)(C) | 2,550 | 2,445 | ||||||||||

Wellfleet CLO, Ser 2017-2A, Cl D | ||||||||||||

12.336%, TSFR3M + 7.012%, 10/20/29(B)(C) | 3,150 | 3,033 | ||||||||||

Wellfleet CLO, Ser 2017-3A, Cl D | ||||||||||||

11.129%, TSFR3M + 5.812%, 01/17/31(B)(C) | 750 | 688 | ||||||||||

Wellfleet CLO, Ser 2018-2A, Cl D | ||||||||||||

11.656%, TSFR3M + 6.332%, 10/20/31(B)(C) | 750 | 726 | ||||||||||

Wellfleet CLO Equity, Ser 2020-2A, Cl SUB | ||||||||||||

19.600%, 07/15/34(A) | 5,000 | 2,228 | ||||||||||

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 8

schedule of investments |

May 31, 2024 |

City National Rochdale Strategic Credit Fund (concluded) |

Description | Face Amount (000) | Value (000) | ||||||||||

York CLO 2 Equity, Ser 2015-1A, Cl SUB | ||||||||||||

11.920%, 01/22/31(A)(C) | $ | 750 | $ | 355 | ||||||||

Total Asset-Backed Securities | ||||||||||||

(Cost $331,627) | 257,472 | |||||||||||

Shares | ||||||||||||

Short-Term Investment [8.7%] | ||||||||||||

SEI Daily Income Trust Government Fund, Cl Institutional, 5.170%** | 23,224,728 | 23,225 | ||||||||||

Total Short-Term Investment | ||||||||||||

(Cost $23,225) | 23,225 | |||||||||||

Total Investments [105.4%] | ||||||||||||

(Cost $354,852) | $ | 280,697 | ||||||||||

Percentages are based on net assets of $266,361 (000).

** | The rate reported is the 7-day effective yield as of May 31, 2024. |

(A) | Level 3 security in accordance with fair value hierarchy. The rate reported is the effective yield as of May 31, 2024. |

(B) | Variable or floating rate security. The rate shown is the effective interest rate as of period end. The rates for certain securities are not based on published reference rates and spreads and are either determined by the issuer or agent based on current market conditions; by using a formula based on the rates of underlying loans; or by adjusting periodically based on prevailing interest rates. |

(C) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration normally to qualified institutions. On May 31, 2024, the value of these securities amounted to $211,503 (000), representing 79.4% of the net assets of the Fund. |

(D) | This is a CLO warehouse position, which is a loan accumulation vehicle. Loan accumulation vehicles are financing structures intended to aggregate loans that may be used to form the basis of a CLO. Total as of May 31, 2024 was $12,838,241. |

(E) | As of May 31, 2024, the investment has been called. Expected value of residual distributions, once received, is anticipated to be recognized as return of capital, pending any amortized cost, and/or, realized gain for any amounts received in excess of such amortized cost. |

(F) | Interest rate or effective yield not available. |

Cl — Class

CLO — Collateralized Loan Obligation

Ser — Series

TSFR3M — 3 Month Term Secured Overnight Financing Rate

The following is a list of the inputs used as of May 31, 2024, in valuing the Fund’s investments carried at value (000):

Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Asset-Backed Securities | $ | — | $ | 74,588 | $ | 182,884 | $ | 257,472 | ||||||||

Short-Term Investment | 23,225 | — | — | 23,225 | ||||||||||||

Total Investments in Securities | $ | 23,225 | $ | 74,588 | $ | 182,884 | $ | 280,697 | ||||||||

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value as of May 31, 2024 (000):

Asset-Backed | ||||

Beginning balance as of June 1, 2023 | $ | 138,961 | ||

Transfers into Level 3 | — | |||

Transfers out of Level 3 | — | |||

Amort | — | |||

Purchases | 64,991 | |||

Sales | (10,059 | ) | ||

Realized gain (loss) | (4,646 | ) | ||

Change in unrealized appreciation (depreciation) | (6,363 | ) | ||

Ending balance as of May 31, 2024 | $ | 182,884 | ||

Net change in unrealized appreciation (depreciation) attributable to Level 3 securities held at May 31, 2024 | $ | (6,363 | ) | |

For the year ended May 31, 2024, there were no transfers in or out of Level 3. See Note 2 in the Notes to Financial Statements.

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 9

statement of assets and liabilities (000) |

May 31, 2024 |

|

| |||

ASSETS: | ||||

Cost of securities | $ | 354,852 | ||

Investments in securities, at fair value | $ | 280,697 | ||

Interest receivable | 2,093 | |||

Receivable for investments sold | 3,951 | |||

Receivable for capital shares issued | 21 | |||

Prepaid expenses | 15 | |||

Total Assets | 286,777 | |||

LIABILITIES: | ||||

Payable for investments purchased | 19,881 | |||

Payable for transfer agent fees | 20 | |||

Investment advisory fees payable | 307 | |||

Payable for legal fees | 31 | |||

Shareholder servicing fees payable | 55 | |||

Payable for pricing fees | 56 | |||

Administration fees payable | 17 | |||

Accrued expenses | 49 | |||

Total Liabilities | 20,416 | |||

Commitment and Contingencies(†) | ||||

Net Assets | $ | 266,361 | ||

NET ASSETS: | ||||

Paid-in capital | $ | 326,958 | ||

Total accumulated losses | (60,597 | ) | ||

Net Assets | $ | 266,361 | ||

Net Assets | $ | 266,361,096 | ||

Total shares outstanding at end of year | 34,718,546 | |||

Net asset value, offering and redemption price per share | ||||

(net assets ÷ shares outstanding) | $ | 7.67 | ||

† | See Note 2 in the Notes to Financial Statements. |

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 10

statement of operations (000) |

For the year ended May 31, 2024 |

|

| |||

INVESTMENT INCOME: | ||||

Interest | $ | 61,196 | ||

Dividends | 683 | |||

Total Investment Income | 61,879 | |||

EXPENSES: | ||||

Investment advisory fees(1) | 3,657 | |||

Shareholder servicing fees | 610 | |||

Administration fees | 195 | |||

Trustees’ fees | 5 | |||

Professional fees | 187 | |||

Transfer agent fees | 61 | |||

Registration fees | 41 | |||

Printing fees | 26 | |||

Custody fees | 28 | |||

Interest expense | 9 | |||

Insurance and other expenses | 236 | |||

Total Expenses | 5,055 | |||

Less, waivers and/or reimbursements of: | ||||

Investment advisory fees(1) | (291 | ) | ||

Net Expenses | 4,764 | |||

Net investment income | 57,115 | |||

Net realized gain (loss) from securities transactions | (357 | ) | ||

Net change in unrealized appreciation (depreciation) on investments | 5,898 | |||

Net increase in net assets resulting from operations | $ | 62,656 | ||

(1) | See Note 4 in the Notes to Financial Statements. |

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 11

statements of changes in net assets (000) |

For the years ended May 31, |

|

|

| ||||||

| 06/01/23 to | 06/01/22 to | ||||||

OPERATIONS: | ||||||||

Net investment income | $ | 57,115 | $ | 39,804 | ||||

Net realized gain (loss) from security transactions | (357 | ) | 706 | |||||

Net change in unrealized appreciation (depreciation) on investments | 5,898 | (41,619 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 62,656 | (1,109 | ) | |||||

DISTRIBUTIONS: | (54,600 | ) | (40,693 | ) | ||||

CAPITAL SHARE TRANSACTIONS: | ||||||||

Class 1 | ||||||||

Shares issued | 47,619 | 60,794 | ||||||

Shares reinvested for distributions | 1,890 | 15,288 | ||||||

Shares redeemed | (33,857 | ) | (22,476 | ) | ||||

Net increase in net assets from share transactions | 15,652 | 53,606 | ||||||

Total increase in net assets | 23,708 | 11,804 | ||||||

NET ASSETS: | ||||||||

Beginning of year | 242,653 | 230,849 | ||||||

End of year | $ | 266,361 | $ | 242,653 | ||||

CAPITAL SHARES ISSUED AND REDEEMED: | ||||||||

Class 1 | ||||||||

Shares issued | 6,416 | 7,650 | ||||||

Shares reinvested for distributions | 263 | 1,964 | ||||||

Shares redeemed | (4,473 | ) | (2,827 | ) | ||||

Net share transactions | 2,206 | 6,787 | ||||||

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 12

statement of cash flows (000) |

For the year ended May 31, 2024 |

Cash Flows from Operating Activities: | ||||

Net Increase in Net Asset Resulting from Operations | $ | 62,656 | ||

Adjustments to Reconcile Net Increase in Net Assets Resulting from Operations to Net Cash Provided by Operating Activities: | ||||

Purchases of investments | (232,793 | ) | ||

Proceeds from disposition of investment securities | 200,300 | |||

Amortization of premium/accretion of discount on investments, net | (1,736 | ) | ||

Net realized loss from security transactions | 357 | |||

Net change in unrealized (appreciation) depreciation on investments | (5,898 | ) | ||

Decrease in interest receivable | 159 | |||

Increase in receivable for investments sold | (3,951 | ) | ||

Decrease in prepaid expenses | 3 | |||

Increase in payable for investment advisory fees | 70 | |||

Increase in shareholder servicing fees payable | 4 | |||

Increase in payable for administration fees | 1 | |||

Increase in payable for legal fees | 31 | |||

Increase in payable for pricing fees | 56 | |||

Increase in payable for transfer agent fees | 20 | |||

Decrease in payable for trustee fees | (1 | ) | ||

Increase in payable for investments purchased | 19,881 | |||

Decrease in accrued expenses | (190 | ) | ||

Net Cash Provided by Operating Activities | 38,969 | |||

Cash Flows From Financing Activities | ||||

Cash distributions paid | $ | (52,710 | ) | |

Proceeds from capital shares issued | 47,598 | |||

Cost of capital shares redeemed | (33,857 | ) | ||

Line of credit borrows | 3,641 | |||

Line of credit repayments | (3,641 | ) | ||

Net Cash (Used) in Financing Activities | (38,969 | ) | ||

Net Change in Cash | — | |||

Cash at beginning of year | — | |||

Cash at end of year | $ | — | ||

Supplemental Disclosure of Cash Flow Information | ||||

Non-cash Financing Activities not included herein consist of | ||||

Reinvestments of Distributions | $ | 1,890 | ||

Interest paid | 9 |

Amount designated as “—” is $0.

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 13

financial highlights |

For a Share Outstanding Throughout each Year Presented |

| Net asset | Net | Net | Total from | Total | Net asset | Total | Net assets | Ratio of | Ratio of | Ratio of | Portfolio | ||||||||||||||||||||||||||||||||||||

Class 1 | ||||||||||||||||||||||||||||||||||||||||||||||||

2024 | $ | 7.46 | $ | 1.74 | $ | 0.16 | $ | 1.90 | $ | (1.69 | ) | $ | 7.67 | 29.29 | % | $ | 266,361 | 1.95 | % | 2.08 | % | 23.47 | % | 22 | % | |||||||||||||||||||||||

2023 | 8.97 | 1.36 | (1.42 | ) | (0.06 | ) | (1.45 | ) | 7.46 | (0.35 | ) | 242,653 | 1.95 | 2.12 | 17.21 | 8 | ||||||||||||||||||||||||||||||||

2022 | 10.83 | 1.71 | (1.49 | ) | 0.22 | (2.08 | ) | 8.97 | 1.46 | 230,849 | 1.95 | 2.09 | 16.74 | 49 | ||||||||||||||||||||||||||||||||||

2021 | 8.64 | 0.95 | 2.22 | 3.17 | (0.98 | ) | 10.83 | 38.39 | 163,214 | 1.95 | 2.27 | 9.56 | 62 | |||||||||||||||||||||||||||||||||||

2020 | 10.55 | 0.97 | (2.06 | ) | (1.09 | ) | (0.82 | ) | 8.64 | (10.54 | ) | 86,976 | 1.95 | 2.87 | 9.42 | 62 | ||||||||||||||||||||||||||||||||

† | Per share calculations are based on average shares outstanding throughout each year. |

‡ | Fee waivers are in effect; if they had not been in effect, performance would have been lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

‡‡ | Portfolio turnover rate is for the period indicated and has not been annualized. |

See accompanying notes to financial statements.

City National Rochdale Strategic Credit Fund | PAGE 14

notes to financial statements |

May 31, 2024 |

1. | ORGANIZATION: |

City National Rochdale Strategic Credit Fund (the “Fund”) is a Delaware statutory trust registered as an investment company under the Investment Company Act of 1940, as amended (the “1940 Act”), and was organized on February 26, 2018. The Fund is a continuously offered, non-diversified, closed-end management investment company. The Fund is an interval fund that offers to make quarterly repurchases of shares at net asset value (“NAV”).

The Fund commenced operations on December 19, 2018. The Fund’s investment adviser, City National Rochdale, LLC (the “Adviser”), a wholly-owned subsidiary of City National Bank, is responsible on a day-to-day basis for investment of the Fund’s portfolio in accordance with its investment objectives and principal investment strategies. The Adviser is registered as an investment adviser with the Securities and Exchange Commission (the “SEC”) under the Investment Advisers Act of 1940, as amended.

The Fund’s primary objective is to generate current income; its secondary objective is long-term capital appreciation.

There can be no assurance that the Fund will achieve its objectives. The Fund pursues its investment objectives by investing in a portfolio of debt securities and other credit-related investments including equity tranches of collateralized loan obligations (“CLOs”), equity interests in CLO warehouses, funds that invest primarily in debt securities, and derivatives that have similar economic characteristics to debt securities.

2. | SIGNIFICANT ACCOUNTING POLICIES: |

The following is a summary of significant accounting policies followed by the Fund.

Use of Estimates – The Fund is an investment company that conforms with accounting principles generally accepted in the United States of America (“GAAP”). Therefore the Fund follows the accounting and reporting guidance for investment companies. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security Valuation – Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ) are valued at the last quoted sale price on the primary exchange or market (foreign or domestic) on which they are traded, or, if there is no such reported sale, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price is used. If available, debt securities are priced based upon valuations provided by independent, third-party pricing agents. Such values generally reflect the last reported sales price if the security is actively traded. The third-party pricing agents may also value debt securities at an evaluated bid price by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Debt obligations with remaining maturities of 60 days or less may be valued at their amortized cost, if the Adviser’s Fair Value Committee (the “Committee”) concludes that such amortized cost approximates market value after taking into account factors such as credit, liquidity and interest rate conditions as well as issuer specific factors. Investments in underlying registered investment companies are valued at their respective daily net assets in accordance with pricing procedures approved by their respective boards. The prices for foreign securities are reported in local currency and converted to U.S. Dollars using currency exchange rates. Prices for most securities held by the Fund are provided daily by recognized independent pricing agents. If a security price cannot be obtained from an independent, third-party pricing agent, the Fund seeks to obtain a bid price from one or more independent brokers.

Securities for which market prices are not “readily available” are valued in accordance with the fair value procedures (the “Fair Value Procedures”) approved by the Fund’s Board of Trustees (the “Board”). The Fund’s Fair Value Procedures are implemented through the Committee designated by the Adviser. Some of the more common reasons that may necessitate that a security be valued using the Fair Value Procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily closed at a time when, under normal conditions, it would be open; for international securities, market events that occur after the close of the foreign markets that make closing prices not representative of fair value; or the security’s primary pricing source is not able or willing to provide a price. When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee. As of May 31, 2024, there were no securities valued in accordance with the Fair Value Procedures.

In accordance with GAAP, the objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability, in an orderly transaction between market participants at the measurement date (an exit price). The fair value hierarchy gives the highest

City National Rochdale Strategic Credit Fund | PAGE 15

notes to financial statements |

May 31, 2024 |

priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The three levels of the fair value hierarchy are described below:

● | Level 1 — Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

● | Level 2 — Quoted prices in inactive markets, or inputs that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

● | Level 3 — Prices, inputs or exotic modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity). |

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3, the fair value measurement of which considers several inputs, may include Level 1 or Level 2 inputs as components of the overall fair value measurement. Transfers in and out of the levels are recognized at the value at the end of the period.

The Fund categorizes some of its investments as Level 3. Additionally, an active market does not exist for the Fund’s Level 3 investments as of May 31, 2024. There were no unobservable inputs that have been internally developed in determining the fair value of the Fund’s investments as of May 31, 2024.

Security Transactions and Related Income – Security transactions are accounted for on the trade date of the security purchase or sale. Costs used in determining the net realized capital gains or losses on the sale of securities are those of the specific securities sold. Interest income is recognized on an accrual basis and dividend income is recognized on the ex-dividend date. Purchase discounts and premiums on securities held by the Fund are accreted and amortized to maturity using the scientific method, which is not materially different from the effective interest method, and approximates the effective interest method over the holding period of a security.

Collateralized Debt Obligations – To the extent consistent with its investment objectives and strategies, the Fund may invest in collateralized debt obligations (“CDOs”), which include CLOs and other similarly structured securities. CLOs are a type of asset-backed security. A CLO is a trust typically collateralized by a pool of loans, which may include, among others, domestic and foreign senior secured loans, senior secured corporate bonds, unsecured corporate bonds, senior unsecured loans, and subordinate corporate loans, including loans that may be rated below investment grade or equivalent unrated loans. CDOs may charge management fees and administrative expenses.

Warehouse Investments — Prior to a CLO closing and issuing CLO securities to CLO investors, in anticipation of such CLO closing, a vehicle (often the future CLO issuer) will purchase and “warehouse” a portion of the underlying loans (and, in the case of European CLOs, bonds) that will be held by such CLO (the “Warehouse”). To finance the accumulation of these assets, a financing facility (a “Warehouse Facility”) is opened, equitized either by the entity or affiliates of the entity that will become the collateral manager of the CLO upon its closing and/or by third-party investors that may or may not invest in the CLO. The period from the date such Warehouse is opened and asset accumulation begins to the date the CLO closes is referred to as the “warehousing period.” The Fund may participate in SSOs during warehousing periods by providing equity capital in support of Warehouses. In practice, a Warehouse investment (“Warehouse Investment”) may be structured in a variety of legal forms (typically determined by the bank engaged to underwrite the associated CLO which will also typically be the provider of senior financing to the Warehouse), including by subscribing for equity interests or a subordinated debt investment in a special purpose vehicle that obtains a Warehouse Facility secured by the assets (primarily SSOs) that are accumulated in anticipation of the related CLO.

Below is a summary of the Fund’s capital commitments, capital funded and capital unfunded details for the following warehouse investments as of May 31, 2024:

Investments | Capital | Capital | Capital | Capital | Capital | |||||||||||||||

Flatiron CLO 25 WH | $ | 12,279 | $ | 10,679 | $ | 1,600 | 87.0 | % | 13.0 | % | ||||||||||

Commitments and Contingencies – In the normal course of business, the Fund enters into contracts that provide general indemnifications by the Fund to the counterparty to the contract. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote. The Fund has determined that none of these arrangements requires disclosure on the Fund’s balance sheet.

Dividends and Distributions to Shareholders – Distributions from net realized capital gains are distributed to shareholders at least annually.

City National Rochdale Strategic Credit Fund | PAGE 16

Income Taxes – The Fund intends to continue to qualify as a “regulated investment company” under Sub-chapter M of the Internal Revenue Code of 1986, as amended. If so qualified, the Fund will not be subject to federal income tax to the extent it distributes substantially all of its net investment income and net capital gains to its shareholders. Accordingly, no provisions for U.S. Federal income taxes would be required.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current period.

The Fund recognizes accrued interest and penalties associated with uncertain tax positions. Management has determined that there are no uncertain tax positions for the current tax year. Therefore, there was no income tax related interest and penalties recorded for the year ended May 31, 2024.

3. | ADMINISTRATION, TRANSFER AGENT, DISTRIBUTION AND SHAREHOLDER SERVICES AGREEMENTS: |

Pursuant to an Administration Agreement dated May 16, 2018, as amended (the “Agreement”), SEI Investments Global Funds Services (the “Administrator”), a wholly owned subsidiary of SEI Investments Company, acts as the Fund’s administrator. Under the terms of the Agreement, the Administrator is entitled to receive an annual fee based on the average daily net assets of the Fund, subject to a minimum annual fee.

U.S. Bank Global Fund Services (the “Transfer Agent”) serves as the Fund’s Transfer Agent, pursuant to a transfer agency agreement.

The Fund is subject to a shareholder service agreement that permits compensation to the Adviser and subjects the Fund to a fee of 0.25% of its average net assets for shareholder services provided to shareholders of the Fund. Because this fee is paid out of the Fund’s assets, over time the fee will increase the cost of a shareholder’s investment. For the year ended May 31, 2024, the Fund incurred $609,510 in shareholder servicing fees.

4. | INVESTMENT ADVISORY FEES AND OTHER AGREEMENTS: |

Under the terms of the advisory agreement between the Fund and the Adviser (the “Advisory Agreement”), the Fund pays the Adviser, as promptly as possible after the last day of each month, a fee for its investment advisory services in the amount of 1.50% of the Fund’s average daily net assets. Pursuant to the investment sub-advisory agreement by and between the Adviser and CIFC Investment Management LLC (the “Sub-Adviser” or “CIFC”) (the “Sub-Advisory Agreement”), the Adviser pays the Sub-Adviser out of the advisory fee it receives from the Fund a fee in the amount of 1.25% of the Fund’s average daily net assets.

The Adviser has contractually agreed to waive its management fee and/or reimburse expenses to the extent necessary to ensure that the Fund’s total annual operating expenses will not exceed 1.95% (after fee waivers and/or expense reimbursements, and exclusive of front-end or contingent deferred loads, taxes, interest, brokerage commissions, acquired fund fees or expenses, extraordinary expenses such as litigation expenses, and other expenses not incurred in the ordinary course of the Fund’s business). These arrangements will continue until October 1, 2024, and shall automatically renew for an additional one-year period unless sooner terminated by the Fund or by the Board upon 60 days’ written notice to the Adviser or termination of the advisory agreement between the Fund and the Adviser. The Adviser may recoup fees waived and expenses reimbursed for a period of three years following the date such reimbursement or reduction was made if such recoupment does not cause current expenses to exceed the expense limit for the Fund in effect at the time the expenses were paid/waived or any expense limit in effect at the time of recoupment. For the year ended May 31, 2024, the Adviser earned investment advisory fees of $3,656,909. For this same period, the Adviser waived its investment advisory fee for operating expenses in the amount of $290,643. As of May 31, 2024, the fees which were previously waived by the Adviser which may be subject to possible future reimbursement, were as follows:

Expiring | Expiring | Expiring | Total | ||||||||||||

| $ | 290,615 | $ | 395,768 | $ | 290,643 | $ | 977,026 | ||||||||

During the year ended May 31, 2024, the Fund did not recapture any previously waived fees and/or reimbursed expenses.

5. | INVESTMENT TRANSACTIONS: |

The cost of security purchases and proceeds from the sale and maturities of securities, other than temporary investments in short-term securities for the year ended May 31, 2024, were as follows:

Purchases | Sales and | ||||||

Other | Other | ||||||

| $ | 68,794 | $ | 45,196 | ||||

City National Rochdale Strategic Credit Fund | PAGE 17

notes to financial statements |

May 31, 2024 |

6. | SHARE CAPITAL: |

The Fund was initially capitalized on October 24, 2018, through the sale of 10,000 common shares for $100,000 ($10.00 per share).

The Fund is open to investors and generally accepts orders to purchase shares on a monthly basis. However, the Fund’s ability to accept orders to purchase shares may be limited, including during periods when, in the judgment of the Adviser, appropriate investments for the Fund are not available. All initial investments in the Fund by or through the Adviser, its advisory partners and its advisory affiliates will be subject to a $1,000,000 minimum per registered investment adviser or intermediary.

As an interval fund, the Fund makes periodic offers to repurchase a portion of its outstanding shares at NAV per share. The Fund has adopted a fundamental policy, which cannot be changed without shareholder approval, to make repurchase offers once every three months. The Fund’s repurchase offers were as follows:

Repurchase Date | Maximum | % of Shares | Number | |||||||||

March 22, 2024 | 8 | % | 2.43 | % | 809 | |||||||

December 15, 2023 | 8 | 4.86 | 1,618 | |||||||||

September 22, 2023 | 8 | 2.86 | 947 | |||||||||

June 23, 2023 | 8 | 3.38 | 1,099 | |||||||||

Repurchase Date | NAV Price | Redemption | Shares | |||||||||

March 22, 2024 | $ | 7.54 | $ | 6,099 | 33,272 | |||||||

December 15, 2023 | 7.51 | 12,151 | 33,277 | |||||||||

September 22, 2023 | 7.75 | 7,342 | 33,152 | |||||||||

June 23, 2023 | 7.52 | 8,265 | 32,513 | |||||||||

For each repurchase offer, the Fund will offer to repurchase at least 5% of its total outstanding shares, unless the Fund’s Board of Trustees has approved a higher amount (but not more than 25% of total outstanding shares) for a particular repurchase offer. The Adviser currently expects under normal market circumstances to recommend that, at each repurchase offer, the Fund will offer to repurchase 8% of its total outstanding shares, subject to approval of the Board of Trustees. There is no guarantee that the Fund will offer to repurchase more than 8% of its total outstanding shares (including all classes of shares) in any repurchase offer, and there is no guarantee that shareholders will be able to sell shares in an amount or at the time the investor desires.

7. | FEDERAL TAX INFORMATION: |

The timing and characterization of certain income and capital gains distributions are determined annually in accordance with Federal tax regulations, which may differ from U.S. GAAP. These book/tax differences are either temporary or permanent in nature. To the extent these differences are permanent, they are charged or credited to paid-in capital, and undistributed earnings, in the period that the differences arise. Permanent differences are primarily attributable to investments in passive foreign investment companies (“PFICs”). None of these permanent differences necessitate a charge to the paid in capital account.

The tax character of dividends and distributions declared during the years ended May 31, were as follows:

| Ordinary | Long-Term | Total | |||||||||

May 31, 2024 | $ | 54,600 | $ | — | $ | 54,600 | ||||||

May 31, 2023 | 40,693 | — | 40,693 | |||||||||

As of May 31, 2024, the components of accumulated losses on a tax basis were as follows (000):

Undistributed ordinary income | $ | 17,132 | ||

Capital loss carryforwards | (1,163 | ) | ||

Other Temporary Differences | (1 | ) | ||

Unrealized appreciation (depreciation) | (76,565 | ) | ||

Total distributable earnings | $ | (60,597 | ) |

During the year ended May 31, 2024, the Fund had $1,163 long-term capital loss carryforwards available to offset capital gains.

For Federal income tax purposes, the cost of investments owned at May 31, 2024, and the net realized gains or losses on investments sold for the period were different from amounts reported for financial reporting purposes. These differences are primarily due to investments in PFICs. The aggregate gross unrealized appreciation on investments, the aggregate gross unrealized depreciation on investments and the net unrealized appreciation (depreciation) for tax purposes as of May 31, 2024, for the Fund were as follows:

Federal Tax | Aggregate | Aggregate | Net | ||||||||||||

| $ | 357,262 | $ | 9,201 | $ | (85,766 | ) | $ | (76,565 | ) | ||||||

City National Rochdale Strategic Credit Fund | PAGE 18

Management has analyzed the Fund’s tax positions taken on Federal income tax returns for all open tax years and has concluded that as of May 31, 2024 no provision for income tax would be required in the Fund’s financial statements. The Fund’s Federal and state income and Federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

8. | CONCENTRATION OF RISK: |

As with all investment companies, a shareholder of the Fund is subject to the risk that his or her investment could lose money. Many factors affect the Fund’s performance. The Fund is subject to the principal risks disclosed in the Fund’s prospectus among other risks, any of which may adversely affect the Fund’s net asset value and ability to meet its investment objectives. Certain principal risks of investing in the Fund are noted below. A more complete description of risks is included in the Fund’s prospectus and statement of additional information.

General – The Fund is a non-diversified, closed-end management investment company designed primarily as a long-term investment and not as a trading tool. The Fund is not a complete investment program and should be considered only as an addition to an investor’s existing portfolio of investments. Due to uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective. In addition, even though the Fund makes periodic offers to repurchase a portion of its outstanding shares to provide some liquidity to shareholders, shareholders should consider the Fund to be an illiquid investment.

Non-diversification risk – The Fund is classified as “non-diversified,” which means that it can invest a higher percentage of its assets in the securities of any one or more issuers than a diversified fund. Being non-diversified may magnify the Fund’s losses from adverse events affecting a particular issuer, and the value of its shares may be more volatile than if it invested more widely.

Debt securities risks – The value of debt securities may go up or down, sometimes rapidly and unpredictably, due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the bond markets or adverse investor sentiment. In addition, the value of a debt security may decline if the issuer or other obligor of the security fails to pay principal and/or interest, otherwise defaults or has its credit rating downgraded or is perceived to be less creditworthy, or the credit quality or value of any underlying assets declines. If the value of debt securities owned by the Fund fall, the value of your investment will go down. Below investment grade, high-yield debt securities (commonly known as “junk bonds”) have a higher risk of default and are considered speculative. Subordinated securities are more likely to suffer a credit loss than non-subordinated securities of the same issuer and will be disproportionately affected by a default, downgrade or perceived decline in creditworthiness. The Fund has a broad mandate with respect to the type and nature of debt investments in which it may participate.

The Fund has a broad mandate with respect to the type and nature of debt investments in which it may participate. While some of the debt securities in which the Fund will invest may be secured, the Fund also may invest in debt securities that are either unsecured and subordinated to substantial amounts of senior indebtedness, or a significant portion of which may be unsecured. In such instances, the ability of the Fund to influence an issuer’s affairs, especially during periods of financial distress or following an insolvency is likely to be substantially less than that of senior creditors. For example, under terms of subordination agreements, senior creditors are typically able to block the acceleration of the debt or other exercises by the Fund of its rights as a creditor. Accordingly, the Fund may not be able to take the steps necessary to protect its investments in a timely manner or at all. In addition, the debt securities in which the Fund will invest may not be protected by financial covenants or limitations upon additional indebtedness, may have limited liquidity and may not be rated by a credit rating agency.

Creditors of loans constituting the Fund’s assets may seek the protections afforded by bankruptcy, insolvency and other debtor relief laws. Bankruptcy proceedings are unpredictable. Additionally, the numerous risks inherent in the insolvency process create a potential risk of loss by the Fund of its entire investment in any particular investment. Insolvency laws may, in certain jurisdictions, result in a restructuring of the debt without the Fund’s consent under the “cramdown” provisions of applicable insolvency laws and may also result in a discharge of all or part of the debt without payment to the Fund.

Debt securities are also subject to other risks, including (i) the possible invalidation of an investment transaction as a “fraudulent conveyance,” (ii) the recovery of liens perfected or payments made on account of a debt in the period before an insolvency filing as a “preference,” (iii) equitable subordination claims by other creditors, (iv) so called “lender liability” claims by the issuer of the obligations, and (v) environmental liabilities that may arise with respect to collateral securing the obligations. Additionally, adverse credit events with respect to any issuer, such as missed or delayed payment of interest and/or principal, bankruptcy, receivership, or distressed exchange, can significantly diminish the value of the Fund’s investment in any such company. The Fund’s investments in debt securities may be subject to early redemption features, refinancing options, pre-

City National Rochdale Strategic Credit Fund | PAGE 19

notes to financial statements |

May 31, 2024 |

payment options or similar provisions which, in each case, could result in the issuer repaying the principal on an obligation held by the Fund earlier than expected. Accordingly, there can be no assurance that the Fund’s investment objective will be realized.

Interest rate risk – The market prices of securities may fluctuate significantly when interest rates change. When interest rates rise, the value of debt (i.e., fixed income) securities generally falls. Recently, the U.S. Federal Reserve has been raising interest rates from historically low levels. It may continue to raise interest rates. Any additional interest rate increases in the future could cause the value of the Fund’s holdings to decrease. A general rise in interest rates may cause investors to move out of debt securities on a large scale, which could adversely affect the price and liquidity of debt securities. A change in interest rates will not have the same impact on all debt securities. Generally, the longer the maturity (i.e., measure of time remaining until the final payment on a security) or duration (i.e., measure of the underlying portfolio’s price sensitivity to changes in prevailing interest rates) of a debt security, the greater the impact of a rise in interest rates on the security’s value. For example, if interest rates increase by 1%, the value of the Fund’s portfolio with a portfolio duration of ten years would be expected to decrease by 10%, all other things being equal. In addition, different interest rate measures (such as short- and long-term interest rates and U.S. and foreign interest rates), or interest rates on different types of securities or securities of different issuers, may not necessarily change in the same amount or in the same direction.

Although CLOs are generally structured to mitigate the risk of interest rate mismatch, there may be some difference between the timing of interest rate resets on the assets and liabilities of a CLO. Such a mismatch in timing could have a negative effect on the amount of funds distributed to CLO investors. In addition, CLOs may not be able to enter into hedge agreements, even if it may otherwise be in the best interests of the CLO to hedge such interest rate risk.

As prevailing interest rates increase, some obligors may not be able to make the increased interest payments on loans or refinance their obligations, resulting in payment defaults and defaulted obligations. Many of the debt obligations underlying CLO or Warehouse Investments, and the debt issued by CLOs and Warehouses, bear interest at floating interest rates. Unlike fixed rate securities, floating rate securities generally will not increase in value if interest rates decline. Changes in interest rates also will affect the amount of interest income the Fund earns on its CLO and floating rate investments.

Credit risk – If an issuer or guarantor of a security held by the Fund or a counterparty to a financial contract with the Fund defaults on its obligation to pay principal and/ or interest, has its credit rating downgraded or is perceived to be less creditworthy, or the credit quality or value of any underlying assets declines, the value of your investment will decline. In addition, the Fund may incur expenses to protect the Fund’s interest in securities experiencing these events. A security may change in price for a variety of reasons. For example, floating rate securities may have final maturities of ten or more years, but their effective durations will tend to be very short. If there is an adverse credit event, or a perceived change in the issuer’s creditworthiness, these securities could experience a far greater negative price movement than would be predicted by the change in the security’s yield in relation to their effective duration. The Fund evaluates the credit quality of issuers and counterparties prior to investing in securities. Credit risk is broadly gauged by the credit ratings of the securities in which the Fund invests. However, ratings are only the opinions of the companies issuing them and are not guarantees as to quality. Securities rated in the lowest category of investment grade (Baa/BBB) may possess certain speculative characteristics.

Prepayment or call risk – Many issuers have a right to prepay their securities. If interest rates fall, an issuer may exercise this right. If this happens, the Fund would be forced to reinvest prepayment proceeds at a time when yields or securities available in the market are lower than the yield on the prepaid security. The Fund may also lose any premium it paid on the security.

Extension risk – When interest rates rise, repayments of debt securities, particularly asset- and mortgage-backed securities, may occur more slowly than anticipated, extending the effective duration of these debt securities at below market interest rates and causing their market prices to decline more than they would have declined due to the rise in interest rates alone. This may cause the Fund’s NAV to be more volatile.

Risks relating to collateralized loan obligations – In the case of most CLOs, the structured finance securities are issued in multiple tranches, offering investors various maturity and credit risk characteristics, often categorized as senior, mezzanine and subordinated/equity according to their degree of risk. If there are defaults or the relevant collateral otherwise underperforms, scheduled payments to senior tranches of such securities take precedence over those of mezzanine tranches, and scheduled payments to mezzanine tranches have a priority in right of payment to subordinated/equity tranches. CLOs may therefore present risks similar to those of other types of debt obligations and, in fact, such risks may be of greater significance in the case of CLOs depending upon the ranking of the Fund’s investment in the capital structure. Investments in structured vehicles, including equity and junior debt tranches of CLOs, involve risks, including credit risk and market risk. Changes in interest rates and credit quality may cause significant price fluctuations.

City National Rochdale Strategic Credit Fund | PAGE 20

In addition to the general risks associated with investing in debt securities, CLO securities carry additional risks, including: (i) the possibility that distributions from collateral assets will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) investments in CLO equity and junior debt tranches will likely be subordinate in right of payment to other senior classes of CLO debt; and (iv) the complex structure of a particular security may not be fully understood at the time of investment and may produce disputes with the issuer or unexpected investment results. Additionally, changes in the collateral held by a CLO may cause payments on the instruments held by the Fund to be reduced, either temporarily or permanently. CLOs also may be subject to prepayment risk. Further, the performance of a CLO may be adversely affected by a variety of factors, including the security’s priority in the capital structure of the issuer thereof, the availability of any credit enhancement, the level and timing of payments and recoveries on and the characteristics of the underlying receivables, loans or other assets that are being securitized, remoteness of those assets from the originator or transferor, the adequacy of and ability to realize upon any related collateral and the capability of the servicer of the securitized assets. There are also the risks that the trustee of a CLO does not properly carry out its duties to the CLO, potentially resulting in loss to the CLO.

The complex structure of CLO securities may produce unexpected investment results, especially during times of market stress or volatility. The complexity of CLOs and related investments gives rise to the risk that investors, parties involved in their creation and issuance, and other parties with an interest in them may not have the same understanding of how these investments behave, or the rights that the various interested parties have with respect to them. Furthermore, the documents governing these investments may contain some ambiguities that are subject to differing interpretations. Even in the absence of such ambiguities, if a dispute were to arise concerning these instruments, there is a risk that a court or other tribunal might not fully understand all aspects of these investments and might rule in a manner contrary to both the terms and the intent of the documents. Therefore, the Fund cannot be fully assured that it will be able to enjoy all of the rights that it expects to have when it invests in CLOs and related investments.

Investing in securities of CLOs involves the possibility of investments being subject to potential losses arising from material misrepresentation or omission on the part of borrowers whose loans make up the assets of such entities. Such inaccuracy or incompleteness may adversely affect the valuation of the receivables or may adversely affect the ability of the relevant entity to perfect or effectuate a lien on the collateral securing its assets. The CLOs in which the Fund invests will rely upon the accuracy and completeness of representations made by the underlying borrowers to the extent reasonable, but cannot guarantee such accuracy or completeness. The quality of the Fund’s investments in CLOs is subject to the accuracy of representations made by the underlying borrowers and issuers. In addition, the Fund is subject to the risk that the systems used by the originators of CLOs to control for accuracy are defective. Under certain circumstances, payments to the Fund may be reclaimed if any such payment or distribution is later determined to have been a fraudulent conveyance or a preferential payment.