| 53rd at Third | ||||||

| 885 Third Avenue | ||||||

| New York, New York 10022-4834 | ||||||

| Tel: +1.212.906.1200 Fax: +1.212.751.4864 | ||||||

| www.lw.com | ||||||

| FIRM / AFFILIATE OFFICES | |||||

| Beijing | Moscow | |||||

| Boston | Munich | |||||

| Brussels | New York | |||||

| Century City | Orange County | |||||

| Chicago | Paris | |||||

| Dubai | Riyadh | |||||

| September 4, 2018 | Düsseldorf | Rome | ||||

| Frankfurt | San Diego | |||||

| Hamburg | San Francisco | |||||

| Hong Kong | Seoul | |||||

| Houston | Shanghai | |||||

| London | Silicon Valley | |||||

| Los Angeles | Singapore | |||||

| Madrid | Tokyo | |||||

| Milan | Washington, D.C. | |||||

VIA EDGAR AND HAND DELIVERY

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549-6010

| Attention: | James Allegretto |

Scott Anderegg |

Mara Ransom |

Lisa Sellars |

| Re: | Farfetch Limited |

Registration Statement on Form F-1 |

Filed on August 20, 2018 |

CIK No. 0001740915 |

Ladies and Gentlemen:

On behalf of Farfetch Limited (the “Company”), we submit this letter to the staff of the Commission (the “Staff”). The Company intends to file Amendment No. 1 (the “Amendment No. 1”) on approximately September 5, 2018 to the Registration Statement on Form F-1 filed on August 20, 2018 (“Registration Statement”) with the Commission through its EDGAR system. The Company previously submitted a Draft Registration Statement on Form F-1 on a confidential basis pursuant to Title I, Section 106 under the Jumpstart Our Business Startups Act with the Securities and Exchange Commission (the “Commission”) on May 30, 2018 (the “Draft Submission”), as amended by Amendment No. 1 to the Draft Submission on July 11, 2018 (“Submission No. 2”) and by the Registration Statement on Form F-1 on August 2, 2018 (“Submission No. 3”). The purpose of this letter is to respond to the comment letter to the Registration Statement received on August 31, 2018 from the Staff.

For ease of review, we have set forth below each of the numbered comments of your letter in bold type followed by the Company’s responses thereto. Unless otherwise indicated, capitalized terms used herein have the meanings to be assigned to them in Amendment No. 1, and all references to page numbers in such responses are to page numbers in Amendment No. 1.

September 4, 2018

Page 2

Registration Statement on Form F-1

Dilution, page 63

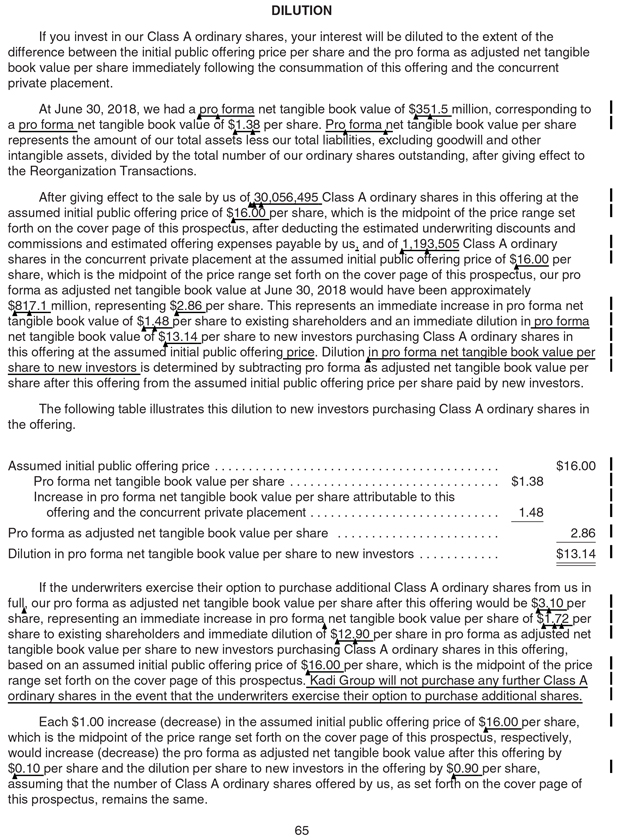

| 1. | We note that you have disclosed as of June 30, 2018 the number of shares that existing shareholders own in the table on page 64 and that you have used this number of shares to calculate your pro forma net tangible book value per share prior to the offering. Please show us how you calculated this number of shares. |

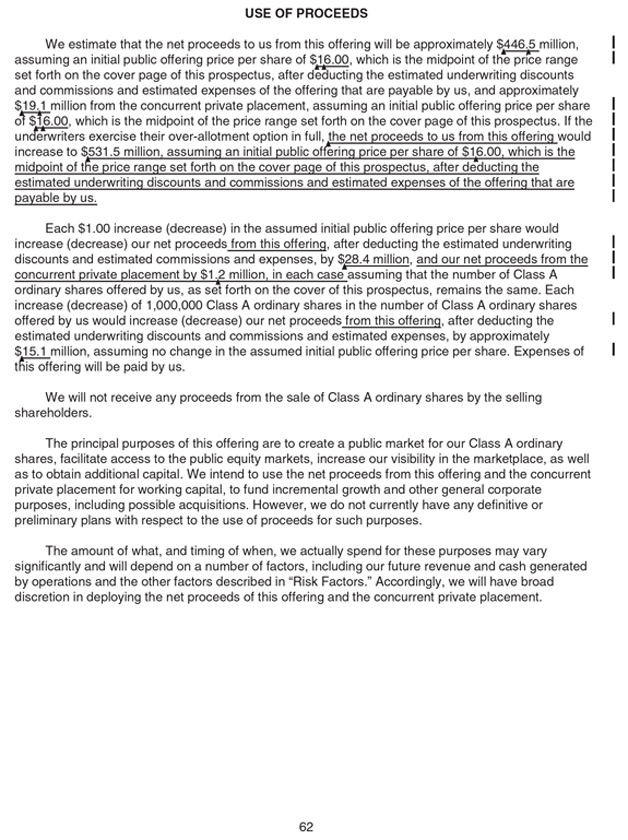

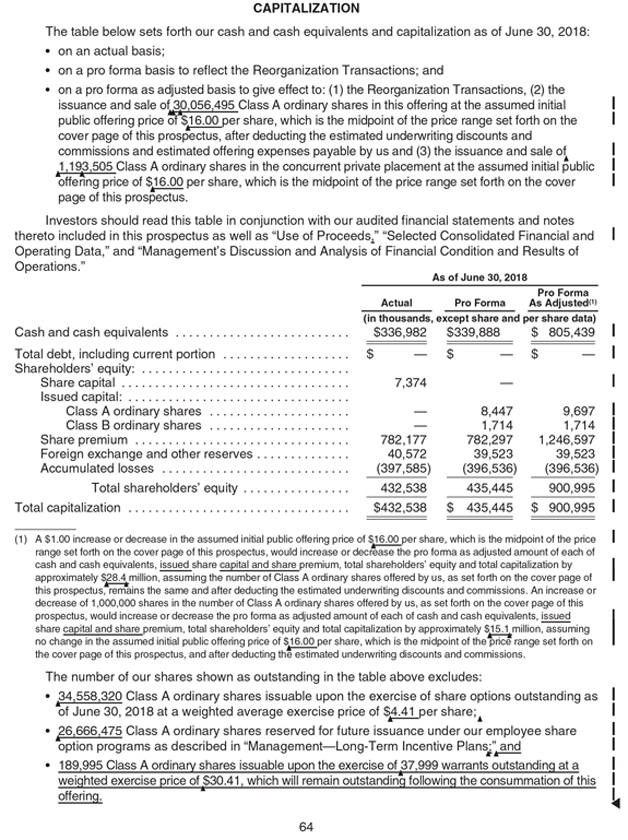

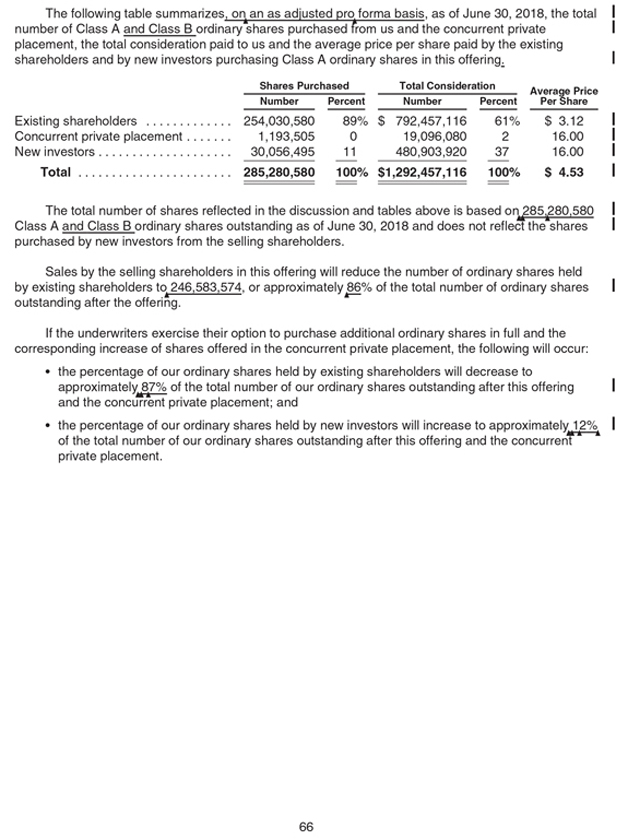

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that it will revise its disclosure on pages 65 and 66 to reflect its updated estimate for the assumed initial public offering price and related share amounts. The Company will also revise pages 62 and 64 for related disclosures in the “Use of Proceeds” and “Capitalization” sections. These changes are appended to this response letter as Appendix A, and the Company will reflect them in Amendment No. 1. |

The updated total shares held by existing shareholders in the “Dilution” section, shown on an as adjusted pro forma basis at 254,030,580 shares, reflects the expected exercise of certain share options, warrants, and restricted linked ordinary shares as well as the effects of the Reorganization Transactions, including the conversion of the Company’s ordinary and preference shares into ordinary shares and the subsequent exchange of the ordinary shares, at a ratio of one-to-five, into Class A and Class B ordinary shares, as applicable. The effects of these transactions are as follows: |

Total Farfetch.com Limited shares outstanding as at June 30, 2018 | 48,592,236 | |||

Pro forma adjustments: | ||||

Exercise of certain share options and warrants and conversion of restricted linked ordinary shares | 2,213,880 | |||

Conversion of ordinary and preferred shares and subsequent one-to-five exchange into Class A and Class B ordinary shares | 203,224,464 | |||

|

| |||

Total as adjusted, pro forma Farfetch Limited shares held by existing shareholders as at August 1, 2018 | 254,030,580 |

| 2. | We note that you disclose the amount of dilution that would occur if the underwriters exercise their option to purchase additional Class A ordinary shares. We also note that this calculation appears to include a corresponding increase of shares offered in the concurrent private placement. However, on page 13 you disclosed that Kadi Group will not purchase additional Class A ordinary shares in the event that the underwriters exercise their option to purchase additional shares. Please clarify for us the number of shares Kadi Group will purchase if the underwriters exercise their option to purchase additional Class A ordinary shares from you, if any. |

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that Kadi Group will not purchase any further Class A ordinary shares in the event that the underwriters exercise their option to purchase additional shares. The Company will revise the disclosure on page 65 of Amendment No. 1 accordingly. |

September 4, 2018

Page 3

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Results of Operations

Demand Generation Expense, page 82

| 3. | Enhance your disclosure of expenditures to explain how “increased sophistication in consumer segmentation and more focus on costs at a channel-by-channel level” has resulted in gained efficiencies. |

Response: The Company respectfully acknowledges the Staff’s comment and will add the following underlined disclosure to page 84 of Amendment No. 1: |

Demand generation expense for the six months ended June 30, 2018 increased by $12.1 million, or (41.7%), compared to the six months ended June 30, 2017 reflecting an increase in orders and GMV generated, partially offset by efficiencies gained in our demand generation spend through increased sophistication in consumer segmentation and more focus on costs at a channel-by-channel level. These improvements allow us to directly target consumers with an interest in luxury fashion and a propensity to spend, while our continued investment in predictive analytics allows us to identify the optimum media channel investment mix across all consumer segments and geographic markets. As a result, demand generation expense declined as a percentage of Adjusted Revenue, from (21.0%) in the six month period ended June 30, 2017 to (19.0%) in the six month period ended June 30, 2018. |

The Company will also add the following underlined disclosure to page 86 of Amendment No. 1: |

Demand generation expense for the year ended December 31, 2017 increased by $20.8 million, or (43.0%), compared to the year ended December 31, 2016. The expenditures related to existing markets and our continued international expansion into emerging markets across all channels. We gained efficiencies in our demand generation spend by scaling marketing operations across the 190 markets in which we have consumers and by automating campaign management and set up, thereby reducing the amount of time it takes to promote new products added to the platform. Demand generation expense declined as a percentage of Adjusted Revenue, from (25.0%) in 2016 to (22.2%) in 2017, resulting in an increase in Platform Order Contribution Margin over the same period, from 35.0% in 2016 to 43.0% in 2017. |

Principal and Selling Shareholders, page 135

| 4. | Please revise to identify the natural persons who have or share beneficial ownership of the securities held by Advent Private Equity Fund IV, Farhold (Luxembourg) S.a.r.l., DST Global IV, L.P., and Advance Publications, Inc. |

Response: The Company respectfully acknowledges the Staff’s comment and will revise the footnote disclosure for Advent Private Equity Fund IV, Farhold (Luxembourg) S.a.r.l., DST Global IV, L.P., and Advance Publications, Inc. on page 139 of Amendment No. 1 accordingly. |

September 4, 2018

Page 4

Correspondence submitted August 24, 2018

| 5. | We note your response to comment 2, however, we are unable to agree with your determination that your LTV/CAC ratio will not be useful to investors in the future without knowing whether or how the efficiencies in your marketing capabilities evolve over time relative to your customer acquisition rates and, therefore, if the ratio will continue to be useful. Please re-assess the usefulness of this disclosure at the time such disclosure is expected to be provided in the future, rather than making this determination now. |

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that it will re-assess the usefulness of this disclosure at the time such disclosure is expected to be provided in the future.

| 6. | We note your response to comment 3 and your proposed disclosure that you believe that the increase in popularity of (y)our app demonstrates the changing dynamics of consumers’ shopping behavior and that the increase in app use results in an increase in GMV. In your previous response, dated August 2, 2018, you stated that you believe the changing dynamics of consumers’ shopping behavior and the improved functionality of the app have led to the increase in the app’s share of GMV, rather than app users being a driver of increased total GMV. You also stated you do not directly monitor the impact of app use as correlated with GMV growth. Please explain your basis for the statement that the increase in app use results in an increase in GMV. Please revise to clearly disclose what, if any, correlation exists. |

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that it will revise the disclosure on page 112 of Amendment No. 1 to remove the statements that “the increase in app use results in an increase in GMV” and “from 2016 to 2017, our app’s share of GMV has increased from 13% to 27%.”

* * *

Please do not hesitate to contact me by telephone at (212) 906-1281 with any questions or comments regarding this correspondence.

| Very truly yours, |

/s/ Marc D. Jaffe |

| Marc D. Jaffe |

| of LATHAM & WATKINS LLP |

| cc: | (via email) |

James Maynard, Farfetch Limited

Ian D. Schuman, Esq., Latham & Watkins LLP

Joshua Kiernan, Esq., Latham & Watkins LLP

James D. Evans, Esq., Fenwick & West LLP

Katherine K. Duncan, Esq., Fenwick & West LLP

September 4, 2018

Page 5

Appendix A

[changed pages enclosed]