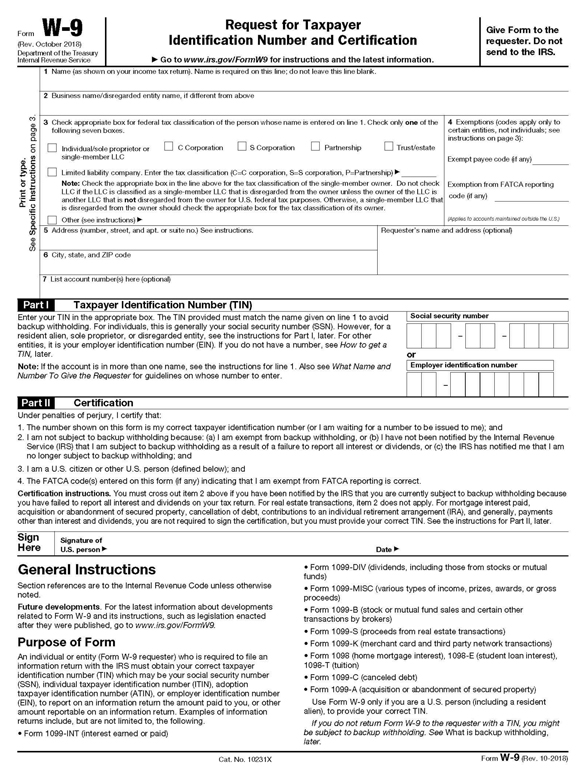

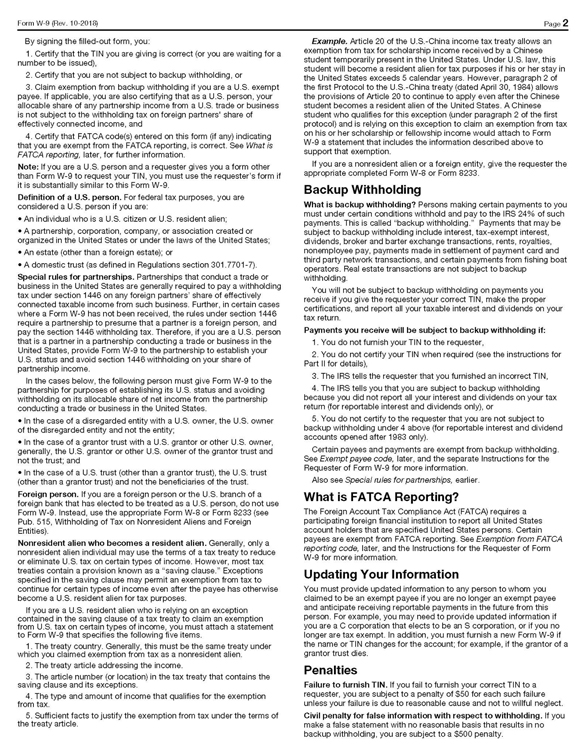

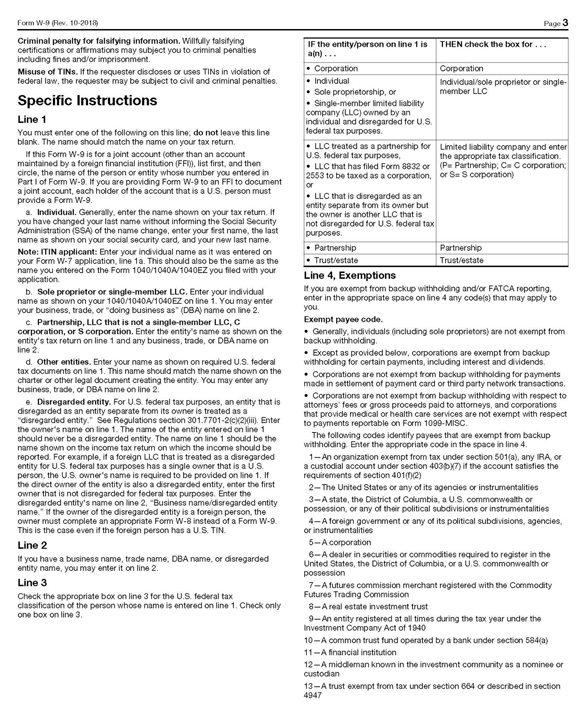

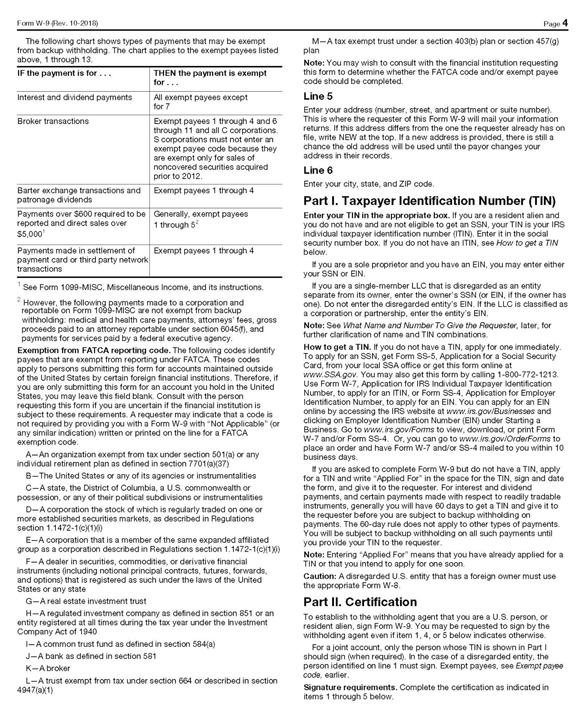

Notes is not tendered, then Old Notes for the principal amount of Old Notes not tendered and New Notes issued in exchange for any Old Notes accepted will be sent to the holder at his or her registered address, unless a different address is provided in the appropriate box on this Letter of Transmittal, promptly after the Old Notes are accepted for exchange.

4. Signatures on this Letter of Transmittal; Bond Powers and Endorsements; Guarantee of Signatures. If this Letter of Transmittal is signed by the record holders of the Old Notes tendered hereby, the signatures must correspond with the names as written on the face of the Old Notes without alteration, enlargement or any change whatsoever. If this Letter of Transmittal is signed by a participant in the DTC, the signature must correspond with the name as it appears on the security position listing as the holder of the Old Notes.

If this Letter of Transmittal is signed by the registered holders of Old Notes listed and tendered hereby and the New Notes issued in exchange therefor are to be issued (or any untendered principal amount of Old Notes is to be reissued) to the registered holders, such holders need not and should not endorse any tendered Old Notes, nor provide a separate bond power. In any other case, such holders must either properly endorse the Old Notes tendered or transmit a properly completed separate bond power with this Letter of Transmittal, with the signatures on the endorsement or bond power guaranteed by an eligible institution.

If this Letter of Transmittal is signed by a person other than the registered holders of any Old Notes listed, such Old Notes must be endorsed or accompanied by appropriate bond powers, in each case signed as the names of the registered holders appear on the Old Notes.

If this Letter of Transmittal or any Old Notes or bond powers are signed by trustees, executors, administrators, guardians, attorneys-in-fact, officers of corporations or others acting in a fiduciary or representative capacity, such persons should so indicate when signing, and, unless waived by the Company, evidence satisfactory to the Company of their authority to act must be submitted with this Letter of Transmittal.

Endorsements on Old Notes or signatures on bond powers required by this Instruction 4 must be guaranteed by an eligible institution. No signature guarantee is required if:

| | • | | this Letter of Transmittal is signed by the registered holders of the Old Notes tendered herein (or by a participant in one of the book-entry transfer facilities whose name appears on a security position listing as the owner of the tendered Old Notes) and the New Notes are to be issued directly to such registered holders (or, if signed by a participant in one of the book-entry transfer facilities, deposited to such participant’s account at the book-entry transfer facility) and neither the box entitled “Special Delivery Instructions” nor the box entitled “Special Issuance Instructions” has been completed; or |

| | • | | such Old Notes are tendered for the account of an eligible institution. |

In all other cases, all signatures on this Letter of Transmittal must be guaranteed by an eligible institution.

5. Special Issuance and Delivery Instructions. Tendering holders should indicate, in the applicable box or boxes, the name and address (or account at the book-entry transfer facility) in and to which New Notes or substitute Old Notes for principal amounts not tendered or not accepted for exchange are to be issued or sent, if different from the name and address of the persons signing this Letter of Transmittal. In the case of issuance in a different name, the taxpayer identification or social security number of the persons named must also be indicated.

6. Transfer Taxes. The Company will pay all transfer taxes, if any, applicable to the transfer and exchange of Old Notes pursuant to the exchange offer. If, however, New Notes or Old Notes for principal amounts not tendered or accepted for exchange are to be delivered to, or are to be registered or issued in the name of, any person other than the registered holders of the Old Notes tendered hereby, or if tendered Old Notes are registered in the name of any person other than the persons signing this Letter of Transmittal, or if a transfer tax is imposed for any reason other than the transfer and exchange of Old Notes to the Company or its order pursuant to the exchange offer, then the amount of any such transfer taxes (whether imposed on the registered holders or any other persons) will be payable by the tendering holders prior to the issuance of the New Notes or delivery or registering of the Old Notes. If satisfactory evidence of payment of such taxes or exemption therefrom is not submitted with this Letter of Transmittal, the amount of such transfer taxes will be billed directly to such tendering holders.

9