Table of Contents

Filed pursuant to Rule 424(b)(3)

Registration No. 333-231465

PROSPECTUS

CHENIERE ENERGY PARTNERS, L.P.

Offer to exchange up to

$1,100,000,000 of 5.625% Senior Notes due 2026

(CUSIP No. 16411Q AD3)

that have been registered under the Securities Act of 1933

for

$1,100,000,000 of 5.625% Senior Notes due 2026

(CUSIP Nos. 16411Q AC5 and U16353 AB7)

that have not been registered under the Securities Act of 1933

THE EXCHANGE OFFER EXPIRES AT 12:00 MIDNIGHT, NEW YORK

CITY TIME, AT THE END OF JULY 26, 2019, UNLESS WE EXTEND IT

Terms of the Exchange Offer:

| • | We are offering to exchange up to $1.1 billion aggregate principal amount of registered 5.625% Senior Notes due 2026 (CUSIP No. 16411Q AD3) (the “New Notes”) for any and all of our $1.1 billion aggregate principal amount of unregistered 5.625% Senior Notes due 2026 (CUSIP Nos. 16411Q AC5 and U16353 AB7) (the “Old Notes” and together with the New Notes, the “notes”) that were issued on September 11, 2018. |

| • | We will exchange all outstanding Old Notes that are validly tendered and not properly withdrawn prior to the expiration of the exchange offer for an equal principal amount of New Notes. |

| • | The terms of the New Notes will be substantially identical to those of the outstanding Old Notes except that the New Notes will be registered under the Securities Act of 1933, as amended (the “Securities Act”), and will not contain restrictions on transfer, registration rights or provisions for additional interest. |

| • | You may withdraw tenders of Old Notes at any time prior to the expiration of the exchange offer. |

| • | The exchange of Old Notes for New Notes will not be a taxable event for U.S. federal income tax purposes. |

| • | We will not receive any cash proceeds from the exchange offer. |

| • | During any Security Requirement Period (as defined below), the notes will be secured on a first-priority basis by a lien on the Collateral (as defined below), subject to certain liens permitted under the indenture, which liens are intended to bepari passu with the liens securing our senior secured credit facilities due 2020, which, as of March 31, 2019, consists of an undrawn $115 million revolving credit facility (the “CQP Credit Facilities”). When a Security Requirement Period is not in effect, the notes will remain senior obligations but will be unsecured. As of the date of this prospectus, the Old Notes are not and the New Notes will not be secured. |

| • | The Old Notes are, and the New Notes will be, unconditionally, jointly and severally guaranteed by each of our existing subsidiaries (including Sabine Pass LNG, L.P. and Cheniere Creole Trail Pipeline, L.P.), with the exception of Sabine Pass Liquefaction, LLC and Sabine PassLNG-LP, LLC. Any other subsidiary that guarantees any of our Material Indebtedness (as defined below) will also guarantee the notes. Please read “Description of Notes—Subsidiary Guarantees.” |

| • | There is no established trading market for the New Notes or the Old Notes. |

| • | We do not intend to apply for listing of the New Notes on any national securities exchange or for quotation through any quotation system. |

Please read “Risk Factors” beginning on page 8 for a discussion of certain risks that you should consider prior to tendering your outstanding Old Notes in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Each broker-dealer that receives New Notes for its own account pursuant to the exchange offer must acknowledge by way of letter of transmittal that it will deliver a prospectus in connection with any resale of New Notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, such broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of New Notes received in exchange for Old Notes where such Old Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. CQP and the Subsidiary Guarantors have agreed that, for a period of 180 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. Please Read “Plan of Distribution.”

The date of this prospectus is June 28, 2019.

Table of Contents

| ii | ||||

| ii | ||||

| iii | ||||

| iv | ||||

| v | ||||

| 1 | ||||

| 8 | ||||

| 13 | ||||

| 14 | ||||

| 17 | ||||

| 26 | ||||

| 59 | ||||

| 60 | ||||

| 61 | ||||

| 61 |

This prospectus incorporates important business and financial information about us that is not included or delivered with this prospectus. We will provide this information to you at no charge upon written or oral request directed to Corporate Secretary, Cheniere Energy Partners, L.P., 700 Milam Street, Suite 1900, Houston, Texas 77002 (telephone number(713) 375-5000).

In order to ensure timely delivery of this information, any request should be made by July 19, 2019, five business days prior to the expiration date of the exchange offer.

i

Table of Contents

This prospectus is part of a registration statement we filed with the U.S. Securities and Exchange Commission, referred to in this prospectus as the SEC. No person has been authorized to give any information or any representation concerning us or the exchange offer (other than as contained in this prospectus or the related letter of transmittal) and we take no responsibility for, nor can we provide any assurance as to the reliability of, any other information that others may give you. We are not making an offer to sell these securities in any state or jurisdiction where the offer is not permitted. You should not assume that the information contained in or incorporated by reference into this prospectus is accurate as of any date other than the date on the front cover of this prospectus or the date of such incorporated documents, as the case may be.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly, current and other reports with the SEC under the Securities and Exchange Act of 1934, as amended (the “Exchange Act”). Our SEC filings are available to the public over the Internet at the SEC’s website athttp://www.sec.gov.We will provide you upon request, without charge, a copy of the notes and the indenture governing the notes. You may request copies of these documents by contacting us at:

Cheniere Energy Partners, L.P.

Attention: Investor Relations Department

700 Milam Street, Suite 1900

Houston, Texas, 77002

(713)375-5000

We also make all periodic and other information filed or furnished with the SEC available, free of charge, on our website atwww.cheniere.comas soon as reasonably practicable after such information is electronically filed with or furnished to the SEC. Except as otherwise set forth herein, information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

ii

Table of Contents

INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

We “incorporate by reference” information into this prospectus, which means that we disclose important information to you by referring you to another document filed separately with the SEC. The information incorporated by reference is deemed to be part of this prospectus, except for any information superseded by information contained expressly in this prospectus. You should not assume that the information in this prospectus is current as of the date other than the date on the cover page of this prospectus.

All documents that we file pursuant to Section 13(a), 13(c), 14 or 15(d) of the Exchange Act after the date the registration statement of which this prospectus forms a part was filed and prior to the effectiveness of such registration statement and until this offering is completed will be deemed to be incorporated by reference in this prospectus and will be a part of this prospectus from the date of filing. Any statement contained in a document incorporated or deemed to be incorporated by reference in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus or in any other subsequently filed document that also is or is deemed to be incorporated by reference in this prospectus modifies or supersedes that statement. Any statement that is modified or superseded will not constitute a part of this prospectus, except as modified or superseded.

We incorporate by reference the documents listed below (excluding any information furnished and not filed with the SEC):

| • | our Annual Report onForm 10-K for the fiscal year ended December 31, 2018 filed with the SEC on February 25, 2019; |

| • | our Quarterly Report onForm10-Q for the quarter ended March 31, 2019 filed with the SEC on May 8, 2019; and |

| • | our Current Reports onForm 8-K filed onJanuary 25, 2019 andApril 26, 2019. |

These reports contain important information about us, our financial condition and our results of operations.

You may request a copy of any document incorporated by reference in this prospectus and any exhibit specifically incorporated by reference in those documents, at no cost, by writing or telephoning us at the following address or phone number:

Cheniere Energy Partners, L.P.

Attention: Investor Relations Department

700 Milam Street, Suite 1900

Houston, Texas 77002

(713)375-5000

iii

Table of Contents

In this prospectus, we rely on and refer to information and statistics regarding our industry. We obtained this market data from independent industry publications or other publicly available information. Although we believe that these sources are reliable, we have not independently verified and do not guarantee the accuracy or completeness of this information.

In this prospectus, unless the context otherwise requires:

| • | Bcfmeans billion cubic feet; |

| • | Bcf/dmeans billion cubic feet per day; |

| • | Bcfemeans billion cubic feet equivalent; |

| • | EPCmeans engineering, procurement and construction; |

| • | GAAPmeans generally accepted accounting principles in the United States; |

| • | LIBORmeans the London Interbank Offered Rate; |

| • | LNGmeans liquefied natural gas, a product of natural gas that, through a refrigeration process, has been cooled to a liquid state, which occupies a volume that is approximately 1/600th of its gaseous state; |

| • | MMBtumeans million British thermal units, an energy unit; |

| • | MMBtu/dmeans million British thermal units per day; |

| • | mtpameans million tonnes per annum; |

| • | SPAmeans an LNG sale and purchase agreement; and |

| • | Trainmeans an industrial facility comprised of a series of refrigerant compressor loops used to cool natural gas into LNG. |

iv

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus, including any information incorporated by reference herein, contains certain statements that are, or may be deemed to be, “forward-looking statements.” All statements, other than statements of historical or present facts or conditions, included herein or incorporated herein by reference are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

| • | statements regarding our ability to pay interest, premium, if any, and principal on the notes; |

| • | statements regarding our expected receipt of cash distributions from SPLNG, SPL or CTPL; |

| • | statements that we expect to commence or complete construction of our proposed LNG terminals, liquefaction facilities, pipeline facilities or other projects, or any expansions or portions thereof, by certain dates, or at all; |

| • | statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North America and other countries worldwide or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure or demand for and prices related to natural gas, LNG or other hydrocarbon products; |

| • | statements regarding any financing transactions or arrangements, or our ability to enter into such transactions; |

| • | statements relating to the construction of our Trains, including statements concerning the engagement of any EPC contractor or other contractor and the anticipated terms and provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto; |

| • | statements regarding any SPA or other agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, natural gas liquefaction or storage capacities that are, or may become, subject to contracts; |

| • | statements regarding counterparties to our commercial contracts, construction contracts, and other contracts; |

| • | statements regarding our planned development and construction of additional Trains, including the financing of such Trains; |

| • | statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities; |

| • | statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections, or objectives, including anticipated revenues, capital expenditures, maintenance and operating costs and cash flows, any or all of which are subject to change; |

| • | statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings, investigations, proceedings or decisions; and |

| • | any other statements that relate tonon-historical or future information. |

All of these types of statements, other than statements of historical or present facts or conditions, are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “should,” “achieve,” “anticipate,” “believe,” “contemplate,” “continue,” “estimate,” “expect,” “intend,” “plan,” “potential,” “predict,” “project,” “pursue,” “target,” the negative of such terms or other comparable terminology. The forward-looking statements contained in this prospectus or incorporated by reference herein are largely based on our expectations, which reflect estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe that such estimates are reasonable, they are inherently uncertain and involve a number of risks and uncertainties beyond our control. In addition, assumptions may prove to be inaccurate. We caution that the forward-looking statements contained in this prospectus or incorporated by reference herein are not guarantees of future performance and that such statements may not be realized or the forward-looking statements or events may not occur. Actual results may differ materially from those anticipated or implied in forward-looking statements as a result of a variety of factors, including those described in “Risk Factors” and elsewhere in this prospectus and incorporated by reference in the other reports and other information that we file with the SEC. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors. These forward-looking statements speak only as of the date made, and other than as required by law, we undertake no obligation to update or revise any forward-looking statement or provide reasons why actual results may differ, whether as a result of new information, future events or otherwise.

All forward-looking statements are expressly qualified in their entirety by the foregoing cautionary statements.

v

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It does not contain all of the information that you should consider before making an investment decision. You should carefully read this entire prospectus for a more complete understanding of our business and the terms of this exchange offer, as well as the tax and other considerations that are important to you in making your investment decision.

As used in this prospectus, the “Partnership,” “CQP,” “we,” “our,” “us” or similar terms refer to Cheniere Energy Partners, L.P. and not any of its subsidiaries or any entities that are consolidated with it for financial reporting purposes, unless otherwise expressly stated or the context otherwise requires. In this prospectus, (i) our “general partner” refers to Cheniere Energy Partners GP, LLC, a Delaware limited liability company and the general partner of the Partnership; (ii) “Cheniere” refers to Cheniere Energy, Inc., a Delaware corporation that owns and controls our general partner; (iii) “SPLNG” refers to Sabine Pass LNG, L.P., a Delaware limited partnership and our wholly owned subsidiary; (iv) “SPL” refers to Sabine Pass Liquefaction, LLC, a Delaware limited liability company and our wholly owned subsidiary; and (v) “CTPL” refers to Cheniere Creole Trail Pipeline, L.P., a Delaware limited partnership and our wholly owned subsidiary. We refer to SPLNG, CTPL and each other of our subsidiaries that guarantees the notes collectively as the “Subsidiary Guarantors.”

Cheniere Energy Partners, L.P.

Overview

We are a publicly traded Delaware limited partnership formed by Cheniere in 2006. Our vision is to provide clean, secure and affordable energy to the world, while responsibly delivering a reliable, competitive and integrated source of LNG, in a safe and rewarding work environment. The liquefaction of natural gas into LNG allows it to be shipped economically from areas of the world where natural gas is abundant and inexpensive to produce to other areas where natural gas demand and infrastructure exist to economically justify the use of LNG. Through our wholly owned subsidiary, SPL, we are developing, constructing and operating natural gas liquefaction facilities (the “Liquefaction Project”) at the Sabine Pass LNG terminal located in Cameron Parish, Louisiana, on the Sabine-Neches Waterway less than four miles from the Gulf Coast. We plan to construct up to six Trains, which are in various stages of development, construction and operations. Trains 1 through 5 are operational and Train 6 is being commercialized and has all necessary regulatory approvals in place. Each Train is expected to have a nominal production capacity, which is prior to adjusting for planned maintenance, production reliability, potential overdesign and debottlenecking opportunities, of approximately 4.5 mtpa of LNG per Train, and run rate adjusted nominal production capacity of approximately 4.5 to 4.9 mtpa of LNG per Train. Through our wholly owned subsidiary, SPLNG, we own and operate regasification facilities at the Sabine Pass LNG terminal, which includespre-existing infrastructure of five LNG storage tanks with aggregate capacity of approximately 16.9 Bcfe, two marine berths that can each accommodate vessels with nominal capacity of up to 266,000 cubic meters and vaporizers with regasification capacity of approximately 4.0 Bcf/d. We also own a94-mile pipeline that interconnects the Sabine Pass LNG terminal with a number of large interstate pipelines (the “Creole Trail Pipeline”) through our wholly owned subsidiary, CTPL.

Principal Executive Offices

Our principal executive offices are located at 700 Milam Street, Suite 1900, Houston, Texas 77002, and our telephone number is(713) 375-5000. Our internet address iswww.cheniere.com.Information on our website is not incorporated by reference herein and our web address is included in this prospectus as an inactive textual reference only.

1

Table of Contents

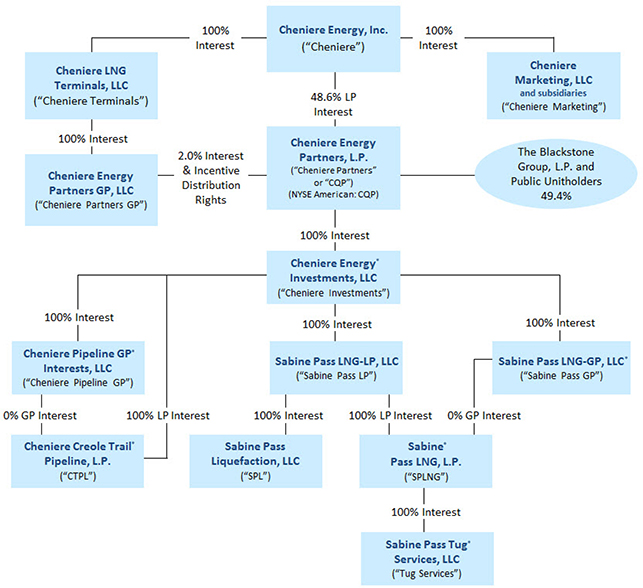

Our Ownership and Organizational Structure

The following diagram depicts our abbreviated organizational structure as of March 31, 2019, including our ownership of certain subsidiaries, and the references to these entities used in this prospectus:

| * | Guarantors |

2

Table of Contents

The Exchange Offer

On September 11, 2018, we completed a private offering of $1.1 billion aggregate principal amount of the Old Notes. As part of this private offering, we entered into a registration rights agreement with the initial purchasers of the Old Notes in which we agreed, among other things, to deliver this prospectus to you and to use our reasonable best efforts to consummate the exchange offer no later than 360 days after the September 11, 2018 private offering. The following is a summary of the exchange offer.

| Old Notes | 5.625% Senior Notes due 2026, which were issued on September 11, 2018. | |

| New Notes | 5.625% Senior Notes due 2026. The terms of the New Notes are substantially identical to the terms of the outstanding Old Notes except that the transfer restrictions, registration rights and provisions for additional interest relating to the Old Notes will not apply to the New Notes. | |

| Exchange Offer | We are offering to exchange up to $1.1 billion aggregate principal amount of our New Notes that have been registered under the Securities Act for an equal amount of our outstanding Old Notes that have not been registered under the Securities Act to satisfy our obligations under the registration rights agreement.

The New Notes will evidence the same debt as the Old Notes for which they are being exchanged and will be issued under, and be entitled to the benefits of, the same indenture that governs the Old Notes. Holders of the Old Notes do not have any appraisal or dissenters’ rights in connection with the exchange offer. Because the New Notes will be registered, the New Notes will not be subject to transfer restrictions, and holders of Old Notes that have tendered and had their Old Notes accepted in the exchange offer will have no registration rights. The New Notes will have a CUSIP number different from that of any Old Notes that remain outstanding after the completion of the exchange offer. | |

| Expiration Date | The exchange offer will expire at 12:00 midnight, New York City time, at the end of July 26, 2019, unless we decide to extend the date. | |

| Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, which we may waive. Please read “The Exchange Offer—Conditions to the Exchange Offer” for more information regarding the conditions to the exchange offer. | |

| Procedures for Tendering Old Notes | You must do one of the following on or prior to the expiration of the exchange offer to participate in the exchange offer:

• tender your Old Notes by sending the certificates for your Old Notes, in proper form for transfer, a properly completed and duly executed letter of transmittal, with any required signature guarantees, and all other documents required by the letter of transmittal, to The Bank of New York Mellon, as registrar and exchange agent, at the address listed under the caption “The Exchange Offer—Exchange Agent”; or

• tender your Old Notes by using the book-entry transfer procedures described below and transmitting a properly completed and duly executed letter of transmittal, with any required signature guarantees, or an agent’s message instead of the letter of transmittal, to the exchange agent. In order for a book-entry transfer to constitute a valid tender of your Old Notes in the exchange offer, The Bank of New York Mellon, as registrar and exchange agent, must receive a confirmation of book-entry transfer of your Old Notes into the exchange agent’s account at The Depository Trust Company (“DTC”) prior to the expiration of the exchange offer. For more information regarding the use of book-entry transfer procedures, including a description of the required agent’s message, please read the discussion under the caption “The Exchange Offer—Procedures for Tendering—Book-entry Transfer.” | |

3

Table of Contents

| Withdrawal;Non-Acceptance | You may withdraw any Old Notes tendered in the exchange offer at any time prior to 12:00 midnight, New York City time, at the end of July 26, 2019 by following the procedures described in this prospectus and the related letter of transmittal. If we decide for any reason not to accept any Old Notes tendered for exchange, the Old Notes will be returned to the registered holder at our expense promptly after the expiration or termination of the exchange offer. In the case of Old Notes tendered by book-entry transfer in to the exchange agent’s account at DTC, any withdrawn or unaccepted Old Notes will be credited to the tendering holder’s account at DTC. For further information regarding the withdrawal of tendered Old Notes, please read “The Exchange Offer—Withdrawal Rights.” | |

| Material U.S. Federal Income Tax Considerations | The exchange of New Notes for Old Notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. Please read the discussion under the caption “Material United States Federal Income Tax Considerations” for more information regarding the tax considerations to you of the exchange offer. | |

| Use of Proceeds | The issuance of the New Notes will not provide us with any new proceeds. We are making this exchange offer solely to satisfy our obligations under the registration rights agreement. | |

| Fees and Expenses | We will pay all of our expenses incident to the exchange offer. | |

| Exchange Agent | We have appointed The Bank of New York Mellon as exchange agent for the exchange offer. For the address, telephone number and fax number of the exchange agent, please read “The Exchange Offer—Exchange Agent.” | |

| Resales of New Notes | Based on interpretations by the staff of the SEC, as set forth inno-action letters issued to third parties that are not related to us, we believe that the New Notes you receive in the exchange offer may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act so long as:

• the New Notes are being acquired in the ordinary course of business;

• you are not participating, do not intend to participate, and have no arrangement or understanding with any person to participate in the distribution of the New Notes issued to you in the exchange offer;

• you are not our affiliate or an affiliate of any of our Subsidiary Guarantors; and

• you are not a broker-dealer tendering Old Notes acquired directly from us for your account.

The SEC has not considered this exchange offer in the context of ano-action letter, and we cannot assure you that the SEC would make similar determinations with respect to this exchange offer. If any of these conditions are not satisfied, or if our belief is not accurate, and you transfer any New Notes issued to you in the exchange offer without delivering a resale prospectus meeting the requirements of the Securities Act or without an exemption from registration of your New Notes from those requirements, you may incur liability under the Securities Act. We will not assume, nor will we indemnify you against, any such liability. Each broker-dealer that receives New Notes for its own account in exchange for Old Notes, where the Old Notes were acquired by such broker-dealer as a result of market-making or other trading activities, must acknowledge that it will deliver a prospectus in connection with any resale of such New Notes. Please read “Plan of Distribution.”

Please read “The Exchange Offer—Resales of New Notes” for more information regarding resales of the New Notes. | |

| Consequences of Not Exchanging Your Old Notes | If you do not exchange your Old Notes in this exchange offer, you will no longer be able to require us to register your Old Notes under the Securities Act, except in the limited circumstances provided under the registration rights agreement. In addition, you will not be able to resell, offer to resell or otherwise transfer your Old Notes unless we have registered the Old Notes under the Securities Act, or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act. | |

4

Table of Contents

| For information regarding the consequences of not tendering your Old Notes and our obligation to file a registration statement, please read “The Exchange Offer— Consequences of Failure to Exchange Old Notes” and “Description of Notes.” |

5

Table of Contents

Terms of the New Notes

The terms of the New Notes will be substantially identical to the terms of the Old Notes except that the transfer restrictions, registration rights and provisions for additional interest relating to the Old Notes will not apply to the New Notes. As a result, the New Notes will not bear legends restricting their transfer and will not have the benefit of the registration rights and additional interest provisions contained in the Old Notes. The New Notes represent the same debt as the Old Notes for which they are being exchanged. The New Notes are governed by the same indenture as that which governs the Old Notes.

The following summary contains basic information about the New Notes and is not intended to be complete. For a more complete understanding of the New Notes, please refer to the section in this prospectus entitled “Description of Notes.” When we use the term “notes” in this prospectus, unless the context requires otherwise, the term includes the Old Notes and the New Notes.

| Issuer | Cheniere Energy Partners, L.P. | |

| Notes Offered | $1,100,000,000 aggregate principal amount of 5.625% senior notes due 2026. | |

| Maturity Date | October 1, 2026. | |

| Interest Rate | 5.625% per year (calculated using a360-day year). | |

| Interest Payment Dates | We will pay interest on the New Notes semi-annually, in cash in arrears, on April 1 and October 1 of each year. | |

| Ranking | As of the date of this prospectus, the Old Notes are, and the New Notes will be, unsecured. During any Security Requirement Period (as defined below), the New Notes will be senior obligations of CQP and will be secured on a first-priority basis by a lien on the Collateral (as defined below), subject to certain liens permitted under the indenture, which liens are intended to bepari passuwith the liens securing the CQP Credit Facilities. When a Security Requirement Period is not in effect, the New Notes will remain senior obligations of CQP, but will be unsecured. The New Notes:

• will rank senior in right of payment to all future obligations of CQP that are, by their terms, expressly subordinated in right of payment to the notes andpari passu in right of payment with all existing and future senior obligations of CQP that are not so subordinated;

• will be structurally subordinated to all liabilities and preferred equity of subsidiaries of CQP that are not Subsidiary Guarantors; and

• will be guaranteed by each subsidiary of CQP that is, or in the future is required to become, a Subsidiary Guarantor.

See “Description of Notes—Ranking” and “Description of Notes—Security for the Notes.” | |

| Guarantees | The New Notes will be unconditionally, jointly and severally guaranteed by each of CQP’s existing subsidiaries (including SPLNG and CTPL and, during any Security Requirement Period, Sabine PassLNG-LP, LLC (“SPL Member”)) with the exception of SPL. Any other subsidiary that guarantees any Material Indebtedness (as defined below) of CQP will also guarantee the New Notes. Please read “Description of Notes—Subsidiary Guarantees.”

As of March 31, 2019, we and our Subsidiary Guarantors had approximately $2.6 billion of debt outstanding (before unamortized premium, discount and debt issuance costs, net), all of which is unsecured. As of March 31, 2019, CQP’snon-guarantor subsidiaries had approximately $13.7 billion of indebtedness outstanding (before unamortized premium, discount and debt issuance costs, net), excluding $421 million aggregate outstanding letters of credit, all of which will rank effectively senior to the New Notes. | |

6

Table of Contents

| Covenants | The indenture governing the New Notes will, among other things, limit our Subsidiary Guarantors’ ability to:

• create liens or other encumbrances;

• engage in certain transactions with affiliates;

• enter into sale-leaseback transactions; and

• merge or consolidate with another entity or sell all or substantially all of our assets.

These covenants are subject to a number of important qualifications and exceptions which are described in “Description of Notes—Covenants.” | |

| Risk Factors | You should refer to “Risk Factors” beginning on page 8 of this prospectus, the risk factors set forth in our Annual Report onForm 10-K for the year ended December 31, 2018, “Forward-Looking Statements” and the other information included in or incorporated by reference into this prospectus for a discussion of the risk factors you should carefully consider before deciding participate in the exchange offer. | |

7

Table of Contents

Before deciding to participate in the exchange offer, you should carefully consider the risks and uncertainties described below as well as the risk factors contained in the section titled “Risk Factors” included in our Annual Report onForm 10-K for the year ended December 31, 2018. The risk factors included or incorporated by reference herein are some of the important factors that could affect our financial performance or could cause actual results to differ materially from estimates or expectations contained in our forward-looking statements. We may encounter risks in addition to those included or incorporated by reference herein. Additional risks and uncertainties not currently known to us, or that we currently deem to be immaterial, may also impair or adversely affect our business, contracts, financial condition, operating results, cash flow, liquidity, prospects and ability to make payments of interest, premium, if any, and principal on the New Notes.

Risks Relating to the Exchange Offer and the New Notes

If you do not properly tender your Old Notes, you will continue to hold unregistered outstanding notes and your ability to transfer outstanding notes will be adversely affected.

We will only issue New Notes in exchange for Old Notes that you timely and properly tender. Therefore, you should allow sufficient time to ensure timely delivery of the Old Notes, and you should carefully follow the instructions on how to tender your Old Notes. Neither we nor the exchange agent is required to tell you of any defects or irregularities with respect to your tender of Old Notes. Please read “The Exchange Offer— Procedures for Tendering” and “Description of Notes.”

If you do not exchange your Old Notes for New Notes in the exchange offer, you will continue to be subject to the restrictions on transfer of your Old Notes described in the legend on the certificates for your Old Notes. In general, you may only offer or sell the Old Notes if they are registered under the Securities Act and applicable state securities laws, or offered and sold under an exemption from these requirements. Except in connection with this exchange offer or as required by the registration rights agreement, we do not intend to register resales of the Old Notes under the Securities Act. For further information regarding the consequences of not tendering your Old Notes in the exchange offer, please read “The Exchange Offer— Consequences of Failure to Exchange Old Notes.”

Some holders who exchange their Old Notes may be deemed to be underwriters and must deliver a prospectus in connection with resales of the New Notes.

If you exchange your Old Notes in the exchange offer for the purpose of participating in a distribution of the New Notes, you may be deemed to have received restricted securities and, if so, will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. If such a holder transfers any New Notes without delivering a prospectus meeting the requirements of the Securities Act or without an applicable exemption from registration under the Securities Act, such a holder may incur liability under the Securities Act. We do not and will not assume or indemnify such a holder against this liability.

Despite our current level of indebtedness, the indenture will permit us and our subsidiaries to incur substantially more indebtedness, some of which may be secured. This could further increase the risks associated with our substantial indebtedness.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future. The terms of our indenture will not prohibit us or our subsidiaries from doing so. If we incur any additional indebtedness that ranks equally with the New Notes and the guarantees, the holders of that indebtedness will be entitled to share ratably with the New Notes and the related guarantees in any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or otherwinding-up of us. If our current debt levels increase, the related risks that we and our subsidiaries now face could intensify.

In addition, we and our subsidiaries are permitted to incur aggregate additional secured indebtedness (other than the 5.250% Senior Notes due 2025 (the “2025 CQP Senior Notes”) or any other series of notes issued under the indenture) up to the greater of (i) $1.5 billion and (ii) 10% of Net Tangible Assets under the terms of the indenture before entering a Security Requirement Period and being required to secure the New Notes to the same extent of such secured indebtedness. The New Notes will be subordinated to any such secured indebtedness, such that the holders of that indebtedness will be entitled to payment from any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or otherwinding-up of us to the extent of such collateral prior to the holders of the notes. This may have the effect of reducing the amount of any proceeds paid to you in such circumstances. See “Description of Notes—Security for the Notes.”

8

Table of Contents

Our future debt levels may impair our financial condition and prevent us from fulfilling our obligations under the New Notes.

As of March 31, 2019, we had no cash and cash equivalents, $1.3 billion of current restricted cash and $16.3 billion of total debt outstanding on a consolidated basis (before unamortized premium, discount and debt issuance costs), excluding $421 million aggregate outstanding letters of credit. We incur, and will incur, significant interest expense relating to the assets at the Sabine Pass LNG terminal and we anticipate needing to incur additional debt to finance the construction of Train 6 of the Liquefaction Project. The level of our future indebtedness could have important consequences to us, including:

| • | making it more difficult for us to satisfy our obligations with respect to the New Notes, our CQP Credit Facilities governing our revolving credit facility and other debt agreements; |

| • | limiting our ability to borrow additional amounts to fund working capital, capital expenditures, acquisitions, debt service requirements, the execution of our growth strategy and other activities; |

| • | requiring us to dedicate a substantial portion of our cash flow from operations to pay interest on our debt, which would reduce our cash flow available to fund working capital, capital expenditures, acquisitions, execution of our growth strategy and other activities; |

| • | making us more vulnerable to adverse changes in general economic conditions, our industry and government regulations and in our business by limiting our flexibility in planning for, and making it more difficult for us to react quickly to, changing conditions; and |

| • | placing us at a competitive disadvantage compared with our competitors that have less debt. |

In addition, we may not be able to generate sufficient cash flow from our operations to repay our indebtedness when it becomes due and to meet other cash needs. Our ability to service our debt will depend upon, among other things, our future financial and operating performance, which will be affected by prevailing economic conditions and financial, business, regulatory and other factors, some of which are beyond our control. In addition, our ability to service our debt will depend on market interest rates, since we anticipate that the interest rates applicable to borrowings under our revolving credit facility will fluctuate. If we are not able to pay our debts as they become due, we will be required to pursue one or more alternative strategies, such as selling assets, refinancing or restructuring our indebtedness or selling additional debt or equity securities. We may not be able to refinance our debt or sell additional debt or equity securities or our assets on favorable terms, if at all, and if we must sell our assets, it may negatively affect our ability to generate revenues.

The New Notes will be structurally subordinated to all liabilities of anynon-guarantor subsidiaries.

The New Notes will be structurally subordinated to the indebtedness and other liabilities of any of our subsidiaries that do not guarantee the New Notes, including indebtedness of SPL and, when a Security Requirement Period is not in effect, SPL Member. Anynon-guarantor subsidiaries are separate and distinct legal entities and will have no obligation, contingent or otherwise, to pay any amounts due pursuant to the New Notes, or to make any funds available therefor, whether by loans, distributions or other payments. Any right that we or the Subsidiary Guarantors have to receive any assets of any suchnon-guarantor subsidiaries upon the liquidation or reorganization of those subsidiaries, and the consequent rights of holders of New Notes to realize proceeds from the sale of any of those subsidiaries’ assets, will be structurally subordinated to the claims of those subsidiaries’ creditors, including trade creditors and holders of preferred equity interests of those subsidiaries. Accordingly, in the event of a bankruptcy, liquidation or reorganization of any suchnon-guarantor subsidiaries, thesenon-guarantor subsidiaries will pay the holders of their debts, holders of preferred equity interests and their trade creditors before they will be able to distribute any of their assets to us. As of March 31, 2019, ournon-guarantor subsidiaries had approximately $13.7 billion of indebtedness outstanding (before unamortized premium, discount and debt issuance costs, net), all of which would rank effectively senior to the New Notes.

Our existing debt agreements have, and the indenture governing the notes will have, substantial restrictions and financial covenants that may restrict our business and financing activities.

We are dependent upon the earnings and cash flow generated by our operations in order to meet our debt service obligations. The operating and financial restrictions and covenants in our CQP Credit Facilities, the New Notes and any future financing agreements may restrict our ability to finance future operations or capital needs and to engage in or expand our business activities. For example, our CQP Credit Facilities and the indenture governing the notes restrict our ability to, among other things:

| • | sell or otherwise dispose of a portion of our assets; |

| • | engage in certain transactions with affiliates; |

9

Table of Contents

| • | enter into sale-leaseback transactions; and |

| • | merge or consolidate with another entity or sell all or substantially all of our assets. |

In addition, our CQP Credit Facilities contain covenants requiring us to maintain certain financial ratios and limits our ability to create liens or other encumbrances.

Our future ability to comply with these restrictions and covenants is uncertain and will be affected by the levels of cash flow from our operations and other events or circumstances beyond our control. If market or other economic conditions deteriorate, our ability to comply with these covenants may be impaired. If we violate any provisions of our CQP Credit Facilities or the notes that are not cured or waived within the appropriate time period provided therein, a significant portion of our indebtedness may become immediately due and payable and the commitment of our revolving credit facility lenders to make further loans to us may terminate. We might not have, or be able to obtain, sufficient funds to make these accelerated payments.

If a Security Requirement Period comes into effect and the New Notes become secured, there may not be sufficient collateral to pay all or any of the New Notes and the rights of holders of the New Notes may be limited.

In the event that a Security Requirement Period later comes into effect, our indebtedness and other obligations under the CQP Credit Facilities, the Old Notes and the existing senior notes of our subsidiaries are, and the New Notes and certain other secured indebtedness that we may incur in the future will be, secured by a first-priority lien on substantially all of our and/or certain of our subsidiaries’ assets, subject to certain exceptions and permitted liens and subject to the terms of the Intercreditor Agreement (as defined below). The value of the collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. By its nature, some or all of the collateral may be illiquid and may have no readily ascertainable market value. The value of the assets pledged as collateral during a Security Requirement Period could be impaired as a result of changing economic conditions, competition or other future trends. Additionally, we may incur additional indebtedness secured by the collateral, which may dilute the value of the rights the holders of the New Notes have in the collateral.

Additionally, during any Security Requirement Period, the trustee will join as a party to the Intercreditor Agreement, or equivalent agreement, via a joinder agreement. Under the terms of the Intercreditor Agreement, any actions that may be taken in respect of the collateral, including the ability to cause the commencement of enforcement proceedings against the collateral and the release of the collateral from any lien, will be at the direction of the administrative agent under the CQP Credit Facilities prior to the discharge of the obligations under the CQP Credit Facilities and until 180 days has passed after an event of default occurred under additional first lien debt. Neither the trustee nor the collateral agent, on behalf of the holders of New Notes, would have the ability to control or to direct such actions, even if an event of default under the New Notes has occurred, except in limited circumstances. See “Description of Notes—Security for the Notes—Intercreditor Agreement.” In addition, subject to limitations adversely affecting the equal and ratable treatment of the security interest of the trustee or imposing new material obligations on the trustee, the collateral agent would be entitled, without the consent of holders of the New Notes or the trustee, to amend the terms of the security documents securing the New Notes and to release the liens of the secured parties on any part of the collateral in accordance with the terms of such agreement. The collateral so released would no longer secure obligations under the New Notes. See “Description of Notes—Security for the Notes—Collateral Agency Agreement” and “—Security for the Notes.”

Federal and state statutes allow courts, under specific circumstances, to void subsidiary guarantees and require noteholders to return payments received from the Subsidiary Guarantors.

Under the federal bankruptcy law and comparable provisions of state fraudulent transfer laws, a subsidiary’s guarantee of the New Notes could be voided, or claims in respect of a guarantee could be subordinated to all other debts of that guarantor, if, among other things, the guarantor, at the time it incurred the debt evidenced by its guarantee:

| • | received less than reasonably equivalent value or fair consideration for the incurrence of such guarantee; |

| • | was insolvent or rendered insolvent by reason of such incurrence; |

| • | was engaged in a business or transaction for which the guarantor’s remaining assets constituted unreasonably small capital; or |

| • | intended to incur, or believed that it would incur, debts beyond its ability to pay such debts as they mature. |

10

Table of Contents

In addition, any payment by that guarantor pursuant to its guarantee could be voided and required to be returned to the guarantor, or to a fund for the benefit of our creditors or the creditors of the guarantor.

The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, a guarantor would be considered insolvent if:

| • | the sum of its debts, including contingent liabilities, was greater than the fair saleable value of all of its assets; |

| • | if the present fair saleable value of its assets was less than the amount that would be required to pay its probable liability on its existing debts, including contingent liabilities, as they become absolute and mature; or |

| • | it could not pay its debts as they become due. |

On the basis of historical financial information, recent operating history and other factors, we believe that each guarantor, after giving effect to its guarantee of the notes, will not be insolvent, will not have unreasonably small capital for the business in which it is engaged and will not have incurred debts beyond its ability to pay such debts as they mature. We cannot assure you, however, as to what standard a court would apply in making these determinations or that a court would agree with our conclusions in this regard.

We may not have the funds necessary to finance the repurchase of the New Notes in connection with a change of control offer required by the indenture.

Upon the occurrence of a change of control, which is followed by a ratings decline within 90 days of the earlier of the change of control and public notice thereof, the indenture governing the notes will require us to make an offer to repurchase the notes at 101% of the principal amount thereof, plus accrued and unpaid interest (and liquidated damages, if any) to, but not including, the date of repurchase. However, it is possible that we will not have sufficient funds, or the ability to raise sufficient funds, at the time of the change of control to make the required repurchase of the New Notes. In addition, restrictions under our CQP Credit Facilities may not allow us to make a repurchase of the New Notes upon a change of control. If we could not refinance such credit facilities or otherwise obtain a waiver from the lenders thereunder, we would be prohibited from repurchasing the New Notes, which would constitute an event of default under the indenture. Because the definition of change of control under our CQP Credit Facilities will differ from that under the indenture that governs the New Notes, there may be a change of control and resulting default under our CQP Credit Facilities at a time when no change of control has occurred under the indenture. Please read “Description of Notes—Repurchase at the Option of Holders—Change of Control.”

Holders of the notes may not be able to determine when a change of control giving rise to their right to have the New Notes repurchased has occurred following a sale of “substantially all” of our assets.

The definition of change of control in the indenture governing the notes will include a phrase relating to the sale of “all or substantially all” of our assets. There is no precise established definition of the phrase “substantially all” under applicable law. Accordingly, the ability of a holder of New Notes to require us to repurchase its notes as a result of a sale of less than all our assets to another person may be uncertain.

Your right to receive payments under the New Notes will be effectively subordinated to indebtedness secured by our assets.

The New Notes will be effectively subordinated to any secured debt we may incur. In the event of a liquidation, dissolution, reorganization, bankruptcy or similar proceeding involving us or our subsidiaries, the assets which serve as collateral for such other debt will be available to satisfy the obligations under such secured debt before any payments are made on the New Notes.

If an active trading market does not develop for the New Notes you may not be able to resell them.

Currently, there is no trading market for the New Notes, and we cannot assure you that an active trading market will develop. If no active trading market develops, you may not be able to resell your notes at their fair market value or at all. Future trading prices of the New Notes will depend on many factors, including, among other things, our ability to effect the exchange offer, prevailing interest rates, our operating results and the market for similar securities. We do not intend to apply to list the New Notes on any securities exchange.

11

Table of Contents

The ratings of the New Notes may be lowered or withdrawn.

The ratings address the likelihood of timely payment of the scheduled interest and principal on each scheduled payment date. The ratings do not address the likelihood of payment of any overdue interest, premiums or any other amounts payable in respect of the New Notes or the timeliness of any accelerated principal payments coming due as the result of the occurrence of an event of default. A rating is not a recommendation to buy, sell or hold a note (or beneficial interests therein) and is subject to revision or withdrawal in the future by each rating agency.

Changes in our credit rating could adversely affect the market price or liquidity of the New Notes.

Credit rating agencies continually revise their ratings for the companies that they follow. Credit rating agencies also evaluate our industry as a whole and may change their credit ratings for us based on their overall view of our industry. We cannot be sure that credit rating agencies will maintain their initial ratings on the New Notes. A negative change in our ratings could have an adverse effect on the trading price or liquidity of the New Notes.

12

Table of Contents

The exchange offer is intended to satisfy our obligations under the registration rights agreement we entered into in connection with the private offering of the Old Notes. We will not receive any proceeds from the issuance of the New Notes in the exchange offer. In consideration for issuing the New Notes as contemplated in this prospectus, we will receive, in exchange, outstanding Old Notes in like principal amount. We will cancel all of the Old Notes surrendered in exchange for New Notes in the exchange offer. As a result, the issuance of the New Notes will not result in any increase or decrease in our indebtedness.

13

Table of Contents

DESCRIPTION OF OTHER INDEBTEDNESS

The following is a summary of our material outstanding indebtedness. It does not include all of the provisions of our material indebtedness, does not purport to be complete and is qualified in its entirety by reference to the provisions of the instruments and agreements described.

CQP Credit Facilities

In February 2016, we entered into the CQP Credit Facilities. The CQP Credit Facilities originally consisted of: (1) a $450 million CTPL tranche term loan that was used to prepay the $400 million term loan facility in February 2016, (2) an approximately $2.1 billion SPLNG tranche term loan that was used to repay and redeem in November 2016 the approximately $2.1 billion of the senior notes previously issued by SPLNG, (3) a $125 million facility that could be used to satisfy asix-month debt service reserve requirement and (4) a $115 million revolving credit facility that may be used for general business purposes. In September 2017 and September 2018, we issued the 2025 CQP Senior Notes and the Old Notes, respectively, and the net proceeds were used to prepay the outstanding term loans under the CQP Credit Facilities. As of March 31, 2019, only a $115 million revolving credit facility, which is currently undrawn, remains as part of the CQP Credit Facilities.

The CQP Credit Facilities mature on February 25, 2020. Any outstanding balance may be repaid, in whole or in part, at any time without premium or penalty, except for interest hedging and interest rate breakage costs. The CQP Credit Facilities contain conditions precedent for extensions of credit, as well as customary affirmative and negative covenants and limit our ability to make restricted payments, including distributions, to once per fiscal quarter as long as certain conditions are satisfied. Under the CQP Credit Facilities, we are required to hedge not less than 50% of the variable interest rate exposure on its projected aggregate outstanding balance, maintain a minimum debt service coverage ratio of at least 1.15x at the end of each fiscal quarter beginning March 31, 2019 and have a projected debt service coverage ratio of 1.55x in order to incur additional indebtedness to refinance a portion of the existing obligations.

The CQP Credit Facilities are unconditionally guaranteed by each of our subsidiaries other than (1) SPL and (2) certain of our subsidiaries owning other development projects, as well as certain other specified subsidiaries and members of the foregoing entities.

CQP Senior Notes

In September 2018, we issued an aggregate principal amount of $1.1 billion of the Old Notes. The existing $1.5 billion of the 2025 CQP Senior Notes and the Old Notes (collectively, the “CQP Senior Notes”) are jointly and severally guaranteed by the Subsidiary Guarantors. The CQP Senior Notes are governed by the indenture. The 2025 CQP Senior Notes are further governed by the First Supplemental Indenture and the Old Notes are further governed by the Second Supplemental Indenture. The indenture contains customary terms and events of default and certain covenants that, among other things, limit our ability and the ability of the Subsidiary Guarantors to incur liens and sell assets, enter into transactions with affiliates, enter into sale-leaseback transactions and consolidate, merge or sell, lease or otherwise dispose of all or substantially all of the applicable entity’s properties or assets.

At any time prior to October 1, 2020 for the 2025 CQP Senior Notes and October 1, 2021 for the Old Notes, we may redeem all or a part of the applicable CQP Senior Notes at a redemption price equal to 100% of the aggregate principal amount of the CQP Senior Notes redeemed, plus the “applicable premium” set forth in the respective supplemental indenture governing the CQP Senior Notes, plus accrued and unpaid interest, if any, to the date of redemption. In addition, at any time prior to October 1, 2020 for the 2025 CQP Senior Notes and October 1, 2021 for the Old Notes, we may redeem up to 35% of the aggregate principal amount of the CQP Senior Notes with an amount of cash not greater than the net cash proceeds from certain equity offerings at a redemption price equal to 105.250% of the aggregate principal amount of the 2025 CQP Senior Notes and 105.625% of the aggregate principal amount of the Old Notes redeemed, plus accrued and unpaid interest, if any, to the date of redemption. We also may at any time on or after October 1, 2020 through the maturity date of October 1, 2025 for the 2025 CQP Senior Notes and October 1, 2021 through the maturity date of October 1, 2026 for the Old Notes, redeem the CQP Senior Notes, in whole or in part, at the redemption prices set forth in the respective supplemental indenture governing the CQP Senior Notes.

The CQP Senior Notes are our senior obligations, ranking equally in right of payment with our other existing and future unsubordinated debt and senior to any of our future subordinated debt. After applying the proceeds from the Old Notes, the CQP Senior Notes became unsecured. In the event that the aggregate amount of our secured indebtedness and the secured indebtedness of the Subsidiary Guarantors (other than the CQP Senior Notes or any other series of notes issued under the indenture) outstanding at any one time exceeds the greater of (1) $1.5 billion and (2) 10% of net tangible assets, the CQP

14

Table of Contents

Senior Notes will be secured to the same extent as such obligations under the CQP Credit Facilities. The obligations under the CQP Credit Facilities are secured on a first-priority basis (subject to permitted encumbrances) with liens on (1) substantially all the existing and future tangible and intangible assets and our rights and the rights of the Subsidiary Guarantors and equity interests in the Subsidiary Guarantors (except, in each case, for certain excluded properties set forth in the CQP Credit Facilities) and (2) substantially all of the real property of SPLNG (except for excluded properties referenced in the CQP Credit Facilities). The liens securing the CQP Senior Notes, if applicable, will be shared equally and ratably (subject to permitted liens) with the holders of other senior secured obligations, which include the CQP Credit Facilities obligations and any future additional senior secured debt obligations.

SPL Working Capital Facility

In September 2015, SPL entered into a $1.2 billion working capital facility (the “SPL Working Capital Facility”), which is intended to be used for loans to SPL (“Working Capital Loans”), the issuance of letters of credit on behalf of SPL, as well as for swing line loans to SPL (“Swing Line Loans”), primarily for certain working capital requirements related to developing and placing into operation the Liquefaction Project. SPL may, from time to time, request increases in the commitments under the SPL Working Capital Facility of up to $760 million and, upon the completion of the debt financing of Train 6 of the Liquefaction Project, request an incremental increase in commitments of up to an additional $390 million. As of March 31, 2019 and December 31, 2018, SPL had $779 million and $775 million of available commitments and $421 million and $425 million aggregate amount of issued letters of credit under the SPL Working Capital Facility, respectively. SPL did not have any amounts outstanding under the SPL Working Capital Facility as of both March 31, 2019 and December 31, 2018.

The SPL Working Capital Facility matures on December 31, 2020, and the outstanding balance may be repaid, in whole or in part, at any time without premium or penalty upon three business days’ notice. Loans deemed made in connection with a draw upon a letter of credit have a term of up to one year. Swing Line Loans terminate upon the earliest of (1) the maturity date or earlier termination of the SPL Working Capital Facility, (2) the date 15 days after such Swing Line Loan is made and (3) the first borrowing date for a Working Capital Loan or Swing Line Loan occurring at least three business days following the date the Swing Line Loan is made. SPL is required to reduce the aggregate outstanding principal amount of all Working Capital Loans to zero for a period of five consecutive business days at least once each year.

The SPL Working Capital Facility contains conditions precedent for extensions of credit, as well as customary affirmative and negative covenants. The obligations of SPL under the SPL Working Capital Facility are secured by substantially all of the assets of SPL as well as all of the membership interests in SPL on apari passu basis with the SPL Senior Notes (as defined below).

SPL Senior Notes

SPL currently has the following senior notes (the “SPL Senior Notes”) outstanding:

| • | $2.0 billion of outstanding 5.625% Senior Secured Notes due 2021; |

| • | $1.0 billion of outstanding 6.25% Senior Secured Notes due 2022; |

| • | $1.5 billion of outstanding 5.625% Senior Secured Notes due 2023; |

| • | $2.0 billion of outstanding 5.75% Senior Secured Notes due 2024; |

| • | $2.0 billion of outstanding 5.625% Senior Secured Notes due 2025; |

| • | $1.5 billion of outstanding 5.875% Senior Secured Notes due 2026 (the “2026 SPL Senior Notes”); |

| • | $1.5 billion of outstanding 5.00% Senior Secured Notes due 2027 (the “2027 SPL Senior Notes”); |

| • | $1.35 billion of outstanding 4.200% Senior Secured Notes due 2028 (the “2028 SPL Senior Notes”); and |

| • | $800 million of outstanding 5.00% Senior Secured Notes due 2037 (the “2037 SPL Senior Notes”). |

The terms of the SPL Senior Notes (except for the 2037 SPL Senior Notes) are governed by a common indenture (the “SPL Indenture”) and the terms of the 2037 SPL Senior Notes are governed by a separate indenture (the “2037 SPL Senior Notes Indenture”). Both the SPL Indenture and the 2037 SPL Senior Notes Indenture contain customary terms and events of default and certain covenants that, among other things, limit SPL’s ability and the ability of SPL’s restricted subsidiaries to incur additional indebtedness or issue preferred stock, make certain investments or pay dividends or distributions on capital stock or subordinated indebtedness or purchase, redeem or retire capital stock, sell or transfer assets, including capital stock of SPL’s restricted subsidiaries, restrict dividends or other payments by restricted subsidiaries, incur liens, enter into transactions with affiliates, dissolve, liquidate, consolidate, merge, sell or lease all or substantially all of SPL’s assets and

15

Table of Contents

enter into certain LNG sales contracts. Subject to permitted liens, the SPL Senior Notes are secured on apari passu first-priority basis by a security interest in all of the membership interests in SPL and substantially all of SPL’s assets. SPL may not make any distributions until, among other requirements, deposits are made into debt service reserve accounts as required and a debt service coverage ratio test of 1.25:1.00 is satisfied. Semi-annual principal payments for the 2037 SPL Senior Notes are due on March 15 and September 15 of each year beginning September 15, 2025. Interest on the SPL Senior Notes is payable semi-annually in arrears.

At any time prior to three months before the respective dates of maturity for each series of the SPL Senior Notes (except for the 2026 SPL Senior Notes, 2027 SPL Senior Notes, 2028 SPL Senior Notes and 2037 SPL Senior Notes, in which case the time period is six months before the respective dates of maturity), SPL may redeem all or part of such series of the SPL Senior Notes at a redemption price equal to the “make-whole” price (except for the 2037 SPL Senior Notes, in which case the redemption price is equal to the “optional redemption” price) set forth in the respective indentures governing the SPL Senior Notes, plus accrued and unpaid interest, if any, to the date of redemption. SPL may also, at any time within three months of the respective maturity dates for each series of the SPL Senior Notes (except for the 2026 SPL Senior Notes, 2027 SPL Senior Notes, 2028 SPL Senior Notes and 2037 SPL Senior Notes, in which case the time period is within six months of the respective dates of maturity), redeem all or part of such series of the SPL Senior Notes at a redemption price equal to 100% of the principal amount of such series of the SPL Senior Notes to be redeemed, plus accrued and unpaid interest, if any, to the date of redemption.

16

Table of Contents

Purpose and Effect of the Exchange Offer

On September 11, 2018, we sold $1.1 billion aggregate principal amount of the Old Notes in a private placement. The Old Notes were sold to the initial purchasers who in turn resold the Old Notes to a limited number of qualified institutional buyers pursuant to Rule 144A of the Securities Act and to certainnon-U.S. persons within the meaning of Regulation S under the Securities Act.

In connection with the sale of the Old Notes, we entered into a registration rights agreement with the initial purchasers of the Old Notes, pursuant to which we agreed to file and to use our reasonable best efforts to cause to be declared effective by the SEC a registration statement with respect to the exchange of the Old Notes for the New Notes. We are making the exchange offer to fulfill our contractual obligations under that agreement. A copy of the registration rights agreement has been filed as an exhibit to the registration statement of which this prospectus is a part.

Pursuant to the exchange offer, we will issue the New Notes in exchange for the Old Notes. The terms of the New Notes are identical in all material respects to those of the Old Notes, except that the New Notes (1) have been registered under the Securities Act and therefore will not be subject to certain transfer restrictions applicable to the Old Notes and (2) will not have registration rights or provide for any liquidated damages related to the obligation to register. Please read “Description of Notes” for more information on the terms of the New Notes.

We are not making the exchange offer to, and will not accept tenders for exchange from, holders of Old Notes in any jurisdiction in which an exchange offer or the acceptance thereof would not be in compliance with the securities or blue sky laws of such jurisdiction. Unless the context requires otherwise, the term “holder” with respect to the exchange offer means any person in whose name the Old Notes are registered on our books or any other person who has obtained a properly completed bond power from the registered holder, or any person whose Old Notes are held of record by DTC, who desires to deliver such Old Notes by book-entry transfer at DTC.

We make no recommendation to the holders of Old Notes as to whether to tender or refrain from tendering all or any portion of their Old Notes pursuant to the exchange offer. In addition, no one has been authorized to make any such recommendation. Holders of Old Notes must make their own decision whether to tender pursuant to the exchange offer and, if so, the aggregate amount of Old Notes to tender after reading this prospectus and the letter of transmittal and consulting with their advisors, if any, based on their own financial position and requirements.

In order to participate in the exchange offer, you must represent to us, among other things, that:

| • | you are acquiring the New Notes in the exchange offer in the ordinary course of your business; |

| • | you do not have, and to your knowledge, no one receiving New Notes from you has, any arrangement or understanding with any person to participate in the distribution of the New Notes; |

| • | you are not one of our or our Subsidiary Guarantors’ “affiliates,” as defined in Rule 405 of the Securities Act; |

| • | you are not engaged in, and do not intend to engage in, a distribution of the New Notes; and |

| • | if you are a broker-dealer that will receive New Notes for your own account in exchange for Old Notes acquired as a result of market-making or other trading activities, you may be a statutory underwriter and will deliver a prospectus in connection with any resale of the New Notes. |

Please read “Plan of Distribution.”

Terms of Exchange

Upon the terms and conditions described in this prospectus and in the accompanying letter of transmittal, which together constitute the exchange offer, we will accept for exchange Old Notes that are properly tendered at or before the expiration time and not properly withdrawn as permitted below. As of the date of this prospectus, $1.1 billion aggregate principal amount of the Old Notes are outstanding. This prospectus, together with the letter of transmittal, is first being sent on or about the date on the cover page of the prospectus to all holders of Old Notes known to us. Old Notes tendered in the exchange offer must be in denominations of principal amount of $2,000 and any integral multiple of $1,000 in excess of $2,000.

17

Table of Contents

Our acceptance of the tender of Old Notes by a tendering holder will form a binding agreement between the tendering holder and us upon the terms and subject to the conditions provided in this prospectus and in the accompanying letter of transmittal.

The form and terms of the New Notes being issued in the exchange offer are the same as the form and terms of the Old Notes except that the New Notes being issued in the exchange offer:

| • | will have been registered under the Securities Act; |

| • | will not bear the restrictive legends restricting their transfer under the Securities Act; |

| • | will not contain the registration rights contained in the Old Notes; and |

| • | will not contain the liquidated damages provisions relating to the Old Notes. |

Expiration, Extension and Amendment

The expiration time of the exchange offer is 12:00 midnight, New York City time, at the end of July 26, 2019. However, we may, in our sole discretion, extend the period of time for which the exchange offer is open and set a later expiration date for the offer. The term “expiration time” as used herein means the latest time and date at which the exchange offer expires, after any extension by us (if applicable). If we decide to extend the exchange offer period, we will then delay acceptance of any Old Notes by giving oral or written notice of an extension to the holders of Old Notes as described below. During any extension period, all Old Notes previously tendered will remain subject to the exchange offer and may be accepted for exchange by us. Any Old Notes not accepted for exchange will be returned promptly to the tendering holder after the expiration or termination of the exchange offer.

Our obligation to accept Old Notes for exchange in the exchange offer is subject to the conditions described below under “—Conditions to the Exchange Offer.” We may decide to waive any of the conditions in our discretion. Furthermore, we reserve the right to amend or terminate the exchange offer, and not to accept for exchange any Old Notes not previously accepted for exchange, upon the occurrence of any of the conditions of the exchange offer specified below under the same heading. We will give oral or written notice of any extension, amendment,non-acceptance or termination to the holders of the Old Notes as promptly as practicable. If we amend the exchange offer in a manner that we determine to constitute a material change, we will promptly disclose such amendment by means of a prospectus supplement. The prospectus supplement will be distributed to the registered holders of the Old Notes. Depending upon the significance of the amendment and the manner of disclosure to the registered holders, we may extend the exchange offer. In the event of a material change in the exchange offer, including the waiver by us of a material condition, we will extend the exchange offer period, if necessary, so that at least five business days remain in the exchange offer period following notice of the material change. We will notify you of any extension by means of a press release or other public announcement no later than 9:00 a.m., New York City time, on the first business day after the previously scheduled expiration time.

Procedures for Tendering

Valid Tender

A tendering holder must, prior to the expiration time, transmit to The Bank of New York Mellon, the exchange agent, at the address listed below under the caption “—Exchange Agent”:

| • | a properly completed and duly executed letter of transmittal, including all other documents required by the letter of transmittal; or |

| • | if Old Notes are tendered in accordance with the book-entry procedures listed below, an agent’s message transmitted through DTC’s Automated Tender Offer Program, referred to as ATOP. |

We are not providing for guaranteed delivery procedures, and therefore you must allow sufficient time for the necessary tender procedures to be completed during normal business hours of DTC on or prior to the expiration time. If you hold your Old Notes through a broker, dealer, commercial bank, trust company or other nominee, you should consider that such entity may require you to take action with respect to the exchange offer a number of days before the expiration time in order for such entity to tender notes on your behalf on or prior to the expiration time. Tenders not completed on or prior to 12:00 midnight, New York City time, at the end of July 26, 2019 will be disregarded and of no effect.

18

Table of Contents

In addition, you must:

| • | deliver certificates, if any, for the Old Notes to the exchange agent at or before the expiration time; or |

| • | deliver a timely confirmation of the book-entry transfer of the Old Notes into the exchange agent’s account at DTC, the book-entry transfer facility, along with the letter of transmittal or an agent’s message. |

The term “agent’s message” means a message, transmitted by DTC to, and received by, the exchange agent and forming a part of a book-entry confirmation, that states that DTC has received an express acknowledgment that the tendering holder agrees to be bound by the letter of transmittal and that we may enforce the letter of transmittal against such holder.