As filed with the Securities and Exchange Commission on June 1, 2018

File No. [ ]

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

MONROE CAPITAL INCOME PLUS CORPORATION

(Exact name of registrant as specified in charter)

| Maryland | 83-0711022 | |

(State or other jurisdiction of incorporation or registration) | (I.R.S. Employer Identification No.) | |

311 South Wacker Drive, Suite 6400 Chicago, Illinois | 60606 | |

| (Address of principal executive offices) | (Zip Code) |

(312) 258-8300

(Registrant’s telephone number, including area code)

with copies to:

Theodore L. Koenig

Chief Executive Officer

311 South Wacker Drive, Suite 6400

Chicago, Illinois 60606

Steven B. Boehm

Stephani M. Hildebrandt

Eversheds Sutherland (US) LLP

700 Sixth Street, NW

Washington, DC 20001

(202) 383-0100

Securities to be registered pursuant to Section 12(b) of the Act:

None

Securities to be registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

(Title of class)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x (do not check if a smaller reporting company) | Smaller reporting company ¨ | |

Emerging growth companyx |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.¨

TABLE OF CONTENTS

Monroe Capital Income Plus Corporation is filing this registration statement on Form 10 (the “Registration Statement”) with the Securities and Exchange Commission (the “SEC”) under the Securities Exchange Act of 1934, as amended (the “1934 Act”), on a voluntary basis in order to permit it to file an election to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”), and to provide current public information to the investment community and to comply with applicable requirements in the event of future quotation or listing of its securities on a national securities exchange or other public trading market.

In this Registration Statement, except where the context suggests otherwise:

| • | the terms “we,” “us,” “our,” and “Company,” refer to Monroe Capital Income Plus Corporation; | ||

| • | the term “MCM Advisors” refers to Monroe Capital Management Advisors, LLC, a Delaware limited liability company, that will serve as our investment adviser and administrator; and | ||

| • | Monroe Capital refers to Monroe Capital LLC, a Delaware limited liability company, and its subsidiaries and affiliates. |

The Company is an emerging growth company as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and the Company will take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “1933 Act”).

This Registration Statement registers shares of the Company’s common stock (“Shares,” each a “Share”), par value $0.001 per share under the 1934 Act; however:

| • | the Company’s Shares may not be sold without the written consent of MCM Advisors; |

| • | the Shares are not currently listed on an exchange, and it is uncertain whether they will be listed or whether a secondary market will develop; and |

| • | an investment in the Company may not be suitable for investors who may need the money they invest in a specified time frame. |

Once this Registration Statement has been deemed effective, we will be subject to the requirements of Section 13(a) of the 1934 Act, including the rules and regulations promulgated thereunder, which will require us, among other things, to file annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and we will be required to comply with all other obligations of the 1934 Act applicable to issuers filing registration statements pursuant to Section 12(g) of the 1934 Act. We also will be subject to the proxy rules in Section 14 of the 1934 Act, and our directors, officers, and principal stockholders will be subject to the reporting requirements of Sections 13 and 16 of the 1934 Act.

| 1 |

This Registration Statement contains forward-looking statements that involve substantial risks and uncertainties. Such statements involve known and unknown risks, uncertainties and other factors and undue reliance should not be placed thereon. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about the Company, our current and prospective portfolio investments, our industry, our beliefs and opinions, and our assumptions. Words such as “anticipates,” “expects,” “intends,” “plans,” “will,” “may,” “continue,” “believes,” “seeks,” “estimates,” “would,” “could,” “should,” “targets,” “projects,” “outlook,” “potential,” “predicts” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements, including without limitation:

| • | our future operating results; |

| • | our business prospects and the prospects of our portfolio companies; |

| • | the dependence of our future success on the general economy and its impact on the industries in which we invest; |

| • | the impact of a protracted decline in the liquidity of credit markets on our business; |

| • | the impact of increased competition; |

| • | the impact of fluctuations in interest rates on our business and our portfolio companies; |

| • | our contractual arrangements and relationships with third parties; |

| • | the valuation of our investments in portfolio companies, particularly those having no liquid trading market; |

| • | actual and potential conflicts of interest with MCM Advisors and other affiliates of Monroe Capital; |

| • | the ability of our portfolio companies to achieve their objectives; |

| • | the use of borrowed money to finance a portion of our investments; |

| • | the adequacy of our financing sources and working capital; |

| • | the timing of cash flows, if any, from the operations of our portfolio companies; |

| • | the ability of MCM Advisors to locate suitable investments for us and to monitor and administer our investments; |

| • | the ability of MCM Advisors or its affiliates to attract and retain highly talented professionals; |

| • | our ability to qualify and maintain our qualification as a RIC and as a business development company; and |

| • | the impact of future legislation and regulation on our business and our portfolio companies. |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this Registration Statement should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in the section entitled “Item 1A. Risk Factors” and elsewhere in this Registration Statement. These forward-looking statements apply only as of the date of this Registration Statement. Moreover, we assume no duty and do not undertake to update the forward-looking statements. Because we are an investment company, the forward-looking statements and projections contained in this Registration Statement are excluded from the safe harbor protection provided by Section 21E of the 1934 Act.

| 2 |

(a)General Development of Business

We were formed on May 30, 2018 as a corporation under the laws of the State of Maryland. We are a specialty finance company organized to maximize the total return to our stockholders in the form of current income and capital appreciation through a variety of investments as described herein.

We intend to elect to be regulated as a BDC under the 1940 Act and intend to elect to be treated, and intend to qualify annually thereafter, as a regulated investment company (a “RIC”) under Subchapter M of the Code for U.S. federal income tax purposes. As a BDC and a RIC, we will be required to comply with certain regulatory requirements. See “Item 1(c). Description of Business — Regulation as a Business Development Company” and “Item 1(c). Description of Business — Certain U.S. Federal Income Tax Considerations.”

Subsequent to our election to be regulated as a BDC under the 1940 Act, we expect to conduct a best efforts, continuous private offering of our common stock to“accredited investors” as defined in Rule 501(a) of Regulation D promulgated under the Securities Act of 1933, as amended (the “1933 Act”) in reliance on exemptions from the registration requirements of the 1933 Act (the “Private Offering”). Each investor will make a capital commitment to purchase shares of our common stock pursuant to a subscription agreement entered into with us. See “Item 1(c). Description of Business — The Private Offering.”

(b)Financial Information about Industry Segments

Our operations comprise only a single reportable segment.

(c)Description of Business

The Company — Monroe Capital Income Plus Corporation

Our investment objective is to provide investors with attractive risk-adjusted returns with the downside protection associated with investing in asset-based and secured corporate private credit opportunities in a manner that is decoupled from public markets’ volatility. We will seek to provide attractive risk-adjusted returns and downside protection by investing primarily in secured private credit transactions and assets, targeting investments that have significant downside protection through a focus on asset coverage. We expect to invest primarily in: (i) senior and junior secured and unsecured loans, notes, bonds, preferred equity (including preferred partnership equity), convertible debt and other securities; (ii) unitranche loans and securities; (iii) asset-based loans and securities; (iv) small business loans and leases; (v) structured debt and structured equity; (vi) syndicated loans; (vii) securitized debt and subordinated notes of collateralized loan obligation (“CLO”) facilities, asset-backed securities and other securitized products and warehouse loan facilities (collectively, “Securitized Products”); (viii) opportunities to acquire illiquid investments from other third-party funds as a result of liquidity constraints resulting from investor redemptions and market dislocations; and (ix) capital investments in the secondary markets. We will not limit ourselves to any particular industry or geographic area when investing in qualifying assets (as defined in Section 55(a) of the 1940 Act and discussed in “—Regulation as a Business Development Company” below), which we expect to constitute at least 70% of our total assets. Subject to that requirement, we may also invest in issuers in the specialty finance, consumer finance, litigation finance, and commercial and residential real estate finance areas, as well as in secondary opportunities in pooled investment funds managed by a third-party investment adviser and private equity fund-level financing backed by the residual value of third-party private equity fund portfolio companies. We will seek to take advantage of the supply and demand gap in multiple segments of the private credit markets throughout an economic cycle.

We may also pursue out-of-favor sectors where we can acquire investments at a significant discount to the fundamental value of an issuer’s underlying assets, such as situations where an issuer has liquidity issues, limited refinancing choices, is under time pressure, or has a complicated or faulty capital structure; companies undergoing, or considered likely to undergo, reorganizations; and other pooled investment funds (which may be managed or advised by an affiliate of the Company) that are dedicated to investing in certain or all of the foregoing.

| 3 |

We have a broad and flexible investment program which allows for maximum flexibility to move quickly and efficiently on sectors and opportunities as economic conditions warrant. This adaptability should facilitate our efforts to seek out inefficiencies and mispricings in markets and in investment arenas in which there is a shortage of financing options. A key advantage for the Company is its ability to shift exposures as markets change and the economic cycle fluctuates, and to capitalize on attractive opportunities and strategies wherever and whatever they might be.

We generally intend to distribute, out of assets legally available for distribution, substantially all of our available earnings, on a quarterly basis, as determined by our Board of Directors (the “Board”) in its discretion.

Overall responsibility for the Company’s operations rests with the Board. The Board is responsible for overseeing MCM Advisors and other service providers in our operations in accordance with the provisions of the 1940 Act, applicable provisions of state and other laws and our articles of incorporation, which we refer to as our charter. The Board is currently composed of three members, two of whom are not “interested persons” of the Company or MCM Advisors as defined in the 1940 Act.

The Investment Adviser — Monroe Capital Management Advisors, LLC

Monroe Capital Management Advisors, LLC (“MCM Advisors”), a registered investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”) will serve as our investment adviser pursuant to an investment advisory agreement (the “Investment Advisory Agreement”) and our administrator pursuant to an administration agreement (the “Administration Agreement”). MCM Advisors is an affiliate of Monroe Capital, LLC (“Monroe Capital”), a leading U.S.-based private credit asset management firm with approximately $5.5 billion in assets under management as of April 1, 2018. Monroe Capital was founded in 2004 by Theodore Koenig, Michael Egan and Thomas Aronson and it is headquartered in Chicago, IL, with additional offices in Atlanta, GA; Boston, MA; Dallas, TX; Los Angeles, CA; Miami, FL; New York, NY; and San Francisco, CA. The senior management team of Monroe Capital has extensive direct origination expertise in the private credit space, and has invested, as a team at Monroe Capital, over $6.0 billion since 2004 across multiple vehicles and has engaged in over 250 directly originated secured loan transactions through March 31, 2018.

Monroe Capital has an investment team consisting of over 50 professionals as of April 1, 2018, which includes senior management, origination, portfolio management credit and underwriting teams. To support the investment team, as of April 1, 2018, Monroe Capital has over 40 professionals focused on finance, accounting, treasury, legal, compliance, loan operations, information technology, marketing, and investor relations.

As our investment adviser, MCM Advisors will be responsible for sourcing potential investments, conducting research and due diligence on prospective investments and their private equity sponsors, analyzing investment opportunities, structuring our investments and managing our investments and portfolio companies on an ongoing basis. Under the Investment Advisory Agreement, we will pay MCM Advisors a base management fee and an incentive fee for its services. See “Investment Advisory Agreement — Base Management Fee and — Incentive Fee” for a discussion of the base management fee and incentive fee payable by us to MCM Advisors. While not expected to review or approve each investment, our Board, including the independent directors, will periodically review MCM Advisors’ services and fees as well as its portfolio management decisions and portfolio performance. In connection with these reviews, our Board, including the independent directors, will consider whether our fees and expenses (including those related to leverage) remain appropriate.

Investment Committee

The investment committee of MCM Advisors for the Company is composed of Mr. Koenig, Aaron Peck and Michael Egan. The investment committee will also be advised by certain senior investment professionals of Monroe Capital from time to time. The investment committee has substantial experience in lending and investing through multiple economic cycles and intends to utilize the established asset management infrastructure and extensive direct lending relationships of MCM Advisors to generate proprietary private credit deal flow. We will employ a conviction-based approach when allocating capital within the portfolio. Rather than equally weighting each investment, factors such as perceived organizational risk, team risk, strategy risk and legal risk in comparison to the potential return and diversification benefits associated with a particular investment or strategy will heavily influence commitment amounts to each underlying transaction. In the event of downturns in the economic cycle, our investment strategy gives us the flexibility to shift investment allocations to areas with the highest risk adjusted return potential.

| 4 |

Theodore L. Koenig has served as our chairman of the Board, chief executive officer and president since our formation. Mr. Koenig has served as the chairman of the board of directors and chief executive officer of Monroe Capital Corporation (Nasdaq: MRCC), a publicly traded BDC, since February 2011 and as chairman of MCM Advisors’ investment committee since our initial public offering in October 2012. Additionally, Mr. Koenig is the chief executive officer and a manager of MCM Advisors. Since founding Monroe Capital in 2004, Mr. Koenig has served continuously as its President and Chief Executive Officer. Prior to founding Monroe Capital, Mr. Koenig served as the President and Chief Executive Officer of Hilco Capital LP from 1999 to 2004, where he invested in distressed debt, junior secured debt and unsecured subordinated debt transactions. From 1986 to 1999, Mr. Koenig was a partner with the Chicago-based corporate law firm, Holleb & Coff. Mr. Koenig is a past President of the Indiana University Kelley School of Business Alumni Club of Chicago. He currently serves as director of the Commercial Finance Association and is a member of the Turnaround Management Association and the Association for Corporate Growth. Mr. Koenig also serves on the Dean’s Advisory Council, Kelley School of Business; Board of Overseers, Chicago-Kent School of Law; and as Vice Chairman of the Board of Trustees of Allendale School, a non-profit residential and educational facility for emotionally troubled children in the greater Chicago area. He is also a Certified Public Accountant. Mr. Koenig received a bachelor of science in accounting, with high honors, from Indiana University and earned a juris doctor, with honors, from Chicago Kent College of Law. Aaron D. Peck has served as chief financial officer, chief investment officer and corporate secretary since our formation. Mr. Peck has also served as a member of the board of directors and as chief financial officer, chief investment officer and corporate secretary of Monroe Capital Corporation (Nasdaq: MRCC), a publicly traded BDC, and as a member of MCM Advisors’ investment committee since October 2012. Mr. Peck has been a managing director of Monroe Capital since September 2012, where he is responsible for portfolio management and strategic initiatives and co-leads Monroe Capital’s specialty financing lending practice. From 2002 to 2003 and from 2004 to June 2011, Mr. Peck worked in various capacities at Deerfield Capital Management LLC, including serving as its Co-Chief Investment Officer and as Managing Director of its Middle Market Lending Group. He also helped establish and served as chief portfolio manager for Deerfield Capital Corp. (f/k/a Deerfield Triarc Capital Corp.), a publicly-traded externally-managed specialty finance hybrid mortgage REIT. For Deerfield Capital Corp., Mr. Peck was the primary point of contact for institutional and retail investors, equity research analysts, investment bankers and lenders. Mr. Peck also served as a member of Deerfield Capital’s Executive Committee, Investment Committee and Risk Management Committee. From 2003 to 2004, Mr. Peck served as Senior Director of AEG Investors LLC and led the company’s efforts in acquiring distressed middle market loans. From 2001 to 2002, Mr. Peck was a senior research analyst at Black Diamond Capital Management LLC. Prior to that, Mr. Peck worked in leveraged credit at several investment firms including Salomon Smith Barney, Merrill Lynch, ESL Investments and Lehman Brothers. Mr. Peck received his bachelor of science in commerce from the University of Virginia, McIntire School of Commerce and received a master of business administration with honors from The University of Chicago, Graduate School of Business. Mr. Peck’s over 25 years of experience in public company management, capital markets, risk management and financial services gives the Board valuable industry knowledge, expertise and insight.

| 5 |

Mr. Egan serves as Executive Vice President, Chief Credit Officer and Chief Operating Officer of Monroe Capital where he is responsible for credit policies and procedures, portfolio and asset management operations. Mr. Egan has over 33 years of experience in commercial finance, credit administration banking, and distressed investing. Prior to Monroe Capital, Mr. Egan served as Executive Vice President and Chief Credit Officer of Hilco Capital from 1999 to 2004. Prior to Hilco Capital, Mr. Egan was with The CIT Group/Business Credit, Inc., for a ten-year period beginning in 1989, where he was Senior Vice President and Regional Manager for the Midwest U.S. Region responsible for all credit, new business and operational functions for the Midwest Region of the United States. Prior to the CIT Group, Mr. Egan was a commercial lending officer with The National Community Bank of New Jersey (now known as The Bank of New York) and a credit analyst with Key Corp, where he completed a formal management and credit training program. Mr. Egan earned a B.S. in Business Management from Ithaca College. He is also a graduate of the American Bankers Association Commercial Lending School at the University of Oklahoma. Mr. Egan is a member of the Turnaround Management Association, and served as the 2016 President of the Chicago/Midwest Chapter and on the Board of Trustees for the Global Chapter. He is also a member of the Commercial Finance Association.

Other Senior Investment Professionals of Monroe Capital

Thomas Aronson serves as a Managing Director, Head of Originations of Monroe Capital where he is responsible for leading all transaction sourcing efforts and structuring investments. Mr. Aronson has over 32 years of lending and credit experience. Prior to Monroe Capital, he served at Hilco Capital sourcing, structuring and underwriting debt transactions since 2002. Prior to Hilco Capital, he was Senior Vice President and Group Head in the Business Banking Group of Cole Taylor Bank, where he was responsible for asset-based lending, correspondent banking, public funds and a commercial lending division. Mr. Aronson also served for seven years as a commercial lender with American National Bank (now JP Morgan Chase Bank) and as Chief Financial Officer of Barton Chemical Corporation, a privately held consumer products company. Mr. Aronson earned his M.B.A. in Management Accounting from DePaul University and a B.S. in Finance and Marketing from Indiana University. He is a member of the Commercial Finance Association, the Turnaround Management Association, the Association for Corporate Growth and serves on the Board of Directors of the Midwest Small Business Investor Alliance.

Kyle Asher serves as a Director of Underwriting and Structuring for the Monroe Capital’s opportunistic private credit funds. He is responsible for assisting the Portfolio Managers in deal screening, structuring, pricing, negotiation and portfolio construction, as well as managing the underwriting resources for this investment strategy, and satisfying various requests of the Fund’s Investment Committee. Prior to Monroe, Mr. Asher was an Analyst with Chicago-based Calder Capital Partners, a direct and fund-of-funds private equity firm partly owned by Goldman Sachs and Ares Capital (formerly Allied Capital), where he performed due diligence on various direct and fund-of-fund investments, sourced transactions and assisted in capital raising. Prior to Calder, Mr. Asher was an Equity Analyst for MindShare Capital, an institutional money-manager where he focused on the valuation and trading patterns of small-cap growth companies. Mr. Asher earned his M.B.A. and his B.A. from Northwestern University.

Carey Davidson serves as Managing Director and Head of Capital Markets of Monroe Capital where she is responsible for buy side club originations, relationship management, and marketing as well as sell side syndications. Ms. Davidson has over 18 years of experience in middle market investing. Prior to Monroe, Ms. Davidson was a senior deal professional at The Carlyle Group’s middle market private debt platform, Carlyle GMS Finance, where she focused on originating, structuring, negotiating, executing and managing middle market loans. Prior to Carlyle, Ms. Davidson was a founding professional and Senior Vice President at Churchill Financial and an Assistant Vice President at GE Antares Capital. Ms. Davidson was recognized by Mergers & Acquisitions as one of 2017’s Most Influential Women in Mid-Market M&A. Ms. Davidson earned her M.B.A. from The University of Chicago Booth School of Business and a B.A. in Communications with a Certificate in Business from The University of Wisconsin – Madison.

Alex Franky serves as a Managing Director, Head of Direct Underwriting of Monroe Capital where he is responsible for investment structuring and investment execution. Mr. Franky has over 24 years of commercial lending experience. Prior to Monroe Capital, he served Hilco Capital LP in a similar capacity since 2002. He was also formerly Assistant Vice-President with GMAC Business Credit in which he was instrumental in structuring and underwriting financing transactions. Prior to GMAC, Mr. Franky was an Assistant Vice-President with FINOVA Capital Corp., where he assembled, negotiated, and closed corporate asset-based and structured finance transactions. Mr. Franky began his professional career at LaSalle Bank in its asset-based lending group, where he was a field examiner, managed portfolios, assisted in developing and structuring new business on middle market companies. Mr. Franky earned his B.S. in Accounting from University of Illinois at Chicago and his M.B.A. in Finance and International Business from Loyola University. He is a member of the Commercial Finance Association.

| 6 |

Cesar Gueikian serves as a co-Portfolio Manager of Monroe Capital’s opportunistic private credit funds. He has 18 years of experience in credit and structured financing, asset-based finance, leveraged finance, credit trading and has significant experience taking and managing risk in the private credit space. He was one of three founders of Melody Capital Partners, an alternative asset manager focused on private debt and secondary investing. Before Melody, Mr. Gueikian was employed by UBS from September 2009 until November 2012, serving in the role of Founder and Global Head of the Special Situations Group (“SSG”) managing 25 people in New York, London, Hong Kong and Tokyo. His responsibility for SSG comprised all structured and private lending. The group he created originated, structured and invested capital on a private basis, leveraging UBS’s ability to act as a principal investor deploying balance sheet. He was also Head of UBS Leveraged Finance Capital Markets (“LCM”) for EMEA starting in October 2010, managing an additional 12 people out of London. His responsibility for LCM included Leveraged Loans and High Yield Bonds across a variety of transaction structures, including acquisition and bridge financings, refinancings and recapitalizations, working primarily with private equity sponsors and their portfolio companies. He co-chaired the Global Investment Committee, was a member of the European Management Committee and a SIF (Significant Influence Function) delegate on behalf of UBS with the Financial Services Authority in London. He was among a select group of senior decision-makers identified as “Key Risk Taker” defined by UBS in its compensation report as individuals who can materially set, commit or control significant amounts of the firm’s resources and exert significant influence on its risk profile. Prior to UBS, Mr. Gueikian headed Illiquid Credit Trading for North America at Merrill Lynch. He began his career with Deutsche Bank’s Credit Trading and Global Principal Finance divisions in both London and New York, where he focused on credit analysis, corporate valuation, capital structure, waterfall and fundamental analysis. Mr. Gueikian earned his MBA from The University of Chicago with a concentration in Analytical Finance and Economics and a BA in Business from Universidad de San Andres, Buenos Aires, Argentina.

Zia Uddin serves as a Managing Director, Portfolio Manager of Monroe Capital’s Private Credit investment vehicles. He joined in 2007 and is a member of Monroe Capital’s investment committee. He is responsible for the private direct lending funds at Monroe Capital. He works extensively with sponsors (funds and private equity) and sits on various boards of directors for Monroe Capital’s investments. Mr. Uddin has over 25 years of management consulting, corporate finance, turnaround and investing experience. Prior to joining Monroe Capital, Mr. Uddin was a Partner and Principal with two middle market private equity funds. Prior to that role, he was a Senior Manager at Arthur Andersen LLP, where he provided management consulting services to a wide range of clients. Mr. Uddin has also had numerous operating roles at middle market companies including Chief Operating Officer, Chief Financial Officer and Chief Revenue Office. Mr. Uddin earned his M.B.A. from The University of Chicago Graduate School of Business and a B.S. from University of Illinois. He is a CFA charter holder and is a non-practicing CPA.

Jeremy VanDerMeid serves as a Managing Director, Portfolio Manager of Monroe Capital where he is responsible for managing the tradeable credit and CLO businesses, executing buy side transactions, and originating middle-market club transactions. Mr. VanDerMeid has over 20 years of credit, lending and corporate finance experience. Prior to Monroe Capital, Vice President for Morgan Stanley Investment Management in the Van Kampen Asset Management Group, where he managed a portfolio of bank loans and also led the firm’s initiative to increase its presence with middle market lenders and private equity firms. Prior to Morgan Stanley, Mr. VanDerMeid worked for Dymas Capital and Heller Financial where he originated, underwrote, and managed various middle-market debt transactions. Mr. VanDerMeid earned his M.B.A. from Northwestern University’s Kellogg School of Business and a B.B.A. from the University of Michigan’s Ross School of Business. Mr. VanDerMeid is a member of the Commercial Finance Association and the Turnaround Management Association.

Investment Advisory Agreement

The description below of the Investment Advisory Agreement is only a summary and is not necessarily complete. The description set forth below is qualified in its entirety by reference to the Investment Advisory Agreement filed as an exhibit to this Registration Statement.

Subject to the overall supervision of the Board and in accordance with the 1940 Act, MCM Advisors will manage our day-to-day operations and provide investment advisory services to us. Under the terms of the Investment Advisory Agreement, MCM Advisors:

| • | determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes; |

| 7 |

| • | assists us in determining what securities we purchase, retain or sell; |

| • | identifies, evaluates and negotiates the structure of the investments we make (including performing due diligence on our prospective portfolio companies); and |

| • | executes, closes, services and monitors the investments we make and does not cause a conflict of interest |

MCM Advisors’ services under the Investment Advisory Agreement are not exclusive, and it is free to furnish similar services to other entities so long as its services to us are not impaired.

Base Management Fee

The base management fee is payable quarterly in arrears. Prior to any future quotation or listing of the Company’s securities on a national securities exchange (an “Exchange Listing”) or any future quotation or listing of its securities on any other public trading market, the base management fee will be calculated at an annual rate of 1.50% of average total assets, which includes assets financed using leverage. Following an Exchange Listing, the base management fee will be calculated at an annual rate of 1.75% of average invested assets (calculated as total assets excluding cash).

Incentive Fee

The incentive fee will consist of two parts. The first part will be calculated and payable quarterly in arrears based on our pre-incentive fee net investment income for the preceding quarter. Pre-incentive fee net investment income means interest income, dividend income and any other income (including any other fees such as commitment, origination, structuring, diligence and consulting fees or other fees that we receive from portfolio companies but excluding fees for providing managerial assistance) accrued during the calendar quarter, minus operating expenses for the quarter (including the base management fee, any expenses payable under our administration agreement between an affiliate of Monroe Capital and MCM Advisors (the “Administration Agreement”) and any interest expense and dividends paid on any outstanding preferred stock, but excluding the incentive fee). Pre-incentive fee net investment income will include, in the case of investments with a deferred interest feature such as market discount, debt instruments with PIK interest, preferred stock with PIK dividends and zero-coupon securities, accrued income that we have not yet received in cash. MCM Advisors is not under any obligation to reimburse us for any part of the incentive fee it received that was based on accrued interest that we never actually receive.

Pre-incentive fee net investment income will not include any realized capital gains, realized capital losses or unrealized capital gains or losses. If any distributions from portfolio companies are characterized as a return of capital, such returns of capital would affect the capital gains incentive fee to the extent a gain or loss is realized. Because of the structure of the incentive fee, it is possible that we may pay an incentive fee in a quarter where we incur a loss. For example, if we receive pre-incentive fee net investment income in excess of the hurdle rate (as defined below) for a quarter, we will pay the applicable incentive fee even if we have incurred a loss in that quarter due to realized and unrealized capital losses.

Pre-incentive fee net investment income, expressed as a rate of return on the value of our net assets (defined as total assets less indebtedness and before taking into account any incentive fees payable during the period) at the end of the immediately preceding calendar quarter, is compared to a fixed “hurdle rate” of 1.50% per quarter (6% annually). If market interest rates rise, we may be able to invest our funds in debt instruments that provide for a higher return, which would increase our pre-incentive fee net investment income and make it easier for MCM Advisors to surpass the fixed hurdle rate and receive an incentive fee based on such net investment income.

We will pay MCM Advisors an incentive fee with respect to our pre-incentive fee net investment income in each calendar quarter as follows:

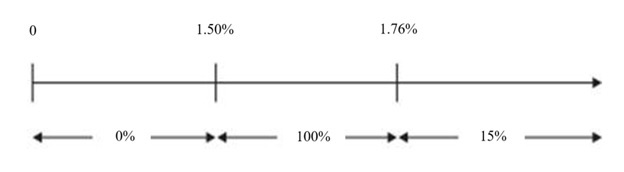

| • | no incentive fee in any calendar quarter in which the pre-incentive fee net investment income does not exceed the hurdle rate of 1.50% (6% annually); |

| 8 |

| • | 100% of our pre-incentive fee net investment income with respect to that portion of such pre-incentive fee net investment income, if any, that exceeds the hurdle rate but is less than 1.76% in any calendar quarter. We refer to this portion of our pre-incentive fee net investment income (which exceeds the hurdle rate but is less than 1.76%) as the “catch-up” provision. Prior to an Exchange Listing, the catch-up is meant to provide MCM Advisors with 15% of the pre-incentive fee net investment income as if a hurdle rate did not apply if this net investment income exceeds 1.76% in any calendar quarter, and following an Exchange Listing, the catch-up is meant to provide MCM Advisors with 20% of the pre-incentive fee net investment income as if a hurdle rate did not apply if this net investment income exceeds 1.88% in any calendar quarter; and |

| • | prior to an Exchange Listing, 15% of the amount of our pre-incentive fee net investment income, if any, that exceeds 1.76% in any calendar quarter, and following an Exchange Listing, 20% of the amount of our pre-incentive fee net investment income, if any, that exceeds 1.88% in any calendar quarter. |

The following is a graphical representation of the calculation of the income-related portion of the incentive fee:

Pre-incentive fee net investment income (expressed as a percentage of the value of net assets)

These calculations will be appropriately prorated for any period of less than three months and adjusted for any share issuances or repurchases during the current quarter.

The second part of the incentive fee is a capital gains incentive fee that will be determined and payable in arrears as of the end of each fiscal year (or upon termination of the investment advisory agreement, as of the termination date), and equals 15% of our realized capital gains as of the end of the fiscal year. In determining the capital gains incentive fee payable to MCM Advisors, we will calculate the cumulative aggregate realized capital gains and cumulative aggregate realized capital losses since our inception, and the aggregate unrealized capital depreciation as of the date of the calculation, as applicable, with respect to each of the investments in our portfolio. For this purpose, cumulative aggregate realized capital gains, if any, equals the sum of the differences between the net sales price of each investment, when sold, and the amortized cost of such investment. Cumulative aggregate realized capital losses equals the sum of the amounts by which the net sales price of each investment, when sold, is less than the amortized cost of such investment since our inception. Aggregate unrealized capital depreciation equals the sum of the difference, if negative, between the valuation of each investment as of the applicable calculation date and the amortized cost of such investment. At the end of the applicable year, the amount of capital gains that will serve as the basis for our calculation of the capital gains incentive fee equals the cumulative aggregate realized capital gains less cumulative aggregate realized capital losses, less aggregate unrealized capital depreciation, with respect to our portfolio of investments. If this number is positive at the end of such year, then the capital gains incentive fee for such year equals 15% of such amount, less the aggregate amount of any capital gains incentive fees paid in respect of our portfolio in all prior years.

| 9 |

Payment of Our Expenses

All investment professionals of MCM Advisors and/or its affiliates, when and to the extent engaged in providing investment advisory and management services to us, and the compensation and routine overhead expenses of personnel allocable to these services to us, will be provided and paid for by MCM Advisors and not by us. We will bear all other out-of-pocket costs and expenses of our operations and transactions, including, without limitation:

| • | organization and offering; |

| • | calculating our net asset value (including the cost and expenses of any independent valuation firm); |

| • | fees and expenses incurred by MCM Advisors payable to third parties, including agents, consultants or other advisors, in monitoring financial and legal affairs for us and in conducting research and due diligence on prospective investments and equity sponsors, analyzing investment opportunities, structuring our investment and monitoring our investments and portfolio companies on an ongoing basis (although none of MCM Advisors’ duties will be subcontracted to sub-advisors); |

| • | interest payable on debt, if any, incurred to finance our investments; |

| • | offerings of our common stock and other securities; |

| • | investment advisory fees; |

| • | administration fees and expenses, if any, payable under the Administration Agreement (including payments under the Administration Agreement between us and MCM Advisors, as our administrator, based upon our allocable portion of the MCM Advisors’ overhead in performing its obligations under the Administration Agreement, including rent and the allocable portion of the cost of our chief financial officer and chief compliance officer, and their respective staffs); |

| • | transfer agent, dividend agent and custodial fees and expenses; |

| • | federal and state registration fees; |

| • | all costs of registration and listing our shares on any securities exchange; |

| • | federal, state and local taxes; |

| • | independent directors’ fees and expenses; |

| • | costs of preparing and filing reports or other documents required by the SEC or other regulators; |

| • | costs of any reports, proxy statements or other notices to stockholders, including printing costs; |

| • | fidelity bond, directors and officers/errors and omissions liability insurance, and any other insurance premiums; |

| • | direct costs and expenses of administration, including printing, mailing, long distance telephone, copying, secretarial and other staff, independent auditors and outside legal costs; |

| • | proxy voting expenses; and |

| • | all other expenses incurred by us or MCM Advisors in connection with administering our business. |

Duration and Termination

Unless terminated earlier as described below, the Investment Advisory Agreement will remain in effect for a period of two years from the date it first becomes effective and will remain in effect from year-to-year thereafter if approved annually by the Board or by the affirmative vote of the holders of a majority of our outstanding voting securities and, in each case, a majority of our directors who are not “interested persons”.

| 10 |

The Investment Advisory Agreement will automatically terminate in the event of its assignment, as defined in the 1940 Act, by MCM Advisors and may be terminated by either party without penalty upon not less than 60 days’ written notice to the other. The holders of a majority of our outstanding voting securities may also terminate the Investment Advisory Agreement without penalty. See “Risk Factors — Risks Relating to Our Business and Structure — We depend upon MCM Advisors’ senior management for our success, and upon its access to the investment professionals of Monroe Capital and its affiliates” and “Risk Factors — Risks Relating to Our Business and Structure — MCM Advisors can resign on 60 days’ notice, and we may not be able to find a suitable replacement within that time, resulting in a disruption in our operations that could adversely affect our financial condition, business and results of operations.”

Indemnification

The Investment Advisory Agreement will provide that, absent willful misfeasance, bad faith or gross negligence in the performance of its duties or by reason of the reckless disregard of its duties and obligations, MCM Advisors and its affiliates’ respective officers, directors, members, managers, stockholders and employees are entitled to indemnification from us from and against any claims or liabilities, including reasonable legal fees and other expenses reasonably incurred, arising out of or in connection with our business and operations or any action taken or omitted on our behalf pursuant to authority granted by the Investment Advisory Agreement, except where attributable to gross negligence, willful misconduct, bad faith or reckless disregard of such person’s duties under the Investment Advisory Agreement.

Board Approval of the Investment Advisory Agreement

The Board will hold an in-person meeting to consider and approve the Investment Advisory Agreement and related matters. The Board will be provided the information it requires to consider the Investment Advisory Agreement, including: (a) the nature, quality and extent of the advisory and other services to be provided to us by MCM Advisors; (b) comparative data with respect to advisory fees or similar expenses paid by other BDCs with similar investment objectives; (c) our projected operating expenses and expense ratio compared to BDCs with similar investment objectives; (d) any existing and potential sources of indirect income to MCM Advisors from its relationship with us and the profitability of that relationship; (e) information about the services to be performed and the personnel performing such services under the Investment Advisory Agreement; (f) the organizational capability and financial condition of MCM Advisors and its affiliates; and (g) the possibility of obtaining similar services from other third-party service providers or through an internally managed structure.

The Board, including a majority of independent directors, will oversee and monitor the investment performance and, beginning with the second anniversary of the effective date of the Investment Advisory Agreement, will annually review the compensation we pay to MCM Advisors to determine that the provisions of the Investment Advisory Agreement are carried out.

Administration Agreement

The description below of the Administration Agreement is only a summary and is not necessarily complete. The description set forth below is qualified in its entirety by reference to the Administration Agreement filed as an exhibit to this Registration Statement.

Pursuant to an Administration Agreement, MCM Advisors will furnish us with office facilities and equipment and provide us clerical, bookkeeping and record keeping and other administrative services at such facilities. Under the Administration Agreement, MCM Advisors will perform, or oversee the performance of, our required administrative services, which include, among other things, being responsible for the financial records that we are required to maintain and preparing reports to our stockholders and reports filed with the SEC. MCM Advisors will also assist us in determining and publishing our net asset value, oversee the preparation and filing of our tax returns, print and disseminate reports to our stockholders and generally oversee the payment of our expenses and the performance of administrative and professional services rendered to us by others. Under the Administration Agreement, MCM Advisors will also provide managerial assistance on our behalf to those portfolio companies that have accepted our offer to provide such assistance.

| 11 |

MCM Advisors may retain third parties to assist in providing administrative services to us. To the extent that MCM Advisors outsources any of its functions, we pay the fees associated with such functions on a direct basis without profit to MCM Advisors. We reimburse MCM Advisors for the allocable portion (subject to the review and approval of our Board) of MCM Advisors’ overhead and other expenses incurred by it in performing its obligations under the Administration Agreement, including rent, the fees and expenses associated with performing its obligations under the Administration Agreement, and our allocable portion of the cost of our chief financial officer and chief compliance officer and their respective staffs. Unless terminated earlier as described below, the Administration Agreement will continue in effect from year to year with the approval of our Board. The Administration Agreement may be terminated by either party without penalty upon 60 days’ written notice to the other party.

License Agreement

We intend to enter into a license agreement with Monroe Capital under which Monroe Capital will agree to grant us a non-exclusive, royalty-free license to use the name “Monroe Capital.” Under this agreement, we will have a right to use the “Monroe Capital” name at no cost for so long as MC Advisors or one of its affiliates remains our investment advisor. Other than with respect to this limited license, we have no legal right to the “Monroe Capital” name. This license agreement will remain in effect for so long as the Investment Advisory Agreement with MC Advisors is in effect.

Employees

We do not have any internal employees. We depend on the diligence, skill and network of business contacts of the senior investment professionals of MCM Advisors to achieve our investment objective. MCM Advisors is an affiliate of Monroe Capital and depends upon access to the investment professionals and other resources of Monroe Capital and Monroe Capital’s affiliates to fulfill its obligations to us under the Investment Advisory Agreement. MCM Advisors also depends upon Monroe Capital to obtain access to deal flow generated by the professionals of Monroe Capital and its affiliates.

Fees and Expenses

The table below provides information about the Company’s estimated annual operating expenses during the following twelve (12) months, expressed as a percentage of average net assets attributable to common stock. The percentages indicated in the table below are estimates and may vary.

| Base Management Fee (1) | [ ] | % | ||

| Incentive Fee (2) | — | |||

| Interest Payments on Borrowed Funds (3) | [ ] | % | ||

| Other Expenses (4) | [ ] | % | ||

| Total Annual Expenses | [ ] | % |

| (1) | Amount assumes that we have $[ ] million of average invested assets during the following twelve (12) months. |

| (2) | For purposes of this chart, we have assumed that no incentive fee will be paid in the following twelve (12) months. |

| (3) | We may borrow funds from time to time to make investments to the extent we determine that it is appropriate to do so. The costs associated with any outstanding borrowings are indirectly borne by our investors. The table assumes borrowings of $[ ] million with a weighted average interest rate of [ ]% during the next twelve months. Although we do not have any current plans to issue debt securities or preferred stock in the next twelve months, we may issue debt securities or preferred stock, subject to our compliance with applicable requirements under the 1940 Act. |

| (4) | Other expenses include, but are not limited to, payments under the Administration Agreement based on our allocable portion of overhead and of expenses incurred by MCM Advisors, as our administrator, accounting, legal and auditing fees, as well as the reimbursement of the compensation of administrative personnel and fees payable to our directors who do not also serve in an executive officer capacity for us or Monroe Capital. The amount presented in the table reflects estimated amounts we expect to pay during the following twelve (12) months. |

| 12 |

Investment Strategy

We expect to invest primarily in: (i) senior and junior secured and unsecured loans, notes, bonds, preferred equity (including preferred partnership equity), convertible debt and other securities; (ii) unitranche loans and securities; (iii) asset-based loans and securities; (iv) small business loans and leases; (v) structured debt and structured equity; (vi) syndicated loans; (vii) securitized debt and subordinated notes of collateralized loan obligations (“CLO”) facilities, asset-backed securities and other securitized products and warehouse loan facilities (collectively, “Securitized Products”); (viii) opportunities to acquire illiquid investments from other third-party funds as a result of liquidity constraints resulting from investor redemptions and market dislocations; and (ix) capital investments in the secondary markets. We will not limit ourselves to any particular industry or geographic area when investing in qualifying assets (as defined in Section 55(a) of the 1940 Act and discussed in “—Regulation as a Business Development Company” below) which generally constitute at least 70% of our total assets. Subject to that requirement, we may also invest in issuers in the specialty finance, consumer finance, litigation finance, and commercial and residential real estate finance areas, as well as in secondary opportunities in pooled investment funds managed by a third-party investment adviser and private equity fund-level financing backed by the residual value of third-party private equity fund portfolio companies. We will seek to take advantage of the supply and demand gap in multiple segments of the private credit markets throughout an economic cycle.

We may also pursue out-of-favor sectors where we can acquire investments at a significant discount to the fundamental value of an issuer’s underlying assets, such as situations where an issuer has liquidity issues, limited refinancing choices, is under time pressure, or has a complicated or faulty capital structure; companies undergoing, or considered likely to undergo, reorganizations; and other pooled investment funds (which may be managed or advised by an affiliate of the Company) that are dedicated to investing in certain or all of the foregoing.

The Company will employ a conviction-based approach when allocating capital within its portfolio. Rather than equally weighting each investment, factors such as perceived organizational risk, team risk, strategy risk and legal risk in comparison to the potential return and diversification benefits associated with a particular investment or strategy will heavily influence commitment amounts to each underlying transaction. In the event of downturns in the economic cycle, the Company’s investment strategy gives the Company the flexibility to shift investment allocations to areas with the highest risk adjusted return potential.

Our investment strategy includes the following:

Protection of Capital: We intend to focus on the safety and protection of invested capital, which directly results from the underwriting process. Depending on the type of transaction, the loan may have structural protection by being collateralized and will typically have a lien on all of the borrower’s tangible and intangible assets, and a pledge of all company stock. Covenants will provide the ability for early intervention in the event of deteriorating financial performance of an underlying borrower. Other types of transactions will be protected by detailed analysis and on-going monitoring of collateral.

Conservative Structure: Depending on the type of transaction, loans are expected to have low leverage ratios, conservative loan-to-value and significant equity capital support. When applicable, loans will also have amortization and excess cash-flow recapture based on a conservative estimate of the borrower’s projected free cash-flow. Each transaction will be executed to provide the Company with the optimal structure for the specific industry.

Return Enhancement: Certain transactions, such as Corporate Loans (defined below), will allow the Company additional yield generation through warrants, equity co-investments, paid-in-kind (“PIK”) interest, success fees and prepayment fees.

| 13 |

Active Investor and Operating Approach to Value Creation:MCM Advisors has significant experience in sourcing, structuring, closing, managing and exiting investments. Prior to making an investment on behalf of the Company, MCM Advisors will conduct a comprehensive financial and operational underwriting process to determine the factors likely to impact ongoing performance by portfolio companies or a proposed restructuring or recapitalization process. This analysis will include the following:

| · | Due Diligence – MCM Advisors will utilize well-defined credit and underwriting criteria and proprietary investment management tools developed over the last 14 years. Standard due diligence items will include in-person meetings with senior management, company and asset owners, onsite corporate and asset visits, and detailed calls with key customers and suppliers. MCM Advisors may also utilize third-party firms to conduct quality of earnings analyses, special purpose accounting reviews, asset and enterprise value appraisals, management background checks on senior company management, field audits and business plan reviews. As part of this detailed process, MCM Advisors will utilize recognized and experienced vendors (such as external legal counsel, field examiners and asset appraisers) in order to promote consistency and efficiency. |

| · | Strategic Planning – MCM Advisors will be actively involved in identification, development and execution of various strategies for portfolio companies. |

| · | Executive Development – MCM Advisors will draw on its network of relationships to assist in the recruiting and developing the management of portfolio companies, as needed. |

| · | Capital Formation– MCM Advisors will draw on its relationships in the banking, finance, private equity, investment banking and capital markets to assist portfolio companies in capital sourcing, as needed. |

Investment Process Overview

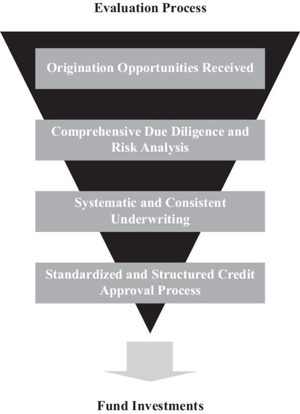

We view our investment process as consisting of four distinct phases described below:

Origination. MCM Advisors seeks to develop investment opportunities through extensive relationships with regional banks, private equity firms, financial intermediaries, management teams and other turn-around advisors. Monroe Capital has developed this network since its formation in 2004. MCM Advisors manages these leads through personal visits and calls by its senior deal professionals. It is these professionals’ responsibility to identify specific opportunities, refine opportunities through due diligence regarding the underlying facts and circumstances and utilize innovative thinking and flexible terms to solve the financing issues of prospective clients. Monroe Capital’s origination professionals are broadly dispersed throughout North America, with seven offices in the United States. Certain of Monroe Capital’s originators are responsible for covering a specified target market based on geography and others focus on specialized industry verticals. We believe MCM Advisors’ origination professionals’ experience is vital to enable us to provide our borrowers with innovative financing solutions. We further believe that their strength and breadth of relationships across a wide range of markets will generate numerous financing opportunities and enable us to be highly selective in our lending activities. In sourcing new transactions, MC Advisors seeks opportunities to work with borrowers domiciled in the United States and Canada and typically focuses on industries in which Monroe Capital has previous lending experience.

Due Diligence. For each of our investments, MCM Advisors prepares a comprehensive new business presentation, which summarizes the investment opportunity and its due diligence and risk analysis, all from the perspective of strengths, weaknesses, opportunities and threats presented by the opportunity. This presentation assesses the borrower and its management, including products and services offered, market position, sales and marketing capabilities and distribution channels; key contracts, customers and suppliers, meetings with management and facility tours; background checks on key executives; customer calls; and an evaluation of exit strategies. MCM Advisors’ presentation typically evaluates historical financial performance of the borrower and includes projections, including operating trends, an assessment of the quality of financial information, capitalization and liquidity measures and debt service capacity. The financial analysis also includes sensitivity analysis against management projections and an analysis of potential downside scenarios, particularly for cyclical businesses. MCM Advisors seeks to also review the dynamics of the borrowers’ industry and assess the maturity, market size, competition, technology and regulatory issues confronted by the industry. Finally, MCM Advisors’ new business presentation includes all relevant third-party reports and assessments, including, as applicable, analyses of the quality of earnings of the prospective borrower, a review of the business by industry experts and third-party valuations. In general, these analyses and reviews are more likely to be completed in agented or club deals in which MCM Advisors will have greater access to the borrower and its management team. MCM Advisors also includes in this due diligence, if relevant, field exams, collateral appraisals and environmental reviews, as well as a review of comparable private and public transactions.

| 14 |

Underwriting. MCM Advisors uses the systematic, consistent approach to credit evaluation developed in house by Monroe Capital with a particular focus on determining the value of a business in a downside scenario. In this process, the senior investment professionals at MCM Advisors bring to bear extensive lending experience with emphasis on lessons learned from the past two credit cycles. We believe that the extensive credit and debt work-out experience of Monroe Capital’s senior management enables us to anticipate problems and minimize risks. Monroe Capital’s underwriting professionals work closely with its origination professionals to identify individual deal strengths, risks and any risk mitigants. MCM Advisors preliminarily screens transactions based on cash flow, enterprise value and asset-based characteristics, and each of these measures is developed on a proprietary basis using thorough credit analysis focused on sustainability and predictability of cash flow to support enterprise value, barriers to entry, market position, competition, customer and supplier relationships, management strength, private equity sponsor track record and industry dynamics. For asset-based transactions, MCM Advisors seeks to understand current and future collateral value, opening availability and ongoing liquidity. MCM Advisors documents this analysis through a new business presentation thoroughly reviewed by at least one member of its investment committee prior to proposing a formal term sheet. We believe this early involvement of the investment committee ensures that our resources and those of third parties are deployed appropriately and efficiently during the investment process and lowers execution risk for our clients. With respect to transactions reviewed by MCM Advisors, we expect that only approximately 10% of our sourced deals will reach the formal term sheet stage.

Credit Approval/Investment Committee Review. MCM Advisors employs a standardized, structured process developed by Monroe Capital when evaluating and underwriting new investments for our portfolio. MCM Advisors’ investment committee considers its comprehensive new business presentation to approve or decline each investment. This committee includes Messrs. Koenig, Peck, and Egan. The committee is committed to providing a prompt turnaround on investment decisions. Each meeting to approve an investment requires a quorum of at least two members of the investment committee, and each investment must receive unanimous approval by such members of the investment committee.

| 15 |

The following chart illustrates the stages of MCM Advisors’ evaluation process:

Execution. We believe Monroe Capital has developed a strong reputation for closing deals as proposed, and we intend to continue this tradition. Through MCM Advisors’ consistent approach to credit evaluation and underwriting, we seek to close deals as fast or faster than competitive financing providers while maintaining the discipline with respect to credit, pricing and structure necessary to ensure the ultimate success of the financing. Upon completion of final documentation, a loan will typically be funded upon the initialing of the new business presentation and closing memo by our appropriate senior officers and confirmation of the flow of funds and wire transfer mechanics.

Monitoring. We benefit from the portfolio management system already in place at Monroe Capital. This monitoring includes meetings on at least a monthly basis between the responsible analyst and our portfolio company to discuss market activity and current events. MCM Advisors’ portfolio management staff closely monitors all credits, with senior portfolio managers covering agented and more complex investments. MCM Advisors segregates our capital markets investments by industry. MCM Advisors’ monitoring process and projections developed by Monroe Capital both have daily, weekly, monthly and quarterly components and related reports, each to evaluate performance against historical, budget and underwriting expectations. MCM Advisors’ analysts monitor performance using standard industry software tools to provide consistent disclosure of performance. MCM Advisors also monitors our investment exposure daily using a proprietary trend analysis tool. When necessary, MCM Advisors updates our internal risk ratings, borrowing base criteria and covenant compliance reports.

As part of the monitoring process, MCM Advisors regularly assesses the risk profile of each of our investments and rates each of them based on an internal proprietary system that uses the following categories, which we refer to as MCM Advisors’ investment performance rating. For any investment rated in grades 3, 4 or 5, MCM Advisors will increase its monitoring intensity and prepare regular updates for the investment committee, summarizing current operating results and material impending events and suggesting recommended actions. MCM Advisors monitors and, when appropriate, changes the investment ratings assigned to each investment in our portfolio. In connection with our valuation process, MCM Advisors reviews these investment ratings on a quarterly basis, and our board of directors reviews and affirms such ratings. A definition of the rating system follows:

| 16 |

| Investment Performance Risk Rating | Summary Description | |

| Grade 1 | Includes investments exhibiting the least amount of risk in our portfolio. The issuer is performing above expectations or the issuer’s operating trends and risk factors are generally positive. | |

| Grade 2 | Includes investments exhibiting an acceptable level of risk that is similar to the risk at the time of origination. The issuer is generally performing as expected or the risk factors are neutral to positive. | |

| Grade 3 | Includes investments performing below expectations and indicates that the investment’s risk has increased somewhat since origination. The issuer may be out of compliance with debt covenants; however, scheduled loan payments are generally not past due. | |

| Grade 4 | Includes an issuer performing materially below expectations and indicates that the issuer’s risk has increased materially since origination. In addition to the issuer being generally out of compliance with debt covenants, scheduled loan payments may be past due (but generally not more than six months past due). For grade 4 investments, we intend to increase monitoring of the issuer. | |

| Grade 5 | Indicates that the issuer is performing substantially below expectations and the investment risk has substantially increased since origination. Most or all of the debt covenants are out of compliance or payments are substantially delinquent. Investments graded 5 are not anticipated to be repaid in full, and we will reduce the fair market value of the loan to the amount we expect to recover. |

Our investment performance ratings do not constitute any ratings of investments by a nationally recognized statistical rating organization or represent or reflect any third-party assessment of any of our investments.

In the event of a delinquency or a decision to rate a loan grade 4 or grade 5, the applicable analyst, in consultation with a member of the investment committee, develops an action plan. Such a plan may require a meeting with the borrower’s management or the lender group to discuss reasons for the default and the steps management is undertaking to address the under-performance, as well as required amendments and waivers that may be required. In the event of a dramatic deterioration of a credit, MCM Advisors forms a team or engages outside advisors to analyze, evaluate and take further steps to preserve its value in the credit. In this regard, we would expect to explore all options, including in a private equity sponsored investment, assuming certain responsibilities for the private equity sponsor or a formal sale of the business with oversight of the sale process by us. Several of Monroe Capital’s professionals are experienced in running debt work-out transactions and bankruptcies.

Competition

We compete with a number of specialty and commercial finance companies to make the types of investments that we make in middle-market companies, including business development companies, traditional commercial banks, private investment funds, regional banking institutions, small business investment companies, investment banks and insurance companies. Additionally, with increased competition for investment opportunities, alternative investment vehicles such as hedge funds may invest in areas they have not traditionally invested in or from which they had withdrawn during the recent economic downturn, including investing in middle-market companies. As a result, competition for investments in lower middle-market companies has intensified, and we expect that trend to continue. Many of our existing and potential competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. For example, some competitors may have a lower cost of funds and access to funding sources that are not available to us. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more relationships than us.

| 17 |

We use the expertise of the investment professionals of MCM Advisors to assess investment risks and determine appropriate pricing and terms for investments in our loan portfolio. In addition, we expect that the relationships of the senior professionals of MCM Advisors will enable us to learn about, and compete effectively for, investment opportunities with attractive middle-market companies, independently or in conjunction with the private equity clients of MCM Advisors. For additional information concerning the competitive risks we face, see “Risk Factors — Risks Relating to Our Business and Structure — We operate in a highly competitive market for investment opportunities, which could reduce returns and result in losses.”

Managerial Assistance

As a BDC, we generally will offer, and must provide upon request, managerial assistance to our portfolio companies. This assistance could involve, among other things, monitoring the operations of our portfolio companies, participating in board and management meetings, consulting with and advising officers of portfolio companies and providing other organizational and financial guidance. We may also receive fees for these services.MCM Advisorswill provide, or arrange for the provision of, such managerial assistance on our behalf to portfolio companies that request this assistance, subject to reimbursement of any fees or expenses incurred on our behalf byMCM Advisorsin accordance with our Administration Agreement.

Emerging Growth Company

We are an emerging growth company as defined in the JOBS Act and we are eligible to take advantage of certain specified reduced disclosure and other requirements that are otherwise generally applicable to public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”). Although we have not made a determination whether to take advantage of any or all of these exemptions, we expect to remain an emerging growth company for up to five years following the completion of our IPO or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1.07 billion, (ii) December 31 of the fiscal year that we become a “large accelerated filer” as defined in Rule 12b-2 under the 1934 Act which would occur if the market value of our common stock that is held by non-affiliates exceeds $700.0 million as of the last business day of our most recently completed second fiscal quarter and we have been publicly reporting for at least 12 months or (iii) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the preceding three-year period. In addition, we will take advantage of the extended transition period provided in Section 7(a)(2)(B) of the 1933 Act for complying with new or revised accounting standards.

Dividend Reinvestment Plan

We intend to adopt a dividend reinvestment plan, pursuant to which we will reinvest all cash dividends declared by the Board on behalf of our stockholders who elect to receive cash. As a result, if the Board authorizes, and we declare, a cash dividend or other distribution, then our stockholders who have not opted out of our dividend reinvestment plan will have their cash distributions automatically reinvested in additional Shares as described below, rather than receiving the cash dividend or other distribution. Any fractional Share otherwise issuable to a participant in the dividend reinvestment plan will instead be paid in cash.

The number of shares to be issued to a stockholder under the dividend reinvestment plan will be determined by dividing the total dollar amount of the distribution payable to such stockholder by the net asset value per Share, as of the last day of our calendar quarter immediately preceding the date such distribution was declared. We intend to use newly issued Shares to implement the plan.

No action is required on the part of a registered stockholder to have his, her, or its dividend or other distribution reinvested in shares of our common stock. A registered stockholder is able to elect to have his, her, or its dividend received in cash by notifying MCM Advisors in writing so that such notice is received by MCM Advisors no later than ten days prior to the record date for distributions to the stockholders.

There are no brokerage charges or other charges to stockholders who participate in the plan.

| 18 |

The plan is terminable by us upon notice in writing mailed to each stockholder of record at least 30 days prior to any record date for the payment of any distribution by us.

Potential Liquidity Options

We intend to offer our stockholders the opportunity to participate in a liquidity event within three years after the date on which the Company first has invested assets of not less than $100 million (subject to two optional extensions of one year each as our Board may determine), or at such earlier time as ourBoardmay determine, taking into account market conditions and other factors. The liquidity event could include, among other options that the Board may determine: (i) a listing of our shares on a national securities exchange; (ii) a merger or another transaction approved by ourBoardin which our stockholders will receive cash or shares of a listed company; (iii) quarterly and upon six months prior written notice, optional redemption of up to 5% of any outstanding shares, (iv) a sale of all or substantially all of our assets either on a complete portfolio basis or individually to an unaffiliated third party or an affiliate followed by a liquidation or (v) an orderly wind down and/or liquidation of the Company.Because the 1940 Act prohibits affiliates from engaging in certain transactions, we will be required to obtain exemptive and/or no-action relief from the SEC to permit us to sell assets to an affiliate of the Company. There can be no assurance that we will be able to obtain such exemptive and/or no-action relief from the SEC. If we are unable to do so, then we will continue our operations in the manner otherwise set forth in this Registration Statement, including engaging in another liquidity option for our shareholders. Alternatively, if we do obtain such exemptive and/or no-action relief, our Board would determine whether (and when) to effectuate such a sale of assets to an affiliate or another liquidity option.There can be no assurance that we will complete a liquidity event within this timeframe or at all. As a result, an investment in our shares is not suitable if you require short-term liquidity with respect to your investment in us.

The Private Offering