UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

----------------------------------------------------------------

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23354

----------------------------------------------------------------

CPG VINTAGE ACCESS FUND II, LLC

(Exact name of registrant as specified in charter)

----------------------------------------------------------------

125 W. 55th Street

New York, New York 10019

(Address of principal executive offices) (Zip code)

Mitchell A. Tanzman

c/o Central Park Advisers, LLC

125 W. 55th Street

New York, New York 10019

(Name and address of agent for service)

----------------------------------------------------------------

Registrant’s telephone number, including area code: (212) 317-9200

Date of fiscal year end: March 31

Date of reporting period: March 31, 2024

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

(a) The Report to Shareholders is attached herewith.

CPG Vintage Access Fund II, LLC

Consolidated Financial Statements

For the Year Ended March 31, 2024

With Report of Independent Registered Public Accounting Firm

CPG Vintage Access Fund II, LLC Table of Contents For the Year Ended March 31, 2024 |

CPG Vintage Access Fund II, LLC Report of Independent Registered Public Accounting Firm March 31, 2024 |

To the Board of Directors and Unitholders of CPG Vintage Access Fund II, LLC

Opinion on the Financial Statements

We have audited the accompanying consolidated statement of assets and liabilities, including the consolidated schedule of investments, of CPG Vintage Access Fund II, LLC and its subsidiaries (collectively referred to as the “Fund”) as of March 31, 2024, the related consolidated statements of operations and cash flows for the year ended March 31, 2024, the consolidated statement of changes in net assets for the year ended March 31, 2024, the statement of changes in net assets for the year ended March 31, 2023, including the related notes, the consolidated financial highlights for the year ended March 31, 2024 and the financial highlights for each of the two years in the period ended March 31, 2023 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of March 31, 2024, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period ended March 31, 2024 and the financial highlights for each of the three years in the period ended March 31, 2024 in conformity with accounting principles generally accepted in the United States of America.

The financial statements of the Fund as of and for the year ended March 31, 2021 and the financial highlights for each of the periods ended on or prior to March 31, 2021 (not presented herein, other than the financial highlights) were audited by other auditors whose report dated May 28, 2021 expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of March 31, 2024 by correspondence with the investee funds; when replies were not received from investee funds, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

/s/ PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

May 31, 2024

We have served as the auditor of one or more Central Park Group investment companies since 2022.

1

CPG Vintage Access Fund II, LLC Consolidated Schedule of Investments March 31, 2024 |

Investments in Private Investment Funds — 104.48%^ | | Original Acquisition Date | | Cost | | Fair

Value |

Asia/Pacific — 8.0% | | | | | | | | | |

Buyout — 8.0% | | | | | | | | | |

North Haven Private Equity Asia V, L.P.a,c | | 12/1/2018 | | $ | 16,689,037 | | $ | 18,581,790 | |

Total Asia/Pacific | | | 16,689,037 | | | 18,581,790 | |

| | | | | | | | | | |

Global — 17.47% | | | | | | | | | |

Buyout — 9.37% | | | | | | | | | |

Adams Street - PE Co-Inv (SI) Fund L.P.a,b,c | | 12/1/2019 | | | 16,416,000 | | | 21,775,719 | |

| | | | | | | | | | |

Credit — 8.1% | | | | | | | | | |

The Varde Fund XIII (A) (Feeder), L.P.a,b,c | | 11/1/2019 | | | 14,086,972 | | | 18,818,917 | |

Total Global | | | 30,502,972 | | | 40,594,636 | |

| | | | | | | | | | |

North America — 79.01% | | | | | | | | | |

Buyout — 35.3% | | | | | | | | | |

Elliott Intermediate Co-Investment II L.P.a,c | | 8/1/2019 | | | 10,934,001 | | | 9,019,893 | |

HarbourVest Partners Co-Investment Fund V L.P.a,b,c | | 7/1/2019 | | | 13,596,336 | | | 25,035,679 | |

NB Select Opportunities Fund II LPa,c,d | | 12/1/2018 | | | 8,497,024 | | | 22,167,712 | |

North Haven Capital Partners VII L.P.a,c,e | | 8/1/2020 | | | 16,955,546 | | | 25,823,230 | |

Total Buyout | | | 49,982,907 | | | 82,046,514 | |

| | | | | | | | | | |

Credit — 23.84% | | | | | | | | | |

CVC Credit Partners Global Special Situations Fund IIa,c | | 12/1/2018 | | | 14,539,532 | | | 18,846,392 | |

Medalist Partners Opportunity Fund II Offshore Feeder, L.P.a | | 3/1/2019 | | | 10,912,132 | | | 15,181,066 | |

Oaktree Special Situations Fund II, L.P.a,b,c | | 2/1/2019 | | | 10,138,080 | | | 21,384,546 | |

Total Credit | | | 35,589,744 | | | 55,412,004 | |

| | | | | | | | | | |

Growth — 19.87% | | | | | | | | | |

Blue Owl Healthcare Opportunities III L.P.a,c | | 9/4/2019 | | | 12,194,555 | | | 10,223,634 | |

EW Healthcare Partners Fund 2, L.P.a,b,c | | 7/24/2019 | | | 12,258,518 | | | 11,856,775 | |

KKR Next Generation Technology Growth Fund IIa,c | | 6/1/2019 | | | 17,853,752 | | | 24,104,395 | |

Total Growth | | | 42,306,825 | | | 46,184,804 | |

Total North America | | | 127,879,476 | | | 183,643,322 | |

Total Private Investment Funds | | $ | 175,071,485 | | $ | 242,819,748 | |

| | | | | | | | | | |

Short-Term Investments — 0.8% | | | | | | | | | |

Money Market Funds: | | | | | | | | | |

UMB Bank, Money Market Special II Deposit Investment, 4.78%ᶠ

(Principal amount $1,864,798) | | $ | 1,864,798 | | $ | 1,864,798 | |

Total Short-Term Investments: | | $ | 1,864,798 | | $ | 1,864,798 | |

| | | | | | | | | | |

Total Investments — 105.28% | | | 176,936,283 | | | 244,684,546 | |

Liabilities in excess of other assets — (5.28%) | | | (12,268,034 | ) |

Net Assets — 100% | | $ | 232,416,512 | |

2

CPG Vintage Access Fund II, LLC Consolidated Schedule of Investments (Continued) March 31, 2024 |

3

CPG Vintage Access Fund II, LLC Consolidated Schedule of Investments (Continued) March 31, 2024 |

Summary of Investments by Type/Region (as a percentage of net assets) | | |

Investments in Private Investment Funds | | | |

Asia/Pacific | | 8.00 | % |

Global | | 17.47 | % |

North America | | 79.01 | % |

Total Private Investment Funds | | 104.48 | % |

Short-Term Investments | | | |

Money Market Funds | | 0.80 | % |

Total Investments | | 105.28 | % |

Liabilities in excess of other assets | | (5.28 | )% |

Total Net Assets | | 100.00 | % |

See accompanying Notes to Consolidated Financial Statements.

4

CPG Vintage Access Fund II, LLC Consolidated Statement of Assets and Liabilities March 31, 2024 |

Assets | | | |

Investments at fair value (cost $176,936,283) | | $ | 244,684,546 |

Cash | | | 948 |

Interest receivable | | | 12,253 |

Capital contributions receivable | | | 8,570 |

Prepaid expenses and other assets | | | 52,660 |

Total Assets | | | 244,758,977 |

| | | | |

Liabilities | | | |

Deferred tax liability payable | | | 8,174,157 |

Payable for contributions to Investment Funds, not yet settled | | | 2,356,316 |

Distribution and servicing fees payable | | | 1,108,536 |

Payable to Adviser | | | 363,582 |

Income tax payable | | | 172,528 |

Professional fees payable | | | 122,587 |

Line of credit fees payable | | | 20,481 |

Accounting and administration fees payable | | | 7,500 |

Other liabilities | | | 16,778 |

Total liabilities | | | 12,342,465 |

Net Assets | | $ | 232,416,512 |

| | | | |

Commitments and Contingencies (see Notes 3 and 7) | | | |

| | | | |

Composition of Net Assets | | | |

Paid-in capital | | $ | 184,871,682 |

Make-up fee | | | 1,535,630 |

Total distributable earnings | | | 46,009,200 |

Net Assets | | $ | 232,416,512 |

| | | | |

Units of Limited Liability Company Interests Outstanding (unlimited number of units authorized) | | | 18,052,848 |

Net Asset Value per Unit | | $ | 12.87 |

See accompanying Notes to Consolidated Financial Statements.

5

CPG Vintage Access Fund II, LLC Consolidated Statement of Operations For the Year Ended March 31, 2024 |

Investment Income | | | | |

Income from Investment Funds | | $ | 253,670 | |

Interest income | | | 240,980 | |

Total Investment Income | | | 494,650 | |

| | | | | |

Expenses | | | | |

Distribution and servicing fees | | | 1,678,726 | |

Management fees | | | 1,454,896 | |

Accounting and administration fees | | | 494,010 | |

Professional fees | | | 213,662 | |

Income tax expense | | | 172,528 | |

Line of credit fees | | | 119,558 | |

Directors’ and Officer fees | | | 102,909 | |

Interest expense | | | 81,585 | |

Other expenses | | | 88,617 | |

Total Expenses | | | 4,406,491 | |

| | | | | |

Net Investment Loss | | | (3,911,841 | ) |

| | | | | |

Net Realized Gain and Change in Unrealized Appreciation on Investments | | | | |

Net realized gain distributions received from Investment Funds | | | 7,472,496 | |

Net change in unrealized appreciation on Investment Funds | | | 15,481,394 | |

Net change on deferred tax | | | (8,174,157 | ) |

Net Realized Gain and Change in Unrealized Appreciation on Investments | | | 14,779,733 | |

Net Increase in Net Assets Resulting from Operations | | $ | 10,867,892 | |

See accompanying Notes to Consolidated Financial Statements.

6

CPG Vintage Access Fund II, LLC Consolidated Statements of Changes in Net Assets |

| | Year Ended

March 31, 2024 | | Year Ended

March 31, 2023^ |

Changes in Net Assets Resulting from Operations | | | | | | | | |

Net investment loss | | $ | (3,911,841 | ) | | $ | (3,998,518 | ) |

Net realized gain distributions received from Investment Funds | | | 7,472,496 | | | | 5,572,498 | |

Net change in unrealized appreciation/(depreciation) on Investment Funds, net of deferred tax | | | 7,307,237 | | | | (681,257 | ) |

Net Change in Net Assets Resulting from Operations | | | 10,867,892 | | | | 892,723 | |

| | | | | | | | | |

Distributions to unit holders | | | | | | | | |

Distributions | | | (9,921,845 | ) | | | (24,885,788 | ) |

Net Change in Net Assets from Distributions | | | (9,921,845 | ) | | | (24,885,788 | ) |

| | | | | | | | | |

Change in Net Assets Resulting from Capital Transactions | | | | | | | | |

Capital contributions | | | 15,661,988 | | | | 26,854,622 | |

Capital withdrawals | | | (45,965 | ) | | | — | |

Net Change in Net Assets Resulting from Capital Transactions | | | 15,616,023 | | | | 26,854,622 | |

| | | | | | | | | |

Total Net Increase in Net Assets | | | 16,562,070 | | | | 2,861,557 | |

| | | | | | | | | |

Net Assets | | | | | | | | |

Beginning of year | | | 215,854,442 | | | | 212,992,885 | |

End of year | | $ | 232,416,512 | | | $ | 215,854,442 | |

| | | | | | | | | |

Units Transactions | | | | | | | | |

Units sold | | | 1,176,820 | | | | 2,219,146 | |

Units redeemed | | | (3,397 | ) | | | — | |

Net change in units | | | 1,173,423 | | | | 2,219,146 | |

See accompanying Notes to Consolidated Financial Statements.

7

CPG Vintage Access Fund II, LLC Consolidated Statement of Cash Flows For the Year Ended March 31, 2024 |

Cash Flows from Operating Activities | | | | |

Net increase in net assets resulting from operations | | $ | 10,867,892 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | | | | |

Net realized gain distributions received from Investment funds | | | (7,472,496 | ) |

Net change in unrealized appreciation on Investment Funds | | | (15,481,394 | ) |

Capital called by Investment Funds | | | (18,394,996 | ) |

Capital distributions received from Investment Funds | | | 20,507,665 | |

Purchases of short-term investments, net | | | (1,864,798 | ) |

Decrease/(Increase) in Assets: | | | | |

Interest receivable | | | (12,253 | ) |

Prepaid expenses and other assets | | | 397 | |

Increase/(Decrease) in Liabilities: | | | | |

Deferred tax liability payable | | | 8,174,157 | |

Payable to Adviser | | | (364,150 | ) |

Income tax payable | | | 172,528 | |

Directors and Officers fees payable | | | (14,378 | ) |

Line of credit fees payable | | | (99,719 | ) |

Distribution and servicing fee payable | | | (13,930 | ) |

Professional fees payable | | | 32,945 | |

Accounting and administration fees payable | | | 6,534 | |

Payable for contributions to Investment Funds, not yet settled | | | 1,546,316 | |

Other liabilities | | | 6,257 | |

Net Cash Used In Operating Activities | | | (2,403,423 | ) |

| | | | | |

Cash Flows from Financing Activities: | | | | |

Payments for line of credit | | | (9,100,000 | ) |

Borrowings from line of credit | | | 4,000,000 | |

Proceeds from capital contributions, net of change in contribution receivable | | | 15,710,918 | |

Capital withdrawals | | | (45,965 | ) |

Distributions to unit holders, net of distributions to unit holders payable | | | (9,932,983 | ) |

Net cash provided by financing activities | | | 631,970 | |

| | | | | |

Net change in cash | | | (1,771,453 | ) |

Cash at beginning of year | | | 1,772,401 | |

Cash at end of year | | $ | 948 | |

| | | | | |

Supplemental disclosure of interest expense paid | | $ | 81,585 | |

See accompanying Notes to Consolidated Financial Statements.

8

CPG Vintage Access Fund II, LLC Consolidated Financial Highlights |

| | For the

Year Ended

March 31, 2024 | | For the

Year Ended

March 31, 2023^ | | For the

Year Ended

March 31, 2022^ | | For the

Year Ended

March 31, 2021^ | | For the

Year Ended

March 31, 2020^ |

Per unit operating performances: | | | | | | | | | | | | | | | | | | | |

Net asset value per unit, beginning of period | | $ | 12.79 | | | $ | 14.53 | | | $ | 11.69 | | | $ | 8.41 | | $ | 9.52 | |

Activity from investment operations:(1) | | | | | | | | | | | | | | | | | | | |

Net investment gain/(loss) | | | (0.08 | ) | | | 0.16 | | | | 0.15 | | | | 0.02 | | | (0.08 | ) |

Net realized and unrealized gain/(loss) on investments | | | 0.71 | | | | (0.21 | ) | | | 3.67 | | | | 3.26 | | | (1.35 | ) |

Total from investment operations | | | 0.63 | | | | (0.05 | ) | | | 3.82 | | | | 3.28 | | | (1.43 | ) |

| | | | | | | | | | | | | | | | | | | | |

Activity from capital transactions | | | | | | | | | | | | | | | | | | | |

Distributions to unit holders from net realized gains | | | (0.55 | ) | | | (1.69 | ) | | | (0.98 | ) | | | 0.00 | | | 0.00 | |

Proceeds from make-up fees | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | 0.32 | |

| | | | (0.55 | ) | | | (1.69 | ) | | | (0.98 | ) | | | 0.00 | | | 0.32 | |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, end of period | | $ | 12.87 | | | $ | 12.79 | | | $ | 14.53 | | | $ | 11.69 | | $ | 8.41 | |

| | | | | | | | | | | | | | | | | | | | |

Net Assets, end of period (in thousands) | | $ | 232,417 | | | $ | 215,854 | | | $ | 212,993 | | | $ | 136,096 | | $ | 59,572 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | |

Net investment loss(2) | | | (1.70)% | | | | (1.91)% | | | | (2.25)% | | | | (4.56)% | | | (6.92)% | |

Net loss excluding line of credit related expenses(2) | | | (1.66)% | | | | (1.84)% | | | | (2.03)% | | | | (4.21)% | | | (6.78)% | |

| | | | | | | | | | | | | | | | | | | | |

Total Expenses(2) | | | 1.92% | | | | 2.02% | | | | 2.59% | | | | 5.11% | | | 7.14% | |

Total Expenses excluding line of credit related expenses(2) | | | 1.88% | | | | 1.95% | | | | 2.37% | | | | 4.76% | | | 7.00% | |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover | | | 0.00% | | | | 0.00% | | | | 0.00% | | | | 0.00% | | | 0.00% | |

Total return(3) | | | 4.93% | | | | 0.38% | | | | 31.79% | | | | 39.00% | | | (11.66)% | |

| | | | | | | | | | | | | | | | | | | | |

Line of Credit: | | | | | | | | | | | | | | | | | | | |

Aggregate principal amount, end of period (000s) | | $ | — | | | $ | 5,100 | | | $ | — | | | $ | 3,800 | | $ | 15,000 | |

Average borrowings outstanding during the period (000s) | | $ | 5,255 | | | $ | 4,402 | | | $ | 12,856 | | | $ | 10,218 | | $ | 7,375 | (4) |

Asset coverage, end of period per $1,000(5) | | $ | — | | | $ | 43,324 | | | $ | — | | | $ | 36,815 | | $ | 3 | |

See accompanying Notes to Consolidated Financial Statements.

9

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements March 31, 2024 |

1. ORGANIZATION

CPG Vintage Access Fund II, LLC (the “Fund”) was organized as a Delaware limited liability company on May 31, 2018. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”) as a closed-end, non-diversified management investment company. The Fund commenced operations on November 9, 2018. CPG VA Acquisition Fund II, LLC and CPG VA Acquisition Fund II No. 2, LLC (“CPG VA Acquisition Fund II” and “CPG VA Acquisition Fund II No. 2”, respectively, and collectively the “Subsidiaries”), wholly owned subsidiaries of the Fund, are consolidated in the Fund’s consolidated financial statements. The Fund’s investment adviser is Central Park Advisers, LLC (the “Adviser”), a Delaware limited liability company registered under the Investment Advisers Act of 1940, as amended. The Fund’s investment objective is to seek long-term attractive risk adjusted returns. The Fund seeks to achieve its investment objective principally by making primary investments in a portfolio of institutional private equity, venture and private debt investment funds managed or sponsored by various asset management firms unaffiliated with the Adviser (the “Investment Funds”) that were represented on the Morgan Stanley Smith Barney LLC (“Morgan Stanley”) platform during the Fund’s vintage period. Morgan Stanley is not a sponsor, promoter, adviser, or affiliate of the Fund.

Subject to the requirements of the 1940 Act, the business and affairs of the Fund shall be managed under the direction of the Fund’s Board of Directors (the “Board,” with an individual member referred to as a “Director”). The Board shall have the right, power and authority, on behalf of the Fund and in its name, to do all things necessary and proper to carry out its duties under the Fund’s Limited Liability Company Agreement (the “LLC Agreement”), as amended and restated from time to time. Each Director shall be vested with the same powers, authority and responsibilities on behalf of the Fund as are customarily vested in each director of a closed-end management investment company registered under the 1940 Act that is organized under Delaware law. No Director shall have the authority individually to act on behalf of or to bind the Fund except within the scope of such Director’s authority as delegated by the Board. The Board may delegate the management of the Fund’s day-to-day operations to one or more officers or other persons (including, without limitation, the Adviser), subject to the investment objective and policies of the Fund and to the oversight of the Board. The Directors have engaged the Adviser to provide investment advice regarding the selection of Investment Funds and to be responsible for the day-to-day management of the Fund. In accordance with Rule 2a-5 promulgated under the 1940 Act, the Board has appointed the Adviser as the Fund’s valuation designee (the “Valuation Designee”) and has assigned to the Adviser general responsibility for determining the value of the Fund’s investments. In that role, the Adviser has established a committee (the “Valuation Committee”) that oversees the valuation of the Fund’s investments pursuant to procedures adopted by the Adviser (the “Valuation Procedures”).

The initial closing date for subscriptions for units of limited liability company interests (“Units”) was November 9, 2018 (“Initial Closing”). Subsequent to the Initial Closing, the Fund offered Units at additional closings, which occurred over a period of nine months following the Initial Closing (the last closing being referred to as the “Final Closing”). An investor that participated in a closing that occurred after the Initial Closing was required to pay a “make-up” fee amount to the Fund. Such “make-up” payment was calculated by applying an annualized rate of 8.0% to the percentage of the aggregate commitments by investors to the Fund (“Commitments”) previously drawn down by the Fund and applied over the period of time since such draw-downs. The amount of the make-up fee payments were paid to and retained as assets of the Fund. This amount is presented as a component of net assets on the Consolidated Statement of Assets and Liabilities.

The Fund does not have a fixed term. The Investment Funds, however, generally will have fixed terms. Investors reasonably can expect to receive distributions from the Fund periodically after the Fund receives distributions from Investment Funds and when Investment Funds terminate, which the Fund anticipates will occur approximately 10 to 12 years after the Final Closing. The Fund will be wound up and dissolved after its final distribution to investors. The Fund may be dissolved prior thereto in accordance with its LLC Agreement.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Fund meets the definition of an investment company and follows the accounting and reporting guidance as issued through the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 946, Financial Services — Investment Companies.

10

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

The following is a summary of significant accounting policies followed by the Fund in the preparation of its consolidated financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

Federal Tax Information: It is the Fund’s policy to qualify as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). The Fund’s policy is to comply with the provisions of the Code applicable to RICs and to distribute to its investors substantially all of its distributable net investment income and net realized gain on investments, if any, earned each year. In addition, the Fund intends to make distributions to avoid excise taxes. Accordingly, no provision for federal income or excise tax has been recorded in these consolidated financial statements.

The Fund has adopted a tax year end of September 30 (the “Tax Year”). As such, the Fund’s tax basis capital gains and losses will only be determined at the end of each Tax Year. Accordingly, tax basis distributions made during the 12 months ended March 31, 2024, but after the Tax Year ended September 30, 2023, will be reflected in the consolidated financial statement footnotes for the fiscal year ended March 31, 2025.

Management evaluates the tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions will “more-likely-than-not” be sustained upon examination by the applicable tax authority. Tax positions deemed to meet the more-likely-than-not threshold that would result in a tax benefit or expense to the Fund would be recorded as a tax benefit or expense in the current year. The 2020, 2021, 2022 and 2023 Tax Years remain subject to examination by the U.S. taxing authorities. The Fund, exclusive of the Subsidiaries, has not recognized any tax liability for unrecognized tax benefits or expenses. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Consolidated Statement of Operations. During the period ended March 31, 2024, the Fund did not incur any interest or penalties.

The character of distributions made during the year from net investment income or net realized gains may differ from the characterization for federal income tax purposes due to differences in the recognition of income, expense and gains or loss items for the consolidated financial statement and tax purposes. Where appropriate, reclassifications between net asset accounts are made for such differences that are permanent in nature.

The tax character of distributions will be evaluated once paid after the Tax Year ended September 30, 2024.

The March 31, 2024 book cost has been adjusted for book/tax basis differences as of the Fund’s last Tax Year end, September 30, 2023. The cost of investments and the net unrealized appreciation and depreciation on investments as of March 31, 2024 are noted below.

Federal tax cost of investments | | $ | 175,273,362 | |

Gross unrealized appreciation | | | 73,697,956 | |

Gross unrealized depreciation | | | (4,286,772 | ) |

Net unrealized appreciation | | $ | 69,411,184 | |

11

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

The tax character of distributions paid during the Tax Year ended September 30, 2023:

| | 2023 |

Long-term capital gains | | $ | 24,885,788 |

As of September 30, 2023, the components of distributable earnings/(loss) on a tax basis were as follows:

Undistributed ordinary income | | $ | — | |

Undistributed long-term capital gains | | | — | |

Net unrealized appreciation | | | 62,004,614 | a |

Accumulated capital & other losses | | | (4,841,732 | )b |

Total distributable earnings/(loss) | | $ | 57,162,882 | |

Permanent book and tax differences, primarily attributable to net operating loss, resulted in reclassification for the Tax Year ended September 30, 2023 as follows:

Paid in capital | | $ | (1,595,909 | ) |

Total distributable earnings/(deficit) | | | 1,595,909 | |

These reclassifications had no effect on net assets.

Cash: Cash consists of monies held at UMB Bank, N.A. (the “Custodian”). Such cash may exceed federally insured limits. The Fund has not experienced any losses in such accounts and does not believe it is exposed to any significant credit risk on such accounts. There are no restrictions on the cash held by the Fund.

Investment Transactions: The Fund accounts for realized gains and losses from its Investment Funds based upon the pro-rata ratio of the fair value and cost of the underlying investments at the date of distribution. Dividends are recorded on ex-date and interest income and expenses are recorded on an accrual basis. Distributions from Investment Funds will be received as underlying investments of the Investment Funds are liquidated. Distributions from Investment Funds occur at irregular intervals, and the exact timing of distributions from the Investment Funds has not been communicated from the Investment Funds. It is estimated that distributions will occur over the life of the Investment Funds.

Use of Estimates: The preparation of the consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

Fair Value of Financial Instruments: The fair value of the Fund’s assets and liabilities which qualify as financial instruments approximates the carrying amounts presented in the Consolidated Statement of Assets and Liabilities. The Fund values its investments in Investment Funds at fair value in accordance with FASB Accounting Standards Codification, Fair Value Measurement (“ASC 820”). See Note 3 for more information.

Distribution and Servicing fee: During the offering period (extending nine months from the Initial Closing) of the Fund, the Distribution and Servicing fee was charged to paid-in capital as a distribution cost. Thereafter the fee was expensed as incurred.

12

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Consolidation of Subsidiaries: The consolidated financial statements include the financial position and the results of operations of the Fund and the Subsidiaries. The Subsidiaries have the same investment objective as the Fund. The Subsidiaries are taxed as corporations and used when the Fund has determined that owning certain investment funds within a domestic limited liability company structure would not be beneficial. As of March 31, 2024, the total assets of investment funds held by CPG VA Acquisition Fund II is $25,823,230, or approximately 10.6% of the Fund’s total assets, and the total assets of investment funds held by CPG VA Acquisition Fund II No. 2 is $22,167,712, or approximately 9.1% of the Fund’s total assets. CPG VA Acquisition Fund II No. 3 did not hold any assets at March 31, 2024.

The Subsidiaries are subject to U.S. federal and state income taxes. These taxable entities are not consolidated for income tax purposes and may generate income tax assets or liabilities that reflect the net tax effect of temporary differences between the carrying amount of the assets and liabilities for financial reporting and tax purposes and tax loss carryforwards.

For financial reporting purposes, the components of income before provision for income taxes were as follows:

| | Year Ended

March 31,

2024 |

Domestic | | $ | (283,584 | ) |

Foreign | | | — | |

Income (loss) before income taxes | | $ | (283,584 | ) |

The Subsidiaries recorded a provision for income tax expense for the year ended March 31, 2024. This provision for income tax expense (benefit) is comprised of the following current and deferred income tax expense (benefit):

| | Year Ended

March 31,

2024 |

Current: | | | |

Federal | | $ | 85,421 |

State | | | 87,107 |

Foreign | | | — |

Total current tax expense (benefit) | | $ | 172,528 |

| | | | |

Deferred: | | | |

Federal | | $ | 4,047,139 |

State | | | 4,127,018 |

Foreign | | | — |

Total deferred tax expense (benefit) | | | 8,174,157 |

Total provision for income taxes | | $ | 8,346,685 |

Total income tax (current and deferred) is computed by applying the federal statutory income tax rate of 21% and estimated applicable state tax statutory rates (net of federal tax benefit) to net investment income and realized and unrealized gains/(losses) on investments before taxes for the year ended March 31, 2024 as follows:

| | Year Ended

March 31, 2024 |

Federal Tax (Benefit) at Statutory Rate | | $ | (59,553 | ) | | 21.00 | % |

State Tax (Benefit), Net of Federal Benefit | | | 3,329,159 | | | (1173.96 | )% |

Other | | | — | | | 0.00 | % |

Adjustments to Deferred tax values | | | 5,077,079 | | | (1790.32 | )% |

Total Provision for Income Taxes | | $ | 8,346,685 | | | (2943.28 | )% |

13

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Significant components of the Subsidiaries’ deferred tax assets and liabilities as of March 31, 2024 are as follows:

Deferred tax liabilities: | | | | |

Net distributive share from underlying investments | | $ | (8,174,157 | ) |

| | | | — | |

Total deferred tax liabilities | | $ | (8,174,157 | ) |

Valuation Allowance | | $ | — | |

Net deferred tax liabilities | | $ | (8,174,157 | ) |

The Federal, New York State, and New York City income tax returns are open to tax examination for the Tax Years 2020, 2021, 2022 and 2023.

3. PORTFOLIO VALUATION

ASC 820 defines fair value as the value that the Fund would receive to sell an investment or pay to transfer a liability in a timely transaction with an independent buyer in the principal market, or in the absence of a principal market, the most advantageous market for the investment or liability. ASC 820 establishes a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions that market participants would use in valuing the asset or liability developed based on the best information available in the circumstances.

The three-tier hierarchy of inputs is summarized below:

• Level 1 — unadjusted quoted prices in active markets for identical financial instruments that the reporting entity has the ability to access at the measurement date.

• Level 2 — inputs other than quoted prices included within Level 1 that are observable for the financial instrument, either directly or indirectly. Level 2 inputs also include quoted prices for similar assets and liabilities in active markets, and quoted prices for identical or similar assets and liabilities in markets that are not active.

• Level 3 — significant unobservable inputs for the financial instrument (including management’s own assumptions in determining the fair value of investments).

Investments in Investment Funds are recorded at fair value, using the Investment Funds’ net asset value (“NAV”) as a practical expedient in accordance with ASC 820 and they are excluded from the fair value hierarchy in accordance with ASU 2015-07. Other investments are assigned a level based upon the observation of the inputs which are significant to the overall valuation.

The Investment Funds are generally restricted securities that are subject to substantial holding periods and are not traded in public markets, so that the Fund may not be able to resell some of its investments for extended periods, which may be several years.

14

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

3. PORTFOLIO VALUATION (continued) |

The NAV of the Fund is determined by, or at the direction of, the Adviser as of the close of business at the end of any fiscal period in accordance with the valuation principles set forth below or as may be determined, from time to time, pursuant to policies adopted by the Adviser. The Fund’s investments are subject to the terms and conditions of the respective operating agreements and offering memoranda, as appropriate. The Fund’s valuation committee (the “Valuation Committee”) oversees the valuation process of the Fund’s investments. The Valuation Committee meets on a quarterly basis and reports to the Board on a quarterly basis. ASC 820 provides for the use of NAV (or its equivalent) as a practical expedient to estimate fair value of investments in Investment Funds, provided certain conditions are met. As such, the Fund’s investments in Investment Funds are carried at fair value which generally represents the Fund’s pro-rata interest in the net assets of each Investment Fund as reported by the administrators and/or investment managers of the underlying Investment Funds. All valuations utilize financial information supplied by each Investment Fund and are net of management and incentive fees or allocations payable to the Investment Funds’ managers or pursuant to the Investment Funds’ agreements. The Investment Funds value their underlying investments in accordance with policies established by each Investment Fund, as described in each of their consolidated financial statements or offering memoranda. The Fund’s valuation procedures require the Adviser to consider all relevant information available at the time the Fund values its portfolio. The Adviser has assessed factors including, but not limited to, the individual Investment Funds’ compliance with fair value measurements, price transparency and valuation procedures in place. The Adviser will consider such information and consider whether it is appropriate, in light of all relevant circumstances, to value such a position at its NAV as reported or whether to adjust such value. The underlying investments of each Investment Fund are accounted for at fair value as described in each Investment Fund’s consolidated financial statements.

The Adviser employs ongoing due diligence policies and processes with respect to Investment Funds and their investment managers. The Adviser assesses the quality of information provided and determines whether such information continues to be reliable or whether additional inquiry is necessary. Such inquiries may require the Adviser to forego its normal reliance on the value provided and to independently determine the fair value of the Fund’s interest in such Investment Fund.

The fair value relating to certain underlying investments of these Investment Funds, for which there is no active market, has been estimated by the respective Investment Fund’s management and is based upon available information in the absence of readily ascertainable fair values and does not necessarily represent amounts that might ultimately be realized. Due to the inherent uncertainty of valuation, those estimated fair values may differ significantly from the values that would have been used had a active market for the investments existed. These differences could be material.

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the inputs used, as of March 31, 2024, in valuing the Fund’s assets carried at fair value:

| | Level 1 | | Level 2* | | Level 3* | | Investments

Measured at Net

Asset Value(1) | | Total |

Investments | | | | | | | | | | | | | | | |

Investments in Private Investment Funds | | $ | — | | $ | — | | $ | — | | $ | 242,819,748 | | $ | 242,819,748 |

Short-Term Investments | | $ | 1,864,798 | | $ | — | | $ | — | | $ | — | | $ | 1,864,798 |

Total Investments | | $ | 1,864,798 | | $ | — | | $ | — | | $ | 242,819,748 | | $ | 244,684,546 |

15

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

3. PORTFOLIO VALUATION (continued) |

The Fund’s private equity financing stage and private credit with their corresponding unfunded commitments and other attributes, as of March 31, 2024, are shown in the table below.

Financing

Stage | | Investment

Strategy | | Fair Value | | Unfunded

Commitments | | Remaining

Life* | | Redemption

Frequency | | Notice Period

(In Days) | | Redemption

Restrictions

Terms* |

Buyout | | Control investments in established companies | | $ | 122,404,023 | | $ | 13,169,193 | | Up to 10 years | | None | | N/A | | N/A |

Credit | | Debt investments made through privately negotiated transactions | | $ | 74,230,921 | | $ | 12,203,576 | | Up to 10 years | | None | | N/A | | N/A |

Growth | | Non-control investments in companies with high growth potential | | $ | 46,184,804 | | $ | 3,479,532 | | Up to 10 years | | None | | N/A | | N/A |

Private equity is a common term for investments that typically are made in non-public companies through privately negotiated transactions.

The following is a summary of investment strategies of the Investment Funds held by the Fund as of March 31, 2024.

• Buyout: Control investments in established, cash flow positive companies are usually classified as buyouts. Buyout investments may focus on small-, mid- or large-capitalization companies, and such investments collectively represent a substantial majority of the capital deployed in the overall private equity market. The use of debt financing, or leverage, is prevalent in buyout transactions — particularly in the large-cap segment.

• Credit: Private credit is a common term for unregistered debt investments made through privately negotiated transactions. Private credit investments may be structured using a range of financial instruments, including but not limited to, first and second lien senior secured loans, unitranche debt, mezzanine debt, unsecured debt, and structurally subordinated instruments. While these strategies, which include special situations investments (including distressed investments), generally focus on originated or secondary purchases of fixed-income senior or subordinated credits of companies, they also may include certain equity features. Distressed investing encompasses a broad range of strategies including control and non-control distressed debt, operational turnarounds, and “rescue” financings. The Fund’s private credit investments may include investments in privately offered business development companies (“BDCs”).

• Growth: Growth strategies typically involve non-control investments in companies with high growth potential that are in need of expansion capital.

4. RELATED PARTY TRANSACTIONS

As of March 31, 2024, the Fund and the Subsidiaries, had no investments in Investment Funds that were related parties.

The Adviser provides investment advisory services to the Fund pursuant to an investment advisory agreement (the “Advisory Agreement”). Pursuant to the Advisory Agreement, the Fund pays the Adviser a quarterly advisory fee at the annual rate of (i) 0.10% of total Commitments for the first 12 months following the Initial Closing, (ii) 0.65% of total Commitments from the one year anniversary of the Initial Closing until the six year anniversary of the Final Closing; (iii) 0.65% of the Fund’s

16

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

4. RELATED PARTY TRANSACTIONS (continued) |

net invested capital from the six year anniversary of the Final Closing until the eight year anniversary of the Final Closing and (iv) 0.30% of the Fund’s net invested capital thereafter for the remaining life of the Fund (the “Management Fee”). The Management Fee will be determined and accrued as of the last day of each quarter, and will be prorated for any period of less than a quarter based on the number of days in such period. During the year ended March 31, 2024, the Fund paid the Adviser $1,454,896 of Management Fees which is included in the Consolidated Statement of Operations, of which $363,582 was payable on March 31, 2024, and is included in Payable to Adviser in the Consolidated Statement of Assets and Liabilities.

Unless otherwise voluntarily or contractually assumed by the Adviser or another party, the Fund bears all expenses incurred in its business, including, but not limited to, the following: all costs and expenses related to investment transactions and positions for the Fund’s account; legal fees; accounting, auditing and tax preparation fees; recordkeeping and custodial fees; costs of computing the Fund’s NAV; fees for data and software providers; research expenses; costs of insurance; registration expenses; certain offering costs; expenses of meetings of investors; directors’ fees; all costs with respect to communications to investors; transfer taxes and taxes withheld on non-U.S. dividends; interest and commitment fees on loans and debit balances; and other types of expenses as may be approved from time to time by the Board.

Each member of the Board who is not an “interested person” of the Fund (the “Independent Directors”), as defined by the 1940 Act, receives an annual retainer of $15,000 (prorated for partial years) plus a fee of $1,000 for each meeting attended and $500 for each meeting by phone. The Board Chair, Audit Committee Chair, Nominating Committee Chair and Contracts Review Committee Chair each receive an additional $2,000 annual retainer. All members of the Board are reimbursed for their reasonable out-of-pocket expenses. Total amounts expensed by the Fund related to Independent Directors for the year ended March 31, 2024 was $88,000 which is included in Directors’ and Officer fees in the Consolidated Statement of Operations.

During the year ended March 31, 2024, the Fund incurred a portion of the annual compensation of the Fund’s Chief Compliance Officer in the amount of $14,909 which is included in Directors’ and Officer fees in the Consolidated Statement of Operations.

Certain officers and the interested director of the Fund are also officers of the Adviser and are registered representatives of Delaware Distributors, L.P.

5. ADMINISTRATION, CUSTODIAN FEES, DISTRIBUTION AND SERVICING FEE

UMB Fund Services, Inc., serves as administrator (the “Administrator”) to the Fund and provides certain accounting, administrative, record keeping and investor related services. For its services, the Fund pays an annual fee to the Administrator based upon average net assets, subject to certain minimums. For the year ended March 31, 2024, the total administration fees were $494,010 which is included as accounting and administration fees in the Consolidated Statement of Operations, $7,500 of which was payable on March 31, 2024.

The Custodian is an affiliate of the Administrator and serves as the primary custodian of the assets of the Fund.

During the offering period, the Distribution and Servicing Fee was considered attributable to distribution only and charged to paid-in capital as soon as Units are sold in accordance with guidance outlined in FASB ASC 946-20-25-5 and 946-20-20-20. Following the offering period (i.e., following Final Closing), the Distribution and Servicing fee was considered attributable to ongoing distribution-related servicing and recorded quarterly as a liability and an expense on the Fund’s books and records. The fee attributed to distribution during the offering period was charged to each investor at an amount equal for 0.5625% of their Commitment.

17

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

5. ADMINISTRATION, CUSTODIAN FEES, DISTRIBUTION AND SERVICING FEE (continued) |

Delaware Distributors, L.P. (the “Placement Agent”) acts as the placement agent of the Fund’s Units. Under the terms of the Placement Agent Agreement, the Placement Agent is authorized to pay third parties including brokers, dealers and certain financial advisors (which may include wealth advisors) and others (collectively, “Sub-Placement Agents”) for the provision of distribution services and services to investors. The Fund pays the Placement Agent a quarterly fee at the annual rate of (i) 0.75% of total Commitments from the Initial Closing until the six year anniversary of the Final Closing, (ii) 0.75% of the Fund’s net invested capital from the six year anniversary of the Final Closing until the eight year anniversary of the Final Closing and (iii) 0.10% of the Fund’s net invested capital thereafter for the remaining life of the Fund (the “Distribution and Servicing Fee”). The Distribution and Servicing Fee will be determined and accrued as of the last day of each calendar quarter and will be prorated for any period of less than a quarter based on the number of days in such period. During the year ended March 31, 2024, the Fund paid the Placement Agent $1,678,726 of Distribution and Servicing Fees which is included on the Consolidated Statement of Operations. There was $1,108,536 payable at March 31, 2024, which is included in Distribution and Servicing fee payable in the Consolidated Statement of Assets and Liabilities.The Placement Agent is an affiliate of the Adviser and is a subsidiary of Macquarie Group Limited (“Macquarie”).

6. INVESTMENTS

For the year ended March 31, 2024, total capital called by Investment Funds and total proceeds from redemptions or other dispositions of investments amounted to $18,394,996 and $0, respectively. The cost of investments in Investment Funds for U.S. federal income tax purposes is adjusted for items of taxable income allocated to the Fund from such Investment Funds. The Fund relies upon actual and estimated tax information provided by the managers of the Investment Funds as to the amounts of taxable income allocated to the Fund as of March 31, 2024.

7. CAPITAL CALL AND COMMITMENTS

As of March 31, 2024, the Fund had outstanding unfunded investment commitments to Investment Funds totaling $28,852,301, as described in Note 3. The Fund has total capital committed of $223,742,681 as of March 31, 2024. Since the commencement of operations of the Fund on November 9, 2018, $196,893,559 capital has been called comprising 88% of the total capital committed. The Fund currently has unfunded capital commitments of $26,849,122.

8. INDEMNIFICATION

Under the Fund’s organizational documents, its Officers and Directors are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the ordinary course of business, the Fund may enter into contracts or agreements that contain indemnification or warranties. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

9. LINE OF CREDIT

The Fund may borrow money for investment purposes and to pay expenses in advance of, or in addition to, calling capital. The Fund also may borrow money to manage its cash flow needs associated with calling Investor Commitments, satisfying capital calls, managing distributions to investors and paying ongoing expenses. The provisions of the 1940 Act provide that the Fund may borrow in an amount up to 33 1/3% of its total assets (including the proceeds from leverage).

18

CPG Vintage Access Fund II, LLC Consolidated Notes to Financial Statements (Continued) March 31, 2024 |

9. LINE OF CREDIT (continued) |

On February 3, 2021, the Fund, along with other funds managed by the Adviser, collectively entered into a $20,800,000 revolving credit facility with Barclays Bank PLC (“Barclays”), which will expire on January 24, 2025, subject to the restrictions and terms of the credit facility (“Line of Credit”). The limit on the Line of Credit was reduced to $18,600,000, $13,600,000, $10,700,000 and $7,700,000 on September 30, 2023, October 28, 2023, December 29, 2023 and March 27, 2024, respectively. As of March 31, 2024, the Fund borrowed $4,000,000 and repaid $9,100,000 (of which $5,100,000 was related to prior year borrowings) on this Line of Credit and the maximum borrowing outstanding during the period was $9,100,000. For borrowing under this Line of Credit, the Fund is charged 2.75% (per annum) plus SOFR (Secured Overnight Financing Rate). The commitment fee on the daily unused loan balance of the line of credit accrues at 0.75% and is included in Line of credit fees on the Consolidated Statement of Operations. For the year ended March 31, 2024, the average annualized interest rate charged and the average outstanding loan payable, was as follows:

Average Annualized Interest Rate | | | 7.65 | % |

Average Outstanding Loan Payable | | $ | 5,255,405 | |

10.SUBSEQUENT EVENTS

Subsequent events after March 31, 2024 have been evaluated through the date the consolidated financial statements were issued. There were no events or material transactions through the date the consolidated financial statements were issued.

19

CPG Vintage Access Fund II, LLC Other Information (Unaudited) March 31, 2024 |

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 are available without charge, upon request, by calling (collect) 1-212-317-9200 and on the Securities and Exchange Commission (the “SEC”) website at http://www.sec.gov.

The Fund is required to file Form N-PX, with its complete proxy voting record for the twelve months ended June 30, no later than August 31. The Fund’s Form N-PX filing is available: (i) without charge, upon request, by calling the Fund (collect) at 1-212-317-9200 or (ii) by visiting the SEC’s website at http://www.sec.gov.

Availability of Quarterly Portfolio Schedules

Disclosure of Portfolio Holdings: The Fund will file a complete schedule of its portfolio holdings with the SEC no more than sixty days after the Fund’s first and third fiscal quarters of each fiscal year on Form N-PORT. For the Fund, this would be for the fiscal quarters ending June 30 and December 31. The Fund’s Form N-PORT filings can be found free of charge on the SEC’s website at http://www.sec.gov.

Management Discussion of Fund Performance

The Fund was up 4.9% during fiscal year 2024 and ended the year marked at 1.5x MOIC as compared to. 1.4x MOIC as of fiscal year-end 2023. On balance, our managers are getting to the later stages of their investment periods, transitioning into their harvest period and ramping up distributions. For the fiscal year, we called 7% of commitments, bringing the Fund’s called commitments to 88%. We distributed 5% of commitments during the fiscal year, bringing the Fund’s total distributions to 21% of commitments. Each of the Fund’s underlying managers is performing well with fiscal year-end net multiples ranging between 1.1x and 2.8x.

The information contained in this Discussion of Fund Performance reflects the views of the Adviser or its affiliates and sources it believes are reliable as of the date of this publication. The Adviser makes no representations or warranties concerning the accuracy of any third-party sourced data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed herein may change at any time after the date of this publication. This Discussion of Fund Performance is for informational purposes only and does not constitute investment advice. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any security, financial instrument, product or service.

20

CPG Vintage Access Fund II, LLC Other Information (Unaudited) (Continued) March 31, 2024 |

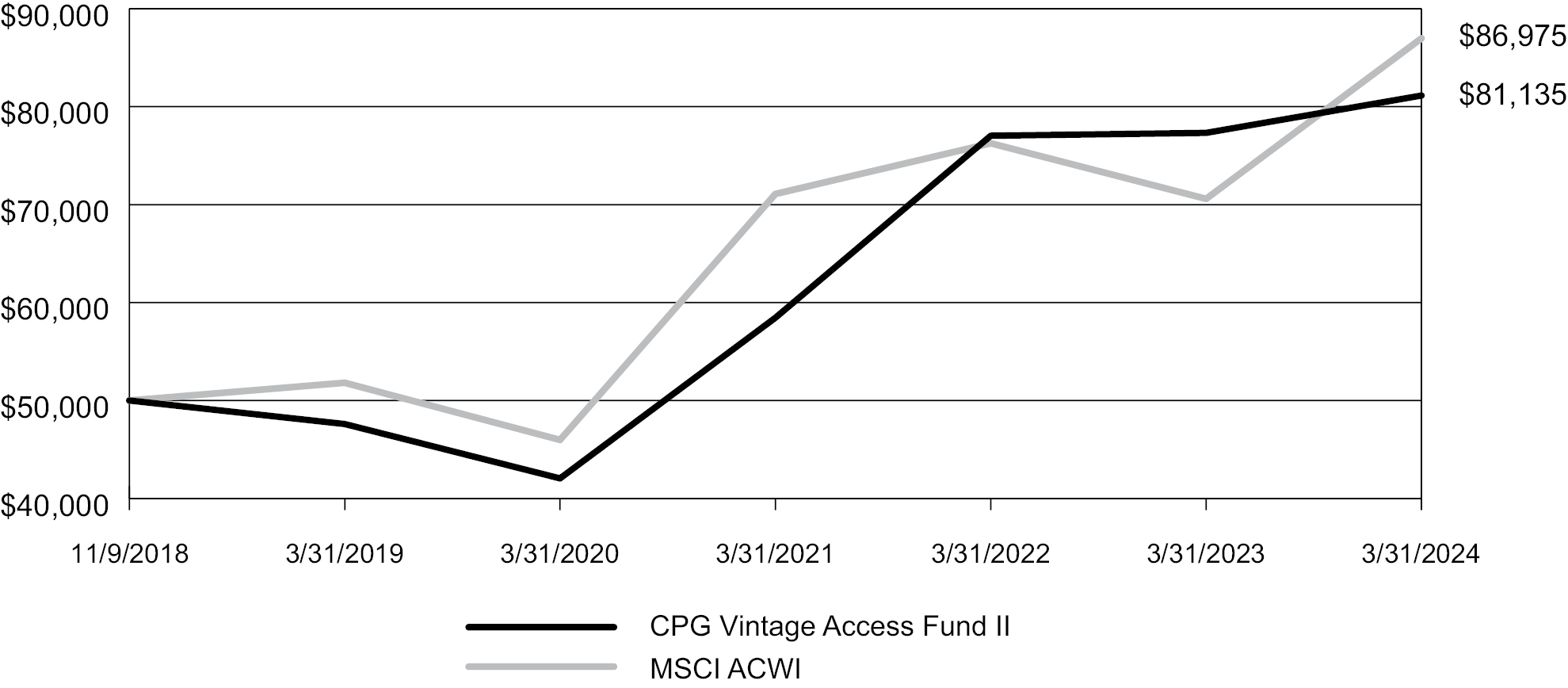

Performance Illustration

Average Annual Returns

| | Trailing 1-Yr | | Trailing 5-Yr | | Trailing 10-Yr | | ITD |

CPG Vintage Access Fund II | | 4.93% | | 11.26% | | NA | | 9.39% |

MSCI ACWI | | 23.22% | | 10.92% | | NA | | 10.81% |

The performance illustration above represents total return based on per unit NAV and reflects the change in NAV based on capital contributions called by the Fund and the effects of the performance of the Fund during the period, and adds back distributions, if any, made during the relevant period1. The performance illustration represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that an investor would pay on Fund distributions. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s units may be worth more or less than their original cost.

Fund returns are estimated, unaudited and presented net of management fee, distribution and servicing fee and underlying fund fees, expenses, carried interest/incentive allocations. The Fund does not charge a placement fee or sales load; however, certain sub-placement agents may charge a one-time placement fee or sales load of up to a maximum of 3.0% of total commitment amounts, which will be paid directly to the agent. Returns do not reflect a placement fee or sales load which would reduce returns.

Index is included to show general trend in market and not intended to imply that past performance was comparable to index either in composition or risk. Unlike the Fund, the index described is unmanaged, is not available for direct investment, and is not subject to management fees and other fees and expenses. The Fund and the underlying investment funds do not restrict their investments to securities in the index, and may have exposure to markets not reflected in the index. No index is directly comparable to the investment strategy of the Fund. Nor does an index reflect the drawdown feature of the Fund for which capital contributions on commitment amounts will be called over time and included in returns. Public market returns are not directly comparable to private equity returns due to the timing of investments. Additionally, there are limitations in comparisons of Fund performance to the index which provides only one approach to comparison of returns. Other indices and benchmarks should be considered. Information regarding the index, including accuracy and completeness, has not been independently verified. The MSCI ACWI Index, a widely quoted global equity index, is designed to represent performance of

21

CPG Vintage Access Fund II, LLC Other Information (Unaudited) (Continued) March 31, 2024 |

the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets. As of April 2024, it covers 2,840 constituents across 11 sectors and approximately 85% of the free float-adjusted market capitalization in each market. The index is built using MSCI’s Global Investable Market Index (GIMI) methodology, which is designed to take into account variations reflecting conditions across regions, market cap sizes, sectors, style segments and combinations.

Approval of Investment Advisory Agreement

At a meeting on December 14, 2023, the Directors, including the Directors who are not “interested persons” as defined in the Investment Company Act of 1940, as amended (the “Independent Directors”), evaluated the Investment Advisory Agreement of the Fund (the “Advisory Agreement”). The Independent Directors met in an executive session during which they were advised by and had the opportunity to discuss with independent legal counsel the approval of the Advisory Agreement. The Directors reviewed materials furnished by the Adviser and Macquarie, and discussed with the Adviser and Macquarie information regarding the Adviser, Macquarie, their affiliates and their personnel, operations and financial condition. Tables prepared by the Adviser indicating comparative fee information and comparative performance information, as well as a summary financial analysis for the Fund, were also included in the meeting materials and were reviewed and discussed. The Directors discussed with representatives of the Adviser and Macquarie the Fund’s operations and the Adviser’s ability to provide advisory and other services to the Fund. In particular, the Board considered the following:

(i) The nature, extent and quality of services provided by the Adviser: In evaluating the nature, extent and quality of services provided by the Adviser, the Directors considered information provided by the Adviser and Macquarie regarding their advisory services, investment philosophy and process, investment management capabilities, business and operating structure, scale of operations, leadership and reputation, distribution capabilities, and financial condition. The Directors also considered the resources that Macquarie has devoted to its risk management program and cybersecurity program and reviewed information provided by Macquarie related to its business, legal, and regulatory affairs. The Directors discussed the ability of the Adviser to manage the Fund’s investments in accordance with the Fund’s stated investment objectives and policies, as well as the services provided by the Adviser to the Fund, including administrative and compliance services, oversight of fund accounting, marketing services, assistance in meeting legal and regulatory requirements and other services necessary for the operation of the Fund. The Directors considered the capabilities, resources and experience of the investment advisory and other personnel of the Adviser providing services to the Fund. The Directors acknowledged the Adviser’s employment of highly skilled investment professionals, research analysts and administrative and compliance staff members to ensure that a high level of quality in investment, compliance and administrative services would be provided to the Fund. The Directors also recognized the benefits that the Fund derives from the resources available to the Adviser. Accordingly, the Directors believed that the quality of services offered by the Adviser to the Fund are appropriate in nature, quality and extent in light of the Fund’s operations and investor needs and that the personnel providing such services had sufficient expertise to manage the Fund, and supported the approval of the Advisory Agreement.

(ii) Investment performance of the Fund: With respect to the performance of the Fund, the Directors considered their review of peer group and benchmark investment performance comparison data relating to the Fund’s performance record presented at the meeting, other Board meetings since its last approval of the Advisory Agreement and/or in response to an Information Request from the Board (the “Information Request”). The Board reviewed the performance of the Fund and compared that performance to the performance of its comparative benchmarks, as available. The Board considered the limitations of such benchmarks given the nature of the asset class and accepted Fund management’s conclusion that it was early in the Fund’s term, and comparative performance would not be meaningful for some time given the time horizon of the private companies invested in by the underlying funds.

Based on information presented to the Board at the meeting, other Board meetings since its last approval of the Advisory Agreement, in response to the Information Request and in its discussions with the Adviser and Macquarie, the Board concluded that the Adviser is capable of generating a level of long-term investment performance that is appropriate in light of the Fund’s investment objectives, strategies and restrictions.

22

CPG Vintage Access Fund II, LLC Other Information (Unaudited) (Continued) March 31, 2024 |

(iii) Fees paid to the Adviser and expenses of the Fund: The Directors next considered the advisory fee being charged by the Adviser for its services to the Fund, as compared to those charged to other investment companies that have an objective and strategy similar to that of the Fund and that are managed by other investment advisers, as well as to the fees that the Adviser charged to manage other funds of private equity funds. The Directors determined that the fees paid under the Advisory Agreevment do not constitute fees that are so disproportionately large as to bear no reasonable relationship to the services rendered and that could not have been the product of arm’s-length bargaining, and concluded that the fees were appropriate under the circumstances and in light of the totality of the services provided.

(iv) The extent to which economies of scale may be realized as the Fund grows larger and whether fee levels reflect such economies of scale for the benefit of the Fund’s investors: The Directors considered potential or anticipated economies of scale in relation to the services the Adviser provides to the Fund. The Directors considered that, because the Fund is a closed-end fund that is not continually offering shares, there are limited opportunities for significant economies of scale to be realized.

(v) Profits realized by the Adviser, Macquarie and their Affiliates from their relationship with the Fund: The Directors considered the benefits the Adviser, Macquarie and their affiliates may derive from their relationship with the Fund. The Directors also considered information on the Adviser’s profitability that was provided in response to the Information Request. The Directors considered that the estimated profitability of the Adviser, Macquarie and their affiliates was not excessive in light of the nature, extent and quality of the services provided to the Fund.

(vi) Fall-out benefits to the Adviser, Macquarie and their Affiliates: The Directors considered the possible fall-out benefits that may accrue to the Adviser, Macquarie and their affiliates. The Board noted that the Adviser’s affiliation with Macquarie provides Macquarie and its affiliates the opportunity to deliver additional alternative investment products to investors and that the Adviser can provide portfolio management services to new alternative investment products sponsored by Macquarie. Based on its review, the Board determined that any “fall-out” benefits that may accrue to the Adviser, Macquarie and their affiliates did not change its conclusions about approving the Advisory Agreement.

Based on the foregoing and other relevant considerations, the Directors, including a majority of the Independent Directors, acting within their business judgment, determined that approval of the Advisory Agreement is in the best interests of the Fund. The Board noted some factors may have been more or less important with respect to the Fund and that no one factor was determinative of its decisions which, instead, were premised upon the totality of factors considered. In this connection, the Board also noted that different Board members likely placed emphasis on different factors in reaching their individual conclusions to vote in favor of the Advisory Agreement.

INVESTMENT PROGRAM

The investment objective of CPG Vintage Access Fund II, LLC (the “Fund”) is to seek long-term attractive risk-adjusted returns. The Fund only makes primary investments (each, a “Primary Investment”) in Investment Funds (as defined below) that are represented on the Morgan Stanley Smith Barney LLC platform (the “Morgan Stanley Platform”). The Fund invests only in institutional offerings. The Fund does not invest in feeder funds or other investment vehicles represented on the Morgan Stanley Platform that provide indirect access to institutional private equity, venture and private debt investment funds managed or sponsored by various asset management firms unaffiliated with the Adviser (as defined below) (“Private Capital Funds”), other than through institutional “funds-of-funds”. Certain of the Investment Funds may be advised by Morgan Stanley or an affiliate thereof, and Morgan Stanley may act as placement agent for the Investment Funds.

The Fund seeks to achieve its investment objective principally by making Primary Investments in Private Capital Funds that were represented on the Morgan Stanley Platform between April 2018 and September 2019 (the “Vintage Period”). Primary Investments are interests or investments in newly established, institutional private fund offerings. Primary investors subscribe for interests during an initial fundraising period, and their capital commitments are then used to fund investments in a number of individual operating companies during a defined investment period. The investments of the fund are usually unknown at the time of commitment, and investors typically have little or no ability to influence the investments that are made during the fund’s life. Because primary investors must rely on the expertise of the fund manager, an accurate assessment of the manager’s capabilities is essential. Most private fund sponsors raise new funds only every two to four years, and many top-performing

23

CPG Vintage Access Fund II, LLC Other Information (Unaudited) (Continued) March 31, 2024 |

funds may be closed to new investors or otherwise difficult to access. Because of the limited windows of opportunity for making Primary Investments in particular funds, strong relationships with leading fund sponsors and the private wealth management brokerage firms that offer their funds, such as Morgan Stanley, are highly important for primary investors.

The Fund also invested in certain assets classes and investment strategies through investments in institutional funds that focus on co-investments that are represented on the Morgan Stanley Platform during the Vintage Period. Unlike the Private Capital Funds, which invest directly in multiple companies, ventures and businesses (“Portfolio Companies”), institutional co-investment funds seek to invest in private capital alongside other Private Capital Funds. These institutional co-investment funds, together with Private Capital Funds, are referred to herein as “Investment Funds.” The Fund does not make secondary investments or co-investments, except that the Fund invested in co-investments through Investment Funds that focus on making co-investments. Additionally, the Fund does not participate in private placement transactions alongside affiliated persons of the Fund that, in light of the facts and circumstances, require relief from Section 17(d) of the 1940 Act and Rule 17d-1 thereunder.

An Investment Fund was considered represented on the Morgan Stanley Platform during the Vintage Period if Morgan Stanley clients could have committed to or invested in it at any time during such period, either directly or indirectly through a feeder fund or other investment vehicle represented on the Morgan Stanley Platform.

Investment Strategies

The principal elements of the investment strategy of Central Park Advisers, LLC, the Fund’s investment adviser (the “Adviser”), include: (i) seeking attractive investment opportunities from among the Investment Funds represented on the Morgan Stanley Platform; (ii) allocating the Fund’s assets to Investment Funds across private market segments; and (iii) seeking to manage risk through ongoing monitoring of the Fund’s portfolio.

• Access. The Fund sought to provide investors (“Investors”) with access to Investment Funds represented on the Morgan Stanley Platform that generally were unavailable to the investing public.

• Asset Allocation. The Adviser sought diversification of the Fund’s investments through exposure to different markets and investment types. The Adviser sought to identify attractive sponsors whose funds were available to high net worth Morgan Stanley clients, and conducted due diligence regarding the Investment Fund Manager, its track record and the investment opportunity.

• Risk Management. The long-term nature of private capital investments requires a commitment to ongoing risk management. In addition to the risk management and due diligence processes of the Adviser, the Fund may benefit by having invested in Investment Funds represented on the Morgan Stanley Platform given its investment expertise, quality of risk management systems and experienced private capital vetting process. The Adviser monitors the performance of Investment Funds and developments at individual Portfolio Companies that represent material positions in Investment Funds held by the Fund.

The Fund seeks to provide Investors with attractive long-term capital appreciation by having invested in a diversified portfolio of Investment Funds. In pursuing its investment objective, the Fund sought to allocate the Fund’s assets across Investment Funds representing a broad spectrum of asset classes and private investment strategies, including, but not limited to:

Buyout. Control (e.g., majority stake) investments in established, cash flow positive companies are usually classified as buyouts. Buyouts attempt to create value by improving management or operations, driving strategic outcomes (such as a merger or acquisition) and/or utilizing leverage, and represent a substantial majority of the capital deployed in the private equity market.

Buyouts are characterized by the use of equity and debt to acquire established companies across a wide range of industries. Typically, private equity firms supply equity capital and arrange for other financial firms (e.g., banks, lending institutions, mezzanine providers) to provide debt and debt-related financing. Often, the assets of the company being acquired are used

24

CPG Vintage Access Fund II, LLC Other Information (Unaudited) (Continued) March 31, 2024 |

as collateral. Returns are typically generated through a combination of revenue growth (both organic and through add-on acquisitions) and margin improvement and are enhanced by the leverage in the capital structure. The buyout landscape can be segmented a number of different ways including by fund size, company size, geography and sector specialization.

The small and mid-cap buyout market offers a large number of investment opportunities. In the small and mid-cap market segment, there are hundreds of thousands of privately owned businesses around the globe suitable for investment or acquisition. Small and mid-cap buyout funds are highly segmented by geography, strategy, industry focus and size and there are numerous manager formations and spinoffs in any given year. In addition, small and mid-cap fund managers tend to be relatively nimble and flexible, and may be well situated to navigate the current marketplace and produce attractive returns.

The large-cap buyout market consists of a moderate number of institutional fund managers that tend to have enormous resources, a large number of investment professionals and operational staff and a significant global presence. Generally, the substantial amount of capital that has been allocated to these fund managers is the result of their historic ability to outperform their peers and generate highly attractive risk-adjusted returns. These funds tend to employ large staffs of highly sophisticated investors and some of the most talented and well-known names within the private equity industry.

Growth Equity and Venture Capital. Growth equity strategies typically involve non-control (e.g., minority stake) equity investments in companies with high growth potential that are in need of expansion capital.