WORTHY FINANCIAL, INC.

![]()

FORM C-AR

ANNUAL REPORT

April 27, 2020

One Boca Commerce Center

551 NW 77 Street, Suite 212

Boca Raton, FL 33487

Phone: (561) 288-8467

www.worthy.us

THE COMPANY

Worthy Financial, Inc. was formed on February 24, 2016 as a Delaware corporation. We were organized to create a “Worthy Community,” focusing on peer financing and secured lending, which we are initially targeting to the millennials who are surpassing the baby boomers as the nation’s largest living generation. For additional information on our company, please see the section entitled “The Company and Its Business.”

No federal or state securities commission or regulatory authority has passed upon the accuracy or adequacy of this document. The U.S. Securities and Exchange Commission (the “SEC”) does not pass upon the accuracy or completeness of any disclosure document or literature. The Company is filing this Form C-AR pursuant to Regulation CF (§ 227.100 et seq.) which requires that it must file a report with the Commission annually and post the report on its website at www.worthy.us no later than 120 days after the end of each fiscal year covered by the report.

THIS FORM C-AR DOES NOT CONSTITUTE AN OFFER TO PURCHASE OR SELL SECURITIES.

TABLE OF CONTENTS

| 2 |

You should rely only on the information contained in this Form C-AR. We have not authorized anyone to provide you with information different from that contained in this Form C-AR. You should assume that the information contained in this Form C-AR is accurate only as of the date of this Form C-AR, regardless of the time of delivery of this Form C-AR. Our business, financial condition, results of operations, and prospects may have changed since that date. Statements contained herein as to the content of any agreements or other document are summaries and, therefore, are necessarily selective and incomplete and are qualified in their entirety by the actual agreements or other documents.

This Annual Report on Form C-AR is dated April 27, 2020 (the “Annual Report”).

When used herein, the terms “we,” “us,” “ours,” “WFI,” and the “Company” refers to Worthy Financial, Inc., a Delaware corporation, our wholly-owned subsidiary Worthy Peer Capital, Inc., a Delaware corporation (“Worthy Peer”), and its wholly owned subsidiary Worthy Lending, LLC, a Delaware limited liability company (“Worthy Lending”), our other wholly-owned subsidiary Worthy Peer Capital II, Inc. a Florida corporation (“Worthy Peer II”) and its wholly owned subsidiary Worthy Lending II, LLC, a Delaware limited liability company (“Worthy Lending II”). We have facilitated a Regulation A offering by Worthy Peer of its worthy bonds (the “Worthy Bonds”) that was closed on March 17, 2020 under SEC File No. 024-10766. We are currently facilitating a Regulation A offering by Worthy Peer II of its worthy II Bonds (the “Worthy II Bonds”) under SEC File No. 024-11150 which was qualified by the SEC on March 17, 2020.

The information which appears on, or is accessible through our websites at www.worthy.us, www.worthybonds.com and www.worthylending.com is not a part of, and is not incorporated by reference into, this Annual Report.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that are based on our beliefs and assumptions and on information currently available to us. Forward-looking statements include information concerning our possible or assumed future results of operations and expenses, business strategies and plans, competitive position, business environment, and potential growth opportunities. Forward-looking statements include all statements that are not historical facts. In some cases, forward-looking statements can be identified by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would,” or similar expressions and the negatives of those terms.

Forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Given these uncertainties, you should not place undue reliance on any forward-looking statements in this Annual Report. You should read this Annual Report and the other documents that we have filed with the SEC, completely and with the understanding that our actual future results may be materially different from what we expect.

Any forward-looking statement made by us in this Annual Report speaks only as of the date on which it is made. Except as required by law, we disclaim any obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. All forward-looking statements are expressly qualified in their entirety by the foregoing cautionary statements.

| 3 |

Investing in our securities involves risks. In addition to the other information contained in this Annual Report, you should carefully consider the following risks. The occurrence of any of the following risks might cause you to lose all or a part of your investment. Some statements in this Annual Report, including statements in the following risk factors, constitute forward-looking statements. Please refer to “Special Note Regarding Forward-Looking Statements” for more information regarding forward-looking statements.

Risks Related to our Industry

The lending industry is highly regulated. Changes in regulations or in the way regulations are applied to our business could adversely affect our business.

Changes in laws or regulations or the regulatory application or judicial interpretation of the laws and regulations applicable to us could adversely affect our ability to operate in the manner in which we intend to conduct business or make it more difficult or costly for us to participate in or otherwise make loans. A material failure to comply with any such laws or regulations could result in regulatory actions, lawsuits, and damage to our reputation, which could have a material adverse effect on our business and financial condition and our ability to participate in and perform our obligations to investors and other constituents.

The initiation of a proceeding relating to one or more allegations or findings of any violation of such laws could result in modifications in our methods of doing business that could impair our ability to collect payments on our loans or to acquire additional loans or could result in the requirement that we pay damages and/or cancel the balance or other amounts owing under loans associated with such violation. We cannot assure you that such claims will not be asserted against us in the future.

Worsening economic conditions may result in decreased demand for loans, cause borrowers’ default rates to increase, and harm our operating results.

Uncertainty and negative trends in general economic conditions in the United States and abroad, including significant tightening of credit markets, historically have created a difficult environment for companies in the lending industry. Many factors, including factors that are beyond our control, may have a detrimental impact on our operating performance. These factors include general economic conditions, unemployment levels, energy costs and interest rates, as well as events such as natural disasters, global pandemics, acts of war, terrorism, and catastrophes.

Our borrowers are small businesses. Accordingly, our borrowers have historically been, and may in the future remain, more likely to be affected or more severely affected than large enterprises by adverse economic conditions. These conditions may result in a decline in the demand for loans by potential borrowers or higher default rates by borrowers.

There can be no assurance that economic conditions will remain favorable for our business or that demand for loans in which we participate or default rates by borrowers will remain at current levels. Reduced demand for loans would negatively impact our growth and revenue, while increased default rates by borrowers may inhibit our access to capital and negatively impact our profitability. Further, if an insufficient number of qualified individuals and small businesses apply for loans, our growth and revenue would be negatively impacted.

We operate in a competitive market which may intensify, and competition may limit our ability to implement our business model and have a material adverse effect on our business, financial condition, and results of operations.

We operate in a competitive market which may intensify, and competition may limit our ability to implement our business model and have a material adverse effect on our business, financial condition, and results of operations. Our competitors may be able to have a lower cost for their services which would lead to borrowers choosing such other competitors over the Company. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of loans and investments, offer more attractive pricing or other terms and establish more relationships than us.

| 4 |

The recent outbreak of the coronavirus may cause an overall decline in the economy as a whole and may materially harm our business, results of operations and financial condition.

If the recent outbreak of the coronavirus continues to grow, the effects of such a widespread infectious disease and epidemic may cause an overall decline in the economy as a whole. The actual effects of the spread of coronavirus are difficult to assess at this time as the actual effects will depend on many factors beyond the control and knowledge of the Company. However, the spread of the coronavirus, if it continues may cause an overall decline in the economy as a whole and therefore may materially harm our business, results of operations and financial condition.

Risks Related to Our Company

We have a history of losses which we expect to continue.

The Company is currently not profitable. The Company expects that it will lose money in the foreseeable future, and we may not be able to achieve profitable operations. In order to achieve profitable operations, we will need to raise significant proceeds from the sale of Worthy II Bonds and effectively deploy those proceeds by making secured loans or other permissible investments that provide a sufficient return to pay the interest payments on the Worthy II Bonds, fund our operating expenses and generate a net profit. The Company cannot be certain that its business will be successful or that it will generate significant revenues and become profitable. An investment in the Company is highly speculative, and no assurance can be given that the stockholders will realize any return on their investment or that they will not lose their entire investment.

There is substantial doubt about our ability to continue as a going concern.

In 2019 we generated net losses and had cash used in operations of approximately $3,713,000 and $1,686,000, respectively. At December 31, 2019 we had a shareholder’s deficit and accumulated deficit of approximately $3,770,000, and $4,986,000, respectively. These conditions raise substantial doubt about our ability to continue as a going concern. Our unaudited consolidated financial statements appearing later in this report have been prepared assuming that we will continue as a going concern. No assurances can be given that we will achieve success in selling any material amount of Worthy II Bonds, or that our operations will provide sufficient revenues to cover interest payments on the Worthy II Bonds and our operating expenses.

We may need to raise additional capital.

We may have substantial future cash requirements but no assured financing source to meet such requirements. To date, our revenues have been minimal and we do not presently generate sufficient revenues to pay the interest on the Worthy Bonds, the Worthy II Bonds and fund our operating expenses. Our future capital requirements will depend on a number of factors, including our ability to generate sufficient “spread” between the interest rate on the Worthy Bonds and the interest Worthy Lending receives from loans and other permissible investments it makes using proceeds it received from the sale of Worthy Bonds. Our future capital requirements will also depend on our ability to generate sufficient “spread” between the interest rate on the Worthy II Bonds and the interest Worthy Lending II receives from loans and other permissible investments it makes using proceeds from the sale of Worthy II Bonds. If adequate funds are not available, the Company may be required to delay or scale back its business plan.

We may experience losses on the loans we make or other permissible investments by Worthy Peer and Worthy Peer II.

While the loans made by Worthy Lending and to be made by Worthy Lending II are and are planned to be primarily secured by the assets of the borrowers, there is no assurance that general economic conditions or the specific business and financial condition of the borrower, will not result in loan defaults. In that event, we would incur the costs to foreclose on our secured interests and there are no assurances that the amount we may recover from the disposal of the assets will equal the amounts of the obligation and associated costs.

| 5 |

Competition for employees is intense, and we may not be able to attract and retain the highly skilled employees whom we need to support our business.

Currently, our staffing needs are satisfied by a total of 14 full time employees and independent contractors who provide a substantial portion of their time to us. We will need to expand our employee base as our company continues to grow. Competition for highly skilled personnel, especially data analytics personnel, is extremely intense, and we could face difficulty identifying and hiring qualified individuals in many areas of our business. We may not be able to hire and retain such personnel. Many of the companies with which we compete for experienced employees have greater resources than we have and may be able to offer more attractive terms of employment. In addition, we intend to invest significant time and expense in training our employees, which increases their value to competitors who may seek to recruit them. If we fail to retain our employees, we could incur significant expenses in hiring and training their replacements and the quality of our services and our ability to serve borrowers could diminish, resulting in a material adverse effect on our business.

We have a limited operating history in a rapidly evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

We have a limited operating history in an evolving industry that may not develop as expected. Assessing our business and future prospects is challenging in light of the risks and difficulties we may encounter. These risks and difficulties include our ability to:

| ● | continue to sell Worthy II Bonds; | |

| ● | expand the user base for the Worthy App and the Worthy Website; | |

| ● | increase the number and total volume of loans and other credit products extended to borrowers; | |

| ● | improve the terms on which loans are made to borrowers as our business becomes more efficient; | |

| ● | increase the effectiveness of our direct marketing and lead generation through referral sources; | |

| ● | successfully develop and deploy new products; | |

| ● | favorably compete with other companies that are currently in, or may in the future enter, the business of lending to small businesses; | |

| ● | successfully navigate economic conditions and fluctuations in the credit market; | |

| ● | effectively manage the growth of our business; and | |

| ● | successfully expand our business into adjacent markets. |

We may not be able to successfully address these risks and difficulties, which could harm our business and cause our operating results to suffer.

We have begun to make loans with the proceeds from the sale of the Worthy Bonds, however our lending history is limited.

Worthy Lending made its first loan in September 2018 and as of April 27, 2020, Worthy Lending has 34 outstanding loans. While we have identified several additional opportunities for investment, our lending history is limited. Interest on the proceeds from the Regulation A offerings of Worthy Peer and Worthy Peer II will not cover interest payments accruing on the bonds or our operating expenses. Accordingly, until such time as we are able to generate significant income we will be required to utilize cash on hand to make the interest payments which will reduce the amount of proceeds available for loans by us.

If the information provided by borrowers is incorrect or fraudulent, we may misjudge a customer’s qualification to receive a loan, and our operating results may be harmed.

Our loan participation or loan decisions are based partly on information provided to us by loan applicants. To the extent that these applicants provide information to us in a manner that we are unable to verify, we may not be able to accurately assess the associated risk. In addition, data provided by third-party sources is a significant component of our underwriting process, and this data may contain inaccuracies. Inaccurate analysis of credit data that could result from false loan application information could harm our reputation, business, and operating results.

| 6 |

Our risk management efforts may not be effective.

We could incur substantial losses, and our business operations could be disrupted if we are unable to effectively identify, manage, monitor, and mitigate financial risks, such as credit risk, interest rate risk, liquidity risk, and other market-related risk, as well as operational risks related to our business, assets, and liabilities. To the extent our models used to assess the creditworthiness of potential borrowers do not adequately identify potential risks, the risk profile of such borrowers could be higher than anticipated. Our risk management policies, procedures, and techniques may not be sufficient to identify all of the risks we are exposed to, mitigate the risks that we have identified, or identify concentrations of risk or additional risks to which we may become subject in the future.

We rely on various referral sources and other borrower lead generation sources, including lending platforms.

Unlike banks and other larger competitors with significant resources, we rely on our smaller-scale marketing efforts, affinity groups, partners, and loan referral services to acquire borrowers. We do not have exclusive rights to referral services, and we cannot control which loans or the volume of loans we are sent. In addition, our competitors may enter into exclusive or reciprocal arrangements with their own referral services, which might significantly reduce the number of borrowers we are referred. Any significant reduction in borrower referrals could have an adverse impact on our loan volume, which will have a correspondingly adverse impact on our operations and our Company.

Our loans may be unsecured obligations of our borrowers.

We believe that some of our loans may be unsecured obligations of the borrowers. This means that, for those loans, we will not be able to foreclose on any assets of our borrowers in the event that they default. This limits our recourse in the event of a default. We may also attract borrowers who have fewer assets and may be engaged in less developed businesses than our peers. If we are unable to access collateral on our loans that default, our results of operations may be adversely impacted.

A significant disruption in our computer systems or a cybersecurity breach could adversely affect our operations.

We rely extensively on our computer systems to manage our loan origination and other processes. Our systems are subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, cyber security breaches, vandalism, severe weather conditions, catastrophic events and human error, and our disaster recovery planning cannot account for all eventualities. If our systems are damaged, fail to function properly or otherwise become unavailable, we may incur substantial costs to repair or replace them, and may experience loss of critical data and interruptions or delays in our ability to perform critical functions, which could adversely affect our business and results of operations. Any compromise of our security could also result in a violation of applicable privacy and other laws, significant legal and financial exposure, damage to our reputation, loss or misuse of the information and a loss of confidence in our security measures, which could harm our business.

Our ability to protect the confidential information of our borrowers and investors may be adversely affected by cyber-attacks, computer viruses, physical or electronic break-ins or similar disruptions.

We process certain sensitive data from our borrowers and investors. While we have taken steps to protect confidential information that we receive or have access to, our security measures could be breached. Any accidental or willful security breaches or other unauthorized access to our systems could cause confidential borrower and investor information to be stolen and used for criminal purposes. Security breaches or unauthorized access to confidential information could also expose us to liability related to the loss of the information, time-consuming and expensive litigation and negative publicity. If security measures are breached because of third-party action, employee error, malfeasance or otherwise, or if design flaws in our software are exposed and exploited, our relationships with borrowers and investors could be severely damaged, and we could incur significant liability.

Because techniques used to sabotage or obtain unauthorized access to systems change frequently and generally are not recognized until they are launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. In addition, federal regulators and many federal and state laws and regulations require companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach are costly to implement and often lead to widespread negative publicity, which may cause borrowers and investors to lose confidence in the effectiveness of our data security measures. Any security breach, whether actual or perceived, would harm our reputation, we could lose borrowers and investors and our business and operations could be adversely affected.

| 7 |

Any significant disruption in service on our platform or in our computer systems, including events beyond our control, could prevent us from processing or posting payments on loans, reduce the attractiveness of our marketplace and result in a loss of borrowers or investors.

In the event of a system outage and physical data loss, our ability to perform our servicing obligations, process applications or make loans available would be materially and adversely affected. The satisfactory performance, reliability and availability of our technology are critical to our operations, customer service, reputation and our ability to attract new and retain existing borrowers and investors.

Any interruptions or delays in our service, whether as a result of third-party error, our error, natural disasters or security breaches, whether accidental or willful, could harm our relationships with our borrowers and investors and our reputation. Additionally, in the event of damage or interruption, our insurance policies may not adequately compensate us for any losses that we may incur. Our disaster recovery plan has not been tested under actual disaster conditions, and we may not have sufficient capacity to recover all data and services in the event of an outage. These factors could prevent us from processing or posting payments on the loans, damage our brand and reputation, divert our employees’ attention, reduce our revenue, subject us to liability and cause borrowers and investors to abandon our marketplace, any of which could adversely affect our business, financial condition and results of operations.

We contract with third parties to provide services related to our online web lending and marketing, as well as systems that automate the servicing of our loan portfolios. While there are material cybersecurity risks associated with these services, we require that our vendors provide industry-leading encryption, strong access control policies, Statement on Standards for Attestation Engagements (SSAE) 16 audited data centers, systematic methods for testing risks and uncovering vulnerabilities, and industry compliance audits to ensure data and assets are protected. To date, we have not experienced any cyber incidents that were material, either individually or in the aggregate.

If our estimates of loan receivable losses are not adequate to absorb actual losses, our provision for loan receivable losses would increase, which would adversely affect our results of operations.

We maintain an allowance for loans receivable losses. To estimate the appropriate level of allowance for loan receivable losses, we consider known and relevant internal and external factors that affect loan receivable collectability, including the total amount of loan receivables outstanding, historical loan receivable charge-offs, our current collection patterns, and economic trends. If customer behavior changes as a result of economic conditions and if we are unable to predict how the unemployment rate, housing foreclosures, and general economic uncertainty may affect our allowance for loan receivable losses, our provision may be inadequate. Our allowance for loan receivable losses is an estimate, and if actual loan receivable losses are materially greater than our allowance for loan receivable losses, our financial position, liquidity, and results of operations could be adversely affected.

We will face increasing competition and, if we do not compete effectively, our operating results could be harmed.

We compete with other companies that lend to small businesses. These companies include traditional banks, merchant cash advance providers, and newer, technology-enabled lenders. In addition, other technology companies that lend primarily to individual consumers, such as Lending Club and Prosper Marketplace, have already begun to focus, or may in the future focus, their efforts on lending to small businesses. If we are not able to compete effectively with our competitors, our operating results could be harmed.

Many of these competitors have significantly more resources and greater brand recognition than we do and may be able to attract borrowers more effectively than we do.

When new competitors seek to enter one of our markets, or when existing market participants seek to increase their market share, they sometimes undercut the pricing and/or credit terms prevalent in that market, which could adversely affect our market share or ability to explore new market opportunities. Our pricing and credit terms could deteriorate if we act to meet these competitive challenges. Further, to the extent that the fees we pay to our strategic partners and borrower referral sources are not competitive with those paid by our competitors, whether on new loans or renewals or both, these partners and sources may choose to direct their business elsewhere. All of the foregoing could adversely affect our business, results of operations, financial condition, and future growth.

| 8 |

The collection, processing, storage, use, and disclosure of personal data could give rise to liabilities as a result of governmental regulation, conflicting legal requirements, or differing views of personal privacy rights.

We receive, collect, process, transmit, store, and use a large volume of personally identifiable information and other sensitive data from borrowers and purchasers of the Worthy Bonds and Worthy II Bonds and services. There are federal, state, and foreign laws regarding privacy, recording telephone calls, and the storing, sharing, use, disclosure, and protection of personally identifiable information and sensitive data. Specifically, personally identifiable information is increasingly subject to legislation and regulations to protect the privacy of personal information that is collected, processed, and transmitted. Any violations of these laws and regulations may require us to change our business practices or operational structure, address legal claims, and sustain monetary penalties, or other harms to our business.

The regulatory framework for privacy issues in the United States and internationally is constantly evolving and is likely to remain uncertain for the foreseeable future. The interpretation and application of such laws is often uncertain, and such laws may be interpreted and applied in a manner inconsistent with other binding laws or with our current policies and practices. If either we or our third-party service providers are unable to address any privacy concerns, even if unfounded, or to comply with applicable laws and regulations, it could result in additional costs and liability, damage our reputation, and harm our business.

We are reliant on the efforts of Sally Outlaw and Alan Jacobs.

We rely on our management team and need additional key personnel to grow our business, and the loss of key employees or inability to hire key personnel could harm our business. We believe our success has depended, and continues to depend, on the efforts and talents of our executive officers, Sally Outlaw, our Chief Executive Officer, and Alan Jacobs, our Executive Vice President. Ms. Outlaw and Mr. Jacobs have expertise that could not be easily replaced if we were to lose any or all of their services. We currently do not have employment agreements with our executive officers.

The nature of our business may subject us to regulation as an investment company pursuant to the Investment Company Act of 1940.

We believe that Worthy Peer and Worthy Peer II fall within the exception of an investment company provided by Section 3(c)(5)(A) and/or Section 3(c)(5)(B) of the Investment Company Act of 1940. Section 3(c)(5)(A) provides an exemption for a company that is primarily engaged in purchasing or otherwise acquiring notes representing part or all of the sales price of merchandise and/or services. Section 3(c)(5)(B) provides an exemption for a company that is primarily engaged in making loans to manufacturers, wholesalers and retailers of and to prospective purchasers of specified merchandise and/or services. To a lesser extent (not more than 40%) Worthy Peer and Worthy Peer II may also make secured loans to other types of borrowers provided the amount and nature of such loans does not cause us to lose our exemption from the registration requirements of the Investment Company Act of 1940. If for any reason we fail to meet the requirements of the exemptions provided by Section 3(c)(5)(A) or 3(c)(5)(B) Worthy Peer and Worthy Peer II will be required to register as an investment company, which could materially and adversely affect our business.

Holders of Worthy Bonds and Worthy II Bonds are exposed to our credit risk.

Worthy Bonds and Worthy II Bonds are our full and unconditional obligations. If we are unable to make payments required by the terms of the notes bondholders will have an unsecured claim against us. Worthy Bonds and Worthy II Bonds are therefore subject to non-payment by us in the event of our bankruptcy or insolvency. In an insolvency proceeding, there can be no assurances that bondholders will recover any remaining funds. Moreover, bondholder claims may be subordinate to that of any senior creditors and any secured creditors to the extent of the value of their security.

| 9 |

We are subject to the risk of fluctuating interests rates, which could harm our business operations.

We expect to generate net income from the difference between the interest rates we charge borrowers or otherwise make from our permissible investments, including loan origination fees paid by borrowers, and the interest we pay to the holders of Worthy Bonds and Worthy II Bonds. Due to fluctuations in interest rates, we may not be able to charge borrower’s an interest rate sufficient for us to generate income, which could harm our planned business operations.

There is no public market for shares of our common stock, and none is expected to develop.

There is no public market for our common stock and the Company does not expect that such a market will develop in the near future. Securities offered and sold to the Company’s stockholders pursuant to Section 4(a)(6) were subject to certain restrictions on transfer for the one-year period following the sale. See “Restrictions on Transfer.” Shareholders may be unable to liquidate their investment immediately and should be prepared to hold their shares for at least one year, but potentially indefinitely.

Worthy Financial, Inc. was formed on February 24, 2016 as a Delaware corporation. Our principal address is One Boca Commerce Center, 551 NW 77 Street, Suite 212, Boca Raton, FL, 33487. Our phone number is (561) 288-8467. The information which appears on, or is accessible through our websites at www.worthy.us, www.worthybonds.com and www.worthylending.com is not a part of, and is not incorporated by reference into, this Annual Report.

The Company was organized to create a “Worthy Community” which we were initially targeting to the millennials who are surpassing the baby boomers as the nation’s largest living generation. Management believes that this demographic in large part has a basic distrust of old guard financial institutions, is burdened by student loans and other debt, change employment frequently and is unable to save money and/or fund a retirement program.

Worthy Fintech Platform

We have developed technology solutions, including the Worthy App and the Worthy Website, that previously facilitated the purchase of Worthy Bonds from Worthy Peer and are currently facilitating the purchase of Worthy II Bonds from Worthy Peer II and provides information on accounts of the Worthy Bond and Worthy II Bond investors. The Company intends in the future to be compensated by its subsidiaries for use of the Worthy Fintech Platform. We refer to these each as the “Worthy App,” the “Worthy Website” and together as the “Worthy Fintech Platform.”

Worthy App

The Worthy App was designed to support the target market for our bonds which we believe is approximately 74 million millennials, who spend more than $600 billion a year. The Worthy App seeks to provide an easy way for our target market to micro invest including monetizing their debit card purchases, checking account linked credit card purchases and other checking account transactions by “rounding up” each purchase to the next highest dollar until the “round up” reaches $10.00 at which time the user would purchase a $10.00 Worthy Bond from Worthy Peer before the closing of the Worthy Peer Regulation A offering, which closed on March 17, 2020 and can be sued to purchase Worthy II Bonds from Worthy Peer II in their current Regulation A offering. The Worthy App is available via the web at worthybonds.com or for Apple iPhone users from the Apple Store and for Android phone users from Google Play.

Worthy Website

By accessing our website atwww.worthybonds.com, prospective investors could create a username and password, and indicate agreement to our terms and conditions and privacy policy.

| 10 |

The following features are available to participants in the Worthy Bonds and Worthy II Bonds program through our website:

| ● | Available Online Directly from Us. Users could previously purchase Worthy Bonds from Worthy Peer through our website prior to the completion of the Worthy Bonds offering, and users can purchase Worthy II Bonds from Worthy Peer II directly through our website; | |

| ● | No Purchase Fees Charged. We have not charged any commission or fees to purchase Worthy Bonds or Worthy II Bonds through our website. Purchasers may have been or may be charged a transaction fee if their method of payment required or requires us to incur an expense. The transaction fee was and will be equal to the amount that the we are charged by the payment processor. However, other financial intermediaries, if engaged by an investor, may have charged commissions or fees; | |

| ● | Invest as Little as $10. Users were able to build ownership of Worthy Bonds, and are able to build ownership of Worthy II Bonds over time by making purchases as low as $10; | |

| ● | Flexible, Secure Payment Options. Users were able to purchase Worthy Bonds electronically or by wire transfer from Worthy Peer through our website prior to the completion of the Worthy Bonds offering, and are able to purchase Worthy II Bonds electronically or by wire transfer from Worthy Peer II through our website; and | |

| ● | View Your Portfolio Online. Users can view their investments, returns, and transaction history online, as well as receive tax information and other portfolio reports. |

In addition to the millennials, we may also seek to establish strategic relationships with local and national companies to incorporate our services to the benefits it provides to its hourly employees, borrowers and users, as well as veterans and municipal employees and colleges and university alumni associations.

Our Subsidiaries: Worthy Peer and Worthy Peer II

Our business is primarily conducted through our Worthy Peer and Worthy Peer II subsidiaries, and their subsidiaries. Under our subsidiaries’ business models, we intend to generate revenue in multiple ways: through fees charged to borrowers, interest generated from each loan that we make or in which we participate and fees from ancillary services that we introduce to our Worthy members and others provided by us.

Worthy Peer and Worthy Lending

Worthy Peer provides at least 60% of its assets to be used for (i) loans to manufacturers, wholesalers and retailers secured by inventory and/or equipment, and (ii) purchase order financing. To a lesser extent (not more than 40% of assets), Worthy Peer may also provide (i) secured loans to other borrowers, (ii) acquire equity interests in real estate; (iii) make fixed income investments; and (iv) provide factoring financing, provided the amount and nature of such activities does not cause it to lose its exemption from regulation as an investment company pursuant to the Investment Company Act of 1940.

Worthy Bonds Offering

In January 2018 Worthy Peer launched an offering pursuant to Regulation A of the Securities Act of 1933, as amended (the “Securities Act”) under the terms of an offering circular that was initially qualified by the SEC on January 4, 2018. On March 17, 2020, the offering was completed. From January 2018 through March 17, 2020, Worthy Peer sold approximately $50 million aggregate principal amount of Worthy Bonds to 12,285 investors. Notwithstanding the completion of the offering, Worthy Peer inadvertently sold after March 17, 2020, $630,380 more than the maximum offering amount allowable under the offering statement due to a coding error as to redemption transactions in our software. As a result of the oversubscription, on March 25, 2020, Worthy Peer rescinded the purchase and sale of the oversubscribed bonds by refunding and crediting the accounts of the 2,250 purchasers of the oversubscribed bonds their respective investment amounts, without any deduction therefrom, and cancelling the oversubscribed bonds.

| 11 |

The Worthy Bonds:

| ● | were priced at $10.00 each; | |

| ● | represent a full and unconditional obligation of Worthy Peer; | |

| ● | bear interest at 5% per annum; | |

| ● | have a term of three years, renewable at the option of the bond holder for up to two additional three-year terms; | |

| ● | may be subject to a put by the holder at a 1% discount (if implemented, may be charged only if exercised during the first year and chargeable against accrued interest and if a put is for more than $50,000, holder must give us 30 days prior written notice); | |

| ● | are subject to a call by Worthy Peer; and | |

| ● | are not payment dependent on any underlying small business loan. |

The Worthy Bonds are not dependent upon any particular loan and remain at all times the general obligations of Worthy. The Worthy Bonds were being offered pursuant to Regulation A of Section 3(6) of the Securities Act of 1933, as amended, for Tier 2 offerings. Proceeds from the sale of the Worthy Bonds were used to fund loans and for general corporate purposes, including the costs of the offering.

Since Worthy Peer has completed the offering, it may no longer offer interest reinvestment in Worthy Bonds under the auto-invest program to bondholders who selected this reinvestment feature as Worthy Peer may not issue any more Worthy Bonds under the offering statement. In lieu of interest reinvestment in Worthy Bonds, Worthy Peer will pay interest on interest (compounded interest) and credit such interest to such bondholders’ accounts.

Worthy Peer’s Loan and Investment Portfolio

Beginning in September of 2018, Worthy Peer began deploying the capital it had raised through the sale of Worthy Bonds in the offering through its subsidiary Worthy Lending by loaning funds directly to borrowers and through participation agreements with other lenders under loan agreements for an aggregate amount of $1,200,000, with small business borrowers based in the United States. During the year ended December 31, 2019 Worthy Peer loaned an additional aggregate amount of $9,269,017 to small business borrowers based in the United States. The balance due Worthy Peer at December 31, 2019 was $10,469,017.

The loans pay interest at varying rates ranging from 0.62% per month to 1.5% per month and collateral management fees ranging from of 0.5% to 1% per month. The loan agreements have customary loan origination fees, which have been netted against loan costs with the net amount recorded as deferred revenue to be recognized as revenue over the term of the loan. One of the loans has an annual facility fee, which is being amortized into income over one year. The term of the loans range from two to three years, with no prepayment penalty and generally pay interest only in year one. The loans are secured by the assets of the borrowers. These investments were funded by sales of the Worthy Bonds. There was no loan allowance required at any time during the year ended December 31, 2018. The loan allowance was $1,841,315 at December 31, 2019.

During the year ended December 31, 2019, Worthy Peer invested in 8 loans for a total of $1,774,000, each loan is secured by a mortgage in the real estate, and is located in the state of Florida. Each loan has a maturity date of 2 years and matures on various dates ranging between March of 2021 and December of 2021.These loans pay interest at rates between 9.5% and 10.5% and is serviced by an outside, unrelated party.

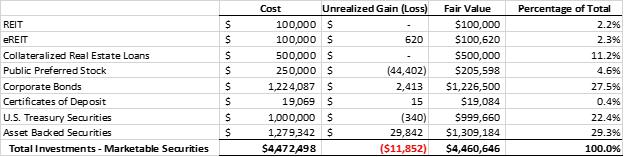

Worthy Peer maintains a portfolio of investments on its consolidated balance sheet as marketable securities held at fair value. Fair value includes gross unrealized gains, gross unrealized losses, accrued interest, and amortized cost. Worthy Peer typically invests in a portfolio of private market real estate investments with the primary objective to earn diversified risk-adjusted returns while the corporate bonds, certificates of deposit, asset backed securities, and U.S. treasury securities are intended to mitigate risk and minimize potential risk of principal loss. Worthy Peer’s investment policy limits the amount of credit exposure to any one issuer and targets 20% portfolio weight in the more conservative investments.

| 12 |

Worthy Peer II and Worthy Lending II

Our other wholly-owned subsidiary Worthy Peer II and its wholly owned subsidiary Worthy Lending II, is currently engaged in a Regulation A offering of its Worthy II Bonds under SEC File No. 024-11150 which was qualified by the SEC on March 17, 2020. Thus far, Worthy Peer II has sold approximately $5,600,000 Worthy II Bonds in the offering.

Worthy Peer II is an early stage company, which, through Worthy Lending II, plans to implement its business model. Worthy Peer II’s business model is centered primarily around providing loans for small businesses including loans to manufacturers, wholesalers, and retailers secured by inventory, accounts receivable and/or equipment and purchase order financing. To a lesser extent, Worthy Peer II may also provide loans to other borrowers, acquire equity interests in real estate, make fixed income and/or equity investments, provide factoring financing and other types of loans and investments provided the amount and nature of such activities does not cause Worthy Peer II to lose its exemption from regulations as an investment company pursuant to the Investment Company Act of 1940. Worthy Peer will sell Worthy II Bonds in its Regulation A offering to provide the capital for these activities.

Worthy II Bonds

The Worthy II Bonds:

| ● | are priced at $10.00 each; | |

| ● | represent a full and unconditional obligation of Worthy Peer II; | |

| ● | bear interest at 5% per annum, for clarification purposes, we will pay interest on interest (compounded interest) and credit such interest to bondholders’ Worthy accounts; | |

| ● | have a three-year term, renewable at the option of the bond holder for up to two additional three-year terms; | |

| ● | are redeemable at any time at the option of the holder subject to certain limitations as further discussed herein; | |

| ● | are subject to a call by us at any time; | |

| ● | are not payment dependent on any underlying small business or other loan; and | |

| ● | are unsecured. |

Worthy Peer II has generated limited revenue and has a limited operating history. Worthy Peer II expects to generate income from the difference between the interest rates it charges borrowers or otherwise makes from its permissible investments, including loan origination fees paid by borrowers, and the interest Worthy Peer II will pay to the holders of Worthy II Bonds. Worthy Peer II also expects to use up to 5% of the proceeds from sales of Worthy II Bonds to provide working capital for Worthy Peer II until such time as its revenues are sufficient to pay its operating expenses.

Competitive Strengths

We believe we benefit from the following competitive strengths compared to our competitors:

We are part of the Worthy Community. The Worthy App and websites are targeted to the millennials who are part of the fastest growing segment of our population. We believe that they have a basic distrust of traditional banking institutions yet they have a need to accumulate assets for retirement or otherwise. We believe that the Worthy FinTech Platform provides for a savings and investing alternative for the millennials.

We are part of the fast-growing online lending industry. Alternative lenders often provide a more appealing financing option to small businesses as they are usually more flexible than larger financial institutions on loan repayment terms and often approve loans much faster than banks. For example, online “peer-to-peer” lending website uses technology to meet market demand where traditional bank and institutional financing has become more difficult to obtain. Lenders often have significant cost advantages over banks, including lower overhead and the absence of branch offices and extensive sales forces. These efficiencies often make it easier for nonbanks to originate loans to borrowers whose options online were traditionally limited to bank.

We focus on an underserved banking sector. Due to higher costs, we believe that banks cannot profitably serve the small business lending market for commercial loans below $500,000. Indeed, traditional banks have been exiting the small business loan market for over a decade. We believe our small business loan program enables us to profitably participate in loans at these levels.

| 13 |

Strategy

Our strategy is to expand our network of online information, social networking, and institutional, (colleges and universities, charities, trade organizations, and employer) sources of introductions and referrals to our targeted users.

Regulation Crowdfunding Offering

In addition to the capital raise previously undertaken by Worthy Peer in its Regulation A offering and Worthy Peer II’s capital raise in its Regulation A offering, as described earlier in this section, in July 2018, we launched a crowdfunding offering pursuant to Section 4(a)(6) of the Securities Act and Regulation Crowdfunding (the “Offering”). The Offering was conducted on the crowdfunding portal assessable at www.startengine.com and each subdomain thereof, which is owned by StartEngine Crowdfunding, Inc. (“StartEngine Crowdfunding”) and operated by StartEngine Crowdfunding and its wholly-owned subsidiary StartEngine Capital, LLC.

We raised net proceeds of $241,695 in the Offering in exchange for the issuance of 54,358 shares of our common stock. The proceeds received were net of costs incurred in connection with the Offering. The Offering was terminated in February 2019.

Employees

We have 14 full-time employees, together with one independent contractor who provides a substantial portion of his time to us. The following table provides the annual compensation for each of our executive officers during 2019.

| Name | Total Compensation Received in 2019 | |||

| Sally Outlaw | $ | 81,000 | ||

| Alan Jacobs | $ | 210,145 | (1) | |

| Jang Centofanti | $ | 108,608 | (2) | |

| (1) | $82,500 was received from Worthy Peer Capital, Inc., $30,000 was received from Worthy Financial, Inc. and $97,645 was received from Worthy Lending, LLC. | |

| (2) | $57,759 was received from Worthy Peer, Inc. and $50,849 was received from Worthy Lending, LLC. |

Our executive officers and directors are as follows:

| Name | Age | Positions | ||

| Sally Outlaw | 57 | Chief Executive Officer, President, Co-Founder, Director | ||

| Alan Jacobs | 78 | Executive Vice President, Chief Strategy Officer, Director | ||

| Jungkun “Jang” Centofanti | 52 | Vice President, Operations, Secretary | ||

| Dara Albright | 50 | Director | ||

| Stefanie Crowe | 51 | Director | ||

| Todd Lazenby | 53 | Director |

| 14 |

Sally Outlaw. Ms. Outlaw, a life-long entrepreneur who is passionate about opening up economic opportunity for all, has served as an officer and director of our Company since founding it in 2016. Ms. Outlaw is also the Chief Executive Officer and director of Worthy Peer. Ms. Outlaw is also the President, Chief Executive Officer and a director of Worthy Peer II. Since October 2019 she has served as President, Chief Executive Officer and a member of the Board of Directors of Worthy Management. From October 2010 to December 2015 she was the president of Peerbackers LLC, which engaged in all aspects of crowd funding and provides services to help clients navigate the world of crowd finance including the capital and investment opportunities offered through The JOBS ACT. Ms. Outlaw is also president and CEO of Peerbackers Advisory LLC, an SEC-registered investment advisor and a wholly owned subsidiary of the Company. Ms. Outlaw received her B.A. in Communications and Media Studies from the University of Minnesota in 1984 and holds a Series 65 license as a Registered Investment Advisor. Ms. Outlaw brings knowledge and experience in the financial industry, which we believe is of great value to our Company.

Alan Jacobs. Mr. Jacobs, who has more than 40 years of experience as a corporate and securities attorney, investment banker, business and financial advisor and entrepreneur/senior executive of both private and public companies, has been an officer and director of our Company since 2016. Mr. Jacobs is also the Executive Vice President and Chief Operating Officer and a director of Worthy Peer and president of Worthy Lending. Mr. Jacobs is also the Executive Vice President, Chief Operating Officer and a member of the Board of Directors of Worthy Peer II and also serves as the president of Worthy Lending II. Since October 2019 he has served as Executive Vice President, Chief Operating Officer and a member of the Board of Directors of Worthy Management. For more than the past five years he has been engaged as a business consultant for various early stage companies. From 2016 to 2018 Mr. Jacobs was the Founder and President of CorpFin Management Group where he was focused on business development, strategic planning and corporate management. From September 2014 to December 2015, Mr. Jacobs was associated with ViewTrade Securities, a FINRA registered broker-dealer where he was focused on advisory and corporate services. Prior to that time and for more than 30 years, Mr. Jacobs was associated with several FINRA registered broker-dealers including Ladenburg Thalman, Josephthal & Company, and Capital Growth Securities. Mr. Jacobs received his bachelor’s degree from Franklin and Marshall College in 1963 and law degree from Columbia University in 1966. He was also president of Wheelchair Fitness Inc. and director of business development of SSTI, Inc. from 2015 to 2018. Mr. Jacobs brings knowledge and experience in the financial industry, which we believe is of great value to our Company

Jungkun (“Jang”) Centofanti. Ms. Centofanti, who has more than 25 years of operational and management experience in a variety of consumer services industries including hospitality, banking and education, has been an officer of our Company since 2017. Ms. Centofanti, has served as Worthy Lending’s senior vice president and chief administrative officer since August 2018. Ms. Centofanti also serves as theSenior Vice President, Chief Administrative Officer and Secretary ofWorthy Peer II since October 2019. She is also Senior Vice President and Chief Administrative Officer of Worthy Lending II.Since October 2019 she has served as Senior Vice President, Chief Administrative Officer and Secretary of Worthy Management. From September 2016 to July 2018 she was Senior Vice President of CorpFin Management Group, a South Florida-based business development and strategic planning company where she handled all aspects of administration, and from January 2017 to July 2018 she served as Vice President of Wheelchair Fitness Solution Inc. Prior to joining CorpFin Management Group, from 2011 to June 2015 she was Administrative and Customer Service Manager for DU20 Holistic Oasis, and from 2004 until 2010 she was Preschool Director for Hazel Crawford School, both South Florida-based companies. Ms.Centofantireceived an Associate of Science in Fashion Marketing and Business from the Art Institute of Fort Lauderdale in 1989.

Dara Albright. Ms. Albright has been a director of our company since 2016. A recognized speaker, writer and influencer on topics covering financial disruption, FinTech, RegTech, Digital/Crowd-Finance, she has been Chief Executive Officer of Dara Albright Media since 2011. Ms. Albright possesses a distinguished 28-year career in financial services encompassing IPO execution, investment banking, trading, corporate communications, financial conference production as well as institutional and retail sales. Ms. Albright presently serves on the board of Entoro Wealth, a boutique investment firm that provides customized risk-mitigated strategies for digital currencies. Ms. Albright received her B.A. in psychology from George Washington University in 1991.

Stefanie Crowe. Ms. Crowe has been a director of our Company since April 2019. She is a wealth advisory and banking veteran, an entrepreneur and an angel investor. From 2014 to the present, she is a Co-Founder and General Partner of The JumpFund, an angel fund supporting female-led ventures. She serves as Director of Wealth, Knowledge & Happiness for Stone Bridge Asset Management, a registered investment advisor based in Chattanooga, TN from September 2016 to the present. After years with Bank of America/US Trust advising affluent families with wealth-building strategies including trust and estate management, investments, private banking and charitable planning, Ms. Crowe joined a de novo bank which facilitated a successful exit in 2015. While there, she launched their Trust & Wealth division and later directed the bank’s marketing, communications, investor relations, community relations and strategic planning efforts. Ms. Crowe obtained her BA in Anthropology from The University of Notre Dame in 1991 and her MBA from University of Tennessee at Chattanooga in 2003. She is a frequent presenter on topics of wealth-building, entrepreneurship, leadership and community-building and she has served on well over a dozen non-profit boards.

| 15 |

Todd Lazenby. Mr. Lazenby has been a director of our company since April 2019. Mr. Lazenby is the founder of Victory Partners bringing over 25 years of private equity, investment banking, and corporate finance experience to the firm, having held increasing senior level positions in start-ups, mid-sized and Fortune 500 companies. He has built an investment and advisory firm catering to wealthy families and family offices that has made control investments in companies comprising over $300 million in enterprise value and has arranged and overseen in excess of $3.0 billion in capital markets and mergers and acquisitions transactions. Prior to founding Victory Partners, Mr. Lazenby was the Managing Partner of Summit Capital Partners, LLC based in Los Angeles, CA, then the managing partner of WP Capital Partners, L.P. based in Dallas, TX, both merchant banking firms representing middle market companies on a national basis. He holds a MS in Finance from Stanford University Graduate School of Business, a MBA and a BS in Communications from Florida State University, and a BSBA from Barry University.

Related Party Transactions

We were obligated to reimburse one of our officers, Alan Jacobs, for advancing us funds to cover costs such as filing fees and organizational expense. The balance due was $0 and $1,096 at December 31, 2019 and 2018, respectively, and was due on demand, unsecured and interest free. This amount was paid back subsequent to December 31, 2019.

During 2018 Ms. Outlaw converted $48,000 we owed her for prior advances to our company into shares of our common stock.

There is $100,000 due from Worthy Peer’s Chief Executive Officer (Sally Outlaw who is the Company’s Chief Executive Officer) and $100,000 due from its Chief Operating Officer (Alan Jacobs who is the Company’s Executive Vice President) to Worthy Peer. The $100,000 due from each are notes receivable accruing interest at 10% per annum. The notes are due August 26, 2022. The notes are secured by 101,772 and 101,771 of the common stock of the Company, respectively. The shares are being held by Worthy Lending, LLC to the extent of the obligation. As of December 31, 2019 the accrued interest on these loans totaled $6,667.

In March of 2020, Worthy Peer II entered into a loan receivable agreement with a small business of which its Chief Financial Officer, Joseph D’Arelli is a minority shareholder and a secured guarantor. The loan commitment is up to $500,000, to date Worthy Peer II has loaned $150,000. The loan receivable pays interest at 18% per annum and has a 3 year term. Worthy Peer II also received a 17.5% equity interest in the small business as a condition of the loan commitment.

OWNERSHIP AND CAPITAL STRUCTURES; RIGHTS OF THE SECURITIES

Ownership

The table below sets forth information as of April 27, 2020, for each person who is the beneficial owner of 20% or more of our outstanding voting equity securities, calculated on the basis of voting power and our officers and directors.

| Common Stock | ||||||||

| Name and Address of Beneficial Owner | Shares | % | ||||||

| Sally Outlaw | 536,598 | 41. 3 | % | |||||

| Alan Jacobs | 274,371 | 21.1 | % | |||||

| Jungkun (“Jang”) Centofanti(1) | 59,876 | 4.6 | % | |||||

| Todd Lazenby(2) | 10,000 | * | ||||||

| Dara Albright(2) | 10,000 | * | ||||||

| Stefanie Crowe(2) | 10,000 | * | ||||||

| All WFI officers and directors as a group (six persons)(1)(2) | 900,845 | 69.4 | % | |||||

| (1) | Includes 36,076 shares issuable upon the exercise of vested stock options. |

| (2) | Non-executive member of WFI’s Board of Directors. |

| 16 |

Capital Stock

Our authorized capital is 10,000,000 shares of common stock, par value $0.0001 per share, and 2,000,000 shares of blank check preferred stock, par value $0.0001 per share. At April 27, 2020, there were 1,299,030 shares of common stock and no shares of preferred stock issued and outstanding.

Common Stock

Voting rights.The holders of shares of our common stock are entitled to one vote for each share held of record on all matters submitted to a vote of our stockholders.

Dividend rights. Subject to preferences that may be granted to any then outstanding preferred stock, holder of shares of our common stock are entitled to receive ratably such dividends as may be declared by the Board of Directors out of funds legally available therefore, as well as any distribution to the stockholders. The payment of dividends on our common stock will be a business decision to be made by our Board of Directors from time to time based upon the results of our operations, our financial condition and any other factors that our Board of Directors considers relevant. Payment of dividends on our common stock may be restricted by law and by loan agreements, indentures and other transactions entered into by us from time to time. We have never paid a dividend on our common stock and we do not intend to pay dividends in the foreseeable future, which means that stockholders may not receive any return on their investment from dividends.

Rights to Receive Liquidation Distributions. In the event of our liquidation, dissolution, or winding up, holders of our common stock are entitled to share ratably in all of our assets remaining after payment of liabilities and the liquidation preference of any then outstanding preferred stock. The rights, preferences and privileges of the holders of our common stock are subject to, and may be adversely affected by, the rights of the holders of shares of any series of our preferred stock and any additional classes of preferred stock that we may designate in the future.

Preferred Stock

Our Board of Directors, without further stockholder approval, may issue preferred stock in one or more series from time to time and fix or alter the designations, relative rights, priorities, preferences, qualifications, limitations and restrictions of the shares of each series. The rights, preferences, limitations and restrictions of different series of preferred stock may differ with respect to dividend rates, amounts payable on liquidation, voting rights, conversion rights, redemption provisions, sinking fund provisions and other matters. Our Board of Directors may authorize the issuance of preferred stock, which ranks senior to our common stock for the payment of dividends and the distribution of assets on liquidation. In addition, our Board of Directors can fix limitations and restrictions, if any, upon the payment of dividends on both classes of our common stock to be effective while any shares of preferred stock are outstanding.

Stock Option Plan

During 2017, our Board of Directors approved a stock option plan for the issuance of up to 200,000 options. During 2018, we issued 106,400 stock options to three employees. During 2019, we issued 122,536 stock options to 6 employees.

On February 20, 2020, our Board of Directors approved a new stock option plan for the issuance of up to 200,000 options. No options have been issued under the 2020 plan at this time.

| 17 |

Convertible Notes

In January 2017, we issued a convertible note payable to a shareholder in the amount of $25,000. The note provided for interest at 9% and matured on January 17, 2019. At maturity, we issued 13,625 shares of common stock for the conversion of this convertible note payable.

During the year ended December 31, 2018, we issued nine convertible notes payable in the amount of $425,000.

During the year ended December 31, 2019, we sold an additional $310,000 of 9% convertible notes. The notes bear interest at 9% and mature in three years from the issuance date. At any time prior to the maturity date that we complete a “Qualified Financing,” the principal amount outstanding and all accrued but unpaid interest due is automatically converted into conversion shares at a discount ranging from 20% to 25% to the Qualified Financing valuation with conversion cap of $5,000,000 without any further action of the noteholder. A “Qualified Financing” is defined as an offering of our equity securities or convertible notes with net proceeds of not less than $3,000,000, either in a single transaction or in a series of transactions which close within six months of each other. In the event we do not have a Qualified Financing prior to the maturity date, holder has the option at the maturity date to convert the principal amount of the note, plus accrued interest, into common shares at a pre-conversion valuation of $5,000,000. Holders of convertible notes have no rights as stockholders of our Company, including the right to vote, until such time as the notes are converted into shares of our common stock in accordance with their respective terms.

What It Means to be a Minority Holder

A minority stockholder of shares of our common stock has a limited ability, if at all, to influence our policies and any other corporate matter, including the election of directors, changes to our corporate governance documents, additional issuances of securities, company repurchases of securities, a sale of the Company or the assets of the Company, or transactions with related parties.

Dilution

Investors should understand the potential for dilution. Each investor’s stake in the Company could be diluted due to the Company issuing additional shares of capital stock. In other words, when the Company issues more shares, the percentage of the Company that an investor owns will decrease, even though the value of the Company may increase. An investor will own a smaller piece of a larger company. The increases in the number of shares outstanding could result from a stock offering (such as an initial public offering, another crowdfunding round, a venture capital round or angel investment), employees exercising stock options, or by conversion of certain instruments (e.g., convertible notes, preferred shares or warrants) into common stock.

If we decide to issue more shares, an investor could experience value dilution, with each share being worth less than before, and control dilution, with the total percentage an investor owns being less than before. There may also be earnings dilution with a reduction in the amount earned per share (although this typically occurs only if we offer dividend and most companies at our stage are unlikely to offer any dividends, preferring to invest any earnings into the Company).

The type of dilution that hurts early-stage investors most likely occurs when a company sells more shares in a “down round,” meaning at a lower valuation than in earlier offerings.

If an investor is making an investment expecting to own a certain percentage of the Company or expecting each share to hold a certain amount of value, it is important to realize how the value of those shares can decrease by actions taken by the Company. Dilution can make drastic changes to the value of each share, ownership percentage, voting control and earnings per share.

| 18 |

Restrictions on Transfer

For the one-year period following issuance of shares of the Company’s common stock in the Offering, such shares may not be transferred, unless such securities are transferred:

| ● | to the Company; | |

| ● | to an accredited investor; | |

| ● | as part of an offering registered with the SEC; or | |

| ● | to a member of the original purchaser’s family or the equivalent, to a trust controlled by the purchaser, to a trust created for the benefit of a member of the family of the purchaser or the equivalent, or in connection it the death or divorce of the purchaser or similar circumstance. |

The term “accredited investor” means any person who becomes within any of the categories set forth in Rule 501(a) of Regulation D, or who the seller reasonably believes comes within any of such categories, at the time of the sale of securities to that person.

The term “member of the family of the investor or equivalent” includes a child, stepchild, grandchild, parent, stepparent, grandparent, spouse or spousal equivalent, sibling, mother-in-law, father-in-law, son-in-law, daughter-in-law, brother-in-law, or sister-in-law of the purchaser, and includes adoptive relationships. the term “spousal equivalent” means a cohabitant occupying a relationship generally equivalent to that of a spouse.

FINANCIAL STATEMENTS AND FINANCIAL CONDITION; MATERIAL INDEBTEDNESS

Financial Statements

Our unaudited consolidated financial statements for the year ended December 31, 2019 and 2018 can be found starting on page F-1 of this Annual Report. These consolidated financial statements are unaudited but have been certified by our Chief Executive Officer to be true and complete in all material respects.

Financial Condition

Operating Results

In 2019, our revenues included revenue from interest income, as well as loan fees. In 2018 our revenues included revenues from interest income, as well as loan fees as compared to revenues solely from interest income in 2017, which reflects our deployment of a portion of the proceeds from the sale of Worthy Bonds in 2018 to make loans and other permissible investments. Interest income represents interest we earn on investments and cash on deposit. Loan fees are charged to the borrowers during loan originations. These fees are offset against loan costs and then deferred to be recognized as non-interest income over the term of the loan. For term loans, we recognize interest income, loan fee income and collateral management fee income over the terms of the underlying loans. Loan fees and collateral management fees are reflected as non-interest income in our consolidated statement of operations. Loan fees typically include due diligence, appraisal and legal fees. Associated costs primarily include costs directly related to evaluating the financial performance of the prospective borrower, preparing and processing loan documentation, employees’ compensation directly related to the loan and costs paid to third parties for legal and appraisal services. The fees and the costs are netted as deferred revenue and amortized into revenue over the life of the loan.

Total interest income for the year ended December 31, 2019 was $771,226, an increase of $735,765 from the year ended December 31, 2018. This increase was the direct result of our increased loan portfolio. At December 31, 2019 our loans receivable held for investments, net balance and mortgage loans held for investment were $10,469,017 and $1,774,000, respectively, which was an increase of $9,269,017 and $1,774,000, respectively from December 31, 2018. Our provision for loan losses also increased at December 31, 2019 as a result of the increased loan portfolio. The balance at December 31, 2019 was $1,533,890 as compared to $0 at December 31, 2018.

Total interest expense for the year ended December 31, 2019 was $572,816, an increase of $545,519 from the year ended December 31, 2018. The increase was the direct result of our increased bond sales during the year ended December 31, 2019 as compared to the year ended December 31, 2018.

Non-interest income totaled $283,785 and consisted primarily of loan fees of $202,118, other income of $75,000, which was income earned by Worthy Peer as an award for being selected the top company in a business accelerator program competition. Also included in non-interest income is $6,667 of interest income from related parties. Included in non-interest income for the year ended December 31,2018 was $12,015 of loan fees.

| 19 |

Our total non-interest expenses included general and administrative expenses, as well as certain additional one-time expenses in 2019. Our general and administrative expenses increased substantially in 2019 as compared to 2018 which represents the growth of our company during 2019. This increase is primarily attributable to increases of approximately $138,000 in marketing expenses, approximately $560,000 in compensation expense, approximately $25,000in professional fees and approximately $350,000 in technology support costs during 2019 as compared to 2018. During 2020 we expect our general and administrative expenses to continue to increase as a result of the continued expansion of our operations and sales of the Worthy Bonds and the Worthy II Bonds. However, we are unable at this time to quantify these expected increases.

During 2019, our subsidiary Worthy Peer sold approximately $32,500,000 of Worthy Bonds and during 2019 approximately $7,700,000 of Worthy Bonds were redeemed. These Worthy Bonds have a three year term and accrue interest at 5%. During 2019 we incurred $566,388 interest on the Worthy Bonds. During 2018 we incurred $27,297 in interest on the Worthy Bonds. . As with the expected increases in our operating expenses, we also expect our interest expense will increase in 2020 as we sold additional Worthy Bonds and as we sell Worthy II Bonds.

Until such time as we begin generating sufficient revenues, if ever, we expect to continue to report net losses.

Liquidity and Capital Resources

At December 31, 2019, we had total shareholder’s deficit of approximately $3,770,000 as compared to a total shareholder’s deficit of approximately $317,000 at December 31, 2018. Our total assets increased substantially at December 31, 2019 as compared to December 31, 2018 which principally reflects approximately $8 million cash on hand from the sale of Worthy Bonds during the year ended December 31, 2019 and approximately $16.7 million of loans receivable held for investment, mortgage loans held for investment and other investments on our balance sheet Our total liabilities also increased substantially in the year ended December 31, 2019 as compared to the year ended December 31, 2018 which is principally related to the liabilities of approximately $27.6 million associated with the Worthy Bonds. We do not have any commitments for capital expenditures.

Net cash used in operating activities for 2019 was approximately $1,686,000 as compared to approximately $605,000 for 2018. In both periods cash was used primarily to fund our losses. Net cash provided by investing activities was approximately $17,035,000 in 2019 which represented primarily loans made and purchases of marketable securities, as compared to a $1,200,000 used in investing activities in 2018 representing loans made . Net cash provided by financing activities in 2019 was approximately $25,328,000, which primarily represented bonds sold less redemptions and to a lesser extent proceeds from the sale of convertible notes payable as compared to approximately $2,982,000 in 2018, which primarily represented net proceeds from the sale of bonds, convertible debt and of our common stocks.

Going Concern and Management’s Plans

The Company is dependent upon proceeds from sales of convertible debt and equity for working capital, and has incurred operating losses since inception. The accompanying unaudited consolidated financial statements have been prepared assuming that the Company will continue as a going concern. Throughout the next 12 months, the Company intends to fund its operations, including the payment of interest on the Worthy Bonds and Worthy II Bonds, with funding from sales of convertible debt and/or equity. The Company, however, is not a party to any binding agreement for the sale of convertible debt and/or equity. If the Company cannot raise any additional short-term capital, the Company may consume all of its cash reserved for operations. There are no assurances that management will be able to raise capital on terms acceptable to the Company. If the Company is unable to obtain sufficient amounts of additional capital, it may be required to reduce the scope of the Company’s planned development, which could harm its business, financial condition and operating results. The unaudited consolidated balance sheet does not include any adjustment that may result from these uncertainties.

| 20 |

Indebtedness

Since inception, the Company has funded a portion of its operations through capital received from the issuance of convertible promissory notes and, during 2018 and 2019, from the sale of Worthy Bonds. The following table provides information on the material indebtedness of the Company at December 31, 2019:

| Type | Principal Amount(2) | Interest Rate | Maturity Date | Other Material Terms | ||||

| Convertible Notes | $710,000 | 9% | Three years from the issuance date | At any time prior to the maturity date the principal amount outstanding and all accrued but unpaid interest due is automatically converted into conversion shares at a discount ranging from 20% to 25% to the Qualified Financing valuation with conversion cap of $5,000,000 without any further action of the noteholder. | ||||

| Worthy Bonds(1) | $27,605,438 | 5%, subject to our option to increase the interest rate up to an additional 1% per annum | Three years from the date of issuance | Renewable at the option of the bond holder; may be subject to a put by the holder at a 1% discount; subject to a call by Worthy Peer. |