Exhibit 99.2

2Q22 EARNINGS REPORT PennyMac Financial Services, Inc. August 2022

2 This presentation contains forward - looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding management’s beliefs, estimates, projections and assumptions with respect to, among other things, our financial results, future operations, business plans and in vestment strategies, as well as industry and market conditions, all of which are subject to change. Words like “believe,” “expect,” “anticipate,” “promise,” “project,” “plan,” and other expression s o r words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward - looking statements. Actual results and o perations for any future period may vary materially from those projected herein and from past results discussed herein. These forward - looking statements include, but are not limited to, statements rega rding the future changes in interest rates and prepayment rates; the impact of the COVID - 19 pandemic; future loan origination, servicing and production, including future production and operating e xpenses; future loan delinquencies and forbearances; future early buyout loans; future custodial balance earnings; future earnings and return on equity as well as other business and financial ex pectations. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not limited to: changes in prevailing interest rates; our expos ure to risks of loss and disruptions in operations resulting from adverse weather conditions, man - made or natural disasters, climate change and pandemics such as COVID - 19; the continually changing feder al, state and local laws and regulations applicable to the highly regulated industry in which we operate; lawsuits or governmental actions that may result from any noncompliance with the laws an d regulations applicable to our businesses; the mortgage lending and servicing - related regulations promulgated by the Consumer Financial Protection Bureau and its enforcement of these regulatio ns; our dependence on U.S. government - sponsored entities and changes in their current roles or their guarantees or guidelines; changes to government mortgage modification programs; the l ice nsing and operational requirements of states and other jurisdictions applicable to our business, to which our bank competitors are not subject; foreclosure delays and changes in foreclosure prac tic es; changes in macroeconomic and U.S. real estate market conditions; difficulties inherent in adjusting the size of our operations to reflect changes in business levels; purchase opp ort unities for mortgage servicing rights and our success in winning bids; our substantial amount of indebtedness; the discontinuation of LIBOR; increases in loan delinquencies and defaults; failure to mo dif y, resell or refinance early buyout loans; our reliance on PennyMac Mortgage Investment Trust (NYSE: PMT) as a significant source of financing for, and revenue related to, our mortgage banking bus iness; maintaining sufficient capital and liquidity and compliance with financial covenants; our obligation to indemnify third - party purchasers or repurchase loans if loans that we originate, acq uire, service or assist in the fulfillment of, fail to meet certain criteria or characteristics or under other circumstances; our obligation to indemnify PMT if our services fail to meet certain criteria o r c haracteristics or under other circumstances; decreases in the returns on the assets that we select and manage for our clients, and our resulting management and incentive fees; the extensive amount o f r egulation applicable to our investment management segment; conflicts of interest in allocating our services and investment opportunities among us and our advised entities; the effect o f p ublic opinion on our reputation; our ability to effectively identify, manage and hedge our credit, interest rate, prepayment, liquidity and climate risks; our initiation or expansion of new business act ivi ties or strategies; our ability to detect misconduct and fraud; our ability to mitigate cybersecurity risks and cyber incidents; our ability to pay dividends to our stockholders; and our organizational st ruc ture and certain requirements in our charter documents. You should not place undue reliance on any forward - looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by the Company with the Securities and Exchange Commission from time to time. The Company undertakes no obligation to p ubl icly update or revise any forward - looking statements or any other information contained herein, and the statements made in this presentation are current as of the date of this presentat ion only. This presentation contains financial information calculated other than in accordance with U.S. generally accepted accounting pri nciples (“GAAP”), such as pretax income excluding valuation - related items that provide a meaningful perspective on the Company’s business results since the Company utilizes this information to eva luate and manage the business. Non - GAAP disclosure has limitations as an analytical tool and should not be viewed as a substitute for financial information determined in accordance wi th GAAP. FORWARD - LOOKING STATEMENTS

SECOND QUARTER HIGHLIGHTS 3 3 PRODUCTION INVESTMENT MANAGEMENT Net income $129mm 2Q22 Results Diluted EPS (1) $2.28 Return on equity 15% Book value per share $65.38 Capital Return Shares repurchased 2.4mm Dividend per common share $0.20 Pretax income $10mm $4.3bn Government correspondent lock volume $11.3bn Broker direct lock volume $2.2bn $26.7bn Pretax income $0.2mm Assets under management $2.1bn Revenue $9.7mm Note: All figures are for 2Q22 or as of 6/30/22 (1) EPS = earnings per share. MSR = mortgage servicing rights. UPB = unpaid principal balance (2) Includes volume fulfilled or subserviced for PennyMac Mortgage Investment Trust (NYSE: PMT) (3) Excludes $233.8 million in MSR fair value gains, $176.0 million in hedging losses and a $21.5 million reversal related to pro vi sions for losses on active loans. See slide 13 for additional details. SERVICING Pretax income $168mm MSR (1) fair value changes and hedging results $58mm Pretax income excluding valuation - related items (3) $88mm MSR fair value changes and hedging impact to EPS $0.75 Total servicing portfolio UPB (1)(2) $527bn Total loan acquisitions and originations (2) Consumer direct lock volume

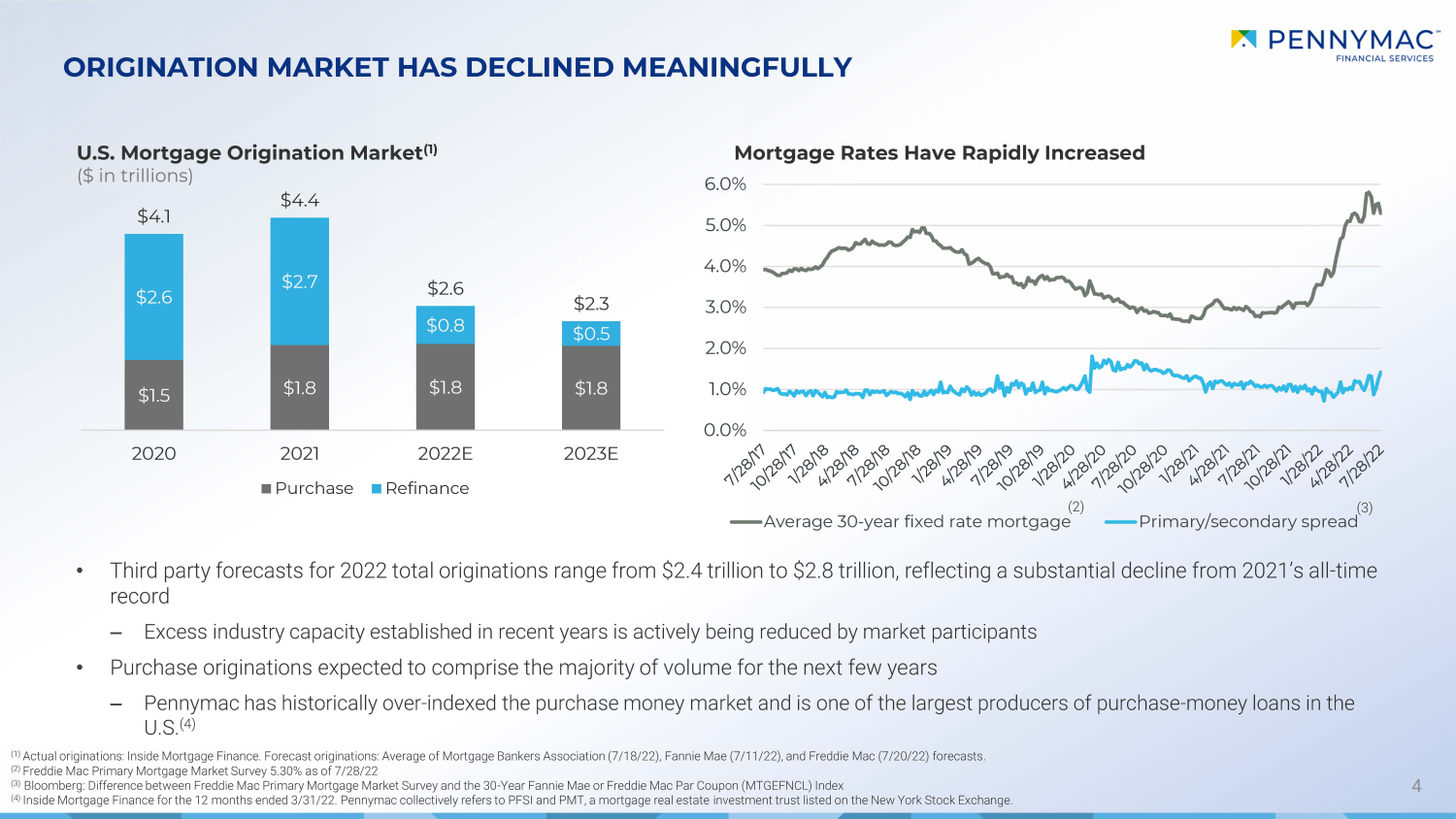

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% Average 30-year fixed rate mortgage Primary/secondary spread 4 ORIGINATION MARKET HAS DECLINED MEANINGFULLY U.S. Mortgage Origination Market (1) ($ in trillions) Mortgage Rates Have Rapidly Increased • Third party forecasts for 2022 total originations range from $2.4 trillion to $ 2.8 trillion, reflecting a substantial decline from 2021’s all - time record ‒ Excess industry capacity established in recent years is actively being reduced by market participants • Purchase originations expected to comprise the majority of volume for the next few years ‒ Pennymac has historically over - indexed the purchase money market and is one of the largest producers of purchase - money loans in the U.S. (4) (1) Actual originations: Inside Mortgage Finance. F orecast originations: Average of Mortgage Bankers Association ( 7 /18/22), Fannie Mae ( 7 /11/22), and Freddie Mac (7/20/22) forecasts . (2) Freddie Mac Primary Mortgage Market Survey 5.30 % as of 7/28/22 (3) Bloomberg: Difference between Freddie Mac Primary Mortgage Market Survey and the 30 - Year Fannie Mae or Freddie Mac Par Coupon ( MTGEFNCL) Index (4) Inside Mortgage Finance for the 12 months ended 3/31/22. Pennymac collectively refers to PFSI and PMT, a mortgage real estate in vestment trust listed on the New York Stock Exchange. (2) (3) $1.5 $1.8 $1.8 $1.8 $2.6 $2.7 $0.8 $0.5 $4.1 $4.4 $2.6 $2.3 2020 2021 2022E 2023E Purchase Refinance

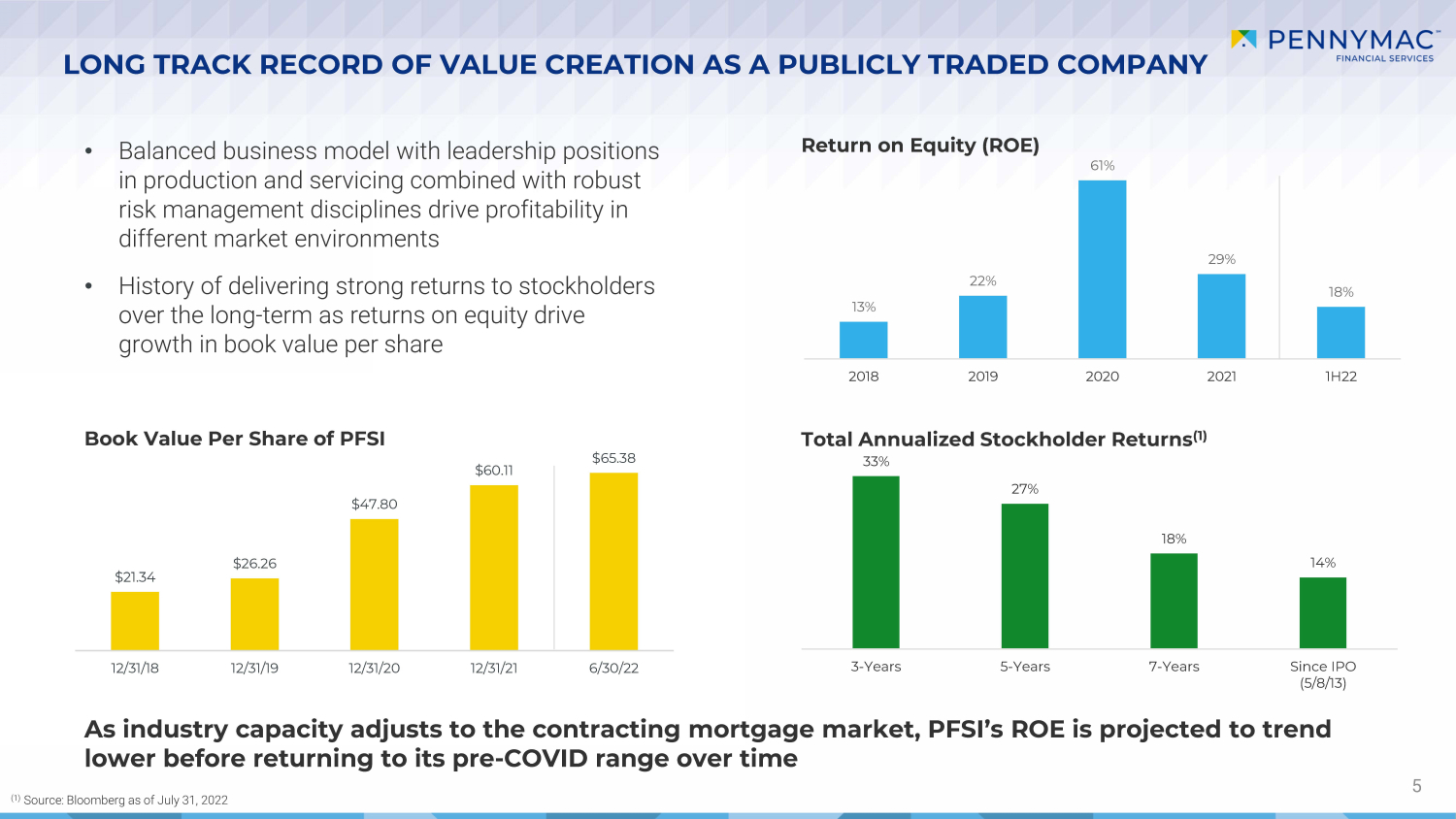

13% 22% 61% 29% 18% 2018 2019 2020 2021 1H22 $21.34 $26.26 $47.80 $60.11 $65.38 12/31/18 12/31/19 12/31/20 12/31/21 6/30/22 5 LONG TRACK RECORD OF VALUE CREATION AS A PUBLICLY TRADED COMPANY Book Value Per Share of PFSI Return on Equity (ROE) • Balanced business model with leadership positions in production and servicing combined with robust risk management disciplines drive profitability in different market environments • History of delivering strong returns to stockholders over the long - term as returns on equity drive growth in book value per share As industry capacity adjusts to the contracting mortgage market, PFSI’s ROE is projected to trend lower before returning to its pre - COVID range over time Total Annualized Stockholder Returns (1) (1) Source: Bloomberg as of July 31, 2022 33% 27% 18% 14% 3-Years 5-Years 7-Years Since IPO (5/8/13)

6 OPPORTUNITIES IN THE CURRENT MARKET ENVIRONMENT Servicing Portfolio Growth Share Repurchases New Loan Products • Continue to leverage Pennymac’s low cost structure and position as the largest correspondent aggregator in the U.S. to profitably grow our servicing portfolio • Greater opportunities to purchase bulk MSR expected to emerge as increased supply comes to market driven by continued pressure on profitability from originations • Driven by expectations for continued book value growth and return on equity over the medium - term • Track record of successful capital management over PFSI’s long history as a publicly - traded company; repurchased 38% of the outstanding shares since program inception (1) • Accretive to book value at current price levels • Addressing the changing demands of our 2.2 million servicing portfolio customers • Introducing new loan products, enabling borrowers to access higher home equity values; recently launched closed - end second lien mortgage loans (1) Through July 31, 2022

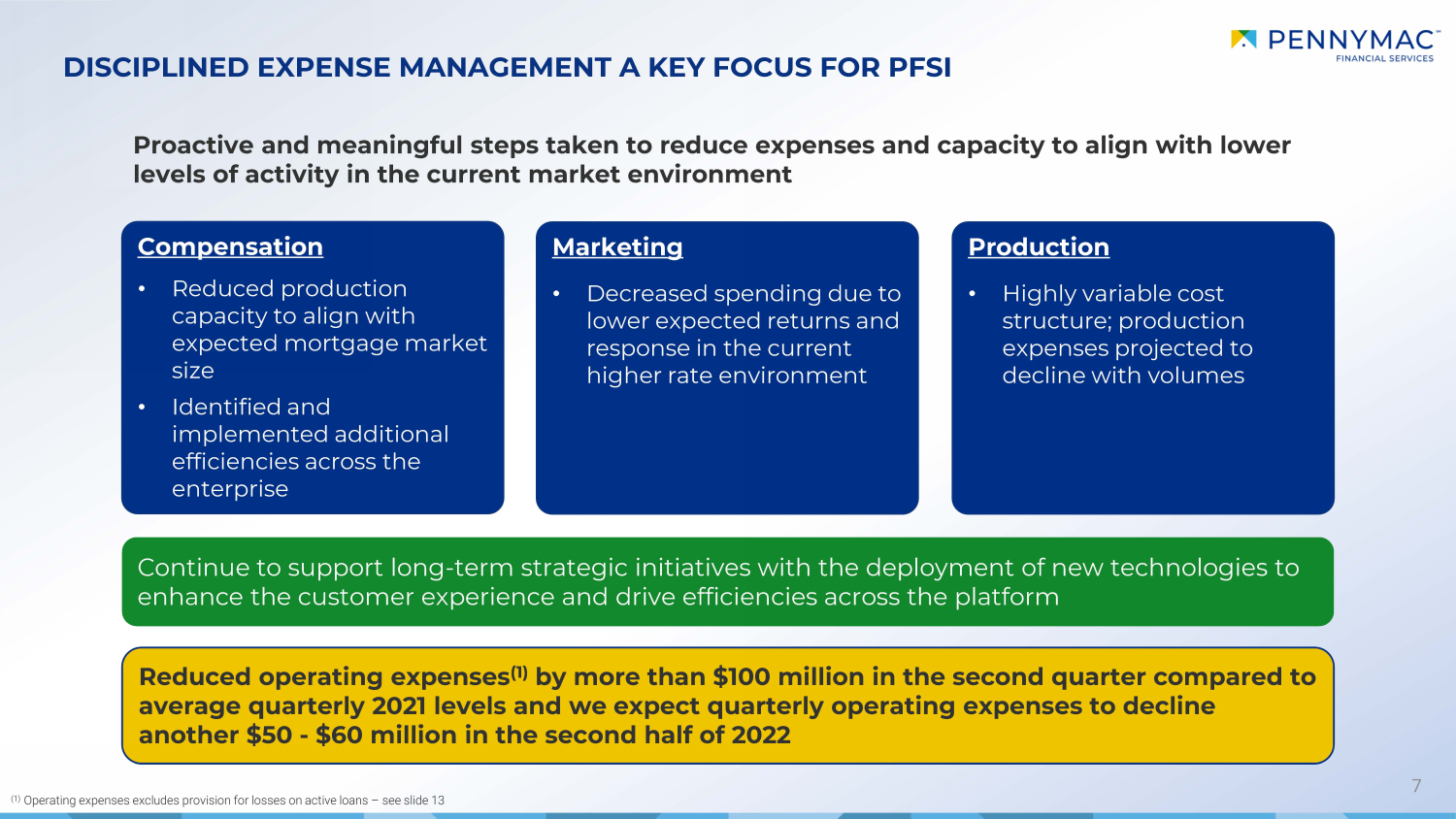

7 DISCIPLINED EXPENSE MANAGEMENT A KEY FOCUS FOR PFSI Compensation • Reduced production capacity to align with expected mortgage market size • Identified and implemented additional efficiencies across the enterprise Marketing • Decreased spending due to lower expected returns and response in the current higher rate environment Production • Highly variable cost structure; production expenses projected to decline with volumes Continue to support long - term strategic initiatives with the deployment of new technologies to enhance the customer experience and drive efficiencies across the platform (1) Operating expenses excludes provision for losses on active loans – see slide 13 Reduced operating expenses (1) by more than $100 million in the second quarter compared to average quarterly 2021 levels and we expect quarterly operating expenses to decline another $50 - $60 million in the second half of 2022 Proactive and meaningful steps taken to reduce expenses and capacity to align with lower levels of activity in the current market environment

0.5% 0.7% 0.9% 1.6% 1.6% 2018 2019 2020 2021 2Q22LTM 0.3% 1.2% 2.1% 2.4% 2.2% 2018 2019 2020 2021 2Q22LTM 2.8% 3.4% 3.7% 4.1% 4.1% 12/31/18 12/31/19 12/31/20 12/31/21 6/30/22 PENNYMAC’S MARKET SHARE OVER TIME ACROSS ITS BUSINESSES 8 Loan Servicing Market Share (1) Correspondent Production Market Share (1) Consumer Direct Market Share (1) Broker Direct Market Share (1) Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Historical market share estimates based on Inside Mortgage Finance. Inside Mortgage Finance estimates $3.5 billion in total o ri gination volume for 2Q22 LTM. For 2Q22, LTM, we estimate the correspondent channel represented 24% of the overall origination market, retail represented 60%, and broker represented 16%. Loan servicing market share is based on PFSI’s servicing portfolio UPB of $527 billion divided by an estimated $13.0 trillion in mortgage debt outstanding. 11.8% 15.3% 17.7% 16.7% 14.7% 2018 2019 2020 2021 2Q22LTM

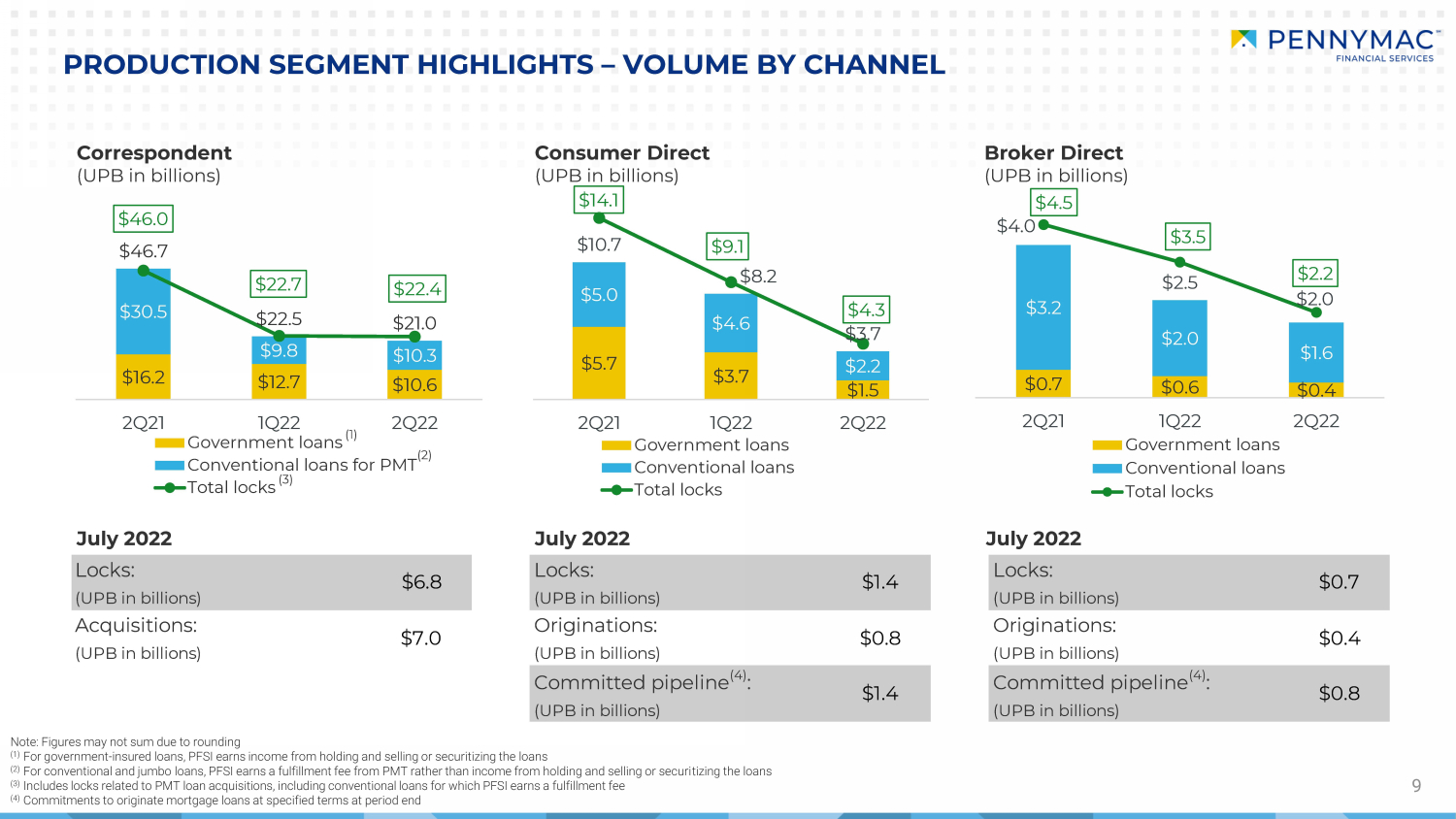

$5.7 $3.7 $1.5 $5.0 $4.6 $2.2 $10.7 $8.2 $3.7 $14.1 $9.1 $4.3 2Q21 1Q22 2Q22 Government loans Conventional loans Total locks $16.2 $12.7 $10.6 $30.5 $9.8 $10.3 $46.7 $22.5 $21.0 $46.0 $22.7 $22.4 2Q21 1Q22 2Q22 Government loans Conventional loans for PMT Total locks PRODUCTION SEGMENT HIGHLIGHTS – VOLUME BY CHANNEL 9 Consumer Direct (UPB in billions) Broker Direct (UPB in billions) July 2022 July 2022 July 2022 Note: Figures may not sum due to rounding (1) For government - insured loans, PFSI earns income from holding and selling or securitizing the loans (2) For conventional and jumbo loans, PFSI earns a fulfillment fee from PMT rather than income from holding and selling or securi ti zing the loans (3) Includes locks related to PMT loan acquisitions, including conventional loans for which PFSI earns a fulfillment fee (4) Commitments to originate mortgage loans at specified terms at period end (1) (2) (3) Correspondent (UPB in billions) $0.7 $0.6 $0.4 $3.2 $2.0 $1.6 $4.0 $2.5 $2.0 $4.5 $3.5 $2.2 2Q21 1Q22 2Q22 Government loans Conventional loans Total locks Locks: (UPB in billions) $6.8 Locks: (UPB in billions) $1.4 Locks: (UPB in billions) $0.7 Acquisitions: (UPB in billions) $7.0 Originations: (UPB in billions) $0.8 Originations: (UPB in billions) $0.4 Committed pipeline (4) : (UPB in billions) $1.4 Committed pipeline (4) : (UPB in billions) $0.8

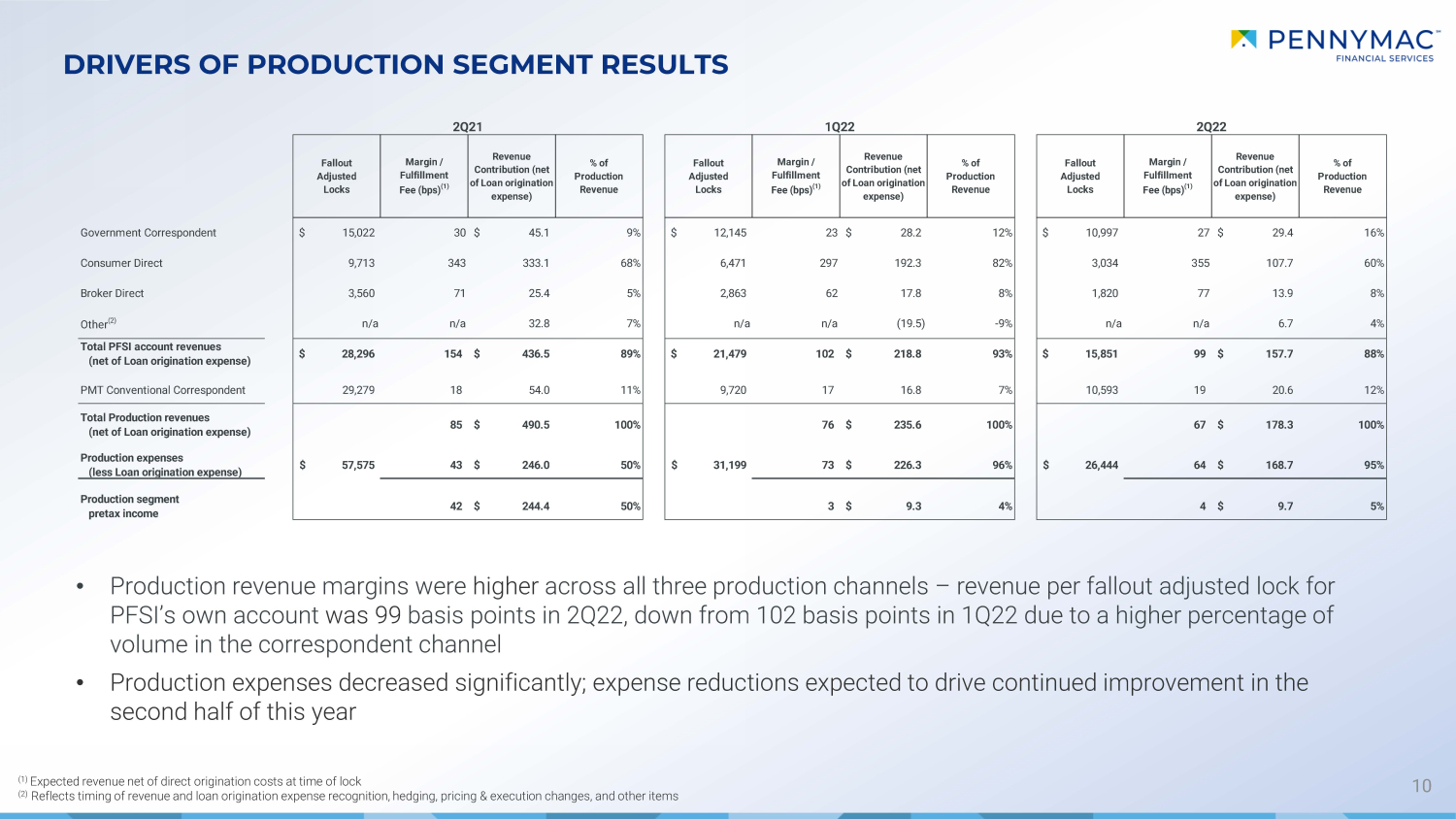

10 (1) Expected revenue net of direct origination costs at time of lock (2) Reflects timing of revenue and loan origination expense recognition, hedging, pricing & execution changes, and other items DRIVERS OF PRODUCTION SEGMENT RESULTS • Production revenue margins were higher across all three production channels – revenue per fallout adjusted lock for PFSI’s own account was 99 basis points in 2Q22, down from 102 basis points in 1Q22 due to a higher percentage of volume in the correspondent channel • Production expenses decreased significantly; expense reductions expected to drive continued improvement in the second half of this year Fallout Adjusted Locks Margin / Fulfillment Fee (bps) (1) Revenue Contribution (net of Loan origination expense) % of Production Revenue Fallout Adjusted Locks Margin / Fulfillment Fee (bps) (1) Revenue Contribution (net of Loan origination expense) % of Production Revenue Fallout Adjusted Locks Margin / Fulfillment Fee (bps) (1) Revenue Contribution (net of Loan origination expense) % of Production Revenue Government Correspondent 15,022$ 30 45.1$ 9% 12,145$ 23 28.2$ 12% 10,997$ 27 29.4$ 16% Consumer Direct 9,713 343 333.1 68% 6,471 297 192.3 82% 3,034 355 107.7 60% Broker Direct 3,560 71 25.4 5% 2,863 62 17.8 8% 1,820 77 13.9 8% Other (2) n/a n/a 32.8 7% n/a n/a (19.5) -9% n/a n/a 6.7 4% Total PFSI account revenues (net of Loan origination expense) 28,296$ 154 436.5$ 89% 21,479$ 102 218.8$ 93% 15,851$ 99 157.7$ 88% PMT Conventional Correspondent 29,279 18 54.0 11% 9,720 17 16.8 7% 10,593 19 20.6 12% Total Production revenues (net of Loan origination expense) 85 490.5$ 100% 76 235.6$ 100% 67 178.3$ 100% Production expenses (less Loan origination expense) 43 246.0$ 50% 73 226.3$ 96% 64 168.7$ 95% Production segment pretax income 42 244.4$ 50% 3 9.3$ 4% 4 9.7$ 5% 2Q21 57,575$ 1Q22 31,199$ 2Q22 26,444$

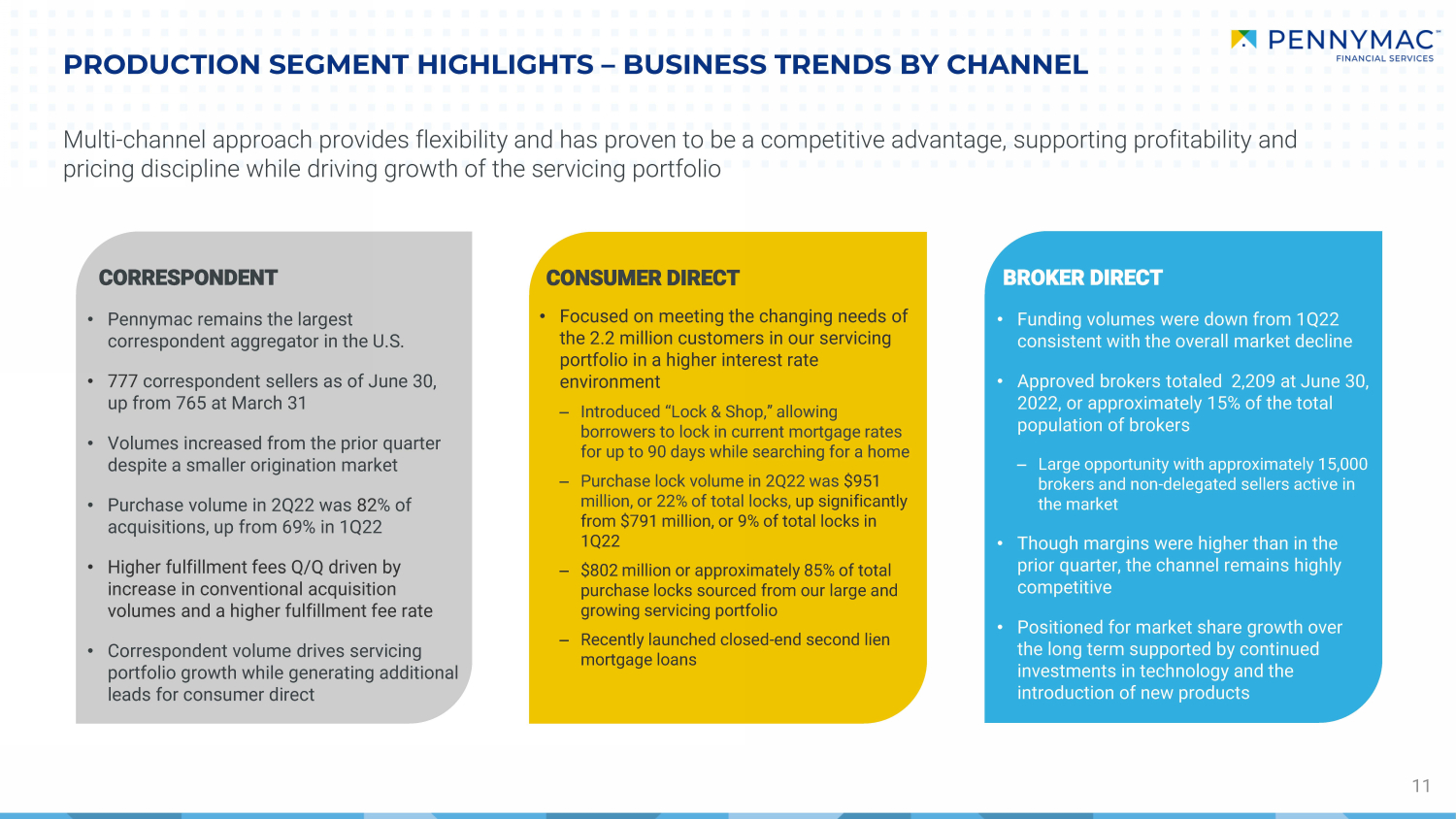

PRODUCTION SEGMENT HIGHLIGHTS – BUSINESS TRENDS BY CHANNEL 11 • Pennymac remains the largest correspondent aggregator in the U.S. • 777 correspondent sellers as of June 30, up from 765 at March 31 • Volumes increased from the prior quarter despite a smaller origination market • Purchase volume in 2Q22 was 82 % of acquisitions, up from 69% in 1Q22 • Higher fulfillment fees Q/Q driven by increase in conventional acquisition volumes and a higher fulfillment fee rate • Correspondent volume drives servicing portfolio growth while generating additional leads for consumer direct • Focused on meeting the changing needs of the 2.2 million customers in our servicing portfolio in a higher interest rate environment ‒ Introduced “Lock & Shop,” allowing borrowers to lock in current mortgage rates for up to 90 days while searching for a home ‒ Purchase lock volume in 2Q22 was $951 million, or 22% of total locks, up significantly from $791 million, or 9% of total locks in 1Q22 ‒ $802 million or approximately 85% of total purchase locks sourced from our large and growing servicing portfolio ‒ Recently launched closed - end second lien mortgage loans • Funding volumes were down from 1Q22 consistent with the overall market decline • Approved brokers totaled 2,209 at June 30, 2022, or approximately 15% of the total population of brokers ‒ Large opportunity with approximately 15,000 brokers and non - delegated sellers active in the market • Though margins were higher than in the prior quarter, the channel remains highly competitive • Positioned for market share growth over the long term supported by continued investments in technology and the introduction of new products CORRESPONDENT CONSUMER DIRECT BROKER DIRECT Multi - channel approach provides flexibility and has proven to be a competitive advantage, supporting profitability and pricing discipline while driving growth of the servicing portfolio

$518.8 $527.3 ($18.2) $26.7 At 3/31/22 Runoff Additions from loan production At 6/30/22 SERVICING SEGMENT HIGHLIGHTS 12 • Servicing portfolio totaled $527.3 billion in UPB at June 30, 2022, up 2% Q/Q and 11% Y/Y • Production volumes more than offset prepayment activity, leading to continued portfolio growth • Decrease in delinquency rates as borrowers continue to emerge from forbearance plans • Decrease in EBO loan volume and modifications as a result of lower delinquency levels and higher mortgage rates Loan Servicing Portfolio Composition (UPB in billions) Net Portfolio Growth (UPB in billions) (1) Owned portfolio is predominantly government - insured and guaranteed loans under the FHA (44%), VA (30%), and USDA (11%) programs. Delinquency data based on loan count (i.e., not UPB). CPR = Conditional Prepayment Rate. (2) Represents PMT’s MSRs. Excludes distressed loan investments. (3) UPB of completed modifications includes loss mitigation efforts associated with partial claims programs (4) Early buyouts of delinquent loans from Ginnie Mae pools during the period (5) Also includes loans sold with servicing released in connection with any asset sales by PMT (6) Includes consumer and broker direct production, government correspondent acquisitions, and conventional conforming and jumbo lo an acquisitions subserviced for PMT (5) (6) $473.2 $518.8 $527.3 6/30/21 3/31/22 6/30/22 Prime owned Prime subserviced and other 1Q22 2Q22 Loans serviced (in thousands) 2,167 2,188 60+ day delinquency rate - owned portfolio (1) 3.9% 3.2% 60+ day delinquency rate - sub-serviced portfolio (2) 0.7% 0.5% Actual CPR - owned portfolio (1) 17.1% 12.0% Actual CPR - sub-serviced (2) 13.0% 9.3% UPB of completed modifications ($ in millions) (3) $5,096 $4,224 EBO loan volume ($ in millions) (4) $2,092 $572 Selected Operational Metrics

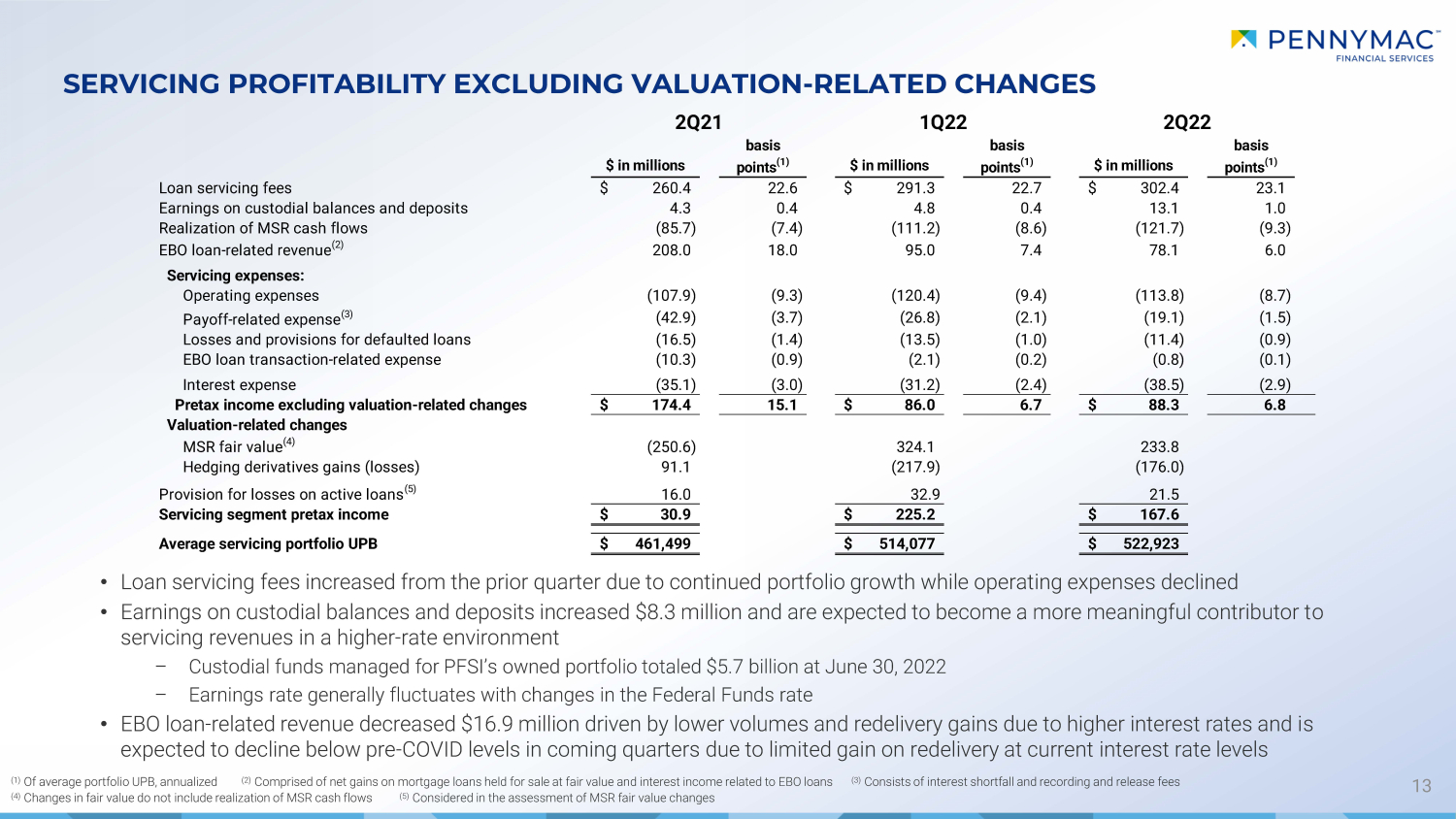

SERVICING PROFITABILITY EXCLUDING VALUATION - RELATED CHANGES 13 (1) Of average portfolio UPB, annualized (2) Comprised of net gains on mortgage loans held for sale at fair value and interest income related to EBO loans (3) Consists of interest shortfall and recording and release fees (4) Changes in fair value do not include realization of MSR cash flows (5) Considered in the assessment of MSR fair value changes • Loan servicing fees increased from the prior quarter due to continued portfolio growth while operating expenses declined • Earnings on custodial balances and deposits increased $8.3 million and are expected to become a more meaningful contributor t o servicing revenues in a higher - rate environment – Custodial funds managed for PFSI’s owned portfolio totaled $5.7 billion at June 30, 2022 – Earnings rate generally fluctuates with changes in the Federal Funds rate • EBO loan - related revenue decreased $16.9 million driven by lower volumes and redelivery gains due to higher interest rates and i s expected to decline below pre - COVID levels in coming quarters due to limited gain on redelivery at current interest rate levels $ in millions basis points (1) $ in millions basis points (1) $ in millions basis points (1) Loan servicing fees 260.4$ 22.6 291.3$ 22.7 302.4$ 23.1 Earnings on custodial balances and deposits 4.3 0.4 4.8 0.4 13.1 1.0 Realization of MSR cash flows (85.7) (7.4) (111.2) (8.6) (121.7) (9.3) EBO loan-related revenue (2) 208.0 18.0 95.0 7.4 78.1 6.0 Servicing expenses: Operating expenses (107.9) (9.3) (120.4) (9.4) (113.8) (8.7) Payoff-related expense (3) (42.9) (3.7) (26.8) (2.1) (19.1) (1.5) Losses and provisions for defaulted loans (16.5) (1.4) (13.5) (1.0) (11.4) (0.9) EBO loan transaction-related expense (10.3) (0.9) (2.1) (0.2) (0.8) (0.1) Interest expense (35.1) (3.0) (31.2) (2.4) (38.5) (2.9) Pretax income excluding valuation-related changes 174.4$ 15.1 86.0$ 6.7 88.3$ 6.8 Valuation-related changes MSR fair value (4) (250.6) 324.1 233.8 Hedging derivatives gains (losses) 91.1 (217.9) (176.0) Provision for losses on active loans (5) 16.0 32.9 21.5 Servicing segment pretax income 30.9$ 225.2$ 167.6$ Average servicing portfolio UPB 461,499$ 514,077$ 522,923$ 2Q222Q21 1Q22

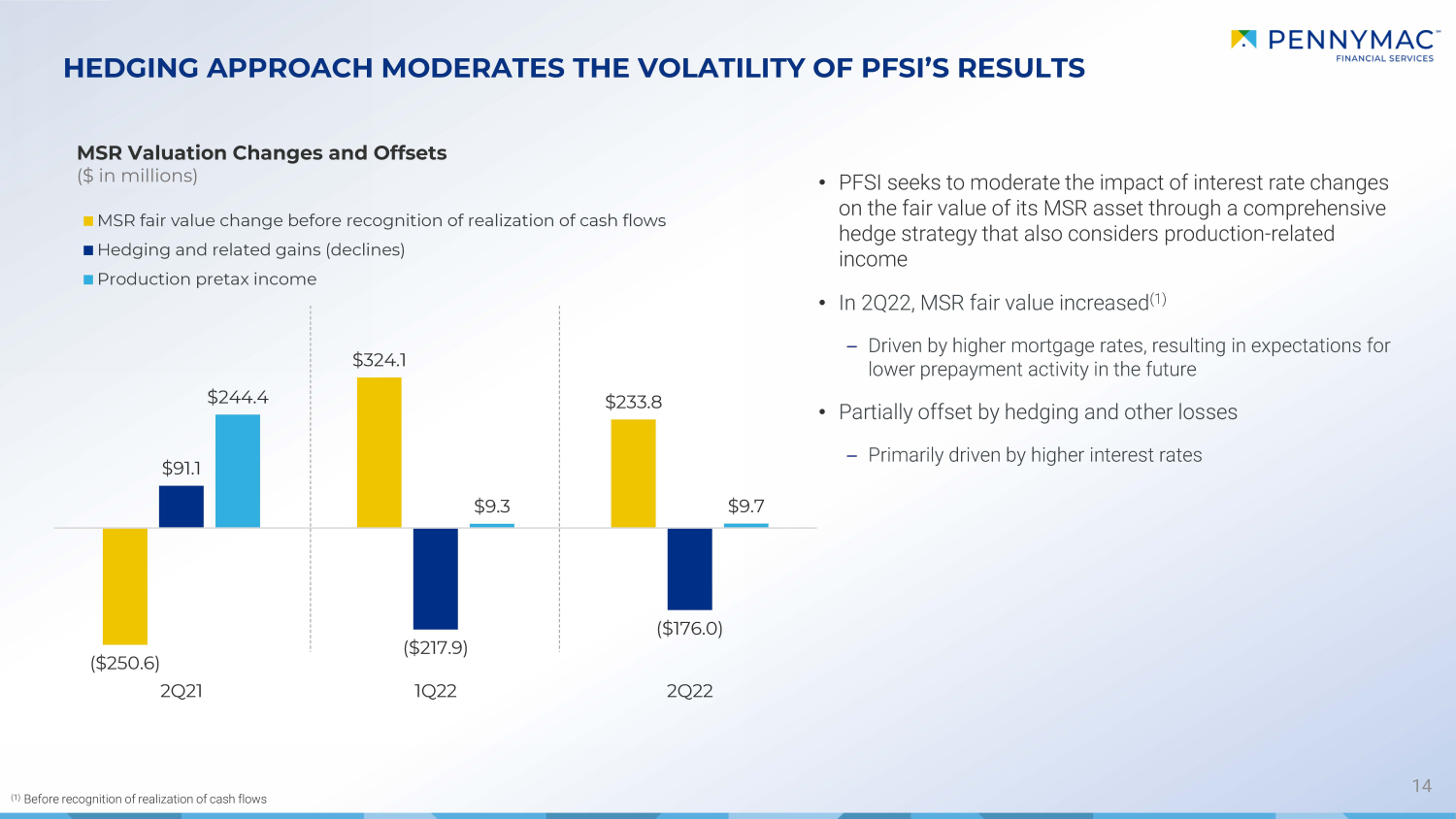

14 HEDGING APPROACH MODERATES THE VOLATILITY OF PFSI’S RESULTS MSR Valuation Changes and Offsets ($ in millions) • PFSI seeks to moderate the impact of interest rate changes on the fair value of its MSR asset through a comprehensive hedge strategy that also considers production - related income • In 2Q22, MSR fair value increased (1) – Driven by higher mortgage rates, resulting in expectations for lower prepayment activity in the future • Partially offset by hedging and other losses – Primarily driven by higher interest rates (1) Before recognition of realization of cash flows ($250.6) $324.1 $233.8 $91.1 ($217.9) ($176.0) $244.4 $9.3 $9.7 2Q21 1Q22 2Q22 MSR fair value change before recognition of realization of cash flows Hedging and related gains (declines) Production pretax income

INVESTMENT MANAGEMENT SEGMENT HIGHLIGHTS 15 • Net AUM as of June 30, 2022 were $ 2.1 billion, down 7% from March 31, 2022 and 12 % from June 30, 2021 ‒ Decrease in AUM primarily due to PMT’s net losses • Investment Management segment revenues were $9.7 million, down 5% from 1Q22 and down 28% from 2Q21 Investment Management AUM ($ in billions) Investment Management Revenues ($ in millions) $2.3 $2.2 $2.1 6/30/21 3/31/22 6/30/22 $10.2 $3.3 $13.5 $10.1 $9.7 2Q21 1Q22 2Q22 Base management fees & other revenue Performance incentive

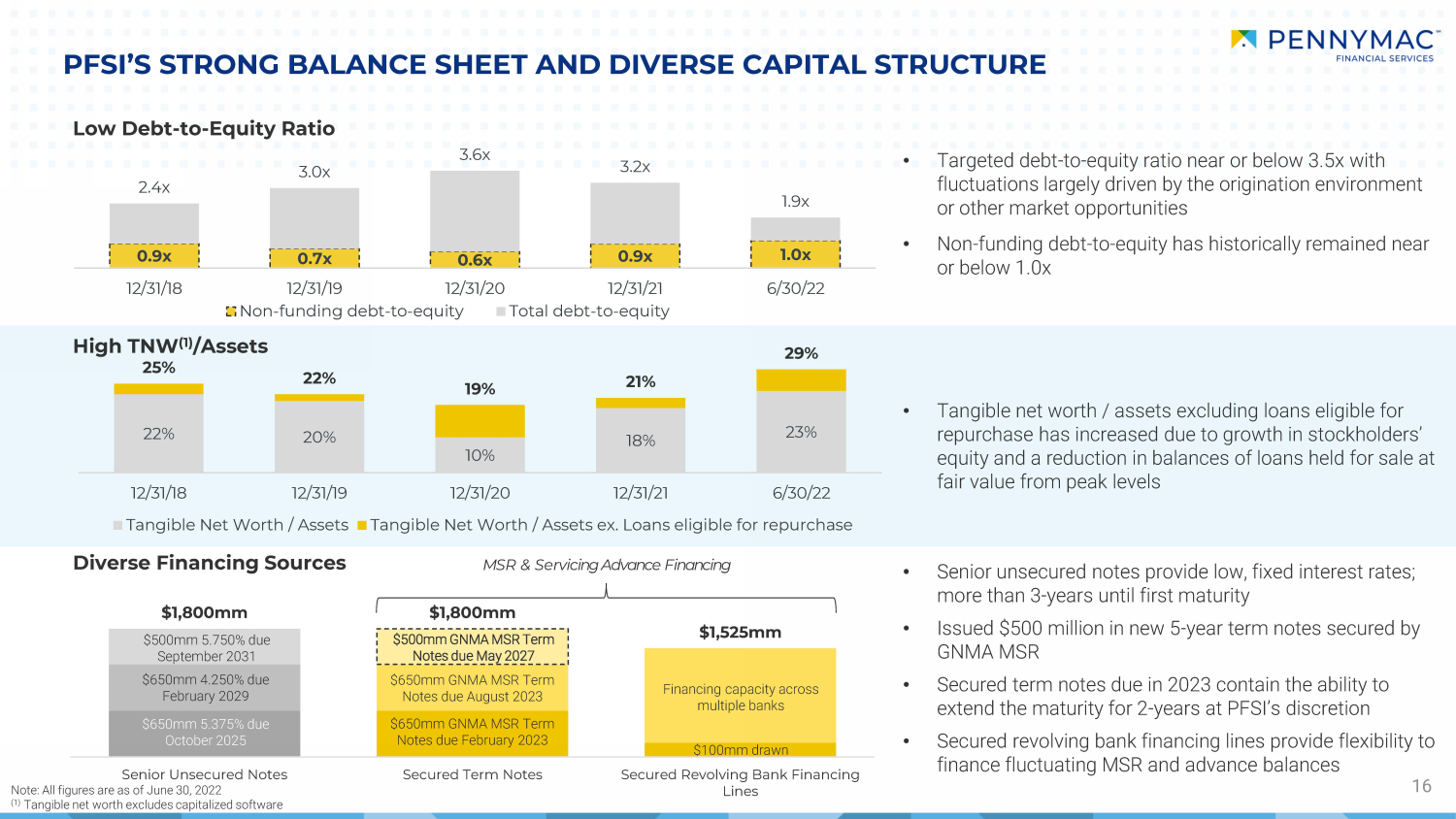

$1,800mm $1,800mm $1,525mm Senior Unsecured Notes Secured Term Notes Secured Revolving Bank Financing Lines 0.9x 0.7x 0.6x 0.9x 1.0x 2.4x 3.0x 3.6x 3.2x 1.9x 12/31/18 12/31/19 12/31/20 12/31/21 6/30/22 Non-funding debt-to-equity Total debt-to-equity 22% 20% 10% 18% 23% 25% 22% 19% 21% 29% 12/31/18 12/31/19 12/31/20 12/31/21 6/30/22 Tangible Net Worth / Assets Tangible Net Worth / Assets ex. Loans eligible for repurchase PFSI’S STRONG BALANCE SHEET AND DIVERSE CAPITAL STRUCTURE 16 Low Debt - to - Equity Ratio Diverse Financing Sources High TNW (1) /Assets • Tangible net worth / assets excluding loans eligible for repurchase has increased due to growth in stockholders’ equity and a reduction in balances of loans held for sale at fair value from peak levels $500mm GNMA MSR Term Notes due May 2027 $650mm GNMA MSR Term Notes due August 2023 $650mm GNMA MSR Term Notes due February 2023 $500mm 5.750% due September 2031 $650mm 4.250% due February 2029 $650mm 5.375% due October 2025 • Targeted debt - to - equity ratio near or below 3.5x with fluctuations largely driven by the origination environment or other market opportunities • Non - funding debt - to - equity has historically remained near or below 1.0x • Senior unsecured notes provide low, fixed interest rates; more than 3 - years until first maturity • Issued $500 million in new 5 - year term notes secured by GNMA MSR • Secured term notes due in 2023 contain the ability to extend the maturity for 2 - years at PFSI’s discretion • Secured revolving bank financing lines provide flexibility to finance fluctuating MSR and advance balances MSR & Servicing Advance Financing Financing capacity across multiple banks Note: All figures are as of June 30, 2022 (1) Tangible net worth excludes capitalized software $100mm drawn

APPENDIX

18 PENNYMAC IS AN ESTABLISHED LEADER IN THE U.S. MORTGAGE MARKET WITH SUBSTANTIAL LONG - TERM GROWTH POTENTIAL $527 billion outstanding IN SER VIC ING (2) YEARS FOR PFSI AS A PUBLIC COMPANY 9 15 YEARS OF OPERATIONS PMT # 4 • CORRESPONDENT PRODUCTION • CONSUMER DIRECT • BROKER DIRECT IN PRODUCTION (1) IS A LEADING RESIDENTIAL MORTGAGE REIT # 7 Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT. All figures are as of 6/30/22 unless othe rwi se noted. (1) Inside Mortgage Finance for the 12 months ended 6/30/22 (2) Inside Mortgage Finance as of 3/31/22 $2.1 billion in assets under management 13 - year track record 2+ million customers $ 166 billion LTM 2Q22

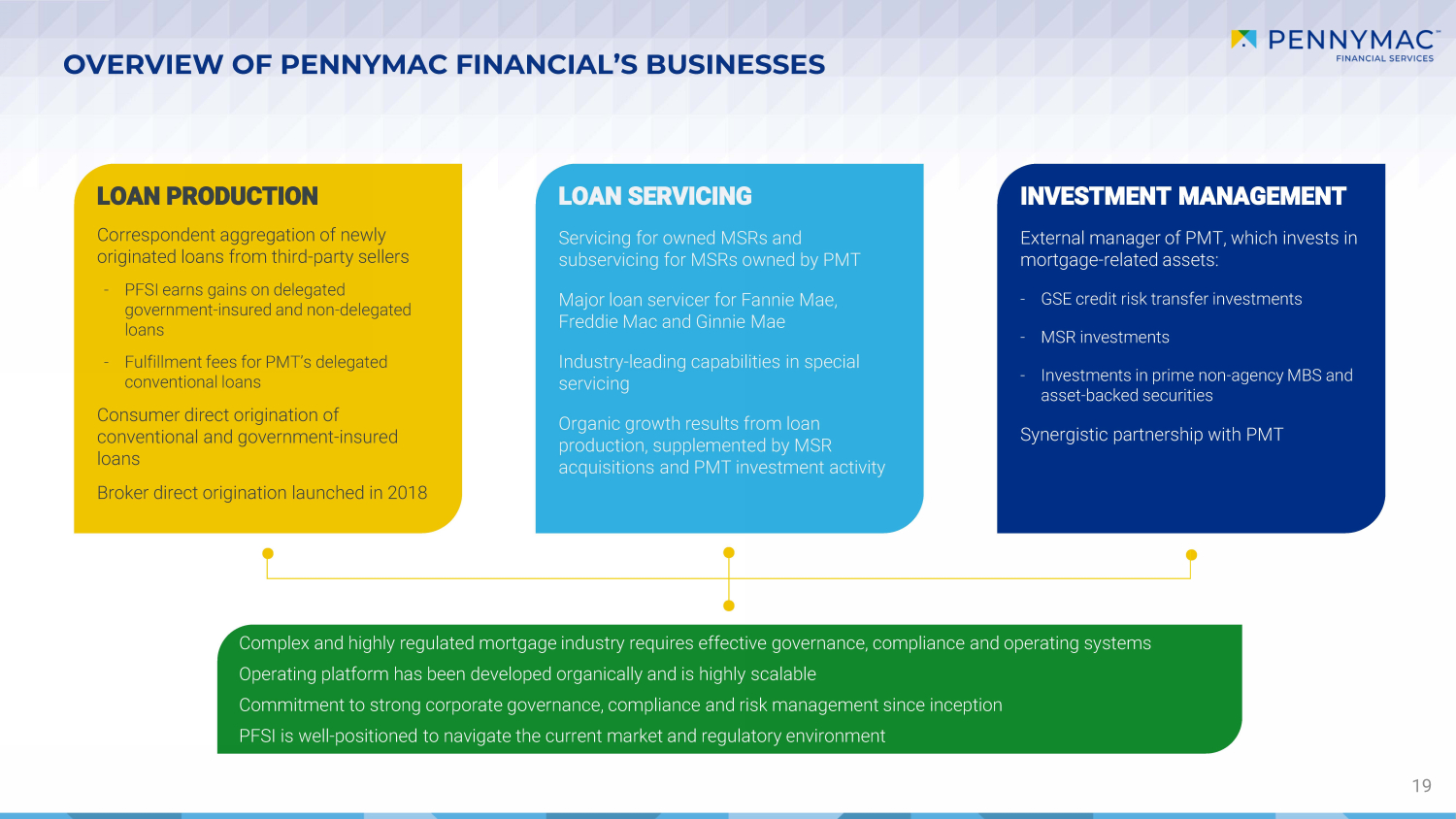

OVERVIEW OF PENNYMAC FINANCIAL’S BUSINESSES 19 LOAN PRODUCTION Correspondent aggregation of newly originated loans from third - party sellers - PFSI earns gains on delegated government - insured and non - delegated loans - Fulfillment fees for PMT’s delegated conventional loans Consumer direct origination of conventional and government - insured loans Broker direct origination launched in 2018 LOAN SERVICING Servicing for owned MSRs and subservicing for MSRs owned by PMT Major loan servicer for Fannie Mae, Freddie Mac and Ginnie Mae Industry - leading capabilities in special servicing Organic growth results from loan production, supplemented by MSR acquisitions and PMT investment activity INVESTMENT MANAGEMENT External manager of PMT, which invests in mortgage - related assets: - GSE credit risk transfer investments - MSR investments - Investments in prime non - agency MBS and asset - backed securities Synergistic partnership with PMT Complex and highly regulated mortgage industry requires effective governance, compliance and operating systems Operating platform has been developed organically and is highly scalable Commitment to strong corporate governance, compliance and risk management since inception PFSI is well - positioned to navigate the current market and regulatory environment

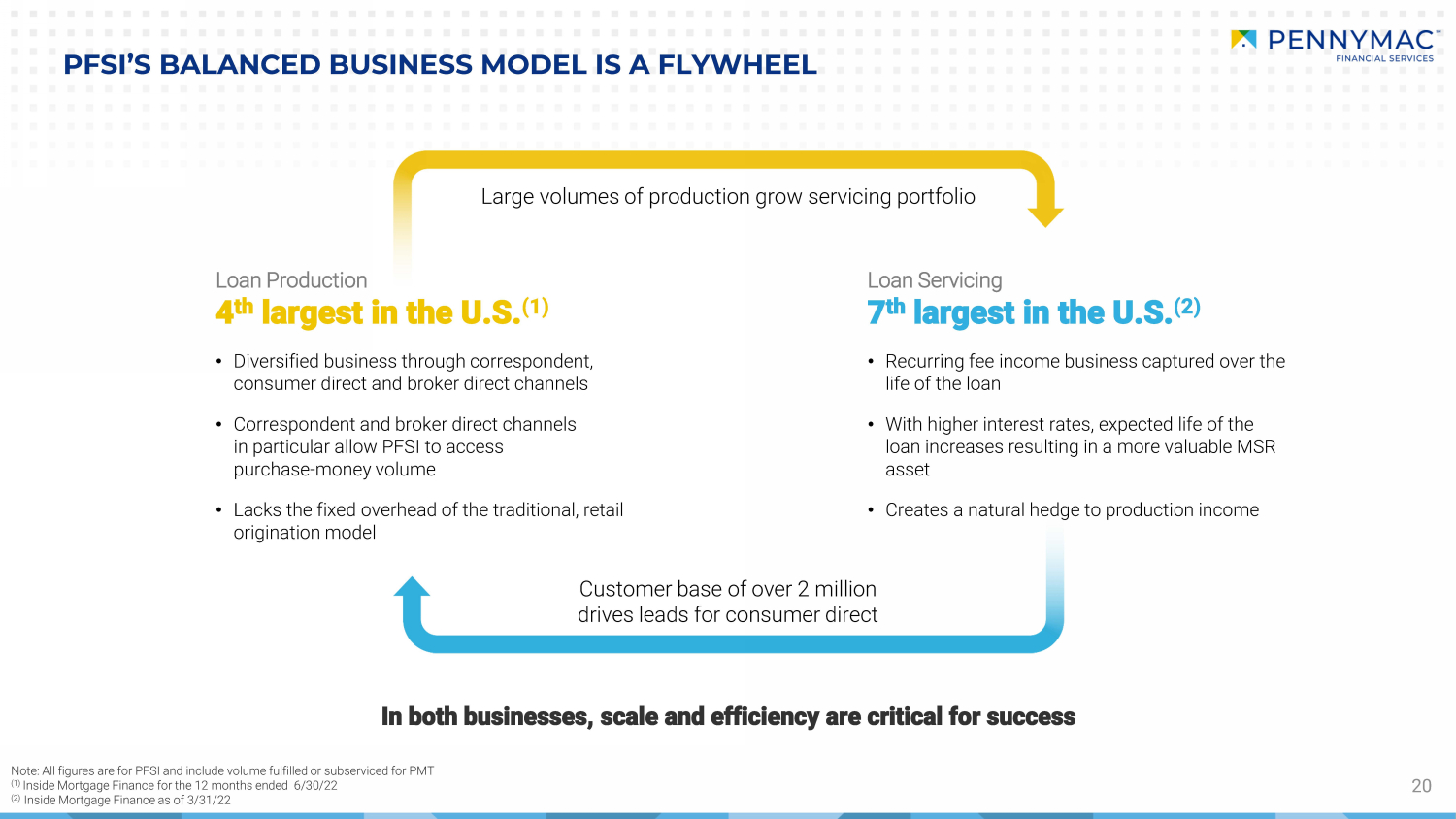

20 PFSI’S BALANCED BUSINESS MODEL IS A FLYWHEEL • Diversified business through correspondent, consumer direct and broker direct channels • Correspondent and broker direct channels in particular allow PFSI to access purchase - money volume • Lacks the fixed overhead of the traditional, retail origination model • Recurring fee income business captured over the life of the loan • With higher interest rates, expected life of the loan increases resulting in a more valuable MSR asset • Creates a natural hedge to production income Customer base of over 2 million drives leads for consumer direct Large volumes of production grow servicing portfolio Loan Production 4 th largest in the U.S. (1) Loan Servicing 7 th largest in the U.S. (2) In both businesses, scale and efficiency are critical for success Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Inside Mortgage Finance for the 12 months ended 6/30/22 (2) Inside Mortgage Finance as of 3/31/22

21 • $1.1 billion in revenue from servicing and sub - servicing fees in 2021 • Higher short - term rates expected to drive increased placement fee income • Cloud - based servicing system built for Pennymac’s unique needs • Operational and cost efficiencies, as well as increased flexibility • Data - based analytics and insights from servicing system • Purchase originations, new products (second liens, HELOCs) • Loss mitigation expertise to assist consumers and minimize losses • Enhanced by flexible and proprietary servicing technology • Offering homeowners insurance to servicing customers through a joint venture • Evaluating additional partnerships and revenue opportunities BENEFITS AND POTENTIAL VALUE FROM PENNYMAC’S LARGE AND GROWING SERVICING PORTFOLIO SERVICING PORTFOLIO Recurring Cash Flows Proprietary Technology New Marketing Opportunities Loss Mitigation Ancillary Products and Services 2.2M customers $527B unpaid principal balance

Reserves maintained for: ROBUST LIQUIDITY RISK MANAGEMENT DISCIPLINE 22 $2.8 billion in available liquidity at June 30, 2022 (1) , significantly in excess of minimum requirements and internally established reserve levels (1) Includes $1.4 billion in cash and short - term investments plus $1.4 billion in amounts that can be immediately borrowed on facil ities with pledged collateral Minimum Regulatory and Counterparty Requirements Ongoing Operations Unexpected Environmental Shocks • Financing covenants and other requirements of counterparties, regulators and rating agencies • Well - positioned to meet the additional eligibility standards recently proposed by FHFA for non - bank, Agency seller/servicers • Fulfillment of known financial commitments and obligations • Operating expenses, expected income tax payments, principal and interest payments on outstanding debt, dividend payments and other • Expected cash needs for business activities and corporate overhead • Potential margin calls related to sudden interest rate changes; also considers potential timing difference between margin calls and ability to draw on certain liquidity sources • Servicing advances in a severe loan delinquency and prepayment rate scenario

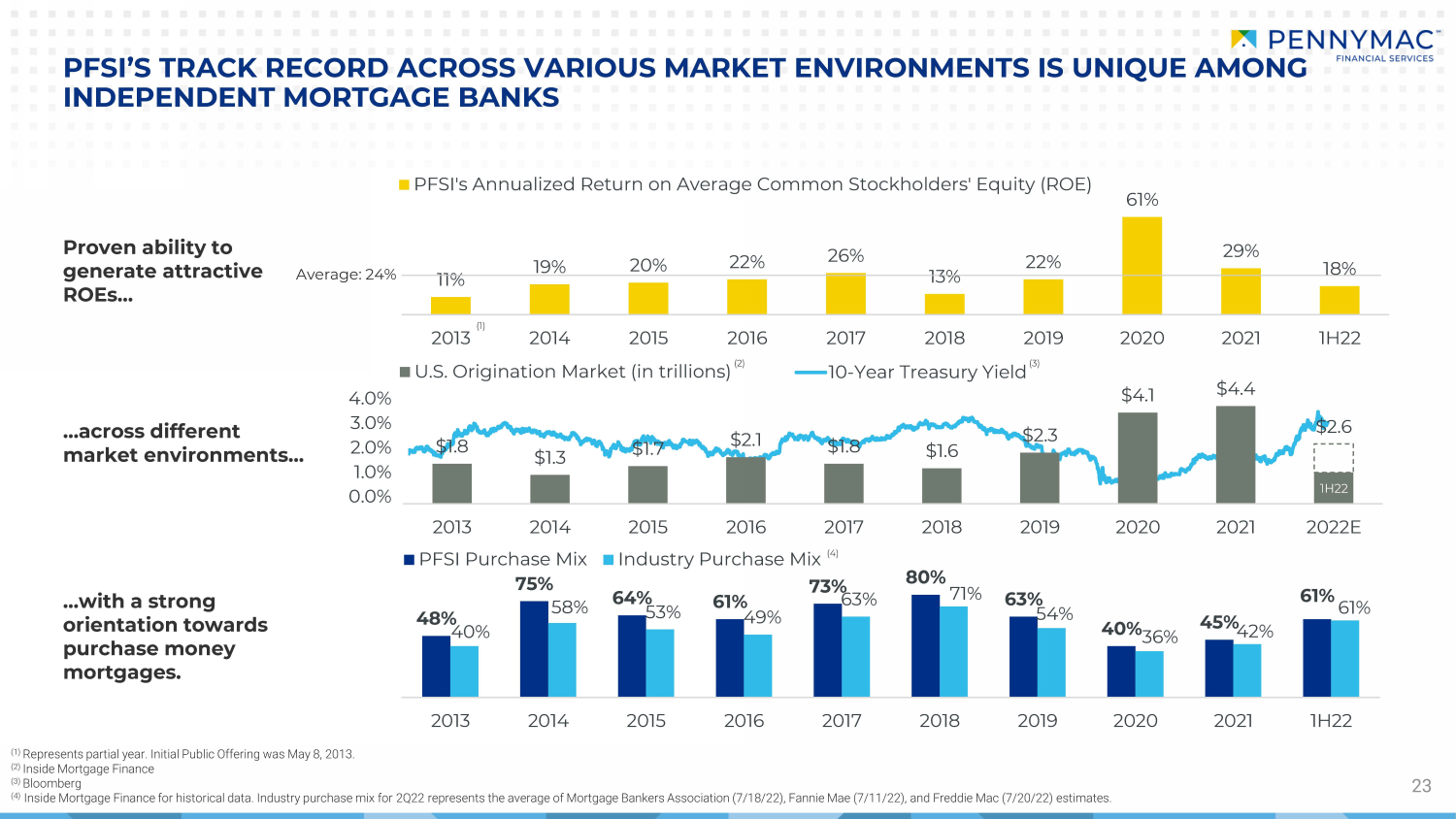

48% 75% 64% 61% 73% 80% 63% 40% 45% 61% 40% 58% 53% 49% 63% 71% 54% 36% 42% 61% 2013 2014 2015 2016 2017 2018 2019 2020 2021 1H22 PFSI Purchase Mix Industry Purchase Mix 0.0% 1.0% 2.0% 3.0% 4.0% 10-Year Treasury Yield 1H22 $1.8 $1.3 $1.7 $2.1 $1.8 $1.6 $2.3 $4.1 $4.4 $2.6 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022E U.S. Origination Market (in trillions) 11% 19% 20% 22% 26% 13% 22% 61% 29% 18% 2013 2014 2015 2016 2017 2018 2019 2020 2021 1H22 PFSI's Annualized Return on Average Common Stockholders' Equity (ROE) 23 PFSI’S TRACK RECORD ACROSS VARIOUS MARKET ENVIRONMENTS IS UNIQUE AMONG INDEPENDENT MORTGAGE BANKS Proven ability to generate attractive ROEs… …across different market environments… …with a strong orientation towards purchase money mortgages. (1) Represents partial year. Initial Public Offering was May 8, 2013. (2) Inside Mortgage Finance (3) Bloomberg (4) Inside Mortgage Finance for historical data. Industry purchase mix for 2 Q22 represents the average of Mortgage Bankers Association (7/18/22), Fannie Mae (7/11/22), and Freddie Mac (7/20/22) estimates. (1) (2) (3) (4) Average: 24%

PENNYMAC HAS DEVELOPED IN A SUSTAINABLE MANNER FOR LONG - TERM SUCCESS 24 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Operations launched; de novo build of legacy - free mortgage servicer Raised $500 million of capital in private opportunity funds PMT formed in an initial public offering raising $320 million Correspondent group established with a focus on operations development and process design Added servicing leadership for prime portfolio and to drive scalable growth Correspondent system launches Expanded infrastructure with flagship operations facility in Moorpark, CA Correspondent leadership team expands Expanded infrastructure in Tampa, FL Became largest non - bank correspondent aggregator PFSI completed initial public offering Expanded infrastructure in Fort Worth, TX Continued organic growth and servicing portfolio UPB reaches $100 billion (1) PFSI stockholders’ equity surpasses $1 billion Substantial growth in PFSI’s consumer direct capacity PFSI issued MSR - backed term notes PFSI launched broker - direct lending channel PFSI completes corporate reorganization Achieved position as the largest correspondent aggregator in the U.S. PFSI launched proprietary, cloud - based Servicing Systems Environment (SSE) Record production volumes across all channels; nearly $200 billion in UPB (1) PFSI issued inaugural $650 million of unsecured Senior Notes PFSI issued an additional $1.15 billion of unsecured Senior Notes Servicing portfolio surpasses 2 million customers (1) (1) All figures are for PFSI and include volume fulfilled or subserviced for PMT • Disciplined growth to address the demands of the GSEs, Agencies, regulators and our financing partners ‒ Since inception, PennyMac has focused on building and testing processes and systems before adding significant transaction vol ume s • Highly experienced management team has created a robust corporate governance system centered on compliance, risk management a nd quality control 2022 Launched “Greatness Lives Here” brand marketing campaign celebrating home as the foundation for achieving life’s aspirations

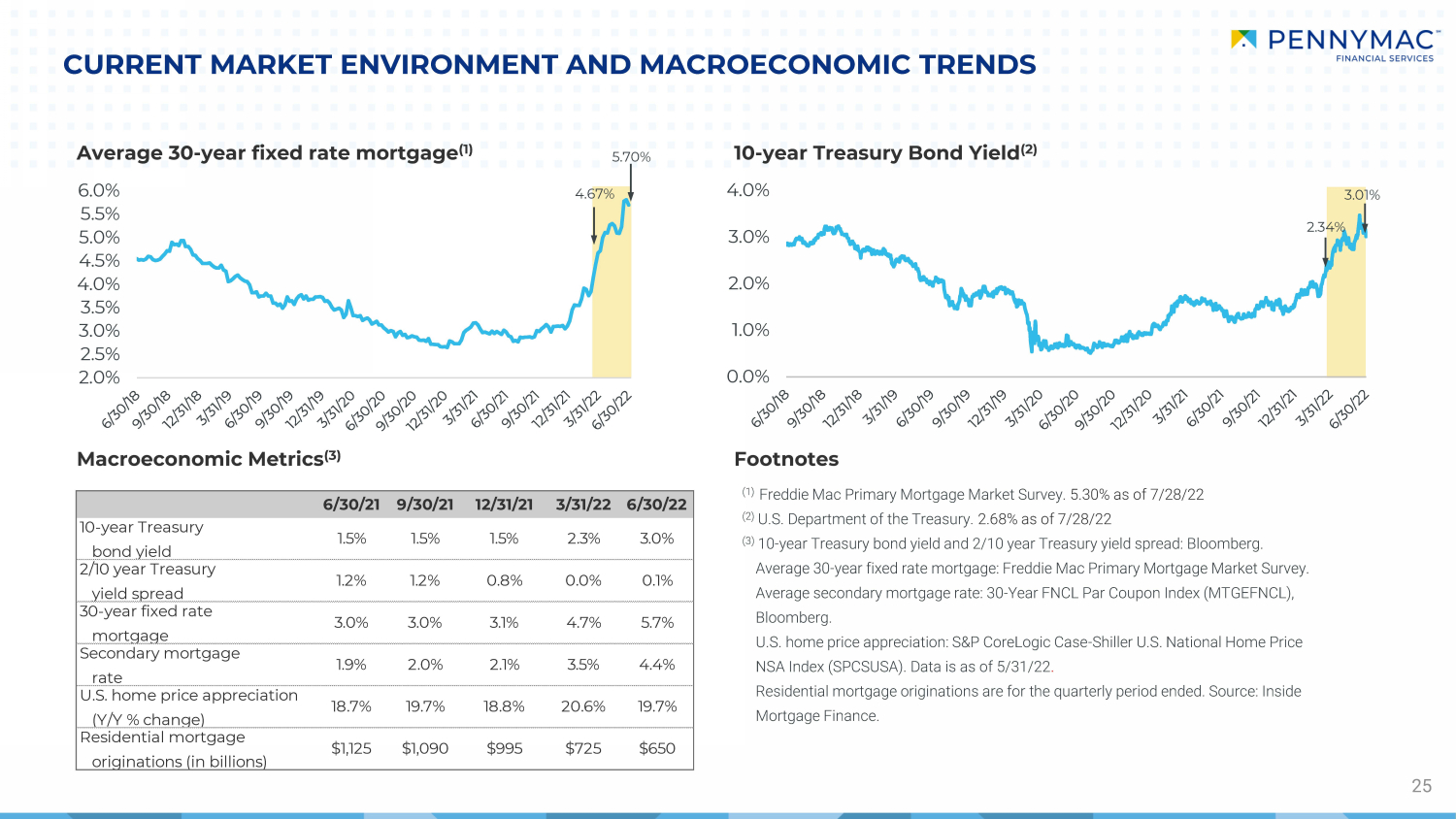

2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 6.0% 0.0% 1.0% 2.0% 3.0% 4.0% 2.34% CURRENT MARKET ENVIRONMENT AND MACROECONOMIC TRENDS 25 Macroeconomic Metrics (3) Footnotes (1) Freddie Mac Primary Mortgage Market Survey. 5.30% as of 7/28/22 (2) U.S. Department of the Treasury. 2.68% as of 7/28/22 (3) 10 - year Treasury bond yield and 2/10 year Treasury yield spread: Bloomberg. Average 30 - year fixed rate mortgage: Freddie Mac Primary Mortgage Market Survey. Average secondary mortgage rate: 30 - Year FNCL Par Coupon Index (MTGEFNCL), Bloomberg. U.S. home price appreciation: S&P CoreLogic Case - Shiller U.S. National Home Price NSA Index (SPCSUSA). Data is as of 5/31/22 . Residential mortgage originations are for the quarterly period ended. Source: Inside Mortgage Finance. Average 30 - year fixed rate mortgage (1) 10 - year Treasury Bond Yield (2) 3.01% 5.70% 4.67% 6/30/21 9/30/21 12/31/21 3/31/22 6/30/22 10-year Treasury bond yield 1.5% 1.5% 1.5% 2.3% 3.0% 2/10 year Treasury yield spread 1.2% 1.2% 0.8% 0.0% 0.1% 30-year fixed rate mortgage 3.0% 3.0% 3.1% 4.7% 5.7% Secondary mortgage rate 1.9% 2.0% 2.1% 3.5% 4.4% U.S. home price appreciation (Y/Y % change) 18.7% 19.7% 18.8% 20.6% 19.7% Residential mortgage originations (in billions) $1,125 $1,090 $995 $725 $650

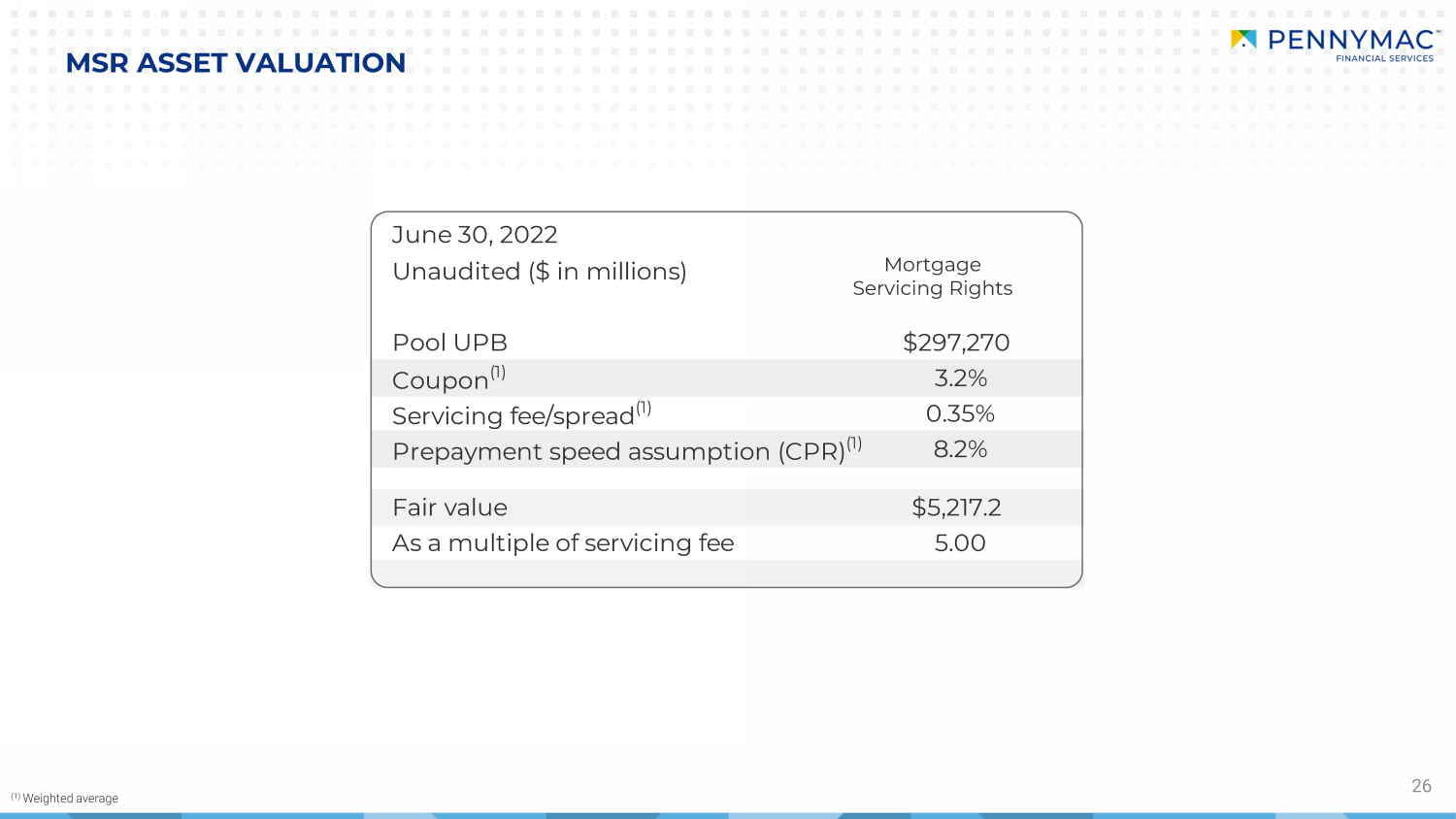

26 MSR ASSET VALUATION (1) Weighted average Mortgage Servicing Rights Pool UPB $297,270 Coupon (1) 3.2% Servicing fee/spread (1) 0.35% Prepayment speed assumption (CPR) (1) 8.2% Fair value $5,217.2 As a multiple of servicing fee 5.00 June 30, 2022 Unaudited ($ in millions)

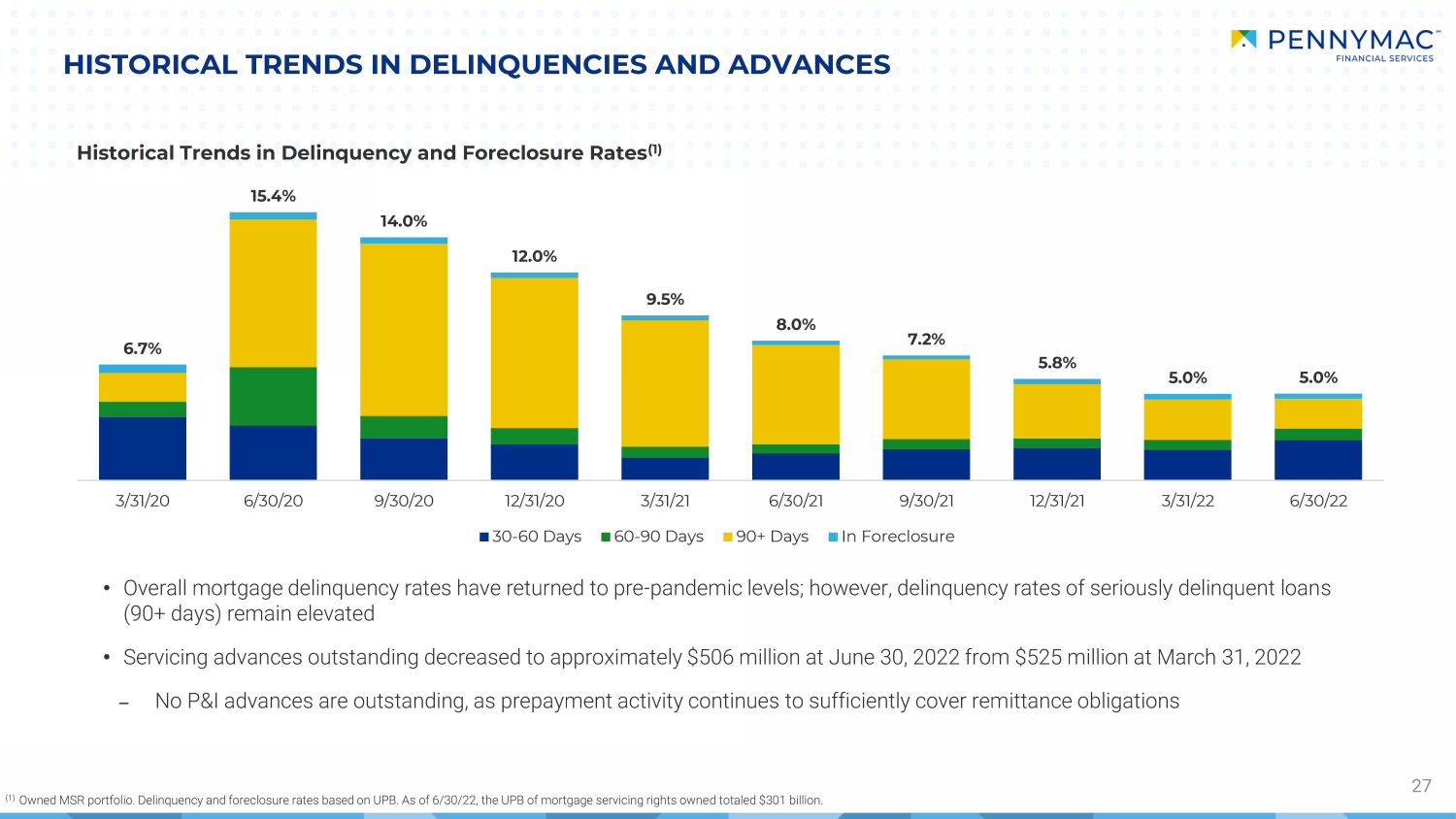

6.7% 15.4% 14.0% 12.0% 9.5% 8.0% 7.2% 5.8% 5.0% 5.0% 3/31/20 6/30/20 9/30/20 12/31/20 3/31/21 6/30/21 9/30/21 12/31/21 3/31/22 6/30/22 30-60 Days 60-90 Days 90+ Days In Foreclosure • Overall mortgage delinquency rates have returned to pre - pandemic levels; however, delinquency rates of seriously delinquent loan s (90+ days) remain elevated • Servicing advances outstanding decreased to approximately $506 million at June 30, 2022 from $525 million at March 31, 2022 – No P&I advances are outstanding, as prepayment activity continues to sufficiently cover remittance obligations HISTORICAL TRENDS IN DELINQUENCIES AND ADVANCES 27 Historical Trends in Delinquency and Foreclosure Rates (1) (1) Owned MSR portfolio. Delinquency and foreclosure rates based on UPB. As of 6/30/22, the UPB of mortgage servicing rights owne d t otaled $301 billion.

ACQUISITIONS AND ORIGINATIONS BY PRODUCT 28 First Lien Acquisitions/Originations Note: Figures may not sum exactly due to rounding Unaudited ($ in millions) 2Q21 3Q21 4Q21 1Q22 2Q22 Correspondent Acquisitions Conventional Conforming 30,479$ 28,605$ 17,157$ 9,768$ 10,320$ Government 16,175 15,375 15,651 12,730 10,649 Jumbo - - - 1 3 Total 46,654$ 43,980$ 32,808$ 22,500$ 20,973$ Consumer Direct Originations Conventional Conforming 5,012$ 6,200$ 6,311$ 4,553$ 2,246$ Government 5,661 4,932 4,289 3,669 1,492 Jumbo - - - - 5 Total 10,672$ 11,131$ 10,600$ 8,222$ 3,744$ Broker Direct Originations Conventional Conforming 3,246$ 3,086$ 2,823$ 1,979$ 1,556$ Government 728 902 860 560 396 Jumbo - - - 2 24 Total 3,974$ 3,988$ 3,684$ 2,541$ 1,976$ Total acquisitions/originations 61,300$ 59,099$ 47,092$ 33,262$ 26,693$ UPB of loans fulfilled for PMT (included in correspondent acquisitions) 30,479$ 28,605$ 17,157$ 9,768$ 10,324$

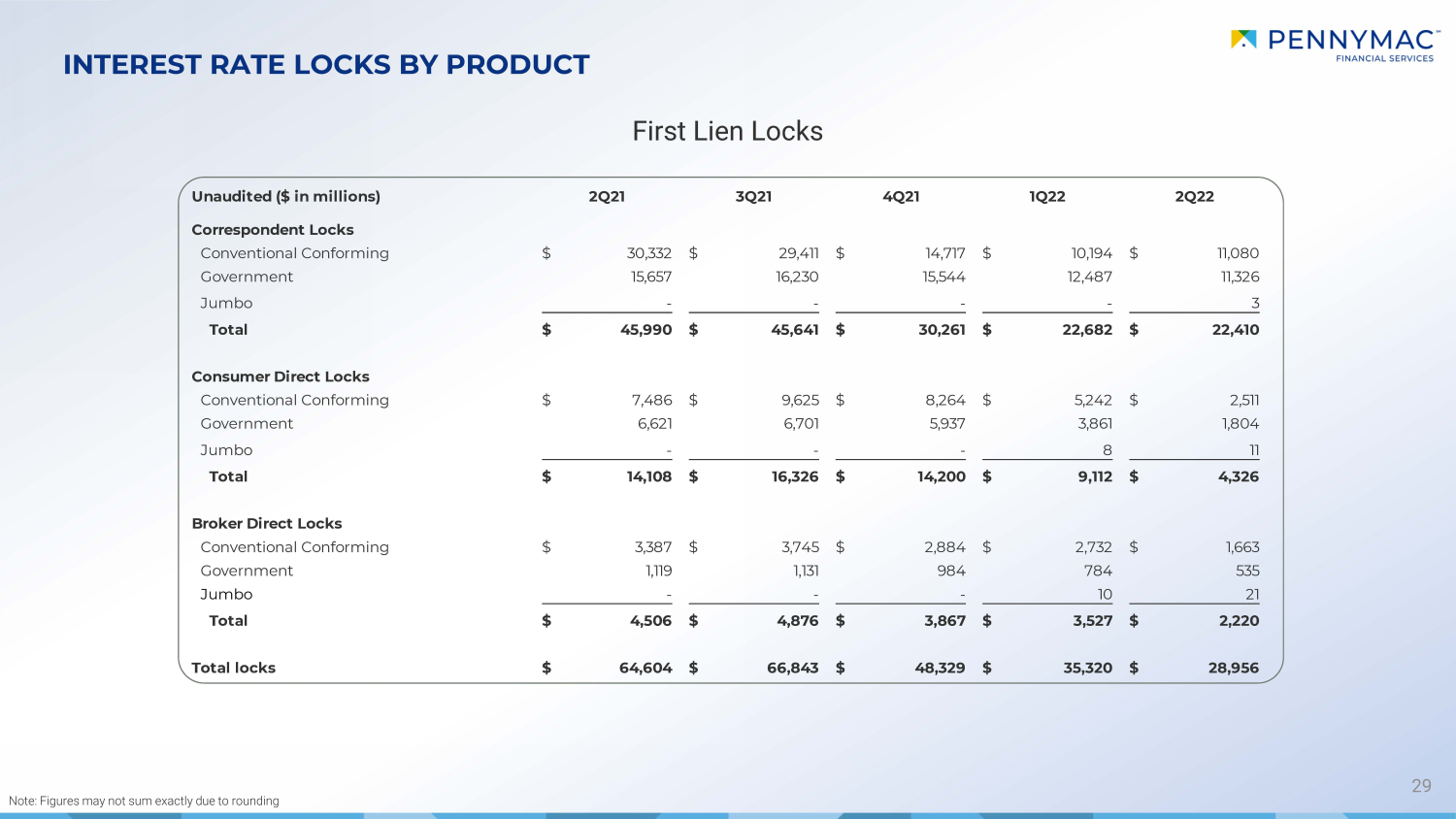

INTEREST RATE LOCKS BY PRODUCT 29 Note: Figures may not sum exactly due to rounding First Lien Locks Unaudited ($ in millions) 2Q21 3Q21 4Q21 1Q22 2Q22 Correspondent Locks Conventional Conforming 30,332$ 29,411$ 14,717$ 10,194$ 11,080$ Government 15,657 16,230 15,544 12,487 11,326 Jumbo - - - - 3 Total 45,990$ 45,641$ 30,261$ 22,682$ 22,410$ Consumer Direct Locks Conventional Conforming 7,486$ 9,625$ 8,264$ 5,242$ 2,511$ Government 6,621 6,701 5,937 3,861 1,804 Jumbo - - - 8 11 Total 14,108$ 16,326$ 14,200$ 9,112$ 4,326$ Broker Direct Locks Conventional Conforming 3,387$ 3,745$ 2,884$ 2,732$ 1,663$ Government 1,119 1,131 984 784 535 Jumbo - - - 10 21 Total 4,506$ 4,876$ 3,867$ 3,527$ 2,220$ Total locks 64,604$ 66,843$ 48,329$ 35,320$ 28,956$

CREDIT CHARACTERISTICS BY ACQUISITION/ORIGINATION PERIOD 30 Correspondent Consumer Direct Broker Direct 2Q21 3Q21 4Q21 1Q22 2Q22 2Q21 3Q21 4Q21 1Q22 2Q22 Government-insured 702 700 693 691 682 Government-insured 42 42 42 43 43 Conventional 757 755 750 750 753 Conventional 34 35 36 36 37 2Q21 3Q21 4Q21 1Q22 2Q22 2Q21 3Q21 4Q21 1Q22 2Q22 Government-insured 708 706 704 708 700 Government-insured 39 40 40 40 42 Conventional 748 744 742 738 727 Conventional 33 33 34 35 37 2Q21 3Q21 4Q21 1Q22 2Q22 2Q21 3Q21 4Q21 1Q22 2Q22 Government-insured 726 731 720 702 694 Government-insured 43 42 44 43 44 Conventional 760 760 755 754 757 Conventional 34 34 35 36 37 Weighted Average FICO Weighted Average DTI Weighted Average FICO Weighted Average DTI Weighted Average FICO Weighted Average DTI

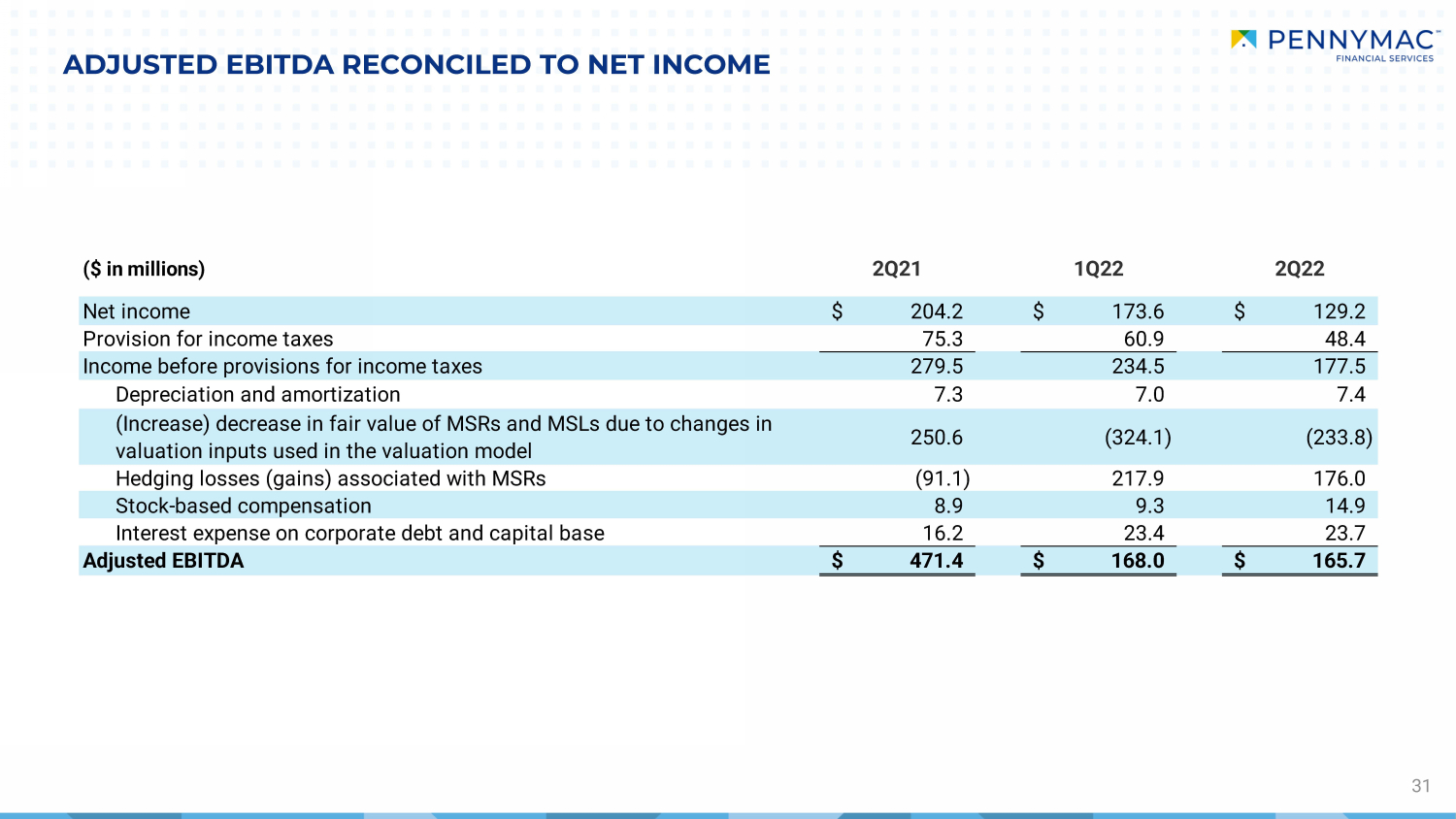

ADJUSTED EBITDA RECONCILED TO NET INCOME 31 ($ in millions) 2Q21 1Q22 2Q22 Net income 204.2$ 173.6$ 129.2$ Provision for income taxes 75.3 60.9 48.4 Income before provisions for income taxes 279.5 234.5 177.5 Depreciation and amortization 7.3 7.0 7.4 (Increase) decrease in fair value of MSRs and MSLs due to changes in valuation inputs used in the valuation model 250.6 (324.1) (233.8) Hedging losses (gains) associated with MSRs (91.1) 217.9 176.0 Stock-based compensation 8.9 9.3 14.9 Interest expense on corporate debt and capital base 16.2 23.4 23.7 Adjusted EBITDA 471.4$ 168.0$ 165.7$