Filed by Bank First Corporation

Pursuant to Rule 425 Under the Securities Act of 1933

And Deemed Filed Pursuant to Rule 14a-12

Under the Securities Exchange Act of 1934

Subject Company: Denmark Bancshares, Inc.

Commission File No. 001-38676

Date: January 19, 2022

MERGER INFORMATION

FOR EMPLOYEES

JANUARY 19, 2022

|  |

References to “Denmark” and “Bank First” refer to

Denmark Bancshares, Inc. and Bank First Corporation, respectively.

CONFIDENTIAL - NOT FOR PUBLIC DISTRIBUTION

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

TABLE OF CONTENTS

| MERGER ANNOUNCEMENT AND TIMELINE | 3 |

| WHO IS BANK FIRST? | 4-5 |

| WHO IS DENMARK STATE BANK? | 6 |

| MAP OF COMBINED LOCATIONS | 7 |

| QUESTIONS & ANSWERS | 8-9 |

| KEY CONTACTS | 10 |

| OFFICIAL PRESS RELEASE | 11-14 |

| LETTER TO DENMARK STATE BANK CUSTOMERS | 15-16 |

| LETTER TO DENMARK BANCSHARES SHAREHOLDERS | 17-18 |

| BANK FIRST YEAR-END EARNINGS RELEASE | 19-26 |

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

MERGER ANNOUNCEMENT

On Tuesday, January 18, 2022, Bank First Corporation, parent company of Bank First, entered into a merger agreement with Denmark Bancshares, Inc., the parent company of Denmark State Bank, to purchase Denmark Bancshares, Inc. and its banking offices in Denmark, Bellevue, Howard, Lawrence, Reedsville, Shawano and Whitelaw (see official press release on page 11 for complete information).

WHAT HAPPENS NEXT?

For Denmark State Bank customers, employees and the general public, things will look and feel the same for a period of time. Transition teams will begin working diligently behind the scenes obtaining approval from our regulators, planning for system conversions, creating customer communication, and working with employees prior to the merger.

During the next few weeks, the teams from both banks will begin introductions and begin planning for a smooth conversion that benefits both organizations, as well as our customers, shareholders and community.

PROJECTED TIMELINE:

JANUARY 18-19 Merger Agreement Signed by Bank First Corporation

Internal Announcement Made at both banks

Public Announcement Press release issued in all markets

Denmark Bancshares, Inc. Shareholders Letter sent |

Regulatory Approval Application sent to the OCC, WDFI, FDIC and Federal Reserve seeking

Conversion Team Banks work with core

Communication Customers, employees, Denmark Bancshares, | __ |

EARLY THIRD QUARTER Target Merger Closing Date Bank First completes the

Conversion Denmark State Bank customer accounts converted. | ||

| Inc. shareholders, and | |||||

| community stakeholders | |||||

| WEEK OF JANUARY 24 Denmark State Bank customer letters and email sent | informed of the transition to

Shareholder Approval Both companies’

| Welcome! under the Bank First name.

(Possibly sooner if Fiserv | |||

3

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

WHO IS BANK FIRST?

Our Promise:

We are a relationship-based bank focused on providing innovative products and services that are value driven to the communities we serve.

Bank First Corporation (BFC) provides financial services through its subsidiary, Bank First N.A., (“Bank First”) which was incorporated in 1894. The bank is an independent community bank with 21 locations throughout Wisconsin and is headquartered in Manitowoc. The bank has grown through both acquisitions and de novo branch expansion. The company employs approximately 293 employees and has assets of $2.9 billion as of 12/31/21.

Bank First offers loan, deposit and treasury management products at each of its banking offices. Insurance services are available through its bond with Ansay & Associates, LLC. Trust, investment advisory and other financial services are offered through the bank’s partnership with Legacy Private Trust, and an alliance with Morgan Stanley. The bank is a co- owner of a bank technology outfitter, UFS, LLC, which provides digital, core, cybersecurity, managed IT and cloud services.

Culture Statement

Bank First’s culture celebrates diversity, creativity, and responsiveness, with the highest ethical standards. We support and encourage employees to develop their careers. They are empowered with the tools to be successful and are held accountable for the results they deliver to our customers and shareholders. We maintain a strong credit culture as a foundation of sound asset quality.

Vision Statement

We will sustain our independence by remaining the top-performing provider of financial services in Wisconsin. Our team will strive to create value for our customers and shareholders by forging strong relationships and offering personalized and innovative solutions.

Diversity & Inclusion Statement

At Bank First, we value and continue to build upon a culture which encourages, supports and celebrates diversity and inclusion for our employees, customers and communities. This collaboration fuels a stronger foundation for innovation and connects us closer to the communities we serve.

QUICK FACTS:

• Founded in 1894 in Manitowoc, WI

• 293 employees

• 21 locations in Wisconsin

• $2.9 billion in assets (as of 12/31/21)

• Website: www.bankfirstwi.bank

• Stock Symbol: BFC

| Bank First Corporation | Financial Highlights | ||||||||||||||||||||

| Dollars in Thousands | 2017 | 2018 | 2019 | 2020 | 2021 | |||||||||||||||

| Net Income | $ | 15,313 | $ | 25,456 | $ | 26,694 | $ | 38,046 | $ | 45,444 | ||||||||||

| Total Assets | $ | 1,753,404 | $ | 1,793,165 | $ | 2,210,168 | $ | 2,718,016 | $ | 2,937,552 | ||||||||||

| Total Loans | $ | 1,397,547 | $ | 1,428,494 | $ | 1,736,343 | $ | 2,191,460 | $ | 2,235,515 | ||||||||||

| Total Deposits | $ | 1,506,642 | $ | 1,557,167 | $ | 1,843,311 | $ | 2,320,963 | $ | 2,528,440 | ||||||||||

| Net Interest Margin | 3.45 | % | 3.89 | % | 3.95 | % | 3.84 | % | 3.47 | % | ||||||||||

| Return on Average Assets | 1.04 | % | 1.43 | % | 1.37 | % | 1.52 | % | 1.60 | % | ||||||||||

| Return on Average Equity | 11.26 | % | 15.36 | % | 13.14 | % | 14.33 | % | 14.64 | % | ||||||||||

| NPAs/ Assets | 1.47 | % | 1.44 | % | 0.31 | % | 0.52 | % | 0.28 | % | ||||||||||

| Book Value (consolidated) | $ | 23.76 | $ | 26.37 | $ | 32.49 | $ | 38.25 | $ | 42.36 | ||||||||||

| Efficiency Ratio | 53.28 | % | 52.16 | % | 51.29 | % | 47.82 | % | 44.05 | % | ||||||||||

4

| SERVING OUR COMMUNITIES Bank First takes great pride in supporting our community. We believe by working together, we can transform lives and build stronger communities for our future generations. We have created a culture focused on community involvement, and our employees are empowered to volunteer and give back in many ways. In 2021, Bank First contributed over $543,000 to 504 local events and non-profit organizations. Our employees donated over 8,145 hours of volunteering in the community as well. Giving back has allowed Bank First to develop meaningful relationships with local families, businesses, and non-profit organizations. We believe these relationships strengthen us and the communities we serve. |  | |

| ||

5

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

WHO IS DENMARK

STATE BANK?

Mission Statement:

By building authentic relationships, we actively support the success of our communities through our expertise, commitment and service to customers

Denmark Bancshares Inc., the parent company of Denmark State Bank, was founded in 1909 in the Village of Denmark, Wisconsin, and relied on the trust and hard work of its customers to be successful. With the passage of time, much has changed within the bank — technology has increased the availability of services offered to customers; locations have been added in local communities; and employees and customers have been added to the bank.

One thing remains the same, the dedicated focus on serving the hard- working people of Northeast Wisconsin. Whether you’re a small business owner, a farmer, a student, a long-time member of the community, or if you have recently moved to Northeast Wisconsin, Denmark State Bank prides itself on giving every single person their utmost attention and respect.

Denmark State Bank has seven full-service banking offices serving primarily Brown, Kewaunee, Manitowoc, Outagamie, Shawano and Sheboygan counties. In each of these communities, the bank is known for its high level of personal service to customers and its commitment to the communities it serves.

Denmark State Bank is dedicated to offering innovative products and providing the most recent technology to its customers. The bank’s business customers have the benefit of a variety of cash management tools, and in addition to its traditional banking services they also offer online and mobile banking, bill pay and e-statements to all of its customers.

QUICK FACTS:

• Founded in 1909 in Denmark, WI • 109 employees • 7 locations in Wisconsin • $687.6 million in assets (as of 12/31/21) • Website: www.denmarkstate.com • Stock Symbols: DMKBA and DMKBB | Denmark State Bank is proud of its roots and continued commitment to the communities where its customers and employees live and work. Each year the bank gives back through monetary donations, sponsorships of local clubs and events, and provides the opportunity for bank employees to volunteer at many local organizations in their respective communities. As a community bank, Denmark State Bank reflects the values lived by the people of Northeast Wisconsin. |

Denmark Bancshares | Financial Highlights

| Dollars in Thousands | 2017 | 2018 | 2019 | 2020 | 2021 | |||||||||||||||

| Net Income | $ | 2,800 | $ | 4,087 | $ | 4,952 | $ | 3,898 | $ | 6,498 | ||||||||||

| Total Assets | $ | 474,520 | $ | 506,202 | $ | 552,593 | $ | 646,441 | $ | 687,646 | ||||||||||

| Total Loans | $ | 372,480 | $ | 420,827 | $ | 434,770 | $ | 475,953 | $ | 479,429 | ||||||||||

| Total Deposits | $ | 396,690 | $ | 417,224 | $ | 457,435 | $ | 563,275 | $ | 614,500 | ||||||||||

| Net Interest Margin | 3.61 | % | 3.90 | % | 3.47 | % | 2.87 | % | 3.29 | % | ||||||||||

| Return on Average Assets | 0.61 | % | 0.84 | % | 0.96 | % | 0.64 | % | 0.98 | % | ||||||||||

| Return on Average Equity | 4.66 | % | 6.70 | % | 7.81 | % | 5.95 | % | 9.63 | % | ||||||||||

| NPAs/ Assets | 0.25 | % | 0.13 | % | 0.08 | % | 0.08 | % | 0.07 | % | ||||||||||

| Book Value (consolidated) | $ | 18.41 | $ | 19.00 | $ | 20.02 | $ | 20.75 | $ | 21.99 | ||||||||||

| Efficiency Ratio | 74.80 | % | 70.24 | % | 69.63 | % | 76.18 | % | 65.21 | % | ||||||||||

6

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

OUR COMBINED FOOTPRINT:

| STRONGER TOGETHER | Total Assets: $3.6 billion

Total Loans: $2.7 billion

Total Deposits: $3.2 billion

*Approximate proforma numbers as of 12/31/2021 |

7

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

QUESTIONS AND ANSWERS ABOUT THE MERGER

Why did Denmark decide to merge?

| • | Merging with a strong, long-standing organization committed to the communities it serves will ensure Denmark has the resources required to meet the growing demands of a competitive market place and continue to deliver innovative products and services to valued customers in Northeast Wisconsin for years to come. |

Why did Denmark choose Bank First?

| • | Similar to Denmark, Bank First is a long-standing organization focused on community banking, dating back to 1894. |

| • | Joining Bank First will allow Denmark to enhance its contributions to its communities. Bank First has created a culture focused on community involvement, and its employees are empowered to volunteer and give back in many ways. In 2021, Bank First contributed over $543,000 to 504 local events and non-profit organizations. Bank First employees donated over 8,145 hours of volunteering in the community as well. In addition to volunteerism and financial support, Bank First takes pride in using customers and local businesses as its vendors. |

| • | Like Denmark, Bank First is a true relationship-based bank. It places utmost importance on getting to know customers on a personal level to help them achieve their financial goals. It takes pride in being the primary bank of each customer, maintaining the loan balances and deposit accounts of each family and organization. Doing so allows Bank First to take in local deposits and reinvest those funds in the communities it serves. |

| • | Bank First values its employees as much as Denmark values theirs. Bank First is committed to excellence and believes in supporting and encouraging employees to develop their careers. Bank First has been named one of the “Best Banks to Work For” in 2018, 2019, and 2020 by American Banker magazine. |

| • | Denmark customers will benefit from Bank First’s 49.8% ownership of UFS, LLC, a bank technology outfitter which provides digital, core, cybersecurity, managed IT, and cloud services to banks in the Midwest. Bank First’s relationship with UFS creates opportunities to access the latest advancements in banking technology at a faster rate than its peers. |

| • | A benefit to business customers will be to leverage the combined organization’s suite of treasury management products and services, specifically taking advantage of Bank First’s in-house merchant services program. |

| • | Bank First has a growing agricultural banking team and is committed to serving the financial needs of farmers and their families across Wisconsin. Denmark’s agricultural customers will benefit from enhanced treasury management services and an increased legal lending limit. Denmark’s current legal lending limit is set at $11.9 million. The legal lending limit of the combined institution will increase to $49.2 million after the merger. |

8

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

QUESTIONS AND ANSWERS (continued)

Why did Bank First choose Denmark?

• The merger brings together two strong, culturally-aligned organizations focused on relationship banking.

| • | The merger aligns with Bank First’s strategy to grow within specific markets in the State of Wisconsin. Denmark has established itself as a leading provider of financial products and services in Northeast Wisconsin, resulting in a strong deposit base. This complements Bank First’s market leading presence in Manitowoc County and enhances its growing footprint in Brown County. Bank First recently announced the purchase of a seven acre parcel of property to build a new flagship office along Shawano Avenue and South Taylor Street next to the Meijer store in Green Bay, solidifying its commitment to Green Bay and the surrounding communities. |

| • | Denmark has significant expertise in agricultural banking dating back to 1909. Its highly knowledgeable team will complement Bank First’s existing agricultural banking group and will be essential as Bank First continues to expand its presence in this sector. In addition, the combined institution will be able to take advantage of the recent disruption in this space. |

| • | Like Bank First, Denmark’s commitment to relationship-based banking is evidenced by the strong character and integrity of its customers. Northeast Wisconsin, Denmark’s core market, boasts some of the highest credit scores in the United States. This aligns well with Bank First’s focus on superior credit quality. |

| • | Denmark’s valued shareholder base is very similar to Bank First’s, featuring multi-generational shareholders who live in and have a deep appreciation for the communities it serves. |

| • | Denmark Bancshares, Inc. is strong financially, evidenced by its stock price per share growing 176% since 2012. Since 2012, it has also reported loan growth at 61% and deposit growth of 82%. |

Will there be branch closures?

| • | Bank First is currently evaluating the footprint of the combined organizations. Its goal is to determine if there will be any branch closures as soon as possible. |

Will there be job losses?

| • | Understandably, there will be overlapping roles once the two institutions are combined. Although there are no job guarantees, Bank First will make every effort to assess its business needs and retain employees. If it is unable to do so, displaced employees will be offered a severance package to assist them with pay and benefits. |

How do Bank First’s employee benefits compare to Denmark State Bank’s benefits?

| • | Bank First will be distributing employee benefit information and FAQs on Friday, January 21. Be sure to write down any questions you have and contact Sherry Jonet with your questions. |

When will the merger be complete?

| • | The closing of the transaction is targeted to take place early third quarter 2022. The conversion will take place thereafter. |

Media Questions

| • | If either company receives questions from the media, those questions should be directed to Kelly Dvorak, General Counsel/Corporate Secretary at Bank First: kdvorak@bankfirstwi.bank, (920) 652-3244. |

9

MERGER INFORMATION FOR EMPLOYEES - JANUARY 19, 2022

KEY CONTACTS:

| BANK FIRST | ||

| Mike Molepske, Chief Executive Officer.................... | mmolepske@bankfirstwi.bank......... | (920) 652-3202 |

| Kevin LeMahieu, Chief Financial Officer.................... | klemahieu@bankfirstwi.bank........... | (920) 652-3362 |

| Kelly Dvorak, General Counsel/Corporate Secretary....... | kdvorak@bankfirstwi.bank............... | (920) 652-3244 |

| Joan Woldt, Chief Operating Officer......................... | jwoldt@bankfirstwi.bank.................. | (920) 901-7971 |

| Deb Weyker, VP Marketing......................................... | dweyker@bankfirstwi.bank.............. | (920) 652-3274 |

| Sherry Jonet, VP Human Resources............................ | sjonet@bankfirstwi.bank................... | (920) 652-3291 |

| Shannon Klahn, Assistant Executive Officer............... | sklahn@bankfirstwi.bank.................. | (920) 652-3222 |

| DENMARK | ||

| Scot Thompson, President/Chief Executive Officer | ||

| Chairman of the Board................................................. | scott@denmarkstate.com............... | (920) 863-1057 |

| Jacqui Engebos, Chief Financial Officer................... | jacquie@denmarkstate.com.......... | (920) 863-1023 |

| Lori Sisel, Executive Assistant........................................ | loris@denmarkstate.com................. | (920) 863-1028 |

10

N E W S R E L E A S E

|  |

P.O. Box 10, Manitowoc, WI 54221-0010

For further information, contact:

Deb Weyker, Vice President Marketing

Phone: (920) 652-3274

dweyker@bankfirstwi.bank

Company Release – 01/19/2022

Bank First Corporation Signs Definitive Agreement to Acquire

Denmark Bancshares, Inc.

Highlights of the Announced Transaction

| § | Aligns with Bank First’s strategic growth plans within the State of Wisconsin |

| § | Benefits customers of both institutions through an enhanced suite of products and services |

| § | Companies share a similar relationship-based, community banking philosophy |

| § | Strengthens Bank First’s franchise through greater deposit market share in Northeast Wisconsin |

| § | Denmark’s expertise in agricultural banking, along with Bank First’s commitment and scale, will allow the combined organization to better serve farmers across Wisconsin. |

MANITOWOC, Wis. and DENMARK, Wis., January 19, 2022 /PRNewswire/ -- Bank First Corporation (Nasdaq: BFC) (“Bank First” or “the Company”), the holding company of Bank First, N.A., announced today the signing of an Agreement and Plan of Merger with Denmark Bancshares, Inc. (OTCQX: DMKBA and DMKBB) (“Denmark”), parent company of Denmark State Bank, a Wisconsin state-chartered bank, under which Bank First has agreed to acquire 100% of the common stock of Denmark in a combined stock-and-cash transaction.

Under the terms of the Agreement and Plan of Merger, each Denmark shareholder will have the option to receive either $38.10 in cash per share or 0.5276 of a share of Bank First’s common stock in exchange for each share of Denmark common stock, subject to customary proration and allocation procedures, such that no less than 80% of Denmark shares will receive stock consideration and no greater than 20% will receive cash consideration. The aggregate consideration is valued at approximately $119.5 million.

11

As of December 31, 2021, Denmark had approximately $687.6 million in consolidated assets, $479.4 million in gross loans, $614.5 million in deposits and $68.0 million in consolidated stockholders’ equity. Based on the financial results as of December 31, 2021, the combined company will have total assets of approximately $3.6 billion, loans of approximately $2.7 billion and deposits of approximately $3.2 billion.

The Agreement and Plan of Merger has been approved by the Boards of Directors of Bank First and Denmark. The closing of the transaction, which is targeted to take place early third quarter 2022, is subject to customary closing conditions, including regulatory approval and approval by the shareholders of Denmark and Bank First.

The two institutions offer a diverse set of competencies that when combined are expected to result in a stronger organization. Denmark has established itself as a leading provider of financial products and services in Northeast Wisconsin, resulting in a strong deposit base. This complements Bank First’s already strong presence in Manitowoc County and enhances its growing footprint in Brown County. Bank First recently announced the purchase of a seven acre parcel of property to build a new flagship office along Shawano Avenue and South Taylor Street next to the Meijer store in Green Bay, solidifying its commitment to Green Bay and the surrounding communities.

Denmark’s customers will benefit from Bank First’s 49.8% ownership of UFS, LLC, a bank technology outfitter which provides digital, core, cybersecurity, managed IT, and cloud services to banks in the Midwest. Bank First’s relationship with UFS creates opportunities to access the latest advancements in banking technology at a faster rate than its peers.

Bank First’s focus on providing innovative products and services will allow the customers of Denmark to benefit from a wide array of retail banking products and loan programs tailored to the unique needs of each individual or family. A benefit to business customers will be to leverage the combined organization’s suite of treasury management products and services, specifically taking advantage of Bank First’s in-house merchant services program. Additionally, Denmark has expertise in agricultural banking dating back to 1909. Denmark’s highly knowledgeable agricultural team will be essential as Bank First continues to expand its presence in this sector.

“We are thrilled to unite with Denmark State Bank and expand our footprint in Wisconsin,” stated Mike Molepske, President and Chief Executive Officer of Bank First. “Similar to Bank First, Denmark is a long-standing organization focused on relationship banking. Bank First and Denmark date back to 1894 and 1909, respectively. Together, we will continue our shared mission of building meaningful relationships and strengthening the communities we serve by providing value-driven financial solutions and giving back through volunteerism and philanthropic initiatives.”

“We look forward to working together to maintain our tradition of community banking in Northeastern Wisconsin,” stated Scot Thompson, President and Chief Executive Officer of Denmark State Bank. “Our core values at Denmark State Bank include integrity, honesty and exemplary customer service, and Bank First is the ideal partner to carry these values forward for years to come. This partnership strengthens our team, provides an enhanced suite of products to our customers and adds value to our loyal shareholders.”

Hovde Group, LLC served as financial advisor to Bank First and Alston & Bird LLP served as legal counsel. Piper Sandler & Co. served as financial advisor to Denmark and Godfrey & Kahn S.C. served as legal counsel.

Bank First Corporation

Bank First Corporation is a bank holding company headquartered in Manitowoc, Wisconsin with total assets of approximately $2.9 billion. Its principal activity is the ownership and operation of Bank First, a nationally-chartered community bank that operates 21 banking centers serving Wisconsin. The bank’s history dates back to 1894 when it was founded as the Bank of Manitowoc. For more information on Bank First, please visit www.bankfirstwi.bank.

12

Denmark Bancshares, Inc.

Denmark Bancshares, Inc. is a bank holding company headquartered in Denmark, Wisconsin with total assets of approximately $687.6 million. Its principal activity is the ownership and operation of Denmark State Bank, an independent community bank that offers seven banking offices in Denmark, Bellevue, Howard, Lawrence, Reedsville, Shawano, and Whitelaw. Denmark State Bank offers a wide variety of financial products and services including loans, deposits, mortgage banking, and investment services.

Forward-Looking Statements

This news release contains “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. In general, forward-looking statements usually use words such as “may,” “believe,” “expect,” “anticipate,” “intend,” “should,” “plan,” “estimate,” “predict,” “continue” and “potential” or the negative of these terms or other comparable terminology, including statements related to the expected timing of the closing of the Merger, the expected returns and other benefits of the Merger to shareholders, expected improvement in operating efficiency resulting from the Merger, estimated expense reductions resulting from the transactions and the timing of achievement of such reductions, the impact on and timing of the recovery of the impact on tangible book value, and the effect of the Merger on Bank First’s capital ratios. Forward-looking statements represent management’s beliefs, based upon information available at the time the statements are made, with regard to the matters addressed; they are not guarantees of future performance. Forward-looking statements are subject to numerous assumptions, risks and uncertainties that change over time and could cause actual results or financial condition to differ materially from those expressed in or implied by such statements.

Factors that could cause or contribute to such differences include, but are not limited to (1) the risk that the cost savings and any revenue synergies from the Merger may not be realized or take longer than anticipated to be realized, (2) disruption from the Merger with customers, suppliers, employee or other business partners relationships, (3) the occurrence of any event, change or other circumstances that could give rise to the termination of the Merger Agreement, (4) the risk of successful integration of Denmark’s business into Bank First, (5) the failure to obtain the necessary approval by the shareholders of Denmark or Bank First, (6) the amount of the costs, fees, expenses and charges related to the Merger, (7) the ability by Bank First to obtain required governmental approvals of the Merger, (8) reputational risk and the reaction of each of the companies’ customers, suppliers, employees or other business partners to the Merger, (9) the failure of the closing conditions in the Merger Agreement to be satisfied, or any unexpected delay in closing of the Merger, (10) the risk that the integration of Denmark’s operations into the operations of Bank First will be materially delayed or will be more costly or difficult than expected, (11) the possibility that the Merger may be more expensive to complete than anticipated, including as a result of unexpected factors or events, (12) the dilution caused by Bank First’s issuance of additional shares of its common stock in the Merger transaction, and (13) general competitive, economic, political and market conditions. Other relevant risk factors may be detailed from time to time in Bank First’s press releases and filings with the Securities and Exchange Commission (the “SEC”). Consequently, no forward-looking statement can be guaranteed. Neither Bank First nor Denmark undertakes any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. For any forward-looking statements made in this news release or any related documents, Bank First and Denmark claim protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

13

Additional Information about the Merger and Where to Find It

This press release does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval with respect to the proposed transaction. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended, and no offer to sell or solicitation of an offer to buy shall be made in any jurisdiction in which such offer or solicitation would be unlawful. In connection with the proposed Merger, Bank First will file with the SEC a registration statement on Form S-4 that will include a joint proxy statement of Denmark and Bank First, and a prospectus of Bank First, as well as other relevant documents concerning the proposed transaction. WE URGE INVESTORS AND SECURITY HOLDERS TO READ THE REGISTRATION STATEMENT ON FORM S-4, THE JOINT PROXY STATEMENT/PROSPECTUS INCLUDED WITHIN THE REGISTRATION STATEMENT ON FORM S-4 AND ANY OTHER RELEVANT DOCUMENTS TO BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED MERGER BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT BANK FIRST, DENMARK AND THE PROPOSED MERGER. The joint proxy statement/prospectus will be sent to the shareholders of Denmark and Bank First seeking the required shareholder approval. Investors and security holders will be able to obtain free copies of the registration statement on Form S-4 and the related joint proxy statement/prospectus, when filed, as well as other documents filed with the SEC by Bank First through the web site maintained by the SEC at www.sec.gov. Documents filed with the SEC by Bank First will also be available free of charge by directing a written request to Bank First Corporation, P.O. Box 10, Manitowoc, Wisconsin 54221-0010, Attn: Kelly Dvorak. Bank First’s telephone number is (920) 652-3100.

Participants in the Transaction

Bank First, Denmark and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of Denmark and Bank First in connection with the proposed transaction. Certain information regarding the interests of these participants and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the joint proxy statement/prospectus regarding the proposed transaction when it becomes available. Additional information about Bank First and its directors and officers may be found on Bank First’s Investor Relations page at www.BankFirstWI.bank.

Contacts

Bank First: Mike Molepske, President & CEO, at mmolepske@bankfirstwi.bank or (920) 652-3202

Denmark: Scot Thompson, Chairman, President & CEO, at scott@denmarkstate.com or (920) 863-1057

14

Dear Valued Customer,

As you may have heard, we are excited to announce Denmark State Bank will soon become part of the Bank First family. On January 18, 2022, Denmark Bancshares, Inc. formally agreed to merge with Bank First Corporation. Our two organizations possess a diverse set of competencies that when combined allow us to offer an enhanced suite of products and services to our customers while strengthening the communities we serve through volunteerism and philanthropic initiatives.

Why did Denmark State Bank decide to merge?

Merging with a strong, long-standing organization will ensure we have the resources required to meet the growing demands of a competitive market place and continue to deliver innovative products and services to our valued customers in Northeast Wisconsin for years to come.

Who is Bank First?

Bank First is an independent, relationship-based bank headquartered in Wisconsin. Through a combination of acquisitions and de novo offices, the bank has expanded to serve the financial needs of individuals, families, businesses and non-profit organizations throughout Wisconsin. Bank First’s growth has been achieved through its relationship-based model of banking. They take pride in knowing their customers on a personal level and working together to create value-based, innovative solutions.

Why did Denmark State Bank choose Bank First?

| • | Similar to Denmark State Bank, Bank First is a long-standing organization focused on community banking, dating back to 1894. |

| • | Joining Bank First will allow us to enhance our contributions to our communities. Bank First has created a culture focused on community involvement, and its employees are empowered to volunteer and give back in many ways. In 2021, Bank First contributed over $543,000 to 504 local events and non-profit organizations. Its employees donated over 8,145 hours of volunteering in the community as well. In addition to volunteerism and financial support, Bank First takes pride in using customers and local businesses as its vendors. | |

| • | Like us, Bank First is a true relationship-based bank. They place utmost importance on getting to know customers on a personal level to help them achieve their financial goals. Bank First takes pride in being the primary bank of each customer, maintaining the loan balances and deposit accounts of each family and organization. Doing so allows the bank to take in local deposits and reinvest those funds in the communities it serves. |

| • | Bank First values its employees as much as we value ours. The bank is committed to excellence and believes in supporting and encouraging employees to develop their careers. Bank First has been named one of the “Best Banks to Work For” in 2018, 2019, and 2020 by American Banker magazine. |

| • | Our customers will benefit from Bank First’s 49.8% ownership of UFS, LLC, a bank technology outfitter which provides digital, core, cybersecurity, managed IT, and cloud services to banks in the Midwest. Bank First’s relationship with UFS creates opportunities to access the latest advancements in banking technology at a faster rate than its peers. |

| • | Bank First’s focus on providing innovative products and services will allow our customers to benefit from a wide array of products tailored to the unique needs of each individual or family. A benefit to business customers will be to leverage the combined organization’s suite of treasury management products and services, specifically taking advantage of Bank First’s in-house merchant services program. |

| DenmarkState.com |  |

15

| • | Bank First has a growing agricultural banking team and is committed to serving the financial needs of farmers and their families across our markets. By partnering with Bank First, our agricultural customers will benefit from enhanced treasury management services and an increased legal lending limit. |

Why did Bank First choose Denmark State Bank?

| • | The merger brings together two strong, culturally-aligned organizations focused on relationship banking. |

| • | The merger aligns with Bank First’s strategy to grow within specific markets in the State of Wisconsin. Denmark has established itself as a leading provider of financial products and services in Brown and Manitowoc counties, resulting in a strong deposit base. This complements Bank First’s market leading presence in Manitowoc County and enhances its growing footprint in Brown County. Bank First recently announced the purchase of a seven acre parcel of property to build a new flagship office along Shawano Avenue and South Taylor Street next to the Meijer store in Green Bay, solidifying its commitment to Green Bay and the surrounding communities. |

| • | Denmark State Bank has significant expertise in agricultural banking dating back to 1909. Our highly knowledgeable team will complement Bank First’s existing agricultural banking group and will be essential as it continues to expand its presence in this sector. |

| • | Like Bank First, Denmark State Bank’s commitment to relationship-based banking is evidenced by the strong character and integrity of our customers. Northeast Wisconsin, our core market, boasts some of the highest credit scores in the United States. This aligns well with Bank First’s focus on superior credit quality. |

| • | Denmark’s valued shareholder base is very similar to Bank First’s, featuring multi-generational shareholders who live in and have a deep appreciation for the communities we serve. |

| • | Denmark Bancshares, Inc. is strong financially, evidenced by our stock price per share growing 176% since 2012. Since 2012, we have also reported loan and deposit growth of 61% and 82%, respectively. |

What can you expect?

You can expect to see no change in the high-quality, personalized level of care and service you currently receive. The closing of the transaction is targeted to take place early third quarter 2022. The conversion will take place thereafter. As the merger approaches, you will receive detailed communication including a comprehensive timeline of events, important account changes, information on Bank First’s products and services, contact information for questions and concerns and frequently asked questions.

We are confident the merger of Denmark State Bank with Bank First will allow us to better meet the needs of our customers, shareholders and communities.

Sincerely,

Scot G. Thompson

Chairman, President & Chief Executive Officer

scott@denmarkstate.com | 920-863-1057

16

Dear Valued Shareholder,

On behalf of the Board of Directors of Denmark Bancshares, Inc. (“Denmark”), I am pleased to inform you that on January 18, 2022, we signed a formal agreement to merge with Bank First Corporation (“Bank First”). Our two organizations possess a diverse set of competencies that when combined allow us to offer an enhanced suite of products and services to our customers while strengthening the communities we serve through volunteerism and philanthropic initiatives.

Who is Bank First?

Bank First is an independent, relationship-based bank headquartered in Manitowoc, Wisconsin. Through a combination of acquisitions and de novo offices, Bank First has expanded to serve the financial needs of individuals, families, businesses and non-profit organizations throughout Wisconsin. Bank First’s growth has been achieved through its relationship-based model of banking. Bank First takes pride in knowing its customers on a personal level and working together to create value-based, innovative solutions. For more information on Bank First, including access to their comprehensive Investor Relations Center, please visit www.BankFirstWI.bank. You can also find Bank First listed on NASDAQ under “BFC”.

Why did Denmark decide to merge with Bank First?

Merging with a strong, long-standing organization will ensure we have the resources required to meet the growing demands of a competitive market place and continue to deliver innovative products and services to our valued customers in Northeast Wisconsin for years to come. Merging also allows us to continue enhancing shareholder value through a partnership with an organization that strongly believes in sharing its success with its shareholders.

Additionally, our financial institutions are culturally aligned, and both groups of shareholders have a rich history with their respective bank. Similar to Denmark, Bank First’s shareholder base features multi-generational shareholders who live in and have a deep appreciation for the communities we serve.

How does a merger with Bank First impact your dividends?

Bank First has long believed that its shareholders should share in its success. As one of the top-performing banks in Wisconsin, Bank First has been sharing that success with its shareholders in the form of a quarterly dividend for well over 40 years. This is consistent with Denmark’s track record of paying dividends to shareholders for 38 consecutive years.

Bank First’s dividend has never decreased and has never been suspended, even during the Great Recession of 2008 and the COVID-19 pandemic. In the first three quarters of 2021, Bank First paid a quarterly dividend of $ 0.21 per share, in addition to a special dividend of $0.29 per share in the third quarter. In the fourth quarter, Bank First increased the quarterly dividend to $0.22 per share. As a publicly-traded institution, it also offers a dividend reinvestment plan (DRIP) to its shareholders, where dividends can be automatically reinvested to purchase more Bank First shares. You will have the opportunity to enroll in the DRIP using Bank First’s transfer agent, Computershare, upon closing of the merger, which is targeted to take place early third quarter 2022.

Next Steps / What to Expect

• If you hold paper stock certificates, we highly recommend that you locate them at your earliest convenience. In order to convert your Denmark stock into Bank First stock or cash, holders of paper certificates will be required to turn in their original Denmark stock certificates. If your certificate is lost, you will be required to replace it. Replacement can be done before the close of the merger through Denmark’s transfer agent, American Stock Transfer & Trust Company, LLC, or after close of the merger, through Bank First’s transfer agent, Computershare. In either case, the cost of replacing a lost certificate is 3-5% of its current market value (depending on the transfer agent), plus an administrative fee of about $75.00. If your Denmark stock is held in book entry or electronic form, no paper certificate is required. If you need to replace a lost certificate, please contact Lori Sisel at (920) 863-1028 or loris@denmarkstate.com.

17

• In the coming months, you will receive an invitation to attend a Special Shareholder Meeting to vote on the proposed merger with Bank First. A packet containing a proxy statement, voting instructions, and a proxy card for the meeting will be enclosed with the invitation. We ask for your support and recommend that you vote your shares “FOR” the proposed merger.

• Upon converting your shares from Denmark to Bank First, your shares will be held electronically with Bank First’s transfer agent, Computershare. You will not receive paper stock certificates. As a shareholder, you will benefit from increased flexibility in accessing information and processing transactions using Computershare’s toll-free shareholder services center, automated telephone support system and Internet capabilities. For more information, please visit www.computershare.com.

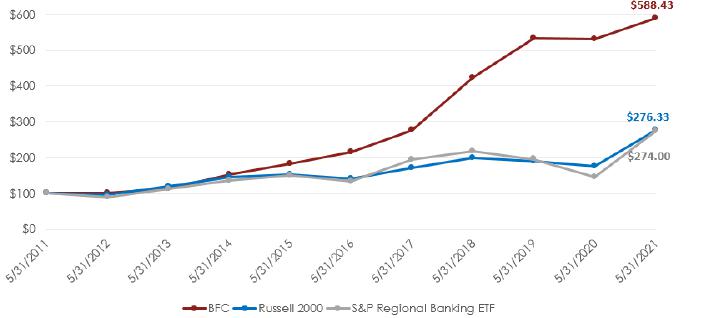

Bank First Stock Performance (Total Return)

Value of $100 invested on June 1, 2011 (10 year)

The closing of the transaction is targeted to take place early third quarter 2022. The conversion will take place thereafter. We are confident the merger of Denmark with Bank First will allow us to better meet the needs of our customers, shareholders and communities. If you have any questions about the transaction, please reach out to me at any time.

Sincerely,

Scot G. Thompson

Chairman, CEO and President

scott@denmarkstate.com | 920-863-1057

18

P.O. Box 10, Manitowoc, WI 54221-0010

For further information, contact:

Kevin M LeMahieu, Chief Financial Officer

Phone: (920) 652-3200 / klemahieu@bankfirstwi.bank

FOR IMMEDIATE RELEASE

Bank First Announces Net Income for the Fourth Quarter of 2021

| • | Net income of $11.2 and $45.4 million for the three months and year ended December 31, 2021 |

| • | Earnings per common share of $1.46 and $5.92 for the three months and year ended December 31, 2021 |

| • | Annualized return on average assets of 1.53% and 1.60% for the three months and year ended December 31, 2021 |

| • | Quarterly cash dividend of $0.22 per share declared, an increase of 4.8% from prior-year fourth quarter quarterly cash dividend |

MANITOWOC, Wis, January 18, 2022 -- Bank First Corporation (NASDAQ: BFC) (“Bank First” or the “Bank”), the holding company for Bank First, N.A., reported net income of $11.2 million, or $1.46 per share, for the fourth quarter of 2021, compared with net income of $11.5 million, or $1.49 per share, for the prior-year fourth quarter. For the year ended December 31, 2021, Bank First earned $45.4 million, or $5.92 per share, compared to $38.0 million, or $5.07 per share for the year ended December 31, 2020.

Operating Results

Net interest income (“NII”) during the fourth quarter of 2021 was $23.2 million, up $0.3 million from the previous quarter but down $1.2 million from the fourth quarter of 2020. NII for the year ended December 31, 2021 was $90.1 million, up from $86.8 million during the prior year.

As mentioned in previous releases, Bank First was a very active participant in the Paycheck Protection Program (“PPP”), a Small Business Administration (“SBA”) loan program aimed at supporting small business through the turbulent economic environment created by the COVID-19 pandemic (“COVID”). Bank First originated over $381.3 million in loans to new and existing customers under this program, $31.1 million of which remained unpaid and unforgiven as of December 31, 2021. Origination fees collected from PPP loan originations totaled over $14.6 million. Under accounting rules, the Bank recognizes these fees as an addition to NII over the contractual life of the related loan, with any remaining fee being fully recognized into NII if the loan is paid off or forgiven prior to the original maturity date. As is the case with any institution participating in PPP originations, this accounting treatment has caused significant variations in the Bank’s NII and interest margins quarter-to-quarter based on how many PPP loans are forgiven during the period. Unrecognized PPP origination fees totaled $1.1 million at December 31, 2021, compared to $2.2 million and $2.6 million at September 30, 2021 and December 31, 2020, respectively.

19

NII related to purchase accounting entries, resulting from our acquisitions of other institutions over the last several years, increased net income (after tax) during the fourth quarter of 2021 by $0.6 million, or $0.07 per share, compared to $0.5 million, or $0.07 per share, for the fourth quarter of 2020. For the years ended December 31, 2021 and 2020, the impact of these purchase accounting entries increased net income (after tax) by $1.5 million, or $0.19 per share, and $3.1 million, or $0.41 per share, respectively.

Net interest margin (“NIM”) was 3.47% for the fourth quarter of 2021, matching the prior quarter and lower than 4.01% for the fourth quarter of 2020. The aforementioned purchase accounting entries added 0.11%, 0.04% and 0.12% to NIM for each of these periods, respectively. NIM created by the presence of PPP activity during these periods added approximately 0.12%, 0.21% and 0.29%, respectively. NIM was 3.47% for the year ended December 31, 2021, including 0.08% from the impact of purchase accounting entries, compared to 3.84%, including 0.19% from the impact of purchase accounting entries, for the year ended December 31, 2020.

Bank First recorded a provision for loan losses of $0.6 million during the fourth quarter of 2021, compared to $1.7 million during the fourth quarter of 2020. Provision expense was $3.1 million for the year ended December 31, 2021 compared to $7.1 million for the year ended December 31, 2020. While provision expense was elevated during 2020 in response to uncertainty created by COVID and society’s response to it, actual asset quality metrics during the course of 2021, as further discussed later in this release, have remained strong and allowed for a reduction in provision expense during the current year.

Noninterest income was $5.7 million for the fourth quarter of 2021, compared to $6.7 million for the fourth quarter of 2020. Loan servicing income, which includes the impact of changes in the valuation of mortgage servicing rights (“MSR”) on the Bank’s balance sheet, totaled $1.6 million for the fourth quarter of 2021, comparing favorably to $0.2 million during the prior-year fourth quarter. During the fourth quarter of 2021 the Bank experienced a positive valuation adjustment to its MSR of $0.6 million compared to a negative valuation adjustment of $0.4 million during the fourth quarter of 2020, leading to much of the improvement year-over-year in this noninterest income classification. Gains on the sale of secondary market mortgage loans declined from $2.2 million during the fourth quarter of 2020 to $1.2 million during the fourth quarter of 2021. While these gains remained elevated through the final two quarters of 2021, they have declined from unprecedented profitability in this area between the fourth quarter of 2020 and the second quarter of 2021. Finally, the Bank recognized a $1.7 million gain due to the sale of a branch location during the fourth quarter of 2020. There was no similar event during 2021, leading to a decrease in other noninterest income.

20

Noninterest expense was $13.6 million in the fourth quarter of 2021, compared to $14.0 million during the fourth quarter of 2020. Occupancy, equipment and office expenses decreased by $0.4 million from elevated levels during the prior-year fourth quarter as the Bank completed several large scale remodel projects during that quarter. Data processing expense decreased $0.2 million from the prior-year fourth quarter, primarily due to expense incurred during the fourth quarter of 2020 from the significant PPP activity during that year. During the fourth quarter of 2021 the Bank incurred a $0.2 million charge-down on its sole foreclosed property owned, leaving a value of $10,000 on that property. This charge-down compared unfavorably to minor gains on sales of foreclosed property during the prior-year fourth quarter, leading to a negative $0.2 million variance year-over-year. Finally, other noninterest expense increased by $0.8 million, or 56.7%, from the prior-year fourth quarter. During the fourth quarter of 2021, Bank First incurred a one-time expense when it purchased a domain name from another institution for $0.8 million as part of a rebranding initiative.

Balance Sheet

Total assets were $2.94 billion at December 31, 2021, a $219.5 million increase from December 31, 2020. Total loans were $2.24 billion at December 31, 2021, up $44.8 million from December 31, 2020. Excluding PPP originations and repayments or forgiveness, loans grew by 9.1% over the trailing twelve months, including annualized growth of 10.5% during the fourth quarter. Total deposits, nearly all of which remain core deposits, were $2.53 billion at December 31, 2021, up $207.5 million from December 31, 2020. Noninterest-bearing demand deposits comprised 32.0% of the Bank’s total core deposits at December 31, 2021, compared to 31.2% at December 31, 2020. Time deposits, which typically carry the highest interest rates of all deposit products, comprised 10.1% of the Bank’s total core deposits at December 31, 2021, compared to 14.8% at December 31, 2020.

21

Asset Quality

Nonperforming assets at December 31, 2021 totaled $8.2 million, down from $12.1 million at the end of the previous quarter and $14.0 million at the end of 2020. Nonperforming assets to total assets ended 2021 at 0.28%, down from 0.42% at the end of the previous quarter and 0.52% at the end of 2020.

Capital Position

Stockholders’ equity totaled $322.7 million at December 31, 2021, an increase of $27.8 million from the end of 2020. Strong earnings served to increase capital while being offset by dividends totaling $8.7 million during the year ended December 31, 2021. Further reducing capital during 2021 was $7.9 million used to repurchase 112,141 shares of common stock. Tangible book value per share of Bank First’s common stock experienced an increase of 13.9% during the trailing twelve months.

Dividend Declaration

Bank First’s Board of Directors approved a quarterly cash dividend of $0.22 per common share, payable on April 6, 2022, to shareholders of record as of March 23, 2022.

Bank First Corporation provides financial services through its subsidiary, Bank First, which was incorporated in 1894. The bank is an independent community bank with 21 banking locations in Wisconsin. The bank has grown through both acquisitions and de novo branch expansion. The company employs approximately 287 full-time equivalent staff and has assets of approximately $2.9 billion. Bank First offers loan, deposit and treasury management products at each of its banking offices. Insurance services are available through our bond with Ansay & Associates, LLC. Trust, investment advisory and other financial services are offered through the bank’s partnership with Legacy Private Trust, an alliance with Morgan Stanley and an affiliation with McKenzie Financial Services, LLC. The bank is a co-owner of a bank technology outfitter, UFS, LLC, which provides digital, core, cybersecurity, managed IT and cloud services. Further information about Bank First Corporation is available by clicking on the Investor Relations tab at www.BankFirstWI.bank.

# # #

Forward Looking Statements: This news release may contain certain “forward-looking statements” that represent Bank First Corporation’s expectations or beliefs concerning future events. Such forward-looking statements are about matters that are inherently subject to risks and uncertainties. Because of the risks and uncertainties inherent in forward looking statements, readers are cautioned not to place undue reliance on them, whether included in this news release or made elsewhere from time to time by Bank First Corporation or on its behalf. Bank First Corporation disclaims any obligation to update such forward-looking statements. In addition, statements regarding historical stock price performance are not indicative of or guarantees of future price performance.

22

Bank First Corporation

Consolidated Financial Summary (Unaudited)

| (In thousands, except per share data) | At or for the Three Months Ended | At or for the Year Ended | ||||||||||||||||||||||||||

| 12/31/2021 | 9/30/2021 | 6/30/2021 | 3/31/2021 | 12/31/2020 | 12/31/2021 | 12/31/2020 | ||||||||||||||||||||||

| Results of Operations: | ||||||||||||||||||||||||||||

| Interest income | $ | 25,043 | $ | 24,898 | $ | 24,003 | $ | 24,442 | $ | 27,094 | $ | 98,386 | $ | 100,700 | ||||||||||||||

| Interest expense | 1,812 | 1,964 | 2,189 | 2,339 | 2,623 | 8,304 | 13,865 | |||||||||||||||||||||

| Net interest income | 23,231 | 22,934 | 21,814 | 22,103 | 24,471 | 90,082 | 86,835 | |||||||||||||||||||||

| Provision for loan losses | 600 | 650 | 950 | 900 | 1,650 | 3,100 | 7,125 | |||||||||||||||||||||

| Net interest income after provision for loan losses | 22,631 | 22,284 | 20,864 | 21,203 | 22,821 | 86,982 | 79,710 | |||||||||||||||||||||

| Noninterest income | 5,706 | 5,028 | 6,574 | 6,210 | 6,744 | 23,518 | 23,520 | |||||||||||||||||||||

| Noninterest expense | 13,621 | 12,466 | 12,221 | 12,225 | 13,972 | 50,533 | 53,353 | |||||||||||||||||||||

| Income before income tax expense | 14,716 | 14,846 | 15,217 | 15,188 | 15,593 | 59,967 | 49,877 | |||||||||||||||||||||

| Income tax expense | 3,552 | 3,628 | 3,669 | 3,674 | 4,063 | 14,523 | 11,831 | |||||||||||||||||||||

| Net income | $ | 11,164 | $ | 11,218 | $ | 11,548 | $ | 11,514 | $ | 11,530 | $ | 45,444 | $ | 38,046 | ||||||||||||||

| Earnings per common share - basic | $ | 1.46 | $ | 1.46 | $ | 1.50 | $ | 1.49 | $ | 1.49 | $ | 5.92 | $ | 5.07 | ||||||||||||||

| Earnings per common share - diluted | 1.46 | 1.46 | 1.50 | 1.49 | 1.49 | 5.92 | 5.07 | |||||||||||||||||||||

| Common Shares: | ||||||||||||||||||||||||||||

| Basic weighted average | 7,570,128 | 7,605,541 | 7,653,317 | 7,657,301 | 7,659,904 | 7,621,632 | 7,441,256 | |||||||||||||||||||||

| Diluted weighted average | 7,595,052 | 7,624,791 | 7,668,740 | 7,677,976 | 7,682,101 | 7,643,167 | 7,481,077 | |||||||||||||||||||||

| Outstanding | 7,616,540 | 7,641,771 | 7,688,795 | 7,729,216 | 7,709,497 | 7,616,540 | 7,709,497 | |||||||||||||||||||||

| Noninterest income / noninterest expense: | ||||||||||||||||||||||||||||

| Service charges | $ | 1,574 | $ | 1,491 | $ | 1,596 | $ | 1,467 | $ | 1,586 | $ | 6,128 | $ | 5,003 | ||||||||||||||

| Income from Ansay | 383 | 756 | 723 | 725 | 169 | 2,587 | 2,740 | |||||||||||||||||||||

| Income from UFS | 776 | 751 | 663 | 366 | 599 | 2,556 | 3,066 | |||||||||||||||||||||

| Loan servicing income | 1,557 | 599 | 1,178 | 505 | 194 | 3,839 | 1,420 | |||||||||||||||||||||

| Net gain on sales of mortgage loans | 1,167 | 1,206 | 2,187 | 2,811 | 2,214 | 7,371 | 5,310 | |||||||||||||||||||||

| Net gain (loss) on sales of securities | - | (3 | ) | - | - | - | (3 | ) | 3,233 | |||||||||||||||||||

| Other noninterest income | 249 | 228 | 227 | 336 | 1,982 | 1,040 | 2,748 | |||||||||||||||||||||

| Total noninterest income | $ | 5,706 | $ | 5,028 | $ | 6,574 | $ | 6,210 | $ | 6,744 | $ | 23,518 | $ | 23,520 | ||||||||||||||

| Personnel expense | $ | 7,307 | $ | 6,996 | $ | 7,121 | $ | 7,091 | $ | 7,604 | $ | 28,515 | $ | 27,273 | ||||||||||||||

| Occupancy, equipment and office | 950 | 1,070 | 968 | 1,210 | 1,352 | 4,198 | 4,719 | |||||||||||||||||||||

| Data processing | 1,334 | 1,259 | 1,358 | 1,393 | 1,519 | 5,344 | 5,515 | |||||||||||||||||||||

| Postage, stationery and supplies | 181 | 204 | 131 | 197 | 204 | 713 | 872 | |||||||||||||||||||||

| Net (gain) loss on other real estate owned | 186 | - | (73 | ) | (133 | ) | (16 | ) | (20 | ) | 1,395 | |||||||||||||||||

| Advertising | 75 | 50 | 53 | 49 | 61 | 227 | 226 | |||||||||||||||||||||

| Charitable contributions | 135 | 121 | 152 | 126 | 214 | 534 | 574 | |||||||||||||||||||||

| Outside service fees | 776 | 741 | 804 | 755 | 1,029 | 3,076 | 4,112 | |||||||||||||||||||||

| Amortization of intangibles | 352 | 351 | 351 | 351 | 522 | 1,405 | 1,636 | |||||||||||||||||||||

| Penalty for early extinguishment of debt | - | - | - | - | - | - | 1,323 | |||||||||||||||||||||

| Other noninterest expense | 2,325 | 1,674 | 1,356 | 1,186 | 1,483 | 6,541 | 5,708 | |||||||||||||||||||||

| Total noninterest expense | $ | 13,621 | $ | 12,466 | $ | 12,221 | $ | 12,225 | $ | 13,972 | $ | 50,533 | $ | 53,353 | ||||||||||||||

23

Bank First Corporation

Consolidated Financial Summary (Unaudited)

| (In thousands, except per share data) | At or for the Three Months Ended | At or for the Year Ended | ||||||||||||||||||||||||||

| 12/31/2021 | 9/30/2021 | 6/30/2021 | 3/31/2021 | 12/31/2020 | 12/31/2021 | 12/31/2020 | ||||||||||||||||||||||

| Period-end balances: | ||||||||||||||||||||||||||||

| Cash and cash equivalents | $ | 296,860 | $ | 299,953 | $ | 251,071 | $ | 261,174 | $ | 170,219 | $ | 296,860 | $ | 170,219 | ||||||||||||||

| Investment securities available-for-sale, at fair value | 212,689 | 148,376 | 153,818 | 167,940 | 165,039 | 212,689 | 165,039 | |||||||||||||||||||||

| Investment securities held-to-maturity, at cost | 5,911 | 5,912 | 5,912 | 5,934 | 6,669 | 5,911 | 6,669 | |||||||||||||||||||||

| Loans | 2,235,515 | 2,208,915 | 2,225,217 | 2,228,892 | 2,191,460 | 2,235,515 | 2,191,460 | |||||||||||||||||||||

| Allowance for loan losses | (20,315 | ) | (20,237 | ) | (19,547 | ) | (18,531 | ) | (17,658 | ) | (20,315 | ) | (17,658 | ) | ||||||||||||||

| Premises and equipment | 49,461 | 44,181 | 43,503 | 43,606 | 43,183 | 49,461 | 43,183 | |||||||||||||||||||||

| Goodwill and other intangibles, net | 59,392 | 59,743 | 60,095 | 60,561 | 60,912 | 59,392 | 60,912 | |||||||||||||||||||||

| Other assets | 98,039 | 99,762 | 98,881 | 96,623 | 98,192 | 98,039 | 98,192 | |||||||||||||||||||||

| Total assets | 2,937,552 | 2,846,605 | 2,818,950 | 2,846,199 | 2,718,016 | 2,937,552 | 2,718,016 | |||||||||||||||||||||

| - | ||||||||||||||||||||||||||||

| Deposits | 2,528,440 | 2,472,258 | 2,446,654 | 2,448,035 | 2,320,963 | 2,528,440 | 2,320,963 | |||||||||||||||||||||

| Securities sold under repurchase agreements | 41,122 | 17,402 | 21,679 | 47,631 | 36,377 | 41,122 | 36,377 | |||||||||||||||||||||

| Borrowings | 25,511 | 26,679 | 26,697 | 30,467 | 40,969 | 25,511 | 40,969 | |||||||||||||||||||||

| Other liabilities | 19,826 | 15,004 | 12,490 | 16,624 | 24,850 | 19,826 | 24,850 | |||||||||||||||||||||

| Total liabilities | 2,614,899 | 2,531,343 | 2,507,520 | 2,542,757 | 2,423,159 | 2,614,899 | 2,423,159 | |||||||||||||||||||||

| Stockholders' equity | 322,653 | 315,262 | 311,430 | 303,442 | 294,857 | 322,653 | 294,857 | |||||||||||||||||||||

| Book value per common share | 42.36 | 41.26 | 40.50 | 39.26 | 38.25 | 42.36 | 38.25 | |||||||||||||||||||||

| Tangible book value per common share | 34.56 | 33.44 | 32.69 | 31.42 | 30.35 | 34.56 | 30.35 | |||||||||||||||||||||

| Average balances: | ||||||||||||||||||||||||||||

| Loans | $ | 2,207,615 | $ | 2,218,324 | $ | 2,247,026 | $ | 2,196,142 | $ | 2,206,207 | $ | 2,217,305 | $ | 2,032,157 | ||||||||||||||

| Interest-earning assets | 2,695,175 | 2,659,584 | 2,633,850 | 2,547,783 | 2,465,713 | 2,634,565 | 2,308,095 | |||||||||||||||||||||

| Total assets | 2,901,685 | 2,861,959 | 2,835,580 | 2,750,471 | 2,671,967 | 2,837,793 | 2,504,682 | |||||||||||||||||||||

| Deposits | 2,513,918 | 2,479,799 | 2,453,156 | 2,355,888 | 2,316,793 | 2,451,203 | 2,135,107 | |||||||||||||||||||||

| Interest-bearing liabilities | 1,759,437 | 1,738,895 | 1,723,395 | 1,694,711 | 1,663,642 | 1,729,313 | 1,588,650 | |||||||||||||||||||||

| Goodwill and other intangibles, net | 59,614 | 59,969 | 60,363 | 60,782 | 60,836 | 60,178 | 56,191 | |||||||||||||||||||||

| Stockholders' equity | 318,837 | 313,868 | 308,201 | 300,331 | 289,916 | 310,370 | 265,504 | |||||||||||||||||||||

| Paycheck Protection Program ("PPP") loan information | ||||||||||||||||||||||||||||

| PPP Loans (period end) | $ | 31,100 | $ | 62,639 | $ | 127,277 | $ | 188,221 | $ | 172,424 | $ | 31,100 | $ | 172,424 | ||||||||||||||

| PPP Loan Deferred Origination Fees (period end) | 1,080 | 2,243 | 4,252 | 4,552 | 2,573 | 1,080 | 2,573 | |||||||||||||||||||||

| PPP Loans (average during the period) | 50,602 | 95,645 | 171,036 | 174,242 | 235,325 | 122,468 | 183,950 | |||||||||||||||||||||

| Interest income recognized during the period (includes recognized origination fees) | 1,290 | 2,251 | 1,922 | 2,368 | 3,833 | 7,831 | 8,739 | |||||||||||||||||||||

| Financial ratios: | ||||||||||||||||||||||||||||

| Return on average assets | 1.53 | % | 1.57 | % | 1.63 | % | 1.67 | % | 1.71 | % | 1.60 | % | 1.52 | % | ||||||||||||||

| Return on average common equity | 13.89 | % | 14.30 | % | 14.99 | % | 15.34 | % | 15.78 | % | 14.64 | % | 14.33 | % | ||||||||||||||

| Average equity to average assets | 10.99 | % | 10.97 | % | 10.87 | % | 10.92 | % | 10.85 | % | 10.94 | % | 10.60 | % | ||||||||||||||

| Stockholders' equity to assets | 10.98 | % | 11.08 | % | 11.05 | % | 10.66 | % | 10.85 | % | 10.98 | % | 10.85 | % | ||||||||||||||

| Tangible equity to tangible assets | 9.15 | % | 9.17 | % | 9.11 | % | 8.72 | % | 8.80 | % | 9.15 | % | 8.80 | % | ||||||||||||||

| Loan yield | 4.25 | % | 4.25 | % | 4.13 | % | 4.34 | % | 4.62 | % | 4.21 | % | 4.69 | % | ||||||||||||||

| Earning asset yield | 3.74 | % | 3.76 | % | 3.71 | % | 3.95 | % | 4.44 | % | 3.79 | % | 4.44 | % | ||||||||||||||

| Cost of funds | 0.41 | % | 0.45 | % | 0.51 | % | 0.56 | % | 0.63 | % | 0.48 | % | 0.87 | % | ||||||||||||||

| Net interest margin, taxable equivalent | 3.47 | % | 3.47 | % | 3.37 | % | 3.57 | % | 4.01 | % | 3.47 | % | 3.84 | % | ||||||||||||||

| Net loan charge-offs to average loans | 0.02 | % | -0.01 | % | -0.01 | % | 0.00 | % | 0.01 | % | 0.02 | % | 0.04 | % | ||||||||||||||

| Nonperforming loans to total loans | 0.37 | % | 0.53 | % | 0.55 | % | 0.63 | % | 0.57 | % | 0.37 | % | 0.57 | % | ||||||||||||||

| Nonperforming assets to total assets | 0.28 | % | 0.42 | % | 0.45 | % | 0.52 | % | 0.52 | % | 0.28 | % | 0.52 | % | ||||||||||||||

| Allowance for loan losses to loans | 0.91 | % | 0.92 | % | 0.88 | % | 0.83 | % | 0.81 | % | �� | 0.91 | % | 0.81 | % | |||||||||||||

24

Bank First Corporation

Average assets, liabilities and stockholders' equity, and average rates earned or paid

| Three Months Ended | ||||||||||||||||||||||||

| December 31, 2021 | December 31, 2020 | |||||||||||||||||||||||

| Interest | Interest | |||||||||||||||||||||||

| Income/ | Income/ | |||||||||||||||||||||||

| Average | Expenses | Rate Earned/ | Average | Expenses | Rate Earned/ | |||||||||||||||||||

| Balance | (1) | Paid (1) | Balance | (1) | Paid (1) | |||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| ASSETS | ||||||||||||||||||||||||

| Interest-earning assets | ||||||||||||||||||||||||

| Loans (2) | ||||||||||||||||||||||||

| Taxable | $ | 2,117,319 | $ | 90,468 | 4.27 | % | $ | 2,100,764 | $ | 97,767 | 4.65 | % | ||||||||||||

| Tax-exempt | 90,296 | 4,152 | 4.60 | % | 105,443 | 5,286 | 5.01 | % | ||||||||||||||||

| Securities | ||||||||||||||||||||||||

| Taxable (available for sale) | 119,901 | 3,311 | 2.76 | % | 107,224 | 3,840 | 3.58 | % | ||||||||||||||||

| Tax-exempt (available for sale) | 71,804 | 2,179 | 3.03 | % | 73,094 | 2,276 | 3.11 | % | ||||||||||||||||

| Tax-exempt (held to maturity) | 5,912 | 151 | 2.55 | % | 6,669 | 163 | 2.44 | % | ||||||||||||||||

| Cash and due from banks | 289,943 | 454 | 0.16 | % | 72,519 | 76 | 0.10 | % | ||||||||||||||||

| Total interest-earning assets | 2,695,175 | 100,715 | 3.74 | % | 2,465,713 | 109,408 | 4.44 | % | ||||||||||||||||

| Non interest-earning assets | 226,891 | 223,179 | ||||||||||||||||||||||

| Allowance for loan losses | (20,381 | ) | (16,925 | ) | ||||||||||||||||||||

| Total assets | $ | 2,901,685 | $ | 2,671,967 | ||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||||||||||||||||||

| Interest-bearing deposits | ||||||||||||||||||||||||

| Checking accounts | $ | 203,363 | $ | 253 | 0.12 | % | $ | 195,094 | $ | 295 | 0.15 | % | ||||||||||||

| Savings accounts | 550,402 | 1,835 | 0.33 | % | 407,287 | 1,426 | 0.35 | % | ||||||||||||||||

| Money market accounts | 687,353 | 1,911 | 0.28 | % | 625,958 | 2,143 | 0.34 | % | ||||||||||||||||

| Certificates of deposit | 248,318 | 2,082 | 0.84 | % | 354,797 | 5,248 | 1.48 | % | ||||||||||||||||

| Brokered Deposits | 12,079 | 349 | 2.89 | % | 19,435 | 556 | 2.86 | % | ||||||||||||||||

| Total interest bearing deposits | 1,701,515 | 6,430 | 0.38 | % | 1,602,571 | 9,668 | 0.60 | % | ||||||||||||||||

| Other borrowed funds | 57,922 | 759 | 1.31 | % | 61,071 | 766 | 1.25 | % | ||||||||||||||||

| Total interest-bearing liabilities | 1,759,437 | 7,189 | 0.41 | % | 1,663,642 | 10,434 | 0.63 | % | ||||||||||||||||

| Non-interest bearing liabilities | ||||||||||||||||||||||||

| Demand Deposits | 812,403 | 714,222 | ||||||||||||||||||||||

| Other liabilities | 11,008 | 4,187 | ||||||||||||||||||||||

| Total Liabilities | 2,582,848 | 2,382,051 | ||||||||||||||||||||||

| Shareholders' equity | 318,837 | 289,916 | ||||||||||||||||||||||

| Total liabilities & sharesholders' equity | $ | 2,901,685 | $ | 2,671,967 | ||||||||||||||||||||

| Net interest income on a fully taxable | 93,526 | 98,974 | ||||||||||||||||||||||

| Less taxable equivalent adjustment | (1,361 | ) | (1,622 | ) | ||||||||||||||||||||

| Net interest income | $ | 92,165 | $ | 97,352 | ||||||||||||||||||||

| Net interest spread (3) | 3.33 | % | 3.81 | % | ||||||||||||||||||||

| Net interest margin (4) | 3.47 | % | 4.01 | % | ||||||||||||||||||||

| (1) | Annualized on a fully taxable equivalent basis calculated using a federal tax rate of 21%. |

| (2) | Nonaccrual loans are included in average amounts outstanding. |

| (3) | Represents the difference between the weighted average yield on interest-earning assets and cost of interest-bearing liabilities. |

| (4) | Represents net interest income on a fully tax equivalent basis as a percentage of average interest-earning assets. |

25

Bank First Corporation

Average assets, liabilities and stockholders' equity, and average rates earned or paid

| For the Year Ended | ||||||||||||||||||||||||

| December 31, 2021 | December 31, 2020 | |||||||||||||||||||||||

| Interest | Interest | |||||||||||||||||||||||

| Income/ | Income/ | |||||||||||||||||||||||

| Average | Expenses | Rate Earned/ | Average | Expenses | Rate Earned/ | |||||||||||||||||||

| Balance | (1) | Paid (1) | Balance | (1) | Paid (1) | |||||||||||||||||||

| (dollars | in | thousands) | ||||||||||||||||||||||

| ASSETS | ||||||||||||||||||||||||

| Interest-earning assets | ||||||||||||||||||||||||

| Loans (2) | ||||||||||||||||||||||||

| Taxable | $ | 2,128,327 | $ | 90,172 | 4.24 | % | $ | 1,918,490 | $ | 90,698 | 4.73 | % | ||||||||||||

| Tax-exempt | 88,978 | 4,113 | 4.62 | % | 113,667 | 5,791 | 5.09 | % | ||||||||||||||||

| Securities | ||||||||||||||||||||||||

| Taxable (available for sale) | 103,277 | 2,788 | 2.70 | % | 114,392 | 3,142 | 2.75 | % | ||||||||||||||||

| Tax-exempt (available for sale) | 70,864 | 2,207 | 3.11 | % | 67,903 | 2,170 | 3.20 | % | ||||||||||||||||

| Taxable (held to maturity) | - | - | - | 9,068 | 216 | 2.38 | % | |||||||||||||||||

| Tax-exempt (held to maturity) | 6,098 | 155 | 2.54 | % | 8,422 | 220 | 2.61 | % | ||||||||||||||||

| Cash and due from banks | 237,021 | 310 | 0.13 | % | 76,153 | 181 | 0.24 | % | ||||||||||||||||

| Total interest-earning assets | 2,634,565 | 99,745 | 3.79 | % | 2,308,095 | 102,418 | 4.44 | % | ||||||||||||||||

| Non interest-earning assets | 222,548 | 211,387 | ||||||||||||||||||||||

| Allowance for loan losses | (19,320 | ) | (14,800 | ) | ||||||||||||||||||||

| Total assets | $ | 2,837,793 | $ | 2,504,682 | ||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||||||||||||||||||

| Interest-bearing deposits | ||||||||||||||||||||||||

| Checking accounts | $ | 209,970 | $ | 252 | 0.12 | % | $ | 194,718 | $ | 669 | 0.34 | % | ||||||||||||

| Savings accounts | 497,958 | 1,773 | 0.36 | % | 356,091 | 1,792 | 0.50 | % | ||||||||||||||||

| Money market accounts | 664,591 | 2,115 | 0.32 | % | 563,847 | 3,076 | 0.55 | % | ||||||||||||||||

| Certificates of deposit | 278,602 | 2,967 | 1.06 | % | 367,054 | 6,405 | 1.74 | % | ||||||||||||||||

| Brokered Deposits | 14,718 | 420 | 2.85 | % | 18,428 | 531 | 2.88 | % | ||||||||||||||||

| Total interest bearing deposits | 1,665,839 | 7,527 | 0.45 | % | 1,500,138 | 12,473 | 0.83 | % | ||||||||||||||||

| Other borrowed funds | 63,474 | 777 | 1.22 | % | 88,512 | 1,392 | 1.57 | % | ||||||||||||||||

| Total interest-bearing liabilities | 1,729,313 | 8,304 | 0.48 | % | 1,588,650 | 13,865 | 0.87 | % | ||||||||||||||||

| Non-interest bearing liabilities | ||||||||||||||||||||||||

| Demand Deposits | 785,364 | 634,969 | ||||||||||||||||||||||

| Other liabilities | 12,746 | 15,559 | ||||||||||||||||||||||

| Total Liabilities | 2,527,423 | 2,239,178 | ||||||||||||||||||||||

| Shareholders' equity | 310,370 | 265,504 | ||||||||||||||||||||||

| Total liabilities & sharesholders' equity | $ | 2,837,793 | $ | 2,504,682 | ||||||||||||||||||||

| Net interest income on a fully taxable | 91,441 | 88,553 | ||||||||||||||||||||||

| Less taxable equivalent adjustment | (1,359 | ) | (1,718 | ) | ||||||||||||||||||||

| Net interest income | $ | 90,082 | $ | 86,835 | ||||||||||||||||||||

| Net interest spread (3) | 3.31 | % | 3.56 | % | ||||||||||||||||||||

| Net interest margin (4) | 3.47 | % | 3.84 | % | ||||||||||||||||||||

| (1) | Annualized on a fully taxable equivalent basis calculated using a federal tax rate of 21%. | |

| (2) | Nonaccrual loans are included in average amounts outstanding. | |

| (3) | Represents the difference between the weighted average yield on interest-earning assets and cost of interest-bearing liabilities. | |

| (4) | Represents net interest income on a fully tax equivalent basis as a percentage of average interest-earning assets. |

26